Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Bristow Group Inc | d696874d8k.htm |

Howard Weil 42

nd

Annual Energy

Conference

Bristow Group Inc.

March 23 -

27, 2014

Exhibit 99.1 |

2

Forward-looking statements

This

presentation

may

contain

“forward-looking

statements”

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

Forward-looking

statements

include

statements

about

our

future

business,

operations,

capital

expenditures,

fleet

composition,

capabilities

and

results;

modeling

information,

earnings

and

adjusted

earnings

growth

guidance,

expected

operating

margins,

cash

flow

stability

and

other

financial

projections;

future

dividends,

share

repurchases

and

other

uses

of

excess

cash;

plans,

strategies

and

objectives

of

our

management,

including

our

plans

and

strategies

to

grow

earnings

and

our

business,

our

general

strategy

going

forward,

our

business

model

and

our

operational

excellence

initiative;

expected

actions

by

us

and

by

third

parties,

including

our

customers,

competitors

and

regulators;

impact

of

grounding

and

the

effects

thereof;

the

valuation

of

our

company

and

its

valuation

relative

to

relevant

financial

indices;

assumptions

underlying

or

relating

to

any

of

the

foregoing,

including

assumptions

regarding

factors

impacting

our

business,

financial

results

and

industry;

expected

input

of

our

investment

in

Eastern

Airways;

and

other

matters.

Our

forward-looking

statements

reflect

our

views

and

assumptions

on

the

date

of

this

presentation

regarding

future

events

and

operating

performance.

They

involve

known

and

unknown

risks,

uncertainties

and

other

factors,

many

of

which

may

be

beyond

our

control,

that

may

cause

actual

results

to

differ

materially

from

any

future

results,

performance

or

achievements

expressed

or

implied

by

the

forward-looking

statements.

These

risks,

uncertainties

and

other

factors

include

fluctuations

in

the

demand

for

our

services;

fluctuations

in

worldwide

prices

of

and

demand

for

natural

gas

and

oil;

fluctuations

in

levels

of

natural

gas

and

oil

exploration

and

development

activities;

the

impact

of

competition;

actions

by

customers;

the

risk

of

reductions

in

spending

on

helicopter

services

by

governmental

agencies;

changes

in

tax

and

other

laws

and

regulations;

changes

in

foreign

exchange

rates

and

controls;

risks

associated

with

international

operations;

operating

risks

inherent

in

our

business,

including

the

possibility

of

declining

safety

performance;

general

economic

conditions

including

the

capital

and

credit

markets;

our

ability

to

obtain

financing;

the

risk

of

grounding

of

segments

of

our

fleet

for

extended

periods

of

time

or

indefinitely;

our

ability

to

re-deploy

our

aircraft

to

regions

with

greater

demand;

our

ability

to

acquire

additional

aircraft

and

dispose

of

older

aircraft

through

sales

into

the

aftermarket;

the

possibility

that

we

do

not

achieve

the

anticipated

benefit

of

our

fleet

investment

program;

availability

of

employees;

political

instability,

war

or

acts

of

terrorism

in

any

of

the

countries

where

we

operate;

and

those

discussed

under

the

captions

“Risk

Factors”

and

“Management’s

Discussion

and

Analysis

of

Financial

Condition

and

Results

of

Operations”

in

our

Annual

Report

on

Form

10-K

for

the

fiscal

year

ended

March

31,

2013

and

our

Quarterly

Report

on

Form

10-Q

for

the

quarter

ended

December

31,

2013.

We

do

not

undertake

any

obligation,

other

than

as

required

by

law,

to

update

or

revise

any

forward-looking

statements,

whether

as

a

result

of

new

information,

future

events

or

otherwise. |

3

Bristow is the leading provider of helicopter services

and is a unique investment in oil field services

•

Ticker: BRS; stock price

*

of

$73.58/share with a market cap

*

~$2.7 billion

•

471 aircraft in ~20 countries with

~3,700 employees

•

Rated “Investment Grade”

by

Standard and Poor’s

•

Quarterly dividend of $0.25/share

(historic growth ~30% annually)

•

Bristow Helicopters Ltd. recently

acquired a 60% interest in Eastern

Airways Ltd.

*NOTE:

Based

on

36.8

million

fully

diluted

weighted

average

shares

outstanding

for

the

three

months

ended

12/31/2013

and

stock

price

as

of

03/14/2014;

Standard

and

Poor’s

secured

rating

is

BBB-

with

the

unsecured

rating

of

BB-

Bristow flies crews for oil and gas

companies and provides search

and rescue (SAR) services for

them and governments alike |

4

TARGET ZERO,

our industry leading safety program,

creates differentiation and client loyalty

•

Safety is our primary core value

•

Bristow’s ‘Target Zero’

program is now the leading

example emulated industry-wide

•

Safety performance accounts for 25% of management

incentive compensation

•

Flight Safety Foundation (FSF) awarded its 2012

President’s Citation to Bristow Group’s Target Zero

program |

5

Bristow services are utilized in every phase of

offshore oil and gas growth, especially production

•

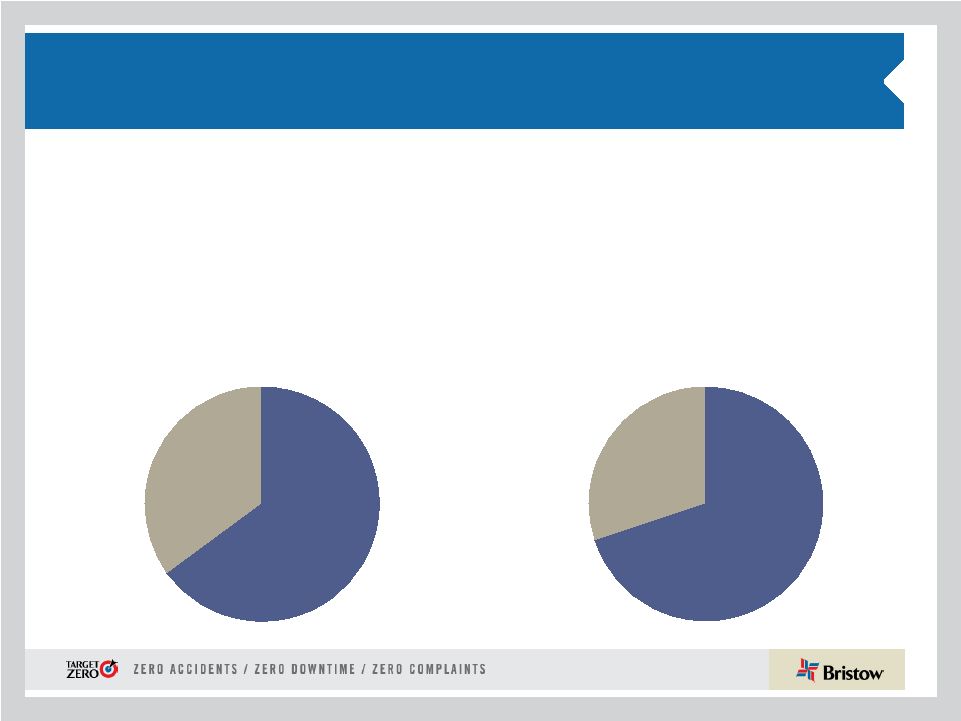

Largest share of revenues (>60%) relates to

oil and gas production, providing stability and

growth opportunities

•

There are ~ 8,000 offshore production

installations worldwide —

compared with

>600 exploratory drilling rigs

•

~1,700 helicopters are servicing the

worldwide oil and gas industry of which

Bristow’s fleet is approximately one-third

•

Bristow revenues are primarily driven by

operating expenditures

Typical revenues by segment

Exploration

20%

Development

10%

Production

60%

Other 10%

ABANDONMENT

EXPLORATION

SEISMIC

DEVELOPMENT

PRODUCTION

H e l i c o p t e r t r a n s p o r t a t i o

n s e r v i c e s |

6

Fixed

monthly

65%

Variable

hourly

35%

Fixed

monthly

70%

Variable

hourly

30%

Bristow’s contract structure generates predictable

income and cash flow

Significant operating leverage

Revenue sources

•

Two-tiered contract structure includes both:

–

Fixed monthly standing charge to reserve helicopter capacity

–

Variable fees based on hours flown with fuel pass-through

•

Bristow contracts earn 65% of revenue without flying

Operating income |

7

Our value proposition will continue to be based on

secular growth, financial safety and balanced return

Long term value for

our shareholders

2. Prudent balance

sheet management

with ample liquidity

1. Growth not dependent

on economic or

commodity cycles

3. Capital return

through dividends and

opportunistic share repurchases

Investment:

FY 2012 -

2016 |

8

$278.0

$311.0

$33.0

$5.2

$5.2

YTD FY13

Operations

Corporate and Other

FX Changes

YTD FY14

$2.77

$3.11

$0.33

$0.11

$0.10

YTD FY13

Operations

Corporate and Other

FX Changes

YTD FY14

Financial highlights YTD:

Adjusted EPS and adjusted EBITDAR summary

YTD FY13 to YTD FY14 adjusted EPS bridge

YTD FY13 to YTD FY14 adjusted EBITDAR bridge (in millions)

*

Adjusted

EPS

and

EBITDAR

amounts

exclude

gains

and

losses

on

dispositions

of

assets

and

any

special

items

during

the

nine

months

ended

December

31,

2013

and

2012.

See

reconciliation

of

these

items

to

GAAP

in

the

appendix

hereto

and

in

our

earnings

release

for

the

quarter

ended

December

31,

2013. |

9

CHANGE:

Bristow Helicopters is making an investment in Eastern Airways,

a UK regional fixed-wing oil and gas focused transport company

•

Bristow Helicopters Limited (Bristow Helicopters)

purchased a 60% interest in the privately owned

Eastern Airways International Limited (Eastern

Airways)

•

Eastern Airways is a regional fixed-wing operator

with both charter and scheduled flights servicing

UK oil and gas industry transport from its main

operational hub in Aberdeen

•

Bristow Helicopters investment is £27M with a

possible £6M earn out over three years and

includes:

A 60% interest in Eastern Airways with

proportional voting and economic rights, with

the existing owners retaining the remaining

40%

30 fixed-wing aircraft as of February 7, 2014

Financial results from Eastern Airways will be

consolidated within Bristow’s EBU

This investment will strengthen our ability to provide a complete suite of

point- to-point transportation services for our existing European based

passengers |

10

Charter services

Scheduled services

Eastern Airways provides scale, stability and positive financial

impact (with less capital) for EBU

This investment expands helicopter services in certain areas like the Shetland

Islands and will create a more integrated logistics solution for our global

clients •

Bristow

Helicopters

and

Eastern

Airways

are

culturally

aligned

with

shared

core

values

of

safety,

quality

and

service

•

Bristow

Helicopters

and

Eastern

Airways

have

a

long

standing

relationship

working

together

on

several

contracts,

including

the

IAC

Scatsta

contract

•

Bristow

Helicopters

and

Eastern

Airways

together

are

positioned

to

facilitate

and

expand

passengers’

transport

experience

from

home

to

offshore

bases,

a

market

niche

underserved

by

major

airlines

•

Eastern

Airways

has

recently

been

awarded

a

contract

by

a

major

oil

company

to

provide

fixed

wing

services

to

Sumburgh

to

be

combined

with

separately

awarded

Bristow

Helicopters

contract

•

Financially

relatively

small

investment

with

expected

positive

EBITDAR,

BVA

and

EPS

impact

See

10-Q

Note

11

“Subsequent

Events”

for

more

information |

11

Opportunity tracker FY15-FY19:

558 Bristow a/c growth opportunities identified |

12

We manage our opportunities through the purchase of

104 a/c options and committed orders

6 on

order

558 aircraft opportunities identified

83 high

probability targets

47 orders

298 demand for new aircraft

185 realistic bid

opportunities

57 options

•

Bristow uses specific

opportunities to create

our order book

•

Opportunities are

condensed to 185

realistic bids

•

83 high probability

targets are derived from

a view that we have an

~33% bid success rate

•

Our order book is then

managed primarily using

capital efficient a/c

options with our original

equipment manufacturers

Source: Bristow business development February 2014 |

13

Our

TSR

has

been

highly

correlated

to

year-over-

year

improvement

in

Bristow

Value

Added

(BVA)

.

.

.

* Based on a study using Capital IQ data as of August 26, 2013. Analyzed the

current members of the Oilfield Services Index (OSX) The correlation statistic is derived from a

regression of actual enterprise value vs. predicted enterprise value.

Predicted enterprise value based on next twelve months (NTM) estimated BVA in perpetuity using a 10.5%

required

return

(NTM

BVA$/10.5%).

Similar

studies

conducted

over

time

have

produced

consistent

results.

Bristow BVA vs. Bristow TSR

•

Overall, BVA shows a much

stronger correlation to

market trading values and

therefore total shareholder

return (TSR)

•

Correlations are particularly

strong for the oil field

services sector at an “R

Squared”

of over 95%*

•

Bristow’s year-over-year

change in BVA has

historically been a leading

indicator of TSR |

14

. . .with Bristow’s three year total shareholder return

(TSR)

over 90% since adopting BVA

Source: Factset |

15

. . . and strong cash generation for a balanced return

as demonstrated in the past several years. . .

Share

repurchase

•

FY12 quarterly dividend initiated at $0.15/share

•

Dividend increased by 33% to $0.20/share in June

2012 quarter and increased by another 25% to

$0.25/share in August 2013

•

Bristow has a 20 -

30% target payout ratio of

forward adjusted EPS

•

In Q3 FY14 and January 2014 Bristow spent ~$33M

to repurchase 450,000 shares at average price of

~$75 and subsequently renewed its $100 million

share repurchase authorization

•

Value is key to our repurchasing decision with net

book value/share and our fleet NAV/share (including

the implied NAV for UK SAR) being the guide posts

Regular

dividend |

16

…

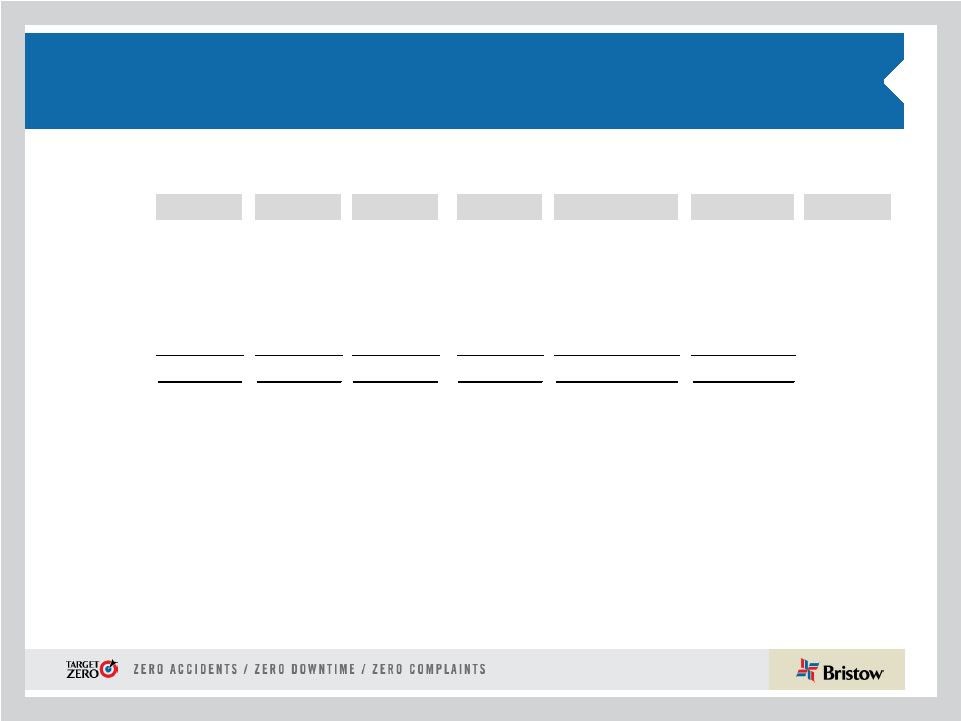

with FY14 guidance reaffirmed

•

FY14 adjusted EPS guidance reaffirmed on February 7, 2014 to

$4.25 -

$4.55, excluding special items and a/c sales. Other

specific items include:

* Assuming FY14 revenue earned in same regions and same mix as in FY13

Long term adjusted EPS growth of 10 -

15% combined with a 20 -

30%

dividend payout policy reflects management’s commitment to deliver a

more stable, growing and predictable total return for shareholders

Average LACE

~160 - 164

Interest expense

~ $30 - $35M

Average LACE rate

~ $8.95 - $9.25M

Rent expense (a/c only)

~$85 - $90M

G & A expense (all inclusive)

~ $175 - $185M

Tax rate*

~ 20 - 24%

Depreciation expense

~ $90 - $95M

Adj. EPS guidance

$4.25 - $4.55

FY14 guidance |

17

Conclusions

•

Safety

continues

to

be

our

#1

core

value

as

we

strive

to

achieve

Target

Zero

and

participate

in

industry

efforts

to

share

best

practices.

Bristow

believes

the

UK

CAA

CAP1145

safety

mandate

will

make

the

helicopter

industry

safer

as

we

continue

to

serve

our

clients’

logistics

needs

•

Despite

industry

concerns

of

soft

activity

in

the

oilfield

services

and

equipment

space,

Bristow

continues

to

see

good

secular

growth

with

meaningful

LACE

and

LACE

rate

increases

as

clients

turn

to

Bristow

as

their

provider

of

choice

due

to

our

global

reach,

financial

strength

and

ongoing

Operational

Excellence

performance

•

Although

the

third

quarter

results

were

lower

sequentially

and

year-over-year,

some

of

this

was

expected,

which

is

why

we

confirmed

annual

FY14

guidance

on

our

Q3

FY14

earnings

call

•

Bristow

Helicopters’

investment

in

Eastern

Airways

expands

services

in

certain

areas

like

the

Shetland

Islands

and

creates

a

more

integrated

logistics

solution

for

our

global

clients |

18

Appendix |

19

Organizational chart -

as of December 31, 2013

Business Unit

(% of Q3 FY14 operating revenue)

Corporate

Region

( # of a/c / # of Locations)

Joint Venture

(# of a/c)

Key

Operated Aircraft

Bristow owned and/or operated 345

aircraft as of December 31, 2013

Affiliated Aircraft

Bristow affiliates and joint

ventures operated 126 aircraft

as of December 31, 2013

* Includes corporate and other |

20

Aircraft Fleet –

medium and large

as of December 31, 2013

Next Generation Aircraft

Medium capacity 12-16 passengers

Large capacity 16-25 passengers

Mature Aircraft

Fair

market

value

of

our

owned

fleet

is

~$1.9

billion

and

leased

fleet

is

~$900

million

Aircraft

Type

No. of PAX

Engine

Consl

Unconsl

Total

Ordered

Large Helicopters

AS332 L Super Puma

18

Twin Turbine

19

-

19

-

AW189

16

Twin Turbine

-

-

-

17

EC175

16

Twin Turbine

-

-

-

5

EC225

19

Twin Turbine

20

-

20

3

Mil MI 8

20

Twin Turbine

7

-

7

-

Sikorsky S-61

18

Twin Turbine

2

-

2

-

Sikorsky S-92

19

Twin Turbine

56

7

63

10

104

7

111

35

LACE

102

Medium Helicopters

AW139

12

Twin Turbine

14

2

16

4

Bell 212

12

Twin Turbine

-

14

14

-

Bell 412

13

Twin Turbine

28

17

45

-

EC155

13

Twin Turbine

1

-

1

-

Sikorsky S-76A/A++

12

Twin Turbine

4

5

9

-

Sikorsky S-76C/C++

12

Twin Turbine

51

34

85

-

Sikorsky S-76D

12

Twin Turbine

2

-

2

8

100

72

172

12

LACE

48 |

21

Aircraft Fleet –

small, training and fixed

as of December 31, 2013 (continued)

Mature Aircraft

Small capacity 4-7 passengers

Training capacity 2-6 passengers

* LACE does not include held for sale, training helicopters and fixed wing

Next Generation Aircraft

Aircraft

Type

No. of PAX

Engine

Consl

Unconsl

Total

Ordered

Small Helicopters

AS350BB

4

Turbine

-

2

2

-

Bell 206B

4

Turbine

1

2

3

-

Bell 206 L Series

6

Turbine

19

6

25

-

Bell 407

6

Turbine

36

-

36

-

BK 117

7

Twin Turbine

2

-

2

-

BO-105

4

Twin Turbine

2

-

2

-

EC135

7

Twin Turbine

3

3

6

-

63

13

76

-

LACE

13

Training Helicopters

AS 355

5

Twin turbine

3

-

3

-

Bell 206B

4

Single Engine

12

-

12

-

Robinson R22

2

Piston

10

-

10

-

Robinson R44

4

Piston

5

-

5

-

Sikorsky 300CB/CBi

2

Piston

44

-

44

-

Fixed Wing

1

-

1

-

75

-

75

-

Fixed Wing

3

34

37

-

Total

345

126

471

47

TOTAL LACE (Large Aircraft Equivalent)*

162 |

22

Operating lease strategy: lowering the cost and amount of

capital needed to grow

•

Of

the

81

a/c

currently

leased

in

our

fleet,

52

are

commercial

(39

LACE)

and

29

are

training

•

39

LACE

a/c

represent

approximately

24%

of

our

commercial

fleet

•

Our

goal

is

for

commercial

fleet

operating

leases

to

account

for

approximately

30-35%

of

our

LACE

Leased aircraft as of December 31, 2013

*

The

percentage

of

LACE

leased

is

calculated

by

taking

the

total

LACE

for

leased

aircraft

divided

by

the

total

LACE

for

all

aircraft

we

operate,

including

both

owned

and

leased

aircraft.

See

10-Q

Note

5

“Commitments

and

contingencies”

for

more

information

provided

on

operating

leases.

Small

Medium

Large

Total

Leased LACE

Total LACE

% Leased

EBU

-

1

21

22

22

59

37%

WASBU

-

1

1

2

2

22

7%

NABU

4

13

3

20

11

34

31%

AUSBU

2

2

4

8

6

20

28%

OIBU

-

-

-

-

-

28

-

Total

6

17

29

52

39

162

24%

* |

23

Consolidated fleet changes and aircraft sales for

Q3 FY14

See

10-Q

Note

5

“Commitments

and

contingencies”

for

more

information

provided

on

operating

leases.

Additionally,

during

Q3

FY14

we

sold

six

aircraft

for

$72.4M,

which

we

subsequently

leased

back.

Leased aircraft in consolidated fleet

Small

Medium

Large

Training

Total

EBU

-

1

21

-

22

WASBU

-

1

1

-

2

NABU

4

13

3

-

20

AUSBU

2

2

4

-

8

OIBU

-

-

-

-

-

Academy

-

-

-

29

29

Total

6

17

29

29

81

Q1 FY14

Q2 FY14

Q3 FY14

YTD

Fleet Count Beginning

351

353

350

351

Delivered

Large

3

2

4

9

Medium

2

3

3

8

Total Delivered

5

5

7

17

Removed

Sales

(4)

(4)

(11)

(19)

Other*

1

(4)

(1)

(4)

Total Removed

(3)

(8)

(12)

(23)

353

350

345

345

* Includes lease returns and commencements

Fleet changes

Held for sale aircraft in consolidated fleet

Small

Medium

Large

Training

Total

EBU

-

-

2

-

2

WASBU

-

2

-

-

2

NABU

11

-

-

-

11

AUSBU

-

-

-

-

-

OIBU

1

3

-

-

4

Academy

-

-

-

2

2

Total

12

5

2

2

21

# of a/c Sold

Cash

received*

Q1 FY14

4

2.0

$

Q2 FY14

4

7.9

Q3 FY14

11

14.3

Total

19

24.2

$

* Amounts stated in millions |

24

Op revenue

1

LACE

LACE rate

2,3

EBU

$452

59

$10.30

WASBU

231

22

14.17

NABU

174

34

6.75

AUSBU

108

20

7.21

OIBU

95

28

4.58

Total

$1,091

162

$8.97

Operating Revenue, LACE, and LACE rate by BU

as of December 31, 2013

Operating revenue, LACE and LACE rate by BU

4

1)

$ in millions

2)

LACE rate is annualized

3)

$ in millions per LACE

4)

Excludes Bristow Academy |

25

Historical LACE by BU

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

EBU

45

45

45

42

42

43

48

46

44

46

46

45

WASBU

23

23

24

25

24

24

21

22

23

22

22

22

NABU

39

36

36

36

39

35

34

29

30

29

30

30

AUSBU

20

20

22

22

20

23

24

20

19

20

20

19

OIBU

36

34

34

35

33

33

33

38

39

38

38

34

Consolidated

163

158

161

160

157

158

159

154

154

154

155

149

Q1

Q2

Q3

Q4

Q1

Q2

Q3

EBU

47

45

51

55

57

59

59

WASBU

22

22

20

21

21

21

22

NABU

30

31

39

37

37

33

34

AUSBU

18

17

17

19

19

19

20

OIBU

32

28

27

27

27

28

28

Consolidated

147

142

154

158

161

160

162

LACE

FY11

FY12

FY10

FY13

FY14 |

26

Historical LACE rate by BU

1) $ in millions

2) LACE rate is annualized

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

EBU

$8.36

$8.28

$8.40

$8.76

$8.20

$8.50

$7.90

$8.40

$9.80

$9.60

$9.63

$10.09

WASBU

9.08

8.81

8.66

8.34

9.70

9.40

10.70

9.90

9.10

10.30

11.17

11.46

NABU

5.05

5.44

5.26

5.23

5.40

6.10

6.00

6.60

5.80

6.30

5.89

5.79

AUSBU

5.38

5.56

5.59

5.67

6.80

6.00

6.00

7.50

8.60

7.10

6.96

7.78

OIBU

3.66

4.09

4.06

3.78

3.90

4.10

4.40

3.90

3.50

3.70

3.78

4.22

Consolidated

$6.31

$6.52

$6.49

$6.45

$6.70

$6.90

$6.90

$7.10

$7.30

$7.40

$7.43

$7.89

Q1

Q2

Q3

Q4

Q1

Q2

Q3

EBU

$10.60

$11.03

$9.74

$9.13

$9.63

$9.95

$10.30

WASBU

12.35

12.24

13.71

13.28

14.26

14.62

14.17

NABU

7.05

7.11

5.84

6.12

6.34

7.13

6.75

AUSBU

8.48

9.29

9.55

8.58

8.04

7.74

7.21

OIBU

4.22

4.62

4.76

4.94

4.97

4.73

4.58

Consolidated

$8.55

$8.95

$8.49

$8.35

$8.78

$9.07

$8.97

LACE rate

1,2

FY10

FY11

FY12

FY13

FY14 |

27

Order and options book as of December 31, 2013

1)

22 large a/c on order and 13 large a/c on option are subject to the

successful development and certification of the aircraft 2)

One oil and gas full SAR /c is under contract

ORDER BOOK¹

#

Helicopter

Class

Delivery Date

Location

Contracted

1

Medium

March 2014

OIBU

1 of 1

1

Medium

March 2014

NABU

2

Large

March 2014

EBU

1 of 2

3

Medium

June 2014

OIBU

1 of 3

2

Large

June 2014

AUSBU

1 of 2

1

Large

June 2014

OIBU

1

Large

June 2014

WASBU

6

Medium

September 2014

WASBU

1

Medium

September 2014

NABU

3

Large

September 2014

EBU

2 of 32

1

Large

September 2014

AUSBU

1 of 1

1

Large

December 2014

EBU

1

Large

March 2015

OIBU

1

Large

March 2015

NABU

1 of 1

1

Large

March 2015

AUSBU

1

Large

March 2015

EBU

1

Large

June 2015

EBU

1

Large

June 2015

AUSBU

1

Large

September 2015

NABU

1

Large

December 2015

NABU

1

Large

March 2016

EBU

2

Large

March 2016

NABU

1

Large

June 2016

NABU

1

Large

June 2016

EBU

36

8 of 36

OPTIONS BOOK

#

Helicopter

Class

Delivery Date

2

Medium

March 2015

1

Large

June 2015

3

Medium

June 2015

3

Large

September 2015

2

Medium

September 2015

3

Large

December 2015

2

Medium

December 2015

2

Large

March 2016

3

Medium

March 2016

3

Large

June 2016

3

Medium

June 2016

4

Large

September 2016

2

Medium

September 2016

5

Large

December 2016

1

Medium

December 2016

3

Large

March 2017

1

Medium

March 2017

3

Large

June 2017

1

Medium

June 2017

3

Large

September 2017

1

Medium

September 2017

4

Large

December 2017

1

Medium

December 2017

1

Large

March 2018

57 |

28

Order and options book as of December 31, 2013

(continued)

UK SAR CONFIGURED ORDER BOOK

#

Helicopter

Class

Delivery Date

Location

Contracted

1

Large

June 2014

EBU

1 of 1

3

Large

September 2014

EBU

3 of 3

2

Large

December 2014

EBU

2 of 2

2

Large

March 2015

EBU

2 of 2

2

Large

March 2015

EBU

2 of 2

2

Large

June 2015

EBU

2 of 2

2

Large

September 2015

EBU

2 of 2

2

Large

September 2015

EBU

2 of 2

2

Large

December 2015

EBU

2 of 2

18

18 of 18

The aircraft that are indicated in grey italic will be leased upon delivery

|

29

Adjusted EBITDAR margin* trend

*

Adjusted

EBITDAR

excludes

special

items

and

asset

dispositions

and

margin

is

calculated

by

taking

adjusted

EBITDAR

divided

by

operating

revenue

FY11

FY12

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

Q4

Full Year

EBU

29.8%

31.5%

34.6%

34.4%

32.7%

33.0%

31.4%

30.7%

36.1%

32.9%

WASBU

33.7%

36.9%

35.8%

34.3%

35.2%

29.5%

35.5%

37.2%

36.6%

35.0%

NABU

20.8%

25.8%

15.9%

8.5%

18.5%

14.3%

20.6%

14.8%

19.4%

17.3%

AUSBU

33.2%

26.1%

27.0%

31.1%

29.3%

20.2%

14.4%

23.5%

35.6%

24.3%

OIBU

18.3%

40.2%

37.4%

59.4%

39.3%

48.1%

19.1%

47.8%

42.9%

39.5%

Consolidated

23.8%

27.5%

25.9%

29.6%

26.7%

23.4%

24.0%

27.6%

31.2%

26.6%

FY13

FY14

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

EBU

32.2%

34.6%

39.5%

38.3%

36.2%

30.3%

35.3%

35.3%

WASBU

31.9%

26.5%

35.0%

31.8%

31.5%

31.3%

30.4%

33.5%

NABU

23.2%

20.7%

29.1%

29.5%

25.7%

29.2%

31.0%

33.1%

AUSBU

27.0%

28.0%

27.3%

26.0%

27.1%

17.7%

21.0%

15.0%

OIBU

36.2%

44.2%

55.7%

51.6%

46.6%

67.4%

39.3%

33.2%

Consolidated

26.3%

26.1%

31.5%

29.4%

28.3%

28.5%

28.7%

27.0% |

30

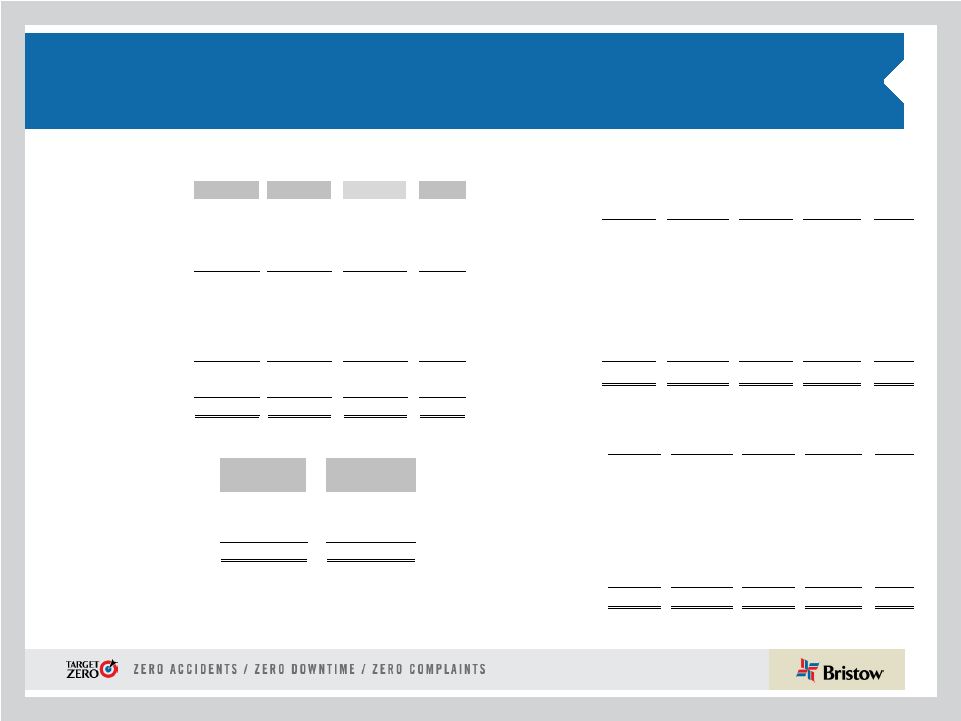

Adjusted EBITDAR* reconciliation

* Adjusted EBITDAR excludes special items and asset dispositions

Fiscal year ended,

3/31/2011

3/31/2012

($ in millions)

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

Q4

Full Year

Net income

$20.9

$38.8

$42.3

$31.2

$133.3

$21.2

$3.0

$26.5

$14.6

$65.2

Income tax expense

8.5

3.3

-11.8

7.1

7.1

6.6

-1.9

7.1

2.4

14.2

Interest expense

11.1

11.5

13.8

9.9

46.2

9.0

9.5

9.8

10.0

38.1

Gain on disposal of assets

-1.7

-1.9

0.0

-5.1

-8.7

-1.4

1.6

2.9

28.6

31.7

Depreciation and amortization

19.3

21.0

21.3

27.7

89.4

22.7

25.4

22.7

25.3

96.1

Special items

0.0

0.0

-1.2

2.4

1.2

0.0

24.6

0.0

3.4

28.1

EBITDA Subtotal

58.1

72.7

64.4

73.3

268.5

58.1

62.1

68.9

84.3

273.4

Rental expense

6.6

6.1

8.7

7.7

29.2

9.0

9.1

12.8

15.1

46.0

Adjusted EBITDAR

$64.7

$78.8

$73.1

$81.1

$297.7

$67.0

$71.2

$81.8

$99.5

$319.5

3/31/2013

3/31/2014

($ in millions)

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

Net income

$24.2

$30.4

$36.7

$40.4

$131.7

$26.9

$109.9

$19.0

Income tax expense

6.2

8.3

7.8

12.7

35.0

7.6

41.1

2.9

Interest expense

8.8

8.6

14.7

10.3

42.4

20.4

9.1

7.3

Gain on disposal of assets

5.3

1.3

-7.4

-7.2

-8.1

1.7

3.1

-4.0

Depreciation and amortization

21.4

23.3

24.9

26.7

96.3

22.8

23.9

23.7

Special items

2.2

-2.8

14.9

1.9

16.2

0.0

-101.8

23.5

EBITDA Subtotal

68.0

69.2

91.6

84.8

313.5

79.4

85.2

72.4

Rental expense

16.3

15.3

17.6

18.3

67.4

23.1

23.3

28.3

Adjusted EBITDAR

$84.3

$84.5

$109.2

$103.0

$381.0

$102.5

$108.5

$100.7 |

31

Bristow stock price reflects improved operational

performance and increasing shareholder returns

Note:

The

net

asset

FMV

per

share

does

not

include

our

UK

SAR

aircraft |

32

Net asset fair market value (FMV) per share

calculation as of December 31, 2013

(in millions)

(+) FMV of a/c

1,949

$

(+) FMV of leased a/c

873

(+) NBV of PPE w/o a/c

540

(+) Working capital

481

(-) LT debt

(833)

(-) Leased imputed debt

(394)

(-) Pension liability

(125)

Net asset FMV

2,492

$

# of common shares

37

Net asset FMV per share

67.71

$ |

33

Bristow Value Added (BVA)

Sample calculation for Q2 FY14 and Q2 FY13

Bristow Value Added = Gross Cash Flow –

(Gross Operating Assets X Capital Charge)

BVA

=

GCF

-

(

GOA

X

10.5%**

)

Bristow Value Added calculation for Q2 FY14

$22.4

=

$109.2*

-

(

$3,309*

X

2.625%**)

Bristow Value Added calculation for Q2 FY13

$2.1

=

$78.8*

-

(

$2,922*

X

2.625%**)

* Reconciliation for these items follows right after this

slide ** Quarterly capital charge of 2.625% is based on annual

capital charge of 10.5% |

34

Bristow Value Added (BVA)

Sample calculation for Q3 FY14 and Q3 FY13

Bristow Value Added = Gross Cash Flow –

(Gross Operating Assets X Capital Charge)

BVA

=

GCF

-

(

GOA

X

10.5%**

)

Bristow Value Added calculation for Q3 FY14

$12.1

=

$100.8*

-

(

$3,378*

X

2.625%**)

Bristow Value Added calculation for Q3 FY13

$9.3

=

$95.1*

-

(

$3,269*

X

2.625%**)

* Reconciliation for these items follows right after this

slide ** Quarterly capital charge of 2.625% is based on annual

capital charge of 10.5% |

35

Gross cash flow reconciliation |

36

Adjusted gross operating assets reconciliation

(in millions)

Adjusted gross operating assets reconciliation

Q2 FY13

Q3 FY13

Q2 FY14

Q3 FY14

Total assets

$2,785

$3,051

$3,166

$3,277

Accumulated depreciation

464

480

518

530

Capitalized operating leases

225

244

373

419

Cash and cash equivalents

(348)

(232)

(314)

(323)

Investment in unconsolidated entities

(215)

(267)

(272)

(255)

Goodwill

(30)

(30)

(30)

(30)

Intangibles

(4)

(4)

(2)

(2)

Assets held for sale: net

(20)

(15)

(27)

(22)

Assets held for sale: gross

83

76

56

48

Adj. for gains and losses on assets sales

120

108

(8)

(5)

Accounts payable

(56)

(63)

(70)

(60)

Accrued maintenance and repairs

(19)

(18)

(17)

(17)

Other accrued taxes

(8)

(8)

(10)

(8)

Accrued wages, benefits and related taxes

(45)

(51)

(49)

(67)

Other accrued liabilities

(27)

(27)

(24)

(145)

Income taxes payable

(13)

(13)

(33)

(20)

Deferred revenue

(13)

(20)

(21)

(23)

ST deferred taxes

(15)

(12)

(2)

(2)

LT deferred taxes

(144)

(147)

(155)

(146)

Adjusted gross operating assets before Lider

$2,723

$3,053

$3,079

$3,150

Adjusted gross operating assets-Lider proportional

199

216

230

228

Adjusted gross operating assets after Lider

$2,922

$3,269

$3,309

$3,378 |

37

GAAP reconciliation

(i) See information about special items in 10-Q or earnings release for Q3 FY14 (ii)

These amounts are presented after applying the appropriate tax effect to each item and dividing by the weighted average shares outstanding during the related period to calculate the earnings per share impact |

38

Leverage reconciliation

*Adjusted EBITDAR excludes gains and losses on dispositions of assets

Debt

Investment

Capital

Leverage

(a)

(b)

(c) = (a) + (b)

(a) / (c)

(in millions)

As of December 31, 2013

$

841.6

$ 1,762.9

$ 2,604.5

32.3%

Adjust for:

Unfunded Pension Liability

125.0

125.0

NPV of Lease Obligations

393.6

393.6

Letters of credit

2.4

2.4

Adjusted

$

1,362.6

(d)

$ 1,762.9

$ 3,125.5

43.6%

Calculation of debt to adjusted EBITDAR multiple

TTM Adjusted EBITDAR*:

FY 2014

$

414.0

(e)

= (d) / (e)

3.29:1 |

39

Bristow Group Inc. (NYSE: BRS)

2103

City

West

Blvd.,

4

th

Floor

Houston, Texas 77042

t

713.267.7600

f

713.267.7620

bristowgroup.com

Contact Us |