Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - EQUAL ENERGY LTD. | Financial_Report.xls |

| EX-32.1 - EX-32.1 - EQUAL ENERGY LTD. | d733918dex321.htm |

| EX-32.2 - EX-32.2 - EQUAL ENERGY LTD. | d733918dex322.htm |

| EX-31.2 - EX-31.2 - EQUAL ENERGY LTD. | d733918dex312.htm |

| EX-31.1 - EX-31.1 - EQUAL ENERGY LTD. | d733918dex311.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

| x | QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2014

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-34759

EQUAL ENERGY LTD.

(Exact name of registrant as specified in its charter)

| Alberta, Canada | 98-0533758 | |

| (State of other jurisdiction of incorporation or organization) |

(I.R.S. Employer identification No.) |

| 4801 Gaillardia Pkwy, Suite 325 Oklahoma City, OK |

73142 | |

| (Address of principal executive offices) | (Zip code) |

Registrant’s telephone number, including area code:

(405) 242-6000

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |||||

| Non-accelerated filer | ¨ | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of July 31, 2014, prior to being acquired by Petroflow Energy Corporation, there were 36,775,467 shares of our common stock, par value $0.01, outstanding. As further described in Note 13, Subsequent Events, on July 31, 2014, the Company was acquired by and became a wholly owned subsidiary of Petroflow Energy Corporation. See Note 13, Subsequent Events, for further discussion.

Table of Contents

EQUAL ENERGY LTD.

| Part I Financial Information |

||||

| Item 1. Consolidated Financial Statements |

||||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 6 | ||||

| 7 | ||||

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations |

16 | |||

| Item 3. Quantitative and Qualitative Disclosures About Market Risk |

27 | |||

| 28 | ||||

| 29 | ||||

| 29 | ||||

| Item 2. Unregistered Sales of Equity Securities and Use of Proceeds |

37 | |||

| 38 | ||||

| 38 | ||||

| 38 | ||||

| 38 | ||||

| 39 | ||||

Page 1 of 39

Table of Contents

EQUAL ENERGY LTD.

GLOSSARY

| Oil and Natural Gas Liquids | Natural Gas | |||||

| NGLs | natural gas liquids | mcf | thousand cubic feet of natural gas | |||

| bbls | barrels | MMcf | million cubic feet of natural gas | |||

| Mbbl | thousand barrels | Bcf | Billion cubic feet of natural gas | |||

| MMbbl | millions of barrels of oil | mcf/d | thousand cubic feet of natural gas per day | |||

| bbls/d | barrels per day | MMcf/d | million cubic feet of natural gas per day | |||

| mmbtu | millions of British Thermal Units | |||||

| Oil Equivalents (6 mcf:1 boe) | ||||||

| boe |

barrels of oil equivalent | |||||

| Mboe |

thousands of barrels of oil equivalent | |||||

| MMboe |

millions of barrels of oil equivalent | |||||

| boe/d |

barrels of oil equivalent per day | |||||

| Mboe/d |

thousands of barrels of oil equivalent per day | |||||

In this Form 10-Q, all currency amounts are in United States dollars unless otherwise indicated. References to “CAD $” refer to Canadian dollars.

Page 2 of 39

Table of Contents

EQUAL ENERGY LTD.

| (unaudited) ( in thousands) |

June 30, 2014 | December 31, 2013 | ||||||

| Assets |

||||||||

| Current assets |

||||||||

| Cash and cash equivalents |

$ | 25,583 | $ | 15,631 | ||||

| Accounts receivable, net |

12,715 | 13,581 | ||||||

| Prepaid expenses, deposits and other |

488 | 1,051 | ||||||

|

|

|

|

|

|||||

| Total current assets |

38,786 | 30,263 | ||||||

| Oil and natural gas properties, full cost method of accounting: |

||||||||

| Proved, net of accumulated depletion of $252 million and $243 million, respectively |

160,565 | 162,061 | ||||||

| Unproved |

4,364 | 4,014 | ||||||

|

|

|

|

|

|||||

| Total oil and natural gas properties |

164,929 | 166,075 | ||||||

| Other capital assets, net of accumulated depreciation of $0.9 million and $0.8 million, respectively |

437 | 152 | ||||||

|

|

|

|

|

|||||

| Total property, plant and equipment, net |

165,366 | 166,227 | ||||||

| Other assets |

772 | 989 | ||||||

| Deferred income tax asset |

27,575 | 30,906 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 232,499 | $ | 228,385 | ||||

|

|

|

|

|

|||||

| Liabilities |

||||||||

| Current liabilities |

||||||||

| Accounts payable and accrued liabilities |

$ | 13,253 | $ | 17,134 | ||||

| Asset retirement obligation |

290 | 278 | ||||||

| Commodity contracts |

1,094 | 341 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

14,637 | 17,753 | ||||||

| Convertible debentures |

42,174 | 42,309 | ||||||

| Asset retirement obligation |

4,526 | 4,362 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

61,337 | 64,424 | ||||||

|

|

|

|

|

|||||

| Shareholders’ Equity |

||||||||

| Common shares, $0.01 par value unlimited authorized shares, and 36,095,117 and 35,806,337 shares issued and outstanding, respectively |

361 | 358 | ||||||

| Additional paid-in capital |

231,119 | 230,574 | ||||||

| Accumulated other comprehensive loss |

(102,102 | ) | (102,102 | ) | ||||

| Retained earnings |

41,784 | 35,131 | ||||||

|

|

|

|

|

|||||

| Total shareholders’ equity |

171,162 | 163,961 | ||||||

|

|

|

|

|

|||||

| Total liabilities and shareholders’ equity |

$ | 232,499 | $ | 228,385 | ||||

|

|

|

|

|

|||||

See accompanying notes to the unaudited consolidated financial statements.

Page 3 of 39

Table of Contents

EQUAL ENERGY LTD.

CONSOLIDATED STATEMENTS OF INCOME and COMPREHENSIVE INCOME

| (unaudited) (in thousands, except per share data) |

Three months ended June 30, |

Six months ended June 30, |

||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Revenues |

||||||||||||||||

| NGL, natural gas and oil revenues |

$ | 20,061 | $ | 14,748 | $ | 42,207 | $ | 29,553 | ||||||||

| (Loss) gain on commodity contracts |

(510 | ) | 3,491 | (2,572 | ) | 220 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues |

19,551 | 18,239 | 39,635 | 29,773 | ||||||||||||

| Expenses |

||||||||||||||||

| Production |

4,205 | 3,529 | 8,266 | 6,984 | ||||||||||||

| Production taxes |

683 | 923 | 1,436 | 1,849 | ||||||||||||

| General and administrative including share-based compensation |

3,242 | 3,857 | 6,554 | 7,010 | ||||||||||||

| Interest expense |

865 | 926 | 1,744 | 1,875 | ||||||||||||

| Depletion and depreciation |

4,663 | 4,160 | 9,181 | 9,027 | ||||||||||||

| Amortization of deferred charges |

111 | 110 | 221 | 221 | ||||||||||||

| Accretion of asset retirement obligation |

95 | 99 | 190 | 200 | ||||||||||||

| Gain on sale of assets |

0 | (90 | ) | (23 | ) | (118 | ) | |||||||||

| Foreign exchange loss (gain) |

1,444 | (1,510 | ) | (83 | ) | (2,480 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 15,308 | 12,004 | 27,486 | 24,568 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income from continuing operations before taxes |

4,243 | 6,235 | 12,149 | 5,205 | ||||||||||||

| Taxes |

||||||||||||||||

| Current tax benefit (expense) |

52 | 0 | (11 | ) | 0 | |||||||||||

| Deferred tax expense |

(1,575 | ) | (1,450 | ) | (3,331 | ) | (650 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income from continuing operations |

2,720 | 4,785 | 8,807 | 4,555 | ||||||||||||

| Discontinued operations: |

||||||||||||||||

| Income (loss) from discontinued operations |

41 | (39 | ) | (287 | ) | 1,722 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

$ | 2,761 | 4,746 | $ | 8,520 | $ | 6,277 | |||||||||

| Other comprehensive income |

||||||||||||||||

| Foreign currency translation adjustment |

0 | 0 | 0 | 61 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Comprehensive income |

$ | 2,761 | $ | 4,746 | $ | 8,520 | $ | 6,338 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings per share information: |

||||||||||||||||

| Basic earnings per share from continuing operations |

$ | 0.08 | $ | 0.13 | $ | 0.24 | $ | 0.13 | ||||||||

| Basic earnings (loss) per share from discontinued operations |

$ | 0.00 | $ | 0.00 | $ | (0.01 | ) | $ | 0.05 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic earnings per share |

$ | 0.08 | $ | 0.13 | $ | 0.23 | $ | 0.18 | ||||||||

| Diluted earnings per share from continuing operations |

$ | 0.07 | $ | 0.13 | $ | 0.23 | $ | 0.12 | ||||||||

| Diluted earnings (loss) per share from discontinued operations |

$ | 0.00 | $ | 0.00 | $ | (0.01 | ) | $ | 0.05 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted earnings per share |

$ | 0.07 | $ | 0.13 | $ | 0.22 | $ | 0.17 | ||||||||

See accompanying notes to the unaudited consolidated financial statements.

Page 4 of 39

Table of Contents

EQUAL ENERGY LTD.

CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

|

Common Stock |

Additional Paid-In Capital |

Retained Earnings |

Accumulated Other Comprehensive Loss |

Total Stockholders’ Equity |

||||||||||||||||||||

| (unaudited) ( in thousands) | Shares | Amount | ||||||||||||||||||||||

| Balances at December 31, 2013 |

35,806 | $ | 358 | $ | 230,574 | $ | 35,131 | $ | (102,102 | ) | $ | 163,961 | ||||||||||||

| Issue of common shares under restricted share plan |

277 | 3 | (3 | ) | — | — | — | |||||||||||||||||

| Share-based compensation |

— | — | 486 | — | — | 486 | ||||||||||||||||||

| Cash Dividends |

— | — | — | (1,805 | ) | — | (1,805 | ) | ||||||||||||||||

| Stock Dividends |

12 | — | 62 | (62 | ) | — | — | |||||||||||||||||

| Income and comprehensive income for the period |

— | — | — | 8,520 | — | 8,520 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Balances at June 30, 2014 |

36,095 | $ | 361 | $ | 231,119 | $ | 41,784 | $ | (102,102 | ) | $ | 171,162 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

See accompanying notes to the unaudited consolidated financial statements.

Page 5 of 39

Table of Contents

EQUAL ENERGY LTD.

CONSOLIDATED STATEMENTS OF CASH FLOWS

| Six months ended June 30, |

||||||||

| (unaudited) (in thousands) |

2014 | 2013 | ||||||

| Operating Activities |

||||||||

| Net income |

$ | 8,520 | $ | 6,277 | ||||

| Net (income) loss from discontinued operations |

287 | (1,722 | ) | |||||

| Adjustments to reconcile net income to net cash provided by operating activities: |

||||||||

| Depletion and depreciation |

9,181 | 9,027 | ||||||

| Accretion of asset retirement obligation |

190 | 200 | ||||||

| Share-based compensation |

486 | 1,122 | ||||||

| Amortization of deferred charges |

221 | 221 | ||||||

| Commodity derivative fair value losses (gains) |

2,572 | (220 | ) | |||||

| Cash (payments) receipts from settled derivatives |

(1,819 | ) | 95 | |||||

| Gain on sale of assets |

(23 | ) | (118 | ) | ||||

| Deferred tax expense |

3,331 | 650 | ||||||

| Cash payment for asset retirement obligation |

(36 | ) | — | |||||

| Unrealized foreign exchange gain |

(83 | ) | (2,480 | ) | ||||

| Change in assets and liabilities: |

||||||||

| Accounts receivable |

866 | 1,041 | ||||||

| Prepaid expenses and other current assets |

563 | 247 | ||||||

| Accounts payable and accrued liabilities |

(1,883 | ) | 3,961 | |||||

|

|

|

|

|

|||||

| Net cash provided by operating activities – continuing operations |

22,373 | 18,301 | ||||||

| Net cash used in operating activities – discontinued operations |

(287 | ) | (2,756 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by operating activities |

22,086 | 15,545 | ||||||

| Investing Activities |

||||||||

| Property, plant and equipment additions |

(10,352 | ) | (14,790 | ) | ||||

| Proceeds on sale of property, plant and equipment |

23 | 146 | ||||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(10,329 | ) | (14,644 | ) | ||||

|

|

|

|

|

|||||

| Financing Activities |

||||||||

| Dividends |

(1,805 | ) | (3,559 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in financing activities |

(1,805 | ) | (3,559 | ) | ||||

|

|

|

|

|

|||||

| Change in cash and cash equivalents |

9,952 | (2,658 | ) | |||||

| Cash and cash equivalents, beginning of period |

15,631 | 23,086 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents, end of period |

$ | 25,583 | $ | 20,428 | ||||

|

|

|

|

|

|||||

| Supplementary Cash Flow Information |

||||||||

| Interest paid |

$ | 1,373 | $ | 1,494 | ||||

| Income tax paid |

— | — | ||||||

|

|

|

|

|

|||||

See accompanying notes to the unaudited consolidated financial statements.

Page 6 of 39

Table of Contents

EQUAL ENERGY LTD.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

| 1. | Basis of Presentation and Significant Accounting Policies |

Prior to its acquisition by Petroflow Energy Corporation on July 31, 2014, Equal Energy Ltd. (“Equal” or the “Company”) was a publicly listed company whose common shares trade on both the Toronto Stock Exchange (“TSX”) and the New York Stock Exchange (“NYSE”) under the symbol EQU. As further described in Note 13, Subsequent Events, on July 31, 2014, the Company was acquired by and became a wholly owned subsidiary of Petroflow Energy Corporation. See Note 13, Subsequent Events, for further information. Equal is engaged in the exploration, development and production of Natural Gas Liquids (“NGLs”), natural gas and oil in the United States and conducts many of its activities jointly with others. These consolidated financial statements reflect only the Company’s proportionate interest in such activities. See Note 13, Subsequent Events, for discussion regarding the acquisition of all of the Company’s issued and outstanding common shares on July 31, 2014.

As required by Rule 3b-4(c) of the United States Securities Exchange Act of 1934, as amended, and Rule 405 of the United States Securities Act of 1933, as amended, Equal has adopted generally accepted accounting principles in the United States of America (“U.S. GAAP”) for financial reporting.

The accompanying unaudited consolidated financial statements have been prepared pursuant to the rules and regulations of the United States Securities and Exchange Commission (“SEC”). Pursuant to such rules and regulations, certain disclosures normally included in financial statements prepared in accordance with U.S. GAAP have been omitted. The accompanying unaudited consolidated financial statements should be read in conjunction with the Company’s consolidated financial statements included in Equal’s Annual Report on Form 10-K for the year ended December 31, 2013, filed with the SEC on March 17, 2014. The accompanying unaudited consolidated financial statements reflect all adjustments that are, in the opinion of management, necessary for a fair presentation of the Company’s financial position as of June 30, 2014, and the Company’s results of operations and cash flows for the three and six month periods ended June 30, 2014 and 2013.

Foreign Currency Transactions

As a result of the 2012 strategic review, all of Equal’s Canadian oil and gas assets were sold in Q4 2012. Starting in January 2013, the Company changed its functional currency from the Canadian dollar to the U.S. dollar, as the Company primarily generates revenue and expends cash in U.S. dollars. In addition, effective January 1, 2013, the Company changed its reporting currency from the Canadian dollar to the U.S. dollar.

RECENT ACCOUNTING STANDARDS

As of January 1, 2017, Equal will be required to adopt Accounting Standards Update (“ASU”) 2014-09, “Revenue from Contracts with Customers” under Topic 606, which was the result of a joint project by the FASB and International Accounting Standards Board. The new standard replaces Topic 605, “Revenue Recognition”, and other industry-specific guidance in the Accounting Standards Codification. The new standard is based on the principle that revenue is recognized on the transfer of promised goods or services to customers in an amount that reflects the consideration the Company expects to be entitled to in exchange for those goods or services. The standard can be applied using either the full retrospective approach or a modified retrospective approach at the date of adoption. Equal is currently assessing the potential impact of the standard on the Company’s consolidated financial statements.

In April 2014, the FASB issued ASU No. 2014-08, “Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity.” This ASU relates to discontinued operations reporting for disposals of components of an entity that represent strategic shifts that have, or will have, a major effect on an entity’s operations and financial results. The standard expands the disclosures for discontinued operations and requires new disclosures related to individually material disposals that do not meet the definition of a discontinued operation. The provisions of this ASU are effective for interim and annual periods beginning after December 15, 2014. The Company does not anticipate that the adoption of this standard will have an impact on its consolidated financial statements or disclosures.

Effective January 1, 2014, Equal adopted ASU No. 2013-11, “Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists” issued by the Financial Accounting Standards Board (“FASB”). This update requires the netting of unrecognized tax benefits against a deferred tax asset for a loss or other carryforward that would apply in settlement of the uncertain tax positions. Under the amended guidance, unrecognized tax benefits are netted against all available same-jurisdiction loss or other tax carryforwards that would be utilized, rather than only against carryforwards that are created by the unrecognized tax benefits. The updated guidance is applied prospectively, effective January 1, 2014. The adoption of this update concerns presentation and disclosure only as it relates to Equal’s consolidated financial statements and had no impact to the Company at June 30, 2014.

Page 7 of 39

Table of Contents

In March 2013, the FASB issued ASU 2013-05, “Foreign Currency Matters: Parent’s Accounting for the Cumulative Translation Adjustment upon Derecognition of Certain Subsidiaries or Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity.” This ASU provides guidance for transactions that require the entire amount of a cumulative translation adjustment related to an entity’s investment in a foreign entity to be released. This guidance is effective for annual and interim periods beginning after December 15, 2013, and had no impact to the Company at June 30, 2014.

| 2. | Accounts Receivable |

The components of account receivable include the following:

| (in thousands) |

June 30, 2014 | December 31, 2013 | ||||||

| Accounts receivable – trade |

$ | 11,910 | $ | 12,211 | ||||

| Accounts receivable – other |

1,038 | 1,733 | ||||||

| Allowance for doubtful accounts |

(233 | ) | (363 | ) | ||||

|

|

|

|

|

|||||

| $ | 12,715 | $ | 13,581 | |||||

|

|

|

|

|

|||||

| 3. | Long-Term Debt |

In June 2014, the Company updated its syndicated bank credit facility of CAD $125 million comprised of a CAD $105 million revolving credit facility and a CAD $20 million operating credit facility and can be drawn against in either Canadian dollars or the United States dollar equivalent. The revolving and operating credit facilities are secured with a first priority charge over the assets of Equal. The maturity date of the revolving and operating credit facilities is June 2015.

Interest rates and standby fees for the credit facilities are set quarterly according to a grid based on the ratio of bank debt to cash flow with the interest rates based on Canadian dollar BA (“Bankers Acceptance”) or U.S. dollar LIBOR rate plus 2.0% to 3.5%, depending on the ratio of bank debt to cash flow. For any unused balance of the credit facility, 0.50% to 0.88% is charged as a standby fee which is recorded in interest expense. At June 30, 2014, the marginal interest rate and standby fee were 2.0% and 0.5%, respectively.

Equal is required to maintain several financial and non-financial covenants. The primary financial covenant is an interest coverage ratio of 3:1 as calculated pursuant to the terms of the credit agreement. For the three months ended June 30, 2014, the interest coverage ratio was 11.64:1. At June 30, 2014, Equal was in compliance with the terms and covenants of the credit facilities. At June 30, 2014, no amount was borrowed against the credit facility and the entire balance of CAD $125 million was available. See Note 13, Subsequent Events, for discussion regarding the acquisition of all of the Company’s issued and outstanding common shares on July 31, 2014, which cancels the bank credit facility under the existing terms and imposed new terms under a new credit facility.

| 4. | Convertible Debentures |

On February 9, 2011, Equal issued CAD $45 million of convertible unsecured junior subordinated debentures with a face value of CAD $1,000 per debenture that mature on March 31, 2016, and bear interest at 6.75% per annum paid semi-annually on March 31 and September 30 of each year (“Debentures”). The Debentures are convertible at the option of the holder into shares at any time prior to the maturity date. Under the terms of the indenture, the common stock dividend payment on May 28, 2014 (See Note 12) resulted in a reduction of the conversion price of each debenture from CAD $8.55 to $8.47 per share and convertible into 118.06 common shares of Equal at June 30, 2014.

At June 30, 2014, the Company had CAD $45 million (US $42.2 million) in face value of Debentures outstanding with an estimated fair value of US $42.4 million.

See Note 13, Subsequent Events, for discussion regarding the acquisition of all of the Company’s issued and outstanding common shares on July 31, 2014, which, as part of the consideration, included a US$0.05 cash dividend payment resulting in an additional reduction of the conversion price of each debenture from CAD$8.47 to $8.39 per share and convertible into 119.19 common shares of Equal.

Page 8 of 39

Table of Contents

| 5. | Asset Retirement Obligation |

The following table reconciles the asset retirement obligation:

| (in thousands) |

June 30, 2014 | December 31, 2013 | ||||||

| Balance, beginning of period |

$ | 4,640 | $ | 4,746 | ||||

| Liabilities added |

20 | 140 | ||||||

| Liabilities settled |

(36 | ) | (43 | ) | ||||

| Revision of estimated obligation |

2 | (614 | ) | |||||

| Accretion of expense on discounted obligation |

190 | 411 | ||||||

|

|

|

|

|

|||||

| Balance, end of period |

$ | 4,816 | $ | 4,640 | ||||

|

|

|

|

|

|||||

| Current portion of Obligation |

$ | 290 | $ | 278 | ||||

|

|

|

|

|

|||||

| 6. | Share-Based Compensation |

As a result of voting at the Company’s shareholders meeting in May 2013, no shares are currently available for future grants under either of the Company’s equity plans. The Company uses the ratable method for calculating compensation expense pursuant to ASC Topic 718, and recognized share-based compensation for share options and restricted shares in General and Administrative expense for the three and six months ended June 30, 2014 and 2013.

Share Options

The Company records compensation expense for share options based on the estimated fair value of the options on the date of grant using the Black-Scholes option-pricing model. Total compensation expense recognized for stock options during the three and six months ended June 30, 2014 was $0 and $14,000, and during the three and six months ended June 30, 2013 was $147,000 and ($124,000), respectively. At June 30, 2014, there was $10,000 of unrecognized compensation expense related to share options, and that cost is expected to be recognized over a weighted-average period of 1.6 years. The amount of unrecognized compensation expense noted above does not necessarily represent the amount that will ultimately be realized by the Company in its unaudited consolidated statement of operations. See Note 13, Subsequent Events, for discussion regarding the acquisition of all of the Company’s issued and outstanding common shares on July 31, 2014, which affects all outstanding share options as of that date.

The following table summarizes Company’s stock option activities for the six months ended June 30, 2014:

| Number of Options (000’s) |

Weighted Average Exercise Price Per Share |

Weighted Average Remaining Contractual Term |

Aggregate Intrinsic Value (000’s) |

|||||||||||||

| Options outstanding at December 31, 2013 |

289 | $ | 6.57 | |||||||||||||

| Options granted |

— | $ | — | |||||||||||||

| Options exercised |

— | $ | — | |||||||||||||

| Options forfeited |

— | $ | — | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Options outstanding at June 30, 2014 |

289 | $ | 6.57 | 1.6 | $ | 129 | ||||||||||

| Options exercisable at June 30, 2014 |

48 | $ | 4.21 | 0.8 | $ | 129 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Vested and expected to vest in the future at June 30, 2014 |

289 | $ | 6.57 | 1.6 | $ | 129 | ||||||||||

Restricted Shares

Total compensation expense recognized for restricted shares during the three and six months ended June 30, 2014 was $232,000 and $472,000, and during the three and six months ended June 30, 2013 was $692,000 and $1,275,000, respectively. At June 30, 2014, there was $1.0 million of unrecognized compensation expense related to restricted shares, and that cost is expected to be recognized over a weighted-average period of 1.3 years. The amount of unrecognized compensation expense noted above does not necessarily represent the amount that will ultimately be realized by the Company in its consolidated statements of operations. See Note 13, Subsequent Events, for discussion regarding the acquisition of all of the Company’s issued and outstanding common shares on July 31, 2014, which affects all outstanding restricted shares as of that date.

Page 9 of 39

Table of Contents

The following table summarizes Company’s non-vested restricted share activities for the quarter ended June 30, 2014:

| Number of Restricted Shares (in thousands) |

Weighted Average Grant Date Fair Value |

|||||||

| Restricted shares outstanding at December 31, 2013 |

981 | $ | 3.90 | |||||

| Restricted shares granted |

6 | $ | 3.57 | |||||

| Restricted shares vested and issued |

(296 | ) | $ | 4.70 | ||||

| Restricted shares forfeited |

(17 | ) | $ | 3.07 | ||||

|

|

|

|

|

|||||

| Restricted shares outstanding at June 30, 2014 |

674 | $ | 3.75 | |||||

|

|

|

|

|

|||||

Page 10 of 39

Table of Contents

| 7. | Earnings per Share |

Basic earnings per share (“EPS”) is computed by dividing net income by the weighted-average number of common shares outstanding during the period. Diluted EPS is based on the combined weighted-average number of common shares and dilutive potential common shares outstanding which include, where appropriate, the assumed exercise of options. In computing diluted EPS, the Company utilizes the treasury stock method.

The computation of weighted-average common and common equivalent shares used in the calculation of basic and diluted EPS is shown in the following table (in thousands, except share and per share data):

| Three Months Ended June 30, |

Six Months Ended June 30, |

|||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Net income – Continuing Operations |

$ | 2,720 | $ | 4,785 | $ | 8,807 | $ | 4,555 | ||||||||

| Net income (loss) – Discontinued Operations |

41 | (39 | ) | (287 | ) | 1,722 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Net income |

$ | 2,761 | $ | 4,746 | $ | 8,520 | $ | 6,277 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic EPS: |

||||||||||||||||

| Weighted-average common shares |

36,098,877 | 35,592,904 | 36,080,963 | 35,560,373 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic EPS – Continuing Operations |

$ | 0.08 | $ | 0.13 | $ | 0.24 | $ | 0.13 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic EPS – Discontinued Operations |

$ | 0.00 | $ | 0.00 | $ | (0.01 | ) | $ | 0.05 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic - Combined |

$ | 0.08 | $ | 0.13 | $ | 0.23 | $ | 0.18 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net Income – Continuing Operations |

$ | 2,720 | $ | 4,785 | $ | 8,807 | $ | 4,555 | ||||||||

| Plus: Income impact of assumed conversion: |

||||||||||||||||

| Interest on 6.75% convertible debentures |

— | — | 1,039 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income after effect of assumed conversion |

$ | 2,720 | $ | 4,785 | $ | 9,846 | $ | 4,555 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted-average common shares, basic |

36,098,877 | 35,592,904 | 36,080,963 | 35,560,373 | ||||||||||||

| Shares issuable pursuant to restricted shares |

448,462 | 1,197,137 | 477,452 | 974,459 | ||||||||||||

| Shares issuable pursuant to dividend equivalent rights |

29,884 | — | 29,913 | — | ||||||||||||

| Shares issuable pursuant to stock options |

19,037 | 6,627 | 19,987 | 4,447 | ||||||||||||

| Shares issuable pursuant to convertible debentures |

— | — | 5,312,869 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average shares outstanding, diluted |

36,596,260 | 36,796,668 | 41,921,184 | 36,539,279 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted EPS – Continuing Operations |

$ | 0.07 | $ | 0.13 | $ | 0.23 | $ | 0.12 | ||||||||

| Diluted EPS – Discontinued Operations |

$ | 0.00 | $ | 0.00 | $ | (0.01 | ) | $ | 0.05 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted EPS – Combined |

$ | 0.07 | $ | 0.13 | $ | 0.22 | $ | 0.17 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

For the calculation of the weighted average number of diluted shares outstanding for the three and six months ended June 30, 2014, the restricted shares and dividend equivalent rights shares were included as they were dilutive to the calculation. For the three months ended June 30, 2014, the convertible debenture shares were excluded from the calculation as they were anti-dilutive, and for the six months ended June 30, 2014, were included as they were dilutive to the calculation. Stock options totaling 217,295 were excluded from the calculation for the three and six months ended June 30, 2014, respectively, as they were anti-dilutive because their exercise prices were higher than the average share price during the quarter.

For the calculation of the weighted average number of diluted shares outstanding for the three and six months ended June 30, 2013, the restricted shares were included as they were dilutive to the calculation, and the Debentures and all options, except for the 34,500 options granted in February 2013, were excluded from the calculation as they were anti-dilutive.

As further described in Note 13, Subsequent Events, on July 31, 2014, the Company was acquired by and became a wholly owned subsidiary of Petroflow Energy Corporation. See Note 13, Subsequent Events, for further information.

| 8. | Fair Value Measurements |

Financial instruments are presented at fair value in the Company’s balance sheets. To estimate fair values of financial instruments, the Company utilizes three levels of input: Level 1, defined as observable inputs for identical instruments such as quoted prices in active markets; Level 2, defined as inputs, other than quoted prices in active markets, that are either directly or indirectly observable; and Level 3, defined as unobservable inputs in which little or no market data exists, therefore requiring an entity to develop its own assumptions. Due to the unavailability of relevant comparable market data for the Company’s fixed price swaps, the discounted cash flow method is used to estimate fair values by discounting future cash flows based on quoted forward prices for commodities and a risk-adjusted discount rate. Such fair value calculation is then compared to the counterparty valuation for reasonableness.

Page 11 of 39

Table of Contents

The carrying values of cash, accounts receivable, accounts payable and accrued liabilities included in the accompanying unaudited consolidated balance sheets approximated fair value at June 30, 2014, and December 31, 2013. The fair value of the Debentures is disclosed in Note 4 and is based on the trading price of the Debentures at the reporting date (Level 1). These assets and liabilities are not presented in the following tables.

The only asset or liability measured at fair value on a recurring basis is the commodity contracts. The fair values of these contracts are based on a market approach and are estimated using inputs which are either directly or indirectly observable at the reporting date, such as exchange and other published prices, broker quotes and observable trading activity. The following tables provide fair value measurement information for commodity derivatives as of June 30, 2014 and December 31, 2013.

| As of June 30, 2014 |

||||||||||||||||||||

| Fair Value Measurements Using: | ||||||||||||||||||||

| (in thousands of dollars) |

Carrying Amount |

Fair Value | Level 1 | Level 2 | Level 3 | |||||||||||||||

| Commodity contracts liability |

1,094 | 1,094 | — | 1,094 | — | |||||||||||||||

| As of December 31, 2013 |

||||||||||||||||||||

| Fair Value Measurements Using: | ||||||||||||||||||||

| (in thousands of dollars) |

Carrying Amount |

Fair Value | Level 1 | Level 2 | Level 3 | |||||||||||||||

| Commodity contracts liability |

341 | 341 | — | 341 | — | |||||||||||||||

Equal’s Debentures actively trade in an established market. There were no transfers in or out of Level 1 or Level 2 measurements for the six months ended June 30, 2014, or the 12 months ended December 31, 2013. The Company’s policy is to recognize transfers between levels as of the beginning of the period in which the event triggering the transfer occurs. The Company had no Level 3 financial instruments at any time during the six months ended June 30, 2014 or 2013.

| 9. | Commodity Contracts |

To minimize the exposure to fluctuations in crude oil and natural gas prices, Equal periodically enters into commodity contracts including fixed price swaps, which currently equal approximately 80% of Equal’s natural gas production and approximately 71% and 6% of the Company’s oil and NGL production, respectively. Such commodity contracts do not qualify for hedge accounting treatment and thus are not designated as hedging instruments. As of June 30, 2014, Equal had financial derivative contracts outstanding with four counterparties. Equal’s commodity contracts are summarized in the table below. See Note 13, Subsequent Events, for discussion regarding the acquisition of all of the Company’s issued and outstanding common shares on July 31, 2014, which cancels all crude oil and natural gas commodity contracts, as of that date.

Page 12 of 39

Table of Contents

| Derivative Instrument |

Commodity | Price | Volume per day | Period | ||||

| Fixed | Gas | 4.25 ($/mmbtu) | 2,000 mmbtu | January 1, 2014 – December 31, 2014 | ||||

| Fixed | Gas | 4.05 ($/mmbtu) | 2,000 mmbtu | January 1, 2014 – December 31, 2014 | ||||

| Fixed | Gas | 4.10 ($/mmbtu) | 2,000 mmbtu | January 1, 2014 – December 31, 2014 | ||||

| Fixed | Gas | 4.06 ($/mmbtu) | 2,000 mmbtu | January 1, 2014 – December 31, 2014 | ||||

| Fixed | Gas | 4.05 ($/mmbtu) | 4,000 mmbtu | January 1, 2014 – December 31, 2014 | ||||

| Fixed | Gas | 4.34 ($/mmbtu) | 2,000 mmbtu | January 1, 2014 – December 31, 2014 | ||||

| Fixed | Gas | 4.55 ($/mmbtu) | 2,000 mmbtu | March 1, 2014 – December 31, 2014 | ||||

| Fixed | Oil | 95.00 ($/bbl) | 200 bbl | March 1, 2014 – December 31, 2014 | ||||

| Fixed | Normal Butane (1) | 54.60 ($/bbl) | 200 bbl | April 1, 2014 – September 30, 2014 |

| (1) | Conway, Propane (in-well) OPIS |

| 10. | Discontinued Operations |

In 2012, Equal announced that its Board of Directors initiated a strategic review process to identify, examine and consider alternatives with the view to enhance shareholder value. As a result of the strategic review process, the Company sold all of its Canadian assets and certain of its Oklahoma assets.

The Canadian asset sales in late 2012 resulted in the discontinuation of operations in Canada. Prior to the initiation of the strategic review, there was a Canadian asset sale which included heavy oil properties in Saskatchewan. Certain Northern Oklahoma assets, which were not included in discontinued operations, were sold in 2012.

The gain of $41,000 and loss of $287,000 from discontinued operations for the three and six months ended June 30, 2014, respectively, primarily relates to equipment sales and abandonment costs. Income of $1.7 million from discontinued operations for the six months ended June 30, 2013 primarily relates to post-closing adjustments.

| 11. | Contingencies |

Equal is party to various legal actions arising in the normal course of business. Matters that are probable of unfavorable outcome to Equal and which can be reasonably estimated are accrued. Such accruals are based on information known about the matters, Equal’s estimates of the outcomes, and its experience in contesting, litigating and settling similar matters. To management’s knowledge, there were no pending legal proceedings which would result in amounts material to Equal’s financial position or results of operations. Actual amounts could differ materially from management’s estimates.

On December 12, 2013, Equal shareholder Andrew Cooke filed a putative class action lawsuit in the District Court of Oklahoma County for the State of Oklahoma against Equal, its directors, Petroflow Energy Corporation and Petroflow Canada Acquisition Corp. (collectively, “Petroflow”): Cooke v. Equal Energy, et al., CJ-2013-6817. Subsequently, three additional putative class actions were also filed by shareholders in the same state court: Olsen v. Equal Energy, et al., CJ-2013-6873; Solak v. Equal Energy, et al., CJ-2013-6959; and Grinberger v. Equal Energy, et al., CJ-2013-7055. These cases alleged that in connection with the proposed Arrangement Agreement (“Arrangement”), the members of the Board breached their fiduciary duties to Equal. The complaints further claimed that Equal and Petroflow aided and abetted those alleged breaches of fiduciary duties. The complaints generally alleged that the Arrangement involves an unfair price, unfair sales process, self-dealing and unfairly preclusive deal protection devices. The plaintiffs in the action sought injunctive relief, including to enjoin the Arrangement, and an award of attorneys’ and other fees and costs. One of these four matters was voluntarily dismissed, while the other three were consolidated into one case: In re Equal Energy Shareholder Litigation, CJ-2013-6873.

Equal and its directors filed a motion to dismiss the state actions on January 23, 2014. Petroflow subsequently filed a similar motion to dismiss. Both motions are fully briefed and remain pending.

Page 13 of 39

Table of Contents

On January 14, 2014, Equal shareholder Johan Van Weelden brought a separate lawsuit in the U.S. District Court for Western District of Oklahoma against Equal, its directors and Petroflow: Van Weelden v. Equal Energy Ltd., et al., No. 14-cv-0047-C. Subsequently three putative class actions were also filed by shareholders in the same federal court: Montemarano et al. v. Equal Energy Ltd., et al., No. 14-cv-0058-C; Cooke v. Equal Energy, Ltd., et al., No. 14-CV-0087-C; Scripture v. Equal Energy Ltd., et al., No. 14-cv-0114-C. These cases allege that disclosures relevant to the proposed Arrangement Agreement with Petroflow violate Section 14(a) and 20(a) of the Securities Exchange Act, that the Equal directors breached their fiduciary duties to Equal shareholders, and that Equal and Petroflow aided and abetted those alleged breaches of fiduciary duties. On May 8, 2014, Judge Cauthron of the U.S. District Court for the Western District of Oklahoma ordered that the cases should be consolidated and appointed Cooke as lead plaintiff and Robbins Gellar Rudman & Dowd LLP as lead counsel.

Equal and its directors filed a motion to dismiss the federal actions on May 15, 2014. Petroflow subsequently filed a similar motion to dismiss. Both motions are fully briefed and remain pending.

Contemporaneous with motion to dismiss briefing, lead counsel in both the state and federal actions and counsel for defendants engaged in arm’s-length negotiations concerning the terms and conditions of a potential resolution of the state and federal actions in which Equal would disclose certain additional information to Equal’s shareholders. On June 12, 2014, Equal filed a revised Definitive Proxy with the SEC containing, among other things, the additional disclosures agreed to in connection with the parties’ agreement. On or around July 10, 2014, counsel for the parties reached an agreement in principle in the federal actions providing for the binding settlement of all claims that all shareholders might have regarding the actions of Equal or its Board while considering or entering into the Petroflow Arrangement Agreement, and while making any disclosures to the marketplace. In exchange Equal agreed to include additional disclosures in its proxy materials, and entered into a memorandum of understanding setting forth the material terms of the settlement. The parties are in the process of drafting the settlement agreement, which will then be submitted to the federal court for review during a final approval hearing.

| 12. | Cash Dividends |

On May 1, 2014, the Petroflow Arrangement Agreement was amended (the “Amendment,” see Item 2 Arrangement to Sell all Issued and Outstanding Shares of the Company) which permitted Equal to declare and pay on or after May 1, 2014, and prior to

the effective date of the Arrangement, a cash dividend of $0.05 per common share, and to declare and pay to its common shareholders who were entitled to receive Arrangement consideration upon completion of the Arrangement a cash dividend of $0.05 cents per common share (the “Arrangement Dividend”). A cash dividend of $1.8 million was paid on May 28, 2014.

Pursuant to the November 27, 2012 announcement of a $0.20 per share annual dividend payable at the end of each calendar quarter of 2013, a $0.05 per share cash dividend was paid during the first two quarters of the 2013 totaling $3.6 million for the six months ended June 30, 2013.

| 13. | Subsequent Events |

In preparing the accompanying unaudited consolidated financial statements, the Company has reviewed events that have occurred after June 30, 2014, through the issuance of the financial statements.

On December 6, 2013, the Company, Petroflow Energy Corporation, a Delaware corporation (“Petroflow”), and Petroflow Canada Acquisition Corp., an Alberta, Canada corporation and wholly-owned subsidiary of Petroflow (“PetroflowSub”), entered into an Arrangement Agreement, pursuant to which Petroflow agreed to acquire, indirectly through PetroflowSub, all of the outstanding common shares of Equal for $5.43 per share in cash, without interest (the “Arrangement”), pursuant to which Equal would become an indirect wholly-owned subsidiary of Petroflow. The Arrangement was completed on July 31, 2014, and the following events were a result of the Arrangement:

| — | Common shareholders of Equal who are entitled to receive Arrangement consideration upon completion of the Arrangement are entitled to receive a cash dividend of $0.05 cents per common share (the “Arrangement Dividend”) following completion of the Arrangement. The $1.8 million cash dividend was paid on July 31, 2014. |

| — | Pursuant to the statutory plan of arrangement, Equal and Petroflow Sub were amalgamated with the combined entity retaining the name Equal Energy Ltd. (herein also referred to as “Equal”). |

| — | Pursuant to the statutory plan of arrangement, each option outstanding immediately prior to the effective time of the Arrangement (whether vested or unvested) was transferred from the holder thereof to Equal in consideration for a cash payment by Equal equal to the amount, if any, by which the Canadian equivalent of the Arrangement consideration, in respect of each option, exceeded the exercise price per share of such option (see Note 6). |

Page 14 of 39

Table of Contents

| — | Pursuant to the statutory plan of arrangement, at the effective time of the Arrangement, all Equal common shares issuable pursuant to Equal’s restricted share and performance share incentive plan were issued and those Equal common shares were converted into the right to receive the Arrangement consideration, less any applicable withholding taxes (see Note 6). |

| — | In connection with the closing of the Arrangement, pursuant to a request submitted by Equal on July 31, 2014, Equal notified the New York Stock Exchange (“NYSE”) and the Toronto Stock Exchange (“TSX”) of the completion of the Arrangement and requested that the NYSE and TSX cease trading of Equal’s common stock and suspend the listing of the common stock prior to the opening of market on July 31, 2014, and that the NYSE file with the SEC an application on Form 25 to delist and deregister the common stock under Section 12(b) of the Exchange Act. |

| — | In connection with the completion of the Arrangement, Equal’s syndicated bank credit facility was cancelled (see Note 3). |

| — | In connection with the Arrangement, on July 31, 2014, Petroflow and Texoak Energy-Project 1C, LLC, as borrowers, entered into a new $250 million first lien credit agreement (the “First Lien Credit Agreement”) and a new $103 million second lien credit agreement (the “Second Lien Credit Agreement” and, together with the First Lien Credit Agreement, the “Credit Agreements” and each a “Credit Agreement”). |

The First Lien Credit Agreement matures on July 31, 2017. The Second Lien Credit Agreement matures on January 31, 2018. There is no scheduled amortization during the term of either Credit Agreement. Loans outstanding under the First Lien Credit Agreement may be voluntarily prepaid at the option of the borrowers, subject to any applicable premium, and, subject to the limitations set forth in the First Lien Credit Agreement and the intercreditor agreement, loans under the Second Lien Credit Agreement may be voluntarily prepaid at the option of the borrowers, subject to any applicable premium. The Credit Agreements contain customary mandatory prepayments, including as a result of asset sales and an annual free cash flow sweep.

Interest rates under the First Lien Credit Agreement are determined, to the extent paid in cash, based on the floating LIBOR rate plus 8% per annum (subject to a LIBOR floor of 1%). Interest rates under the Second Lien Credit Agreement are based on a fixed rate of 12% per annum to extent paid in cash. Each of the First Lien Credit Agreement and Second Lien Credit Agreement provides for an additional 3% of interest per annum for interest that is paid-in-kind.

All domestic subsidiaries of Petroflow, including Equal at such time as it becomes a domestic subsidiary, are required to guarantee the obligations of the borrowers under each of the First Lien Credit Agreement and Second Lien Credit Agreement. Equal is expected to be domesticated as a U.S. subsidiary within thirty days from the effective day of the Arrangement. Substantially all of the borrowers’ and the guarantors’ assets, including their respective interests in oil and gas properties, are pledged as security on a first or second lien basis, as applicable, for the First Lien Credit Agreement and Second Lien Credit Agreement.

Each of the First Lien Credit Agreement and Second Lien Credit Agreement contains customary representations and warranties, affirmative covenants, negative (including financial) covenants and events of default for financings of this type.

| — | In connection with the completion of the Arrangement, Equal has defeased all of the Debentures by depositing cash, in trust with the trustee under the indenture governing the Debentures (the “Indenture”), sufficient to fully pay, satisfy and discharge all obligations under the Debentures. The completion of the Arrangement constitutes a change of control under the Indenture. As a result, pursuant to its obligations under the Indenture, Equal will be offering to repurchase Debentures at a purchase price equal to 101% of the principal amount thereof plus accrued interest, subject to the terms and conditions set out in the Indenture (the “Change of Control Purchase Offer”). Holders that do not accept the Change of Control Purchase Offer shall be entitled to continue to receive interest on the Debentures until they are redeemed at par on March 31, 2016 in accordance with the provisions of the Indenture. The Debentures remain listed for trading on the TSX under the symbol EQU.DB.B. |

Pursuant to the Indenture, following the Arrangement, each debentureholder no longer has the right to receive common shares on conversion of Debentures, but has the right to receive, in lieu of such shares, the US$5.43 in cash per share which such debentureholder would have been entitled to receive had it been the holder of such number of shares at the effective time of the Arrangement that it was entitled to acquire pursuant to its conversion right. The Debentures currently have a conversion price that is significantly greater than the Arrangement consideration.

Equal has filed an application with the Alberta and Ontario securities commissions for relief from the requirements of continuous disclosure in all provinces and territories in Canada, including its obligations under National Instrument 51-102—Continuous Disclosure Obligations. If the relief is granted, Equal will be exempt from its continuous disclosure filing obligations, but will be required (i) to provide annual alternative disclosure that will state the principal amount of Debentures that remain outstanding and (ii) upon the occurrence of a change in the affairs of Equal or the trustee under the Indenture that would reasonably be expected to have a significant effect upon the market price or value of any of the Debentures, to forthwith, upon becoming aware of such a change, issue and file a news release disclosing the nature and substance of the change.

Page 15 of 39

Table of Contents

| — | In connection with the completion of the Arrangement, all of Equal’s crude oil and natural gas commodity contracts were cancelled (see Note 9). |

| — | Pursuant to the terms of the statutory plan of arrangement, the articles of amalgamation filed, on the effective date with the Registrar of Corporations for the Province of Alberta, were deemed to be articles of incorporation of the corporation continuing from the amalgamation, and the certificate of amalgamation issued by the Registrar of Corporations for the Province of Alberta was deemed to be the certificate of incorporation of the corporation continuing from the amalgamation. In addition, pursuant to the terms of the statutory plan of arrangement, at the effective time of the Arrangement, the bylaws of Equal were deemed to be the same as the bylaws of Petroflow Sub. |

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Forward-Looking Statements

The information discussed in this quarterly report on Form 10-Q includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”). All statements, other than statements of historical facts, included herein concerning, among other things, planned capital expenditures, changes in oil and gas production, the number of anticipated wells to be drilled after the date hereof, future cash flows and borrowings, pursuit of potential acquisition opportunities, our financial position, business strategy and other plans and objectives for future operations, are forward-looking statements. These forward-looking statements are identified by their use of terms and phrases such as “may,” “expect,” “estimate,” “project,” “plan,” “believe,” “intend,” “achievable,” “anticipate,” “will,” “continue,” “potential,” “should,” “could,” and similar terms and phrases. Although we believe that the expectations reflected in these forward-looking statements are reasonable, they do involve certain assumptions, risks and uncertainties. Our results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including, among others:

| — | risks and uncertainties associated with the intended offer to repurchase convertible debentures; |

| — | risks associated with drilling oil and natural gas wells; |

| — | the volatility of oil and natural gas prices; |

| — | uncertainties in estimating oil and natural gas reserves; |

| — | the need to replace the oil and natural gas the Company produces; |

| — | the Company’s ability to execute its growth strategy by drilling wells as planned; |

| — | risks and liabilities associated with acquired properties and risks related to the integration of acquired businesses; |

| — | amount, nature and timing of capital expenditures, including future development costs, required to develop the Company’s undeveloped areas; |

| — | concentration of operations in Central Oklahoma; |

| — | inability to retain drilling rigs and other services; |

| — | risk of currency fluctuations; |

| — | the potential adverse effect of commodity price declines on the carrying value of the Company’s oil and natural gas properties; |

| — | severe or unseasonable weather that may adversely affect production and drilling; |

| — | availability of satisfactory oil and natural gas marketing and transportation; |

| — | availability and terms of capital to fund capital expenditures; |

| — | amount and timing of proceeds of asset sales and asset monetization; |

| — | limitations on operations resulting from debt restrictions and financial covenants; |

| — | potential financial losses or earnings reductions from commodity derivatives; |

| — | potential elimination or limitation of tax incentives; |

| — | competition in the oil and natural gas industry; |

Page 16 of 39

Table of Contents

| — | general economic conditions, either internationally or domestically or in the areas where the Company operates; |

| — | inability to obtain required regulatory approvals for development activities; |

| — | costs to comply with current and future governmental regulation of the oil and natural gas industry, including environmental, health and safety laws and regulations, and regulations with respect to water disposal and hydraulic fracturing; |

| — | the need to maintain adequate internal control over financial reporting. |

Finally, our future results will depend upon various other risks and uncertainties, including, but not limited to, those detailed in the section entitled “Risk Factors” included in our 2013 Annual Report on Form 10-K. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements in this section and elsewhere in this report. Other than as required under securities laws, we do not assume a duty to update these forward-looking statements, whether as a result of new information, subsequent events or circumstances, changes in expectations or otherwise.

The following discussion and analysis addresses material changes in our results of operations and capital resources and uses for the three and six months ended June 30, 2014, compared to the three and six months ended June 30, 2013, and in our financial condition and liquidity since December 31, 2013, and should be read in conjunction with “Item 1. Consolidated Financial Statements” of this report and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our 2013 Annual Report on Form 10-K.

In addition, the following discussion is for our continuing operations (U.S. operations) for the three and six months ended June 30, 2014.

Overview

Equal Energy Ltd. is a Calgary, Alberta based company headquartered in Oklahoma City, Oklahoma, engaged in the exploration, acquisition, development and production of petroleum and natural gas in Oklahoma. The Company also reviews new drilling opportunities and potential acquisitions in Oklahoma to supplement its exploration and development activities.

The Company averaged approximately 7,125 and 7,049 boe/d of production for the three and six months ended June 30, 2014, respectively, which was comprised of approximately 48% natural gas, 48% NGLs and 4% crude oil. At June 30, 2014, the Company had 146 gross (120 net) producing wells, virtually all of which it operates, and approximately 85,500 gross (58,600 net) acres under lease or held by production.

On December 6, 2013, Equal, Petroflow Energy Corporation, a Delaware corporation (“Petroflow”), and Petroflow Canada Acquisition Corp., an Alberta, Canada corporation and wholly-owned subsidiary of Petroflow (“PetroflowSub”), entered into an Arrangement Agreement, pursuant to which Petroflow agreed to acquire, indirectly through PetroflowSub, all of the outstanding common shares of Equal for $5.43 per share in cash, without interest (the “Arrangement”), pursuant to which Equal would become an indirect wholly-owned subsidiary of Petroflow. The Arrangement was completed on July 31, 2014. Common shareholders of Equal who are entitled to receive Arrangement consideration upon completion of the Arrangement will also receive a cash dividend of $0.05 cents per common share (the “Arrangement Dividend”) following completion of the Arrangement.

In connection with the completion of the Arrangement, Equal entered into option cancellation agreements (“Option Agreements”) with each option holder in respect of all options.

In addition, at the effective time of the Arrangement, all Equal common shares issuable pursuant to Equal’s restricted share and performance share incentive plan were issued and those Equal common shares were converted into the right to receive the Arrangement consideration, less any applicable withholding taxes.

Petroflow has agreed that following the effective date of the Arrangement, Petroflow will satisfy or cause Equal to satisfy, all of Equal’s obligations regarding its convertible debentures, including that Petroflow will cause Equal to make an offer to purchase all of Equal’s outstanding CAD $45 million of convertible debentures within 30 days. In accordance with the terms of the indenture governing the convertible debentures, cash consideration equal to 101% of the face value, plus accrued and unpaid interest, will be offered to holders of the convertible debentures.

Page 17 of 39

Table of Contents

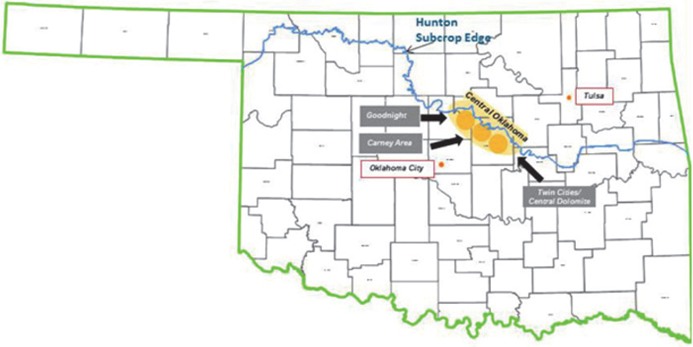

Equal’s Properties

The Company’s production comes from its Oklahoma based operations. The core area assets are located in Lincoln and Logan counties of Oklahoma. The Company also has an inventory of minor producing assets, minor royalty interests and various exploration and exploitation prospects on undeveloped lands in Oklahoma.

In Oklahoma, the key producing horizon is the Hunton formation. The Hunton is a carbonate rock formation which has been largely ignored by the industry in areas with high water/hydrocarbon production ratios. Over the last decade, new drilling and production techniques have enabled profitable development of the Hunton formation. Extensive dewatering lowers reservoir pressure, allowing the liberation and mobilization of oil, natural gas and NGLs from smaller rock pores. Typical peak wellhead hydrocarbon production rates average 150 boe/d per horizontal well and are generally observed within six months of production commencement.

Average Hunton production for the three months ended June 30, 2014, was approximately 20.2 MMcf/d of natural gas, 3.4 Mbbl/d of NGLs and 0.3 Mbbl/d of oil and for the six months ended June 30, 2014 was approximately 20.1 MMcf/d of natural gas, 3.4 Mbbl/d of NGLs and 0.3 Mbbl/d of oil. At December 31, 2013, the reserve report attributed proved reserves of 280 Mbbl of crude oil, 66 Bcf of natural gas and 12,993 Mbbl of NGLs.

As of June 30, 2014, the Company had approximately 27,000 gross (11,000 net) undeveloped acres of land under leasehold, primarily located in Lincoln and Logan counties of Oklahoma comprising of interests in 84 sections.

Market Conditions

Prices of natural gas, NGLs, and oil that we produce can vary significantly, which impacts our revenues and cash flows. The following table lists average New York Mercantile Exchange (“NYMEX”) prices for natural gas, West Texas Intermediate (“WTI”) prices for crude oil, and propane prices at Conway, KS for the three and six months ended June 30, 2014 and 2013.

| Three months ended June 30, | ||||||||

| 2014 | 2013 | |||||||

| Propane, Conway, KS (US$ per bbl) |

$ | 43.80 | $ | 35.88 | ||||

| NYMEX natural gas (US$ per mcf) |

$ | 4.67 | $ | 3.88 | ||||

| WTI (US$ per bbl) |

$ | 103.07 | $ | 94.10 | ||||

| Six months ended June 30, | ||||||||

| 2014 | 2013 | |||||||

| Propane, Conway, KS (US$ per bbl) |

$ | 55.01 | $ | 35.15 | ||||

| NYMEX natural gas (US$ per mcf) |

$ | 4.70 | $ | 3.63 | ||||

| WTI (US$ per bbl) |

$ | 100.88 | $ | 94.26 | ||||

Page 18 of 39

Table of Contents

Results of Operations for the three months ended June 30, 2014, and June 30, 2013

For the three months ended June 30, 2014, Equal Energy’s production was from the Central Oklahoma properties.

The following table sets forth selected operating data for the periods indicated.

| (in thousands, except for boe/d) | Three months ended Central Oklahoma |

|||||||||||||||

| June 30, 2014 | June 30, 2013 | Change | % Change | |||||||||||||

| Net Production per Day: |

||||||||||||||||

| Oil (Bbl) |

323 | 136 | 187 | 137 | % | |||||||||||

| NGL (Bbl) |

3,434 | 3,079 | 355 | 12 | % | |||||||||||

| Natural Gas (Mcf) |

20,207 | 18,429 | 1,778 | 10 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total (Boe/d) |

7,125 | 6,287 | 838 | 13 | % | |||||||||||

| Net Production: |

||||||||||||||||

| Oil (MBbl) |

29 | 12 | 17 | 142 | % | |||||||||||

| NGL (MBbl) |

313 | 280 | 33 | 12 | % | |||||||||||

| Natural Gas (MMcf) |

1,839 | 1,677 | 162 | 10 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total (MBoe) |

649 | 572 | 77 | 13 | % | |||||||||||

| Net Sales: |

||||||||||||||||

| Oil Sales |

$ | 2,938 | $ | 1,127 | $ | 1,811 | 161 | % | ||||||||

| NGL Sales |

10,484 | 8,249 | 2,235 | 27 | % | |||||||||||

| Natural Gas Sales |

6,639 | 5,372 | 1,267 | 24 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | 20,061 | $ | 14,748 | $ | 5,313 | 36 | % | |||||||||

| Average Sales Prices: |

||||||||||||||||

| Oil (per Bbl) |

$ | 101.30 | $ | 90.96 | $ | 10.34 | 11 | % | ||||||||

| NGL (per Bbl) |

33.49 | 29.44 | 4.05 | 14 | % | |||||||||||

| Natural Gas (per Mcf) |

3.61 | 3.20 | 0.41 | 13 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Per Boe |

$ | 30.93 | $ | 25.78 | $ | 5.15 | 20 | % | ||||||||

| Operating Expenses: |

||||||||||||||||

| Production Expenses |

$ | 4,205 | $ | 3,529 | $ | 676 | 19 | % | ||||||||

| Production Taxes |

683 | 923 | (240 | ) | -26 | % | ||||||||||

| Expenses (per Boe): |

||||||||||||||||

| Production Expenses |

$ | 6.48 | $ | 6.17 | $ | 0.31 | 5 | % | ||||||||

| Production Taxes |

1.05 | 1.61 | (0.56 | ) | -35 | % | ||||||||||

| Net Producing Wells at Period End |

120 | 110 | 10 | 9 | % | |||||||||||

The following table sets forth selected operating data as reported for the three months ending:

| June 30, 2014 | June 30, 2013 | Change | % Change | |||||||||||||

| Operating Expenses: |

||||||||||||||||

| General and Administrative Expense |

||||||||||||||||

| (Including Share Based Compensation) |

$ | 3,242 | $ | 3,857 | $ | (615 | ) | -16 | % | |||||||

| Interest Expense |

865 | 926 | (61 | ) | -7 | % | ||||||||||

| Depletion of Oil and Gas Properties |

4,641 | 4,117 | 524 | 13 | % | |||||||||||

| Costs and Expenses (per Boe): |

||||||||||||||||

| General and Administrative Expense |

||||||||||||||||

| (Including Share Based Compensation) |

$ | 5.00 | $ | 6.74 | $ | (1.74 | ) | -26 | % | |||||||

| Interest Expense |

1.33 | 1.62 | (0.29 | ) | -18 | % | ||||||||||

| Depletion of Oil and Gas Properties |

7.16 | 7.20 | (0.04 | ) | -1 | % | ||||||||||

Page 19 of 39

Table of Contents

Oil, Natural Gas and NGL Sales:

Sales in all categories benefited from higher production, as compared to the prior year’s quarter. Equal initiated a one-rig program in January 2013 which was originally budgeted to drill 10 wells during the year. Better than anticipated efficiencies allowed the rig to drill 12 wells during the year. Nine of these wells were completed in 2013 and the final three wells were completed in January 2014. All 12 wells proved very successful, and with several being drilled in oilier parts of the play, we saw a significant jump in oil production as compared to the first quarter of 2013.

Oil Sales

Oil revenue was $2.9 million for the second quarter of 2014 as compared to $1.1 million for the same period last year. The $1.8 million increase was primarily a result of a 137% increase in daily production attributable to successful drilling in 2013, in addition to an 11% increase in average price, excluding commodity contracts.

Gas Sales

Gas revenue for the second quarter of 2014 was $6.6 million as compared to $5.4 million for the same period last year. The $1.2 million increase was primarily due to a 13% increase in average price, excluding commodity contracts, in addition to a 10% increase in daily production attributable to successful drilling in 2013. Price increases were largely consistent with the broad improvement of gas prices in the North American market.

NGL Sales

NGL revenue for the second quarter of 2014 was $10.5 million as compared to $8.2 million for the same period last year. The $2.3 million increase was a result of a 14% increase in average price, excluding commodity contracts, and a 12% increase in daily production. The higher realized prices were largely due to increases in NGL index prices at the Conway, KS hub. The increase in NGL production was attributable to successful drilling in 2013.

Production Expenses

Production expenses were $4.2 million for the second quarter of 2014 compared to $3.5 million for the same period last year. The $0.7 million increase was primarily attributable to the increase in daily production in the current quarter as compared to the same period last year. On a per unit-of-production basis, production expenses per boe increased from $6.17 in the second quarter of 2013 to $6.48 in the second quarter of 2014 primarily due to increased workover expenses.

Production Taxes

The company normally pays a base rate of 7% in production taxes based on realized oil, NGL and natural gas sales. Production taxes were $0.7 million for the second quarter of 2014 compared to $0.9 million for the same period last year. As a percentage of net sales, our production tax rates averaged 3.4% and 6.3% in the second quarter of 2014 and 2013, respectively. The average production tax rate for the second quarter of 2014 was lower than the same period last year due to new horizontal wells drilled in 2013 qualifying for a 48-month six percent Oklahoma production tax rate reduction. During the three months ended December 31, 2013, prior period errors were identified relating to the recording of tax rebates from the Oklahoma Tax Commission (“OTC”) for production activities in 2009, 2010 and 2011, together with the related recognition of deferred income tax assets and expenses. The final settlement with the OTC related to the prior period tax rebates resulted in a $0.4 million decrease of the estimated liability in the second quarter of 2014, which reduced second quarter 2014 production tax expense. Excluding this $0.4 million adjustment, production taxes would have been 5.2% of realized oil, NGL and natural gas sales.

Page 20 of 39

Table of Contents

Commodity Contracts

For the second quarter of 2014, Equal had a net loss on commodity contracts of $0.5 million as compared to a net gain of $3.5 million for the same period last year. The significant decrease in profit is due to higher commodity prices relative to contracted hedges. Equal made cash payments on settled derivatives of $0.7 million in the second quarter of 2014, as compared to $0.1 million for the same period last year. At June 30, 2014, all the derivative contracts were recorded at their fair value, which was a net liability of $1.1 million, an increase of $0.8 million from the $0.3 million of net liability recorded at December 31, 2013.

General and Administrative Expense

General and administrative expense was $3.2 million for the second quarter of 2014 as compared to $3.9 million for the same period last year, excluding discontinued operations. The $0.7 million decrease was due to the decrease in share-based compensation costs due primarily to 2013 forfeitures. On a per unit-of production basis, the general and administrative expense per boe was favorable at $5.00 for the second quarter of 2014 compared to $6.74 for the second quarter of 2013. This reduction in costs per boe is due to increased production and lower costs.

Depletion of Oil and Gas Properties

Depletion of oil and gas properties was $4.6 million, in the second quarter of 2014 as compared to $4.1 million for the same period last year. The $0.5 million increase in expense was attributable to increased production. On a per unit-of production basis, the depletion expense per boe was $7.16 for the second quarter of 2014 compared to $7.20 for the second quarter of 2013.

Interest Expense

Interest expense was $0.9 million for the second quarter of 2014 and for the same period last year, and is comprised of interest on the CAD $45 million, 6.75% convertible debentures and fees associated with the unused CAD $125 million credit facility.

Income Tax Provision

The provision for income tax expense was $1.5 million in the second quarter of 2014 and for the same period last year. The effective income tax rate differs from the statutory rate of 35% due to permanent differences, the change in valuation allowance, and AMT credits.

Page 21 of 39

Table of Contents

Results of Operations for the six months ended June 30, 2014, and June 30, 2013

For the six months ended June 30, 2014, Equal Energy’s production was from the Central Oklahoma properties.

The following table sets forth selected operating data for the periods indicated:

| (in thousands, except for boe/d) | Six months ended Central Oklahoma |

|||||||||||||||

| June 30, 2014 | June 30, 2013 | Change | % Change | |||||||||||||

| Net Production per Day: |

||||||||||||||||

| Oil (Bbl) |

282 | 147 | 135 | 92 | % | |||||||||||

| NGL (Bbl) |

3,423 | 3,083 | 340 | 11 | % | |||||||||||

| Natural Gas (Mcf) |

20,067 | 18,339 | 1,728 | 9 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total (Boe/d) |

7,049 | 6,286 | 763 | 12 | % | |||||||||||

| Net Production: |

||||||||||||||||

| Oil (MBbl) |

51 | 27 | 24 | 89 | % | |||||||||||

| NGL (MBbl) |

620 | 558 | 62 | 11 | % | |||||||||||

| Natural Gas (MMcf) |

3,632 | 3,319 | 313 | 9 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total (MBoe) |

1,276 | 1,139 | 137 | 12 | % | |||||||||||

| Net Sales: |

||||||||||||||||

| Oil Sales |

$ | 5,028 | $ | 2,433 | $ | 2,595 | 107 | % | ||||||||

| NGL Sales |

22,961 | 17,391 | 5,570 | 32 | % | |||||||||||

| Natural Gas Sales |