Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - GRAPHITE CORP | Financial_Report.xls |

| EX-31.1 - CERTIFICATION - GRAPHITE CORP | grph_ex311.htm |

| EX-31.2 - CERTIFICATION - GRAPHITE CORP | grph_ex312.htm |

| EX-32.1 - CERTIFICATION - GRAPHITE CORP | grph_ex321.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2013

Commission File No. 000-54336

GRAPHITE CORP.

(Exact name of registrant as specified in its charter)

|

Nevada

|

26-0641585

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

1031 Railroad Street, Suite 102A

Elko, Nevada 89801

(Address of principal executive offices, zip code)

(775) 753-6605

(Registrant’s telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to section 12(g) of the Act:

Common Stock, $.00001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) Yes ¨ No x

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

|

o |

Accelerated filer

|

o |

|

Non-accelerated filer

|

o |

Smaller reporting company

|

x |

|

(Do not check if a smaller reporting company)

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

At June 30, 2013, the last business day of the Registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting common stock held by non-affiliates of the Registrant (without admitting that any person whose shares are not included in such calculation is an affiliate) was approximately $4,592,000. At March 28, 2014, there were 27,700,000 shares of the Registrant’s common stock, $0.00001 par value per share, outstanding. At December 31, 2013, the end of the Registrant’s most recently completed fiscal year, there were 28,700,000 shares of the Registrant’s common stock, par value $0.00001 per share, outstanding.

GRAPHITE CORP.

TABLE OF CONTENTS

|

Page No.

|

|||||

| PART I | |||||

|

Item 1.

|

Business

|

4

|

|||

|

Item 1A.

|

Risk Factors

|

14

|

|||

|

Item 1B.

|

Unresolved Staff Comments

|

14

|

|||

|

Item 2.

|

Properties

|

14

|

|||

|

Item 3.

|

Legal Proceedings

|

14

|

|||

|

Item 4.

|

Mine Safety Disclosures

|

14

|

|||

| PART II | |||||

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

15

|

|||

|

Item 6.

|

Selected Financial Data

|

16

|

|||

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

16

|

|||

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

22

|

|||

|

Item 8.

|

Financial Statements and Supplementary Data

|

23 | |||

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

24 | |||

|

Item 9A.

|

Controls and Procedures

|

24 | |||

|

Item 9B.

|

Other Information

|

25 | |||

| PART III | |||||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

26

|

|||

|

Item 11.

|

Executive Compensation

|

28 | |||

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

30 | |||

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

30

|

|||

|

Item 14.

|

Principal Accounting Fees and Services

|

30

|

|||

| PART IV | |||||

|

Item 15.

|

Exhibits and Financial Statement Schedules

|

32

|

|||

|

Signatures

|

33

|

||||

2

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K of Graphite Corp., a Nevada corporation, contains “forward-looking statements,” as defined in the United States Private Securities Litigation Reform Act of 1995. In some cases, you can identify forward-looking statements by terminology such as “may”, “will”, “should”, “could”, “expects”, “plans”, “intends”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of such terms and other comparable terminology. These forward-looking statements include, without limitation, statements about our market opportunity, our strategies, competition, expected activities and expenditures as we pursue our business plan, and the adequacy of our available cash resources. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Actual results may differ materially from the predictions discussed in these forward-looking statements. The economic environment within which we operate could materially affect our actual results. Additional factors that could materially affect these forward-looking statements and/or predictions include, among other things: the volatility of minerals prices, the possibility that exploration efforts will not yield economically recoverable quantities of minerals, accidents and other risks associated with mineral exploration and development operations, the risk that the Company will encounter unanticipated geological factors, the Company’s need for and ability to obtain additional financing, the possibility that the Company may not be able to secure permitting and other governmental clearances necessary to carry out the Company’s exploration and development plans, other factors over which we have little or no control; and other factors discussed in the Company’s filings with the Securities and Exchange Commission (“SEC”).

Our management has included projections and estimates in this Form 10-K, which are based primarily on management’s experience in the industry, assessments of our results of operations, discussions and negotiations with third parties and a review of information filed by our competitors with the SEC or otherwise publicly available. We caution readers not to place undue reliance on any such forward-looking statements, which speak only as of the date made. We disclaim any obligation subsequently to revise any forward-looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

All references in this Form 10-K to the “Company”, “Graphite”, “we”, “us,” or “our” are to Graphite Corp.

3

PART I

|

ITEM 1.

|

BUSINESS

|

We were incorporated in the State of Nevada on August 3, 2007 under the name Medzed, Inc. We were originally established for the purpose of becoming a third party reseller of medical office business solutions. However, due to poor performance related to the sales of the medical office business solutions, we believe as of September 30, 2008, the Company became a “shell” company, as that term is defined in Rule 12b-2 of the Securities Exchange Act of 1934.

From the time that the Company was considered a shell company until the time that we ceased being a shell company, we had focused our efforts on developing a new business, merging with, or acquiring an operating company with an operating history and assets. Accordingly, we refocused the Company's business direction to include a new business plan based on the exploration of mineral claims. We decided to enter the mining business because we were seeking out viable and feasible alternatives to create value for our shareholders. We determined that staking and exploring potential mineral claims could be an excellent long term investment strategy that could lead to lucrative business opportunities. To reflect the Company’s new focus, on August 19, 2010, we filed an amendment to our Articles of Incorporation with the Nevada Secretary of State changing our name to First Resources Corp. The Company subsequently narrowed its focus to graphite mining and on June 14, 2012, we again filed an amendment to our Articles of Incorporation with the Nevada Secretary of State changing our name to Graphite Corp.

We are considered an exploration or exploratory stage company because we are involved in the examination and investigation of land that we believe may contain valuable minerals, for the purpose of discovering the presence of graphite and other minerals, if any, and their extent. Because we are an exploration stage company, there is no assurance that a commercially viable mineral deposit exists on the properties underlying our mineral claims, and a great deal of further exploration will be required before a final evaluation as to the economic and legal feasibility for our future exploration is determined. We have no known reserves of any type of mineral. To date, we have not discovered an economically viable mineral deposit, and there is no assurance that we will discover one.

Exploration for minerals is a speculative venture involving substantial risk. The expenditures to be made by us on our exploration program may not result in the discovery of commercially exploitable reserves of valuable minerals. The probability of a mineral claim ever having commercially exploitable reserves is extremely remote, and in all probability, our mineral claims may not contain any reserves. If we are unable to find reserves of valuable minerals or if we cannot remove the minerals because we either do not have the capital to do so, or because it is not economically feasible to do so, then we will cease operations and potential investors will lose their investment.

We anticipate that any additional funding that we require will be in the form of equity financing from the sale of our Common Stock. However, there is no assurance that we will be able to raise sufficient funding from the sale of our Common Stock. The risky nature of this enterprise and lack of tangible assets places debt financing beyond the credit-worthiness required by most banks or typical investors of corporate debt until such time as an economically viable mine can be demonstrated. We do not have any arrangements in place for any future equity financing. If we are unable to secure additional funding, we will cease or suspend operations. We have no plans, arrangements or contingencies in place in the event that we cease operations.

If we discontinue our exploration of our properties, we may seek to acquire other natural resource exploration properties. Any such acquisition(s) will involve due diligence costs in addition to the acquisition costs. We will also have an ongoing obligation to maintain our periodic filings with the appropriate regulatory authorities, which will involve legal and accounting costs. In the event that our available capital is insufficient to acquire an alternative resource property and sustain minimum operations, we will need to secure additional funding or else we will be compelled to discontinue our business. We are presently in the exploration stage of our business and have not commenced planned principal operations. We can provide no assurance that we will discover commercially exploitable levels of mineral resources on our properties, or if such deposits are discovered, that we will enter into further substantial exploration programs.

If commercially marketable quantities of mineral deposits exist on the properties underlying our mineral claims and sufficient funds are available, we will evaluate the financial viability, technical and financial risks of extraction, including an evaluation of the economically recoverable portion of the deposit, the metallurgy and ore recoverability, marketability and payability of the ore concentrates, engineering concerns, milling and infrastructure costs, finance and equity requirements and an analysis of the proposed mine from the initial excavation all the way through to reclamation. After we conduct this analysis and determine that a given ore body is worth recovering, we will begin the development process. Development will require us to obtain a processing plant and other necessary equipment including delivery equipment to transport the processed ore to our future customers.

4

To date, we have not earned any revenues and have incurred a net loss of $369,650, in the year ended December 31, 2013 and a net loss of $2,453,955 since inception. We do not anticipate earning revenues until such time as we enter into commercial production of our mineral properties. These factors raise substantial doubt about the Company’s ability to continue as a going concern. The ability of the Company to continue as a going concern is dependent upon its ability to successfully accomplish its plan of operations described herein and eventually attain profitable operations.

Glossary of Technical Geological Terms

The following defined technical geological terms are used in our annual report:

|

Term

|

Definition

|

|

|

Adularia

|

A feldspar mineral and potassium aluminosilicate (KAlSi3O8). It commonly forms colourless, glassy, prismatic, twinned crystals in low-temperature veins of felsic plutonic rocks and in cavities in crystalline schists.

|

|

|

Amphibole

|

Any of a large group of structurally similar hydrated double silicate minerals, such as hornblende, containing various combinations of sodium, calcium, magnesium, iron, and aluminum.

|

|

|

Assay

|

The act of testing the purity of precious metals.

|

|

|

Biotite

|

A black, dark brown, or greenish black micaceous mineral.

|

|

|

Calcite

|

A carbonate mineral and the most stable polymorph of calcium carbonate (CaCO3).

|

|

|

Dip

|

The angle that a rock unit, fault or other rock structure makes with a horizontal plane. Expressed as the angular difference between the horizontal plane and the structure. The angle is measured in a plane perpendicular to the strike of the rock structure.

|

|

|

Fault

|

A fracture or fracture zone in rock along which movement has occurred.

|

|

|

Feldspar

|

Any of a group of abundant rock-forming minerals occurring principally in igneous, plutonic, and some metamorphic rocks.

|

|

|

Foliation

|

The set of layers visible in many metamorphic rocks as a result of the flattening and stretching of mineral grains during metamorphism.

|

|

|

Gneiss

|

A metamorphic rock with a banded or foliated structure, typically coarse-grained.

|

|

|

Hornblende

|

A green to black amphibolic mineral formed in the late stages of cooling in igneous rock.

|

|

|

Igneous

|

Relating to or involving volcanic processes.

|

|

|

Listric Fault

|

A type of fault in which the fault plane is curved.

|

|

|

Lode

|

A mineral deposit in solid rock.

|

|

|

Mafic

|

A term used to describe an igneous rock that has a large percentage of dark-colored minerals such as amphibole, pyroxene and olivine. Also used in reference to the magmas from which these rocks crystallize. Mafic rocks are generally rich in iron and magnesium.

|

|

|

Metallurgy

|

Domain of materials science that studies the physical and chemical behavior of metallic elements, their intermetallic compounds, and their mixtures, which are called alloys. It is also the technology of metals: the way in which science is applied to their practical use.

|

|

|

Metamorphic Rock

|

Rock that has undergone a change from its original form due to changes in temperature, pressure or chemical alteration.

|

|

| Mica |

A shiny silicate mineral with a layered structure, found as minute scales in granite and other rocks, or as crystals.

|

|

|

Mineralization

|

The concentration of metals and their chemical compounds within a body of rock.

|

|

|

Monzonite

|

An intermediate igneous intrusive rock composed of approximately equal amounts of sodic to intermediate plagioclase and orthoclase feldspars with minor amounts of hornblende, biotite and other minerals.

|

|

|

Muscovite

|

A silver-gray form of mica occurring in many igneous and metamorphic rocks.

|

|

|

Ore

|

A mixture of minerals and gangue from which at least one metal can be extracted at a profit.

|

5

|

Outcrop

|

A segment of bedrock exposed to the atmosphere.

|

|

|

Pegmatitic

|

A coarsely crystalline granite or other igneous rock with crystals several centimeters in length.

|

|

|

Porphyry

|

A heterogeneous rock characterized by the presence of crustals in a relatively finer- grained matrix.

|

|

|

Precambrian

|

Noting or pertaining to the earliest era of earth history, ending 570 million years ago, during which the earth's crust formed and life first appeared in the seas.

|

|

|

Quartz

|

A mineral whose composition is silicon dioxide. A crystalline form of silica.

|

|

|

Reserve

|

(For the purposes of this report): that part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. Reserves consist of:

|

|

|

1)

|

Proven (Measured) Reserves. Reserves for which: (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling; and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established.

|

|

|

2)

|

Probable (Indicated) Reserves. Reserves for which quantity and grade and/or quality are computed from information similar to that used for proven (measured) reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven (measured) reserves, is high enough to assume continuity between points of observation.

|

|

|

Schist

|

A coarse-grained metamorphic rock that consists of layers of different minerals.

|

|

|

Sediment

|

Any particulate matter that can be transported by fluid flow and which eventually is deposited as a layer of solid particles on the bed or bottom of a body of water or other liquid.

|

|

|

Sedimentary

|

A type of rock which has been created by the deposition of solids from a liquid.

|

|

|

Silica

|

A hard, unreactive, colorless compound, SiO2, that occurs as the mineral quartz.

|

|

|

Silicate

|

Any of the many minerals consisting of silica combined with metal oxides, forming a major component of the rocks of the earth's crust.

|

|

|

Stockwork

|

A complex system of structurally controlled or randomly oriented veins. Stockworks are common in many ore deposit types and especially notable in greisens. They are also referred to as stringer zones.

|

|

|

Tertiary

|

Relating to the first period of the Cenozoic era, about 65 to 1.64 million years ago.

|

|

|

Trenching

|

The removal of overburden to expose the underlying bedrock.

|

|

|

Vein

|

An occurrence of ore with an irregular development in length, width and depth usually from an intrusion of igneous rock.

|

|

|

Volcanic

|

Characteristic of, pertaining to, situated in or upon, formed in, or derived from volcanoes.

|

6

The Company had previously staked four claims, the MDZ Lode Claims, situated in Mohave County, Arizona. The Company staked the land and provided the Arizona Bureau of Land Management with the requisite Location Notice of Lode Mining Claim. Upon providing the location notice and the requisite fees, the Company was entitled to enter onto the property with its employees, representatives and agents, and to prospect, explore, test, develop, work and mine the property as the Company saw fit. As of the date of this Report, the Company has not renewed the MDZ Lode Claims for the year 2013.

On October 22, 2011, the Company entered into that certain Property Option Agreement (the "Option Agreement") with MinQuest, Inc. ("MinQuest"). Pursuant to the terms and conditions of the Option Agreement, MinQuest granted the Company with the right and option (the “Option”) to acquire one hundred percent (100%) of the mining interests in that certain Property known as Sheep Mountain West (the “Sheep Mountain Property”), which is comprised of 27 mining claims and is located in Yavapai County, Arizona. As of the date of this Report, the Company has elected not to exercise the Option.

On July 11, 2012, the Company entered into that certain Minerals Lease Agreement (the “Agreement") with Mr. Jonathan B. Smith, Mr. James I. Smith and Ms. Celinda S. Hicks (the "Lessors"), giving the Company the right to conduct mineral exploration activities on and in certain land and mining claims, which are comprised of a total of approximately one hundred acres (100) collectively known as the “Crystal Project” situated in Beaverhead County, Montana, for a term of twenty five (25) years (the “Term”) with the right to renew. As consideration, the Company shall pay Lessors: (i) an annual payment of three thousand five hundred dollars ($3,500) over the Term of the Agreement; and (ii) a production royalty (the “Royalty”) equal to three percent (3%) of the net smelter returns on the 1st of each month, per the terms and conditions of the Agreement. The Agreement also provides that the Company shall have a one-time right to purchase one and one half percent (1.5%) of the Royalty in the Crystal Project for one million five hundred thousand dollars ($1,500,000). Additionally, pursuant to the Agreement, the Company shall be granted the subsequent right to participate in the development of minerals from the Crystal Project subject to the terms and conditions of the Agreement. The above description of the Agreement is intended as a summary only and is qualified in its entirety by the terms and conditions set forth therein, and may not contain all information that is of interest to the reader. For further information regarding the terms and conditions of the Agreement, this reference is made to such agreement, which was filed on August 1, 2012 with the SEC as part of our Current Report on Form 8-K.

The Company recorded an impairment allowance on the property as the Company has not been able to prove certainty around future production, reserves, cash flows or salvage value. As such, the Company recorded an impairment allowance of $25,381.

Location and Access

The Crystal Project is located in Beaverhead County, Montana, in Section 31, Township 8S, Range 7W, located towards the southern end of the Ruby Range, about 10 miles east of Dillon, at an altitude of approximately 7,500 feet. The property is without known reserves and our proposed program for exploration of the property is exploratory in nature. The main source of water is ground water and the main source of power is ten miles away in Dillon, Montana. The leased portion of the Crystal property consists of approximately 100 acres total; it includes approximately 40 acres in Township 8S, Range, 7W, Section 29 Principal Meridian, and approximately 60 acres in Section 30 Township 8S, Range 7W Principal Meridian and Base Line. During September of 2012, 83 unpatented lode claims were staked and filed in the area around the leased portion of the Crystal Project that is administered by the US Bureau of Land Management (BLM). The process of staking and filing the claims gives Graphite Corp. 100% of the mineral rights on the land that was staked. Graphite Corp intends to maintain the mineral rights by filing the annual maintenance fees of approximately $140 per claim per year prior to September 1st every year with the BLM. The claims are named CM-1 through CM-47 and CM 48 through CM 83 and added approximately 1600 acres of mineral rights to the project. Claims CM-1 through CM-47 are immediately adjacent to the leased portions of the Crystal Property in Township 8S Range 7W Sections 29 through 32 and claims CM 48 through CM 83 are in Township 8S, Range 8W, Sections 23-26, 35, and 36. For an unknown reason the BLM lists claims CM-11 through CM 83 as C-11 through C-83 when searching for the claims on the BLM’s LR2000 website but the claims have all been filed with the prefix “CM”.

7

The Crystal Project can be reached by a gravel and dirt road that is in relatively good condition, and passable during a good portion of the year.

Climate

The climate of Beaverhead County is both cold and dry. Precipitation varies widely; average annual amounts range from 10 inches in Dillon to over 50 inches in mountains forming the Continental Divide to the west. Two-thirds of precipitation in mountains is snow.

The average temperature in January is 21 degrees Fahrenheit and the average temperature in July is 66 Fahrenheit.

Property Geology

The rocks on the Crystal Project are a metamorphosed sedimentary series that has been correlated with the Cherry Creek group of Precambrian age. Garnetiferous granite gneiss, schists, marbles, and quartzites strike approximately N. 60°- 75° E. and dip 70°- 80° NW. but show local variation. They contain small pegmatitic bodies that range from nearly massive un-metamorphosed to markedly metamorphosed.

The richest graphite mineralization in the deposit occurs as fracture fillings in pegmatite and gneiss. The fillings range from thin films to veins more than 2 feet thick. They are short, and very few reach lengths of 50 feet. In places the veins form closely spaced intersecting networks that resemble stockworks. The veins contain graphite as the only primary mineral, but movement along the fractures has dragged fragments of the wall rock into the veins in places, apparently both during and after graphite deposition. The graphite occurs mostly as coarse interlocking plates as much as 1 inch long, but in places it shows well developed comb or needle structure. Contacts between graphite veins and wall rock are sharp, and no alteration of the wall rock is evident.

8

Graphite also occurs as flakes, films, and rosettes disseminated in the pegmatites and the gneisses which is noticeably more abundant near the graphite veins. In the wall rocks the graphite occupies minute fractures between or within mineral grains and occurs as flakes formed by replacement of quartz or feldspar. Where the country rock is foliated, the graphite flakes are oriented parallel to the foliation. There is evidence that structural features have helped to localize graphite deposition, with the deposit being associated with an isoclinal fold that strikes about N. 50° E. and dips about 45° NW. The nose of this fold plunges N. 20° W. at about 45 degrees. There is extensive fracturing around the nose of the fold both on the surface and in underground exposures. These fractures contain graphite that constitutes the richest ore body exposed in the deposit.

The Crystal Property has multiple adits that were excavated during historical mining activities. Exploration on the property was active as early as 1899 and mining began in approximately 1903 but the mine has been inactive since 1944. No mining equipment or infrastructure remains on the property other than a dirt road/trail that is not maintained. The adits lead to what is reported by the USGS as approximately 3500 feet of underground workings. Exploration information from the period of mining activity is not available. The mine records are not available either but the following figures are believed to be correct: according to the 1960 USGS report “Strategic Graphite A Survey” by Cameron and Weis the Birds Nest mine reportedly initially shipped 50 tons of graphite ore and up until 1940 the total production was 2150 tons, all further production came from the Groundhog claim. From 1929 to 1940 the mine was intermittently worked and produced about 50 tons of graphite ore. In 1941 a small flotation mill was built and until 1944 it shipped approximately 150 tons of graphite concentrates from the mine ore and old dumps. Operations ceased in 1945 and although graphite was produced until 1948 none was sold. Graphite concentrates still remain on the property in small dumps but the amount and grade has not been calculated to date.

Discontinuation of Project in Alabama

On March 28, 2014, the Company decided not to continue with its plan of operation as it related to solely the Carr Leases and Cahaba Forest management Leases Option, and will not pursue and exploration in connection with the Carr Leases and Cahaba Forest management Leases Option. In connection therewith, on March 25, 2014, pursuant to a Stock Redemption Agreement dated February 24, 2014, by and between the Company and Stanley Smith, the Company redeemed 1,000,000 shares (the “Shares”) of the Company’s common stock, for a purchase price of $0.00001 per share, for an aggregate purchase price of $10.00. The sale closed on March 14, 2014. Subsequently, on March 19, 2014, the Company canceled the Shares, returning them to the authorized capital stock of the Company. Mr. Smith was a party to the Carr Leases and Cahaba Forest management Leases Option with the Company. The previous Carr Cahaba Property of the Company is situated in Clay County, Alabama, near the towns of Ashland and Lineville. The property was without known reserves and our proposed program for exploration of the property was exploratory in nature.

Management Experience

Our President, Brian Goss, has ten years of experience in mineral exploration and the mining industry, but limited experience working in an actual mine. As such, he may not be able to recognize or take advantage of potential acquisition and exploration opportunities in the sector without the aid of additional qualified geological consultants.

Competitive Factors

We are a new mineral resources exploration company. The mining industry is highly fragmented and we will be competing with many other exploration companies looking for minerals. While we will generally compete with other exploration companies, there is no competition for the exploration or removal of minerals from our acquired properties.

However, we will compete with other mineral resource exploration companies for the acquisition of new mineral properties and for available resources. Many of the mineral resource exploration companies with whom we will compete have greater financial and technical resources than those available to us. Accordingly, these competitors may be able to spend greater amounts on acquisitions of mineral properties of merit, on exploration of their mineral properties and on development of their mineral properties. In addition, they may be able to afford more geological expertise in the targeting and exploration of mineral properties. This competition could result in competitors having mineral properties of greater quality and interest to prospective investors who may finance additional exploration. This competition could adversely impact our ability to finance further exploration and development of our mineral properties. We will be competing with other mineral resource exploration companies for available resources, including, but not limited to: professional geologists, camp staff, mineral exploration supplies and drill rigs. Competing for available resources will depend on our technical abilities, financial capacities, industry contacts, and any consulting arrangements we may have in place.

9

We will also compete with other mineral resource exploration companies for financing from investors that are prepared to make investments in mineral resource exploration companies. The presence of competing mineral resource exploration companies may impact our ability to raise additional capital in order to fund our exploration programs if investors view our competitors as more attractive investments, based on the merit of the mineral properties under investigation and the price of the investment offered to investors.

Plan of Operation

The Crystal Project

During September of 2012, 83 claims were filed in the area around the leased portion of the Crystal Project. The claims added approximately 1600 acres of mineral rights to the project. During the claim staking, samples were collected to test the surface rocks for graphite.

Samples taken from the Crystal Project were consistent with prior observations. The rock type the samples were taken in were a pegmatite and the metamorphic rocks adjacent to the pegmatite. The samples were taken from the historically mined localities throughout the Crystal Project and the grades were all over 10% graphite and multiple samples contained >20%, exceeding the 20% limitation of the assay method. The sample results from the Crystal Project are as follows:

|

C-Graphite

|

|

|

Sample

|

%

|

|

AB-20120912-02

|

10.5

|

|

AB-20120912-05

|

>20

|

|

AB-20120912-13

|

>20

|

|

AB-20120912-17

|

13

|

|

AB-20120912-18

|

>20

|

The geological work was directed by our President, Brian Goss, and Director, Jason Babcock. The assay work was conducted by INSPECTORATE (A Bureau Veritas Group Company) of Sparks, Nevada. The samples were taken using industry standard geologists’ best practices for rock chip sampling. The types of rock chip samples included spot/grab samples, composite rock chip samples, and channel samples. All the samples were taken from outcropping rocks or roadcuts at surface. Inspectorate processed the samples through its sister company, ACME Labs in Vancouver, BC. The process used to assay the samples for graphitic carbon was Inspectorate code C-GP-OR and/or ACME code 2A09. The process involved preparing the sample by crushing it, heating the sample to 600 degrees C, using an HCl leach, and testing the residue for graphitic carbon by using the LECO method. ACME Lab is an ISO 17025 certified lab and its internal check assays and equipment calibration meet the ISO 17025 standards. The field study also included a physical review of the mineral lease areas to include specific details and features of interest.

The following table represents the work that Graphite Corp plans and the associated costs to accomplish the first phase of graphite exploration on the property underlying the Crystal Project in the upcoming 12-month period. Initially the work will entail geologic mapping and additional geochemical sampling and a geophysical physical survey. The data generated by the mapping, sampling, and geophysics will be used to plan trenching and drill targets. Once the trenching and drilling program planning is finalized Graphite Corp. will apply for a permit with the BLM for the construction of the drill pads and roads and the digging of the trenches. The trenches will provide additional exposure to conduct geologic mapping and geochemical sampling and assist in further refining the drill program. Once drilling is completed and assays are reported, Graphite Corp. will compile the results and assess the property for further exploration or mining potential, if any. The final step in this exploration plan is to re-claim the surface disturbance of the drill pads, roads, and trenches that will no longer be needed and either recover all or some of the bond with the BLM or put the bond money towards additional disturbance on the property. We have not budgeted or planned any reclamation of disturbance that is due to historical activities, mining or otherwise. The past surface disturbance will not require reclamation and there is no known environmental concern due to the past mining activities on surface or in ground water. We will need to secure additional funding to accomplish all the work in the plan and the amount of work may be cut or re-prioritized based on available funding.

10

|

Item

|

Cost

|

|||

|

Land Holding

|

$ | 28,966 | ||

|

Planning

|

$ | 19,500 | ||

|

Geophysical EM baseline study

|

$ | 15,000 | ||

|

Geophysical EM survey

|

$ | 35,000 | ||

|

Disturbance Permit Preperation and Application

|

$ | 8,000 | ||

|

Reclamation Bond

|

$ | 25,000 | ||

|

Dirtwork-Trench Excavation

|

$ | 25,000 | ||

|

Dirtwork oversight and Geologic Mapping

|

$ | 15,000 | ||

|

Geochemical Sampling-Surface

|

$ | 10,000 | ||

|

Surface Sampling Assay Cost (300 samples * $45/sample)

|

$ | 13,500 | ||

|

Dirtwork-Road and Pad Building

|

$ | 35,000 | ||

|

Reverse Circulation Rig-Drill 5 holes

|

$ | 65,000 | ||

|

Drilling Project Geologist/Supervisor

|

$ | 25,000 | ||

|

Dirtwork-Reclamation

|

$ | 30,000 | ||

|

Bond Refund

|

$ | (25,000 | ) | |

|

10% Contingency

|

$ | 32,497 | ||

|

Total Budget for Crystal Project:

|

$ | 357,463 | ||

We plan to commence the exploration program detailed above in the spring of 2014. We expect the work program to take approximately 12 months to complete, assuming the company raises the funds to complete the work. The Company does not have the funds to commence work. Costs are management’s estimates and the actual project costs may exceed our estimates. To date, we have not commenced exploration. In order to begin work detailed above on the property underlying the Crystal Project, we will need to raise approximately $357,463. Until such funds are obtained by the Company via debt, equity or other form of financing, we will be unable to take concrete steps towards the implementation of work plan. In order to commence work, we will need to secure additional financing. Currently, we have no plan or commitment which would provide us with the required capital to begin work. The Company plans to hire third-parties to perform the work detailed above.

The Industry

The recent surge in interest and value of graphite is built on long standing and solid fundamentals as a well-established industrial mineral. Natural graphite has been mostly consumed in steel making; for refractories and foundry facings; as a lubricant and as a containment lining in nuclear applications. Other uses have included automobile brake linings and transmission components, but with the extraordinary increase in the use of lithium-Ion batteries, graphite has experienced a huge growth surge and the auto industry is sure to be at the forefront of this growth.

11

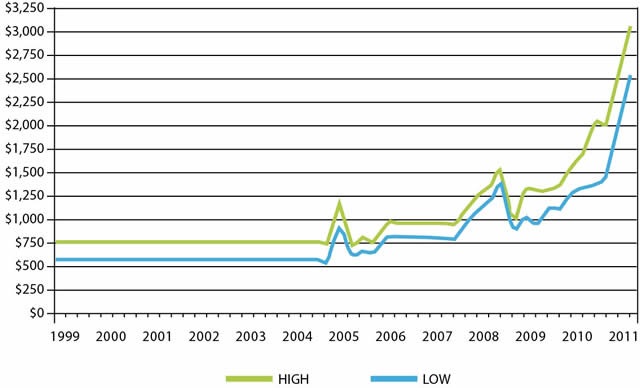

Prices of large-flake, high carbon graphite has increased from $600 per metric ton during the 1990s to highs of approximately $2,500 per metric ton recently. Industry participants believe that positive trends in graphite prices could continue in the coming years as China is expected to continue to tighten regulations regarding exports of graphite.

A report by Industrial Minerals, a leading source of information on critical minerals, stated that the Chinese government is focused on consolidating the domestic graphite industry and is going ahead with plans to reduce the number of graphite mines in Hunan province from 230 to around 20, with increased government supervision aimed at reducing environmental impact due to harmful mining practices. This is expected to lead to a loss of around 100,000 metric tons of graphite per year, or approximately 10 percent of the global supply.

Recent prices for flake graphite has seen $1,500 - 3,000 per tonne depending on flake size and grade. Graphite prices have seen increases for large flake, high purity graphite (+80 mesh, 94-97%C) and have more than doubled in recent years. China, which produces about 80 percent of the world's graphite, is reducing its 200 amorphous graphite mines to 20 and creating a state-run monopoly causing disruptions in supply. Industrial Minerals recently reported exports from China in January and February 2012 have been reduced by 55.3% and 60.1% from 2011 level exports from Hunan Province. It is not expected that current graphite mines in other countries could replace Chinese amorphous supply.

12

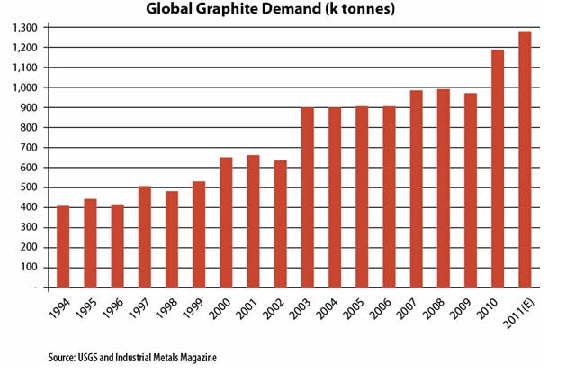

Currently, the largest graphite mines produce only 20,000 tonnes per year. Predictions are that the current world-wide graphite consumption of 1.2 million tonnes per year will increase by 200,000 tonnes per year by 2015. This would require approximately ten mines of 20,000 tonnes per year to come on stream to meet demand. If changes to graphite mining in China are fully implemented, there could be added pressure on demand and a corresponding price increase as indicated by the increasing prices in the last two years.

Government Regulation

Exploration activities are subject to various national, state, foreign and local laws and regulations, which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances and other matters. We believe that we are in compliance in all material respects with applicable mining, health, safety and environmental statutes and the regulations promulgated by the States of Arizona, Montana, Alabama and the United States Federal Government. Currently, there are no costs associated with our compliance with such regulations and laws.

Our exploration activities are subject to various federal, state and local laws and regulations governing protection of the environment. These laws are continually changing and, as a general matter, are becoming more restrictive. Our policy is to conduct business in a way that safeguards public health and the environment. We believe that our exploration activities are conducted in material compliance with applicable laws and regulations. Changes to current local, state or federal laws and regulations in the jurisdictions where we operate could require additional capital expenditures and increased operating and/or reclamation costs. Although we are unable to predict what additional legislation, if any, might be proposed or enacted, additional regulatory requirements could render certain exploration activities uneconomic.

On land that is administered by the US Bureau of Land Management (BLM) such as a large portion of the land at the Crystal Project in Montana, permitting must be obtained prior to disturbing the land in ways that is typical for mineral exploration. Low level disturbance, less than 10 acres, that is typical for early stage exploration and may include road building and drill pad construction, requires a Notice of Intent (NOI) to be approved by the BLM. Exploration and/or mining activities that have a total disturbance of more than 10 acres total for one project may require additional permits, such as an Environmental Impact Assessment (EIA) or an Environmental Impact Statement (EIS). In general, higher levels of disturbance for exploration and mining require more data collection and more stringent permitting processes to assist the government and community in deciding how a mine may affect the surrounding area, both positively and negatively. The permitting process for private land in Alabama is currently unknown but is expected to be somewhat similar to the process for public land in the western United States. It is expected that consultants who specialize in land use permitting will be used to assist us to apply for and receive the necessary permits for exploration on all our projects.

13

EMPLOYEES

We currently have no employees other than our directors. We intend to retain the services of geologists, prospectors and consultants on a contract basis to conduct the exploration programs on our mineral claims and to assist with regulatory compliance and preparation of financial statements.

As a “smaller reporting company,” as defined in Rule 12b-2 of the Exchange Act, we are not required to provide the information called for by this Item.

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

None.

|

ITEM 2.

|

PROPERTIES

|

Our current business address is 1031 Railroad Street, Suite 102A, Elko, Nevada 89801. Our telephone number is (775) 753-6605.

We believe that this space is adequate for our current needs.

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

We are not currently involved in any legal proceedings and we are not aware of any pending or potential legal actions.

|

ITEM 4.

|

MINE SAFETY DISCLOSURE

|

None.

14

PART II

|

ITEM 5.

|

MARKET FOR REGISTRANT’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS MARKET INFORMATION

|

Our shares of common stock are quoted on the OTC Bulletin Board and the OTCQB tier of OTC Markets Group, Inc., and our ticker symbol is “GRPH.” The following table shows the reported high and low closing bid prices per share for our common stock based on information provided by the OTCQB. The over-the-counter market quotations set forth for our common stock reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions.

|

BID PRICE PER SHARE

|

||||||||

|

HIGH

|

LOW

|

|||||||

|

Three Months Ended December 31, 2013

|

$

|

0.10

|

$

|

0.02

|

||||

|

Three Months Ended September 30, 2013

|

$

|

0.17

|

$

|

0.07

|

||||

|

Three Months Ended June 30, 2013

|

$

|

0.28

|

$

|

0.35

|

||||

|

Three Months Ended March 31, 2013

|

$

|

0.77

|

$

|

0.23

|

||||

|

Three Months Ended December 31, 2012

|

$

|

1.01

|

$

|

0.55

|

||||

|

Three Months Ended September 30, 2012

|

$

|

0.35

|

$

|

0.35

|

||||

|

Three Months Ended June 30, 2012

|

$

|

0.80

|

$

|

0.0001

|

||||

|

Three Months Ended March 31, 2012

|

$

|

1.05

|

$

|

0.75

|

||||

HOLDERS

As of December 31, 2013, the Company had 28,700,000 shares of common stock issued and outstanding held by approximately 7 shareholders of record. 21,100,000 of such shares were held of record by CEDE & Co.

DIVIDENDS

Historically, we have not paid any dividends to the holders of our common stock and we do not expect to pay any such dividends in the foreseeable future as we expect to retain our future earnings for use in the operation and expansion of our business.

TRANSFER AGENT

Our transfer agent is Securities Transfer Corp., whose address is 2591 Dallas Parkway, Suite 102, Frisco, Texas 75034, and whose telephone number is (469) 633-0101.

RECENT SALES OF UNREGISTERED SECURITIES

None.

SECURITIES AUTHORIZED FOR ISSUANCE UNDER EQUITY COMPENSATION PLANS

We have not established any compensation plans under which equity securities are authorized for issuance.

15

PURCHASES OF EQUITY SECURITIES BY THE REGISTRANT AND AFFILIATED PURCHASERS

We did not purchase any of our shares of common stock or other securities during the year ended December 31, 2013. However, as reported on a Current Report on Form 8-K on March 25, 2014, pursuant to a Stock Redemption Agreement dated February 24, 2014, by and between the Company and Stanley Smith, the Company redeemed 1,000,000 shares (the “Shares”) of the Company’s common stock, for a purchase price of $0.00001 per share, for an aggregate purchase price of $10.00. The sale closed on March 14, 2014. Subsequently, on March 19, 2014, the Company canceled the Shares, returning them to the authorized capital stock of the Company.

As a “smaller reporting company,” as defined in Rule 12b-2 of the Exchange Act, we are not required to provide the information called for by this Item.

|

ITEM 7.

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

RESULTS OF OPERATIONS

For the year ended December 31, 2013, we incurred total expenses of $369,650, comprised of $115,112 in mineral claims and exploration, $46,205 in professional fees, $36,000 in consulting fees, and $172,333 in general and administrative expenses. By comparison for the year ended December 31, 2012, we incurred total expenses of $713, 869, comprised of $99,682 in mineral claims and exploration, $375,831 in mineral claim impairment, $77,591 in professional fees, $102,125 in consulting fees, and $58,640 in general and administrative expenses. Additionally, in 2012, we had a debt settlement of $4,668.

At December 31, 2013 and 2012, we incurred net losses of $369,650 and $718,537 respectively, and our net loss since inception on August 3, 2007 through December 31, 2013 is $2,453,955.

Graphite Corp. is an exploration stage company and currently has minimal operations. Our independent auditor has issued an audit opinion for Graphite Corp. which includes a statement raising substantial doubt as to our ability to continue as a going concern.

LIQUIDITY AND CAPITAL RESOURCES

Our cash balance at December 31, 2013 was $253 with $103,424 in outstanding liabilities. Total expenditures over the next 12 months are expected to be approximately $230,508. If we experience a shortage of funds prior to generating revenues from operations we may utilize funds from our directors, who have informally agreed to advance funds to allow us to pay for operating costs, however they have no formal commitment, arrangement or legal obligation to advance or loan funds to us. Management believes our current cash balance will not be sufficient to fund our operations for the next six months.

16

Working Capital

|

December 31,

2013

$

|

December 31,

2012

$

|

|||||||

|

Current Assets

|

253 | 190,352 | ||||||

|

Current Liabilities

|

103,424 | 20,700 | ||||||

|

Working Capital (Deficit)

|

(103,171 | ) | 169,652 | |||||

Cash Flows

|

Year ended

December 31,

2013

$

|

Year ended

December 31,

2012

$

|

|||||||

|

Cash Flows from (used in) Operating Activities

|

(214,736 | ) | (373,285 | ) | ||||

|

Cash Flows from (used in) Financing Activities

|

30,000 | 708,204 | ||||||

|

Cash Flows from (used in) Investing Activities

|

- | (150,000 | ) | |||||

|

Net Increase (decrease) in Cash During Period

|

(184,736 | ) | 184,919 | |||||

Operating Revenues

Operating revenues for the period ended December 31, 2013 was $Nil.

Operating revenues for the period ended December 31, 2012 was $Nil.

Operating Expenses and Net Loss

Operating expenses for the years ended December 31, 2013 and 2012 was $369,650 and $713,869 and is comprised of expenses related to mineral claims and general and administrative expenses.

Net loss for the years ended December 31, 2013 and 2012 was $369,650 and $718,537 is comprised of expenses related to mineral claims and general and administrative expenses.

Liquidity and Capital Resources

As at December 31, 2013, the Company’s cash and total asset balance was $253 compared to $190,302 as at December 31, 2012. The decrease in total assets is attributed cash expendetures.

17

CRITICAL ACCOUNTING POLICIES

Basis of Presentation

The Company’s financial statements and related notes are presented in accordance with accounting principles generally accepted in the United States, and are expressed in US dollars. The Company’s fiscal year-end is December 31.

Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents

The Company considers all highly liquid instruments with maturity of three months or less at the time of issuance to be cash equivalents. As of December 31, 2013 and December 31, 2012, the Company had no cash equivalents.

Mineral Properties

Costs of exploration, carrying and retaining unproven mineral lease properties are expensed as incurred. Mineral property acquisition costs are capitalized including licenses and lease payments. Although the Company has taken steps to verify title to mineral properties in which it has an interest, these procedures do not guarantee the Company's title. Such properties may be subject to prior agreements or transfers and title may be affected by undetected defects. Impairment losses are recorded on mineral properties used in operations when indicators of impairment are present and the undiscounted cash flows estimated to be generated by those assets are less than the assets’ carrying amount.

Stock-based Compensation

The Company accounts for stock-based compensation issued to employees based on ASC Topic “Share Based Payment” which establishes standards for the accounting for transactions in which an entity exchanges its equity instruments for goods or services. It also addresses transactions in which an entity incurs liabilities in exchange for goods or services that are based on the fair value of the entity’s equity instruments or that may be settled by the issuance of those equity instruments.

The Topic does not address the accounting for employee share ownership plans, which are subject to AICPA Statement of Position 93-6, “Employers’ Accounting for Employee Stock Ownership Plans”.

18

It requires an entity to measure the cost of employee services received in exchange for an award of equity instruments based on the grant-date fair value of the award (with limited exceptions). That cost will be recognized over the period during which an employee is required to provide service in exchange for the award – the requisite service period (usually the vesting period). It further requires that the compensation cost relating to share-based payment transactions be recognized in financial statements. That cost will be measured based on the fair value of the equity or liability instruments issued. The scope of the Topic includes a wide range of share-based compensation arrangements including share options, restricted share plans, performance-based awards, share appreciation rights, and employee share purchase plans.

As at December 31, 2013, the Company had not adopted a stock option plan. For the period ended December 31, 2013, stock option expense of $72,421 was recorded for the 250,000 options granted on December 10, 2012 (see note 6).

Basic and Diluted Net Loss Per Share

The Company computes net loss per share in accordance with ASC 260, Earnings Per Share, which requires presentation of both basic and diluted earnings per share (EPS) on the face of the income statement. Basic EPS is computed by dividing net loss available to common shareholders (numerator) by the weighted average number of shares outstanding (denominator) during the period. Diluted EPS gives effect to all dilutive potential common shares outstanding during the period using the treasury stock method and convertible preferred stock using the if-converted method. In computing Diluted EPS, the average stock price for the period is used in determining the number of shares assumed to be purchased from the exercise of stock options or warrants. Diluted EPS excludes all dilutive potential shares if their effect is anti dilutive.

Income Taxes

Potential benefits of income tax losses are not recognized in the accounts until realization is more likely than not. The Company has adopted ASC 740, Income Taxes, as of its inception. Pursuant to ASC 740, the Company is required to compute tax asset benefits for net operating losses carried forward. The potential benefits of net operating losses have not been recognized in these financial statements because the Company cannot be assured it is more likely than not it will utilize the net operating losses carried forward in future years.

Comprehensive Loss

ASC 220, Comprehensive Income, establishes standards for the reporting and display of comprehensive loss and its components in the financial statements. As at December 31, 2013 and December 31, 2012, the Company has no items that represent comprehensive loss and, therefore, has not included a schedule of comprehensive loss in the financial statements.

Financial Instruments

The Company adopted the FASB standard related to fair value measurement at inception. The standard defines fair value, establishes a framework for measuring fair value and expands disclosure of fair value measurements. The standard applies under other accounting pronouncements that require or permit fair value measurements and, accordingly, does not require any new fair value measurements. The standard clarifies that fair value is an exit price, representing the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. As such, fair value is a market-based measurement that should be determined based on assumptions that market participants would use in pricing an asset or liability. The recorded values of long-term debt approximate their fair values, as interest approximates market rates. As a basis for considering such assumptions, the standard established a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value as follows.

· Level 1. Observable inputs such as quoted prices in active markets;

· Level 2. Inputs, other than quoted prices in active markets, that are observable either directly or indirectly; and

· Level 3. Unobservable inputs in which there is little or no market data, which require the reporting entity to develop its own assumptions.

19

The Company’s financial instruments are cash, accounts receivable, and accounts payable. The recorded values of cash, accounts receivable, and accounts payable approximate their fair values based on their short-term nature.

The following table presents assets and liabilities within the fair value hierarchy utilized to measure fair value on a recurring basis as of December 31, 2013 and December 31, 2012:

|

Description

|

Level 1

|

Level 2

|

Level 3

|

Total Realized Loss

|

||||||||||||||

|

Dec. 31, 2013

|

None

|

$ | - | $ | - | $ | - | $ | - | |||||||||

|

Dec. 31, 2012

|

None

|

$ | - | $ | - | $ | - | $ | - | |||||||||

Recently issued accounting pronouncements

In July 2013, FASB issued ASU No. 2013-11, "Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists." The provisions of ASU No. 2013-11 require an entity to present an unrecognized tax benefit, or portion thereof, in the statement of financial position as a reduction to a deferred tax asset for a net operating loss carryforward or a tax credit carryforward, with certain exceptions related to availability. ASU No. 2013-11 is effective for interim and annual reporting periods beginning after December 15, 2013. The adoption of ASU No. 2013-11 is not expected to have a material impact on the Company's Consolidated Financial Statements.

In February 2013, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2013-02, Comprehensive Income (Topic 220): Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income, to improve the transparency of reporting these reclassifications. Other comprehensive income includes gains and losses that are initially excluded from net income for an accounting period. Those gains and losses are later reclassified out of accumulated other comprehensive income into net income. The amendments in the ASU do not change the current requirements for reporting net income or other comprehensive income in financial statements. All of the information that this ASU requires already is required to be disclosed elsewhere in the financial statements under U.S. GAAP. The new amendments will require an organization to:

|

·

|

Present (either on the face of the statement where net income is presented or in the notes) the effects on the line items of net income of significant amounts reclassified out of accumulated other comprehensive income - but only if the item reclassified is required under U.S. GAAP to be reclassified to net income in its entirety in the same reporting period; and

|

|

·

|

Cross-reference to other disclosures currently required under U.S. GAAP for other reclassification items (that are not required under U.S. GAAP) to be reclassified directly to net income in their entirety in the same reporting period. This would be the case when a portion of the amount reclassified out of accumulated other comprehensive income is initially transferred to a balance sheet account (e.g., inventory for pension-related amounts) instead of directly to income or expense.

|

The amendments apply to all public and private companies that report items of other comprehensive income. Public companies are required to comply with these amendments for all reporting periods (interim and annual). The amendments are effective for reporting periods beginning after December 15, 2012, for public companies. Early adoption is permitted. The adoption of ASU No. 2013-02 is not expected to have a material impact on our financial position or results of operations.

In January 2013, the FASB issued ASU No. 2013-01, Balance Sheet (Topic 210): Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities, which clarifies which instruments and transactions are subject to the offsetting disclosure requirements originally established by ASU 2011-11. The new ASU addresses preparer concerns that the scope of the disclosure requirements under ASU 2011-11 was overly broad and imposed unintended costs that were not commensurate with estimated benefits to financial statement users. In choosing to narrow the scope of the offsetting disclosures, the Board determined that it could make them more operable and cost effective for preparers while still giving financial statement users sufficient information to analyze the most significant presentation differences between financial statements prepared in accordance with U.S. GAAP and those prepared under IFRSs. Like ASU 2011-11, the amendments in this update will be effective for fiscal periods beginning on, or after January 1, 2013. The adoption of ASU 2013-01 is not expected to have a material impact on our financial position or results of operations.

20

In October 2012, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2012-04, “Technical Corrections and Improvements” in Accounting Standards Update No. 2012-04. The amendments in this update cover a wide range of Topics in the Accounting Standards Codification. These amendments include technical corrections and improvements to the Accounting Standards Codification and conforming amendments related to fair value measurements. The amendments in this update will be effective for fiscal periods beginning after December 15, 2012. The adoption of ASU 2012-04 is not expected to have a material impact on our financial position or results of operations.

In August 2012, the FASB issued ASU 2012-03, “Technical Amendments and Corrections to SEC Sections: Amendments to SEC Paragraphs Pursuant to SEC Staff Accounting Bulletin (SAB) No. 114, Technical Amendments Pursuant to SEC Release No. 33-9250, and Corrections Related to FASB Accounting Standards Update 2010-22 (SEC Update)” in Accounting Standards Update No. 2012-03. This update amends various SEC paragraphs pursuant to the issuance of SAB No. 114. The adoption of ASU 2012-03 is not expected to have a material impact on our financial position or results of operations.

In July 2012, the FASB issued ASU 2012-02, “Intangibles – Goodwill and Other (Topic 350): Testing Indefinite-Lived Intangible Assets for Impairment” in Accounting Standards Update No. 2012-02. This update amends ASU 2011-08, Intangibles – Goodwill and Other (Topic 350): Testing Indefinite-Lived Intangible Assets for Impairment and permits an entity first to assess qualitative factors to determine whether it is more likely than not that an indefinite-lived intangible asset is impaired as a basis for determining whether it is necessary to perform the quantitative impairment test in accordance with Subtopic 350-30, Intangibles - Goodwill and Other - General Intangibles Other than Goodwill. The amendments are effective for annual and interim impairment tests performed for fiscal years beginning after September 15, 2012. Early adoption is permitted, including for annual and interim impairment tests performed as of a date before July 27, 2012, if a public entity’s financial statements for the most recent annual or interim period have not yet been issued or, for nonpublic entities, have not yet been made available for issuance. The adoption of ASU 2012-02 is not expected to have a material impact on our financial position or results of operations.

21

PLAN OF OPERATION

Our plan of operation for the twelve months following the date of this Form 10-K is to complete the first and second of the three phases of the exploration program on our prospects. In addition to the $357,463 we anticipate spending for the first two phases of the exploration program as outlined below, we anticipate spending an additional $50,000 on general and administration expenses including fees payable in connection with complying with our reporting obligations, and general administrative costs. Total expenditures over the next 12 months are therefore expected to be approximately $407,463. We will experience a shortage of funds prior to funding and we may utilize funds from our president, however they have no formal commitment, arrangement or legal obligation to advance or loan funds to the company.

The following table represents the work that Graphite Corp plans and the associated costs to accomplish the first phase of graphite exploration on the property underlying the Crystal Project in the upcoming 12-month period. Initially the work will entail geologic mapping and additional geochemical sampling and a geophysical physical survey. The data generated by the mapping, sampling, and geophysics will be used to plan trenching and drill targets. Once the trenching and drilling program planning is finalized Graphite Corp. will apply for a permit with the BLM for the construction of the drill pads and roads and the digging of the trenches. The trenches will provide additional exposure to conduct geologic mapping and geochemical sampling and assist in further refining the drill program. Once drilling is completed and assays are reported, Graphite Corp. will compile the results and assess the property for further exploration or mining potential, if any. The final step in this exploration plan is to re-claim the surface disturbance of the drill pads, roads, and trenches that will no longer be needed and either recover all or some of the bond with the BLM or put the bond money towards additional disturbance on the property. We have not budgeted or planned any reclamation of disturbance that is due to historical activities, mining or otherwise. The past surface disturbance will not require reclamation and there is no known environmental concern due to the past mining activities on surface or in ground water. We will need to secure additional funding to accomplish all the work in the plan and the amount of work may be cut or re-prioritized based on available funding.

|

Item

|

Cost

|

|||

|

Land Holding

|

$ | 28,966 | ||

|

Planning

|

$ | 19,500 | ||

|

Geophysical EM baseline study

|

$ | 15,000 | ||

|

Geophysical EM survey

|

$ | 35,000 | ||

|

Disturbance Permit Preperation and Application

|

$ | 8,000 | ||

|

Reclamation Bond

|

$ | 25,000 | ||

|

Dirtwork-Trench Excavation

|

$ | 25,000 | ||

|

Dirtwork oversight and Geologic Mapping

|

$ | 15,000 | ||

|

Geochemical Sampling-Surface

|

$ | 10,000 | ||

|

Surface Sampling Assay Cost (300 samples * $45/sample)

|

$ | 13,500 | ||

|

Dirtwork-Road and Pad Building

|

$ | 35,000 | ||

|

Reverse Circulation Rig-Drill 5 holes

|

$ | 65,000 | ||

|

Drilling Project Geologist/Supervisor

|

$ | 25,000 | ||

|

Dirtwork-Reclamation

|

$ | 30,000 | ||

|

Bond Refund

|

$ | (25,000 | ) | |

|

10% Contingency

|

$ | 32,497 | ||

|

Total Budget for Crystal Project:

|

$ | 357,463 | ||

Crystal Project Operating Budget

We plan to commence the exploration program detailed above in the spring of 2014. We expect the work program to take approximately 12 months to complete, assuming the company raises the funds to complete the work. The Company does not have the funds to commence work. Costs are management’s estimates and the actual project costs may exceed our estimates. To date, we have not commenced exploration. In order to begin work detailed above on the property underlying the Crystal Project, we will need to raise approximately $357,463. Until such funds are obtained by the Company via debt, equity or other form of financing, we will be unable to take concrete steps towards the implementation of work plan. In order to commence work, we will need to secure additional financing. Currently, we have no plan or commitment which would provide us with the required capital to begin work. The Company plans to hire third-parties to perform the work detailed above. We cannot provide any assurance that we will be able to raise sufficient funds to proceed with any work in the exploration program.

OFF-BALANCE SHEET ARRANGEMENTS

We have no off-balance sheet arrangements.

|

ITEM 7A.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

As a “smaller reporting company,” as defined in Rule 12b-2 of the Exchange Act, we are not required to provide the information called for by this Item.

22

|

ITEM 8.

|

FINANCIAL STATEMENTS

|

Index to the Financial Statements

|

Contents

|

Page(s)

|

|||

|

Report of Independent Registered Public Accounting Firm

|

F-1

|

|||

|

Balance Sheets at December 31, 2013 and December 31, 2012

|

F-2

|

|||

|

Statement of Operations for the Years Ended December 31, 2013 and 2012, and for the period from August 3, 2007 (Inception) through December 31, 2013

|

F-3

|

|||

|

Statement of Stockholders’ Equity (Deficit) for the period from August 3, 2007 (Inception) through December 31, 2013

|

F-4

|

|||

|

Statement of Cash Flows for the Years Ended December 31, 2013 and 2012, and for the period from August 3, 2007 (Inception) through December 31, 2013.

|

F-5

|

|||

|

Notes to Financial Statements

|

F-6

|

|||

23

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors

Graphite Corp.

(An Exploration Stage Company)

We have audited the accompanying balance sheets of Graphite Corp. (An Exploration Stage Company) as of December 31, 2013 and 2012 and the related statements of operations, stockholders’ deficit and cash flows for the years then ended and for the period from August 3, 2007 (inception) through December 31, 2013. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Graphite Corp. as of December 31, 2013 and 2012 and the results of its operations and cash flows for the periods described above in conformity with accounting principles generally accepted in the United States of America.

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the financial statements, the Company suffered a net loss from operations and has a net capital deficiency, which raises substantial doubt about its ability to continue as a going concern. Management’s plans regarding those matters are also described in Note 2. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ M&K CPAS, PLLC

www.mkacpas.com

Houston, Texas

April 4, 2014

F-1

|

(An Exploration Stage Company)

|

||||||||

|

Balance Sheets

|

|