Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Aleris Corp | d751121d8k.htm |

Aleris Investor Presentation

June 2014

Exhibit 99.1 |

Forward-Looking and Other Information

1

IMPORTANT INFORMATION

FORWARD-LOOKING INFORMATION

NON-GAAP INFORMATION

INDUSTRY INFORMATION

Certain statements in this presentation are “forward-looking statements” within the

meaning of the federal securities laws. Statements about our beliefs and expectations and

statements containing the words “may,” “could,” “would,” “should,” “will,” “believe,” “expect,” “anticipate,” “plan,” “estimate,” “target,”

“project,” “look forward to,” “intend” and similar

expressions intended to connote future events and circumstances constitute forward-looking statements. Forward-looking statements

include statements about, among other things, future costs and prices of commodities, production

volumes, industry trends, demand for our products and services, anticipated cost savings,

anticipated benefits from new products or facilities, and projected results of operations. Forward-looking statements involve known and

unknown risks and uncertainties, which could cause actual results to differ materially from those

contained in or implied by any forward-looking statement. Some of the important factors

that could cause actual results to differ materially from those expressed or implied by forward-looking statements include, but are not limited to, the

following: (1) our ability to successfully implement our business strategy; (2) the cyclical

nature of the aluminum industry, material adverse changes in the aluminum industry or our

end-use segments, such as global and regional supply and demand conditions for aluminum and aluminum products, and changes in our customers’

industries; (3) our ability to fulfill our substantial capital investment requirements; (4)

variability in general economic conditions on a global or regional basis; (5) our ability to

retain the services of certain members of our management; (6) our ability to enter into effective metal, natural gas and other commodity derivatives or

arrangements with customers to manage effectively our exposure to commodity price fluctuations and

changes in the pricing of metals, especially London Metal Exchange-based aluminum prices;

(7) our internal controls over financial reporting and our disclosure controls and procedures may not prevent all possible errors that

could occur; (8) increases in the cost of raw materials and energy; (9) the loss of order volumes from

any of our largest customers; (10) our ability to retain customers, a substantial number of

whom do not have long-term contractual arrangements with us; (11) our ability to generate sufficient cash flows to fund our capital expenditure

requirements and to meet our debt service obligations; (12) competitor pricing activity, competition

of aluminum with alternative materials and the general impact of competition in the industry

segments we serve; (13) risks of investing in and conducting operations on a global basis, including political, social, economic, currency and

regulatory factors; (14) current environmental liabilities and the cost of compliance with and

liabilities under health and safety laws; (15) labor relations (i.e., disruptions, strikes or

work stoppages) and labor costs; (16) our levels of indebtedness and debt service obligations, including changes in our credit ratings, material increases in

our cost of borrowing, or the failure of financial institutions to fulfill their commitments to us

under committed credit facilities; (17) our ability to access the credit and capital markets;

(18) the possibility that we may incur additional indebtedness in the future; and (19) limitations on operating our business as a result of covenant

restrictions under our indebtedness. Investors, potential investors and other readers are urged to

consider these factors carefully in evaluating the forward-looking statements and are

cautioned not to place undue reliance on such forward-looking statements. We undertake no obligation to publicly update or revise any forward-

looking statements, whether in response to new information, futures events or otherwise, except as

otherwise required by law.

The non-GAAP financial measures contained in this presentation (including, without limitation,

EBITDA, Adjusted EBITDA, commercial margin, and variations thereof) are not measures of

financial performance calculated in accordance with U.S. GAAP and should not be considered as alternatives to net income and loss attributable to

Aleris Corporation or any other performance measure derived in accordance with GAAP or as alternatives

to cash flows from operating activities as a measure of our liquidity. Non-GAAP measures

have limitations as analytical tools and should be considered in addition to, not in isolation or as a substitute for, or as superior to, our

measures of financial performance prepared in accordance with GAAP. Management believes that certain

non-GAAP performance measures may provide investors with additional meaningful comparisons

between current results and results in prior periods. Management uses non-GAAP financial measures as performance metrics

and believes these measures provide additional information commonly used by the holders of our senior

debt securities and parties to the ABL Facility with respect to the ongoing performance of our

underlying business activities, as well as our ability to meet our future debt service, capital expenditures and working capital needs.

These adjustments are based on currently available information and certain adjustments that we believe

are reasonable and are presented as an aid in understanding our operating results. They are not

necessarily indicative of future results of operations that may be obtained by the Company.

Information regarding market and industry statistics contained in this presentation is based on

information from third party sources as well as estimates prepared by us using certain

assumptions and our knowledge of these industries. Our estimates, in particular as they relate to our general expectations concerning the aluminum

industry, involve risks and uncertainties and are subject to changes based on various factors,

including those discussed under “Risk Factors” in our filings with the Securities and

Exchange Commission. This information is current only as of its date and may have changed. We undertake no obligation to

update this information in light of new information, future events or otherwise. This

information contains certain financial projections and forecasts and other forward looking information concerning our business, prospects, financial

condition and results of operations, and we are not making any representation or warranty that this

information is accurate or complete. See “Forward-Looking Information” below.

|

Contents

Aleris Overview

Key Highlights

Financial Overview

2 |

3

3

Aleris Overview

3 |

4

Aleris’

Position in the Aluminum Value Chain

Limited exposure to upstream aluminum volatility and costs

Aleris participates in select

segments of the aluminum

fabricated products industry

4

Bauxite

mining

Alumina

refining

Aluminum

smelting

End use

applications

Recycling

Processing |

Successful History of Acquisitions

Strategic growth has led to diversity in capabilities and industries served

ALSCO

Ormet

Alumitech

EKCO

Wabash

Alloys

Corus

AE

Inc.

HT

Aluminum

Voerde

Nichols

5

2012

2013

2010

2011

2004

2009

2008

2007

2006

2005

2003

2014

2015

2016

Commonwealth Aluminum

IMCO Recycling Inc.

|

Leading Global Downstream Aluminum Company

Rolled & Extruded Products

Recycling & Specification Alloys

Business Segments:

RPNA, RPEU, RPAP, Extrusions

Global Market Segments:

-

Aerospace

-

Automotive

-

Heat Exchanger

-

Commercial Plate & Defense

Regional Industries

-

Engineering

-

Building & Construction

-

Distribution

#1 in North America building and construction

Leading player in auto body sheet in Europe

Leading player in aerospace sheet and plate globally

Business Segments:

RSAA, RSEU

Recycling

-

Packaging (can sheet)

-

Transportation

-

General Industrial

-

Deox (steel production)

Specification Alloys:

-

Auto

-

General Industrial

Global leader in merchant aluminum recycling and

supply of specification alloys in U.S. / Europe

LTM March ‘14 Adj. EBITDA: $199m

1

LTM March ‘14 Adj. EBITDA: $68m

1

1

Excludes $36M of corporate overhead

2

Year ended revenue 12/31/2013; includes intercompany revenue

Revenue:

$3.0

billion

2

Revenue:

$1.5

billion

2

RPEU

RPNA

Extrusions

RSEU

RSAA

RPAP

12%

48%

40%

37%

63%

6 |

Global Platform

North America

Europe

Key Facilities

China

Koblenz

Duffel

Specialized facilities,

high value products

Zhenjiang

Bonn

Lewisport

Uhrichsville

Richmond

Morgantown

Grevenbroich

Ability to deliver molten

aluminum

Stuttgart

Wabash

Davenport

Modern and highly efficient facilities in key countries

7

Low cost production,

maximum use of scrap |

Light-weight:

approximately 1/3 the weight of steel

Exceptional strength-to-weight

ratio

Corrosion resistant

High electrical and heat

conductivity

Highly recyclable

Consumption rises with

economic development

Leveraging Aluminum’s Value & Sustainability

Uniquely positioned to grow through sustainability

Global Drive to Sustainability

Significant customer demand for

sustainable solutions

Strong shift from Primary

Aluminum to Recycled Scrap

95% more energy efficient vs.

primary aluminum

Leader in Scrap Processing

Leader in merchant supply and

recycling for internal

consumption

Approximately 2 million tons of

scrap processed in 2013

Customer “closed loop”

relationships

Key Attributes of Aluminum

8 |

2013 Revenue

1

Serving customers in diverse industries worldwide

1.

2013 information does not include Nichols business as the transaction closed in the second quarter of

2014. 2.

Rolled Products Asia Pacific segment revenue was excluded from this chart as the segment’s

revenue was less than 1% of consolidated revenue for the year ended December 31, 2013.

Other

11%

Aerospace

10%

Automotive

32%

Heat Exchanger

6%

Europe

Building &

Construction

4%

N. America

Building &

Construction

10%

Engineering 1%

Packaging 4%

Transportation 7%

Distribution

15%

Revenue by Reportable Segment

2

Revenue by End Use

RPNA

28%

RPEU

30%

Extrusion

8%

RSAA

22%

RSEU

12%

9 |

Foundation for Growth in Place*

More than $600M committed to support growth

CHINA

$350M

DUFFEL

$70M

ASHVILLE

$20M

TIANJIN

$10M

RECYCLING

$20M

R&D INSOURCING

$30M

NICHOLS

ACQUISITION

$110M

10

2013

2014

2011

2012

2009

2010

2015

Relocated 28Mn press

from Duffel

Numerous capacity

expansion and

productivity projects

Collaboration with

customers

Proprietary alloys

Wide Coating Line

Benefit from Nichols

acquisition

250kT Hot Mill

35kT Phase 1 Plate Mill

Nadcap certification June

2014

Wide Auto Body Sheet Cold

Mill

Capturing transformational

growth opportunity

1 Hot Mill, 3 Finishing

Plants

Complementary Rolling Mill

asset base; expected

significant synergies

*Represents capital expenditure estimates from 2010 – 2014. |

11

11

Key Highlights |

Key

Highlights Strong, experienced management team

Flexible capital structure; adequate liquidity and limited amortization requirements

Significant growth investments underpin future performance

Well-positioned to benefit from economic recovery and growth in aluminum

consumption

12 |

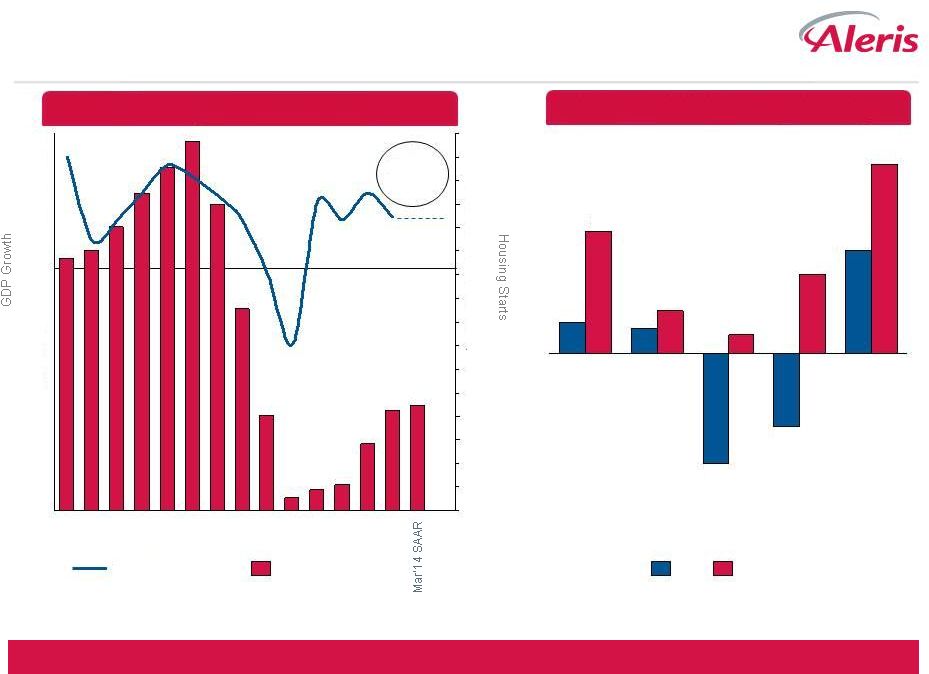

13

13

Poised to benefit from recoveries

U.S. Housing and Europe Recovery Gaining Momentum

5.0

4.0

3.0

2.0

1.0

0.0

(1.0)

(2.0)

(3.0)

(4.0)

2005

2000

2010

Housing starts (M)

US GDP Growth %

Germany

Italy

France

UK

Spain

2013

2014F

US Housing Starts & GDP Growth

EU Real GDP Growth by Country

1.7

-1.2

-1.8

0.4

0.5

3.1

1.3

0.3

0.7

2.0

Source: Barclays Economic Research – May 2014 Source:

US census for actuals, GDP actuals - US census, Barclays Economic Research – May 2014

2014 Forecast

1.9%

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1 |

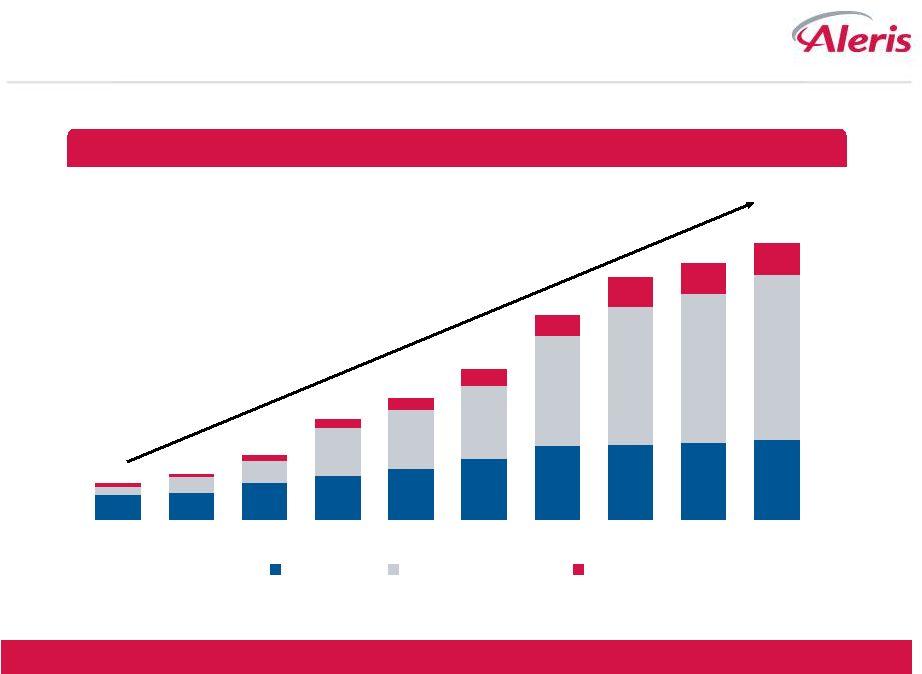

14

14

Healthy Global FRP Growth

Transportation sector leading growth; Aleris well-positioned

Transport

B&C

Industrial

CAGR ‘13-’18 (%)

China

North America

1

Western Europe

10.7%

2018

2013

1,855

3,085

5.6

15.3

3.4

5.0%

2018

2013

2,217

1,741

2.1

8.3

1.5

8.9%

2013

2,217

2018

3,392

8.1

10.3

8.9

(kT)

Source: CRU Aluminum Outlook Quarterly Report Feb 2014, Aleris Analysis |

15

15

192

812

254

Aircraft Backlogs Remain at Record Levels

+16%

11

7,966

10

6,676

09

6,484

08

6,942

07

6,443

06

4,803

05

3,899

04

2,545

YTD 14

10,532

12

8,948

Boeing

Airbus

A380

A350

A330

A320

4256

46

884

388

B747

B787

B777/767

B737

3778

Order backlog expected to support production for 6 to 8 years

13

10,610

Airbus backlog break out per AC

Boeing backlog break out per AC

Order Backlog (# planes)

Source: Airbus & Boeing reports Note: Backlog defined as Net Orders

(Gross Orders – Conversions/Cancellations) minus Deliveries |

16

16

Aluminum

Auto

Body

Sheet

–

Transformative

Opportunity

Source: IHS & Aleris internal projections

Structural shift underway

12

13

14

15

16

17

18

19

20

21

China

North America

Europe

Projected Global ABS Demand, including non-CALP Qualities (2012-2021)

|

17

17

Key Growth Initiatives

Execution on track; beginning to realize benefits

Aerospace growth and shift in

demand to Asia

Significant latent optionality

given under utilized Hot Mill

Built to exacting standards for

our Koblenz, Germany Mill

Capturing transformative shift

in automotive

Global customer base

Widest ABS Rolling Mill in

Europe

Well-timed to benefit from

housing recovery

Comparable asset base;

similar technologies

Significant synergy opportunity

NICHOLS

ACQUISITION

$110M

CHINA

$350M

DUFFEL

$70M |

18

18

Aleris Zhenjiang –

Summary Overview

World class rolling mill initially targeting value added heat-treat

plate applications, including aerospace

State-of-the-art machinery

Plant engineered to exacting German standards used in

Aleris’

Koblenz, Germany mill

Employee training conducted in Koblenz

Unmatched “know how”

and capability in China

Leverages Aleris reputation in aerospace

Significant growth options with 250kT Hot Mill capacity and

35kT annual Phase 1 plate capacity

Plate expansion

Coil and auto body sheet

Aerospace qualification agreements in place; aerospace

shipments expected 2H14

AS9100 certification achieved in 4Q13

Nadcap certification achieved 2Q14

Laser-focus on Aerospace qualification process

2324

1649

1852

1142

132

0

500

1000

1500

2000

2500

1Q14

4Q13

3Q13

2Q13

1Q13

Overview

Plant

Shipments by Qtr (T) |

19

19

Aerospace Qualification (Nadcap) Process Complete

First aerospace shipments imminent

Agreements with all 4 major OEMs (Boeing,

COMAC, Bombardier, Airbus) in place

Approval of heat treatment facilities

Accreditation of lab by OEMs underway

Produced AC plate qualification material

ISO 9001 certification

AS 9100 certification (Aerospace certification)

Implemented ultrasonic test device

Achieved Nadcap certification in 2Q14

Develop/confirm process control documents

Pass final OEM audits end 3Q14

Achievements

Next steps / Main priorities

Required to sell to

OEMs |

20

20

Duffel Automotive –

Solid Foundation for Growth

Wide Automotive Body Sheet (WABS)

1Q14 Automotive volumes increased 43% vs 1Q13

New cold rolling mill

Furnaces

Automation

$70M investment completed |

21

21

Nichols Acquisition Update

Company Overview

Key North American aluminum sheet

supplier to building & construction

and transportation industries

Four facilities

–

Davenport, IA (2)

–

Lincolnshire, IL

–

Decatur, AL

Approximately 550 employees

2013 shipments of ~300 million lbs

1

2013 fiscal results from Quanex SEC filings.

1 |

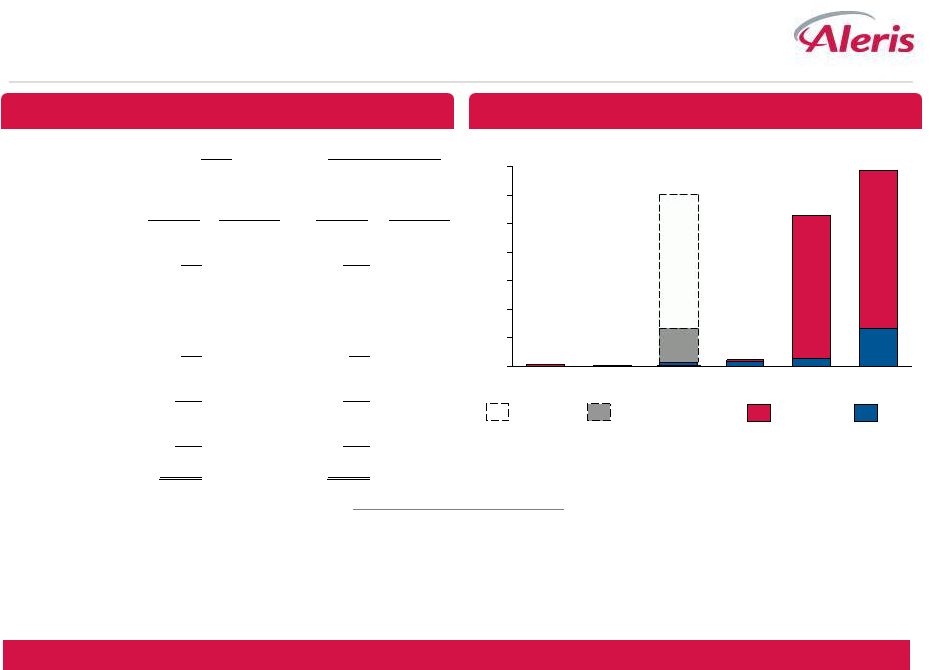

22

22

Continuous Cast Profitability Comparison

Synergistic Nichols acquisition expected to generate attractive returns

|

23

23

Experienced Management Team

Name

Title

Yrs. w/ Company

Previous Experience

Industrial Experience

Roeland Baan

Eric Rychel

Sean Stack

Chairman and CEO

EVP and CEO –

Europe

& Asia Pacific

SVP and CFO

EVP and CEO –

Rolled

Products North America

11

6

2

10

CEO of Noveon

CEO of Mittal Steel Europe

VP and Treasurer of Noveon

31

31

2

23

Steven Demetriou

Chris Clegg

Tom Weidenkopf

EVP, General Counsel and

Secretary

EVP of HR and

Communications

SVP, General Counsel and

Secretary of Noveon

SVP, HR for Honeywell

International

10

5

29

31

1

Includes years with Aleris and/or Commonwealth

John Zhu

Ingrid Joerg

SVP, President of China

3

28

China President for Wartsila

SVP and GM of RPEU

2

17

President, Alcoa FRP Europe &

Brazil

Managing Director, Barclays &

Deutsche Bank

Aleris formed in 2004 through combination of IMCO Recycling and Commonwealth Industries

Proven acquirer; successfully integrated 13 acquisitions since 2004 including Corus Aluminum

1

Successfully restructured during downturn – lowered costs and repositioned business (2008 –

2009) |

24

24

Financial Overview |

25

25

Key

Performance

Metrics

–

Total

Aleris

Volume (kT

1

)

EBITDA ($M)

1

Excludes Brazil &Voerde

Business and Earnings Drivers

Key Areas of Impact on Drivers

1963

1936

1925

2006

0

500

1,000

1,500

2,000

2,500

1Q14 LTM

2013

2011

2012

236

231

294

332

0

50

100

150

200

250

300

350

0

50

100

150

200

2011

1Q14 LTM

2013

2012

EBITDA

EBITDA $/ton

Economic recovery, growth initiatives, share gains

Quality and service, supply and demand

Growth in value-added Aero, ABS and recovery in B&C

LME, scrap availability and processing capabilities

Productivity focus, volume leverage from recovery & initiatives

Volume

Rolling margin / conversion price

Mix

Scrap and metal spreads

Cash conversion costs |

26

26

Capital Expenditures

Capital Expenditures Summary

Capital expenditures returning to normalized levels

92

112

103

100

36

113

278

135

65

12

$48

1Q14

2014E

$165

2012

$390

2011

$205

2013

$238

Maintenance

Growth |

27

27

Capital Structure and Amortization Schedule

$700

600

100

0

400

500

200

300

Thereafter

685

2018

529

2017

19

2016

611

2015

2

2014

8

China

Recourse

Revolver Funded

Revolver

Capital Structure Highlights

•

No near term amortization requirements

•

No maintenance or performance covenants unless liquidity drops substantially

•

Unsecured, except for working capital assets

1Q14 Debt Maturity Profile

1

Summary Capitalization Table

Actual

Pro Forma for Nichols¹

Net Debt -

Net Debt -

Mult of 1Q14

Mult of 1Q14

3/31/2014

LTM EBTIDA

3/31/2014

LTM EBTIDA

Cash

$51.3

$51.3

Revolver

10.0

120.0

Total Secured Debt

10.0

120.0

Senior Notes due 2018

500.0

500.0

Senior Notes due 2020

500.0

500.0

Exchangeable Notes

44.8

44.8

Other Debt

16.0

4.4 x

16.0

4.8 x

Total Recourse Debt

1,070.8

1,180.8

China Debt

191.8

5.2 x

191.8

5.6 x

Total Debt

1,262.6

1,372.6

Total Shareholders' Equity

361.3

361.3

Total Capitalization

$1,623.9

$1,733.9

1

Includes $110M for Nichols acquisition and estimated $6M for Nichols LTM EBITDA

added to Total Aleris EBITDA. Near term amortization requirements

limited |

28

28

First Quarter Performance Overview

Sequential Adjusted EBITDA improvement affirms recovering fundamentals

1Q14 Adjusted EBITDA of $59 million

Significantly higher automotive volumes

Global aerospace volumes impacted by customer destocking

North American rolled products volumes down due to MWP volatility

Weather affected volume, scrap availability and natural gas costs in NA

Improvement in Specification Alloy metal spreads |

29

29

1Q14 Volume Recap & Highlights

Volume Change vs. 1Q13

Volume Drivers

1

Excludes

2013

shipments

of

semi-finished

product

to

Zhenjiang,

China

and

from

Voerde

cast

house;

including these shipments volume was (4%).

2

Excludes impact of idling production at Saginaw, Michigan facility; including this

impact volume was (5%). RPNA

(9%)

Distribution

(11%)

-

High and volatile Midwest Premium, weather

Transportation

3%

-

Steady trailer builds

B&C

(18%)

-

Harsh winter weather; MWP volatility

RPEU / Global Market Segments

1

5%

Aerospace

(7%)

-

Customer inventory overhang

Automotive

43%

-

Premium auto builds; Aluminum penetration

Heat Exchanger

11%

-

Share gain; rebound from cycle lows

Plate & Sheet

(3%)

-

Overcapacity in plate market

Extrusions

10%

-

Improved Automotive demand; EU rebound

RSAA

2

1%

Spec / Automotive

2

5%

-

NA Auto builds

Recycling

(4%)

-

Winter weather; scrap availability

RSEU

1%

Spec / Automotive

17%

-

Improved Automotive demand

Recycling

(29%)

-

Scrap availability; furnace redeployment |

30

30

Scrap Environment Update

NA Spec Alloy Metal Spreads

RPNA Scrap Spreads

Current scrap flows recovering from winter disruptions

More dramatic winter impact in 1Q14

Decreased scrap exports

Scrap processing equip increasing flexibility

Low LME limiting scrap spreads

Increased competition for scrap

Regional premium very volatile

Mar

12

Mar

13

Mar

14

Spread Indexed to 9 Yr Avg

9 Yr Avg Spread

Winter

impact

Winter

impact

$0.70

$0.90

$1.10

$0.80

$1.00

$0.15

$0.25

$0.20

$0.30

$0.10

Mar

14

Mar

13

Mar

12

MLC Diff. to P1020

P1020 (right axis)

Ptd. Siding Diff. to P1020

0.6

0.7

0.8

0.9

1.0

1.1

1.2 |

31

31

Adjusted EBITDA Bridge

($M)

2

1Q14 vs. 1Q13 |

Key

Highlights Strong, experienced management team

Flexible capital structure; adequate liquidity and limited amortization requirements

Significant growth investments underpin future performance

Well-positioned to benefit from economic recovery and growth in aluminum

consumption

32 |

33

33

Appendix |

34

34

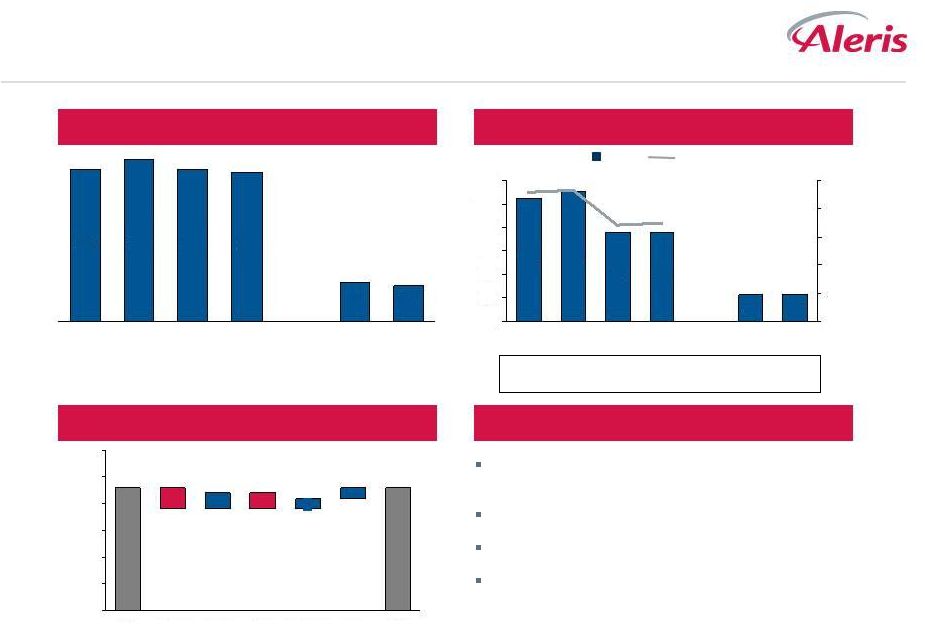

RPNA

Volume (kT)

Adjusted EBITDA

1Q14 Performance

1Q Adjusted EBITDA Bridge ($M)

2011

1Q14

1Q13

LTM

2013

2012

23

2

2

3

3

4

23

1Q14

1Q13

LTM

2013

2012

2011

Adj. EBITDA / ton

283

281 205 209 246

269

Adjusted EBITDA ($M)

EBITDA as % of Commercial Margin

Lower volumes due to weather and Midwest Premium

volatility

Tighter scrap spreads and availability

MWP impact on lower priced inventory

Productivity partly offset inflation

1Q14

Other

Productivity

Inflation

Margin /

Scrap

Spreads

Volume /

Mix

1Q13

371

396

364

86

95

372

105

111

76

23

23

76

0%

5%

10%

15%

20%

25%

0

20

40

60

80

100

120

30

20

10

5

15

0

25 |

35

35

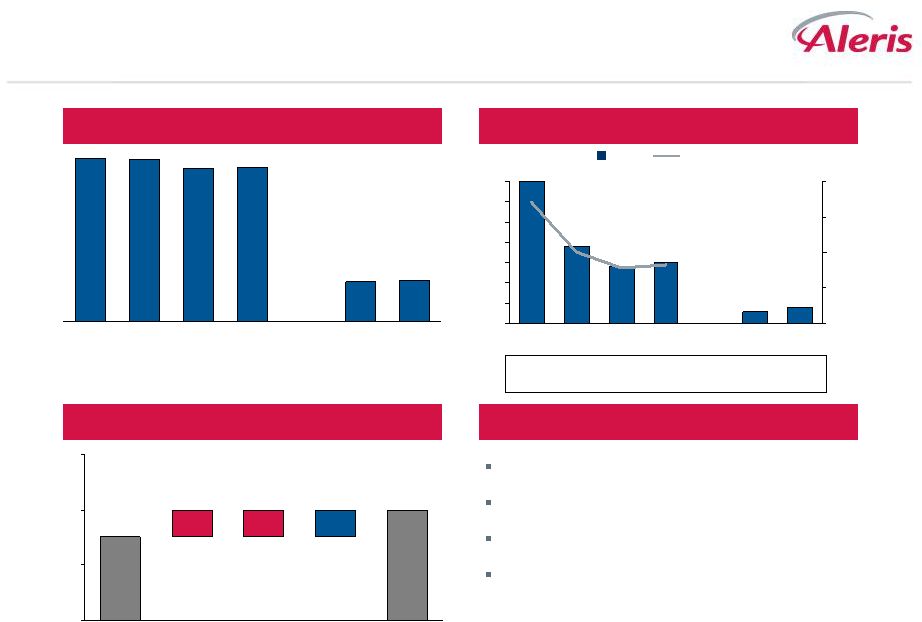

RPEU

Volume (kT)

Adjusted EBITDA

1Q14 Performance

1Q Adjusted EBITDA Bridge ($M)

314

299

342

87

90

345

1Q14

1Q13

LTM

2013

2012

2011

20

25

30

35

40

3

Price

2

Volume/Mix

1

1Q13

34

30

1Q14

Currency

3

Productivity

Margin/Scrap Inflation

spreads

2

3

152

112

30

34

137

115

0

50

100

150

200

10%

15%

20%

25%

30%

1Q14

1Q13

2013

LTM

2012

2011

Adj. EBITDA / ton

482

457 334 327 374

349

Adjusted EBITDA ($M)

EBITDA as % of Commercial Margin

Strong volume growth in Automotive

Aerospace impacted by customer destocking

Recovering regional plate and sheet pricing

Higher costs for aluminum slabs

Weaker U.S. Dollar impacted margins & AR |

36

36

Extrusions

Volume (kT)

Adjusted EBITDA

1Q14 Performance

1Q Adjusted EBITDA Bridge ($M)

0

2

4

1Q14

3

Productivity

1

Inflation

Volume/Mix

1Q13

2

8

14

11

3

2

11

0

2

4

6

8

10

12

14

0%

2%

4%

6%

8%

10%

LTM

2013

2012

2011

1Q13

1Q14

Adj. EBITDA / ton

104

202 159 158

137 134 Adjusted EBITDA ($M)

EBITDA as % of Commercial Margin

Volume growth in automotive projects

Productivity offset inflation

Continuing to gain momentum; well positioned for

recovery

76

68

71

19

17

69

LTM

2013

2012

2011

1Q14

1Q13

1

1 |

37

37

RSAA

Volume (kT)

Adjusted EBITDA

1Q14 Performance

1Q Adjusted EBITDA Bridge ($M)

895

868

847

206

217

857

1Q14

LTM

2013

2012

2011

1Q13

6

8

10

12

1Q14

9

Inflation

3

Margin/Scrap

spreads

3

1Q13

10

LTM

2012

2011

1Q14

1Q13

2013

Adj. EBITDA / ton

90

62 63 62

48 43

Adjusted EBITDA ($M)

EBITDA as % of Commercial Margin

Continued improvement in YoY metal spreads

Higher automotive volumes

Harsh winter weather had significant impact on natural

gas costs, scrap availability, operations and caused

numerous lost shipping days

1

Volume /

Mix

100

25%

60

40

20

80

0

20%

0%

15%

10%

5%

81

54

54

52

10

9 |

38

38

RSEU

Volume (kT)

Adjusted EBITDA

1Q14 Performance

1Q Adjusted EBITDA Bridge ($M)

387

385

365

96

95

364

LTM

2013

2012

2011

1Q14

1Q13

0

2

4

6

1Q14

4

Productivity

1

Inflation

1

Margin/Scrap

spreads

1

1Q13

3

35

15

4

3

19

14

0

5

10

15

20

25

30

35

0%

5%

10%

15%

20%

LTM

2013

2012

2011

1Q13

1Q14

Adj. EBITDA / ton

91

50 39 42

34 45

Adjusted EBITDA ($M)

EBITDA as % of Commercial Margin

Slightly higher volumes

Redeployed furnace to support customer demand

Continued improvement in metal spreads

Productivity offset inflation |

39

39

Limited Commodity Exposure

Robust risk management processes

Balances credit lines and reduces

liquidity risk

Risk

Mitigation

Expected Impact

Match physical purchases

Eliminate LT fixed price sales

Forward purchase LME

LME volatility

Business model

Pass thru pricing

Tolling

Pass thru pricing-tolling

Forward buy / hedge

Revenue and margin % volatility

Minimal earnings impact

No hedge accounting treatment

Locks in rolling margin

Reduce multi-year dated derivatives

Maintains toll margin

Fixes costs

Reduces FIFO “metal lag”

volatility

Balances hedge book and counter

party exposures

Active position management

Counterparty Management

Forward price sales

Energy

Inventory exposure

Sell open inventory forward |

40

40

2011 –

1Q14 LTM Adjusted EBITDA Reconciliation

LTM

1Q 2014

2013

2012

2011

Adjusted EBITDA

230.9

$

236.2

$

293.6

$

331.6

$

Reorganization items, net

-

-

-

1.3

Unrealized gains on derivative financial instruments

(18.9)

0.7

14.3

(37.8)

Impact of recording assets at fair value through fresh-start and purchase accounting

0.1

0.1

0.9

(3.4)

Restructuring gains (charges)

(10.3)

(10.7)

(9.6)

(4.4)

Unallocated currency exchange (losses) gains on debt

(2.4)

(2.9)

0.8

(0.7)

Stock-based compensation expense

(12.8)

(14.3)

(11.4)

(10.1)

Start-up expenses

(32.8)

(35.8)

(27.4)

(10.2)

Favorable metal price lag

16.6

23.0

16.0

18.9

Other

(11.7)

(8.6)

(7.1)

(11.2)

EBITDA

158.7

187.7

270.1

274.0

Loss (income from discontinued operations)

-

-

-

-

Interest expense, net

(103.2)

(97.9)

(52.4)

(46.3)

Benefit from (provision for) income taxes

4.6

2.6

(25.4)

4.2

Depreciation and amortization

(135.5)

(129.5)

(84.8)

(70.3)

Net (loss) income attributable to Aleris Corporation

(65.6)

(37.1)

107.5

161.6

Net income (loss) attributable to noncontrolling interest

0.9

1.0

(0.5)

(0.4)

Net (loss) income

(64.7)

$

(36.1)

$

107.0

$

161.2

$

For the years ended

December 31, |

41

41

1Q 2014 Adjusted EBITDA Reconciliation

March 31, 2014

March 31, 2013

Adjusted EBITDA

59.2

$

64.5

$

Unrealized (losses) gains on derivative financial

instruments (9.3)

10.3

Restructuring charges

(0.5)

(0.9)

Unallocated currency exchange

losses on debt -

(0.5)

Stock-based compensation

expense (4.2)

(2.7)

Start-up expenses

(8.4)

(11.4)

Favorable metal price lag

12.0

5.6

Other

(2.6)

0.5

EBITDA

46.2

65.4

Interest expense, net

(26.3)

(21.0)

Provision for income taxes

(4.3)

(6.3)

Depreciation and

amortization (33.2)

(27.2)

Net (loss) income attributable to Aleris

Corporation (17.6)

10.9

Net income attributable to

noncontrolling interest 0.3

0.4

Net (loss) income

(17.3)

11.3

Depreciation and amortization

33.2

27.2

Provision for deferred income

taxes 0.5

1.0

Stock-based

compensation expense 4.2

2.7

Unrealized losses (gains)

on derivative financial instruments 9.3

(10.3)

Currency exchange losses on debt

0.3

0.4

Amortization of debt

issuance costs 2.0

1.9

Other

1.1

(2.1)

Change in operating assets and

liabilities: Change in accounts receivable

(83.5)

(105.5)

Change in inventories

(11.1)

(14.1)

Change in other assets

2.3

(12.0)

Change in accounts payable

90.3

52.2

Change in accrued liabilities

(3.5)

(8.3)

Net cash provided by operating

activities 27.8

$

(55.6)

$

For the three months ended

(in millions) |

42

42

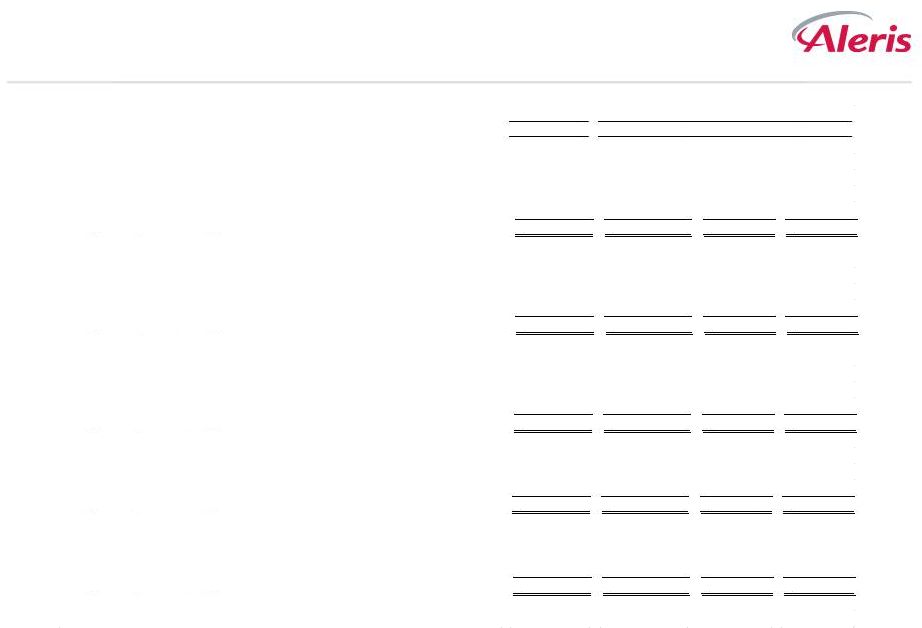

1Q14 & 1Q13 Adjusted EBITDA Reconciliation by Segment

March 31, 2014

March 31, 2013

RPNA

Segment income

26.9

$

23.5

$

Favorable metal price

lag (3.7)

(0.1)

Segment

Adjusted EBITDA (1) 23.2

$

23.4

$

RPEU

Segment income

38.1

$

38.5

$

Impact of recording amounts

at fair value through fresh-start and purchase accounting -

-

Favorable metal price lag

(7.9)

(4.8)

Segment

Adjusted EBITDA (1) 30.3

$

33.6

$

RPAP

Segment loss

-

$

(0.3)

$

Segment Adjusted EBITDA

(2) -

(0.3)

Extrusions

Segment income

3.0

$

3.0

$

Favorable metal

price lag (0.5)

(0.6)

Segment

Adjusted EBITDA (1) 2.6

$

2.4

$

RSAA

Segment income

9.0

$

10.4

$

Segment Adjusted EBITDA

(2) 9.0

10.4

RSEU

Segment income

4.3

$

3.3

$

Segment

Adjusted EBITDA (2) 4.3

3.3

(1)

Amounts may not foot as they represent the calculated totals based on actual amounts and not the rounded amounts presented in this table.

(2) There was no difference between segment income and segment Adjusted EBITDA for this

segment. For the three months ended |

43

43

2011 –

1Q14 LTM Adjusted EBITDA Reconciliation by Segment

LTM

March 31, 2014

2013

2012

2011

RPNA

Segment income

85.2

$

81.8

$

117.6

$

111.1

$

Impact of recording amounts at fair value through fresh-start and purchase

accounting -

-

-

-

Favorable metal price lag

(9.2)

(5.6)

(6.4)

(6.2)

Segment Adjusted EBITDA (1)

76.0

$

76.2

$

111.1

$

104.9

$

RPEU

Segment income

131.7

$

132.1

$

144.6

$

157.6

$

Impact of recording amounts at fair value through fresh-start and purchase

accounting (0.1)

(0.1)

(0.8)

3.8

Favorable metal price lag

(19.7)

(16.6)

(7.1)

(9.9)

Segment Adjusted EBITDA

112.0

$

115.3

$

136.7

$

151.5

$

Extrusions

Segment (loss) income

11.7

$

11.7

$

16.4

$

10.9

$

Impact of recording amounts at fair value through fresh-start and purchase

accounting -

-

(0.1)

(0.3)

Unfavorable (favorable) metal price lag

(0.6)

(0.7)

(2.6)

(2.7)

Segment Adjusted EBITDA (1)

11.2

$

11.0

$

13.8

$

7.9

$

RSAA

Segment income

52.6

$

54.0

$

53.6

$

80.9

$

Impact of recording amounts at fair value through fresh-start and purchase

accounting -

-

-

-

Segment Adjusted EBITDA

52.6

$

54.0

$

53.6

$

80.9

$

RSEU

Segment income

15.3

$

14.3

$

19.4

$

35.3

$

Impact of recording amounts at fair value through fresh-start and purchase

accounting -

-

-

-

Segment Adjusted EBITDA

15.3

$

14.3

$

19.4

$

35.3

$

(1) Amounts

may

not

foot

as

they

represent

the

calculated

totals

based

on

actual

amounts

and

not

the

rounded

amounts

presented

in

this

table.

(in millions)

For the years ended December 31, |