Attached files

| file | filename |

|---|---|

| EX-10.17 - AMENDMENT NO 3 TO HAGEN SAVILLE EMPLOYMENT AGREEMENT - MCG CAPITAL CORP | ex-1017amendmentno3saville.htm |

| EX-10.5 - BFP POTOMAC TOWERS LEASE - MCG CAPITAL CORP | ex-105leasemcgcapitalbfppo.htm |

| EX-10.20 - KENNEDY SEVERANCE AGREEMENT - MCG CAPITAL CORP | ex-1020kennedyseveranceagr.htm |

| EX-21 - SUBSIDIARIES - MCG CAPITAL CORP | ex-21123113subsidiaries.htm |

| EX-32.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO 18 U.S.C - MCG CAPITAL CORP | ex-321123113.htm |

| EX-10.19 - AMENDMENT NO 1 TO REICHERT SEVERANCE AGREEMENT - MCG CAPITAL CORP | ex-1019amendmentno1reichert.htm |

| EX-31.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO RULES 13A-14(A) - MCG CAPITAL CORP | ex-311123113.htm |

| EX-23.1 - CONSENT OF ERNST & YOUNG LLP - MCG CAPITAL CORP | ex-231123113.htm |

| EX-32.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO 18 U.S.C - MCG CAPITAL CORP | ex-322123113.htm |

| EX-31.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO RULES 13A-14(A) - MCG CAPITAL CORP | ex-312123113.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2013

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______ to ______

___________________

Commission file number 0-33377

MCG CAPITAL CORPORATION

(Exact name of registrant as specified in its charter)

Delaware | 54-1889518 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

1001 19th Street North, 10th Floor, Arlington, VA | 22209 | |

(Address of principal executive offices) | (Zip Code) | |

(703) 247-7500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: | ||

Title of each class | Name of each exchange on which registered | |

Common Stock, par value $0.01 per share | The NASDAQ Global Select Market | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer x |

Non-accelerated filer o | Smaller reporting company o |

(Do not check if a smaller reporting company) | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the Registrant’s voting shares of common stock held by non-affiliates of the Registrant on June 30, 2013, was $356,905,163, based on $5.21 per share, the last reported sale price of the shares of common stock on the NASDAQ Global Select Market. For purposes of this computation, shares held by certain stockholders and by directors and executive officers of the Registrant have been excluded. Such exclusion of shares held by such persons is not intended, nor shall it be deemed, to be an admission that such persons are affiliates of the Registrant. There were 70,510,441 shares of the Registrant’s common stock outstanding as of February 21, 2014.

Documents Incorporated by Reference

Portions of the Registrant’s definitive Proxy Statement relating to its 2014 Annual Meeting of Stockholders, to be filed pursuant to Regulation 14A with the Securities and Exchange Commission, are incorporated by reference into Part III of this Annual Report on Form 10-K as indicated herein.

TABLE OF CONTENTS

PART I | ||

Item 1. | Business | |

Item 1A. | Risk Factors | |

Item 1B. | Unresolved Staff Comments | |

Item 2. | Properties | |

Item 3. | Legal Proceedings | |

Item 4. | Mine Safety Disclosures | |

PART II | ||

Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

Item 6. | Selected Consolidated Financial Data | |

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | |

Item 8. | Financial Statements and Supplementary Data | |

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

Item 9A. | Controls and Procedures | |

Item 9B. | Other Information | |

PART III | ||

Item 10. | Directors, Executive Officers and Corporate Governance | |

Item 11. | Executive Compensation | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

Item 14. | Principal Accountant Fees and Services | |

PART IV | ||

Item 15. | Exhibits and Financial Statement Schedules | |

SIGNATURES | ||

PART I

ITEM 1. | BUSINESS |

General

We are a solutions-focused commercial finance company that provides capital and advisory services to lower middle-market companies throughout the United States. Generally, our portfolio companies use our capital investment to finance acquisitions, recapitalizations, buyouts, organic growth, working capital and other general corporate purposes.

We are an internally managed, non-diversified, closed-end investment company that has elected to be regulated as a business development company, or BDC, under the Investment Company Act of 1940, as amended, or the 1940 Act. As a BDC we must meet various regulatory tests, which include investing at least 70% of our total assets in private or thinly traded public U.S.-based companies and limitations on our ability to incur indebtedness unless immediately after such borrowing we have an asset coverage for total borrowings (excluding SBIC debt) of at least 200% (i.e., the amount of debt generally may not exceed 50% of the value of our assets).

In addition, we have elected to be treated for federal income tax purposes as a regulated investment company, or RIC, under Subchapter M of the Internal Revenue Code. In order to continue to qualify as a RIC for federal income tax purposes and obtain favorable RIC tax treatment, we must meet certain requirements, including certain minimum distribution requirements. If we satisfy these requirements, we generally will not have to pay corporate-level taxes on any income we distribute to our stockholders as distributions, allowing us to substantially reduce or eliminate our corporate-level tax liability. From time to time, our wholly owned subsidiaries may execute transactions that trigger corporate-level tax liabilities. In such cases, we recognize a tax provision in the period when it becomes more likely than not that the taxable event will occur.

Corporate Structure

We make a portion of our investments in qualifying small businesses through Solutions Capital I, L.P., or Solutions Capital, our wholly owned subsidiary licensed by the United States Small Business Administration, or the SBA, to operate as a Small Business Investment Company, or SBIC, under the Small Business Investment Act of 1958, as amended, or the SBIC Act. As an SBIC, Solutions Capital is subject to a variety of regulations concerning, among other things, the size and nature of the companies in which it may invest and the structure of those investments.

We also make investments through other wholly owned subsidiaries, all of which are structured as Delaware corporations and limited liability companies, to hold the assets of one or more of our portfolio companies. Some of these subsidiaries in turn have wholly owned subsidiaries, all of which are Delaware corporations that hold the assets of certain of our portfolio companies.

Company Background

We were incorporated in Delaware in 1998. On March 18, 1998, we changed our name from MCG, Inc. to MCG Credit Corporation and, on June 14, 2001, to MCG Capital Corporation. Our principal executive offices are located at 1001 19th Street North, 10th Floor, Arlington, VA 22209 and our telephone number is (703) 247-7500.

In this Annual Report on Form 10-K, the terms “Company,” “MCG,” “we,” “us” and “our” refer to MCG Capital Corporation and its wholly owned subsidiaries (including its affiliated securitization trust) unless the context otherwise requires.

We are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and, accordingly, file reports, proxy statements and other information with the Securities Exchange Commission, or the SEC. Such reports, proxy statements and other information can be read and copied at the public reference facilities maintained by the SEC at the Public Reference Room, 100 F Street, N.E., Washington, D.C. 20549. Information regarding the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains a web site (http://www.sec.gov) that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

Our Internet address is www.mcgcapital.com. We are not including the information contained on our website as a part of, or incorporating it by reference into, this Annual Report on Form 10-K. We make available free of charge on our website our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC.

1

Our logo, trademarks and service marks are the property of MCG. Other trademarks or service marks appearing in this Annual Report on Form 10-K are the property of their respective holders.

Significant Developments in 2013

• | Originations and Advances — For the three and twelve month periods ended December 31, 2013, we made $37.1 million and $128.1 million, respectively, in originations and advances to new and existing portfolio companies. |

• | Loan Monetizations — For the three and twelve month periods ended December 31, 2013, we received $37.0 million and $199.4 million, respectively, in loan payoffs and amortization payments. |

• | Equity Monetizations and Realizations — For the three and twelve month periods ended December 31, 2013, we received $2.6 million and $10.7 million, respectively, in proceeds from the sale of equity investments, principally the sale of securities in each of Miles Media Group, LLC, NDSSI Holdings, LLC and Jenzabar, Inc. |

• | Loans on Non-Accrual — As of December 31, 2013, loans on non-accrual were $21.4 million at cost (6.1% of the total loan portfolio), and $4.5 million at fair value (1.3% of the total loan portfolio). On December 15, 2013, Color Star Growers of Colorado, Inc., or Color Star, filed for voluntary relief under Chapter 11 of Title 11 of the United States Code. In the quarter ended December 31, 2013, we realized a $13.5 million loss on our subordinated loan to Color Star. |

• | Operating Costs — For the twelve month period ended December 31, 2013, our total operating costs, excluding interest expense, were $11.5 million, or 2.2% of total assets of $514.0 million. During this same period, we incurred severance costs of $0.8 million, offset by the reversal of $0.3 million of amortization expense associated with the forfeiture of restricted stock that we included in total operating costs. |

• | Reduced Leverage — For the twelve month period ended December 31, 2013, we reduced our outstanding borrowings under our MCG Commercial Loan Trust 2006-1, or 2006-1 Trust, by $72.9 million, reducing our borrowings under our 2006-1 Trust from $98.1 million to $25.2 million as of December 31, 2013. On January 21, 2014, we repaid and terminated our 2006-1 Trust. |

• | Open-Market Purchases of Our Stock — For the three and twelve month periods ended December 31, 2013, we repurchased 512,100 and 1,016,739 shares of our common stock at weighted average purchase prices of $4.73 and $4.62, respectively. We acquired these shares from sellers in open market transactions. We retire these shares upon settlement, thereby reducing the number of shares issued and outstanding. |

• | Second SBIC License — On November 8, 2013, we withdrew our application for a second license from the SBA to operate an additional subsidiary as an SBIC. We elected to withdraw our application for a second license until such time as the SBA has an opportunity to further evaluate organizational results in connection with our restructuring efforts and our position in relation to other specialty finance companies. The SBA indicated that we may petition the SBA for permission to re-file our application at a future date. The withdrawal of the license application for the second SBIC license does not impact Solutions Capital, its existing license or operations. |

Outlook

In 2013, we successfully improved our operating efficiency by reducing operating costs, excluding interest expense, as a percentage of total assets from 3.6% in 2011 to 2.2%, which we believe places us in the top quartile of all BDCs. In 2014, we anticipate that our fixed-cost cash operating expenses, excluding interest and variable incentive compensation, to be approximately $10 million. In addition, we anticipate incurring non-recurring general and administrative expenses of $1.0-2.0 million primarily related to Color Star litigation and recruitment expenses.

During 2014, we plan to reorganize our Asset Management department to more effectively address the markets we serve and to better leverage the vertical market industry expertise we possess in healthcare, software, information services, for-profit education and consumer products, among others. We expect that the majority of our new business will continue to come from private equity sponsors operating in the lower middle-market with loan proceeds used in connection with M&A, business expansion and recapitalization transactions. We will also continue to provide unitranche, second lien and subordinated debt solutions and, to a small degree, equity co-investment.

We believe that current market conditions in our primary lending markets are consistent with the peak of a credit cycle. The current supply of debt capital exceeds the demand by issuers in our markets, resulting in lower pricing and weaker

2

contractual protections. A noteworthy development is that, in our view, many issuers in the lower middle-market can currently obtain financing on pricing and terms comparable to larger companies. As a result of these market conditions, we intend to redeploy our excess liquidity in a cautious and deliberate manner and we expect to generate, net operating income, or NOI of 25-30 cents per share for 2014. Based on our assumptions of normalized expenses and 100 basis points of yield compression, fully-deployed we expect to generate 11% yield on $470 million of total investments and to generate annual NOI of approximately 40-45 cents per share before leverage, or approximately 10-12 cents per share on a quarterly basis. Fully-deployed, we estimate that a 100 basis point change in yield on our portfolio has an approximately 7 cent per share impact on NOI.

During the two year period ending December 31, 2013, we monetized $622 million of our investment portfolio, $155 million more than our forecast resulting in lower overall earning assets and associated revenue and earnings for that period. We expect repayments of approximately $100-125 million in 2014; however, depending upon market conditions, it is possible that monetization levels could run meaningfully higher. Depending on the market, during 2014 and 2015, we expect to originate and advance approximately $100-150 million annually in new investments, which would result in full deployment of our balance sheet in the next six to eight quarters at the earliest.

On January 21, 2014, we repaid the remaining indebtedness associated with our 2006-1 Trust, thus eliminating all funded indebtedness associated with our BDC asset coverage test. Given our equity capital base of $334 million we believe that we have substantial leverage capacity available to support asset acquisition above our cash balances and provide associated incremental earnings power to the extent leverage is available.

On February 28, 2014, our board of directors approved an increase in our current stock repurchase program from $25 million to $35 million and we expect to repurchase stock at share price levels that we believe are accretive to our stockholders.

Also on February 28, 2014, our board of directors declared a 12.5 cent per share distribution to stockholders of record on March 14, 2014 and payable on March 28, 2014. We expect that our board of directors will declare distributions on a quarterly basis at a level approximating our quarterly NOI. Due to the continuing high velocity of our loan portfolio and challenging market conditions generally, subject to review and approval by our board of directors, we anticipate lowering our quarterly distributions to 7 cents per share at least for the remainder of 2014.

MCG’s Investment Portfolio

As of December 31, 2013, the majority of our investment portfolio is loans to lower middle-market companies that generate annual revenue of less than $50 million and earnings before interest, taxes, depreciation and amortization, or EBITDA, in the range of $3-$15 million. Generally, our portfolio companies use our capital investments to finance acquisitions, recapitalizations and buyouts, as well as for organic growth and working capital. We identify and source new portfolio companies through multiple channels, including private equity sponsors, investment bankers, brokers, fund-less sponsors, institutional syndication partners, owner operators, and other club lenders that facilitate peer-to-peer loans. We generally invest in some combination of senior debt, second-lien debt, secured and unsecured subordinated debt and equity.

3

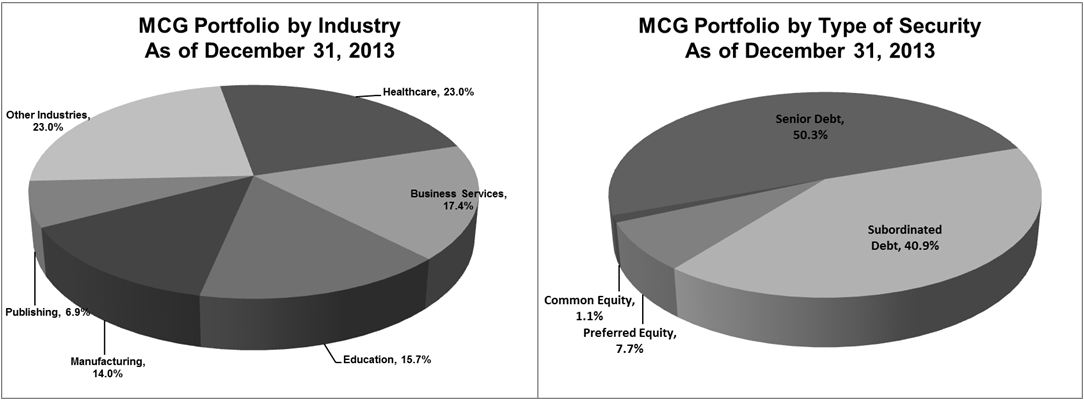

As of December 31, 2013, we had debt and equity investments in 34 portfolio companies with a combined fair value of $368.9 million. As shown in the following chart, over 90% of the fair value of our portfolio as of December 31, 2013 was invested in senior and subordinated debt, while the remainder was invested in preferred and common equity securities. Our diversified investment portfolio spans 15 industries. We have concentrations in excess of 10% of the fair value of our total portfolio in the following four industries: Healthcare (23.0%), Business Services (17.4%), Education (15.7%) and Manufacturing (14.0%). Approximately 98% of our portfolio at fair value is concentrated in ten industries. Since we target investments in industries in which we have expertise and, given the size of our investment base, we anticipate that our portfolio will remain concentrated in fewer than ten industries. See Portfolio Composition and Investment Activity in our Management’s Discussion and Analysis of Financial Condition and Results of Operations for additional detail about our investment portfolio, including a detailed listing of the industries represented in our investment portfolio.

Most of the loans in our portfolio were originated directly with our portfolio companies; however, we have also participated in loan syndications or other transactions, which are often referred to as "passive participations" which make up less than 5% of our portfolio at value as of December 31, 2013.

Our debt instruments bear contractual interest rates ranging from 2.5% to 15.5%, a portion of which may be deferred. As of December 31, 2013, approximately 73.3% of the fair value of our loan portfolio had variable interest rates, based on either the London Interbank Offer Rate, or LIBOR, or the prime rate, and 26.7% of the fair value of our loan portfolio had fixed interest rates. As of December 31, 2013, approximately 60.2% of the fair value of our loan portfolio had LIBOR floors between 1.0% and 3.0% on a LIBOR-based index or prime floors between 2.50% and 6.0%. At origination, our loans generally have four- to six-year stated maturities. Borrowers typically pay an origination fee based on a percent of the total commitment and a fee on undrawn commitments.

From time to time, we make equity investments in companies in which we have also made debt investments. Our equity investments include preferred stock, common stock and warrants and, in many cases, board observation rights. We may invest across the capital structure of our portfolio companies using a combination of debt and equity investments to meet our portfolio companies’ needs and achieve favorable risk-adjusted returns.

4

The following table summarizes the fair value and revenue contributions of our ten largest investments. As of December 31, 2013, these ten investments comprised 54.3% of the fair value of our portfolio and contributed 42.1% of our total revenues during 2013. We originated approximately 12% of the fair value of our top ten largest portfolio investments in the fourth quarter of 2013.

(dollars in thousands) | As of December 31, 2013 | Year ended December 31, 2013 | |||||||||

Company | Industry | Fair Value | % of Portfolio | Revenues | % of Total Revenues | ||||||

RadioPharmacy Investors, LLC | Healthcare | $ | 31,656 | 8.6 | % | $ | 4,474 | 8.9 | % | ||

G&L Investment Holdings, LLC(1) | Insurance | 23,619 | 6.4 | 3,129 | 6.2 | ||||||

Cruz Bay Publishing, Inc. | Publishing | 21,483 | 5.8 | 2,624 | 5.2 | ||||||

C7 Data Centers, Inc. | Business Services | 20,574 | 5.6 | 1,466 | 2.9 | ||||||

Education Management, Inc. | Education | 19,791 | 5.4 | 2,562 | 5.1 | ||||||

TCFI CP LLC | Manufacturing | 19,667 | 5.3 | 372 | 0.7 | ||||||

Miles Media Group, LLC | Business Services | 18,913 | 5.1 | 2,380 | 4.7 | ||||||

IDOC, LLC | Healthcare | 16,427 | 4.4 | 1,510 | 3.0 | ||||||

SC Academy Holdings, Inc. | Education | 14,577 | 4.0 | 1,982 | 3.9 | ||||||

Ted's Café Escondido Holdings, Inc. | Restaurants | 13,691 | 3.7 | 761 | 1.5 | ||||||

Total—ten largest investments | 200,398 | 54.3 | % | 21,260 | 42.1 | % | |||||

Other portfolio companies | 168,475 | 45.7 | % | 29,225 | 57.9 | % | |||||

Total investment portfolio | $ | 368,873 | 100.0 | % | $ | 50,485 | 100.0 | % | |||

___________________________________________

(1) | In February 2014, we exited our investment in G&L Investment Holdings, LLC |

As of December 31, 2013, our control companies comprised 11.9% of the fair value of our portfolio and contributed 10.3% of our total revenues during 2013.

Competition

We compete with many types of investors for the portfolio companies in which we invest, including public and private funds (including other BDCs and SBICs), commercial and investment banks, commercial financing companies and, to the extent they provide an alternative form of financing, private equity funds or hedge funds. Some of our existing and potential competitors are substantially larger and have considerably greater financial, technical and marketing resources than we do. Some may also have higher risk tolerances or different risk assessments, allowing them to consider a wider variety of investments and establish more relationships than we can.

The competitive pressures we face require our management team to develop and maintain strong relationships with intermediaries, private equity funds, financial institutions, investment bankers, commercial bankers, financial advisors, attorneys, accountants, consultants and other individuals within our network in order to keep apprised of potential investment opportunities.

Winning attractive investment opportunities requires that we offer terms and conditions on a par with or better than our peers. While we do not seek to compete primarily based on the interest rates we offer, we may lose investment opportunities if we do not match our competitors' pricing, terms and structure. We may be precluded from taking advantage of attractive investment opportunities from time to time as a result of an inability to meet market terms.

Life Cycle of Debt and Equity Originations

The key aspects of our portfolio origination, servicing and monitoring process are set forth below. Generally, we intend to keep the amount of our investment in any one company at or below $15 million, which we may accomplish by selling a portion of our initial investment to another investor post-close. We generally make loans with four- to six-year stated maturities. We believe the market-average hold period of a loan is approximately three years, although that figure has recently declined. Our equity investments generally do not have maturity dates.

INVESTMENT OBJECTIVE AND STRATEGIES

Our investment objective is to achieve attractive returns by generating current income and capital gains on our investments. We seek to increase our earnings and NAV by investing primarily in debt securities of lower middle-market companies. On a more limited basis, we make equity investments, which we anticipate limiting to approximately

5

10% of the fair value of our investments. We intend to earn interest, dividends and fees on our investments and we may report unrealized appreciation and depreciation as the fair value of our investments periodically increases or decreases. We realize capital gains or losses when the investment is eventually monetized.

The cost basis of our investments include unamortized original issue discount, premiums and fees, as well as paid-in-kind interest and dividends that are generally due at maturity or upon our exit from the investment.

When we originate debt and equity investments, we strive to achieve favorable risk-adjusted rates of return in the form of current income and capital gains, while maintaining credit and investment quality in our portfolio. Before making investments, we apply well established credit processes to assess investment risk and we structure and price our investments accordingly. We have developed proprietary analytics, data and knowledge to support our business activities. We designed our investment process to achieve the following strategic objectives:

• | generate favorable risk-adjusted rates of return by delivering capital and strategic insight to increase our portfolio companies’ enterprise value; |

• | maintain sound credit and investment discipline and pricing practices, regardless of market conditions, to avoid adverse investment selection; and |

• | manage risk by utilizing an integrated team approach to business development, underwriting and investment servicing. |

We maintain a flexible approach to funding that permits us to adjust price, maturity and other transaction terms to accommodate the needs of our portfolio companies.

ORGANIZATION OF MCG’S INVESTMENT PROFESSIONALS

Our organization includes experienced professionals with the ability to originate, underwrite, finance, syndicate, monitor and exit investments that generate attractive returns. The following bullets describe the key functional teams that are responsible for our investment processes:

• | Asset Management—Our Asset Management department is responsible for identifying and performing a financial and risk analysis of potential investment opportunities. This department also underwrites and manages our investment portfolio, and leads any work-out or restructuring that may occur from time to time. After an investment is approved and funded, individual deal teams, comprised generally of a Managing Director or Vice President, an analyst and an in-house attorney, have continuing ongoing responsibility for monitoring the performance of our investments. |

• | Credit Committee—Prospective investments are presented to MCG's credit committee for review and approval prior to issuing a term sheet. Final approval by the credit committee generally occurs after the deal team has substantially completed the underwriting process. The credit committee includes our Chief Executive Officer, Chief Financial Officer, Head of Asset Management and General Counsel. Our board of directors has delegated authority to the credit committee to (i) originate, underwrite and fund any non-control, non-distressed investment of $15 million or less provided that the equity component does not exceed $3 million, (ii) originate any distressed investment of $5 million or less and (iii) increase any existing investment previously approved by the Company's investment and valuation committee up to a certain over-line or established amount. As a matter of practice, our board of directors is invited to participate at every credit committee meeting and in the review and approval of all investments, irrespective of investment size. |

• | Investment and Valuation Committee of the Board of Directors—The investment and valuation committee reviews and approves all investments over $15 million and has the discretion to review and approve other investments. Subsequent to the review and funding of an investment, the investment and valuation committee makes recommendations that are used by our board of directors for its quarterly determination of the fair value of our investment portfolio. |

The following sections provide additional information on how we conduct the investment process. In addition to the teams described above, we also have a group of professionals that provide accounting, finance, human resources, investor relations, legal, and other services that support our investment professionals and other corporate, compliance and governance functions.

6

BUSINESS DEVELOPMENT

MCG and its predecessors have been active investors in lower middle-market companies since 1990. We believe our experience in lower middle-market investing is a meaningful competitive advantage that we use to operate our business. Our senior investment professionals and members of our credit committee have, on-average, each made over $500 million of investments throughout their careers, principally in lower middle-market companies and in industries that we target, such as healthcare, business services, education, technology, software, information services and consumer directed businesses.

Our deal teams identify and source new investments through multiple channels, including private equity sponsors, investment bankers, brokers, fund-less sponsors, institutional syndication partners, other club lenders and owner-operators. The deal teams also market to prospective portfolio companies identified through past relationships with executives, information gathered through proprietary and public research and relationships with investment bankers, accountants, lawyers and other professionals.

Once we identify a prospective portfolio company, we review its financial reports, business plan, corporate activities and other relevant information gathered from third-party databases, industry reports and publications. We focus on a company’s fundamental performance against industry conditions and operational benchmarks, and evaluate acceptable risks and returns. We work with our current and prospective portfolio companies to understand their business, as well as the costs and benefits of their corporate development initiatives, opportunities and competition. Our detailed analysis allows us to support our portfolio companies’ corporate development decisions, even in some cases where short-term financial ratios or other metrics may decline temporarily.

RISK ANALYSIS

After identifying a prospective investment, we review the company’s operating history, executive leadership team, opportunities and the market for the company's products and services during the life of our investment, as well as the potential risks and threats to the business or the markets in which it competes. As early as possible in the process, we generally conduct on-site meetings with key executives to learn more about the investment directly from the company's leadership team and tour the company's key facilities or operating locations.

To assess the validity and stability of the company's historical and projected financial performance we often, either ourselves or through a third-party firm, perform a review of quality of earnings. For select transactions, we may engage or rely on the research of industry specific due diligence firms that provide market research or insights that we judge as prudent or helpful in in the underwriting process.

Based on our experience, we also look at the company's capitalization, proposed sources and uses of proceeds, structural considerations of various securities in the capital structure, leverage, expected cash generation, affirmative and negative covenants, methods for repayment or exit from the investment and other important considerations specific to the investment.

In particular, we analyze certain key risks in light of our underwriting criteria, including financial characteristics and portfolio-specific risk that might arise from the new investment, including, but not limited to, the following:

• | Industry Risks—maturity, cyclicality and seasonality associated with the industries in which we invest, as well as the proportion of our portfolio that is invested in specific industries and individual portfolio companies; |

• | Competitive Risks—strengths and weaknesses of the prospective portfolio company relative to their competitors’ pricing, product quality, customer loyalty, substitution and switching costs, brand positioning and capitalization. We also assess the defensibility of a prospect’s market position and its opportunity for increasing market share; |

• | Management Risks—track records, industry experience, turnover in leadership, concentration of knowledge, the prospective portfolio company’s business plan and management incentives; |

• | Regulatory Risks—industry specific regulation and regulation reform (e.g., healthcare reform, increased regulatory oversight, government reimbursement of for-profit schools, etc.), and economic or macro issues that may affect an investment (e.g., cost of utilities or access to power at historical rates in certain regions, access to nuclear materials for medical imaging, etc.), as well as regulations that may change the incentives of partners or investors in the investment (e.g., tax reform that may impact private equity funds or hedge funds, regulations of commercial banks, and potential reforms of BDCs or SBIC regulations); |

• | Customer Concentration and Market Risks—sustainability, stability and opportunities for the growth of the prospective portfolio company's customer base, including the number and size of its customers, attrition rates and dependence on one or a limited number of customers; and |

7

• | Technology Risks—impact of technological advances in the industries and portfolio companies in which we may invest. |

In addition, we evaluate industry-specific comparisons, such as cash flow margins, product and cash flow diversification, revenue growth rates, cost structure and other operating benchmarks that are derived from historical and projected financial statements. Qualitative attributes we evaluate may include management skill and depth, industry risk, substitution risk, sensitivity to economic cycles, cyclicality, geographic diversification, facilities infrastructure, administration requirements and product quality and ranking.

We have developed a series of valuation techniques to assist us in determining the risk of a potential investment and quantifying its underlying value. Analyses of comparative public and private market transactions and other data form the basis of our enterprise valuations, along with current and projected market conditions. We also look to comparable public companies to benchmark the value of the proposed investment using public market data. Using these methods provides multiple views of the value of the enterprise allowing us to calculate certain metrics used in both risk assessment and product pricing, such as loan-to-value ratios for our debt investments.

UNDERWRITING AND RISK MANAGEMENT

We initiate our underwriting process in tandem with the business development process, focusing on investment risk analysis. We perform standard due diligence on a prospective portfolio company’s financial performance, as well as customized analyses of its operations, systems, accounting policies, human resources and competitive, legal and regulatory environments.

In addition to gaining an in-depth understanding of a prospective portfolio company, our research and due diligence process evaluates industry-wide operational, strategic and valuation issues. We also examine emerging trends and competitive threats to the portfolio company, as well as the industry in which it operates. Portfolio companies may later draw on our valuable knowledge and insight obtained through our research to refine their strategic plans, identify acquisition opportunities and set appropriate financial and operational goals.

When presenting a prospective investment to our credit committee for approval, the deal team delivers a detailed investment memorandum. Should the dollar amount of the proposed investment exceed certain pre-defined thresholds, or include a significant investment in equity, the investment memorandum is also submitted to the investment and valuation committee of our board of directors for review and approval. The investment memorandum generally consists of the following:

• | a transaction overview, including a description of the business and the investment opportunity; |

• | transaction rationale, underwriting considerations and an assessment of risks and mitigants; |

• | historical financial analyses, projections and scenario modeling; |

• | a service or product overview, customer and industry analyses, operational and regulatory analyses; |

• | an assessment of the company's enterprise valuation relative to comparable public and private companies; |

• | a description of the capital structure and the investment risk and return characteristics; and |

• | a review of insights or reports obtained from third-party experts or due diligence firms. |

INVESTMENT STRUCTURE

We evaluate our portfolio companies’ needs to develop investment structures that meet their capital requirements and business plans while protecting our own capital, with an expectation toward generating risk-adjusted returns through current income on our loans and capital gains on our equity investments. We structure our debt investments to mitigate risk by requiring appropriate financial and collateral coverage thresholds. To create the most effective and responsive deal structures, we consider payment priority, collateral or asset value, and financial support from guarantors and other credit enhancements. Since our investments typically include cash-flow loans, rather than asset-backed loans, we factor the enterprise value of the prospective portfolio company’s assets into our credit decisions. For loans classified as senior secured, second-lien and subordinated secured, we receive a security interest in all or a portion of the portfolio companies’ tangible and intangible assets, entitling us to a preferred position relative to both unsecured creditors and more junior lenders on the proceeds of those assets in the event of liquidation. In addition, our loan documents generally include affirmative covenants that require our portfolio companies to provide periodic financial information, notification of material events and compliance with laws, as well as restrictive covenants that prevent the portfolio company from taking a range of significant actions, such as incurring additional indebtedness or making acquisitions. Financial covenants require the portfolio companies to maintain or achieve specified financial ratios, such as cash flow leverage, interest charge coverage, total charge coverage, and, in certain cases, meet specific operational benchmarks.

8

Our business strategy dictates that we generally invest in some combination of the following securities:

• | Senior Secured Debt—We provide cash flow based senior secured debt in the form of revolving credit facilities as well as amortizing term loans, bullet maturity term loans and uni-tranche loans that blend characteristics of both senior and subordinated financing. Senior secured debt ranks senior in priority of payment to other debt and equity, and benefits from a first priority security interest in the assets of the borrower that serve as collateral for the loan(s). As such, virtually all other creditors rank junior to senior secured debt in the event of insolvency. Some of our borrowers grant a first lien on working capital collateral (i.e., receivables) to asset-based lenders that is outside of our collateral pool. Assuming we have a first lien on all other collateral, in such cases we would still classify our security as senior secured. Due to its lower risk profile and often more restrictive covenants as compared to other debt, senior secured debt generally earns a lower return. |

• | Second-Lien Debt—We, on occasion, provide second-lien term loans on a sole-source or participant basis where assets or enterprise-value based borrowing capacity is not readily available within typical senior debt leverage constraints. Second-lien debt ranks senior in priority of payment to subordinated debt, unsecured debt, select junior securities, and equity. While second lien debt benefits from a collateral interest in the assets of the borrower, its liens are subordinated to those of senior secured debt in a liquidation. As such, senior secured creditors rank ahead of second lien creditors in the event of insolvency with respect to pursuing remedies against the collateral of a portfolio company, and receiving the proceeds thereof. Due to its higher risk profile and often less restrictive covenants as compared to senior debt, second-lien debt generally earns a higher return than senior debt. We classify second-lien term loans as "Subordinated Secured" debt in our consolidated financial statements. |

• | Secured and Unsecured Subordinated Debt—We invest in secured and unsecured subordinated debt, which may be structured with a combination of current interest, deferred interest and equity-linked components. Payment of all subordinated debt, whether secured or unsecured, ranks behind payment of senior secured and second-lien debt. While the security interest of subordinated secured debt ranks behind that of the senior secured and second-lien debt, subordinated unsecured debt enjoys no security interest in the borrower's assets. In the event of insolvency, senior secured and second-lien creditors will be paid in full before the subordinated secured and subordinated unsecured creditors. Due to its higher risk profile and often less restrictive covenants as compared to other types of loans, subordinated debt generally earns a higher return than other debt. |

• | Equity—We may from time-to-time invest in minority equity positions with private equity partners or on our own. In addition, we may receive warrants to purchase preferred or common stock of a portfolio company that are related to our debt investments in such portfolio company. Preferred stock ranks senior to common stock, and often carries the right to receive a preferential return upon the sale of the company. |

To protect our investments and maximize our returns, we negotiate carefully the structure of each debt and equity security in our investment portfolio, and may require board observation rights as part of our initial investment to keep abreast of company matters. Our loan and equity documentation generally includes terms governing interest rate, amortization, prepayment premiums, financial covenants, operating covenants, ownership and corporate governance parameters, dilution parameters, liquidation preferences, voting rights, and put or call rights. In some cases, our loan agreements also allow for interest rate increases and decreases to the extent the portfolio company's financial or operational performance varies materially from the portfolio company's business plan.

In addition to capital, we also offer managerial assistance to our portfolio companies. Typically, this assistance involves strategic advice, evaluation of business plans, financial modeling assistance and industry research and expertise. Providing assistance to our portfolio companies enables us to maximize our value proposition for our portfolio companies, which, in turn, helps maximize our investment returns.

INVESTMENT APPROVAL PROCESS

Our investment approval process begins with an initial screening of a business plan or financing solicitation by either a Managing Director or a Vice President, referred to as a deal sponsor, to assess eligibility, sector, risk profile, investment fit and expected returns. There is a weekly meeting at which all prospective investments are discussed. The Asset Management department prepares a pipeline report consisting of an internal summary of the opportunity, company materials and an investment structuring worksheet for review by the credit committee. Simultaneously, a non-binding indication of interest may also be executed in support of a private equity firm issuing a bid for the transaction. Deals are judged by, among other things, a prospect's revenue run rate, continuity of solid cash flow, percentage of recurring revenue, gross profit margin, bad debt as a percentage of revenue, customer renewal rate, the prospect's marketing niche, level of competition, customer base quality and concentration and strength of the management team.

9

The credit committee determines whether the investment should be pursued, giving consideration to the risk return profile, industry concentrations and general economic outlook for the sector in which the business operates. In these meetings the credit committee also offers the deal sponsor insight into key issues that must be resolved before a potential investment is funded. If the credit committee agrees to move forward with an investment, the terms are documented initially by a signed term sheet or letter of intent, as applicable, consistent with the pipeline report and committee clearance, and the deal proceeds to the documentation stage. The term sheet establishes the terms and conditions under which we propose to enter into a credit or investment relationship.

Generally, our underwriting process begins after the Asset Management team receives a signed term sheet or letter of intent. The assigned deal team is responsible for oversight and completion of comprehensive due diligence, and is expected to investigate and report on all critical aspects of the proposed investment. Our due diligence often includes review of financial statements, discussion with key members of management, review of material contracts, background checks, reviews of customer and vendor relationships, confirmation of historical results and assumptions underlying forecasted results. When necessary or advisable based on industry or the history of the prospect itself, third party diligence is conducted. The underwriting process includes legal and business due diligence and typically an on-site visit with the prospect company, including its management team and any other key employees.

Once the underwriting process is complete, the deal sponsor presents a credit approval memorandum, including detailed findings of the foregoing underwriting process, to the credit committee and, if required, the investment and valuation committee. If approved, the deal proceeds to final documentation and closure. All of our investments are approved by our credit committee. In addition, investments of over $15 million must also be approved by the investment and valuation committee of our board of directors.

INVESTMENT FUNDING

We fund our investments using cash from our balance sheet and some of the loans in turn are used as collateral in our secured debt facility. In 2013, our secured debt facilities included certain restrictions on the types of investments that could be used as collateral. See the Liquidity and Capital Resources-Borrowings section of our Management's Discussion and Analysis of Financial Condition and Results of Operations for additional information. As a BDC, we are also subject to certain restrictions on incurring debt. For example, we are not permitted to incur indebtedness unless immediately after such borrowing we meet a coverage ratio of total assets to total senior securities (which include all of our borrowings, excluding those made by our SBIC, and any preferred stock we have then issued) of at least 200%.

INVESTMENT MONITORING AND RESTRUCTURING

We monitor the status and financial performance of each company in our portfolio in order to evaluate overall portfolio quality and to facilitate quarterly valuations, which are approved by our board of directors. We are proactive in advising and communicating with companies that are underperforming and, in many instances, have added stricter covenant protection and rights over time. During the process of monitoring a loan in default, if required or necessary to protect our security interest, we will send a notice of non-compliance outlining the specific defaults that have occurred and preserving our contractual rights and remedies, followed by a review of the collateral, if any.

When our attempts to collect past due principal and/or interest on a loan are unsuccessful, we analyze the appropriate course of action. In some cases, we may consider restructuring the investment to better reflect the current financial performance of the portfolio company. We may need to extend liquidity to companies from time to time as part of a restructuring. Such a restructuring may, among other things, involve deferring principal and interest payments, adjusting interest rates or warrant positions, imposing additional fees, amending financial or operating covenants or converting debt to equity. In connection with a restructuring, we generally receive compensation from the portfolio company. When a restructuring is not an appropriate course of additional action, we generally pursue remedies available to us to minimize potential losses, including initiating foreclosure, liquidation proceedings or selling the loan.

When one of our loans becomes more than 90 days past due, or if we otherwise do not expect the portfolio company to be able to service its debt and other obligations, we will, as a general matter, place all or a portion of the loan on non-accrual status and cease recognizing interest income on that loan until all principal and interest has been brought current through payment or restructuring such that the interest income is deemed to be collectible. However, we may make exceptions to this policy if the loan has sufficient collateral value and is in the process of collection. If the fair value of a loan is below cost, we may cease recognizing paid-in-kind interest and/or the accretion of a discount on the debt investment until such time that the fair value equals or exceeds cost.

10

INVESTMENT POLICIES

Our investment policies provide that we will not:

• | act as an underwriter of securities of other issuers, except to the extent that we may be deemed an “underwriter” of securities (i) purchased by us that must be registered under the Securities Act of 1933, as amended, before they may be offered or sold to the public, or (ii) in connection with offerings of securities by our portfolio companies; |

• | sell securities short in an uncovered position; |

• | write or buy uncovered put or call options, except to the extent of options, warrants or conversion privileges in connection with our loans or other investments, and rights to require the issuers of such investments or their affiliates to repurchase them under certain circumstances; |

• | engage in the purchase or sale of commodities or commodity contracts, including futures contracts, except for the purpose of hedging in the ordinary course of business or where necessary in working out distressed loan or investment situations; or |

• | acquire more than 3% of the voting stock of, or invest more than 5% of our total assets in any securities issued by, any other investment company, except if we acquire them as part of a merger, consolidation or acquisition of assets or if they result from a sale of a portfolio company, or otherwise as permitted under the 1940 Act. |

All of the above policies and the investment and lending guidelines set by our board of directors or any committees, including our investment objective to achieve current income and capital gains, are not “fundamental” as defined under the 1940 Act. Therefore, our board may change them without notice to, or approval by, our stockholders. However, any change may require the consent of our lenders.

Other than the restrictions pertaining to the issuance of senior securities under the 1940 Act, the percentage restrictions on investments generally apply on the effective date of the transaction. A subsequent change in a percentage resulting from market fluctuations or any cause other than an action by us will not require us to dispose of portfolio securities or to take other action to satisfy the percentage restriction.

We intend to conduct our business so as to retain our status as a BDC. As such, we may not acquire any assets, other than non-investment assets necessary and appropriate to our operations as a BDC, if after giving effect to such acquisition the value of our “qualifying assets” is less than 70% of the value of our total assets.

Investment Adviser

We have no investment adviser and are internally managed by our executive officers under the supervision of the board of directors. Our investment decisions are made by our officers, directors and senior investment professionals who serve on our credit and investment and valuation committees. None of our executive officers or other employees has the unilateral authority to approve any investment.

Regulation

INVESTMENT COMPANY ACT OF 1940

As a BDC, we are regulated under the 1940 Act. The BDC structure provides stockholders the ability to retain the liquidity of a publicly traded stock, while sharing in the possible benefits, if any, of investing in primarily privately owned companies.

In part, the 1940 Act requires us to be organized in the United States for the purpose of investing in, or lending to, primarily private companies and making managerial assistance available to them. As a BDC we may use capital provided by public stockholders and from other sources to invest in long-term, private investments in businesses.

We may not, however, change the nature of our business so as to cease to be, or withdraw our election as, a BDC unless authorized by vote of a majority of our outstanding voting securities. The 1940 Act defines a majority of the outstanding voting securities as the lesser of:

i. | 67% or more of such company’s shares present at a meeting if more than 50% of the outstanding shares of such company are present or represented by proxy; or |

ii. | more than 50% of the outstanding shares of such company. |

We currently do not anticipate any substantial change in the nature of our business.

11

Qualifying Assets

A BDC must have been organized and have its principal place of business in the United States and must be operated for the purpose of making investments in the types of securities described in (1), (2) or (3) below. Thus, under the 1940 Act, we may not acquire any asset other than those of the type listed in Section 55(a) of the 1940 Act, which are referred to as qualifying assets, unless, at the time the acquisition is made, qualifying assets represent at least 70% of the company’s total assets. The principal categories of qualifying assets relevant to our business are the following:

1. | Securities purchased in transactions not involving any public offering from the issuer of such securities, which issuer (subject to certain limited exceptions): |

a. | is an eligible portfolio company, or from any person who is, or has been during the preceding 13 months, an affiliated person of an eligible portfolio company, or from any other person, subject to such rules as may be prescribed by the SEC. An eligible portfolio company is defined in the 1940 Act as any issuer that: |

i. | is organized under the laws of, and has its principal place of business in, the United States; |

ii. | is not an investment company (other than a small business investment company wholly owned by us) or a company that would be an investment company but for certain exclusions under the 1940 Act; and |

iii. | does not have any class of securities listed on a national securities exchange; |

b. | is a company that meets the requirements of (a)(i) and (ii) above, but is not an eligible portfolio company because it has issued a class of securities on a national securities exchange, if: |

i. | at the time of the purchase, we own at least 50% of the (x) greatest number of equity securities of such issuer and securities convertible into or exchangeable for such securities; and (y) the greatest amount of debt securities of such issuer, held by us at any point in time during the period when such issuer was an eligible portfolio company; and |

ii. | we are one of the 20 largest holders of record of such issuer’s outstanding voting securities; or |

c. | is a company that meets the requirements of (a)(i) and (ii) above, but is not an eligible portfolio company because it has issued a class of securities on a national securities exchange, if the aggregate market value of such company’s outstanding voting and non-voting common equity is less than $250.0 million. |

2. | Securities of any eligible portfolio company that we control. |

3. | Securities purchased in a private transaction from a U.S. issuer that is not an investment company or from an affiliated person of the issuer, or in transactions incident thereto, if the issuer is in bankruptcy and subject to reorganization or if the issuer, immediately prior to the purchase of its securities was unable to meet its obligations as they came due without material assistance other than conventional lending or financing arrangements. |

4. | Securities of an eligible portfolio company purchased from any person in a private transaction if there is no ready market for such securities and we already own 60% of the outstanding equity of the eligible portfolio company. |

5. | Securities received in exchange for or distributed on or with respect to securities described in (1) through (4) above, or pursuant to the exercise of warrants or rights relating to such securities. |

6. | Cash, cash items, U.S. Government securities or high-quality debt securities maturing in one year or less from the time of investment. |

Control, as defined by the 1940 Act, is presumed to exist where a BDC beneficially owns more than 25% of the outstanding voting securities of the portfolio company. For the foreseeable future, we do not expect to add new control positions to our portfolio.

Significant Managerial Assistance

In order to count portfolio securities as qualifying assets for the purpose of the 70% test discussed above, we must either control the issuer of the securities or offer to make available significant managerial assistance; except that, where we act together to purchase such securities in conjunction with one or more other persons, one of the other persons in the group may make available such managerial assistance. Making available significant managerial assistance means, among other things, to offer to provide and, if accepted, provide significant guidance and counsel

12

concerning the management, operations or business objectives and policies of a portfolio company through monitoring of its operations, selective participation in board and management meetings, consulting with and advising its officers and directors or other organizational or financial guidance.

Warrants and Options

Under the 1940 Act, we are subject to restrictions on the amount of warrants, options, restricted stock or rights to purchase shares of capital stock that we may have outstanding at any time. In particular, the amount of capital stock that would result from the conversion or exercise of all outstanding warrants, options or rights to purchase capital stock cannot exceed 25% of our total outstanding shares of capital stock. This amount is reduced to 20% of our total outstanding shares of capital stock if the amount of warrants, options or rights issued pursuant to an executive compensation plan would exceed 15% of our total outstanding shares of capital stock. We have received exemptive relief from the SEC permitting us to issue restricted stock to our employees and directors subject to the above conditions, among others.

Indebtedness and Senior Securities

We will be permitted, under specified conditions, to issue multiple classes of indebtedness and one class of stock senior to our common stock if our asset coverage, as defined in the 1940 Act, is at least equal to 200% immediately after each such issuance. In addition, we may not be permitted to declare any cash dividend or other distribution on our outstanding common shares, or purchase any such shares, unless, at the time of such declaration or purchase, we have asset coverage of at least 200% after deducting the amount of such dividend, distribution, or purchase price. We may also borrow amounts up to 5% of the value of our total assets for temporary or emergency purposes.

Capital Structure

As a BDC, we generally cannot issue and sell our common stock at a price below the current NAV per share. We may, however, sell our common stock, or warrants, options or rights to acquire our common stock, at a price below the current NAV of our common stock in a rights offering to our stockholders if: 1) our board of directors determines that such sale is in the best interests of the Company and our stockholders; 2) our stockholders approve the sale of our common stock at a price that is less than the current NAV; and 3) the price at which our common stock is to be issued and sold is not less than a price that, in the determination of our board of directors, closely approximates the market value of such securities (less any sales load).

We may also be prohibited under the 1940 Act from participating in certain transactions with our affiliates without the prior approval of our directors who are not interested persons and, in some cases, prior approval by the SEC.

We do not intend to acquire securities issued by any investment company that exceed the limits imposed by the 1940 Act. Under these limits, we generally cannot acquire more than 3% of the voting stock of any registered investment company (as defined in the 1940 Act), invest more than 5% of the value of our total assets in the securities of one such investment company or invest more than 10% of the value of our total assets in the securities of such investment companies in the aggregate.

1940 Act Code of Ethics

We have adopted and will maintain a code of ethics that establishes procedures for personal investments and restricts certain personal securities transactions by our officers and directors. Personnel subject to the code may invest in securities for their personal investment accounts, including securities that may be purchased or held by us, so long as such investments are made in accordance with the code’s requirements. Our Amended and Restated Code of Ethics, or 1940 Act Code of Ethics, will generally not permit investments by our employees in securities that may be purchased or held by us. We may be prohibited under the 1940 Act from conducting certain transactions with our affiliates without the prior approval of our directors who are not interested persons and, in some cases, the prior approval of the SEC.

A copy of our 1940 Act Code of Ethics is available on our website at www.mcgcapital.com. We are not including the information contained on our website as a part of, or incorporating it by reference into, this Form 10-K. In addition, you may read and copy the 1940 Act Code of Ethics at the SEC’s Public Reference Room in Washington, D.C. You may obtain information on the operation of the Public Reference Room by calling the SEC at (202) 551-8090. In addition, the 1940 Act Code of Ethics attached as an exhibit to our registration statement and is available on the EDGAR Database on the SEC’s Internet site at http://www.sec.gov. You may also obtain copies of the 1940 Act Code

13

of Ethics, after paying a duplicating fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Section, 100 F Street, N.E., Washington, D.C. 20549.

PRIVACY PRINCIPLES

We are committed to maintaining the privacy of our stockholders and safeguarding their non-public personal information. The following information is provided to help you understand what personal information we collect, how we protect that information and why, in certain cases, we may share information with select other parties.

Generally, we do not receive any non-public personal information relating to our stockholders, although certain non-public personal information of our stockholders may become available to us. We do not disclose any non-public personal information about our stockholders or former stockholders, except as permitted by law or as is necessary in order to service stockholder accounts (for example, to a transfer agent).

We restrict access to non-public personal information about our stockholders to our employees with a legitimate business need for the information. We maintain physical, electronic and procedural safeguards designed to protect the security of the non-public personal information of our stockholders.

PROXY VOTING POLICIES AND PROCEDURES

We vote proxies relating to our portfolio securities in the best interest of our stockholders. We review on a case-by-case basis each proposal submitted to a stockholder vote to determine its impact on the portfolio securities held by us. Although we generally vote against proposals that may have a negative impact on our portfolio securities, we may vote for such a proposal if there are compelling long-term reasons to do so.

Our proxy voting decisions are discussed with the committee that is responsible for monitoring each of our investments. To ensure that our vote is not the product of a conflict of interest, we require that: (i) anyone involved in the decision-making process disclose to our General Counsel and Chief Compliance Officer any potential conflict that he or she is aware of and any contact that he or she has had with any interested party regarding a proxy vote; and (ii) employees involved in the decision-making process or vote administration are prohibited from revealing how we intend to vote on a proposal in order to reduce any attempted influence from interested parties.

EXEMPTIVE AND OTHER RELIEF

We have received an exemptive order from the SEC to permit us to issue restricted shares of our common stock as part of the compensation packages for certain of our employees and directors. We believe that the particular characteristics of our business, the dependence we have on key personnel to conduct our business effectively and the highly competitive environment in which we operate require the use of equity-based compensation for our personnel in the form of restricted stock. The issuance of restricted shares of our common stock requires the approval of our stockholders. In June 2006, our stockholders approved our Amended and Restated 2006 Employee Restricted Stock Plan, or the 2006 Plan, and our Amended and Restated 2006 Non-Employee Director Restricted Stock Plan.

Awards under the 2006 Plan must comply with all aspects of the SEC's order, including the following:

• | no one person may be granted awards totaling more than 25% of the shares available; |

• | in any fiscal year, no person may be granted awards in excess of 500,000 shares of our common stock; and |

• | the total number of shares that may be outstanding as restricted shares under all of our compensation plans may not exceed 10% of the total number of our shares of common stock authorized and outstanding at any time. |

In October 2008, we received exemptive relief from the SEC, which effectively allows us to exclude debt issued by Solutions Capital from the calculation of our consolidated BDC asset coverage ratio.

We requested the assurance of the staff of the Division of Investment Management that it would not recommend enforcement action to the SEC under the 1940 Act or Rule 17d-1 thereunder if we engaged in a stock repurchase program and did not rescind awards of restricted stock previously awarded in compliance with the terms and conditions of the exemptive order of the SEC so long as we agreed not to issue additional restricted stock under any compensation plan unless such issuance, together with all restricted stock outstanding under all compensation plans, does not exceed 10% of our outstanding common stock at the time of such issuance less the total number of shares previously issued, in the aggregate, pursuant to all compensatory plans. On September 27, 2013, the no-action letter was issued by the SEC.

14

OTHER

We will be examined periodically by the SEC for compliance with the Exchange Act and the 1940 Act.

As with other companies regulated by the 1940 Act, we must adhere to certain substantive regulatory requirements. A majority of our directors must be persons who are not interested persons, as that term is defined in the 1940 Act. We must provide and maintain a bond issued by a reputable fidelity insurance company to protect us against larceny and embezzlement. Furthermore, as a BDC, we cannot protect any director or officer against any liability to our stockholders arising from willful misfeasance, bad faith, gross negligence or reckless disregard of the duties involved in the conduct of such person’s office.

We are required to adopt and implement written policies and procedures reasonably designed to prevent violation of the federal securities laws, and to review these policies and procedures annually for their adequacy and the effectiveness of their implementation. Mr. Tod K. Reichert, our General Counsel and Chief Compliance Officer, is responsible for administering these policies and procedures.

Recently, legislation was introduced in the U.S. House of Representatives, which may revise certain regulations applicable to BDCs. The legislation provides for (i) increasing the amount of funds BDCs borrow by reducing asset to debt limitations from 2:1 to 3:2, (ii) permitting BDCs to file registration statements with the SEC that incorporate information by reference, (iii) utilizing other streamlined registration processes afforded to operating companies, and (iv) allowing BDCs to own investment adviser subsidiaries. There are no assurances as to when the legislation will be enacted by Congress, if at all,or, if enacted, what final form the legislation would take.

COMPLIANCE WITH THE SARBANES-OXLEY ACT OF 2002 AND THE NASDAQ GLOBAL SELECT MARKET CORPORATE GOVERNANCE REGULATIONS

The Sarbanes-Oxley Act of 2002, or Sarbanes-Oxley Act, imposes a wide variety of regulatory requirements on publicly held companies and their insiders. The Sarbanes-Oxley Act requires us to review our policies and procedures to determine whether we comply with it and the regulations promulgated thereunder.

The NASDAQ Global Select Market has also adopted various corporate governance requirements as part of its listing standards. We believe we are in compliance with such corporate governance listing standards.

SMALL BUSINESS ADMINISTRATION REGULATIONS

In December 2004, we formed Solutions Capital and Solutions Capital G.P., LLC. In September 2007, Solutions Capital received final approval to be licensed as an SBIC. Solutions Capital has borrowed funds from the SBA against eligible investments and additional deposits of regulatory capital. As of January 2012, we had borrowed $150.0 million of SBA-guaranteed debentures under the SBIC program, which is the maximum amount of outstanding leverage available to single-license SBIC. SBA-guaranteed debentures are non-recourse, interest-only debentures with interest payable semi-annually and a ten-year maturity. The principal amount of SBA-guaranteed debentures is not required to be paid prior to maturity, but may be prepaid at any time without penalty.

SBICs are designed to stimulate the flow of private capital to eligible small businesses. Under SBA regulations, Solutions Capital is subject to regulatory requirements including making investments in SBA eligible businesses, investing at least 25% of regulatory capital in eligible “smaller” businesses, placing certain limitations on the financing terms of investments, prohibiting investing in certain industries, required capitalization thresholds, and is subject to periodic audits and examinations among other regulations. If Solutions Capital fails to comply with applicable SBA regulations, the SBA could, depending on the severity of the violation, limit or prohibit its use of debentures, declare outstanding debentures immediately due and payable, and/or limit Solutions Capital from making new investments. In addition, the SBA can revoke or suspend a license for willful or repeated violation of, or willful or repeated failure to observe, any provision of the SBIC Act or any rule or regulation promulgated thereunder. These actions by the SBA would, in turn, negatively affect us because Solutions Capital is our wholly owned subsidiary.

Eligible Small and Smaller Businesses

Under current SBA regulations, eligible small businesses include those that have a tangible net worth not exceeding $18 million and average annual net income not exceeding $6 million for the two most recent fiscal years. In addition, an SBIC must devote 25% of its investment activity to “smaller” concerns as defined by the SBA. A smaller concern is one that has a tangible net worth not exceeding $6 million and average annual net income not exceeding $2 million for the two most recent fiscal years. SBA regulations also provide alternative size standard criteria to determine eligibility, which depend on the industry in which the business is engaged and are based on such factors as the number

15

of employees or gross sales. According to SBA regulations, SBICs may make long-term loans to small businesses and invest in the equity securities of such businesses. Once an SBIC has invested in a company, it may generally continue to make follow-on investments in the company, regardless of the size of the business, up and until the time a business offers its securities in a public market. Through Solutions Capital, we plan to continue to provide long-term loans to, and non-control equity investments in, qualifying small businesses.

Financing Limitations

SBA regulations also include restrictions on a “change of control” of an SBIC where a transfer would result in any person or group owning 10% or more of a class of capital stock (or its equivalent in the case of a partnership) of a licensed SBIC and require that SBICs invest idle funds in accordance with SBA regulations. In addition, our SBIC subsidiary may also be limited in its ability to make distributions to us if it does not have sufficient earnings and capital, in accordance with SBA regulations. The SBA places certain limits on the financing terms of investments by SBICs, including limiting the interest rate on debt securities and loans provided to portfolio companies of the SBIC. The SBA also limits fees, prepayment terms and certain other economic arrangements that are common in lending environments.

SBA Leverage or Debentures

SBA-guaranteed debentures are non-recourse to us, have a ten-year maturity and may be prepaid at any time without penalty. The interest rate of SBA-guaranteed debentures is fixed at the time of issuance at a market-based spread over ten-year U.S. Treasury Notes. Obtaining leverage, or borrowings, through SBA guaranteed debentures is subject to required capitalization thresholds. Current SBA regulations limit the amount that Solutions Capital may borrow to a maximum of $150 million, which is up to twice its regulatory capital.