Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - DESTINATION XL GROUP, INC. | d738163dex312.htm |

| EX-31.1 - EX-31.1 - DESTINATION XL GROUP, INC. | d738163dex311.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K/A

(Amendment No. 1)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

| For the fiscal year ended February 1, 2014 (Fiscal 2013) |

Commission File Number 01-34219 |

DESTINATION XL GROUP, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 04-2623104 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

| 555 Turnpike Street, Canton, MA | 02021 | |

| (Address of principal executive offices) | (Zip Code) | |

(781) 828-9300

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, $0.01 par value | The NASDAQ Stock Market, LLC |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of August 3, 2013, the aggregate market value of the Common Stock held by non-affiliates of the registrant was approximately $235.5 million, based on the last reported sale price on that date. Shares of Common Stock held by each executive officer and director and by each person who owns 10% or more of the outstanding Common Stock have been excluded on the basis that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily determinative for other purposes.

The registrant had 50,542,399 shares of Common Stock, $0.01 par value, outstanding as of May 2, 2014.

DOCUMENTS INCORPORATED BY REFERENCE

None.

EXPLANATORY NOTE

We are filing this Amendment No. 1 to our Annual Report on Form 10–K for the fiscal year ended February 1, 2014 pursuant to General Instruction G(3) to Form 10–K for the purposes of filing the information required to be disclosed pursuant to Part III of Form 10–K.

This Form 10–K/A does not reflect events occurring after the filing of the original Form 10–K. Except for the amendments described above, this Form 10–K/A does not modify or update the disclosure in our Annual Report on Form 10–K for the fiscal year ended February 1, 2014 originally filed with the Securities and Exchange Commission on March 17, 2014.

PART III.

Item 10. Directors, Executive Officers and Corporate Governance

Set forth below is certain information regarding our directors, including information furnished by them as to their principal occupations and business experience for the past five years, certain directorships held by each director within the past five years, their respective ages as of June 1, 2014 and the year in which each became a director of our Company:

| NAME |

AGE | POSITION |

DIRECTOR SINCE |

|||||||

| Seymour Holtzman |

78 | Chairman of the Board and Director (1) |

2000 | |||||||

| David A. Levin |

63 | President, Chief Executive Officer and Director |

2000 | |||||||

| Alan S. Bernikow |

73 | Director (4),(5) |

2003 | |||||||

| Jesse Choper |

78 | Director (4),(5),(6) |

1999 | |||||||

| John Edward Kyees |

67 | Director, Interim Chief Financial Officer (2) |

2010 | |||||||

| Willem Mesdag |

60 | Director (3),(4),(6) |

2014 | |||||||

| Ward K. Mooney |

65 | Director (6) |

2006 | |||||||

| George T. Porter, Jr. |

67 | Director (6) |

1999 | |||||||

| Mitchell S. Presser |

49 | Director (5) |

2007 | |||||||

| Ivy Ross |

58 | Director |

2013 | |||||||

| (1) | Mr. Holtzman has served as Chairman of the Board of Directors since April 2000. |

| (2) | Mr. Kyees was a member of the Audit Committee until February 2, 2014 when he was appointed Interim Chief Financial Officer. Mr. Kyees served as Interim Chief Financial Officer until May 31, 2014. |

| (3) | Mr. Mesdag was elected a director of the Company on January 29, 2014. |

| (4) | Current member of the Audit Committee. |

| (5) | Current member of the Nominating and Corporate Governance Committee. |

| (6) | Current member of the Compensation Committee. |

Seymour Holtzman, has been a director since April 7, 2000 and Chairman of the Board since April 11, 2000. On May 25, 2001, the Board of Directors hired Mr. Holtzman as an employee. Mr. Holtzman has been involved in the retail business for over 40 years. For many years, he has been the President and Chief Executive Officer of Jewelcor, Incorporated, a former New York Stock Exchange listed company that operated a chain of retail stores. From 1986 to 1988, Mr. Holtzman was Chairman of the Board and also Chief Executive Officer of Gruen Marketing Corporation, an American Stock Exchange listed company involved in the nationwide distribution of watches. For at least the last five years Mr. Holtzman has served as Chairman and Chief Executive Officer of Jewelcor Management, Inc., a company primarily involved in investment and management services. Mr. Holtzman is the Chief Executive Officer and indirectly the owner of C.D. Peacock, Inc., a Chicago, Illinois retail jewelry establishment, the managing member of Luxury Swiss, LLC, a retail Rolex Watch establishment, and the Chief Executive Officer and owner of Homeclick, LLC, a privately held internet retailer specializing in luxury brands for the home. Mr. Holtzman was the Chief Executive Officer and Co-Chairman of the Board of George Foreman Enterprises, Inc., formerly MM Companies, Inc. until his resignation in November 2010. Mr. Holtzman is a successful entrepreneur with extensive experience working with public companies and provides valuable insight to the Board with respect to strategic planning.

David A. Levin has been our President and Chief Executive Officer since April 10, 2000 and a director since April 11, 2000. From 1999 to 2000, he served as the Executive Vice President of eOutlet.com. Mr. Levin was President of Camp Coleman, a division of The Coleman Company, from 1998 to 1999. Prior to that, Mr. Levin was President of Parade of Shoes, a division of J. Baker, Inc., from 1995 to 1997. Mr. Levin was also President of Prestige Fragrance & Cosmetics, a division of Revlon, Inc., from 1991 to 1995. Mr. Levin has worked in the retail industry for over 30 years. Since joining the Company, Mr. Levin has been instrumental in transforming the Company from a company which exclusively operated Levi Strauss & Co. branded apparel to the largest specialty retailer of big & tall men’s apparel. In May 2012, Mr. Levin joined the board of directors of Christopher & Banks Corporation, a New York Stock Exchange listed company that specializes in women’s apparel. Mr. Levin brings to the Board valuable experience in merchandising and marketing initiatives.

Alan S. Bernikow has been a director since June 29, 2003. From 1998 until his retirement in May 2003, Mr. Bernikow was the Deputy Chief Executive Officer at Deloitte & Touche LLP where he was responsible for assisting the firm on special projects such as firm mergers and acquisitions, litigation matters and partner affairs. He was a member of Deloitte & Touche’s Executive & Management Committees; Chairman for the Professional Asset Indemnity Limited (“PAIL”) Bermuda Big 4 Insurance Representatives; and President for the PAIL Vermont Insurance Company Big 4 Insurance Representatives. Mr. Bernikow joined Touche Ross, the

predecessor firm of Deloitte & Touche LLP, in 1977, prior to which Mr. Bernikow was the National Administrative Partner in Charge for the accounting firm of J.K. Lasser & Company. Mr. Bernikow is a member of the Board of Directors of Revlon, Inc., a NYSE-listed company, and Revlon Consumer Products Corporation and serves as Chairman of the Audit Committee of Revlon, Inc.; as well as Chairman of the Revlon, Inc. Compensation and Stock Plan Committee; a member of the Board of Directors of Mack-Cali, as well as the Chairman of the Audit Committee and a member of the Executive Committee of Mack-Cali; and serves as a Director of the Board of the UBS Global Asset Management (US) Inc., a wholly owned subsidiary of UBS AG, including serving as Chairman of its Audit Committee. Mr. Bernikow has had extensive international experience in his role in Deloitte & Touche’s management/risk management group, as well as worldwide insurance responsibilities. Mr. Bernikow provides the Board with substantial financial expertise and strategic planning as a result of his years of experience at Deloitte & Touche LLP. His strong financial background qualifies him as an “audit committee financial expert”. Mr. Bernikow provides the Board with valuable insight with respect to financial reporting based on his experiences serving on the audit committees of several boards.

Jesse Choper has been a director since October 8, 1999. Mr. Choper is the Earl Warren Professor of Public Law at the University of California at Berkeley School of Law, where he has taught since 1965. From 1960 to 1961, Professor Choper was a law clerk for Supreme Court Chief Justice Earl Warren. Mr. Choper is a member of the California Horseracing Board. Mr. Choper was a member of the Board of Directors of George Foreman Enterprises, Inc. until his resignation in November 2010. Mr. Choper provides valuable legal expertise to the Board. His specific legal background makes him an authority on ethical behavior and he provides valuable insight with respect to corporate governance. Mr. Choper’s tenure and service as a director for over ten years is also considered a valuable asset to the Board.

John E. Kyees has been a director since May 3, 2010. From February 2, 2014 until May 31, 2014, Mr. Kyees assumed the position of Interim Chief Financial Officer of the Company. From 2003 until his retirement in 2010, Mr. Kyees was the Chief Financial Officer of Urban Outfitters, Inc. and also served as the Chief of Investor Relations for Urban Outfitters in 2010. Prior to that, from 2002 to 2003, Mr. Kyees was the Chief Financial Officer and Chief Administrative Officer of bebe Stores, Inc. Mr. Kyees is a member of the Board of Directors of Vera Bradley, Inc., a publicly-traded company, and serves as Chairman of the Audit Committee. Mr. Kyees was a member of the Board of Directors of Hot Topic, Inc., a formerly publicly-traded company, and was a member of the Audit Committee. Mr. Kyees is a member of the Board of Directors of Rackwise, Inc., a publicly-traded company, and is a member of the Audit Committee. In addition, Mr. Kyees is also a director of Arhaus Furniture, a privately-held retailer. Mr. Kyees brings to the Board extensive executive-level retail experience having served as Chief Financial Officer for several prominent retailers. His insight with respect to merchandising, operational activities and finance is an asset to our Board. Institutional Investor magazine selected Mr. Kyees as a top specialty retail chief financial officer on five separate occasions, evidencing his strong skills in corporate finance, strategic and accounting matters.

Willem Mesdag has been a director since January 29, 2014. Mr. Mesdag is the Managing Partner of Red Mountain Capital Partners LLC, an investment firm based in Los Angeles, California. Prior to founding Red Mountain in 2005, Mr. Mesdag was a Partner and Managing Director of Goldman, Sachs & Co., which he joined in 1981. Prior to Goldman, Sachs he was a securities lawyer at Ballard, Spahr, Andrews & Ingersoll, which he joined in 1978. He currently serves on the boards of Encore Capital Group Inc., a NASDAQ-listed company, and Nature’s Sunshine Products Inc., a NASDAQ-listed company. He previously served on the boards of 3i Group plc, Cost Plus, Inc. and Skandia Group AB. Having had an extensive career in international investment banking and finance, Mr. Mesdag brings to the Board significant expertise related to business and financial issues and corporate governance.

Ward K. Mooney has been a director since July 31, 2006. Mr. Mooney is a founding partner of Crystal Financial LLC and since March 2010 has been the Chief Executive Officer. Prior to that, Mr. Mooney was the President of Bank of America Retail Finance Group and Chief Operating Officer of Back Bay Capital, both of which were formerly Bank of Boston businesses which Mr. Mooney founded. Mr. Mooney provides the Board with valuable insight with respect to his extensive experience as a lender in the retail industry.

George T. Porter, Jr. has been a director since October 28, 1999. Mr. Porter was President of Levi’s USA for Levi Strauss & Co. from 1994 to 1997. Beginning in 1974, Mr. Porter held various positions at Levi Strauss & Co., including President of Levi’s Men’s Jeans Division. Mr. Porter was also Corporate Vice President and General Manager of Nike USA from 1997 to 1998. Mr. Porter provides the Board with extensive merchandising experience having worked at two highly prominent companies. Mr. Porter’s tenure and service as a director for over ten years is also considered a valuable asset to the Board.

Mitchell S. Presser has been a director since May 1, 2007. Since January 2014, Mr. Presser has been a Senior Advisor to Paine & Partners, LLC, a private equity firm. From November 2006 to January 2014, Mr. Presser was a founding partner of Paine & Partners, LLC. Prior to that, Mr. Presser was a partner with the law firm of Wachtell, Lipton, Rosen & Katz, specializing in mergers & acquisitions. Mr. Presser serves as a director on the boards of several privately-held companies. Mr. Presser’s extensive experience in private equity and strategic planning provides valuable insight to the Board.

Ivy Ross has been a director since January 31, 2013. In May 2014, Ms. Ross joined Google X as Head of Glass. From July 2011 until April 2014, Ms. Ross was the Chief Marketing Officer of Art.com from where she oversaw the company’s marketing, branding, merchandising and user-experience functions. Prior to Art.com, from June 2008 to June 2011, Ms. Ross was EVP of Marketing for the Gap brand, and acted as the Creative Catalyst for all brands within Gap, Inc. Ms. Ross also has held senior creative and product design positions at Disney Stores North America, Mattel, Calvin Klein, Coach, Liz Claiborne, Swatch Watch and Avon. Chosen by Fast Company and BusinessWeek as the new face of leadership, Ross was a contributing author of The Change Champions Field Guide and Best Practices in Leadership Development and Organizational Change. She has also served on Proctor and Gamble’s design board since its inception. With her industry insight and marketing expertise, Ms. Ross provides a valuable perspective to the Board as the Company builds its Destination XL brand.

All directors hold office until the next Annual Meeting of Stockholders and until their respective successors have been duly elected and qualified or until their earlier death, resignation or removal.

Current Non-Director Executive Officers

Peter H. Stratton, Jr., 42, became our Senior Vice President, Chief Financial Officer and Treasurer on June 1, 2014. From August 2009 to May 31, 2014, Mr. Stratton was our Senior Vice President of Finance, Corporate Controller and Chief Accounting Officer. Mr. Stratton joined us in June 2009 as Vice President of Finance. Prior to joining the Company, Mr. Stratton served as Senior Director of Corporate Accounting at BearingPoint, Inc from May 2007 to June 2009. Prior to May 2007, Mr. Stratton held various finance and accounting leadership positions at Legal Sea Foods, Inc., Shaw’s Supermarkets, Inc. and Cintas Corporation.

Francis Chane, 51, has been our Senior Vice President of Distribution and Logistics since June 2011. Prior to that, Mr. Chane was our Vice President of Distribution & Logistics since joining the Company in June 2008. Prior to joining our Company, Mr. Chane was Vice President Operations & Facilities for Redcats USA, a division of the French multi-national company PPR, from 1999 to April 2008.

Angela Chew, 47, has been our Senior Vice President of Global Sourcing and Product Development since March 2013. Prior to that, from May 2010 to March 2013, Ms. Chew was our Vice President of Global Sourcing. Ms. Chew joined the Company in February 2009 as our Director of Global Sourcing. Prior to joining our Company, from October 2007 to December 2008 Ms. Chew was the Senior Product Manager for Redcats USA. From 2007 to 2009, Ms. Chew was an Independent Retail Consultant and Analyst with the Gerson Lehrman Group and in 2006, she held the positions of Director and Executive Vice President of Global Sourcing for Rocawear. Prior to that, Ms. Chew was the founder & partner of several apparel manufacturing companies & franchise restaurants. She also held various merchandising management positions with Macy’s corporate in New York and Hong Kong.

Kenneth M. Ederle, 49, has been our Senior Vice President and Chief Merchandising Officer since April 2013. Prior to that, from May 2011 until April 2013, Mr. Ederle was our Senior Vice President – General Merchandising Manager DXL. Mr. Ederle served as our Vice President, General Merchandise Manager of Rochester Clothing from August 2008 until May 2011. From January 2008 to August 2008, Mr. Ederle was our Merchandise Manager of Sportswear for Rochester Clothing and prior to that was one of our Merchandise Managers for Casual Male from November 2006 to December 2007. Prior to joining the Company in 2006, Mr. Ederle was a Senior Buyer and Senior Planner for Limited Brands.

Jack R. McKinney, 58, has been our Senior Vice President and Chief Information Officer since June 2002. Mr. McKinney began his career with Casual Male Corp. in 1997 and joined our Company in May 2002 as part of our acquisition of Casual Male Corp.

Robert S. Molloy, 54, has been our Senior Vice President and General Counsel since April 2010 and became Secretary of the Company on May 15, 2014. Prior to that, Mr. Molloy was the Vice President and General Counsel since joining the Company in February 2008. Prior to joining the Company, Mr. Molloy served as Vice President, Assistant General Counsel at Staples, Inc. from May 1999 to February 2008. Prior to May 1999, Mr. Molloy was a trial attorney.

Brian S. Reaves, 53, joined our Company in May 2010 as our Senior Vice President of Store Sales and Operations. Prior to joining our Company, Mr. Reaves was the Vice President – Outreach and Group Sales for David’s Bridal from 2007 to 2009. Before that, Mr. Reaves was the Senior Vice President of Sales for The Bridal Group from 2004 to 2007.

Peter E. Schmitz, 55, has been our Senior Vice President and Chief Real Estate Officer since June, 2013. Prior to that, Mr. Schmitz was our Senior Vice President, Real Estate and Store Development. Prior to joining the Company, Mr. Schmitz was the Vice President of Real Estate for Brooks/Eckerd Pharmacy Chain since 1995.

Vickie S. Smith, 57, joined the Company in February 2008 as our Senior Vice President, Merchandise Planning and Allocation. Prior to that, Ms. Smith worked at Urban Brands as Senior Vice President, Planning, Allocation and Marketing from May 2006 to November 2007. From May 2001 to December 2005, Ms. Smith was the Vice President, Corporate Planning and Allocation at JCPenney.

Walter E. Sprague, 65, has been our Senior Vice President of Human Resources since May 2006. From August 2003 through April 2006, Mr. Sprague was our Vice President of Human Resources. Prior to joining our Company, Mr. Sprague was the Managing Director Northeast, for Marc-Allen Associates, a nationwide executive recruiting firm. From 1996 to 2002, Mr. Sprague was the Assistant Vice President – Senior Director of Human Resources for Foot Locker Inc. and prior to that, the Assistant Vice President – Senior Director of Human Resources for Woolworth Corporation, the predecessor company to Foot Locker Inc.

Derrick Walker, 45, has been our Senior Vice President and Chief Marketing Officer since May 2012. Prior to joining our Company, Mr. Walker was the Vice President of Marketing for Lenscrafters from December 2009 to November 2011. Before that, Mr. Walker was the Vice President of Marketing for Finish Line from December 2006 to September 2009.

Former Non-Director Executive Officers

Dennis R. Hernreich, 56, was our Executive Vice President, Chief Operating Officer, Chief Financial Officer, Treasurer and Secretary from September 2002 until January 30, 2014. Prior to that, Mr. Hernreich served as our Senior Vice President, Chief Financial Officer and Treasurer upon joining us in September 2000. Prior to joining our Company, from 1996 through 1999, Mr. Hernreich held the position of Senior Vice President and Chief Financial Officer of Loehmann’s, a national retailer of women’s apparel. From 1999 to August 2000, Mr. Hernreich was Senior Vice President and Chief Financial Officer of Pennsylvania Fashions, Inc., a 275-store retail outlet chain operating under the name Rue 21.

John R. Wagner, 59, was our Vice President, Merchandise Manager for Tailored Clothing and Dress Furnishings from November 2010 until April 2014. Prior to joining our Company, Mr. Wagner was President of Innovative Sourcing Group, a New York based product development and sourcing firm specializing in men’s apparel. From 2001 to 2007, Mr. Wagner held the positions of Vice President of Manufacturing and Product Development and Vice President of Tailored Clothing for S&K Famous Brands, a men’s specialty retail chain based in Richmond, Virginia.

There are no family relationships between any of our directors and executive officers.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), requires our executive officers and directors, and persons who own more than 10% of a registered class of our equity securities (collectively, the “Reporting Persons”), to file reports of ownership and changes in ownership with the Securities and Exchange Commission (the “SEC”). The Reporting Persons are required to furnish us with copies of all Section 16(a) reports they file. Based solely upon a review of Forms 3, 4 and 5 and amendments thereto furnished to us during fiscal 2013, we believe that the current Reporting Persons complied with all applicable Section 16(a) reporting requirements and that all required reports were filed in a timely manner, with the following exceptions: Ms. Chew and Mr. Wagner both filed a late Form 4 on June 7, 2013 for the sale of shares; Ms. Ross filed a late Form 3 and Form 4 on February 13, 2013 related to her election as a director and for an initial stock option grant of 15,000 shares on January 31, 2013; and Mr. Mesdag filed a late Form 4 on February 7, 2014 for an initial stock option grant of 15,000 shares on January 29, 2014.

Code of Ethics

We have adopted a Code of Ethics which applies to our directors, Chief Executive Officer, Chief Financial Officer and Chief Accounting Officer, as well as our other senior officers. The full text of the Code of Ethics can be found under “Corporate Governance –Charters & Policies” on the Investor Relations page of the our corporate web site, which is at http://investor.destinationxl.com.

Audit Committee

We have a separately-designated standing Audit Committee established in accordance with section 3(a)(58)(A) of the Exchange Act. The Audit Committee is currently comprised of Messrs. Choper, Bernikow and Mesdag. Mr. Kyees served as a member of the Audit Committee until February 2, 2014, when he was appointed Interim Chief Financial Officer. Each of the current members of the Audit Committee is independent, as independence for Audit Committee members is defined under the rules of NASDAQ. In addition, the Board of Directors has determined that Mr. Bernikow is an “audit committee financial expert” under the rules of the SEC. No other directors attend audit committee meetings.

The Audit Committee operates under a written charter, which can be found under “Corporate Governance- Charters & Policies” on the Investor Relations page of our website at http://investor.destinationxl.com.

Item 11. Executive Compensation

Compensation Discussion and Analysis

This Compensation Discussion and Analysis discusses the compensation paid to our key executives which includes our Chief Executive Officer and our former Chief Financial Officer (“Key Executives”) as well as our other executive officers (the “Senior Executives”). For the purposes of this Form 10-K/A, the Key Executives and our next three most highly-compensated Senior Executives for fiscal 2013 are collectively referred to herein as our “Named Executive Officers.”

The Named Executive Officers for fiscal 2013 are: David A. Levin, President and Chief Executive Officer, Dennis R. Hernreich, former Executive Vice President, Chief Financial Officer, Chief Operating Officer, Treasurer and Secretary, Kenneth M. Ederle, Senior Vice President and Chief Merchandising Officer, Robert S. Molloy, Senior Vice President and General Counsel and Brian S. Reaves, Senior Vice President, Store Sales and Operations.

Mr. Levin is a Key Executive officer and Mr. Hernreich was a Key Executive until his departure on January 30, 2014. Our Senior Executives are listed above under “Item 10. Directors, Executive Officers and Corporate Governance-Current Non-Director Executive Officers.”

With Mr. Hernreich’s departure, John E. Kyees, a director of the Company, was appointed and served as Interim Chief Financial Officer from February 2, 2014 until May 31, 2014. Effective June 1, 2014, Peter H. Stratton, Jr., Senior Vice President Finance, Corporate Controller and Chief Accounting Officer was promoted to Senior Vice President, Chief Financial Officer and Treasurer of the Company.

The Compensation Committee of our Board of Directors determines the compensation for our Named Executive Officers. The responsibility of our Compensation Committee is to establish, implement and continually monitor adherence to our compensation philosophy, as well as ensure that the total compensation is fair, reasonable, competitive and consistent with the interests of the Company’s stockholders.

Say on Pay

At our 2011 Annual Meeting, stockholders voted on a non-binding advisory proposal as to the frequency with which we should conduct an advisory vote on executive compensation (a “say-on-pay proposal”). At that meeting, and in accordance with the recommendation of our Board of Directors, 93.5% of votes cast voted for the “one-year” frequency for advisory votes on executive compensation and we intend to hold such vote every year, until our next “say-on-pay” frequency vote, which we anticipate to be held at our 2017 annual meeting.

At our 2013 Annual Meeting, stockholders had an opportunity to cast a non-binding advisory vote on executive compensation as disclosed in the 2013 Proxy Statement. Of the votes cast on the say-on-pay proposal, 94.2% voted in favor of the proposal. The Compensation Committee considered the results of the 2013 advisory vote and believes that it affirms stockholders’ support of our approach to executive compensation, which approach is to align short- and long-term incentives with performance. We will continue to consider the outcome of subsequent say-on-pay votes when making future compensation decisions for our executive officers.

Executive Summary

We believe that our executive compensation policies and practices appropriately balance the interests of our executives with those of our stockholders. Performance is a key component of our philosophy for executive compensation. Accordingly, our executives’ compensation, specifically our compensation for our Chief Executive Officer, is heavily weighted toward “at risk” performance-based compensation. Our executives’ compensation consists of base salary (“fixed compensation”) and performance-based compensation (“at-risk compensation”).

For fiscal 2013, performance-based compensation consisted of an annual cash incentive based on achievement of specified performance goals under our annual incentive plan (or “AIP”) and a new long-term incentive plan with performance targets reflecting the longer-term goals and objectives of the Company. These two plans work together by setting targets aimed to reach our ultimate long-term strategic goals.

In April 2013, the Compensation Committee approved a new long-term incentive plan (the “2013-2016 LTIP”). Whereas our previous long-term incentive plan was based on achievement of current year targets with long-term vesting, our 2013-2016 LTIP is based on achievement of our long-term goals and the effective implementation of our business strategies, specifically, the successful

roll-out and growth of our DXL store concept. The 2013-2016 LTIP was originally designed as a four-year plan, consistent with our initial DXL store roll-out strategy, consisting of a combination of cash, stock options and restricted stock awards, of which half are subject to time-vesting conditions (to minimize attrition during these key years) and half are subject to the achievement of revenue and operating margin targets beginning in fiscal 2015. The philosophy behind the structure of the 2013-2016 LTIP was to encourage retention during this transition phase while also providing our management team an opportunity to earn compensation, commensurate with shareholder returns, if performance targets were achieved.

Under the terms of awards for the 2013-2016 LTIP, the time-based compensation portion of awards will not begin to vest until the end of fiscal 2014, and there was no opportunity for achievement of any of the performance-based targets in fiscal 2013. Because there was no opportunity in fiscal 2013 to earn any pay-out under the 2013-2016 LTIP, the base for target compensation that could be earned by our executives was significantly lower than when compared to fiscal 2012.

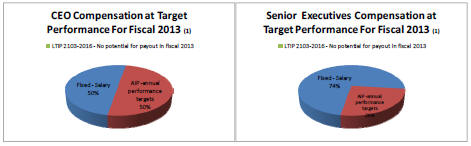

The following charts show the breakdown of compensation opportunity for our Chief Executive Officer (“CEO”) and Senior Executives in fiscal 2013, assuming performance under our AIP was achieved at “target” levels. As noted above, the following charts do not include any amounts attributable to the 2013-2016 LTIP because there was no opportunity for our executives to earn any pay-out under the LTIP in fiscal 2013. Accordingly, as reflected in the chart below, the percentage of fixed compensation to total compensation was higher for fiscal 2013 as compared to fiscal 2012 (when fixed compensation represented 33% and 49% for our Chief Executive Officer and Senior Executives, respectively), because there was an opportunity to earn a payout under the long-term incentive plan in fiscal 2012.

For fiscal 2013, with the exception of Mr. Ederle who was promoted to Chief Merchandising Officer, the base salary for our Named Executive Officers remained unchanged from fiscal 2012 levels. Accordingly, the only opportunity for our Named Executive Officers to achieve compensation above fiscal 2012 levels was to achieve the performance thresholds established under our AIP.

As a result of our actual earnings for fiscal 2013, the only additional compensation beyond salary that our executives earned in fiscal 2013 was a partial payout under our AIP, which approximated 14.3% of Mr. Levin’s salary and 5% of our Senior Executives’ salaries.

Summary of Fiscal 2013 Performance Compared to Fiscal 2012

For fiscal 2013, we reported a net loss of $59.8 million, or $(1.23) per diluted share, as compared to net income of $6.1 million, or $0.13 per diluted share, in fiscal 2012. The comparability of our operating results for fiscal 2013 was affected by an incremental non-cash charge of $51.3 million to establish a valuation allowance against our deferred tax assets, an asset impairment charge of $1.5 million and approximately $2.3 million in executive severance costs, which were accrued at the end of fiscal 2013. On a non-GAAP basis, our adjusted net loss was $6.2 million, or $(0.13) per diluted share. See footnote 4 to the table below for a reconciliation of these non-GAAP measures to GAAP.

This decrease in earnings, before consideration of the valuation allowance and executive severance costs, is primarily attributable to lower than expected sales. While our results for fiscal 2013 included approximately $23.2 million, or $0.29 per diluted share, in transition costs and incremental marketing to support our DXL roll-out, we expected that an increase in sales volume, driven by our store growth, would offset the majority of these costs.

Despite the lower than expected sales volumes in fiscal 2013, we remain very confident in our DXL strategy. Fiscal 2013 was a significant transitional year for us. The process of opening a significant number of new DXL stores, while at the same time liquidating twice as many Casual Male XL legacy stores, was challenging. Notwithstanding some of our misses in fiscal 2013, we are confident that we can improve upon our roll-out strategy as we move into fiscal 2014. Our plan was to complete the transition by the end of fiscal 2015, with 215 to 230 DXL stores opened and substantially all of our Casual Male XL stores closed. We are taking a more measured approach going forward and for fiscal 2014 we plan to open only 40 DXL stores and close 38 Casual Male XL and 2 Rochester clothing stores. We currently do not expect our transition will be complete until fiscal 2017, at which time, we expect we will have 250 DXL stores open.

| For the fiscal year ending: | ||||||||

| February 1, 2014 (Fiscal 2013) |

February 2, 2013 (Fiscal 2012) |

|||||||

| Financial Highlights: | (in millions, except per share and percentages) | |||||||

| Sales |

$ | 388.0 | $ | 399.6 | ||||

| Transition and increased marketing costs (1) |

$ | 23.2 | $ | 9.0 | ||||

| Operating income (loss) |

$ | (13.1 | ) | $ | 13.9 | |||

| EBITDA, a non-GAAP measure (2) |

$ | 7.8 | $ | 29.4 | ||||

| Tax provision (3) |

$ | 45.7 | $ | 5.2 | ||||

| Net income (loss) |

$ | (59.8 | ) | $ | 6.1 | |||

| Net income (loss) per diluted share |

$ | (1.23 | ) | $ | 0.13 | |||

| Adjusted net loss, non-GAAP measure(4) |

$ | (6.2 | ) | |||||

| Adjusted loss per diluted share, non-GAAP measure (4) |

$ | (0.13 | ) | — | ||||

| Shareholder Return(5): |

||||||||

| Total 1-year Shareholder Return |

17.0 | % | ||||||

| Total 2-year Shareholder Return |

60.6 | % | ||||||

| Total 3-year Shareholder Return |

30.0 | % | ||||||

| (1) | Transition costs summarize the one-time costs that are being incurred in connection with opening DXL stores and closing existing Casual Male XL and Rochester Clothing stores. These costs include preopening rent, lease termination costs, pre-opening payroll and training costs, and costs to close existing stores. |

| (2) | EBITDA, a non-GAAP measure, is defined as income from continuing operations before interest, taxes, depreciation and amortization. EBITDA should not be considered superior to or as a substitute for net income derived in accordance with GAAP. We use EBITDA because it: (i) measures performance over the periods in which executives can have significant impact, (ii) is directly linked to our annual incentive plan and long-term growth plan, and (iii) is a key metric used by management and the Board to assess our operating performance. EBITDA for fiscal 2013 was calculated as loss from continuing operations of $(59.7) million, plus interest of $1.0 million, taxes of $45.7 million and depreciation and amortization of $20.8 million. EBITDA for fiscal 2012 is calculated as income from continuing operations of $8.1 million, plus interest of $0.6 million, taxes of $5.2 million and depreciation and amortization of $15.5 million. |

| (3) | In the fourth quarter of fiscal 2013, based on our three-year cumulative loss and our forecasted operating loss for fiscal 2014, we established a full valuation allowance against our net deferred tax assets. |

| (4) | Adjusted Net Loss and Adjusted Loss per Diluted Share are non-GAAP measures and are not meant to be superior to or as a substitute for Net Loss or Loss per Diluted Share on a GAAP basis. No adjustments were made for fiscal 2012. The net loss for fiscal 2013 has been adjusted to exclude $2.3 million of executive severance costs, an asset impairment charge of $1.5 million and an incremental non-cash charge of $51.3 million for the establishment of the valuation allowance. For comparative purposes, an assumed normal tax rate of 40.2% was used. For fiscal 2013 Adjusted Net Loss and Adjusted Loss Per Share was calculated as follows: |

GAAP TO NON-GAAP RECONCILIATION

| $ Per diluted share | ||||||||

| (in millions, except per share data) |

||||||||

| Net loss, GAAP basis |

$ | (59.8 | ) | $ | (1.23 | ) | ||

| Add back: |

||||||||

| Executive severance accrual of $2.3 million, less tax at 40.2% of $0.9 million |

$ | 1.4 | $ | 0.03 | ||||

| Asset impairments of $1.5 million, less tax at 40.2% of $0.6 million |

$ | 0.9 | $ | 0.02 | ||||

| Charge to establish full valuation allowance |

51.3 | $ | 1.05 | |||||

|

|

|

|

|

|||||

| Adjusted net loss, non-GAAP basis |

$ | (6.2 | ) | $ | (0.13 | ) | ||

| Weighted average number of common shares outstanding on a diluted basis |

48.5 | |||||||

| (5) | Total 1-year Shareholder Return for fiscal 2013 was calculated by taking the percentage change in stock price from February 1, 2013 to January 31, 2014. Total 2-year Shareholder Return for fiscal 2013 was calculated by taking the percentage change in stock price from January 27, 2012 to January 31, 2014. Total 3-year Shareholder Return for fiscal 2012 was calculated by taking the percentage change in stock price from January 28, 2011 to January 31, 2014. No dividends were paid by us. We calculated all shareholder returns using the closing price of our common stock on the last business day of each fiscal year. |

Summary of Total Compensation Earned for Fiscal 2013 Compared to Fiscal 2012

As described above, because we did not achieve even the threshold in the majority of our performance goals in fiscal 2013, our Named Executive Officers earned only a partial award under the AIP for fiscal 2013. The actual results compared to the respective targets are discussed below under “Components of Executive Compensation –Performance-based annual cash incentives.”

As discussed above, our executives’ compensation for fiscal 2013 includes the initial grant of time-based equity awards under the LTIP 2013-2016 that will become 20% vested at the end of fiscal 2014, 40% at the end of fiscal 2015 with the remaining 40% vesting at the end of fiscal 2016. While the cash and performance-based components of the 2013-2016 LTIP will not be reflected until the time-vested cash component vests and the performance targets are achieved, the fair value of these time-based equity awards have to be reflected in the year of grant, or fiscal 2013.

With the exception of accrued severance for Mr. Hernreich and Mr. Ederle’s promotion to Chief Merchandising Officer, the increase in compensation for our Named Executive Officers for fiscal 2013 as compared to fiscal 2012 is solely due to the fair value of the time-vested portion of the equity awards granted under the 2013-2016 LTIP, which do not begin to vest until the end of fiscal 2014. As a result, our executives’ total compensation for fiscal 2013 appears substantially higher than fiscal 2012. Except as noted above, without consideration of the fair value of the time-vested portion of the awards under the 2013-2016 LTIP, total compensation for each of our Named Executive Officers in fiscal 2013 decreased over fiscal 2012. The following table summarizes total compensation earned by each Named Executive Officer for fiscal 2013 as compared to fiscal 2012. See the “Summary Compensation Table” below for a detailed description of compensation for each Named Executive Officer.

| Named Executive Officer |

% Change (1) |

February 1, 2014 (Fiscal 2013) (1) |

February 2, 2013 (Fiscal 2012) |

|||||||||

| David A. Levin, President and Chief Executive Officer |

73.7 | % | $ | 2,182,462 | $ | 1,256,675 | ||||||

| Dennis R. Hernreich (2) Former Executive Vice President, Chief Financial Officer, Chief Operating Officer, Treasurer and Secretary |

497.6 | % | $ | 3,909,699 | $ | 654,194 | ||||||

| Kenneth M. Ederle, Senior Vice President, Chief Merchandising Officer |

101.2 | % | $ | 691,969 | $ | 343,886 | ||||||

| Robert S. Molloy Senior Vice President, General Counsel and Secretary |

75.4 | % | $ | 707,704 | $ | 403,468 | ||||||

| Brian S. Reaves Senior Vice President, Store Sales and Operations |

74.8 | % | $ | 601,914 | $ | 344,423 | ||||||

| (1) | The amounts in this column include the following amounts attributable to the fair value of time-vested equity awards made to each Named Executive Officer under the 2013-2016 LTIP in fiscal 2013, none of which vested in fiscal 2013: Mr. Levin - $1,216,800; Mr. Hernreich - $932,880; Mr. Ederle - $341,250; Mr. Molloy - $341,250; Mr. Reaves - $288,750. |

| (2) | Mr. Hernreich’s time-vested awards, with a fair value of $932,880, were forfeited as a result of his termination of employment of January 30, 2014. Compensation for fiscal 2013 includes $2.3 million for accrued severance. |

Executive Compensation Philosophy and Objectives

Our Compensation Committee’s overarching compensation guiding principle is to reward our executives for the achievement of our primary business objectives: successfully complete the transformation to our DXL format, to grow our market share within the Big & Tall retail industry, to increase earnings and operating margins and, ultimately, to increase stockholder returns through increased stock price due to the increase in earnings and operating margins. For fiscal 2013, given the transformation that the Company had embarked upon, and the fact that the transition from our Casual Male XL format to our DXL format is a multi-year plan, the Committee was challenged with providing competitive, short and long-term compensation opportunities to our executives during this important transition period.

The Compensation Committee believes that the most effective executive compensation program is one designed to:

| • | Attract, retain and engage the executive talent we need to deliver on our performance expectations; |

| • | Reward the achievement of specific annual, long-term and strategic goals through a combination of both cash and stock-based compensation; |

| • | Align the executives’ interests with those of our stockholders; and |

| • | Deliver a total compensation opportunity competitive with those available to similarly situated executives at our peer companies. |

When reviewing compensation, the Compensation Committee evaluates the pay structure in two primary ways: “total cash compensation” and “total direct compensation.” The total cash compensation, which consists of the executive’s base salary and an annual performance-based cash incentive award, is tied to our annual performance targets, which is generally EBITDA but also includes other performance targets. The total direct compensation includes the total cash compensation plus target long-term incentive awards. Our current long-term incentives reward the achievement of our long-term objectives of increasing revenue and operating margin percentage, which we believe is aligned with stockholder returns.

We seek to balance the mix of short and long-term compensation in order to ensure adequate base compensation and annual incentive opportunities to attract and retain executive talent, while providing meaningful incentives for them to create long-term sustained value for our Company and our stockholders.

With respect to the overall compensation paid to our Chief Executive Officer, the Compensation Committee’s objective is to achieve a total direct compensation amount that is within our peer median if we are able to achieve financial targets. As such, the Compensation Committee’s objective is to allocate the Chief Executive Officer’s total direct compensation equally between base salary, annual and long-term incentive awards.

For our Senior Executives, the Compensation Committee’s overall objective is to provide them with a competitive base salary that is within our peer median, while providing them with an opportunity for short- and long-term compensation if our Company meets or exceeds its financial targets, such as EBITDA and operating margins.

Over the years, the Compensation Committee has continued to fine-tune the pay for performance and shareholder alignment focus of our executive compensation programs. Prior to fiscal 2008, we provided cash compensation in the form of base salary to meet competitive salary norms and rewarded performance against specific short-term goals in the form of cash bonuses. Additionally, we provided stock options to reward superior performance against specific objectives and long-term strategic goals. In fiscal 2008, with the adoption of a Long-Term Incentive Plan (“LTIP”), which was first amended in May 2010, our management team was offered a compensation plan designed to award superior performance against short-term objectives. However, any award earned (which could be in the form of cash, stock options, restricted stock or any combination thereof based on the prior election of the executives) was subject to a ratable three-year vesting period commencing on the first anniversary of the date of grant. Beginning in fiscal 2010, there were further refinements made with the intention of improving alignment of executive compensation with stockholders’ interest and the Company’s long-term strategic goals. Specifically, all participants in our LTIP, which include our Named Executive Officers, were required to elect at least 50% of any award earned in equity, either through stock options or shares of restricted stock or a combination thereof, in order to be more aligned with our stockholders.

For fiscal 2013, the Compensation Committee redefined the metrics for both the AIP and 2013-2016 LTIP to align the potential awards under these plans with the Company’s current multi-year year strategic plan to transition to the DXL format as communicated to the investment community and its shareholders. See “Components of Executive Compensation” below for more information about the 2013 AIP and 2013-2016 LTIP.

Risk Assessment

We believe that our compensation programs do not provide incentives for unnecessary risk taking by our employees. Our employment agreements with each of our executives include a “clawback” provision which permits us to demand full repayment of all amounts paid to the executive in the event we learn after the executive’s termination that the executive could have been terminated for “justifiable cause.” Our emphasis on performance-based annual and long-term incentive awards is also designed to align executives with preserving and enhancing shareholder value. Based on these considerations, among others, we do not believe that our compensation policies and practices create risks that are likely to have a material adverse effect on our Company.

Compensation Committee Process

In periodic consultations with Sibson Consulting, an independent firm which specializes in benefits and compensation, the Compensation Committee has developed a compensation program that is competitive within our peer group. Our Compensation Committee has assessed the independence of Sibson Consulting and has concluded that no conflict of interest exists with respect to the services that Sibson Consulting performs for our Compensation Committee. Sibson Consulting did not provide any services to the Company other than with respect to the services provided to the Compensation Committee as described below. The consultant most recently analyzed compensation and benefits for our Named Executive Officers in fiscal 2011 and again for Mr. Levin in the Spring of 2014, as it relates to compensation and benefits for fiscal 2014.

The Compensation Committee has the authority to retain compensation consultants and other outside advisors, without Board or management approval, to assist it in carrying out its duties, including the evaluation of compensation to be paid to our Named Executive Officers. The Compensation Committee may accept, reject or modify any recommendations by compensation consultants or other outside advisors. Since 2006, the Compensation Committee has retained Sibson Consulting to analyze compensation and benefits of our peer companies with respect to our Key Executive compensation. In 2011, the consultant analyzed total compensation for the past five-year period for our Named Executive Officers and compared that information with that of our peer companies. In addition, the consultants also reviewed total compensation paid to our Named Executive Officer in comparison to our Company’s financial performance. In fiscal 2012 and fiscal 2013, Sibson Consulting also worked with the Compensation Committee on updating and revising our current annual incentive plan and long–term incentive plan. Sibson Consulting continues to work with the Compensation Committee on an on-going basis to ensure that its compensation program remains in line with our peer group as well as with our own business objectives.

When determining peer companies, we chose public companies within the specialty retail apparel business with comparable sales and market capitalization. In April 2014, the Compensation Committee removed Coldwater Creek, The Finish Line, Hot Topic, JoS A. Bank and Rue 21 from the peer group. The Compensation Committee added bebe stores, inc., Body Central Corp., Kirkland’s Inc., MarineMax, Inc., and Zumiez, Inc. This revised peer group will be in effect for compensation decisions made in fiscal 2014:

| • bebe, inc. |

• Christopher & Banks |

• MarineMax, Inc. | ||

| • Big 5 Sporting Goods |

• Citi Trends |

• Pacific Sunwear | ||

| • Body Central Corp. |

• dELiA*s |

• Sport Chalet | ||

| • The Buckle |

• Destination Maternity |

• Wet Seal | ||

| • Cache. |

• Hibbett Sports |

• Zumiez, Inc. | ||

| • Cato Group |

• Kirkland’s, Inc. |

-Key Executives

The Committee’s overall goal is for Mr. Levin’s total direct compensation to fall within the median of our peer group; however, this guideline may differ depending on an individual’s qualifications, role content and scope, past performance, the demand for individuals with the executive’s specific expertise and experience, achievement of our financial objectives and the executive’s contribution to such achievement and overall responsibility, among other criteria.

The Compensation Committee is directly responsible for determining the compensation paid to Mr. Levin. The Compensation Committee, working with Sibson Consulting, compares each element of compensation to published survey data and proxy data from our peer group for executives with comparable positions and responsibilities. Based on that detailed review which was completed at the end of fiscal 2011, the Committee concluded that the total cash compensation and total direct compensation for Mr. Levin, as well as, Mr. Hernreich were appropriate. This conclusion was based on the following observations:

| • | Assuming that the Company’s performance targets are achieved and Mr. Levin receives performance-based compensation, Mr. Levin’s total cash compensation and total direct compensation is competitive and within our peer median. (The Committee measures “competitive” as compensation that is between 85% to 115% of targeted market level among our peers). |

| • | Mr. Hernreich’s total cash compensation and total direct compensation was above the market median for either a chief financial officer or chief operating officer when compared to our peers. However, our Company is organized differently from our peers. Until his departure, Mr. Hernreich served in multiple roles as our Executive Vice President, Chief Operating Officer, Chief Financial Officer, Treasurer and Secretary. Because of Mr. Hernreich’s multiple responsibilities, the Committee believed that compensation above the median was appropriate recognition of Mr. Hernreich’s multi-faceted responsibilities. Further, the Committee believed Mr. Hernreich’s total compensation was far below the expense which would be incurred by adding additional executives to fill each of the many roles filled by Mr. Hernreich. |

Sibson Consulting was engaged in April 2014 to review Mr. Levin’s compensation and no adjustments were made to his compensation or benefits for fiscal 2014. The Compensation Committee believes that Mr. Levin’s salary continues to be competitive and within our peer median.

-Senior Executives

Our Chief Executive Officer and the Senior Vice President of Human Resources are primarily responsible for determining the compensation paid to our Senior Executives, subject to ratification or approval by the Compensation Committee. For benchmarking purposes, several published industry compensation surveys are utilized when determining compensation packages for our Senior Executives. Through our subscriptions with Salary.com and the National Retail Federation, we have access to the latest compensation data, which includes both base salary and total compensation, inclusive of incentives. While these sites do not identify the specific companies included in the survey, we are able to access information based on industry, size, such as sales volumes, and regional area, among others. In general, we benchmark compensation against companies in the retail industry which are of similar size, based on comparative sales volumes. When recruiting a senior management position, we will also benchmark against larger or more complex business structures to ensure we retain the best talent to support future growth. A combination of performance, achievement of goals and survey data, among other criteria, is used to determine each Senior Executive’s total direct compensation opportunity. Like our Chief Executive Officer, the Senior Executives are provided with a competitive base salary within our retail industry and are provided with an opportunity to earn performance awards each year which are primarily driven by our overall financial targets. See “Components of Executive Compensation – Performance–based annual cash bonuses and –Long-term performance based awards.”

Periodically, our Compensation Committee will engage Sibson Consulting to review the compensation for Senior Executives who are also Named Executive Officers. Sibson Consulting conducted a detailed review of the Company’s top six positions in May 2011 and an updated review of compensation of the Company’s Named Executive Officers in January 2012 for fiscal 2012. As a result of the in-depth study in May 2011, the Compensation Committee observed that the compensation earned for fiscal 2010 was at or below the 50th percentile of our peer group. Further, the Committee noted that the compensation paid to our Senior Executives is more heavily weighted toward incentive programs than with our peer group. That comprehensive study was conducted during a year when bonuses were earned under the Annual Incentive Plan and the LTIP. Based on Sibson’s work, the Committee determined that the compensation opportunity for the Senior Executives who are also Named Executive Officers was appropriate given their specific roles with the Company and the intent of the Committee to emphasize rewards based on achievement of performance goals.

Components of Executive Compensation

The primary components of compensation for our Named Executive Officers include base salary, annual performance-based cash incentives and long-term incentives. The components of compensation are described as follows:

| • | Base salary |

The base salary represents the fixed component of an executive’s annual compensation. In order to be competitive in the marketplace and attract the top executive talent, we believe that it is important that our base salary be competitive, generally falling within the median of our industry peers.

Base salaries are reviewed annually and adjustments are influenced by our performance in the previous fiscal year and the executive’s contribution to that performance. The executive’s performance is measured by various factors, including, but

not limited to, achievement of specific individual and department goals. Additionally, adjustments may consider the individual’s promotion that may have occurred during the fiscal year, and any modifications in the individual’s level of responsibility.

As mentioned above, the Compensation Committee reviews Mr. Levin’s overall compensation. The Committee expects Mr. Levin’s base salary to generally fall in a range that is within the proxy peer median and that approximately one-third of his total direct compensation will be in the form of base salary. In making base salary decisions for our Senior Executives, Mr. Levin, working with Human Resources, will rely on published industry compensation surveys and target the market median range.

With the exception of Mr. Ederle, who was promoted to Senior Vice President and Chief Merchandising Officer in April 2013, the base salaries of our Named Executive Officers have remained flat for the past five years. In April 2014, Mr. Ederle received a 7.7% increase, which included a merit increase and salary adjustment as a result of a compensation review of peers and Mr. Molloy received a merit increase of 3.1%.

| • | Performance-based annual cash incentives |

The Compensation Committee believes that a substantial portion of each executive’s compensation should tie directly to our financial performance. Our compensation program includes eligibility for an annual performance-based cash incentive opportunity for all executives as well as selected non-executive employees. The Committee believes that an annual cash incentive component of compensation is necessary to provide additional incentive to help achieve the annual goals, which ultimately benefit our stockholder value.

2013 Annual Incentive Plan

With the assistance of Sibson Consulting, the Compensation Committee re-designed the financial metrics and targets for the Annual Incentive Plan (“AIP”) for fiscal 2013. With the DXL transformation, there were metrics beyond EBITDA that the Compensation Committee felt were important and warranted focus, and that the metrics should be both challenging and result in a measurable positive impact on the Company. The Committee deemed it important that performance be measured in part by how margins and debt were managed and controlled in a year when we planned increased marketing and capital expenditures. In addition, the Compensation Committee wanted to reward management for improvement in our sales growth and customer base as we continue to transition to the DXL concept. Accordingly, the Compensation Committee identified four target metrics for fiscal 2013, each of which was independent of the other, of which two were financial measures and two were strategic measures.

On April 23, 2013, the financial metrics and targets were approved by the Compensation Committee. The targets were as follows:

| Metric |

Award % Attributable to Each Target |

Minimum/Maximum Potential Payout |

Actual Results | |||||||

| Target 1 | EBITDA | 50.0 | % | -85% of EBITDA target to receive minimum payout of 50%

-125% of EBITDA target to receive maximum payout of 150% |

The EBITDA target for fiscal 2013 was $23.0 million. Actual EBITDA was $7.8 million; accordingly, there was no payout under Target 1. | |||||

| Target 2 | Merchandise Margin (internal metric) and Net Debt | 25.0 | % | -Both metrics must be met to earn 100%; otherwise no payout

-The merchandise margin target for fiscal 2013 was considered achievable, with a 50% probability

-If the maximum payout of 150% is achieved in all three of the other targets, then 150% would be paid out under this target |

Although our merchandise margin was met, our Net Debt had to be less than or equal to $13.0 million. Actual Net Debt was $21.2 million. Accordingly, there was no payout under Target 2. | |||||

| Target 3 | Customer Base Growth | 12.5 | % | 100% of payout at set target, with pro-rata percent increase up to a maximum payout of 150% at 125% of target; and a pro-rata payout for any percentage increase up to 100% of set target | The Customer Base Growth target for fiscal 2013 was an increase of 1.6% in new customers. Actual customer base did not increase; accordingly, there was no payout under Target 3. | |||||

| Target 4 | DXL Comparable Sales | 12.5 | % | -80% of DXL Store Comp target to receive minimum payout of 50%

-200% of DXL Store Comp target to receive maximum payout of 150% |

Our DXL comparable sales had to increase 15% to receive 12.5% payout. Actual DXL comparable sales were 19.3%, which resulted in a payout percentage of 114.4% of the 12.5% attributed to Target 4. | |||||

As a result of exceeding the DXL Comparable Sales target for fiscal 2013, on March 5, 2014 the Compensation Committee approved a cash bonus payout equal to 114.4% of the 12.5% target. The total cash award paid under the 2013 AIP was approximately $535,000, of which approximately $271,000 was paid to our Senior Executives and Mr. Levin. As part of his severance, Mr. Hernreich received a pro-rata portion of his award, see “Employment Agreements – Key Executives” below.

2014 Annual Incentive Plan

Similar to our 2013 AIP, the metrics for achievement under our Annual Incentive Plan for fiscal 2014 represent the primary financial goals for the Company which are to increase top line revenues while protecting merchandise margin and managing expenses during our DXL transition. In addition, increasing our sales per square foot and comparable sales from our DXL stores remain key metrics for our long-term profitability. For fiscal 2014, 10% of the award will be based on each participant’s achievement of generally two to four agreed-upon personal goals. This will reward each participant for success that may not directly tie into our financial performance, but we believe will contribute to the success of our DXL transformation. The Committee approved the financial targets and metrics on April 1, 2014. The targets were as follows:

| Metric |

Award % Attributable to Each Target |

Minimum/Maximum Potential Payout | ||||||

| Target 1 |

Sales |

25.0 | % | 100% payout at set target, with 50% payout at 98% of set target and 150% payout at 105% | ||||

| Target 2 |

EBITDA |

25.0 | % | 100% payout out at set target, with 50% payout at 90% of set target and 150% payout at 128% | ||||

| Target 3 |

Merchandise Margin |

15.0 | % | Target must be achieved for a minimum payout of 100%, with 125% payout at 102.5% of target and 150% of payout at 105% of target. | ||||

| Target 4 |

DXL Comparable Sales |

15.0 | % | 100% payout at set target, with 50% payout at 71.4% of target and 150% of payout at 1.21% of target | ||||

| Target 5 |

DXL Sales per Square Foot |

10.0 | % | 100% payout at set target, with 50% payout at 93.7% of target and 150% of payout at 109.4% | ||||

| Target 6 |

Personal Goals |

10.0 | % | Participants must achieve all personal goals for 100% payout but if all goals are not achieved participants will be able to receive a partial payout equal to the number of personal goals that were achieved. | ||||

Assuming a 100% payout is achieved under the 2014 AIP, if the 2014 AIP were to be paid today based on salaries as of May 1, 2014, the 2014 AIP would be based on salaries earned of $811,200 for Mr. Levin, $350,000 for Mr. Ederle, $335,000 for Mr. Molloy and $275,000 for Mr. Reaves. Mr. Kyees, in his interim role as Interim Chief Financial Officer, is also eligible to participate in the AIP for fiscal 2014 at a rate of 75% of his total per diem amount paid for his services as Interim Chief Financial Officer. Assuming we achieve 100% of the above targets for fiscal 2014, we estimate that the total potential payout would be approximately $4.5 million, of which $2.5 million would be paid to our Chief Executive Officer and Senior Executives and the remaining amount would be paid to the approximately 100 other participants in the AIP. The Compensation Committee believes this is a competitive level of compensation and provides incentives to all of our senior executives and other employees of the Company who serve in important job functions if we are to achieve our annual financial goals.

The Compensation Committee believes that it is possible to meet or exceed the targets set for fiscal 2014. The established targets are intended to be achievable within an approximate 50% probability as a result of executing our operating plan. The target levels are derived from our annual operating plan and budget for the fiscal year. The operating plan and budget set forth our internal goals and objectives for our growth and development and are expected to require substantial efforts by the entire Company to achieve. As a result, the likelihood of achieving the 2014 targets reflects the challenges inherent in achieving the goals and objectives in the operating plan and budget. The Compensation Committee considered the likelihood of achieving the target levels when approving the target amount, including historical achievement by our executive officers.

| • | Long-term performance based plans |

From fiscal 2008 through fiscal 2012, our long-term incentive based plan rewarded the achievement of meeting the current year objectives with the awards vesting over a three-year period once earned, ultimately benefiting our stockholders while developing and retaining a strong management team. On May 28, 2013, the 2008 Long-Term Incentive Plan (“LTIP”), as amended, was terminated and superseded by our 2013-2016 Long-Term Incentive Plan (“2013-2016 LTIP”). The 2013-2016 LTIP was designed for the specific purposes of retaining and rewarding the efforts required for the Company to transition to the DXL, which was originally expected to be four years.

2013-2016 Long-Term Incentive Plan (the “2013-2016 LTIP”)

The structure of the 2013-2016 LTIP was designed by the Compensation Committee working with Sibson Consulting. Its two primary goals are to help retain our management team during our transition to the DXL concept while also tying the reward to the achievement of our long-term objectives. Unlike the previous LTIP, the performance targets are not based solely on current year performance. Given that the Company is undergoing a several year strategic transformation of its business and the four-year 2013-2016 LTIP is a significant departure from our previous annual LTIP plan, at the request of the Compensation Committee, the full board reviewed the design and structure of the plan on May 9, 2013. On May 28, 2013, the Compensation Committee approved the 2013-2016 LTIP.

On May 28, 2013, each participant was granted an unearned and unvested award equal to four times their annual salary multiplied by their long-term incentive program percentage, which is 100% for the Chief Executive Officer and 70% for the Senior Executives. This award amount is referred to as the “Projected Benefit Amount.” Each participant was granted 50% of the Projected Benefit Amount in shares of restricted stock, 25% in stock options with the remaining 25% in cash. The closing price of the Company’s common stock on May 28, 2013 was used to determine the number of shares of restricted stock and to determine the Black-Scholes value in calculating the number of stock options issued.

Of the total Projected Benefit Amount, 50% is subject to time-based vesting and 50% is subject to performance-based vesting. The time-vested portion of the award (half of the shares of restricted stock, options and cash) will vest in three installments with 20% vesting at the end of fiscal 2014, 40% at the end of fiscal 2015 and the remaining 40% vesting at the end of fiscal 2016.

For the performance-based portion of the award to vest, the Company must achieve, during any rolling four fiscal quarter period that ends on or before the end of fiscal 2015, revenue of at least $550 million and an operating margin of not less than 8.0%. In the event that the Company achieves its target of $550 million in revenue with an operating margin not less than 8.0% during any rolling fiscal four quarters prior to the commencement of fiscal 2016, then the total Projected Benefit Amount vests in full.

If the targets for vesting of the performance-based portion of the award are not met by the end of fiscal 2015, then the performance-based target can still be met in fiscal 2016. In fiscal 2016, the Company must achieve revenue of at least $600 million and an operating margin of not less than 8.0% for participants to receive 100% vesting of the performance-based portion of the Projected Benefit Amount. If the Company does not meet the performance target at the end of fiscal 2016, but the Company is able to achieve revenue equal to or greater than $510 million at the end of fiscal 2016 and the operating margin is not less than 8.0%, then the participants will receive a pro-rata portion of the performance-based award based on minimum sales of $510 million (50% payout) and $600 million (100% payout).

Unlike the previous LTIP, the participants are not able to achieve greater than 100% of the Projected Benefit Amount. The Committee, working with Sibson Consulting, decided to construct the 2013-2016 LTIP such that any upside to be gained by participants for their efforts during this multi-year year transition to the DXL concept should be aligned with shareholders and come only from any increase in the value of the equity granted to participants at May 28, 2013.

The Compensation Committee initially believed when adopting the 2013-2016 LTIP that there was an approximate 50% probability of meeting the performance targets set forth in the plan. We believe that our performance targets were established at levels that were intended to be difficult but attainable. The target levels of the performance objectives were derived from our five-year operating plan and budget. The operating plan and budget set forth our internal goals and objectives for our growth and development and are expected to require substantial efforts by the entire Company to achieve. As a result, the likelihood of achieving the performance targets reflected the challenges inherent in achieving the goals and objectives in the operating plan and budget. The Compensation Committee considered the likelihood of achieving the target levels when approving the target amounts, including historical achievement by the Company. Based on actual results through fiscal 2013 and the expectation that the DXL roll-out will not be completed until the end of fiscal 2017, the probability of meeting the original performance targets established in May 2013 have become much more difficult. As discussed above, as the Company has determined to take a more measured approach going forward, the Company currently does not plan on the transition being completed until fiscal 2017. As a result, the Compensation Committee is currently reviewing and considering whether changes to the 2013-2016 LTIP are appropriate given the Company’s current expectations on completion of the DXL roll-out.

Assuming we achieve the performance target and 100% of the Projected Benefit Amount vests, without forfeiture, the total potential payout over this four year period will be approximately $18.5 million, of which $11.5 million would be paid to our Chief Executive Officer and Senior Executives. The compensation expense related to the time-vested portion of the award, or half of the $18.5 million, is being expensed in three tranches, based on the above vesting dates. The remaining compensation expense related to the performance-based portion of the award will not begin to be expensed until it becomes probable that the Company will be able to achieve the performance targets. We cannot predict if and how much of this award will be earned and/or vested.

Because of the long-term nature of the 2013-2016 LTIP, the plan includes provisions regarding the impact on unvested awards after fiscal 2013 of the termination of employment of a participant due to retirement, death, or disability of the participant, termination by the Company of a participant without justifiable cause (as defined in the plan) and termination by the participant for good reason (as defined in the plan) and termination in connection with a change in control of the Company. The impact on unvested awards differs depending on the nature and timing of the termination, as described below.

Termination due to Retirement

Fiscal 2014-Fiscal 2016 - The participant will be entitled to the pro-rata portion of their time-based award that would have vested at the end of the fiscal year in which the participant retired. The time-vested portion will immediately be paid out. With respect to the performance-based portion of the award, the participant will become vested in his/her pro-rata portion of the award as of the date of his termination of employment; however, the participant will not receive a payout of the award unless the Company subsequently meets its performance target, at which time, the participant will receive a payout based on the performance target achieved, if any, at the pro-rata vesting percentage at the time of retirement.

Termination due to Death or Disability of Participant

Fiscal 2014 – The participant will be entitled to the pro-rata portion of his/her time-based award. The time-vested portion will immediately be paid out. With respect to the performance-based portion of the award, the participant will become vested based on a pro-rata basis as of the date of termination and will immediately be paid out on that pro-rata basis. Such calculation will assume that the performance target will be achieved.

Fiscal 2015 – Fiscal 2016 - The participant will be entitled to 100% of his/her time-based award. The time-vested portion will immediately be paid out. With respect to the performance-based portion of the award, the participant will become 100% vested and the award will be paid out only if, when and to the extent any performance target is achieved.

Termination by the Company without justifiable cause or by the participant for good reason

Fiscal 2014 – The participant will be entitled to the pro-rata portion of his/her time-based award. The time-vested portion will immediately be paid out. With respect to the performance-based portion of the award, the participant will become vested based on a pro-rata basis as of the date of termination and will immediately be paid out on that pro-rata basis. Such calculation will assume that the performance target will be achieved.

Fiscal 2015 – Fiscal 2016 - The participant will be entitled to 100% of his/her time-based award. The time-vested portion will immediately be paid out. With respect to the performance-based portion of the award, the participant will become 100% vested and the award will be paid out only if, when and to the extent any performance target is achieved.

Termination in connection with a Change in Control

The 2013-2016 LTIP also includes a “double trigger” change in control provision that requires payment in the event of termination other than for cause or retirement 6 months before or within 18 months after a change in control in the Company. The Company believes that such “double trigger” represents good corporate governance practice. In the event of a change in control, if a participant is terminated within 6 months before or within 18 months after the change in control for any reason other than retirement or by the Company for cause, the unvested portion of the participant’s award will immediately vest and be paid out (as of the date of the change in control or the termination, whichever occurred last).