Attached files

| file | filename |

|---|---|

| EX-10.37 - AMENDED AND RESTATED WARRANT AGREEMENT - Gannett Co., Inc. | d639494dex1037.htm |

| EX-21.1 - SUBSIDIARIES OF NEW MEDIA INVESTMENT GROUP INC. - Gannett Co., Inc. | d639494dex211.htm |

| EX-23.3 - CONSENT OF ERNST & YOUNG LLP REGARDING GATEHOUSE - Gannett Co., Inc. | d639494dex233.htm |

| EX-23.4 - CONSENT OF ERNST & YOUNG LLP REGARDING DOW JONES LOCAL MEDIA - Gannett Co., Inc. | d639494dex234.htm |

| EX-23.2 - CONSENT OF ERNST & YOUNG LLP REGARDING NEW MEDIA - Gannett Co., Inc. | d639494dex232.htm |

Table of Contents

As filed with the Securities and Exchange Commission on January 28, 2014

Registration No. 333-192736

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2 to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

New Media Investment Group Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 2711 | 38-3910250 | ||||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) | ||||

1345 Avenue of the Americas

New York, New York, 10105

212-479-3160

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Cameron D. MacDougall, Esq.

Fortress Investment Group LLC

1345 Avenue of the Americas

New York, New York 10105

212-479-1522

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a copy to:

Duane McLaughlin, Esq.

Cleary Gottlieb Steen & Hamilton LLP

One Liberty Plaza

New York, New York 10006

(212) 225-2000

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be |

Proposed Maximum Aggregate Offering Price per Share |

Proposed Offering Price(3) |

Amount of Registration Fee(3)(4) | ||||

| Common stock, par value $0.01 per share |

25,373,120 | N/A(2) | $329,175,635 | $42,397.82 | ||||

|

| ||||||||

|

| ||||||||

| (1) | This prospectus (“Prospectus”) relates to shares of common stock, par value $0.01 per share, of New Media Investment Group Inc. (“New Media” or the “Registrant”) which will be distributed pursuant to a spin-off transaction to the holders of common stock, par value $0.01 per share, of Newcastle Investment Corp. (“Newcastle”). The amount of New Media common stock to be registered represents the maximum number of shares of New Media common stock that will be distributed to the holders of Newcastle common stock upon consummation of the spin-off. Immediately prior to the time of the spin-off, Newcastle will hold approximately 84.6% of New Media’s outstanding shares of common stock. |

| (2) | Not included pursuant to Rule 457(o) under the Securities Act. |

| (3) | Estimated solely for purposes of calculating the registration fee pursuant to Rule 457(f)(2) of the Securities Act. The Company estimates that the book value of the securities to be registered is equal to $329,175,635, which represents approximately 84.6% of the book value of New Media as of September 29, 2013. |

| (4) | Previously paid. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such dates as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this Prospectus is not complete and may be changed. We may not issue these securities until the registration statement filed with the Securities and Exchange Commission is effective. This Prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION

PRELIMINARY PROSPECTUS DATED JANUARY 28, 2014

New Media Investment Group Inc.

Common Stock

(Par Value, $0.01 per share)

This Prospectus is being furnished to you as a stockholder of Newcastle Investment Corp. (“Newcastle”) in connection with the planned distribution (the “Distribution” or the “spin-off”) by Newcastle to its stockholders of all the shares of common stock, par value $0.01 per share, of New Media Investment Group Inc. (“New Media”) (the “Common Stock”) held by Newcastle immediately prior to the spin-off. Immediately prior to the time of the Distribution, Newcastle will hold 84.6% of New Media’s outstanding shares of Common Stock.

At the time of the Distribution, Newcastle will distribute all of the outstanding shares of Common Stock held by Newcastle on a pro rata basis to holders of Newcastle common stock. Each share of Newcastle common stock outstanding as of 5:00 PM, Eastern Time, on February 6, 2014, the record date for the spin-off (the “Record Date”), will entitle the holder thereof to receive 0.07219 shares of Common Stock. The Distribution will be made in book-entry form. Fractional shares of Common Stock will not be distributed in the spin-off. Holders of Newcastle common stock will receive cash in lieu of fractional shares of New Media Common Stock.

The Distribution will be effective after the close of trading on the New York Stock Exchange (the “NYSE”) on February 13, 2014, which we refer to hereinafter as the “Distribution Date.” Immediately after the Distribution is completed, we will be a publicly traded company independent from Newcastle.

No action will be required of you to receive shares of Common Stock, which means that:

| • | no vote of Newcastle stockholders is required in connection with this Distribution and we are not asking you for a proxy and you are requested not to send us a proxy; |

| • | you will not be required to pay for the shares of our Common Stock that you receive in the Distribution; and |

| • | you do not need to surrender or exchange any of your shares of Newcastle common stock in order to receive shares of our Common Stock, or take any other action in connection with the spin-off. |

There is currently no trading market for our Common Stock, although we expect that a limited market, commonly known as a “when-issued” trading market, will develop on or shortly before the Record Date for the Distribution, and we expect “regular-way” trading of New Media Common Stock on a major U.S. national securities exchange to begin on the first trading day following the completion of the Distribution. New Media’s Common Stock has been authorized for listing on the NYSE under the symbol “NEWM,” subject to official notice of issuance.

In reviewing this Prospectus, you should carefully consider the matters described under “Risk Factors” beginning on page 32 of this Prospectus.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

This Prospectus does not constitute an offer to sell or the solicitation of an offer to buy any securities.

The date of this Prospectus is , 2014.

Table of Contents

i

Table of Contents

Presentation of Information

Except as otherwise indicated or unless the context otherwise requires, we have presented in this Prospectus the historical consolidated financial information of GateHouse Media, Inc. and its consolidated subsidiaries (“GateHouse” or our “Predecessor”). Unless the context otherwise requires, any references in this Prospectus to “we,” “our,” “us” and the “Company” refer to New Media Investment Group Inc. and its consolidated subsidiaries as in effect upon the completion of the Distribution. For periods prior to the Effective Date (as defined below) any references in this Prospectus to “we,” “our,” “us” and the “Company” refer to GateHouse, our Predecessor, and its consolidated subsidiaries, unless the context requires otherwise. Subsequent to the Effective Date, any references to GateHouse refer to GateHouse Media, LLC and its consolidated subsidiaries and any references to GateHouse Media Intermediate Holdco, Inc. refer to GateHouse Media Intermediate Holdco, LLC. References in this Prospectus to “Newcastle” generally refer to Newcastle Investment Corp. and its consolidated subsidiaries, unless the context requires otherwise. All figures included in this Prospectus are as of September 29, 2013, unless stated otherwise.

ii

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE SPIN-OFF

The following questions and answers briefly address some commonly asked questions about the spin-off. They may not include all the information that is important to you. We encourage you to read carefully this entire Prospectus and the other documents to which we have referred you. We have included references in certain parts of this section to direct you to a more detailed discussion of each topic presented in this section.

What will Newcastle stockholders receive in the spin-off?

To effect the spin-off, Newcastle will make a distribution of all of the outstanding shares of New Media Common Stock held by Newcastle to Newcastle’s common stockholders as of the Record Date, which will be 5:00 PM, Eastern Time, on February 6, 2014. For each share of Newcastle common stock held on the Record Date for the Distribution, Newcastle will distribute 0.07219 shares of New Media Common Stock. The Distribution will be made in book-entry form. Fractional shares of Common Stock will not be distributed in the spin-off. Instead, as soon as practicable after the spin-off American Stock Transfer & Trust Company, LLC, the distribution agent, will aggregate the fractional shares of our Common Stock and sell these shares in the open market at prevailing market prices and distribute the applicable portion of the aggregate net cash proceeds of these sales to each holder who otherwise would have been entitled to receive a fractional share in the spin-off. You will not be entitled to any interest on the amount of the cash payment made in lieu of fractional shares.

Newcastle stockholders will not be required to pay for shares of our Common Stock received in the Distribution, or to surrender or exchange any shares of Newcastle common stock or take any other action to be entitled to receive our Common Stock. The Distribution of our Common Stock will not cancel or affect the number of outstanding shares of Newcastle common stock.

Immediately after the Distribution, holders of Newcastle common stock as of the Record Date will hold 84.6% of the outstanding shares of our Common Stock. Based on the number of shares of Newcastle common stock outstanding on January 24, 2014, Newcastle expects to distribute approximately 25,373,120 shares of our Common Stock in the spin-off. For a more detailed description, see “The Spin-Off and Restructuring” in this Prospectus.

Why is Newcastle spinning off New Media?

Newcastle’s board of directors periodically reviews strategic alternatives. Newcastle’s board of directors determined upon careful review and consideration in accordance with the applicable standard of review under Maryland law that the spin-off of New Media is in the best interests of Newcastle. Newcastle’s board of directors believes that media assets are currently undervalued and being sold at substantial discounts. Newcastle’s board of directors also believes that New Media’s value can be increased over time through a strategy aimed at acquiring local media assets and organically growing New Media’s digital marketing business. In addition, Newcastle’s board of directors believes New Media’s prospects would be enhanced by being able to operate unfettered by REIT requirements. Accordingly, Newcastle’s board of directors has determined that the separation of New Media from Newcastle, as opposed to a sale of New Media’s Common Stock or other transaction, will provide Newcastle’s stockholders with the best opportunity to benefit from the anticipated appreciation of New Media’s value over time. Moreover, Newcastle’s board of directors believes that the execution risk of a spin-off is lower than for other types of transactions. Newcastle’s board of directors’ determination was based on a number of factors, including those set forth below.

| • | Added focus and simplification. We believe the spin-off of New Media will enhance Newcastle’s focus on its primary strategy of opportunistically investing in, and actively managing, a variety of real-estate related and other investments. The spin-off will simplify Newcastle’s business by separating an asset class (media assets) that is unrelated to the remainder of Newcastle’s investment portfolio. As a result, we believe the spin-off will facilitate investor and analyst understanding of Newcastle’s core businesses. In addition, the spin-off will create a dedicated vehicle to pursue a significant investment opportunity in the media industry. |

1

Table of Contents

| • | Tailored capital structure and financing options. New Media and Newcastle will have distinct and unrelated businesses, and the spin-off will enable each to create a capital structure tailored to its individual needs. In addition, tailored capital structures will facilitate each company’s ability to pursue acquisitions, possibly using common stock as currency, and other strategic alliances. Following the spin-off, each company may be able to attain more favorable financing terms on a stand-alone basis than Newcastle could obtain currently. |

| • | Newcastle’s Real Estate Investment Trust (“REIT”) status. As a REIT, Newcastle is not suited to own an operating business indefinitely. Newcastle’s current investment in New Media originated with a 2007 debt investment in GateHouse. GateHouse became overleveraged in the financial crisis, and Newcastle determined to maximize the value of its investment by proposing and supporting a restructuring that resulted in the conversion of its debt into equity. Following the Restructuring, a spin-off will facilitate Newcastle’s compliance with the REIT qualification tests. |

Additionally, in determining whether to effect the spin-off, Newcastle’s board of directors also considered the costs and risks relating to the spin-off, including: (i) potential costs and disruptions to the businesses as a result of the spin-off, (ii) risks of being unable to achieve the benefits expected from the spin-off, (iii) the reaction of Newcastle’s stockholders to the spin-off, (iv) the risk that one-time and ongoing costs of the spin-off may be greater than expected and (v) the tax impact of the spin-off to Newcastle and its stockholders. Newcastle’s board of directors determined that in the aggregate the potential benefits of the spin-off outweighed the potential negative factors. See “Risk Factors—Risks Related to the Distribution” and “The Spin-Off and Restructuring—Reasons for the Distribution.”

The anticipated benefits of the spin-off are based on a number of assumptions, and there can be no assurance that such benefits will materialize to the extent anticipated or at all. In the event that the spin-off does not result in such benefits, the costs associated with the transaction and the expenses New Media will incur as an independent public company, including management compensation and general and administrative expenses, could have a negative effect on each company’s financial condition and ability to make distributions to its stockholders. For more information about the risks associated with the separation, see “Risk Factors.”

What businesses will Newcastle engage in after the spin-off?

Newcastle will continue to be a real estate investment trust that focuses on opportunistically investing in, and actively managing, a variety of real estate-related and other investments.

Who is entitled to receive shares of our Common Stock in the spin-off?

Holders of Newcastle common stock as of 5:00 PM, Eastern Time, on February 6, 2014, the Record Date for the spin-off, will be entitled to receive shares of our Common Stock in the spin-off.

When will the Distribution occur?

We expect that Newcastle will distribute the shares of our Common Stock on February 13, 2014 to holders of record of Newcastle common stock as of 5:00 PM, Eastern Time, on February 6, 2014, subject to certain conditions described under “The Spin-Off and Restructuring—Conditions to the Distribution.”

What do I need to do to receive my shares of New Media Common Stock?

Nothing, but we urge you to read this Prospectus carefully. Stockholders who hold Newcastle common stock as of the Record Date will not need to take any action to receive your shares of our Common Stock in the Distribution. No stockholder approval of the Distribution is required or sought. We are not asking you for a proxy, and you are requested not to send us a proxy. You will not be required to make any payment, surrender or exchange your shares of Newcastle common stock or take any other action to receive your shares of our

2

Table of Contents

Common Stock. If you own Newcastle common stock as of 5:00 PM, Eastern Time, on the Record Date, Newcastle, with the assistance of American Stock Transfer & Trust Company, LLC, the distribution agent, will electronically issue shares of our Common Stock to you or to your brokerage firm on your behalf by way of direct registration in book-entry form. The distribution agent will mail you a book-entry account statement that reflects your shares of New Media Common Stock, or your bank or brokerage firm will credit your account for the shares. If you sell shares of Newcastle common stock in the “regular-way” market through the Distribution Date, you will also sell your right to receive shares of New Media Common Stock in the Distribution. Following the Distribution, stockholders whose shares are held in book-entry form may request that their shares of New Media Common Stock held in book-entry form be transferred to a brokerage or other account at any time, without charge.

Will I receive physical certificates representing shares of New Media Common Stock following the Distribution?

No. Following the Distribution, neither Newcastle nor New Media will be issuing physical certificates representing shares of New Media Common Stock. Instead, Newcastle, with the assistance of American Stock Transfer & Trust Company, LLC, the distribution agent, will electronically issue shares of our Common Stock to you or to your bank or brokerage firm on your behalf by way of direct registration in book-entry form. The distribution agent will mail you a book-entry account statement that reflects your shares of New Media Common Stock, or your bank or brokerage firm will credit your account for the shares. A benefit of issuing stock electronically in book-entry form is that there will be none of the physical handling and safekeeping responsibilities that are inherent in owning physical stock certificates.

What will govern my rights as a New Media stockholder?

Your rights as a New Media stockholder will be governed by Delaware law, as well as our amended and restated certificate of incorporation and our amended and restated bylaws. A description of these rights is included in this Prospectus under the heading “Description of Our Capital Stock.”

Who will be the stockholders of New Media Common Stock after the Distribution?

Immediately following the Distribution, Newcastle stockholders as of the Record Date for the Distribution will own 84.6% of our Common Stock. The remainder of the outstanding Common Stock will be owned by holders of GateHouse’s Outstanding Debt (as defined below) who elected to receive Common Stock in the Restructuring (as defined below) of GateHouse. See “The Spin-Off and Restructuring,” “Restructuring Agreements” and Note 21 to GateHouse’s Consolidated Financial Statements, “Subsequent Events and Going Concern Considerations” in this Prospectus for more information.

Are there risks associated with the spin-off and our business after the spin-off?

Yes. You should carefully review the risks described in this Prospectus under the heading “Risk Factors” beginning on page 32.

Is stockholder approval needed in connection with the spin-off?

No vote of Newcastle stockholders is required or will be sought in connection with the spin-off.

Where will I be able to trade shares of New Media Common Stock?

There is not currently a public market for New Media Common Stock. New Media’s Common Stock has been authorized for listing on the NYSE under the symbol “NEWM,” subject to official notice of issuance. We anticipate that trading in shares of our Common Stock will begin on a “when-issued” basis on or shortly before

3

Table of Contents

the Record Date and will continue through the Distribution Date and that “regular-way” trading in shares of our Common Stock will begin on the first trading day following the Distribution Date. If trading begins on a “when-issued” basis, you may purchase or sell our Common Stock up to and including through the Distribution Date, but your transaction will not settle until after the Distribution Date. We cannot predict the trading prices for our Common Stock before, on or after the Distribution Date. If the Distribution is cancelled, your transaction will not settle and will have to be disqualified.

What if I want to sell my Newcastle common stock or New Media Common Stock?

You should consult with your financial advisors, such as your stockbroker, bank or tax advisor. Neither Newcastle nor New Media makes any recommendations on the purchase, retention or sale of Newcastle common stock or the shares of New Media Common Stock to be distributed in the spin-off.

If you decide to sell any shares before the Distribution, you should make sure your stockbroker, bank or other nominee understands whether you want to sell your Newcastle common stock or the shares of Common Stock you will receive in the Distribution. If you sell your Newcastle common stock in the “regular-way” market up to and including the Distribution Date, you will also sell your right to receive shares of Common Stock in the Distribution. If you own Newcastle common stock as of 5:00 PM, Eastern Time, on the Record Date and sell those shares on the “ex-distribution” market up to and including the Distribution Date, you will still receive the shares of Common Stock that you would be entitled to receive in respect of the Newcastle common stock you owned as of 5:00 PM, Eastern Time, on the Record Date. See “The Spin-Off and Restructuring—Trading Between the Record Date and Distribution Date” in this Prospectus for more information.

Will I be taxed on the shares of New Media Common Stock that I receive in the Distribution?

Yes. The Distribution will be in the form of a taxable special dividend to Newcastle stockholders. An amount equal to the fair market value of the shares of our Common Stock received by you will be treated as a taxable dividend to the extent of your ratable share of any current or accumulated earnings and profits of Newcastle, with the excess treated as a non-taxable return of capital to the extent of your tax basis in Newcastle common stock and any remaining excess treated as capital gain. If this special dividend is distributed in the structure and timeframe currently anticipated, the special dividend is expected to satisfy a portion of Newcastle’s 2014 REIT taxable income distribution requirements. For a more detailed discussion, see “Material U.S. Federal Income Tax Consequences of the Distribution.”

How will the Distribution affect my tax basis and holding period in Newcastle common stock?

Your tax basis in shares of Newcastle held at the time of the Distribution will be reduced (but not below zero) to the extent the fair market value of the shares of our Common Stock distributed by Newcastle in the Distribution exceeds Newcastle’s current and accumulated earnings and profits, as adjusted to take account of other distributions made by Newcastle in the taxable year that includes the Distribution. Your holding period for such Newcastle shares will not be affected by the Distribution. See “Material U.S. Federal Income Tax Consequences of the Distribution.” You should consult your own tax advisor as to the particular tax consequences of the Distribution to you, including the applicability of any U.S. federal, state, local and non-U.S. tax laws.

What will my tax basis and holding period be for the stock of New Media that I receive in the Distribution?

Your tax basis in the shares of our Common Stock received will equal the fair market value of such shares on the date of the Distribution. Your holding period for such shares will begin the day after the date of the Distribution. See “Material U.S. Federal Income Tax Consequences of the Distribution.”

You should consult your own tax advisor as to the particular tax consequences of the Distribution to you, including the applicability of any U.S. federal, state, local and non-U.S. tax laws.

4

Table of Contents

Can Newcastle decide to cancel the Distribution or modify its terms if all conditions to the Distribution have been met?

Yes. Although the Distribution is subject to the satisfaction or waiver of certain conditions, Newcastle has the right to not to complete the Distribution if at any time prior to the Distribution Date (even if all such conditions are satisfied), its board of directors determines, in its sole discretion, that the Distribution is not in the best interest of Newcastle or that market conditions are such that it is not advisable to separate New Media from Newcastle.

The conditions to the Distribution are that (i) our registration statement on Form S-1, of which this Prospectus is a part, shall have become effective under the Securities Act of 1933, as amended (the “Securities Act”), and no stop order related to the registration statement shall be in effect; (ii) the listing of our Common Stock on the NYSE shall have been approved, subject to official notice of issuance; (iii) the Plan shall have been approved by the United States Bankruptcy Court for the District of Delaware (the “Bankruptcy Court”) without any appeals by any parties; and (iv) no order, injunction or decree issued by any court of competent jurisdiction or other legal restraint or prohibition preventing consummation of the Distribution or any of the transaction related thereto, shall be in effect. We note that other than the federal securities laws, there are no federal or state regulatory requirements with which we must comply. If Newcastle’s board of directors were to waive a material condition to or abandon the Distribution, Newcastle would notify its stockholders of the decision by filing a Current Report on Form 8-K.

Does New Media plan to pay dividends?

We currently expect New Media to distribute a substantial portion of free cash flow as a dividend, subject to satisfactory financial performance and approval by New Media’s board of directors. The Board of Directors’ determinations regarding dividends will depend on a variety of factors, including the Company’s GAAP net income, free cash flow generated from operations or other sources, liquidity position and potential alternative uses of cash, such as acquisitions, as well as economic conditions and expected future financial results. However, our ability to pay dividends is subject to a number of risks and uncertainties, and there can be no assurance regarding whether we will pay dividends in the future. See, for example, “Risk Factors—Risks Related to Our Business—We may not be able to pay dividends in accordance with our announced intent or at all.”

Will the number of Newcastle shares I own change as a result of the Distribution?

No. The number of shares of Newcastle common stock you own will not change as a result of the Distribution.

What will happen to the listing of Newcastle common stock?

Nothing. It is expected that after the Distribution of New Media Common Stock, Newcastle common stock will continue to be traded on the NYSE under the symbol “NCT.”

Will the Distribution affect the market price of my Newcastle shares?

Yes. As a result of the Distribution, we expect the trading price of shares of Newcastle common stock immediately following the Distribution to be lower than immediately prior to the Distribution because the trading price will no longer reflect the value of New Media’s assets. Furthermore, until the market has fully analyzed the value of Newcastle without New Media’s assets, the price of Newcastle shares may fluctuate significantly. In addition, although Newcastle believes that over time following the separation, the common stock of the separated companies should have a higher aggregate market value, on a fully distributed basis and assuming the same market conditions, than if Newcastle were to remain under its current configuration, there can be no assurance, and thus the combined trading prices of Newcastle common stock and New Media Common Stock after the Distribution may be equal to or less than the trading price of shares of Newcastle common stock before the Distribution.

5

Table of Contents

Where can Newcastle stockholders get more information?

Before the Distribution, if you have any questions relating to the Distribution, you should contact:

Newcastle Investment Corp.

Investor Relations

1345 Avenue of the Americas

New York, NY 10105

Tel: 212-479-3195

www.newcastleinv.com

After the Distribution, if you have any questions relating to our Common Stock, you should contact:

New Media Investment Group Inc.

Investor Relations

1345 Avenue of the Americas

New York, NY 10105

Tel: 212-479-3160

www.newmediainvestmentgroup.com

6

Table of Contents

This summary of certain information contained in this Prospectus may not include all the information that is important to you. To understand fully and for a more complete description of the terms and conditions of the spin-off, you should read this Prospectus in its entirety and the documents to which you are referred. See “Where You Can Find More Information.”

Our Company

We will be a newly listed company primarily focused on investing in a high quality, diversified portfolio of local media assets and on growing our existing online advertising and digital marketing businesses.

We are one of the largest publishers of locally based print and online media in the United States as measured by number of daily publications. We operate in 338 markets across 24 states. Our portfolio of products, which includes 435 community publications, 353 related websites, 329 mobile sites and six yellow page directories, serves more than 128,000 business advertising accounts and reaches approximately 10 million people on a weekly basis.

Our print and online products focus on the local community from both a content and advertising standpoint. As a result of our focus on small and midsize markets, we are usually the primary, and sometimes the sole, provider of comprehensive and in-depth local market news and information in the communities we serve. Our content is primarily devoted to topics that we believe are highly relevant and of interest to our audiences such as local news and politics, community and regional events, youth sports, opinion and editorial pages, and local schools.

More than 83% of our daily newspapers have been published for more than 100 years and 99% have been published for more than 50 years. We believe that the longevity of our publications demonstrates the value and relevance of the local information that we provide and has created a strong foundation of reader loyalty as well as a highly recognized media brand name in each community we serve.

The newspaper industry has experienced declining revenue and profitability over the past several years due to, among other things, advertisers’ shift from print to digital media and general market conditions. GateHouse, our Predecessor, was affected by this trend and experienced net losses of $160.8 million during the nine month period ended September 29, 2013 and $29.8 million during the fiscal year ended December 30, 2012. Total revenue decreased by 1.9% to $356.2 million for the nine months ended September 29, 2013 and 5.1% to $488.6 million for the year ended December 30, 2012.

We acquired our operations as part of the restructuring of GateHouse. On September 27, 2013, GateHouse commenced Chapter 11 cases in the Bankruptcy Court (the “Restructuring”) in which it sought confirmation of its Joint Prepackaged Chapter 11 Plan (as modified, amended or supplemented from time to time, the “Plan”) sponsored by Newcastle, as the holder of the majority of the Outstanding Debt (as defined below). The Bankruptcy Court confirmed the Plan on November 6, 2013. GateHouse effected the transactions contemplated by the Plan and emerged from Chapter 11 protection on November 26, 2013 (the “Effective Date”).

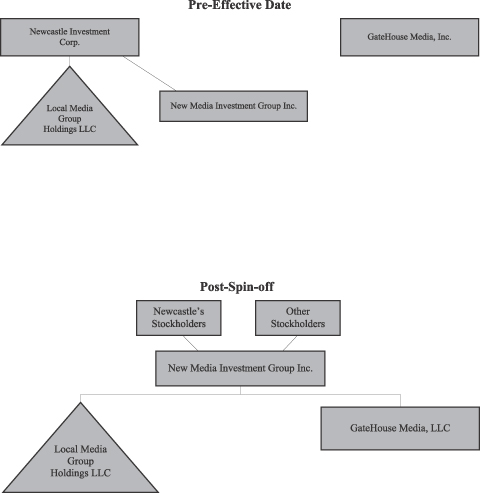

The Plan effectuated the Restructuring of GateHouse. On the Effective Date (1) reorganized GateHouse became a wholly owned subsidiary of New Media as a result of (a) the cancellation and discharge of the currently outstanding equity interests of Gatehouse (the holders of which received warrants issued by New Media) and (b) the issuance of equity interests in the reorganized GateHouse to New Media; (2) Local Media Group Holdings LLC (“Local Media Parent”), which was a wholly owned subsidiary of Newcastle, became a wholly owned subsidiary of New Media as a result of Newcastle’s transfer of Local Media Parent to New Media; and (3) all of

7

Table of Contents

GateHouse’s Outstanding Debt was cancelled and discharged and the holders of the Outstanding Debt received, at their option, their pro rata share of the (i) Cash-Out Offer (as defined below) and/or (ii) New Media Common Stock and the net proceeds of new credit facilities raised by reorganized GateHouse. Pursuant to the Cash-Out Offer, Newcastle offered to buy the claims of the holders of the Outstanding Debt (as defined below). As a result of these transactions, Newcastle owns 84.6% of New Media as of the Effective Date. See “—Recent Developments,” “The Spin-Off and Restructuring,” “Restructuring Agreements” and Note 21 to GateHouse’s Consolidated Financial Statements, “Subsequent Events and Going Concern Considerations.”

As of the Effective Date of the Plan, New Media’s debt structure consists of multiple credit facilities. The Revolving Credit, Term Loan and Security Agreement (the “First Lien Credit Facility”) dated November 26, 2013 by and among GateHouse, GateHouse Media Intermediate Holdco, Inc. (“GMIH”), certain wholly-owned subsidiaries of GMIH (collectively with GMIH and GateHouse, the “Loan Parties”), PNC Bank, National Association, as the administrative agent, Crystal Financial LLC, as term loan B agent and each of the lenders party thereto provides for (i) a term loan A in the aggregate principal amount of $25 million, a term loan B in the aggregate principal amount of $50 million, and a revolving credit facility in an aggregate principal amount of up to $40 million (of which $25 million was funded on the Effective Date). Borrowings under the First Lien Credit Facility bear interest at a rate per annum equal to (i) with respect to the revolving credit facility, the applicable Revolving Interest Rate (as defined the First Lien Credit Agreement), (ii) with respect to the term loan A, the Term Loan A Rate (as defined in the First Lien Credit Agreement) and (iii) with respect to the term loan B, the Term Loan B Rate (as defined in the First Lien Credit Agreement). Amounts outstanding under the term loans and revolving credit facility will be fully due and payable on November 26, 2018.

The Term Loan and Security Agreement (the “Second Lien Credit Facility” and together with the First Lien Credit Facility, the “New Credit Facilities”) dated November 26, 2013 by and among the Loan Parties, Mutual Quest Fund and each of the lenders party thereto provides for a term loan in an aggregate principal amount of $50 million. Borrowings under the Second Lien Credit Facility bear interest, at the Loan Parties’ option, equal to (1) the LIBOR Rate (as defined in the Second Lien Credit Facility) plus 11.00% or (2) the Alternate Base Rate (as defined in the Second Lien Credit Facility) plus 10.00%. The outstanding principal will be fully due and payable on the maturity date of November 26, 2019.

Pursuant to the Plan, holders of the Outstanding Debt who elected to receive New Media Common Stock received their pro rata share of the proceeds of the New Credit Facilities, net of certain transaction expenses (the “Net Proceeds”). The Net Proceeds distributed to holders of the Outstanding Debt totaled $149 million. GateHouse’s entry into the New Credit Facilities was not a condition to the effectiveness of the Plan. The proceeds of additional drawings of the revolving credit facility under the First Lien Credit Facility after the Effective Date will be applied towards ongoing working capital needs, general corporate purposes, capital expenditures and potential acquisitions.

Additionally, the Credit Agreement dated September 3, 2013, by and among Local Media Parent, the borrowers party thereto, the lenders party thereto, Capital One Business Credit Corp., as successor to Credit Suisse AG, Cayman Islands Branch, as administrative agent and collateral agent and Credit Suisse Loan Funding LLC, as lead arranger (the “Local Media Credit Facility”) provides for a $33.0 million senior secured term loan which was funded on September 3, 2013 and a senior secured asset-based revolving credit facility in an aggregate principal amount of up to $10 million, whose full availability was activated on October 25, 2013.

The Restructuring significantly reduced New Media’s interest expense. In addition, New Media intends to focus its business strategy on building its digital marketing business and growing its online advertising business, which we believe will offset many of the challenges experienced by GateHouse. With its new capital structure and digital focus, we believe that New Media will be able to create stockholder value given its strengths and strategy. However, there can be no assurance that we will be profitable. See “Risk Factors.”

8

Table of Contents

We intend to create stockholder value through growth in our revenue and cash flow by expanding our digital marketing business, growing our online advertising business and pursuing strategic acquisitions of high quality local media assets. However, there is no guarantee that we will be able to accomplish any of these strategic initiatives. Our strategy will be to acquire and operate traditional local media businesses and transform them from print-centric operations to dynamic multi-media operations, through our existing online advertising and digital marketing businesses. We will also leverage our existing platform to operate these businesses more efficiently. We believe all of these initiatives will lead to revenue and cash flow growth for New Media and will enable us to pay dividends to our stockholders. We expect to distribute a substantial portion of our free cash flow as a dividend to stockholders, subject to satisfactory financial performance and approval by our Board of Directors. The Board of Directors’ determinations regarding dividends will depend on a variety of factors, including the Company’s GAAP net income, free cash flow generated from operations or other sources, liquidity position and potential alternative uses of cash, such as acquisitions, as well as economic conditions and expected future financial results.

Our Manager

We are managed by FIG LLC (our “Manager”), an affiliate of Fortress, pursuant to the terms of a Management and Advisory Agreement dated as of November 26, 2013 (the “Management Agreement”), between us and our Manager. We will draw upon the long-standing expertise and resources of Fortress, a global investment management firm with approximately $58.0 billion in fee paying assets under management as of September 30, 2013.

Pursuant to the terms of the Management Agreement, our Manager, subject to oversight by our Board of Directors, is responsible for: (1) performing day-to-day functions, (2) determining investment criteria in conjunction with, and subject to the supervision of, our Board of Directors, (3) sourcing, analyzing and executing on investments and sales, (4) performing investment and liability management duties, including financing and hedging, and (5) performing financial and accounting management. For its services, our Manager is entitled to an annual management fee and eligible to receive incentive compensation that is based on our performance.

Our Manager also manages Newcastle, a publicly traded REIT that pursues a broad range of real estate related investments. Our management team will not be required to exclusively dedicate their services to us and will provide services for other entities affiliated with our Manager, including, but not limited to, Newcastle.

Reasons for Distribution

Newcastle’s board of directors periodically reviews strategic alternatives. The Newcastle board determined upon careful review and consideration in accordance with the applicable standard of review under Maryland law that the spin-off of New Media is in the best interests of Newcastle. Newcastle’s board of directors believes that media assets are currently undervalued and being sold at substantial discounts. Newcastle’s board of directors also believes that New Media’s value can be increased over time through a strategy aimed at acquiring local media assets and organically growing New Media’s digital marketing business. In addition, Newcastle’s board of directors believes New Media’s prospects would be enhanced by being able to operate unfettered by REIT requirements. Accordingly, Newcastle’s board of directors has determined that the separation of New Media from Newcastle, as opposed to a sale of New Media’s Common Stock or other transaction, will provide Newcastle’s stockholders with the best opportunity to benefit from the anticipated appreciation of New Media’s value over time. Moreover, Newcastle’s board of directors believes that the execution risk of a spin-off is lower than for other types of transactions. Newcastle’s board of directors’ determination was based on a number of factors, including those set forth below.

| • | Added focus and simplification. We believe the spin-off of New Media will enhance Newcastle’s focus on its primary strategy of opportunistically investing in, and actively managing, a variety of |

9

Table of Contents

| real-estate related and other investments. The spin-off will simplify Newcastle’s business by separating an asset class (media assets) that is unrelated to the remainder of Newcastle’s investment portfolio. As a result, we believe the spin-off will facilitate investor and analyst understanding of Newcastle’s core businesses. In addition, the spin-off will create a dedicated vehicle to pursue a significant investment opportunity in the media industry. |

| • | Tailored capital structure and financing options. New Media and Newcastle will have distinct and unrelated businesses, and the spin-off will enable each to create a capital structure tailored to its individual needs. In addition, tailored capital structures will facilitate each company’s ability to pursue acquisitions, possibly using common stock as currency, and other strategic alliances. Following the spin-off, each company may be able to attain more favorable financing terms on a stand-alone basis than Newcastle could obtain currently. |

| • | Newcastle’s Real Estate Investment Trust (“REIT”) status. As a REIT, Newcastle is not suited to own an operating business indefinitely. Newcastle’s current investment in New Media originated with a 2007 debt investment in GateHouse. GateHouse became overleveraged in the financial crisis, and Newcastle determined to maximize the value of its investment by proposing and supporting a restructuring that resulted in the conversion of its debt into equity. Following the Restructuring, a spin-off will facilitate Newcastle’s compliance with the REIT qualification tests. |

Additionally, in determining whether to effect the spin-off, Newcastle’s board of directors also considered the costs and risks relating to the spin-off, including: (i) potential costs and disruptions to the businesses as a result of the spin-off, (ii) risks of being unable to achieve the benefits expected from the spin-off, (iii) the reaction of Newcastle’s stockholders to the spin-off, (iv) the risk that one-time and ongoing costs of the spin-off may be greater than expected and (v) the tax impact of the spin-off to Newcastle and its stockholders. Newcastle’s board of directors determined that in the aggregate the potential benefits of the spin-off outweighed the potential negative factors. See “Risk Factors—Risks Related to the Distribution” and “The Spin-Off and Restructuring—Reasons for the Distribution.”

Our Strengths

High Quality Assets with Leading Local Businesses. Our publications benefit from a long history in the communities we serve as one of the leading, and often sole, providers of comprehensive and in-depth local content. This has resulted in brand recognition for our publications, reader loyalty and high local audience penetration rates, which are highly valued by local advertisers. We continue to build on long-standing relationships with local advertisers and our in-depth knowledge of the consumers in our local markets.

Strong Value Proposition for Our Advertisers. Our portfolio enjoys a devoted readership in the local communities where we operate. By providing access to these communities, we help advertisers maximize the efficiency of their advertising spending. We offer advertisers several alternatives (daily, weekly, shopper, and niche print publications as well as an array of web, mobile and tablet products) to reach consumers and to tailor the nature and frequency of their marketing messages. We also offer advertisers the ability to target consumers based on their behavior online which is an effective and efficient way for businesses to market to their target customers.

Diverse Revenue Streams. Our revenue streams are diversified in terms of type of revenue, product source for revenue, geographic distribution of revenues and numbers of customers. We also benefit from our strong local franchises who serve local consumers and businesses in small to mid-size markets. During the twelve months ended September 29, 2013, we generated revenue in 338 markets across 24 states, serving a fragmented and diversified local customer base. During the nine months ended September 29, 2013, the Company generated approximately 41% of its total revenue in two states in the Northeast and approximately 28% of its total revenue

10

Table of Contents

in two states in the Midwest. For full year 2012, we served over 128,000 business advertising accounts in our publications, and our top 20 advertisers contributed less than 5% of our total revenues. Over 3.8 million classified advertisements were placed in our publications in 2012. Additionally, for the full year 2012 we generated 60% of revenue from print product advertising, 27% from subscription income from customers, 6% from digital advertising and 7% from commercial printing work for external customers and affiliated parties.

Scale Yields Operating Profit Margins and Allows Us to Realize Operating Synergies. We believe we can generate higher operating profit margins than our publications could achieve on a stand-alone basis by leveraging our operations and implementing revenue initiatives, especially digital initiatives, across a broader local footprint in a geographic cluster and by centralizing certain back office production, accounting, administrative and corporate operations. We also benefit from economies of scale in the purchase of insurance, newsprint and other large strategic supplies and equipment. Finally, we have the ability to further leverage our centralized services and buying power to reduce operating costs when making future strategic accretive acquisitions.

Local Business Profile Generates Significant Cash Flow. Our local business profile will allow us to generate significant recurring cash flow due to our diversified revenue base, operating profit margins and our low capital expenditure and working capital requirements. As a result of the Restructuring, which extinguished GateHouse’s Outstanding Debt, our interest and debt servicing expenses are significantly lower than GateHouse’s interest and debt servicing expenses. As of the Effective Date, our debt structure consists of the New Credit Facilities and the Local Media Credit Facility. We estimate that we will have significant available cash flow totaling $50 to $70 million in 2014 which we believe will create stockholder value through our investments in organic growth, investments in accretive acquisitions and the return of cash to stockholders in the form of dividends, subject to approval by our Board of Directors. We further believe the strong cash flows generated and available to be invested will lead to consistent future dividend growth.

Large Locally Focused Sales Force. We have large and well known feet on the street local sales forces in the markets we serve. They are generally one of the largest locally oriented media sales forces in their respective communities. Our sales forces and their respective local media brands tend to have strong credibility and trust within the local business communities. We have long-standing relationships with many local businesses and have the ability to get in the door with most local businesses due to these unique characteristics we enjoy. We believe that these qualities also provide leverage for our sales force to grow additional future revenue streams in our markets.

Ability to Acquire and Integrate New Assets. We have created a national platform for consolidating local media businesses and have demonstrated an ability to successfully identify, acquire and integrate local media asset acquisitions. We have acquired over $1.7 billion of assets since 2006. We have acquired both traditional newspaper and directory businesses. We have a very scalable infrastructure and platform to leverage with future acquisitions.

Experienced Management Team. Our senior management team is made up of executives who have an average of over 20 years of experience in the media industry, including strong traditional and digital media expertise. Our executive officers have broad industry experience with regard to both growing new digital business lines and identifying and integrating strategic acquisitions. Our management team also has key strengths in managing wide geographically disbursed teams, including the sales force, and identifying and centralizing duplicate functions across businesses leading to reduced core infrastructure costs.

The newspaper industry has experienced declining revenue and profitability over the past several years due to, among other things, advertisers’ shift from print to digital media and general market conditions. GateHouse, our Predecessor, was affected by this trend and experienced net losses of $160.8 million during the nine month period ended September 29, 2013 and $29.8 million during the fiscal year ended December 30, 2012. Total

11

Table of Contents

revenue decreased by 1.9% to $356.2 million for the nine months ended September 29, 2013 and 5.1% to $488.6 million for the year ended December 30, 2012. The Restructuring significantly reduced New Media’s interest expense. In addition, New Media intends to focus its business strategy on building its digital marketing business and growing its online advertising business, which we believe will offset many of the challenges experienced by GateHouse. With its new capital structure and digital focus, we believe that New Media will be able to create stockholder value given its strengths and strategy. However, there can be no assurance that we will be profitable. See “Risk Factors.”

Our Strategy

We intend to create stockholder value through growth in our revenue and cash flow by expanding our digital marketing business, growing our online advertising business and pursuing strategic acquisitions of high quality local media assets. However, there is no guarantee that we will be able to accomplish any of these strategic initiatives. Our strategy will be to acquire and operate traditional local media businesses and transform them from print-centric operations to dynamic multi-media operations, through our existing online advertising and digital marketing businesses. We will also leverage our existing platform to operate these businesses more efficiently. We believe all of these initiatives will lead to revenue and cash flow growth for New Media and will enable us to pay dividends to our stockholders, subject to satisfactory financial performance and approval by our Board of Directors. The Board of Directors’ determinations regarding dividends will depend on a variety of factors, including the Company’s GAAP net income, free cash flow generated from operations or other sources, liquidity position and potential alternative uses of cash, such as acquisitions, as well as economic conditions and expected future financial results. The key elements of our strategy include:

Maintain Our Leading Position in the Delivery of Proprietary Content in Our Communities. We seek to maintain our position as a leading provider of local content in the markets we serve and to leverage this position to strengthen our relationships with both readers and advertisers, thereby increasing penetration rates and market share. A critical aspect of this approach is to continue to provide local content that is not readily obtainable elsewhere and to be able to deliver that content to our customers across multiple print and digital platforms. We believe it is very important for us to protect the content from unauthorized users who use it for their own commercial purposes. We also believe it is important for us to develop subscription revenue streams from our digitally distributed content.

Stabilize Our Core Business Operations. We have four primary drivers in our strategic plans to stabilize our core business operations, including: (i) identifying permanent structural expense reductions in our traditional business cost infrastructure and re-deploying a portion of those costs toward future growth opportunities, primarily on the digital side of our business; (ii) accelerating the growth of both our digital audiences and revenues through improvements to current products, new product development, training, opportunistic changes in hiring to create an employee base with a more diversified skill set and sharing of best practices; (iii) accelerating our consumer revenue growth through subscription pricing increases and growth in our subscriber base, which we aim to improve by employing additional strategic customer acquisition techniques, driving digital only subscriber growth through our pay meter strategy and improving our customer retention programs; and (iv) stabilizing our core print advertising revenues through improvements to pricing (understanding and selling the unique value of our local audience reach and level of engagement, at the sales rep level), packaging of products for customers that will produce the best results for them (needs based selling), more technology and training for sales management and sales representatives and increased accountability through consistent setting of expectations and measuring against those expectations on a regular basis.

Grow New Digital Business and Revenue Streams Leveraging Key Strengths. We plan to scale and expand our two new recently created digital businesses, Propel Marketing and adhance media. Propel Marketing will allow us to sell digital marketing services to small and medium sized businesses (“SMBs”) both in and outside existing markets. The SMB demand for digital service solutions is great and represents a rapidly expanding

12

Table of Contents

opportunity. adhance media, our private advertising exchange, allows us to more fully monetize our (and third parties’) valuable unsold digital advertising space. Advertising bought programmatically through private exchanges is expected to grow rapidly over the next five years, especially in private exchanges where advertisers get priority access to the advertising space. We also aim to leverage our large local sales forces and strong local media brands to create new business opportunities at the local market level.

Pursue Strategic Accretive Acquisitions. We intend to capitalize on the highly fragmented and distressed newspaper and directory industries. We initially expect to focus our investments in the local newspaper and yellow page directory sectors, primarily in the United States. We believe we have a strong operational platform, which currently owns local newspaper and directory businesses, as well as a scalable digital services business, Propel Marketing. This platform, along with deep industry specific knowledge and experience that our management team has can be leveraged to reduce costs, stabilize the core business and grow digital revenues at acquired properties. The size and fragmentation of the addressable newspaper and yellow page directory market place in the United States, the greatly reduced valuation levels that exist in these industries, and our deep experience, make this an attractive place for our initial consolidation focus and capital allocation. Over the longer term we also believe there may be opportunity to diversify and acquire these types of assets internationally, as well other traditional local media assets such as broadcast TV, out of home advertising (billboards) and radio, in the United States and internationally.

Increase Sales Force Productivity. We aim to increase the effectiveness and productivity of our sales force and, in turn, help maximize advertising revenues. We also aim to shift the culture of our sales force from that of print-centric to multi-media and feel that is critical to our long term success. Our approach includes changes to sales force compensation to be more aligned with long term strategic goals, ongoing company-wide training of sales representatives and sales managers that focuses on strengthening their ability to perform needs based assessments and selling. We set expectations by sales representatives, manager and team and regularly evaluate the performance of our sales representatives and sales management against those expectations. We believe stronger accountability and measurement of our sales force, when combined with enhanced training and access to better technologies, demographic and marketing information, will lead to greater productivity and revenue from our sales force.

Introduce New Products or Modify Our Products to Enhance our Value Proposition to Local Businesses. We believe that our established positions in local markets, combined with our publishing and distribution capabilities, allow us to develop and customize new products to address the evolving interests and needs of our readers and local businesses. A primary source for product enhancement and growth we believe exists in the digital space. Product improvement and new product development across the web, mobile and tablets will be a key component to long term success. We are actively scaling web and mobile products, including deal platforms, digital service offerings, including Propel Marketing, mobile websites and applications, and we continue to expand on our offering of behavioral targeted and audience extension advertising options.

Pursue a Content-Driven Digital Strategy. As consumers continue to spend more time online especially with regard to consumption of news, we believe that we are well-positioned to increase our digital penetration and generate additional online audience and revenues due to both our ability to deliver unique local content online, and the relationship our local brand names have with readers and advertisers. We believe this presents an opportunity to increase our overall audience penetration rates and drive additional subscription revenues in each of the communities we serve. We have developed pay meters at most of our daily newspaper websites and several of our largest weeklies, which we use to charge customers fees for access to our content. These meters will enable us to grow our digital subscription income and capture revenues that shift to the web as consumers shift to the web. Finally, we intend to share resources across our organization in order to give each of our publications access to technology, digital management expertise, content and advertisers that they may not have been able to obtain or afford if they were operating independently.

13

Table of Contents

The newspaper industry has experienced declining revenue and profitability over the past several years due to, among other things, advertisers’ shift from print to digital media and general market conditions. GateHouse, our Predecessor, was affected by this trend and experienced net losses of $160.8 million during the nine month period ended September 29, 2013 and $29.8 million during the fiscal year ended December 30, 2012. Total revenue decreased by 1.9% to $356.2 million for the nine months ended September 29, 2013 and 5.1% to $488.6 million for the year ended December 30, 2012. The Restructuring significantly reduced New Media’s interest expense. In addition, New Media intends to focus its business strategy on building its digital marketing business and growing its online advertising business, which we believe will offset many of the challenges experienced by GateHouse. With its new capital structure and digital focus, we believe that New Media will be able to create stockholder value given its strengths and strategy. However, there can be no assurance that we will be profitable. See “Risk Factors.”

Challenges

We will likely face challenges commonly encountered by recently reorganized entities, including the risks that:

| • | even under our new capital structure, we may not be profitable; and |

| • | the Restructuring may cause our vendors and suppliers to stop providing supplies or services to us or to offer to provide such services or supplies only on unfavorable terms. |

As a publisher of locally based print and online media, we face a number of additional challenges, including the risks that:

| • | the growing shift within the publishing industry from traditional print media to digital forms of publication may compromise our ability to generate sufficient advertising revenues; |

| • | investments in growing our digital business may not be successful, which could adversely affect our results of operations; and |

| • | our advertising and circulation revenues may decline if we are unable to compete effectively with other companies in the local media industry. |

For more information about New Media’s risks and challenges, see “Risk Factors.”

Management Agreement

On the Effective Date, we entered into a Management Agreement with our Manager. Our Management Agreement requires our Manager to manage our business affairs subject to the supervision of our Board of Directors.

Our Management Agreement has an initial three-year term and will be automatically renewed for one-year terms thereafter unless terminated either by us or our Manager. From the commencement date of our Common Stock trading on the “regular way” market on a major U.S. national securities exchange (the “Listing”), our Manager is (a) entitled to receive from us a management fee, (b) eligible to receive incentive compensation that is based on our performance and (c) eligible to receive options to purchase New Media Common Stock upon the successful completion of an offering of shares of our Common Stock or any shares of preferred stock with an exercise price equal to the price per share paid by the public or other ultimate purchaser in the offering. In addition, we are obligated to reimburse certain expenses incurred by our Manager. Our Manager is also entitled to receive a termination fee from us under certain circumstances.

14

Table of Contents

The terms of our Management Agreement are summarized below and described in more detail under “Our Manager and Management Agreement” elsewhere in this Prospectus.

| Type |

Description | |

| Management Fee |

1.5% per annum of our total equity calculated and payable monthly in arrears in cash, commencing from the Listing. Total equity is generally the equity transferred by Newcastle on the date on which our Common Stock trades in the “regular way” market on a major U.S. national securities exchange, plus total net proceeds from any equity capital raised (including through stock offerings), plus certain capital contributions to subsidiaries, plus the equity value of assets contributed to the Company prior to or after the date of the Management Agreement, less capital distributions and repurchases of common stock. | |

| Incentive Compensation |

Our Manager is eligible to receive on a quarterly basis annual incentive compensation in an amount equal to the product of 25% of the dollar amount by which (a) the adjusted net income of the Company exceeds (b)(i) the weighted daily average total equity (plus cash capital raising costs), multiplied by (ii) a simple interest rate of 10% per annum. “Adjusted net income” means net income (computed in accordance with U.S. generally accepted accounting principles, (“GAAP”)), plus depreciation and amortization, and after adjustments for unconsolidated partnerships, joint ventures and permanent cash tax savings. Adjusted net income will be computed on an unconsolidated basis. The computation of adjusted net income may be adjusted at the direction of the independent directors based on changes in, or certain applications, of GAAP. | |

| Reimbursement of Expenses |

Commencing from the Listing, we will pay, or reimburse our Manager’s employees for performing certain legal, accounting, due diligence tasks and other services that outside professionals or outside consultants otherwise would perform, provided that such costs and reimbursements are no greater than those which would be paid to outside professionals or consultants on an arm’s-length basis. We also pay all operating expenses, except those specifically required to be borne by our Manager under our Management Agreement. | |

15

Table of Contents

| Our Manager is responsible for all costs incident to the performance of its duties under the Management Agreement, including compensation of our Manager’s employees, rent for facilities and other “overhead” expenses. The expenses required to be paid by us include, but are not limited to, issuance and transaction costs incident to the acquisition, disposition, operation and financing of our investments, legal and auditing fees and expenses, the compensation and expenses of our independent directors, the costs associated with the establishment and maintenance of any credit facilities and other indebtedness of ours (including commitment fees, legal fees, closing costs, etc.), expenses associated with other securities offerings of ours, the costs of printing and mailing proxies and reports to our stockholders, costs incurred by employees of our Manager for travel on our behalf, costs associated with any computer software or hardware that is used solely for us, costs to obtain liability insurance to indemnify our directors and officers and the compensation and expenses of our transfer agent. | ||

| Termination Fee |

The termination fee is payable to the Manager under the circumstances described in the section entitled “Our Manager and Management Agreement—Term; Termination.” The termination fee is equal to the sum of (1) the amount of the management fee during the 12 months immediately preceding the date of termination, and (2) the “Incentive Compensation Fair Value Amount,” if such option is exercised by the Company or the Manager. The Incentive Compensation Fair Value Amount is an amount equal to the Incentive Compensation that would be paid to the Manager if our assets were sold for cash at their then current fair market value (as determined by an appraisal, taking into account, among other things, the expected future value of the underlying investments). | |

| Grant of Options to Our Manager |

Commencing from the Listing, upon the successful completion of an offering of shares of our Common Stock or any shares of preferred stock, we will grant our Manager options equal to 10% of the number of shares being sold in the offering (excluding the shares issued to Newcastle in the Local Media Contribution (as defined below)), with an exercise price equal to the offering price per share paid by the public or other ultimate purchaser. For the avoidance of doubt, the listing of our Common Stock does not constitute an offering for purposes of this provision. | |

16

Table of Contents

Conflicts of Interest

Although we have established certain policies and procedures designed to mitigate conflicts of interest, there can be no assurance that these policies and procedures will be effective in doing so. It is possible that actual, potential or perceived conflicts of interest could give rise to investor dissatisfaction, litigation or regulatory enforcement actions.

One or more of our directors have responsibilities and commitments to entities other than us, including, but not limited to, Newcastle. For example, one of our directors is also a director of Newcastle. In addition, we do not have a policy that expressly prohibits our directors, officers, security holders or affiliates from engaging for their own account in business activities of the types conducted by us. Newcastle and other Fortress affiliates will not be restricted from pursuing other opportunities that may create conflicts or competition for us. However, our code of business conduct and ethics prohibits, subject to the terms of our amended and restated certificate of incorporation, the directors, officers and employees of our Manager from engaging in any transaction that involves an actual conflict of interest with us. See “Risk Factors—Risks Relating to Our Manager—There may be conflicts of interest in our relationship with our Manager, including with respect to corporate opportunities.”

Transactions between the Manager and any affiliate must be approved in advance by the majority of the independent directors and be determined by such independent directors to be in the best interests of the Company. If any affiliate transaction involving the acquisition of an asset from the Manager or an affiliate of the Manager is not approved in advance by a majority of the independent directors, then the Manager may be required to repurchase the asset at the purchase price (plus closing costs) to the Company.

The structure of the Manager’s compensation arrangement may have unintended consequences for us. We have agreed to pay our Manager a management fee that is not tied to our performance and incentive compensation that is based entirely on our performance. The management fee may not sufficiently incentivize our Manager to generate attractive risk-adjusted returns for us, while the performance-based incentive compensation component may cause our Manager to place undue emphasis on the maximization of earnings, including through the use of leverage, at the expense of other objectives, such as preservation of capital, to achieve higher incentive distributions. Investments with higher yield potential are generally riskier or more speculative than investments with lower yield potential. This could result in increased risk to the value of our portfolio of assets and your investment in us.

On the Effective Date, we entered into a Management Agreement with an affiliate of Fortress pursuant to which our management team will not be required to exclusively dedicate their services to us and will provide services for other entities affiliated with our Manager, including, but not limited to, Newcastle.

The ability of our Manager and its officers and employees to engage in other business activities, subject to the terms of our Management Agreement with our Manager, may reduce the amount of time our Manager, its officers or other employees spend managing us. In addition, we may engage in material transactions with our Manager or another entity managed by our Manager or one of its affiliates, including Newcastle, that present an actual, potential or perceived conflict of interest. It is possible that actual, potential or perceived conflicts could give rise to investor dissatisfaction, litigation or regulatory enforcement actions. Appropriately dealing with conflicts of interest is complex and difficult, and our reputation could be damaged if we fail, or appear to fail, to deal appropriately with one or more potential, actual or perceived conflicts of interest. Regulatory scrutiny of, or litigation in connection with, conflicts of interest could have a material adverse effect on our reputation, which could materially adversely affect our business in a number of ways, including causing an inability to raise additional funds, a reluctance of counterparties to do business with us, a decrease in the prices of our equity securities and a resulting increased risk of litigation and regulatory enforcement actions.

17

Table of Contents

Recent Developments

Support Agreement

On September 4, 2013, GateHouse and its affiliated debtors (the “Debtors”) announced that GateHouse, the Administrative Agent (as defined below), Newcastle and other lenders (the “Participating Lenders”) under the Amended and Restated Credit Agreement by and among certain affiliates of GateHouse, the lenders from time to time party thereto and Cortland Products Corp., as administrative agent (the “Administrative Agent”), dated February 27, 2007 (as amended, the “2007 Credit Facility”) entered into the Restructuring Support Agreement (the “Support Agreement”), effective September 3, 2013, as may be amended, supplemented or modified from time to time, in which the parties agreed to support, subject to the terms and conditions of the Support Agreement, the Restructuring pursuant to the Plan.

In the Support Agreement, the parties agreed to support the Restructuring of GateHouse’s obligations under the 2007 Credit Facility and certain interest rate swaps secured thereunder (collectively, the “Outstanding Debt”) and GateHouse’s equity pursuant to the Plan. Under the Support Agreement, each of the Participating Lenders agreed to (a) support and take any reasonable action in furtherance of the Restructuring, (b) timely vote their Outstanding Debt to accept the Plan and not change or withdraw such vote, (c) support approval of the disclosure statement for the Plan (the “Disclosure Statement”) and confirmation of the Plan, as well as certain relief to be requested by Debtors from the Bankruptcy Court, (d) refrain from taking any action inconsistent with the confirmation or consummation of the Plan, and (e) not propose, support, solicit or participate in the formulation of any plan other than the Plan. The Support Agreement terminated on the Effective Date of the Plan.

Pursuant to the Restructuring, Newcastle offered to purchase the Outstanding Debt claims in cash and at 40% of (i) $1,167,449,812.96 of principal of claims under the 2007 Credit Facility, plus (ii) accrued and unpaid interest at the applicable contract non-default rate with respect thereto, plus (iii) all amounts, excluding any default interest, arising from transactions in connection with interest rate swaps secured under the 2007 Credit Facility (the “Cash-Out Offer”) on the Effective Date. The holders of the Outstanding Debt had the option of receiving, in satisfaction of their Outstanding Debt, their pro rata share of the (i) Cash-Out Offer and/or (ii) New Media Common Stock and Net Proceeds, if any, of the New Credit Facilities. All pensions, trade and all other unsecured claims will be paid in the ordinary course.