Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - Caesars Acquisition Co | d579522dex232.htm |

| EX-23.1 - EX-23.1 - Caesars Acquisition Co | d579522dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on August 20, 2013

Registration No. 333-189876

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CAESARS ACQUISITION COMPANY

(Exact name of registrant as specified in its charter)

| DELAWARE | 7993 | 46-2672999 | ||

| (State or other jurisdiction of Incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

One Caesars Palace Drive

Las Vegas, NV 89109

(702) 407-6000

(Address, including zip code, and telephone number, including area code, of Registrant’s Principal Executive Offices)

Mitch Garber

Chief Executive Officer

Caesars Acquisition Company

One Caesars Palace Drive

Las Vegas, NV 89109

(702) 407-6000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a copy to:

Monica K. Thurmond, Esq.

Paul, Weiss, Rifkind, Wharton & Garrison LLP

1285 Avenue of the Americas

New York, New York 10019-6064

(212) 373-3000

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. þ

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | þ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee | ||

| Class A common stock, par value $0.001 per share |

$ 1,182,000,000 | $161,225(2) | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended (the “Securities Act”). Represents the estimated maximum aggregate gross proceeds from the exercise of the maximum number of subscription rights that may be issued. |

| (2) | Previously paid. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated August 20, 2013

PROSPECTUS

CAESARS ACQUISITION COMPANY

Up To 125,359,584 Shares of Class A Common Stock Issuable Upon the Exercise of Subscription Rights At $9.43 Per Share

Caesars Entertainment Corporation, or “Caesars Entertainment,” is distributing to each holder of its common stock as of the close of business on , 2013, the record date, at no charge, of non-transferable subscription rights to purchase up to an aggregate of 125,359,584 shares of Class A common stock, par value $0.001 per share, of Caesars Acquisition Company, or “CAC,” at a price of $9.43 per whole share, or the “rights offering.” Each holder of Caesars Entertainment’s common stock as of the record date will receive one subscription right for each full common share owned by that stockholder as of the record date. Each subscription right will entitle its holder to purchase from CAC one share of CAC’s Class A common stock. Additionally, holders of subscription rights who fully exercise all of their basic subscription rights may also make a request to purchase additional shares of CAC’s Class A common stock, through exercise of the over-subscription privilege, although we cannot assure you that any over-subscriptions will be filled.

To the extent you properly exercise your over-subscription privilege for an amount of shares of Class A common stock that exceeds the number of the unsubscribed shares allocated to you, the subscription agent will return to you any excess subscription payments, without interest or penalty, as soon as practicable following the expiration of the rights offering. We are not requiring a minimum individual or overall subscription to complete the rights offering. Caesars Entertainment has engaged to serve as the subscription agent (the “Subscription Agent”) for the rights offering, to serve as information agent (the “Information Agent”) for the rights offering and to serve as solicitation agent (the “Solicitation Agent”) for the rights offering. will hold in escrow the funds we receive from subscribers until we complete or cancel the rights offering.

The subscription rights will expire if they are not exercised by 5:00 p.m., New York City time, on , 2013, the th business day following the distribution of the rights, unless Caesars Entertainment extends the rights offering period for additional periods ending no later than . The rights offering is subject to the satisfaction or waiver by Caesars Entertainment or CAC, as applicable, of certain conditions. In addition, Caesars Entertainment has the right to withdraw and cancel the rights offering if, at any time prior to its expiration, the board of directors of Caesars Entertainment determines, in its sole discretion, that the Transactions cannot proceed on the terms contemplated. See “The Rights Offering—Conditions, Withdrawal and Cancellation.”

As of the date hereof, approximately 70% of the common stock of Caesars Entertainment is beneficially owned by Hamlet Holdings LLC (“Hamlet Holdings”), the members of which are comprised of three individuals affiliated with affiliates of Apollo Global Management, LLC (collectively with its subsidiaries, “Apollo”) and two individuals affiliated with affiliates of TPG Global, LLC (together with its affiliates, “TPG,” and together with Apollo, the “Sponsors”), through an irrevocable proxy that gives Hamlet Holdings sole voting and sole dispositive power over the stock that is held by funds affiliated with and controlled by the Sponsors and their co-investors. The Sponsors have advised Caesars Entertainment that the affiliates of the Sponsors holding common stock of Caesars Entertainment intend to exercise subscription rights of at least $500.0 million (which would represent approximately 42% of our Class A common stock assuming the subscription rights are exercised in full by all holders of the subscription rights), though they have not entered into any agreement to do so. Consummation of the Transactions is contingent on the exercise of subscription rights of at least $500.0 million by affiliates of the Sponsors. The affiliates of the Sponsors, along with their co-investors, plan to grant Hamlet Holdings an irrevocable proxy for sole voting and sole dispositive power of the Class A common stock of CAC received as a result of this offering (the “Sponsor CAC Proxy”). As a result, we expect that Hamlet Holdings will beneficially own at least % of our Class A common stock, and that we will qualify as and, if listed, elect to be, a “controlled company” under the NASDAQ Marketplace rules following the completion of the rights offering and the listing of our Class A common stock, if any. This election would allow us to rely on exemptions from certain corporate governance requirements otherwise applicable to NASDAQ-listed companies. See “Risk Factors—Risks Related to Our Class A Common Stock—We will be a “controlled company” within the meaning of the NASDAQ Marketplace rules and, as a result, will qualify for, and intend to rely on, exemptions from certain corporate governance requirements.”

You should carefully consider whether to exercise your subscription rights before the rights offering expires. All exercises of subscription rights are irrevocable. However, exercises of subscription rights will be revocable if there is a fundamental change to the terms of this offering and related transactions.

The purchase of and investing in shares of our Class A common stock involves a high degree of risk. You should read the section entitled “Risk Factors” beginning on page 42 for a discussion of certain risks that you should consider before exercising your subscription rights and investing in shares of our Class A common stock. Neither Caesars Entertainment nor CAC’s board of directors is making any recommendation regarding your exercise of the subscription rights.

The subscription rights are non-transferable. We intend to apply to list shares of our Class A common stock for trading on the NASDAQ Global Select Market under the symbol “CGP,” however, we cannot assure you that we will achieve a listing upon completion of this offering or thereafter. No public market currently exists for our Class A common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Prospectus dated , 2013.

Table of Contents

| 1 | ||||

| Questions and Answers About the Company and the Rights Offering |

29 | |||

| 42 | ||||

| 79 | ||||

| 81 | ||||

| 82 | ||||

| 83 | ||||

| 84 | ||||

| 94 | ||||

| 95 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

96 | |||

| 126 | ||||

| 134 | ||||

| 153 | ||||

| 162 | ||||

| Security Ownership of Certain Beneficial Owners and Management |

173 | |||

| 175 | ||||

| 182 | ||||

| 185 | ||||

| 189 | ||||

| 190 | ||||

| 200 | ||||

| 207 | ||||

| 209 | ||||

| 209 | ||||

| 209 | ||||

| F-1 |

You should rely only on the information contained in this prospectus or to which we have referred you. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the United States: Neither we nor Caesars Entertainment have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus outside of the United States.

Caesars Entertainment Corporation and its subsidiaries have certain proprietary rights to a number of trademarks used in this prospectus that are important to its business, including, without limitation, Caesars, Harrah’s, Horseshoe, Total Rewards and Planet Hollywood. Caesars Interactive Entertainment, Inc. has proprietary rights to the trademarks related to World Series of Poker. We have omitted the ® and ™ trademark designations for such trademarks named in this prospectus.

i

Table of Contents

The following summary contains information about Caesars Acquisition Company and its Class A common stock. It does not contain all of the information that may be important to you in making a decision to participate in the offering. For a more complete understanding of Caesars Acquisition Company, we urge you to read this prospectus carefully, including the sections entitled “Risk Factors,” “Cautionary Statements Concerning Forward Looking Statements” and “Where You Can Find Additional Information.” Unless otherwise noted or indicated by the context, (a) the terms “CAC,” “the Company,” “we,” “us” and “our” refer to Caesars Acquisition Company, (b) the term “CGP LLC” refers to Caesars Growth Partners, LLC and (c) the term “Growth Partners” refers to Caesars Growth Partners, LLC and its consolidated subsidiaries, in each case, after giving effect to the consummation of the Transactions described below under “—The Transactions.”

Caesars Acquisition Company

CAC is incorporated under the laws of Delaware and was formed to make an equity investment in Growth Partners, a joint venture between CAC and Caesars Entertainment, the world’s most diversified casino-entertainment provider and the most geographically diverse U.S. casino-entertainment company. CAC does not expect to own any other material assets or have any operations other than through its interest in CGP LLC. Upon consummation of the Transactions (as described below), CAC will serve as CGP LLC’s managing member and sole holder of all of its outstanding voting units, and Caesars Entertainment and/or certain of its subsidiaries will hold all of CGP LLC’s outstanding non-voting units. The voting units and non-voting units of CGP LLC participate ratably in distributions and are identical economically, other than as described under “Certain Relationships and Related Party Transactions—Limited Liability Company Agreement of CGP LLC—Liquidation Right” and “Certain Relationships and Related Party Transactions—Agreements with Caesars Entertainment and its Subsidiaries—Limited Liability Company Agreement of CGP LLC—Call Right.” Caesars Entertainment, through its subsidiaries, will own between an estimated 57% and 77% of the economic interests in CGP LLC, in each case, comprised of the value of the Contributed Assets (as defined below) and an additional 5%. The percentage owned will depend on the number of subscription rights exercised in the rights offering. This ownership range is also subject to adjustment at the closing of the Transactions due to the relative value of the Contributed Assets and certain other potential adjustments. See “—The Transactions.”

Growth Partners

Growth Partners is a casino asset and entertainment company focused on acquiring and developing a portfolio of high-growth operating assets and equity and debt investments in the gaming and interactive entertainment industry. Upon consummation of the Transactions, Caesars Entertainment and/or certain of its subsidiaries will own all of the outstanding non-voting units of CGP LLC and will be the majority economic shareholder of Growth Partners, and therefore will have a large direct stake in Growth Partners’ financial performance and growth potential. Through its relationship with Caesars Entertainment, Growth Partners has the ability to access Caesars Entertainment’s proven management expertise, brand equity, Total Rewards loyalty program and structural synergies. With 47 million members, the Total Rewards loyalty program is considered to be one of the leading loyalty rewards programs in the casino entertainment industry, as evidenced by Caesars Entertainment receiving COLLOQUY’s Master of Enterprise Loyalty Award in September 2012.

We anticipate the combination of Growth Partners’ flexible capital structure and Caesars Entertainment’s leading brands and management capabilities will provide a competitive advantage in the pursuit of high return, capital intensive investment opportunities in land-based, or “brick-and-mortar”, casino gaming, regulated online real-money gaming, and social and mobile games. Many development projects in the land-based casino and entertainment industries require lengthy and involved development and regulatory processes and therefore often

1

Table of Contents

require a significant initial capital outlay but have delayed cash flows generated from operations. Growth Partners’ capital structure is specifically designed to accommodate these dynamics, and we believe Growth Partners’ streamlined business model will create a unique venture-oriented investment vehicle for potential equity investors. In addition, social and mobile games industry characteristics and the speculative nature of online real money gaming in the United States are better served by a company with greater access to liquidity and equity capital. Therefore, the separation of this business from Caesars Entertainment’s core operating business and its leveraged capital structure will create a flexible organization that is well positioned to pursue business and growth strategies.

Through its two businesses—Interactive Entertainment and Casino Properties and Developments—Growth Partners will focus on acquiring or developing assets with strong value creation potential and leveraging interactive technology with well-known online brands. Growth Partners’ Interactive Entertainment business is expected to initially consist of Caesars Interactive Entertainment, Inc. and its subsidiaries (collectively referred to as “CIE” or “Caesars Interactive”), which has three businesses: social and mobile games, the World Series of Poker (“WSOP”) and regulated online real money gaming. Growth Partners’ Casino Properties and Developments business is expected to initially consist of Caesars Entertainment’s existing interests in the Planet Hollywood Resort and Casino located in Las Vegas, Nevada (“Planet Hollywood”), the casino to be developed by the Maryland Joint Venture (as defined below) in Baltimore, Maryland (the “Horseshoe Baltimore”), and a 50% interest in the management fee revenues to be received by certain subsidiaries of Caesars Entertainment Operating Company, Inc. (“CEOC”), a wholly-owned subsidiary of Caesars Entertainment, in connection with the management of Planet Hollywood and Horseshoe Baltimore. In addition, Growth Partners is expected to own a portfolio of debt investments consisting of notes previously issued by CEOC. These notes will provide Growth Partners with additional cash flow to fund future investment and acquisition opportunities.

When we consider new investment and acquisition opportunities, we will have to submit them to Caesars Entertainment. A committee of the board of directors of Caesars Entertainment comprised of disinterested directors will make the determination on behalf of Caesars Entertainment to (1) pursue any potential project itself or (2) decline the project for itself, after which Growth Partners may elect or decline to pursue the project. When Caesars Entertainment considers new investment and acquisition opportunities, Caesars Entertainment will have the option to (1) pursue any potential project itself or (2) decline the project for itself, after which Growth Partners may elect or decline to pursue the project. Although not required, we anticipate that any future investment and acquisition opportunities undertaken by Growth Partners will be managed by Caesars Entertainment and its subsidiaries. The CGP Operating Agreement (as described under “Certain Relationship and Related Party Transactions—Agreements with Caesars Entertainment its Subsidiaries”) will include a framework with respect to the structuring of compensation related to future projects between Caesars Entertainment and Growth Partners. In the event Caesars Entertainment declines an opportunity and Growth Partners undertakes the opportunity, Growth Partners will retain a 50% interest in the management fee to be received by Caesars Entertainment, unless otherwise agreed, and Growth Partners will acquire 100% of the new equity in such opportunity. With its equity-dominated capital structure and its relationship with Caesars Entertainment, we believe Growth Partners should be able to respond quickly to, and have access to required capital for, potential development opportunities. Because of its majority economic stake, Caesars Entertainment will have an incentive to bring opportunities to Growth Partners when Caesars Entertainment elects not to pursue such opportunities directly for itself.

Interactive Entertainment

By forming CIE, Caesars Entertainment recognized the importance of positioning itself for the convergence of interactive games, regulated online real money gaming and the “brick-and-mortar” casino-entertainment industry, while at the same time taking advantage of the synergies between them. CIE is a stand-alone company with an entrepreneurial culture that innovates upon the way brick-and-mortar gaming companies traditionally view and distribute casino entertainment.

2

Table of Contents

CIE has three distinct, but complementary, businesses that reinforce and build upon each other: social and mobile games, the World Series of Poker (“WSOP”), and regulated online real money gaming. It is the ecosystem created by the intersection of these three businesses, together with its relationship with Caesars Entertainment, including its rights to use Caesars Entertainment’s portfolio of brands and its access to the Total Rewards loyalty program, that we believe will allow CIE to capitalize on the growth of social and mobile casino-themed games and regulated online real money gaming, especially in the United States.

Social and Mobile Games. CIE has become one of the world’s leading interactive social and mobile casino-themed game providers. CIE’s current portfolio of games includes Slotomania, which was one of the top ten highest grossing casino-themed games on Facebook, Inc. (“Facebook”), iOS and Android platforms as of June 30, 2013 according to App Annie and www.facebook.com/appcenter. CIE’s launch of the Caesars Casino application on Facebook in January 2012 was the first visible instance of how CIE intends to leverage its relationship with Caesars Entertainment in the future. In December 2012, CIE acquired substantially all of the assets of Buffalo Studios LLC (“Buffalo Studios”), including the application Bingo Blitz, which is a leading bingo game on Facebook, Android and iOS. In May 2013, CIE acquired the World Series of Poker social and mobile game assets and intellectual property from Electronic Arts.

The World Series of Poker. CIE has derived considerable benefit from growing and building upon its ownership and management of the WSOP franchise. The WSOP, which was founded in 1970, had 79,471 entrants in its flagship annual tournament in Las Vegas in 2013 (the “WSOP Las Vegas”). The WSOP also benefits from a television contract with ESPN through 2017, sponsorship agreements with a number of leading brands, such as Miller Lite, Red Bull, Frito-Lay and Jacks Link’s in 2013. The WSOP also has licensing arrangements for a wide variety of consumer products including a licensing arrangement with Microsoft for a new Xbox game scheduled to launch in the United States in September 2013. CIE is positioning the WSOP brand to be one of the leading poker sites in Nevada, New Jersey and other states, if any, that legalize online real money gaming in the future.

Regulated Online Real Money Gaming. CIE has built the foundation of what it intends to be a leader in regulated U.S. online real money gaming environment. According to H2 Gaming Capital (“H2GC”), it is estimated that the regulated U.S. online real money poker market may generate up to approximately $9.6 billion in gross revenue annually. While online real money gaming has not been legalized at the federal level, in December 2011, Nevada approved interactive gaming regulations allowing for intrastate online poker and Delaware and New Jersey recently passed online real money gaming laws. The New Jersey legislation passed in February 2013 includes a provision for casino games such as slots, blackjack and roulette in addition to poker and allows only existing brick-and-mortar casino operators (or their affiliates) in the state to apply for a license to offer real money poker and casino games online to anyone within New Jersey state lines. CIE is actively participating in the U.S. lobbying effort for other states to follow Nevada, Delaware and New Jersey’s lead, and is supportive of a Federal framework as well. In December 2012, CIE received its operator’s license in Nevada and plans to launch in 2013 upon receipt of regulatory approval. Outside of the United States, CIE began offering real money online gaming in the United Kingdom (the “UK”) under the WSOP and Caesars brands in 2009 and entered the France and Italy markets through brand licensing agreements in 2011. In tandem with its lobbying efforts in the United States, CIE recently secured the use of two online real money poker software platforms for use in new markets: Fordart Limited’s (“888”) poker software through a licensing agreement and LB Poker SAS (“Barrière Poker”) through a source code assignment and co-development agreement. CIE believes that if online real money gaming continues to be legalized in the United States on either a state-by-state basis or on the federal level, it presents a substantial opportunity, translating into a potential large revenue generator for Growth Partners.

For the year ended December 31, 2012, our Interactive Entertainment segment generated net revenues of $207.7 million, net income of $34.1 million and Adjusted Segment EBITDA of $76.2 million. For the six months ended June 30, 2013, our Interactive Entertainment segment generated net revenues of $142.6 million, net loss of $15.3 million and Adjusted Segment EBITDA of $40.7 million. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Reconciliations of Adjusted Segment EBITDA of Net Income” for a discussion of Adjusted Segment EBITDA.

3

Table of Contents

Casino Properties and Developments

Growth Partners’ portfolio of casino-related assets consists of Planet Hollywood and an investment in a casino project under development in Baltimore, Maryland, the Horseshoe Baltimore. In addition, Growth Partners is entitled to a 50% interest in the management fee revenues received by certain subsidiaries of CEOC in connection with the management of Planet Hollywood and Horseshoe Baltimore. Planet Hollywood and the interests in the management agreements provide a base of cash flow to supplement Growth Partners’ ongoing development opportunities, including its investment in the Maryland Joint Venture.

Details of Growth Partners’ existing list of currently operating and development projects are shown in the table below.

| Property |

Location |

Status |

Ownership | Anticipated | ||||||

| Planet Hollywood Resort and Casino |

Las Vegas, NV | Operating | 100 | % | Open | |||||

| Horseshoe Baltimore |

Baltimore, MD | Under development |

52 | %(1) | Third quarter of 2014 | |||||

| (1) | Represents an indirect ownership in the Maryland Joint Venture through a 58.5% ownership in CR Baltimore Holdings LLC, the developer of the Maryland Joint Venture, which in turn has an 88.6% direct interest in the Maryland Joint Venture. Following the closing of the CVPR Sale described below, Growth Partners’ indirect economic ownership of the Maryland Joint Venture will be approximately 41%. |

For the year ended December 31, 2012, the Casino Properties and Developments segment generated net revenues of $303.7 million, net loss of $1.0 million and Adjusted Segment EBITDA of $69.1 million. For the six months ended June 30, 2013, the Casino Properties and Developments segment generated net revenues of $165.6 million, net income of $6.8 million and Adjusted Segment EBITDA of $44.1 million. The historical figures reflect that Planet Hollywood historically paid annual management fees of approximately $16.1 million to a subsidiary of CEOC pursuant to its management agreement and the Adjusted Segment EBITDA is calculated after giving effect to the payment of such management fees. As part of the Transactions, Growth Partners will pay $90.0 million for a 50% interest in the Planet Hollywood and Horseshoe Baltimore annual management fees. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Reconciliations of Adjusted Segment EBITDA to Net Income” for a discussion of Adjusted Segment EBITDA.

Planet Hollywood Resort & Casino

Planet Hollywood, which was originally constructed in 2001 and renovated in 2007, is a casino resort located on the Las Vegas Strip in Las Vegas, Nevada. Planet Hollywood was acquired by Caesars Entertainment in February 2010 and is managed by a subsidiary of CEOC and therefore benefits from Total Rewards, one of the leading loyalty rewards programs in the casino entertainment industry. Planet Hollywood benefits from its prime location on a 35-acre site on the east side of the Las Vegas Strip and is part of a contiguous strip of casinos owned by Caesars Entertainment, with which it shares certain services and costs.

Planet Hollywood includes a 2,500-room hotel, which offers deluxe guestrooms and suites. The facility also has an outdoor pool area and an approximately 32,000-square foot spa that is leased to a third party. In addition, the facility adjoins to a retail mall, the Miracle Mile Shops, with 170 retailers and 15 restaurants, and a 1,201 room timeshare tower operated by Hilton Grand Vacations. The adjoining mall and timeshare tower, as well as the additional amenities featured at Planet Hollywood, stimulate additional traffic through the Planet Hollywood complex, including the casino and its amenities. For a description of amenities featured at Planet Hollywood, see “Business—Growth Partners—Casino Properties and Developments—Planet Hollywood Resort & Casino.”

4

Table of Contents

Planet Hollywood’s 64,500 square foot casino features 1,100 slot machines and 79 table games. The casino offers a diverse selection of the most popular slot and video poker machines in a wide variety of denominations, and is also home to a race-and-sports-books facility. The casino’s live table games include traditional blackjack, craps and roulette, in addition to a variety of other popular games, such as Baccarat and Pai Gow Poker. Planet Hollywood’s casino also offers daily poker tournaments in an 11 table World Series of Poker-branded poker room, as well as a variety of live poker games including Texas Hold ‘Em and other casino poker games.

Planet Hollywood complements this product offering with both a high limit table game area featuring 9 high limit table games as well as a high limit slot area featuring over 60 high denomination slot machines. Additional amenities, such as an exclusive enclosed lounge and VIP cage access, target the needs of its VIP customer base. Planet Hollywood also features amenities such as ten food and beverage outlets, gift and merchandise shops operated by the Marshall Retail Group, over 80,000 square feet of convention, trade show and meeting facilities and a 7,000-seat theater known as PH Live.

Planet Hollywood targets a growing younger demographic segment that values the offerings of the non-gaming entertainment that complements the casino’s gaming activities. Growth Partners’ flexible capital structure will allow it to invest in Planet Hollywood and elevate its guests’ experience by offering premium, Hollywood-themed entertainment and non-gaming options that remain fresh and relevant. We believe these investments should lead to revenue and EBITDA growth.

Horseshoe Baltimore, Maryland

Growth Partners owns an indirect interest in CBAC Gaming, LLC (the “Maryland Joint Venture”), a joint venture with an affiliate of Rock Gaming LLC and other local investors. CBAC Borrower, LLC, a subsidiary of the Maryland Joint Venture (“CBAC Borrower”), holds a license to operate a casino in the City of Baltimore.

Caesars Entertainment is leading the development of the casino, and a subsidiary of CEOC will serve as the manager of Horseshoe Baltimore. After consummation of the Transactions, Growth Partners will receive a 50% interest in the management fee revenue received by a subsidiary of CEOC in connection with the management of Horseshoe Baltimore. The property is anticipated to be an integrated casino with a 110,000 square-foot floor holding approximately 2,500 video lottery terminals (“VLTs”), 100 table games and 30 poker tables. In addition to the gaming space, Growth Partners anticipates the casino facility at Horseshoe Baltimore will contain a 10,000 square foot meeting facility, seven restaurants and/or bars, and a Diamond Lounge for its highest-value gaming customers. The Maryland Joint Venture will also develop an adjacent 3,400-space parking garage, which will facilitate ease of access to the casino for its customers. The project is anticipated to open in the third quarter of 2014 at a cost of approximately $400 million. The Maryland Joint Venture is funded with approximately $107.5 million of total equity and approximately $340 million in debt. Growth Partners’ share of the equity contribution and of the ownership will be approximately 52%. Growth Partners, together with another member of the Maryland Joint Venture, have an agreement in principle to sell approximately 18% of the equity interest in the Maryland Joint Venture to CVPR Gaming Holdings, LLC, an existing third member of the Maryland Joint Venture (the “CVPR Sale”). The CVPR Sale is subject to regulatory approval. Following the closing of the CVPR Sale, Growth Partners’ equity contribution and indirect ownership in the Maryland Joint Venture will be approximately 41%, through its continued 58.5% indirect ownership in CR Baltimore Holdings LLC, which after the sale will own approximately 70% of the Maryland Joint Venture.

As of the date of this prospectus, Caesars Entertainment has contributed $55.7 million of cash equity in the Maryland Joint Venture and may have to contribute up to an additional $22.3 million of capital contributions under the terms of Maryland Joint Venture’s operating agreement. Growth Partners will assume all of Caesars Entertainment’s uncalled capital commitments. On July 2, 2013, CBAC Borrower obtained a credit facility (the “Baltimore Credit Facility”) that provides for up to $310 million of project financing for the development of Horseshoe Baltimore. Concurrently with the closing of the Baltimore Credit Facility, CBAC Borrower also

5

Table of Contents

entered into a term loan facility that provides for up to $30 million of equipment financing (the “Baltimore FF&E Facility”). See “Description of Indebtedness” for descriptions of the Baltimore Credit Facility and the Baltimore FF&E Facility.

The Maryland Joint Venture represents a unique opportunity to enter a major market with favorable demographics. The casinos in Maryland draw customers primarily from the Washington D.C. Metropolitan Statistical Area (“MSA”), which encompasses Washington D.C. and portions of Maryland, Virginia and West Virginia, and it is the eighth largest MSA in the United States with over 5.5 million residents. The Washington D.C. MSA has more adults per gaming position than the average of eight comparable regional gaming markets, including Cincinnati, Pittsburgh and Philadelphia, indicating that the gaming market in Maryland can support additional casinos. In addition, the Washington D.C. MSA has favorable demographics, with a median income of $83,080 and average income of $106,509 compared to a national average of $42,494 and $55,999 respectively. For additional information, see “Industry—Maryland.”

In 2008, the Maryland General Assembly passed enabling legislation that limited gaming to five VLT facilities in predetermined geographic areas at a 67% gaming tax rate. See “Business—Growth Partners—Casino Properties and Developments—Horseshoe Baltimore, Maryland.” The Maryland Joint Venture was conditionally awarded a license in July 2012 and all conditions were removed in June 2013, provided that issuance of the license remains subject to completion and opening of the project to the general public and receipt of approvals from gaming authorities regarding the operations of the casino prior to its opening. In connection with the Baltimore Credit Facility, the Maryland Joint Venture transferred its license to CBAC Borrower, its wholly-owned subsidiary and the borrower under the Baltimore Credit Facility and the Baltimore FF&E Facility. A lawsuit has been filed challenging certain aspects of the project. See “Risk Factors—Risks Related to Growth Partners’ Casino Properties and Developments Business—Adverse outcomes in legal proceedings could adversely affect the Horseshoe Baltimore Casino, including a delay in construction and ultimately the opening of the casino and possible abandonment of the project.” For further discussion, see “Business—Growth Partners—Casino Properties and Developments—Horseshoe Baltimore, Maryland.”

CEOC Notes

Upon consummation of the Transactions, Growth Partners will own approximately $1.1 billion of aggregate principal amount of senior notes previously issued by CEOC (the “CEOC Notes”). The CEOC Notes have fixed interest rates ranging from 5.625% to 10.75% and maturities ranging from 2015 to 2018. For additional information with respect to the CEOC Notes, see “Business—Casino Properties and Development—CEOC Notes.”

Competitive Strengths

We anticipate that CAC and Growth Partners will have significant competitive advantages that differentiate them from their competition:

Opportunity for investors to get access to a growth-oriented gaming investment vehicle that is supported by Caesars Entertainment. We will be a growth-oriented company whose business is focused entirely on owning operating assets, equity and debt investments in the gaming and interactive entertainment industry. Investors will benefit from Caesars Entertainment’s scale and market leading position, in combination with its proprietary marketing technology and consumer loyalty programs, which will help Growth Partners’ businesses achieve operational efficiencies and support future growth opportunities.

Simple capital structure and access to liquidity provide ability to support growth projects in new and expanding markets. Growth Partners has a simple and flexible capital structure because (i) many of its assets are unencumbered, such as CIE’s assets, (ii) its casino properties and development projects that are encumbered,

6

Table of Contents

such as Planet Hollywood and Horseshoe Baltimore, solely have property or project level financing without any guarantees from other subsidiaries of Growth Partners and (iii) the lack of leverage, generally, on its assets. Growth Partners’ simple and flexible capital structure provides it with the ability to invest in new casino projects in new and expanding markets quickly without the constraints of a more complex or levered capital structure. We believe that Growth Partners’ capital structure will provide greater access to the equity and debt markets for additional liquidity, which will position Growth Partners to capitalize on new growth opportunities. In addition, Growth Partners owns a portfolio of debt investments, from which it will receive meaningful current cash flows.

Potential access to future growth opportunities through the relationship with Caesars Entertainment. In connection with the Transactions, Growth Partners will enter into the CGP Operating Agreement with CAC and Caesars Entertainment and/or its subsidiaries, which will provide Growth Partners the ability to participate in new investment and acquisition opportunities developed by Caesars Entertainment, at the sole option of Caesars Entertainment to be determined by a committee of the board of directors of Caesars Entertainment comprised of disinterested directors. We believe that Caesars Entertainment’s brand portfolio and recognition, coupled with the power of the Total Rewards loyalty program, uniquely positions Caesars Entertainment to identify opportunistic acquisitions and developments. See “—Growth Partners” above for discussions of the arrangement among Caesars Entertainment and Growth Partners for identifying and considering new investment and acquisition opportunities.

Capitalize upon regulated online real money gaming in the United States by growing infrastructure and strategic relationships. CIE is currently operating its real money WSOP and Caesars-branded poker, bingo and casino online sites in the UK and has brand licensing agreements in Italy and France. Through these pursuits, CIE has developed meaningful strategic relationships with companies that have international experience in online real money gaming. As a result of its strategic partnership in the UK, CIE has an agreement with 888 to provide technology services for its real money gaming offerings in Nevada and New Jersey. Similarly, CIE has had an ongoing relationship with Groupe Lucien Barriere and Barriere Poker through WSOP Europe since 2011. Both relationships help to further increase CIE’s knowledge for building regulated online real money gaming operations in the United States.

Access to leading casino brands and a global network of casinos and the Total Rewards loyalty program. As of June 30, 2013, Caesars Entertainment owned, operated and managed 52 casinos that bear many of the most recognized brand names in the gaming industry. Planet Hollywood’s close proximity to other casino properties of, and operated by, Caesars Entertainment allows it to leverage the Caesars brands to attract customers to its casino and resort. Additionally, Planet Hollywood, Horseshoe Baltimore and CIE have or will have access to the Total Rewards loyalty program. We expect that any future development projects of Growth Partners will have access to the Total Rewards loyalty program. The Total Rewards loyalty program is considered to be one of the leading loyalty rewards programs in the casino entertainment industry. We believe that the Total Rewards loyalty program, along with other marketing tools, provide Planet Hollywood, Horseshoe Baltimore and CIE with a significant competitive advantage that enables them to efficiently market their products to a large and recurring customer base.

Highly scalable social and mobile games business model with rapid revenue growth and profitability. CIE’s revenue and profitability have grown rapidly and significantly. As CIE continues to leverage its existing franchises (including Slotomania, Bingo Blitz, World Series of Poker and Caesars Casino) and development pipeline, we anticipate that CIE’s revenue growth and EBITDA will accelerate due to its ability to utilize its live service game and development teams, which are largely based in low-cost production centers, and the design of CIE’s existing games, which generally require little modification across platforms.

Experienced senior management team in the social and mobile games, regulated online real money gaming and traditional land-based casino industries. The extensive experience of CIE’s senior management team positions CIE to take advantage of opportunities in the social and mobile games and regulated online real

7

Table of Contents

money gaming markets and to continue to develop the infrastructure needed to support online real money gaming as it becomes legalized and regulated in the United States. Mitch Garber, CEO of CAC and CIE, has worked in the gaming and interactive entertainment industry for over 20 years and most recently was CEO of PartyGaming plc (now bwin.party digital entertainment plc (“bwin.party”)), one of the largest online real money gaming companies in the world.

Planet Hollywood is, Horseshoe Baltimore will be, and we expect Growth Partners’ other land-based casinos will be, managed by subsidiaries of Caesars Entertainment, which has a senior management team, led by CEO Gary W. Loveman, with substantial experience and a proven track record.

Well-known, large casino entertainment facility on the Las Vegas Strip generating significant revenue and operating income. We believe the location of Planet Hollywood offers distinct advantages. Planet Hollywood is located on a 35-acre site on the east side of the Las Vegas Strip and sits among a contiguous strip of casinos owned by Caesars Entertainment. We believe Planet Hollywood’s prime location, adjoining facilities and accessibility enables it to attract a significant customer base and continue to capture growth in market share. For the year ended December 31, 2012, the Casino Properties and Developments segment generated net revenues of $303.7 million, net loss of $1.0 million and Adjusted Segment EBITDA of $69.1 million. For the six months ended June 30, 2013, the Casino Properties and Developments segment generated net revenues of $165.6 million, net income of $6.8 million and Adjusted Segment EBITDA of $44.1 million.

Ownership in development project in highly attractive new market. Growth Partners owns an interest in the Maryland Joint Venture, a high-potential conditionally licensed development project in Baltimore, Maryland. The Maryland Joint Venture represents a unique opportunity for Growth Partners to enter a new gaming market with attractive growth prospects. See “Business—Casino Properties and Developments—Horseshoe Baltimore, Maryland” for an overview of the gaming legislation passed by the Maryland General Assembly and the Maryland gaming market.

Business Strategy

Pursue opportunistic investment in development projects. We expect that Growth Partners’ simple and flexible capital structure will provide access to liquidity and low-cost of capital which will position Growth Partners to benefit from potential growth opportunities that may not be available to Caesars Entertainment or other “brick-and-mortar” casino gaming companies. As new markets become accessible across the United States and internationally, Growth Partners will deploy its capital to establish an initial foothold to gain and maintain an advantage in such markets as Growth Partners is doing in Maryland. Due to its complementary investment objectives and relationship with Caesars Entertainment, Growth Partners can also benefit from access to additional opportunities if Caesars Entertainment decides these opportunities are better suited for Growth Partners and declines to pursue the opportunity.

Develop, construct and successfully open the casino to be operated by the Maryland Joint Venture. Growth Partners intends to devote capital and resources, including its relationship with Caesars Entertainment, to the successful development and construction of Horseshoe Baltimore.

Continue to create and distribute compelling social and mobile casino-themed games to increase domestic and international presence. CIE’s management, as well as its creative and technical teams, appreciate that CIE’s core competency is casino-themed entertainment. In a short period of time, CIE has gained recognition in the online industry for its ability to create sophisticated and commercially successful social and mobile games, such as Slotomania. In January 2012, Caesars Casino was launched on Facebook and based on its success CIE plans to launch Caesars Slots on mobile platforms in the third quarter 2013. In December 2012, CIE acquired substantially all of the assets of Buffalo Studios, including the application Bingo Blitz, which is among the

8

Table of Contents

leading bingo games on Facebook, iOS and Android. In May 2013, CIE acquired the World Series of Poker social and mobile game assets and intellectual property from Electronic Arts. CIE regularly updates its games to encourage social interactions and add new content and features that encourage players to continue playing its games. In addition, CIE expects to continue to successfully leverage various technologies and standardized processes that are designed to enable rapid, timely, high-quality and cost-effective development of social and mobile games.

Ensure that CIE is well positioned to succeed in a regulated U.S. online real money gaming environment. CIE’s access to the globally recognized Caesars and WSOP brands and CIE’s dedicated online gaming management team position it to take advantage of opportunities in the U.S. and global online real money gaming markets and to continue to develop the infrastructure needed to launch in Nevada and New Jersey and additional states, if any, as they legalize online real money game. CIE will continue to use its online real money WSOP and Caesars-branded poker, bingo and casino online sites in the UK, its alliances with online gaming providers in Italy and France, and its relationships with 888 and Barrière Poker to further increase its knowledge for building its regulated online real money gaming operations in the U.S.

Capitalize on relationship with Caesars Entertainment. Growth Partners’ access to the industry-leading Total Rewards loyalty program, which includes over 47 million members as of June 30, 2013, improves the ability of its businesses to cross market and cross promote with Caesars Entertainment’s database and many of its casinos. This relationship will allow Planet Hollywood to utilize Caesars Entertainment’s sophisticated customer database and technology systems to efficiently and effectively manage its existing customer relationships. In addition, we believe CIE has a significant competitive advantage over its competitors due to CIE’s cross-marketing and trademark license agreement with Caesars Entertainment that allows CIE to distribute Caesars Entertainment’s brands online.

The Sponsors

Immediately upon the completion of this offering but prior to granting the Sponsor CAC Proxy, affiliates of the Sponsors will beneficially own at least approximately 42% of our outstanding Class A common stock (assuming that the subscription rights are exercised in full without the exercise of any over-subscription privilege by affiliates of the Sponsors). In addition, approximately % of our Class A common stock (assuming the subscription rights are exercised in full by all holders of subscription rights) will be subject to the Sponsor CAC Proxy that gives Hamlet Holdings, an entity comprised of six persons that are leaders at the respective Sponsor, sole voting and dispositive power with respect to those shares of Class A common stock. Moreover, four of the seven directors of CAC are individuals affiliated with the Sponsors.

Apollo

Founded in 1990, Apollo is a leading global alternative investment manager with offices in New York, Los Angeles, Houston, London, Frankfurt, Luxembourg, Singapore, Hong Kong and Mumbai. As of June 30, 2013, Apollo had assets under management of approximately $113 billion in its private equity, credit and real estate businesses.

TPG

TPG is a leading global private investment firm founded in 1992 with approximately $56.7 billion of assets under management as of March 31, 2013 and offices in San Francisco, Fort Worth, Austin, Beijing, Chongqing, Hong Kong, London, Luxembourg, Melbourne, Moscow, Mumbai, New York, Paris, São Paulo, Shanghai, Singapore and Tokyo. TPG has extensive experience with global public and private investments executed through leveraged buyouts, recapitalizations, spinouts, growth investments, joint ventures and restructurings.

9

Table of Contents

Relationship with Caesars Entertainment

In connection with the Transactions, CAC and Growth Partners will enter into a management services agreement with CEOC (the “CGP Management Services Agreement”), pursuant to which CEOC and certain of its subsidiaries will, at the request of CAC or Growth Partners, respectively, provide services, including certain corporate services and back-office support and business advisory services, allowing CAC and Growth Partners to leverage Caesars Entertainment’s brands and infrastructure. See “Certain Relationships and Related Party Transactions—Agreements with Caesars Entertainment and its Subsidiaries—CGP Management Services Agreement” for additional details on the CGP Management Services Agreement. In addition, pursuant to the organizational documents of CAC and Growth Partners, Caesars Entertainment and/or certain of its subsidiaries will have certain rights including a call right for all or a portion of the issued and outstanding voting units of Growth Partners (or, at our election, shares of CAC’s Class A common stock) and a right of first offer for new business opportunities and for any contemplated asset sale by Growth Partners. See “Certain Relationships and Related Party Transactions—Agreements with Caesars Entertainment and its Subsidiaries—Limited Liability Company Agreement of CGP LLC” and “Description of Capital Stock” for details on the call rights. Growth Partners may only proceed with a new business opportunity if the disinterested members of Caesars Entertainment’s board of directors decline the opportunity for itself or CEOC and if Caesars Entertainment decides not to pursue and take such opportunity to a third party. See “Certain Relationships and Related Party Transactions.”

In exchange for the provision of the services under the CGP Management Services Agreement, CAC and/or Growth Partners will pay a service fee in an amount equal to the fully allocated cost of such services plus a margin of % per annum. In addition, as partial consideration for the services provided under the CGP Management Services Agreement, Growth Partners will deliver $ aggregate amount of CAC’s Class A common stock (contributed to it by CAC) to CEOC, which CEOC and its subsidiaries may allocate to their employees and consultants in their discretion.

Caesars Entertainment is the world’s most diversified casino-entertainment provider and the most geographically diverse U.S. casino-entertainment company. As of June 30, 2013, Caesars Entertainment owned, operated and managed, through various subsidiaries, 52 casinos in 13 U.S. states and six countries. The majority of these casinos operate in the United States and England and Caesars Entertainment uses the Total Rewards loyalty program to market promotions and to generate customer play across its network of properties in North America. As of the date hereof, approximately 70% of Caesars Entertainment’s common stock is beneficially owned by Hamlet Holdings.

The Transactions

CAC and Growth Partners were recently formed in connection with a number of transactions described below, including this offering, pursuant to which CAC, through its investment in Growth Partners, will acquire control of certain assets contributed by or purchased from subsidiaries of Caesars Entertainment and establish a number of service, management and other relationships between Growth Partners and Caesars Entertainment. See “Questions and Answers About the Company and the Rights Offering—Why is Caesars Entertainment conducting the rights offering?”

In connection with the distribution of the subscription rights, affiliates of the Sponsors have advised Caesars Entertainment that they intend to exercise subscription rights of at least $500.0 million, though they have not entered into any agreement to do so. Consummation of the Transactions is contingent on the exercise of subscription rights of at least $500.0 million by affiliates of the Sponsors. CAC will use the proceeds from this offering to acquire all of the voting interests in Growth Partners. Caesars Entertainment will contribute all of the

10

Table of Contents

shares of CIE’s outstanding common stock held by a subsidiary of Caesars Entertainment and approximately $1.1 billion in aggregate principal amount of the CEOC Notes that are owned by another subsidiary of Caesars Entertainment to Growth Partners in exchange for non-voting units, the quantum of which will be based on the combined ascribed value of $1.275 billion, subject to certain potential value-related adjustments at the closing of the Transactions. Of the $1.275 billion of combined ascribed value, $525 million is attributable to CIE (before the valuation adjustments discussed below) and approximately $750 million is attributable to the CEOC Notes, subject to adjustment as further described below. The value of the CEOC Notes was determined as of April 3, 2013 and reflects the 90-day average market trading value of the bonds with a liquidity discount and a discount for assumed transaction fees and expenses. Growth Partners will own approximately 90.2% of the outstanding shares of CIE’s common stock, which may be reduced to approximately 84.5% upon conversion of the $47.7 million convertible promissory note issued by CIE to Rock Gaming Interactive LLC (“Rock Gaming”) (subject to required regulatory approval), in each case not giving effect to any options or warrants that are exercisable. Assuming Rock Gaming exercises the convertible promissory note and after giving effect to other options, restricted stock and warrants that are exercisable, Growth Partners will own approximately 76% of CIE on a fully-diluted basis. See note 10 to the audited combined financial statements of Growth Partners included elsewhere in this prospectus for a description of the convertible notes issued to Rock Gaming. We refer to these transactions as the “Contribution Transaction” and these assets as the “Contributed Assets.” As a result of these asset contributions, Caesars Entertainment, through its subsidiaries, will own between an estimated 57% and 77% of the economic interests in CGP LLC, in each case, comprised of the value of the Contributed Assets and an additional 5%. The percentage owned will depend on the number of subscription rights exercised in the rights offering. This ownership range is also subject to adjustment at the closing of the Transactions due to the relative value of the contributed assets and certain other potential adjustments.

This agreed valuation is subject to potential increase by up to $225.0 million based on earnings from CIE’s social and mobile games business exceeding a specified amount in 2015, which would be conveyed to Caesars Entertainment or its subsidiaries in the form of additional non-voting units of CGP LLC or Class B common stock of CAC. If prior to the date that is nine months after the closing of the Transactions, Growth Partners sells or agrees to sell all of its interests in CIE (or any of its component parts) to any third party other than Caesars Entertainment, then Caesars Entertainment will receive concurrent with the closing of such sale, that number of additional non-voting units of CAC that would have been issued to Caesars Entertainment if the value of CIE (or any of its component parts) at the time of contribution to Growth Partners were increased by the difference between such third party sale price and the applicable valuation price of $525 million as it relates to CIE (or any of its component parts).

Additionally, Growth Partners intends to use $360.0 million of proceeds received from CAC to purchase from subsidiaries of Caesars Entertainment (i) Planet Hollywood, (ii) Caesars Entertainment’s joint venture interests in the Horseshoe Baltimore and (iii) a 50% interest in the management fee revenues for both of those properties. Of the $360.0 million proceeds to be used for the purchase, $280.0 million is attributable to the purchase of Planet Hollywood and the 50% interest in the management fee revenue for Planet Hollywood and the remaining $80.0 million is attributable to the purchase of Caesars Entertainment’s joint venture interests in the Horseshoe Baltimore and the 50% interest in the management fee revenue for the Horseshoe Baltimore. The purchase price for these assets is subject to adjustment based on Caesars Entertainment’s equity contribution to the Maryland Joint Venture prior to the closing of the offering. We refer to these transactions as the “Purchase Transaction” and these assets as the “Purchased Assets.” A subsidiary of Growth Partners will assume the $513.2 million of outstanding secured term loan related to Planet Hollywood (the “PHW Loan”) in connection with the Purchase Transaction. The purchase of Planet Hollywood and the assumption of the PHW Loan by Growth Partners are subject to the receipt of approval of lenders of the PHW Loan and any requirements the lenders may impose.

11

Table of Contents

The Transactions will include certain value-related adjustments at closing, as follows.

| • | Value of the CEOC Notes. The actual value of the CEOC Notes will be recalculated on the closing date of the Transactions using the 90 day trading average closing price for each tranche of the CEOC Notes for the period ended on the closing date of the Contribution Transaction, net of certain costs, commissions and discounts. The ownership percentages of Caesars Entertainment and CAC in CGP LLC will be recalculated accordingly. |

| • | Return of the aggregate value of the rights. The aggregate value (the “rights value”), if any, of the CAC subscription rights that are distributed by Caesars Entertainment will be restored to Caesars Entertainment by CGP LLC in the form of CEOC Notes with equivalent value to the rights value. The rights value shall be determined by an independent third-party valuation firm, which shall deliver an opinion immediately prior to the distribution of the subscription rights by Caesars Entertainment. |

After the third anniversary of the closing of the Transactions, Caesars Entertainment will have the right, which it may assign to any of its affiliates or to any transferee of all non-voting units of CGP LLC held by Caesars Entertainment, to acquire all or a portion of the voting units of CGP LLC (or, at our option, shares of CAC’s Class A common stock) not otherwise owned by Caesars Entertainment and/or its subsidiaries at such time. On the eighth year and six month anniversary of the closing of the Transactions (unless otherwise agreed by Caesars Entertainment and CAC), if the board of directors of CAC has not previously exercised its liquidation right, Growth Partners shall, and the board of directors of CAC shall cause Growth Partners to, effect a liquidation. See “Certain Relationships and Related Party Transactions—Agreements with Caesars Entertainment and its Subsidiaries—Limited Liability Company Agreement of CGP LLC” and “Description of Capital Stock” for details on the call rights and liquidation rights. In addition, see “Risk Factors—Risks Related to Our Class A Common Stock— Caesars Entertainment’s call right on our Class A common stock may result in you being forced to sell our Class A common stock at a disadvantageous time and will cause you to own stock of Caesars Entertainment. This call right may not occur at all due to the discretion of Caesars Entertainment or the inability of Caesars Entertainment to achieve sufficient liquidity to exercise such right” and “Growth Partners will be required to be liquidated in eight years and six months, which may result in you receiving less than the full value of your Class A common stock” for a discussion of certain risks related to the call right and liquidation right.

In connection with the Purchase Transaction and the Contribution Transaction, CAC and Growth Partners will enter into agreements with CEOC and its subsidiaries to provide certain corporate services and back-office support and business advisory services to CAC, Growth Partners and their subsidiaries. See “Certain Relationships and Related Party Transactions.” We refer to the Purchase Transaction, Contribution Transaction and the entering into such agreements collectively as the “Transactions.”

Closing

At the election of the Sponsors, in lieu of a single closing, the Transactions and the rights offering may close in multiple stages. Upon the receipt of the required regulatory approvals, (i) Caesars Entertainment will distribute the subscription rights to its stockholders as of the record date, (ii) CAC, Growth Partners and Caesars Entertainment and its subsidiaries will consummate the Contribution Transaction and (iii) affiliates of the Sponsors will use $500.0 million (the “Sponsor Commitment”) to purchase CAC’s Class A common stock at a price of $9.43 per whole share and CAC will use such proceeds to acquire voting units of CGP LLC. We refer to the foregoing steps as the “Initial Closing.” In connection with the Initial Closing, affiliates of the Sponsors will agree not to exercise their subscription rights upon expiration of the rights offering; provided, that affiliates of the Sponsors will be eligible to exercise their over-subscription privileges, if any.

On or after the Initial Closing, Growth Partners will use the proceeds to consummate the Purchase Transaction, subject to receipt of lenders’ approval (and any requirements the lenders may impose) and regulatory approval with respect to the purchase of Caesars Entertainment’s joint venture interests in Horseshoe

12

Table of Contents

Baltimore. Prior to the consummation of the Purchase Transaction and the rights offering, Growth Partners will hold the proceeds from the Sponsor Commitment in escrow and will not otherwise invest or deploy such proceeds.

Upon expiration of the rights offering, holders of the subscription rights (other than affiliates of the Sponsors) may exercise their subscription rights to purchase CAC’s Class A common stock at a price of $9.43 per whole share. CAC will use the proceeds from the participating holders to acquire additional voting units of CGP LLC.

Organizational Structure

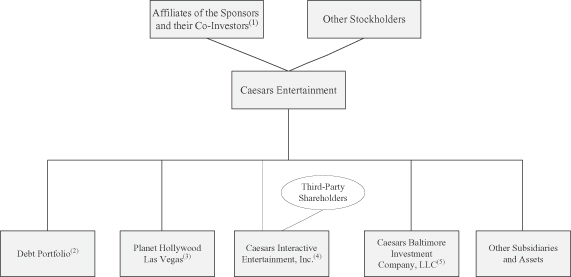

The chart below depicts the organizational structure of Caesars Entertainment and related entities prior to the Transactions:

| (1) | All shares held by funds affiliated with and controlled by the Sponsors and their co-investors, representing approximately 70% of Caesars Entertainment’s outstanding common stock, are subject to an irrevocable proxy that gives Hamlet Holdings, the members of which are comprised of three individuals affiliated with Apollo and two individuals affiliated with TPG, sole voting and sole dispositive power with respect to such shares. |

| (2) | Consists of approximately $1.1 billion in aggregate principal amount of the CEOC Notes held by Harrah’s BC, Inc. |

| (3) | Consists of the equity interests of PHW Las Vegas, LLC, which holds all of the assets and liabilities of Planet Hollywood, and PHW Manager, LLC, which manages Planet Hollywood. As of June 30, 2013, Planet Hollywood had a $513.2 million principal balance outstanding under the PHW Loan. |

| (4) | Consists of 90.2% of the outstanding shares of CIE’s common stock, which would be reduced to approximately 84.5% of the outstanding shares of CIE’s common stock upon conversion by Rock Gaming of the convertible promissory note issued by CIE, in each case not giving effect to any options or warrants that are exercisable. As of June 30, 2013, CIE had $39.8 million of loans outstanding under its revolving credit facility with Caesars Entertainment. |

| (5) | Owns approximately 58% equity interest in an entity that holds approximately 88% of the equity interests in CBAC Gaming, LLC equating to an effective 52% ownership of CBAC Gaming, LLC. Also holds all of the interest in the management fee revenue to be received by a subsidiary of CEOC in connection with the management of Horseshoe Baltimore. |

13

Table of Contents

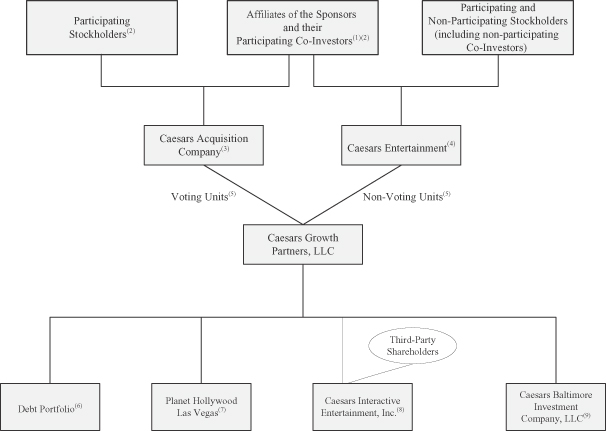

The chart below depicts our organizational structure following the consummation of this offering.

| (1) | All shares held by funds affiliated with and controlled by the Sponsors and their participating co-investors, representing % of CAC’s outstanding common stock (assuming the subscription rights are exercised in full by all holders of subscription rights), will be subject to an irrevocable proxy that gives Hamlet Holdings, the members of which are comprised of three individuals affiliated with Apollo and two individuals affiliated with TPG, sole voting and sole dispositive power with respect to such shares. As a result of the exercise of the subscription rights, and the applicability of the irrevocable proxy, Hamlet Holdings will control a majority of CAC’s outstanding common stock. |

| (2) | Shares held by certain participating stockholders (other than affiliates of the Sponsors and their participating co-investors), representing % of CAC’s outstanding Class A common stock (assuming the subscription rights are exercised in full by all holders of subscription rights), will be eligible for resale upon effectiveness of the registration statement of which this prospectus forms a part and will be listed on the NASDAQ Global Select Market following this offering if we meet the NASDAQ Global Select Market listing requirements. |

| (3) | CAC will own % of the total outstanding equity units in CGP LLC assuming the subscription rights are exercised in full by all holders of subscription rights. |

| (4) | Caesars Entertainment, through two of its subsidiaries, HIE Holdings, Inc. and Harrah’s BC, Inc., collectively own 100% of CGP LLC’s outstanding non-voting units, representing % of the economic interests in Growth Partners (assuming the subscription rights are exercised in full by all holders of subscription rights). |

| (5) | All holders of CGP LLC’s equity units will be entitled to share equally in distributions, subject to the distribution waterfall in connection with a liquidation, partial liquidation or sale of material assets and the call right held by Caesars Entertainment and/or its subsidiaries as further described under “Certain |

14

Table of Contents

| Relationships and Related Party Transactions—Agreements with Caesars Entertainment and its Subsidiaries—Limited Liability Company Agreement of CGP LLC”. |

| (6) | Consists of approximately $1.1 billion in aggregate principal amount of the CEOC Notes. |

| (7) | Consists of the equity interests of a subsidiary of PHW Las Vegas, LLC, which will hold all of the assets and liabilities of PHW Las Vegas, LLC, including Planet Hollywood, and a 50% interest in the management fee revenue received by PHW Manager, LLC in connection with the management of Planet Hollywood. As of June 30, 2013, Planet Hollywood had a $513.2 million principal balance outstanding under the PHW Loan. |

| (8) | Consists of 90.2% of the outstanding shares of CIE’s common stock, which would be reduced to approximately 84.5% of the outstanding shares of CIE’s common stock upon conversion by Rock Gaming of the convertible promissory note issued by CIE, in each case not giving effect to any options or warrants that are exercisable. As of June 30, 2013, CIE had $39.8 million of loans outstanding under its revolving credit facility with Caesars Entertainment. |

| (9) | Owns approximately 58% equity interest in an entity that holds approximately 88% of the equity interests in CBAC Gaming, LLC equating to an effective 52% ownership of CBAC Gaming, LLC. Following the CVPR Sale, Growth Partners’ indirect ownership in CBAC Gaming, LLC will be approximately 41%. Also owns a 50% interest in the management fee revenue to be received by a subsidiary of CEOC in connection with the management of Horseshoe Baltimore. On July 2, 2013, CBAC Borrower, a subsidiary of CBAC Gaming, LLC, obtained the Baltimore Credit Facility that provides up to $310 million of project financing for the development of Horseshoe Baltimore and the Baltimore FF&E Facility that provides up to $30 million of equipment financing. As of July 2, 2013, $225.0 million of term B loans were funded and outstanding under the Baltimore Credit Facility. |

Additional Information

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) because our total gross revenue was less than $1.0 billion for the fiscal year ended December 31, 2012, our most recently completed fiscal year. For further information on the implications of this distinction, see “Risk Factors—Risks Related to the Rights Offering.” Moreover, upon the closing of this offering, we will be a “controlled company” within the meaning of NASDAQ corporate governance standards because more than 50% of our voting common stock will continue to be beneficially owned by Hamlet Holdings after the granting of the Sponsor CAC Proxy. For further information on the implications of this distinction, see “Risk Factors—Risks Related to the Rights Offering” and “Management—Committees of Our Board of Directors.”

Our principal executive offices are located at One Caesars Palace Drive, Las Vegas, NV 89109, and our telephone number is (702) 407-6000. The address of our Internet site is . This Internet address is provided for informational purposes only and is not intended to function as a hyperlink. Accordingly, no information contained in this Internet address is included or incorporated by reference herein.

15

Table of Contents

The Rights Offering

The following summary describes the principal terms of the rights offering, but it is not intended to be a complete description of the offering. See “The Rights Offering” in this prospectus for a more detailed description of the terms and conditions of the distribution of rights and the offering of shares of Caesars Acquisition Company’s Class A common stock.

| Securities Offered |

Caesars Entertainment is distributing, at no charge, to holders of shares of Caesars Entertainment’s common stock as of the record date, non-transferable subscription rights to purchase up to an aggregate of 125,359,584 shares of CAC, at a price of $9.43 per whole share. Each holder of Caesars Entertainment’s common stock as of the record date will receive one subscription right for each full common share owned by that stockholder as of the record date. Each subscription right will entitle its holder to purchase from CAC one share of CAC’s Class A common stock. Each subscription right entitles the holder to a basic subscription right and an over-subscription privilege, as described below. The subscription rights will expire if they are not exercised by 5:00 p.m. New York City time, on , 2013. CAC expects the gross proceeds from the rights offering and the exercise of the subscription rights will be approximately $1,182.0 million, assuming that the subscription rights are exercised in full. |

| Basic Subscription Right |

The basic subscription right gives holders of the subscription rights the right to purchase from CAC, in the aggregate, 125,359,584 shares of CAC’s Class A common stock at a subscription price of $9.43 per whole share. Caesars Entertainment has distributed to each stockholder of record on the record date one subscription right for every share of Caesars Entertainment’s common stock such stockholder owned at that time. Fractional shares or cash in lieu of fractional shares will not be issued in the rights offering. Instead, fractional shares resulting from the exercise of the basic subscription right will be eliminated by rounding up to the nearest whole share. Affiliates of the Sponsors have advised Caesars Entertainment that they intend to exercise subscription rights of at least $500.0 million, though they have not entered into any agreement to do so. Consummation of the Transactions is contingent on the exercise of subscription rights of at least $500.0 million by affiliates of the Sponsors. |

| Over-subscription Privilege |

If you purchase all of the shares of CAC’s Class A common stock available to you pursuant to your basic subscription right, you may also choose to subscribe for a portion of any shares of CAC’s Class A common stock that other holders of subscription rights do not purchase through the exercise of their basic subscription rights. Over-subscription privileges will only be available with respect to shares of CAC’s Class A common stock underlying basic subscription rights that are not exercised or affirmatively retained by the holders of such basic subscription rights. If a holder of the basic subscription rights elects to retain any or all of its subscription rights that are not exercised, such holder must return a completed and signed rights certificate with the appropriate election to the Subscription Agent before the rights offering |

16

Table of Contents

| expires on , 2013, at 5:00 p.m. New York City time. For the avoidance of doubt, a holder may not elect to retain more than the number of basic subscription rights actually issued to such holder. |

Affiliates and co-investors of the Sponsors are also eligible to exercise the over-subscription privilege. If co-investors of the Sponsors elect not to exercise any of their basic subscription rights, affiliates of the Sponsors, which control the co-invest vehicles, will cause the co-invest vehicles to retain the basic subscription rights not exercised by the co-investors. To the extent that shares of our Class A common stock are available pursuant to the over-subscription privilege, Hamlet Holdings, after the granting of the Sponsor CAC Proxy, may obtain a percentage beneficial ownership in our Class A common stock of greater than approximately %.

| Subscription Price |