Attached files

| file | filename |

|---|---|

| EX-31.1 - EX-31.1 - AVANIR PHARMACEUTICALS, INC. | d652551dex311.htm |

| EX-31.2 - EX-31.2 - AVANIR PHARMACEUTICALS, INC. | d652551dex312.htm |

| EX-32.1 - EX-32.1 - AVANIR PHARMACEUTICALS, INC. | d652551dex321.htm |

| EXCEL - IDEA: XBRL DOCUMENT - AVANIR PHARMACEUTICALS, INC. | Financial_Report.xls |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the quarterly period ended December 31, 2013

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the transition period from to .

Commission File No. 1-15803

AVANIR PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 33-0314804 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 20 Enterprise Suite 200, Aliso Viejo, California | 92656 | |

| (Address of principal executive offices) | (Zip Code) |

(949) 389-6700

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities and Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO x

As of January 31, 2014, the registrant had 152,296,065 shares of common stock issued and outstanding.

Table of Contents

| Page | ||||||

| Item 1. |

||||||

| 3 | ||||||

| 4 | ||||||

| 5 | ||||||

| 6 | ||||||

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

21 | ||||

| Item 3. |

31 | |||||

| Item 4. |

31 | |||||

| Item 1. |

32 | |||||

| Item 1A. |

33 | |||||

| Item 2. |

53 | |||||

| Item 3. |

53 | |||||

| Item 4. |

53 | |||||

| Item 5. |

54 | |||||

| Item 6. |

54 | |||||

| 55 | ||||||

2

Table of Contents

CONDENSED CONSOLIDATED BALANCE SHEETS

| December 31, 2013 | September 30, 2013 | |||||||

| (unaudited) | (audited) | |||||||

| ASSETS | ||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 43,897,733 | $ | 55,259,073 | ||||

| Restricted cash and cash equivalents |

1,316,896 | 965,986 | ||||||

| Trade receivables, net of allowances of $207,828 as of December 31, 2013 and September 30, 2013, respectively |

4,199,014 | 12,525,992 | ||||||

| Royalty receivable |

1,425,815 | 542,596 | ||||||

| Other receivables |

2,789,261 | 246,975 | ||||||

| Inventories, net |

605,833 | 710,179 | ||||||

| Prepaid expenses |

1,714,980 | 1,391,210 | ||||||

| Other current assets |

158,606 | 201,629 | ||||||

|

|

|

|

|

|||||

| Total current assets |

56,108,138 | 71,843,640 | ||||||

| Restricted long-term investments |

1,303,938 | 1,303,938 | ||||||

| Property and equipment, net |

2,568,341 | 1,592,791 | ||||||

| Non-current inventories, net |

773,130 | 784,186 | ||||||

| Other assets |

517,069 | 554,452 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 61,270,616 | $ | 76,079,007 | ||||

|

|

|

|

|

|||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 4,145,275 | $ | 5,876,425 | ||||

| Accrued expenses |

11,836,746 | 11,908,570 | ||||||

| Accrued compensation and payroll taxes |

4,626,727 | 7,775,761 | ||||||

| Deferred royalty revenues |

640,465 | 1,288,514 | ||||||

| Current portion of notes payable, net of debt discount |

10,870,170 | 7,942,945 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

32,119,383 | 34,792,215 | ||||||

| Other liabilities |

1,611,046 | 1,393,075 | ||||||

| Notes payable, net of current portion and debt discount |

18,596,831 | 21,422,163 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

52,327,260 | 57,607,453 | ||||||

|

|

|

|

|

|||||

| Commitments and contingencies |

||||||||

| Stockholders’ equity: |

||||||||

| Preferred stock - $0.0001 par value, 10,000,000 shares authorized, no shares issued |

— | — | ||||||

| Common stock - $0.0001 par value, 200,000,000 shares authorized; 152,273,131 and 152,063,621 shares issued and outstanding as of December 31, 2013 and September 30, 2013, respectively |

15,227 | 15,206 | ||||||

| Additional paid-in capital |

520,410,555 | 518,992,237 | ||||||

| Accumulated deficit |

(511,482,426 | ) | (500,535,889 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

8,943,356 | 18,471,554 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 61,270,616 | $ | 76,079,007 | ||||

|

|

|

|

|

|||||

The accompanying notes to condensed consolidated financial statements are an integral part of this statement.

3

Table of Contents

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

| Three Months Ended December 31, | ||||||||

| 2013 | 2012 | |||||||

| Revenues: |

||||||||

| Net product sales |

$ | 23,299,027 | $ | 14,879,262 | ||||

| Revenues from royalties |

2,089,314 | 1,626,010 | ||||||

| Revenues from co-promote activities |

1,358,078 | — | ||||||

| Revenues from research grant services |

— | 15,000 | ||||||

|

|

|

|

|

|||||

| Total revenues |

26,746,419 | 16,520,272 | ||||||

|

|

|

|

|

|||||

| Operating expenses: |

||||||||

| Cost of product sales |

1,292,411 | 838,129 | ||||||

| Cost of research grant services |

— | 9,398 | ||||||

| Research and development |

9,525,320 | 6,648,091 | ||||||

| Selling and marketing |

17,475,404 | 13,522,419 | ||||||

| General and administrative |

8,449,890 | 6,538,403 | ||||||

|

|

|

|

|

|||||

| Total operating expenses |

36,743,025 | 27,556,440 | ||||||

|

|

|

|

|

|||||

| Loss from operations |

(9,996,606 | ) | (11,036,168 | ) | ||||

| Other income (expense): |

||||||||

| Interest income |

4,552 | 19,331 | ||||||

| Interest expense |

(954,895 | ) | (1,059,245 | ) | ||||

| Other, net |

412 | — | ||||||

|

|

|

|

|

|||||

| Net loss |

$ | (10,946,537 | ) | $ | (12,076,082 | ) | ||

|

|

|

|

|

|||||

| Basic and diluted net loss per share |

$ | (0.07 | ) | $ | (0.09 | ) | ||

|

|

|

|

|

|||||

| Basic and diluted weighted average number of common shares outstanding |

152,100,388 | 136,772,557 | ||||||

|

|

|

|

|

|||||

The accompanying notes to condensed consolidated financial statements are an integral part of this statement.

4

Table of Contents

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

| Three Months Ended December 31, | ||||||||

| 2013 | 2012 | |||||||

| Cash flows from operating activities: |

||||||||

| Net loss |

$ | (10,946,537 | ) | $ | (12,076,082 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

| Depreciation and amortization |

222,210 | 199,115 | ||||||

| Amortization of debt discount and debt issuance costs |

120,179 | 163,446 | ||||||

| Share-based compensation expense |

1,388,117 | 1,407,008 | ||||||

| Changes in operating assets and liabilities: |

||||||||

| Trade receivables, net |

8,326,978 | 397,737 | ||||||

| Royalty receivable |

(883,219 | ) | (676,435 | ) | ||||

| Other receivables |

(2,542,286 | ) | (45,000 | ) | ||||

| Inventories, net |

115,402 | 37,231 | ||||||

| Prepaid expenses and other assets |

(261,650 | ) | (542,203 | ) | ||||

| Accounts payable |

(1,732,342 | ) | 1,082,716 | |||||

| Accrued expenses and other liabilities |

209,499 | (455,015 | ) | |||||

| Accrued compensation and payroll taxes |

(3,149,034 | ) | (1,698,367 | ) | ||||

| Deferred royalty revenues |

(648,049 | ) | (474,607 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in operating activities |

(9,780,732 | ) | (12,680,456 | ) | ||||

|

|

|

|

|

|||||

| Cash flows from investing activities: |

||||||||

| Purchases of property and equipment |

(1,259,920 | ) | (179,661 | ) | ||||

| Purchases of restricted investments and restricted cash and cash equivalents |

(350,910 | ) | (1,802 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(1,610,830 | ) | (181,463 | ) | ||||

|

|

|

|

|

|||||

| Cash flows from financing activities: |

||||||||

| Proceeds from exercise of stock options and warrants |

30,222 | 26,131 | ||||||

|

|

|

|

|

|||||

| Net cash provided by financing activities |

30,222 | 26,131 | ||||||

|

|

|

|

|

|||||

| Net change in cash and cash equivalents |

(11,361,340 | ) | (12,835,788 | ) | ||||

| Cash and cash equivalents at beginning of period |

55,259,073 | 69,778,406 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of period |

$ | 43,897,733 | $ | 56,942,618 | ||||

|

|

|

|

|

|||||

| Supplemental disclosures of cash flow information: |

||||||||

| Interest paid |

$ | 671,250 | $ | 671,250 | ||||

| Income taxes paid |

$ | 3,200 | $ | 3,200 | ||||

| Supplemental disclosures of non-cash investing and financing activities: |

||||||||

| Purchases of property and equipment in accounts payable and accrued expenses |

$ | 100,500 | $ | — | ||||

The accompanying notes to condensed consolidated financial statements are an integral part of this statement.

5

Table of Contents

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

1. DESCRIPTION OF BUSINESS AND BASIS OF PRESENTATION

Description of Business

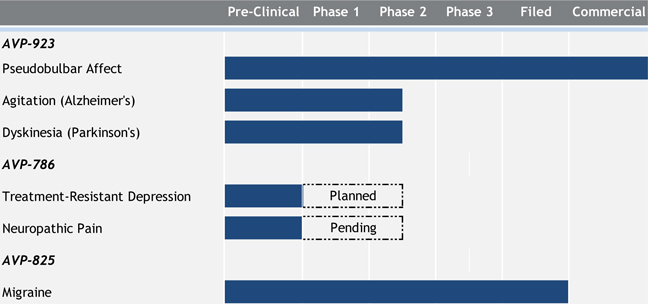

Avanir Pharmaceuticals, Inc. and subsidiaries (“Avanir”, the “Company” or “we”) is a biopharmaceutical company focused on acquiring, developing and commercializing novel therapeutic products for the treatment of central nervous system disorders. The Company’s lead product NUEDEXTA® (referred to as AVP-923 during clinical development) is a first-in-class dual N-methyl-D-aspartate (“NMDA”) receptor antagonist and sigma-1 agonist. NUEDEXTA, 20/10 mg, was approved in the United States in October 2010 for the treatment of pseudobulbar affect (“PBA”). It is also approved for the treatment of PBA in the European Union in two dose strengths, NUEDEXTA 20/10 mg and NUEDEXTA 30/10 mg. The Company commercially launched NUEDEXTA in the United States in February 2011 and it is currently assessing plans regarding the potential commercialization of NUEDEXTA in the European Union.

The Company is studying the clinical utility of AVP-923 in other mood/behavior disorders and movement disorders. The Company has two ongoing Phase II clinical trials exploring the potential treatment of agitation in patients with Alzheimer’s disease and potential treatment of levodopa-induced dyskinesia in Parkinson’s disease (the “LID study”). The LID study is supported by a grant from the Michael J. Fox Foundation.

The Company is also developing AVP-786, a next generation drug product containing deuterium-modified dextromethorphan and quinidine for the treatment of neurologic and psychiatric disorders. The Company completed a pharmacokinetic study with AVP-786, and based on this data, the Company believes that it has identified a formulation of AVP-786 with a comparable pharmacokinetic profile, and likely a comparable safety and tolerability profile to AVP-923. This AVP-786 formulation contains significantly less quinidine than used in AVP-923.

The Company is also developing a novel Breath Powered™ intranasal delivery system containing low-dose sumatriptan powder to treat acute migraine, AVP-825. If approved, this product would be the first and only fast-acting dry-powder nasal delivery form of sumatriptan. AVP-825 is licensed from OptiNose AS (“OptiNose”). Under the terms of the agreement, the Company assumed responsibility for regulatory, manufacturing, supply-chain and commercialization activities for the investigational product. The Company filed a New Drug Application (“NDA”) with the U.S. Food and Drug Administration (“FDA”) in January 2014.

The Company entered into a multi-year agreement with Merck Sharp & Dohme Corp. (“Merck”) to co-promote Merck’s type 2 diabetes therapies JANUVIA® (sitagliptin) and the sitagliptin family of products in the long-term care institutional setting in the United States beginning October 1, 2013. The term of the Agreement will continue for three years following the launch date of the co-promotion activities. Under the terms of the Agreement, the Company will be compensated via a (i) fixed monthly fee and (ii) performance fee based on the amount of the products sold by the Company above a predetermined baseline. A significant majority of the fee is performance based. Over the three years of the agreement, Avanir could receive up to a maximum of $60.0 million in compensation.

In addition to the Company’s focus on products for the central nervous system, the Company also has partnered programs in other therapeutic areas which may generate future revenue. The Company’s first commercialized product, docosanol 10% cream, (sold in the United States and Canada as Abreva® by its marketing partner GlaxoSmithKline Consumer Healthcare) is the only over-the-counter treatment for cold sores that has been approved by the FDA.

The Company’s operations are subject to certain risks and uncertainties frequently encountered by companies in the early stages of operations, particularly in the evolving market for small biotech and specialty pharmaceutical companies. Such risks and uncertainties include, but are not limited to, the occurrence of adverse safety events with NUEDEXTA; that NUEDEXTA may not gain broader acceptance by the medical field or that the indicated use may

6

Table of Contents

not be clearly understood; the Company’s dependence on third parties for manufacturing and distribution of NUEDEXTA; that the Company may not adequately build or maintain the necessary sales, marketing, supply chain management and reimbursement capabilities on its own or enter into arrangements with third parties to perform these functions in a timely manner or on acceptable terms; the ability to successfully protect and enforce its intellectual property rights relating to NUEDEXTA; timing and uncertainty of achieving milestones in clinical trials; obtaining approvals by the FDA, European Medicines Agency (“EMA”) and regulatory agencies in other countries; and potential regulatory delays or rejections in the filing or acceptance of an NDA. The Company’s ability to generate revenues in the future may depend on market acceptance of NUEDEXTA for the treatment of PBA, pricing and reimbursement in European countries, the ability to obtain a partner to market NUEDEXTA in the EU, commercial market estimates and related revenue projections for AVP-825 and the timing and success of reaching clinical development milestones and obtaining regulatory approvals for other formulations and indications for AVP-923 and AVP-786. The Company’s cash expenditures depend substantially on the level of expenditures for the ongoing marketing of NUEDEXTA, clinical development activities for AVP-923 and AVP-786, milestone payments related to AVP-786 and AVP-825 and regulatory activities for AVP-825.

Avanir was incorporated in California in August 1988 and was reincorporated in Delaware in March 2009.

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements of Avanir have been prepared in accordance with the rules and regulations of the Securities and Exchange Commission (“SEC”) for interim reporting including the instructions to Form 10-Q. These condensed consolidated financial statements do not include all disclosures for annual audited financial statements required by accounting principles generally accepted in the United States of America (“U.S. GAAP”) and should be read in conjunction with the Company’s audited consolidated financial statements and related notes included in the Company’s Annual Report on Form 10-K for the year ended September 30, 2013. The Company believes these condensed consolidated financial statements reflect all adjustments (consisting only of normal, recurring adjustments) that are necessary for a fair presentation of the financial position and results of operations for the periods presented. Results of operations for the interim periods presented are not necessarily indicative of results to be expected for the year.

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts and the disclosures of commitments and contingencies in the financial statements and accompanying notes. Actual results could differ from those estimates.

Reclassifications

Royalty receivable and other receivables at September 30, 2013 are now reported under their own captions, separate from other current assets, in the accompanying condensed consolidated balance sheets and as separate components of cash flows from operating activities in the condensed consolidated statements of cash flows for the three months ended December 31, 2012, in order to conform to the current period presentation.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The following represents an update for the three months ended December 31, 2013 to the significant accounting policies described in the Company’s Annual Report on Form 10-K for the fiscal year ended September 30, 2013.

Concentration of credit risk and sources of supply

Financial assets that potentially subject the Company to concentrations of credit risk consist of cash and cash equivalents, trade receivables, royalty receivable and other receivables. The Company’s cash and cash equivalents are placed in various money market mutual funds and at financial institutions of high credit standing. At times, deposits held with these financial institutions may exceed the amount of insurance provided by the Federal Deposit Insurance Corporation (FDIC). Generally, these deposits may be redeemed upon demand and, therefore, bear minimal risk. The Company performs ongoing credit evaluations of customers’ financial condition and may limit the amount of credit extended if necessary; however, the Company has historically required no collateral from its customers.

7

Table of Contents

The Company currently has sole suppliers for the active pharmaceutical ingredients (“APIs”) for NUEDEXTA and a sole manufacturer for the finished form of NUEDEXTA. In addition, these materials are custom and available from only a limited number of sources. Any material disruption in manufacturing could cause a delay in shipments and possible loss of revenue. If the Company is required to change manufacturers, the Company may experience delays associated with finding an alternative manufacturer that is properly qualified to produce NUEDEXTA in accordance with FDA requirements and the Company’s specifications.

Deferred rent

The Company accounts for rent expense related to operating leases by determining total minimum rent payments on the leases over their respective periods and recognizing the rent expense on a straight-line basis. The difference between the actual amount paid and the amount recorded as rent expense in each fiscal year is recorded as an adjustment to deferred rent. Deferred rent as of December 31, 2013 and September 30, 2013 was approximately $427,000 and $367,000, respectively, and is included in accrued expenses and other liabilities in the accompanying condensed consolidated balance sheets.

Fair value of financial instruments

The Company measures the fair value of certain of its financial assets on a recurring basis. A fair value hierarchy is used to rank the quality and reliability of the information used to determine fair values. Financial assets and liabilities carried at fair value will be classified and disclosed in one of the following three categories:

| • | Level 1-Quoted prices (unadjusted) in active markets for identical assets and liabilities. |

| • | Level 2-Inputs other than Level 1 that are observable, either directly or indirectly, such as unadjusted quoted prices for similar assets and liabilities, unadjusted quoted prices in the markets that are not active, or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities. |

| • | Level 3-Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities. |

At December 31, 2013 and September 30, 2013, the Company’s financial instruments include cash and cash equivalents, restricted cash and cash equivalents, trade receivables, royalty receivable, other receivables, restricted investments, accounts payable, accrued expenses, accrued compensation and payroll taxes, other liabilities and notes payable. The carrying amount of cash and cash equivalents, restricted cash and cash equivalents, trade receivables, royalty receivable, other receivables, accounts payable, accrued expenses, accrued compensation and payroll taxes, and other liabilities approximates fair value due to the short-term maturities of these instruments. The Company’s restricted investments are carried at amortized cost which approximates fair value. Based on borrowing rates currently available to the Company, the carrying value of notes payable approximates fair value.

Restricted cash, cash equivalents and restricted investments

Restricted cash and cash equivalents and restricted long-term investments consist of certificates of deposit, which are classified as held-to-maturity.

Restricted cash and cash equivalents consist of a certificate of deposit relating to the Company’s corporate credit card agreement and automatically renews every three months.

Restricted long-term investments consist of two certificates of deposit related to irrevocable standby letters of credit connected to fleet rentals and an office lease with an expiration date in 2018. The certificates of deposit automatically renew annually.

Debt issuance costs and debt discount

Debt issuance costs are stated at cost, net of accumulated amortization in other assets in the condensed consolidated balance sheets. Debt discount is recorded within notes payable in the condensed consolidated balance sheets. Amortization expense of debt issuance costs and the debt discount is calculated using the interest method over the term of the debt and is recorded in interest expense in the accompanying condensed consolidated statements of operations.

8

Table of Contents

Revenue recognition

The Company has historically generated revenues from product sales, collaborative research and development arrangements, and other commercial arrangements such as royalties, the sale of royalty rights and sales of technology rights. Payments received under such arrangements may include non-refundable fees at the inception of the arrangements, milestone payments for specific achievements designated in the agreements, royalties on sales of products resulting from collaborative arrangements, and payments for the sale of rights to future royalties.

The Company recognizes revenue when all of the following criteria are met: (1) persuasive evidence of an arrangement exists; (2) delivery has occurred or services have been rendered; (3) the Company’s price to the buyer is fixed or determinable; and (4) collectability is reasonably assured. In addition, certain product sales are subject to rights of return. For products sold where the buyer has the right to return the product, the Company recognizes revenue at the time of sale only if (1) the Company’s price to the buyer is substantially fixed or determinable at the date of sale, (2) the buyer has paid the Company, or is obligated to pay the Company and the obligation is not contingent on resale of the product, (3) the buyer’s obligation to the Company would not be changed in the event of theft or physical destruction or damage of the product, (4) the buyer acquiring the product for resale has economic substance apart from that provided by the seller, (5) the Company does not have significant obligations for future performance to directly bring about resale of the product by the buyer, and (6) the amount of future returns can be reasonably estimated. The Company recognizes such product revenues when either it has met all the above criteria, including the ability to reasonably estimate future returns, or when it can reasonably estimate that the return privilege has substantially expired, whichever occurs first.

Product Sales — NUEDEXTA. NUEDEXTA is sold primarily to third-party wholesalers that, in turn, sell this product to retail pharmacies, hospitals, and other dispensing organizations. The Company has entered into agreements with wholesale customers, certain medical institutions and third-party payers throughout the United States. These agreements frequently contain commercial terms, which may include favorable product pricing and discounts and rebates payable upon dispensing the product to patients. Additionally, these agreements customarily provide the customer with rights to return the product, subject to the terms of each contract. Consistent with pharmaceutical industry practice, wholesale customers can return purchased product during an 18-month period that begins six months prior to the product’s expiration date and ends 12 months after the expiration date. The Company recognizes revenue upon shipment of NUEDEXTA to its wholesalers and other customers.

The Company’s net product sales represent gross product sales less allowances for customer credits, including estimated discounts, rebates, chargebacks and co-pay assistance. These allowances provided by the Company to a customer are presumed to be a reduction of the selling prices of the Company’s products or services and, therefore, are characterized as a reduction of revenue when recognized in the Company’s condensed consolidated statement of operations. Allowances for discounts, rebates, chargebacks and co-pay assistance are estimated based on contractual terms with customers and sell-through data purchased from third parties. The Company estimates future returns and records a returns reserve as a reduction to gross product sales. The returns reserve is estimated based on contractual terms with customers and historical trends. The Company believes the assumptions used to estimate these allowances are reasonable considering known facts and circumstances. However, actual rebates, chargebacks and returns could differ materially from estimated amounts because of, among other factors, unanticipated changes in prescription trends and any change in assumptions affecting sell-through data purchased from third parties. Product shipping and handling costs are included in cost of product sales.

Product Sales — Active Pharmaceutical Ingredient docosanol (“docosanol”). Revenue from sales of the Company’s docosanol is recorded when title and risk of loss have passed to the buyer, provided the criteria for revenue recognition have been met. The Company sells the docosanol to various licensees upon receipt of a written order for the materials. Shipments generally occur fewer than three times per year. The Company’s contracts for sales of the docosanol include buyer acceptance provisions that give the Company’s buyers the right of replacement if the delivered product does not meet specified criteria. That right requires that they give the Company notice within 30 days after receipt of the product. The Company has the option to refund or replace any such defective materials; however, it has historically demonstrated that the materials shipped from the same pre-inspected lot have consistently met the specified criteria and no buyer has rejected any of the Company’s shipments from the same pre-inspected lot to date. Therefore, the Company recognizes revenue at the time of delivery without providing any returns reserve. The Company has not recognized revenue from the sale of docosanol during the first quarter of fiscal 2014 and fiscal 2013.

9

Table of Contents

Multiple Element Arrangements. The Company has, in the past, entered into arrangements whereby it delivers to the customer multiple elements including technology and/or services. Such arrangements have included some combination of the following: antibody generation services; licensed rights to technology, patented products, compounds, data and other intellectual property; and research and development services. At the inception of each such arrangement, the Company analyzes the multiple elements contained within the arrangement to determine whether the elements can be separated. If a product or service is not separable, the combined deliverables will be accounted for as a single unit of accounting.

A delivered element can be separated from other elements when it meets both of the following criteria: (1) the delivered item has value to the customer on a standalone basis; and (2) if the arrangement includes a general right of return relative to the delivered item, delivery or performance of the undelivered item is considered probable and substantially in the Company’s control. If an element can be separated, the Company allocates amounts based upon the selling price of each element. The Company determines the selling price of a separate deliverable using the price it charges other customers when it sells that product or service separately; however, if the Company does not sell the product or service separately, it uses third-party evidence of selling price of a similar product or service to a similarly situated customer. The Company considers licensed rights or technology to have standalone value to its customers if it or others have sold such rights or technology separately or its customers can sell such rights or technology separately without the need for the Company’s continuing involvement. The Company has not entered into any multiple element arrangements which have required the Company to estimate selling prices during the first quarter of fiscal 2014 and fiscal 2013.

License Arrangements. License arrangements may consist of non-refundable up-front license fees, data transfer fees, research reimbursement payments, exclusive licensed rights to patented or patent pending compounds, technology access fees, and various performance or sales milestones. These arrangements are often multiple element arrangements.

Non-refundable, up-front fees that are not contingent on any future performance by the Company, and require no consequential continuing involvement on its part, are recognized as revenue when the license term commences and the licensed data, technology and/or compound is delivered. Such deliverables may include physical quantities of compounds, design of the compounds and structure-activity relationships, the conceptual framework and mechanism of action, and rights to the patents or patents pending for such compounds. The Company defers recognition of non-refundable up-front fees if it has continuing performance obligations without which the technology, right, product or service conveyed in conjunction with the non-refundable fee has no utility to the licensee that is separate and independent of the Company’s performance under the other elements of the arrangement. In addition, if the Company has required continuing involvement through research and development services that are related to its proprietary know-how and expertise of the delivered technology, or can only be performed by the Company, then such up-front fees are deferred and recognized over the period of continuing involvement.

Payments related to substantive, performance-based milestones in a research and development arrangement are recognized as revenues upon the achievement of the milestones as specified in the underlying agreements when they represent the culmination of the earnings process.

Royalty Arrangements. The Company recognizes royalty revenues from licensed products when earned in accordance with the terms of the license agreements. Net sales amounts generally required to be used for calculating royalties include deductions for returned product, pricing allowances, cash discounts, freight and warehousing. These arrangements are often multiple element arrangements.

Certain royalty arrangements provide that royalties are earned only if a sales threshold is exceeded. Under these types of arrangements, the threshold is typically based on annual sales. For royalty revenue generated from the license agreement with GlaxoSmithKline (“GSK”), the Company recognizes royalty revenue in the period in which the threshold is exceeded.

When the Company sells its rights to future royalties under license agreements and also maintains continuing involvement in earning such royalties, it defers recognition of any up-front payments and recognizes them as revenues over the life of the license agreement. The Company recognizes revenues for the sale of an undivided

10

Table of Contents

interest of its Abreva® license agreement to Drug Royalty USA under the “units-of-revenue method.” Under this method, the amount of deferred revenues to be recognized in each period is calculated by multiplying the ratio of the royalty payments due to Drug Royalty USA by GSK for the period to the total remaining royalties the Company expects GSK will pay Drug Royalty USA over the remaining term of the agreement.

Co-Promotion Arrangements. The Company recognizes both a fixed monthly fee and a performance fee as revenues from co-promote activities in the condensed consolidated statements of operations. The fixed monthly fee is recognized ratably over the period earned. The performance fee is recognized when the products sold exceeds a predetermined baseline for the period. The receivable from the co-promotion fee is recorded in other receivables in the condensed consolidated balance sheets.

Share-based compensation

The Company grants options, restricted stock units and restricted stock awards to purchase the Company’s common stock to employees, directors and consultants under stock option plans. The benefits provided under these plans are share-based payments that the Company accounts for using the fair value method.

The fair value of each option award is estimated on the date of grant using a Black-Scholes-Merton option pricing model (“Black-Scholes model”) that uses assumptions regarding a number of complex and subjective variables. These variables include, but are not limited to, expected stock price volatility, actual and projected employee stock option exercise behaviors, risk-free interest rate and expected dividends. Expected volatilities are based on the historical volatility of the Company’s common stock and other factors. The expected terms of options granted are based on analyses of historical employee termination rates and option exercises. The risk-free interest rate is based on the U.S. Treasury yield in effect at the time of the grant. Since the Company does not expect to pay dividends on common stock in the foreseeable future, it estimated the dividend yield to be 0%.

Share-based compensation expense recognized during a period is based on the value of the portion of share-based payment awards that are ultimately expected to vest and is amortized under the straight-line attribution method. As share-based compensation expense recognized in the accompanying condensed consolidated statements of operations for periods in fiscal 2014 and 2013 is based on awards ultimately expected to vest, it has been reduced for estimated forfeitures. The fair value method requires forfeitures to be estimated at the time of grant and revised, if necessary, in subsequent periods if actual forfeitures differ from those estimates. The Company estimates forfeitures based on historical experience. Changes to the estimated forfeiture rate are accounted for as a cumulative effect of change in the period the change occurred.

Total compensation expense related to all of the Company’s share-based awards for the three month periods ended December 31, 2013 and 2012, was comprised of the following:

| Three months ended December 31, |

||||||||

| 2013 | 2012 | |||||||

| Share-based compensation classified as: |

||||||||

| Research and development expense |

$ | 287,466 | $ | 268,144 | ||||

| Selling and marketing expense |

472,255 | 315,529 | ||||||

| General and administrative expense |

628,396 | 823,335 | ||||||

|

|

|

|

|

|||||

| Total |

$ | 1,388,117 | $ | 1,407,008 | ||||

|

|

|

|

|

|||||

| Three months ended December 31, |

||||||||

| 2013 | 2012 | |||||||

| Share-based compensation expense from: |

||||||||

| Stock options |

$ | 1,110,228 | $ | 1,047,986 | ||||

| Restricted stock units |

277,889 | 359,022 | ||||||

|

|

|

|

|

|||||

| Total |

$ | 1,388,117 | $ | 1,407,008 | ||||

|

|

|

|

|

|||||

11

Table of Contents

Since the Company has a net operating loss carry-forward as of December 31, 2013, no excess tax benefits for the tax deductions related to share-based awards were recognized in the accompanying condensed consolidated statements of operations. Additionally, no incremental tax benefits were recognized from stock options exercised in the three month periods ended December 31, 2013 and 2012, which would have resulted in a reclassification from cash flows from operating activities to cash flows from financing activities.

Income taxes

The Company accounts for income taxes and the related accounts under the liability method. Deferred tax assets and liabilities are determined based on the differences between the consolidated financial statement carrying amounts and the income tax bases of assets and liabilities. A valuation allowance is applied against any net deferred tax asset if, based on available evidence, it is more likely than not that some or all of the deferred tax assets will not be realized.

The Company recognizes any uncertain income tax positions on income tax returns at the largest amount that is more-likely-than-not to be sustained upon audit by the relevant taxing authority. An uncertain income tax position will not be recognized if it has less than a 50% likelihood of being sustained.

The total unrecognized tax benefit resulting in a decrease in deferred tax assets and corresponding decrease in the valuation allowance at December 31, 2013 was $3.6 million. There are no unrecognized tax benefits included in the condensed consolidated balance sheets that would, if recognized, affect the Company’s effective tax rate.

The Company’s policy is to recognize interest and/or penalties related to income tax matters in income tax expense. The Company had $0 accrued for interest and penalties on the Company’s condensed consolidated balance sheets at December 31, 2013 and September 30, 2013.

The Company is subject to taxation in the U.S. and various state jurisdictions. The Company’s tax years for 1995 and forward for federal purposes and 1989 and forward for California purposes are subject to examination by the U.S. and California tax authorities due to the carryforward of unutilized net operating losses and research and development credits.

The Company does not foresee material changes to its gross uncertain income tax position liability within the next twelve months.

Recent authoritative guidance

In July 2013, the FASB issued Accounting Standards Update (“ASU”) No. 2013-11, “Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists.” ASU 2013-11 provides explicit guidance on the financial statement presentation of an unrecognized tax benefit when a net operating loss carryforward, a similar tax loss, or a tax credit carryforward exists. The guidance is effective prospectively for fiscal years, and interim periods within those years, beginning after December 15, 2013, with an option for early adoption. The Company intends to adopt this guidance at the beginning of its first quarter of fiscal year 2015, and is currently evaluating the impact on its consolidated financial statements and disclosures.

Proposed Amendments to Current Accounting Standards. The Financial Accounting Standard Board (“FASB”) is currently working on amendments to existing accounting standards governing a number of areas including, but not limited to, revenue recognition and lease accounting.

In June 2010, the FASB issued an exposure draft, Revenue from Contracts with Customers, which would supersede most of the existing guidance on revenue recognition in Accounting Standards Codification (“ASC”) Topic 605, Revenue Recognition. In November 2011, the FASB re-exposed this draft and it expects a final standard to be issued during the first half of calendar 2014. As the standard-setting process is still ongoing, the Company is unable to determine the impact this proposed change in accounting will have in the Company’s consolidated financial statements at this time.

12

Table of Contents

In August 2010, the FASB issued an exposure draft, Leases, which would result in significant changes to the accounting requirements for both lessees and lessors in ASC Topic 840, Leases. In May 2013, the FASB re-exposed this draft and the comment period closed in September 2013. As the standard-setting process is still ongoing, the Company is unable to determine the impact this proposed change in accounting will have in the Company’s consolidated financial statements at this time.

3. INVENTORIES

Inventories are comprised of NUEDEXTA finished goods and the active pharmaceutical ingredients of NUEDEXTA, dextromethorphan (“DM”) and quinidine (“Q”), as well as the active pharmaceutical ingredient docosanol.

The composition of inventories as of December 31, 2013 and September 30, 2013 is as follows:

| December 31, 2013 |

September 30, 2013 |

|||||||

| (audited) | ||||||||

| Raw materials |

$ | 929,234 | $ | 936,856 | ||||

| Work in progress |

49,265 | 36,453 | ||||||

| Finished goods |

400,464 | 521,056 | ||||||

|

|

|

|

|

|||||

| Total inventory |

1,378,963 | 1,494,365 | ||||||

| Less: current portion |

(605,833 | ) | (710,179 | ) | ||||

|

|

|

|

|

|||||

| Non-current portion |

$ | 773,130 | $ | 784,186 | ||||

|

|

|

|

|

|||||

The amount classified as non-current inventories is comprised of the raw material components for NUEDEXTA, dextromethorphan and quinidine, which will be used in the manufacture of NUEDEXTA capsules beyond the Company’s one year operating cycle.

4. ACCRUED EXPENSES

Accrued expenses at December 31, 2013 and September 30, 2013 are as follows:

| December 31, 2013 |

September 30, 2013 |

|||||||

| (audited) | ||||||||

| Accrued royalties, rebates, chargebacks, and distribution fees (1) |

$ | 6,224,729 | $ | 5,525,103 | ||||

| Accrued research and development expenses |

2,144,010 | 2,146,210 | ||||||

| Accrued selling and marketing expenses |

1,589,570 | 2,139,429 | ||||||

| Accrued general and administrative expenses |

1,455,611 | 1,752,966 | ||||||

| Other current liabilities |

422,826 | 344,862 | ||||||

|

|

|

|

|

|||||

| Total accrued expenses |

$ | 11,836,746 | $ | 11,908,570 | ||||

|

|

|

|

|

|||||

| (1) | Accrued royalties, rebates, chargebacks and distribution fees are directly impacted by product revenue and will fluctuate over time in relation to the change in product revenue. |

5. DEFERRED REVENUES

The following table sets forth as of December 31, 2013, the deferred revenue balances for the Company’s sale of future Abreva® royalty rights to Drug Royalty USA.

| Drug Royalty USA Agreement |

||||

| Deferred revenues as of September 30, 2013 |

$ | 1,288,514 | ||

| Changes during the period: |

||||

| Recognized as revenues during period |

(648,049 | ) | ||

|

|

|

|||

| Deferred revenues as of December 31, 2013 |

$ | 640,465 | ||

|

|

|

|||

13

Table of Contents

Drug Royalty USA Agreement — In November 2002, the Company sold to Drug Royalty USA an undivided interest in the Company’s rights to receive future Abreva royalties under the license agreement with GSK for $24.1 million (the “Drug Royalty Agreement” and the “GSK License Agreement,” respectively). Under the Drug Royalty Agreement, Drug Royalty USA has the right to receive royalties from GSK on sales of Abreva until the expiration of the patent for Abreva on April 28, 2014. The Company retained the right to receive 50% of all royalties (a net of 4%) under the GSK License Agreement for annual net sales of Abreva in the U.S. and Canada in excess of $62.0 million. During the three months ended December 31, 2013 and 2012, the Company recognized royalties related to the annual net Abreva sales in excess of $62.0 million in the amount of approximately $1.4 million and $1.2 million, respectively, which is included in the accompanying condensed consolidated statements of operations as revenues from royalties.

Revenues are recognized when earned, collection is reasonably assured and no additional performance of services is required. The Company classified the proceeds received from Drug Royalty USA as deferred revenue, and is recognizing the revenue over the life of the license agreement because of the Company’s continuing involvement over the term of the Drug Royalty Agreement. Such continuing involvement includes overseeing the performance of GSK and its compliance with the covenants in the GSK License Agreement, monitoring patent infringement, adverse claims or litigation involving Abreva, and undertaking to find a new license partner in the event that GSK terminates the agreement. The Drug Royalty Agreement contains both covenants and events of default that require such performance on the Company’s part. Therefore, nonperformance on the Company’s part could result in default of the arrangement, and could give rise to additional rights in favor of Drug Royalty USA under a separate security agreement with Drug Royalty USA, which could result in loss of the Company’s rights to share in future Abreva royalties if wholesale sales by GSK exceed $62.0 million a year. The deferred revenue is being recognized as revenue using the “units-of-revenue method” over the life of the license agreement. Based on a review of the Company’s continuing involvement, the Company concluded that the sale proceeds did not meet any of the rebuttable presumptions that would require classification of the proceeds as debt.

6. NOTES PAYABLE

In May 2012, the Company entered into a Loan and Security Agreement (the “Loan Agreement”) with Oxford Finance LLC and Silicon Valley Bank. The Loan Agreement provides for a term loan of $30.0 million which was funded upon closing of the transaction in June 2012. Under the terms of the Loan Agreement, interest accrues on the outstanding balance at a rate of 8.95% per annum. In the third fiscal quarter of 2013, the Company met the criteria to extend the interest only payment for six months. Therefore, the Company will make monthly payments of interest only until January 1, 2014 (the “Amortization Date”). Beginning on the Amortization Date, the outstanding loan balance will be repaid in thirty equal monthly payments of principal and interest. In addition to the original principal, a final payment equal to 7% of the original principal amount of the loan will be due thirty months from the Amortization Date. The final payment is being accreted as interest expense over the term of the debt using the interest method and the related liability of approximately $1.3 million and $1.1 million as of December 31, 2013 and September 30, 2013, respectively, is included in other liabilities in the accompanying condensed consolidated balance sheets.

In accordance with the terms of the Loan Agreement, the Company issued to the lenders warrants to purchase shares of the Company’s common stock equal to 4.55% of the original principal at a price per share equal to the lower of the 10-day average share price prior to closing or the price per share on the day of funding. Accordingly, the Company issued to the lenders warrants to purchase 491,007 shares of the Company’s common stock at an exercise price of $2.78 per share. The relative fair value of the warrants was approximately $1.2 million and was estimated using the Black-Scholes model with the following assumptions: fair value of the Company’s common stock at issuance of $2.80 per share; ten year contractual term; 96.7% volatility; 0% dividend rate; and a risk-free

14

Table of Contents

interest rate of 1.8%. The relative fair value of the warrants was recorded as a debt discount, decreasing notes payable and increasing additional paid-in capital on the accompanying condensed consolidated balance sheets. The debt discount is being amortized to interest expense over the term of the debt using the interest method. For the three months ended December 31, 2013 and 2012, debt discount amortization was approximately $102,000 and $138,000, respectively.

The loan is secured by a first priority security interest in all of the Company’s assets, other than its intellectual property and its rights under license agreements granting it rights to intellectual property.

The Loan Agreement contains standard affirmative and restrictive covenants. The affirmative covenants include, among other items, that the Company maintain a minimum sales level relative to projected NUEDEXTA revenues, measured on a trailing three-month basis, or maintain cash and cash equivalents in accounts subject to control agreements in favor of the collateral agent equal to at least 1.5 times the outstanding amount of obligations under the Loan Agreement. Additionally, the affirmative and restrictive covenants, among other items, restrict the Company’s ability to incur additional indebtedness or guarantees; incur liens; make investments, loans and acquisitions; consolidate or merge; sell assets, including capital stock of subsidiaries; alter the business of the Company; engage in transactions with affiliates; and enter into agreements limiting dividends and distributions of certain subsidiaries. The Loan Agreement also includes events of default, including, among other things, payment defaults, breaches of representations, warranties or covenants, certain bankruptcy events, the occurrence of certain material adverse changes, and a commercial, generic version of NUEDEXTA (for the treatment of PBA) becoming available. Upon the occurrence of an event of default and following any cure periods (if applicable), a default interest rate of an additional 5.0% per annum may be applied to the outstanding loan balances, and the lenders may declare all outstanding obligations immediately due and payable and take such other actions as set forth in the Loan Agreement. As of December 31, 2013, the Company was in compliance with all covenants in the Loan Agreement.

7. COMPUTATION OF NET LOSS PER COMMON SHARE

Basic net loss per common share is computed by dividing net loss by the weighted-average number of common shares outstanding during the period, excluding restricted stock that has been issued but is not yet vested. Diluted net loss per common share is computed by dividing net loss by the weighted-average number of common shares outstanding during the period plus additional weighted-average common equivalent shares outstanding during the period. Common equivalent shares result from the assumed exercise of outstanding stock options and warrants (the proceeds of which are then presumed to have been used to repurchase outstanding stock using the treasury stock method) and the vesting of restricted shares of common stock. In loss periods, certain of the common equivalent shares are excluded from the computation of diluted net loss per share, because their effect would have been anti-dilutive.

For the three month periods ended December 31, 2013 and 2012, the following options and warrants to purchase shares of common stock and restricted stock units were excluded from the computation of diluted net loss per share, as the inclusion of such shares would be anti-dilutive:

| 2013 | 2012 | |||||||

| Stock options |

10,071,519 | 9,848,654 | ||||||

| Stock warrants |

53,957 | 764,066 | ||||||

| Restricted stock units (1) |

2,705,176 | 2,887,017 | ||||||

| (1) | Includes 1,319,590 and 1,124,126 shares of restricted stock at December 31, 2013 and 2012, respectively, awarded to directors that have vested but are still restricted until the directors resign. |

8. STOCKHOLDERS’ EQUITY

Common stock

During the three months ended December 31, 2013, the Company issued 196,950 shares of common stock in connection with the vesting of restricted stock units and 12,560 shares of common stock in connection with the exercise of stock options resulting in proceeds of approximately $30,000.

15

Table of Contents

During the three months ended December 31, 2013, restricted stock unit awards for a total of 52,375 shares awarded to directors vested, but the issuance and delivery of these shares are deferred until the director resigns.

Warrants Outstanding

As of December 31, 2013, warrants to purchase 53,957 shares of the Company’s common stock at an exercise price of $2.78 per share remained outstanding and exercisable. The warrants were issued in connection with the Loan Agreement (see Note 6, “Notes Payable”) and expire in May 2022.

9. EMPLOYEE EQUITY INCENTIVE PLANS

The Company currently has one equity incentive plan, which is the 2005 Equity Incentive Plan (the “2005 Plan”). The 2000 Stock Option Plan (the “2000 Plan”) and the 2003 Equity Incentive Plan (the “2003 Plan” and, together with 2000 Plan and 2005 Plan, the “Plans”) are expired and the Company no longer grants share-based awards from these plans, however, grants are still outstanding under each of these plans at December 31, 2013. All of the Plans were approved by the stockholders, except for the 2003 Plan, which was approved solely by the Board of Directors. Share-based awards are subject to terms and conditions established by the Compensation Committee of the Company’s Board of Directors. The Company’s policy is to issue new common shares upon the exercise of stock options, conversion of share units or purchase of restricted stock.

During the three month periods ended December 31, 2013 and 2012, the Company granted share-based awards under the 2005 Plan. Under the 2005 Plan, options to purchase shares, restricted stock units, restricted stock and other share-based awards may be granted to the Company’s directors, employees and consultants. Pursuant to the provisions for annual increases of the 2005 Plan, the number of authorized shares of common stock for issuance increased by 325,000 shares effective November 15, 2013. As of December 31, 2013, the Company had an aggregate of 12,507,121 shares of its common stock reserved for future issuance. Of those shares, 12,315,995 shares were related to outstanding options and other awards and 191,126 shares were available for future grants of share-based awards. As of December 31, 2013, no equity awards were outstanding to consultants. The Company may also, from time to time, issue share-based awards outside of the Plans to the extent permitted by NASDAQ rules. As of December 31, 2013, there were 460,700 equity awards that were issued outside of the Plans (inducement option grants) outstanding. None of the share-based awards are classified as a liability as of December 31, 2013.

Stock Options. Stock options are granted with an exercise price equal to the current market price of the Company’s common stock at the grant date and have 10-year contractual terms. For option grants to employees, generally 25% of the option shares vest and become exercisable on the first anniversary of the grant date and the remaining 75% of the option shares vest and become exercisable quarterly in equal installments thereafter over three years. Certain option awards provide for accelerated vesting if there is a change in control (as defined in the Plans).

Summaries of stock options outstanding and changes during the three months ended December 31, 2013 are presented below.

| Number of Shares |

Weighted Average Exercise Price per Share |

Weighted Average Remaining Contractual Term (In Years) |

Aggregate Intrinsic Value |

|||||||||||||

| Outstanding at September 30, 2013 |

8,823,041 | $ | 2.85 | |||||||||||||

| Granted |

1,309,556 | $ | 3.15 | |||||||||||||

| Exercised |

(12,560 | ) | $ | 2.41 | ||||||||||||

| Forfeited |

(48,518 | ) | $ | 2.94 | ||||||||||||

|

|

|

|||||||||||||||

| Outstanding at December 31, 2013 |

10,071,519 | $ | 2.89 | 7.5 | $ | 8,496,661 | ||||||||||

|

|

|

|||||||||||||||

| Vested and expected to vest in the future at December 31, 2013 |

9,665,402 | $ | 2.88 | 7.4 | $ | 8,269,135 | ||||||||||

|

|

|

|||||||||||||||

| Exercisable at December 31, 2013 |

5,383,232 | $ | 2.81 | 6.3 | $ | 5,780,736 | ||||||||||

|

|

|

|||||||||||||||

The weighted average grant-date fair value of options granted during the three month periods ended December 31, 2013 and 2012 was $2.15 and $1.78 per share, respectively. The total intrinsic value of options exercised during the three month periods ended December 31, 2013 and 2012 was approximately $25,000 and $39,000, respectively,

16

Table of Contents

based on the differences in market prices on the dates of exercise and the option exercise prices. As of December 31, 2013, the total unrecognized compensation cost related to unvested options was approximately $9.8 million which is expected to be recognized over the weighted-average period of 2.8 years, based on the vesting schedules. No tax benefit was realized for the tax deductions from option exercise of the share-based payment arrangements in the three month periods ended December 31, 2013 and 2012.

The fair value of each option award is estimated on the date of grant using the Black-Scholes model, which uses the assumptions noted in the following table. Expected volatilities are based on historical volatility of the Company’s common stock and other factors. The expected term of options granted is based on analyses of historical employee termination rates and option exercises. The expected risk-free interest rate is based on the U.S. Treasury yield for a period consistent with the expected term of the option in effect at the time of the grant. The dividend yield is based on the Company’s expectation of not paying dividends in the foreseeable future.

Assumptions used in the Black-Scholes model for options granted during the three months ended December 31, 2013 were as follows:

| Expected volatility |

84% | |

| Expected term in years |

5.4 | |

| Expected risk-free interest rate (zero coupon U.S. Treasury Note) |

1.5%-1.7% | |

| Expected dividend yield |

0% |

Restricted stock units (“RSU”). RSUs granted to employees generally vest based on three or four years of continuous service from the date of grant. RSUs granted to non-employee directors generally vest over the term of one year from the grant date and are not released until the awardee’s termination of service. Vesting for non-employee director grants allow for accelerated vesting of RSUs in the case of a non-employee director’s resignation where either: (i) he/she has served for at least four years as a member of the Board and is in good standing at the time of resignation, or (ii) he/she resigns for reasons related to health or family matters and is otherwise in good standing at the time of resignation.

The following table summarizes the RSU activities for the three months ended December 31, 2013:

| Number of Shares |

Weighted Average Grant Date Fair Value |

|||||||

| Unvested at September 30, 2013 |

1,637,210 | $ | 2.40 | |||||

| Vested |

(249,325 | ) | $ | 2.51 | ||||

| Forfeited |

(2,299 | ) | $ | 2.06 | ||||

|

|

|

|||||||

| Unvested at December 31, 2013 |

1,385,586 | $ | 2.38 | |||||

|

|

|

|||||||

The grant-date fair value of RSUs granted during the three months ended December 31, 2012 was approximately $2.4 million. There were no RSUs granted during the three months ended December 31, 2013. As of December 31, 2013, the total unrecognized compensation cost related to unvested shares was approximately $2.7 million which is expected to be recognized over a weighted-average period of 2.3 years, based on the vesting schedules.

At December 31, 2013, there were 1,319,590 shares of restricted stock with a weighted-average grant date fair value of $2.11 per share awarded to directors that have vested but are still restricted until the director resigns.

During the three months ended December 31, 2013, the Company granted 961,316 RSUs and 464,024 performance-based RSUs to employees contingent on approval of the 2014 Incentive Plan (“2014 Plan”) by the Company’s shareholders. These awards are not considered granted until the 2014 Plan is approved and are not reflected in the above table of unvested RSUs.

17

Table of Contents

10. COMMITMENTS AND CONTINGENCIES

Legal contingencies –

NUEDEXTA ABBREVIATED NEW DRUG APPLICATION (“ANDA”) Litigation

In fiscal 2011 and 2012, the Company received Paragraph IV certification notices from five separate companies contending that certain of its patents listed in the FDA’s publication, “Approved Drug Products with Therapeutic Equivalence Evaluation” (“FDA Orange Book”) (U.S. Patents 7,659,282 (“’282 Patent”), 8,227,484 (“’484 Patent”) and RE 38,115 (“’115 Patent”), which expire in August 2026, July 2023 and January 2016, respectively) are invalid, unenforceable and/or will not be infringed by the manufacture, use, sale or offer for sale of a generic form of NUEDEXTA as described in those companies’ abbreviated new drug application (“ANDA”). The FDA Orange Book provides potential competitors, including generic drug companies, with a list of issued patents covering approved drugs. In August 2011 and March 2012, the Company filed lawsuits in the U.S District Court for the District of Delaware against Par Pharmaceutical, Inc. and Par Pharmaceutical Companies, Inc. (collectively “Par”), Actavis South Atlantic LLC and Actavis, Inc. (collectively “Actavis”), Wockhardt USA, LLC and Wockhardt, Ltd. (collectively, “Wockhardt”), Impax Laboratories, Inc. (“Impax”) and Watson Pharmaceuticals, Inc., Watson Laboratories, Inc. and Watson Pharma, Inc. (collectively “Watson”) (Par, Actavis, Wockhardt, Impax and Watson, collectively the “Defendants”). In September and October 2012, the Company filed lawsuits in the U.S. District Court for the District of Delaware against the Defendants. All lawsuits (collectively, the “ANDA Actions”) were filed on the basis that the Defendants’ submissions of their respective ANDAs to obtain approval to manufacture, use, sell, or offer for sale generic versions of NUEDEXTA prior to the expiration of the ‘282 Patent, the ‘484 Patent and the ‘115 Patent listed in the FDA Orange Book constitute infringement of one or more claims of those patents. On October 31, 2012, Watson announced the divestiture of its ANDA for a generic form of NUEDEXTA to Sandoz, Inc. (“Sandoz”). As a result of Sandoz’ acquisition and maintenance of said ANDA, on May 30, 2013, the Company filed suit in the U.S. District Court for the District of Delaware against Sandoz. This suit was filed on the basis that Sandoz’ ANDA to obtain approval to manufacture, use, sell, or offer for sale generic versions of NUEDEXTA prior to the expiration of the ’282 Patent, the ’484 Patent and the ’115 Patent listed in the FDA Orange Book constitutes infringement of one or more claims of those patents.

On December 3, 2012, the Company received a Memorandum Opinion and Order (the “Order”) issued by Judge Leonard P. Stark of the United States District Court for the District of Delaware (the “Court”) related to the Markman hearing held October 5, 2012 in the Company’s ongoing patent infringement case against the Defendants. The Order establishes the meaning of patent claim terms in dispute between the parties. After comprehensive briefing and oral argument, Judge Stark’s Order adopted the Company’s proposed or stipulated patent term constructions.

A bench trial was held in September 2013 and concluded on October 15, 2013. The Company is currently awaiting Judge Stark’s decision.

On August 9, August 30, and September 6, 2013, Avanir entered into settlement agreements with Sandoz, Actavis and Wockhardt, respectively, to resolve pending patent litigation in response to their ANDAs seeking approval to market generic versions of NUEDEXTA capsules. The settlement agreements grant Sandoz, Actavis and Wockhardt the right to begin selling a generic version of NUEDEXTA on July 30, 2026, or earlier under certain circumstances. The parties also filed stipulations and orders of dismissal with the United States District Court for the District of Delaware which conclude the litigation with respect to Sandoz, Actavis and Wockhardt. The settlements do not end the Company’s ongoing litigation against the other two ANDA filers.

The 30-month stay associated with the filing of the ANDA Actions expired on December 30, 2013. In order to launch a generic form of NUEDEXTA, the Defendants must first receive FDA approval and as of February 4, 2014, the FDA has not granted approval to any Defendant’s ANDA. The Company intends to vigorously enforce its intellectual property rights relating to NUEDEXTA, but the Company cannot predict the outcome of these ANDA Actions.

18

Table of Contents

MASTERS LITIGATION

On January 14, 2014, a purported shareholder of the Company brought a claim against the Company and its directors, as well as a former director, in connection with the Company’s 2014 Annual Meeting proxy statement. The action is captioned Masters v. Avanir Pharmaceuticals, Inc., et al., Case No. 14-cv-00053, and is pending in the United States District Court for the Central District of California (the “Masters Action”). The Masters Action complaint alleges that the defendants violated Section 14(a) of the Securities Exchange Act, and further alleges that the individual defendants breached their fiduciary duties, based upon purported deficiencies in disclosures relating to Proposal 4 contained in the Company’s proxy statement, with respect to the Company’s equity compensation plan and practices. The complaint seeks, among other things, equitable relief that would enjoin the consummation of the shareholder vote on Proposal 4, declaratory relief, and attorney’s fees and costs. The Company intends to defend the Master’s Action vigorously, however, all litigation is inherently uncertain, and there can be no assurance that its defense of these or similar actions would be successful.

GENERAL AND OTHER

In the ordinary course of business, the Company may face various claims brought by third parties and the Company may, from time to time, make claims or take legal actions to assert the Company’s rights, including intellectual property rights as well as claims relating to employment and the safety or efficacy of products. Any of these claims could subject the Company to costly litigation and, while the Company generally believes that it has adequate insurance to cover many different types of liabilities, the Company’s insurance carriers may deny coverage or policy limits may be inadequate to fully satisfy any damage awards or settlements. If this were to happen, the payment of any such awards could have a material adverse effect on the Company’s consolidated operations, cash flows and financial position. Additionally, any such claims, whether or not successful, could damage the Company’s reputation and business. Management believes the outcomes of currently pending claims and lawsuits will not likely have a material effect on the Company’s consolidated operations or financial position.

In addition, it is possible that the Company could incur termination fees and penalties if it elected to terminate contracts with certain vendors, including clinical research organizations.

Guarantees and Indemnities. The Company indemnifies its directors, officers and certain executives to the maximum extent permitted under the laws of the State of Delaware, and various lessors in connection with facility leases for certain claims arising from such facilities or leases. Additionally, the Company periodically enters into contracts that contain indemnification obligations, including contracts for the purchase and sale of assets, wholesale distribution agreements, clinical trials, pre-clinical development work and securities offerings. These indemnification obligations provide the contracting parties with the contractual right to have Avanir pay for the costs associated with the defense and settlement of claims, typically in circumstances where Avanir has failed to meet its contractual performance obligations in some fashion.

19

Table of Contents

The maximum amount of potential future payments under such indemnifications is not determinable. The Company has not incurred significant costs related to these guarantees and indemnifications, and no liability has been recorded in the condensed consolidated financial statements for guarantees and indemnifications as of December 31, 2013 and September 30, 2013.

Center for Neurologic Study (“CNS”) — The Company holds the exclusive worldwide marketing rights to NUEDEXTA for certain indications pursuant to an exclusive license agreement with CNS.

The Company paid a $75,000 milestone upon FDA approval of NUEDEXTA for the treatment of PBA in fiscal 2011. In addition, the Company is obligated to pay CNS a royalty ranging from approximately 5% to 8% of net U.S. GAAP revenue generated by sales of NUEDEXTA. During the three months ended December 31, 2013 and 2012, royalties of approximately $1.2 million and $744,000, respectively, were recorded to cost of product sales in the accompanying condensed consolidated statements of operations. Under certain circumstances, the Company may have the obligation to pay CNS a portion of net revenues received if the Company sublicenses NUEDEXTA to a third party.

Under the agreement with CNS, the Company is required to make payments on achievements of up to a maximum of ten milestones, based upon five specific clinical indications. Maximum payments for these milestone payments could total approximately $1.1 million if the Company pursued the development of NUEDEXTA for all five of the licensed indications. In general, individual milestones range from $75,000 to $125,000 for each accepted NDA and a similar amount for each approved NDA in addition to the royalty discussed above on net U.S. GAAP revenues. The Company does not have the obligation to develop additional indications under the CNS license agreement.

Concert Pharmaceuticals, Inc. – The Company holds the exclusive worldwide marketing rights to develop and commercialize Concert’s d-DM compounds for the potential treatment of neurological and psychiatric disorders, as well as certain rights to other deuterium-modified dextromethorphan compounds pursuant to a license agreement with Concert.

Under the agreement with Concert, the Company is obligated to make milestone and royalty payments to Concert based on successful advancement of d-DM products for one or more indications in the United States, Europe, and Japan. Individual milestone payments range from $2.0 — $6.0 million, $1.5 — $15.0 million, and $25.0 — $60.0 million for clinical, regulatory and commercial targets respectively, and in aggregate could total over $200 million. Royalty payments are tiered, beginning in the single-digits and increasing to the low double-digits for worldwide net sales of d-DM products exceeding $1.0 billion annually. As of December 31, 2013, the Company has paid $2.0 million for milestones that have been achieved pursuant to this agreement, which was recorded in the second quarter of fiscal 2013.

OptiNose AS — In July 2013, the Company entered into an exclusive license agreement for the development and commercialization of a novel Breath Powered intranasal delivery system containing low-dose sumatriptan powder to treat acute migraine, AVP-825.

AVP-825 is licensed from OptiNose. Under the terms of the agreement, OptiNose received an up-front cash payment of $20.0 million in fiscal 2013, which was recorded to research and development expense. The Company and OptiNose will share certain development costs. OptiNose is eligible to receive up to an additional $90.0 million in aggregate milestone payments resulting from the achievement of future clinical, regulatory and commercial milestones. In addition, following product approval, Avanir will be required to make tiered royalty payments to OptiNose of a low double-digits percentage of net sales in the United States, Canada and Mexico.

11. SEGMENT INFORMATION

The Company operates its business on the basis of a single reportable segment, which is the business of discovery, development and commercialization of novel therapeutics for chronic diseases. The Company’s chief operating decision-maker is the Chief Executive Officer, who evaluates the Company as a single operating segment.

20

Table of Contents

The Company categorizes revenues by geographic area based on selling location. All of the Company’s operations are currently located in the United States; therefore, total revenues for the three month periods ended December 31, 2013 and 2012 are attributed to the United States. All long-lived assets at December 31, 2013 and September 30, 2013 are located in the United States.

The Company sells NUEDEXTA to a limited number of wholesalers. Three wholesalers accounted for 91% and 86% of net product sales for the three month periods ended December 31, 2013 and 2012, respectively. In addition, the three wholesalers accounted for 86% and 91% of trade receivables at December 31, 2013 and September 30, 2013, respectively.

12. SUBSEQUENT EVENTS

The Company has evaluated subsequent events through the filing date of this Form 10-Q, and determined that no subsequent events have occurred that would require recognition in the condensed consolidated financial statements or disclosure in the notes thereto other than discussed in the accompanying notes.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS