Attached files

| file | filename |

|---|---|

| EX-14.1 - EX 14.1 - NORSTRA ENERGY INC | ex14-1.htm |

| EX-32.1 - EX 32.1 - NORSTRA ENERGY INC | ex32-1.htm |

| EX-31.2 - EX 31.2 - NORSTRA ENERGY INC | ex31-2.htm |

| EX-32.2 - EX 32.2 - NORSTRA ENERGY INC | ex32-2.htm |

| EX-31.1 - EX 31.1 - NORSTRA ENERGY INC | ex31-1.htm |

| EXCEL - IDEA: XBRL DOCUMENT - NORSTRA ENERGY INC | Financial_Report.xls |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended February 28, 2013

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from [ ] to [ ]

Commission file number: 333-181042

NORSTRA ENERGY INC.

(Exact name of registrant as specified in its charter)

|

Nevada |

27-1833279 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

|

|

|

2860 Exchange Boulevard, Suite 400, South Lake TX |

76092 |

|

(Address of principal executive offices) |

(Zip Code) |

Registrant's telephone number, including area code: (888) 474-8077

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

Name of Each Exchange On Which Registered |

|

N/A |

N/A |

|

|

|

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the last 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registration statement was required to submit and post such files).

Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer [ ] |

Accelerated filer [ ] |

|

Non-accelerated filer [ ] (Do not check if a smaller reporting company) |

Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes [ ] No [X]

The aggregate market value of Common Stock held by non-affiliates of the Registrant on August 31, 2012, was $Nil based on a $Nil average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. (There was no bid or ask price of our common shares during this quarter).

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the latest practicable date.

38,250,000 as of June 4, 2013

DOCUMENTS INCORPORATED BY REFERENCE

None.

.

TABLE OF CONTENTS

3

PART I

Cautionary Note Regarding Forward-Looking Statements

Except for historical information, this annual report contains forward-looking statements. Such forward-looking statements involve risks and uncertainties, including, among other things, statements regarding our business strategy, future revenues and anticipated costs and expenses. Such forward-looking statements include, among others, those statements including the words “expects,” “anticipates,” “intends,” “believes” and similar language. Our actual results may differ significantly from those projected in the forward-looking statements. Factors that might cause or contribute to such differences include, but are not limited to, those discussed in the sections “Business,” “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” You should carefully review the risks described in this Annual Report on Form 10-K and in other documents we file from time to time with the Securities and Exchange Commission. You are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date of this report. We undertake no obligation to publicly release any revisions to the forward-looking statements or reflect events or circumstances after the date of this document.

Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from such forward-looking statements.

All references in this Form 10-K to “company,” “Norstra Energy,” “we,” “us” or “our” mean Norstra Energy Inc., unless otherwise indicated.

Item 1. Business

Corporate Overview

We are an exploration stage company, incorporated in the State of Nevada on November 12, 2010 under the name Norstra Inc., as a for-profit company. Our fiscal year end is February 28. Our office is located at 2860 Exchange Boulevard, Suite 400, South Lake TX 76092. Our telephone number is 1-888-474-8077. Our website and further information about our company can be found at http://www.norstraenergy.com.

On November 18, 2011, we filed a certificate of amendment with the Nevada Secretary of State to change our name from Norstra Inc. to Norstra Energy Inc.

On March 28, 2012, we filed a certificate of change with the Nevada Secretary of State to effect a 2 new for 1 old forward split of our authorized and issued and outstanding shares of common stock such that our authorized capital increased from 75,000,000 shares of common stock with a par value of $0.001 to 150,000,000 shares of common stock with a par value of $0.001.

Effective February 27, 2013, the Nevada Secretary of State accepted for filing a Certificate of Amendment, wherein our company amended our Articles of Incorporation to create 50,000,000 shares of preferred stock, $0.001 par value for which our board of directors may fix and determine the designations, rights, preferences or other variations of each class or series within each class of preferred stock of our company. The creation of the preferred stock was approved on February 26, 2013 by written consent by our board of directors and the holders of 54.94% of our voting securities. Our company’s authorized capital now consists of 150,000,000 shares of common stock and 50,000,000 shares of preferred stock, all with a par value of $0.001.

Current Business

We are engaged in the exploration and development of oil and gas properties.

On February 1, 2011, we entered into an agreement with an unrelated third-party entity to purchase a 100% interest and an 80% net revenue interest in an oil and mineral lease in Reno County, Kansas. As consideration for the purchase, our company paid $15,000 in cash. Our company has not incurred any exploration or development costs in connection with this lease. We have had limited operations and have been issued a "going concern" opinion by our auditor, based upon our reliance on the sale of our common stock as the sole source of funds for our future operations.

Effective February 27, 2013, we entered into a secured promissory note in an aggregate principal amount of $100,000 pursuant to the terms of a subscription agreement between our company and Jackson Bennett, LLC. The note bears interest at an annual rate of 10% which is to be paid with principal in full on the maturity date of February 27, 2015. The principal amount of the note together with interest may be converted into shares of our common stock, at the option of Jackson Bennett, LLC, at a conversion price of $0.25 per share.

Additionally, on March 1, 2013, we entered into consulting agreements with Mr. Glen Landry, our president, chief executive officer, secretary, treasurer and director, and Mr. Dallas Kerkenezov, our chief financial officer. Mr. Landry will receive a consulting fee of $5,000 per month and shall be issued 1,000,000 shares of our preferred stock, which will be convertible into 10,000,000 shares of our common stock upon achievement of production from the South Sun River Bakken Prospect. Mr. Kerkenezov shall receive $500 a month for performing duties as our chief financial officer. Both agreements have a term of 12 months.

Also on March 1, 2013, Mr. Kerkenezov, or chief financial officer and Ms. Heredia, our former director, cancelled a total of 35,513,100 shares of our common stock held by them. Mr. Kerkenezov cancelled 27,013,100 and Ms. Heredia cancelled 8,500,000. These shares were cancelled in order to make our company more attractive for financing, given the capital requirements of the South Sun River Bakken Prospect.

On March 12, 2013, we entered into a farmout agreement with Summit West Oil, LLC for approximately 10,000 acres of oil and gas exploration property in northwest Montana known as the South Sun River Bakken Prospect. This property has since become our main focus. Under the terms of the farmout agreement, we are required to carry out the following expenditures in order to earn ownership of the property:

- $60,000 by April 5, 2013 for the acquisition of seismic and other exploration data; (requirement met);

- $140,000 by April 30, 2013 for the reinterpretation of the seismic data as well as delineation and surveying of potential drill locations; (requirement met);

- Drilling of an additional horizontal well at an estimated expenditure of $5,000,000 by June 30, 2013;

- Drilling of a horizontal well at an estimated expenditure of $5,000,000 by December 31, 2013; and

- Drilling of an additional horizontal well at an estimated expenditure of $5,000,000 by December 31, 2014.

5

Once we complete the above obligations, we will hold a 100% interest in the property, subject to an underlying 20% burden to Summit West Oil, LLC and the State of Montana.

Effective April 5, 2013, we entered into a secured promissory note in an aggregate principal amount of $50,000 pursuant to the terms of a subscription agreement. The note bears interest at an annual rate of 10% which is to be paid with principal in full on the maturity date of April 5, 2015. The principal amount of the note together with interest may be converted into shares of our common stock at the option of the holder, at a conversion price of $0.30 per share.

Effective April 25, 2013, we entered into a secured promissory note in an aggregate principal amount of $180,000 pursuant to the terms of a subscription agreement between our company and Jackson Bennett, LLC. The note bears interest at an annual rate of 10% which is to be paid with principal in full on the maturity date of April 25, 2015. The principal amount of the note together with interest may be converted into shares of our common stock at the option of the holder, at a conversion price of $0.50 per share.

We have had limited operations and have been issued a "going concern" opinion by our auditor, based upon our reliance on the sale of our common stock as the sole source of funds for our future operations.

Markets

The availability of a ready market and the prices obtained for produced oil and gas depends on many factors, including the extent of domestic production and imports of oil and gas, the proximity and capacity of natural gas pipelines and other transportation facilities, fluctuating demand for oil and gas, the marketing of competitive fuels, and the effects of governmental regulation of oil and gas production and sales. A ready domestic market for oil and gas exists because of the presence of pipelines to transport oil and gas. The existence of an international market exists depends upon the presence of international delivery systems and political and pricing factors.

If we are successful in producing oil and gas in the future, the target customers for our oil and gas are expected to be refiners, remarketers and third party intermediaries, who either have, or have access to, consumer delivery systems. We intend to sell our oil and gas under both short-term (less than one year) and long-term (one year or more) agreements at prices negotiated with third parties. Typically either the entire contract (in the case of short-term contracts) or the price provisions of the contract (in the case of long-term contracts) are renegotiated at intervals ranging in frequency from daily to annually.

We have not yet adopted any specific sales and marketing plans. However, as we purchase future properties, the need to hire marketing personnel will be addressed.

Competition

The oil and gas industry is highly competitive. We are a new exploration stage company and have a weak competitive position in the industry. We compete with junior and senior oil and gas companies, independent producers and institutional and individual investors who are actively seeking to acquire oil and gas properties throughout the world together with the equipment, labor and materials required to operate on those properties. Competition for the acquisition of oil and gas interests is intense with many oil and gas leases or concessions available in a competitive bidding process in which we may lack the technological information or expertise available to other bidders.

6

Many of the oil and gas companies with which we compete for financing and for the acquisition of oil and gas properties have greater financial and technical resources than those available to us. Accordingly, these competitors may be able to spend greater amounts on acquiring oil and gas interests of merit or on exploring or developing their oil and gas properties. This advantage could enable our competitors to acquire oil and gas properties of greater quality and interest to prospective investors who may choose to finance their additional exploration and development. Such competition could adversely impact our ability to attain the financing necessary for us to acquire further oil and gas interests or explore and develop our current or future oil and gas properties.

We also compete with other junior oil and gas companies for financing from a limited number of investors that are prepared to invest in such companies. The presence of competing junior oil and gas companies may impact our ability to raise additional capital in order to fund our acquisition or exploration programs if investors perceive that investments in our competitors are more attractive based on the merit of their oil and gas properties or the price of the investment opportunity. In addition, we compete with both junior and senior oil and gas companies for available resources, including, but not limited to, professional geologists, land specialists, engineers, camp staff, helicopters, float planes, oil and gas exploration supplies and drill rigs.

General competitive conditions may be substantially affected by various forms of energy legislation and/or regulation introduced from time to time by the governments of the United States and other countries, as well as factors beyond our control, including international political conditions, overall levels of supply and demand for oil and gas, and the markets for synthetic fuels and alternative energy sources.

In the face of competition, we may not be successful in acquiring, exploring or developing profitable oil and gas properties or interests, and we cannot give any assurance that suitable oil and gas properties or interests will be available for our acquisition, exploration or development. Despite this, we hope to compete successfully in the oil and gas industry by:

· keeping our costs low;

· relying on the strength of our management's contacts; and

· using our size and experience to our advantage by adapting quickly to changing market conditions or responding swiftly to potential opportunities.

Government Regulations

GENERAL. Our exploration activities are subject to federal, state and local laws and regulations governing exploration, environmental matters, occupational health and safety, taxes, labor standards and other matters. All material licenses, permits and other authorizations currently required for our operations have been obtained or timely applied for. Compliance is often burdensome, and failure to comply carries substantial penalties. The regulatory burden on the oil and gas industry increases the cost of doing business and affects profitability.

ENVIRONMENTAL MATTERS. Our operations are subject to numerous laws relating to environmental protection. These laws impose substantial penalties for any pollution resulting from our operations. We believe that our operations substantially comply with applicable environmental laws.

7

HAZARDOUS SUBSTANCES. The Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), also known as the "Superfund" law, imposes liability, without regard to fault or the legality of the original conduct, on some classes of persons that are considered to have contributed to the release of a "hazardous substance" into the environment. These persons include but are not limited to the owner or operator of the site or sites where the release occurred or was threatened and companies that disposed or arranged for the disposal of the hazardous substances found at the site. Persons responsible for releases of hazardous substances under CERCLA may be subject to joint and several liability for the costs of cleaning up the hazardous substances and for damages to natural resources. Despite the RCRA exemption that encompasses wastes directly associated with crude oil and gas production and the "petroleum exclusion" of CERCLA, we may generate or arrange for the disposal of "hazardous substances" within the meaning of CERCLA or comparable state statutes in the course of our ordinary operations. Thus, we may be responsible under CERCLA (or the state equivalents) for costs required to clean up sites where the release of a "hazardous substance" has occurred. Also, it is not uncommon for neighboring landowners and other third parties to file claims for cleanup costs as well as personal injury and property damage allegedly caused by the hazardous substances released into the environment. Thus, we may be subject to cost recovery and to some other claims as a result of our operations.

AIR. Our operations are also subject to regulation of air emissions under the Clean Air Act, comparable state and local requirements and the OCSLA. The scheduled implementation of these laws could lead to the imposition of new air pollution control requirements on our operations. Therefore, we may incur future capital expenditures to upgrade our air pollution control equipment. We do not believe that our operations would be materially affected by these requirements, nor do we expect the requirements to be any more burdensome to us than to other companies our size involved in exploration and production activities.

WATER. The Clean Water Act prohibits any discharge into waters of the United States except in strict conformance with permits issued by federal and state agencies. Failure to comply with the ongoing requirements of these laws or inadequate cooperation during a spill event may subject a responsible party to civil or criminal enforcement actions. Similarly, the Oil Pollution Act of 1990 imposes liability on "responsible parties" for the discharge or substantial threat of discharge of oil into navigable waters or adjoining shorelines. A "responsible party" includes the owner or operator of a facility or vessel, or the lessee or permittee of the area in which a facility is located. The Oil Pollution Act assigns liability to each responsible party for oil removal costs and a variety of public and private damages. While liability limits apply in some circumstances, a party cannot take advantage of liability limits if the spill was caused by gross negligence or willful misconduct, or resulted from violation of a federal safety, construction or operating regulation. If the party fails to report a spill or to cooperate fully in the cleanup, liability limits likewise do not apply. Even if applicable, the liability limits for offshore facilities require the responsible party to pay all removal costs, plus up to $75 million in other damages. Few defenses exist to the liability imposed by the Oil Pollution Act.

The Oil Pollution Act also requires a responsible party to submit proof of its financial responsibility to cover environmental cleanup and restoration costs that could be incurred in connection with an oil spill. The Oil Pollution Act requires parties responsible for offshore facilities to provide financial assurance in amounts that vary from $35 million to $150 million depending on a company's calculation of its "worst case" oil spill. We intend to have insurance to cover our facilities' "worst case" oil spill under the Oil Pollution Act regulations if we enter operations. As a result, we believe that we are in compliance with the Oil Pollution Act.

SAFETY AND HEALTH REGULATIONS. We are also subject to laws and regulations concerning occupational safety and health. We do not currently anticipate making substantial expenditures because of occupational safety and health laws and regulations. We cannot predict how or when these laws may be changed, or the ultimate cost of compliance with any future changes. However, we do not believe that any action taken will affect us in a way that materially differs from the way it would affect other companies in our industry.

Intellectual Property

We do not currently hold rights to any intellectual property and have not filed for copyright or trademark protection for our name or services.

Research and Development

Since our inception to the date of this annual report, we have not spent any money on research and development activities.

Employees

We are an exploration stage company and currently have no employees, other than our officers and directors who provide their services on a consulting basis.

Reports to Security Holders

We are required to file quarterly, annual and current reports, proxy statements and other information with the Securities and Exchange Commission pursuant to Section 12(b) or (g) of the Exchange Act. The public may read and copy any materials filed by us with the SEC at the SEC's Public Reference Room at 100 F Street NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The Company files its reports electronically with the SEC. The SEC maintains an Internet site that contains reports, proxy and information statements, and other electronic information regarding issuers that file electronically with the SEC at http://www.sec.gov.

Item 1A. Risk Factors

Risks Associated With Our Company.

Our independent auditors have issued and audit opinion for our company, which includes a statement describing our going concern status. Our financial status creates a doubt whether we will continue as a going concern.

Our auditors have issued a going concern opinion regarding our company. This means there is substantial doubt we can continue as an ongoing business for the next twelve months. The financial statements do not include any adjustments that might result from the uncertainty regarding our ability to continue in business. As such we may have to cease operations and investors could lose part or all of their investment in our company.

The oil and natural gas industry is highly competitive and there is no assurance that we will be successful in acquiring leases.

The oil and natural gas industry is intensely competitive. Although we do not compete with other oil and gas companies for the sale of any oil and gas that we may produce, as there is sufficient demand in the world market for these products, we compete with numerous individuals and companies, including many major oil and natural gas companies which have substantially greater technical, financial and operational resources and staff. Accordingly, there is a high degree of competition for desirable oil and natural gas leases, suitable properties for drilling operations and necessary drilling equipment, as well as for access to funds. We cannot predict if the necessary funds can be raised or that any projected work will be completed.

9

There can be no assurance that we will discover oil or natural gas in any commercial quantity on our properties.

Exploration for economic reserves of oil and natural gas is subject to a number of risks. There is competition for the acquisition of available oil and natural gas properties. Few properties that are explored are ultimately developed into producing oil and/or natural gas wells. If we cannot discover oil or natural gas in any commercial quantity thereon, our business will fail.

Even if we are able to engage in exploration on our property and establish that it contains oil or natural gas in commercially exploitable quantities, the potential profitability of oil and natural gas ventures depends upon factors beyond the control of our company.

The potential profitability of oil and natural gas properties is dependent upon many factors beyond our control. For instance, world prices and markets for oil and natural gas are unpredictable, highly volatile, potentially subject to governmental fixing, pegging, controls or any combination of these and other factors, and respond to changes in domestic, international, political, social and economic environments. Additionally, due to worldwide economic uncertainty, the availability and cost of funds for production and other expenses have become increasingly difficult, if not impossible, to project. In addition, adverse weather conditions can hinder drilling operations. These changes and events may materially affect our future financial performance. These factors cannot be accurately predicted and the combination of these factors may result in our company not receiving an adequate return on invested capital.

In addition, a productive well may become uneconomic in the event water or other deleterious substances are encountered which impair or prevent the production of oil and/or natural gas from the well. Production from any well may be unmarketable if it is impregnated with water or other deleterious substances. Also, the marketability of oil and natural gas which may be acquired or discovered will be affected by numerous related factors, including the proximity and capacity of oil and natural gas pipelines and processing equipment, market fluctuations of prices, taxes, royalties, land tenure, allowable production and environmental protection, all of which could result in greater expenses than revenue generated by the well.

The marketability of natural resources will be affected by numerous factors beyond our control which may result in us not receiving an adequate return on invested capital to be profitable or viable.

The marketability of natural resources which may be acquired or discovered by us will be affected by numerous factors beyond our control. These factors include market fluctuations in oil and natural gas pricing and demand, the proximity and capacity of natural resource markets and processing equipment, governmental regulations, land tenure, land use, regulation concerning the importing and exporting of oil and natural gas and environmental protection regulations. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in us not receiving an adequate return on invested capital to be profitable or viable.

Oil and natural gas operations are subject to comprehensive regulation which may cause substantial delays or require capital outlays in excess of those anticipated causing an adverse effect on our company.

Oil and natural gas operations are subject to federal, state, and local laws relating to the protection of the environment, including laws regulating removal of natural resources from the ground and the discharge of materials into the environment. Oil and natural gas operations are also subject to federal, state, and local laws and regulations which seek to maintain health and safety standards by regulating the design and use of drilling methods and equipment. Various permits from government bodies are required for drilling operations to be conducted; no assurance can be given that standards imposed by federal, provincial, or local authorities may be changed and any such changes may have material adverse effects on our activities. Moreover, compliance with such laws may cause substantial delays or require capital outlays in excess of those anticipated, thus causing an adverse effect on us. Additionally, we may be subject to liability for pollution or other environmental damages. To date, we have not been required to spend any material amount on compliance with environmental regulations. However, we may be required to do so in the future and this may affect our ability to expand or maintain our operations.

10

Exploration and production activities are subject to certain environmental regulations which may prevent or delay the commencement or continuation of our operations.

In general, our exploration and production activities are subject to certain federal, state and local laws and regulations relating to environmental quality and pollution control. Such laws and regulations increase the costs of these activities and may prevent or delay the commencement or continuation of a given operation. Specifically, we may be subject to legislation regarding emissions into the environment, water discharges and storage and disposition of hazardous wastes. In addition, legislation has been enacted which requires well and facility sites to be abandoned and reclaimed to the satisfaction of state authorities. However, such laws and regulations are frequently changed and we are unable to predict the ultimate cost of compliance. Generally, environmental requirements do not appear to affect us any differently or to any greater or lesser extent than other companies in the industry.

Exploratory drilling involves many risks and we may become liable for pollution or other liabilities which may have an adverse effect on our financial position.

Drilling operations generally involve a high degree of risk. Hazards such as unusual or unexpected geological formations, power outages, labor disruptions, blow-outs, sour natural gas leakage, fire, inability to obtain suitable or adequate machinery, equipment or labor, and other risks are involved. We may become subject to liability for pollution or hazards against which it cannot adequately insure or which it may elect not to insure. Incurring any such liability may have a material adverse effect on our financial position and operations.

Any change to government regulation/administrative practices may have a negative impact on our ability to operate and our profitability.

The business of oil and natural gas exploration and development is subject to substantial regulation under various countries laws relating to the exploration for, and the development, upgrading, marketing, pricing, taxation, and transportation of oil and natural gas and related products and other matters. Amendments to current laws and regulations governing operations and activities of oil and natural gas exploration and development operations could have a material adverse impact on our business. Permits, leases, licenses, and approvals are required from a variety of regulatory authorities at various stages of exploration and development. There can be no assurance that the various government permits, leases, licenses and approvals sought will be granted in respect of our activities or, if granted, will not be cancelled or will be renewed upon expiry. There is no assurance that such permits, leases, licenses, and approvals will not contain terms and provisions which may adversely affect our exploration and development activities.

11

Risks Associated with Our Common Stock

Our shares are defined as "penny stock." The rules imposed on the sale of the shares may affect your ability to resell any shares you may purchase, if at all.

Our shares are defined as a “penny stock” under the Securities and Exchange Act of 1934, and rules of the Commission. The Exchange Act and such penny stock rules generally impose additional sales practice and disclosure requirements on broker-dealers who sell our securities to persons other than certain accredited investors who are, generally, institutions with assets in excess of $5,000,000 or individuals with net worth in excess of $1,000,000 or annual income exceeding $200,000, or $300,000 jointly with spouse, or in transactions not recommended by the broker-dealer. For transactions covered by the penny stock rules, a broker-dealer must make a suitability determination for each purchaser and receive the purchaser's written agreement prior to the sale. In addition, the broker-dealer must make certain mandated disclosures in penny stock transactions, including the actual sale or purchase price and actual bid and offer quotations, the compensation to be received by the broker-dealer and certain associated persons, and deliver certain disclosures required by the Commission. Consequently, the penny stock rules may affect the ability of broker-dealers to make a market in or trade our common stock and may also affect your ability to resell any shares you may purchase.

Market for penny stock has suffered in recent years from patterns of fraud and abuse

Stockholders should be aware that, according to SEC Release No. 34-29093, the market for penny stocks has suffered in recent years from patterns of fraud and abuse. Such patterns include:

· Control of the market for the security by one or a few broker-dealers that are often related to the promoter or issuer;

· Manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases;

· Boiler room practices involving high-pressure sales tactics and unrealistic price projections by inexperienced salespersons;

· Excessive and undisclosed bid-ask differential and markups by selling broker-dealers; and,

· The wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired level, along with the resulting inevitable collapse of those prices and with consequential investor losses.

Our management is aware of the abuses that have occurred historically in the penny stock market. Although we do not expect to be in a position to dictate the behavior of the market or of broker-dealers who participate in the market, management will strive within the confines of practical limitations to prevent the described patterns from being established with respect to our securities. The occurrence of these patterns or practices could increase the volatility of our share price.

We will incur ongoing costs and expenses for SEC reporting and compliance.

Going forward, our company will have ongoing SEC compliance and reporting obligations. Such ongoing obligations will require our company to expend additional amounts on compliance, legal and auditing costs. In order for us to remain in compliance we will require future revenues to cover the cost of these filings, which could comprise a substantial portion of our available cash resources.

Our directors will control and make corporate decisions that may differ from those that might be made by the other shareholders.

Due to the controlling amount of their share ownership in our company, our directors will have a significant influence in determining the outcome of all corporate transactions, including the power to prevent or cause a change in control. Their interests may differ from the interests of other stockholders and thus result in corporate decisions that are disadvantageous to other shareholders.

12

Inability and unlikelihood to pay dividends

To date, we have not paid, nor do we intend to pay in the foreseeable future, dividends on our common stock, even if we become profitable. Earnings, if any, are expected to be used to advance our activities and for general corporate purposes, rather than to make distributions to stockholders. Prospective investors will likely need to rely on an increase in the price of our company’s stock to profit from his or her investment. There are no guarantees that any market for our common stock will ever develop or that the price of our stock will ever increase.

Since we are not in a financial position to pay dividends on our common stock and future dividends are not presently being contemplated, investors are advised that return on investment in our common stock is restricted to an appreciation in the share price. The potential or likelihood of an increase in share price is questionable at best.

Item 1B. Unresolved Staff Comments

As a “smaller reporting company”, we are not required to provide the information required by this Item.

Item 2. Properties

Our company’s principal place of business and corporate offices are located at 2860 Exchange Boulevard, Suite 400, South Lake TX 76092, our telephone number is 1-888 474-8077. We pay rent at approximately $1,000 per month.

Reno County, Kansas Property

On February 1, 2011, we entered into an agreement with an unrelated third-party entity to purchase a 100% interest and an 80% net revenue interest in an oil and mineral lease in Reno County, Kansas. As consideration for the purchase, our company paid $15,000 in cash. Our company has not incurred any exploration or development costs in connection with this lease. We have had limited operations and have been issued a "going concern" opinion by our auditor, based upon our reliance on the sale of our common stock as the sole source of funds for our future operations.

On February 15, 2012, our company and Keta Oil and Gas Inc. concluded the transaction in which our company paid $15,000 to acquire 100% working interest in the oil and gas leases described as T26S R08W the E/2 NE/4 Section 30, containing 83 acres more or less, located in Reno County, State of Kansas. The purchase price was made up of $10 for the lease assignment and $14,990 as a lease bonus payment.

The lease is for a three year term with a commencement date of original acquisition of February 15, 2012 and grants our company the right to explore for potential petroleum and natural gas opportunities on the lease. The ability to renew the lease is to be renegotiated before or upon termination if our company should choose to renew the leasing rights.

LOCATION

The acreage is located in the Great Plains physiographic province of Kansas and the surface terrain consists of gently rolling plains. Ground elevations range from 1,500-1750 feet above sea level. The land is primarily used for agriculture and cattle grazing. There are no adverse environmental conditions on the surface or subsurface. There are numerous highway and county roads that allow easy access to the acreage and future well sites upon development of the play.

13

The Lerado Extension is within the oil and gas producing region of Central Kansas and lays along the southern flank of the Central Kansas Uplift, with a portion of the acreage falling within the Sedgwick Basin.

GEOLOGY

Across the uplift the normal inclination of strata is interrupted in places to form gently plunging anticlines, numerous closed structures and complex faulted areas. The rock strata dip into the basins with closed structures, plunging anticlines, and stratigraphic traps forming along the flanks of the uplift. Structural features, such as those mentioned above, are often associated with accumulation of hydrocarbons in the area. Stratigraphic traps formed as a result of differences or variations between or within stratified rock layers, creating a change or loss of porosity and/or permeability are also of major importance in hydrocarbon entrapment. Large amounts of oil and gas have produced on the uplift and on the flanks of this major Pre-Mississippian and Middle Pennsylvanian structural province.

The rocks of the Lansing-Kansas City Group account for approximately 23% of all the oil produced in the State of Kansas, the majority of which comes from the Central Kansas Uplift and the basins flanking the uplift. The Lansing-Kansas City zone in central Kansas is composed of interblended carbonates and shale's with occasional minor coals and sandstones. In the general vicinity of the Lerado Extension, the Lansing- Kansas City zones is between 100-225 feet of thickness. Of the dozen or so individual zones with-in the Lansing-Kansas City, several of the zones have potential to produce oil and gas from each well drilled.

EXPLORATION PROGRAM

Since acquiring the South Sun River Bakken Prospect, we have changed our focus away from the Reno County Property. Depending on the results of the South Sun River Bakken operations, we may abandon or renew exploration activity on the Reno County Property.

We have not recognized any revenue from our oil and gas project and do not expect to generate any revenue for at least 12 months. This property does not contain any known reserves or resources of oil or gas.

South Sun River Bakken Prospect

On March 12, 2013, we entered into a farmout agreement with Summit West Oil, LLC for approximately 10,000 acres of oil and gas exploration property in northwest Montana known as the South Sun River Bakken Prospect. Under the terms of the farmout agreement, we are required to carry out the following expenditures in order to earn ownership of the property:

- $60,000 by April 5, 2013 for the acquisition of seismic and other exploration data; (requirement met)

- $140,000 by April 30, 2013 for the reinterpretation of the seismic data as well as delineation and surveying of potential drill locations; (requirement met)

- Drilling of an additional horizontal well at an estimated expenditure of $5,000,000 by June 30, 2013;

- Drilling of a horizontal well at an estimated expenditure of $5,000,000 by December 31, 2013; and

- Drilling of an additional horizontal well at an estimated expenditure of $5,000,000 by December 31, 2014.

14

Once we complete the above obligations, we will hold a 100% interest in the property, subject to an underlying 20% burden to Summit West Oil, LLC and the State of Montana.

LOCATION AND GEOLOGY

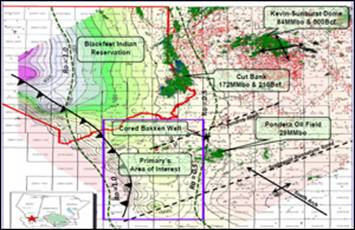

The South Sun River Bakken Prospect is an over-pressured Bakken shale resource play in Lewis & Clark County, Montana, in the developed Bakken Fairway that extends southwards from Alberta, Canada into northwest Montana. Potential oil production is estimated throughout the literature and publications at 10-15 MMBO per square mile in areas where the Bakken is thermally mature and where the critical middle Sappington Member is between 20’-30’ thick. It encompasses a superb land package of 10,097.99 mineral acres. It is where the western edge of the Bakken Fairway plunges into contact with the tectonically heated Thrust Zone and where we believe the resulting thermal maturity of the Bakken offers the highest potential for oil production.

Oil generation from organically rich shale units is considered to commence at Ro=0.65%, with peak oil generation occurring at Ro=1.00% and the end of oil generation occurring when Ro >1.3%. Ro values associated with the Bakken range from 0.6% in the east to >1.00% toward the west and south.

15

RESISTIVITY

There are excellent resistivity readings in the Upper and Lower Bakken members in key wells in the prospect area. The wells show excellent sections of the Bakken with resistivity readings over 400 ohms, well in excess of the minimum 35 ohms needed for possible oil production. The Middle Member of the Bakken, known as the Sappington Silt, is also well developed, with adequate porosity (3-15%) and permeability (1-20 md) for oil production.

Below are several wells in the prospect area and their Bakken section thickness and corresponding resistivity readings.

|

Sec.22 T17N-R6W |

ARCO/Steinbach # 1 |

Bakken: 76' |

Ohms: >2,000 |

|

Sec.32 T18N-R5W |

Shell/Krone 31-32 |

Bakken: 70' |

Ohms: 400 |

|

Sec.3-T14N-R6W |

Suncor/Flesher 14603 |

Bakken: 52' |

Ohms: 100- 300 |

|

Sec.9-T19N-R8W |

Sun Exploration/JB Long # 1-9 |

Ohms: >200 |

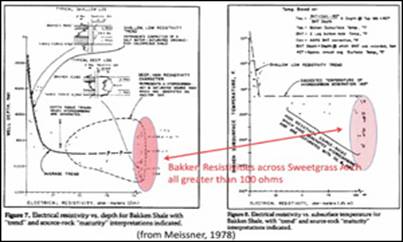

Although resistivity values do not distinguish whether oil has been generated in situ within the shales at a given location, or has migrated into the shales, extensive Bakken core research by Schmoker and Hester (1990) has indicated that a resistivity value of greater than 35 ohm-m coincides with the onset of observable oil generation within Bakken shale.

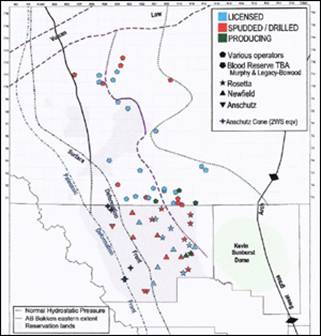

Electric logs in the South Sun River Bakken Prospect area record resistivity readings in excess of 400 ohms, and over 2,000 ohms in certain wells. The Bakken is oil productive with as little as 35 Ohms. Currently, there is intense leasing activity in the area as many major companies are rapidly acquiring lease positions. Majors like Newfield Energy, Anschutz, Rosetta Resources and at least a dozen other companies have been extremely active in the area. Primary Petroleum and their major partner are just completing their last well of a 6 well drilling program in the South Sun River Bakken Prospect area.

Well control in the vicinity of the South Sun River Bakken Prospect displays excellent maturity in the Bakken that is superior to the above model. The Bakken is at a depth of 6,896’ feet in the key Krone # 31-32 well drilled by Shell. Resistivity in the Krone 31-32 well is in excess of 400 ohms, and throughout the South Sun River Bakken Prospect.

16

The Bakken Formation

The Bakken Shale Formation was entirely undeveloped until the oil and gas industry developed new technologies for horizontal drilling and fracking. Since then, development of this formation throughout Montana, North Dakota, Saskatchewan and Alberta has been unprecedented. The Bakken is America’s most immediate opportunity for a path to energy independence.

In the past 5 years the Bakken Shale has already doubled the proven oil reserves of the USA, with growing estimates of over 40 billion barrels of oil, compared to 21 billion for the rest of the country. On November 3, 2011, a new production record was set for a Bakken well when the Whiting Petroleum Tarpon Federal # 21-4H posted an IP of 7,009 BO in a 24 hour period. Wells with IP’s over 5,000 BOPD in the Williston Basin are no longer unusual. Currently, North Dakota has over 450,000 BO monthly production and is expected to top 1,000,000 BO by 2015. Industry experts predict that drilling will not slow until 2030, and that Bakken production will continue until 2100.

17

“The U.S. Geological Survey (USGS) has called the Bakken Formation the largest continuous oil accumulation it has ever assessed as much as 500 billion barrels of oil sitting untapped beneath Montana, North Dakota a potential supply of oil four times as large as that held in Saudi Arabia’s massive Ghawar region.”

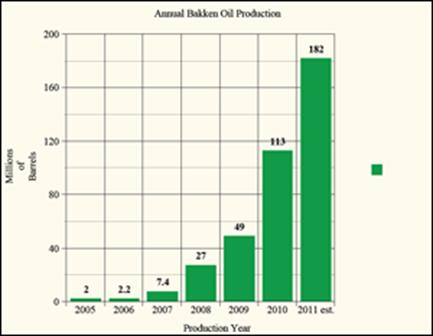

In 2004, production was 278,540 barrels, and in 2007 the yield jumped to just shy of 5 million barrels. In 2011, over 180 million barrels were produced. With more and more companies buying and developing Bakken Formation land, this trend is unlikely to stop in the coming years.

In January, 2012, Whiting Petroleum announced a $1.6 billion budget that allocates $851 million for 218 Bakken wells. Whiting Petroleum is generally credited for the advances in fracking technology that has resulted in the huge increase oil production from Bakken wells. Whiting Petroleum produced 24.8 million BO in 2011.

Likewise, Kodiak Oil & Gas announced a 2012 budget of $550 million to drill 73 Bakken wells. Magnum Hunter will spend $200 million in 2012 on Bakken wells and expects to increase their production by 85-90%. Continental Resources invested $1.36 billion in Bakken activity 2011, has over 900,000 leased mineral acres, and completed 26 Bakken wells in the 4th quarter of 2011.

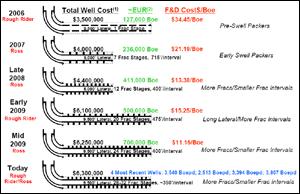

A large reason for the increase in production has been the effectiveness of drilling and extraction techniques. Below is an example of the increasing efficiency of Bakken production.

18

EXPLORATION PROGRAM

Our company is interpreting and evaluating seismic data in order to render the most accurate possible graphic representation of specific portions of the South Sun River Project's subsurface geological structure.

Our company's geological team has defined three sections of its current holdings that are diagonally offsetting along the strike of the thrust sheets. There is an abundance of seismic data available on this portion of the Sun River Prospect. Several major oil companies including Arco, Shell, Occidental, and Exxon were pursuing deeper targets than the Bakken in the 1980s resulting in considerable seismic data in our area. Most of the seismic is high quality 12 fold dynamite lines and nearly all the major oil companies have made their data available through representatives.

The images that our company has already acquired, as well as additional data that it is evaluating for potential acquisition, allow our company and our geophysical consultants, R. J. Grundy & Associates, to accurately evaluate the Bakken prospect for drill sight location. With the recorded seismic "signatures" our company and our geophysicist have the tools to produce the truest possible image of the sub-surface geological structure on the South Sun River Project. Norstra has acquired 14 miles of seismic lines and plans to double its portfolio of seismic information as it extends its study to the northwest of the initial 3 sections currently under consideration for the first drill location.

Our seismic experts, R. J. Grundy & Associates, of Denver, have over 35 years of global experience in oil and gas exploration and geophysical interpretation. They have previously done historic seismic work within 2 miles of the target area which is of great value for us. The initial seismic evaluation for the first of 3 sections is near completion. The first thrust sheet west of the Krone well which was drilled by Shell Oil Company, is clearly visible. Additional review will be conducted along the strike of the sheet.

Acquisition of seismic data involves the transmission of controlled acoustic energy into the earth, and recording the energy that is reflected back from geological boundaries in the subsurface. Processing these reflections produces a synthetic image of the earth's subsurface geological structure.

Our company is finalizing the evaluation of technical data for the first drill location on its South Sun River Prospect. We received the first seismic interpretation from our geophysical team in Denver and are reviewing the proposed first drill location internally. Once we have evaluated and cross-referenced the proposed location with the actual surface conditions for the drilling operations we will send our surveying team out to stake the location and design the drilling pad.

Central to the viability of our company's South Sun River Prospect are the subsurface well logs in the area. Our company is fortunate to have acreage that is near wells that show the likelihood of commercial oil in the Bakken Oil Formation.

19

There are three key wells in the immediate vicinity of the first potential Norstra drill site.

- Krone #3132 drilled by Shell Oil Company. This well demonstrates those essential parameters for a commercial well in the Bakken Oil Formation. There are 24 feet of Bakken middle member present. The middle member of the Bakken Oil Formation produces most of the oil today. The reservoir rock displays a resistivity of 200 ohms suggesting oil and gas is present. The well is less than 2.5 miles away from the first proposed Norstra drill site.

- Steinbach #1 drilled by Arco. The Steinbach # 1 well is around 3,000 feet deeper than the Krone well. The same reservoir is present, but with deeper buried shales that are heated at a higher temperature resulting in higher resistivities from the generations of oil and gas. The resistivity here is over 2,000 ohms. The well is less than 5 miles south of the first proposed drill site.

- Soap Creek Cattle Co. #1331 drilled by Flying J Oil and Gas. The well is not studied much because it did not penetrate the Bakken Oil Formation. It still has some very significant information for our project. The well stopped in the middle member of the Blackleaf Oil Formation at a depth of 5,480 feet. The Bakken is perhaps 3,000 feet deeper. What is of interest is that in one of the many faults present, there is oil described by the geologist, M.K. Jones. The oil is described from 4,928 to 4,994 feet. It is in a fractured member of the Taft Hill and the oil has been biodegraded to a heavy crude due to the presence of the water in the fractures. This oil has migrated up the thrust from deeper formations. The source for the oil could be the Bakken Oil Formation. This well is less than 0.75 miles from the proposed first drillsite away. Just the fact that oil is present so close to the Company's proposed well site is extremely significant.

It is expected that a fully completed and fracked horizontal well on the South Sun River Bakken Prospect will cost approximately $5,000,000. We currently do not have sufficient funds on hand, nor financing commitments sufficient to drill or complete a well on the property and there can be no assurance that we will be able to secure such financing.

Item 3. Legal Proceeding

We know of no material, existing or pending legal proceedings against our company, nor are we involved as a plaintiff in any material proceeding or pending litigation. There are no proceedings in which our director, officer or any affiliates, or any registered or beneficial shareholder, is an adverse party or has a material interest adverse to our interest.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

Our company's common stock is quoted on the OTC Bulletin Board under the symbol "NORX". Our stock did not begin trading until March 5, 2013.

20

Holders

As of June 4, 2013, there were 12 stockholders of record and an aggregate of 38,250,000 shares of our common stock were issued and outstanding. Our common shares are issued in registered form. The transfer agent of our company's common stock is Empire Stock Transfer, Inc. at 1859 Whitney Mesa Dr., Henderson, NV 89014.

Description of Securities

The authorized capital stock of our company consists of 150,000,000 of common stock, at $0.001 par value, and 50,000,000 shares of preferred stock, at $0.001 par value.

Dividend Policy

We have not paid any cash dividends on our common stock and have no present intention of paying any dividends on the shares of our common stock. Our current policy is to retain earnings, if any, for use in our operations and in the development of our business. Our future dividend policy will be determined from time to time by our board of directors.

Equity Compensation Plan Information

We do not have in effect any compensation plans under which our equity securities are authorized for issuance and we do not have any outstanding stock options.

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

We did not sell any equity securities which were not registered under the Securities Act during the year ended February 28, 2013, that were not otherwise disclosed on our quarterly reports on Form 10-Q or our current reports on Form 8-K filed during the year ended February 28, 2013.

During July to September 2012 we sold 33,250,000 shares at $0.01 per share for total proceeds of $33,250, under our recent S-1 Registration Statement offering.

Purchase of Equity Securities by the Issuer and Affiliated Purchasers

We did not purchase any of our shares of common stock or other securities during our fourth quarter of our fiscal year ended February 28, 2013.

Item 6. Selected Financial Data

As a “smaller reporting company,” we are not required to provide the information required by this Item.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with our audited financial statements and the related notes that appear elsewhere in this annual report. The following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to those discussed below and elsewhere in this annual report, particularly in the section entitled "Risk Factors" beginning on page 9 of this annual report.

21

Our audited financial statements are stated in United States Dollars and are prepared in accordance with United States Generally Accepted Accounting Principles.

Results of Operations

We have generated no revenues and have incurred $44,090 in expenses since inception through February 28, 2013.

The following table provides selected financial data about our company for the year ended February 28, 2013 and February 29, 2012.

|

Balance Sheet Date |

|

02/28/13 |

|

02/29/12 | ||

|

|

|

|

|

|

|

|

|

Cash |

|

$ |

99,550 |

$ |

177 |

|

|

Total Assets |

|

$ |

125,114 |

$ |

19,241 |

|

|

Total Liabilities |

|

$ |

114,473 |

$ |

4,392 |

|

|

Stockholders’ Equity |

|

$ |

10,641 |

$ |

14,849 |

|

Plan of Operation

We are a start-up, exploration-stage company and have not yet generated or realized any revenues from our business operations.

Our auditors have issued a going concern opinion on our audited financial statements for the year ended February 28, 2013. This means that there is substantial doubt that we can continue as an on-going business for the next twelve months unless we obtain additional capital to pay our bills. This is because we have not generated any revenues and no revenues are anticipated until we begin removing and selling minerals. There is no assurance we will ever reach this point. Accordingly, we must raise cash from sources from other sources. Our only other source for cash at this time is investments by others. We must raise cash to implement our project and stay in business. As of February 28, 2013, our company had $99,550 in cash on hand.

On March 12, 2013 our company entered into a farmout agreement with Summit West Oil, LLC for approximately 10,000 acres of oil and gas exploration property in northwest Montana. Under the terms of the farmout agreement, we are required to carry out the following expenditures in order to earn ownership of the property:

· $60,000 by April 5, 2013 for the acquisition of seismic and other exploration data (requirement met);

· $140,000 by April 30, 2013 for the reinterpretation of the seismic data as well as delineation and surveying of potential drill locations (requirement met);

· Drilling of an additional horizontal well at an estimated expenditure of $5,000,000 by June 30, 2013;

· Drilling of a horizontal well at an estimated expenditure of $5,000,000 by December 31, 2013; and

· Drilling of an additional horizontal well at an estimated expenditure of $5,000,000 by December 31, 2014.

If we are unable to complete any phase of exploration because we do not have sufficient capital, we will cease operations until we raise more money. If we cannot or do not raise additional capital, we will cease operations. If we cease operations, we do not have any additional plans at this time.

22

Limited Operating History; Need for Additional Capital

There is no historical financial information about us upon which to base an evaluation of our performance. We are an exploration stage corporation and have not generated any revenues from operations. We cannot guarantee we will be successful in our business operations. Our business is subject to risks inherent in the establishment of a new business enterprise, including limited capital resources, possible delays in the exploration of our properties, and possible cost overruns due to price and cost increases in services.

To become profitable and competitive, we must conduct the research and exploration of our properties before we start production of any minerals we may find. We sought equity financing to provide for the capital required to implement our research and exploration phases. We believe that the funds raised from our offering will allow us to operate for one year.

We have no assurance that future financing will be available to us on acceptable terms. If financing is not available on satisfactory terms, we may be unable to continue, develop or expand our operations. Equity financing could result in additional dilution to existing shareholders.

Liquidity and Capital Resources

Working Capital

|

|

|

Year Ended, |

| ||||

|

|

|

February 28, |

|

|

|

February 29, |

|

|

|

|

|

|

|

|

|

|

|

Current Assets |

$ |

106,050 |

|

|

$ |

177 |

|

|

Current Liabilities |

$ |

9,387 |

|

|

$ |

Nil |

|

|

Working Capital Deficit |

$ |

96,663 |

|

|

$ |

177 |

|

Cash Flows

|

|

|

Year Ended |

| ||||

|

|

|

February 28, |

|

|

|

February 29, |

|

|

|

|

|

|

|

|

|

|

|

Cash Flows from (used in) Operating Activities |

$ |

(40,377 |

) |

|

$ |

(80 |

) |

|

Cash Flows from (used in) Investing Activities |

$ |

Nil |

|

|

|

(15,000 |

) |

|

Cash Flows from (used in) Financing Activities |

$ |

139,750 |

|

|

$ |

15,257 |

|

|

Net Increase (decrease) in Cash During Period |

$ |

99,373 |

|

|

$ |

177 |

|

As at February 28, 2013, our company’s cash balance was $99,550 compared to $177 as at February 29, 2012 and our total assets were $125,114 compared with $19,241 as at February 29, 2012. The increase in cash was primarily due to a secured promissory note (the “Note”) in an aggregate principal amount of $100,000 pursuant to the terms of a subscription. The Note bears interest at an annual rate of 10% which is to be paid with principal in full on the maturity date of February 27, 2015. The principal amount of the Note together with interest may be converted into shares of our common stock, at the option of the holder, at a conversion price of $0.25 per share.

23

As at February 28, 2013, our company had total liabilities of $114,473 compared with total liabilities of $4,392 as at February 29, 2012. The increase in total liabilities was primarily attributed to a convertible notes payable.

As at February 28, 2013, our company had a working capital of $96,663 compared with a working capital of $177 as at February 29, 2012. The increase in working capital was primarily attributed to a secured promissory note (the “Note”) in an aggregate principal amount of $100,000 pursuant to the terms of a subscription. The Note bears interest at an annual rate of 10% which is to be paid with principal in full on the maturity date of February 27, 2015. The principal amount of the Note together with interest may be converted into shares of our common stock, at the option of the holder, at a conversion price of $0.25 per share.

Cash Flow from Operating Activities

During the year ended February 28, 2013, our company used $40,377 in cash from operating activities compared to the use of $80 of cash for operating activities during the year ended February 29, 2012. The increase in cash used for operating activities was attributed to increases in expenses paid on our company’s behalf by a related party, accretion expenses on the oil and gas property and accounts payable.

Cash Flow from Investing Activities

During the year ended February 28, 2013, our company used $Nil cash for investing activities compared to cash used in investing activities of $15,000 during the year ended February 28, 2012.

Cash Flow from Financing Activities

During the year ended February 28, 2013, our company received $139,750 in cash in financing activities primarily from proceeds from convertible notes payable and the issuance of common shares compared to cash provided by financing activities of $15,257 for the year ended February 29, 2012.

To meet our need for cash we raised $33,250 from the sale of 33,250,000 registered shares pursuant to our S-1 Registration Statement filed with the SEC, which became effective on July 12, 2012.

Our directors have verbally agreed to advance funds, on an as-needed basis, to assist in start-up operations, including expenses associated with our current offering, and to continue limited operations if sufficient funds are not raised in our offering. The directors both proposed the verbal commitment to loan in order to ensure that our company would be able to continue its operations in the event sufficient funds are not raised in our offering. While they have agreed to advance the funds, the agreement is verbal. Because there is no written agreement to loan funds and the verbal agreement may be withdrawn at any time, the verbal agreement is unenforceable. To date, Dallas Kerkenezov, one of our officers and directors, is the only director to advance funds to our company. As of February 28, 2013, Mr. Kerkenezov has advanced $8,274.

We received our initial funding of $20,257 through the sale of common stock to Dallas Kerkenezov, who purchased 30,513,100 shares of common stock at $0.001 in February 2012 for $10,257 and for forgiveness of a note payable for $5,000, and, 10,000,000 shares to Sasha Heredia for a $5,000 subscription receivable which was paid in August 2012. During the year ended February 28, 2013, we issued 33,250,000 shares of common stock at $0.001, resulting in total shares issued and outstanding as of February 28, 2013 of 73,763,100. From inception until the date of this filing, we have had limited operating activities. Our financial statements from inception (November 12, 2010) through the period ended February 28, 2013, reported no revenues and a net loss of $44,090.

24

Effective February 27, 2013, our company entered into a secured promissory note in an aggregate principal amount of $100,000 pursuant to the terms of a subscription. The note bears interest at an annual rate of 10% which is to be paid with principal in full on the maturity date of February 27, 2015. The principal amount of the note together with interest may be converted into shares of our common stock, at the option of the holder, at a conversion price of $0.25 per share.

Subsequent to February 28, 2013, our company entered in the following notes:

· Effective April 5, 2013, we entered into a secured promissory note in an aggregate principal amount of $50,000 pursuant to the terms of a subscription agreement. The note bears interest at an annual rate of 10% which is to be paid with principal in full on the maturity date of April 5, 2015. The principal amount of the note together with interest may be converted into shares of our common stock at the option of the holder, at a conversion price of $0.30 per share.

· Effective April 25, 2013, we entered into a secured promissory note in an aggregate principal amount of $180,000 pursuant to the terms of a subscription agreement between our company and Jackson Bennett, LLC. The note bears interest at an annual rate of 10% which is to be paid with principal in full on the maturity date of April 25, 2015. The principal amount of the note together with interest may be converted into shares of our common stock at the option of the holder, at a conversion price of $0.50 per share.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures, or capital resources that is material to investors.

Critical Accounting Policies

Basis of Presentation

The financial statements of our company have been prepared in accordance with generally accepted accounting principles in the United States of America and are presented in US dollars. Our company's fiscal year end is February 28.

Cash and Cash Equivalents

Our company considers all highly liquid instruments with a maturity of three months or less at the time of issuance to be cash equivalents. Our company had $99,550 and $177 of cash and cash equivalents at February 28, 2013 and February 29, 2012, respectively.

Use of Estimates and Assumptions

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Income Taxes

Income taxes are accounted for under the assets and liability method. Deferred tax assets and liabilities are recognized for the estimated future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax bases and operating loss and tax credit carry forwards. Deferred tax assets and liabilities are measured using enacted tax rates in effect for the year in which those temporary differences are expected to be recovered or settled.

25

Basic and Diluted Net Loss per Share

Our company computes net loss per share in accordance with SFAS No. 128,"Earnings per Share". SFAS No. 128 requires presentation of both basic and diluted earnings per share (EPS) on the face of the income statement.

Basic EPS is computed by dividing net loss available to common shareholders (numerator) by the weighted average number of shares outstanding (denominator) during the period. Diluted EPS gives effect to all potentially dilutive common shares outstanding during the period. Diluted EPS excludes all potentially dilutive shares if their effect is anti-dilutive. At February 28, 2013 and February 29, 2012, no potentially dilutive shares were issued or outstanding.

Oil and Gas Properties

Our company uses the full cost method of accounting for oil and natural gas properties. Under this method, all acquisition, exploration and development costs, including certain payroll, asset retirement costs, other internal costs, and interest incurred for the purpose of finding oil and natural gas reserves, are capitalized. Internal costs that are capitalized are directly attributable to acquisition, exploration and development activities and do not include costs related to production, general corporate overhead or similar activities. Costs associated with production and general corporate activities are expensed in the period incurred. Proceeds from the sale of oil and natural gas properties are applied to reduce the capitalized costs of oil and natural gas properties unless the sale would significantly alter the relationship between capitalized costs and proved reserves, in which case a gain or loss is recognized.

Capitalized costs associated with impaired properties and capitalized costs related to properties having proved reserves, plus the estimated future development costs, and asset retirement costs under ASC 410 “Asset Retirement and Environmental Obligations”, are amortized using the unit-of-production method based on proved reserves. Capitalized costs of oil and natural gas properties, net of accumulated amortization and deferred income taxes, are limited to the total of estimated future net cash flows from proved oil and natural gas reserves, discounted at ten percent, plus the cost of unevaluated properties.

There are many factors, including global events that may influence the production, processing, marketing and price of oil and natural gas. A reduction in the valuation of oil and natural gas properties resulting from declining prices or production could adversely impact depletion rates and capitalized cost limitations. Capitalized costs associated with properties that have not been evaluated through drilling or seismic analysis, including exploration wells in progress at February 29, 2012, are excluded from the unit-of-production amortization. Exclusions are adjusted annually based on drilling results and interpretative analysis.

Sales of oil and natural gas properties are accounted for as adjustments to the net full cost pool with no gain or loss recognized, unless the adjustment would significantly alter the relationship between capitalized costs and proved reserves. If it is determined that the relationship is significantly altered, the corresponding gain or loss will be recognized in the statements of operations.

Costs of oil and gas properties are amortized using the units of production method.

26

Ceiling test: Under the full-cost method of accounting, the net book value of oil and gas properties, less related deferred income taxes, may not exceed a calculated “ceiling.” The ceiling limitation is the estimated after-tax future net cash flows from proved oil and gas reserves, discounted at 10 percent per annum and adjusted for cash flow hedges. Estimated future net cash flows exclude future cash outflows associated with settling accrued asset retirement obligations. Our company has adopted U.S. Securities and Exchange Commission (“SEC”) Release 33-8995 and the amendments to ASC 932, “Extractive Industries — Oil and Gas” (the Modernization Rules). Under the Modernization Rules, estimated future net cash flows are calculated using end-of-period costs and an unweighted arithmetic average of commodity prices in effect on the first day of each of the previous 12 months, held flat for the life of the production, except where prices are defined by contractual arrangements.

Any excess of the net book value of proved oil and gas properties, less related deferred income taxes, over the ceiling is charged to expense and reflected as additional depletion, depreciation and amortization expense (“DD&A”) in the accompanying statement of operations. Such limitations are tested quarterly. As of February 28, 2013 and February 29, 2012, capitalized costs did not exceed the ceiling limitation, and no write-down was indicated.

Recent Accounting Pronouncements

Except for rules and interpretive releases of the SEC under authority of federal securities laws and a limited number of grandfathered standards, the FASB Accounting Standards Codification™ (“ASC”) is the sole source of authoritative GAAP literature recognized by the FASB and applicable to our company. Management has reviewed the aforementioned rules and releases and believes any effect will not have a material impact on our company's present or future consolidated financial statements.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

As a “smaller reporting company”, we are not required to provide the information required by this Item.

Item 8. Financial Statements and Supplementary Data

27

NORSTRA ENERGY, INC.

(An Exploration Stage Company)

INDEX TO AUDITED FINANCIAL STATEMENTS

From Inception on November 12, 2010 through February 28, 2013

|

|

Page |

|

|

|

|

Audit Report of Independent Accountants |

F-2 |

|

|

|

|

Balance Sheets |

F-3 |

|

|

|

|

Statements of Operations |

F-4 |

|

|

|

|

Statement of Stockholders’ Equity (Deficit) |

F-5 |

|

|

|

|

Statements of Cash Flows |

F-6 |

|

|

|

|

Notes to the Audited Financial Statements |

F-7 |

_______________________________________

F-1

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors

Norstra Energy, Inc.