Attached files

| file | filename |

|---|---|

| 8-K - 8-K - UMB FINANCIAL CORP | d585125d8k.htm |

Second Quarter 2013

UMB Financial

Exhibit 99.1 |

This

document may contain forward-looking statements of expected future developments. We wish to

ensure such statements are accompanied by meaningful cautionary statements pursuant

to the safe harbor established by the Private Securities Litigation Reform

Act of 1995. Such forward-looking statements may refer to projections of

future financial performance and financial items, plans and objectives of

future operations, and other matters. The forward-looking statements reflect

management’s expectations and are based on currently available data; however,

actual future results are subject to future events and uncertainties, which

could materially affect actual performance and cause

future

results

to

differ

materially

from

those

referred

to

in

the

forward-looking

statements.

Such

future

events

and

uncertainties

include,

but

are

not

limited

to,

changes

in:

loan

demand,

the

ability

of

customers to repay loans, consumer saving habits, employee costs, pricing,

interest rates, competition, legal or regulatory requirements or

restrictions, U.S. or international economic or political conditions

such

as

inflation

or

fluctuation

in

interest

rates

or

in

the

values

of

securities

traded

in

the

equity markets. Any forward-looking statements should be read in conjunction

with information about risks and uncertainties set forth in the

company’s Securities and Exchange Commission reports, including its

annual report, Form 10-K for the year ended December 31, 2012 and the 8-K filing which

includes the press release for the quarter ended June 30, 2013. Forward-looking

statements speak only as of the date they are made, and the Company does not

intend to review or revise any particular forward-looking

statement

in

light

of

events

that

occur

thereafter

or

to

reflect

the

occurrence

of

unanticipated events.

Safe Harbor Statement

2 |

A Different

Kind of Bank The company

The business model

The performance |

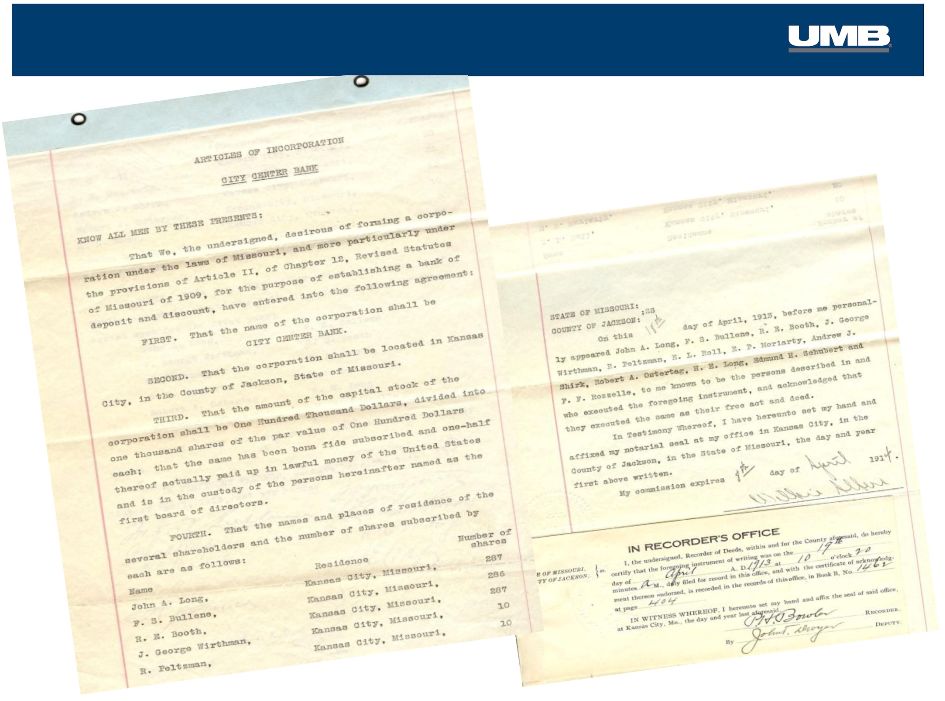

UMB

is

Born

as

City

Center

Bank

-

1913

4 |

A

Leader

in

Serving

our

Customers

“Beginning today, motorists can do business with the

City Bank, Eighteenth Street & Grand Avenue, from the

alley between Grand & McGee streets. They can drive

to the new “cage”

and make deposits without leaving

the

car.”

The

City

Bank

is

the

first

bank

in

Kansas

City

to

utilize such a plan to overcome traffic conditions

inconvenient for patrons.”

The Kansas City Star

January 29, 1931

1931 –

KC’s First “Drive Through Bank”

5 |

Self-Reliance and Stability

1934 –

Emerging from the Great Depression

6

No need for

government

assistance –

then

or now.

“If we were to liquidate this bank today, we

could pay our depositors one hundred cents

on the dollar and collect our entire Surplus

and

Capital

Account

of

$700,000

and

a

large

part of the Undivided Profits Account.”

-

R. Crosby Kemper, Sr. in a letter to the

Missouri Banking Commissioner, Oct. 1933 |

“Our company has remained

true to its values and the

results are evident in our

shareholder returns.”

Mariner Kemper

Chairman & Chief Executive Officer |

Total Returns Reflect Long-Term Performance

Total Shareholder Return

June1993 –

June 2013

8

416.8%

$100

302.4%

UMBF

S&P 500

SNL U.S. Bank

506.6% |

UMB At A

Glance Assets under management

Banking presence

Branches/ATMs

Acquisitions last 10 years

Market cap

Dividend payout ratio*

$35.6B

$35.6B

8 states

8 states

115/320+

115/320+

23

23

>$2.4B

>$2.4B

31.8%

31.8%

Total assets

$15.3B

$15.3B

Revenue from fee businesses

58.0%

58.0%

*Average over past 4 quarters

As of June 30, 2013

9 |

We Have

Repositioned UMB… National

Regional

Low

High

Geographic

focus

Diversity of revenue streams

More than a typical bank

More stable earnings

Faster growth

10 |

…Resulting in a Growing National Presence

Fund Services

Prairie Capital

Healthcare

Services

–

National

Sales

Scout

Investment

Advisors

–

National

Sales

Corporate Trust

UMB Bank presence

Loan Production Office

11 |

…

With Diverse Revenue Streams

0%

50%

100%

FY'04

FY'05

FY'06

FY'07

FY'08

FY'09

FY'10

FY'11

FY'12

2Q12

2Q13

Net Interest Income

Noninterest Income

High level of fee income reduces reliance on margin

12 |

Today: UMB is More

than a Regional Bank… …We are a diversified

financial services company 13

DIVERSIFIED FINANCIAL SERVICES

Healthcare

Services

Corporate

Trust

UMB Fund

Services

Scout

Investments

•JD Clark

Prairie

Capital

•Reams

Trust

Services

TRADITIONAL BANKING

Card

Services

Treasury

Management

Diversified

financial

Products / services

Banking

National

Regional

Geographic

focus

UMB

Insurance |

A

Financial Services Company The company

The business model

The performance |

+

+

+

High Quality Credit

Diverse Revenue Streams

Low-cost Funding

Strong

Balance Sheet

Our Time-Tested Business Model |

Our Credit

Quality Outpaces the Industry Peer Average as of 1Q13; Source: SNL

Financial Midwest Bank Peers as defined by Raymond James & Associates in

their April 11, 2011 report. 2Q 2013

NPLs =

0.40%

Shaded area is high/low range of the peer group

Non-Performing Loans

% of average loans

16

Peer Average

UMBF

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.0

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

Peer

Average

2.85% |

Today: More

Fee Revenue than Our Peers % of Total Revenue from Fees

2Q13

•

More stable earnings

•

Greater growth opportunities

Industry Median as of 1Q13; Source: SNL Financial

17

3X

vs. Industry

18.5%

58.0%

Industry

Median |

Successful Record Growing Fee Businesses

Noninterest

Income

($000’s)

*Includes Scout Investments and UMB Bank wealth management

Asset Management

Businesses

(Total Company Assets Under Management*)

18

$62.4

$113.6

2Q13

2Q05

$8.2B

$35.6B

2Q13

2005 |

At June 30

40.0%

vs.

Industry Median* of

18.6%

non-interest bearing

deposits

Low Cost Funding Sources

>2X

vs. Industry

Average Non-Interest Bearing

Deposits as % of Total Deposits

*Industry Median as of 1Q13; Source: SNL Financial

19

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2Q'13

UMBF

Industry Median |

Balance

Sheet

–

Strong

with

Growth

Potential

Tier 1 Capital Ratio

2Q 2013

Without Federal bailout funds

Highly Liquid –

Low Average Loan to Deposit Ratio

2Q 2013

Industry Median as of 1Q13; Source: SNL Financial

20

13.94%

10.72%

Industry

Median

76.2%

54.0%

Industry

Median |

Commercial Real Estate

Commercial & Industrial

Consumer Real Estate

Credit Card

Home Equity

Consumer

Commercial

Real Estate

Commercial &

Industrial

Changing Loan Mix

Consumer

Quality Loan Composition

2Q 2013

Year-End 2006

Commercial &

Industrial

Commercial

Real Estate

21

21.0%

5.2%

4.6%

20.0%

44.1%

5.1%

54.7%

24.8%

3.9%

6.7%

1.0%

9.0% |

A Financial

Services Company The company

The business model

The performance |

23

Consistent Performance –

Despite Headwinds

6.2%

11.7%

7.0%

5.0%

Revenue growth

Average Asset Growth

Average Equity Growth

EPS growth

5 year CAGR

(2Q’08--2Q’13)

26.5%

Total Assets Under Management

(diluted) |

-16.7%

-14.8%

-4.2%

-3.6%

-3.6%

-3.2%

0.0%

0.01%

1.1%

2.0%

3.4%

4.99%

7.3%

8.2%

5-Year

Diluted

Earnings

Per

Share

2Q’08

–

2Q’13

CAGR

UMBF vs. Traditional Peers

*Bank industry defined as all publicly traded banks per SNL Financial;

EPS Growth vs. the Industry & Peers

CYN

Bank Industry Median *

ONB

BOH

BXS

FMER

CFR

TRMK

CBSH

HBHC

COBZ

TCB

FMBI

*All publicly traded banks with 2Q’13 reported EPS per SNL Financial

24 |

2

nd

Quarter

2013

Highlights |

Changing

Earning Asset Mix 2Q’08

Net Loans –

54.9%

Total

Securities

–

41.3%

26

48.5%

44.6%

41.9%

43.0%

44.9%

45.1%

49.4%

50.2%

53.2%

51.7%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2Q'09

2Q'10

2Q'11

2Q'12

2Q'13

Net loans

Total securities

Fed funds & resell agreements

Interest Bearing Due From Banks |

Average Balance:

$7.2 billion

Average Yield:

1.95%

Investment Mix

Mortgage-Backed Securities

Municipals

CDs & Corporates

Agencies

Treasuries

Trading Securities

Investment Portfolio Statistics

27

Roll off

Purchased

($ millions)

Yield

($ millions)

Yield

2Q12

$396

2.52%

$636

1.69%

1Q13

$413

1.98%

$769

1.31%

2Q13

$340

2.13%

$815

1.41%

Scheduled

Cash

Flow

3Q13

$269

1.81%

Next 12 months

$1,230

1.88%

Duration/Life

(in months)

at 06/30/13

at 03/31/13

Avg. Life Total

48.67

42.79

Avg. Life Core

48.98

43.67

Avg. Life Noncore

32.48

5.29

Duration Total

46.80

39.75

Duration Core

47.11

40.54

Securities Gains

($ millions)

2Q12

3,222

$

3Q12

259

$

4Q12

210

$

1Q13

5,893

$

2Q13

1,519

$

1.4%

14.6%

45.1%

31.1%

7.0%

0.7% |

Liabilities

Deposit Growth & % of Free Funds

($ billions)

2Q’13

Cost of Funds 0.18%

Including DDA 0.11%

28

38.5%

40.8%

41.7%

34.0%

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

Interest Bearing

Non-Interest Bearing

$11.7

$10.3

$9.9

$8.4 |

Capital

Total Shareholder Equity

29

Shareholder Equity ($billions)

TCE Ratio

Q2'10

Q3'10

Q4'10

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

Q2'12

Q3'12

Q4'12

Q1'13

Q2'13

4.0%

6.0%

8.0%

10.0%

8.13%

7.71%

6.26%

5.97%

6.66%

7.36%

6.76%

6.90%

7.48%

7.78%

7.49%

6.55%

6.37%

$1.07

$1.09

$1.06

$1.08

$1.13

$1.17

$1.19

$1.21

$1.25

$1.29

$1.28

$1.29

$1.23 |

Net

Interest Income 2Q’13 net interest income increased 2.4% vs. 2Q’12;

driven by earning asset growth and improved deposit pricing

30

$77.7

$78.4

$78.8

$78.4

$79.9

$79.1

$79.5

$79.1

$80.4

$80.4

$80.2

$79.5

$82.3

3.13%

3.09%

3.15%

2.90%

2.98%

2.98%

2.91%

2.75%

2.82%

2.80%

2.64%

2.51%

2.56%

$65.0

$67.0

$69.0

$71.0

$73.0

$75.0

$77.0

$79.0

$81.0

$83.0

$85.0

2Q'10

3Q'10

4Q'10

1Q'11

2Q'11

3Q'11

4Q'11

1Q'12

2Q'12

3Q'12

4Q'12

1Q'13

2Q'13

Net Interest Income

NIM% |

Noninterest

Income Highlights 5 Year

CAGR

2Q’08–

2Q’13

13.9%

Trust & Securities Process Revenue

Trust & Securities Processing Composition

:

Bankcard Fees

Deposit Service Charges

Insurance Fees & Commissions

Trading & Investment Banking

Trust & Securities Processing

Gains on Sale of Securities

Brokerage Fees

Other

$63.5 million in 2Q13

Primary components:

•$29.2M -

Institutional Investment Management

•$19.3M –

Asset Servicing

•$15.0M –

Personal & Institutional Asset Mgmt in

the Bank segment

31

55.9%

4.8%

18.4%

1.1%

2.5%

14.1%

1.3%

1.9%

$33.1

$28.6

$38.6

$53.6

$55.8

$63.5 |

Noninterest

Expense 32

Noninterest expense increased 3.9% to $150.3 million vs. 2Q’12

•

Increase primarily driven by higher salary and benefits expense of $5.6

million and increased processing fees of $1.7 million related to

fees

paid to third-party distributors of the Scout Funds.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$40

$60

$80

$100

$120

$140

$160

$180

Salary/Benefit Expense

Noninterest Income

Total Noninterest Expense

Coverage Ratio*

Salary

CAGR

8.7%

NI

Income

CAGR

7.6%

NI

Expense

CAGR

7.2%

Managed FTE Costs; Growing Noninterest Income |

Business Segment Updates |

Institutional

Investment Management $22.4

$22.6

$23.5

$25.7

$26.3

2Q'12

3Q'12

4Q'12

1Q'13

2Q'13

Total Scout Assets Under Management

($ billions)

* Industry data source: Strategic Insight

AUM increased 17.5% year-

over-year to $26.3 billion

Net inflows of $902 million for

Q2’13; year-to-date flows of

$2.5 billion

Q2’13 industry stats: Equity

funds realized $68.8B in net

inflows; Taxable bond funds

realized $3.0B in net inflows

2

nd

Quarter

2013

Highlights

Institutional Investment Management Operating Results

3 mos Ended

March 31,

Year-Over-Year

Linked-Quarter

2013

2012

2013

Net Interest income

(10)

-

-

-

-

Noninterest income

29,160

23,625

28,553

23.43%

2.13%

Noninterest expense

18,932

16,486

18,958

14.84%

-0.14%

NI before taxes

10,218

7,139

9,595

43.13%

6.49%

Income tax expense

2,691

2,197

2,635

22.49%

2.13%

Net income

7,527

4,942

6,960

52.31%

8.15%

pre-tax profit margin

35.1%

30.2%

33.6%

Ended June 30,

% Change

3 mos Ended

34 |

$51.6

$119.8

$1,435.7

$171.8

$703.5

$606.4

$585.7

($84.0)

($622.9)

$204.1

$134.4

$729.9

$354.0

$2.4

$48.7

($250.4)

-$1,000

-$500

$0

$500

$1,000

$1,500

$2,000

$2,500

3Q'12

4Q'12

1Q'13

2Q'13

Equity Flows

Equity Market Impact

Fixed Income Flows

Fixed Income Market Impact

AUM Drivers

($millions)

$2,204.5

$932.7

$486.2

Total Change

($millions)

$25,746.8

$23,542.3

$22,609.6

Total AUM

($millions)

$567.3

$26,314.1

Institutional Investment Management

35 |

Total AUM

$19.9B

$19.7B

$23.5B

$25.7B

$26.3B

Institutional Investment Management

36

$8.1

$8.2

$10.4

$11.0

$11.1

$0.2

$0.6

$0.9

$1.0

$1.3

$0.8

$0.6

$0.6

$0.8

$2.3

$2.3

$10.2

$10.3

$11.4

$11.4

$11.6

2010

2011

2012

1Q13

2Q13

Equity Mutual Funds

Fixed Income Mutual Funds

Money Market

Equity Institutional & Other

Fixed Income Institutional & Other |

AUM

by

Strategy

–

As

of

2Q’13

Acquired Reams Asset

Management in

December 2010

37

Equity Strategies

International

Mid Cap

International ADR

Emerging Markets

Global

Small Cap

Other:

Equity

Fixed Income

49.0%

51.0%

Fixed Income Strategies

Core Plus

Core

Low Duration

Long Duration

Intermediate

Unconstrained

Global Aggregate

70.4%

24.7%

2.7%

1.9%

0.2%

29.4%

9.7%

23.3%

16.1%

2.1%

19.2%

0.2% |

Fixed Income Rotation

Change in Fixed Income

Strategies

Core Plus

Core

Low Duration

Long Duration

Intermediate

Unconstrained

Global Aggregate

2Q’13

2Q’12

38

47.3%

14.7%

21.3%

12.4%

2.1%

2.0%

0.1%

29.4%

9.7%

23.3%

16.1%

2.1%

19.2%

0.2% |

Asset

Servicing 39

$162.4

$179.3

$206.4

$156.0

$165.4

$168.0

2009

2010

2011

2012

1Q13

2Q13

Asset Servicing Operating Results

3 mos Ended

March 31,

Year-Over-Year

Linked-Quarter

2013

2012

2013

Net interest income

587

463

675

26.78%

-13.04%

Noninterest income

19,275

18,779

20,278

2.64%

-4.95%

Noninterest expense

17,054

17,296

19,932

-1.40%

-14.44%

NI before taxes

2,808

1,946

1,021

44.30%

175.02%

Income tax expense

967

838

578

15.39%

67.30%

Net income

1,841

1,108

443

66.16%

315.58%

pre-tax profit margin

14.1%

10.1%

4.9%

% Change

Ended June 30,

3 mos Ended

2

nd

Quarter

2013

Highlights

Assets Under Administration

Total AUA increased by 14% to

$168 billion

Multiple-Series Trust surpasses

$5 billion; doubled assets in < 1

year |

Asset Servicing Fund Accounting & Administration

Alternative Asset Servicing

Custody

Transfer Agency

Business Metrics

40

$30.5

$35.9

$40.2

$39.8

$41.7

$44.1

$48.4

$52.1

2010

2011

1Q'12

2Q'12

3Q'12

4Q'12

1Q'13

2Q'13

Assets Under Administration

# of Funds Serviced

179

181

116

160

170

170

170

182

$21.3

$24.7

$25.2

$25.8

$26.1

$26.3

$27.9

$28.3

2010

2011

1Q'12

2Q'12

3Q'12

4Q'12

1Q'13

2Q'13

Assets Under Administration

# of Funds Serviced

406

467

487

504

520

532

543

549

$101.4

$115.6

$129.0

$48.5

$50.9

$54.9

$58.5

$56.2

2010

2011

1Q'12

2Q'12

3Q'12

4Q'12

1Q'13

2Q'13

Assets Under Administration

# of Custody Accounts

470

499

511

418

423

443

432

400

554.9

802.4

884.1

882.1

946.8

1,058.7

1,213.8

2010

2011

1Q'12

2Q'12

3Q'12

4Q'12

1Q'13

2Q'13

# of Shareholders

# of Funds Serviced

227

256

244

272

255

270

275

284

944.8 |

Payment

Solutions Total

Card

Purchase

Volume

&

Interchange

Revenue

Durbin

effective

Payment Solutions Operating Results

3 mos Ended

March 31,

Year-Over-Year

Linked-Quarter

2013

2012

2013

Net interest income

11,192

10,556

11,548

6.03%

-3.08%

Provision for loan losses

3,318

2,278

1,743

45.65%

90.36%

Noninterest income

18,649

18,106

19,437

3.00%

-4.05%

Noninterest expense

21,986

16,620

20,051

32.29%

9.65%

NI before taxes

4,537

9,764

9,191

-53.53%

-50.64%

Income tax expense

1,350

2,791

2,786

-51.63%

-51.54%

Net income

3,187

6,973

6,405

-54.30%

-50.24%

pre-tax profit margin

15.2%

34.1%

29.7%

% Change

Ended June 30,

3 mos Ended

Purchase

Volume

2Q ‘09–’13

18.1%

Inter-

change

2Q ‘09–’13

12.6%

CAGR

Total debit and credit card

purchase volume +16.5% to

$1.72 billion

Interchange revenue +10% to

$17.1 million

2

nd

Quarter 2013 Highlights

41

$0.88

$0.85

$0.85

$1.04

$1.10

$1.06

$1.08

$1.31

$1.36

$1.29

$1.26

$1.58

$1.48

$1.37

$1.38

$1.79

$1.72

$10.7

$13.7

$15.8

$15.6

$17.1

Purchase Volume ($ billions)

Interchange ($ millions) |

Payment

Solutions Health Savings Accounts & Balances

* Deposits and investment assets

Healthcare card purchase volume

+39.6% to $748.6 million

Interchange contribution +43% to

$2.7 million

2

Quarter 2013 Highlights

Healthcare Services

Card Utilization

42

Commitments

Outstandings

Utilization

2009

2010

2011

2012

2Q '13

$296.7

$405.8

$422.4

$429.4

$410.2

18.5%

22.9%

17.0%

16.4%

15.6%

$1,602.5

$1,774.7

$2,484.1

$2,613.1

$2,629.0

HSA Balances*

# of accts

2009

2010

2011

2012

1Q13

2Q13

1.3

1.8

2.5

3.1

3.1

3.2

$190.7

$279.9

$323.3

$433.4

$607.6

$596.2

1.0

2.0

3.0

4.0

5.0

nd |

Bank

Assets Under Management

($ billions)

Bank Operating Results

3 mos Ended

March 31,

Year-Over-Year

Linked-Quarter

2013

2012

2013

Net interest income

70,558

69,354

67,260

1.74%

4.90%

Provision for loan losses

1,682

2,222

257

-24.30%

554.47%

Noninterest income

46,501

49,716

52,748

-6.47%

-11.84%

Noninterest expense

92,339

94,284

91,437

-2.06%

0.99%

NI before taxes

23,038

22,564

28,314

2.10%

-18.63%

Income tax expense

5,664

6,422

7,181

-11.80%

-21.13%

Net income

17,374

16,142

21,133

7.63%

-17.79%

pre-tax profit margin

19.7%

19.0%

23.6%

3 mos Ended

% Change

Ended June 30,

HELOC Lending

Individual & institutional wealth management assets in Bank segment

Small Business Banking loans

increased 25% year-over-year to

$158.5 million

Private Banking exceeded $280 million

in average loan balances, an increase

of 40.9% over Q2 2012

UMB ranked #1 in C&I and CRE loan

growth for 1Q13 vs. 4Q12 compared to

our “Regional Competitor Banks”

(Source: SNL Financial)

2

Quarter 2013 Highlights

43

nd

Commitments

Balances

Utilization

2008

2009

2010

2011

2012

2Q13

$365

$430

$465

$524

$548

$551

49.3%

49.2%

49.4%

49.0%

47.1%

46.1%

$741

$873

$941

$1,070

$1,163

$1,196

2008

2009

2010

2011

2012

2Q13

$4.4

$4.5

$8.0

$8.3

$9.6

$9.2 |

$3.03

$3.46

$3.46

$3.75

$4.20

$5.00

2Q'08

2Q'09

2Q'10

2Q'11

2Q'12

2Q'13

Bank

High Growth Regions

2Q’13 vs. 2Q’12

•

Arizona

+67%

•

Nebraska

+37%

48.5%

48.2%

47.3%

46.1%

43.9%

42.8%

0%

50%

100%

2Q'08

2Q'09

2Q'10

2Q'11

2Q'12

2Q'13

KC

CO

STL

Greater MO

KS

OK

AZ

NE

Commercial Loan Concentration By Region

•

St. Louis

+26%

•

Oklahoma +20%

Commercial Loan Growth

(C&I and CRE Loans)

44

5 yr

CAGR

2Q ‘08–’13

10.6% |

Bank

Total Deposits

5 yr

CAGR

2Q ‘08–’13

16.5%

Deposits By Region

45

31.3%

32.3%

33.5%

33.7%

40.0%

40.0%

$6.3

$7.6

$8.3

$9.5

$10.3

$11.6

2Q'08

2Q'09

2Q'10

2Q'11

2Q'12

2Q'13

Interest Bearing

Non-Interest Bearing

52.4%

54.3%

55.3%

58.8%

60.2%

63.6%

0%

50%

100%

2Q'08

2Q'09

2Q'10

2Q'11

2Q'12

2Q'13

KC

STL

CO

Gtr MO

KS

OK

AZ

NE |

Strengths We

are Leveraging Growing fee

businesses

Infrastructure

Success building a diversified

financial services company

Building scale through

strategic acquisitions

Existing technology, operations,

products, distribution

46

Diversified

revenue |

Building a company

for the next 100 years.

UMB Financial

Second Quarter 2013 |