Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Virolab, Inc. | Financial_Report.xls |

| EX-31.1 - EXHBIT 31.1 - Virolab, Inc. | ex311.htm |

| EX-32.1 - EXHBIT 32.1 - Virolab, Inc. | ex321.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended March 31, 2013

OR

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

|

Commission file number: 000-54059

VIROLAB, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

27-2787170

|

|

|

State or other jurisdiction of incorporation or organization

|

(I.R.S. Employer Identification No.)

|

|

|

951 Mariners Island Blvd, Suite 300, San Mateo, California

|

94404

|

|

|

(Address of principal executive office)

|

(Zip Code)

|

Registrant’s telephone number, including area code (650) 283-2653

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

|

None

|

None

|

| Securities registered pursuant to Section 12(g) of the act: |

| Common Stock, par value $0.0001 per share |

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

Non-accelerated filer o

|

Smaller reporting company x

|

|

(Do not check if a smaller reporting company)

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes No x

The aggregate market value of the voting stock held by non-affiliates of the registrant was $0 as of March 31, 2012 because there was no trading market for the registrant’s securities and all outstanding stock was owned by an affiliate.

On July 14, 2013, there were 25,350,000 shares of the registrant’s common stock outstanding.

1

TABLE OF CONTENTS

|

PART I

|

||

|

ITEM 1.

|

BUSINESS

|

3 |

|

ITEM 1A.

|

RISK FACTORS

|

12 |

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

12 |

|

ITEM 2.

|

PROPERTIES

|

12 |

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

12 |

|

ITEM 4.

|

(REMOVED AND RESERVED)

|

13 |

|

PART II

|

||

|

ITEM 5.

|

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

13 |

|

ITEM 6.

|

SELECTED FINANCIAL DATA

|

13 |

|

ITEM 7.

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION

|

13 |

|

ITEM 7A.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

18 |

|

ITEM 8.

|

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

18 |

|

ITEM 9.

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

|

19 |

|

ITEM 9B.

|

OTHER INFORMATION

|

19 |

|

PART III

|

||

|

ITEM 10.

|

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

20 |

|

ITEM 11.

|

EXECUTIVE COMPENSATION

|

21 |

|

ITEM 12.

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

22 |

|

ITEM 13.

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE

|

23 |

|

ITEM 14

|

PRINCIPAL ACCOUNTANT FEES AND SERVICES

|

23 |

|

PART IV

|

||

|

ITEM 15.

|

EXHIBITS, FINANCIAL STATEMENT SCHEDULES

|

24 |

|

SIGNATURES

|

25 | |

2

PART I

ITEM 1. BUSINESS

This report contains forward-looking statements. In some cases, these statements may be identified by terminology such as “anticipates,” “believes,” “continue,” “estimates,” “expects,” “may,” “plans,” “potential,” “predicts,” “should,” “will,” and other comparable terminology. These forward-looking statements are subject to known and unknown risks, uncertainties and other factors which may cause actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. These forward-looking statements were based on various factors and were derived utilizing numerous assumptions and other factors that could cause our actual results to differ materially from those in the forward-looking statements. These factors include, but are not limited to, our ability to develop our operations, our ability to satisfy our obligations, our ability to raise capital as necessary, our ability to generate revenues and pay our operating expenses, our ability to consummate the acquisition of additional assets, economic, political and market conditions and fluctuations, government and industry regulation, U.S. and global competition, and other factors. Most of these factors are difficult to predict accurately and are generally beyond our control. You should consider the areas of risk described in connection with any forward-looking statements that may be made herein. Readers are cautioned not to place undue reliance on these forward-looking statements and readers should carefully review this report in its entirety, including the risks described in Item 1A - "Risk Factors" as well as the risk factors described in our other filings with the Securities and Exchange Commission. Except for our ongoing obligations to disclose material information under the Federal securities laws, we undertake no obligation to update any of our forward-looking statements. These forward-looking statements speak only as of the date of this report, and you should not rely on these statements without also considering the risks and uncertainties associated with these statements and our business. “We,” “us,” “our,” the “Company,” “Accelerated Acquisitions X, Inc.,” and “Virolab” as used in this report refer to Virolab, Inc., a Delaware corporation..

None of the Company’s securities are registered for resale with the Securities and Exchange Commission. The outstanding shares of common stock may only be resold through registration under the Securities Act of 1933, or under an applicable exemption from registration.

From inception on May 4, 2010, Accelerated Acquisitions X, Inc. was organized as a vehicle to investigate and, if such investigation warranted, acquire a target company or business seeking the perceived advantages of being a publicly held corporation. Our principal business objectives were to achieve long-term growth potential through a combination with a business rather than immediate, short-term earnings.

On May 4, 2010, the Company sold 5,000,000 shares of Common Stock to Accelerated Venture Partners, LLC, or AVP, for an aggregate investment of $2,000. The Company sold these shares of Common Stock under the exemption from registration provided by Section 4(2) of the Securities Act.

On February 27, 2011, Virolab S de RL de CV (the “Purchaser” or “Virolab Mexico”) acquired 22,350,000 shares of the Company’s common stock par value $0.0001 for a price of $0.0001 per share. At the same time, AVP tendered 3,500,000 of their 5,000,000 shares of the Company’s common stock for cancellation. In addition, AVP received an option to purchase 1,500,000 shares of the Company’s common stock for a price of $0.0001 per share, which AVP immediately exercised. The 1,500,000 shares purchased under option by AVP are subject to repurchase by the Company as described in the February 27, 2011 Consulting Services Agreement disclosure below. Following these transactions, Virolab S de RL de CV., owned 88.2% of the Company’s 25,350,000 issued and outstanding shares of common stock and AVP owned the remaining 11.8%. Simultaneously with the share purchase, Ricardo Rosales, PhD was appointed to the Company’s Board of Directors. Such action represents a change of control of the Company.

Prior to the purchase of the shares, the Purchaser was not affiliated with the Company. However, the Purchaser will be deemed an affiliate of the Company after the share purchase as a result of its stock ownership interest in the Company and position on the Board of Directors. The purchase of the shares by the Purchaser was completed pursuant to a written Subscription Agreement with the Company. The purchase was not subject to any other terms and conditions other than the sale of the shares in exchange for the cash payment. Following the sale of common stock to the Purchaser, the Company was still seeking to achieve its objective of acquiring a target company or business.

3

On February 27, 2011, the Company entered into a Consulting Services Agreement with AVP. The agreement requires AVP

to provide the Company with certain advisory services that include reviewing the Company’s business plan, identifying and introducing prospective financial and business partners, and providing general business advice regarding the Company’s operations and business strategy in consideration of (a) an option granted by the Company to AVP to purchase 1,500,000 shares of the Company’s common stock at a price of $0.0001 per share (the “AVP Option”) (which was immediately exercised by the holder) subject to a repurchase option granted to the Company to repurchase the shares at a price of $0.0001 per share in the event the Company fails to complete funding as detailed in the agreement subject to the following milestones:

|

●

|

Milestone 1 – Company’s right of repurchase will lapse with respect to 60% of the shares upon securing $5 million in available cash from funding;

|

|

●

|

Milestone 2 – Company’s right of repurchase will lapse with respect to 40% of the Shares upon securing $10 million in available cash (inclusive of any amounts attributable to Milestone 1);

|

and (b) cash compensation at a rate of $66,667 per month. The payment of the cash compensation is subject to the Company’s achievement of certain designated milestones, specifically, cash compensation of $400,000 is due consultant upon the achievement of Milestone 1, and an additional $400,000 is due upon the achievement of Milestone 2. Upon achieving each Milestone, the cash compensation is to be paid to consultant in the amount then due at the rate of $66,667 per month. The total cash compensation to be received by the consultant is not to exceed $800,000 unless Virolab receives an amount of funding in excess of the amount specified in Milestone 2. If the Company receives equity or debt financing that is an amount less than Milestone 1, in between any of the above Milestones or greater than the above Milestones, the cash compensation earned by the Consultant under this Agreement will be prorated according to the above Milestones. The Company also has the option to make a lump sum payment to AVP in lieu of the monthly cash payments.

On March 8, 2011, the Company entered into a Licensing Agreement (“Licensing Agreement”) with Virolab Nevada, LLC (“Licensor”) pursuant to which the Company was granted an exclusive, non-transferrable worldwide license for the commercial rights to an investigational therapeutic vaccine for the human papillomavirus, or HPV, and HPV-related cancers and a specific blood test for HPV (the “Technology”). Rather than acquiring an operating company, the Company acquired an exclusive license to trade secrets, patents, know-how and other intellectual property that had been developed in Mexico. We will lose our rights to the Technology that we licensed if we do not raise at least $0.5 million for its future development before March 8, 2012, if we do not raise at least $1.0 million for its future development before March 8, 2013, and if we do not raise at least $2.0 million for its future development before March 8, 2014. Although the Company did not spend the $0.5 million additional funds per the Licensing Agreement before March 8, 2012, we have not received a default letter and as of March 31, 2013 the Company was in negotiations to extend the terms of the Agreement.

Prior to the licensing transaction entered into on March 8, 2011, the Company was a “blank check company.” Shares of the Company’s common stock are not registered under the securities laws of any state or other jurisdiction, and accordingly there is no public trading market for our common stock. Therefore, outstanding shares of our common stock cannot be offered, sold, pledged or otherwise transferred unless subsequently registered pursuant to, or exempt from registration under, the Securities Act and any other applicable federal or state securities laws or regulations. Shares of our common stock including shares issued to AVP cannot be sold under the exemptions from registration provided by Rule 144 under or Section 4(1) of the Securities Act (“Rule 144”) for at least 12 months after the Company ceases to be a “shell company,” provided the Company otherwise is in compliance with the applicable rules and regulations. Compliance with the criteria for securing exemptions under federal securities laws and the securities laws of the various states is extremely complex, especially in respect of those exemptions affording flexibility and the elimination of trading restrictions in respect of securities received in exempt transactions and subsequently disposed of without registration under the Securities Act or state securities laws.

AVP has indicated to the Company that it will pay the on-going administrative expenses of the Company until Virolab enters into a financing transaction. These on-going administrative expenses differ from the services covered in the Consulting Services Agreement. Through March 31, 2013, the Company has incurred approximately $110,675 of expenses related to its operations, and of this amount approximately $108,795 remained due to AVP. Virolab currently does not pay any cash compensation to its directors, officers or employees, but plans to do so if it succeeds in securing additional financing.

Throughout this document, we refer to our therapeutic vaccine as “investigational” or as a “candidate” because it has not received approval for commercial sale anywhere in the world, and we also refer to the investigational vaccine as “therapeutic” because it is designed to treat an existing viral infection and the resulting cervical lesions. Most of the currently approved vaccines for all diseases are not therapeutic, but instead are designed to prevent an infection from occurring before a patient is actually exposed to a virus or other infectious agent. We believe the intended therapeutic nature of our vaccine candidate differentiates it from other vaccines.

4

We believe that the HPV therapeutic vaccine technology that we have in development has the potential to be the first therapeutic to clear pre-cancerous and cancerous lesions of the Cervix along with the underlying HPV viral infection. This belief is based on the results of two phase 2 clinical trials and one phase 3 clinical conducted in Mexico in which cancerous and pre-cancerous cervical lesions were eliminated or regressed in 88% to 97% of the patients. In addition, detectable HPV virus was eliminated from approximately half of the 1,246 patients treated in the three trials. All studies showed the vaccine candidate to be well tolerated, although headaches and other flu-like symptoms appeared in some of the patients. More detailed results from the trials conducted by Virolab Mexico are contained in the section “Clinical Trials of Therapeutic Vaccine Candidate” below.

In addition to the therapeutic vaccine candidate, Virolab has licensed rights to a specific blood-based diagnostic test for HPV that is in development. Currently, diagnosis of an infection with HPV requires a gynecological examination and testing of cervical tissue samples. We believe that a diagnosis from a simple blood draw will be less expensive and more convenient for patients.

The Company is evaluating its options to commercialize its therapeutic vaccine candidate and diagnostic test. These product candidates have not been approved for commercial sale anywhere in the world, and each country has different requirements for approval, so the commercialization process is likely to be lengthy and complex. The Company may employ different strategies in different areas of the world, such as sublicensing development and commercialization rights for some territories while retaining rights for other territories. Based on the historical work of Virolab Mexico in the country of Mexico, the Company believes that the path to obtain government approval may be shorter in the Latin America countries.

The Company will not be able to commercialize either its vaccine candidate or its diagnostic test without additional capital. The Company is evaluating various means of raising this capital, including through the sale of equity securities, licensing agreements or other means. If the Company does not raise additional funds of at least $2 million for the advancement of its technology over the next three years it will lose its rights to the technology. The Company plans to seek at least $10 million of capital within the next 12 months, and plans to use these funds to determine the FDA’s requirements for approval of its vaccine candidate, begin working on these requirements, file patents on its technology, broaden its pipeline of investigational drugs, vaccines and/or diagnostics, establish a biotechnology laboratory, and continue the process of seeking approval of its vaccine candidate and diagnostic test outside of the United States. The Company is not presently able to allocate the specific costs for its plans because it does not yet know the requirements for approval of either its vaccine candidate or its diagnostic test.

HPV and Cervical Cancer Background

According to The World Health Organization, or WHO, cervical cancer is the second most frequent form of cancer among women in the world and second most frequent among women aged 15 – 44 years. WHO also reports that about 300 million women, about 10% of women worldwide, are estimated to be infected with HPV at a given time and that virtually 100% of cervical cancer cases are caused by HPV infection. HPV is transmitted through sexual contact and is extremely contagious. While the WHO estimates that an equal number of men are infected with HPV, in general HPV infected men do not show symptoms, although genital warts and codylomata may appear.

HPV-infected women can develop pre-cancerous cervical lesions of increasing seriousness known as CIN 1, CIN 2, and CIN 3 which can develop into cancer and, if they do, can ultimately cause the death of the patient. Since the virus may foster the growth of cancer cells anytime from six months to 15 years after infection, women at risk currently have to undergo gynecological testing and pap-smears for early detection of potential cancer at least once a year.

Under current treatment practices, when a cervical lesion is detected, outpatient surgery is generally performed to remove the lesion. The underlying HPV infection, however, remains and new lesions can develop. Therefore, recommended check up frequency is increased to twice a year for these patients.

Virolab’s goal is to complete the clinical development of its therapeutic vaccine candidate, and seek regulatory approval to commercialize the therapeutic vaccine throughout the world. We believe that a vaccine which has potential to clear an underlying HPV infection from patients would be a cost effective and advantageous alternative to surgery that does not clear the underlying viral infection from patients. However, we must raise additional funds, conduct additional positive clinical trials and establish qualified manufacturing facilities in order for us to meet this goal of commercializing the vaccine candidate.

5

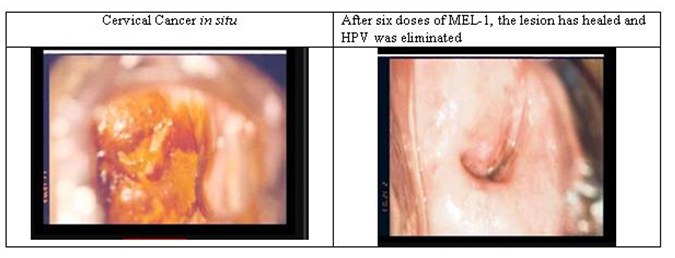

Virolab’s Therapeutic Vaccine Candidate

Below is an example of a cervical cancer before and after treatment with the investigational therapeutic vaccine candidate exclusively licensed to Virolab. This illustration was taken from one of the women that have been treated with the vaccine candidate in clinical trials.

The technology licensed to Virolab involves the key process of developing production of the therapeutic vaccine candidate, which is referred to as MEL-1. MEL-1 is derived from the smallpox virus vaccine MVA, which was originally developed in Germany during the 1940s. The World Health Organization has approved MVA for use in other human vaccines in the early 1990s (note that this does not imply that the U.S. Food and Drug Administration, or FDA, or any other governmental regulatory agency will approve any vaccine based on the use of MVA). Scientists working for Virolab Mexico experimented by inserting certain genes from the Bovine Papillomavirus into MVA. One of the genes inserted was E2, an anti-tumor protein that self-regulates the activity of HVP’s tumor-generating proteins.

Under the protocols of completed phase 1, 2, and 3 clinical trials, the modified vaccine with the E2 gene inserted is injected directly into the cervix. This then produces an overdose of anti-tumor E2 protein immediately surrounding the HPV-infected tumor cells of the host. The immunological system of the patient reacts and destroys weakened HPV-infected cells. As a result, the patient develops antibodies against HPV and against additional foreign contents that may be contained in those cells.

The MEL-1 therapeutic vaccine has demonstrated in clinical trials conducted in Mexico that it can regress and heal pre-cancerous or cancerous lesions of the cervix in 88% to 97% of patients treated and eliminate detectable levels of HPV in approximately half of the treated patients. The standard treatments used in the clinical trials include weekly injections of MEL-1 for a period of six weeks. See more detailed information on the clinical trials immediately below.

To our knowledge, no other treatment has demonstrated elimination of detectable levels of HPV from patients.

Clinical Trials of Therapeutic Vaccine Candidate

Medical protocols under which Virolab Mexico’s human clinical trials were conducted were reviewed in Mexico by the Health Ministry at the State and Governmental levels. Because the trials were not conducted in the United States, no protocols were submitted to or reviewed by the U.S. FDA, nor has an Investigational New Drug Application (“IND”) been submitted to the U.S. FDA. As is customary in human clinical trials, the proposed clinical trials of the therapeutic vaccine and subsequent results from its use were also reviewed by various Hospital Ethics Committees before each approved their institution’s participation in the trials. In addition, the clinical trials were conducted in accordance with international standards for Good Clinical Practice and all study patients met pre-defined enrollment criteria and provided signed informed consent after being fully advised of the risks and potential benefits of participating in the trials.

The therapeutic vaccine candidate licensed by Virolab is a recombinant live virus vaccine based on a highly attenuated vaccinia virus vector, known as MVA, or Modified Vaccinia Ankara. Viroloab’s licensors have spliced into MVA a gene encoding the E2 protein from the bovine papillomavirus, which is similar to HPV, the human papillomavirus, to create the Company’s therapeutic vaccine candidate. Virolab refers to its therapeutic vaccine candidate as the MEL-1 vaccine. MVA is a very well characterized vaccine that has been used commercially for decades and tested on more than 100,000 people as a vaccine to prevent smallpox. It is currently stockpiled by the U.S. Department of Health and Human Services and similar organizations in other countries in the event of future smallpox outbreaks.

6

Virolab’s MEL-1 therapeutic vaccine has been evaluated in multiple animal models (preclinical) and has completed phase 1, 2, and 3 clinical trials in Mexico. We expect additional clinical trials will be required before the vaccine candidate can be considered for approval in the United States.

The following table summarizes the results of the clinical trials conducted with Virolab’s MEL-1 HPV therapeutic vaccine candidate, all of which received requisite governmental approval in Mexico before initiation. Unless noted separately below, each of these trials evaluated the use of MEL-1 as a therapeutic vaccine for treating pre-cancerous or cancerous cervical lesions in women who have been infected with human papillomavirus. In each study MEL-1 was administered by injection directly into the cervix in a radial manner, at 12 o’clock, three o’clock, six o’clock, and nine o’clock positions, once per week for six weeks. Each weekly injection consisted of 107 MEL-1 virus units per dose. All women who enrolled in the trials completed the study. Efficacy was evaluated at study week 9, three weeks after completion of treatment and was determined by regression in lesion size and severity and reduction in detectable HPV viral DNA. According to the American Association of Cancer Research (AACR) task force on treatment and prevention of intra-epithelial neoplasia, obtaining a 50% regression rate in CIN2/3 with a new treatment is clinically meaningful. Regression Rate is defined by the AACR as both Complete Response (CR) and Partial Response (PR) where CR is regression to normal histology and PR is regression of CIN 2/3 to CIN 1, with no new CIN 2/3 lesions in at least 50% of treated patients (Clin. Cancer Res., (8):314-346, 2002).

|

Phase 1

|

1st Phase 2

|

2nd Phase 2

|

Phase 3

|

|||||

|

Primary endpoint

|

Human safety study

|

Safety and lesion reduction

|

Elimination of high-grade lesions

|

Reduction in lesions

|

||||

|

Dates conducted

|

1999

|

2000-2002

|

2002-2004

|

2004-2008

|

||||

|

Treatment protocol

|

Evaluate safety in volunteers

|

Evaluate vaccine candidate against cryosurgery

|

Evaluate vaccine candidate against conization

|

Evaluate reduction in viral load and reduction in lesions

|

||||

|

Patient eligibility

|

Disease-free women with no cervical lesioins

|

Women with HPV and cervical lesions (CIN 1-3)

|

Women with HPV and high-grade lesions (CIN 2-3)

|

Women with HPV and pre-cancerous lesions (CIN 1-3) or carcinoma

|

||||

|

Number of participants

|

120

|

78 total

36 MEL-1

42 Control (cryosurgery)

|

54 total

34 MEL-1

20 Control (conization)

|

1,176

All patients treated with MEL-1

|

||||

|

Dosage and administration of study medication

|

MEL-1 vaccine injection into uterus once per week for 6 weeks at 107 MEL-1 virus units per dose.

|

MEL-1 vaccine injection into uterus once per week for 6 weeks at 107 MEL-1 virus units per dose.

|

MEL-1 vaccine injection into uterus once per week for 6 weeks at 107 MEL-1 virus units per dose.

|

MEL-1 vaccine injection into uterus once per week for 6 weeks at 107 MEL-1 virus units per dose.

|

||||

|

Trial type

|

Open label safety study

|

Open-label vs. control

|

Open label vs. control

|

No control group

|

||||

|

Trial outcome

|

Established initial safety database to allow commencement of trials to evaluate efficacy

|

Demonstrated lesion regression or elimination in 94% of MEL-1 treated patients and HPV virus elimination or significant reduction in 50% of MEL-1 treated patients

|

Elimination and regression of lesions in 88% of MEL-1 treated patients and HPV virus elimination or significant reduction in all MEL-1 patients

|

Elimination of lesions in 97% of participants. Elimination of HPV virus in 50% of patients

|

||||

|

Trial location

|

Mexico City

|

Mexico City

|

Mexico City

|

Mexico City; Michoacan, Mexico; Barquisimento, Venezuela

|

||||

|

Major adverse effects noted

|

Flu-like symptoms

|

Headaches, flu-like symptoms, chills, transient fever (>39º C), abdominal pain

|

Headaches, flu-like symptoms, chills, transient fever (>39º C), abdominal pain

|

Headaches, flu-like symptoms, chills, transient fever (>39º C), abdominal pain

|

||||

|

Outcome publication

|

Not published

|

Human Gene Therapy, May 2004 (Peer Reviewed)

|

Cancer Gene Therapy, February 2006 (Peer Reviewed)

|

Publication submitted

|

||||

7

In addition to the completed trials, in 2009 Virolab Mexico initiated an open-label phase 4 clinical trial at three different sites in Mexico. The Company refers to this trial as a phase 4 because this is how it is classified in Mexico, although the drug is not approved for commercial sale as is often the case with other phase 4 trials. To date, approximately 1,000 patients have been enrolled and treated in the trial, and efficacy results are consistent with the outcomes of the phase 2 and 3 clinical trials. Due to the Company’s limited funds, no on-going responsibility for the clinical trial has been assigned to Virolab, Inc., although it may at a future date if the Company is able to secure additional financing.

Market and Competition for Therapeutic Vaccine Candidate

According to The World Health Organization, or WHO, cervical cancer is the second most frequent form of cancer among women in the world and second most frequent among women aged 15 – 44 years. WHO also reports that approximately 300 million women, about 10% of women worldwide, are estimated to be infected with HPV at a given time and that virtually 100% of cervical cancer cases are caused by HPV infection. Also according to WHO, of the women infected with HPV, over 500,000 will develop cervical cancer and over half of them will die from their HPV-caused cancer.

Based on extrapolations of CIN 1 lesions of 1.2 per 1,000 population, and CIN 2/3 lesions of 1.5 per 1,000 population (the Company’s own estimates), the Company estimates the candidate patients for its therapeutic vaccine as follows:

|

Region

|

Candidate Patients

|

|||

|

Americas

|

935,000 | |||

|

Europe

|

880,000 | |||

|

Asia

|

4,010,000 | |||

|

Africa

|

840,000 | |||

|

Oceania

|

36,000 | |||

|

World Total

|

6,700,000 | |||

The Company has not estimated prices yet for its therapeutic vaccine candidate, if it receives approval. Initial pricing studies are currently planned.

Two vaccines are currently available to prevent infection by some HPV types. These preventative vaccines are Gardasil, marketed by Merck, and Cervarix, marketed by GlaxoSmithKline. Both vaccines protect against initial infection with HPV types 16 and 18, which cause most of the HPV-associated cancer cases. Gardasil also protects against HPV types 6 and 11, which cause 90% of genital warts. However, the vaccines provide little benefit to women who have already been infected with HPV types 16 and 18. For this reason the vaccines are recommended primarily for those women who have not yet been exposed to HPV. Both preventative vaccines are delivered in three shots over six months. In most countries they are approved only for female use, but are approved for male use in relevant countries like USA and UK. These approved vaccines do not have any therapeutic effect on existing HPV infections or cervical lesions, the target market for Virolab’s therapeutic vaccine candidate.

We are also aware of several development-stage and established enterprises, including major pharmaceutical and biotechnology firms, which are actively engaged in infectious disease and cancer vaccine research and development. These include Crucell, Sanofi-Aventis, Novartis, GlaxoSmithKline plc, MedImmune, Inc., a wholly owned subsidiary of AstraZeneca, Merck and Pfizer Inc. The company may also experience competition from companies that have acquired or may acquire technologies from companies, universities and other research institutions. As these companies develop their technologies, they may develop proprietary technologies which may materially and adversely affect our business.

In addition, a number of companies are developing products to address the same diseases that we are targeting. For example, Merck and GlaxoSmithKline have products on the market for cervical cancer in the therapeutic setting. Transgene, Inc. has a cervical cancer product in Phase II trials. Inovio, Inc. is also working on a vaccine for cervical cancer.

8

There are seven main approaches that we are aware of under which companies are investigating HPV vaccine product candidates:

|

1.

|

Live vectors

|

|

2.

|

Peptides

|

|

3.

|

Proteins

|

|

4.

|

DNA

|

|

5.

|

RNA replicon

|

|

6.

|

Dendritic cell

|

|

7.

|

Tumor cell

|

Refer to Ma, et al., HPV and Therapeutic Vaccines: Where are we in 2010? Current Cancer Therapy Reviews, 2010, 6, 81-103, for a more thorough review of the potential approaches. Of the live vector approaches which are similar to the approach used to develop our therapeutic vaccine candidate, the Virolab investigational therapeutic vaccine is the only candidate using the E2 protein.

If any of our competitors develop products with efficacy or safety profiles significantly better than our products, we may not be able to commercialize our products. Some of our competitors and potential competitors have substantially greater product development capabilities and financial, scientific, marketing and human resources than we do. Competitors may develop products earlier, obtain FDA approvals for products more rapidly, or develop products that are more effective than the single vaccine candidate under development by us. We intend to seek to expand our technological capabilities to remain competitive, however, research and development by others may render our technologies or products obsolete or noncompetitive, or result in treatments superior to ours.

Our competitive position will be affected by the disease indications addressed by our product candidates and those of our competitors, the timing of market introduction for these products and the stage of development of other technologies to address these disease indications. For us and our competitors, proprietary technologies, the ability to complete clinical trials on a timely basis and with the desired results, and the ability to obtain timely regulatory approvals to market these product candidates are likely to be significant competitive factors. Other important competitive factors will include the efficacy, safety, ease of use, reliability, availability and price of products and the ability to fund operations during the period between technological conception and commercial sales.

The FDA and other regulatory agencies may expand current requirements applicable to virus-based products and product candidates, which may harm our competitive position relative to other companies developing virus-based products for similar indications.

Virolab’s HPV Diagnostic Test

The HPV diagnostic test recently licensed to the Company, referred to as EDIVPH, uses a standard Enzyme-linked immunosorbent assay, or ELISA, procedure to test for HPV antibodies in the blood serum. ELISA tests are widely-used blood-based diagnostic method of detecting diseases. The advantage compared to other HPV diagnostics is the quick and easy access to blood samples requiring no gynecological examination, as the other marketed tests for HPV require. Virolab plans to investigate ways to commercialize its diagnostic test throughout the world. Virolab does not have approval to market the test in any countries, and government regulations vary from country to country.

Virolab Mexico has conducted a study of 172 HPV-infected women in which the HPV diagnostic test was compared to tissue samples using traditional HPV diagnostic methods. Results indicated that using different traditional diagnostic methods on the same patients did not consistently produce similar test results (approximately 20% could be diagnosed incorrectly as either positive or negative). The study was conducted in Mexico in patients with known current or previous HPV infections, and was published in the Journal of Medical Virology in 2001. Based on the results, Virolab believes that its blood-based test has potential to be more accurate. However, additional clinical comparisons will be necessary to verify this belief and additional clinical work will be necessary to seek approval to market the test.

Competition for the HPV Diagnostic Test

The Company’s EDIVPH blood test is the only method of detecting HPV of which we are aware that does not involve a gynecological examination or biopsies or smears from the cervix. Virolab’s HPV test is done as an immunological reaction in a sample of blood serum. Since a specialist does not need to examine the patient and technicians to take blood samples are widespread, we believe that our method will allow the examination of thousands of patients by a single lab-based technician familiar with the technology. We believe the diagnostic process can be readily automated and results can be obtained overnight.

9

Competitive HPV diagnostics methods include Hybrid Capture, Liquid Cytology, PCR and Thin Prep DNA determination, all of which require tissue samples from the cervix. Virolab believes that all of these diagnostic tests are readily used in practice, and each test’s usage depends on facilities available to diagnosing physicians and individual preferences.

Specific HPV diagnostic tests are increasingly being used in conjunction with routine annual gynecological examination and PAP smears as a means for identifying women at risk for developing cervical cancer. Currently, a portion of the tissue collected during a gynecological examination is utilized in a clinical laboratory for conducting an HPV test using one of the currently available test kits while the remainder of the tissue is examined microscopically for evidence of cancer cells or precancerous cellular changes. We believe a blood-based test will offer advantages for patients because they would not need a separate gynecological examination.

An experimental Light Sensitive Device method, involves the insertion of the device in the vagina and taking the sample to a lab with a spectrometer to measure light absorptions, but is not approved for use in most countries.

Patents

The company and its licensor have written a PCT patent application covering its therapeutic vaccine candidate MEL-1and the method of application directly to carcinomas and plans to submit the application shortly. The Company plans a similar filing in the United States. Virolab owns proprietary information and trade secrets relating to its HPV diagnostic technology and also plans patent applications. To date, no patents have issued.

Government Regulation

Regulations applicable to Therapeutic Vaccine Candidate

In the United States, drugs are subject to regulation under the Federal Food, Drug and Cosmetic Act, or the FDC Act. Biological products, in addition to being subject to provisions of the FDC Act, are regulated in the United States under the Public Health Service Act. Both statutes and related regulations govern, among other things, testing, manufacturing, safety, efficacy, labeling, storage, record keeping, advertising, and other promotional practices.

Obtaining FDA approval or comparable approval from similar agencies in other countries is a costly and time-consuming process, and the results of seeking approval are uncertain. Generally, FDA approval requires that preclinical studies be conducted in the laboratory and in animal model systems to gain preliminary information on efficacy and to identify any major safety concerns. In the United States, the results of these studies are submitted as a part of an IND application which the FDA must review and allow before human clinical trials can start.

A company must submit an IND application or equivalent application in other countries for each proposed product and must conduct clinical studies to demonstrate the safety and efficacy of the product necessary to obtain FDA approval or comparable approval from similar agencies in other countries. For example, in the United States, the FDA receives reports on the progress of each phase of clinical testing and may require the modification, suspension, or termination of clinical trials if an unwarranted risk is presented to patients.

Obtaining FDA approval prior to marketing a pharmaceutical product typically requires several phases of clinical development to demonstrate the safety and efficacy of the product candidate. Clinical trials are the means by which experimental treatments are tested in humans, and are conducted following preclinical testing. Upon successful completion of clinical trials, approval to market the treatment for a particular patient population may be requested from the FDA and/or its counterparts in other countries.

Clinical trials are normally done in three phases. Phase 1 clinical trials are typically conducted with a small number of patients or healthy subjects to evaluate safety, determine a safe dosage range, identify side effects, and, if possible, gain early evidence of effectiveness. Phase 2 clinical trials are conducted with a larger group of patients to evaluate effectiveness of an investigational product for a defined patient population, and to determine common short-term side effects and risks associated with the drug. Phase 3 clinical trials involve large scale, multi-center, comparative trials that are conducted to evaluate the overall benefit-risk relationship of the investigational product and to provide an adequate basis for product labeling.

10

After completion of clinical trials of a new product, FDA marketing approval must be obtained, or equivalent approval by comparable agencies in other countries. For the FDA, if the product is regulated as a biologic, as we expect for our investigational therapeutic vaccine, a Biologics License Application, or BLA, is required. The BLA must include results of product development activities, preclinical studies, and clinical trials in addition to detailed chemistry, manufacturing and control information.

Applications submitted to the FDA are subject to an unpredictable and potentially prolonged approval process. Despite good-faith communication and collaboration between the applicant and the FDA during the development process, the FDA may ultimately decide, upon final review of the data, that the application does not satisfy its criteria for approval or requires additional product development or further preclinical or clinical studies. Even if FDA regulatory clearances are obtained, a marketed product is subject to continual review, and later discovery of previously unknown problems or failure to comply with the applicable regulatory requirements may result in restrictions on the marketing of a product or withdrawal of the product from the market.

Before marketing clearance for a product can be secured, the facility in which the product is manufactured must be inspected by the FDA and must comply with current Good Manufacturing Practices, or cGMP, regulations. In addition, after marketing clearance is secured, the manufacturing facility may be inspected periodically for cGMP compliance by FDA inspectors.

Regulations Applicable to Diagnostic Test

In the United States, diagnostic tests are regulated by the FDA as medical devices. Medical devices are classified into one of three classes on the basis of the controls deemed by the FDA to be necessary to reasonably ensure their safety and effectiveness. Class I devices are subject to general controls, including labeling, premarket notification and adherence to FDA’s quality system regulations, which are device-specific good manufacturing practices. Class II devices are subject to general controls and special controls, including performance standards and postmarket surveillance. Class III devices are subject to most of the previously identified requirements as well as to premarket approval. Class I devices are exempt from premarket submissions to the FDA; most Class II devices require the submission of a 510(k) premarket notification to the FDA; and Class III devices require submission of a premarket approval application, or PMA. Most in vitro diagnostic tests are regulated as Class I or Class II devices and are either exempt from premarket notification or require a 510(k) submission. We presently do not know how the FDA will classify our HPV diagnostic test, but currently assume it is most likely to be a Class III device, since it would be the first blood-based diagnostic for HPV.

Class III devices require the submission and approval of a PMA prior to product sale. The PMA must be supported by detailed and comprehensive scientific evidence, including clinical data, to demonstrate the safety and efficacy of the medical device for its intended purpose. From start to finish the approval process may take several years, and the FDA may also request additional clinical data as a condition of approval or after the PMA is approved. Product changes after approval typically require a supplemental submission with FDA review cycles ranging from 30 to 180 days.

Any products manufactured or distributed pursuant to FDA clearances or approvals are subject to pervasive and continuing regulation by the FDA, including recordkeeping requirements, reporting of adverse experiences with the use of the device, and restrictions on advertising and promotion. Device manufacturers are required to register their establishments and list their devices with the FDA and are subject to periodic inspections by the FDA and certain state agencies. Noncompliance with applicable FDA requirements can result in, among other things, warning letters, fines, injunctions, civil penalties, recalls or seizures of products, total or partial suspension of production, refusal of the FDA to grant PMA approval for devices, withdrawal of PMA approvals, or criminal prosecution.

Employees

As of March 31, 2013, we had two full time employees. AVP also provided us with administrative support as needed. These positions are currently unpaid also until we secure additional financing.

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to these reports are electronically filed with or furnished to the Securities and Exchange Commission, or SEC. These reports may be obtained directly from the SEC’s website, www.sec.gov.

11

As a “smaller reporting company” as defined by Item 10 of Regulation S-K, the Company is not required to provide this information.

At this time, the Company maintains its designated office at 1840 Gateway Drive, Suite 200, Foster City, CA 94404. The Company’s telephone number is 650-378-1232.

While we are not currently a party to any material pending legal proceedings, from time to time we may be named as a party to lawsuits in the normal course of our business.

12

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

There is no established trading market for our common stock or any other class of our equity securities.

As of March 31, 2012, 2013, there were two (2) holders of record of our common stock and a total of 25,350,000 shares of common stock outstanding. All common stock currently outstanding was issued by the Company under applicable exemptions from registration under the Securities Act. None of our stock is registered under the Exchange Act, and no stock may be sold or offered unless registered with the SEC or sold under an applicable exemption from registration. There were no holders in “street name.”

To date, Virolab has not paid any dividends. Virolab does not intend to pay dividends in the foreseeable future, as the Company plans to retain its funds for operating purposes.

Not applicable.

OVERVIEW

Our discussion includes forward-looking statements within the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. All statements made which are not purely historical are forward-looking, and are based upon current expectations that involve risks and uncertainties. Actual results and the timing of events could differ materially from those anticipated or implied in these forward-looking statements as a result of a number of factors, including those set forth In Item 1A -“Risk Factors” of this Annual Report on Form 10-K. We use words such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “could,” and similar expressions to identify forward-looking statements.

13

Plan of Operation

On March 8, 2011, we entered into a Licensing Agreement with Virolab Nevada, LLC pursuant to which we were granted an exclusive, non-transferrable worldwide license for certain intellectual property developed by Licensor, principally comprising the technology, intellectual property, know-how, trade secret information, clinical trial data, and all other commercial rights to an investigational therapeutic vaccine for HPV (human papillomavirus) and HPV-related cancers and a blood test for HPV. Before this transaction we were a shell company, as defined in Rule 12b-2 of the Securities Exchange Act of 1934.

We believe that the HPV therapeutic vaccine technology that we have in development has the potential to be the first therapeutic to clear pre-cancerous and cancerous lesions of the cervix along with the underlying HPV viral infection. This belief is based on the results of two phase 2 clinical trials and one phase 3 clinical conducted in Mexico in which cancerous and pre-cancerous cervical lesions were eliminated or regressed in 88% to 97% of the patients. In addition, detectable HPV virus was eliminated from approximately 50% of the 1,246 patients treated in the three trials. All studies showed the vaccine candidate to be well tolerated, although headaches and other flu-like symptoms appeared in some of the patients.

In addition to the therapeutic vaccine candidate, Virolab has licensed rights to a specific blood-based diagnostic test for HPV. Currently, diagnosis of an infection with HPV requires a gynecological examination as well as a cervical tissue sample. We believe that a diagnosis from a simple blood draw will be less expensive and more convenient for patients.

The Company is evaluating its options to commercialize its therapeutic vaccine candidate and diagnostic test. These product candidates have not been approved for commercial sale anywhere in the world, and each country has different requirements for approval, so the commercialization process is likely to be lengthy and complex. The Company may employ different strategies in different areas of the world, such as sublicensing development and commercialization rights for some territories while retaining rights for other territories. Based on the historical work of Virolab Mexico in the country of Mexico, the Company believes that the path to obtain government approval may be shorter in the Latin America countries.

The Company will not be able to commercialize either its therapeutic vaccine candidate or its diagnostic test without additional capital. The Company is evaluating various means of raising this capital, including through the sale of equity securities, licensing agreements or other means. If the Company does not raise additional funds of at least $2 million for the advancement of its technology before March 8, 2014 it will lose its rights to the technology (including at least $0.5 million of which must be raised before March 8, 2012, and $1 million of which must be raised before March 8, 2013). The Company plans to seek at least $10 million of capital within the next 12 months, and plans to use these funds to determine the FDA’s requirements for approval of our therapeutic vaccine candidate, begin working on these requirements, file patents on our technology, broaden our pipeline of investigational drugs, vaccines and/or diagnostics, establish a biotechnology laboratory, and continue the process of seeking approval of our therapeutic vaccine candidate and diagnostic test outside of the United States. The Company is not presently able to allocate the specific costs for its plans because it does not yet know the requirements for approval of either its therapeutic vaccine candidate or its diagnostic test. While the Company plans to raise additional capital, and may seek to do so by offering equity securities of the Company, none of the Company’s securities have been registered with the Securities and Exchange Commission, and they may only be sold under registration or an applicable exemption from registration.

If the Company or a sublicense is successful in commercializing its therapeutic vaccine candidate or diagnostic test, the Company will be obligated to pay the Licensor two percent (2%) of any royalties received if the Company grants any third parties royalty-bearing licenses to the Technology. In addition, the Company has agreed to pay Licensor a royalty of one quarter of one percent (0.25%) of all gross revenue resulting from use of the Technology by the Company.

Although the Company did not spend the $0.5 million additional funds per the Licensing Agreement before March 8, 2012, we have not received a default letter and as of March 31, 2013 the Company was in negotiations to extend the terms of the Agreement.

Going Concern

Because we only had no cash at March 31, 2013, which is insufficient to fund any operations, the report of our independent registered public accounting firm on our financial statements for the period ended March 31, 2013 contains an explanatory paragraph regarding their substantial doubt about our ability to continue as a going concern. Our auditors’ opinion is based upon our operating losses and our need to obtain additional financing to sustain operations. Our ability to continue as a going concern will be dependent upon our ability to obtain the necessary financing to meet our obligations and repay our liabilities when they become due, and to generate sufficient revenues from our operations to pay our operating expenses. We will need to raise substantial funds in order to develop the HPV products which we have recently licensed from Virolab Nevada, and if we cannot raise additional funds we may need to abandon development of these products and cease operations.

14

Results of Operations

The following is a summary of the Company’s operation results for the years ended March 31, 2013 and 2012:

|

2013

|

2012

|

|||||||

|

Total operating expenses

|

$

|

778,239

|

$

|

2,172,220

|

||||

|

Total other income (expense)

|

---

|

--

|

||||||

|

Net loss

|

$

|

(778,239

|

)

|

$

|

(2,172,220

|

)

|

||

We were incorporated on May 4, 2010, and have incurred expenses of approximately $3,014,759 through March 31, 2013. These expenses largely consist of formation expenses, stock-based compensation and administrative expenses related to the start-up and organization of our business that have been incurred by and funded by the founder of the Company, Accelerated Venture Partners, LLC, or AVP. Expenses include stock-based compensation, legal fees, accounting fees, costs associated with SEC filings and preparation of documents.

For the year ended March 31, 2013, we had no revenue and incurred general and administrative expenses of $778,239. Our net loss was $778,239, due to general and administrative expenses. General and administrative expenses for the first nine months of fiscal 2013 consisted of $750,699 for the estimated fair value of stock-based compensation and $27,530 for administrative support, which mostly consisted of document preparation and EDGAR filing with the SEC.

The estimated value of stock based compensation for our two executive officers was based on the employment agreements with James A.D. Smith, our Chief Executive Officer, and Matthew M. Loar, our Chief Financial Officer, which provide for 1,250,000 and 900,000 stock options, respectively, each vesting over approximately four years beginning April 15, 2011 and May 23, 2011, respectively. The stock based compensation expense is an estimate and significant judgment was involved in attempting to determine the value of the company, Virolab, Inc., for which the options are exercisable. The actual value of our common stock may turn out to be much higher or lower than estimated amount, due to the lack of any reliable data on the Company’s current valuation. Virolab common stock has never traded publicly, and no stock has traded in private markets either, except for privately negotiated sales to the founder of the company and the founder of the technology from which the company subsequently licensed rights. No common stock has been sold in any manner since Virolab emerged from its shell-company status. The Company does not have any offers for purchase of its common stock in any stage, and no stock is registered with the Securities and Exchange Commission; therefore if any stock were to be sold the Company would need to do so under an effective registration statement or under an applicable exemption from registration. With the limited data points available to the Company and its board of directors regarding the Company’s valuation, we have estimated the value of common stock at $4 per share for financial reporting purposes. This amount was determined based on the minimum stock price required for listing on any Nasdaq market, and it closely approximates a $100 million valuation for the entire Company (considered “micro-cap” by most equity analysts), which we do not believe unreasonable for a development stage company with phase 3 data for an underserved medical condition. Each $1 change in estimated per-share value of our common stock would change the estimated stock-based compensation expense as reported for the year ending March 31, 2013 by approximately $56,651, so that a $3 estimated value for Virolab, Inc. common stock ($1 less per share) would result in general and administrative expenses of approximately $169,955 instead of the reported $226,606, likewise a $5 estimated value for Virolab, Inc. common stock would result in general and administrative expenses of approximately $283,257. Due to the low exercise price offered to our executive offers in their employment contracts ($0.10 per share, since they are currently not receiving any cash compensation) as compared to the estimated value for financial reporting purposes, the stock price volatility, stock option term and interest rate assumptions do not have a significant impact on the estimated value of the options as they would if the options were granted at market price. As noted above, the actual value of our common stock may turn out to be much higher or lower than the amount estimated for financial reporting purposes, due to the current lack of any reliable data on the Company’s current valuation. As of November 21, 2012 all the employee option had expired.

General and administrative expenses were lower in the year ended in March 31, 2013 compared to the period ended March 31, 2012 because:

|

●

|

We were no longer a shell company for the fiscal 2013 period,

|

|

●

|

We incurred lower costs to prepare and file our current and periodic reports with the SEC in the fiscal 2013 period, and

|

|

●

|

We incurred lower costs for stock based compensation, as noted above, compared to no stock-based compensation in the prior period.

|

15

To date, our general and administrative expenses, which in most other cases are paid in cash by the reporting companies, have been funded by Accelerated Venture Partners, LLC, or AVP. Expenses include legal fees, accounting fees, costs associated with SEC filings and preparation of documents.

We expect that, if we are successful in securing additional capital, future general and administrative expenses will increase significantly as compared to the period ended March 31, 2013. In addition, we expect to incur research and development expenses as we seek to advance our product candidates.

Liquidity and Capital Resource

As of March 31, 2013, we had a cash balance of $0. There were no other assets, and accrued expenses were approximately $3,014,759, of which 108,795 was due to AVP, a related party. We had a stockholders’ deficit of approximately $110,675 and no means to pay the liabilities in excess of our assets. AVP has agreed to fund certain administrative operating expenses of Virolab until the Company succeeds in raising additional funds, at which point the administrative operating expenses will be due. However, AVP may seek to force earlier payment of the amounts which we owe, or AVP may decide in the future not to continue funding costs on behalf of Virolab, although we are not aware of any plans for them to do so. If we are not successful in raising additional capital, we may not be able to pay our liabilities and may have to cease operations.

We plan to seek to raise at least $10 million of capital through the sale of equity or other means that could dilute existing shareholders within the next 12 months, and plan to use these funds to determine the FDA’s requirements for approval of our therapeutic vaccine candidate, begin working on these requirements, file patents on our technology, broaden our pipeline of investigational drugs, vaccines and/or diagnostics, establish a biotechnology laboratory, and continue the process of seeking approval of our therapeutic vaccine candidate and diagnostic test outside of the United States. We are not presently able to determine the specific costs for our plans because we do not yet know the requirements for approval of either our therapeutic vaccine candidate or our diagnostic test.

We have a consulting agreement with AVP under which AVP has agreed to provide us with certain advisory services that include reviewing our business plan, identifying and introducing prospective financial and business partners, and providing general business advice regarding our operations and business strategy. Under the consulting agreement, cash compensation of $400,000 is due to AVP upon our securing $5 million in available cash from funding, and an additional $400,000 is due upon our securing $10 million in available cash from funding (inclusive of the first $5 million). The cash compensation is to be paid to AVP at the rate of $66,667 per month. The total cash compensation to be received by AVP under the consulting agreement is not to exceed $800,000 unless we receive an amount of funding in excess of $10 million. If we receive equity or debt financing that is an amount less than $5 million, in between $5 million and $10 million, or greater than $10 million, the cash compensation earned by the AVP under its consulting services agreement will be prorated. We have the option to make a lump sum payment to AVP in lieu of the monthly cash payments.

If we do not raise additional funds of at least $2 million for the advancement of our technology before July 12, 2015, we will lose our rights to the HPV technology that we recently licensed; at least $0.5 million of these additional funds must be raised before July 12, 2013, and at least $1 million must be raised before July 12, 2014.

If we or a sublicense is successful in commercializing our therapeutic vaccine candidate or diagnostic test, we will be obligated to pay the licensor two percent (2%) of any royalties received if we grant any third parties royalty-bearing licenses to the technology. In addition, we have agreed to pay the licensor a royalty of one quarter of one percent (0.25%) of all gross revenue resulting from use of the licensed technology.

We plan to measure our future liquidity primarily by the cash and working capital available to fund our operations, if we are ever able to raise capital. To date we have not raised any capital and, accordingly; do not have any capital available to fund our operations, as stated above. We will not be able to commercialize either our therapeutic vaccine candidate or our diagnostic test without additional capital. We are evaluating various means of raising our initial capital, including through the sale of equity securities, licensing agreements or other means. We expect to incur losses for at least several years into the future as we develop our investigational therapeutic vaccine and diagnostic test, and we are unable to estimate when, if ever, we will receive revenue or have a positive cash flow.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a material current or future effect on our financial condition, results of operations, liquidity or capital resources.

16

Critical Accounting Policies and Use of Estimates

Our significant accounting policies are more fully disclosed in Note 1 to our financial statements. However, some of our accounting policies may be more particularly important to the portrayal of our financial position and results of operations and require the application of significant judgment by our management. To date, due to our limited operations, we do not believe any specific accounting policies have required significant judgment or use of estimates, other than our assumption that we will continue as a going concern, as described above. If we succeed in securing additional financing and commencing research and development activities, we expect the preparation of our financial statements will require a greater number of estimates and more significant judgment. We currently believe the following critical accounting policies will require significant judgments and estimates in the preparation of our future financial statements.

Stock-Based Compensation

We plan to account for stock awards granted to recipients using an estimate of the fair value of the stock award on the date that the award is granted. This estimated fair value will be recognized as an expense in the statement of operations on a straight-line basis over the vesting period of the underlying stock option, generally four years for employees. There is a high degree of subjectivity involved in estimating the input values needed to estimate the fair value of stock options and other awards. For Virolab in particular, our stock has never traded and therefore it will be difficult to determine the underlying fair value of our common stock on each date a stock award is made. Changes in any of the assumptions required to estimate the fair value, particularly the estimated value of the underlying stock and the estimated volatility, as well as the estimated term of the options, can materially affect the resulting estimates of the fair values of the awards that are granted. Also, the expenses recorded for stock-based compensation in our financial statements may differ significantly from the actual value realized by the recipients of the stock options, and these expenses are not adjusted to the actual amounts, if any, realized by the stock option recipients. Users of the financial statements should also understand that the expenses we recognize for stock-based compensation do not result in payments of cash by us.

Research and development expenses

We plan to expense our research and development costs as incurred. If we succeed in securing additional funding, research and development expenses are expected to include clinical trial costs, development and manufacturing costs for investigational drugs, payments to clinical and contract research organizations, compensation expenses for drug development personnel, consulting and advisor costs, preclinical studies and other costs related to development of our product candidates. Research and development expenses are expected to include expenses that are incurred over multiple reporting periods, such as fees for contractors and consultants, patient treatment costs related to clinical trials and investigational drug manufacturing costs. It may be difficult to determine the accounting period in which certain research and development costs are incurred, particularly when outside contractors are involved and there are differences between clinical trial assumptions and actual experience (such as rate of patient enrollment, levels and timing of services provided, review and correction of data inconsistencies, etc.). We plan to assess the level and related costs of the services provided during each reporting period, including the percentage of work completed through each reporting period, to determine the portion to expense in each period. The assessment of the percentage of work completed that determines the amount of research and development expense that should be recognized in a given period sometimes requires significant judgment. We plan to apply our judgment and base our estimates on our historical experience at other companies and on the best information available at the time of reporting.

Revenue recognition

While we do not expect to have any products ready for commercial sale for several years, if at all, we may enter into contractual arrangements with other entities that provides us with revenue before our product candidates are approved. Under such contractual arrangements, if we succeed in entering into any, we plan to recognize revenues when our performance requirements have been fulfilled, the amount of revenue is fixed and determinable, and collection is reasonably assured.

Revenue from license fees with non-cancelable, non-refundable terms and no future performance obligations would be recognized when collection is assured. Milestone payments would be recognized when we fulfill the development milestone requirements and collection is assured. We expect that future royalty revenue, if any, would be recorded when payments are received, since we do not expect that we will be able to reasonably estimate the sales upon which the royalties are based.

If we enter into revenue arrangements with multiple components, we expect to divide the components into separate units of accounting. Consideration received would be allocated among the separate units of accounting based on their relative fair values, and the applicable revenue recognition criteria identified and applied to each of the units.

17

Recent Accounting Pronouncements

We recently commenced our operations and do not believe that there are any recently issued accounting pronouncements that we have not adopted which are likely to have a material impact on our financial position, results of operations or other disclosures.

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

18

INDEX TO FINANCIAL STATEMENTS

|

Report of Independent Registered Public Accounting Firms

|

F-2

|

|

Balance Sheets as of March 31, 2013 and March 31, 2012

|

F-4

|

|

Statements of Operations for the period ended March 31, 2013, period ended March 31, 2012 and from inception (May 4, 2010) through March 31, 2013

|

F-5

|

|

Statement of Changes in Stockholders’ Deficit for the period from inception (May 4, 2010) through March 31, 2013

|

F-6

|

|

Statement of Cash Flows for the period ended March 31, 2013, period ended March 31, 2012 and from inception (May 4, 2010) through March 31, 2013

|

F-7

|

|

Notes to Financial Statements

|

F-8

|

F-1

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Stockholders

Virolab, Inc.

(A Development Stage Company)

We have audited the accompanying balance sheets of Virolab, Inc. (the “Company”) as of March 31, 2013, and the related statements of operations, stockholder's deficit and cash flows for the year then ended and for the period from inception (May 4, 2010) to March 31, 2013. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audit. The financial statements of the Company as of March 31, 2012, were audited by other auditor, whose report, dated June 27, 2012, expressed an unqualified opinion on those financial statements and also included an explanatory paragraph that raise substantial doubt about the Company’s ability to continue as a going concern.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control over financial reporting. Accordingly, we express no such opinion. Our audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our audit also includes assessing the accounting principles used and significant estimates made by management, as well as, evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Company as of March 31, 2013, and the results of its operations and its cash flows for the year ended and for the period from inception (May 4, 2010) to March 31, 2013, in conformity with accounting principles generally accepted in the United States of America.

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the financial statements, the Company is a development stage enterprise, had an accumulated deficit of $110,675 as of March 31, 2013 and continues to experience losses. These considerations raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans regarding those matters are also described in Note 2 which contemplates equity financing through a reverse merger transaction and/ or related party advances. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ Anton & Chia LLP

Newport Beach, CA

July 15, 2013

F-2

|

Peter Messineo

Certified Public Accountant

1982 Otter Way Palm Harbor FL 34685

peter@pm-cpa.com

T 727.421.6268 F 727.674.0511

|

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Stockholders of

Virolab, Inc.