Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - Otter Tail Corp | ex32-1.htm |

| EX-31.1 - EXHIBIT 31.1 - Otter Tail Corp | ex31-1.htm |

| EX-32.2 - EXHIBIT 32.2 - Otter Tail Corp | ex32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - Otter Tail Corp | ex31-2.htm |

| EXCEL - IDEA: XBRL DOCUMENT - Otter Tail Corp | Financial_Report.xls |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

|

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the quarterly period ended

|

June 30, 2014

|

OR

|

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the transition period from

|

to

|

|

Commission file number

|

0-53713

|

|

OTTER TAIL CORPORATION

|

|

(Exact name of registrant as specified in its charter)

|

|

Minnesota

|

27-0383995

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

incorporation or organization)

|

Identification No.)

|

|

215 South Cascade Street, Box 496, Fergus Falls, Minnesota

|

56538-0496

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

866-410-8780

|

|

(Registrant’s telephone number, including area code)

|

|

(Former name, former address and former fiscal year, if changed since last report)

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.:

Large accelerated filer x Accelerated filer o

Non-accelerated filer o Smaller reporting company o

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes o No x

Indicate the number of shares outstanding of each of the issuer’s classes of Common Stock, as of the latest practicable date:

July 31, 2014 – 36,649,018 Common Shares ($5 par value)

OTTER TAIL CORPORATION

INDEX

|

Page No.

|

|||

|

2 & 3

|

|||

|

4

|

|||

|

5

|

|||

|

6

|

|||

|

7-36

|

|||

|

37-55

|

|||

|

56

|

|||

|

56

|

|||

|

57

|

|||

|

57

|

|||

|

57

|

|||

|

58

|

|||

|

58

|

|||

| 1 |

|

Item 1. Financial Statements

|

||

|

Otter Tail Corporation

|

||

|

(not audited)

|

|

(in thousands)

|

June 30,

2014

|

December 31,

2013

|

||||||

|

ASSETS

|

||||||||

|

Current Assets

|

||||||||

|

Cash and Cash Equivalents

|

$ | -- | $ | 1,150 | ||||

|

Accounts Receivable:

|

||||||||

|

Trade—Net

|

101,088 | 83,572 | ||||||

|

Other

|

11,531 | 9,790 | ||||||

|

Inventories

|

82,698 | 72,681 | ||||||

|

Deferred Income Taxes

|

43,342 | 35,452 | ||||||

|

Unbilled Revenues

|

16,222 | 18,157 | ||||||

|

Costs and Estimated Earnings in Excess of Billings

|

5,505 | 4,063 | ||||||

|

Regulatory Assets

|

18,423 | 17,940 | ||||||

|

Other

|

13,528 | 7,747 | ||||||

|

Assets of Discontinued Operations

|

10 | 38 | ||||||

|

Total Current Assets

|

292,347 | 250,590 | ||||||

|

Investments

|

8,875 | 9,362 | ||||||

|

Other Assets

|

30,056 | 28,834 | ||||||

|

Goodwill

|

38,808 | 38,971 | ||||||

|

Other Intangibles—Net

|

12,839 | 13,328 | ||||||

|

Deferred Debits

|

||||||||

|

Unamortized Debt Expense

|

4,330 | 4,188 | ||||||

|

Regulatory Assets

|

77,168 | 83,730 | ||||||

|

Total Deferred Debits

|

81,498 | 87,918 | ||||||

|

Plant

|

||||||||

|

Electric Plant in Service

|

1,507,065 | 1,460,884 | ||||||

|

Nonelectric Operations

|

195,302 | 194,872 | ||||||

|

Construction Work in Progress

|

210,960 | 187,461 | ||||||

|

Total Gross Plant

|

1,913,327 | 1,843,217 | ||||||

|

Less Accumulated Depreciation and Amortization

|

695,276 | 676,201 | ||||||

|

Net Plant

|

1,218,051 | 1,167,016 | ||||||

|

Total Assets

|

$ | 1,682,474 | $ | 1,596,019 | ||||

|

See accompanying notes to condensed consolidated financial statements.

|

||||||||

| 2 |

|

Otter Tail Corporation

|

||

|

Consolidated Balance Sheets

|

||

|

(not audited)

|

|

(in thousands, except share data)

|

June 30,

2014

|

December 31,

2013

|

||||||

|

LIABILITIES AND EQUITY

|

||||||||

|

Current Liabilities

|

||||||||

|

Short-Term Debt

|

$ | 28,143 | $ | 51,195 | ||||

|

Current Maturities of Long-Term Debt

|

194 | 188 | ||||||

|

Accounts Payable

|

108,589 | 113,457 | ||||||

|

Accrued Salaries and Wages

|

17,436 | 19,903 | ||||||

|

Billings In Excess Of Costs and Estimated Earnings

|

4,717 | 13,707 | ||||||

|

Accrued Taxes

|

9,652 | 12,491 | ||||||

|

Derivative Liabilities

|

5,513 | 11,782 | ||||||

|

Other Accrued Liabilities

|

8,695 | 6,532 | ||||||

|

Liabilities of Discontinued Operations

|

3,353 | 3,637 | ||||||

|

Total Current Liabilities

|

186,292 | 232,892 | ||||||

|

Pensions Benefit Liability

|

50,516 | 69,743 | ||||||

|

Other Postretirement Benefits Liability

|

45,683 | 45,221 | ||||||

|

Other Noncurrent Liabilities

|

22,248 | 25,209 | ||||||

|

Commitments and Contingencies (note 9)

|

||||||||

|

Deferred Credits

|

||||||||

|

Deferred Income Taxes

|

218,981 | 195,603 | ||||||

|

Deferred Tax Credits

|

27,381 | 28,288 | ||||||

|

Regulatory Liabilities

|

78,695 | 73,926 | ||||||

|

Other

|

754 | 718 | ||||||

|

Total Deferred Credits

|

325,811 | 298,535 | ||||||

|

Capitalization

|

||||||||

|

Long-Term Debt, Net of Current Maturities

|

498,591 | 389,589 | ||||||

|

Cumulative Preferred Shares– Authorized 1,500,000 Shares Without Par Value;

Outstanding - None

|

-- | -- | ||||||

|

Cumulative Preference Shares – Authorized 1,000,000 Shares Without Par Value;

Outstanding - None

|

-- | -- | ||||||

|

Common Shares, Par Value $5 Per Share—Authorized, 50,000,000 Shares;

|

||||||||

|

Outstanding, 2014—36,623,317 Shares; 2013—36,271,696 Shares

|

183,117 | 181,358 | ||||||

|

Premium on Common Shares

|

263,048 | 255,759 | ||||||

|

Retained Earnings

|

108,834 | 99,441 | ||||||

|

Accumulated Other Comprehensive Loss

|

(1,666 | ) | (1,728 | ) | ||||

|

Total Common Equity

|

553,333 | 534,830 | ||||||

|

Total Capitalization

|

1,051,924 | 924,419 | ||||||

|

Total Liabilities and Equity

|

$ | 1,682,474 | $ | 1,596,019 | ||||

|

See accompanying notes to condensed consolidated financial statements.

|

||||||||

| 3 |

|

Otter Tail Corporation

|

||||

|

(not audited)

|

|

Three Months Ended

June 30,

|

Six Months Ended

June 30,

|

|||||||||||||||

|

(in thousands, except share and per-share amounts)

|

2014

|

2013

|

2014

|

2013

|

||||||||||||

|

Operating Revenues

|

||||||||||||||||

|

Electric

|

$ | 92,903 | $ | 82,838 | $ | 211,951 | $ | 183,814 | ||||||||

|

Product Sales

|

101,461 | 94,557 | 197,379 | 185,118 | ||||||||||||

|

Construction Services

|

40,247 | 34,994 | 65,753 | 61,411 | ||||||||||||

|

Total Operating Revenues

|

234,611 | 212,389 | 475,083 | 430,343 | ||||||||||||

|

Operating Expenses

|

||||||||||||||||

|

Production Fuel - Electric

|

12,603 | 15,603 | 34,633 | 33,556 | ||||||||||||

|

Purchased Power - Electric System Use

|

16,476 | 11,245 | 38,261 | 27,884 | ||||||||||||

|

Electric Operation and Maintenance Expenses

|

39,774 | 35,805 | 74,396 | 68,252 | ||||||||||||

|

Cost of Products Sold (depreciation included below)

|

80,178 | 72,337 | 154,117 | 140,124 | ||||||||||||

|

Cost of Construction Revenues Earned (depreciation included below)

|

33,881 | 31,600 | 56,243 | 55,875 | ||||||||||||

|

Other Nonelectric Expenses

|

15,104 | 12,176 | 28,665 | 25,954 | ||||||||||||

|

Depreciation and Amortization

|

14,969 | 14,835 | 29,749 | 29,755 | ||||||||||||

|

Property Taxes - Electric

|

3,387 | 3,009 | 6,358 | 5,925 | ||||||||||||

|

Total Operating Expenses

|

216,372 | 196,610 | 422,422 | 387,325 | ||||||||||||

|

Operating Income

|

18,239 | 15,779 | 52,661 | 43,018 | ||||||||||||

|

Interest Charges

|

7,627 | 6,877 | 14,222 | 13,857 | ||||||||||||

|

Other Income

|

858 | 696 | 2,681 | 1,557 | ||||||||||||

|

Income Before Income Taxes—Continuing Operations

|

11,470 | 9,598 | 41,120 | 30,718 | ||||||||||||

|

Income Tax Expense—Continuing Operations

|

1,486 | 2,094 | 9,774 | 7,980 | ||||||||||||

|

Net Income from Continuing Operations

|

9,984 | 7,504 | 31,346 | 22,738 | ||||||||||||

|

Discontinued Operations

|

||||||||||||||||

|

Income - net of Income Tax Expense (Benefit) of

$1, $131, $50 and ($74) for the respective periods |

9 | 197 | 77 | 116 | ||||||||||||

|

Gain on Disposition - net of Income Tax Expense of

$6 for the six months ended June 30, 2013 |

-- | -- | -- | 210 | ||||||||||||

|

Net Income from Discontinued Operations

|

9 | 197 | 77 | 326 | ||||||||||||

|

Net Income

|

9,993 | 7,701 | 31,423 | 23,064 | ||||||||||||

|

Preferred Dividend Requirements and Other Adjustments

|

-- | -- | -- | 513 | ||||||||||||

|

Earnings Available for Common Shares

|

$ | 9,993 | $ | 7,701 | $ | 31,423 | $ | 22,551 | ||||||||

|

Average Number of Common Shares Outstanding—Basic

|

36,409,753 | 36,170,353 | 36,325,052 | 36,122,742 | ||||||||||||

|

Average Number of Common Shares Outstanding—Diluted

|

36,652,684 | 36,373,606 | 36,568,030 | 36,325,527 | ||||||||||||

|

Basic Earnings Per Common Share:

|

||||||||||||||||

|

Continuing Operations (net of preferred dividend requirement and other adjustments)

|

$ | 0.27 | $ | 0.21 | $ | 0.87 | $ | 0.61 | ||||||||

|

Discontinued Operations

|

-- | -- | -- | 0.01 | ||||||||||||

| $ | 0.27 | $ | 0.21 | $ | 0.87 | $ | 0.62 | |||||||||

|

Diluted Earnings Per Common Share:

|

||||||||||||||||

|

Continuing Operations (net of preferred dividend requirement and other adjustments)

|

$ | 0.27 | $ | 0.21 | $ | 0.86 | $ | 0.61 | ||||||||

|

Discontinued Operations

|

-- | -- | -- | 0.01 | ||||||||||||

| $ | 0.27 | $ | 0.21 | $ | 0.86 | $ | 0.62 | |||||||||

|

Dividends Declared Per Common Share

|

$ | 0.3025 | $ | 0.2975 | $ | 0.6050 | $ | 0.5950 | ||||||||

|

See accompanying notes to consolidated financial statements.

|

||||||||||||||||

| 4 |

|

Otter Tail Corporation

|

||||||||||||||||

|

(not audited)

|

||||||||||||||||

|

Three Months Ended

June 30,

|

Six Months Ended

June 30,

|

|||||||||||||||

|

(in thousands)

|

2014

|

2013

|

2014

|

2013

|

||||||||||||

|

Net Income

|

$ | 9,993 | $ | 7,701 | $ | 31,423 | $ | 23,064 | ||||||||

|

Other Comprehensive Income:

|

||||||||||||||||

|

Unrealized Gain on Available-for-Sale Securities:

|

||||||||||||||||

|

Reversal of Previously Recognized Gains Realized on Sale of

Investments and Included in Other Income During Period |

-- | -- | (17 | ) | (25 | ) | ||||||||||

|

Gains (Losses) Arising During Period

|

36 | (80 | ) | 19 | (85 | ) | ||||||||||

|

Income Tax (Expense) Benefit

|

(13 | ) | 28 | (1 | ) | 39 | ||||||||||

|

Change in Unrealized Gains on Available-for-Sale Securities – net-of-tax

|

23 | (52 | ) | 1 | (71 | ) | ||||||||||

|

Pension and Postretirement Benefit Plans:

|

||||||||||||||||

|

Amortization of Unrecognized Postretirement Benefit Losses

and Costs (note 12) |

51 | 146 | 101 | 291 | ||||||||||||

|

Income Tax (Expense)

|

(20 | ) | (59 | ) | (40 | ) | (117 | ) | ||||||||

|

Pension and Postretirement Benefit Plans – net-of-tax

|

31 | 87 | 61 | 174 | ||||||||||||

|

Total Other Comprehensive Income

|

54 | 35 | 62 | 103 | ||||||||||||

|

Total Comprehensive Income

|

$ | 10,047 | $ | 7,736 | $ | 31,485 | $ | 23,167 | ||||||||

|

See accompanying notes to consolidated financial statements.

|

||||||||||||||||

| 5 |

|

Otter Tail Corporation

|

||

|

(not audited)

|

|

Six Months Ended

June 30,

|

||||||||

|

(in thousands)

|

2014

|

2013

|

||||||

|

Cash Flows from Operating Activities

|

||||||||

|

Net Income

|

$ | 31,423 | $ | 23,064 | ||||

|

Adjustments to Reconcile Net Income to Net Cash Provided by Operating Activities:

|

||||||||

|

Net Gain from Sale of Discontinued Operations

|

-- | (210 | ) | |||||

|

Net Income from Discontinued Operations

|

(77 | ) | (116 | ) | ||||

|

Depreciation and Amortization

|

29,749 | 29,755 | ||||||

|

Deferred Tax Credits

|

(907 | ) | (955 | ) | ||||

|

Deferred Income Taxes

|

14,850 | 9,882 | ||||||

|

Change in Deferred Debits and Other Assets

|

129 | 7,519 | ||||||

|

Discretionary Contribution to Pension Plan

|

(20,000 | ) | (10,000 | ) | ||||

|

Change in Noncurrent Liabilities and Deferred Credits

|

(936 | ) | 4,971 | |||||

|

Allowance for Equity/Other Funds Used During Construction

|

(759 | ) | (567 | ) | ||||

|

Change in Derivatives Net of Regulatory Deferral

|

95 | 486 | ||||||

|

Stock Compensation Expense—Equity Awards

|

736 | 786 | ||||||

|

Other—Net

|

(1,264 | ) | 867 | |||||

|

Cash (Used for) Provided by Current Assets and Current Liabilities:

|

||||||||

|

Change in Receivables

|

(18,148 | ) | (10,126 | ) | ||||

|

Change in Inventories

|

(10,057 | ) | (4,075 | ) | ||||

|

Change in Other Current Assets

|

(2,673 | ) | (783 | ) | ||||

|

Change in Payables and Other Current Liabilities

|

(20,469 | ) | (1,362 | ) | ||||

|

Change in Interest and Income Taxes Receivable/Payable

|

2,664 | (313 | ) | |||||

|

Net Cash Provided by Continuing Operations

|

4,356 | 48,823 | ||||||

|

Net Cash Used in Discontinued Operations

|

(185 | ) | (1,971 | ) | ||||

|

Net Cash Provided by Operating Activities

|

4,171 | 46,852 | ||||||

|

Cash Flows from Investing Activities

|

||||||||

|

Capital Expenditures

|

(80,749 | ) | (51,153 | ) | ||||

|

Net Proceeds from Disposal of Noncurrent Assets

|

3,184 | 1,603 | ||||||

|

Net Increase in Other Investments

|

(1,639 | ) | (25 | ) | ||||

|

Net Cash Used in Investing Activities - Continuing Operations

|

(79,204 | ) | (49,575 | ) | ||||

|

Net Proceeds from Sale of Discontinued Operations

|

-- | 12,842 | ||||||

|

Net Cash Provided by Investing Activities - Discontinued Operations

|

7 | 193 | ||||||

|

Net Cash Used in Investing Activities

|

(79,197 | ) | (36,540 | ) | ||||

|

Cash Flows from Financing Activities

|

||||||||

|

Change in Checks Written in Excess of Cash

|

2,785 | -- | ||||||

|

Net Short-Term (Repayments) Borrowings

|

(23,051 | ) | 1,117 | |||||

|

Proceeds from Issuance of Common Stock

|

8,452 | 1,462 | ||||||

|

Common Stock Issuance Expenses

|

(310 | ) | -- | |||||

|

Payments for Retirement of Capital Stock

|

(459 | ) | (15,723 | ) | ||||

|

Proceeds from Issuance of Long-Term Debt

|

150,000 | 40,900 | ||||||

|

Short-Term and Long-Term Debt Issuance Expenses

|

(516 | ) | (52 | ) | ||||

|

Payments for Retirement of Long-Term Debt

|

(40,993 | ) | (25,222 | ) | ||||

|

Dividends Paid and Other Distributions

|

(22,029 | ) | (22,097 | ) | ||||

|

Net Cash Provided by (Used in) Financing Activities - Continuing Operations

|

73,879 | (19,615 | ) | |||||

|

Net Cash Used in Financing Activities - Discontinued Operations

|

(11 | ) | -- | |||||

|

Net Cash Provided by (Used in) Financing Activities

|

73,868 | (19,615 | ) | |||||

|

Net Change in Cash and Cash Equivalents - Discontinued Operations

|

8 | (784 | ) | |||||

|

Net Change in Cash and Cash Equivalents

|

(1,150 | ) | (10,087 | ) | ||||

|

Cash and Cash Equivalents at Beginning of Period

|

1,150 | 52,362 | ||||||

|

Cash and Cash Equivalents at End of Period

|

$ | -- | $ | 42,275 | ||||

|

See accompanying notes to consolidated financial statements.

|

| 6 |

OTTER TAIL CORPORATION

(not audited)

In the opinion of management, Otter Tail Corporation (the Company) has included all adjustments (including normal recurring accruals) necessary for a fair presentation of the condensed consolidated financial statements for the periods presented. The condensed consolidated financial statements and notes thereto should be read in conjunction with the consolidated financial statements and notes included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2013. Because of seasonal and other factors, the earnings for the three and six month periods ended June 30, 2014 should not be taken as an indication of earnings for all or any part of the balance of the year.

The following notes are numbered to correspond to numbers of the notes included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2013.

1. Summary of Significant Accounting Policies

Revenue Recognition

Due to the diverse business operations of the Company, revenue recognition depends on the product produced and sold or service performed. The Company recognizes revenue when the earnings process is complete, evidenced by an agreement with the customer, there has been delivery and acceptance, and the price is fixed or determinable. In cases where significant obligations remain after delivery, revenue recognition is deferred until such obligations are fulfilled. Provisions for sales returns and warranty costs are recorded at the time of the sale based on historical information and current trends. In the case of derivative instruments, such as Otter Tail Power Company (OTP) forward energy contracts, marked-to-market and realized gains and losses are recognized on a net basis in revenue in accordance with the Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 815, Derivatives and Hedging. Gains and losses on forward energy contracts subject to regulatory treatment, if any, are deferred and recognized on a net basis in revenue in the period realized.

For the Company’s operating companies recognizing revenue on certain products when shipped, those operating companies have no further obligation to provide services related to such product. The shipping terms used in these instances are FOB shipping point.

The companies in the Construction segment enter into fixed-price construction contracts. Revenues under these contracts are recognized on a percentage-of-completion basis. The method used to determine the progress of completion is based on the ratio of costs incurred to total estimated costs on construction projects. Following are the percentages of the Company’s consolidated revenues recorded under the percentage-of-completion method:

|

Three Months Ended June 30,

|

Six Months Ended June 30,

|

|||

|

2014

|

2013

|

2014

|

2013

|

|

|

Percentage-of-Completion Revenues

|

14.7%

|

16.3%

|

11.9%

|

14.1%

|

The following table summarizes costs incurred and billings and estimated earnings recognized on uncompleted contracts:

|

June 30,

|

December 31,

|

|||||||

|

(in thousands)

|

2014

|

2013

|

||||||

|

Costs Incurred on Uncompleted Contracts

|

$ | 389,389 | $ | 361,487 | ||||

|

Less Billings to Date

|

(398,964 | ) | (377,608 | ) | ||||

|

Plus Estimated Earnings Recognized

|

10,363 | 6,477 | ||||||

|

Net Costs in Excess of Billings plus Estimated Earnings on Uncompleted Contracts

|

$ | 788 | $ | (9,644 | ) | |||

The following amounts are included in the Company’s consolidated balance sheets:

|

June 30,

|

December 31,

|

|||||||

|

(in thousands)

|

2014

|

2013

|

||||||

|

Costs and Estimated Earnings in Excess of Billings on Uncompleted Contracts

|

$ | 5,505 | $ | 4,063 | ||||

|

Billings in Excess of Costs and Estimated Earnings on Uncompleted Contracts

|

(4,717 | ) | (13,707 | ) | ||||

|

Net Costs in Excess of Billings plus Estimated Earnings on Uncompleted Contracts

|

$ | 788 | $ | (9,644 | ) | |||

| 7 |

The Company has a standard quarterly Estimate at Completion process in which management reviews the progress and performance of the Company’s contracts accounted for under percentage-of-completion accounting. As part of this process, management reviews include, but are not limited to, any outstanding key contract matters, progress towards completion and the related program schedule, identified risks and opportunities, and the related changes in estimates of revenues and costs. The risks and opportunities include management’s judgment about the ability and cost to achieve the schedule, technical requirements and other contract requirements. Management must make assumptions regarding labor productivity and availability, the complexity of the work to be performed, the availability of materials, the length of time to complete the contract, and performance by subcontractors, among other variables. Based on this analysis, any adjustments to net sales, costs of sales, and the related impact to operating income are recorded as necessary in the period they become known. These adjustments may result from positive program performance and an increase in operating profit during the performance of individual contracts if management determines it will be successful in mitigating risks surrounding the technical, schedule, and cost aspects of those contracts or realizing related opportunities. Likewise, these adjustments may result in a decrease in operating profit if management determines it will not be successful in mitigating these risks or realizing related opportunities. Changes in estimates of net sales, costs of sales, and the related impact to operating income are recognized using a cumulative catch-up, which recognizes, in the current period, the cumulative effect of the changes on current and prior periods based on a contract’s percent complete. A significant change in one or more of these estimates could affect the profitability of one or more of the Company’s contracts. If a loss is indicated at a point in time during a contract, a projected loss for the entire contract is estimated and recognized.

Warranty Reserves

The Company establishes reserves for estimated product warranty costs at the time revenue is recognized based on historical warranty experience and additionally for any known product warranty issues. Certain Company products carry one to fifteen year warranties. Although the Company engages in extensive product quality programs and processes, the Company’s warranty obligations have been and may in the future be affected by product failure rates, repair or field replacement costs and additional development costs incurred in correcting product failures. The warranty reserve balance as of December 31, 2013 and June 30, 2014 relates entirely to products produced by the Company’s former wind tower and waterfront equipment manufacturing companies and is included in liabilities of discontinued operations. See note 17 to condensed consolidated financial statements.

Retainage

Accounts Receivable include the following amounts, billed under contracts by the Company’s construction subsidiaries, that have been retained by customers pending project completion:

|

(in thousands)

|

June 30,

2014

|

December 31,

2013 |

||||||

|

Accounts Receivable Retained by Customers

|

$ | 7,695 | $ | 7,125 | ||||

Fair Value Measurements

The Company follows ASC Topic 820, Fair Value Measurements and Disclosures (ASC 820), for recurring fair value measurements. ASC 820 provides a single definition of fair value, requires enhanced disclosures about assets and liabilities measured at fair value and establishes a hierarchal framework for disclosing the observability of the inputs utilized in measuring assets and liabilities at fair value. The three levels defined by the hierarchy and examples of each level are as follows:

Level 1 – Quoted prices are available in active markets for identical assets or liabilities as of the reported date. The types of assets and liabilities included in Level 1 are highly liquid and actively traded instruments with quoted prices, such as equities listed by the New York Stock Exchange and commodity derivative contracts listed on the New York Mercantile Exchange (NYMEX).

Level 2 – Pricing inputs are other than quoted prices in active markets, but are either directly or indirectly observable as of the reported date. The types of assets and liabilities included in Level 2 are typically either comparable to actively traded securities or contracts, such as treasury securities with pricing interpolated from recent trades of similar securities, or priced with models using highly observable inputs, such as commodity options priced using observable forward prices and volatilities.

Level 3 – Significant inputs to pricing have little or no observability as of the reporting date. The types of assets and liabilities included in Level 3 are those with inputs requiring significant management judgment or estimation and may include complex and subjective models and forecasts.

| 8 |

The following tables present, for each of the hierarchy levels, the Company’s assets and liabilities that are measured at fair value on a recurring basis as of June 30, 2014 and December 31, 2013:

|

June 30, 2014 (in thousands)

|

Level 1

|

Level 2

|

Level 3

|

|||||||||

|

Assets:

|

||||||||||||

|

Current Assets – Other:

|

||||||||||||

|

Forward Energy Contracts

|

$ | -- | $ | -- | $ | 2,733 | ||||||

|

Forward Gasoline Purchase Contracts

|

83 | |||||||||||

|

Money Market and Mutual Funds - Nonqualified Retirement Savings Plan

|

120 | |||||||||||

|

Investments:

|

||||||||||||

|

Corporate Debt Securities – Held by Captive Insurance Company

|

7,274 | |||||||||||

|

U.S. Government Debt Securities – Held by Captive Insurance Company

|

1,264 | |||||||||||

|

Other Assets:

|

||||||||||||

|

Money Market and Mutual Funds - Nonqualified Retirement Savings Plan

|

681 | |||||||||||

|

Total Assets

|

$ | 801 | $ | 8,621 | $ | 2,733 | ||||||

|

Liabilities:

|

||||||||||||

|

Derivative Liabilities - Forward Energy Contracts

|

$ | -- | $ | -- | $ | 5,513 | ||||||

|

Total Liabilities

|

$ | -- | $ | -- | $ | 5,513 | ||||||

|

December 31, 2013 (in thousands)

|

Level 1

|

Level 2

|

Level 3

|

|||||||||

|

Assets:

|

||||||||||||

|

Current Assets – Other:

|

||||||||||||

|

Forward Energy Contracts

|

$ | -- | $ | -- | $ | 338 | ||||||

|

Forward Gasoline Purchase Contracts

|

62 | |||||||||||

|

Money Market and Mutual Funds - Nonqualified Retirement Savings Plan

|

110 | |||||||||||

|

Investments:

|

||||||||||||

|

Corporate Debt Securities – Held by Captive Insurance Company

|

7,671 | |||||||||||

|

U.S. Government Debt Securities – Held by Captive Insurance Company

|

1,271 | |||||||||||

|

Other Assets:

|

||||||||||||

|

Money Market and Mutual Funds - Nonqualified Retirement Savings Plan

|

866 | |||||||||||

|

Total Assets

|

$ | 976 | $ | 9,004 | $ | 338 | ||||||

|

Liabilities:

|

||||||||||||

|

Derivative Liabilities - Forward Energy Contracts

|

$ | -- | $ | 103 | $ | 11,679 | ||||||

|

Total Liabilities

|

$ | -- | $ | 103 | $ | 11,679 | ||||||

The valuation techniques and inputs used for the Level 2 fair value measurements in the table above are as follows:

Forward Energy Contracts – Prices used for the fair valuation of these forward purchases and sales of electricity, which have illiquid trading points, are indexed to a price at an active market.

Forward Gasoline Purchase Contracts – These contracts are priced based on NYMEX quoted prices for Reformulated Blendstock for Oxygenate Blending (RBOB) Gasoline contracts. Prices used for the fair valuation of these contracts are based on NYMEX daily reporting date quoted prices for RBOB contracts with the same settlement periods.

Corporate and U.S. Government Debt Securities Held by the Company’s Captive Insurance Company – Fair values are determined on the basis of valuations provided by a third-party pricing service which utilizes industry accepted valuation models and observable market inputs to determine valuation. Some valuations or model inputs used by the pricing service may be based on broker quotes.

Fair values for OTP’s forward energy contracts with delivery points that are not at an active trading hub included in Level 3 of the fair value hierarchy in the table above as of June 30, 2014 and December 31, 2013, are based on prices indexed to observable prices at an active trading hub. Prices at illiquid trading points are based on a basis spread between that trading point and more liquid trading hub prices. These basis spreads are determined based on available market price information and the use of forward price curve models. The June 30, 2014 Level 3 forward electric basis spreads ranged from $0.00 to $7.28 per megawatt-hour under the active trading hub price. The weighted average price was $40.28 per megawatt-hour.

| 9 |

In the table above, the fair value of the Level 3 forward energy contracts in derivative asset and derivative liability positions as of June 30, 2014 are related to power purchase contracts where OTP intends to take or has taken physical delivery of the energy under the contract. When OTP takes physical delivery of the energy purchased under these contracts the costs incurred are subject to recovery in base rates and through fuel clause adjustments. Any derivative assets or liabilities and related gains or losses recorded as a result of the fair valuation of these power purchase contracts will not be realized and are 100% offset by regulatory liabilities and assets related to fuel clause adjustment treatment of purchased power costs. Therefore, the net impact of any recorded fair valuation gains or losses related to these contracts on the Company’s consolidated net income is $0 and the net income impact of any future fair valuation adjustments of these contracts will be $0. When energy is delivered under these contracts, they will be settled at the original contract price and any fair valuation gains or losses and related derivative assets or liabilities recorded over the life of the contracts will be reversed along with any offsetting regulatory liabilities or assets. Because of regulatory accounting treatment, any price volatility related to the fair valuation of these contracts had no impact on the Company’s reported consolidated net income for the three and six month periods ended June 30, 2014 and 2013.

The following table presents changes in Level 3 forward energy contract derivative asset and liability fair valuations for the six-month periods ended June 30, 2014 and 2013:

|

Six Months Ended

|

||||||||

|

June 30,

|

||||||||

|

(in thousands)

|

2014

|

2013

|

||||||

|

Forward Energy Contracts - Fair Values Beginning of Period

|

$ | (11,341 | ) | $ | (17,782 | ) | ||

|

Less: Amounts Reversed on Settlement of Contracts Entered into in Prior Periods

|

1,161 | 3,776 | ||||||

|

Changes in Fair Value of Contracts Entered into in Prior Periods

|

7,400 | 1,851 | ||||||

|

Cumulative Fair Value Adjustments of Contracts Entered into in Prior Years at End of Period

|

(2,780 | ) | (12,155 | ) | ||||

|

Net Increase in Value of Open Contracts Entered into in Current Period

|

-- | 41 | ||||||

|

Forward Energy Contracts - Net Derivative Liability Fair Values End of Period

|

$ | (2,780 | ) | $ | (12,114 | ) | ||

Inventories

Inventories consist of the following:

|

June 30,

|

December 31,

|

|||||||

|

(in thousands)

|

2014

|

2013

|

||||||

|

Finished Goods

|

$ | 24,732 | $ | 20,649 | ||||

|

Work in Process

|

11,251 | 9,942 | ||||||

|

Raw Material, Fuel and Supplies

|

46,715 | 42,090 | ||||||

|

Total Inventories

|

$ | 82,698 | $ | 72,681 | ||||

Goodwill and Other Intangible Assets

In the first quarter of 2014, Aevenia, Inc. (Aevenia) recorded a $289,000 gain on the sale of its data communication installation and services business which, over the years of its existence, did not provide a materially significant impact to Aevenia’s operating results. In connection with this sale, Aevenia disposed of $163,000 in goodwill associated with the purchase of this business in May 2004.

The following table summarizes changes to goodwill by business segment during 2014:

|

(in thousands)

|

Gross Balance

December 31, 2013 |

Accumulated

Impairments |

Balance (net of

impairments) December 31, 2013 |

Adjustments

to Goodwill in 2014 |

Balance (net of impairments)

June 30,

2014

|

|||||||||||||||

|

Manufacturing

|

$ | 12,186 | $ | -- | $ | 12,186 | $ | -- | $ | 12,186 | ||||||||||

|

Plastics

|

19,302 | -- | 19,302 | -- | 19,302 | |||||||||||||||

|

Construction

|

7,483 | -- | 7,483 | 163 | 7,320 | |||||||||||||||

|

Total

|

$ | 38,971 | $ | -- | $ | 38,971 | $ | 163 | $ | 38,808 | ||||||||||

| 10 |

Intangible assets with finite lives are amortized over their estimated useful lives and reviewed for impairment in accordance with requirements under ASC 360-10-35, Property, Plant, and Equipment—Overall—Subsequent Measurement. The following table summarizes the components of the Company’s intangible assets at June 30, 2014 and December 31, 2013:

|

June 30, 2014 (in thousands)

|

Gross

Carrying Amount |

Accumulated Amortization

|

Net Carrying

Amount

|

Remaining

Amortization

Periods

|

|||||||||

|

Amortizable Intangible Assets:

|

|||||||||||||

|

Customer Relationships

|

$ | 16,811 | $ | 5,359 | $ | 11,452 |

66-166 months

|

||||||

|

Other Intangible Assets

|

639 | 352 | 287 |

27 months

|

|||||||||

|

Total

|

$ | 17,450 | $ | 5,711 | $ | 11,739 | |||||||

|

Indefinite-Lived Intangible Assets:

|

|||||||||||||

|

Trade Name

|

$ | 1,100 | -- | $ | 1,100 | ||||||||

|

December 31, 2013 (in thousands)

|

|||||||||||||

|

Amortizable Intangible Assets:

|

|||||||||||||

|

Customer Relationships

|

$ | 16,811 | $ | 4,935 | $ | 11,876 |

72-172 months

|

||||||

|

Other Intangible Assets Including Contracts

|

825 | 473 | 352 |

33 months

|

|||||||||

|

Total

|

$ | 17,636 | $ | 5,408 | $ | 12,228 | |||||||

|

Indefinite-Lived Intangible Assets:

|

|||||||||||||

|

Trade Name

|

$ | 1,100 | -- | $ | 1,100 | ||||||||

The amortization expense for these intangible assets was:

|

Three Months Ended

|

Six Months Ended

|

|||||||||||||||

|

June 30,

|

June 30,

|

|||||||||||||||

|

(in thousands)

|

2014

|

2013

|

2014

|

2013

|

||||||||||||

|

Amortization Expense – Intangible Assets

|

$ | 244 | $ | 244 | $ | 488 | $ | 488 | ||||||||

The estimated annual amortization expense for these intangible assets for the next five years is:

|

(in thousands)

|

2014

|

2015

|

2016

|

2017

|

2018

|

|||||||||||||||

|

Estimated Amortization Expense – Intangible Assets

|

$ | 977 | $ | 977 | $ | 945 | $ | 849 | $ | 849 | ||||||||||

Supplemental Disclosures of Cash Flow Information

|

As of June 30,

|

||||||||

|

(in thousands)

|

2014

|

2013

|

||||||

|

Noncash Investing Activities:

|

||||||||

|

Accounts Payable Outstanding Related to Capital Additions1

|

$ | 21,992 | $ | 14,935 | ||||

|

Accounts Receivable Outstanding Related to Joint Plant Owner’s Share of Capital Additions2

|

$ | 4,373 | $ | -- | ||||

|

1Amounts are included in cash used for capital expenditures in subsequent periods when payables are settled.

2Amounts are deducted from cash used for capital expenditures in subsequent periods when cash is received.

|

||||||||

| 11 |

Coyote Station Lignite Supply Agreement – Variable Interest Entity

In October 2012, the Coyote Station owners, including OTP, entered into a lignite sales agreement (LSA) with Coyote Creek Mining Company, L.L.C. (CCMC), a subsidiary of The North American Coal Corporation, for the purchase of coal to meet the coal supply requirements of Coyote Station for the period beginning in May 2016 and ending in December 2040. The price per ton to be paid by the Coyote Station owners under the LSA will reflect the cost of production, along with an agreed profit and capital charge. CCMC was formed for the purpose of mining lignite coal to meet the coal fuel supply requirements of Coyote Station from May 2016 through December 2040 and, based on the terms of the LSA, is considered a variable interest entity (VIE) due to the transfer of all operating and economic risk to the Coyote Station owners, as the agreement is structured so that the price of the coal would cover all costs of operations as well as future reclamation costs. The Coyote Station owners are also providing a guarantee of the value of the assets of CCMC as they would be required to buy the assets at book value should they terminate the contract prior to the end of the contract term and are providing a guarantee of the value of the equity of CCMC in that they are required to buy the entity at the end of the contract term at equity value. Under current accounting standards, the primary beneficiary of a VIE is required to include the assets, liabilities, results of operations and cash flows of the VIE in its consolidated financial statements. No single owner of Coyote Station owns a majority interest in Coyote Station and none, individually, has the power to direct the activities that most significantly impact CCMC. Therefore, none of the owners individually, including OTP, is considered a primary beneficiary of the VIE and CCMC is not required to be consolidated in the Company’s consolidated financial statements.

Under the LSA, all development period costs of the Coyote Creek coal mine incurred during the development period will be recovered from the Coyote Station owners over the full term of the production period, which commences with the first delivery of coal to Coyote Station, scheduled for May 2016, by being included in the cost of production. The development fee and the capital charge incurred during the development period will be recovered from the Coyote Station owners over the first 52 months of the production period by being included in the cost of production during those months. OTP’s 35% share of development period costs, development fees and capital charges incurred by CCMC through June 30, 2014 is $13.0 million. In the event the contract is terminated because regulations or legislation render the burning of coal cost prohibitive and the assets worthless, OTP’s maximum exposure to loss as a result of its involvement with CCMC as of June 30, 2014 could be as high as $13.0 million.

Revisions to Presentation

Beginning with the Company’s 2013 Annual Report on Form 10-K, the Company is reporting revenues and costs related to the sale of products by its manufacturing and plastic pipe companies separately from the revenues and costs of its construction companies on the face of its consolidated statements of income. Its nonelectric revenues and cost of goods sold for the three and six month periods ended June 30, 2013 have been revised in a similar manner to be consistent with, and comparable to, the presentation of revenues and costs for the three and six month periods ended June 30, 2014. The change in presentation of 2013 nonelectric revenues and cost of goods sold had no effect on the Company’s reported consolidated revenues, costs, operating income or net income for the three and six month periods ended June 30, 2013.

New Accounting Standards

Accounting Standards Update (ASU) 2013-11

In July 2013, the FASB issued ASU 2013-11, Income Taxes (Topic 740) (ASC 740), Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists, which requires an entity with unrecognized tax benefits to present the unrecognized tax benefits as a reduction to a deferred tax asset related to a net operating loss carryforward, a similar tax loss, or a tax credit carryforward when such net operating loss carryforward, similar tax loss, or tax credit carryforward is available at the reporting date under the tax law of the applicable jurisdiction to settle any additional income taxes that would result from the disallowance of a tax position. The ASU 2013-11 amendments to ASC 740 are effective for fiscal years beginning after December 15, 2013. The Company adopted the reporting requirements in ASU 2013-11 in the first quarter of 2014 on a prospective basis. The Company’s long-term deferred income tax reported on its June 30, 2014 consolidated balance sheet include $4.3 million of unrecognized tax benefits.

ASU 2014-09

In May 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers (Topic 606) (ASC 606). ASC 606 is a comprehensive, principles-based accounting standard which amends current revenue recognition guidance with the objective of improving revenue recognition requirements by providing a single comprehensive model to determine the measurement of revenue and the timing of revenue recognition. ASC 606 also requires expanded disclosures to enable users of financial statements to understand the nature, amount, timing and uncertainty of revenue and cash flows arising from contracts with customers.

| 12 |

ASU 2014-09 amendments to the ASC are effective for fiscal years beginning after December 15, 2016. Application methods permitted are: (1) full retrospective, (2) retrospective using one or more practical expedients and (3) retrospective with the cumulative effect of initial application recognized at the date of initial application. Early application of the ASU amendments is not permitted. The Company is currently reviewing ASU 2014-09, identifying key impacts to its businesses, reviewing revenue streams and contracts to determine areas where the amendments in ASU 2014-09 will be applicable and evaluating transition options.

2. Segment Information

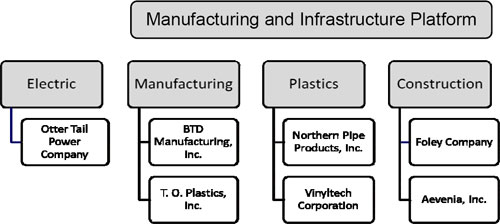

The Company’s businesses have been classified into four segments to be consistent with its business strategy and the reporting and review process used by the Company’s chief operating decision makers. These businesses sell products and provide services to customers primarily in the United States. The four segments are: Electric, Manufacturing, Plastics and Construction.

Electric includes the production, transmission, distribution and sale of electric energy in Minnesota, North Dakota and South Dakota by OTP. In addition, OTP is an active wholesale participant in the Midcontinent Independent System Operator, Inc. (MISO) markets. OTP’s operations have been the Company’s primary business since 1907.

Manufacturing consists of businesses in the following manufacturing activities: contract machining, metal parts stamping and fabrication, and production of material and handling trays, horticultural containers and produce packaging. These businesses have manufacturing facilities in Illinois and Minnesota and sell products primarily in the United States.

Plastics consists of businesses producing polyvinyl chloride (PVC) pipe at plants in North Dakota and Arizona. The PVC pipe is sold primarily in the upper Midwest and Southwest regions of the United States.

Construction consists of businesses involved in commercial and industrial electric contracting and construction of fiber optic, electric distribution, water, wastewater and HVAC systems primarily in the central United States.

OTP is a wholly owned subsidiary of the Company. All of the Company’s other businesses are owned by its wholly owned subsidiary, Varistar Corporation (Varistar). The Company’s corporate operating costs include items such as corporate staff and overhead costs, the results of the Company’s captive insurance company and other items excluded from the measurement of operating segment performance. Corporate assets consist primarily of cash, prepaid expenses, investments and fixed assets. Corporate is not an operating segment. Rather, it is added to operating segment totals to reconcile to totals on the Company’s consolidated financial statements.

No single customer accounted for over 10% of the Company’s consolidated revenues in 2013. All of the Company’s long-lived assets are within the United States.

| 13 |

The following table presents the percent of consolidated sales revenue by country:

|

Three Months Ended June 30,

|

Six Months Ended June 30,

|

|||||||||||||||

|

2014

|

2013

|

2014

|

2013

|

|||||||||||||

|

United States of America

|

96.1 | % | 97.6 | % | 96.8 | % | 97.7 | % | ||||||||

|

Mexico

|

2.6 | % | 1.2 | % | 2.3 | % | 1.2 | % | ||||||||

|

Canada

|

1.1 | % | 1.1 | % | 0.8 | % | 1.0 | % | ||||||||

|

All Other Countries (none greater than 0.06%)

|

0.2 | % | 0.1 | % | 0.1 | % | 0.1 | % | ||||||||

The Company evaluates the performance of its business segments and allocates resources to them based on earnings contribution and return on total invested capital. Information for the business segments for the three and six months ended June 30, 2014 and 2013 and total assets by business segment as of June 30, 2014 and December 31, 2013 are presented in the following tables:

Operating Revenue

|

Three Months Ended

|

Six Months Ended

|

|||||||||||||||

|

June 30,

|

June 30,

|

|||||||||||||||

|

(in thousands)

|

2014

|

2013

|

2014

|

2013

|

||||||||||||

|

Electric

|

$ | 92,911 | $ | 82,862 | $ | 211,999 | $ | 183,872 | ||||||||

|

Manufacturing

|

53,370 | 49,793 | 108,805 | 102,959 | ||||||||||||

|

Plastics

|

48,090 | 44,761 | 88,573 | 82,161 | ||||||||||||

|

Construction

|

40,247 | 34,994 | 65,753 | 61,419 | ||||||||||||

|

Intersegment Eliminations

|

(7 | ) | (21 | ) | (47 | ) | (68 | ) | ||||||||

|

Total

|

$ | 234,611 | $ | 212,389 | $ | 475,083 | $ | 430,343 | ||||||||

Interest Charges

|

Three Months Ended

|

Six Months Ended

|

|||||||||||||||

|

June 30,

|

June 30,

|

|||||||||||||||

|

(in thousands)

|

2014

|

2013

|

2014

|

2013

|

||||||||||||

|

Electric

|

$ | 6,059 | $ | 4,264 | $ | 11,138 | $ | 9,072 | ||||||||

|

Manufacturing

|

813 | 816 | 1,621 | 1,631 | ||||||||||||

|

Plastics

|

274 | 256 | 521 | 504 | ||||||||||||

|

Construction

|

169 | 110 | 269 | 217 | ||||||||||||

|

Corporate and Intersegment Eliminations

|

312 | 1,431 | 673 | 2,433 | ||||||||||||

|

Total

|

$ | 7,627 | $ | 6,877 | $ | 14,222 | $ | 13,857 | ||||||||

Income Taxes

|

Three Months Ended

|

Six Months Ended

|

|||||||||||||||

|

June 30,

|

June 30,

|

|||||||||||||||

|

(in thousands)

|

2014

|

2013

|

2014

|

2013

|

||||||||||||

|

Electric

|

$ | (992 | ) | $ | (817 | ) | $ | 4,758 | $ | 3,265 | ||||||

|

Manufacturing

|

1,336 | 1,373 | 3,007 | 3,591 | ||||||||||||

|

Plastics

|

2,114 | 2,627 | 4,247 | 5,230 | ||||||||||||

|

Construction

|

1,238 | 20 | 829 | (703 | ) | |||||||||||

|

Corporate

|

(2,210 | ) | (1,109 | ) | (3,067 | ) | (3,403 | ) | ||||||||

|

Total

|

$ | 1,486 | $ | 2,094 | $ | 9,774 | $ | 7,980 | ||||||||

| 14 |

Earnings (Loss) Available for Common Shares

|

Three Months Ended

|

Six Months Ended

|

|||||||||||||||

|

June 30,

|

June 30,

|

|||||||||||||||

|

(in thousands)

|

2014

|

2013

|

2014

|

2013

|

||||||||||||

|

Electric

|

$ | 5,242 | $ | 3,583 | $ | 21,895 | $ | 15,514 | ||||||||

|

Manufacturing

|

2,300 | 2,045 | 5,196 | 5,363 | ||||||||||||

|

Plastics

|

3,433 | 3,925 | 6,893 | 7,812 | ||||||||||||

|

Construction

|

1,853 | 24 | 1,233 | (1,068 | ) | |||||||||||

|

Corporate

|

(2,844 | ) | (2,073 | ) | (3,871 | ) | (5,396 | ) | ||||||||

|

Discontinued Operations

|

9 | 197 | 77 | 326 | ||||||||||||

|

Total

|

$ | 9,993 | $ | 7,701 | $ | 31,423 | $ | 22,551 | ||||||||

Identifiable Assets

|

June 30,

|

December 31,

|

|||||||

|

(in thousands)

|

2014

|

2013

|

||||||

|

Electric

|

$ | 1,352,535 | $ | 1,290,416 | ||||

|

Manufacturing

|

125,870 | 119,302 | ||||||

|

Plastics

|

95,011 | 76,853 | ||||||

|

Construction

|

54,820 | 49,440 | ||||||

|

Corporate

|

54,228 | 59,970 | ||||||

|

Discontinued Operations

|

10 | 38 | ||||||

|

Total

|

$ | 1,682,474 | $ | 1,596,019 | ||||

3. Rate and Regulatory Matters

Below are descriptions of OTP’s major capital expenditure projects that have had, or will have, a significant impact on OTP’s revenue requirements, rates and alternative revenue recovery mechanisms, followed by summaries of specific electric rate or rider proceedings with the Minnesota Public Utilities Commission (MPUC), the North Dakota Public Service Commission (NDPSC), the South Dakota Public Utilities Commission (SDPUC) and the Federal Energy Regulatory Commission (FERC), impacting OTP’s revenues in 2014 and 2013.

Major Capital Expenditure Projects

Multi-Value Transmission Projects—On December 16, 2010, FERC approved the cost allocation for a new classification of projects in the MISO region called Multi-Value Projects (MVP). MVPs are designed to enable the region to comply with energy policy mandates and to address reliability and economic issues affecting multiple areas within the MISO region. The cost allocation is designed to ensure that the costs of transmission projects with regional benefits are properly assigned to those who benefit. On October 20, 2011 the FERC reaffirmed the MVP cost allocation on rehearing. On February 24, 2014 the U.S. Supreme Court denied petitions for a writ of certiorari of the United States Court of Appeals, Seventh Circuit decision upholding the FERC’s MVP orders. The petitioners did not seek rehearing. Effective January 1, 2012, the FERC authorized OTP to recover 100% of prudently incurred Construction Work in Progress (CWIP) and Abandoned Plant recovery on two projects approved by MISO as MVPs in MISO’s 2011 Transmission Expansion Plan: the Big Stone South – Brookings MVP and the Big Stone South – Ellendale MVP. Abandoned Plant recovery provides a basis for OTP to request recovery of prudently incurred costs in the event a project is cancelled for reasons beyond OTP’s control. The following projects have been approved by MISO as MVPs under the MISO Open Access Transmission, Energy and Operating Reserve Markets Tariff (Tariff).

The Big Stone South – Brookings Project—This is a planned 345 kiloVolt (kV) transmission line that will extend approximately 70 miles between a proposed substation near Big Stone City, South Dakota and the Brookings County Substation near Brookings, South Dakota. OTP and Xcel Energy jointly developed this project. MISO approved this project as an MVP under the MISO Tariff in December 2011. A Notice of Intent to Construct Facilities (NICF) was filed with the SDPUC on February 29, 2012. This line is expected to be in service in 2017. The SDPUC approved the certification for the northern portion of the route on April 9, 2013. The SDPUC granted OTP and Xcel Energy approval of a route permit for the southern portion of the Big Stone South - Brookings line on February 18, 2014. On August 1, 2014 OTP and Xcel Energy entered into agreements to construct the project.

| 15 |

The Big Stone South – Ellendale Project—This is a proposed 345 kV transmission line that will extend 160 to 170 miles between a proposed substation near Big Stone City, South Dakota and a proposed substation near Ellendale, North Dakota. OTP is jointly developing this project with Montana-Dakota Utilities Co., a Division of MDU Resources Group, Inc. (MDU). MISO approved this project as an MVP under the MISO Tariff in December 2011. OTP and MDU jointly filed an NICF with the SDPUC in March of 2012. On August 25, 2013 the NDPSC granted Certificates of Public Convenience and Necessity to OTP and MDU for the ten miles of the proposed line to be built in North Dakota. On July 10, 2014 the NDPSC approved a Certificate of Corridor Compatibility and a route permit for the North Dakota section of the proposed line. A joint route permit application was filed on August 23, 2013 with the SDPUC. The SDPUC is expected to take formal action on the route permit application in August 2014.

Capacity Expansion 2020 (CapX2020) Transmission Line Projects—CapX2020 is a joint initiative of eleven investor-owned, cooperative, and municipal utilities in Minnesota and the surrounding region to upgrade and expand the electric transmission grid to ensure continued reliable and affordable service. The CapX2020 companies identified four major transmission projects for the region: (1) the Fargo–Monticello 345 kV Project (the Fargo Project), (2) the Brookings–Southeast Twin Cities 345 kV Project (the Brookings Project), (3) the Bemidji–Grand Rapids 230 kV Project (the Bemidji Project), and (4) the Twin Cities–LaCrosse 345 kV Project. OTP is an investor in the Fargo Project, the Brookings Project and the Bemidji Project. Recovery of OTP’s CapX2020 transmission investments is through the MISO Tariff (the Brookings Project as an MVP) and, currently, Minnesota, North Dakota and South Dakota Transmission Cost Recovery (TCR) Riders.

The Fargo Project—All major permits have been received from state regulatory bodies and project agreements have been signed for the construction of the Fargo Project. The Monticello to St. Cloud portion of the Fargo Project was placed into service on December 21, 2011. The St. Cloud to Alexandria portion of the Fargo Project was placed into service on April 23, 2014. Construction is underway for the remaining portions of the project, which are expected to be in service in 2015.

The Brookings Project—All major permits have been received from state regulatory bodies and project agreements have been signed for the construction of the Brookings Project. The MISO also granted unconditional approval of the Brookings Project as an MVP under the MISO Tariff in December 2011. The first phase of the 250 mile Brookings Project was energized in March 2014. Additional segments of the line were energized in April 2014. The entire project is expected to be in service in 2015.

The Bemidji Project—The Bemidji-Grand Rapids transmission line was fully energized and put into service on September 17, 2012.

Big Stone Plant Air Quality Control System (AQCS)—The South Dakota Department of Environment and Natural Resources (DENR) determined that the Big Stone Plant is subject to Best-Available Retrofit Technology (BART) requirements of the Clean Air Act (CAA), based on air dispersion modeling indicating that Big Stone’s emissions reasonably contribute to visibility impairment in national parks and wilderness areas in Minnesota, North Dakota, South Dakota and Michigan. Under the U.S. Environmental Protection Agency’s (EPA) regional haze regulations, South Dakota developed and submitted its implementation plan and associated implementation rules to the EPA on January 21, 2011. The DENR and the EPA agreed on non-substantive rule revisions, which were adopted by the South Dakota Board of Minerals and Environment and became effective on September 19, 2011.

South Dakota developed and submitted its revised implementation plan and associated implementation rules to the EPA on September 19, 2011. Under the South Dakota implementation plan, and its implementing rules, the Big Stone Plant must install and operate a new BART-compliant AQCS to reduce emissions as expeditiously as practicable, but no later than five years after the EPA’s approval of South Dakota’s implementation plan. On March 29, 2012 the EPA took final action to approve South Dakota’s Regional Haze State Implementation Plan (SIP), finding that South Dakota’s SIP submittal met all applicable regional haze regulations. The EPA’s final approval of the SIP was effective on May 29, 2012.

OTP is currently in the process of constructing the BART-compliant AQCS at Big Stone Plant for a current projected cost of approximately $384 million (OTP’s 53.9% share would be $207 million) with an expected commercial operation date of October 2015. OTP’s share of AQCS construction expenditures incurred through June 30, 2014 is $128 million.

| 16 |

Big Stone II Project—On June 30, 2005 OTP and a coalition of six other electric providers entered into several agreements for the development of a second electric generating unit, named Big Stone II, at the site of the existing Big Stone Plant near Milbank, South Dakota. On September 11, 2009 OTP announced its withdrawal—both as a participating utility and as the project’s lead developer—from Big Stone II. On November 2, 2009, the remaining Big Stone II participants announced the cancellation of the Big Stone II project. OTP requested jurisdictional recovery in Minnesota, North Dakota and South Dakota of amounts it had invested in the Big Stone II Project at the time of its withdrawal, discussed below under the respective jurisdictional sections of this note.

Minnesota

2010 General Rate Case—OTP’s most recent general rate increase in Minnesota of approximately $5.0 million, or 1.6%, was granted by the MPUC in an order issued on April 25, 2011 and effective October 1, 2011. The MPUC’s written order included: (1) recovery of Big Stone II costs over five years, (2) moving recovery of wind farm assets from rider recovery to base rate recovery, (3) transfer of a portion of Minnesota Conservation Improvement Program (MNCIP) costs from rider recovery to base rate recovery, (4) transfer of the investment in two transmission lines from rider recovery to base rate recovery, and (5) changing the mechanism for providing customers with a credit for margins earned on asset-based wholesale sales of electricity from a credit to base rates to a credit to the Minnesota Fuel Clause Adjustment.

Renewable Energy Standards, Conservation, Renewable Resource Riders—Minnesota has a renewable energy standard which requires OTP to generate or procure sufficient renewable generation such that the following percentages of total retail electric sales to Minnesota customers come from qualifying renewable sources: 17% by 2016; 20% by 2020 and 25% by 2025. In addition, a new standard established by the 2013 legislature requires 1.5% of total electric sales to be supplied by solar energy by the year 2020. OTP is currently evaluating potential options for meeting that standard. Under certain circumstances and after consideration of costs and reliability issues, the MPUC may modify or delay implementation of the standards. OTP has acquired renewable resources and expects to acquire additional renewable resources in order to maintain compliance with the Minnesota renewable energy standard. OTP’s compliance with the Minnesota renewable energy standard will be measured through the Midwest Renewable Energy Tracking System.

Under the Next Generation Energy Act of 2007, an automatic adjustment mechanism was established to allow Minnesota electric utilities to recover investments and costs incurred to satisfy the requirements of the renewable energy standard. The MPUC is authorized to approve a rate schedule rider to enable utilities to recover the costs of qualifying renewable energy projects that supply renewable energy to Minnesota customers. Cost recovery for qualifying renewable energy projects can be authorized outside of a rate case proceeding, provided that such renewable projects have received previous MPUC approval. Renewable resource costs eligible for recovery may include return on investment, depreciation, operation and maintenance costs, taxes, renewable energy delivery costs and other related expenses.

The costs for three major wind farms previously approved by the MPUC for recovery through OTP’s Minnesota Renewable Resource Adjustment (MNRRA) were moved to base rates as of October 1, 2011 under the MPUC’s April 25, 2011 general rate case order with the exception of the remaining balance of the MNRRA regulatory asset. The MNRRA rate continued to collect the remaining regulatory asset balance through April 30, 2013, when the balance was estimated to be very near zero. On April 4, 2013 the MPUC authorized that any remaining unrecovered balance be retained as a regulatory asset to be recovered in OTP’s next general rate case. Effective May 1, 2013 the resource adjustment on OTP’s Minnesota customers’ bills no longer includes MNRRA costs.

Conservation Improvement Programs—Under Minnesota law, every regulated public utility that furnishes electric service must make annual investments and expenditures in energy conservation improvements, or make a contribution to the state’s energy and conservation account, in an amount equal to at least 1.5% of its gross operating revenues from service provided in Minnesota. The Next Generation Energy Act of 2007 transitioned from a conservation spending goal to a conservation energy savings goal in 2010.

The Minnesota Department of Commerce (MNDOC) may require a utility to make investments and expenditures in energy conservation improvements whenever it finds that the improvement will result in energy savings at a total cost to the utility less than the cost to the utility to produce or purchase an equivalent amount of a new supply of energy. Such MNDOC orders can be appealed to the MPUC. Investments made pursuant to such orders generally are recoverable costs in rate cases, even though ownership of the improvement may belong to the property owner rather than the utility. OTP recovers conservation related costs not included in base rates under the MNCIP through the use of an annual recovery mechanism approved by the MPUC.

| 17 |

In December 2012, the MPUC ordered a change in the MNCIP cost recovery methodology used by OTP from a percentage of a customer’s bill to an amount per kilowatt-hour (kwh) consumed. On January 1, 2013 OTP’s MNCIP surcharge decreased from 3.8% of the customer’s bill to $0.00142 per kwh, which equates to approximately 1.9% of a customer’s bill. On October 10, 2013 the MPUC approved OTP’s 2012 financial incentive request for $2.7 million as well as its request for an updated surcharge rate to be implemented on November 1, 2013. OTP recognized $3.9 million in MNCIP financial incentives in 2013 related to the results of its conservation improvement programs in Minnesota in 2013. On April 1, 2014 OTP submitted its annual 2013 financial incentive filing request for $4.0 million along with a request for an updated surcharge rate. The MNDOC issued comments on July 8, 2014. A decision by the MPUC is expected in the third quarter of 2014.

OTP had a regulatory asset of $7.7 million for allowable costs and financial incentives eligible for recovery through the MNCIP rider that had not been billed to Minnesota customers as of June 30, 2014. OTP recognized revenue for Minnesota conservation costs and incentives earned totaling $1.5 million in the three month period ended June 30, 2014, compared with $1.7 million in the three month period ended June 30, 2013, and $3.0 million in the six month period ended June 30, 2014, compared with $3.3 million in the six month period ended June 30, 2013.

Transmission Cost Recovery (TCR) Rider—In addition to the MNRRA rider, the Minnesota Public Utilities Act provides a similar mechanism for automatic adjustment outside of a general rate proceeding to recover the costs of new transmission facilities that have been previously approved by the MPUC in a Certificate of Need (CON) proceeding, certified by the MPUC as a Minnesota priority transmission project, made to transmit the electricity generated from renewable generation sources ultimately used to provide service to the utility’s retail customers, or exempt from the requirement to obtain a Minnesota CON. The MPUC may also authorize cost recovery via such TCR riders for charges incurred by a utility under a federally approved tariff that accrue from other transmission owners’ regionally planned transmission projects that have been determined by the MISO to benefit the utility or integrated transmission system. The 2013 legislature passed legislation that also authorizes TCR riders to recover the costs of new transmission facilities approved by the regulatory commission of the state in which the new transmission facilities are to be constructed, to the extent approval is required by the laws of that state, and determined by the MISO to benefit the utility or integrated transmission system. Such TCR riders allow a return on investment at the level approved in a utility’s last general rate case. Additionally, following approval of the rate schedule, the MPUC may approve annual rate adjustments filed pursuant to the rate schedule. OTP’s initial request for approval of a TCR rider was granted by the MPUC on January 7, 2010, and became effective February 1, 2010.

MISO regional cost allocation allows OTP to recover some of the costs of its transmission investment from other MISO customers. On March 26, 2012 the MPUC approved an update to OTP’s Minnesota TCR rider along with an all-in method for MISO regional cost allocations in which OTP’s retail customers would be responsible for the entire investment OTP made in transmission facilities that qualify for regional cost allocation under the MISO Tariff, with an offsetting credit for revenues received from other MISO utilities under the MISO Tariff for projects included in the TCR. OTP’s updated Minnesota TCR rider went into effect April 1, 2012.

On May 24, 2012 OTP filed a petition with the MPUC to seek a determination of eligibility for the inclusion of twelve additional transmission related projects in subsequent Minnesota TCR rider filings. On February 20, 2013 the MPUC approved three of the additional projects as eligible for recovery through the TCR rider. OTP filed its annual update to the TCR rider on February 7, 2013 to include the three new projects as well as updated costs associated with existing projects. In a written order issued on March 10, 2014, the MPUC approved OTP’s 2013 TCR rider update but disallowed recovery of capitalized internal costs, costs in excess of CON estimates and a carrying charge in the TCR rider. These items were removed from OTP’s Minnesota TCR rider effective March 1, 2014. OTP will be allowed to seek recovery of these costs in a future rate case. In response to the MPUC approval of OTP’s annual TCR update, OTP submitted a compliance filing in April 2014 reflecting the TCR rider revenue requirements changes relating to the MPUC’s ruling and requesting no rate change be implemented at the time. The MPUC approved OTP’s compliance filing on June 19, 2014. OTP filed its 2014 annual update on May 1, 2014 with a proposed implementation date of July 1, 2014. The MNDOC was granted an extension through August 1, 2014 to issue comments on the 2014 update.

OTP had a regulatory asset of $2.1 million for amounts eligible for recovery through the Minnesota TCR rider that had not been billed to Minnesota customers as of June 30, 2014. OTP recognized revenue for amounts eligible for recovery through the Minnesota TCR rider of $1.8 million in the three month period ended June 30, 2014, compared with $1.1 million in the three month period ended June 30, 2013, and $4.1 million in the six month period ended June 30, 2014, compared with $2.2 million in the six month period ended June 30, 2013.

| 18 |

Environmental Cost Recovery (ECR) Rider—In a written order issued on January 23, 2012 the MPUC granted OTP’s petition for Advance Determination of Prudence (ADP) for costs associated with the design, construction and operation of the BART-compliant AQCS at Big Stone Plant attributable to serving OTP’s Minnesota customers. On May 24, 2013 legislation was enacted in Minnesota which allowed OTP to file an emission-reduction rider for recovery of the revenue requirements of the AQCS. The legislation authorizes the rider to allow a current return on investment (including CWIP) at the level approved in OTP’s most recent general rate case, unless a different return is determined by the MPUC to be in the public interest. On December 18, 2013 the MPUC granted approval of OTP’s Minnesota ECR rider for recovery of OTP’s Minnesota jurisdictional share of the revenue requirements of its investment in the Big Stone Plant AQCS effective January 1, 2014. The ECR rider recoverable revenue requirements include a current return on the project’s CWIP balance at the level approved in OTP’s most recent general rate case. The rate charged to customers will be updated in an annual filing with the MPUC until the costs are rolled into base rates at an undetermined future date. OTP filed its 2014 annual update on July 31, 2014 with a proposed implementation date of October 1, 2014.

OTP had a regulatory asset of $0.2 million for amounts eligible for recovery through the Minnesota ECR rider that had not been billed to Minnesota customers as of June 30, 2014. OTP recognized revenue for amounts eligible for recovery through the Minnesota ECR rider in the three and six month periods ended June 30, 2014 of $1.7 million and $3.5 million, respectively.