Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - Transocean Partners LLC | d715676dex231.htm |

| EX-3.1 - EX-3.1 - Transocean Partners LLC | d715676dex31.htm |

| EX-23.6 - EX-23.6 - Transocean Partners LLC | d715676dex236.htm |

| EX-23.5 - EX-23.5 - Transocean Partners LLC | d715676dex235.htm |

Table of Contents

As filed with the Securities and Exchange Commission on June 20, 2014

Registration Statement No. 333-

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Transocean Partners LLC

(Exact name of registrant as specified in its charter)

| Republic of the Marshall Islands | 1381 | 66-0818288 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

Transocean Deepwater House

Kingswells Causeway

Prime Four Business Park

Aberdeen, AB15 8PU

Scotland

United Kingdom

+44 1224 654436

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Jill S. Greene

Transocean Deepwater House

Kingswells Causeway

Prime Four Business Park

Aberdeen, AB15 8PU

Scotland

United Kingdom

+44 1224 654436

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Gene J. Oshman Joshua Davidson Andrew J. Ericksen Baker Botts L.L.P. 910 Louisiana Houston, Texas 77002 (713) 229-1234 |

Catherine S. Gallagher Adorys Velazquez Vinson & Elkins L.L.P. 2200 Pennsylvania Avenue NW Suite 500W Washington, DC 20037 (202) 639-6500 |

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||||

| Non-accelerated filer | ¨ | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||||

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Offering Price(1)(2) |

Amount of Registration Fee | ||

| Common units representing limited partner interests |

$350,000,000 | $45,080 | ||

|

| ||||

|

| ||||

| (1) | Includes common units issuable upon exercise of the underwriters’ option to purchase additional common units. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o). |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state or jurisdiction where the offer or sale is not permitted.

PROSPECTUS

Subject To Completion, dated June 20, 2014

Common Units

Representing Limited Liability Company Interests

This is the initial public offering of Transocean Partners LLC. Transocean Partners Holdings Limited, or the selling unitholder, is offering common units representing limited liability company interests in this offering. We will not receive any proceeds from the sale of common units by the selling unitholder. Prior to this offering, there has been no public market for our common units.

We are a Marshall Islands limited liability company formed by an affiliate of Transocean Ltd., or Transocean, a leading international provider of offshore contract drilling services for oil and gas wells. We will be treated as a corporation for U.S. federal income tax purposes. We intend to apply to list the common units on the New York Stock Exchange under the symbol “RIGP.” We are an “emerging growth company,” and we are eligible for reduced reporting requirements. See “Summary—Implications of Being an Emerging Growth Company.”

Investing in our common units involves a high degree of risk. Before buying any common units, you should carefully read the discussion of material risks of investing in our common units in “Risk Factors” beginning on page 19.

These risks include the following:

| • | We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses to enable us to pay the minimum quarterly distribution on our units. |

| • | We must make substantial capital and operating expenditures to maintain the operating capacity of our fleet, which will reduce cash available for distribution. |

| • | Financing agreements containing operating and financial restrictions and other covenants may restrict our business and financing activities. |

| • | We currently derive all of our revenues from two customers, and the loss of either of these customers or a dispute that leads to a loss of a customer could have a material adverse impact on our financial condition, results of operations and cash flows. |

| • | Any limitation in the availability or operation of any of our three drilling rigs, or the inability to obtain new and favorable contracts for the drilling rigs upon any termination or expiration, could have a material adverse effect on us. |

| • | We depend on affiliates of Transocean to assist us in operating and expanding our business. |

| • | Unitholders have limited voting and other rights. |

| • | Transocean and its affiliates own a controlling interest in us, have conflicts of interest and may favor their own interests to the detriment of us and our other common unitholders. |

| • | You will experience immediate and substantial dilution of $ per common unit. |

| • | A change in tax laws, treaties or regulations, or their interpretation, of any country in which we are resident or in which we have operations, or a loss of a major tax dispute or a successful tax challenge to our intercompany pricing policies in certain countries, could have a material adverse impact on our financial condition, results of operations and cash flows. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per |

Total |

|||||||

| Public offering price |

$ | $ | ||||||

| Underwriting discount(1) |

$ | $ | ||||||

| Proceeds to the selling unitholder (before expenses) |

$ | $ | ||||||

| (1) | Excludes a structuring fee equal to 0.5% of the gross proceeds of this offering payable by the selling unitholder to Morgan Stanley & Co. LLC and Barclays Capital Inc. Please read “Underwriting.” |

The selling unitholder has granted the underwriters a 30-day option to purchase up to an additional common units on the same terms and conditions as set forth above if the underwriters sell more than common units in this offering.

The underwriters expect to deliver the common units to purchasers on or about , 2014 through the book-entry facilities of The Depository Trust Company.

| Morgan Stanley | Barclays |

Prospectus dated , 2014

Table of Contents

[Cover art to be filed by amendment.]

Table of Contents

You should rely only on the information contained in this prospectus or in any free writing prospectus we may authorize to be delivered to you. Neither we, the selling unitholder nor the underwriters have authorized anyone to provide you with additional or different information. If anyone provides you with different or inconsistent information, you should not rely on it. Neither we, the selling unitholder nor the underwriters are making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

i

Table of Contents

| Adjustment to the Minimum Quarterly Distribution and Target Distribution Levels |

81 | |||

| 82 | ||||

| 84 | ||||

| 86 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

87 | |||

| 87 | ||||

| 88 | ||||

| 88 | ||||

| 91 | ||||

| 96 | ||||

| 99 | ||||

| 99 | ||||

| 103 | ||||

| 104 | ||||

| 105 | ||||

| 105 | ||||

| 107 | ||||

| 109 | ||||

| 110 | ||||

| 111 | ||||

| 114 | ||||

| 115 | ||||

| 116 | ||||

| 118 | ||||

| 118 | ||||

| 119 | ||||

| 120 | ||||

| 121 | ||||

| 122 | ||||

| 124 | ||||

| 125 | ||||

| 127 | ||||

| 127 | ||||

| 127 | ||||

| 127 | ||||

| 128 | ||||

| 128 | ||||

| 128 | ||||

| 133 | ||||

| 133 | ||||

| 133 | ||||

| 133 | ||||

| 135 | ||||

| 135 | ||||

| 136 | ||||

| 136 | ||||

| 137 | ||||

| 137 | ||||

| 137 | ||||

| 138 | ||||

| 138 | ||||

| 138 | ||||

| 139 |

ii

Table of Contents

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

140 | |||

| 142 | ||||

| 143 | ||||

| Distributions and Payments to the Transocean Member and Its Affiliates |

143 | |||

| 144 | ||||

| Procedures for Review, Approval and Ratification of Related Person Transactions |

152 | |||

| 153 | ||||

| 153 | ||||

| 157 | ||||

| 161 | ||||

| 161 | ||||

| 161 | ||||

| 161 | ||||

| 163 | ||||

| 163 | ||||

| 163 | ||||

| 163 | ||||

| 163 | ||||

| 163 | ||||

| 165 | ||||

| 166 | ||||

| 167 | ||||

| 167 | ||||

| 167 | ||||

| 169 | ||||

| Special Vote Required for Combinations with Interested Unitholders |

170 | |||

| 171 | ||||

| 171 | ||||

| 172 | ||||

| 173 | ||||

| 173 | ||||

| 173 | ||||

| 174 | ||||

| 174 | ||||

| 174 | ||||

| 176 | ||||

| 176 | ||||

| 176 | ||||

| 177 | ||||

| 177 | ||||

| 177 | ||||

| 177 | ||||

| 178 | ||||

| 178 | ||||

| Our Limited Liability Company Agreement and Registration Rights |

178 | |||

| 179 | ||||

| 179 | ||||

| 180 | ||||

| 180 | ||||

| 180 | ||||

| 184 | ||||

| 185 | ||||

| 185 | ||||

| 185 |

iii

Table of Contents

| 187 | ||||

| 187 | ||||

| 187 | ||||

| 189 | ||||

| 192 | ||||

| 192 | ||||

| 192 | ||||

| 195 | ||||

| 195 | ||||

| 195 | ||||

| 196 | ||||

| 196 | ||||

| F-1 | ||||

| APPENDIX A—Form of First Amended and Restated Limited Liability Agreement of Transocean Partners LLC |

A-1 | |||

| B-1 |

iv

Table of Contents

This summary provides a brief overview of information contained elsewhere in this prospectus. It does not contain all of the information that you should consider before investing in the common units. You should carefully read the entire prospectus, including “Risk Factors” and the historical and pro forma financial statements and accompanying notes included elsewhere in this prospectus, before investing in our common units. Unless we otherwise specify, all references to information and data in this prospectus about our business and fleet refer to our business and fleet immediately after the closing of this offering. Unless otherwise indicated, the information in this prospectus assumes (i) an initial public offering price of $ per unit (the midpoint of the price range set forth on the cover of this prospectus) and (ii) that the underwriters do not exercise their option to purchase additional common units. Unless otherwise indicated, all references to “dollars” and “$” in this prospectus are to, and amounts are presented in, U.S. Dollars.

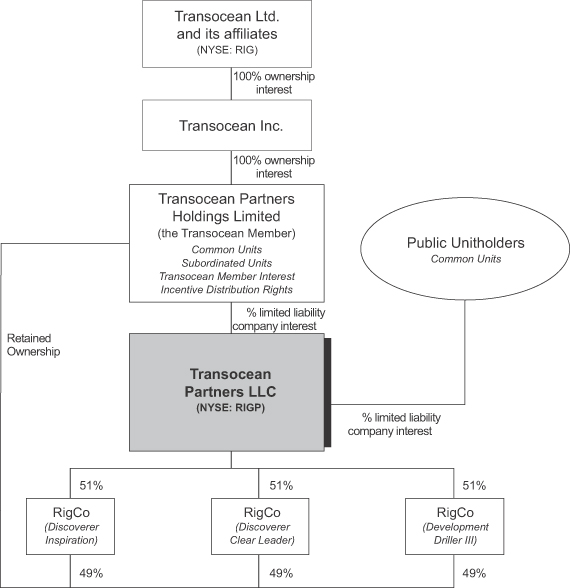

All references in this prospectus to “Transocean Partners,” “we,” “our,” “us,” and “the company” refer to Transocean Partners LLC and its subsidiaries, including the RigCos, unless the context otherwise indicates. We will own a 51 percent interest and Transocean will own a 49 percent noncontrolling interest in each of the entities that own and operate Discoverer Inspiration, Discoverer Clear Leader and Development Driller III. Each of these drilling rigs will be owned by and operated by separate subsidiaries of ours. We refer to the rig-owning and rig-operating company for each drilling rig together as a “RigCo” and collectively for all of our drilling rigs as the “RigCos.” References in this prospectus to our fleet, refer to the drilling rigs in which we hold interests indirectly through the RigCos. Unless otherwise specifically noted, financial results and operating data are shown on a 100 percent basis and are not adjusted to reflect Transocean’s 49 percent noncontrolling interest in the RigCos.

References in this prospectus to “Transocean” refer, depending on the context, to Transocean Ltd. (NYSE: RIG, SIX: RIGN) and/or to any one or more of its direct and indirect subsidiaries, other than us. References in this prospectus to “Transocean Member” refer to the owner of the Transocean Member interest, initially Transocean Partners Holdings Limited, the selling unitholder in this offering and an indirect wholly owned subsidiary of Transocean Ltd. The Transocean Member interest is a non-economic interest in Transocean Partners that includes the right to appoint three members of our board of directors. References in this prospectus to “Chevron” and “BP” refer to the subsidiaries of Chevron Corporation and BP plc, respectively, that are our customers. We have provided definitions for some of the terms we use to describe our business and industry and other terms used in this prospectus in the “Glossary of Terms” beginning on page B-1 of this prospectus.

We are a growth-oriented limited liability company recently formed by Transocean, one of the world’s largest offshore drilling contractors, to own, operate and acquire modern, technologically advanced offshore drilling rigs. Our initial assets consist of 51 percent interests in the RigCos that own and operate three ultra-deepwater drilling rigs that are currently operating in the U.S. Gulf of Mexico. Transocean owns the remaining 49 percent noncontrolling interest in each of the RigCos. We generate revenue through contract drilling services, which involves contracting our mobile offshore drilling fleet, related equipment and work crews on a dayrate basis to large international energy companies to drill oil and gas wells.

Our drilling rigs currently operate under long-term contracts with Chevron and BP, two leading international energy companies, with an average remaining contract term of approximately 4.2 years as of June 16, 2014. We believe that our drilling contracts will generate stable and reliable cash flows over their term. We intend to use the relationships and expertise of Transocean to re-contract our fleet when the existing contracts expire and identify opportunities to expand our fleet through acquisitions.

1

Table of Contents

The following table provides information about the rigs in our initial fleet:

| Our Interest |

Year Entered Service |

Water Depth (feet) |

Drilling Depth (feet) |

Location | Current Contract Terms, Dayrates and Customers | |||||||||||||||||||||||

| Rig Name |

Start Date(1) | Completion Date(1) |

Dayrate(2) | Customer | ||||||||||||||||||||||||

| Drillships |

||||||||||||||||||||||||||||

| Discoverer Inspiration |

51 | % | 2010 | 12,000 | 40,000 | USA (Gulf of Mexico) |

March 2010 April 2015 |

March 2015 April 2020 |

$ $ |

526,000 585,000 |

|

Chevron Chevron | ||||||||||||||||

| Discoverer Clear Leader |

51 | % | 2009 | 12,000 | 40,000 | USA (Gulf of Mexico) |

August 2009 September 2014 |

September 2014 September 2018 |

$ $ |

569,000 590,000 |

(3)

|

Chevron Chevron | ||||||||||||||||

| Semisubmersible |

||||||||||||||||||||||||||||

| Development Driller III |

51 | % | 2009 | 7,500 | 35,000 | USA (Gulf of Mexico) |

November 2009 | November 2016 | $ | 428,000 | BP | |||||||||||||||||

| (1) | Contract start and completion dates are estimated. Contracts could be longer in duration because of a provision that allows the customer to finish drilling a well-in-progress and due to other factors not under our control. New contracts do not commence until the prior contract has been completed. |

| (2) | Represents the maximum contractual operating dayrate (which could change in the future due to cost escalations), but excludes amortization of drilling contract intangible revenues and certain cash and non-cash pre-operating revenues that terminate at the end of the rigs’ current contracts. For a description of amortizing revenues included in the dayrates presented in this table, please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Performance and Other Key Indicators—Contract Backlog.” |

| The average dayrate actually earned over the term of the contract will reflect various reduced rates received under the contract as a result of time billed according to standby rates, waiting-on-weather rates, maintenance rates or any other similar rates, which are typically less than the contract dayrate. In addition, the amount shown does not reflect incentive programs, which are typically based on the rig’s operating performance against a performance curve. For the three months ended March 31, 2014, average daily revenue was $533,200, $579,700 and $467,200 for Discoverer Inspiration, Discoverer Clear Leader and Development Driller III, respectively, and the revenue efficiency of the rigs in our initial fleet was 98 percent. For the year ended December 31, 2013, average daily revenue was $500,700, $450,500 and $416,100 for Discoverer Inspiration, Discoverer Clear Leader and Development Driller III, respectively, and the revenue efficiency of the rigs in our initial fleet was 86 percent. For additional information about average daily revenue earned and revenue efficiency in historical periods, please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Performance and Other Key Indicators.” |

| (3) | The dayrate for the remainder of the contract is linked to the standard West Texas Intermediate crude oil price with a floor of $40 per barrel resulting in a contract dayrate of $400,000 and a ceiling of $70 per barrel resulting in a contract dayrate of $500,000, before cost escalation adjustments of $50,000 per day and pre-operating revenues of $19,000 per day. |

For the three months ended March 31, 2014, we had operating revenues of $148 million, net income of $63 million and Adjusted EBITDA of $72 million. For the year ended December 31, 2013, we had operating revenues of $526 million, net income of $189 million and Adjusted EBITDA of $221 million. Please read “—Non-GAAP Measures” and “Selected Historical Financial and Operating Data—Non-GAAP Measures” for the definition of the term Adjusted EBITDA and a reconciliation of Adjusted EBITDA to net income, the most directly comparable financial measure calculated and presented in accordance with U.S. generally accepted accounting principles, or U.S. GAAP.

2

Table of Contents

Our Relationship with Transocean

One of our principal strengths is our relationship with Transocean. Transocean is a leading international provider of offshore contract drilling services for oil and gas wells. As of June 16, 2014, Transocean owned or had partial ownership interests in and operated 77 mobile offshore drilling units, including our initial drilling rigs. As of June 16, 2014, Transocean’s fleet, including the rigs in our fleet, consisted of 46 high-specification floaters (ultra-deepwater, deepwater and harsh environment semisubmersibles and drillships), 21 midwater floaters and 10 high-specification jackups. At such date, Transocean also had nine ultra-deepwater drillships and five high-specification jackups under construction or under contract to be constructed.

We believe that our relationship with Transocean will provide us with access to leading international energy companies, as well as suppliers and other key service providers for our industry. We also believe that Transocean’s operational and managerial expertise will enable us to compete more effectively for contract opportunities than other contract drilling companies similar in size to us.

Under an omnibus agreement to be entered into at the closing of this offering, Transocean will grant us a right of first offer for its remaining ownership interests in each of the RigCos should Transocean decide to sell such interests. Transocean also will be required to offer us the opportunity to purchase not less than a 51 percent interest in four of the six drillships listed below within the five years following the closing of this offering at a purchase price equal to the greater of the fair market value (taking into account the anticipated cash flows under the associated drilling contracts) or the all-in construction cost, plus transaction costs. Transocean will select which of these rigs it will offer to us, the timing of the offers and whether it will offer us the opportunity to purchase a greater than 51 percent interest in any offered rig.

| Expected Construction Completion |

Water Depth (feet) |

Drilling Depth (feet) |

Location | Current Contract Term, Dayrate and Customers | ||||||||||||||||||

| Rig Name |

Start Date(1) | Completion Date(1) |

Dayrate(2) | Customer | ||||||||||||||||||

| Deepwater Invictus |

Q2 2014 | 12,000 | 40,000 | USA (Gulf of Mexico) |

Q3 2014 | Q2 2017 | $ | 595,000 | BHP Billiton | |||||||||||||

| Deepwater Thalassa |

Q1 2016 | 12,000 | 40,000 | TBA | Q1 2016 | Q4 2025 | $ | 519,000 | Shell | |||||||||||||

| Deepwater Proteus |

Q2 2016 | 12,000 | 40,000 | TBA | Q2 2016 | Q2 2026 | $ | 519,000 | Shell | |||||||||||||

| Deepwater Pontus |

Q1 2017 | 12,000 | 40,000 | TBA | Q1 2017 | Q4 2026 | $ | 519,000 | Shell | |||||||||||||

| Deepwater Poseidon |

Q2 2017 | 12,000 | 40,000 | TBA | Q2 2017 | Q2 2027 | $ | 519,000 | Shell | |||||||||||||

| Deepwater Conqueror |

Q4 2016 | 12,000 | 40,000 | USA (Gulf of Mexico) |

Q4 2016 | Q4 2021 | $ | 599,000 | Chevron | |||||||||||||

| (1) | Contract start and completion dates are estimated. Contract start dates depend on delivery by shipyards, testing and customer acceptance. Contracts could be longer in duration because of a provision that allows the customer to finish drilling a well-in-progress and due to other factors not under our control. |

| (2) | Represents the maximum contractual operating dayrate. The average dayrate actually earned over the term of the contract will reflect various reduced rates received under the contract as a result of time billed according to standby rates, waiting-on-weather rates, maintenance rates or any other similar rates, which typically are less than the contract dayrate. In addition, the amount shown does not reflect incentive programs, which are typically based on the rig’s operating performance against a performance curve. Each of these drilling rigs is currently under construction and, therefore, has no operating history. |

In addition, subject to specified exceptions, Transocean will be required to offer us the opportunity to purchase any drilling rigs that Transocean acquires or contracts to build after the closing date of this offering that are subject to a drilling contract with a remaining term of five years or longer, and any existing drilling rigs in its fleet that entered into service in 2009 or later and are placed under an extension or a new drilling contract with a term of five years or longer. In addition, we generally will agree not to acquire, own, operate or contract for

3

Table of Contents

certain drilling rigs operating under drilling contracts of less than five years. Relatively few drilling contracts have a term of five years or greater, particularly in the case of contracts that are not associated with newbuild units. As a result, we expect that Transocean will effectively have a right of first refusal on most drilling contract opportunities. Please read “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Omnibus Agreement.”

The consummation and timing of any acquisitions from Transocean will depend upon, among other things, our ability to obtain any necessary consents, the determination that the acquisition is appropriate for our business at that particular time, our ability to agree on mutually acceptable terms of purchase, including price, and our ability to obtain financing on acceptable terms.

Following this offering, Transocean will retain a significant interest in us through its ownership of common and subordinated units, representing an aggregate percent limited liability company interest in us, and all of our incentive distribution rights. We believe that Transocean is motivated to facilitate the growth of our distributions per unit, including through future contribution or sales to us of additional rigs and its remaining interests in each of the RigCos. In addition to the drillships discussed above, Transocean has a number of newer rigs that are operating under long-term drilling contracts and rigs under construction. Although Transocean is not obligated to offer these rigs to us, we believe that these rigs would be particularly suitable for future contribution or sale to us.

Our primary business objectives are to operate and maintain our fleet to generate stable cash flows and increase our quarterly cash distributions per unit over time. We intend to accomplish these objectives by executing the following business strategies:

| • | Grow through strategic acquisitions. We intend to pursue strategic opportunities to grow our company and fleet through acquisitions from Transocean or third parties that will enable us to increase our quarterly distributions per unit. Pursuant to the omnibus agreement, Transocean will be required, under certain circumstances, to offer us the opportunity to purchase its remaining interests in one or more of the RigCos, as well as certain drilling rigs (including a majority ownership interest in four of the ultra-deepwater drillships that are currently under construction and are supported by long-term contracts). |

| • | Pursue assets with contracts that help maintain stable cash flows. We are focused on generating and maintaining stable cash flows by pursuing drilling rigs operated under long-term contracts with creditworthy counterparties. We believe that employing our rigs under long-term contracts will improve the stability and predictability of our cash flows and should also contribute to our growth strategy by facilitating our access to debt and equity financing. We also believe that our relationship with Transocean will enhance our ability to compete for contract opportunities. |

| • | Conduct safe, efficient and reliable operations. We participate in Transocean’s programs designed to maintain and improve the safety, reliability and efficiency of all our operations, which are vital to our ability to retain and attract our customers. We believe that our relationship with Transocean and our relatively young and high-specification fleet will enable us to operate safely, efficiently and cost effectively. We expect that these factors will enhance our ability to secure additional long-term contracts and extend existing contracts, enabling us to maintain high asset utilization. |

| • | Maintain a modern and reliable fleet. We have one of the most capable and technologically advanced fleets in the industry. We plan to invest both in growing our modern and reliable fleet and in continually maintaining the quality and operational integrity of our assets. We believe that investing in high-quality assets with proven and reliable drilling rig technology is an important component in our strategy to provide our customers with safe and reliable operations and services. |

4

Table of Contents

We believe we are well positioned to execute our business strategies based on the following competitive strengths:

| • | Relationship with Transocean provides industry expertise and facilitates our growth strategy. Transocean specializes in operations in technically demanding regions of the global offshore drilling industry with a particular focus on ultra-deepwater and harsh environment drilling services. Transocean believes its mobile offshore drilling fleet is one of the most versatile fleets in the world, consisting of drillships, semisubmersibles and high-specification jackups used in support of offshore drilling activities and offshore support services on a worldwide basis. We believe that our relationship with Transocean will facilitate our acquisition and growth strategy, provide access to premier customers and suppliers and allow us to capitalize on Transocean’s operational expertise. In addition, we believe that our relationship with Transocean will assist us in securing new contracts for our rigs as we complete our current contracts. We believe Transocean’s history as an efficient and reliable contractor and its operational and management expertise will enhance our ability to obtain new long-term contracts. |

| • | Long-term contracts with high-quality customers promote stable cash flows. All of our revenues and associated cash flows are derived from our existing long-term contracts. Our rigs are contracted to high-quality, creditworthy customers for an average remaining contract term of approximately 4.2 years as of June 16, 2014. Our drilling contracts provide for payment on a fixed-dayrate basis for the applicable contract term. We believe these agreements will enhance cash flow dependability and predictability, providing us with the financial stability we need to make cash distributions and obtain financing for future growth. |

| • | High-quality, well-maintained, modern and young fleet provides strong operational results. We believe that we have one of the most capable, technologically advanced and efficient fleets in the offshore drilling industry and that we can become a preferred provider of offshore drilling services. Our fleet is comprised of technologically advanced drilling rigs designed to operate in ultra-deepwater environments, as well as in deepwater and midwater environments. All of our rigs were placed into service in 2009 or 2010, with an average age of approximately 4.4 years as of June 16, 2014. In general, customers prefer newer, more technologically advanced rigs. Accordingly, we expect to have relatively low maintenance and replacement capital expenditures, high utilization rates and efficient and reliable operations. |

| • | Financial flexibility to execute growth strategy. Upon the closing of this offering, we expect to have an undrawn committed $300 million revolving credit facility with an affiliate of Transocean that allows for uncommitted increases in amounts to be agreed upon by Transocean and us. We expect that our borrowing capacity under this credit facility as well as access to the capital markets and other financing sources will be conducive to the execution of our acquisition strategy and enable us to pursue other expansion opportunities. |

| • | Experienced leadership team. Our management team has an average of years of experience in the energy industry. Our management team has established strong relationships with customers, suppliers and other industry participants, which we believe will be beneficial to us in pursuing our business strategies. |

An investment in our common units involves risks associated with our business, our limited liability company structure and the tax characteristics of our common units, including the risks described below. You should carefully consider these risks and the other risks described in “Risk Factors” beginning on page 19 and the other information in this prospectus before investing in our common units.

5

Table of Contents

Risks Inherent in Our Business

| • | We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses to enable us to pay the minimum quarterly distribution on our common units and subordinated units. |

| • | The assumptions underlying our forecast of cash available for distribution are inherently uncertain and subject to risks and uncertainties that could cause actual results to differ materially from those forecasted. |

| • | We must make substantial capital and operating expenditures to maintain the operating capacity of our fleet, and we may be required to make significant capital expenditures to maintain our competitiveness and to comply with laws and the applicable regulations and standards of governmental authorities and organizations, or to execute our growth plan, each of which could negatively affect our financial condition, results of operations and cash flows and reduce cash available for distribution. |

| • | We currently derive all of our revenues from two customers, and the loss of either of these customers or a dispute that leads to a loss of a customer could have a material adverse impact on our financial condition, results of operations and cash flows. |

| • | Any limitation in the availability or operation of any of our three drilling rigs could have a material adverse effect on our business, results of operations and financial condition and could significantly reduce our ability to make distributions to our unitholders. |

| • | Our revenues will initially be derived from assets that are operating in the U.S. Gulf of Mexico, making us vulnerable to risks associated with operating in that single geographic area. |

| • | We may be unable to renew or obtain new and favorable drilling contracts for rigs whose contracts are expiring or are terminated, which could adversely affect our revenues and profitability. |

Risks Inherent in an Investment in Us

| • | Transocean and its affiliates may compete with us, and we are limited in our ability to compete with Transocean. In addition, we generally will agree not to acquire, own operate or contract for certain drilling rigs operating under drilling contracts of less than five years. Relatively few drilling contracts have a term of five years or greater, particularly in the case of contracts that are not associated with newbuild units. As a result, we expect that Transocean will effectively have a right of first refusal on most drilling contract opportunities. |

| • | The Transocean Member and its other affiliates own a controlling interest in us and have conflicts of interest and limited duties to us and our common unitholders, and the Transocean Member and its other affiliates may favor their own interests to the detriment of us and our other common unitholders. |

| • | Our limited liability company agreement limits the duties that the Transocean Member and our directors and officers may have to our unitholders and restricts the remedies available to unitholders for actions taken by the Transocean Member or our directors and officers. |

| • | Holders of our common units have limited voting rights. |

| • | There is no existing market for our common units, and a trading market that will provide you with adequate liquidity may not develop. The price of our common units may fluctuate significantly, and unitholders could lose all or part of their investment in us. |

Tax Risks

| • | A change in tax laws, treaties or regulations, or their interpretation, of any country in which we have operations, are incorporated or are resident could result in a higher tax rate on our worldwide earnings, which could result in a significant negative impact on our earnings and cash flows from operations. |

6

Table of Contents

| • | A loss of a major tax dispute or a successful tax challenge to our operating structure, intercompany pricing policies or the taxable presence of our key subsidiaries in certain countries could result in a higher tax rate on our worldwide earnings, reducing our cash available for distribution to you. |

We were formed on February 6, 2014 as a Marshall Islands limited liability company to own and operate a fleet of offshore drilling rigs.

At or prior to the closing of this offering, the following transactions will occur:

| • | subsidiaries of Transocean that own Discoverer Inspiration, Discoverer Clear Leader and Development Driller III will sell each of these rigs to the Transocean Member in exchange for cash and/or a note; |

| • | the Transocean Member will contribute each of Discoverer Inspiration, Discoverer Clear Leader and Development Driller III to its wholly owned holding company subsidiaries, which will further contribute each rig to the respective rig-owning company for that rig, each of which is an indirect wholly owned subsidiary of the Transocean Member; |

| • | a subsidiary of Transocean will sell to holding company subsidiaries of the Transocean Member a 100 percent ownership interest in the respective rig-operating companies that operate and hold the drilling contracts for Discoverer Inspiration, Discoverer Clear Leader and Development Driller III in exchange for cash and/or a note; |

| • | the Transocean Member will contribute or sell to us a 51 percent ownership interest in each of the holding companies that own the RigCos; |

| • | we will issue (a) to the Transocean Member (i) common units and subordinated units, representing a 60 percent and a 40 percent limited liability company interest in us, (ii) the non-economic Transocean Member interest, and (iii) all of the incentive distribution rights, which entitle the Transocean Member to increasing percentages of the cash that we distribute in excess of $ per unit per quarter, and (b) to an affiliate of Transocean notes payable of approximately $ million for cash proceeds of $ million and initial working capital; |

| • | the Transocean Member will sell common units to the public, representing a percent limited liability company interest in us; and |

| • | the Transocean Member will grant the underwriters a 30-day option to purchase up to an additional common units on the same terms and conditions as the common units sold to the public; |

| • | we will enter into the omnibus agreement with Transocean and the Transocean Member; |

| • | we will enter into master services agreements with Transocean; |

| • | we will enter into support and secondment agreements with Transocean; and |

| • | we will enter into a $300 million five-year revolving credit facility, or the Five-Year Revolving Credit Facility, with an affiliate of Transocean. |

We are a holding company and will conduct our operations and business through subsidiaries, as is common for publicly traded limited liability companies. Initially, we will conduct all of our operations through the

RigCos. We will own and operate each of the drilling rigs in our initial fleet through separate RigCos. This ownership structure provides us the flexibility to purchase additional interests in individual drilling rigs rather than interests in our entire fleet, if we believe that is the appropriate way to grow our business.

7

Table of Contents

Organizational Structure After the Formation Transactions

The following diagram depicts our simplified organizational and ownership structure after giving effect to the offering and related transactions described above.

| Number of Units | Percentage Ownership | |||||

| Public common units |

% | |||||

| Transocean common units |

% | |||||

| Transocean subordinated units |

40.0 | % | ||||

|

|

|

|

||||

| Total |

100.0 | % | ||||

|

|

|

|

||||

8

Table of Contents

Our limited liability company agreement provides that our board of directors has authority to oversee and direct our operations, management and policies on an exclusive basis. Our executive officers will manage our day-to-day activities consistent with the policies and procedures adopted by our board of directors. We currently do not employ any of our executive officers and rely on Transocean to provide us with personnel who will perform executive officer services for our benefit pursuant to agreements with Transocean and who will be responsible for our day-to-day management subject to the direction of our board of directors. All references in this prospectus to “our officers” include those personnel of Transocean or its affiliates who perform executive officer functions for our benefit.

We will reimburse Transocean and its affiliates for their reasonable costs and expenses incurred in connection with providing management, administrative, financial and other support services to us. In addition, we will pay Transocean a services fee for providing these services to us. We expect that we will pay approximately $ million in total under the master services agreements and the support or secondment agreements for the twelve months ending September 30, 2015. There is no cap on the amount of fees and cost reimbursements that we may be required to pay pursuant to these agreements. For a more detailed description of these agreements, please read “Management—Directors and Executive Officers” and “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions.”

Principal Executive Offices and Internet Address

Our registered and principal executive offices are located at Transocean Deepwater House, Kingswells Causeway, Prime Four Business Park, Aberdeen, AB15 8PU, Scotland, United Kingdom, and our phone number is . Following the completion of this offering, our website will be located at www. .com. We expect to make our periodic reports and other information filed with or furnished to the U.S. Securities and Exchange Commission, or the SEC, available, free of charge, through our website as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

Summary of Conflicts of Interest and Duties

Our directors have a legal duty to manage us in a manner beneficial to us, subject to the limitations described under “Conflicts of Interest and Duties.” However, several of our directors and all of our officers hold positions with Transocean or its affiliates, resulting in those persons owing legal duties to those entities. As a result of these relationships, conflicts of interest may arise between us and our unaffiliated members on the one hand, and Transocean and its affiliates, including the Transocean Member, on the other hand. The resolution of these conflicts may not be in the best interest of us or our unitholders. In particular:

| • | all of our current executive officers and directors also serve as executive officers or directors of Transocean or its affiliates; |

| • | Transocean and its other affiliates may compete with us, subject to the restrictions contained in the omnibus agreement; |

| • | we will be restricted in our ability to compete with Transocean, subject to the exceptions contained in the omnibus agreement; and |

| • | we have entered into arrangements, and may enter into additional arrangements, with Transocean and certain of its subsidiaries, relating to the purchase of interests in drilling rigs, the provision of certain services to us by Transocean and other matters. In the performance of their obligations under these agreements, Transocean and its subsidiaries are generally held to the standard of care specified in these agreements. |

9

Table of Contents

For a more detailed description of our management structure, please read “Management—Directors and Executive Officers” and “Certain Relationships and Related Party Transactions.”

Although a majority of our directors will over time be elected by common unitholders, Transocean will likely have substantial influence on decisions made by our board of directors due to its ability to appoint certain of our directors and its significant ownership of our units. Our board of directors will have a conflicts committee composed of independent directors. Our board may, but is not obligated to, seek approval of the conflicts committee for resolutions of conflicts of interest that may arise as a result of the relationships between the Transocean Member and its affiliates, on the one hand, and us and our unaffiliated members, on the other.

For a more detailed description of the conflicts of interest and duties of our directors and officers, please read “Conflicts of Interest and Duties.” For a description of our other relationships with our affiliates, please read “Certain Relationships and Related Party Transactions.”

Implications of Being an Emerging Growth Company

As a company with less than $1 billion in revenues during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As an emerging growth company, we may, for up to five years, take advantage of specified exemptions from reporting and other regulatory requirements that are otherwise applicable generally to public companies. These exemptions include:

| • | the presentation of only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in the registration statement of an initial public offering of common equity securities; |

| • | exemption from the auditor attestation requirement on the effectiveness of our system of internal controls over financial reporting; |

| • | delayed adoption of new or revised financial accounting standards; and |

| • | reduced disclosure about our executive compensation arrangements. |

We may take advantage of these provisions until we are no longer an emerging growth company, which will occur on the earliest of (1) the last day of the fiscal year following the fifth anniversary of this offering, (2) the last day of the fiscal year in which we have more than $1 billion in annual revenues, (3) last day of the fiscal year in which we have more than $700 million in market value of our common units held by non-affiliates as of the end of our fiscal second quarter or (4) the date on which we issue more than $1 billion of non-convertible debt over a three-year period.

We have elected to take advantage of all of the applicable JOBS Act provisions, including the exemption that allows emerging growth companies to extend the transition period for complying with new or revised financial accounting standards. This election to take advantage of the extended transition period for complying with new or revised financial accounting standards is irrevocable. Accordingly, the information that we provide you may be different than what you may receive from other public companies in which you hold equity interests.

10

Table of Contents

| Common units offered to the public by the selling unitholder |

common units.

common units if the underwriters exercise their option to purchase additional common units in full. | |

| Units outstanding after this offering |

common units and subordinated units, representing a 60 percent and 40 percent limited liability company interest in us, respectively. | |

| Use of proceeds |

We will not receive any proceeds from the sale of common units by the selling unitholder in this offering. See “Use of Proceeds.” | |

| Cash distributions |

We intend to make minimum quarterly distributions of $ per common unit ($ per unit on an annualized basis) to the extent we have sufficient cash from operations after establishment of cash reserves and payment of fees and expenses, including payments to Transocean. We refer to this cash as “available cash,” and we define its meaning in our limited liability company agreement and in the glossary of terms attached as Appendix B.

We will adjust the minimum quarterly distribution for the period from the closing of the offering through , 2014 based on the actual length of the period.

In general, we will pay any cash distributions we make each quarter in the following manner:

• first, to the holders of common units, pro rata, until each common unit has received a minimum quarterly distribution of $ plus any arrearages from prior quarters;

• second, to the holders of subordinated units, pro rata, until each subordinated unit has received a minimum quarterly distribution of $ ; and

• third, to all unitholders, pro rata, until each unit has received an aggregate distribution of $ .

Within 60 days after the end of each fiscal quarter (beginning with the quarter ending , 2014), we will distribute all of our available cash to unitholders of record on the applicable record date. Our ability to pay our minimum quarterly distribution is subject to various restrictions and other factors described in more detail under the caption “Our Cash Distribution Policy and Restrictions on Distributions.” | |

11

Table of Contents

| If cash distributions to our unitholders exceed $ per unit in a quarter, holders of our incentive distribution rights (initially, the Transocean Member) will receive increasing percentages, up to 50 percent, of the cash we distribute in excess of that amount; provided that for any fiscal quarter in which the application of our distribution formula would result in the holders of the common units receiving, in the aggregate, less than a majority of the aggregate distribution of available cash for such quarter, then the distribution to the holders of the incentive distribution rights will be reduced, pro rata, to the extent necessary to cause the aggregate distribution to the holders of the common units to represent a majority of the aggregate distribution of available cash for such quarter. We refer to these distributions as “incentive distributions.” The amount of available cash may be greater than or less than the aggregate amount of the minimum quarterly distribution to be distributed on all units.

We believe, based on the estimates contained in and the assumptions listed under “Our Cash Distribution Policy and Restrictions on Distributions—Estimated Cash Available for Distribution for the Twelve Months Ending September 30, 2015,” that we will have sufficient cash available for distribution to enable us to pay the minimum quarterly distribution of $ on all of our common and subordinated units for the twelve months ending September 30, 2015. However, unanticipated events may occur which could adversely affect the actual results we achieve during the forecast period. Consequently, our actual results of operations, cash flows and financial condition during the forecast period may vary from the forecast, and such variations may be material. | ||

| Subordinated units |

Transocean will initially own all of our subordinated units. The principal difference between our common units and subordinated units is that in any quarter during the subordination period the subordinated units are entitled to receive the minimum quarterly distribution of $ per unit only after the common units have received the minimum quarterly distribution and arrearages in the payment of the minimum quarterly distribution from prior quarters. Subordinated units will not accrue arrearages. | |

12

Table of Contents

| Conversion of subordinated units |

The subordination period generally will end if we have earned and paid at least $ (the minimum quarterly distribution on an annualized basis) on each outstanding common and subordinated unit for any three consecutive, non-overlapping four-quarter periods ending on or after , 2019, provided there are no arrearages on our common units at that time.

The subordination period also will end upon the removal of the Transocean Member other than for cause if no subordinated units or common units held by the Transocean Member or its affiliates are voted in favor of that removal.

When the subordination period ends as provided above, all subordinated units will convert into common units on a one-for-one basis, and all common units will no longer be entitled to arrearages.

Please read “Provisions of Our Limited Liability Company Agreement Relating to Cash Distributions—Subordination Period.” | |

| Issuance of additional units |

We can issue an unlimited number of additional units, including units that are senior to the common units in rights of distribution, liquidation and voting, on the terms and conditions determined by our board of directors, without the consent of our unitholders. Please read “Units Eligible for Future Sale” and “The Limited Liability Company Agreement—Issuance of Additional Interests.” | |

| Board of directors |

We will hold a meeting of the members every year to elect one or more members of our board of directors and to vote on any other matters that are properly brought before the meeting. Prior to the closing of this offering, the Transocean Member, in its capacity as the initial holder of the common units, will elect three of the seven members of our board of directors who will serve as initial directors, and such elected directors may elect an additional elected director. Prior to the 2015 annual meeting, the Transocean Member may also appoint additional directors to fill the appointed director positions, provided that the number of elected directors must, immediately after such appointment, exceed the number of appointed directors. At our 2015 annual meeting, the common unitholders will elect four of our directors. The four directors elected by our common unitholders at our 2015 annual meeting initially will serve for one-year terms. Upon the election by the Transocean Member to classify our board of directors, the four directors | |

13

Table of Contents

| elected by our common unitholders will be divided into three classes to be elected by our common unitholders on a staggered basis to serve for three-year terms. Transocean may vote any common units held by it in the election of directors; however, subordinated units will not be voted in the election of directors. Our governance documents require that, at all times, at least a majority of the members of our board of directors be United Kingdom (“U.K.”) tax residents. | ||

| Voting rights |

Each outstanding common unit is entitled to one vote on matters subject to a vote of common unitholders.

You will have no right to elect the Transocean Member on an annual or other continuing basis. The Transocean Member may not be removed except by a vote of the holders of at least 66 2⁄3 percent of the outstanding units, including any units owned by the Transocean Member and its affiliates, voting together as a single class. Upon consummation of this offering, Transocean will own of our common units and all of our subordinated units, representing a percent limited liability company interest in us. If the underwriters’ option to purchase additional common units is exercised in full, Transocean will own of our common units and all of our subordinated units, representing a percent limited liability company interest in us. As a result, you will initially be unable to remove the Transocean Member without Transocean’s consent because Transocean will own sufficient units upon completion of this offering to be able to prevent the Transocean Member’s removal. Please read “The Limited Liability Agreement—Voting Rights.” | |

| Limited call right |

If at any time the Transocean Member and its affiliates own more than 80 percent of the outstanding common units, the Transocean Member has the right, but not the obligation, to purchase all, but not less than all, of the remaining common units at a price equal to the greater of (x) the average of the daily closing prices of the common units over the 20 trading days preceding the date three days before the notice of exercise of the call right is first mailed and (y) the highest price paid by the Transocean Member or any of its affiliates for common units during the 90-day period preceding the date such notice is first mailed. The Transocean Member may assign this right to its affiliates, including us. The Transocean Member is not obligated to obtain a fairness opinion, nor will the unitholders be entitled to dissenter’s rights of appraisal, regarding the value of the common units to be repurchased by the Transocean Member upon the exercise of this limited call right. | |

14

Table of Contents

| U.S. federal income tax considerations |

We are organized as a limited liability company that is treated as a corporation for U.S. federal income tax purposes. Consequently, distributions you receive from us will constitute dividends to the extent of our current-year or accumulated earnings and profits (as computed for U.S. federal income tax purposes). The remaining portion of such distributions will be treated first as a non-taxable return of capital to the extent of your tax basis in your common units and thereafter as capital gain. We estimate that if you hold the common units that you purchase in this offering through the period ending December 31, 2016, the distributions you receive, on a cumulative basis, that will constitute dividends for U.S. federal income tax purposes will be less than percent of the total cash distributions received during that period. Please read “Material U.S. Federal Income Tax Considerations—U.S. Holders—Ratio of Dividend Income to Distributions” for the basis for this estimate. For a discussion of other material U.S. federal income tax consequences that may be relevant to prospective unitholders, please read “Material U.S. Federal Income Tax Considerations.” | |

| Non-U.S. tax considerations |

For a discussion of the material Marshall Islands and U.K. tax consequences that may be relevant to prospective unitholders, please read “Non-United States Tax Considerations.” | |

| Directed unit program |

At our request, the underwriters have reserved for sale, at the initial public offering price, up to percent of the common units offered hereby for our directors, officers, employees and certain other persons associated with us. The number of common units available for sale to the general public will be reduced to the extent such persons purchase such reserved common units. Any reserved common units which are not so purchased will be offered by the underwriters to the general public on the same terms as the other common units offered hereby. Please read “Underwriting—Directed Unit Program.” | |

| Exchange listing |

We intend to apply to list the common units on the New York Stock Exchange under the symbol “RIGP.” | |

15

Table of Contents

SUMMARY FINANCIAL AND OPERATING DATA

The following table presents, in each case for the periods and as of the dates indicated, summary historical financial and operating data of Transocean Partners LLC Predecessor, which includes the operating results, assets and liabilities of the drilling rigs in our initial fleet. The summary historical financial data of Transocean Partners LLC Predecessor as of and for the years ended December 31, 2013 and 2012 are derived from the audited combined financial statements of Transocean Partners LLC Predecessor, prepared in accordance with U.S. GAAP, which are included elsewhere in this prospectus. The summary historical financial data of Transocean Partners LLC Predecessor as of March 31, 2014 and for the three months ended March 31, 2014 and 2013 are derived from the unaudited condensed combined financial statements of Transocean Partners LLC Predecessor, prepared in accordance with U.S. GAAP, which are included elsewhere in this prospectus.

The following financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the historical combined financial statements of Transocean Partners LLC Predecessor and the notes thereto, our unaudited pro forma combined balance sheet and the notes thereto and our forecasted results of operations for the twelve months ending September 30, 2015, in each case included elsewhere in this prospectus.

Our financial position, results of operations and cash flows could differ from those that would have resulted if we operated autonomously or as an entity independent of Transocean in the periods for which historical financial data are presented below, and such data may not be indicative of our future operating results or financial performance.

| Three months ended March 31, |

Years ended December 31, |

|||||||||||||||

| 2014 | 2013 | 2013 | 2012 | |||||||||||||

| (In millions, except fleet data) | ||||||||||||||||

| Statement of operations data |

||||||||||||||||

| Operating revenues |

$ | 148 | $ | 116 | $ | 526 | $ | 569 | ||||||||

| Costs and expenses |

79 | 76 | 318 | 293 | ||||||||||||

| Operating income |

69 | 40 | 208 | 276 | ||||||||||||

| Interest income |

— | — | 4 | 3 | ||||||||||||

| Income before income tax expense |

69 | 40 | 212 | 279 | ||||||||||||

| Income tax expense |

6 | 4 | 23 | 24 | ||||||||||||

| Net income |

63 | 36 | 189 | 255 | ||||||||||||

| Balance sheet data (at end of period) |

||||||||||||||||

| Cash and cash equivalents |

$ | — | $ | — | $ | — | $ | — | ||||||||

| Property and equipment, net |

2,005 | 2,082 | 2,038 | 2,098 | ||||||||||||

| Total assets |

2,432 | 2,506 | 2,468 | 2,557 | ||||||||||||

| Total long-term liabilities |

78 | 117 | 87 | 131 | ||||||||||||

| Total net investment |

2,320 | 2,351 | 2,344 | 2,388 | ||||||||||||

| Cash flow data |

||||||||||||||||

| Cash provided by operating activities |

$ | 70 | $ | 73 | $ | 239 | $ | 340 | ||||||||

| Cash used in investing activities(1) |

(1 | ) | — | (4 | ) | (15 | ) | |||||||||

| Cash used in financing activities |

(69 | ) | (73 | ) | (235 | ) | (325 | ) | ||||||||

| Fleet data |

||||||||||||||||

| Number of rigs |

3 | 3 | 3 | 3 | ||||||||||||

| Average age of fleet at end of period (in years) |

4.3 | 3.3 | 4.1 | 3.1 | ||||||||||||

| Operating days(2) |

270 | 270 | 1,095 | 1,098 | ||||||||||||

| Average daily revenue(3) |

$ | 526,700 | $ | 403,900 | $ | 455,800 | $ | 491,500 | ||||||||

| Revenue efficiency(4) |

98 | % | 77 | % | 86 | % | 97 | % | ||||||||

| Rig utilization(5) |

100 | % | 100 | % | 100 | % | 99 | % | ||||||||

| Other financial data |

||||||||||||||||

| EBITDA(6) |

$ | 85 | $ | 56 | $ | 274 | $ | 341 | ||||||||

| Adjusted EBITDA(6) |

72 | 43 | 221 | 287 | ||||||||||||

16

Table of Contents

| (1) | Represents cash used to fund capital expenditures. |

| (2) | An operating day is defined as a calendar day during which a rig is contracted to earn a dayrate during the firm contract period after commencement of operations. |

| (3) | Average daily revenue is defined as contract drilling revenues earned per operating day. Our average daily revenue fluctuates relative to market conditions and our revenue efficiency. Average daily revenues increased in the three months ended March 31, 2014 relative to the three months ended March 31, 2013 due to an increase in revenue efficiency resulting from lower unplanned downtime and an increase in operating dayrates associated with cost escalation adjustments that reflect increases in our operating costs. Average daily revenues decreased in the year ended December 31, 2013 relative to the year ended December 31, 2012 due to a decrease in revenue efficiency resulting from unplanned downtime. This decrease was slightly offset by an increase in operating dayrates associated with cost escalation adjustments that reflect increases in our operating costs. |

| (4) | Revenue efficiency is defined as actual contract drilling revenues for the measurement period divided by the maximum revenue calculated for the measurement period, expressed as a percentage. Maximum revenue is defined as the greatest amount of contract drilling revenues the drilling unit could earn for the measurement period, excluding amounts related to incentive provisions. Our revenue efficiency rate varies due to revenues earned under alternative contractual dayrates, such as a waiting-on-weather rate, repair rate, standby rate, force majeure rate or zero rate, that may apply under certain circumstances. Revenue efficiency increased in the three months ended March 31, 2014 relative to the three months ended March 31, 2013 resulting from lower unplanned downtime associated primarily with repairs to blowout preventers and other subsea equipment. Revenue efficiency was lower in the year ended December 31, 2013 relative to the year ended December 31, 2012 due to unplanned downtime associated primarily with repairs to blowout preventers and other subsea equipment. |

| (5) | Rig utilization is defined as the total number of operating days divided by the total number of rig calendar days in the measurement period, expressed as a percentage. Our rig utilization rate declines as a result of idle and stacked rigs and during shipyard and mobilization periods to the extent these rigs are not earning revenues. |

| (6) | Please read “—Non-GAAP Measures” described below for a description and a reconciliation of EBITDA and Adjusted EBITDA to net income, the most directly comparable U.S. GAAP measure. |

We present our operating results in accordance with U.S. GAAP. We believe that certain financial measures which are not in conformity with U.S. GAAP, or non-GAAP measures, provide users of our financial statements with additional useful information in evaluating our operating performance. We define EBITDA as earnings before interest expense net of interest income, taxes, depreciation and amortization and Adjusted EBITDA as EBITDA adjusted for amortization of prior certification costs and license fees, non-cash recognition of royalty fees, amortization of the drilling contract intangible and amortization of pre-operating revenues. EBITDA and Adjusted EBITDA are used as supplemental financial measures by which management and external users of our financial statements, such as investors and commercial banks, can assess:

| • | our performance from period to period and against the performance of other companies in our industry, without regard to financing methods, historical cost basis or capital structure; |

| • | the ability of our assets to generate sufficient cash flow to make distributions to our members; |

| • | our ability to incur and service debt and fund capital expenditures; and |

| • | the viability of acquisitions and other capital expenditure projects and the returns on investment of various investment opportunities. |

17

Table of Contents

We believe that the presentation of EBITDA and Adjusted EBITDA in this prospectus provides information useful to investors in assessing our financial condition and results of operations. The U.S. GAAP measure most directly comparable to EBITDA and Adjusted EBITDA is net income. EBITDA and Adjusted EBITDA should not be considered an alternative to net income, operating income, net cash provided by operating activities or any other measure of financial performance presented in accordance with U.S. GAAP. EBITDA and Adjusted EBITDA excludes some, but not all, items that affect net income and these measures may vary among other companies. Therefore, EBITDA and Adjusted EBITDA, as presented above, may not be comparable to similarly titled measures of other companies.

The following table presents a reconciliation of net income, the most directly comparable U.S. GAAP financial measure, to EBITDA and Adjusted EBITDA for each of the periods indicated.

| Three months ended March 31, |

Years ended December 31, |

|||||||||||||||

| 2014 | 2013 | 2013 | 2012 | |||||||||||||

| (In millions) |

||||||||||||||||

| Net income |

$ | 63 | $ | 36 | $ | 189 | $ | 255 | ||||||||

| Plus: |

||||||||||||||||

| Income tax expense |

6 | 4 | 23 | 24 | ||||||||||||

| Interest income(1) |

— | — | (4 | ) | (3 | ) | ||||||||||

| Depreciation expense |

16 | 16 | 66 | 65 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| EBITDA |

85 | 56 | 274 | 341 | ||||||||||||

| Plus: |

||||||||||||||||

| Amortization of prior certification costs and license fees |

1 | 1 | 3 | 3 | ||||||||||||

| Non-cash recognition of royalty fees(2) |

— | — | — | — | ||||||||||||

| Less: |

||||||||||||||||

| Amortization of drilling contract intangible |

4 | 4 | 18 | 19 | ||||||||||||

| Amortization of pre-operating revenues |

10 | 10 | 38 | 38 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA |

$ | 72 | $ | 43 | $ | 221 | $ | 287 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Includes interest earned on long-term accounts receivable from our customers. We record long-term accounts receivable at their present value and recognize interest income on the outstanding balance using the effective interest method through the dates of payment. |

| (2) | Following this offering, the Transocean Member will retain the obligation for the payment of quarterly patent fees through the patent expiration, and we will recognize a non-cash expense for the fees paid on our behalf. |

18

Table of Contents

Common units are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. You should carefully consider the following risk factors together with all of the other information included in this prospectus in evaluating an investment in our common units.

If any of the following risks were actually to occur, our business, financial condition, results of operations and cash flows could be materially adversely affected. In that case, we might not be able to make distributions on our common units, the trading price of our common units could decline, and you could lose all or part of your investment in us.

Risks Inherent in Our Business

We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses to enable us to pay the minimum quarterly distribution on our common units and subordinated units.

We may not have sufficient cash from operations to pay the minimum quarterly distribution of $ per unit, or $ per unit on an annualized basis, on our common units and subordinated units, which will require us to have available cash of approximately $ million per quarter, or $ million per year, based on the number of common and subordinated units to be outstanding after the completion of this offering. We may not have sufficient available cash each quarter to enable us to pay the minimum quarterly distribution. The amount of cash we can distribute on our units principally depends upon the amount of cash we generate from our operations, which may fluctuate from quarter to quarter based on the risks described in this section, including, among other things:

| • | our ability to re-contract our drilling rigs in their current configuration upon expiration or termination of an existing drilling contract and the dayrates we obtain under such contracts; |

| • | the dayrates we obtain under our drilling contracts; |

| • | the level of reimbursable revenues and expenses; |

| • | the level of our rig operating costs, such as the cost of crews, repairs, maintenance and insurance; |

| • | the effect of governmental regulations and maritime self-regulatory organization standards on the conduct of our business; |

| • | rig downtime or less than full utilization, which would result in a reduction of revenues under our drilling contracts; |

| • | changes in local income tax rates, tax treaties and tax laws; |

| • | the timeliness of payments from customers under drilling contracts; |

| • | time spent mobilizing drilling rigs to the customer location; |

| • | resolution of tax assessments; |

| • | currency exchange rate fluctuations and currency controls; and |

| • | prevailing global economic and market conditions. |

In addition, the actual amount of cash we will have available for distribution will depend on other factors, some of which are beyond our control, including:

| • | the level and timing of capital expenditures we make; |

19

Table of Contents

| • | the level of our operating, maintenance and rig and shore-based general and administrative expenses, including reimbursements to the Transocean Member and its affiliates for services provided to us and additional expenses we will incur as a result of being a public company; |

| • | our debt service requirements and other liabilities; |

| • | fluctuations in our working capital needs; |

| • | the cost of acquisitions, if any; |

| • | our ability to borrow funds and access capital markets; |

| • | restrictions on distributions contained in our debt agreements; and |

| • | the amount of cash reserves, including reserves for future maintenance and replacement capital expenditures, working capital and other matters, established by our board of directors. |

For a description of additional restrictions and factors that may affect our ability to make cash distributions, please read “Our Cash Distribution Policy and Restrictions on Distributions.”

The assumptions underlying our forecast of cash available for distribution are inherently uncertain and are subject to risks and uncertainties that could cause actual results to differ materially from those forecasted.

The forecast of cash available for distribution set forth in “Our Cash Distribution Policy and Restrictions on Distributions” includes our forecast of operating results and cash flows for the twelve months ending September 30, 2015. Our ability to pay the full minimum quarterly distribution in the forecast period is based on a number of assumptions that may not prove to be correct, which are discussed in “Our Cash Distribution Policy and Restrictions on Distributions.”

Our financial forecast has been prepared by management, and we have neither received nor requested an opinion or report on it from our or any other independent auditor. The assumptions underlying the forecast are inherently uncertain and are subject to significant business, economic, regulatory and operational risks and uncertainties that could cause actual results to differ materially from those forecasted. If we do not achieve the forecasted results, we may be unable to pay the full minimum quarterly distribution or any amount on our common units or subordinated units, in which event the market price of our common units may decline materially.

The amount of cash we have available for distribution to holders of our common and subordinated units depends primarily on our cash flow rather than on our profitability, which may prevent us from making distributions, even during periods in which we record net income.