Attached files

| file | filename |

|---|---|

| 8-K - 8-K - UDR, Inc. | d626935d8k.htm |

| 388 Beale - San Francisco, CA NAREIT Presentation November 2013 Channel @ Mission Bay - San Francisco, CA Development CitySouth - San Mateo, CA Redevelopment Exhibit 99.1 |

| The Residences at Bella Terra - Huntington Beach, CA UDR, Inc. TABLE OF CONTENTS UDR, Inc. TABLE OF CONTENTS PAGE About UDR, Inc. 3 2013 Objectives / Recent Highlights 4 Differentiating Characteristics 5 UDR Strategic Priorities 6 Capital Allocation 7 Development 8 Redevelopment 11 Joint Ventures 12 Operational Excellence 13 Balance Sheet Management 14 Portfolio Improvement 15 APPENDIX 2013 Earnings Guidance 17 UDR 2013 Market Growth Expectations 18 Operating Trends Update 19 Why Multifamily Demand 20 New Multifamily Supply 21 Single-Family Housing 22 Definitions and Reconciliations 23 2 |

| About UDR, INC. 3 As of September 30, 2013. Source: Company and peer documents. The Facts (1) S&P 400 company $13 billion enterprise, 3rd largest U.S. apartment REIT 40-year track record of paying dividends 2013 annualized dividend of $0.94, ~4% yield $1.2 billion development and redevelopment pipeline West: 38% Southwest: 8% Southeast: 13% Mid-Atlantic: 22% Northeast: 20% UDR owns, operates, acquires, develops, redevelops and manages apartment communities with a focus on markets with above-average job growth, a high propensity to rent, low homeownership affordability and limited new multifamily supply. Cirque - Dallas, TX % of Total Portfolio NOI(1) |

| 2013 objectives Generated strong 3Q13 growth SS Revenue Growth: +4.9% SS NOI Growth: +6.0% 1 2 3 4 Generate strong organic growth SS Revenue Guidance: +4.75% to +5.00% SS NOI Guidance: +5.75% to +6.00% 1 Recent Highlights Progress $1.2 billion development and redevelopment pipeline Development: Trended yields avg. 150-200 basis points over market cap rates Redevelopment: 7.0% to 9.0% avg. COC stabilized yield + cap rate compression 2 Position UDR for strong cash flow per share growth in '14 and '15 3 Execute UDR's 3-Year Strategic Plan 4 Issued $300 million of unsecured debt 3.7%, 7-year unsecured debt that matures on October 1, 2020. Recent operating trends Move-outs to home purchase at 12.7% in 3Q versus UDR's LT average of 14.5% Rent-to-income at 17% in 3Q See page 19 for market-level detail 717 Olympic - Los Angeles, CA Source: Company documents. SS Growth New Lease Renewal Occupancy October 2013 1.4% 5.1% 96.2% 3Q 2013 +3.7% +5.5% 96.1% |

| 1 2 3 4 ECONOMIES OF SCALE plus NAV ACCRETIVE GROWTH OPPORTUNITIES Capital advantages and G&A efficiencies similar to larger multifamily REITs NAV-accretive investments of moderate size still "move the value creation needle" Advantageous market mix and asset quality 85% of NOI is expected to be generated by core markets by year-end 2015 Diversified mix of urban and suburban locations + A and B quality communities = strong operating results in a variety of economic environments Best-in-class operating platform Market revenue growth augmented by well-located portfolio and revenue enhancing projects Driving greater efficiencies through technology investments and cost reduction initiatives Have generated strong results that stack up well versus peers over time Extensive Joint Venture partnerships Simple, long-term partnerships with advantageous governance structures Stable and sustainable sources of capital and fee income UDR differentiating characteristics 5 Source: Company documents. Columbus Square - Manhattan |

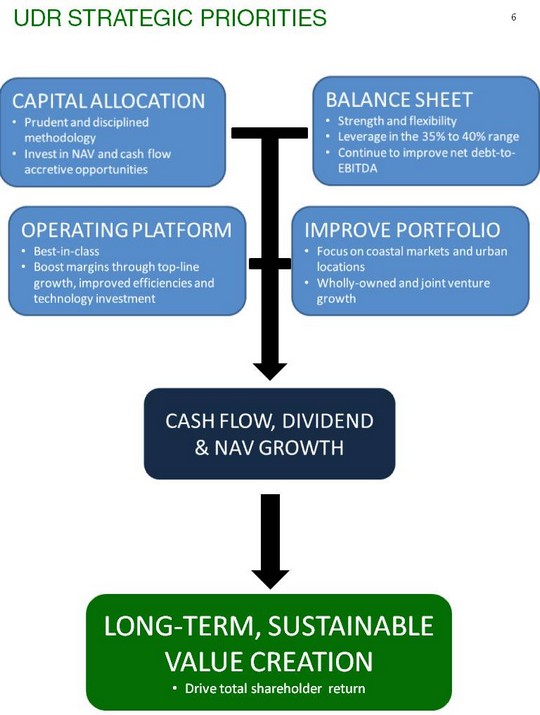

| UDR Strategic priorities 6 CASH FLOW, DIVIDEND & NAV GROWTH LONG-TERM, SUSTAINABLE VALUE CREATION Drive total shareholder return CAPITAL ALLOCATION Prudent and disciplined methodology Invest in NAV and cash flow accretive opportunities BALANCE SHEET Strength and flexibility Leverage in the 35% to 40% range Continue to improve net debt-to- EBITDA OPERATING PLATFORM Best-in-class Boost margins through top-line growth, improved efficiencies and technology investment IMPROVE PORTFOLIO Focus on coastal markets and urban locations Wholly-owned and joint venture growth |

| Capital Allocation Invest in growth opportunities that are accretive to cash flow and NAV per share Partially fund with (1) equity issued at NAV or at a premium to NAV or with (2) asset sales at NAV to maintain or improve leverage Weigh the merits of investment opportunities against the cost and availability of capital Currently, development and redevelopment represent solidly accretive uses of capital Capitol View on 14th - Washington, D.C. 7 |

| As of September 30, 2013. Source: Company documents. Capital Allocation (Development) 8 Pipeline statistics(1) Size: 3,142 homes at 100% Cost: $1.1 billion, $365K per home at 100% Spent to date: $771 million (71% of total cost) Expected completion year of remaining in- process development (by %, $): 2013: 30%, $286 million 2014: 48%, $461 million 2015: 23%, $218 million Why develop? Value Creation Potential: Stabilized yield on cost (6.0% to 6.5% currently) 150 to 200 basis points above market cap rates on a trended basis Portfolio Improvement: Improves the quality of UDR's portfolio; reduces its age and cap ex requirements Channel @ Mission Bay - San Francisco, CA The Residences at Bella Terra - Huntington Beach, CA Land portfolio Markets: So. California, Dallas, Boston, San Francisco Bay Area and Seattle Book value: ~$150 million at UDR ownership interest; ~$349 million at 100% Underway development ($M) |

| Source: Axiometrics, Company documents. (CHART) Capital Allocation (Development) 9 our development assets are expected to create significant Value Where to develop? Demographic trends, economic drivers (i.e., job growth, etc.) and how multifamily fundamentals / valuations have trended over the long-term govern our review process on where to allocate development capital Our targeted coastal markets screen well +36% Next Three Years Annual Expectations Next Three Years Annual Expectations Next Three Years Annual Expectations Last 15-Year Cumulative Last 15-Year Cumulative Market Job Growth Supply Growth Demand > Supply Rev Growth > U.S. Avg. (28%) Seattle 2.6% 2.0% ? 35% ? San Fran Area 2.9% 1.3% ? 38% ? Los Angeles 1.6% 0.7% ? 50% ? Orange Cnty 2.1% 1.1% ? 47% ? San Diego 2.2% 1.2% ? 52% ? Dallas 2.9% 2.1% ? 13% ? Metro D.C. 1.8% 2.0% ? 55% ? New York 1.5% 0.7% ? 43% ? Boston 1.9% 1.1% ? 40% ? |

| We are achieving or beating the effective rental rate per square foot estimates in our project plans for our 6 lease-ups However, occupancy at 3 of the projects is lower than expected Capital Allocation (Development) 10 Progress of development projects in lease-up Development pipelines typically include projects that both outperform and underperform versus their respective plans For our 6 development projects currently in lease-up, some projects are performing above our estimated 150 to 200 basis point average spread, some are in range and some are below. The current weighted average spread is near the middle of the range 13th and Market - San Diego, CA; Bella Terra - Huntington Beach, CA; Channel - San Francisco, CA; Los Alisos - Mission Viejo, CA; Domain College Park - University of Maryland; Fiori - Dallas, TX. Source: Company documents. A majority of the projects in lease-up are progressing ahead of plan. Spread - Trended Construction Yield versus Market Cap Rate for Current Lease-ups Spread - Trended Construction Yield versus Market Cap Rate for Current Lease-ups Spread - Trended Construction Yield versus Market Cap Rate for Current Lease-ups Projects (1) Budgeted Cost ABOVE RANGE: > 200 BPS Channel @ Mission Bay; 13th and Market $217M IN RANGE: 150-200 BPS Bella Terra $150M BELOW RANGE: < 150 BPS Fiori; Los Alisos; Domain College Park $198M |

| Why redevelop? Strong Return: Cash on cash stabilized returns of 7-9% provide a strong, low-risk return Value Creation: Significantly repositioning a community can lower its cap rate by an average of 50 to 75 bps As of September 30, 2013. Before: est. fair market value of the assets prior to redevelopment + redevelopment cost. After: est. fair market value of the assets. Based on redevelopment spend. Source: Company documents. (CHART) Capital Allocation (redevelopment) 11 Current Pipeline statistics(1) Size: 1,670 homes Budgeted Cost: $135 million Cost per home: $81,000 Redevelopment ($M) New York: $60 Orange County: $75 After: Before: Recent Redevelopment Completions Communities: The Westerly, CitySouth, and Barton Creek Landing Locations: Marina del Rey, CA, San Mateo, CA, and Austin, TX Total Homes: 969 Total Spend: $84M (Avg. $87K per home) Avg. Return on Cost: 8.1% +60% Before After ? Avg. Rent per Home $1,426 $2,067 +45% Avg. Cap Rate 5.2% 4.6% -60 bps NAV Creation ($M) $65(2) +77%(3) The Westerly on Lincoln - Marina del Rey, CA |

| (CHART) Excludes Lodge at Stoughton, Domain College Park and 13th & Market Measured as gross book value Source: Company documents. Columbus Square - New York, NY UNCONSOLIDATED JV(1) SIZE ($M)(2) OWN. INTEREST TYPE UDR/MetLife II $1,595 50% Long-term partnership in high-quality, core assets UDR/MetLife I $891 13% Long-term partnership in high-quality, core assets UDR/MetLife Vitruvian Park(r) $284 50% Long-term partnership in master planned development Kuwait Finance House $282 30% Medium-term partnership focused on Washington, D.C. Texas $323 20% Medium/Short-term partnership UDR has three primary operating joint venture relationships that comprise $3.5 billion of apartment communities. These relationships: Provide a stable source of long-term capital, and Reduce effective cost of capital while enhancing returns via promotes and fee income Capital Allocation (Joint Ventures) 12 Current - San Diego, CA (CHART) Above UDR's SS rev. growth of 5.1% YTD. |

| (CHART) Operational excellence drives property cash flow growth which supports dividend per share growth over time Investments in technology will continue to drive efficiency and improve our resident's experiences Best-in-class operating platform Operational Excellence 13 UDR's operational performance stacks up well over time and versus peers Source: Company and peer documents. Strata - San Diego, CA Peer Group avg.: 40% |

| METRIC YEAR-END 2009 3Q13 YEAR-END 2013E YEAR-END 2015E Debt-to-assets 53% 39% 38% to 40% 35% to 40% Net debt-to-EBITDA 10.0x 7.0x 6.8x to 7.2x 6.0x to 6.5x Fixed Charge Coverage 2.0x 3.2x 2.9x to 3.1x 3.1x to 3.3x Balance sheet management 14 3 Well-Laddered Maturity Schedule with 90% fixed-rate debt 4 Investment Grade Ratings S&P: BBB, stable outlook Moody's: Baa2, positive outlook (CHART) n/a 9% 16% 4% 9% 25% 9% 12% 4% Source: Company documents. 11% n/a (CHART) |

| The Westerly on Lincoln - Marina del Rey, CA Portfolio is Still Improving $1.2 billion pipeline of high-quality, well-located development and redevelopment But recycling of capital will continue Employ a prudent and disciplined approach to capital allocation Continued recycling will take place through normal business activities Continue to target core markets for expansion Primarily urban locations in high barrier-to-entry coastal markets with strong multifamily fundamentals Strategic portion of UDR's portfolio repositioning is complete Portfolio improvement 15 TOTAL PORTFOLIO NOI CONCENTRATIONS TOTAL PORTFOLIO NOI CONCENTRATIONS TOTAL PORTFOLIO NOI CONCENTRATIONS TOTAL PORTFOLIO NOI CONCENTRATIONS Year-End 2009 3Q 2013 Year-End 2015E(1) Core Markets 57% 77% 85% Capital Warehouse Markets 30% 18% 15% Non-Core Markets 13% 5% --- Total 100% 100% 100% Includes 2013 - 2015 acquisition/disposition assumptions and current development/redevelopment projects. Source: Company documents. |

| Rivergate - Manhattan UDR, Inc. Appendix UDR, Inc. Appendix PAGE 2013 Earnings Guidance 17 2013 Market Growth Expectations 18 Operating Trends Update 19 Why Multifamily Demand 20 New Multifamily Supply 21 Single-Family Housing 22 Definitions and Reconciliations 23 16 |

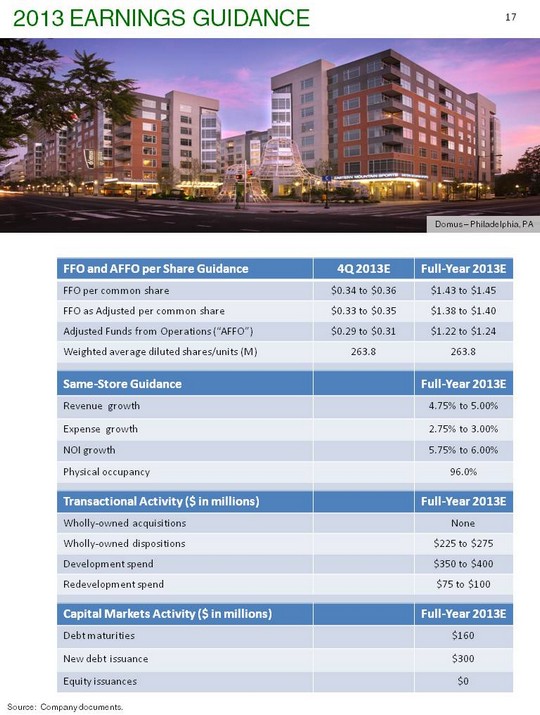

| 2013 Earnings Guidance 17 FFO and AFFO per Share Guidance 4Q 2013E Full-Year 2013E FFO per common share $0.34 to $0.36 $1.43 to $1.45 FFO as Adjusted per common share $0.33 to $0.35 $1.38 to $1.40 Adjusted Funds from Operations ("AFFO") $0.29 to $0.31 $1.22 to $1.24 Weighted average diluted shares/units (M) 263.8 263.8 Same-Store Guidance Full-Year 2013E Revenue growth 4.75% to 5.00% Expense growth 2.75% to 3.00% NOI growth 5.75% to 6.00% Physical occupancy 96.0% Transactional Activity ($ in millions) Full-Year 2013E Wholly-owned acquisitions None Wholly-owned dispositions $225 to $275 Development spend $350 to $400 Redevelopment spend $75 to $100 Capital Markets Activity ($ in millions) Full-Year 2013E Debt maturities $160 New debt issuance $300 Equity issuances $0 Source: Company documents. Domus - Philadelphia, PA |

| 2013E 2013E 2013E REVENUES EXPENSES NOI Same-Store ("SS") Growth 4.75% to 5.00% 2.75% to 3.00% 5.75% to 6.00% Revenue growth based on UDR's current 2013 forecast. Source: Company documents. Core Markets: Seattle, San Francisco Bay Area, Los Angeles, Orange County, San Diego, Denver, Austin, Dallas, Boston, New York, Baltimore/Washington D.C. area and Philadelphia. Capital Warehouse Markets: Portland, Inland Empire, Nashville, Richmond, Tampa, Orlando and Other FL. Non-Core Markets: Sacramento, Monterey Peninsula and Norfolk. Includes our Core Markets and Warehouse Capital/Non-Core markets that generated in excess of 2% of portfolio NOI in 3Q13. 2013 Market Growth Expectations 18 Market % of 3Q13 SS NOI Market % of 3Q13 SS NOI Market % of 3Q13 SS NOI Austin 2.4% Nashville 4.0% Monterey Peninsula 3.2% Baltimore 6.1% New York 4.9% San Diego 1.0% Boston 4.7% Norfolk 2.4% Seattle 5.9% Dallas 4.8% Orange County 10.2% San Francisco Bay Area 12.6% Los Angeles 3.3% Orlando 5.3% Tampa 6.0% Metro Washington, D.C. 13.9% Richmond 3.1% TOTAL 93.8% |

| Includes our SS Core Markets and Warehouse Capital and Non-Core markets that generated in excess of 2% of portfolio NOI in 3Q13. Source: Company documents. Operating Trends Update 19 % Total NOI % SS NOI Effective YOY SS New Lease Rate Growth Effective YOY SS New Lease Rate Growth Effective YOY SS Renewal Lease Rate Growth Effective YOY SS Renewal Lease Rate Growth Annualized SS Turnover as of 10/31/2013 Annualized SS Turnover as of 10/31/2013 Same-Store (SS) Market(1) 3Q 2013 3Q 2013 October2013 3Q 2013 October2013 3Q 2013 YTD 2013 YTD 2012 Metro D.C. 12.9% 13.9% -1.8% -0.4% 3.9% 4.7% 47.2% 46.5% New York 13.1% 4.9% 1.9% 6.1% 6.7% 7.4% 42.2% 46.1% San Francisco Bay Area 9.8% 12.6% 5.5% 8.1% 7.7% 7.8% 58.5% 60.0% Orange County 10.0% 10.2% 2.4% 3.3% 5.0% 5.0% 65.7% 64.6% Seattle 6.5% 5.9% 3.7% 6.8% 6.6% 6.1% 59.5% 59.7% Boston 5.8% 4.7% 2.4% 6.5% 5.7% 5.5% 47.0% 49.1% Baltimore 4.7% 6.1% -1.7% 0.9% 4.3% 4.5% 54.0% 52.3% Tampa 4.6% 6.0% 1.8% 1.0% 4.0% 5.1% 50.9% 52.8% Dallas 4.9% 4.8% -2.1% 2.6% 5.6% 6.0% 57.3% 54.4% Los Angeles 4.4% 3.3% 1.4% 3.4% 2.8% 4.8% 64.8% 59.1% Orlando 4.1% 5.3% 4.4% 4.6% 5.7% 6.0% 55.4% 56.8% Nashville 3.1% 4.0% 5.3% 4.9% 4.0% 4.7% 56.8% 55.5% Monterey Peninsula 2.5% 3.2% 2.0% 3.7% 5.0% 4.1% 50.3% 62.6% Austin 2.4% 2.4% 4.3% 5.8% 5.8% 6.3% 53.0% 53.6% Richmond 2.4% 3.1% -2.9% 1.7% 3.2% 3.2% 57.7% 67.9% Norfolk 1.8% 2.4% -7.3% -2.3% 2.8% 2.5% 60.5% 58.4% San Diego 1.0% 1.0% -4.8% 2.0% 3.2% 5.0% 80.7% 73.8% Total SS Wtd. Avg. 94.0% 93.8% 1.4% 3.7% 5.1% 5.5% 55.7% 56.6% |

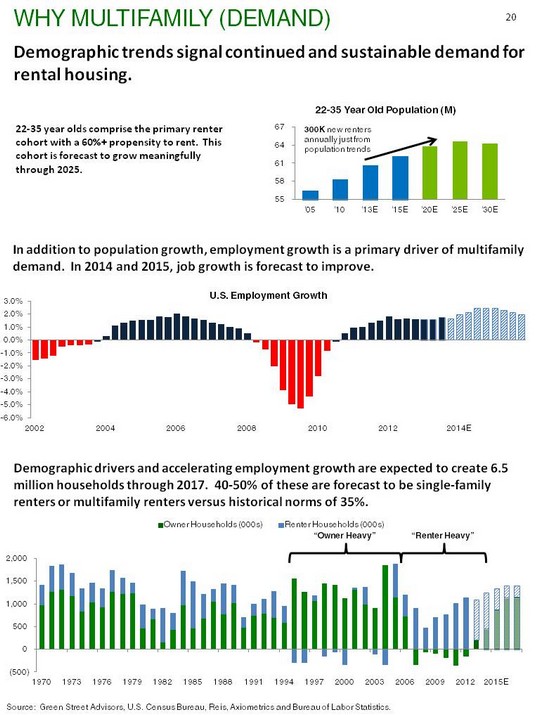

| Why Multifamily (Demand) (CHART) Source: Green Street Advisors, U.S. Census Bureau, Reis, Axiometrics and Bureau of Labor Statistics. 20 22-35 year olds comprise the primary renter cohort with a 60%+ propensity to rent. This cohort is forecast to grow meaningfully through 2025. In addition to population growth, employment growth is a primary driver of multifamily demand. In 2014 and 2015, job growth is forecast to improve. Demographic drivers and accelerating employment growth are expected to create 6.5 million households through 2017. 40-50% of these are forecast to be single-family renters or multifamily renters versus historical norms of 35%. (CHART) Demographic trends signal continued and sustainable demand for rental housing. (CHART) "Owner Heavy" "Renter Heavy" |

| However, when comparing new supply to expected job growth, UDR's portfolio is well positioned. Why Multifamily (MF Supply) 21 Portland New multifamily supply is expected to return to levels consistent with its long-term historical average. (CHART) '13E to '17E Traditional Apt. Supply Growth Gross Units: +1.0M Net units after obsolescence loss: +800K Size of dots represents UDR's total NOI concentration in a market. Includes joint venture homes at UDR's pro-rata ownership interest. Source: U.S. Census Bureau, Green Street Advisors, Axiometrics and Bureau of Labor Statistics. |

| Utilizes National Association of Realtors Home Affordability Index methodology. 100 indicates exactly enough household income to purchase a median priced home in a market. Source: Green Street Advisors, U.S. Census Bureau, Reis, Axiometrics, Bureau of Labor Statistics and Case-Shiller. Demand for single-family continues to improve, but still stringent down payment requirements, reduced mortgage loan availability and, more recently, increasing mortgage rates continue to hinder sales. This is positive for coastally focused owners/operators where home affordability is lower. Why Multifamily (SF Housing) 22 (CHART) (CHART) Single-family affordability has improved but UDR's core markets remain less affordable versus the U.S. and other primary markets where the Company does not own assets(1). The homeownership rate continues to decline. Every 1% drop in the homeownership rate results in an estimated 1.0 million new renters. |

| Please see the Company's most recent Earnings Supplement, available at www.udr.com, for a full list of definitions, reconciliations and details on the financial position and operating results of the Company. Adjusted Funds From Operations ("AFFO"): The Company defines AFFO as FFO as Adjusted less recurring capital expenditures that are necessary to help preserve the value of and maintain functionality at our communities. Management considers AFFO a useful supplemental performance metric for investors as it is more indicative of the Company's operational performance than FFO or FFO as Adjusted. AFFO is not intended to represent cash flow or liquidity for the period, and is only intended to provide an additional measure of our operating performance. The Company believes that net income attributable to UDR, Inc. is the most directly comparable GAAP financial measure to AFFO. Management believes that AFFO is a widely recognized measure of the operations of REITs, and presenting AFFO will enable investors to assess our performance in comparison to other REITs. However, other REITs may use different methodologies for calculating AFFO and, accordingly, our AFFO may not always be comparable to AFFO calculated by other REITs. AFFO should not be considered as an alternative to net income (determined in accordance with GAAP) as an indication of financial performance, or as alternative to cash flows from operating activities (determined in accordance with GAAP) as a measure of our liquidity, nor is it indicative of funds available to fund our cash needs, including our ability to make distributions. A reconciliation from net income attributable to UDR, Inc. to AFFO is provided on page 27 of this presentation. Funds From Operations ("FFO"): The Company defines FFO as net income (computed in accordance with GAAP), excluding impairment write-downs of depreciable real estate or of investments in non-consolidated investees that are driven by measurable decreases in the fair value of depreciable real estate held by the investee, gains (or losses) from sales of depreciable property, plus real estate depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. This definition conforms with the National Association of Real Estate Investment Trust's definition issued in April 2002. In the computation of diluted FFO, OP units, unvested restricted stock, stock options, and the shares of Series E Cumulative Convertible Preferred Stock are dilutive; therefore, they are included in the diluted share count. Activities of our taxable REIT subsidiary (TRS), RE3, include development and land entitlement. From time to time, we develop and subsequently sell a TRS property which results in a short-term use of funds that produces a profit that differs from the traditional long-term investment in real estate for REITs. We believe that the inclusion of these TRS gains in FFO is consistent with the standards established by NAREIT as the sort-term investment is incidental to our main business. TRS gains on sales, net of taxes, are defined as net sales proceeds less a tax provision and the gross investment basis of the asset before accumulated depreciation. Management considers FFO a useful metric for investors as the Company uses FFO in evaluating property acquisitions and its operating performance and believes that FFO should be considered along with, but not as an alternative to, net income and cash flow as a measure of the Company's activities in accordance with GAAP. FFO does not represent cash generated from operating activities in accordance with GAAP and is not necessarily indicative of funds available to fund our cash needs. A reconciliation from net income attributable to UDR, Inc. to FFO is provided on page 27 of this presentation. Funds From Operations as Adjusted: The Company defines FFO as Adjusted as FFO excluding the impact of acquisition-related costs and other non-comparable items including, but not limited to, prepayment costs/benefits associated with early debt retirement, gains on sales of marketable securities and TRS property, deferred tax valuation allowance increases and decreases, storm-related expenses, severance costs and legal costs. Management believes that FFO as Adjusted is useful supplemental information regarding our operating performance as it provides a consistent comparison of our operating performance across time periods and allows investors to more easily compare our operating results with other REITs. FFO as Adjusted is not intended to represent cash flow or liquidity for the period, and is only intended to provide an additional measure of our operating performance. The Company believes that net income attributable to UDR, Inc. is the most directly comparable GAAP financial measure to FFO as Adjusted. However, other REITs may use different methodologies for calculating FFO as Adjusted or similar FFO measure and, accordingly, our FFO as Adjusted may not always be comparable to FFO as Adjusted or similar FFO measure calculated by other REITs. FFO as Adjusted should not be considered as an alternative to net income (determined in accordance with GAAP) as an indication of financial performance, or as an alternative to cash flows from operating activities (determined in accordance with GAAP) as a measure of our liquidity. A reconciliation from net income attributable to UDR, Inc. to FFO as Adjusted is provided on page 27 of this presentation. Net Asset Value: Net Asset Value ("NAV") is defined as marked-to-market value of assets less marked-to-market value of liabilities and preferred equity, divided by total outstanding diluted shares and operating units. Management considers NAV a useful metric for investors as it provides context to portfolio value changes over time based on widely accepted market inputs. Definitions and reconciliations 23 |

| Stabilization Period for Development Yield: The Company defines the stabilization period for development property yield as the forward twelve month NOI, excluding any remaining lease-up concessions outstanding, commencing one year following the delivery of the final home of the project. Stabilization Period for Redevelopment Yield: The Company defines the stabilization period for a redevelopment property for purposes of computing the Projected Weighted Average Return on Incremental Capital Invested, as the forward twelve month NOI, excluding any remaining lease-up concessions outstanding, following the delivery of the final home of a project. Effective New Lease Rate Growth: The Company defines effective new lease rate growth as the increase in gross potential rent realized less all concessions for the new lease term (current effective rent) versus prior resident effective rent for the prior lease term on all new leases commenced during the current quarter. Management considers effective new lease rate growth a useful metric for investors as it is useful when assessing market-level new demand trends. Effective Renewal Lease Rate Growth: The Company defines effective renewal lease rate growth as the increase in gross potential rent realized less all concessions for the new lease term (current effective rent) versus prior effective rent for the prior lease term on all renewed leases commenced during the current quarter. Management considers effective renewal lease rate growth a useful metric for investors as it assesses market-level, in-place demand trends. JV Return on Equity ("ROE"): The Company defines JV ROE as the pro rata share of property NOI plus property and asset management fee revenue less interest expense, divided by the average of beginning and ending equity capital for the quarter. Management considers ROE a useful metric for investors as it provides a widely used measure of how well the Company is investing its capital on a leveraged basis. JV Return on Invested Capital ("ROIC"): The Company defines JV ROIC as the pro rata share of property NOI plus property and asset management fee revenue divided by the average of beginning and ending invested capital for the quarter. Management considers ROIC a useful metric for investors as it provides a widely used measure of how well the Company is investing its capital on an unleveraged basis. Stabilized Yield on Developments: Expected stabilized yields on development are calculated as follows, projected stabilized NOI less management fees divided by budgeted construction cost on a project-specific basis. Projected stabilized NOI for development projects, calculated in accordance with the NOI reconciliation provided on page 26 of this presentation, is set forth in the definition of Stabilization Period for Development Yield. Given the differing completion dates and years for which NOI is being projected for these communities as well as the complexities associated with estimating other expenses upon completion such as corporate overhead allocation, general and administrative costs and capital structure, a reconciliation to GAAP measures is not meaningful. Projected NOI for these projects is neither provided, nor is representative of Management's expectations for the Company's overall financial performance or cash flow growth and there can be no assurances that forecast NOI growth implied in the estimated construction yield of any project will be achieved. Management considers estimated stabilized yield on development as a useful metric for investors as it helps provide context to the expected effects that development projects will have on the Company's future performance once stabilized. Total Revenue per Occupied Home: The Company defines total revenue per occupied home as rental and other revenues, calculated in accordance with GAAP, divided by the product of occupancy and the number of apartment homes. Management considers total revenue per occupied home a useful metric for investors as it serves as a proxy for portfolio quality, both geographic and physical. Value Creation: Value creation is defined as the difference between the Company's best estimate of the current or expected market value of a community and its original purchase price or cost basis. Underlying valuation estimates and model inputs are provided by the Company. Estimated value creation is not representative of the Company's expectations for its overall financial performance or cash flow growth and there can be no assurances that the value creation implied for any of the Company's communities will be achieved. Management considers value creation a useful metric for investors as it quantifies how successful the Company's past investments have been and current investments are expected to be. Definitions and reconciliations 24 |

| Net Debt to EBITDA: The Company defines net debt to EBITDA as total debt net of cash and cash equivalents divided by EBITDA. EBITDA is defined as net income, excluding the impact of interest expense, real estate depreciation and amortization of wholly owned and other joint venture communities, other depreciation and amortization, noncontrolling interests, net gain on the sale of depreciable property, and RE3 income tax. Management considers net debt to EBITDA a useful metric for investors as it provides ratings agencies, investors and lending partners with a widely-used measure of the Company's ability to service its debt obligations as well as compare leverage against that of its peer REITs. A reconciliation between net income and EBITDA is provided below: Net Debt-to-EBITDA ($000s) Quarter Ended September 30, 2013 Net income/(loss) attributable to UDR, Inc. $ 3,188 Adjustments (includes continuing and discontinued operations): Interest expense 30,939 Real estate depreciation and amortization 84,266 Real estate depreciation and amortization on unconsolidated joint ventures 10,514 Other depreciation and amortization 1,176 Noncontrolling interests 47 Income tax expense/(benefit) (2,658) EBITDA $ 127,472 Joint venture financing and acquisition fees (36) Hurricane-related recoveries, net (4,059) EBITDA - adjusted for non-recurring items $ 123,377 Annualized EBITDA - adjusted for non-recurring items $ 493,508 Total debt $ 3,463,172 Cash 11,149 Net Debt $ 3,452,023 Net Debt-to-EBITDA, adjusted for non-recurring items 7.0x Definitions and reconciliations 25 |

| Net Operating Income ("NOI"): The Company defines NOI as rental income less direct property rental expenses. Rental income represents gross market rent less adjustments for concessions, vacancy loss and bad debt. Rental expenses include real estate taxes, insurance, personnel, utilities, repairs and maintenance, administrative and marketing. Excluded from NOI is property management expense which is calculated as 2.75% of property revenue to cover the regional supervision and accounting costs related to consolidated property operations, and land rent. Management considers NOI a useful metric for investors as it is a more meaningful representation of a community's continuing operating performance than net income as it is prior to corporate-level expense allocations, general and administrative costs, capital structure and depreciation and amortization and is a widely used input, along with capitalization rates, in the determination of real estate valuations. A reconciliation from net income attributable to UDR, Inc. to NOI is provided below. Net Operating Income ($000s) 3Q 2013 2Q 2013 1Q 2013 4Q 2012 3Q 2012 YTD 2013 YTD 2012 Net Income/(loss) attributable to UDR, Inc. $ 3,188 $ 5,192 $ (268) $ (12,300) $ (9,031) $ 8,112 $ 224,477 Property management 5,236 5,187 5,068 5,017 4,998 15,491 14,615 Other operating expenses 1,787 1,807 1,643 1,464 1,467 5,237 4,284 RE depreciation and amortization 84,266 85,131 83,442 83,456 88,223 252,839 260,604 Interest expense 30,939 30,803 30,981 30,660 31,845 92,723 108,132 Hurricane-related (recoveries)/charges, net (6,460) (2,772) (3,021) 8,495 - (12,253) - General and administrative 11,364 9,866 9,476 10,653 10,022 30,706 33,139 Tax benefit , net (includes valuation adjustment) (2,658) (2,683) (1,973) (1,628) (2,960) (7,314) (28,654) Income/(loss) from unconsolidated entities 3,794 (515) 2,802 2,757 719 6,081 5,822 Interest and other income, net (829) (1,446) (1,016) (1,157) (1,235) (3,291) (2,435) Joint venture management and other fees (3,207) (3,217) (2,923) (2,817) (3,320) (9,347) (9,026) Other depreciation and amortization 1,176 1,138 1,146 1,092 1,078 3,460 3,013 Income from discontinued operations, net of tax - - - (156) 1,133 - (263,183) Net income/(loss) attributable to noncontrolling interests 47 162 (41) (655) (645) 168 8,781 Total consolidated NOI $ 128,643 $ 128,653 $ 125,316 $ 124,881 $ 122,294 $ 382,612 $ 359,569 Definitions and reconciliations 26 |

| Definitions and reconciliations 27 In thousands, except per share amounts Quarter Ended September 30, 2013 Net income attributable to UDR, Inc. $ 3,188 Distributions to preferred stockholders (931) Real estate depreciation and amortization, including discontinued operations 84,266 Noncontrolling interest 47 Real estate depreciation and amortization on unconsolidated joint ventures 10,514 Net (gain)/loss on the sale of depreciable property in discontinued operations, excluding TRS - Premium on preferred stock redemptions, net - Funds from operations ("FFO") - basic $ 97,084 Distributions to preferred stockholders - Series E (Convertible) 931 FFO, diluted $ 98,015 FFO per common share, basic $ 0.37 FFO per common share, diluted $ 0.37 Weighted average number of common shares and OP Units outstanding - basic 259,308 Weighted average number of common shares, OP Units, and common stock equivalents outstanding - diluted 263,813 Impact of adjustments to FFO: Joint venture financing and acquisition fees $ (36) Hurricane-related recoveries, net(1) (4,059) $ (4,095) FFO as Adjusted, diluted $ 93,920 FFO as Adjusted per common share, diluted $ 0.36 Recurring capital expenditures (11,989) AFFO $ 81,931 AFFO per common share, diluted $ 0.31 (1) Adjustment primarily represents the portion of Hurricane Sandy insurance recoveries in 2013 that relate to the $9.3M in charges added back to FFO as Adjusted in 4Q 2012. The $2.4M difference between the $6.5M hurricane-related recoveries reflected on the Consolidated Statements of Operations for the three months ended September 30, 2013 and the $4.1M adjustment above represents the amount of 2013 business interruption recoveries during the quarter. The business interruption insurance recoveries for the three months ended September 30, 2013 are offset by lost rental revenues from the business interruption in 2013. |

| Certain statements made in this presentation may constitute "forward-looking statements." Words such as "expects," "intends," "believes," "anticipates," "plans," "likely," "will," "seeks," "estimates" and variations of such words and similar expressions are intended to identify such forward-looking statements. Forward-looking statements, by their nature, involve estimates, projections, goals, forecasts and assumptions and are subject to risks and uncertainties that could cause actual results or outcomes to differ materially from those expressed in a forward-looking statement, due to a number of factors, which include, but are not limited to, unfavorable changes in the apartment market, changing economic conditions, the impact of inflation/deflation on rental rates and property operating expenses, expectations concerning availability of capital and the stabilization of the capital markets, the impact of competition and competitive pricing, acquisitions, developments and redevelopments not achieving anticipated results, delays in completing developments, redevelopments and lease-ups on schedule, expectations on job growth, home affordability and demand/supply ratio for multifamily housing, expectations concerning development and redevelopment activities, expectations on occupancy levels, expectations concerning the joint ventures with third parties, expectations that automation will help grow net operating income, expectations on annualized net operating income and other risk factors discussed in documents filed by the Company with the Securities and Exchange Commission from time to time, including the Company's Annual Report on Form 10-K and the Company's Quarterly Reports on Form 10-Q. Actual results may differ materially from those described in the forward-looking statements. These forward-looking statements and such risks, uncertainties and other factors speak only as of the date of this presentation, and the Company expressly disclaims any obligation or undertaking to update or revise any forward-looking statement contained herein, to reflect any change in the Company's expectations with regard thereto, or any other change in events, conditions or circumstances on which any such statement is based, except to the extent otherwise required under the U.S. securities laws. This presentation and these forward-looking statements include UDR's analysis and conclusions and reflect UDR's judgment as of the date of these materials. UDR assumes no obligation to revise or update to reflect future events or circumstances. * Green Street Advisors ("GSA") is an independent research, trading and consulting firm. By referencing reports included on GSA's website, UDR does not intend to incorporate any of the information included on that website into this presentation, or to otherwise adopt or endorse any analysis, statements or communications made by GSA on its website or elsewhere. Forward Looking Statements 28 |

| Notes 29 |

| Notes 30 |

| Notes 31 |

| Investor Relations Contact: Chris Van Ens cvanens@udr.com 720.348.7762 |