Attached files

| file | filename |

|---|---|

| 8-K - 8-K - InvenTrust Properties Corp. | d655419d8k.htm |

Financial Update & Estimated Share Price

Presentation

Exhibit 99.1 |

2

Forward-Looking Statements

This presentation contains “forward-looking statements,” which

are not historical facts, within the meaning of the Private Securities Litigation Reform Act of 1995. We intend that

these forward-looking statements be subject to the safe harbor

provisions created by Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of

1934. These statements include statements regarding management's intentions,

beliefs, expectations, representations, plans or predictions of the future, including certain events for

which the timing and occurrence thereof require Board approval. Our actual

results, performance or achievements may differ materially from those expressed or implied by these

forward-looking statements. In some cases, you can identify

forward-looking statements by the use of words such as “may,” “could,” “should,” “expect,” “intend,” “plan,” “goal,”

“seek,” “anticipate,” “believe,”

“estimate,” “predict,” “variables,” “potential,” “continue,” “expand,” “maintain,” “create,” “strategies,” “likely,” “will,”

“would” and variations of these terms and similar

expressions, or the negative of these terms or similar expressions. Such forward-looking statements are necessarily based upon estimates and assumptions

that, while considered reasonable by us and our management, are inherently

uncertain. These forward-looking statements involve numerous risks and uncertainties that could cause

actual results to be materially different from those set forth in the

forward-looking statements. Factors that may cause actual results to differ materially from current expectations are

outlined more particularly in our filings with the SEC, including our Annual

Report on Form 10-K for the year ended December 31, 2012 and any subsequent Quarterly Reports on

Form 10-Q or Current Reports on Form 8-K, which filings are

available from the SEC. These factors include, but are not limited to:

• financial market disruptions current and future economic conditions

could adversely affect our ability to refinance or secure additional debt financing at attractive terms as well as

the values of our investments;

• our ongoing strategy involves the disposition of properties; however,

we may be unable to sell a property at acceptable terms and conditions, if at all. Our strategy also depends on

future acquisitions, and we may not be successful in identifying and

consummating these transactions; • our ability to successfully close certain sale transactions and

receive related proceeds is subject to a number of conditions outside our control, which may not be satisfied;

• there is no assurance that we will be able to continue paying cash

distributions or that distributions will increase over time; • an ongoing investigation by the SEC and the receipt of a derivative

demand by stockholders to conduct investigations and a lawsuit related to the derivative demand. The SEC’s

investigation, the derivative demand, or both could have a material adverse

impact on our business; • funding distributions from sources other than cash flow from

operating activities may negatively impact our ability to sustain or pay distributions and will result in us having less

cash available for other uses;

• there is no established public market for our shares, and

stockholders may not be able to sell their shares, including through our share repurchase program;

• increasing vacancy rates for certain classes of real estate assets

and possible disruption in the financial markets could adversely affect the value of our assets;

• we may suffer adverse consequences due to the financial difficulties,

bankruptcy or insolvency of our tenants; • our investments in equity and debt securities have materially

impacted, and may in the future, materially impact our results; • the financial covenants under our credit agreement may

restrict our ability to make distributions and our operating and acquisition activities;

• our borrowings may reduce the funds available for distribution and

increase the risk of loss since defaults may cause us to lose the properties securing the loans;

• two tenants generated a significant portion of our revenue, and

rental payment defaults by these significant tenants could adversely affect our results of operations;

• we are subject to conflicts of interest with affiliates of our

sponsor, which may affect our acquisition of properties and financial performance;

• The estimated value of our common stock is based on a number of

assumptions and estimates that may not be accurate or complete and is also subject to a number of limitations;

• we rely on our business manager and property managers to manage our

business and assets, and pay significant fees to these parties; and • if we fail to qualify as a REIT, our operations and distributions to

stockholders will be adversely affected. We caution you not to place undue reliance on any forward-looking

statements, which are made as of the date of this presentation. We undertake no obligation to update publicly

any of these forward-looking statements to reflect actual results, new

information or future events, changes in assumptions or changes in other factors affecting forward-looking

statements, except to the extent required by applicable law. If we update

one or more forward-looking statements, no inference should be drawn that we will make additional

updates with respect to those or other forward-looking statements.

This material is neither an offer to sell nor the solicitation of an offer

to buy any security, which can be made only by a prospectus which has been filed or registered with

appropriate state and federal regulatory agencies. The companies

depicted in the photographs herein may have proprietary interests in their trade names and trademarks and

nothing herein shall be considered to be an endorsement, authorization or

approval of Inland American by the companies. Furthermore, none of these companies are affiliated with

Inland American in any manner.

|

3

2013 Accomplishments

•

Announced a transaction to sell $2.1 billion of our net lease

assets

•

Sold an apartment portfolio for $460 million

•

Formed a new $600 million joint venture with PGGM, a highly

respected Dutch pension fund

•

Completed more than $1.2 billion in acquisitions, including 14

lodging properties, 3 student housing assets and 4 multi-tenant

retail centers |

4

2013 Accomplishments

•

Closed on a new $500 million credit facility

•

Proposed important charter changes to give us a greater ability

to execute on our long-term strategy.

WE DID ALL THIS WHILE

•

Minimized earnings dilution

•

Maintained our annualized distribution rate

•

Slightly increased the share value |

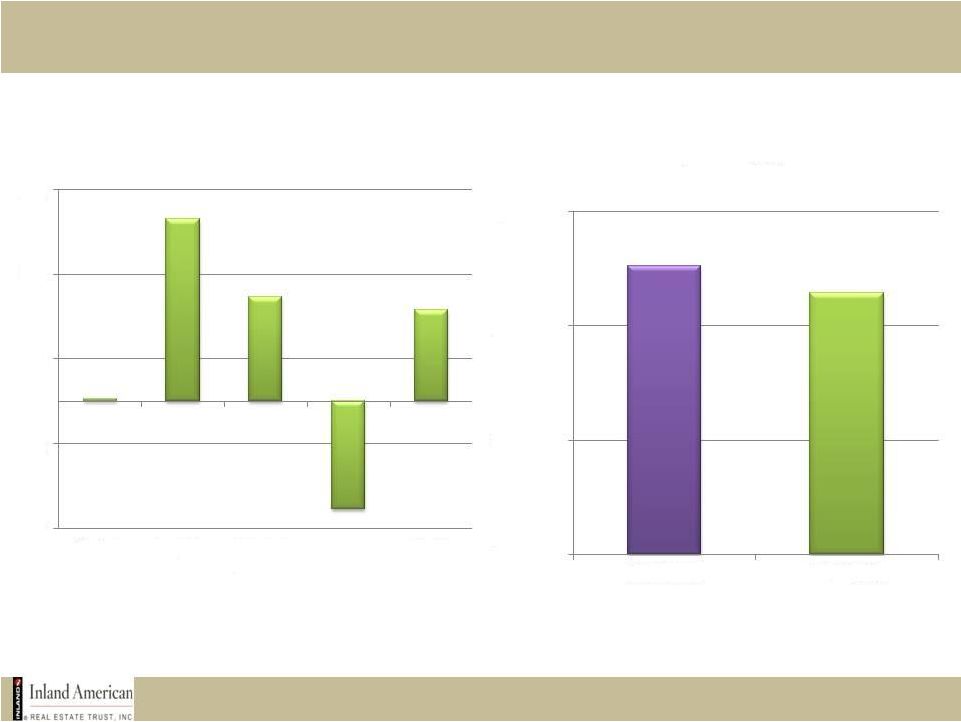

5

Quick Financial Update

Up 4.3% for the first 9 months of 2013

Same-Store NOI Growth

FFO

for

First

9

Months

-

$0.39

per

share

0.1%

8.6%

4.9%

4.3%

-6%

-2%

2%

6%

10%

Retail

Lodging

Student

Housing

Non-Core

Total

$350,521

$345,669

$300,000

$320,000

$340,000

$360,000

YTD 2013

YTD 2012

FFO in ‘000s

-5.1% |

6

Quick Financial Update

•

Total Cash = $384 million

(as of 9/30/13)

•

$4.8 billion of debt with a 45%* leverage ratio (as of 9/30/13)

•

Distributions Declared (as of 9/30/13)

* Based on line of credit covenants.

1 –

From August 2005 to April 2009

$336 million 2013 YTD

$2.7 billion paid since inception

As

of

Dec.

2013,

Inland

American

investors

have

received

between

$2.33

and $4.42

1

per share in distributions, depending on the timing of their

investment |

7

New Estimated Per Share Valuation Details

•

The

Audit

Committee

of

independent

directors

engaged

Real

Globe,

an

independent third party real estate advisory firm.

•

Real Globe valued each of our real estate assets based on a discounted cash

flow analysis. The per share value estimate was arrived at by

using the NAV method.

•

The NAV method:

Aggregates a value range of each of our real estate assets

Subtracts the debt including any fair market adjustments

And then divides the outcome by the total number of our common shares

outstanding

•

The audit committee received both Real Globe’s report and

recommendation as

well

as

a

report

and

recommendation

from

the

business

manager

and

on

December 19, 2013 unanimously recommended to the board a new estimated

per share value of $6.94 per share. |

8

FAQ #1

With the significant portfolio changes this

year, a comparison of the 2013 estimated

share value to the 2012 estimated share

value may be difficult, but can you

provide a same-store comparison? |

9

Significant Variances Between 2012 & 2013 NAV

•

Our same-store property values increased approximately

3.5% in the aggregate over last year.

•

This increase was offset by

Transaction costs from our $1.8 billion in sales through 9/30/13

A downward adjustment in the fair value of our debt

An increase in the number of shares outstanding.

No disposition or acquisition fees were paid to any affiliates of the

Inland American Business Manager for the transactions completed in

2013 |

10

FAQ #2

How does your estimated valuation

compare with the share price

performance of traded REITs? |

11

Differences Between Traded REIT Pricing & NAV

•

Traded REITs can trade above or below their NAV

•

Traded REIT indexes traded flat to slightly down this year

•

We do not believe the comparison is relevant

•

Our NAV did not give any weight to the relationship between the

NAV of traded REITs and their trading price

•

We did not attempt to quantify how that relationship may have

impacted our estimated share value.

•

The NAV method does not factor in any premium or discount

that may exist for the size of our portfolio or the enterprise value

of the entire REIT, if listed on a national securities exchange.

|

12

FAQ #3

Why did Inland American use the

NAV method? |

13

Valuation Guidelines

•

Our audit committee, our entire board and Real Globe all

followed the most recently published industry guidelines by the

IPA

•

Those guidelines suggest that non-listed REITs use an

independent, third party to value our assets and that the

estimated per share value be based on the NAV method

•

Third party determines a range of values resulting from its

analysis

•

The NAV method is currently the most commonly used

valuation method for the non-listed REIT industry.

|

14

FAQ #4

How is the value going to increase in

the future? |

15

Long-Term Strategy Fueling Increased Value

•

New estimated share value remained relatively flat vs. 2012

•

Management believes our recent 2013 acquisitions and long-

term strategy will have a more positive impact on this value in

the future.

By concentrating our assets in student housing, lodging and

multi-tenant retail, we believe we will:

o

Capture rent increases

o

Future property appreciation

o

Allows us to further focus our evaluation of possible liquidity

events. |

16

For More Information

Review our Form 8-K filed on

December 27, 2013, available on our

website -

inlandamerican.com

or

Please feel free to contact our Investor

Services team at 800.826.8228 |

17

FFO Reconciliation Slide

In Millions

9/30/2013

9/30/2012

Net income (loss) attributable to the Company

209,265

(65,771)

Add:

Depreciation and amortization related to investment properties and investment in

unconsolidated entities 323,446

365,800

Provision for asset impairment reflected in continuing and discontinued operations

229,486

66,888

Impairment, loss and (gain) of investment in unconsolidated entities, net

6,039

5,756

Impairment, loss and (gain) of investment property reflected in equtiy in earnings of

unconsolidated entities, net (2,792)

(1,928)

Gaon on sale of property reflected in net income attributed to noncontrolling interest

-

4,601

Less:

Gains from property sales and transfer of assets

414,923

29,677

Funds from Operations

350,521

345,669

Weighted Average Shares Outstanding

897,300,455

877,280,730

Nine months ended |