Attached files

| file | filename |

|---|---|

| 8-K - 8-K - CarParts.com, Inc. | d688106d8k.htm |

1

U.S. Auto Parts Network, Inc.

Leading online source for automotive aftermarket parts and repair information

Investor Presentation

March 11, 2014

Exhibit 99.1 |

Safe

Harbor This presentation may contain certain forward-looking statements and

management may make additional forward-looking statements in response to

your questions. These statements do not guarantee future performance and

speak only as of the date hereof, and qualify for the safe harbor provided by

Section 21E of the Securities Exchange Act of 1934, as amended, and Section

27A of the Securities Act of 1933. We refer all of you to the risk

factors contained in US Auto Parts Annual Report on Form 10-K and

quarterly reports on

Form

10-Q

filed

with

the

Securities

and

Exchange

Commission,

for

more

detailed

discussion

on

the

factors

that

can

cause

actual

results

to

differ

materially from those projected in any forward-looking statements.

2 |

3

Broad Auto Parts Product Offering

Body Parts

Engine Parts

Performance & Accessories

*Represents USAP online mix

**Source; AAIA Factbook Research

19%

41%

40%

$15B

$15B

Revenue*

Overall Market**

$50B

Brake Discs

Catalytic

Converters

Radiators

Headers

Oxygen

Sensors

Alternators

Exhaust

Driveshaft

Fuel Injection /

Delivery

Lamps

Mirrors

Bumpers

Hoods

Tailgates

Doors

Grills

Wheels

Window

Regulators

Seat Covers

Car Covers

Floor Mats /

Carpeting

Cold Air

Intakes

Vent Visors

Tonneau

Covers

Nerf Bars

Bug Shields

Car Bras |

Online

sales

of

automotive

parts

and

accessories

continue

to

grow

Google

has

experienced

a

6

year

compound

annual

growth

rate

(“CAGR”)

of

16%

in

queries

for

automotive

parts

4

$1.3

$1.3

$1.2

$1.3

$1.5

$1.6

$1.5

$1.5

$1.8

$1.8

$1.9

$1.9

$2.0

$2.2

$2.1

$1.0

$1.1

$1.2

$1.3

$1.4

$1.5

$1.6

$1.7

$1.8

$1.9

$2.0

$2.1

$2.2

$2.3

Source: eBay filings, press releases

Source: Google

eBay Parts Sales Continue to Increase

Google Queries for Parts Growing

Online Market is Vibrant and Growing

Aftermarket e-Commerce Overview

Mobile year over year queries increased 50% and 80% for cellphones and tablets, respectively, for

September 2013 YTD 300%

250%

200%

150%

100%

50%

0%

2008

2009

2010

2011

2012

2013

16% CAGR |

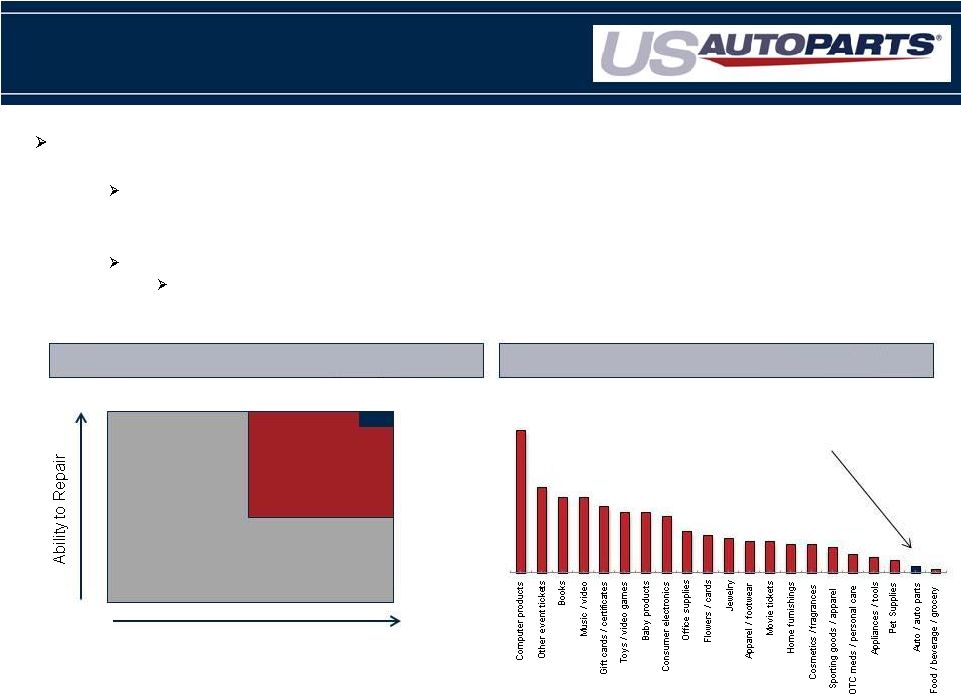

Online penetration for auto parts has trailed penetration rates of other consumer

product categories for two reasons: 1)

Auto parts are traditionally bought by demographics that have lower internet

access rates We believe consumer buying will shift from offline to online as

mobile device penetration increases for these demographics 2)

Shopping for auto parts online can be difficult for consumers

The complexity required to buy an auto part online increases consumers concerns it

will not fit their vehicle Online retailers continue to make improvements to

online shopping, reducing concerns and increasing conversion Size and

Penetration of Online Automotive Parts Aftermarket e-Commerce

Overview 5

Source: Morgan Stanley and Forrester Research

Low Automotive Online Sales Penetration

Source: AAIA

Estimate

based

on

AAAI

Fact

book

-

$85B

in

parts,

$70B

in

labor

* Excludes eBay

Automotive Aftermarket by Segment

Desire to Repair

High

Low

$155B

Do-It-For-Me

$45B

Do-It-Yourself

(USAP Target Market)

$3.1B-$4.0B

Online Sales*

High

Online penetration rates for most

consumer products categories

range from 4% to 6%

Online sales of automotive

parts significantly lag other

product categories

45%

27%

24%

24%

21%

19%

19%

18%

13%

12%

11%

10%

10%

9%

9%

8%

6%

5%

4%

3%

1%

Product Category |

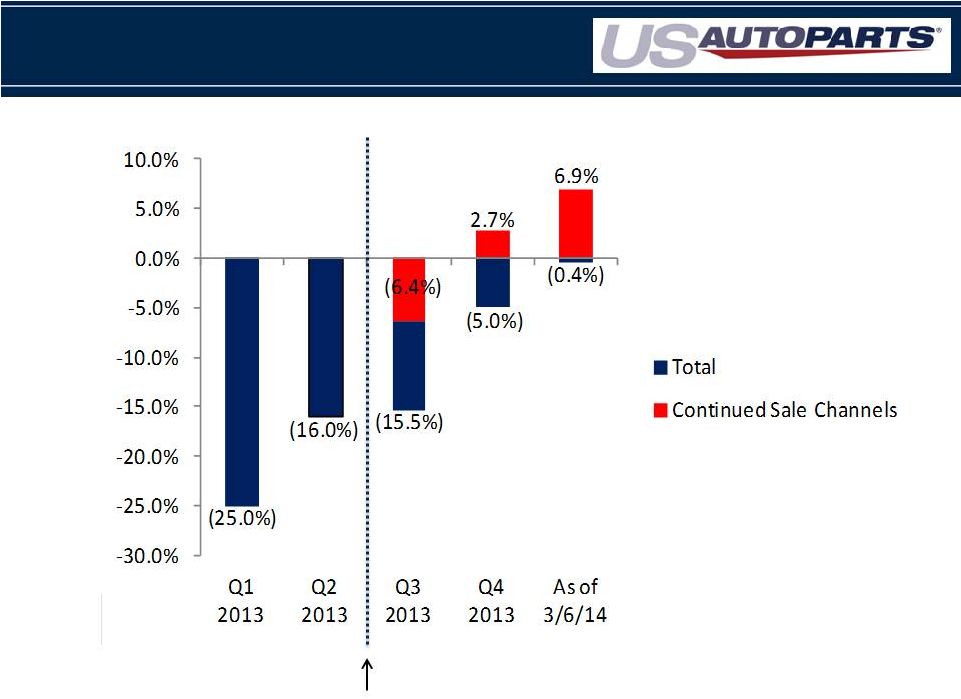

Changes to Our Business

6

* FCF is defined as Adjusted EBITDA less CAPX

2012 -

2013

•

Traffic and revenue declined resulting from

search engine changes forcing us to

consolidate websites

•

Gross margin compression from increased

competition

•

Cost reductions could not be eliminated fast

enough to keep up with gross profit dollar

lost

Go Forward

•

Traffic is stabilizing and revenue from go

forward sales channels has turned slightly

positive

•

Larger focus on Private Label business with

healthier margins at competitive prices

•

Cost reductions have now exceeded gross

profit

dollars

loss

from

2012

–

2013

$0 |

Product Assortment

•

Over 50% of product sales directly sourced from

Asia

•

Transition away from lower margin stock ship

branded product while expanding private label mix

•

Broad assortment

Marketing

•

Over 10 million unique monthly visitors to our

websites

•

Unique visitors more than two times higher then

any other auto parts retailer

•

$7 customer acquisition cost (“CAC”)

USAP has two main competitive advantages

Competitive Advantages

•

Over 40,000 private label SKUs

•

Over 1.5M branded SKUs

7 |

USAP’s Supply Chain Creates Pricing Advantage

USAP’s ability to competitively price products while maintaining healthy

margins is a function of the Company’s ability to leverage its robust

private label supply chain. The Company is working to increase margins by

shifting its product mix toward increased private label offerings

-

current

margins

range

from

29%

-

31%

The Company sources product directly from over 200 factories in Asia

8

Margin %

In-Stock

Private Label

(Asia Sourced)

Branded

(U.S. Sourced)

40% -

70%

25% -

40%

10% -

25%

Drop Shipped

Current Mix

55%

45%

Current Mix

63%

37%

75%

25%

Goal

70%

30%

Goal |

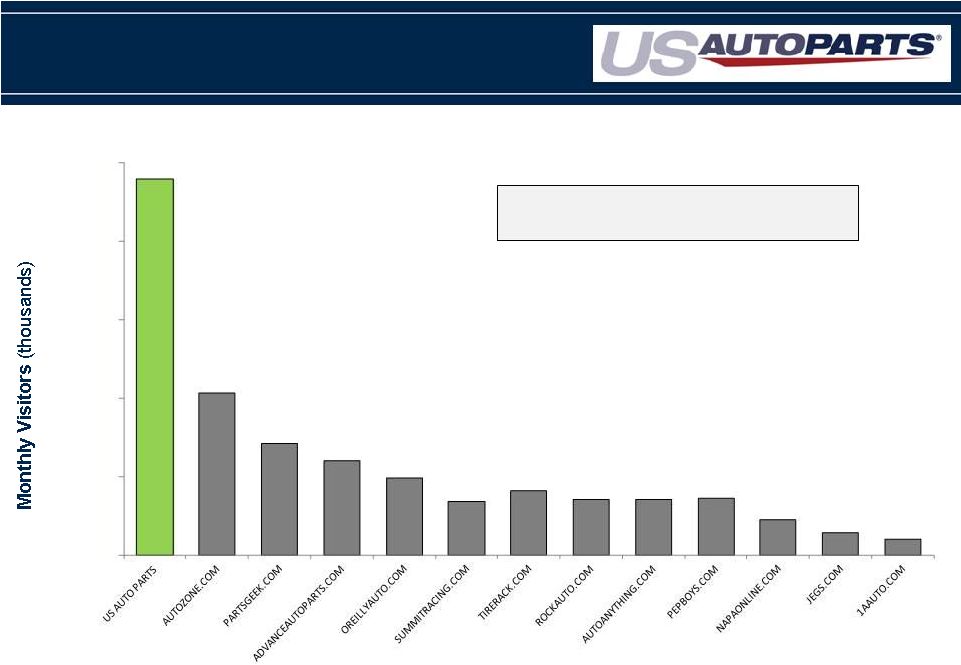

US

Auto

Parts

Dominant

Reach-

Largest

Pure Play Internet Retailer

9

0

2,000

4,000

6,000

8,000

10,000

USAP traffic includes traffic from USAP continued sales channels and WAG since the

acquisition

Competitive sites’ traffic based on Compete December 2013 reports

(some overlap of monthly visitors across websites)

USAP’s traffic is 2x larger than any other

pure play online auto parts seller |

Revenue

100%

Gross Margins

29% -

31%

Variable OPEX Costs

15%

Fixed Costs

0%

Incremental Flow Thru

14% -

16%

10

Growth and Profitability

Incremental Flow Thru |

11

•

Excludes stock based compensation, depreciation and amortization

•

For every incremental year required to achieve growth levels, fixed expenses

increase $1.0M or 3% Financial Sensitivity

Our business model has significant cost leverage as revenues grow

Base

10%

20%

30%

40%

Revenue

$250

$275

$300

$325

$350

Gross Margin %

Variable:

Fulfillment

3.2%

3.2%

3.2%

3.2%

3.2%

Marketing

9.3%

9.3%

9.3%

9.3%

9.3%

Technology

0.7%

0.7%

0.7%

0.7%

0.7%

G&A

1.8%

1.8%

1.8%

1.8%

1.8%

Total Variable

14.9%

14.9%

14.9%

14.9%

14.9%

Fixed:

Fulfillment

2.5%

2.2%

2.0%

1.9%

1.8%

Marketing

4.0%

3.6%

3.3%

3.0%

2.8%

Technology

1.2%

1.1%

1.0%

0.9%

0.9%

G&A

4.0%

3.6%

3.3%

3.1%

2.9%

Total Fixed

11.6%

10.6%

9.7%

9.0%

8.3%

Adjusted EBITDA %

Adjusted EBITDA $

$6 –

$11

$10 –

$15

$13 –

$19

$17 –

$23

$20 –

$27

29.0% –

31.0%

29.0% –

31.0%

29.0% –

31.0%

29.0% –

31.0%

29.0% –

31.0%

2.4% –

4.4%

3.5% –

5.5%

4.4% –

6.4%

5.1% –

7.1%

5.8% –

7.8% |

12

AutoMD –

Addressing the DIFM Market |

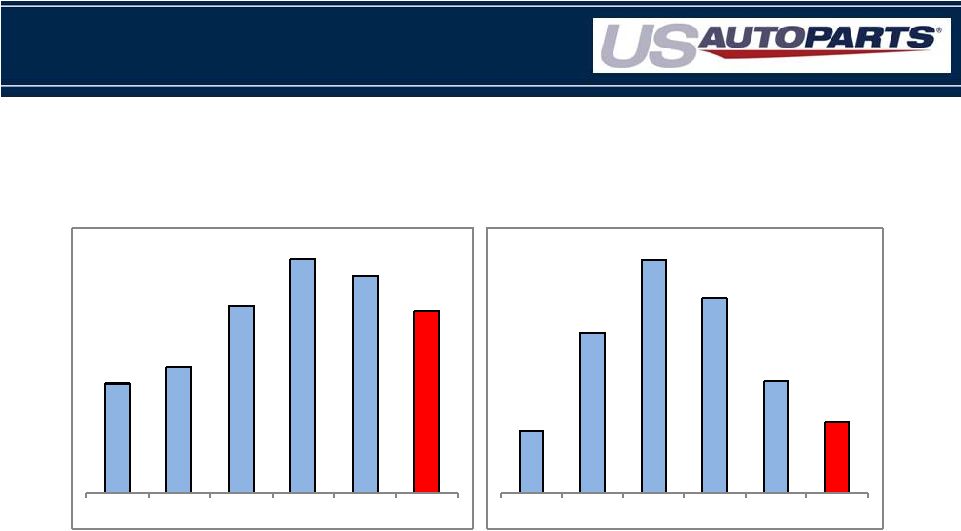

$153.4

$176.3

$262.3

$327.1

$304.0

$254.8

2008

2009

2010

2011

2012

2013

$5.2

$13.5

$19.5

$16.3

$9.4

$6.0

2008

2009

2010

2011

2012

2013

13

Sales & Adjusted EBITDA

Consolidated

Sales

1

Consolidated

Adjusted

EBITDA

2

($ In Millions)

($ In Millions)

Adj. EBITDA Margin

3%

5%

8%

7%

3%

2%

1.

JC Whitney was acquired in Aug 2010 adding revenue of $39.1M in 2010 and $83.4M in 2011. Amounts

not separately disclosed after 2011.

2.

Non-GAAP financial measure EBITDA consists of net income before (a) interest expense, net; (b)

income tax provisions; (c) amortization of intangible assets; (d) depreciation and

amortization. Adjusted EBITDA excludes restructuring costs and other one time charges of $0.4M,

$5.8M, $8.0M, $0.7M and $0.8M in 2009, 2010, 2011, 2012 and 2013, respectively, stock based

compensation of $2.9M, $3.3M, $2.7M, $2.6M, $1.7M and $1.3M in 2008, 2009, 2010, 2011, 2012 and 2013 respectively. There were no restructuring or other one time

charges in 2008.

|

Recent Revenue Trends

Completed the retirement of a number of websites by the end of 2Q ‘13

14 |

Adjusted EBITDA

(Non-GAAP

Financial Measure – in thousands

)

15

Thirteen Weeks Ended

Fifty-Two Weeks Ended

December 28

December 29

December 28

December 29

2013

2012

2013

2012

Net loss

(1,325)

$

(30,783)

$

(15,634)

$

(35,978)

$

Interest expense, net

276

274

972

774

Income tax provision

(48)

(1,230)

43

(937)

Amortization of intangible assets

82

177

381

1,189

Depreciation and amortization expense

2,439

3,671

12,175

15,204

EBITDA

1,424

(27,891)

(2,063)

(19,748)

Impairment loss on goodwill

-

18,854

-

18,854

Impairment loss on property and equipment

-

1,960

4,832

1,960

Impairment loss on intangible assets

-

5,613

1,245

5,613

Shared-based compensation expense

198

265

1,263

1,673

Loss on debt extinguishment

-

-

-

360

Legal costs related to intellectual property

-

67

-

67

Restructuring costs

-

-

723

640

Adjusted EBITDA

1,622

$

(1,132)

$

6,000

$

9,419

$

|

Consolidated Statements of Comprehensive Operations

(Unaudited, in Thousands, Except Per Share Data)

16

Thirteen Weeks Ended

Fifty-two Weeks Ended

December 28

December 29

December 28

December 29

2013

2012

2013

2012

Net sales

59,735

$

62,848

$

254,753

$

304,017

$

Cost of sales

(1)

42,260

45,072

180,620

212,379

Gross profit

17,475

17,776

74,133

91,638

Operating expenses:

Marketing

9,284

12,079

41,045

51,416

General and administrative

3,941

4,347

17,567

19,857

Fulfillment

4,112

5,023

18,702

22,265

Technology

1,093

1,448

5,128

6,274

Amortization of intangible

assets 82

177

381

1,189

Impairment loss on

goodwill -

18,854

-

18,854

Impairment loss on property and

equipment -

1,960

4,832

1,960

Impairment loss on

intangible assets -

5,613

1,245

5,613

Total operating expenses 18,512

49,501

88,900

127,428

Loss from operations

(1,037)

(31,725)

(14,767)

(35,790)

Other income (expense):

Other income (expense), net

(66)

(14)

148

20

Interest expense

(270)

(274)

(972)

(785)

Loss on debt

extinguishment -

-

-

(360)

Total other expense,

net (336)

(288)

(824)

(1,125)

Loss before income tax provision

(1,373)

(32,013)

(15,591)

(36,915)

Income tax provision

(48)

(1,230)

43

(937)

Net loss

(1,325)

(30,783)

(15,634)

(35,978)

Other comprehensive income, net of tax:

Foreign currency translation adjustments

24

(4)

55

31

Unrealized gains on investments

3

(4)

7

26

Total other comprehensive

income 27

(8)

62

57

Comprehensive

loss (1,298)

$

(30,791)

$

(15,572)

$

(35,921)

$

Basic and diluted net loss per share

(0.04)

$

(0.99)

$

(0.48)

$

(1.17)

$

Shares used in computation of basic and

diluted net loss per share

33,308

31,128

32,697

30,818

(1)

Excludes depreciation and amortization expense which is included in

marketing, general and administrative and fulfillment expense. |

Consolidated Balance Sheets

(In Thousands, Except Par and Per Share Liquidation Value)

17

December 28

December 29

ASSETS

2013

2012

Current assets:

Cash and cash equivalents

818

$

1,030

$

Short-term investments

47

110

Accounts

receivable,

net

of

allowances

of

$213

and

$221

at December 28, 2013 and December 29, 2012, respectively

5,029

7,431

Inventory

36,986

42,727

Deferred income taxes

-

39

Other current assets

3,234

4,176

Total current assets

46,114

55,513

Property and equipment, net

19,663

28,559

Intangible assets, net

1,601

3,227

Other non-current assets

1,804

1,578

Total assets

69,182

$

88,877

$

LIABILITIES AND

STOCKHOLDERS' EQUITY Current liabilities:

Accounts payable

19,669

$

28,025

$

Accrued

expenses 5,959

10,485

Revolving loan payable

6,774

16,222

Current portion of capital leases payable

269

70

Other current liabilities

3,682

4,738

Total current liabilities

36,353

59,540

Capital leases payable, net of current portion

9,502

70

Deferred income taxes

335

314

Other non-current liabilities

2,126

1,309

Total liabilities

48,316

61,233

Commitments and contingencies

Stockholders' equity:

Series A convertible preferred stock, $0.001 par value; $1.45

per share liquidation value or aggregate of $6,017; 4,150

shares authorized; 4,150 and 0 shares issued and outstanding

at December 28, 2013 and December 29, 2012, respectively

4

-

Common stock, $0.001 par value; 100,000 shares authorized;

33,352 shares and 31,128 shares issued and outstanding

at December 28, 2013 and December 29, 2012, respectively

33

31

Additional paid-in capital

168,693

159,781

Common stock dividend distributable

60

-

Accumulated other comprehensive income

446

384

Accumulated deficit

(148,370)

(132,552)

Total stockholders' equity

20,866

27,644

Total liabilities and equity

69,182

$

88,877

$

|

Thank You

18 |