Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - VinCompass Corp. | Financial_Report.xls |

| EX-10.3 - EXHIBIT 10.3 - VinCompass Corp. | exhibit10-3.htm |

| EX-32.1 - EXHIBIT 32.1 - VinCompass Corp. | exhibit32-1.htm |

| EX-32.2 - EXHIBIT 32.2 - VinCompass Corp. | exhibit32-2.htm |

| EX-31.1 - EXHIBIT 31.1 - VinCompass Corp. | exhibit31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - VinCompass Corp. | exhibit31-2.htm |

UNITED STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[ X ] ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended FEBRUARY 28, 2013

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE EXCHANGE ACT

For the transition period from _____to _______

Commission file number: 000-54567

TIGER JIUJIANG MINING,

INC.

(Exact name of small business issuer in its charter)

| Wyoming | 80-0552115 |

| (State or jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 6F, No.81 Meishu East 6 Road, Kaohsiung, Taiwan | 804 |

| (Address of principal executive offices) | (Zip Code) |

Issuer’s telephone number: (888) 755-9766

Issuer’s

email address: tigerjiujiangmining@gmail.com

Securities Registered Under Section 12(b) of the Exchange Act: None

Securities Registered Under Section 12(g) of the Exchange

Act:

Common Stock, $0.001 par value

(Title of class)

Indicate by check mark if the registrant is a well-known

seasoned issuer as defined by Rule 405 of the Securities Act (the “Act” or

“Securities Act”)

Yes [ ] No [ x ]

Indicate by check mark if the registrant is not required

to file reports pursuant to Rule 13 or Section 15(d) of the Act

Yes [ ] No [ x ]

Indicate by check mark whether the issuer (1) has filed

all reports required to be filed by Section 13 or 15(d) of the Exchange Act

during the past 12 months (or for such shorter period that the registrant was

required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days.

Yes [ x ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant Rule 405 of Regulation S-T (s 220.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files. Yes [ x ] No [ ]

Check if disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained in this form, and no disclosure will be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, a non-accelerated filer or a smaller reporter.

| Large accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated filer [ ] | Smaller reporting company [ x ] |

Indicate by check mark whether the registrant is a shell

company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ x ] No [ ]

Issuer's revenues for its most recent fiscal year: $0.

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed fiscal quarter: 8,500,000 common shares at $0.05* = $425,000. (* - last price at which the Corporation’s stock was issued through its initial public offering; although the Corporation is quoted on the OTC-BB, no shares have been traded electronically or otherwise in the past year).

2

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

State the number of shares outstanding of each of the Issuer's classes of common stock, as of the latest practicable date: 8,500,000 common shares issued and outstanding as of the date of this report.

Transitional Small Business Disclosure Format (Check one):

Yes

[ ] No [ x ]

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K into which the document is incorporated: (1) any annual report to shareholders; (2) any proxy or information statement and (3) any prospectus filed pursuant to Rule 424(b) or (c) under the Securities Act of 1933, as amended (the “Securities Act”):

- Registration Statement on Form S-1 as amended on October 26, 2011, and which became effective on December 8, 2011 whereby we offered up to 2,000,000 shares of common stock and five shareholders resold 1,500,000 previously issued shares. The offering closed on April 30, 2011, following the sale of 2,000,000 common shares to 35 subscribers. Included with the S-1 registration statements were our audited financial statements for the year ending February 28, 2011.

- Exhibit 3.1 (Articles of Incorporation) dated January 18 2010, Exhibit 3.2 (Bylaws) dated January 31, 2010, Exhibit 10.1 (Option To Purchase And Royalty Agreement between Tiger Jiujiang Mining, Inc. and Kiukiang Gold Mining Company of Jiujiang City, Jiujiang, China) dated February 22, 2011, Exhibit 10.2 (Code Of Business Conduct & Ethics and Compliance Program) dated February 22, 2010, Exhibit 10.3 (First Amendment to Option to Purchase and Royalty Agreement) dated May 2, 2011, all filed as exhibits to Tiger’s Form S-1 dated October 26, 2011.

TABLE OF CONTENTS

Cautionary Statement Regarding Forward-Looking Statements

This annual report contains forward-looking statements as that term is defined in the Private Securities Litigation Reform Act of 1995. These statements relate to future events or our future financial performance. Some discussions in this report may contain forward-looking statements that involve risk and uncertainty. A number of important factors could cause our actual results to differ materially from those expressed in any forward-looking statements made in this report. Forward-looking statements are often identified by words like: “believe”, “expect”, “estimate”, “anticipate”, “intend”, “project” and similar expressions or words which, by their nature, refer to future events.

In some cases, you can also identify forward-looking statements by terminology such as “may”, “will”, “should”, “plans”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors”, beginning on page 4, that may cause our or our industry's actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

3

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

Our financial statements are stated in United States Dollars (US$) and are prepared in accordance with United States Generally Accepted Accounting Principles. References to common shares refer to common shares in our capital stock.

Our optioned mineral exploration property is located in China and costs expressed in the geological report are expressed in Renminbi (“RMB”) or Yuan. For purposes of consistency and to express United States Dollars throughout this registration statement, Yuan or RMB have been converted into United States currency at current rates of approximately 7.5 RMB to 1 U.S. Dollar. Our agreements and related items are all in U.S. Dollars.

As used in this annual report, the terms “we”, “us”, “our”, and “Tiger” mean Tiger Jiujiang Mining, Inc. unless otherwise indicated.

Tiger is an exploration stage Corporation. There is no assurance that commercially viable mineral deposits exist on the claims we have under option. Further exploration and/or drilling will be required before a final evaluation as to the economic and legal feasibility of our projects is determined.

Glossary of Exploration Terms

The following terms, when used in this report, have the respective meanings specified below:

| Deposit |

When mineralized material has been systematically drilled and explored to the degree that a reasonable estimate of tonnage and economic grade can be made. |

| Development |

Preparation of a mineral deposit for commercial production, including installation of plant and machinery and the construction of all related facilities. The development of a mineral deposit can only be made after a commercially viable mineral deposit, a reserve, has been appropriately evaluated as economically and legally feasible. |

| Diamond drill |

A type of rotary drill in which the cutting is done by abrasion rather than percussion. The cutting bit is set with diamonds and is attached to the end of long hollow rods through which water is pumped to the cutting face. The drill cuts a core of rock, which is recovered in long cylindrical sections an inch or more in diameter. |

| Exploration |

The prospecting, trenching, mapping, sampling, geochemistry, geophysics, diamond drilling and other work involved in searching for mineral bodies’ a mining prospect which has not yet reached either the development or production stage. |

| Mineral |

A naturally occurring inorganic element or compound having an orderly internal structure and characteristic chemical composition, crystal form and physical properties. |

| Mineral |

A mineral reserve is that part of a deposit which could be economically and legally |

| Reserve |

extracted or produced at the time of the reserve determination. |

| Mineralization |

Rock containing an undetermined amount of minerals or metals. |

| Oxide |

Mineralized rock in which some of the original minerals, usually sulphide, have been oxidized. Oxidation tends to make the mineral more porous and permits a more complete permeation of cyanide solutions so that minute particles of gold in the interior of the minerals will be more readily dissolved. |

| Stratigraphy |

A branch of geology dealing with the classification, nomenclature, correlation, and interpretation of stratified rocks. |

4

|

Trenching |

The digging of long, narrow excavation through soil, or rock, to expose potential mineralization for geological examination or assays. |

| Waste | Material that is too low in grade to be mined and milled at a profit. |

PART I

Item 1. Description of Business.

Overview

We were incorporated in the State of Wyoming on January 28, 2010, and established a fiscal year end of February 28. Our statutory registered agent's office is located at 1620 Central Avenue, Suite 202, Cheyenne, Wyoming 82001 and our business office is located at 6F, No.81 Meishu East 6 Road, Kaohsiung, Taiwan 804.

We have not had any bankruptcy, receivership or similar proceeding since incorporation. There have been no material reclassifications, mergers, consolidations or purchases or sales of any significant amount of assets not in the ordinary course of business since the date of incorporation. We are a start-up, exploration stage company engaged in the search for gold and related minerals. There is no assurance that a commercially viable mineral deposit, a reserve, exists in our claim or can be shown to exist until sufficient and appropriate exploration is done and a comprehensive evaluation of such work concludes economic and legal feasibility.

Our Current Business – Mineral Exploration

On February 22, 2010, as amended on May 2, 2011, and as further amended on May 22, 2013, we entered into an option agreement to finance a two-phase exploration program whereby we can earn a 50 percent or greater interest in the Tiger gold exploration property in northern Jiujiang Province, China. The Option To Purchase And Royalty Agreement is with Kiukiang Gold Mining Company of Jiujiang City, Jiujiang, China, the beneficial owner, an arms-length Chinese corporation whereby we can acquire an interest by making certain expenditures and carrying out certain exploration work. The property is in good standing until December 8, 2015.

Under the terms of the agreement and the amendment, Kiukiang granted to Tiger the right to acquire 50% of the right, title and interest of Kiukiang in the property, subject to its receiving annual payments and a royalty, in accordance with the terms of the agreement, as follows:

| (a) |

Tiger contributing exploration expenditures on the property of a minimum of $15,000 on or before May 31, 2012 (* paid and work completed but report still pending); | |

| (b) |

Tiger contributing exploration expenditures of a further US $45,000 for aggregate minimum contributed exploration expenses of $60,000 on or before May 31, 2014; | |

| (c) |

Tiger shall allot and issue 1,000,000 shares in the capital of Tiger to Kiukiang upon completion of a phase I exploration program as recommended by a competent geologist with the proviso that the report recommends further work be carried out on the Tiger property; | |

| (d) |

Tiger will pay to Kiukiang an annual royalty equal to three percent (3%) of Net Smelter Returns; | |

| (e) |

Upon exercise of the option, Tiger will pay to Kiukiang $25,000 per annum commencing on May 31, 2016, as prepayment of the NSR; and | |

| (f) |

Tiger has the right to acquire an additional 25% of the right, title and interest in and to the property by the payment of $10,000 and by incurring an additional $50,000 in exploration expenditures on or before May 31, 2015. |

Further, the Agreement and the Option will terminate:

| (a) |

on May 31, 2012 at 11:59 P.M., unless on or before that date, Tiger Jiujiang has incurred exploration expenditures of a minimum of US $20,000 on the Property; | |

| (b) |

on May 31, 2013 at 11:59 P.M., unless on or before that date, Tiger Jiujiang has incurred exploration expenditures of a cumulative minimum of US $60,000 on the Property; |

5

| (c) |

at 11:59 P.M. on May 31 of each and every year, commencing on May 31, 2015, unless Tiger Jiujiang has paid to Kiukiang the sum of US $25,000 on or before that date. |

The property is unencumbered and there are no competitive conditions which affect it. Further, there is no insurance covering the property. We believe that no insurance is necessary since it is unimproved and contains no buildings or improvements.

If the results of phase I are unfavourable, we will terminate the option agreement and will not be obligated to make any subsequent payments. Similarly, if the results of phase II are unfavourable, we will terminate the option and will not be obligated to make any subsequent payments.

To date we have completed the field work portion of the first phase work program on the Tiger property but have encountered delays in obtaining the final report and do not anticipate receiving the finalized report until approximately July, 2013; we have not spent any money on research and development activities. Tiger is an exploration stage corporation. There is no assurance that a commercially viable deposit exists on the mineral claims that we have under option. Further exploration will be required before an evaluation as to the economic and legal feasibility of the claims is determined.

Our Proposed Exploration Program – Plan of Operation

Our business plan is to proceed with initial exploration of the Tiger property to determine if there are commercially exploitable deposits of gold. We plan a two-phase exploration program to properly evaluate the potential of the property. We must conduct exploration to determine if gold exists and if any is found it can be economically extracted and profitably processed. We do not claim to have any ores or reserves whatsoever at this time.

We anticipated that our portion of the phase I planned geological exploration program would cost $20,000 (which is 50% of the totally budgeted cost of $40,000; we advanced our portion of the required funding on May 31, 2012) which is a reflection of local costs for the specified type of work. Phase I commenced on August 13, 2012, and required six weeks for the base work which was completed on September 20, 2012, and was to require an additional four to six months for analysis, evaluation of the work completed and the preparation of a report which has been well exceeded; we now expect to receive the final report on the phase I work in July, 2013. Costs for phase I were made up of wages, fees, geological and geochemical supplies, assaying, equipment, diamond drilling and operation costs. We will assess the results of this program upon receipt of an appropriate engineering or geological report. It is our intention to retain a North American educated geoscientist to evaluate and conform to American standards the phase I work program and to author a report to American standards for future capital raising. No agreements to retain such an engineer or geoscientist have been entered into as of the date of this registration statement. We had $913 in cash reserves as of February 28, 2013.

Phase II will not be carried out until late 2013 or Spring 2014 and will be contingent upon favourable results from phase I and specific recommendations of a professional geoscientist based on those results. Favourable results means that a geoscientist, engineer or other recognized professional states that there is a strong likelihood of value being added by completing the next phase of exploration, makes a written recommendation that we proceed to the next phase of exploration, a resolution is approved by the Board indicating such work should proceed and that it is feasible to finance the next phase of the exploration. Phase II will be directed towards additional trenching on selected areas and further diamond drilling and may require up to six weeks work; total costs will be approximately $100,000, with Tiger’s portion being $50,000, comprised of wages, fees, trenching, diamond drilling, assays and related. The cost estimate is based on local costs for the specified type of efforts planned. A further three to four months may be required for analysis, evaluation of the work accomplished and the preparation of a report.

ITEM 1A RISK FACTORS

Risks Associated with Tiger Jiujiang Mining, Inc., Our Financial Condition and Our Business Model

6

1. Because our auditors have issued a going concern opinion and because our officer and director has not indicated a willingness to loan any additional funds to us, it is likely we will not be able to achieve our objectives and will have to cease operations.

Our financial statements for the year ended February 28, 2013, were prepared assuming that we will continue our operations as a going concern. However, our auditors have issued a going concern opinion. This means that there is doubt that we can continue as an ongoing business for the next twelve months. We were incorporated on January 28, 2010, and do not have a history of earnings. As a result, our independent accountants in their audit report have expressed substantial doubt about our ability to continue as a going concern. Continued operations are dependent on our ability to complete equity or debt financings or generate profitable operations. Such financings may not be available or may not be available on reasonable terms. Our financial statements do not include any adjustments that may result from the outcome of this uncertainty. Junior exploration companies often fail to achieve or maintain successful operations, even in favorable market conditions.

2. We are an exploration stage corporation, lack a business history and have losses that we expect to continue into the future. If the losses continue we will have to suspend operations or cease functioning.

We were incorporated on January 28, 2010, and have not started our proposed business or realized any revenues. We have no business history upon which an evaluation of our future success or failure can be made. Our net loss since inception is $123,138. Our ability to achieve and maintain profitability and positive cash flow is dependent upon finding a profitable exploration property, generating revenues; and reducing exploration costs.

Based upon current plans, we expect to incur losses in future periods. This will happen because there are expenses associated with our exploration program. We may not be successful in generating revenues in the future. Failure to generate revenues will cause us to go out of business.

Potential investors should be aware of the difficulties normally encountered by a new enterprise and the high rate of failure of such enterprises. The potential for future success must be considered in light of the problems, expenses, difficulties complications and delays encountered in connection with the development of a business in the area in which we intend to operate and in connection with the formation and commencement of operations of a new business in general. These include, but are not limited to, competition and additional costs and expenses that may exceed current estimates. There is no history upon which to base any assumption as to the likelihood that we will prove successful, and there can be no assurance that we will generate significant operating revenues in the future or ever achieve profitable operations.

3. We have no known mineral reserves and we may not find any gold or if we find gold it may not be in economic quantities. If we fail to find any gold or if we are unable to find gold in economic quantities, we will have to cease operations.

We have no known mineral reserves. Even if we find gold it may not be of sufficient quantity so as to warrant recovery. Additionally, even if we find gold in sufficient quantity to warrant recovery it ultimately may not be recoverable. Finally, even if any gold is recoverable, we do not know that this can be done at a profit. Failure to locate gold deposits in economically recoverable quantities will ultimately cause us to cease operations.

4. We require substantial funds merely to determine if mineral reserves exist on our optioned property.

Any potential development of our exploration property depends upon the results of exploration programs and/or feasibility studies and the recommendations of duly qualified engineers and geologists. Such programs require substantial additional funds. Any decision to further expand our plans on these exploration properties will involve the consideration and evaluation of several significant factors including, but not limited to:

7

- costs of bringing the property into production including exploration work, preparation of production feasibility studies, and construction of production facilities;

- availability and costs of financing;

- ongoing costs of production;

- market prices for the products to be produced;

- environmental compliance regulations and restraints; and

- political climate and/or governmental regulation and control.

5. Good title to the Tiger property is registered in the name of another person. Failure of Tiger to obtain good title will result in Tiger having to cease operations.

Title to the property we intend to explore is not held in our name but rather that of Kiukiang Gold Mining Company (“Kiukiang”), a corporate resident of the People’s Republic of China. In the event Kiukiang were to grant another person a deed of ownership which was subsequently registered prior to our deed, the third party would obtain good title and we would have nothing. Similarly, if it were to grant an option to another party, that party would be able to enter the property, carry out certain work commitments and earn right and title to the property and we would have little recourse as we would be harmed, will not own any property and would have to cease operations. The option agreement does not specifically reference these risks or the recourse provided. Although we would have recourse against Kiukiang under the laws of Wyoming in the situations described, there is a question as to whether that recourse would have specific value.

6. Currently Tiger has no right to the Tiger gold property. In order to exercise its rights under the option agreement we must incur certain exploration costs and make royalty payments. Failure by Tiger to incur the exploration expenditures or to make the royalty payments will result in forfeiture of Tiger’s right to acquire a 50% interest in the property.

Under the terms of the option agreement and the attendant amendments, Tiger has the right to acquire a 50% interest in the right and title to the Tiger gold property upon incurring exploration expenses of a minimum of $15,000 by May 31, 2012 (paid and completed except for the final report), incurring additional exploration expenses in the amount of $45,000 by May 31, 2014, and making annual advance on royalty payments in the amount of $25,000 commencing May 31, 2016. Failure by Tiger to make any of the payments or to incur the required exploration expenses will result in the loss of the option to acquire an interest in the property. Should we lose the option Tiger would have to cease operations. If we were to fail, after the exercise of the option, to make the required $25,000 annual payment as prepayment of the net smelter royalty we would be in default of section 5.1(c) of the option agreement and would have to remedy the default. If we failed to remedy the default this would result in the loss of the interest in the property and would force us to cease operations.

7 Our common stock is classed as a “penny stock”. Trading of our stock may be restricted by the SEC's penny stock regulations which may limit a stockholder's ability to buy and sell our stock.

Rules 15g-1 through 15g-9 promulgated under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) impose sales practice and disclosure requirements on certain brokers-dealers who engage in transactions involving a “penny stock.” The SEC has adopted regulations which generally define “penny stock” to be any equity security that has a market price less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Our common stock is covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and “accredited investors”. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form prepared by the SEC which provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction and monthly account statements showing the market value of each penny stock held in the customer's account. The bid and offer quotations, and the broker-dealer and salesperson compensation information, must be given to the customer orally or in writing prior to effecting the transaction and must be given to the customer in writing before or with the customer's confirmation. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to these penny stock rules. Consequently, these penny stock rules may affect the ability of broker-dealers to trade our securities. We believe that the penny stock rules may discourage investor interest in and limit the marketability of our common stock.

8

In addition to the “penny stock” rules, the Financial Industry Regulatory Authority ( “FINRA”) has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer's financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low priced securities will not be suitable for at least some customers. FINRA’s requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock and have an adverse effect on the market for our shares.

8. We will be required to evaluate our internal controls under Section 404 of the Sarbanes-Oxley Act of 2002, and any adverse results from such evaluation could result in a loss of investor confidence in our financial reports and have an adverse effect on the price of our shares of common stock.

Under the requirements of the Sarbanes Oxley Act of 2002 and pursuant to Section 404 of that Act, we are required to undergo an annual and quarterly assessment which includes inventorying all controls, identifying the key controls using a top down approach and testing the key controls to ensure the controls are in place and working as designed. Following consultation with our independent accountant we have determined that the process is overly time consuming and costly to Tiger. As a result, we have not completed this process to date. With a limited staff, management can override any implemented program of controls and procedures which renders the control system ineffective. If our auditors need to be involved in numeric changes or material changes to footnotes then, by definition, the controls have failed and are ineffective. In addition, our auditors have recommended journal entries and adjustments following management’s preparation of the financial statements and notes thereto which indicates our controls to be ‘ineffective’. Other elements of an effective control system would include developing a code of conduct, which we have completed, and having independent board members – of which we have none. Thus, we state in our filing that our controls are determined to be “ineffective”.

If we are unable to assert that our internal control over financial reporting is effective as of February 28, 2011, (or if our auditors are unable to attest that our management’s report is fairly stated or they are unable to express an opinion on the effectiveness of our internal controls), we could lose investor confidence in the accuracy and completeness of our financial reports, which would have a material adverse effect on our stock price.

Failure to comply with the new rules may make it more difficult for us to obtain certain types of insurance, including director and officer liability insurance, and we may be forced to accept reduced policy limits and coverage and/or incur substantially higher costs to obtain the same or similar coverage. The impact of these events could also make it more difficult for us to attract and retain qualified persons to serve on our board of directors, on committees of our board, or as executive officers.

9. Upon completion of the phase I exploration program, each party to the option agreement will have the ability to decide as to whether they will carry on with phase II based on the recommendations of their own geological evaluation. If the phase I exploration program is successful and our geoscientists recommend that a phase II is recommended, should Kiukiang decide to not proceed to phase II and we elect to carry on, we will have to pay our share of the program as well as that of Kiukiang.

9

If the first phase of the planned two-phase exploration program is successful and a competent engineer and our independent evaluation both recommend proceeding with a phase II program it is possible that Kiukiang may elect to not proceed to phase II. In that event, Tiger would either have to totally fund phase II (estimated at $100,000) or find a joint venture partner to pay a portion of the costs. If we are not successful in raising the required funding or finding a partner, we could be forced to abandon the project and cease operations.

10. We may, in the future, issue additional common shares which would reduce investors' percentage of ownership and may dilute the value of our shares.

Our Articles of Incorporation authorize the issuance of 400,000,000 shares of common stock. As of the date of this report we have 8,500,000 shares of common stock outstanding. Accordingly, we may issue up to an additional 391,500,000 shares of common stock. The future issuance of common stock may result in substantial dilution in the percentage of our common stock held by our then existing shareholders. We may value any common stock issued in the future on an arbitrary basis. The issuance of common stock for future services or acquisitions or other corporate actions may have the effect of diluting the value of the shares held by our investors, and might have an adverse effect on any trading market for our common stock. Tiger has agreed that it shall issue 1,000,000 shares to Kiukiang upon completion of a phase I exploration program as recommended by a competent geologist with the proviso that the report recommends further work be carried out on the Tiger property; i.e. if the engineering reports recommends that a phase II exploration program be carried out, Tiger is obligated to issue 1,000,000 shares to Kiukiang which will further dilute the investor’s percentage of ownership.

Risks Associated With Doing Business in China

Various matters that are specific to doing business in China may create additional risks or increase the degree of such risks associated with our business activities. These risks are discussed below.

1. The Chinese legal system is different from the U.S. justice system. Most of the material agreements to which we or our affiliates are party or will be party in the future with respect to mining assets in the PRC are expected to be governed by Chinese law and some may be with Chinese governmental entities. The Chinese legal system embodies uncertainties that could limit the legal protection available to Tiger and its shareholders. The outcome of any litigation may be more uncertain than usual because: (i) the experience of the Chinese judiciary is relatively limited, and (ii) the interpretation of China’s laws may be subject to policy changes reflecting domestic political changes.

(a) Legal System - The Chinese use a civil law system based on written statutes. Unlike common law systems (the system in the U.S.), it is a system in which decisions in earlier legal cases do not generally have precedential value. The overall effect of legislation enacted over the past 20 years has been to enhance the protections afforded to foreign, such as Tiger, invested enterprises in China. However, these laws, regulations and legal requirements remain relatively recent and are evolving rapidly; their interpretation and enforcement involve uncertainties. These uncertainties could limit the legal protections available to foreign investors such as the right of foreign invested enterprises to hold licenses and permits such as business licenses. Because our business activities are located outside the U.S., it could be difficult for investors to effect service of process in the U.S., or to enforce a judgment obtained in the U.S. against us or any of these persons or entities.

(b) Limited Interpretation - The laws that do exist are relatively recent and their interpretation and enforcement involve uncertainties, which could limit the available legal protections. Even where adequate Chinese law exists it may be impossible to obtain swift and equitable enforcement of such law or to obtain enforcement of judgments by a court of another jurisdiction. The inability to enforce or obtain a remedy under such agreements would have a material adverse impact on our operations.

The Chinese government has enacted some laws and regulations dealing with matters such as corporate organization and governance, foreign, such as Tiger, investment, taxation and trade. However, their experience in implementing, interpreting and enforcing these laws and regulations is limited, and our ability to enforce commercial property rights or to resolve commercial disputes is unpredictable. If our new business venture is unsuccessful, or other adverse circumstances arise from these transactions, we face the risk that the parties to these ventures may seek ways to terminate the transactions, or, may hinder or prevent us from accessing important information regarding the financial and business operations of these companies. The resolution of these matters may be subject to the exercise of considerable discretion by agencies of the Chinese government and forces unrelated to the legal merits of a particular matter or dispute may influence their determination. Any rights we may have to specific performance or to seek an injunction, in either of these cases, may be severely limited and without a means of recourse by virtue of the Chinese legal system, we may be unable to prevent these situations from occurring. The occurrence of any such events could have a material adverse effect on our business, financial condition and results of operations.

10

(c) Corporate Organization – When we commence mining operations, which means we would have successfully proven reserves in such quality and sufficient quantity to ensure for a profitable mining operation, we would form a joint venture with Kiukiang which may involve either the formation of a Sino-foreign or domestic Sino corporate entity. Continuing efforts are being made to improve civil, administrative, criminal and commercial law in China especially since its accession into the WTO. This includes the development of laws governing foreign investment in China, including a regime for Sino-foreign cooperative joint ventures and increased foreign participation in mineral resource exploration and mining. Conversely, the laws were recently changed such that there is no taxation benefit to having a wholly foreign owned enterprise which further demonstrates the ongoing evolution of the Chinese economic model and system. The interpretation and enforcement of the laws of the PRC involve uncertainties which could limit the legal protections available to foreign investors, such as the right of foreign invested enterprises to hold licenses and permits such as requisite business licenses. In addition, substantially all the assets of Sino corporations are located outside the U.S; as a result, there remains much uncertainty as to the future evolution of the laws in China and, therefore, it could be difficult for investors to effect service of process in the U.S., or to enforce a judgment obtained in the U.S. against any of these persons or corporations.

(d) General – Until we formally enter into a joint venture with Kiukiang and have proven reserves on the Tiger Property all of our success in China will, in part, be based on the actions of Kiukiang. The risk to investors is that Kiukiang mishandles critical phases of the exploration and/or development of the property into the future resulting in losses or damages to Tiger. In addition, investors in Tiger risk that the existing laws of China will change over time as the country becomes more capitalist oriented and that some of those changes will have a deleterious effect on Tiger and its operations in China. What happens to investment in China is a question that can only be answered with time. At some point in the future Tiger may have to rethink and reorganize our investment plans and projects to minimize the tax costs. However, it must also be recognized that tax rates in China remain attractive in comparison to many competing nations.

2. The Chinese Enterprise Income Tax Law may have a material impact on our operations effectively causing a form of ‘double taxation’ if we enter into a future formalized joint venture with Kiukiang.

We have no reason to believe at the current time and given the status of the Corporation and its sole asset that the Enterprise Income Tax Law that was effective on January 1, 2008, will have any material effect on Tiger in the foreseeable future – at least not until a formal joint venture is entered into and we have established reserves that would indicate we have a potentially viable mining operation which is a number of years in the future. The Enterprise Income Tax Law pertains, for our current purposes, to wholly foreign owned entities, such as Tiger, and to the fact that under the law, there is no longer preferential tax treatment given to foreign investors. The concern for our investors is that the enterprise tax will become consolidated all the way back to the holding company which may mean a form of double taxation. Tiger is a foreign corporation and has no physical operations in China. Kiukiang is the only party under the option agreement directly facing China and its laws at the current time. However, when we commence mining operations and formalize a joint venture with a Chinese corporation, we will have to consider the issues at that time but since that is a number of years in the future and the Law will continue to evolve we cannot predict what the effect will be at that time. We will review the issue as we get closer to that event and will update the relevant disclosure in our future 10Q and 10K filings.

11

Where we refer to “foreign” as it pertains to Tiger being a foreign corporation we have indicated “such as Tiger” and where we otherwise refer to “foreign” we refer to a potential joint venture between Tiger and Kiukiang. Foreign generally means an enterprise or individual that is not legally bound to the PRC. Repatriation refers solely to the situation of the removal of Tiger’s funds invested in China to Tiger’s accounts in the United States.

3. Our sole officer and director, Ms. Chang Ya-Ping, is a resident and citizen of Taiwan which embodies uncertainties that could limit the legal protection available to Tiger’s shareholders.

Because Ms. Chang is a citizen and resident of Taiwan, in the event that U.S. investors sought service of process against Ms. Chang, it may be difficult for investors to effect service of process in the U.S., or to enforce a judgment obtained in the U.S. against Ms. Chang. Further, it would be difficult to enforce judgements against her which were obtained in U.S. courts based on the civil liability provisions of U.S. federal securities laws and enforcing judgements of U.S. courts based on civil liability provisions of U.S. federal securities laws in foreign courts against Ms. Chang would likewise be difficult as would the bringing of an original action in foreign courts to enforce liabilities based on those U.S. federal securities laws.

4. There are many risks to doing business in China that may affect our future business operations that would not apply or are at variance with operating in the United States. There are regulations that apply to foreign ownership, such as Tiger, to mergers and acquisitions by foreign investors and others that would affect currency conversion and on dividends. Each may or may not impact, to some degree, our operations should we form a Chinese joint venture and continue to explore and develop our optioned mineral property. Any of these risks could cause us to be able to continue with the development of the project and may force us to suspend or cease operations.

We may find that the future rulings in regards to foreign ownership of companies involved in our business may make it more restrictive than that which we see at the present time and may force us to cease operations in China should we either form a joint venture or seek a merger with another company to continue exploration on our optioned property. We may find it difficult to form a joint venture that would be satisfactory to the Chinese government in order to be able to carry out our long tern exploration and development goals. If we were not able to arrange for a joint venture that would be acceptable to the PRC we may not be able to recoup our investment in full or may have to terminate our operations and write off whatever investment we had made to that point. That may result in our having to cease operations or go out of business.

We may not be successful in our efforts to form a joint venture as a result of non-approval by regulatory authorities and may have to suspend or cease operations because all joint ventures to be entered into must be pre-approved by both the Ministry of Commerce (“MOC”) and the State Development and Reform Commission (“SDRC”) in Beijing or their provincial bureaus. The risk that we face is that for reasons that may not be known at this time or because of changes in the regulatory regime, we may not be able to enter into a formal joint venture in which case we would either have to seek a buyer for the project or simply abandon all our previous efforts and cease operation.

In the event that we were to be successful in developing a mining property with reserves and commenced full mining operations, we may not be able to repatriate our full investment in the project which may lessen dividends available to be paid to Tiger’s shareholders. Foreign currency exchange regulation in China is primarily governed by the Foreign Currency Administration Rules (1996), as amended, (the “Exchange Rules”) and Administration Rules of the Settlement, Sale and Payment of Foreign Exchange (1996), (the “Administration Rules”). Under the Exchange Rules, the Renminbi is convertible for current account items, including the distribution of dividends, interest payments, trade and service-related foreign exchange transactions. Conversion of Renminbi for capital account items, such as direct investment, loan, security investment and repatriation of investment, however, is still subject to the approval of the State Administration of Foreign Exchange (“SAFE”). Under the Administration Rules, companies in China with foreign investments may only buy, sell and/or remit foreign currencies at those banks authorized to conduct foreign exchange business after providing valid commercial documents and, in the case of capital account item transactions, obtaining approval from the SAFE. foreign

12

The State Administration of Foreign Exchange (the “SAFE”) promulgated Circular on Issues Relating to Foreign Exchange Administration of Equity Financings and Return Investments by Domestic Residents through Offshore Special Purpose Vehicles (“Circular 75” or the “Circular”) on October 21, 2005, which legalizes, and further regulates, the offshore holding company structure favored by private enterprises in their offshore fundraising activities with a view toward channeling foreign venture capital and private equity investments back into China’s private sector and took effect on November 1, 2005. The rules promulgated under this Circular may impact on our ability to form a Chinese joint venture in the future as well as our ability to invest in a Chinese project to the degree that we may require and may preclude us from the benefits of a joint venture. There appears yet to be a great deal of uncertainty as to how Circular 75 will be managed in the longer term. Since we are at least two to five years away from having to form a joint venture and having to deal with the ramifications of SAFE and Circular 75 we do not believe we are yet in a position to determine what we will do in the future; we will, however, have to be mindful of the implications of Circular 75 and monitor the changes that occur in the future.

The rules pertaining to acquisitions and mergers by foreign investors, such as Tiger, may impact our ability to operate long term in the PRC if we are successful in developing a mining project beyond the exploration stage and wish to merge with or be acquired by another entity because recently changed rules in China now require that both foreign investors and Chinese companies incorporated overseas must obtain approval for merger and acquisition activity from the Ministry of Commerce and we may not be able to obtain those approvals in the future which may jeopardize our long tern development plans.

ITEM 1B. UNRESOLVED STAFF COMMENTS

As of the date of this report, there are no unresolved comments pending from the SEC.

ITEM 2 PROPERTIES

Our business office is located at 6F, No.81 Meishu East 6 Road, Kaohsiung, Taiwan 804. Our telephone number is (360) 353-4013. Our principal office is provided by our officer and director at no cost. We believe that the condition of our principal office is satisfactory, suitable and adequate for current needs.

On February 22, 2010, as amended on May 2, 2012, and May 20, 2013, we entered into an option agreement to finance a two-phase exploration program whereby we can earn a 50 percent or greater interest on a gold exploration and mining property known as the Tiger mining property located in northern Jiujiang Province, China. The Option To Purchase And Royalty Agreement is with Kiukiang Gold Mining Company of Jiujiang City, Jiujiang, China, the beneficial owner, an arms-length Chinese corporation whereby we can acquire an interest by making certain expenditures and carrying out certain exploration work. The property is in good standing until December 8, 2015.

Under the terms of the agreement and the amendment, Kiukiang granted to Tiger the right to acquire 50% of the right, title and interest of Kiukiang in the property, subject to its receiving annual payments and a royalty, in accordance with the terms of the agreement, as follows:

| (a) |

Tiger contributing exploration expenditures on the property of a minimum of $15,000 on or before May 31, 2012 (paid in full and currently awaiting the final report on the work performed); | |

| (b) |

Tiger contributing exploration expenditures of a further US $45,000 for aggregate minimum contributed exploration expenses of $60,000 on or before May 31, 2014; | |

| (c) |

Tiger shall allot and issue 1,000,000 shares in the capital of Tiger to Kiukiang upon completion of a phase I exploration program as recommended by a competent geologist with the proviso that the report recommends further work be carried out on the Tiger property; | |

| (d) |

Tiger will pay to Kiukiang an annual royalty equal to three percent (3%) of Net Smelter Returns; | |

| (e) |

Upon exercise of the option, Tiger will pay to Kiukiang $25,000 per annum commencing on May 31, 2016, as prepayment of the NSR; and |

13

| (f) |

Tiger has the right to acquire an additional 25% of the right, title and interest in and to the property by the payment of $10,000 and by incurring an additional $50,000 in exploration expenditures on or before May 31, 2015. |

Further, the Agreement and the Option will terminate:

| (a) |

on May 31, 2014 at 11:59 P.M., unless on or before that date, Tiger Jiujiang has incurred exploration expenditures of a cumulative minimum of US $60,000 on the Property; | |

| (b) |

at 11:59 P.M. on May 31 of each and every year, commencing on May 31, 2016, unless Tiger Jiujiang has paid to Kiukiang the sum of US $25,000 on or before that date. |

If the results of phase I are unfavourable, we will terminate the option agreement and will not be obligated to make any subsequent payments. Similarly, if the results of phase II are unfavourable, we will terminate the option and will not be obligated to make any subsequent payments.

To date we have not performed any work on the Tiger property nor have we spent any money on research and development activities.

The property is unencumbered and there are no competitive conditions which affect it. Further, there is no insurance covering the property. We believe that no insurance is necessary since it is unimproved and contains no buildings or improvements.

Our Proposed Exploration Program – Plan of Operation

Our business plan is to proceed with initial exploration of the Tiger property to determine if there are commercially exploitable deposits of gold. We planned a two-phase exploration program to properly evaluate the potential of the property and completed the physical work of the first phase and are awaiting the final engineering report on that work. We must conduct exploration to determine if gold exists and if any is found it can be economically extracted and profitably processed. We do not claim to have any ores or reserves whatsoever at this time.

Our portion of the phase I planned geological exploration program cost $20,000 (which is 50% of the totally budgeted cost of $40,000) and is a reflection of local costs for the specified type of work. Phase I required six weeks for the base work and an additional six months for analysis, evaluation of the work completed and the preparation of a report. Costs for phase I were made up of wages, fees, geological and geochemical supplies, assaying, equipment, diamond drilling and operation costs. We will assess the results of this program upon receipt of an appropriate engineering or geological report which is currently expected to be in our hands in July, 2013. It is our intention to retain a North American educated geoscientist to evaluate and conform to American standards the phase I work program and to author a report to American standards for future capital raising. No agreements to retain such an engineer or geoscientist have been entered into as of the date of this report. We had $913 in cash reserves as of February 28, 2013. Accordingly, we will not be able to proceed with the first phase of the exploration program without additional financing.

Phase II will not be carried out until late 2013 or the spring of 2014 and will be contingent upon favourable results from phase I and specific recommendations of a professional geoscientist based on those results. Favourable results means that a geoscientist, engineer or other recognized professional states that there is a strong likelihood of value being added by completing the next phase of exploration, makes a written recommendation that we proceed to the next phase of exploration, a resolution is approved by the Board indicating such work should proceed and that it is feasible to finance the next phase of the exploration. Phase II will be directed towards additional trenching on selected areas and further diamond drilling and may require up to six weeks work; total costs will be approximately $100,000, with Tiger’s portion being $50,000, comprised of wages, fees, trenching, diamond drilling, assays and related. The cost estimate is based on local costs for the specified type of efforts planned. A further three to four months may be required for analysis, evaluation of the work accomplished and the preparation of a report.

14

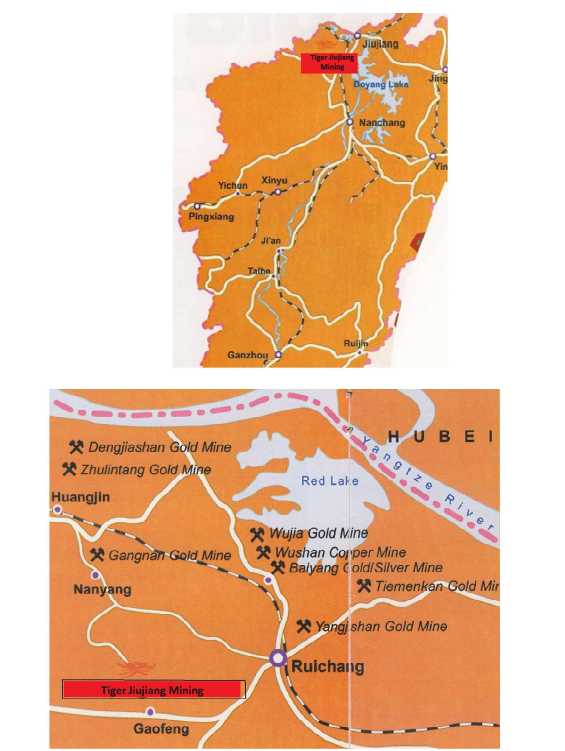

The following Property Location Maps indicates approximately where the claim blocks are located west of Jiujiang City in north-western Jiangxi.

Figure 1 – Map of location of Jiangxi Province in China

15

Figure 2 – Tiger Mining Property – General Location

Physiography, Location and Access

The Tiger property is located 20 km west of Ruichang City which is approximately 400 km west of Shanghai and is governed under the Ruichang Township of Jiujiang Province and is accessed by local roads.

16

Regional Geology

The exploration area is located at the southeast edge of the Yangtze and Jiangnan platforms in the northwestern slopes of the deep fracture belts in the northwest of Jiangxi Province. The exposure of the stratums in this area is mainly in the form of metamorphic rocks which were laid down in the times of Proterozoic or Later Proterozoic Eras of the Shuangqiao Mountain Group and the Climbing Mountain Group. The geological structure is well developed and magmatic actives are frequent which has provided good formative conditions for gold ore depositions. These are all indicators of the possible presence of gold in the area. Three sites of potential interest have been located and received minor exploration work consisting of pitting, geology, sampling and a magnetic survey. These sites will become the focus of exploration during phase I.

In 2009, in order to further explore and define the prospect, Kiukiang engaged the Jiangxi Geological and Engineering Company, a locally based geological and engineering group to develop the property area and to expand the exploration to other sections outside the previously worked explored areas which had recently been acquired by Kiukiang.

Previous Work

No previous work has been performed on the property by Tiger.

Our Proposed Exploration Program – Plan of Operation

Our business plan is to proceed with the initial exploration of the Tiger property to determine if there are commercially exploitable deposits of gold and silver. Poon Man Sin, Senior Engineer authored the Report in which his firm recommends a two-phase exploration program to properly evaluate the potential of the property. We must conduct exploration to determine if gold exists and if any gold which is found can be economically extracted and profitably processed.

We do not claim to have any ores or reserves whatsoever at this time on our optioned property.

Or portion of phase I of the recommended geological exploration program cost $20,000 of a total $40,000 planned expenditure with the balance being funded by Kiukiang based on the Report which is a reflection of local costs for the specified type of operation. We had $913 in cash reserves as of February 28, 2013. Accordingly, we will not be able to proceed with the next phase of the exploration program without additional financing.

We retained the services of the Jiangxi Geological and Engineering Company and Mr. Poon prior to commencement of work to complete the first phase of the work program. We will assess the results of this program upon receipt of the report. The parties to the option agreement agreed that Tiger would control the exploration work and that Kiukiang would contract for and carry out the physical work under the supervision of Tiger. They are located in the area and have ready access to labor and equipment and are familiar with local conditions.

Initially, we ran a grid over a portion of the property and reviewed maps of the results of past geological and geochemical programs correlating all past information to our grid, then completed a geological survey to evaluate certain specific targets previously identified.

The laying out of a grid and line cutting involved the physical cutting of any underbrush and overlay to establish an actual grid on the ground whereby items can be related one to another more easily and with greater accuracy. When we map, we essentially generate a drawing of the physical features of the land as well as a depiction of what may have been found in relation to the property boundaries. So we will actually draw a scale map of the area and make notes on it as to the location where anything was found that was of interest or not.

17

Geophysical surveying involves the measurement of various physical properties of the rocks at the site as well as interpreting that information in terms of the structure and nature of the rock. The geoscientist takes different measurements of the various physical and geological properties of the rocks and interprets the results in terms of what we seek. These methods include magnetic, electrical and seismic measurements. He then interprets all the data obtained, plots it on the map he has generated and provides his best estimate of the chances of finding gold and what additional efforts we must undertake in a follow-up phase.

Previously run magnetometer and VLF-EM (very low frequency electromagnetic surveys) will be used as an aid to mapping and structural interpretation and may assist in locating gold and the delineation of the various physical properties of the rock which can be used as pointers towards whether gold may be present or not. Anomalies will be evaluated closely to help in determining their economic potential.

Phase 1 began by establishing a base line grid with 25-meter stations and cross lines run every 50 meters for 100 meters each side of the baseline. We then related previous ground and airborne electromagnetic surveys over the grid. Samples taken from various locations have been tested for traces of gold, silver, lead, copper, zinc, iron and other metals; however, our primary focus is the search for gold. We then compare relative concentrations of gold, silver, lead and other indicator metals in samples so the results from different samples can be compared in a more precise manner and plotted on a map to evaluate their significance.

Phase II will not be carried out until late 2013 or the Spring of 2014 and will be contingent upon favourable results from phase I and any specific recommendations of the report. Specifics of the work to be carried out have not yet been determined and will be delineated as recommendations in the reporting of the results of phase I but initial estimates are that the second phase may require up to six weeks work and will cost approximately $100,000 in total (Tiger’s portion being $50,000) comprised of wages, fees, camp, equipment rental, trenching, diamond drilling, assays and related. A further three to four months may be required for analysis and the preparation of a report and evaluation on the work accomplished.

There is no power available on the property or within a reasonable distance. All contract work will involve bringing to the site portable power generation units.

We do not expect any changes or hiring of employees since contracts are given to consultants and subcontractor specialists in specific fields of expertise for the exploration work. We do not expect to purchase or sell any plant or significant equipment. We intend to lease or rent any equipment, such as a backhoe, diamond drill, generators and so on, that we will need in order to carry out our exploration activities.

Over the next year we intend to review the results of the first phase of the exploration plan on our optioned property which was obtained through an option agreement with Kiukiang Gold Mining Company, the beneficial owner and then to determine if it is our best interests to proceed with longer term exploration. If that is the case and we determine we will carry on with phase II, we will need to raise sufficient additional capital for the work plus sufficient for our administrative operations and working capital through the sale of Tiger’s equity shares in the form of a private placement or public offering, loans or advances from officers or directors or others or convertible debentures.

Our plan of operation for the period through February 28, 2014, is:

March to June, 2013 – Tiger will maintain its business and will remain compliant with regulatory requirements.

July to October, 2013 – We and Kiukiang will review the engineering results of the phase I portion of our planned exploration program and will engage a North American educated geoscientist to evaluate and conform to American standards the phase I work program and to make his own recommendations independent of the Kiukiang report. We will then be in a position to determine what the next step will be in the development of our business plan. If the report is favourable and advises that we proceed to phase II of the exploration program, we will then have to determine how we can raise the funds required for the second phase which are estimated at $50,000 ($100,000 being the total budget and currently planned cost of phase II). If the report advises abandoning the property as having little or no value, we will terminate the option.

18

October, 2013, to February 28, 2014 – assuming the report recommends carrying forward with phase II, we will work to obtain the funding needed. In the event the report were to recommend against further work, we would use this period to investigate other mining opportunities that may be presented or made available to us.

Environmental Laws

In the past ten years, laws and policies for environmental protection in China have moved towards stricter compliance and stronger enforcement. The basic laws in China governing environmental protection in the mineral industry sector of the economy are the Environmental Protection Law, the Environment Impact Assessment Law and the Mineral Resources Law. The State Administration of Environmental Protection and its provincial counterparts are responsible for the supervision implementation and enforcement of environment protection laws and regulations. Provincial governments also have the power to issue implementing rules and policies in relation to environmental protection in their respective jurisdictions. Applicants for exploration rights must submit environmental impact “assessments” and those projects that fail to meet environmental protection standards will not be granted licenses.

In addition, after exploration the licensee must perform water and soil maintenance and take steps towards environmental protection. After the exploration rights have expired or the concessionaire stops mining during the permit period and the mineral resources have not been fully developed, the concessionaire must perform water and soil maintenance, land recovery and environmental protection in compliance with the original development scheme, or must pay the costs of land recovery and environmental protection. After closing, the mining enterprises shall perform water and soil maintenance, land recovery and environmental protection in compliance with mine closure approval reports, or must pay the costs of land recovery and environmental protection.

Penalties for breaching the Environmental Protection Law include a warning, payment of a penalty calculated on the damage incurred, or payment of a fine. When an entity fails to adopt preventative measures or control facilities that meet the requirements of the enacted environmental protection standards, it is subject to suspension of production or operations and for payment of a fine. Material violations of environmental laws and regulations causing property damage or casualties may result in criminal liabilities.

ITEM 3. LEGAL PROCEEDINGS

We know of no material, existing or pending legal proceedings against us, nor are we involved as a plaintiff in any material proceeding or pending litigation. There are no proceedings in which any of our directors, officers or affiliates, or any registered or beneficial shareholder, is an adverse party or has a material interest adverse to Tiger.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

Our last annual general meeting was held on August 24, 2012, at which time stockholders approved the following actions:

- received and approved the financial statements of the Corporation for its financial year ended February 29, 2012, together with the report of the independent auditors thereon;

- fixed the number of directors at one for the coming year;

- elected Chang Ya-Ping to serve as a director until the next annual general meeting of shareholders or until her successor(s) is/are elected or appointed;

- ratified the appointment of Gruber & Associates, L.L.C., as independent auditors of the Corporation for the financial year ended February 28, 2013.

19

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS and ISSUER PURCHASES OF EQUITY SECURITIES

The shares of our common stock became available for quotation on the Over-the-Counter Bulletin Board (OTC-BB) under the symbol “TIGY” on October 10, 2012. The market for our common shares is limited and can be volatile. The following table sets forth the high and low bid prices of our common stock on a quarterly basis for the periods indicated as quoted on the OTC-BB. These quotations reflect inter-dealer prices without retail mark-up, mark-down or commissions and may not reflect actual transactions.

| Quarter Ended | High Bid | Low Bid |

| November 30, 2012 | $0.05 | $0.05 |

| February 28, 2013 | $0.05 | $0.05 |

As of the date of this report, the shareholders’ list of our common shares showed 41 registered shareholders holding 8,500,000 shares with no shares being held by broker-dealers. There are 8,500,000 shares issued and outstanding.

Our common shares are issued in registered form through our stock transfer agent VStock Transfer, LLC. of 77 Spruce St., Ste 201, Cedarhurst, NY 11516. They can be contacted by telephone at 1-855-987-8625.

We have not declared any dividends since incorporation and do not anticipate that we will do so in the foreseeable future. Although there are no restrictions that limit the ability to pay dividends on our common shares, our intention is to retain future earnings for use in our operations and the expansion of our business.

ITEM 6. SELECTED FINANCIAL DATA

As a “smaller reporting company”, we are not required to provide the information required by this Item.

ITEM 7. MANAGEMENT’S DISCUSSION and ANALYSIS OF FINANCIAL CONDITION and RESULTS OF OPERATIONS

The following discussion should be read in conjunction with our audited financial statements and the related notes that appear elsewhere in this Annual Report. The following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward looking statements. Factors that could cause or contribute to such differences include, but are not limited to those discussed below and elsewhere in this Annual Report, particularly in the section entitled “Risk Factors”.

We are an exploration stage company and have not generated any revenue to date. We have incurred recurring losses to date. Our financial statements have been prepared assuming that we will continue as a going concern and, accordingly, do not include adjustments relating to the recoverability and realization of assets and classification of liabilities that might be necessary should we be unable to continue in operation.

We were incorporated in the State of Wyoming on January 20, 2010, as Tiger Jiujiang Mining, Inc. and established a fiscal year end of February 28. Our statutory registered agent's office is located at 1620 Central Avenue, Suite 202, Cheyenne, Wyoming 82001 and our business office is located at 6F, No.81 Meishu East 6 Road, Kaohsiung, Taiwan 804. Our telephone number is (888) 755-9766. We are a start-up, exploration stage company engaged in the search for gold and related minerals. There is no assurance that a commercially viable mineral deposit, a reserve, exists in our claim or can be shown to exist until sufficient and appropriate exploration is done and a comprehensive evaluation of such work concludes economic and legal feasibility.

Tiger Mining Property - Physiography, Location and Access

We refer the reader to pages 14 and 15 of this report for maps as to the relative location of Tiger’s mining property. The Tiger property is located 20 km west of Ruichang City which is approximately 400 km west of Shanghai and is governed under the Ruichang Township of Jiujiang Province.

20

Our Proposed Exploration Program – Plan of Operation – Results of Operations

Our business plan is to proceed with the initial exploration of the Tiger property to determine if there are commercially exploitable deposits of gold and silver. Poon Man Sin, Senior Engineer authored the Report in which his firm recommends a two-phase exploration program to properly evaluate the potential of the property. We must conduct exploration to determine if gold exists and if any gold which is found can be economically extracted and profitably processed.

We do not claim to have any ores or reserves whatsoever at this time on our optioned property.

Or portion of phase I of the recommended geological exploration program cost $20,000 of a total $40,000 planned expenditure with the balance being funded by Kiukiang based on the Report which is a reflection of local costs for the specified type of operation. We had $913 in cash reserves as of February 28, 2013. Accordingly, we will not be able to proceed with the next phase of the exploration program without additional financing.

We retained the services of the Jiangxi Geological and Engineering Company and Mr. Poon prior to commencement of work to complete the first phase of the work program. We will assess the results of this program upon receipt of the report. The parties to the option agreement agreed that Tiger would control the exploration work and that Kiukiang would contract for and carry out the physical work under the supervision of Tiger. They are located in the area and have ready access to labor and equipment and are familiar with local conditions.

Initially, we ran a grid over a portion of the property and reviewed maps of the results of past geological and geochemical programs correlating all past information to our grid, then completed a geological survey to evaluate certain specific targets previously identified. The laying out of a grid and line cutting involved the physical cutting of any underbrush and overlay to establish an actual grid on the ground whereby items can be related one to another more easily and with greater accuracy. When we map, we essentially generate a drawing of the physical features of the land as well as a depiction of what may have been found in relation to the property boundaries. So we will actually draw a scale map of the area and make notes on it as to the location where anything was found that was of interest or not.

Geophysical surveying involves the measurement of various physical properties of the rocks at the site as well as interpreting that information in terms of the structure and nature of the rock. The geoscientist takes different measurements of the various physical and geological properties of the rocks and interprets the results in terms of what we seek. These methods include magnetic, electrical and seismic measurements. He then interprets all the data obtained, plots it on the map he has generated and provides his best estimate of the chances of finding gold and what additional efforts we must undertake in a follow-up phase.

Previously run magnetometer and VLF-EM (very low frequency electromagnetic surveys) will be used as an aid to mapping and structural interpretation and may assist in locating gold and the delineation of the various physical properties of the rock which can be used as pointers towards whether gold may be present or not. Anomalies will be evaluated closely to help in determining their economic potential.

Phase 1 began by establishing a base line grid with 25-meter stations and cross lines run every 50 meters for 100 meters each side of the baseline. We then related previous ground and airborne electromagnetic surveys over the grid. Samples taken from various locations have been tested for traces of gold, silver, lead, copper, zinc, iron and other metals; however, our primary focus is the search for gold. We then compare relative concentrations of gold, silver, lead and other indicator metals in samples so the results from different samples can be compared in a more precise manner and plotted on a map to evaluate their significance.

21

Phase II will not be carried out until late 2013 or the Spring of 2014 and will be contingent upon favourable results from phase I and any specific recommendations of the report. Specifics of the work to be carried out have not yet been determined and will be delineated as recommendations in the reporting of the results of phase I but initial estimates are that the second phase may require up to six weeks work and will cost approximately $100,000 in total (Tiger’s portion being $50,000) comprised of wages, fees, camp, equipment rental, trenching, diamond drilling, assays and related. A further three to four months may be required for analysis and the preparation of a report and evaluation on the work accomplished.

Over the next year we intend to review the results of the first phase of the exploration plan on our optioned property which was obtained through an option agreement with Kiukiang Gold Mining Company, the beneficial owner and then to determine if it is our best interests to proceed with longer term exploration. If that is the case and we determine we will carry on with phase II, we will need to raise sufficient additional capital for the work plus sufficient for our administrative operations and working capital through the sale of Tiger’s equity shares in the form of a private placement or public offering, loans or advances from officers or directors or others or convertible debentures.

Our plan of operation for the period through February 28, 2014, is:

March to June, 2013 – Tiger will maintain its business and will remain compliant with regulatory requirements.