Attached files

| file | filename |

|---|---|

| EX-3.1 - EX-3.1 - PARAGON OFFSHORE PLC | d635036dex31.htm |

| EX-23.1 - EX-23.1 - PARAGON OFFSHORE PLC | d635036dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on December 20, 2013

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

NOBLE SPINCO LIMITED

(Exact name of registrant as specified in its charter)

| England and Wales | 1381 | 98-1146017 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

Devonshire House, 1 Mayfair Place

London W1J 8AJ

England

+44 20 3300 2300

(Address, including zip code and telephone number, including area code, of registrant’s principal executive offices)

James A. MacLennan

Devonshire House, 1 Mayfair Place

London W1J 8AJ

England

+44 20 3300 2300

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| David L. Emmons | Andrew R. Keller | |

| Hillary H. Holmes | Simpson Thacher & Bartlett LLP | |

| Baker Botts L.L.P. | 425 Lexington Avenue | |

| 910 Louisiana Street | New York, New York 10017 | |

| Houston, Texas 77002 | (212) 455-2000 | |

| (713) 229-1234 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||||

| Non-accelerated filer | x | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price (1)(2) |

Amount of Registration Fee | ||

| Ordinary Shares, nominal value $ per share |

$400,000,000 | $51,520 | ||

|

| ||||

|

| ||||

| (1) | This amount represents the proposed maximum aggregate offering price of the securities registered hereunder that may be sold by the registrant. Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes additional shares that the underwriters have the option to purchase. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated December 20, 2013

PROSPECTUS

Noble Spinco Limited

Ordinary Shares

This is the initial public offering of ordinary shares of Noble Spinco Limited. We are offering ordinary shares. No public market currently exists for our ordinary shares.

We intend to apply to list our shares on The New York Stock Exchange under the symbol “ .”

We anticipate that the initial public offering price will be between $ and $ per share.

Following the completion of this offering and related transactions, Noble Corporation plc, our ultimate parent company, will continue to own a majority of our outstanding shares. As a result, we expect to be a “controlled company” within the meaning of the corporate governance standards of The New York Stock Exchange.

Investing in our shares involves risks. See “Risk Factors” beginning on page 13 of this prospectus.

| Per Share | Total | |||||||

| Price to public |

$ | $ | ||||||

| Underwriting discounts and commissions |

$ | $ | ||||||

| Proceeds to us (before expenses) |

$ | $ | ||||||

We have granted the underwriters the option to purchase up to additional shares on the same terms and conditions set forth above if the underwriters sell more than shares in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2014.

| Barclays | Deutsche Bank Securities | J.P. Morgan |

Prospectus dated , 2014.

Table of Contents

| Page | ||||

| 1 | ||||

| 9 | ||||

| 10 | ||||

| 13 | ||||

| 39 | ||||

| 40 | ||||

| 41 | ||||

| 42 | ||||

| 44 | ||||

| 45 | ||||

| 52 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

53 | |||

| 70 | ||||

| 75 | ||||

| 89 | ||||

| 92 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

95 | |||

| 96 | ||||

| 101 | ||||

| 102 | ||||

| 109 | ||||

| 111 | ||||

| 115 | ||||

| 122 | ||||

| 122 | ||||

| 122 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by us or on our behalf that we have referred you to. We have not, and the underwriters have not, authorized anyone to provide you with any additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We are offering to sell, and seeking offers to buy, our shares only in jurisdictions where such offers and sales are permitted. The information in this prospectus or any free writing prospectus is accurate only as of its date, regardless of its time of delivery or the time of any sale of our shares. Our business, financial condition, results of operations and prospects may have changed since that date.

i

Table of Contents

Market, Industry and Other Data

The market data and other statistical information used throughout this prospectus is based on independent industry publications, government publications, reports by market research firms or other published independent sources. Some market data and other statistical information is also based on our good faith estimates, which are derived from management’s review of internal data and information, as well as the independent sources listed above. We believe that these external sources and estimates are reliable, but we have not independently verified the external sources.

ii

Table of Contents

The following is a summary of material information discussed in this prospectus. This summary may not contain all the details concerning our business, our shares or other information that may be important to you. You should carefully review this entire prospectus, including the “Risk Factors” section and our financial statements and the related notes included elsewhere in this prospectus, before making an investment decision. Some of the statements in this summary constitute forward-looking statements. Please read “Cautionary Statement Concerning Forward-Looking Statements.”

As used in this prospectus, unless the context otherwise indicates, references to “our business,” “we,” “our” or “us” or similar terms, (a) when used in the historical context, refer to the standard specification drilling business (as defined below) as owned and operated by Noble (as defined below), which business is our Predecessor for accounting purposes, and (b) when used in the present or future context, refer to Noble Spinco Limited (or, following the conversion that will take place prior to the commencement of this offering, Noble Spinco plc), or Noble Spinco, together with, where appropriate, its consolidated subsidiaries after the completion of the Transactions (as defined below). “Noble” refers to Noble Corporation plc, a public limited company incorporated under the laws of England and Wales (NYSE: NE) and its subsidiaries. We refer to the ownership and operation of the standard specification offshore drilling rigs and related assets and liabilities of Noble as the “standard specification drilling business.” Our business will include all of Noble’s standard specification drilling business other than three rigs to be retained by Noble. Please read “Business—Our Fleet.” Unless otherwise indicated or the context otherwise requires, the information contained in this prospectus assumes the completion of the Transactions we expect to consummate prior to or in connection with the closing of this offering.

Our Company

We are the leading pure-play global provider of standard specification offshore drilling rigs by operating revenues. Our drilling fleet consists solely of standard specification rigs and includes 34 jackups and eight floaters (five drillships and three semisubmersibles). This focus on a single specification supports our strategy to deliver our services in an efficient and cost-effective manner. Our primary business is to contract our rigs, related equipment and work crews to conduct oil and gas drilling and workover operations for our exploration and production, or E&P, customers on a dayrate basis around the world.

We believe that the scale of our geographically diverse fleet, well-established customer relationships and multi-year contract backlog position us to take advantage of strong market dynamics in the offshore drilling industry. We operate in significant hydrocarbon-producing geographies throughout the world, including Mexico, Brazil, the North Sea, West Africa, the Middle East, India and Southeast Asia. Our current shallow water, midwater and deepwater operations span 12 countries on five continents and provide services to approximately 20 customers. We have well-established relationships with many of our customers, including Petróleo Brasileiro S.A., or Petrobras; Petróleos Mexicanos, or Pemex; Oil and Natural Gas Corporation Limited, or ONGC; ExxonMobil Corporation, or Exxon; Total S.A., or Total; Nexen Energy ULC, or Nexen; and Centrica plc, or Centrica. In addition, in the five-year period ended December 1, 2013, 23 of our rigs have worked an average of approximately 4.6 years for their current customers. As of September 30, 2013, our pro forma contract backlog was over $3.0 billion and included contracts with leading national, international and independent oil and gas companies. Over 80% of our pro forma contract backlog is attributable to customers with investment grade ratings.

We have one of the largest diversified fleets of standard specification offshore drilling rigs in the world. Our jackups provide drilling services in shallow water with capabilities up to a maximum water depth of 390 feet. All of our jackups are independent leg and cantilevered, or ILC, which provides customers greater operational flexibility than some other jackup designs, such as mat-slot, mat-cantilever and independent-slot jackup designs.

1

Table of Contents

Seven of our jackups are also capable of operations in harsh environments, which typically command higher dayrates than operations conducted in other environments. Our drillships and semisubmersibles, which we refer to collectively as “floaters,” provide drilling services in midwater and deepwater, with capabilities up to a maximum water depth of 7,200 feet. Noble has actively invested in our assets through a disciplined capital expenditure program, spending a total of approximately $1.7 billion since January 1, 2010 to refurbish, upgrade and extend the lives of our rigs. We believe that Noble’s consistent investment in our fleet has allowed us to provide safe, reliable and effective offshore drilling services for our customers and has made our rigs more competitive in the global marketplace.

Our pro forma operating revenues were $1.25 billion and $1.35 billion for the nine months ended September 30, 2013 and the year ended December 31, 2012, respectively. Our pro forma operating income was $297 million and $115 million for the nine months ended September 30, 2013 and the year ended December 31, 2012, respectively. For more information, please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations.”

Our Market Opportunity

We believe the following trends in the oil and gas industry will support our contract drilling services business:

| • | Global energy demand is expected to continue to increase. According to the International Energy Agency, or IEA, the total global energy requirement is expected to grow to approximately 349 million barrels of oil-equivalent, or BOE, per day in 2035, increasing the demand for oil and gas by approximately 27% from 2011 levels. We believe an overall continued rise in the demand for energy, coupled with natural production decline rates from producing oil and gas reserves, correlates with positive demand for contract drilling services. |

| • | Global E&P spending has increased and a significant portion of future spending is expected to be in water depths we serve. According to Cowen and Company, global E&P capital spending (onshore and offshore) increased from approximately $328 billion in 2003 to over $600 billion in 2012. Oil and gas consultancy Infield Systems Ltd., or Infield, predicts that global offshore E&P spending between 2013 and 2017 in water depths of less than 4,900 feet will total more than $400 billion, representing approximately 74% of the global offshore E&P capital spending. We believe this E&P spending will continue to increase and we will benefit from increased E&P activity offshore. |

| • | Significant oil and gas reserves are present offshore. The 2013 BP Statistical Review of World Energy estimates that current worldwide proved oil and gas reserves total approximately 2.9 trillion BOE. Many regions in which we have an operating presence, such as Mexico, Brazil, the North Sea, West Africa and the Middle East, have major offshore hydrocarbon producing basins which contribute to the proved reserve base. Infield predicts that more than 1,335 new offshore fields will be brought on-stream between 2013 and 2017 with more than 60% of these fields in water depths less than approximately 4,900 feet. We believe that this activity will create exploration and development work opportunities for our rigs. |

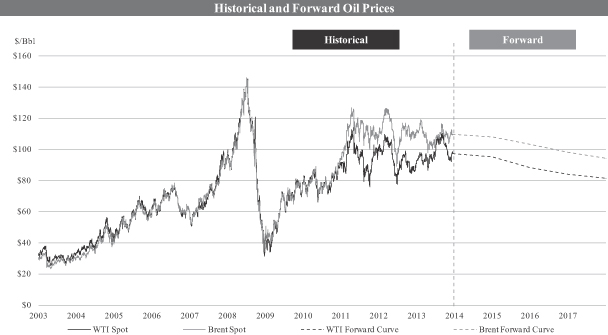

| • | Oil prices have supported investment in the offshore E&P industry. Over the past decade, on an inflation-adjusted basis, West Texas Intermediate, or WTI, oil prices have increased from approximately $30 per barrel to more than $90 per barrel and have exceeded $100 per barrel multiple times. According to IEA, oil production costs for conventional oil developments, including shallow water and deepwater resources, range from approximately $10 to $70 per barrel. We believe oil prices would have to decrease significantly from current levels for a meaningful period of time before offshore drilling activity, particularly in shallow water, would be materially impacted. |

| • | We expect the customer base for offshore drilling services to continue to include national, international and independent oil and gas companies. Offshore oil and gas E&P activities are conducted by national, international, and independent oil and gas companies. Offshore E&P activity is a |

2

Table of Contents

| core focus of many of these companies given the attractive full-cycle break-even prices for economic production of offshore oil developments. We believe the variety of types of companies with diverse strategies engaged in offshore oil and gas E&P activities provides us an attractive current and future customer base, making the demand for our services more predictable. |

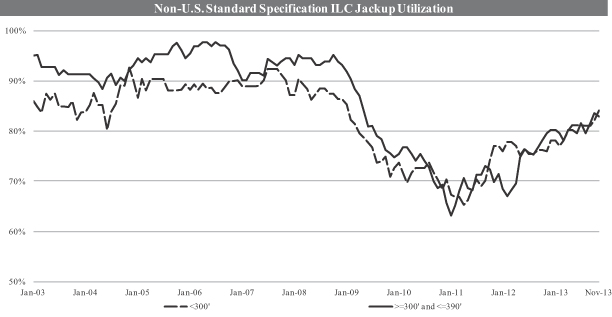

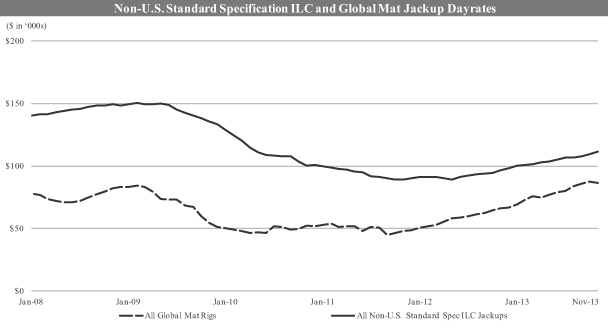

| • | The jackup market is robust. According to RigLogix, for the month of November 2013, global utilization of non-U.S. standard specification ILC jackups was approximately 83%, with an average dayrate of $111,000. These statistics represent increases in both utilization and dayrates since 2011 and reflect ongoing demand for standard specification jackups in the global marketplace despite an increase in supply from the delivery of 69 new ILC jackups between 2011 and November 2013. We believe that we are well-positioned to benefit from this demand given our geographically diverse and well-maintained fleet and its history of operating safety. |

| • | The industry is fragmented and may present acquisition opportunities. The offshore drilling industry is a large and highly fragmented industry comprising more than 100 offshore drilling contractors of which no single contractor has a dominant market share. A number of these contractors may consider divesting some or all of their standard specification rigs, and we believe this market environment may present an opportunity to expand our fleet through value-adding, accretive acquisitions of capable standard specification rigs. |

Our Fleet

Our drilling fleet consists solely of standard specification rigs, which we generally view as those rigs that are more than 15 years old. Our rigs are widely deployed in the global offshore drilling rig market. Our rigs feature proven, reliable technology and processes, utilizing mechanical features with lower operating costs compared to newer, higher specification units. Within their given water depth capabilities, our rigs are suitable for the majority of our customers’ offshore drilling operations.

Our total fleet comprises 44 standard specification offshore drilling rigs, including 34 jackups, eight floaters (five drillships and three semisubmersibles) and two submersibles, and one floating production storage and offloading unit, or FPSO. We also provide drilling and maintenance services (but do not provide a rig) on the Hibernia Project in the Canadian Atlantic under a five-year contract with a joint venture in which Exxon is the primary operator.

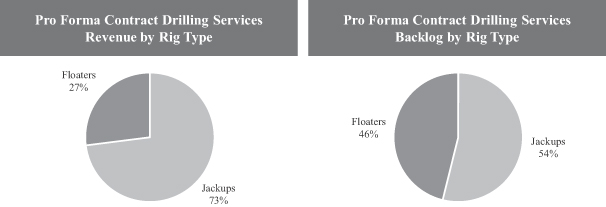

The following charts illustrate pro forma operating revenues generated by our jackups and floaters for the nine months ended September 30, 2013, and our pro forma contract backlog attributable to our jackups and floaters as of September 30, 2013.

3

Table of Contents

Jackups are mobile, self-elevating drilling platforms equipped with legs that can be lowered to the ocean floor until a foundation is established for support. All of our jackups are ILC jackups, allowing each leg to be raised or lowered independently of any other, and permitting the drilling platform to be extended out from the hull to perform drilling or workover operations over certain types of preexisting platforms or structures. We believe these design features provide greater operational flexibility and are generally considered more desirable than alternative designs. Our jackups are capable of drilling in water depths of up to 390 feet. Twenty-one of our 34 jackups can operate in water depths of 300 feet or greater. Seven of our jackups are capable of operating in harsh environments.

Drillships are self-propelled vessels that maintain their position over the well through the use of either a computer-controlled dynamic positioning system or a fixed mooring system. Our drillships are capable of drilling in water depths of up to 7,200 feet.

Semisubmersibles are floating platforms which, by means of a water ballasting system, can be submerged to a predetermined depth so that a substantial portion of the hull is below the water surface during drilling operations in order to improve stability. Our semisubmersibles maintain their position over the well through the use of a fixed mooring system. Our semisubmersibles are capable of drilling in water depths of up to 4,000 feet.

Our Competitive Strengths

We believe we have a number of competitive strengths that will allow us to execute our business strategies successfully:

| • | Significant scale, size and expertise. We are one of the world’s largest contractors of standard specification offshore drilling rigs. We are one of the primary providers of jackups in Mexico, the North Sea and West Africa and a substantial provider of floaters in Brazil. We believe the established history that our rigs and employees have with national, international and independent oil companies contributes to our credibility and distinguishes us from smaller and regional operators of standard specification offshore drilling rigs. |

| • | Well-maintained “workhorse” fleet of rigs. Our fleet comprises well-maintained drilling rigs with proven technology and operating capabilities. Noble has actively invested in capital expenditures for maintenance, rig reactivations, major projects and upgrades to our fleet, spending a total of approximately $1.7 billion since January 1, 2010, including approximately $0.9 billion for floater-specific major upgrades that we do not expect to incur again for those rigs. We believe that the quality of our fleet and our well-developed maintenance program result in low downtime and strengthen our ability to secure contracts. |

| • | Strong backlog coupled with a well-established customer base and diverse standard specification fleet. As of September 30, 2013, our pro forma contract backlog was over $3.0 billion and included contracts with leading national, international and independent oil and gas companies, including Petrobras, Pemex, ONGC, Exxon, Total, Nexen and Centrica. As of September 30, 2013, our jackups provided 54% of our pro forma contract backlog, and our floaters provided the remaining 46% of our pro forma contract backlog, which extends into 2017 and provides cash flow stability. Our current operations span 12 countries on five continents, providing services to approximately 20 customers. We believe that because dayrates and demand in different geographic regions and water depths may change independently of each other, our operational and geographic diversity provide greater opportunity, stability and downside protection. |

| • | Commitment to safety and quality. We believe that customers recognize our commitment to safety and that our performance history and reputation for safe operations provide us with a competitive advantage. For the six months ended June 30, 2013, the total recordable incident rate, or TRIR, for our rigs was |

4

Table of Contents

| 0.38 as compared to the International Association of Drilling Contractors, or IADC, average of 0.61. For the year ended December 31, 2012, the TRIR for our rigs was 0.50 as compared to the IADC average of 0.61. We believe that safety and operational excellence promote stronger relationships with multiple important stakeholders, including our employees, our customers and the local communities in which we operate, and reduce both downtime and costs. |

Our Business Strategies

Our principal business objective is to increase shareholder value. We expect to achieve this objective through the following strategies:

| • | Focus on standard specification drilling operations. We focus entirely on standard specification drilling operations in shallow water, midwater and deepwater up to 7,200 feet, and we are the leading pure-play global provider of standard specification offshore drilling rigs by operating revenues. We believe that our dedicated focus enables us to secure attractive customer contracts for our fleet through targeted marketing efforts and conduct our operations in an efficient and cost-effective manner. |

| • | Maintain and invest in our current fleet of standard specification drilling rigs. We currently have a large, well-maintained and diversified fleet of standard specification drilling rigs. We intend to continue to invest capital to maintain, refurbish and strategically upgrade our assets. By investing in our fleet, we believe that we can prolong our rigs’ lives, reduce operational downtime and generate better returns for our shareholders. |

| • | Capitalize on increased exploration and development activity. We believe the market outlook for offshore drilling remains favorable as worldwide E&P spending has increased since the beginning of 2011. We intend to continue identifying core basins and expansion areas for which our rigs’ capabilities are best suited in order to strategically position our fleet to most effectively capitalize on increasing demand for contract drilling services. |

| • | Leverage strategic relationships with high-quality, long-term customers. We are committed to maintaining and leveraging the geographic diversity of our operations and the quality and longevity of our customer relationships. Our current operations span 12 countries on five continents, and we provide services to approximately 20 customers. We believe that our geographic diversity and strong customer relationships will reduce our exposure to market volatility and position us well to identify, react quickly to and benefit from positive market dynamics. |

| • | Pursue strategic growth opportunities. We plan to consider opportunistic, value-adding acquisitions of standard specification rigs, especially rigs with contracted backlog, that add to our fleet’s average capability, customer base and geographic diversification. The offshore drilling industry is a large and highly fragmented industry. Given our large operating and geographic footprint and strong balance sheet, we believe we are well positioned to take advantage of acquisition opportunities around the world. |

| • | Remain financially disciplined and return capital to shareholders. We intend to maintain a responsible capital structure and appropriate levels of liquidity. We also intend to implement a dividend policy in order to return capital to our shareholders as described in “Dividend Policy.” We intend to make investment decisions, including refurbishments, maintenance, upgrades and acquisitions, in a disciplined and diligent manner, carefully evaluating these investments based on their ability to maintain or improve our competitive position and strengthen our financial profile while returning capital to our shareholders. |

5

Table of Contents

Structure and Formation of Our Company

We are an indirect, wholly-owned subsidiary of Noble. We were formed under the laws of England and Wales, which we refer to as “U.K. law,” in December 2013. In connection with this offering, we and Noble expect to engage in a series of transactions through which we will acquire from Noble our standard specification drilling business. Our standard specification drilling business will include all of Noble’s standard specification drilling business except for three rigs to be retained by Noble. We collectively refer to these transactions as summarized below throughout this prospectus as the “Transactions”:

| • | Noble expects to transfer the standard specification drilling business to us in exchange for of our shares and intercompany indebtedness in an aggregate principal amount of $ . |

| • | We expect to incur approximately $ of indebtedness from unaffiliated third-party lenders. |

| • | We expect to sell shares in this offering for net proceeds of approximately $ (assuming an initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus). |

| • | We expect to (i) use all of the net proceeds from this offering and $ of the net proceeds from third-party debt financings to repay the intercompany indebtedness described above and (ii) retain approximately $ of the net proceeds of third-party debt financings for general corporate purposes. |

Prior to the closing of this offering, we will enter into a master separation agreement and other arrangements with Noble and certain of its subsidiaries. Please read “Certain Relationships and Related Party Transactions.” Upon completion of this offering, purchasers of our shares will own % of our outstanding shares (or % if the underwriters exercise their option to purchase additional shares in full) and Noble will own % of our outstanding shares (or % if the underwriters exercise their option to purchase additional shares in full).

Our Relationship with Noble and the Planned Distribution

Noble is a leading offshore drilling contractor for the oil and gas industry. Upon the closing of this offering, Noble will own approximately % of our outstanding shares, or approximately % if the underwriters exercise their option to purchase additional shares in full, and we will continue to be controlled by Noble. For purposes of The New York Stock Exchange, or NYSE, rules, we will be a “controlled company” after the closing of this offering. Please read “Management—Controlled Company” for more information.

Noble has informed us that, following this offering, it expects to make a tax-free distribution to its shareholders of all of its remaining equity interest in us, which distribution would be effected as a dividend to all Noble shareholders. We refer to any such potential distribution of our shares as the “Distribution.” Noble has no obligation to pursue or consummate any further dispositions of its ownership interest in us, including through the Distribution, by any specified date or at all. The Distribution would be subject to various conditions, including receipt of any necessary regulatory or other approvals, the existence of satisfactory market conditions, the validity of a private letter ruling obtained from the Internal Revenue Service, or IRS, and an opinion of counsel (which will rely, in part, on the continuing validity of the private letter ruling) substantially to the effect that the Distribution would be tax-free to Noble, its shareholders, and us for U.S. federal income tax purposes. The conditions to the Distribution may not be satisfied, or Noble may decide not to consummate the Distribution even if the conditions are satisfied.

However, Noble could elect to dispose of our shares in a number of different types of transactions or combinations of transactions, including additional public offerings, open market sales, sales to one or more third parties or split-off offerings to Noble’s shareholders that would allow for the opportunity to exchange Noble

6

Table of Contents

shares for our shares. However, the determination of whether, and if so, when, to proceed with any of these transactions is entirely within Noble’s discretion. Except for the 180-day “lock-up” period described under “Underwriting,” Noble is not subject to any contractual obligation to maintain its share ownership. Please read “Risk Factors—Risks Related to This Offering and Ownership of Our Shares—Substantial sales of our shares by us or our shareholders could cause our share price to decline and issuances by us will dilute your ownership in our company.”

Prior to the closing of this offering, we will enter into various agreements to complete the separation of our business from Noble, including, among others, a master separation agreement, an employee matters agreement, a tax sharing agreement and a transition services agreement. The agreements between us and Noble will govern our various interim and ongoing relationships. The master separation agreement will provide for, among other things, our responsibility for liabilities relating to our business and the responsibility of Noble for liabilities related to its, and in certain limited cases, our, business. The master separation agreement will also contain indemnification obligations and ongoing commitments by us and Noble. The employee matters agreement will allocate liabilities and responsibilities between us and Noble relating to employment, compensation and benefits and related employment matters. The tax sharing agreement will provide for the allocation of taxes and tax benefits between us and Noble and other matters relating to taxes. Under the transition services agreement, Noble will continue to provide various interim support services to us. The terms of our separation from Noble, the related agreements and other transactions with Noble were determined by Noble, and thus may be less favorable to us than the terms we could have obtained from an unaffiliated third party. Please read “Certain Relationships and Related Party Transactions” for a description of these agreements and the other agreements that we will enter into with Noble.

Risk Factors

Our business is subject to numerous risks, as discussed more fully in the section entitled “Risk Factors” beginning on page 13 of this prospectus. In particular:

| • | Our business depends on the level of activity in the oil and gas industry. Adverse developments affecting the industry, including a decline in oil or gas prices, reduced demand for oil and gas products and increased regulation of drilling and production, could have a material adverse effect on our business, financial condition and results of operations. |

| • | The contract drilling industry is a highly competitive and cyclical business. If we are unable to compete successfully, our profitability may be reduced. |

| • | An over-supply of jackup rigs may lead to a reduction in dayrates and demand for our rigs and therefore may materially impact our profitability. |

| • | Our standard specification rigs are at a relative disadvantage to higher specification rigs. |

| • | The majority of our drilling rigs are more than 30 years old and may require significant amounts of capital for upgrades and refurbishment. |

| • | Our business involves numerous operating hazards. |

| • | Our inability to renew or replace expiring contracts or the loss of a significant customer or contract could have a material adverse effect on our financial results. |

| • | We are exposed to risks relating to operations in international locations. |

| • | Changes in, compliance with, or our failure to comply with certain laws and regulations may negatively impact our operations and could have a material adverse effect on our results of operations. |

| • | We may be unable to achieve some or all of the benefits that we expect to achieve from our separation from Noble. |

7

Table of Contents

| • | Our historical combined and unaudited pro forma combined financial information are not necessarily indicative of our future financial condition, future results of operations or future cash flows nor do they reflect what our financial condition, results of operations or cash flows would have been as an independent public company during the periods presented. |

Corporate Information

Our principal executive offices are located at Devonshire House, 1 Mayfair Place, London W1J 8AJ England, and our telephone number at that address is +44 20 3300 2300.

We maintain a website at . We expect to make our periodic reports and other information filed with or furnished to the U.S. Securities and Exchange Commission, or SEC, available, free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

8

Table of Contents

| Ordinary shares offered by us |

shares (or shares if the underwriters’ option to purchase additional shares is exercised in full). |

| Ordinary shares to be held by Noble immediately after this offering |

shares (or shares if the underwriters’ option to purchase additional shares is exercised in full). |

| Ordinary shares to be outstanding immediately after this offering |

shares (or shares if the underwriters’ option to purchase additional shares is exercised in full). |

| Option to purchase additional shares |

We have agreed to allow the underwriters to purchase up to an additional shares from us, at the public offering price less underwriting discounts and commissions, within 30 days from the date of this prospectus. |

| Use of proceeds |

We estimate that the net proceeds from this offering received by us will be approximately $ (assuming an initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus), after deducting underwriting discounts and commissions and estimated offering expenses payable by us. We expect to use all of the net proceeds from this offering to repay intercompany indebtedness issued to Noble as partial consideration for the standard specification drilling business transferred to us. |

| Dividend policy |

We expect to pay regular quarterly cash dividends, subject to the discretion of our board of directors, certain conditions under U.K. law and restrictions on our ability to pay dividends that may be caused by agreements governing certain of our indebtedness. There can be no assurance that we will pay, or continue to pay, any dividend. Please read “Dividend Policy.” |

| Proposed listing symbol |

We intend to apply to list our shares on the NYSE, under the symbol “ .” |

Unless otherwise indicated, all information in this prospectus relating to the number of shares to be outstanding immediately after this offering:

| • | assumes no exercise by the underwriters of their option to purchase up to additional shares from us; |

| • | excludes an aggregate of shares reserved for issuance under the equity incentive plan we intend to adopt in connection with this offering; and |

| • | assumes an initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus. |

9

Table of Contents

SUMMARY HISTORICAL AND PRO FORMA FINANCIAL DATA

The following table shows summary historical and pro forma financial data of Noble’s standard specification drilling business, which is our Predecessor for accounting purposes, as of the dates and for the periods indicated. The summary historical statement of operations data for the years ended December 31, 2012, 2011 and 2010 and the balance sheet data as of December 31, 2012 and 2011 have been derived from the audited combined financial statements of our Predecessor included elsewhere in this prospectus. The summary balance sheet data as of December 31, 2010 have been derived from the unaudited combined financial statements of our Predecessor not included elsewhere in this prospectus. The summary historical statement of operations data for the nine months ended September 30, 2013 and 2012 and the balance sheet data as of September 30, 2013 were derived from the unaudited combined financial statements of our Predecessor included elsewhere in this prospectus, which include all adjustments, consisting of normal recurring adjustments, which management considers necessary for a fair presentation of our Predecessor’s financial position and the results of operations for such periods. Results for the interim periods may not necessarily be indicative of results for the full year.

Our Predecessor’s historical combined financial statements include expenses of Noble that were allocated to us for certain administrative and operational support functions which were performed by Noble and certain of its subsidiaries. These expenses were allocated in our Predecessor’s historical results of operations in a manner consistent with Noble’s internal reporting for evaluation purposes. We consider the expense-allocation methodology and results to be reasonable for all periods presented. However, these allocations may not necessarily be indicative of the actual expenses we would have incurred as an independent publicly traded company during the periods prior to this offering nor are they representative of the costs which we will incur in the future.

The historical financial data included in this prospectus may not be indicative of our future performance and do not necessarily reflect what our financial position and results of operations would have been had we operated as a standalone public company during the periods presented, including changes that will occur in our operations and capital structure as a result of the Transactions, including this offering. Furthermore, the historical financial data include the effect of the ownership and operation of three rigs owned by Noble that will not be transferred to us in the Transactions and one rig sold by Noble in July 2013.

The summary unaudited pro forma combined financial data of Noble Spinco have been derived from the application of pro forma adjustments to our Predecessor’s historical combined financial statements included elsewhere in this prospectus. The summary unaudited pro forma combined statements of operations give effect to the Transactions as if they had occurred on January 1, 2012. The summary unaudited pro forma combined balance sheet gives effect to the Transactions as if they had occurred on September 30, 2013. Please read “Unaudited Pro Forma Combined Financial Statements” for additional information. The pro forma adjustments are based upon available information and certain assumptions which we believe to be reasonable. The summary unaudited pro forma combined financial information does not purport to represent what our results of operations or financial position would have been if we had operated as a public company during the periods presented and may not be indicative of our future performance. The summary unaudited combined pro forma financial data are presented for informational purposes only.

10

Table of Contents

The following tables should be read together with, and are qualified in their entirety by reference to, the historical and unaudited pro forma combined financial statements and the accompanying notes included elsewhere in this prospectus. Among other things, the historical combined financial statements include more detailed information regarding the basis of presentation for the information in the following table. The tables should also be read together with the sections entitled “Unaudited Pro Forma Combined Financial Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Certain Relationships and Related Party Transactions” included elsewhere in this prospectus.

| Predecessor Historical | Noble Spinco Pro Forma | |||||||||||||||||||||||||||

| Year Ended December 31, | Nine Months Ended September 30, |

Nine Months Ended September 30, 2013 |

Year Ended December 31, 2012 |

|||||||||||||||||||||||||

| 2012 | 2011 | 2010 (1) | 2013 | 2012 | ||||||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||||||||

| (In thousands, except for dayrates and utilization) | ||||||||||||||||||||||||||||

| Statement of Income Data: |

||||||||||||||||||||||||||||

| Operating revenues |

$ | 1,541,857 | $ | 1,370,557 | $ | 1,667,370 | $ | 1,408,697 | $ | 1,124,553 | $ | 1,254,185 | $ | 1,346,312 | ||||||||||||||

| Operating income |

176,712 | 136,947 | 536,802 | 395,984 | 119,409 | 296,938 | 115,455 | |||||||||||||||||||||

| Net income per share |

||||||||||||||||||||||||||||

| Basic |

N/A | N/A | N/A | N/A | N/A | |||||||||||||||||||||||

| Diluted |

N/A | N/A | N/A | N/A | N/A | |||||||||||||||||||||||

| Weighted average shares outstanding |

||||||||||||||||||||||||||||

| Basic |

N/A | N/A | N/A | N/A | N/A | |||||||||||||||||||||||

| Diluted |

N/A | N/A | N/A | N/A | N/A | |||||||||||||||||||||||

| Balance Sheet Data (at end of period): |

||||||||||||||||||||||||||||

| Cash and cash equivalents (2) |

$ | 70,538 | $ | 75,767 | $ | 76,892 | $ | 55,656 | N/A | $ | $ | |||||||||||||||||

| Property and equipment, net |

3,551,813 | 3,373,817 | 3,280,820 | 3,519,936 | N/A | |||||||||||||||||||||||

| Total assets |

4,118,072 | 3,866,756 | 3,780,121 | 4,098,413 | N/A | |||||||||||||||||||||||

| Long-term debt |

339,809 | 975,000 | 40,000 | 1,312,864 | N/A | |||||||||||||||||||||||

| Total debt (3) |

339,809 | 975,000 | 40,000 | 1,312,864 | N/A | |||||||||||||||||||||||

| Equity |

3,365,232 | 2,441,823 | 3,247,743 | 2,384,653 | N/A | |||||||||||||||||||||||

| Cash Flows Data: |

||||||||||||||||||||||||||||

| Cash flows from operating activities |

$ | 405,484 | $ | 466,100 | $ | 1,029,552 | $ | 587,514 | $ | 236,078 | N/A | N/A | ||||||||||||||||

| Cash flows from investing activities |

(540,867 | ) | (493,255 | ) | (1,724,109 | ) | (239,603 | ) | (406,308 | ) | N/A | N/A | ||||||||||||||||

| Cash flows from financing activities |

130,154 | 26,030 | 693,973 | (362,793 | ) | 176,572 | N/A | N/A | ||||||||||||||||||||

| Other Data (4): |

||||||||||||||||||||||||||||

| Working capital (5) |

$ | 253,816 | $ | 123,004 | $ | 74,008 | $ | 260,326 | N/A | |

N/A |

|

N/A | |||||||||||||||

| Average dayrate |

||||||||||||||||||||||||||||

| Jackups |

$ | 88,120 | $ | 79,257 | $ | 94,832 | $ | 101,911 | $ | 86,298 | $ | 102,710 | $ | 88,941 | ||||||||||||||

| Floaters |

236,767 | 233,052 | 230,596 | 253,521 | 251,283 | 242,487 | 228,629 | |||||||||||||||||||||

| Average utilization (6) |

||||||||||||||||||||||||||||

| Jackups |

81 | % | 77 | % | 80 | % | 92 | % | 79 | % | 91 | % | 79 | % | ||||||||||||||

| Floaters |

62 | % | 61 | % | 87 | % | 66 | % | 58 | % | 61 | % | 57 | % | ||||||||||||||

| Total capital expenditures (7) |

$ | 532,404 | $ | 518,455 | $ | 408,726 | $ | 283,290 | $ | 384,140 | $ | 277,790 | $ | 522,300 | ||||||||||||||

| (1) | Balance sheet data for 2010 is unaudited. |

| (2) | Consists of cash and cash equivalents as reported on our combined balance sheet. |

| (3) | Consists of long-term debt and current portion of long-term debt. |

11

Table of Contents

| (4) | Other Data for our Predecessor includes results from two standard specification jackups and one standard specification floater to be retained by Noble and one jackup sold by Noble in July 2013. Our pro forma Other Data, excluding these rigs, was as follows: |

| Noble Spinco Pro Forma | ||||||||||||||||||||

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2012 | 2011 | 2010 | 2013 | 2012 | ||||||||||||||||

| Average dayrate |

||||||||||||||||||||

| Jackups |

$ | 88,941 | $ | 79,518 | $ | 95,728 | $ | 102,710 | $ | 87,397 | ||||||||||

| Floaters |

228,629 | 263,792 | 243,544 | 242,487 | 247,713 | |||||||||||||||

| Average utilization |

||||||||||||||||||||

| Jackups |

79 | % | 77 | % | 83 | % | 91 | % | 77 | % | ||||||||||

| Floaters |

57 | % | 56 | % | 86 | % | 61 | % | 53 | % | ||||||||||

| Total capital expenditures (in thousands) (7) |

$ | 522,300 | $ | 493,107 | $ | 380,055 | $ | 277,790 | $ | 377,939 | ||||||||||

| (5) | The difference between our Predecessor’s historical working capital and our pro forma working capital is not meaningful. We will have approximately $ of cash and cash equivalents at the closing of this offering. |

| (6) | We define utilization for a specific period as the total number of days our rigs, including cold stacked rigs, are under contract, divided by the product of the number of our rigs and the number of calendar days in such period. |

| (7) | Capital expenditures for 2010-2012 include approximately $0.9 billion for floater-specific major upgrades that we do not expect to incur again for those rigs. |

12

Table of Contents

This offering and an investment in our shares involve a high degree of risk. You should carefully consider the risks described below, together with the financial and other information contained in this prospectus, before you decide to purchase our shares. The risks described below are not the only risks facing us and our business prospects. If any of the following risks actually occurs, our business, financial condition, results of operations and prospects could be materially and adversely affected. As a result, the trading price of our shares could decline and you could lose all or part of your investment in our shares.

Risks Related to Our Business

Our business depends on the level of activity in the oil and gas industry. Adverse developments affecting the industry, including a decline in oil or gas prices, reduced demand for oil and gas products and increased regulation of drilling and production, could have a material adverse effect on our business, financial condition and results of operations.

Demand for drilling services depends on a variety of economic and political factors and the level of activity in offshore oil and gas exploration and development and production markets worldwide. Commodity prices, and market expectations of potential changes in these prices, may significantly affect this level of activity, as well as dayrates for our services. However, higher current prices do not necessarily translate into increased drilling activity because our clients’ expectations of future commodity prices typically drive demand for our rigs. Oil and gas prices and the level of activity in offshore oil and gas exploration and development are volatile and are affected by numerous factors beyond our control, including:

| • | the cost of exploring for, developing, producing and delivering oil and gas; |

| • | potential acceleration in the development, and the price and availability, of alternative fuels; |

| • | increased supply of oil and gas resulting from growing onshore hydraulic fracturing activity and shale development; |

| • | worldwide production and demand for oil and gas, which are impacted by changes in the rate of economic growth in the global economy; |

| • | worldwide financial instability or recessions; |

| • | regulatory restrictions or any moratorium on offshore drilling; |

| • | expectations regarding future energy prices; |

| • | the discovery rate of new oil and gas reserves; |

| • | the rate of decline of existing and new oil and gas reserves; |

| • | available pipeline and other oil and gas transportation capacity; |

| • | oil refining capacity; |

| • | the ability of oil and gas companies to raise capital; |

| • | advances in exploration, development and production technology; |

| • | technical advances affecting energy consumption; |

| • | merger and divestiture activity among oil and gas producers; |

| • | the availability of, and access to, suitable locations from which our customers can produce hydrocarbons; |

| • | rough seas and adverse weather conditions, including hurricanes and typhoons; |

| • | tax laws, regulations and policies; |

13

Table of Contents

| • | laws and regulations related to environmental matters, including those addressing alternative energy sources and the risks of global climate change; |

| • | the political environment of oil-producing regions, including uncertainty or instability resulting from civil disorder, an outbreak or escalation of armed hostilities or acts of war or terrorism; |

| • | the ability of the Organization of Petroleum Exporting Countries, or OPEC, to set and maintain production levels and pricing; |

| • | the level of production in non-OPEC countries; and |

| • | the laws and regulations of governments regarding exploration and development of their oil and gas reserves or speculation regarding future laws or regulations. |

Adverse developments affecting the industry as a result of one or more of these factors, including a decline in oil or gas prices, a global recession, reduced demand for oil and gas products and increased regulation of drilling and production, particularly if several developments were to occur in a short period of time as in 2008 and 2009, could have a material adverse effect on our business, financial condition and results of operations.

The contract drilling industry is a highly competitive and cyclical business. If we are unable to compete successfully, our profitability may be reduced.

The offshore contract drilling industry is a highly competitive and cyclical business characterized by high capital and operating costs and evolving operational capability of newer rigs. Drilling contracts are traditionally awarded on a competitive bid basis. Intense price competition, rig availability, location and suitability, experience of the workforce, efficiency, safety performance record, technical capability and condition of equipment, operating integrity, reputation, industry standing and client relations are all factors in determining which contractor is awarded a job. Our future success and profitability will partly depend upon our ability to keep pace with our customers’ demands with respect to these factors. Other drilling companies, including those with both high specification and standard specification rigs, may have greater financial, technical and personnel resources that allow them to upgrade equipment and implement new technical capabilities before we can. If current competitors or new market entrants implement new technical capabilities, services or standards that are more attractive to our customers, it could have a material adverse effect on our operations.

In addition to intense competition, our industry is highly cyclical. It has been especially cyclical with respect to the jackup market, where market conditions are subject to rapid change. There have been periods of high demand, short rig supply and high dayrates, followed by periods of lower demand, excess rig supply and low dayrates. Periods of low demand or excess rig supply intensify the competition in the industry and may result in some of our rigs being idle or earning substantially lower dayrates for long periods of time. Additionally, drilling contracts for our jackups generally have shorter terms than contracts for our floaters, meaning that most of our fleet does not have the benefit of the price protection that longer-term contracts provide. The volatility of the industry, coupled with the short-term nature of many of our contracts could have a material adverse effect on our business, financial condition and results of operations.

An over-supply of jackup rigs may lead to a reduction in dayrates and demand for our rigs and therefore may materially impact our profitability.

During the recent period of high utilization and high dayrates, industry participants have increased the supply of drilling rigs by building new drilling rigs, including some drilling rigs that have not yet entered service. Historically, this has often resulted in an oversupply of drilling rigs, which has contributed to a decline in utilization and dayrates, sometimes for extended periods of time.

The increase in supply created by the number and types of rigs being built, as well as changes in our competitors’ drilling rig fleets, could intensify price competition and require higher capital investment to keep

14

Table of Contents

our rigs competitive. According to RigLogix, as of December 12, 2013, the total non-U.S. jackup fleet comprises 456 units (20 of which are cold stacked). An additional 110 jackup drilling rigs are under construction or on order, which would bring the total non-U.S. jackup fleet to 566 units (assuming no further newbuilds are ordered and delivered and there is no attrition of the current fleet). To the extent that the drilling rigs currently under construction or on order have not been contracted for future work, there may be increased price competition as such vessels become operational, which could lead to a reduction in dayrates. Lower utilization and dayrates would adversely affect our revenues and profitability. Prolonged periods of low utilization or low dayrates could also result in the recognition of impairment charges on our drilling rigs if future cash flow estimates, based upon information available to management at the time, indicate that the carrying value of these drilling rigs may not be recoverable.

Our standard specification rigs are at a relative disadvantage to higher specification rigs.

Our standard specification rigs do not have certain capabilities and technology that can be found on higher specification rigs and that may increase the operating parameters and efficiency of higher specification drilling rigs. If the demand for offshore drilling rigs were to decrease for any reason, it is possible that higher specification rigs may begin to compete with standard specification rigs for the same contracts. In that case, higher specification rigs would have an advantage over standard specification rigs in securing those contracts and demand for and utilization of standard specification rigs may decrease. Such a decrease in demand for and utilization of standard specification rigs could have a material adverse effect on our business, financial condition and results of operations.

Many of our competitors have fleets that include high specification rigs, making these competitors more operationally diverse. Some of our customers have expressed a preference for newer rigs and, in some areas, higher specification rigs may be more likely to obtain contracts than standard specification rigs such as ours. Our rigs are further constrained by the water depths in which they are capable of operating. In recent years, an increasing amount of E&P expenditures has been concentrated in deepwater drilling programs and deeper formations, requiring higher specification jackup rigs, semisubmersibles or drillships. This trend could result in a decline in demand for standard specification rigs like ours, which could have a material adverse effect on our business, financial condition and results of operations.

The majority of our drilling rigs are more than 30 years old and may require significant amounts of capital for upgrades and refurbishment.

The majority of our drilling rigs were initially put into service during the years 1976 to 1982 and may require significant capital investment to continue operating in the future, particularly as compared to their newer high specification counterparts. From time to time, some of our customers, including Pemex, express a preference for newer rigs. We may be required to spend significant capital on upgrades and refurbishment to maintain the competitiveness of our fleet in the offshore drilling market. Our rigs typically do not generate revenue while they are undergoing refurbishment and upgrades. Rig upgrade or refurbishment projects for older assets such as ours could increase our indebtedness or reduce cash available for other opportunities. Further, such projects may require proportionally greater capital investments as a percentage of total rig value, which may make such projects difficult to finance on acceptable terms. To the extent we are unable to fund such projects, we will have fewer rigs available for service or our rigs may not be attractive to potential or current customers. Such demands on our capital or reductions in demand for our fleet could have a material adverse effect on our business, financial condition and results of operations.

Our business involves numerous operating hazards.

Our operations are subject to many hazards inherent in the drilling business, including:

| • | well blowouts; |

| • | fires; |

15

Table of Contents

| • | collisions or groundings of offshore equipment; |

| • | punch-throughs; |

| • | mechanical or technological failures; |

| • | failure of our employees to comply with our internal environmental, health and safety guidelines; |

| • | pipe or cement failures and casing collapses, which could release oil, gas or drilling fluids; |

| • | geological formations with abnormal pressures; |

| • | spillage handling and disposing of materials; and |

| • | adverse weather conditions, including hurricanes, typhoons, winter storms and rough seas. |

These hazards could cause personal injury or loss of life, suspend drilling operations, result in regulatory investigation or penalties, seriously damage or destroy property and equipment, result in claims by employees, customers or third parties, cause environmental damage and cause substantial damage to oil and gas producing formations or facilities. Operations also may be suspended because of machinery breakdowns, abnormal drilling conditions, and failure of subcontractors to perform or supply goods or services or personnel shortages. Accordingly, the occurrence of any of the hazards we face could have a material adverse effect on our business, financial condition and results of operations.

Our inability to renew or replace expiring contracts or the loss of a significant customer or contract could have a material adverse effect on our financial results.

Our ability to renew our customer contracts or obtain new contracts and the terms of any such contracts will depend on many factors beyond our control, including market conditions, the global economy and our customers’ financial condition and drilling programs. Moreover, any concentration of customers increases the risks associated with any possible termination or nonperformance of drilling contracts. For the nine months ended September 30, 2013, our five largest customers in the aggregate accounted for 61% of our consolidated operating revenues. We expect Pemex and Petrobras, which accounted for approximately 21% and 17% of our consolidated operating revenues for the nine months ended September 30, 2013, respectively, to continue to be significant customers in 2014. Our contract drilling backlog for 2014 as of September 30, 2013 includes $456 million, or approximately 29%, and $308 million, or approximately 20%, attributable to contracts with Petrobras and Pemex, respectively, for operations offshore Brazil and Mexico. Our floaters working for Petrobras are under contracts that expire in 2017. Petrobras has announced a program to construct 29 newbuild floaters, which may reduce or eliminate its need for our rigs. These new drilling units, if built, would compete with, and could displace, our floaters completing contracts and could materially adversely affect our utilization rates, particularly in Brazil. Further, some national oil companies have considered regulations limiting the age of rigs in operation. Such reforms, if adopted, could significantly increase our costs or render some of our rigs ineligible for contracts with such companies.

Our customers may generally terminate our term drilling contracts if a drilling rig is destroyed or lost or if we have to suspend drilling operations for a specified period of time as a result of a breakdown of major equipment or, in some cases, due to other events beyond the control of either party. In the case of nonperformance and under certain other conditions, our drilling contracts generally allow our customers to terminate without any payment to us. The terms of some of our drilling contracts permit the customer to terminate the contract after specified notice periods by tendering contractually specified termination amounts. These termination payments may not fully compensate us for the loss of a contract. Our drilling contracts with our largest customer, Pemex, allow early cancellation with 30 days or less notice to us without any early termination payment. Our second largest customer, Petrobras, has the right to terminate its contracts in the event of downtime that exceeds certain thresholds. The early termination of a contract may result in a rig being idle for an extended period of time and a reduction in our contract backlog and associated revenue, which could have a material adverse effect on our business, financial condition and results of operations.

16

Table of Contents

In addition, during periods of depressed market conditions, we may be subject to an increased risk of our customers seeking to repudiate their contracts. Our customers’ ability to perform their obligations under drilling contracts with us may also be adversely affected by restricted credit markets and economic downturns. If our customers cancel or are unable to renew some of their contracts and we are unable to secure new contracts on a timely basis and on substantially similar terms, if contracts are disputed or suspended for an extended period of time or if a number of our contracts are renegotiated, it could have a material adverse effect on our business, financial condition and results of operations.

We are exposed to risks relating to operations in international locations.

We operate in various regions throughout the world that may expose us to political and other uncertainties, including risks of:

| • | seizure, nationalization or expropriation of property or equipment; |

| • | monetary policies, government credit rating downgrades and potential defaults, and foreign currency fluctuations and devaluations; |

| • | limitations on the ability to repatriate income or capital; |

| • | complications associated with repairing and replacing equipment in remote locations; |

| • | repudiation, nullification, modification or renegotiation of contracts; |

| • | limitations on insurance coverage, such as war risk coverage, in certain areas; |

| • | import-export quotas, wage and price controls, imposition of trade barriers and other forms of government regulation and economic conditions that are beyond our control; |

| • | delays in implementing private commercial arrangements as a result of government oversight; |

| • | financial or operational difficulties in complying with foreign bureaucratic actions; |

| • | changing taxation rules or policies; |

| • | other forms of government regulation and economic conditions that are beyond our control and that create operational uncertainty; |

| • | governmental corruption; |

| • | piracy; and |

| • | terrorist acts, war, revolution and civil disturbances. |

Further, we operate in certain less-developed countries with legal systems that are not as mature or predictable as those in more developed countries, which can lead to greater uncertainty in legal matters and proceedings. Examples of challenges of operating in these countries include:

| • | potential restrictions presented by local content regulations in Nigeria; |

| • | ongoing changes in Brazilian laws related to the importation of rigs and equipment that may impose bonding, insurance or duty-payment requirements; |

| • | procedural requirements for temporary import permits, which may be difficult to obtain; and |

| • | the effect of certain temporary import permit regimes, such as in Nigeria, where the duration of the permit does not coincide with the general term of the drilling contract. |

17

Table of Contents

Our ability to mobilize our drilling rigs between locations and the time and costs of such mobilization may be material to our business.

Our ability to mobilize our drilling rigs to more desirable locations may be impacted by governmental regulation and customs practices, the significant costs of moving a drilling rig, weather, political instability, civil unrest, military actions and the technical capability of the drilling rig to relocate and operate in various environments. In addition, as our rigs are mobilized from one geographic location to another, labor and other operating and maintenance costs can vary significantly. If we relocate a rig to another geographic location without a customer contract, we will incur costs that will not be reimbursable by future customers, and even if we relocate a rig with a customer contract, we may not be fully compensated during the mobilization period. These impacts of rig mobilization could have a material adverse effect on our business, results of operations and financial condition.

Operating and maintenance costs of our operating rigs and costs relating to idle rigs may be significant and may not correspond to revenue earned.

Our operating expenses and maintenance costs depend on a variety of factors including crew costs, costs of provisions, equipment, insurance, maintenance and repairs, and shipyard costs, many of which are beyond our control. Our total operating costs are generally related to the number of drilling rigs in operation and the cost level in each country or region where such drilling rigs are located. Equipment maintenance costs fluctuate depending upon the type of activity that the drilling rig is performing and the age and condition of the equipment. Operating and maintenance costs will not necessarily fluctuate in proportion to changes in operating revenues. While operating revenues may fluctuate as a function of changes in dayrate, costs for operating a rig may not be proportional to the dayrate received and may vary based on a variety of factors, including the scope and length of required rig preparations and the duration of the contractual period over which such expenditures are amortized. Any investments in our rigs may not result in an increased dayrate for or income from such rigs. A disproportionate amount of operating and maintenance costs in comparison to dayrates could have a material adverse effect on our business, financial condition and results of operations.

During idle periods, to reduce our costs, we may decide to “warm stack” a rig, which means the rig is kept fully operational and ready for redeployment, and maintains most of its crew. As a result, our operating expenses during a warm stacking will not be substantially different than those we would incur if the rig remained active. We may also decide to cold stack the rig, which means the rig is neither operational nor ready for deployment, does not maintain a crew and is stored in a harbor, shipyard or a designated offshore area. However, reductions in costs following the decision to cold stack a rig may not be immediate, as a portion of the crew may be required to prepare the rig for such storage. Currently, five of our rigs and our FPSO are cold stacked. Our cold stacked rigs may require significant capital expenditures to return them to operation, making reactivation of such assets more financially demanding.

Any violation of anti-bribery or anti-corruption laws, including the Foreign Corrupt Practices Act, the United Kingdom Bribery Act, or similar laws and regulations could result in significant expenses, divert management attention, and otherwise have a negative impact on us.

We operate in countries known to have a reputation for corruption. We are subject to the risk that we, our affiliated entities or their respective officers, directors, employees and agents may take action determined to be in violation of such anti-corruption laws, including the U.S. Foreign Corrupt Practices Act of 1977, or FCPA, the United Kingdom Bribery Act 2010, or U.K. Bribery Act, and similar laws in other countries.

In 2007, Noble began, and voluntarily contacted the SEC and the U.S. Department of Justice, or DOJ, to advise them of, an internal investigation of the legality under the FCPA and local laws of certain reimbursement payments made by Noble’s Nigerian affiliate to our customs agents in Nigeria. In 2010, Noble finalized settlements of this matter and paid fines and penalties to the DOJ and the SEC. Any violation of the FCPA, the U.K. Bribery Act or other applicable anti-corruption laws could result in substantial fines, sanctions, civil or

18

Table of Contents

criminal penalties and curtailment of operations in certain jurisdictions and might adversely affect our business, results of operations or financial condition. Actual or alleged violations could also damage our reputation and ability to do business. Further, detecting, investigating, and resolving actual or alleged violations is expensive and can consume significant time and attention of our senior management.

Changes in, compliance with, or our failure to comply with the certain laws and regulations may negatively impact our operations and could have a material adverse effect on our results of operations.

Our operations are subject to various laws and regulations in countries in which we operate, including laws and regulations relating to:

| • | the importing, exporting, equipping and operation of drilling rigs; |

| • | repatriation of foreign earnings; |

| • | currency exchange controls; |

| • | oil and gas exploration and development; |

| • | taxation of offshore earnings and earnings of expatriate personnel; and |

| • | use and compensation of local employees and suppliers by foreign contractors. |

Legal and regulatory proceedings relating to the energy industry, and the complex government regulations to which our business is subject, have at times adversely affected our business and may do so in the future. Governmental actions and initiatives by OPEC may continue to cause oil price volatility. In some areas of the world, this activity has adversely affected the amount of exploration and development work done by major oil companies, which may continue. In addition, some governments favor or effectively require the awarding of drilling contracts to local contractors, require use of a local agent or require foreign contractors to employ citizens of, or purchase supplies from, a particular jurisdiction. These practices may adversely affect our ability to compete and our results of operations.

Public and regulatory scrutiny of the energy industry has resulted in increased regulations being either proposed or implemented. In addition, existing regulations might be revised or reinterpreted, new laws, regulations and permitting requirements might be adopted or become applicable to us, our rigs, our customers, our vendors or our service providers, and future changes in laws and regulations could significantly increase our costs and could have a material adverse effect on our business, financial condition and results of operations. In addition, we may be required to post additional surety bonds to secure performance, tax, customs and other obligations relating to our rigs in jurisdictions where bonding requirements are already in effect and in other jurisdictions where we may operate in the future. These requirements would increase the cost of operating in these countries, which could materially adversely affect our business, financial condition and results of operations.

Adverse effects may continue as a result of the uncertainty of ongoing inquiries, investigations and court proceedings, or additional inquiries and proceedings by federal or state regulatory agencies or private plaintiffs. In addition, we cannot predict the outcome of any of these inquiries or whether these inquiries will lead to additional legal proceedings against us, civil or criminal fines or penalties, or other regulatory action, including legislation or increased permitting requirements. Legal proceedings or other matters against us, including environmental matters, suits, regulatory appeals, challenges to our permits by citizen groups and similar matters, might result in adverse decisions against us. The result of such adverse decisions, either individually or in the aggregate, could be material and may not be covered fully or at all by insurance.

19

Table of Contents

Shipyard projects are subject to risks, including delays and cost overruns, which could have an adverse impact on our results of operations and financial condition.

We may make significant repairs, refurbishments and upgrades to our fleet from time to time, particularly given the age of our fleet. Some of these expenditures will be unplanned. In addition, we may decide to construct new rigs or acquire rigs under construction. These projects and other efforts of this type are subject to risks of cost overruns or delays inherent in any large construction project as a result of numerous factors, including the following:

| • | shortages of equipment, materials or skilled labor; |

| • | work stoppages and labor disputes; |

| • | unscheduled delays in the delivery of ordered materials and equipment; |

| • | local customs strikes or related work slowdowns that could delay importation of equipment or materials; |

| • | weather interferences; |

| • | difficulties in obtaining necessary permits or approvals or in meeting permit or approval conditions; |

| • | design and engineering problems; |

| • | inadequate regulatory support infrastructure in the local jurisdiction; |