Attached files

| file | filename |

|---|---|

| EX-23.3 - EX-23.3 - SiriusPoint Ltd | d532633dex233.htm |

Table of Contents

As filed with the Securities and Exchange Commission on July 16, 2013

Registration No. 333-189960

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

THIRD POINT REINSURANCE LTD.

(Exact name of registrant as specified in its charter)

| Bermuda | 6331 | Not Applicable | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

The Waterfront, Chesney House

96 Pitts Bay Road

Pembroke HM 08 Bermuda

+1 441 542-3300

(Address, including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

Registered Agent Solutions, Inc.

99 Washington Avenue

Suite 1008

Albany, NY 12260

(888) 705-7274

(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

Copies to:

| Steven J. Slutzky, Esq. | John R. Berger | Michael Groll, Esq. | ||

| Debevoise & Plimpton LLP | Chief Executive Officer | Willkie Farr & Gallagher LLP | ||

| 919 Third Avenue | Third Point Reinsurance Ltd. | 787 Seventh Avenue | ||

| New York, New York 10022 | 96 Pitts Bay Road | New York, New York | ||

| (212) 909-6000 | Pembroke HM 08 Bermuda | (212) 728-8000 | ||

| +1 441 542-3300 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date hereof.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||||

| Non-accelerated filer | x | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||||

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state or jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED July 16, 2013

Shares

Common Shares

This is the initial public offering of common shares of Third Point Reinsurance Ltd. We are offering common shares to be sold in the offering. The selling shareholders identified in this prospectus are offering an additional common shares. We will not receive any proceeds from the sale of shares by the selling shareholders. No public market currently exists for our common shares. The estimated initial public offering price is between $ and $ per share.

We intend to apply to list our common shares on the New York Stock Exchange (the “NYSE”) under the symbol “TPRE.”

We are an “emerging growth company” as defined under applicable federal securities laws and may utilize reduced public company reporting requirements. Investing in our common shares involves risks. See “Risk Factors” beginning on page 15 of this prospectus.

| Per Share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions |

$ | $ | ||||||

| Proceeds, before expenses, to Third Point Reinsurance Ltd.(1) |

$ | $ | ||||||

| Proceeds, before expenses, to Selling Shareholders |

$ | $ | ||||||

| (1) | We estimate that we will incur approximately in expenses in connection with this offering, including fees and expenses incident to any required review by the Financial Industry Regulatory Authority, Inc. (“FINRA”). See “Underwriting (Conflicts of Interest).” |

The underwriters also may purchase up to additional shares from us and from the selling shareholders at the initial offering price less the underwriting discounts and commissions to cover over-allotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We intend to apply for, and expect to receive, consent under the Bermuda Exchange Control Act 1972 (and its related regulations) from the Bermuda Monetary Authority (the “BMA”) for the issue and transfer of our common shares to and between residents and non-residents of Bermuda for exchange control purposes provided our common shares remain listed on an appointed stock exchange, which includes the NYSE. In granting such consent the BMA accepts no responsibility for our financial soundness or the correctness of any of the statements made or opinions expressed in this prospectus.

The underwriters expect to deliver the shares to purchasers on or about , 2013.

| J.P. Morgan | Credit Suisse | Morgan Stanley |

| BofA Merrill Lynch | Citigroup | |

| Aon Benfield Securities, Inc. |

Dowling & Partners Securities LLC |

Keefe, Bruyette & Woods A Stifel Company |

| Macquarie Capital | Sandler O’Neill + Partners, L.P. |

, 2013.

Table of Contents

| Page | ||||

| 1 | ||||

| 12 | ||||

| 15 | ||||

| 50 | ||||

| 52 | ||||

| 53 | ||||

| 54 | ||||

| 55 | ||||

| 56 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

59 | |||

| 93 | ||||

| 119 | ||||

| 130 | ||||

| 136 | ||||

| 145 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS, MANAGEMENT AND SELLING SHAREHOLDERS |

154 | |||

| 157 | ||||

| 162 | ||||

| 169 | ||||

| 171 | ||||

| UNDERWRITING (CONFLICTS OF INTEREST) |

183 | |||

| 189 | ||||

| 189 | ||||

| ENFORCEMENT OF CIVIL LIABILITIES UNDER U.S. FEDERAL SECURITIES LAWS |

189 | |||

| 190 | ||||

| F-1 | ||||

| GLOSSARY OF SELECTED INSURANCE, REINSURANCE AND FINANCIAL TERMS |

G-1 | |||

You should rely only on the information contained in this prospectus or any free writing prospectus prepared by or on behalf of us or to which we have referred you. Neither we nor the underwriters have authorized anyone to provide you with additional or different information. Neither this prospectus nor any free writing prospectus is an offer to sell anywhere or to anyone where or to whom we are not permitted to offer or to sell securities under applicable law. The information in this prospectus or any free writing prospectus is accurate only as of the date of this prospectus or such free writing prospectus, as applicable.

For investors outside the United States: Neither we, the selling shareholders, nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus outside of the United States.

i

Table of Contents

The following summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider before investing in our common shares. You should read this entire prospectus, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes to those statements, before making an investment decision. Unless the context otherwise indicates or requires, the terms “we,” “our,” “us,” and the “Company,” as used in this prospectus, refer to Third Point Reinsurance Ltd. and its directly and indirectly owned subsidiaries, including Third Point Reinsurance Company Ltd. (“Third Point Re”), as a combined entity, except where otherwise stated or where it is clear that the terms mean only Third Point Reinsurance Ltd. exclusive of its subsidiaries. We refer to Third Point Reinsurance Investment Management Ltd. as the “Catastrophe Fund Manager,” Third Point Reinsurance Opportunities Fund Ltd. as the “Catastrophe Fund” and Third Point Re Cat Ltd. as the “Catastrophe Reinsurer.” For your convenience, we have included a glossary beginning on page G-1 of selected insurance, reinsurance and financial terms. All dollar amounts referred to in this prospectus are in U.S. dollars unless otherwise indicated.

Overview

We are a Bermuda-based property and casualty reinsurer with a reinsurance and investment strategy that we believe differentiates us from our competitors. Our goal is to deliver attractive equity returns to shareholders by combining profitable reinsurance underwriting with superior investment management provided by Third Point LLC, our investment manager.

Our reinsurance strategy is to be highly opportunistic and disciplined. During periods of extremely competitive or soft reinsurance market conditions we intend to be selective with regard to the amount and type of reinsurance we write and conserve our risk-taking capital for periods when market conditions are more favorable to us from a pricing perspective.

Substantially all of our investable assets are managed by our investment manager, Third Point LLC, which is wholly owned by Daniel S. Loeb, one of our founding shareholders. Third Point LLC is an SEC-registered investment adviser headquartered in New York, managing $13.5 billion in assets as of May 31, 2013. We directly own our investments, which are held in a separate account and managed by Third Point LLC on substantially the same basis as its main hedge funds, including Third Point Partners L.P., the original Third Point LLC hedge fund.

We were incorporated on October 6, 2011 and completed our initial capitalization transaction on December 22, 2011 with $784.3 million of equity capital, and commenced underwriting business on January 1, 2012. In January 2012, we received an A- (Excellent) financial strength rating from A.M. Best Company, Inc., or A.M. Best.

Our management team is led by John R. Berger, a highly-respected reinsurance industry veteran with over 30 years of experience, the majority of which was spent as the principal executive officer of three successful reinsurance companies. In addition, we have recruited a management team around Mr. Berger that also has significant senior leadership and underwriting experience in the reinsurance industry. We believe that our experience and longstanding relationships with our insurance company clients, senior reinsurance brokers, insurance regulators and credit rating agencies are an important competitive advantage.

For the year ended December 31, 2012, we generated net income of $99.4 million, which represented a return on beginning shareholders’ equity attributable to shareholders as of December 31, 2011 of 13.0%. For 2012 and for the three months ended March 31, 2013, our gross premiums written totaled $190.4 million and $96.0 million, respectively, and earned premiums totaled $96.5 million and $33.5 million, respectively. For

1

Table of Contents

the same periods our net investment income totaled $136.4 million and $80.7 million, respectively, which represent net returns of 17.7% and 8.7%, respectively, on our investments managed by Third Point LLC. In 2012, our combined ratio for our property and casualty reinsurance segment was 135.5%, reflecting the impact of high general and administrative expenses relative to earned premiums due to the start-up nature of our business in 2012; a $10.0 million underwriting loss in our crop line of business attributable to the severe drought that impacted most of the U.S. farm belt in 2012; and the fact that crop was our largest line of business by earned premium, representing almost half of earned premium for the year. Our combined ratio for our property and casualty reinsurance segment for the three months ended March 31, 2013 was 116.0% due to a significant decrease in general and administrative expenses as a percentage of earned premium. As of March 31, 2013, we had shareholders’ equity attributable to shareholders of $944.7 million.

Reinsurance Strategy

Our reinsurance strategy is to build a reinsurance portfolio that generates stable underwriting profits, with margins commensurate with the amount of risk assumed, by opportunistically targeting sub-sectors of the market and specific situations where reinsurance capacity and alternatives may be constrained. Our management team has differentiated expertise that allows us to identify profitable reinsurance opportunities. The level of volatility in our reinsurance portfolio will be determined by market conditions but will typically be lower than that of most other reinsurance companies. We manage reinsurance volatility by focusing on lines of business that have historically demonstrated more stable return characteristics, such as limited catastrophe exposed property, which we refer to as “property quota share”, auto, workers compensation and certain segments of crop. These lines of business are often characterized as having exposure to higher frequency and lower severity claims activity. We seek to further manage the volatility of our reinsurance results by writing reinsurance contracts on a quota share basis, where we assume an agreed percentage of premiums and losses for a portfolio of insurance policies. We also make use of contractual terms and conditions within our reinsurance contracts that include individual or aggregate loss occurrence limits, which limit the dollar amount of loss that we can incur from a particular occurrence or series of occurrences within the term of a reinsurance contract; loss ratio caps, which limit the maximum loss we can incur pursuant to a contract to a defined loss ratio; sliding scale commissions that vary with accordance to the client’s performance; and sub-limits and exclusions for particular risks not covered by a particular reinsurance contract.

We wrote 11 quota share contracts and one deposit accounted reserve cover during 2012 in our property and casualty reinsurance segment, and a further five quota share contracts in our property and casualty reinsurance segment during the three months ended March 31, 2013, all with underlying U.S. exposure. For the year ended December 31, 2012, three contracts each contributed more than 10% of our gross premiums written. These three contracts contributed 22%, 20% and 12%, respectively, of total gross premiums written for the year ended December 31, 2012. For the three months ended March 31, 2013, two contracts each contributed more than 10% of total gross premiums written. These two contracts each represented 36.5% of total gross premiums written for the three months ended March 31, 2013. As we expand our business over time, we expect that the proportion of total gross premiums written represented by individual contracts will decline. Under current market conditions, we focus primarily on writing quota share agreements pursuant to which we assume an agreed percentage of premiums and losses for a portfolio of insurance policies and share that percentage of premiums and losses with the reinsured.

We underwrite a mix of short to medium tail personal lines and commercial lines. We intend to increase our geographic spread over time by adding reinsurance programs from European, Asian and South American clients; however, we expect that a majority of our reinsurance business will continue to be composed of U.S. exposure.

Most of our clients buy reinsurance from us for capital management purposes, primarily to increase their capacity to write insurance premium. The most common form of reinsurance used for this purpose is quota share

2

Table of Contents

reinsurance. Many of the clients that buy these contracts are growing as a result of securing primary rate increases and growth in the number of policies they write. Because quota share reinsurance typically includes structural and contractual features that limit the amount of risk assumed by the reinsurer, it therefore carries relatively lower expected margins than excess of loss reinsurance and other more volatile forms of reinsurance. During periods of less favorable market conditions, margins on quota share reinsurance written for the capital management purposes of our clients typically remain stable and are sufficient to support our business plan. As market conditions improve, we may expand the lines of business and forms of reinsurance on which we focus to increase our risk-adjusted returns.

We typically write larger customized reinsurance contracts that require significant interaction during the course of negotiations between the client, intermediaries and our management. Our management team lead underwrites most of our reinsurance contracts, meaning that we establish the pricing and terms and conditions of the reinsurance contract, except in certain instances where we will follow terms and conditions established by our competitors if we believe the opportunity meets our return hurdles and helps us balance our reinsurance portfolio.

Our property and casualty reinsurance operations also generate excess cash flows, or float, which we track in managing our business. We believe that continuing to seek net investment income from float is a key part of our reinsurance strategy and an important consideration in evaluating the overall contribution of our property and casualty reinsurance operations to our consolidated results.

In contrast to many reinsurers with whom we compete, we have elected to limit our underwriting of property catastrophe exposures and write excess of loss catastrophe reinsurance exclusively through the Catastrophe Fund, which is a separately capitalized reinsurance fund vehicle. We established the Catastrophe Fund, the Catastrophe Fund Manager and the Catastrophe Reinsurer on June 15, 2012, in partnership with Hiscox Insurance Company (Bermuda) Limited, or Hiscox. Our investment in and management of the Catastrophe Fund allow us to provide a product that is critical to most of our reinsurance clients and to earn fee income over time. Because the Catastrophe Fund is capitalized in part by investments from unrelated parties, our financial exposure to the higher volatility and liquidity risks associated with property catastrophe losses is limited to our investment commitment to the Catastrophe Fund, which as of the date hereof was $50 million, out of total commitments of $94.7 million. Until our investment in the Catastrophe Fund drops below 50% of total investment in the Catastrophe Fund, we will consolidate the financial results of the Catastrophe Fund. As there are no additional guarantees or recourse to us beyond this investment, we anticipate that our property catastrophe exposures will consistently remain relatively low when compared to many other reinsurers with whom we compete.

The following table provides a breakdown by line of business of gross premiums written for the year ended December 31, 2012 and for the three month period ended March 31, 2013:

| Three Months Ended March 31, 2013 |

Year Ended December 31, 2012 |

|||||||||||||||

| Gross Premiums Written |

Amount | Percentage of Total |

Amount | Percentage of Total |

||||||||||||

| ($ in thousands) | ||||||||||||||||

| Property and Casualty Reinsurance Segment |

||||||||||||||||

| Property |

$ | 350 | 0.3 | % | $ | 103,174 | 54.2 | % | ||||||||

| Casualty |

52,208 | 54.4 | % | 44,700 | 23.5 | % | ||||||||||

| Specialty |

40,313 | 42.0 | % | 42,500 | 22.3 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 92,871 | 96.7 | % | 190,374 | 100.0 | % | |||||||||||

| Catastrophe Risk Management Segment |

3,149 | 3.3 | % | — | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 96,020 | 100.0 | % | $ | 190,374 | 100.0 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

3

Table of Contents

Investment Strategy

Our investment strategy distinguishes us from most other reinsurers, who typically concentrate their investment portfolios on long-only, investment grade, shorter-term, fixed income securities. As implemented by our investment manager, Third Point LLC, our investment strategy is intended to achieve superior risk-adjusted returns by deploying capital in both long and short investments with favorable risk/reward characteristics across select asset classes, sectors and geographies. Third Point LLC identifies investment opportunities via a bottom-up, value-oriented approach to single security analysis supplemented by a top-down view of portfolio and risk management. Third Point LLC seeks dislocations in certain areas of the capital markets or in the pricing of particular securities and supplements single security analysis with an approach to portfolio construction that includes sizing each investment based on upside/downside calculations, all with a view towards appropriately positioning and managing overall exposures. Dislocations in capital markets refer to any major movements in prices of the capital markets as a whole, certain segments of the market, or a specific security. If Third Point LLC has what it considers to be a differentiated view from the perceived market sentiment with respect to such movement, Third Point LLC may trade securities in our investment account based on that differentiated view. If the ultimate market reaction with respect to the event or movement ultimately proves to be closer to Third Point LLC’s original viewpoint, we may have investment gains in our investment portfolio as a result of the shift in market sentiment. Through our investment manager, Third Point LLC, we make investments globally, in both developed and emerging markets, in all sectors, and in equity, credit, commodity, currency, options and other instruments.

Third Point LLC has historically favored event-driven situations, in which it believes that a catalyst, either intrinsic or extrinsic, will unlock value or alter the lens through which the greater market values a particular investment. Third Point LLC attempts to apply this event framework to each of its single security investments and this approach informs the timing and risk of each investment. For additional detail regarding Third Point LLC’s investment strategy and event-driven framework utilized in managing our investment portfolio, please refer to the expanded description under “Investments—Investment Strategies.”

As our investment manager, Third Point LLC has the contractual right to manage substantially all of our investable assets pursuant to an investment management agreement that has an initial term expiring on December 22, 2016, subject to automatic renewal for additional successive three-year terms unless a party notifies the other parties of its intention to terminate at least six months prior to the end of a term. Third Point LLC is required to follow our investment guidelines and to act in a manner that is fair and equitable in allocating investment opportunities to us. However, it is not otherwise restricted with respect to the nature or timing of making investments for our account. Our investment guidelines require Third Point LLC to manage our investment portfolio on a substantially equivalent basis to its main funds; but in any event to keep at least 60% of the investment portfolio in debt and equity securities, cash, cash equivalents or precious metals; limit single position concentration to no more than 15% of the portfolio assets managed; and limit net exposure to no greater than 1.5 times portfolio assets managed for more than 10 trading days in any 30-day period. Net exposure represents the short exposure subtracted from the long exposure in a given category. We have the contractual right to withdraw funds from our managed account to pay claims and expenses as needed. The net increase in the value of our investment portfolio for the year ended December 31, 2012 was 17.7%. For the three months ended March 31, 2013, the net increase in the value of our investment portfolio was 8.7% compared to 4.5% for the three months ended March 31, 2012.

4

Table of Contents

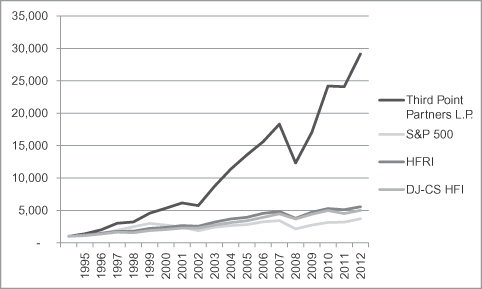

Third Point Partners L.P., which is Third Point LLC’s oldest fund, has reported a compounded annualized return of approximately 21.0% from its formation in June 1995 through December 31, 2012, and a compounded annual return of 9.7% and 17.7% for the five- and ten-year periods ended December 31, 2012. The following chart sets forth Third Point Partners L.P.’s total return after fees and incentive allocation for each year in the period since inception as measured against various equity and alternative management indices. The linear graph below illustrates the compounded growth of a hypothetical $1,000 investment in Third Point Partners L.P. at inception in June 1995, assuming no redemptions and net of fees and expenses as described below:

| Historical Performance of Third Point |

Illustrative Return After Fees, Expenses and Incentive Allocation Since Inception— Third Point Partners L.P.(2)(3)(4) | |||||

| 2012 |

20.96 | % |

| |||

| 2011 |

-0.35 | % | ||||

| 2010 |

41.81 | % | ||||

| 2009 |

38.44 | % | ||||

| 2008 |

-32.75 | % | ||||

| 2007 |

17.31 | % | ||||

| 2006 |

15.03 | % | ||||

| 2005 |

19.51 | % | ||||

| 2004 |

30.36 | % | ||||

| 2003 |

52.02 | % | ||||

| 2002 |

-6.65 | % | ||||

| 2001 |

15.05 | % | ||||

| 2000 |

17.07 | % | ||||

| 1999 |

42.16 | % | ||||

| 1998 |

6.61 | % | ||||

| 1997 |

52.07 | % | ||||

| 1996 |

44.29 | % | ||||

| 1995 |

37.00 | % | ||||

| (1) | For 2012, results of Third Point Partners L.P. as reported are higher than results for our investment portfolio due primarily to timing of the initial investment of our portfolio and differences in management and performance fees. |

| (2) | Past performance is not necessarily indicative of future results. All investments involve risk including the loss of principal. |

| (3) | The historical performance of Third Point Partners L.P. (i) for the years 2001 through 2012 reflects the total return after incentive allocation for each such year as included in the audited statement of financial condition of Third Point Partners L.P. for those years and (ii) for the years 1995 through 2000 reflects the total return after incentive allocation for each such year as reported by Third Point Partners L.P. Total return after incentive allocation for the years 2001 through 2012 is based on the net asset value for all limited partners of Third Point Partners L.P. taken as a whole, some of whom pay no incentive allocation or management fees, whereas total return after incentive allocation for the years 1995 through 2000 is based on the net asset value for only those limited partners of Third Point Partners L.P. that paid incentive allocation and management fees. In each case, results are presented net of management fees, brokerage commissions, administrative expenses, and accrued performance allocation, if any, and include the reinvestment of all dividends, interest, and capital gains. |

| (4) | The illustrative return is calculated as a theoretical investment of $1,000 in Third Point Partners, L.P. at inception relative to the same theoretical investment in two hedge fund indices designed to track performance of certain “event-driven” hedge funds over the same period of time. All references to the Dow Jones Credit Suisse HFI Event Driven Index (“DJ-CS HFI”) and HFRI Event-Driven Total Index (“HFRI”) reflect performance calculated through December 31, 2012. The DJ-CS HFI is an asset-weighted index and includes only funds, as opposed to separate accounts. The DJ-CS HFI uses the Dow Jones Credit Suisse database and consists only of event driven funds deemed to be “event-driven” by the index and that have a minimum of $50 million in assets under management, a minimum of a 12-month track record, and audited financial statements. The HFRI consists only of event driven funds with a minimum of $50 million in assets under management or a minimum of a 12-month track record. Both indices state that returns are reported net of all fees and expenses. Please see the glossary included in this prospectus beginning on page G-1 for a description of how these indices are calculated. While Third Point Partners L.P. has been compared here with the performance of well-known and widely recognized indices, the indices have not been selected to represent an appropriate benchmark for Third Point Partners L.P., whose holdings, performance and volatility may differ significantly from the securities that comprise the indices. |

5

Table of Contents

Competitive Strengths

Our operations are designed to achieve superior results through a combination of our reinsurance underwriting and our investment management strategies. We believe that our flexible business model has the potential to outperform through both reinsurance and capital markets cycles, which differentiates us from many of the reinsurers with whom we compete:

| • | Balanced Business Model: Our reinsurance underwriting strategy and portfolio construction and our investment strategy are designed to be complementary and to maximize the risk-taking opportunity set available to us. |

| • | Disciplined and Opportunistic Underwriting Approach: We will focus on reinsurance transactions where we can compete most efficiently through cultivating our relationships with intermediaries and insurance and reinsurance company clients, contributing to our ability to structure the coverage and lead underwrite the terms and conditions of the transactions on which we focus. We intend to manage reinsurance pricing cycles by reducing our risk-taking during periods of less favorable market conditions and potentially increasing our risk-taking when conditions improve. |

| • | Differentiated Investment Strategy: Our investment portfolio is managed by our investment manager, Third Point LLC, according to its event-driven opportunistic strategy, which we believe will lead to higher risk-adjusted returns than can be achieved by the portfolios of many of the reinsurers with whom we compete, which are typically concentrated in long-only, investment grade, shorter-term, fixed income securities. |

| • | Experienced Management Team: We have assembled an experienced management team led by industry veteran John Berger. Our management team’s breadth of underwriting experience and strong relationships with key intermediaries and insurance company clients provide access to a significant flow of reinsurance opportunities. |

| • | Strong Balance Sheet: We have a strong balance sheet with no debt, low operating leverage, no legacy liabilities, limited catastrophe exposure and minimal liquidity risk. |

Market Trends and Opportunities

The reinsurance markets in which we operate have historically been cyclical. During periods of excess underwriting capacity, as defined by the availability of capital, competition can result in lower pricing and less favorable policy terms and conditions for insurers and reinsurers. During periods of reduced underwriting capacity, pricing and policy terms and conditions are generally more favorable for insurers and reinsurers. Historically, underwriting capacity has been affected by several factors, including industry losses, the impact of catastrophes, changes in legal and regulatory guidelines, new entrants, investment results (including interest rate levels) and the credit ratings and financial strength of competitors.

While our management believes that pricing trends for the type of quota share business on which we focus have been relatively stable, there is significant underwriting capacity currently available, and we therefore believe market conditions will remain competitive in the near term. We believe there are several market developments, however, that indicate the potential for improving conditions in the medium term. These include improving pricing in several primary insurance lines of business which historically have flowed through to the reinsurance market, decelerating reserve releases from prior underwriting years, and the rapid decrease in recent periods in yields from the investment portfolios consisting mostly of long-only, investment grade, shorter-term, fixed income securities. These companies are now focused on the need for pricing increases to offset the drop in investment income or on increasing the risk profile of their investment portfolios, which consumes more of their risk capital.

6

Table of Contents

We anticipate that we will continue to see attractive opportunities for the following reasons: intermediaries and reinsurance buyers are increasingly familiar with Third Point Re, leading to increased submission volume in the lines and types of reinsurance we target; our primary insurance company clients are growing gross premium primarily through realizing rate increases and, to a lesser extent, adding to the number of policies they write and consequently increasing their need for quota share reinsurance; and the number of distressed situations for which our customized solutions may be helpful appears to be increasing.

We intend to continue to monitor market conditions to participate in future underserved or capacity constrained lines of business as they arise and offer products that we believe will generate favorable returns on equity over the long term. For instance, we recently reinsured certain obligations of a U.S. mortgage insurance company with respect to newly originated residential mortgages. The U.S. mortgage market suffered severe dislocation during the financial crisis of 2008 and as a result, mortgage insurers suffered severe losses and several needed to increase their capital both by means of new equity issuances and buying increased amounts of reinsurance. At the same time, we believe that the quality of the mortgages that mortgage insurers now insure has generally improved due to more rigorous lending standards imposed by banks and other industry participants. We believe this recent transaction presented an attractive opportunity because of the improved quality of newly originated mortgages, the underlying risk of the reinsurance contract, and the recapitalization of the mortgage insurer, which eliminated most of the residual servicer performance risk.

We also believe that increasingly competitive market conditions in the property catastrophe reinsurance market, due to an influx of capacity from collateralized reinsurance funds and separately capitalized reinsurance vehicles managed by traditional reinsurance companies, which are often termed “sidecars,” has affected business opportunities available to us in two ways: First, over 36.5% of our property and casualty gross premiums written since inception represented property quota share business, where the clients purchase separate catastrophe coverage from another reinsurer. To the extent these clients are able to access more attractively priced catastrophe reinsurance from another reinsurer, the profitability of their underlying business is increased, thereby improving their financial condition and reducing our residual counterparty credit risk. Second, while the expected margins generated by our Catastrophe Fund are expected to be negatively impacted by decreasing reinsurance pricing, the expected overall impact on our results is tempered by our catastrophe fund’s portfolio construction and focus on smaller, regional companies. These companies may have more limited access to collateralized reinsurance funds because of the size of their reinsurance programs and tend to favor reinsurance providers with whom they have had a long term relationship.

Summary Risk Factors

Our business is subject to numerous risks described in the section entitled “Risk Factors” and elsewhere in this prospectus. You should carefully consider these risks before making an investment. Some of these risks include:

| • | limited history of operations; |

| • | reinsurance underwriting and/or investment losses; |

| • | fluctuation in results of operations; |

| • | losses exceeding reserves; |

| • | dependence on Third Point LLC to implement our investment strategy; |

| • | risks associated with our investment strategy being greater than those faced by our competitors; |

| • | increased regulation or scrutiny of alternative investment advisers affecting our reputation; |

| • | potentially being deemed an investment company under U.S. federal securities law; |

| • | potential characterization of Third Point Reinsurance Ltd. and/or Third Point Re as a passive foreign investment company for U.S. federal income tax purposes; and |

| • | other risks and factors listed under “Risk Factors” and elsewhere in this prospectus. |

7

Table of Contents

Ownership and Certain Corporate Information

Founders Overview

Third Point Reinsurance Ltd. was incorporated on October 6, 2011. On December 22, 2011, KEP TP Holdings, L.P. and KIA TP Holdings, L.P., which are affiliates of Kelso & Company (collectively, “Kelso”) and Pine Brook L VR, L.P., an affiliate of Pine Brook Road Partners, LLC (collectively, “Pine Brook”, and Pine Brook and together with Kelso, the “Lead Investors” and each individually, a “Lead Investor”), Dowling Capital Partners I, L.P., an affiliate of Dowling Capital Management, LLC (collectively, “Dowling”), P RE Opportunities Ltd. (“PROL”), Third Point LLC, Daniel S. Loeb and affiliates associated with Mr. Loeb (collectively, the “Loeb Entities”) and our chief executive officer John R. Berger (collectively, the “Founders”), together with certain members of management, committed $523.0 million to capitalize Third Point Reinsurance Ltd.

Daniel S. Loeb

Mr. Loeb is a successful and experienced figure in the investment management industry. Mr. Loeb is the Chief Executive Officer of Third Point LLC, which he founded in 1995. Mr. Loeb leads portfolio management, risk management and research activities at Third Point LLC.

Before founding Third Point LLC, Mr. Loeb worked as a capital markets professional on both the buy and the sell sides for over a decade, gaining dedicated experience in distressed debt, high-yield bond sales, risk arbitrage, and private investments. He built a network of resources and gained an understanding of the investment spectrum that provides significant yields for his investors today.

Immediately before starting Third Point LLC, Mr. Loeb was Vice-President of high-yield bond sales at Citigroup. Previously, he was a Senior Vice-President in the distressed debt department at Jefferies & Co., where he worked as a bankruptcy analyst, bank loan trader, and as a distressed securities salesman. Before Jefferies, he was a risk arbitrage Analyst at Lafer Equity Investors. He began his finance career as an Associate in private equity at Warburg Pincus. Mr. Loeb graduated from Columbia University with an A.B. in economics.

Mr. Loeb has a majority of his investable net worth in Third Point LLC’s funds.

Kelso & Company

Kelso is one of the oldest and most established firms specializing in private equity. Since 1980, Kelso has invested in over 120 companies in a broad range of industry sectors, with aggregate initial capitalization at closing of over $45.0 billion. Kelso is currently investing its eighth investment partnership, Kelso Investment Associates VIII, L.P., with $5.1 billion of committed capital.

Pine Brook

Pine Brook is a New York-based investment firm that provides “business building” and other equity to new and growing businesses, primarily in the energy and financial services sectors. Over the course of their careers, Pine Brook’s financial services investment professionals have invested over $3.0 billion in more than 30 financial services companies, 17 of which were (re)insurance companies. Pine Brook’s experience in (re)insurance includes investments in companies such as Arch Capital Group Ltd., Catlin Group Limited, Lancashire Holdings Limited, Montpelier Re Holdings Ltd. and Renaissance Re Holdings Ltd.

8

Table of Contents

Dowling Capital Partners

Dowling Capital Partners is a private equity firm focused on investing in insurance and related services and distribution companies. Collectively, the management of Dowling Capital Partners has over 80 years of senior level industry experience, including insurance-related private equity investment management, investment banking, industry research and operational and board-level roles within major insurance, reinsurance and brokerage companies. V.J. Dowling, on behalf of his business partners and his family, has invested in 28 individual insurance-related private equity investments since 1998. Thirteen of these transactions involved the funding of start-up entities, including prominent (re)insurers Axis Capital Holdings Limited, Montpelier Re Holdings Ltd., Validus Group, Ariel Holdings Ltd. and Ironshore Insurance Ltd.

P RE Opportunities Ltd. and the Permal Group

PROL serves as an investment vehicle for certain of Permal Asset Management LLC’s discretionary advisory clients. Permal Asset Management LLC is a member of the Permal Group, a global alternative asset manager offering investment solutions through established funds and customized portfolios. Today, the Permal Group manages approximately $24 billion with a global investment team based in New York and London, and additional investment resources in Singapore and Paris. Established in 1973, the Permal Group is today part of the Legg Mason Group of Companies. Legg Mason is one of the world’s largest asset management firms with a diverse family of independent investment managers.

As of May 31, 2013, Kelso owned approximately 33.6% of our issued and outstanding common shares, on an as converted basis, Pine Brook owned approximately 16.9% of our issued and outstanding common shares, on an as converted basis, the Loeb Entities owned approximately 10.8% of our issued and outstanding common shares, on an as converted basis, PROL owned approximately 6.8% of our issued and outstanding common shares, on an as converted basis, Dowling owned approximately 2.1% of our issued and outstanding common shares, on an as converted basis and Mr. Berger owned approximately 1.4% of our issued and outstanding common shares, on an as converted basis, in each case after giving effect to the exercise of applicable options and warrants as described under “Security Ownership of Certain Beneficial Ownership of Certain Beneficial Owners, Management and Selling Shareholders”. Following the completion of this offering and assuming that the underwriters do not exercise their option to purchase additional shares, Kelso, Pine Brook, the Loeb Entities, Dowling, PROL and Mr. Berger will own approximately %, %, %, %, %, and %, of our issued and outstanding common shares, respectively on an as converted basis.

Our Corporate Information

We are incorporated in Bermuda and our corporate offices are located at The Waterfront, Chesney House, 96 Pitts Bay Road, Pembroke HM 08, Bermuda. Our telephone number is +1 (441) 542-3300. Our website address is http://www.thirdpointre.bm. None of the information contained on, or that may be accessed through, our website or any other website identified herein is part of, or incorporated into, this prospectus. All website addresses in this prospectus are intended to be inactive textual references only.

9

Table of Contents

The Offering

| Common shares offered by us |

shares |

| Common shares offered by selling shareholders |

shares |

| Total common shares offered |

shares |

| Option to purchase additional common shares |

The underwriters have a 30-day option to purchase an additional common shares from us and the selling shareholders to cover over-allotments, if any. |

| Common shares to be issued and outstanding after this offering |

shares (or shares if the over-allotment option is exercised in full) |

| Use of proceeds |

We intend to use the net proceeds from this offering for general corporate purposes, including the costs associated with being a public company. We will not receive any proceeds from the sale of shares by the selling shareholders. See “Use of Proceeds.” |

| Risk factors |

See “Risk Factors” for a discussion of factors you should carefully consider before deciding whether to invest in our common shares. |

| Conflicts of Interest |

One of the underwriters in offering, Sandler O’Neill & Partners, L.P. is considered to be an affiliate of Kelso for purposes of Rule 5121 of the Conduct Rules of FINRA. Since Kelso owns more than 10% of our issued and outstanding common shares, a “conflict of interest” would be deemed to exist under Rule 5121(f) (5)(B). Accordingly, we intend that this offering will be made in compliance with the applicable provisions of Rule 5121. Since Sandler O’Neill & Partners, L.P. is not primarily responsible for managing this offering, pursuant to FINRA Rule 5121, the appointment of a qualified independent underwriter is not necessary. As such, Sandler O’Neill & Partners, L.P. will not confirm sales to accounts in which it exercises discretionary authority without the prior written consent of the customer. |

| Dividend policy |

We do not currently expect to pay dividends on our common shares for the foreseeable future. |

| Proposed NYSE trading symbol |

TPRE |

As of the date of this prospectus, 78,432,132 of our common shares were issued and outstanding. See “Description of Share Capital.”

10

Table of Contents

Unless we indicate otherwise, the information in this prospectus:

| • | gives effect to the issuance of common shares in this offering; |

| • | assumes no exercise by the underwriters of their option to purchase additional shares; |

| • | assumes that the initial public offering price of our common shares will be $ per share (which is the midpoint of the price range set forth on the cover page of this prospectus); |

| • | does not give effect to shares issuable pursuant to warrants to purchase common shares held by certain of the Founders and certain entities that acted as advisors in connection with our initial capitalization, which following the completion of this offering will represent the right to receive an aggregate of 4,651,163 common shares, with a weighted average exercise price of $10.00 per share, assuming that this offering yields proceeds to us of not less than $215.7 million; |

| • | does not give effect to shares issuable pursuant to common share purchase options held by our directors and officers, with a weighted average exercise price of $13.20 per share, which following the completion of this offering will be exercisable (subject to vesting) for 10,666,139 common shares, assuming that this offering yields proceeds to us of not less than $215.7 million; |

| • | does not give effect to any future issuances of options to purchase up to 755,816 common shares available for grant under our current equity incentive compensation plan, assuming that this offering yields proceeds to us of not less than $215.7 million; |

| • | does not give effect to 619,300 currently issued and outstanding restricted shares; and |

| • | gives effect to amendments to our bye-laws to be adopted prior to the completion of this offering. |

11

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

The following table sets forth our summary financial data for the fiscal year ended December 31, 2012, the period from October 6, 2011 (which is our incorporation date) to December 31, 2011 and for the three months ended March 31, 2013 and March 31, 2012. We were capitalized in December 2011 and commenced underwriting operations in January 2012. Because we have a limited operating history, period-to-period comparisons of our results of operations for full fiscal years are not yet possible and may not be meaningful in the near future. We derived the financial data for the year ended December 31, 2012 and the period from October 6, 2011 (which is our incorporation date) to December 31, 2011 from our audited financial statements included elsewhere in this prospectus, which have been prepared in accordance with accounting principles generally accepted in the United States, or U.S. GAAP. The financial data for the three months ended March 31, 2012 and March 31, 2013 have been derived from our unaudited condensed consolidated financial statements included elsewhere in this prospectus. These historical results are not necessarily indicative of future results, and the unaudited interim results for the three months ended March 31, 2013 are not necessarily indicative of results that may be expected for the full year ended December 31, 2013. You should read the following summary financial data together with our audited financial statements and related notes included elsewhere in this prospectus and the information under “Selected Consolidated Financial and Other Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| Three Months Ended March 31, |

Year

Ended December 31, 2012 |

Period from October 6, 2011 to December 31, 2011 |

||||||||||||||

| 2013 | 2012 | |||||||||||||||

| (In thousands, except share and per share data and ratios) | ||||||||||||||||

| Selected Statement of Income Data: |

||||||||||||||||

| Gross premiums written |

$ | 96,020 | $ | 92,650 | $ | 190,374 | $ | — | ||||||||

| Net premiums earned |

33,541 | 13,837 | 96,481 | |||||||||||||

| Net investment income |

80,691 | 33,848 | 136,422 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues |

114,232 | 47,685 | 232,903 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss and loss adjustment expenses incurred, net |

18,638 | 12,285 | 80,306 | — | ||||||||||||

| Acquisition costs, net |

13,073 | 712 | 24,604 | — | ||||||||||||

| General and administrative expenses |

7,008 | 4,159 | 27,376 | 1,130 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total expenses |

38,719 | 17,156 | 132,286 | 1,130 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) including non-controlling interests |

75,513 | 30,529 | 100,617 | (1,130 | ) | |||||||||||

| Income attributable to non-controlling interests |

(1,083 | ) | (306 | ) | (1,216 | ) | — | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | 74,430 | $ | 30,223 | $ | 99,401 | $ | (1,130 | ) | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings (loss) per share(1): |

||||||||||||||||

| Basic |

$ | 0.95 | $ | 0.39 | $ | 1.27 | $ | (0.01 | ) | |||||||

| Diluted |

$ | 0.85 | $ | 0.35 | $ | 1.14 | $ | (0.01 | ) | |||||||

| Weighted average number of ordinary shares: |

||||||||||||||||

| Basic |

78,432,132 | 78,432,132 | 78,432,132 | 78,432,132 | ||||||||||||

| Diluted |

87,777,462 | 85,335,404 | 87,253,760 | 78,432,132 | ||||||||||||

| Selected ratios: |

||||||||||||||||

| Property and casualty reinsurance – underwriting ratios(2): |

||||||||||||||||

| Loss ratio(3) |

57.1 | % | 88.8 | % | 83.2 | % | n/a | |||||||||

| Acquisition cost ratio(4) |

39.8 | % | 5.1 | % | 25.5 | % | n/a | |||||||||

| General and administrative expense ratio(5) |

19.1 | % | 30.1 | % | 26.8 | % | n/a | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Combined ratio(6) |

|

116.0 |

% |

124.0 | % | 135.5 | % | n/a | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net investment return(7) |

8.7 | % | 4.5 | % | 17.7 | % | n/a | |||||||||

| (1) | Basic earnings (loss) per share are based on the weighted average number of common shares and participating securities outstanding during the period. The weighted average number of common shares excludes the dilutive effect of warrants currently held by the Founders and Aon Corporation, or Aon, which acted as an advisor in connection with our initial capitalization, which following the |

12

Table of Contents

| completion of this offering will represent the right to receive an aggregate of 4,651,165 common shares, assuming that this offering yields proceeds to us of not less than $215.7 million, options held by our directors and officers, which, following the completion of this offering will be exercisable (subject to vesting) for 10,666,139 common shares, assuming that this offering yields net proceeds to us of not less than $215.7 million, and 619,300 unvested restricted shares. |

| (2) | Underwriting ratios are for the property and casualty reinsurance segment only. See additional information in Note 23 of the Notes to Consolidated Financial Statements. |

| (3) | Loss ratio is calculated by dividing loss and loss adjustment expenses incurred, net, by net premiums earned. |

| (4) | Acquisition cost ratio is calculated by dividing acquisition costs, net by net premiums earned. |

| (5) | General and administrative expense ratio is calculated by dividing general and administrative expenses by net premiums earned. |

| (6) | Combined ratio is calculated by dividing the sum of loss and loss adjustment expenses incurred, net, acquisition costs, net and general and administrative expenses by net premiums earned. |

| (7) | Net investment return represents the return on our investments managed by Third Point LLC, net of fees. |

| As of March 31, 2013 |

As of December, 31 | |||||||||||

| 2012 | 2011 | |||||||||||

| (In thousands, except share and per share data) |

||||||||||||

| Selected Balance Sheet Data: |

||||||||||||

| Total investments in securities and commodities |

$ | 968,976 | $ | 937,690 | $ | — | ||||||

| Cash and cash equivalents(1) |

37,739 | 34,005 | 603,841 | |||||||||

| Restricted cash and cash equivalents |

90,557 | 77,627 | — | |||||||||

| Securities purchased under an agreement to sell |

38,110 | 60,408 | — | |||||||||

| Reinsurance balances receivable, net |

136,998 | 84,280 | — | |||||||||

| Deferred acquisition costs, net |

53,270 | 45,383 | — | |||||||||

| Total assets |

1,498,197 | 1,402,017 | 605,263 | |||||||||

| Deposit liability(2) |

51,116 | 50,446 | — | |||||||||

| Unearned premium reserves |

153,878 | 93,893 | — | |||||||||

| Losses and loss adjustment expense reserves |

75,321 | 67,271 | — | |||||||||

| Securities sold, not yet purchased, at fair value |

149,071 | 176,454 | — | |||||||||

| Total liabilities |

527,539 | 473,696 | 19,838 | |||||||||

| Shareholders’ equity attributable to shareholders(3) |

944,726 | 868,544 | 585,425 | |||||||||

| Non-controlling interests |

25,932 | 59,777 | — | |||||||||

| Total shareholders’ equity |

$ | 970,658 | $ | 928,321 | $ | 585,425 | ||||||

| Book value per share data: |

||||||||||||

| Book value per share(4) |

$ | 12.05 | $ | 11.07 | $ | 9.73 | ||||||

| Diluted book value per share(5) |

$ | 11.76 | $ | 10.89 | $ | 9.73 | ||||||

| Selected ratios: |

||||||||||||

| Growth in diluted book value per share(6) |

8.0 | % | 11.9 | % | n/a | |||||||

| Return on beginning shareholders’ equity(7) |

8.6 | % | 13.0 | % | n/a | |||||||

| (1) | Cash and cash equivalents consists of cash, cash held with investment managers and other short-term, highly liquid investments with original maturity dates of ninety days or less. |

| (2) | Management exercises significant judgment in determining whether contracts should be accounted for as reinsurance contracts or deposit contracts. During 2012, one contract was deemed to not transfer sufficient insurance risk and has been accounted for using the deposit method of accounting. Using the deposit method of accounting, a deposit liability, rather than written premium, is initially recorded based upon the consideration received less any explicitly identified premiums or fees. In subsequent periods, the deposit liability is adjusted by calculating the effective yield on the deposit to reflect actual payments to date and future expected payments. |

| (3) | Shareholders’ equity attributable to shareholders and total shareholders’ equity as of December 31, 2011 is reflected net of subscriptions receivable of $177.5 million in accordance with SEC Regulation S-X. |

| (4) | Book value per share is a non-GAAP financial measure. Book value per share is calculated by dividing shareholders’ equity attributable to shareholders, adjusted for subscriptions receivable, by the number of issued and outstanding shares at period end. See the reconciliation under “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Book Value Per Share and Fully Diluted Book Value Per Share.” |

13

Table of Contents

| (5) | Diluted book value per share is a non-GAAP financial measure. Diluted book value per share is calculated by dividing shareholders’ equity attributable to shareholders, adjusted for subscriptions receivable, and adjusted to include unvested restricted shares and the exercise of all in-the-money options and warrants. For purposes of this calculation, the market share price is assumed to be equal to the fully diluted book value per share. See the reconciliation under “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Book Value Per Share and Fully Diluted Book Value Per Share.” |

| (6) | Growth in diluted book value per share is calculated by taking the change in diluted book value per share divided by the beginning of period diluted book value per share. |

| (7) | Return on beginning shareholders’ equity as presented is a non-GAAP financial measure. Return on beginning shareholders’ equity is calculated by dividing net income by the beginning of year total shareholders’ equity. For purposes of determining December 31, 2011 equity, we add back the impact of subscriptions receivable to total shareholders’ equity. Management believes this adjustment more fairly presents the return on equity over the period. |

14

Table of Contents

Investing in our common shares involves a high degree of risk. You should consider and read carefully all of the risks and uncertainties described below, as well as other information included in this prospectus, including our consolidated financial statements and related notes appearing at the end of this prospectus, before making an investment decision. The risks described below are not the only ones facing us. The occurrence of any of the following risks or additional risks and uncertainties not presently known to us or that we currently believe to be immaterial could materially and adversely affect our business, financial condition or results of operations. In that case, the trading price of our common shares could decline, and you may lose all or part of your original investment. This prospectus also contains forward-looking statements and estimates that involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements as a result of specific factors, including the risks and uncertainties described below.

Risks Relating to Our Business

We are a start-up operation with limited historical information available for investors to evaluate our performance or a potential investment in our shares.

We have a limited history of operations. We were incorporated on October 6, 2011 and began underwriting reinsurance transactions on January 1, 2012. As a result, there is limited historical information available to help prospective investors evaluate our performance or an investment in our shares.

In general, reinsurance and insurance companies in their initial stages of development present substantial business and financial risks and may suffer significant losses. They must develop business relationships, establish operating procedures, hire staff, install information technology systems, implement management processes and complete other tasks appropriate for the conduct of their intended business activities. In particular, our ability to implement our reinsurance underwriting strategy will depend on, among other things:

| • | our ability to attract clients; |

| • | our ability to attract and retain personnel with sufficient underwriting, actuarial and accounting and finance expertise; |

| • | our ability to maintain at least an A- (Excellent) rating from A.M. Best or a similar financial strength rating from one or more other ratings agencies; |

| • | our ability to evaluate the risks we assume under reinsurance contracts that we write; |

| • | our reliance on third parties to provide certain services; and |

| • | the risk of being deemed a passive foreign investment company or an investment company if we are deemed to not be in the active conduct of an insurance business or to not be predominantly engaged in an insurance business. See ‘‘Risks Relating to Insurance and Other Regulations—We are subject to the risk of becoming an investment company under U.S. federal securities law’’ and “Risks Relating to Taxation—United States persons who own our shares may be subject to United States federal income taxation on our undistributed earnings and may recognize ordinary income upon disposition of shares.” |

We cannot assure you that there will be sufficient demand for the reinsurance products we plan to write to support our planned level of operations, or that we will accomplish the tasks necessary to implement our business strategy.

15

Table of Contents

Our operational structure is currently being developed.

We are in the process of developing and implementing our operational structure and enterprise risk management framework, including exposure management, financial reporting, information technology and internal controls, with which we will conduct our business activities. Our operations are currently supplemented by manual processes, and we expect to migrate over time to a fully-automated control system. While we utilize manual processes, our controls may not be adequate to identify or eliminate risks. There can be no assurance that the development of our operational structure or the implementation of our enterprise risk management framework will proceed smoothly or on our projected timetable or achieve the aforementioned goals.

The preparation of our financial statements requires us to make many estimates and judgments, which are even more difficult than those made in a mature company, and which, if inaccurate, could cause volatility in our results.

Our consolidated financial statements have been prepared in accordance with U.S. GAAP. Management believes the item that requires the most subjective and complex estimates is the reserve for losses and loss expenses. Due to our relatively short operating history, loss experience is limited and reliable evidence of changes in trends of numbers of claims incurred, average settlement amounts, numbers of claims outstanding and average losses per claim may take years to develop. In addition, the possibility of future litigation or legislative change that may affect interpretation of policy terms further increases the degree of uncertainty in the reserving process. The uncertainties inherent in the reserving process, together with the potential for unforeseen developments, including changes in laws and the prevailing interpretation of policy terms, may result in losses and loss expenses materially different from the reserves initially established. Changes to prior year reserves will affect current underwriting results by increasing net income if the prior year reserves prove to be redundant or by decreasing net income if the prior year reserves prove to be insufficient. We expect volatility in results in periods in which significant loss events occur because U.S. GAAP does not permit insurers or reinsurers to reserve for loss events until they have occurred and are expected to give rise to a claim. As a result, we are not allowed to record contingency reserves to account for expected future losses. We anticipate that claims arising from future events may require the establishment of substantial reserves from time to time.

Our results of operations fluctuate from period to period and may not be indicative of our long-term prospects.

The performance of our reinsurance operations and our investment portfolio fluctuate from period to period. Fluctuations result from a variety of factors, including:

| • | reinsurance contract pricing; |

| • | our assessment of the quality of available reinsurance opportunities; |

| • | the volume and mix of reinsurance products we underwrite; |

| • | loss experience on our reinsurance liabilities; |

| • | our ability to assess and integrate our risk management strategy properly; and |

| • | the performance of our investment portfolio. |

In particular, we seek to underwrite products and make investments to achieve favorable return on equity over the long term. In addition, our opportunistic nature and focus on long-term growth in book value result in fluctuations in total premiums written from period to period as we concentrate on underwriting contracts that we believe will generate better long-term, rather than short-term, results. Accordingly, our short-term results of operations may not be indicative of our long-term prospects.

16

Table of Contents

Established competitors with greater resources may make it difficult for us to effectively market our products or offer our products at a profit.

The reinsurance industry is highly competitive. We compete with major reinsurers, many of which have substantially greater financial, marketing and management resources than we do, as well as other potential providers of capital willing to assume insurance or reinsurance risk. Competition in the types of business that we underwrite is based on many factors, including:

| • | price of reinsurance coverage; |

| • | the general reputation and perceived financial strength of the reinsurer; |

| • | relationships with reinsurance brokers; |

| • | terms and conditions of products offered; |

| • | ratings assigned by independent rating agencies; |

| • | speed of claims payment and reputation; and |

| • | the experience and reputation of the members of our underwriting team in the particular lines of reinsurance we seek to underwrite. |

Our competitors include, among others, Tokio Millennium Re Ltd., Endurance Specialty Reinsurance Ltd., AXIS Specialty Limited, Arch Reinsurance Ltd., ACE Tempest Reinsurance Ltd., Transatlantic Reinsurance Company and S.A.C. Re, Ltd. In addition, Greenlight Reinsurance, Ltd. has a business model similar to ours, and we expect to compete with them in many lines of business and geographies. In addition, in the future, we may have to compete for the type of reinsurance we intend to underwrite with new start-up companies that have a business model similar to ours.

We cannot assure you that we will be able to compete successfully in the reinsurance market. Our failure to compete effectively would significantly and negatively affect our financial condition and results of operations and may increase the likelihood that we are deemed to be a passive foreign investment company or an investment company. See “Risks Relating to Insurance and Other Regulations—We are subject to the risk of becoming an investment company under U.S. federal securities law” and “Risks Relating to Taxation—United States persons who own our shares may be subject to United States federal income taxation on our undistributed earnings and may recognize ordinary income upon disposition of shares.”

If actual renewals of our existing contracts do not meet expectations, our premiums written in future years and our future results of operations could be materially adversely affected.

Many of our contracts are generally written for a one-year term. In our financial forecasting process, we make assumptions about the renewal of our prior year’s contracts. The insurance and reinsurance industries have historically been cyclical businesses with intense competition, often based on price. If actual renewals do not meet expectations or if we choose not to write on a renewal basis because of pricing conditions, our premiums written in future years and our future operations would be materially adversely affected. This risk is especially prevalent in the first quarter of each year when a larger number of reinsurance contracts are subject to renewal.

The inherent uncertainty of models and the use of such models as a tool to evaluate risk may have an adverse effect on our financial results.

We license analytic and modeling capabilities software from third parties to facilitate our pricing, capital modeling software and objective risk assessment relating to risks in our reinsurance portfolio. These models help us to control risk accumulation, inform management and other stakeholders of capital requirements and to improve the risk/return profile or minimize the amount of capital required to cover the risks in each reinsurance contract in our overall portfolio of reinsurance contracts. However, given the inherent uncertainty of modeling techniques and the application of such techniques, these models and databases may not accurately address the emergence of a variety of matters which might be deemed to impact certain of our coverages. Accordingly, these models may understate the exposures we are assuming and our financial results may be adversely impacted, perhaps significantly.

17

Table of Contents

Operational risks, including human or systems failures, are inherent in our business.

Operational risks and losses can result from many sources including fraud, errors by employees, failure to document transactions properly or to obtain proper internal authorization, failure to comply with regulatory requirements or information technology failures.

We believe our modeling, underwriting and information technology and application systems are critical to our business and reputation. Moreover, our technology and applications are an important part of our underwriting process and our ability to compete successfully. We have licensed certain systems and data from third parties. We cannot be certain that we will have access to these, or comparable systems, or that our technology or applications will continue to operate as intended. In addition, we cannot be certain that we would be able to replace these systems without slowing our underwriting response time. A major defect or failure in our internal controls or information technology and application systems could result in management distraction, harm to our reputation, a loss or delay of revenues or increased expense.

Technology breaches or failures, including those resulting from a malicious cyber-attack on us or our business partners and service providers, could disrupt or otherwise negatively impact our business.

We rely on information technology systems to process, transmit, store and protect the electronic information, financial data and proprietary models that are critical to our business. Furthermore, a significant portion of the communications between our employees and our business, banking and investment partners depends on information technology and electronic information exchange. Like all companies, our information technology systems are vulnerable to data breaches, interruptions or failures due to events that may be beyond our control, including, but not limited to, natural disasters, theft, terrorist attacks, computer viruses, hackers and general technology failures.

We believe that we have established and implemented appropriate security measures, controls and procedures to safeguard our information technology systems and to prevent unauthorized access to such systems and any data processed or stored in such systems, and we periodically evaluate and test the adequacy of such systems, controls and procedures. In addition, we have established a business continuity plan which is designed to ensure that we are able to maintain all aspects of our key business processes functioning in the midst of certain disruptive events, including any disruptions to or breaches of our information technology systems. Our business continuity plan is routinely tested and evaluated for adequacy. Despite these safeguards, disruptions to and breaches of our information technology systems are possible and may negatively impact our business.

It is possible that insurance policies we have in place with third parties would not entirely protect us in the event that we experienced a breach, interruption or widespread failure of our information technology systems. Furthermore, we have not secured insurance coverage designed to specifically protect us from an economic loss resulting from such events.

Although we have never experienced any known or threatened cases involving unauthorized access to our information technology systems or unauthorized appropriation of the data contained within such systems, we have no assurance that such technology breaches will not occur in the future.

We may not be able to manage our growth effectively.

We intend to grow our business in the future, which could require additional capital, systems development and skilled personnel. We cannot assure you that we will be able to meet our capital needs, expand our systems effectively, allocate our human resources optimally, identify and hire qualified employees or incorporate effectively the components of any businesses we may acquire in our effort to achieve growth. Additionally, as we grow, the ability of our management to source sufficient reasonably priced reinsurance business in the segments we target may be limited. The failure to manage our growth effectively could have a material adverse effect on our business, financial condition, and results of operations.

18

Table of Contents

Our losses may exceed our loss reserves, which could significantly and negatively affect our business.

Our results of operations and financial condition depends upon our ability to assess accurately the potential losses associated with the risks we reinsure. Reserves are estimates of claims an insurer ultimately expects to pay, based upon facts and circumstances known at the time, predictions of future events, estimates of future trends in claim severity and other variable factors. The inherent uncertainties of estimating loss reserves generally are greater for reinsurance companies as compared to primary insurers, primarily due to:

| • | the lapse of time from the occurrence of an event to the reporting of the claim and the ultimate resolution or settlement of the claim; |

| • | the diversity of development patterns among different types of reinsurance treaties; and |

| • | the necessary reliance on the client for information regarding claims. |

Actual losses and loss adjustment expenses paid may deviate substantially from the estimates of our loss reserves, to our detriment. If we determine our loss reserves to be inadequate, we will increase our loss reserves with a corresponding reduction in our net income in the period in which we identify the deficiency. Such a reduction would negatively affect our results of operations. If our losses exceed our loss reserves, our financial condition may be significantly and negatively affected.