Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - OCEANFIRST FINANCIAL CORP | d550137d8k.htm |

NASDAQ: OCFC

1

OceanFirst Financial Corp.

OceanFirst Financial Corp.

INVESTOR PRESENTATION

INVESTOR PRESENTATION

JUNE 2013

JUNE 2013

Exhibit 99.1 |

NASDAQ: OCFC

2

OceanFirst Financial Corp.

OceanFirst Financial Corp.

Forward Looking Statements:

This

presentation

contains

certain

forward-looking

statements

within

the

meaning

of

the

Private

Securities

Reform

Act

of

1995

which

are

based

on

certain

assumptions

and

describe

future

plans,

strategies

and

expectations

of

the

Company.

These

forward-looking

statements

are

generally

identified

by

use

of

the

words

"believe,"

"expect,"

"intend,"

"anticipate,"

"estimate,"

"project,"

"will,"

"should,"

"may,"

"view,"

"opportunity,"

"potential,"

or

similar

expressions

or

expressions

of

confidence.

The

Company's

ability

to

predict

results

or

the

actual

effect

of

future

plans

or

strategies

is

inherently

uncertain.

Factors

which

could

have

a

material

adverse

effect

on

the

operations

of

the

Company

and

its

subsidiaries

include,

but

are

not

limited

to,

changes

in

interest

rates,

general

economic

conditions,

levels

of

unemployment

in

the

Bank’s

lending

area,

real

estate

market

values

in

the

Bank’s

lending

area,

the

level

of

prepayments

on

loans

and

mortgage-backed

securities,

legislative/regulatory

changes,

monetary

and

fiscal

policies

of

the

U.S.

Government

including

policies

of

the

U.S.

Treasury

and

the

Board

of

Governors

of

the

Federal

Reserve

System,

the

quality

or

composition

of

the

loan

or

investment

portfolios,

demand

for

loan

products,

deposit

flows,

competition,

demand

for

financial

services

in

the

Company's

market

area

and

accounting

principles

and

guidelines.

These

risks

and

uncertainties

are

further

discussed

in

the

Company’s

Annual

Report

on

Form

10-K

for

the

year

ended

December

31,

2012

and

should

be

considered

in

evaluating

forward-looking

statements

and

undue

reliance

should

not

be

placed

on

such

statements.

The

Company

does

not

undertake

-

and

specifically

disclaims

any

obligation

-

to

publicly

release

the

result

of

any

revisions

which

may

be

made

to

any

forward-looking

statements

to

reflect

events

or

circumstances

after

the

date

of

such

statements

or

to

reflect

the

occurrence

of

anticipated

or

unanticipated

events. |

NASDAQ: OCFC

3

111 Years of Growth and Capital Management

111 Years of Growth and Capital Management

Founded in Point Pleasant, NJ, in 1902, OceanFirst has grown from a small

one-town savings and loan to a full-service community bank serving

the Central New Jersey shore. Rebuilt capital through the Great Recession with

retained earnings and completion of a follow-on common stock

offering in November 2009. OceanFirst issued stock for the first time in 1996

and over the ensuing years generated value for

shareholders,

largely

through

the

successful

implementation

and

execution

of

our

community bank model, and the strategic repurchase of 62.4% of original IPO

shares. 2011 and 2012 share repurchase plans begin the redeployment of the

excess capital rebuilt since 2008. Under the current authorization,

580,444 shares remain available for repurchase. |

NASDAQ: OCFC

4

Community Bank serving the Central

Jersey Shore -

$2.3 billion in assets

and 25 branch offices

Market Cap $253.8 million (as of

June 3, 2013)

Core deposit funded –

87.5%

of total

deposits

Locally originated loan portfolio with

no brokered loans

Residential and commercial

mortgages

Consumer equity loans and lines

C&I loans and lines

Corporate Profile

Corporate Profile

Note: See Appendix 1 for Market Demographic information.

!

(

Ocean

Burlington

Morris

Sussex

Atlantic

Salem

Warren

Monmouth

Hunterdon

Cumberland

Bergen

Mercer

Somerset

Middlesex

Gloucester

Camden

Passaic

Cape May

Essex

Union

Hudson

Philadelphia

New York |

NASDAQ: OCFC

5

Experienced Executive Management Team

Experienced Executive Management Team

Substantial

insider

ownership

of

27.3%

–

aligned

with

shareholders’

interest

OceanFirst Bank ESOP 10.5%

Directors & Senior Executive Officers 9.7% (CEO 5.7%)

Director and Proxy Officer Stock Ownership Guidelines

OceanFirst Foundation 7.1%

As of the March 12, 2013 proxy

record date.

Name

Position

# of Years in

Banking

# of Years

at OCFC

John R. Garbarino

Chairman, Chief Executive Officer

41

41

Christopher D. Maher

President, Chief Operating Officer

25

-

Michael J. Fitzpatrick

Executive Vice President, Chief Financial Officer

31

20

Joseph R. Iantosca

Executive Vice President, Chief Administrative Officer

35

9

Joseph J. Lebel III

Executive Vice President, Chief Lending Officer

29

7

Succession

planning

refreshed

in

2013 –

new

President

recruited

and

2

new

Executive Vice Presidents promoted |

NASDAQ: OCFC

6

Our Strategy

Our Strategy

Positioned as the leading Community Bank in attractive Central

Jersey Shore market –

growing revenue and creating additional

value for our shareholders

Offering a full range of consumer and commercial banking products

generating diversified income streams

Guarding

credit

quality

in

ALL

business

cycles

Transitioning the balance sheet with emphasis on core deposit

funding and commercial lending growth

On the watch for roll-up opportunities presented by in-market

“regulatory fatigued”

competitors |

NASDAQ: OCFC

7

Earnings per share of $0.26 -

adversely impacted by extraordinary loan

repurchase reserve activity

Tangible book value continues to grow, increasing to $12.43

Strong capital position –

tangible common equity of 9.5% of assets

Returning Excess Capital –

254,340 shares repurchased in quarter

Grew core deposits (i.e. all deposits excluding time deposits)

$29.5 million, now comprising 87.5% of total deposits

Credit quality stabilizing with NPL’s (excluding the increase caused by

Sandy) decreasing $406,000 from December 31, 2012

Highlights –

Highlights –

First Quarter 2013

First Quarter 2013 |

NASDAQ: OCFC

8

Substantial Primary Market Deposit Share

Substantial Primary Market Deposit Share

June 30, 2012

# of

Dep. In Mkt.

Mkt. Shr.

Rank

Institution

Branches

($000)

(%)

Ocean County, NJ

1

Hudson City Bancorp Inc. (NJ)

14

2,610,613

18.65

2

Wells Fargo Bank NA (CA)

26

2,360,712

16.87

3

TD Bank, National Association (Canada)

21

2,149,131

15.36

4

OceanFirst Financial Corp. (NJ)

19

1,477,780

10.56

5

Banco Santander S.A. (Spain)

25

1,321,262

9.44

6

Bank of America Corp. (NC)

22

1,161,899

8.30

7

Investors Bancorp Inc. (MHC) (NJ)

8

654,369

4.68

8

PNC Financial Services Group (PA)

14

436,177

3.12

9

Manasquan Savings Bank (NJ)

3

252,922

1.81

10

JPMorgan Chase Bank, National Association (OH)

10

230,732

1.65

Total For Institutions In Market

200

13,996,221

Source: FDIC |

NASDAQ: OCFC

9

Strategic Deposit Composition Transition

Strategic Deposit Composition Transition |

NASDAQ: OCFC

10

Strategic Loan Composition Transition

Strategic Loan Composition Transition |

NASDAQ: OCFC

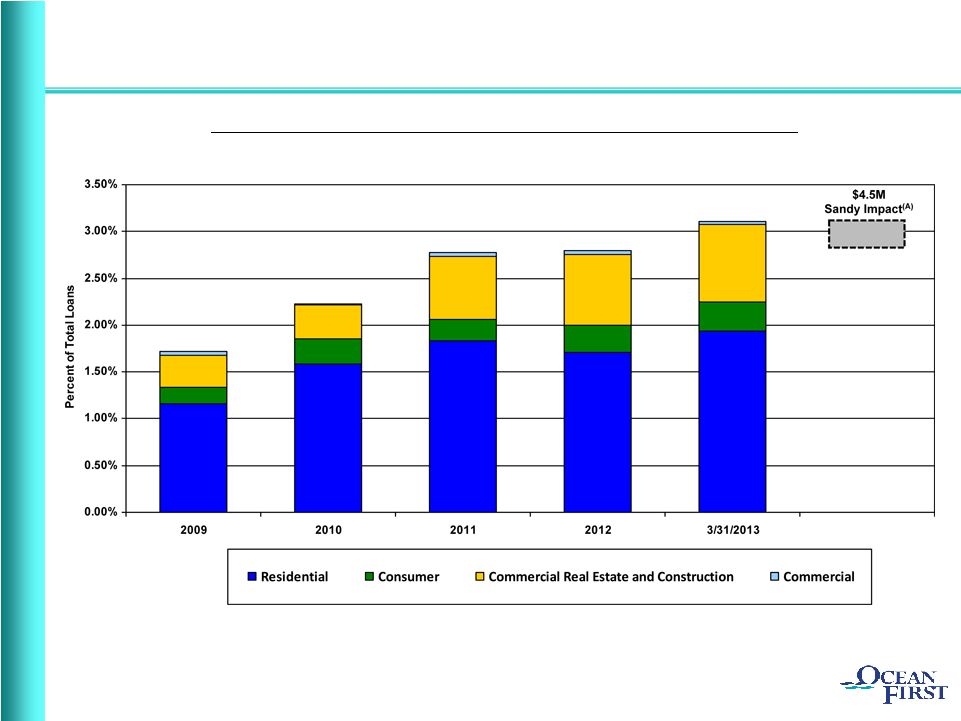

11

Stabilized NPL’s in a Diversified Portfolio

Stabilized NPL’s in a Diversified Portfolio

Non-performing loan (“NPL”).

Data as of December 31, unless otherwise noted.

(A)

Increase traced to superstorm Sandy.

Exposure Concentrated in Lower Risk One-to-Four Family

|

NASDAQ: OCFC

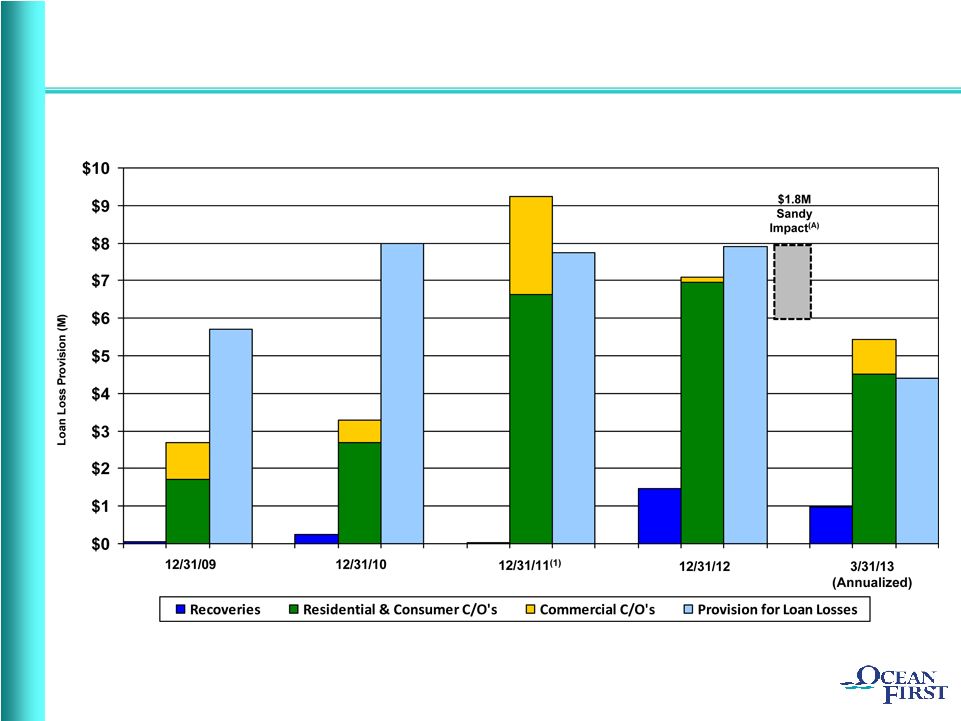

12

Prudently Provisioning for Credit Costs

Prudently Provisioning for Credit Costs

(1)

Increase in charge-offs was primarily due to a change in the Company’s

charge-off policy to recognize the charge-off when the loan is

deemed uncollectible rather than when the foreclosure process is complete. The additional charge-off

relating to the change in policy through 2011 was $5.7 million, all of which was

previously specifically reserved for by the Company.

(A)

Increase traced to superstorm Sandy. |

NASDAQ: OCFC

13

Net Interest Margin

Net Interest Margin

Remaining Under Pressure in Low Interest Rate Environment

|

NASDAQ: OCFC

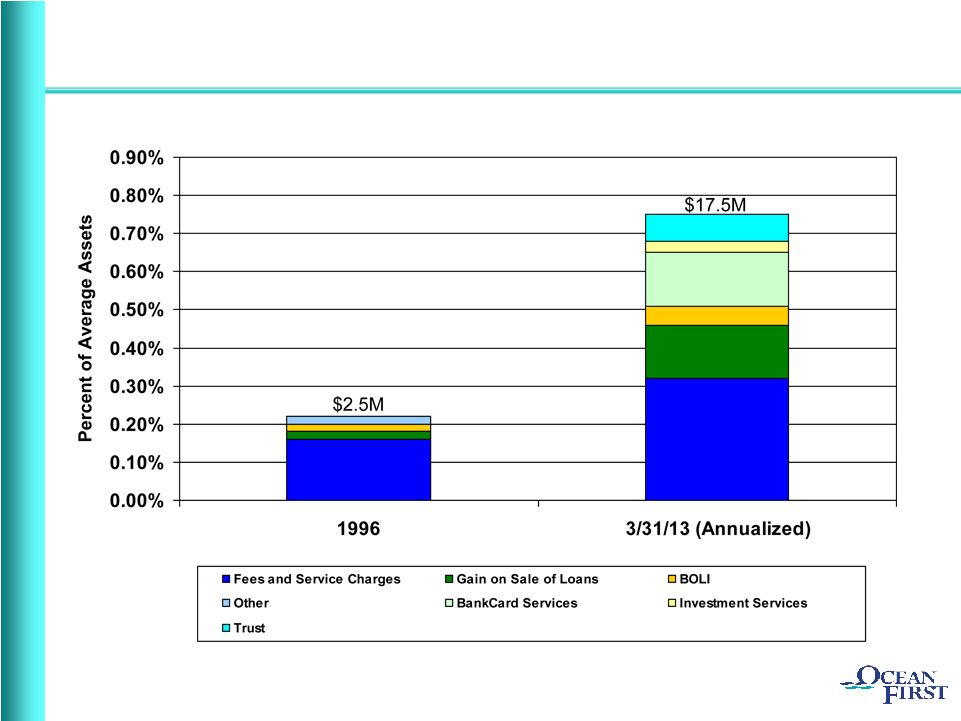

14

Diversified Streams of Non-Interest Income

Diversified Streams of Non-Interest Income

2011

Non-Interest Income excludes gain/loss from other real estate operations, gain

on sale of equity securities and provision for repurchased loans.

|

NASDAQ: OCFC

15

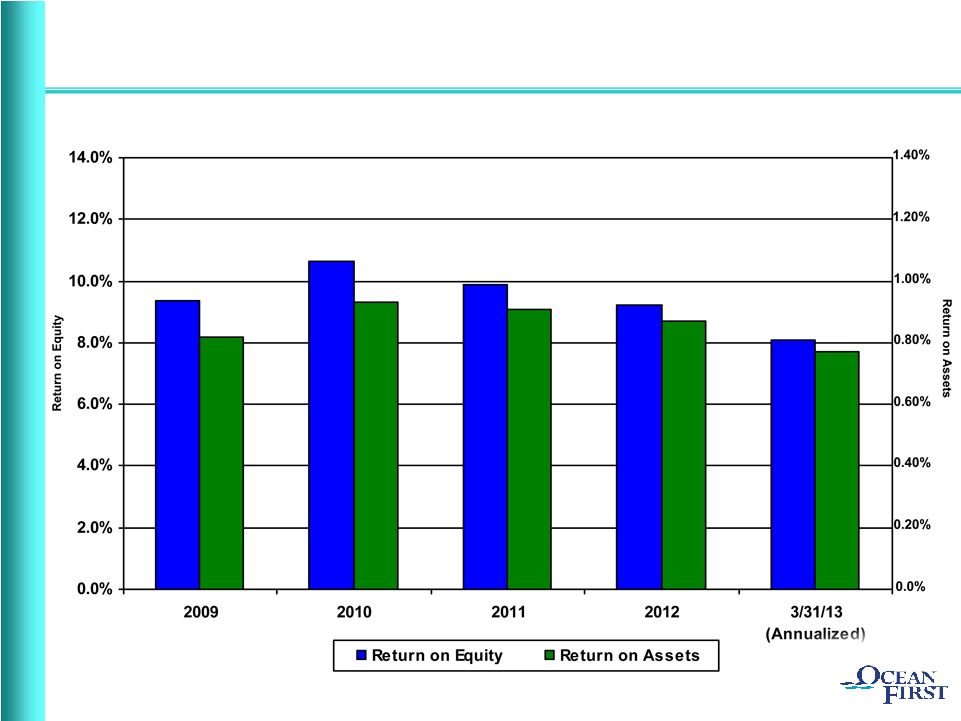

Generating Attractive Returns

Generating Attractive Returns |

NASDAQ: OCFC

16

Challenge Today is to Grow Revenue

Challenge Today is to Grow Revenue

Build Shareholder Value

Build Shareholder Value

Target growth within existing market –

increasing share

Fourteen de novo branches since 2000 have performed well –

still present

opportunity for additional growth

Expanding presence in Monmouth County with the Red Bank Financial

Solutions Center opened in May

Opportunity to meet extraordinary loan demand –

Sandy recovery

Non-interest income streams have been diversified, ever more important

as margin remains under pressure

Assessing opportunistic roll-up of community banks in market

Share repurchases safely return excess capital in the short term

Financial performance to Plan builds value and preserves the right to

remain independent |

NASDAQ: OCFC

17

(1)

Peers include: DCOM, FFIC, FLIC, HVB, LBAI, ORIT, PBNY, PGC, RCKB, SNBC,

SUBK, UVSP and WSFS Note:Financial data as of the most recent period

available; market data as of June 3, 2013. Source: Sandler

O’Neill. Attractive Valuation Metrics

Attractive Valuation Metrics

OCFC

Peers

(1)

Valuation

Price / Tang. Book Value

116%

133%

Price / LQA EPS

13.8x

15.6x

Price / Estimated EPS

13.3x

14.2x

Cash Dividend Yield

3.3%

2.9% |

NASDAQ: OCFC

18

Why OCFC…?

Why OCFC…?

Fundamental

franchise

value

–

superior

market

demographics

Crisis tested management team

Sandy response and experience

Substantial

insider

ownership

–

aligned

with

shareholders

Succession planning refreshed

Attractive deposit mix and market share

Conservative credit culture and profile

Solid

financial

performance

–

developing

shareholder

value

Strong balance sheet and capital base

Attractive current valuations |

|

NASDAQ: OCFC

20

Market Demographics

Market Demographics

APPENDIX 1

Ocean

Monmouth

Middlesex

New Jersey

National

Number of Offices

19

4

1

% of OceanFirst Deposits

85.7

11.1

3.2

Market Rank

4

18

34

Market Share (%)

10.6

1.0

0.2

Population

578,728

649,429

794,605

Projected 2010-2015

Population Growth (%)

4.0

2.0

1.8

1.2

3.8

Median Household Income ($)

60,936

82,974

78,561

72,519

54,442

Projected 2010-2015 Median

Household Income Growth (%)

15.5

14.3

17.5

14.7

12.4

Deposit data as of June 30, 2012.

Demographic data as of June 30, 2010.

Source: SNL Financial |

NASDAQ: OCFC

21

One-to-Four Family (1-4)

Average size of mortgage loans

$185,000

Interest-only loans - Amount

$35.3 million

- % of total 1-4 family loans

4.4%

- Weighted average loan-to-value ratio

(using original or most recent appraisal) 74%

Stated income loans - Amount

$45.6 million

- % of total 1-4 family

loans 5.7%

Portfolio weighted average loan-to-value ratio (using original or most recent appraisal)

56%

- Originated for the three months ended March

31, 2013 61%

- Originated for the year ended December 31,

2012 59%

Average FICO score

748

- Loans originated for the three months ended

March 31, 2013 767

- Loans originated for the year ended December

31, 2012 767

% of loans outside the New York/New Jersey market

4.7%

% of loans outside Ocean/Monmouth Counties

34.2%

% of jumbo loans at time of origination

43.8%

% of loans for second homes

7.6%

APPENDIX 2

Residential Portfolio Metrics

Residential Portfolio Metrics

As of March 31, 2013, unless

otherwise noted. |

NASDAQ: OCFC

22

Commercial Real Estate (CRE)

Total portfolio

(1)

$470.5 million

Average size of CRE loans

$770,000

Largest CRE loan

$16.2 million

(Secured by local university dormitory housing)

Commercial Loans

Total portfolio

(1)

$63.7 million

Average size of commercial loan

$258,000

Largest commercial loan

$4.7 million

(1)

Commercial portfolio relationships total 382, excluding small business loans.

APPENDIX 2

(Cont’d)

Commercial Portfolio Metrics

Commercial Portfolio Metrics

As of March 31, 2013. |

NASDAQ: OCFC

23

Commercial Portfolio Segmentation

Commercial Portfolio Segmentation

Real Estate

Investment, 32.0%

Arts/Entertainment/

Recreation, 7.4%

Other Services, 4.0%

Retail Trade, 3.8%

Public

Administration, 6.5%

Miscellaneous, 6.1%

Manufacturing, 4.3%

Educational Services,

4.7%

Accommodations/

Food Services, 7.8%

Healthcare, 9.9%

Wholesale Trade,

6.4%

Construction, 7.1%

Total Commercial Loan Exposure

by Industry Concentration

Real Estate Investment by

Property Concentration

Office, 34.6%

Shopping Center, 9.1%

Retail Store, 8.0%

Multi-Family, 3.5%

Miscellaneous, 14.2%

Commercial

Development, 10.4%

Industrial/

Warehouse, 13.6%

Residential

Development, 6.6%

As of March 31, 2013.

APPENDIX 2

(Cont’d) |

NASDAQ: OCFC

24

Impact of Superstorm Sandy

Impact of Superstorm Sandy

APPENDIX 3

Residential loans as of March 31, 2013:

Borrowers impacted by the storm

124

Principal Balance

$30.1 million

Average Loan Size

$243,000

Loan Status:

Borrowers

Balance (000’s)

Loans repaid or brought current

80

$19,421

Temporary repayment plan agreed to under which the borrower is performing

18

4,494

Loan is 30-89 days delinquent

8

1,705

Loan is 90 days or more delinquent

18

4,469

Total

124

$30,089

Using conservative assumptions, specific impairments total $326,000. These

impairments are covered by a year-end provision of $1.8 million related to the

adverse impact of Sandy and expectation of increasing levels of non-performing

loans in the recovery period. Commercial loans as of March 31, 2013:

No adverse impact. |