Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - SOUTH AMERICAN GOLD CORP. | Financial_Report.xls |

| EX-31.1 - EXHIBIT311 - SOUTH AMERICAN GOLD CORP. | exhibit311.htm |

| EX-32.1 - EXHIBIT321 - SOUTH AMERICAN GOLD CORP. | exhibit321.htm |

| EX-31.2 - EXHIBIT312 - SOUTH AMERICAN GOLD CORP. | exhibit312.htm |

| EX-32.2 - EXHIBIT322 - SOUTH AMERICAN GOLD CORP. | exhibit322.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

(Mark One)

|

x

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended September 30, 2013

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ________ to ________

Commission File Number: 000-52156

South American Gold Corp.

(Exact name of registrant as specified in its charter)

|

Nevada

|

98-0486676

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

3645 E. Main Street, Suite 119, Richmond, IN 47374

|

|

(Address of principal executive offices)

|

|

(765) 356-9726

|

|

(Registrant’s telephone number, including area code)

|

|

______________________________________________________________________

|

|

(Former name, former address and former fiscal year, if changed since last report)

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” and “a smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o

Non-accelerated filer o (Do not check if a smaller reporting company) Smaller reporting company x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes x No

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

|

Class

|

Outstanding Shares as of September 30, 2013

|

|

|

Common Stock, $0.001 par value

|

289,062,039

|

|

FORM 10-Q

SOUTH AMERICAN GOLD CORP.

September 30, 2013

|

Page

|

|

|

PART I – FINANCIAL INFORMATION

|

||

|

Item 1.

|

3

|

|

|

Item 2.

|

4

|

|

|

Item 3.

|

19

|

|

|

Item 4.

|

19

|

|

|

PART II – OTHER INFORMATION

|

||

|

Item 1.

|

21

|

|

|

Item 1A.

|

21

|

|

|

Item 2.

|

21

|

|

|

Item 3.

|

21

|

|

|

Item 4.

|

21

|

|

|

Item 5.

|

21

|

|

|

Item 6.

|

22

|

|

| 23 | ||

PART I - FINANCIAL INFORMATION

|

Our unaudited financial statements included in this Form 10-Q are as follows:

|

|

|

F-1

|

|

|

F-2

|

|

|

F-3

|

|

|

F-4

|

|

These unaudited financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America for interim financial information and the SEC instructions to Form 10-Q. In the opinion of management, all adjustments considered necessary for a fair presentation of the results of operations and financial position have been included and all such adjustments are of a normal recurring nature. Operating results for the interim period ended September 30, 2013 are not necessarily indicative of the results that can be expected for the full year.

|

SOUTH AMERICAN GOLD CORP. AND SUBSIDIARIES

|

||||||||

|

(An Exploration Stage Company)

|

||||||||

|

September 30,

|

June 30,

|

|||||||

|

2013

|

2013

|

|||||||

|

(Unaudited)

|

||||||||

|

Assets

|

||||||||

|

Current Assets

|

||||||||

|

Cash and cash equivalents

|

$ | 53 | $ | 118 | ||||

|

Other Receivable

|

1,000 | - | ||||||

|

Total current assets

|

1,053 | 118 | ||||||

|

Equipment net of depreciation

|

1,000 | 1,063 | ||||||

|

Investments

|

10,500 | - | ||||||

|

Total Assets

|

$ | 12,553 | $ | 1,181 | ||||

|

Liabilities and Stockholders' Equity (Deficit)

|

||||||||

|

Current Liabilities

|

||||||||

|

Accounts payable and accrued expenses

|

||||||||

|

(including related party amounts of $87,862 and $72,827)

|

$ | 306,686 | $ | 264,557 | ||||

|

Convertible Notes Payable, net of discount of $23,329

|

36,758 | 39,938 | ||||||

|

Notes payable

|

9,500 | |||||||

|

Derivative Liability

|

97,261 | 142,609 | ||||||

|

Current Liabilities

|

450,205 | 447,104 | ||||||

|

Notes Payable

|

18,500 | 18,500 | ||||||

|

Total Liabilities

|

468,705 | 465,604 | ||||||

|

Stockholders' Equity (Deficit)

|

||||||||

|

Common stock, $0.001 par value, 450,000,000 shares

|

||||||||

|

authorized, 289,062,039 & 221,123,407 issued & outstanding

|

||||||||

|

as of September 30, 2013 & June 30, 2013, respectively

|

289,062 | 221,123 | ||||||

|

Additional paid-in capital

|

4,126,627 | 4,110,421 | ||||||

|

Accumulated other comprehensive income

|

355 | (2,665 | ) | |||||

|

Deficit accumulated during the exploration stage

|

(4,872,196 | ) | (4,793,302 | ) | ||||

|

Total Stockholders' Equity (Deficit)

|

(456,152 | ) | (464,423 | ) | ||||

|

Total liabilities and stockholders' equity (deficit)

|

$ | 12,553 | $ | 1,181 | ||||

|

The accompanying notes are an integral part of these condensed consolidated financial statements

|

||||||||

|

SOUTH AMERICAN GOLD CORP. AND SUBSIDIARIES

|

||||||||||||

|

(Exploration Stage Company)

|

||||||||||||

|

(Unaudited)

|

||||||||||||

|

For the three months ended

September 30,

|

For the Period

May 25, 2005 (Inception) to |

|||||||||||

|

2013

|

2012

|

September 30, 2013

|

||||||||||

|

Revenues

|

$ | - | $ | - | $ | - | ||||||

|

Operating Expenses

|

||||||||||||

|

Exploration Expense

|

6,000 | 15,272 | 741,034 | |||||||||

|

Stock Based Compensation

|

- | - | 1,566,348 | |||||||||

|

Impairment loss on Goodwill

|

- | - | 1,285,710 | |||||||||

|

Impairment loss on Mining Lease

|

- | 29,000 | 29,000 | |||||||||

|

Depreciation

|

63 | - | 1,908 | |||||||||

|

General & Administrative Expense

|

44,088 | 38,355 | 1,273,548 | |||||||||

|

Total Operating Expense

|

50,151 | 82,627 | 4,897,548 | |||||||||

|

Income (loss) from operations

|

(50,151 | ) | (82,627 | ) | (4,897,548 | ) | ||||||

|

Other Income (Expense)

|

||||||||||||

|

Gain (Loss) on derivative liability

|

(5,054 | ) | (20,323 | ) | 23,348 | |||||||

|

Gain on sale of mining lease

|

8,500 | - | 8,500 | |||||||||

|

Interest Expense

|

(32,189 | ) | (22,082 | ) | (264,742 | ) | ||||||

|

Interest income

|

- | - | 12,713 | |||||||||

|

Total Other Income

|

(28,743 | ) | (42,405 | ) | (220,181 | ) | ||||||

|

Net Loss

|

(78,894 | ) | (125,032 | ) | (5,117,729 | ) | ||||||

|

Net loss attributable to non-controlling interest

|

- | - | (245,532 | ) | ||||||||

|

Net loss attributable to South American Gold Corp.

|

$ | (78,894 | ) | $ | (125,032 | ) | $ | (4,872,197 | ) | |||

|

Net Loss

|

$ | (78,894 | ) | $ | (125,032 | ) | $ | (5,117,729 | ) | |||

|

Other comprehensive income (loss)

|

||||||||||||

|

Unrealized gain on Investments

|

3,000 | - | 3,000 | |||||||||

|

Foreign currency translation adjustment

|

20 | (22 | ) | 5,694 | ||||||||

|

Foreign currency translation adjustment attributable to

non-controlling interest attributable to non-controlling interest

|

- | - | (8,339 | ) | ||||||||

|

Total other comprehensive income (loss)

|

3,020 | (22 | ) | 355 | ||||||||

|

Comprehensive income (loss)

|

$ | (75,874 | ) | $ | (125,054 | ) | $ | (5,117,374 | ) | |||

|

Net loss per common share outstanding,

|

||||||||||||

|

basic and diluted

|

$ | (0.00 | ) | $ | (0.00 | ) | ||||||

|

Weighted average shares outstanding of common

|

||||||||||||

|

stock, basic and diluted

|

282,687,758 | 82,146,673 | ||||||||||

|

The accompanying notes are an integral part of these condensed consolidated financial statements

|

||||||||||||

|

SOUTH AMERICAN GOLD CORP. AND SUBSIDIARIES

|

||||||||||||

|

(Exploration Stage Company)

|

||||||||||||

|

|

For the period

|

|||||||||||

|

For the three months ended

|

May 25, 2005

|

|||||||||||

|

September 30,

|

(inception) to

|

|||||||||||

|

2013

|

2012

|

September 30, 2013

|

||||||||||

|

Cash Flows Used in Operating Activities:

|

||||||||||||

|

Net Loss

|

$ | (78,894 | ) | $ | (125,032 | ) | $ | (5,117,729 | ) | |||

|

Adjustments to reconcile net loss to net cash used in operations

|

- | |||||||||||

|

Expenses paid by shareholders

|

- | - | 39,000 | |||||||||

|

Stock Based Compensation

|

- | - | 1,566,348 | |||||||||

|

Impairment loss on goodwill

|

- | - | 1,285,710 | |||||||||

|

Impairment loss on Mining Lease

|

- | 29,000 | 29,000 | |||||||||

|

(Gain) Loss on derivative liability

|

5,054 | 20,323 | (23,348 | ) | ||||||||

|

Gain on sale of mining lease

|

(8,500 | ) | - | (8,500 | ) | |||||||

|

Amortization of debt discount and interest expense

|

29,320 | 21,530 | 244,136 | |||||||||

|

Depreciation

|

63 | - | 1,908 | |||||||||

|

Changes in operating assets and liabilities

|

||||||||||||

|

Prepaid Expenses

|

- | (5,487 | ) | - | ||||||||

|

Accounts Payable and accrued expenses

|

43,372 | 13,384 | 531,525 | |||||||||

|

Net Cash Used In Operating Activities

|

(9,585 | ) | (46,282 | ) | (1,451,950 | ) | ||||||

|

Net Cash Used In Investing Activities

|

||||||||||||

|

Acquisition of Equipment

|

- | (1,250 | ) | (2,907 | ) | |||||||

|

Proceeds from Business Acquisition

|

- | - | (200,343 | ) | ||||||||

|

Net Cash Used In Investing Activities

|

- | (1,250 | ) | (203,250 | ) | |||||||

|

Cash Flows From Financing Activities:

|

||||||||||||

|

Proceeds from convertible note payable

|

- | 47,500 | 167,500 | |||||||||

|

Proceeds from loans

|

9,500 | - | 9,500 | |||||||||

|

Proceeds from issuance of common stock

|

- | - | 1,506,450 | |||||||||

|

Net Cash Provided by Financing Activities

|

9,500 | 47,500 | 1,683,450 | |||||||||

|

Effect of Foreign Currency on Cash

|

20 | (22 | ) | (28,197 | ) | |||||||

|

Net Increase (Decrease) in Cash

|

(65 | ) | (54 | ) | 53 | |||||||

|

Cash at Beginning of Period

|

118 | 87 | - | |||||||||

|

Cash at End of Period

|

$ | 53 | $ | 33 | $ | 53 | ||||||

|

Supplemental disclosure of cash flow information:

|

||||||||||||

|

Expenses paid by shareholders

|

$ | - | $ | - | $ | 39,000 | ||||||

|

Shares issued for debt

|

$ | 33,800 | $ | - | $ | 237,394 | ||||||

|

Shares issued for Property Acquisition

|

$ | - | $ | 29,000 | $ | 29,000 | ||||||

|

Shares issued for accounts payable

|

$ | - | $ | - | $ | 79,500 | ||||||

|

Derivative liability extinguished due to debt conversions

|

$ | 50,344 | $ | 59,875 | $ | 143,713 | ||||||

|

The accompanying notes are an integral part of these condensed consolidated financial statements

|

||||||||||||

SOUTH AMERICAN GOLD CORP. AND SUBSIDIARIES

(Exploration Stage Company)

September 30, 2013

(Unaudited)

1. ORGANIZATION

The Company, South American Gold Corp., was incorporated under the laws of the State of Nevada on May 25, 2005 with the authorized capital stock of 75,000,000 shares at $0.001 par value. In January 2008, a majority of the shareholders agreed to an increase in the authorized capital stock to 450,000,000 shares at $0.001 par value.

The Company was organized for the purpose of acquiring and developing mineral properties. The Company has not established the existence of a commercially minable ore deposit and therefore is considered to be in the exploration stage.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The interim financial statements for the three months ended September 30, 2013 and 2012 are unaudited. These financial statements were prepared in accordance with requirements for unaudited interim periods, and consequently do not include all disclosures required to be in conformity with accounting principles generally accepted in the United States of America.

In the opinion of management, all adjustments (consisting solely of normal recurring adjustments) necessary to present fairly the financial position, results of operations, and cash flows for all periods presented have been made. The information for the consolidated balance sheet as of June 30, 2013 was derived from audited financial statements. The results of operations for the three months ended September 30, 2013 are not necessarily indicative of the results to be expected for the year ending June 30, 2014.

Principles of Consolidation

The accompanying consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles. All significant intercompany accounts and transactions have been eliminated upon consolidation.

Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents

For purposes of the cash flow statements, the Company considers all highly liquid investments with original maturities of three months or less at the time of purchase to be cash equivalents.

Revenue Recognition

The Company recognizes revenue based on FASB Account Standards Codification (“ASC”) 605 “Revenue Recognition”. In all cases, revenue is recognized only when the price is fixed or determinable, persuasive evidence of an arrangement exists, the service is performed and collectability of the resulting receivable is reasonably assured. Revenues from service contracts are recognized on a monthly, quarterly or semiannual basis as specified in the terms of a given contract. Revenues from additional services are recognized currently as the work is performed.

Basic and Diluted Net Income (Loss) Per Share

The Company computes net income (loss) per share in accordance with ASC 260 “Earnings per Share”. ASC 260 requires presentation of both basic and diluted earnings per share (“EPS”) on the face of the income statement. Basic EPS is computed by dividing net income (loss) available to common shareholders (numerator) by the weighted average number of shares outstanding (denominator) during the period. Diluted EPS gives effect to all dilutive potential common shares outstanding during the period using the treasury stock method and convertible preferred stock using the if-converted method. In computing diluted EPS, the average stock price for the period is used in determining the number of shares assumed to be purchased from the exercise of stock options or warrants. Diluted EPS excluded all dilutive potential shares if their effect is anti-dilutive. As of September 30, 2013 and 2012, there were 172,908,676 and 22,727,273 potential common shares outstanding, respectively. The stock options are anti-dilutive having an exercise price of $.59, and the convertible debt is at varying prices.

Property and Equipment

Property and equipment is stated at the historical cost. Maintenance and repairs of property and equipment are charged to operations as incurred. Depreciation is computed using the straight-line method over estimated useful lives of 3-5 years.

Evaluation of Long-Lived Assets

The Company reviews and evaluates long-lived assets for impairment when events or changes in circumstances indicate that the related carrying amounts may not be recoverable. The assets are subject to impairment consideration under ASC 360-10-35-17 if events or circumstances indicate that their carrying amounts might not be recoverable. When the Company determines that an impairment analysis should be done, the analysis will be performed using rules of ASC 930-360-35, Asset Impairment, and 360-10-15-3 through 15-5, Impairment or Disposal of Long-Lived Assets.

Foreign Currency Translation

The Company’s functional and reporting currency is the U.S. dollar. The consolidated financial statements of the Company are translated to U.S. dollars in accordance with ASC 830, “Foreign Currency Matters.” Monetary assets and liabilities denominated in foreign currencies are translated using the exchange rate prevailing at the balance sheet date. Gains and losses arising on translation or settlement of foreign currency denominated transactions or balances are included in the determination of income.

The Company has not, to the date of these financial statements, entered into derivative instruments to offset the impact of foreign currency fluctuations.

Income Taxes

The Company utilizes the liability method of accounting for income taxes. Under the liability method deferred tax

assets and liabilities are determined based on differences between financial reporting and the tax bases of the assets and liabilities and are measured using the enacted tax rates and laws that will be in effect, when the differences are expected to be reversed. An allowance against deferred tax assets is recorded, when it is more likely than not, that such tax benefits will not be realized.

Advertising and Market Development

The company expenses advertising and market development costs as incurred.

Goodwill

Goodwill consists of the excess of cost of acquired enterprises over the sum of the amounts assigned to identifiable assets acquired less liabilities assumed. Goodwill is reviewed for impairment annually at the beginning of the Company’s fourth fiscal quarter, or more frequently if there are indicators that the fair value of the related reporting unit is less than the carrying value of the Goodwill. We compare our fair value, which is determined utilizing both a market value method and discounted projected future cash flows, to our carrying value for the purpose of identifying impairment. Our annual impairment review requires extensive use of accounting judgment and financial estimates.

Mineral Property Acquisition and Exploration Costs

Mineral property acquisition costs are initially capitalized as tangible assets when purchased. At the end of each fiscal quarter end, the Company assesses the carrying costs for impairment. If proven and probable reserves are established for a property and it has been determined that a mineral property can be economically developed, costs will be amortized using the units-of-production method over the estimated life of the probable reserve. Mineral property exploration costs are expensed as incurred.

Estimated future removal and site restoration costs, when determinable are provided over the life of proven reserves on a units-of-production basis. Costs, which include production equipment removal and environmental remediation, are estimated each period by management based on current regulations, actual expenses incurred, and technology and industry standards. Any charge is included in exploration expense or the provision for depletion and depreciation during the period and the actual restoration expenditures are charged to the accumulated provision amounts as incurred. As of the date of these financial statements, the Company has not established any proven or probable reserves on its mineral properties and incurred only acquisition and exploration costs.

Although the Company has taken steps to verify title to mineral properties in which it has an interest, according to the usual industry standards for the stage of exploration of such properties, these procedures do not guarantee the Company’s title. Such properties may be subject to prior agreements or transfers and title may be affected by undetected defects.

Fair Value Measurements

Topic 820 in the Accounting Standards Codification (ASC 820) defines fair value, establishes a framework for measuring fair value in generally accepted accounting principles and expands disclosures about fair value measurements. ASC 820 applies whenever other standards require (or permit) assets or liabilities to be measured at fair value but does not expand the use of fair value in any new circumstances. In this standard, the FASB clarifies the principle that fair value should be based on the assumptions market participants would use when pricing the asset or liability. In support of this principle, ASC 820 establishes a fair value hierarchy that prioritizes the information used to develop those assumptions. The fair value hierarchy is as follows:

|

·

|

Level 1 inputs — Unadjusted quoted process in active markets for identical assets or liabilities that the entity has the ability to access at the measurement date.

|

|

·

|

Level 2 inputs — Inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These might include quoted prices for similar assets and liabilities in active markets, and inputs other than quoted prices that are observable for the asset or liability, such as interest rates and yield curves that are observable at commonly quoted intervals.

|

|

·

|

Level 3 inputs — Unobservable inputs for determining the fair values of assets or liabilities that reflect an entity’s own assumptions about the assumptions that market participants would use in pricing the assets or liabilities.

|

Investments

Investments on the balance sheet are classified as available-for-sale as they have readily determinable fair values and are not considered trading or held-to-maturity securities. Available-for-sale investments are reported at fair value with the unrealized holding gain or loss reported in other comprehensive income.

Environmental Requirements

At the report date environmental requirements related to the mineral claim acquired are unknown and therefore any estimate of any future cost cannot be made.

Stock-based compensation

The Company follows the provisions of ASC 718, whereby stock-based compensation cost is measured at the grant date, based on the calculated fair value of the award, and is recognized as an expense over the employees’ requisite services period (generally the vesting period of the equity grant).

Recent Accounting Pronouncements

The Company does not expect that the adoption of other recent accounting pronouncements will have a material impact on its financial statements.

3. MINERAL PROPERTIES

Kon Tum

In February 2008, the Company purchased the Kon Tum Gold Claim located in Vietnam for $5,000. The Company had not established the existence of a commercially minable ore deposit on the Kon Tum Gold Claim. The claim has no expiry date and only if the Company decides to abandon them will it no longer have an interest in the minerals thereon. The acquisition costs have been impaired and expensed because there has been no exploration activity nor have there been any reserves established and we cannot currently project any future cash flows or salvage value for the coming years and the acquisition costs might not be recoverable. The company has elected to not pursue further activities on these claims nor maintain ownership.

GB Project

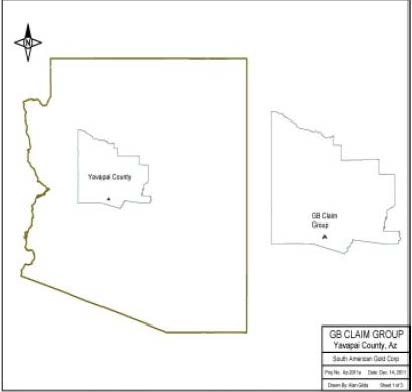

On December 14, 2011 the company signed an agreement to purchase one unpatented mining claim and lease nine unpatented mining claims in Yavapai County, Arizona covering approximately two hundred acres. The purchased unpatented claims were for $1,000 and the vendor retained a two percent net smelter return from any future production. The leased claims are for a period of fifteen (15) years; any production subject to a two percent net smelter return to the vendor, and annual lease payments of $750.The company subsequently acquired an additional two unpatented mining claims as part of the GB project by location.

Lucky Boy Silver Project

In December 2011 the company staked five unpatented mining claims in Hawthorne, Nevada covering approximately one hundred acres. The company abandoned this property in the three month period ending September 30,2013.

Baltimore Silver Mine Project

On August 6, 2012, the Company signed an agreement to lease, with an option to purchase, the Baltimore Mine located in Western Montana. The lease payment will be $10,000 per year, plus $500 per quarter; or, $2,000 per year in restricted stock at SAGD’s option, provided such restricted stock has a market bid price in excess of $20,000 for the twenty days prior to payment. Payment will be on July 31 of each year beginning July 31, 2013. SAGD may terminate the lease with ninety days’ notice; however, such determination has no bearing on cash payments or issuance of stock to Western prior to the termination of the lease option. The term of the lease is ten years and may be extended for an additional 15 years with a payment of one hundred thousand dollars ($100,000) at any time.

SAGD will have an option to purchase the property free and clear of any lien or encumbrance, for the term of this agreement, in the amount of five hundred thousand dollars ($500,000), at which time the lease would terminate and no royalty would be due afterwards from the property.

Should SAGD cause to be issued a property report meeting the industry guidelines indicating probable or proven reserves in excess of two million ounces of silver on the property, Western shall receive an additional thirty thousand dollars in cash or restricted shares value determined as (3) above, within thirty days of publication of such report.

The acquisition price of this option was 10,000,000 shares of SAGD restricted stock, based on the contractually stated value of $29,000, using the closing market price of the Company’s common stock on August 17, 2012, plus an additional $25,000 payable in the form of cash or restricted common stock, at SAGD’s option, valued at the ten day average bid price for the company’s common stock. This additional $25,000 is payable during the period January 1, 2013 to July 1, 2013. As of September 30, 2012, the Company identified there were indicators of impairment. As such, it conducted a cash flow assessment on this mining lease, and based on that assessment, the Company recorded an impairment loss of $29,000 in its statement of operations.

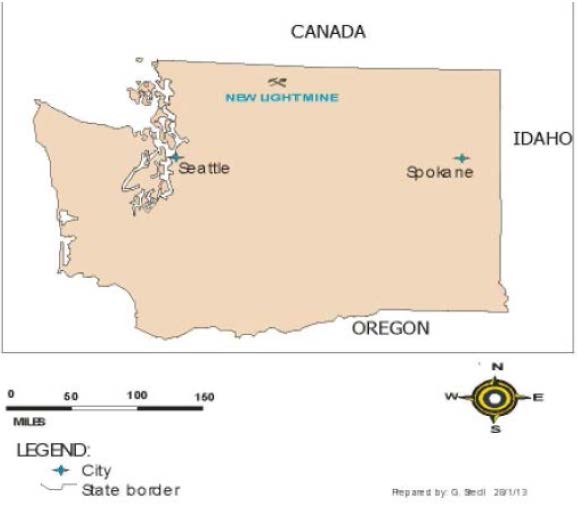

New Light Mine Project

On January 16, 2013 the Company signed a mining lease agreement for two unpatented mining claims in Whatcom County, Washington. The lease is for fifteen years and is subject to a net smelter return of two percent and annual advance royalty payments of $500 in the first year and $750 thereafter. The advance royalty payment of $500 was paid in May 2013.

In addition, the Company is to perform a minimum of $500 in assessment work for the benefit of the property for the assessment year ended September 1, 2013 (which has been done), and a cumulative minimum of $500 for every assessment year thereafter in which the Company continues this lease beyond July 1 of the assessment year.

4. INVESTMENTS

On September 19, 2013 the Company assigned the New Light Mine Project lease to Kalahari Greentech, Inc. (“Kalahari”) in exchange for $1,000 in cash (not received as of the date of these financial statements) and 5,000,000 shares of restricted common stock of Kalahari. Additionally, on October 14, 2013, the Company signed a Letter of Intent with Kalahari to acquire a 40% interest in the lease by spending or incurring $200,000 in exploration expenditures, including associated overhead, within 24 months of the signing of a definitive agreement.

The shares of Kalahari were valued using the closing price of its common stock on September 19, 2013 ($0.0015). As the Company had a zero cost basis in the lease, a gain of $8,500 was recorded in the statement of operations. Also, as these shares are considered available-for-sale securities, the Company remeasured these shares at September 30, 2013, and recorded an unrealized gain of $3,000 in other comprehensive income.

5. CONVERTIBLE NOTE PAYABLE AND DERIVATIVE LIABILITY

Convertible Note Payable

Convertible Note #3

On December 18, 2012, the Company entered into a securities purchase agreement and convertible note agreement, for $32,500 in cash. The note has a maturity date of September 20, 2013, and carries an interest rate of 8%, per annum. Principal and interest is due on September 20, 2013, and any amount of principal or interest not paid by this date, will accrue interest at 22% per annum. This note, plus accrued interest, is convertible 180 days from the date of the Note, at a variable conversion price of 45% of the lowest three trading prices for the common stock of the Company during the thirty trading day period ending on the latest complete trading day prior to the conversion date.

Pursuant to the conversion option, in the month of July 2013, the third party converted $32,500 of related debt ( plus $1,300 of accrued interest) to 67,938,632 shares of common stock, fully extinguishing this note

Convertible Note #4

On March 28, 2013, the Company entered into a securities purchase agreement and convertible note agreement, for $32,500 in cash. The note has a maturity date of January 2, 2014, and carries an interest rate of 8%, per annum. Principal and interest is due on January 2, 2014, and any amount of principal or interest not paid by this date, will accrue interest at 22% per annum. This note, plus accrued interest, is convertible 180 days from the date of the Note, at a variable conversion price of 45% of the lowest three trading prices for the common stock of the Company during the thirty trading day period ending on the latest complete trading day prior to the conversion date. Accrued interest on this note, as of September 30, 2013, was $1,324.

Convertible Note #5

On April 30, 2013, the Company entered into a securities purchase agreement and convertible note agreement, for $27,500 in cash. The note has a maturity date of February 3, 2014, and carries an interest rate of 8%, per annum. Principal and interest is due on January 30, 2014, and any amount of principal or interest not paid by this date, will accrue interest at 22% per annum. This note, plus accrued interest, is convertible 180 days from the date of the Note, at a variable conversion price of 45% of the lowest three trading prices for the common stock of the Company during the thirty trading day period ending on the latest complete trading day prior to the conversion date. Accrued interest on this note, as of September 30, 2013, was $923.

Derivative Liabilities

Convertible Note #3

The Company has determined that the conversion feature in this note is not indexed to the Company’s stock, and is considered to be a derivative that requires bifurcation. The Company calculated the fair value of this conversion feature using the Black-Scholes model and the following assumptions: Risk-free interest rates ranging from 0.02% to 0.16%; Dividend rate of 0%; and, historical volatility rates ranging from 145.97% to 346.31%. Based on this calculation, the Company recorded a derivative liability of $52,817 and interest expense of $20,317. This derivative is remeasured at each reporting period, with the change in fair value being recorded to the statement of operations. The calculated fair values of the derivative liability at December 31, 2012, March 31, 2013, and June 30, 2013 were $52,817, $47,848, and $44,109, respectively, and $0 at July 18, 2013, when the final note balance was converted to equity. From its initial valuation on December 18, 2012 to July 18, 2013, the Company has recorded a net gain on derivative liability of $2,472, in the statement of operations.

Based on the above calculations, the Company also recorded a discount on debt of $32,500. This discount has been fully amortized due to the note being converted to equity. Total amortization expense for the three months ended September 30, 2013 was $9,573, which includes discount amortization of $8,545 related to the conversion of $32,500 to equity.

Convertible Note #4

The Company has determined that the conversion feature in this note is not indexed to the Company’s stock, and is considered to be a derivative that requires bifurcation. The Company calculated the fair value of this conversion feature using the Black-Scholes model and the following assumptions: Risk-free interest rates ranging from 0.02% to 0.13%; Dividend rate of 0%; and, historical volatility rates ranging from 134.59% to 260.56%. Based on this calculation, the Company recorded a derivative liability of $57,988 and interest expense of $25,488. This derivative is remeasured at each reporting period, with the change in fair value being recorded to the statement of operations. The calculated fair value of the derivative liability at March 31, 2013 and June 30, 2013 was $57,474 and $52,932 respectively, and $52,200 at September 30, 2013. From its initial valuation on March 28, 2013 to September 30, 2013, the Company has recorded a related net gain on derivative liability of $5,788 in the statement of operations.

Based on the above calculations, the Company also recorded a discount on debt of $32,500. This discount will be amortized to interest expense over the 9 month term of the convertible note. Total amortization for the three months ended September 30, 2013 was $10,911.Total amortization expense for the three month period ended September 30, 2013 was $10,679.

Convertible Note #5

The Company has determined that the conversion feature in this note is not indexed to the Company’s stock, and is considered to be a derivative that requires bifurcation. The Company calculated the fair value of this conversion feature using the Black-Scholes model and the following assumptions: Risk-free interest rates ranging from 0.03% to 0.13%; Dividend rate of 0%; and, historical volatility rates ranging from 251.38% to 285.31%. Based on this calculation, the Company recorded a derivative liability of $55,053 and interest expense of $27,553. This derivative is remeasured at each reporting period, with the change in fair value being recorded to the statement of operations. The calculated fair value of the derivative liability at June 30, 2013 and September 30, 2013 was $45,568 and $45,060, respectively. From its initial valuation on April 30, 2013 to September 30, 2013, the Company has recorded a related net gain on derivative liability of $9,993 in the statement of operations.

Based on the above calculations, the Company also recorded a discount on debt of $27,500. This discount will be amortized to interest expense over the 9 month term of the convertible note. Total amortization expense for the three months ended September 30, 2013 was $9,068.

6. Notes Payable

The Company has issued long term notes payable in settlement of account payable. Each note has a duration of twenty four months and bears simple interest of five per cent per annum, payable quarterly beginning June 30, 2013

The Company has issued a short term note for funds borrowed with a duration of ninety days that carries a simple interest of five per cent per annum, payable upon maturity.

|

Issue Date

|

Maturity

|

|

||||

|

September 30,2013

|

12/29/2103

|

$

|

9,500 | |||

|

March 28, 2013

|

3/28/15

|

11,500

|

||||

|

March 31, 2013

|

3/31/15

|

7,000

|

||||

|

Sub Total

|

28,000

|

|||||

|

Less : Short term notes payable

|

( 9,500

|

)

|

||||

|

Long term notes payable

|

|

18,500

|

7. RELATED PARTY TRANSACTIONS

As of September 30, 2013 and 2012, the current officers were owed $87,862 and $72,827 for management fees and expenses, which are recorded in accounts payable on the balance sheet. Officers-directors also have made contributions to capital of $39,000, since inception, in the form of expenses paid for the Company.

8. STOCKHOLDERS’ DEFICIT

Issuance of Stock

On August 17, 2012, the Company issued 10,000,000 shares of SAGD restricted common stock, valued at $29,000, based on the market value of the stock on the date of issuance, for the acquisition of a lease option on mineral properties.

In January 2013, the Company issued 26,500,000 shares of common stock in settlement of $79,500 in accounts payable, based on the market value at the date of issuance.

During March 2013, the Company issued 17,527,337 shares of common stock upon conversion of $15,100 in notes payable.

During the period April 1, 2013 through June 30, 2013, the Company issued 87,884,190 shares of common stock upon conversion of $62,900 in notes payable (including $3,000 in accrued interest).

During the three month period ended September 30, 2013, the Company issued 67,938,632 shares of common stock upon conversion of $33,800 in notes payable (including $1,300 in accrued interest).

Stock Options

During the year ended 30 June 2011, the Company granted 2,900,000 stock options to employees and directors of the Company, entitling the holders to purchase common shares of the Company for proceeds of $0.59 per common share expiring March 21, 2021, of which 1,200,000 were granted to employees and 1,700,000 were granted to non-employees of the Company. The fair value of the portion of the options which vested in the period, estimated using Black-Scholes model, was $1,566,378. This amount has been expensed as stock-based compensation.

The following incentive stock options were outstanding at September 30, 2013:

|

Exercise

Price

|

Number of

options

|

Remaining

contractual

life (years)

|

||||||||||

|

Options

|

$

|

0.59

|

2,900,000

|

7.3

|

||||||||

|

2,900,000

|

||||||||||||

The following is a summary of stock option activities during the three months ended September 30, 2013:

|

Number of

options

|

Weighted

average

exercise

price

|

|||||||

|

Outstanding and exercisable at June 30, 2013

|

2,900,000

|

0.59

|

||||||

|

Granted

|

-

|

-

|

||||||

|

Exercised

|

-

|

-

|

||||||

|

Cancelled

|

-

|

-

|

||||||

|

Outstanding and exercisable at September 30, 2013

|

2,900,000

|

0.59

|

||||||

The aggregate intrinsic value of all warrants and stock options outstanding and exercisable at September 30, 2013 was $0.

9. FAIR VALUE MEASUREMENTS

Our financial assets and (liabilities) carried at fair value measured on a recurring basis as of September 30, 2013 consisted of the following:

|

Fair Value Measurements Using

|

||||||||||||||

|

Total Fair

|

Quoted prices in

|

Significant other

|

Significant

|

|||||||||||

|

Value at

|

active markets

|

observable inputs

|

Unobservable inputs

|

|||||||||||

|

Description

|

September 30, 2013

|

(Level 1)

|

(Level 2)

|

(Level 3)

|

||||||||||

|

Derivative liability

|

$

|

(97,261

|

)

|

$

|

—

|

$

|

(97,261

|

)

|

$

|

—

|

||||

10. GOING CONCERN

Our financial statements have been prepared on the basis of accounting principles applicable to a going concern. As a result, they do not include adjustments that would be necessary if we were unable to continue as a going concern and would therefore be obligated to realize assets and discharge our liabilities other than in the normal course of operations. The Company does not have sufficient working capital to service its debt or for its planned activity, which raises substantial doubt about its ability to continue as a going concern. The Company’s plans are to seek additional debt and equity investment to sustain operations.

11. SUBSEQUENT EVENTS

On October 9, 2013, the Company entered into a securities purchase agreement and convertible note agreement for $7,500 in cash. The note has a maturity date of July 18 2014, and carries an interest rate of 8%, per annum. Principal and interest is due on July 18,2014 and any amount of principal or interest not paid by this date, will accrue interest at 22% per annum. This note, plus accrued interest, is convertible 180 days from the date of the Note, at a variable conversion price of 45% of the lowest three trading prices for the common stock of the Company during the thirty trading day period ending on the latest complete trading day prior to the conversion date.

For the period October 1 through November 14, 2013 common shares of 142,466,666 were issued upon conversion of $31,100 in convertible debt.

This Quarterly Report on Form 10-Q contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The words “believe,” “expect,” “anticipate,” “intend,” “estimate,” “may,” “should,” “could,” “will,” “plan,” “future,” “continue,” and other expressions that are predictions of or indicate future events and trends and that do not relate to historical matters identify forward-looking statements. These forward-looking statements are based largely on our expectations or forecasts of future events, can be affected by inaccurate assumptions, and are subject to various business risks and known and unknown uncertainties, a number of which are beyond our control. Therefore, actual results could differ materially from the forward-looking statements contained in this document, and readers are cautioned not to place undue reliance on such forward-looking statements. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. A wide variety of factors could cause or contribute to such differences and could adversely impact revenues, profitability, cash flows and capital needs. There can be no assurance that the forward-looking statements contained in this document will, in fact, transpire or prove to be accurate.

Important factors that may cause the actual results to differ from the forward-looking statements, projections or other expectations include, but are not limited to, the following:

|

●

|

risks related to failure to obtain adequate financing on a timely basis and on acceptable terms for our contemplated acquisition and exploration and development projects;

|

|

●

|

risk that Federal and State permissions required for exploration on our properties are not available, or conflicting property interests preclude exploration and production on unpatented mining claims:

|

|

●

|

risk that we cannot attract, retain and motivate qualified personnel, particularly employees, consultants and contractors for our operations;

|

|

●

|

Risks and uncertainties relating to the interpretation of drill results, the geology, grade and continuity of mineral deposits;

|

|

●

|

results f initial feasibility, pre-feasibility and feasibility studies, and the possibility that future exploration, development or mining results will not be consistent with our expectations;

|

|

●

|

mining and development risks, including risks related to accidents, equipment breakdowns, labor disputes or other unanticipated difficulties with or interruptions in production;

|

|

●

|

the potential for delays in exploration or development activities or the completion of feasibility studies;

|

|

●

|

risks related to the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses;

|

|

●

|

risks related to commodity price fluctuations;

|

|

●

|

the uncertainty of profitability based upon our history of losses;

|

|

●

|

risks related to environmental regulation and liability;

|

|

●

|

risks that the amounts reserved or allocated for environmental compliance, reclamation, post-closure control measures, monitoring and on-going maintenance may not be sufficient to cover such costs;

|

|

●

|

risks related to tax assessments;

|

|

●

|

political and regulatory risks associated with mining development and exploration; and other risks and uncertainties related to our prospects, properties and business strategy;

|

|

●

|

risks related to failure to obtain adequate financing on a timely basis and on acceptable terms for our contemplated acquisition and exploration and development projects;

|

|

●

|

risk that Federal and State permissions required for exploration on our properties are not available, or conflicting property interests preclude exploration and production on unpatented mining claims;

|

|

●

|

risk that we cannot attract, retain and motivate qualified personnel, particularly employees, consultants and contractors for our operations ;

|

|

●

|

risks and uncertainties relating to the interpretation of drill results, the geology, grade and continuity of mineral deposits;

|

|

●

|

results of initial feasibility, pre-feasibility and feasibility studies, and the possibility that future exploration, development or mining results will not be consistent with our expectations;

|

|

●

|

mining and development risks, including risks related to accidents, equipment breakdowns, labor disputes or other unanticipated difficulties with or interruptions in production;

|

|

●

|

the potential for delays in exploration or development activities or the completion of feasibility studies;

|

|

●

|

risks related to the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses;

|

|

●

|

risks related to commodity price fluctuations;

|

|

●

|

the uncertainty of profitability based upon our history of losses;

|

|

●

|

risks related to environmental regulation and liability;

|

|

●

|

risks that the amounts reserved or allocated for environmental compliance, reclamation, post-closure control measures, monitoring and on-going maintenance may not be sufficient to cover such costs;

|

|

●

|

risks related to tax assessments; and

|

|

●

|

political and regulatory risks associated with mining development and exploration; and other risks and uncertainties related to our prospects, properties and business strategy.

|

The forgoing list is not an exhaustive list of the factors that may affect any of our forward-looking statements. These and other factors should be considered carefully and readers should not place undue reliance on our forward-looking statements.

As used in this Quarterly Report, the terms “we,” “us,” “our,” and “Company” mean South American Gold Corp., unless otherwise indicated.

Overview

The Company’s current focus is on the acquisition, exploration, and potential development of mining properties in in the United States, though we are also seeking mineral property interests in Colombia, Mexico, and southeastern Europe. Though no such interests for acquisition have been identified at this time. Our common stock is currently quoted over-the-counter (the “OTC QB”) under the trading symbol “SAGD”.

As a part of our business plan, we intend to seek out and acquire interests in other mineral exploration properties which, in the opinion of our management, offer attractive mineral exploration opportunities. During the fiscal years ending June 30, 2013 and a 2102 acquired mineral property interests in Arizona, Nevada and Montana; we have also begun due diligence activities with the objective of additional properties in the United States and Southeastern Europe. In the fiscal year ending June 30, 2013, we continued exploration of properties including sampling, geologic mapping and beginning to review bonding requirements for forecast exploration activities. We actively reviewed several projects presented to us. We also signed a Memorandum of Understanding in regards to a Montana property interest which as of the end of the quarter ended September 30, 2013 had not been finalized.

We are an exploration stage mining company and while our objective is to develop profitable mining operations, currently we produce no cash flow from operations. Junior exploration stage mining companies generally seek to acquire mineral properties and mineral property interests, to explore, develop or joint-venture. Value is added through exploration and discovery of the potential for commercial mineralization on properties, and by joint venturing, selling or leasing properties. Companies at our stage generally use equity or equity-type financing, with pure debt financing generally only available from producing operations or upon completion of a bankable feasibility study. We have relied in the last year on convertible debt financing, which can be highly dilutive to shareholders, in absence of other funding availability.

Our business plan is highly contingent on our ability to secure financing under acceptable terms which is not assured.

Substantially, all of our assets will be put into commercializing mining rights and mineral claims located within a limited geographical area. Accordingly, any adverse circumstances that affect these areas would affect us financially. If any adverse circumstances were to arise, we would need to consider alternatives, both in terms of our prospective operations and for the financing of our activities. Management cannot provide assurance that we will ultimately achieve profitable operations or become cash-flow positive, or raise additional debt and/or equity capital. If we are unable to raise additional capital, we will continue to experience liquidity problems and management expects that we will need to curtail operations, liquidate assets, seek additional capital on less favorable terms and/or pursue other remedial measures including ceasing operations. We may also consider entering into a joint venture arrangement to provide the required funding to acquire and explore any mineral property interests. We have not undertaken any efforts to locate a joint venture participant. Even if we determine to pursue a joint venture participant, there is no assurance that any third party would enter into a joint venture agreement with us in order to fund the acquisition and exploration of mineral property interests. If we enter into a joint venture arrangement, we would likely have to assign a percentage of any mineral property interest we may hold to the joint venture participant.

North American Exploration and Acquisition Activities

We have commenced regular activities to locate and evaluate potential projects in North America. Initial projects under review have been in Mexico (Zactaecas region) and the United States (principally projects in Nevada, Arizona and Montana). These activities included site visits to the lease mining claims in Arizona and the Lucky Boy Silver project in Nevada, and the Baltimore Silver Mine project in Montana, which are discussed below. These efforts include reviewing historical literature, contacting property owners, compiling and reviewing information on properties, and where merited site visits and negotiations with property owners, and in addition exploration preparation for our GB Claims in Arizona. The lucky boy Silver project the company has elected tonot pursue, and the relevant mining claims were dropped.

GB Claims – Arizona

GB 2 Gold

Leased Claims

The nine unpatented mining claims underlying the GB2 Lease cover approximately 180 acres and are located in the Black Rock Mining District of Yavapai County, Arizona. Set forth below are the claim reference numbers.

Claim Reference Numbers

|

BLM Recording Number

|

County Recording Number

|

|||||

|

GB 1

|

AMC

|

393641

|

8 4608

|

P 313

|

||

|

GB 3

|

393643

|

8 4608

|

P 315

|

|||

|

GB 4

|

393644

|

8 4608

|

P 316

|

|||

|

GB 5

|

393645

|

8 4608

|

P 317

|

|||

|

GB 6

|

393646

|

8 4608

|

P 318

|

|||

|

GB 7

|

393647

|

8 4608

|

P 319

|

|||

|

GB 8

|

393648

|

8 4608

|

P 320

|

|||

|

GB 23

|

393931

|

8 4608

|

P 983

|

|||

|

GB 25

|

393930

|

8 4608

|

P 984

|

|||

Owned Claims

The single Claim acquired by the Company has a BLM recording number of AMC 3993932 and county recording number of 84608P-982.

Location

The Black Rock Mining District is located in the southeast part of Yavapai County between the east foothills of the Bradshaw Mountains and the Agua Fria River. The following map shows the general location of the leased and owned unpatented mining claims we acquired in Yavapai County, Arizona:

Access

The Property is readily accessed from Wickenberg, Arizona (approximately sixty five miles northwest of Phoenix, Arizona), which lies on Federal Highway 93. Wickenberg is the nearest large town that has services necessary for mineral exploration and mining. From Wickenberg, paved Constellation Highway is followed about two miles, thence sixteen miles of dirt road lead to the Property. Unimproved tracks provide access to the claim group. Road access to the east side of the Property is limited.

History

The Yavapai County area of Arizona is an area of historic gold prospecting and production activities. However, the Company is not aware of any recorded history of production from the Property underlying the Lease or the Claim.

Climate, Local resources, Infrastructure, Physiography

Climate

The climate is semi-arid with roughly 12.2 inches/year precipitation, mostly in late winter. The Property can be accessed year-round because of the mild climate, good road access, and low elevation of about 1200 meters above mean sea level.

Water Rights, Power, and Mining Personnel

The status of water rights at the Property is uncertain. The amount of water in the vicinity of the Property is adequate for exploratory drilling in the winter, but may not be adequate for mineral processing. The nearest power lines are about 16 miles distant. Mining personnel are not available locally.

The most important natural feature on the Property is tertiary sandstones on the north end of the property.

Tailings Storage Areas, Waste Disposal Areas, and Plant Sites

The Company has not identified private land adjacent to the Property or within close proximity that could be used for potential storage areas, waste disposal or processing sites. There is public land in the vicinity, but it is unknown whether permits would be granted for such uses. There is evidence of old tailings on the project which have not been sampled.

Permitting

Preliminary geological mapping, sampling, and geophysical surveys can be conducted without any permits. A Plan of Operations (“POO”) will have to be filed and approved by the Bureau of Land Management before mechanized work such as access work or drilling can be undertaken on the Property. There is no cost to file a POO with the Bureau of Land Management. Water for drilling would need to be hauled into the property according to initial site visits. Permits are often granted in a short period of time as long as they do not significantly impact existing water rights or unduly degrade riparian areas.

Further mining exploration and exploitation activities are subject to federal, state and local laws, regulations and policies, including laws regulating surface disturbance, water discharge, and the removal of natural resources from the ground and the discharge of materials into the environment. These regulations mandate, among other things, the maintenance of air and water quality standards and land reclamation. They also set forth limitations on the generation, transportation, storage and disposal of solid and hazardous waste. Exploration and exploitation activities are also subject to federal, state and local laws and regulations which seek to maintain health and safety standards by regulating the design and use of exploration methods and equipment. The Company is unable to quantify at this time the potential cost of such regulations and permitting. (see also “Risk Factors).

Infrastructure

There is no ascertainable infrastructure on the Property at present.

No adits or trenches have been identified on the property.

Regional Geology

The Property lies on the southern margin of Arizona’s Transition Zone physiographic province. The majority of the area is underlain by Precambrian gneiss, and at the north end of district Tertiary sandstone predominate. Historical information refers to complex igneous and metamorphic host rocks in the general area.

Geology and Mineralization

The Property is characterized by the Precambrian gneiss, with the westerly part exposed hornblende diorite porphyry-type mineralization identified form initial examination of the breccias pipes #4, #5 and #6. The host rock is mostly composed of Proterozoic formations intruded by younger igneous rocks.

Metallurgical

No metallurgical testing has been conducted.

Reserves

There are no established probable or proven reserves on the Property. Our due diligence activities have been limited, and to a great extent, have relied upon information provided to us by third parties. We have not established and cannot provide any assurance that any of the properties underlying the Lease or the Claim contain adequate, if any, amounts of gold or other mineral reserves to make mining economically feasible to recover that gold or other mineral reserves, or to make a profit in doing so.

Project Exploration Plan

The project area is an early stage prospect with potential identified to date from reconnaissance exploration. The initial objective is to identify the presence of and extent of breccia pipes on the Property. This will require an initial work plan of geologic mapping, surface sampling and soil analysis, after which a more comprehensive plan would be developed with an objective of identifying drill targets and developing a Plan of Operation to be filed with the BLM for permission to conduct such an exploration program.

During 2013, exploration efforts have focused on the area adjacent to the identified breccias pipes, evaluating nearby properties for acquisition or lease, and considering potential bonding requirements for a drilling plan. Initial summary maps were prepared, and some surface sampling was conducted on a limited basis. Surface sampling was conducted and results considered positive to merit further exploration. However bonding requirements may preclude the Company drilling until additional financing is put in place.

We estimate the initial work plan described above to require an estimated five thousand dollars ($5,000) for geological consulting, travel expenses, and sampling analysis costs. The Company is reviewing the cost of providing necessary bonding for the project, and due to limited finances will consider in the upcoming fiscal year seeking a joint venture partner or selling the project while retaining a net smelter return. The Company is actively considering joint-ventures or a sale of the project while retaining a Net Smelter Return and looking upon effecting such a transaction while looking for additional land position in the area.

Lucky Boy Silver Project - Nevada

In December 2011, we staked five unpatented mining claims in the Walker Lane Mineral Belt in western Nevada which we are referring to as the “Lucky Boy Silver Project”.

In connection with our consideration of whether to stake these unpatented mining claims, we conducted a diligence review of the Lucky Boy Silver Project. The description of the Lucky Boy Silver Project contained herein is the product of our due diligence from an initial site visits conducted in December 2011 and certain historical information publicly available which we have not been able to independently verify. Further description of the project may be found in our Annual Report on Form 10-K for the year ended June 30, 2013.

Land Status

We staked the following five unpatented mining claims in December 2011 covering approximately 100 acres of the Lucky Boy Silver Project:

|

Claim

|

BLM Recording No.

|

|

LB#1

|

NMC 1062491

|

|

LB#2

|

NMC 1062492

|

|

LB#3

|

NMC 1062493

|

|

LB#4

|

NMC1062494

|

|

LB#5

|

NMC 1062495

|

The Company was unsuccessful at acquiring mineral property rights to adjacent patented land in the fiscal year ending June 30, 2013. The Company forfeited these claims in the quarter ended September 30, 2013.

Baltimore Silver Mine

On August 6, 2012, the Company entered into a binding Memorandum of Understanding (the “Agreement”) with Western Continental, Inc. (“Western”) to lease with option to purchase three patented mining claims ( the “Baltimore Silver Mine”) subject to a definitive agreement to be signed within ninety days, with an effective lease date of August 3, 2012. Our Current Report on Form 8-K filed August 9, 2012 provided property information and is incorporated herein by reference, as is our recently filed 10k report for the period ending June 30, 2013.

Western and the Company agreed to a Definitive Agreement (“the Agreement”) to Lease with Option to Purchase the Baltimore Silver Mine. The Company effected the Agreement September 5, 2012. The lease will be for a term of ten years beginning August 2, 2012, and may be extended for an additional 15 years with a payment of $100,000 at any time. During the term of this lease, the Company will be responsible for the payment of any property taxes, indemnify Western for any and all activities the Company conducts on the property, and secure all required permits and operating licenses for the Company activities on the property. The lease payment will be $10,000 per year in cash payments, which may be paid in restricted stock as the Company’s option provided such restricted stock has a market bid price in excess of $20,000 for the 20 days average bid price for the stock prior to payment, and a quarterly cash payment of $500 per quarter. Payment will be on July 31st of each year beginning in 2013.

The Company will pay a production royalty of all minerals mined from the property in the form of a Net Smelter Return to Western of 3%. The Company will have for the term of this agreement an option to purchase the property free and clear of any lien or encumbrance in the amount of $500,000 at which time the lease would terminate and no royalty would be due afterwards from the property. Should the Company cause to be issued a property report meeting standard industry guidelines indicating probable or proven reserves in excess of two million ounces of silver on the property, Western shall receive an additional $30,000 in cash or restricted shares valued as described above, within 30 days of publication of such report. The Company has issued 10,000,000 shares of its restricted common stock to Western. The Company will also pay $25,000 in cash or restricted stock, valued at the ten day average bid price for the stock, between January 1, 2013 and July 1, 2013. The Company is currently negotiating and amendment and has not received notification of default as a result of these discussions.

Description of Property

Land Status

The property consists of three patented mining claims covering approximately 60 acres.

|

Name of Claim

|

Mineral Survey #

|

|

Last Hope

|

9689

|

|

Baltimore

|

1540

|

|

Mona

|

9689

|

The Company has also staked two unpatented claims as part of the project, thus the project as a whole contains approximately 100 acres.

Location

The Baltimore Mine property is located in Jefferson County Montana, approximately twenty two miles northeast of Butte, MT and four miles northwest of Boulder, MT. Coordinates are Section 7, Township 6 N, Range 4W, Jefferson County, Montana. The Company is collating information and preparing general maps on the project.

Access

Access is generally from Boulder by four miles of unimproved county road thence along the Boomerang Creek Road.

Climate and Physiography

The climate is relatively temperate allowing work generally all year around. The mine is on the eastern slope area of Sugarloaf Mountain, with ridges one thousand foot above the main valley. Elevations on the property range from 6,250 feet on ridge top to 5,800 feet above sea level near the Baltimore Mine. Vegetation consists of mostly sage but stands of conifers are common on the north slopes.

Local Resources

There are sufficient local resources for general material and supplies, and general labor. Electric power lines are within a mile of the property and water supply appears adequate for the property, though an assessment will be required for water supply for expanded drilling programs and future potential milling requirements.

Geology

The geology of the area is dominated by the monzonites of the Butte Batholith intruding into the older Elkhorn volcanics, consisting of green-gray welded tuffs and sites. East-westerly striking pyrite-galena bearing quartz veins have been deposited along or near to fault or shear zones with some Scricitic alteration. The Baltimore shear or alteration zone can be traced can be traced over five thousand feet on the surface.

Metallurgy

The Company has no metallurgical tests relating to the property, or historical information as to recoveries of metal from ore formerly produced.

Reserves and Mineralized Material

There are no established reserves or mineralized material on the property according to available information on the project.

History and Historical Information on the Property

The following information has been provided by independent sources not been independently verified by the Company but provided for general informational purposes, and it should not be assumed that prior production results are an indication of potential future results.

The mine apparently was discovered in the nineteenth century with regular shipments ore reported in 1903 by lessees, and two thousand feet of workings. In 1907, it was reported the mine had six adits and a 140 foot shaft. In 1912, 60 men were employed at the mine, and it was extended an additional six hundred feet. By 1935 the underground workings were estimated at three thousand feet of crosscuts and drifts, and with tunnels. In 1960 it was reported that the mine had produced 18,148 tons of ore which yielded 1,734 ounces of gold, 275,489 ounces of silver, and 271,266 pounds of copper, 1,273,965 pounds of lead and 280,750 pounds of zinc. Past production is no indicator of future production potential which can only be determined through additional information on the property.

Limited sampling was conducted on the property in 1966, 1979, and in 1989, a 4,985 foot drilling program was conducted on the property. The Company is reviewing assays from these programs and working to correlate to available assay maps and considers that data contained as encouraging further exploration.

Development Work on the Property

The underground workings of the property include six tunnels reported by 1960 and a shaft at a vertical interval of four hundred feet, and three thousand feet of underground workings. Prior operator reports indicates that four of these tunnels the Hope Tunnel, Tunnel No. 4, 5, and 6,were evidently designed to explore the northeastern vein structure of the property.

The Company is considering a budget for rehabilitation of the Portals to gain further underground access.

Exploration Plan

The Company’s initial plans include compiling and reviewing all historical information on the property, and conducting initial site visits to determine costs and schedules for geological mapping, and status of the underground workings, and determining the optimum exploration plan based on this initial work. Our exploration plan will focus on confirming historic grades, and targeting areas that may yield commercial grades and sufficient tonnages to justify rehabilitation of underground workings and drilling to delineate potential ore reserves. This preliminary assessment will consider initial approximate cost estimates including the availability of any regional milling facilities. The Company estimates a budget of $5,000 to $50,000 may be required in initial stages of exploration.

We have begun our Phase I exploration which has included a thorough review of the current status of access to the tunnels ad underground workings, having a professional geologist and a mining engineer work on the property. We have completed an initial survey of the dump material, and review of the historical literature. Exploration objectives include (a) further determination of the economics of processing the dump material (b) rehabilitation work to gain access further underground to conduct channel sampling and determining drill targets (c) detailed geologic mapping. We believe that while some potential is in identifying mineralized areas former mining with limited technology may have missed that there may be much deeper exploration targets to be tested form underground or surface drilling. We also intent to prepare the necessary plan of operations for the unpatented portion of the project, and consider applications for any state mining permits.

Summary Exploration Plans

Exploration work continues to advance knowledge of the areas, conduct surveying and geologic mapping activities, determine prime areas for soil sediment sampling and re-sampling prospects pits we believe present. Our primary objective during Phase I exploration is identifying drill targets, preparing logistical arrangements for a drilling plan, begin assembling data necessary for a Plan of Operations to be submitted to the BLM, which has been submitted and preparation for data to support our subsequent applications for regulatory approval of exploration activities, and review data of prior exploration in the area along with field work to verify historical data. We plan in the second quarter to expand these activities. Our Phase II exploration phase, subject to results and timing of the completion Phase I exploration and regulatory approvals. We are forecasting subject to capital availability and timing of regulatory approvals required to explore in the area, a company budget of approximately $240,000 for our projects over the next 18 months. We also are actively considering projects for acquisition in Mexico in addition to the United States and Colombia, and expect general due diligence, exploration and initial acquisition expenses over the next 18 months at $120,000, for a total operating budget of $360,000 over 18 months, subject to availability of capital, permits and recommendations of our technical staff and consultants.

Based on initial field work at the Baltimore Silver Mine has been sufficiently positive to date that management has designated this project as our main project for the current period. The Company is also conducting due diligence to acquire new mineral property interests in its area of geographic focus.

Our current cash on hand is insufficient to complete any of the planned exploration activities and the full implementation of our planned exploration program is dependent on our ability to secure sufficient financing and the necessary permits. We can provide no assurance that we will secure sufficient financing or that any required permits will be approved. We are currently in negotiations with the property owner about a modification of terms, and considering various options to finance the next steps in our exploration process.

New Light Project

New Light Mine - Description of the Property

Land Status

Effective January 22, 2012, the Company leased from a private party two unpatented claims covering a significant portion of the former New Light Mine. The lease covers:

BLM recording numbers OMC 169670 and 169671

County recording numbers 2121100607 and 2121100608

Location

The property is situated in the Slate Creek Mining District, Section 27, T38N, R17E, in Whatcom County, Washington.

We have not finished detailed mapping on the property.

-

Access and Elevation

The elevation of the New Light property area ranges from 5,300 to 6,900 feet.