Attached files

| file | filename |

|---|---|

| EX-10.24 - EX-10.24 - RetailMeNot, Inc. | d610696dex1024.htm |

| EX-10.24.1 - EX-10.24.1 - RetailMeNot, Inc. | d610696dex10241.htm |

| EX-10.14.1 - EX-10.14.1 - RetailMeNot, Inc. | d610696dex10141.htm |

| EX-23.1 - EX-23.1 - RetailMeNot, Inc. | d610696dex231.htm |

| EX-23.2 - EX-23.2 - RetailMeNot, Inc. | d610696dex232.htm |

Table of Contents

As filed with the Securities and Exchange Commission on December 2, 2013

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

RETAILMENOT, INC.

(Exact name of Registrant as Specified in Its Charter)

| Delaware | 7389 | 26-0159761 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification No.) | ||

301 Congress Avenue, Suite 700

Austin, Texas 78701

(512) 777-2970

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

G. Cotter Cunningham

Chief Executive Officer

301 Congress Avenue, Suite 700

Austin, Texas 78701

(512) 777-2970

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

| Samer M. Zabaneh Philip W. Russell DLA Piper LLP (US) 401 Congress Avenue, Suite 2500 Austin, Texas 78701 (512) 457-7000 |

Louis J. Agnese, III General Counsel and Secretary RetailMeNot, Inc. 301 Congress Avenue, Suite 700 Austin, Texas 78701 (512) 777-2970 |

Paul R. Tobias Joseph M. Alcorta Wilson Sonsini Goodrich & Rosati, Professional Corporation 900 South Capital of Texas Highway Las Cimas IV, Fifth Floor Austin, Texas 78746 (512) 338-5400 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”), check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). (check one): ¨ Large accelerated filer, ¨ Accelerated filer, x Non-accelerated filer (do not check if a smaller reporting company) or ¨ Smaller reporting company.

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities To Be Registered |

Proposed Maximum Aggregate |

Amount of Registration Fee | ||

| Series 1 common stock, par value $0.001 |

$200,000,000 | $25,760.00 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the amount of the registration fee in accordance with Rule 457(o) under the Securities Act. Includes offering price of additional shares that the underwriters have the option to purchase. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to such Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We and the selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Registration No. 333-

PROSPECTUS (subject to completion), dated December 2, 2013

Shares

Series 1 Common Stock

RetailMeNot, Inc. is offering shares of its Series 1 common stock, and the selling stockholders identified in this prospectus are offering an additional shares of Series 1 common stock. We intend to offer approximately $75 million of shares and the remainder will be offered by the selling stockholders. We will not receive any of the proceeds from the sale of the shares being offered by the selling stockholders.

We have two classes of common stock, Series 1 common stock and Series 2 common stock. The rights of the holders of Series 1 common stock and Series 2 common stock are identical, except for voting and conversion rights. Each share of Series 1 common stock is entitled to one vote. Each share of Series 2 common stock is also entitled to one vote other than with respect to the election of members of the board of directors and may be converted at any time at the election of the holder into one share of Series 1 common stock. As such, only holders of Series 1 common stock are entitled to vote on the election of members of the board of directors. After this offering, our executive officers, directors, beneficial owners of 5.0% or more of our outstanding shares of capital stock, and affiliated entities, will own approximately % of our capital stock. In addition, in connection with this offering, our executive officers, directors, beneficial owners of 5.0% or more of our outstanding shares of capital stock, and affiliated entities, will receive approximately $ million of net proceeds from the sale of shares in this offering, after deducting underwriting discounts and commissions payable by such selling stockholders.

Our Series 1 common stock is listed on the NASDAQ Global Select Market under the symbol “SALE”. On November 29, 2013, the last reported sale price of our common stock on the NASDAQ Global Select Market was $28.67 per share.

We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012, or JOBS Act, and, as such, are subject to reduced public company reporting requirements.

Investing in our Series 1 common stock involves risks. See “Risk Factors” beginning on page 13.

PRICE $ A SHARE

| Price to Public |

Underwriting Discounts and Commissions(1) |

Proceeds to Company |

Proceeds to Selling Stockholders |

|||||||||||||

| Per Share |

$ | $ | $ | $ | ||||||||||||

| Total |

$ | $ | $ | $ | ||||||||||||

| (1) | We have agreed to reimburse the underwriters for certain expenses. See the section titled “Underwriting” on page 142. |

The selling stockholders have granted the underwriters the right to purchase up to an additional shares of Series 1 common stock.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on December , 2013.

| GOLDMAN, SACHS & CO. | MORGAN STANLEY | CREDIT SUISSE |

| JEFFERIES | RBC CAPITAL MARKETS | |

| STIFEL | WILLIAM BLAIR | |

December , 2013.

Table of Contents

Table of Contents

| 1 | ||||

| 13 | ||||

| Special Note Regarding Forward-Looking Statements and Industry Data |

42 | |||

| 43 | ||||

| 44 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

51 | |||

| 82 | ||||

| 103 | ||||

| 110 | ||||

| 119 | ||||

| 125 | ||||

| 130 | ||||

| 135 | ||||

| Material U.S. Federal Tax Consequences To Non-U.S. Holders Of Series 1 Common Stock |

138 | |||

| 142 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

| F-1 |

You should rely only on the information contained in this prospectus or in any free-writing prospectus we may authorize to be delivered or made available to you. We have not, the selling stockholders have not and the underwriters have not authorized anyone to provide you with additional or different information. We and the selling stockholders are offering to sell, and seeking offers to buy, shares of our Series 1 common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus or any free-writing prospectus is accurate only as of its date, regardless of its time of delivery or of any sale of shares of our Series 1 common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the U.S.: We have not, the selling stockholders have not and the underwriters have not done anything that would permit this offering, or possession or distribution of this prospectus, in any jurisdiction where action for that purpose is required, other than in the U.S. Persons outside the U.S. who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of Series 1 common stock and the distribution of this prospectus outside of the U.S.

Table of Contents

This summary highlights information contained elsewhere in this prospectus and is a brief overview of key aspects of the offering. Before investing in our Series 1 common stock, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes and the information set forth in the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Some of the statements in this prospectus constitute forward-looking statements. See the section titled “Special Note Regarding Forward-Looking Statements and Industry Data” for more information.

RETAILMENOT, INC.

Overview

We operate the world’s largest digital coupon marketplace, connecting consumers with leading retailers and brands. In 2012, our marketplace featured digital coupons from over 60,000 retailers and brands, and according to our internal data compiled using Google Analytics, we had more than 450 million total visits to our desktop and mobile websites. As of December 31, 2012, we had contracts with more than 10,000 retailers, or paid retailers. We own and operate the largest digital coupon marketplaces in the U.S. (RetailMeNot.com) and the U.K. (VoucherCodes.co.uk) and the largest portfolio of digital coupon websites in France (Web.Bons-de-Reduction.com, Poulpeo.com and Ma-Reduc.com).

We are the leading digital coupon destination for consumers. In 2013, our marketplace featured more than 500,000 digital coupons in each month. Digital coupons are coupons, coupon codes and brand or category specific discounts made available online or through mobile applications that are used by consumers to make online or in-store purchases directly from retailers. Our websites, mobile applications, email newsletters, alerts and social media presence enable consumers to search for, discover and redeem hundreds of thousands of relevant digital coupons from retailers and brands. Our marketplace features digital coupons across multiple product categories, including clothing; electronics; health and beauty; home and office; travel, food and entertainment; personal and business services; and shoes. We believe our investments in digital coupon content quality, product innovation and direct retailer relationships allow us to offer a compelling experience to consumers looking to save money, whether online or in-store.

We believe we are a trusted partner to retailers and brands. During 2010, 2011 and 2012, our paid retailers realized over $0.2 billion, $1.2 billion and $2.4 billion, respectively, in sales attributable to consumer traffic from digital coupons in our marketplace. We estimate that during the five-day period from November 22, 2012, Thanksgiving Day, through November 26, 2012, commonly known as Cyber Monday, sales attributable to consumer traffic from digital coupons in our marketplace accounted for approximately 2% of retail e-commerce spending in the U.S. We provide our retailers and brands access to a large and engaged consumer audience. We help retailers and brands drive sales and acquire new customers, online through our websites and mobile applications, and in-store by displaying a digital coupon on our mobile applications. We enter into contracts with retailers using a pay-for-performance model that enables us to have a mutually beneficial relationship with our paid retailers, as they pay a commission to us only after a sale is made. Retailers are able to identify consumer traffic referred by our websites and measure the sales they realize from it.

We believe our marketplace benefits from network effects. As more consumers use our marketplace, we are better able to obtain high quality digital coupons from retailers and brands, which in turn attracts a larger consumer audience. We seek to reinforce our position as the leading digital coupon destination by continuing to increase consumer traffic and growing the breadth and depth of our digital coupons, as well as our retailer and brand relationships.

1

Table of Contents

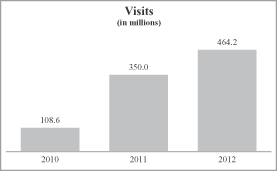

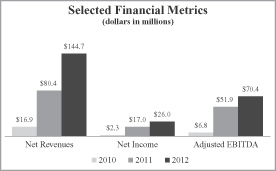

Since we entered the digital coupon market in 2009, we have experienced significant growth. Our net revenues increased from $16.9 million in 2010 to $144.7 million in 2012, representing a 192.9% compound annual growth rate, or CAGR. In the same period, our net income increased from $2.3 million to $26.0 million, representing a 233.0% CAGR, and adjusted EBITDA increased from $6.8 million in 2010 to $70.4 million in 2012, representing a 221.7% CAGR. Our historic growth has been driven organically and through acquisitions. From 2011 to 2012, our consolidated net revenues grew from $80.4 million to $144.7 million. During this period, net revenues from RetailMeNot.com grew organically from $60.5 million to $113.4 million. This $52.9 million increase in net revenues from RetailMeNot.com represents 82.3% of our consolidated net revenues growth. During the nine months ended September 30, 2013, we generated net revenues of $131.3 million, representing a 39.8% increase from the $93.9 million in net revenues we generated during the nine months ended September 30, 2012. Net income changed from $18.2 million for the nine months ended September 30, 2012 to $17.7 million for the nine months ended September 30, 2013, representing a 2.7% decrease from the nine months ended September 30, 2012. Adjusted EBITDA for the nine months ended September 30, 2013 grew to $50.4 million, a 3.5% increase from the $48.7 million in adjusted EBITDA generated during the nine months ended September 30, 2012. From the nine months ended September 30, 2012 to the nine months ended September 30, 2013, organic net revenues grew from $93.9 million to $126.9 million. This $33.0 million increase represented 88.1% of our consolidated net revenues growth. For further discussion regarding adjusted EBITDA, our use of this measure, the limitations of this measure and a reconciliation of adjusted EBITDA to net income, see the section titled “Selected Consolidated Financial and Other Data” on page 47.

In 2012 and the first nine months of 2013, we generated 82.9% and 79.4% of our net revenues, respectively, in the U.S. and the balance in the U.K., France, Canada, Germany and the Netherlands. As of September 30, 2013, we had 414 full-time employees and operations in the U.S., U.K., France, Germany and the Netherlands.

The below charts set forth the growth in our visits, net revenues, net income and adjusted EBITDA for the years ended December 31, 2010, 2011 and 2012:

|

|

Our Industry

We enable consumers to save money while shopping online and in-store and help retailers to drive sales and acquire new customers. The retail industry is large. According to data compiled by Euromonitor International, the worldwide retail industry, excluding grocery retailers, totaled $7.7 trillion in 2012, of which $2.9 trillion was in the markets in which we currently operate. The following trends are driving our industry:

| • | Consumers are increasingly using the Internet to inform purchase decisions and to shop online. According to the Worldwide New Media Market Model published in July 2013 by IDC, the consumer e-commerce market in 2012 was $992.6 billion globally and is projected to grow at a CAGR of 16.7% between 2012 and 2017. |

2

Table of Contents

| • | Mobile commerce is growing rapidly. The proliferation of smartphone devices and tablets makes business to consumer mobile commerce, or m-commerce, one of the fastest growing retail channels. The IDC Worldwide New Media Mobile estimates that m-commerce represented $64.5 billion globally in 2012 and expects it to grow at a 35.5% CAGR between 2012 and 2017. |

| • | Consumers have a mindset for savings. In a January 2013 article, eMarketer estimated that 48.0% of U.S. adult Internet users redeemed a digital coupon for online or offline shopping in the past year. |

| • | Retailers are focused on the return on investment, or ROI, of their marketing spend and are adopting solutions, like digital coupons, which allow them to measure and optimize the impact of their promotional campaigns. |

Consumers and retailers face various challenges that represent barriers to increased retail commerce activity, online and in-store.

Consumers face the following challenges:

| • | difficulty finding relevant coupons for the products and brands they want to purchase; |

| • | invalid or expired coupons; and |

| • | inconvenience associated with traditional coupons found in newspapers and circulars. |

Retailers face the following challenges:

| • | difficulty reaching consumers at scale; |

| • | difficulty engaging consumers across channels; and |

| • | ineffective and difficult to measure marketing solutions. |

Our Solution

We operate the world’s largest digital coupon marketplace, connecting consumers with leading retailers and brands. Consumers are able to visit a trusted destination that allows them to search for, discover and redeem digital coupons from leading retailers, online or in-store. We aggregate digital coupons from retailers, performance marketing networks, our large user community, our employees and outsourced providers. Retailers are able to drive sales and acquire new customers by effectively attracting and engaging a large audience of consumers who are shopping across multiple channels. Our solution enables retailers to better manage their customer acquisition spend and effectively measure their marketing ROI.

Solutions for Consumers

| • | Save money with a broad selection of digital coupons. In 2013, we have featured more than 500,000 digital coupons in each month from retailers and brands across multiple product categories. |

| • | Depth of digital coupon selection from leading retailers within each category. In 2012, we offered thousands of digital coupons per category. Our strong relationships with leading retailers allow us to offer digital coupons exclusive to our marketplace. |

| • | Reliability and curation of digital coupon content. We believe that we provide a high quality experience to consumers by actively monitoring and curating the most frequently visited digital coupon content in our marketplace and incorporating feedback from our large user community. Our merchandising team actively monitors the most frequently visited digital coupon content in our marketplace to ensure content quality and curates such digital coupon content by updating and changing the display and the description of digital coupons. We also provide users the ability to rank |

3

Table of Contents

| digital coupons made available through our marketplace to tell us if a digital coupon made available through our marketplace is valid or not and to submit comments about digital coupon content. Our merchandising team monitors the comments submitted by consumers for additional feedback on digital coupons, such as whether or not the description of the digital coupon contains an error, or is expired, and updates our digital coupon content accordingly. |

| • | Relevance and personalization. We keep consumers informed whenever a digital coupon from one of their preferred retailers becomes available. Consumers can sign up for alerts for digital coupons for specific retailers they have a personal affinity for that come from us via email or submit their brand “likes” and otherwise engage with us on Facebook. We then maintain and use this information to keep our users informed via email or Facebook whenever a digital coupon from one of their preferred retailers becomes available through our marketplace. |

| • | Anytime, anywhere availability and consistency of digital coupons online and in-store. Consumers can search for and discover our digital coupons at virtually any time via our websites, mobile applications, email newsletters and alerts or social media presence. |

Solutions for Retailers

| • | Access to a large consumer audience. In 2012, we had on average over 24.2 million monthly unique visitors to our websites, more traffic than the majority of our retailers’ own websites attract. |

| • | Multichannel engagement with consumers. We enable retailers and brands to consistently engage with consumers online (via our websites, mobile applications, email newsletters, email alerts and social media presence) and in-store (via mobile applications and printed coupons). We have had more than eight million mobile application downloads and have more than thirteen million email subscribers. |

| • | Trusted partnerships and strategic dialogues with retailers. We help optimize digital coupon campaigns for our paid retailers to provide a consistent, high-quality user experience, which we believe reflects positively on the brand image of these retailers. |

| • | Quantifiable, pay-for-performance model that helps retailers measure marketing ROI. Our paid retailers pay a commission to us only after a consumer has made a purchase and are able to track the performance of their digital coupons. |

Our Competitive Strengths

Global leader with scale and strong brands. According to comScore data, we are the largest web property focused on digital coupons as measured by unique visitors. Unique visitors are visitors who have visited one of our websites at least once in a given month. We believe that our strong brand recognition has allowed our marketplace to become the leading destination for consumers looking to save money on retail purchases. As a result, over 90% of traffic to our websites was generated from unpaid sources in 2012. In addition to RetailMeNot.com, our international brand portfolio includes VoucherCodes.co.uk in the U.K., Web.Bons-de-Reduction.com, Poulpeo.com and Ma-Reduc.com in France, Actiepagina.nl in the Netherlands, Deals.com in Germany and RetailMeNot.ca in Canada.

Trusted partner to leading retailers. In 2012, we maintained relationships with more than 10,000 paid retailers, including 367 of the top 500 retailers as ranked in the Internet Retailer 2012 Top 500 Guide, or the 2012 IR500. Additionally, our relationships with most of our top paid retailers are growing. Our top 500 paid retailers paid us, on average, total commission revenues of $235,544 in 2012, demonstrating growth from 2011, when we had paid relationships with 488 of these same retailers, with average total commission revenues of $121,523. During the twelve-month period ended September 30, 2013, we had paid relationships with 498 of these same retailers, with average total commission revenues of $274,811.

4

Table of Contents

Network effects. As more consumers use our marketplace, we are better able to obtain high quality digital coupons from retailers and brands, which in turn attracts a larger consumer audience.

Strong technology platform and proprietary data. Our technology platform is designed to provide the reliability and security necessary to support a large and growing base of consumers, retailers and brands in our marketplace. As engagement through our marketplace increases, we are able to collect more proprietary data on consumer shopping behavior, which allows us to further develop and improve our marketplace in order to better serve consumers and offer more value and insight to our paid retailers. Additionally, our scalable technology serves as a basis to design and support innovative solutions and to further automate and standardize our processes.

Large community of actively engaged users. We leverage our user community’s passion for savings by allowing them to submit digital coupons to our marketplace and to rank and comment on the digital coupons they find the most compelling and relevant, thereby enhancing the content made available to our broad consumer audience. We believe that this engagement by our consumers increases the quality of our content, while lowering our costs to curate and moderate that content ourselves.

Attractive business model with compelling value proposition. In the last three years, we have achieved a compelling combination of growth and profitability. From 2010 to 2012 our net revenues, net income and adjusted EBITDA grew at CAGRs of 192.9%, 233.0% and 221.7%, respectively. We believe our strong financial performance is in part a result of our mutually beneficially relationship with our paid retailers: we generate revenues on a commission basis when retailers complete a sale and consumers save money. For further discussion regarding adjusted EBITDA, our use of this measure, the limitations of this measure and a reconciliation of adjusted EBITDA to net income, see the section titled “Selected Consolidated Financial and Other Data” on page 47.

Our Growth Strategies

Our objective is to expand our position as the largest digital coupon marketplace, connecting consumers with leading retailers and brands. Our strategies to achieve this goal include:

| • | increase traffic and monetization; |

| • | grow depth of paid relationships with retailers; |

| • | enhance mobile solutions and in-store enablement; |

| • | invest in technology and innovation; |

| • | expand internationally; and |

| • | pursue strategic acquisitions. |

Risks Affecting Us

Our business is subject to a number of risks that you should understand before making an investment decision. These risks are discussed more fully in the section titled “Risk Factors” following this prospectus summary. Some of these risks are:

| • | We are an early-stage company with a limited operating history, which makes it difficult to evaluate our current business and future prospects and may increase the risk of your investment. |

| • | We depend on search engines for traffic. Changes to search engine algorithms or practices could adversely affect our ability to generate unpaid traffic, leading to lower revenues and/or increased traffic acquisition costs. |

5

Table of Contents

| • | If we are unable to retain existing retailers, expand our business with existing retailers or attract new consumers, our net revenues may not grow or could decline. |

| • | We depend on performance marketing networks as intermediaries. Factors adversely affecting our relationships with performance marketing networks may adversely affect our ability to attract and retain business and our operating results. |

| • | The market in which we participate is intensely competitive, and we may not be able to compete successfully. |

| • | If we are unsuccessful in expanding the capabilities of our digital coupon solutions for our mobile platforms to allow us to generate net revenues, our net revenues could decline. |

| • | Changes in consumer sentiment or laws, rules or regulations regarding the use of cookies and other tracking technologies and other privacy matters could have a material adverse effect on our ability to generate net revenues and could adversely affect our ability to collect proprietary data on consumer shopping behavior. |

| • | We may be sued by third parties for infringement or other violation of their intellectual or proprietary rights. |

| • | If Texas or any other jurisdiction in which we are resident implements regulations that impose sales tax on certain e-commerce or m-commerce transactions involving the use of performance marketing programs, our net revenues could decline and our business, financial condition and operating results could be adversely affected. |

Corporate Information

We were organized in May 2007 under the name smallponds LLC, which we incorporated into a corporation in September 2007, and are headquartered in Austin, Texas. Our principal executive offices are located at 301 Congress Avenue, Suite 700, Austin, Texas 78701. Our telephone number is (512) 777-2970. Our corporate website address is www.retailmenot.com. The information contained in, or that can be accessed through, our website is not part of this prospectus.

RetailMeNot, VoucherCodes.co.uk, Deals2Buy, Web.Bons-de-Reduction, Poulpeo, Ma-Reduc, Deals.com and Actiepagina.nl are trademarks or logos appearing in this prospectus owned by RetailMeNot, Inc. or one of its subsidiaries. All other trademarks, service marks and trade names appearing in this prospectus are the property of their respective owners.

6

Table of Contents

THE OFFERING

| Series 1 common stock offered by us |

shares |

| Series 1 common stock offered by selling stockholders |

shares |

| Series 1 common stock to be outstanding after this offering |

shares |

| Series 2 common stock to be outstanding after this offering |

6,107,494 shares |

| Total Series 1 and Series 2 common stock to be outstanding after this offering |

shares |

| Use of proceeds |

We intend to use the net proceeds from this offering for working capital and other general corporate purposes, including developing new technologies, funding capital expenditures or making investments in or acquisitions of other businesses, solutions or technologies. We will not receive any of the proceeds from the sale of shares by the selling stockholders. See the section titled “Use of Proceeds.” |

| Proceeds to be paid to certain affiliated parties |

In connection with this offering, our executive officers, directors, beneficial owners of 5.0% or more of our outstanding shares of capital stock, and affiliated entities, will receive approximately $ million of net proceeds from the sale of shares in this offering, after deducting underwriting discounts and commissions payable by such selling stockholders. |

| Risk Factors |

See the section titled “Risk Factors” for a discussion of factors that you should consider carefully before deciding whether to purchase shares of our Series 1 common stock. |

| Voting Rights |

Shares of Series 1 common stock are entitled to one vote per share. Shares of Series 2 common stock are also entitled to one vote per share other than with respect to the election of members of the board of directors. Shares of Series 2 common stock are convertible into an equal number of shares of Series 1 common stock at any time at the election of the holder. See the section titled “Description of Capital Stock.” |

| NASDAQ Global Select Market symbol |

SALE |

7

Table of Contents

Our fiscal year ends on December 31. Except as otherwise indicated, all information in this prospectus (i) is based upon 50,560,515 shares of Series 1 common stock and Series 2 common stock outstanding as of September 30, 2013, and (ii) excludes:

| • | 5,555,499 shares of Series 1 common stock issuable upon the exercise of options outstanding as of September 30, 2013 having a weighted-average exercise price of $10.96 per share; |

| • | 4,089,786 shares of Series 1 common stock, subject to increase on an annual basis, reserved for future issuance under our 2013 Equity Incentive Plan; and |

| • | 560,907 shares of Series 1 common stock, subject to increase on an annual basis, reserved for future issuance under our 2013 Employee Stock Purchase Plan. |

8

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following tables summarize the consolidated financial and operating data for the periods indicated. The summary consolidated statements of operations data for the years ended December 31, 2010, 2011 and 2012 and the summary consolidated balance sheet data as of December 31, 2011 and 2012 have been derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary consolidated statements of operations data presented below for the nine months ended September 30, 2012 and 2013 and the summary consolidated balance sheet data as of September 30, 2013 have been derived from the unaudited interim consolidated financial statements that are included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future. You should read the summary financial data presented below in conjunction with our consolidated financial statements and related notes and the sections titled “Selected Consolidated Financial and Other Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| (in thousands, except per share amounts) | ||||||||||||||||||||

| Consolidated Statements of Operations Data: |

| |||||||||||||||||||

| Net revenues |

$ | 16,862 | $ | 80,402 | $ | 144,685 | $ | 93,895 | $ | 131,312 | ||||||||||

| Costs and expenses: |

||||||||||||||||||||

| Cost of net revenues |

1,848 | 3,980 | 9,113 | 6,475 | 8,735 | |||||||||||||||

| Product development |

658 | 4,388 | 14,481 | 9,326 | 21,103 | |||||||||||||||

| Sales and marketing |

5,661 | 15,341 | 40,672 | 22,543 | 40,974 | |||||||||||||||

| General and administrative |

2,472 | 6,883 | 15,758 | 10,777 | 19,919 | |||||||||||||||

| Amortization of purchased intangible assets |

3,394 | 11,296 | 13,158 | 10,244 | 8,673 | |||||||||||||||

| Other operating expenses |

— | 35 | 6,006 | 2,611 | 1,299 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total costs and expenses |

14,033 | 41,923 | 99,188 | 61,976 | 100,703 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from operations |

2,829 | 38,479 | 45,497 | 31,919 | 30,609 | |||||||||||||||

| Other income (expense): |

||||||||||||||||||||

| Interest expense, net |

(930 | ) | (7,784 | ) | (3,221 | ) | (2,519 | ) | (2,410 | ) | ||||||||||

| Fair value change of common stock warrant |

— | (2,103 | ) | — | — | — | ||||||||||||||

| Fair value change of contingent consideration, net |

1,994 | — | — | — | — | |||||||||||||||

| Other income (expense), net |

(16 | ) | (129 | ) | 77 | 49 | 451 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income taxes |

3,877 | 28,463 | 42,353 | 29,449 | 28,650 | |||||||||||||||

| Provision for income taxes |

(1,533 | ) | (11,502 | ) | (16,360 | ) | (11,201 | ) | (10,959 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 2,344 | $ | 16,961 | $ | 25,993 | $ | 18,248 | $ | 17,691 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Preferred stock dividends on participating preferred stock |

(3,247 | ) | (64,715 | ) | (24,577 | ) | (18,388 | ) | (19,928 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total undistributed earnings (loss) |

(903 | ) | (47,754 | ) | 1,416 | (140 | ) | (2,237 | ) | |||||||||||

| Undistributed earnings allocated to participating preferred stock |

— | — | (1,390 | ) | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) attributable to common stockholders |

$ | (903 | ) | $ | (47,754 | ) | $ | 26 | $ | (140 | ) | $ | (2,237 | ) | ||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) per share attributable to common stockholders: |

||||||||||||||||||||

| Basic and diluted |

$ | (1.27 | ) | $ | (64.19 | ) | $ | 0.03 | $ | (0.17 | ) | $ | (0.16 | ) | ||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted-average number of shares used in computing net income (loss) per share: |

||||||||||||||||||||

| Basic |

709 | 744 | 841 | 821 | 13,703 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted |

709 | 744 | 2,277 | 821 | 13,703 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

9

Table of Contents

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| Consolidated Statements of Operations as Percentage of Net Revenues: |

||||||||||||||||||||

| Net revenues |

100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||||

| Costs and expenses: |

||||||||||||||||||||

| Cost of net revenues |

11.0 | 5.0 | 6.3 | 6.9 | 6.7 | |||||||||||||||

| Product development |

3.9 | 5.5 | 10.0 | 9.9 | 16.1 | |||||||||||||||

| Sales and marketing |

33.6 | 19.1 | 28.1 | 24.0 | 31.2 | |||||||||||||||

| General and administrative |

14.7 | 8.6 | 10.9 | 11.5 | 15.2 | |||||||||||||||

| Amortization of purchased intangible assets |

20.1 | 14.0 | 9.1 | 10.9 | 6.6 | |||||||||||||||

| Other operating expenses |

— | — | 4.2 | 2.8 | 0.9 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total costs and expenses |

83.3 | 52.2 | 68.6 | 66.0 | 76.7 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from operations |

16.7 | 47.8 | 31.4 | 34.0 | 23.3 | |||||||||||||||

| Other income (expense): |

||||||||||||||||||||

| Interest expense, net |

(5.5 | ) | (9.7 | ) | (2.2 | ) | (2.7 | ) | (1.8 | ) | ||||||||||

| Fair value change of common stock warrant |

— | (2.6 | ) | — | — | — | ||||||||||||||

| Fair value change of contingent consideration, net |

11.8 | — | — | — | — | |||||||||||||||

| Other income (expense), net |

(0.1 | ) | (0.2 | ) | 0.1 | 0.1 | 0.3 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income taxes |

22.9 | 35.3 | 29.3 | 31.4 | 21.8 | |||||||||||||||

| Provision for income taxes |

(9.1 | ) | (14.3 | ) | (11.3 | ) | (12.0 | ) | (8.3 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

13.8 | % | 21.0 | % | 18.0 | % | 19.4 | % | 13.5 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| As of December 31, | As of September 30, 2013 |

|||||||||||

| 2011 | 2012 | |||||||||||

| (dollars in thousands) | ||||||||||||

| Consolidated Balance Sheet Data: |

||||||||||||

| Cash and cash equivalents |

$ | 88,234 | $ | 97,142 | $ | 136,408 | ||||||

| Working capital |

78,631 | 98,152 | 141,122 | |||||||||

| Total assets |

347,326 | 370,920 | 432,171 | |||||||||

| Total liabilities |

74,817 | 63,266 | 69,725 | |||||||||

| Redeemable convertible preferred stock |

321,450 | 349,027 | — | |||||||||

| Total stockholders’ equity (deficit) |

(48,941 | ) | (41,373 | ) | 362,446 | |||||||

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| (in thousands, except net revenues per visit) | ||||||||||||||||||||

| Operating Metrics:(1) |

||||||||||||||||||||

| Visits |

108,574 | 349,992 | 464,240 | 315,802 | 376,289 | |||||||||||||||

| Net revenues per visit |

$ | 0.16 | $ | 0.23 | $ | 0.31 | $ | 0.30 | $ | 0.35 | ||||||||||

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

| Other Financial Data: |

||||||||||||||||||||

| Adjusted EBITDA(2) |

$ | 6,800 | $ | 51,895 | $ | 70,373 | $ | 48,657 | $ | 50,357 | ||||||||||

| (1) | See the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Financial and Operating Metrics” on page 54 for a description of these operating metrics. |

10

Table of Contents

| (2) | We define adjusted EBITDA as net income plus depreciation, amortization of intangible assets, stock-based compensation expense, third party acquisition-related costs, other non-cash operating expenses (including asset impairment charges and compensation-related charges associated with seller notes issued in connection with acquisitions), net interest expense, other non-operating income or expense (including changes in fair value of warrant liabilities and contingent consideration) and income taxes, net of any foreign exchange income or expense. |

The following table presents a reconciliation of adjusted EBITDA to net income for each of the periods indicated:

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

| Reconciliation of Adjusted EBITDA: |

||||||||||||||||||||

| Net income |

$ | 2,344 | $ | 16,961 | $ | 25,993 | $ | 18,248 | $ | 17,691 | ||||||||||

| Depreciation and amortization expense |

3,460 | 11,556 | 14,192 | 10,938 | 10,076 | |||||||||||||||

| Stock-based compensation expense |

68 | 471 | 4,048 | 2,559 | 7,068 | |||||||||||||||

| Third-party acquisition-related costs |

443 | 1,354 | 630 | 630 | 1,305 | |||||||||||||||

| Other operating expenses |

— | 35 | 6,006 | 2,611 | 1,299 | |||||||||||||||

| Interest expense, net |

930 | 7,784 | 3,221 | 2,519 | 2,410 | |||||||||||||||

| Fair value change of common stock warrant |

— | 2,103 | — | — | — | |||||||||||||||

| Fair value change of contingent consideration, net |

(1,994 | ) | — | — | — | — | ||||||||||||||

| Other (income) expense, net |

16 | 129 | (77 | ) | (49 | ) | (451 | ) | ||||||||||||

| Provision for income taxes |

1,533 | 11,502 | 16,360 | 11,201 | 10,959 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

$ | 6,800 | $ | 51,895 | $ | 70,373 | $ | 48,657 | $ | 50,357 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

The following tables present depreciation and stock-based compensation expense as included in the various lines of our consolidated statements of operations:

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

| Depreciation Expense: |

||||||||||||||||||||

| Cost of net revenues |

$ | 16 | $ | 62 | $ | 99 | $ | 45 | $ | 199 | ||||||||||

| Product development |

12 | 74 | 380 | 236 | 570 | |||||||||||||||

| Sales and marketing |

27 | 84 | 382 | 302 | 417 | |||||||||||||||

| General and administrative |

11 | 40 | 173 | 111 | 217 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total depreciation expense |

$ | 66 | $ | 260 | $ | 1,034 | $ | 694 | $ | 1,403 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

| Stock-Based Compensation Expense: |

||||||||||||||||||||

| Cost of net revenues |

$ | 1 | $ | 23 | $ | 157 | $ | 81 | $ | 449 | ||||||||||

| Product development |

12 | 164 | 1,144 | 713 | 1,641 | |||||||||||||||

| Sales and marketing |

23 | 113 | 993 | 592 | 1,568 | |||||||||||||||

| General and administrative |

32 | 171 | 1,754 | 1,173 | 3,410 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total stock-based compensation expense |

$ | 68 | $ | 471 | $ | 4,048 | $ | 2,559 | $ | 7,068 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

11

Table of Contents

Non-GAAP Financial Measures

Adjusted EBITDA

To provide investors with additional information regarding our financial results, we have disclosed in the table above and elsewhere in this prospectus adjusted EBITDA, a non-GAAP financial measure. We have provided a reconciliation above of adjusted EBITDA to net income, the most directly comparable GAAP financial measure.

We have included adjusted EBITDA in this prospectus because it is a key measure used by our management and board of directors to understand and evaluate our operating performance for the following reasons:

| • | our management uses adjusted EBITDA in conjunction with GAAP financial measures as part of our assessment of our business and in communications with our board of directors concerning our financial performance; |

| • | our management and board of directors use adjusted EBITDA in establishing budgets, operational goals and as an element in determining executive compensation; |

| • | adjusted EBITDA provides consistency and comparability with our past financial performance, facilitates period-to-period comparisons of operations that could otherwise be masked by the effect of the expenses that we exclude in this non-GAAP financial measure and facilitates comparisons with other peer companies, many of which use similar non-GAAP financial measures to supplement their GAAP results; |

| • | securities analysts use a measure similar to our adjusted EBITDA as a supplemental measure to evaluate the overall operating performance and comparison of companies, and we include adjusted EBITDA in our investor and analyst presentations; and |

| • | adjusted EBITDA excludes non-cash charges, such as depreciation, amortization and stock-based compensation, because such non-cash expenses in any specific period may not directly correlate to the underlying performance of our business operations and can vary significantly between periods. |

Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are:

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future, and adjusted EBITDA does not reflect cash capital expenditure requirements for such replacements or for new capital expenditure requirements; |

| • | adjusted EBITDA excludes stock-based compensation expense which has been, and will continue to be for the foreseeable future, a significant recurring expense in our business and is an important part of our employees’ compensation; |

| • | adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| • | adjusted EBITDA does not reflect tax payments that may represent a reduction in cash available to us; and |

| • | other companies, including companies in our industry, may calculate adjusted EBITDA differently, which reduces its usefulness as a comparative measure. |

Because of these limitations, you should consider adjusted EBITDA alongside other financial performance measures, including various cash flow metrics, net income and our other GAAP results.

12

Table of Contents

An investment in our Series 1 common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below and all other information contained in this prospectus before deciding whether to purchase shares of our Series 1 common stock. Our business, prospects, financial condition or operating results could be materially adversely affected by any of these risks, as well as other risks not currently known to us or that are currently considered immaterial. The trading price of our Series 1 common stock could decline due to any of these risks, and you may lose all or part of your investment. In assessing these risks, you should also refer to the other information contained in this prospectus, including our consolidated financial statements and related notes, before deciding to purchase any shares of our Series 1 common stock.

Risks Related to Our Business

We are an early-stage company with a limited operating history, which makes it difficult to evaluate our current business and future prospects and may increase the risk of your investment.

We began our operations in September 2007 and did not enter the digital coupons industry until late 2009. Our limited operating history may make it difficult to evaluate our current business and our future prospects. We have encountered and will continue to encounter risks and difficulties frequently experienced by growing companies in rapidly changing industries, including challenges in accurate financial planning and forecasting. You should consider our business and prospects in light of the risks and difficulties we may encounter as an early-stage company.

If we are unable to continue to attract visitors to our websites from search engines, then consumer traffic to our websites could decrease, which could negatively impact the number of purchases generated for our retailers through our marketplace, and therefore negatively impact our ability to maintain or grow our net revenues and profitability.

We generate consumer traffic to our websites using various methods, including search engine marketing, or SEM, search engine optimization, or SEO, email campaigns and social media referrals. Our net revenues and profitability levels are dependent upon our continued ability to use a combination of these methods to generate consumer traffic to our websites in a cost-efficient manner. We have experienced and continue to experience fluctuations in search result rankings for a number of our websites. There can be no assurances that we will be able to grow or maintain current levels of consumer traffic to our websites.

Our SEM and SEO techniques have been developed to work with existing search algorithms utilized by the major search engines. Major search engines frequently modify their search algorithms. Changes in these algorithms could cause our websites to receive less favorable placements, which could reduce the number of users who visit our websites. We may be unable to modify our SEM and SEO strategies in response to any future search algorithm changes made by the major search engines, which could require a change in the strategy we use to generate consumer traffic to our websites.

In addition, websites must comply with search engine guidelines and policies. These guidelines and policies are complex and may change at any time. If we fail to follow such guidelines and policies properly, search engines may rank our content lower in search results or could remove our content altogether from their indices. If we fail to understand and comply with these guidelines, our SEO strategy may become unsuccessful.

If we are listed less prominently or fail to appear in search result listings for any reason, including as a result of our failure to successfully execute our SEM and SEO strategies, or our failure to comply with search engine guidelines and policies, it is likely that the number of visitors to our websites will decline. Any such decline in consumer traffic to our websites could adversely impact the number of purchases we generate for our retailers, which could adversely affect our net revenues. We may not be able to replace this traffic with the same volume

13

Table of Contents

of visitors or in the same cost-effective manner from other channels, such as cost-per-click search engine marketing or display or other advertising, or at all. An attempt to replace this traffic through other channels may require us to increase our sales and marketing expenditures, which would adversely affect our operating results and which may not be offset by additional net revenues.

If we are unable to retain our existing retailers, expand our business with existing retailers or attract new retailers and consumers, our net revenues could decline.

Our ability to continue to grow our net revenues will depend in large part on expanding our business with existing retailers and attracting new retailers. The number of our current retailers may not expand materially beyond our existing base and may decline. Furthermore, even for our largest retailers, the amount they pay us is typically only a small fraction of their overall advertising budget. Retailers may view their spend with us as experimental and may either reduce or terminate their spend with us if they determine a superior alternative for generating sales. In addition, retailers may determine that distributing digital coupons through our platform results in undesirably broad distribution of their coupons or otherwise does not provide a compelling value proposition. Some retailers have demanded that we remove digital coupons relating to their products or services from our websites, and we anticipate that some retailers will do so in the future. Retailers also may reduce the commission rates they pay to us for sales our websites facilitate. If we are unable to negotiate favorable terms with current or new retailers in the future, including the commission rates they pay us, our operating results will be adversely affected. Additionally, retailers may fail to pay the performance marketing networks the fees the retailers owe, which is a prerequisite to us receiving our commissions from the networks.

Retailers do not enter into long-term obligations with us requiring them to use our solutions and their contracts with us are cancelable upon short or no notice and without penalty. We cannot be sure that our retailers will continue to use our solutions or that we will be able to replace retailers that do not renew their campaigns with new ones generating comparable revenues.

If we are unable to attract new consumers and maintain or increase consumer traffic to our websites, new retailers may choose not to use, and existing retailers may not continue to use, our solutions for their promotional campaigns, and our volume of new digital coupon inventory may suffer as the perceived usefulness of our marketplace declines. If our existing retailers do not continue to use our solutions for their promotional campaigns, or if we are unable to attract and expand the amount of business we do with new retailers, our sales will decrease and our operating results will be adversely affected.

We are highly dependent on performance marketing networks as intermediaries. Factors adversely affecting our relationships with performance marketing networks, or the termination of these networks, may adversely affect our ability to attract and retain business and our operating results.

Most of our net revenues comes from commissions earned for promoting digital coupons on behalf of retailers. Often, the commissions we earn are tracked and paid by performance marketing networks. For 2012, 96.4% of our net revenues came from retailers that pay us through performance marketing networks, primarily Commission Junction, LinkShare and Google Affiliate Network. Performance marketing networks provide retailers with affiliate tracking links for revenues attribution to publishers and the ability to distribute digital coupon content to multiple publishers. We do not have exclusive relationships with performance marketing networks. They do not enter into long-term commitments to us allowing us to use their solutions, and their contracts with us are cancelable upon short or no notice and without penalty.

Our sales could be adversely impacted by industry changes relating to the use of performance marketing networks. For example, if retailers seek to bring the distribution of their digital coupon content in-house rather than using a performance marketing network, we would need to develop relationships with more retailers directly, which we might not be able to do and which could increase our sales, marketing and product expenses. Additionally, we face challenges associated with consumers’ increasing use of mobile devices to complete their

14

Table of Contents

online purchases. For example, many retailers currently do not recognize affiliate tracking links on their mobile-optimized websites or applications, and tracking mechanisms on mobile websites or applications may not function to allow retailers to properly attribute sales to us. As a result, we may not receive commission revenues when a consumer makes a purchase from their mobile device on a retailer’s mobile-optimized website after clicking through a digital coupon displayed on one of our websites or mobile applications if the retailer’s mobile monetization mechanisms are not enabled.

Moreover, as a result of dealing primarily with performance marketing networks, we have less of a direct relationship with retailers than would be the case if we dealt directly with retailers. The presence of performance marketing networks as intermediaries between us and retailers creates a challenge to building our own brand awareness and affinity with retailers. Additionally, in the event that our relationship with a performance marketing network were to terminate, our mechanism for receiving payments from the retailers we service through that network would terminate, which could materially and adversely impact our net revenues.

Some performance marketing networks that we work with could be considered our competitors because they also offer some components of our solution, including publishing digital coupons on their own websites. If they further develop these capabilities, they may offer their own competitive solutions to retailers and, as a result, our ability to compete effectively could be significantly compromised and our business and operating results could be adversely affected.

If retailers alter the way they attribute credit to publishers in their performance marketing programs, our net revenues could decline and our operating results could be adversely affected.

Retailers often advertise and market digital coupons through performance marketing programs, a type of performance-based marketing in which a retailer rewards one or more publishers for each visitor or customer generated by the publisher’s own marketing efforts. When a consumer executes a purchase on a retailer’s website as a result of a performance marketing program, most performance marketing conversion tracking tools credit the most recent link or ad clicked by the consumer prior to that purchase. This practice is generally known as “last-click attribution.” We generate the vast majority of our net revenues through transactions for which we receive last-click attribution. In recent years, some retailers have sought, and in some cases adopted, alternatives to last-click attribution. These alternatives are primarily “first-click attribution,” which credits the first link or ad clicked by a consumer prior to executing a purchase, or “multichannel attribution,” which applies weighted values to each of a retailer’s advertisements and tracks how each of those advertisements contributed to a purchase. If retailers widely adopt first-click attribution, multichannel attribution or otherwise alter the ways they attribute credit for purchases to us, and if we are unable to adapt our business practices to such alterations, our net revenues could decline and our business, financial condition and operating results could be adversely affected.

The market in which we participate is intensely competitive, and we may not be able to compete successfully.

The market for digital coupon solutions is highly competitive, fragmented and rapidly changing. Our competition for traffic from consumers seeking to save money on online or in-store purchases includes digital coupon websites and mobile applications, cash back and loyalty websites, retailers, search engines, social networks, comparison shopping websites, newspapers and direct mail campaigns. Our competition for retailer marketing spend includes digital coupon sites that offer a pay-for-performance model, search engines and social networks that compete for online advertising spend and television, magazines and newspapers that compete for offline advertising spend. With the introduction of new technologies and the influx of new entrants to the market, we expect competition to persist and intensify in the future, which could harm our ability to increase sales and maintain our profitability. We also expect competition in e-commerce generally, and digital coupon solutions in particular, to continue to increase because there are no significant barriers to entry. A substantial number of digital coupon websites, including those that attempt to replicate our business model, have emerged globally. In addition to such competitors, we are experiencing increasing competition from other large businesses that offer digital coupons similar to ours as an add-on to their core business. For example, Groupon and Living Social are

15

Table of Contents

now offering digital coupons, and Google and PayPal are now offering digital coupons for in-store purchases. We also expect to compete against other Internet sites that serve niche markets and interests. In addition, we compete with traditional offline coupon and discount services, as well as newspapers, magazines and other traditional media companies that provide coupons and discounts on products and services.

Our success depends on the breadth, depth, quality and reliability of our digital coupon selection, as well as our continued innovation and ability to provide features that make our marketplace useful and appealing to consumers. If we are unable to develop quality features that consumers want to use, then consumers may become dissatisfied with our marketplace and elect to use the offerings of one of our competitors, which could adversely affect our operating results.

Certain of our larger potential competitors may have the resources to significantly change the nature of the digital coupon industry to their advantage, which could materially disadvantage us. For example, Google, PayPal, Yahoo!, Bing and Facebook have widely adopted industry platforms which they could leverage to distribute digital coupons that could be disadvantageous to our competitive position.

Our current and potential competitors may have significantly more financial, technical, marketing and other resources than we have, be able to devote greater resources to the development, promotion, sale and support of their products and services, have more extensive consumer bases and deeper relationships, and may have longer operating histories and greater name recognition than we have. As a result, these competitors may be better able to respond quickly to new technologies, develop deeper retailer relationships or offer services at lower prices. Any of these developments would make it more difficult for us to sell our solutions and could result in increased pricing pressure, reduced profit margins, increased sales and marketing expenses or the loss of market share.

In the traditional coupon landscape, our primary competitors for advertising spend include publishers of printable coupons. Many of these competitors have significant consumer reach, well-developed retailer relationships, and much larger financial resources and longer operating histories than we have.

We also directly and indirectly compete with retailers for consumer traffic. Many retailers market and offer their own digital coupons directly to consumers using their own websites, email newsletter and alerts, mobile applications, social media presence and other distribution channels. Our retailers could be more successful than we are at marketing their own digital coupons or could decide to terminate their relationship with us because they no longer want to pay us to compete against them.

We may face competition from companies we do not yet know about. If existing or new companies develop, market or resell competitive digital coupon solutions, acquire one of our existing competitors or form a strategic alliance with one of our competitors, our ability to compete effectively could be significantly compromised and our operating results could be harmed.

We have experienced rapid growth in recent periods. If we fail to manage our growth, our financial performance may suffer.

We have expanded our overall business, consumer traffic, paid retailers, employee headcount and operations in recent periods. We increased our total number of full-time employees and contractors from 35 as of December 31, 2010 to 414 as of September 30, 2013. We have also established or acquired operations in other countries. In 2011, we acquired the business of VoucherCodes.co.uk, which is based in the U.K. In 2012, we acquired Web.Bons-de-Reduction.com and Poulpeo.com, which are based in France, and relaunched Deals.com in Germany. In March 2013, we acquired Actiepagina.nl, which is based in the Netherlands. In July 2013, we acquired Ma-Reduc.com, which is based in France. In most of these instances, we previously had no presence in these countries. Our business is becoming increasingly complex, especially in light of the number of acquisitions we have integrated and are in the process of integrating. Our limited operating history, reliance on multiple websites and brands and our rapid expansion have placed, and will continue to place, a significant strain on our managerial, operational, product development, sales and marketing, administrative, financial and other resources.

16

Table of Contents

We expect to continue to increase headcount and to hire more specialized personnel in the future. We will need to continue to hire, train and manage additional qualified website developers, software engineers, partner management personnel and sales and marketing staff in order to improve and maintain our technology to properly manage our growth. If our new hires perform poorly, if we are unsuccessful in hiring, training, managing and integrating these new employees or if we are not successful in retaining our existing employees, our business may be harmed.

Further, to accommodate our expected growth we must add new hardware and software and improve and maintain our technology, systems and network infrastructure. Failure to effectively upgrade our technology or network infrastructure to support our expected increases in traffic volume could result in unanticipated system disruptions, slow response times or poor experiences for consumers. To manage the expected growth of our operations and personnel and to support financial reporting requirements as a public company, we will need to improve our transaction processing and reporting, operational and financial systems, procedures and controls. These improvements will be particularly challenging if we acquire new operations with different back-end systems. For example, we are in the process of converting the method of collecting a substantial portion of the data necessary to record our net revenues. Our current and planned personnel, systems, procedures and controls may not be adequate to support our future operations. If we are unable to manage our growth successfully and hire additional qualified personnel in an efficient manner, our business, financial conditions and operating results could be adversely affected.

We experience quarterly fluctuations in our operating results due to a number of factors that make our future results difficult to predict and could cause our operating results to fall below expectations or our guidance.

Our business is subject to seasonal fluctuations. Specifically, our net revenues are traditionally strongest in the third and fourth quarters of each year due to increases in holiday shopping. Conversely, our first and second quarter net revenues are typically lower.

Since the majority of our expenses are personnel-related and include salaries and stock-based compensation, benefits and incentive-based compensation plan expenses, we have not experienced significant seasonal fluctuations in the timing of our expenses from period to period other than increases in discretionary advertising and promotional spending during the third and fourth quarter holiday shopping period. We plan to continue to increase our investment in sales and marketing and product development substantially as we seek to leverage our solution to capitalize on what we see as a growing global opportunity. We also expect that our general and administrative expenses will increase both to support our growing operations and manage increased costs of operating as a public company. For the foregoing reasons or other reasons we may not anticipate, historical patterns should not be considered indicative of our future sales activity, expenditure levels or performance.

Factors that may affect our quarterly operating results include the following:

| • | the number and quality of the digital coupons on our websites and mobile applications; |

| • | consumer visits to our websites and use of our mobile applications, and purchases of retail products by consumers resulting from those visits; |

| • | the success and costs of our online advertising and marketing initiatives, including advertising costs for paid search keywords that we deem relevant to our business; |

| • | the levels of compensation that retailers are willing to pay us to attract customers; |

| • | the amount that consumers spend when they make purchases using the digital coupons we provide; |

| • | market acceptance of our current and future solutions, including our ability to sell additional solutions to existing retailers and to add new retailers to our business in multiple regions around the world; |

| • | overall levels of consumer spending; |

17

Table of Contents

| • | the budgeting cycles of our retailers; |

| • | the cyclical and discretionary nature of marketing spend and any resulting changes in the number and quality of digital coupons that retailers choose to offer; |

| • | changes in the competitive dynamics of the digital coupon industry, including consolidation among competitors, performance marketing networks or customers, and our reputation and brand strength relative to our competitors; |

| • | the response of consumers to our digital coupon content; |

| • | our ability to control costs, including our operating expenses; |

| • | network outages, errors in our solutions or security breaches and any associated expenses and collateral effects; |

| • | our ability to achieve the growth rate that was anticipated by us in setting our operating and capital expense budgets; |

| • | foreign currency exchange rate fluctuations, as our foreign sales and costs are denominated in local currencies; |

| • | costs related to acquisitions or licensing of, or investments in, products, services, technologies or other businesses and our ability to integrate and manage any acquisitions successfully; and |

| • | general economic and political conditions in our domestic and international markets. |

As a result of these and other factors, we have a limited ability to forecast the amount of future net revenues and expenses, and our operating results may vary from quarter to quarter and may fall below our estimates or the expectations of public market analysts and investors. Fluctuations in our quarterly operating results may lead analysts to change their long-term models for valuing our common stock, cause us to face short-term liquidity issues, impact our ability to retain or attract key personnel or cause other unanticipated issues, all of which could cause our stock price to decline. As a result of the potential variations in our quarterly net revenues and operating results, we believe that quarter-to-quarter comparisons of our net revenues and operating results may not be meaningful and the results of any one quarter should not be relied upon as an indication of future performance.

If online commerce does not continue to grow, or contracts, our business may suffer.

The business of selling goods and services over the Internet, and the use of digital coupons in those transactions, is dynamic and relatively new. Concerns about fraud, privacy and other challenges may discourage additional consumers from adopting the Internet as a medium of commerce. Acquiring new customers for our marketplace and increasing consumer traffic may become more difficult and costly than it has been in the past, particularly in markets where our marketplace has been available for some time. In order to increase consumer traffic to our websites and use of our mobile applications, we must appeal to consumers who historically have used traditional means of commerce to purchase goods and services and may prefer alternatives to our websites, such as the retailer’s own website. If these consumers prove to be less active than consumers who are already providing traffic to our websites, or we are unable to gain efficiencies in our operating costs, including our cost of increasing consumer traffic to our websites, our business could be adversely impacted. Furthermore, to the extent that weak economic conditions cause consumer spending to decline or cause our customers and potential customers to freeze or reduce their marketing budgets, particularly in the online retail market, demand for our solutions may be negatively affected.

If we are not able to maintain a positive perception of the content available through our marketplace, maintain and enhance our RetailMeNot brand and the brands associated with each of our other websites, our reputation and business may suffer.

A decrease in the quality of the digital coupons available through our marketplace could harm our reputation and damage our ability to attract and retain consumers and retailers, which could adversely affect our business.

18

Table of Contents

Additionally, maintaining and enhancing our RetailMeNot brand and the brands of each of our other websites are critical to our ability to attract new retailers and consumers to our marketplace, generate net revenues and successfully introduce new solutions. We may not be able to successfully build our RetailMeNot brand in the U.S. without losing some or all of the value associated with, or decreasing the effectiveness of, our other brands. We expect that the promotion of our brands will require us to make substantial investments and as our market becomes more competitive, these branding initiatives may become increasingly difficult and expensive. The successful promotion of our brands will depend largely on our marketing and public relations efforts. If we do not successfully maintain and enhance our brands, we could lose consumer traffic, which could, in turn, cause retailers to terminate or reduce the extent of their relationship with us. Our brand promotion activities may not be successful or may not yield net revenues sufficient to offset this cost, which could adversely affect our reputation and business.