Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Discovery Energy Corp. | Financial_Report.xls |

| EX-21.1 - EXHIBIT 21.1 - Discovery Energy Corp. | v346218_ex21-1.htm |

| EX-32.01 - EXHIBIT 32.01 - Discovery Energy Corp. | v346218_ex32-01.htm |

| EX-31.01 - EXHIBIT 31.01 - Discovery Energy Corp. | v346218_ex31-01.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(MARK ONE)

| x | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 28, 2013

| ¨ | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-53520

discovery energy Corp.

f/k/a “Santos Resource Corp.”

(Exact name of registrant as specified in its charter)

| Nevada | 98-0507846 | |

| (State or other jurisdiction

of incorporation or organization) |

(I.R.S. Employer Identification

No.) |

| One Riverway Drive, Suite 1700, Houston, Texas | 77056 | |

| (Address of principal executive offices) | (Zip Code) |

Issuer’s telephone number: (713) 840-6495

Securities registered under Section 12(b) of the Exchange Act: None

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, par value $.001 per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes S No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

| (Do not check if smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes ¨ No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $3,267,700.

State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date: 138,295,500 as of May 17, 2013.

DOCUMENTS INCORPORATED BY REFERENCE

None.

DISCOVERY ENERGY CORP.

FORM 10-K

FOR THE FISCAL YEAR ENDED FEBRUARY 28, 2013

TABLE OF CONTENTS

| PART I | ||

| Item 1. | Business | 1 |

| Item 1A. | Risk Factors | 13 |

| Item 1B. | Unresolved Staff Comments | 19 |

| Item 2. | Properties | 19 |

| Item 3. | Legal Proceedings | 19 |

| Item 4. | Mine Safety Disclosures | 19 |

| PART II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 20 |

| Item 6. | Selected Financial Data | 24 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 24 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 30 |

| Item 8. | Financial Statements and Supplementary Data | 30 |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 30 |

| Item 9A. | Controls and Procedures | 31 |

| Item 9B. | Other Information | 32 |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 33 |

| Item 11. | Executive Compensation | 36 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 37 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 37 |

| Item 14. | Principal Accounting Fees and Services | 38 |

| PART IV | ||

| Item 15. | Exhibits, Financial Statement Schedules | 39 |

CAUTIONARY STATEMENT FOR FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We have based these forward-looking statements on our current expectations and projections about future events. These forward-looking statements are subject to known and unknown risks, uncertainties and assumptions about us that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as "may," "will," "should," "could," "would," "expect," "plan," "anticipate," "believe," "estimate," "continue," or the negative of such terms or other similar expressions. Factors that might cause or contribute to such a discrepancy include, but are not limited to, those described in this Annual Report on Form 10-K and in our other Securities and Exchange Commission filings.

PART I

Item 1. Business.

General

Our company, Discovery Energy Corp., f/k/a "Santos Resource Corp.," was incorporated under the laws of the state of Nevada on May 24, 2006. Our current business plan is to explore for and produce oil and gas from a tract of land (the "Prospect") covered by Petroleum Exploration License (PEL) 512 (the "License") in the State of South Australia. We adopted this business plan near the end of our fiscal 2012, after having previously abandoned our initial business plan involving mining claims in Quebec, Canada and after we had been dormant from a business perspective for a period of time. In connection with the adoption of our current business plan, we had a change in control of our company, a change in our management, a change in our corporate name, and a change of our status from a “shell” company, as that term is defined in Rule 405 of the Securities Act of 1933 and Rule 12b-2 under the Securities Exchange Act of 1934.

During our fiscal 2013, we made significant strides in our new business plan, as the License was formally granted to us after the satisfaction of a number of significant preconditions to the grant. To further our new business plan, we are currently involved in efforts to complete a major capital raising transaction or to procure a major joint venture partner. The achievement of either of these goals (or some combination of the two) would likely enable us to start the development of the Prospect in a meaningful way. We have no assurance that we will be successful in achieving either of the preceding goals.

In the remainder of this Report, Australian dollar amounts are prefaced by "AU$" while United States dollar amounts are prefaced simply by "$" or (when used in close proximity to Australian dollar amounts) by "US$." When United States dollar amounts are given as equivalents of Australian dollar amounts, such United States dollar amounts are approximations only and not exact figures. During the past year, that exchange rate has varied from a low of AU$1.00/US$0.968 to a high of AU$1.00/US$1.079.

| 1 |

Description of Prospect – Petroleum Exploration License (PEL) 512

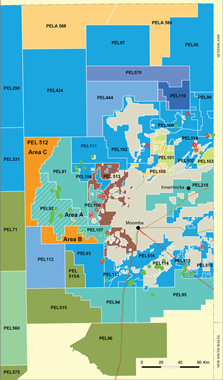

Granted on October 26, 2012, the License accords to us a 100% working interest (82% net revenue interest) in the Prospect. The Prospect covers 584,651 gross acres in the State of South Australia that overlays portions of geological systems commonly referred to as the Cooper and Eromanga Basins. This geologic system, which covers the northeast corner of South Australia and the southwest corner of Queensland State (see location map below), is the most prolific producing onshore region in Australia. Since 1963, 244 gas fields and 193 oil fields have been put on production in the Cooper/Eromanga Basins. Cumulative production in the Basins is in excess of 500 trillion cubic feet of natural gas since 1970 with crude oil and condensate production over 229 million barrels since 1983. Through February of this year, exploration and development drilling in the South Australia portion of the Copper/Eromanga Basins has consisted of more than 667 exploration wells, 482 appraisal wells and 836 development wells. (Source: PEPS database - Feb 2013)

Location Map |

|

The Cooper Basin is comprised of 32 million acres. It developed in late Carboniferous Period to the early Permian Period, and features a maximum thickness of sediments of about 9,000 feet. This basin is divided into several depo-centers by faulted anticlinal trends. The Permian Period formations within the Cooper Basin are characterized by alternating fluvial sandstones/floodplain siltstones. Overlaying the Permian Period are Triassic Period formations characterized by fluvial/floodplain sediments. The Eromanga Basin is comprised of 250 million acres, which developed as an interior sag over the central and eastern region of Australia during the Jurassic and Cretaceous Periods. In the south, the depo-centers coincide with underlying Cooper Basin synclines. The younger Eromanga Basin covers the entire Cooper Basin. The geological characteristics of these two basins cause them in effect to form a basin system that for many purposes can best be thought of in terms of a single geological phenomenon rather than two.

In South Australia where the Prospect is located, hydrocarbons were first produced in 1963 when the Gidgealpa-2 discovery well was completed. The prolific Moomba gas field was discovered in 1966. The first commercial oil was discovered in 1970 in the Tirrawarra oil field. To date this localized system has produced nearly 60 oil fields and 150 gas fields. While natural gas production and associated liquids at the giant Moomba gas field have been in decline, crude oil production has seen a resurgence largely due to the award of new exploration licenses under the South Australia Government bid process, greater drilling activity fueled by higher oil prices, and the use of new 3-D seismic data which has resulted in higher exploration and development drilling success rates.

From January 2002 thru September 2012, new Cooper Basin explorers drilled 188 exploration wells and 82 appraisal/development wells. Most wells have targeted oil, although both oil and gas have been discovered. These new explorers have reported a technical success rate of 47% on exploration and 97% commercial success rate on appraisal and development wells. In addition, 49 exploration wells and 356 appraisal/development wells were drilled in the Petroleum Production Licenses (PPLs) and permits that were issued prior to 2000 and operated by Santos Limited. (Santos Limited is another company that is in no way related to us despite our former name of “Santos Resource Corp.”)

| 2 |

Santos Limited reported the technical success rate for exploration drilling was 51% and the commercial success rate for appraisal and development drilling in these PPLs was a very respectable 96%. (Source: PIRSA website - Dec 2012)

PEL 512 Permit Map

|

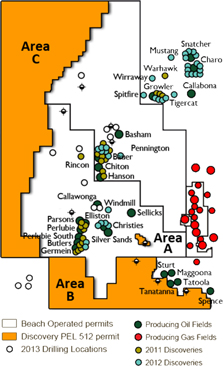

Recent Drilling Activity Map

|

The Prospect comprises 584,651 gross acres overlaying portions of the Cooper and Eromanga basins. The Prospect is located in what is generally referred to as the Western Oil Flank of the Cooper Basin and is directly adjacent to permits operated by Beach Energy in joint venture with Cooper Energy on PEL 92 and Drillsearch Energy on PEL 91.

The PEL 512 Lycium area (Area A, ≈4,000 Acres) is the smallest portion of the Prospect, the PEL 512 South area (Area B, ≈181,000 acres) is the next largest portion of the Prospect, and the PEL 512 West area (Area C, ≈400,000 acres) is the largest portion of the Prospect. The Permit Map set forth above indicates these areas of the Prospect in orange to the left of the center of the map.

During the late 1980s and again during 2005-2006, various operators drilled 10 wells in the extreme southeast corner of Area B. Reports filed with the South Australian government indicate that some of these wells exhibited "oil shows" but none were completed as commercial producers. Previous operators also conducted extensive seismic surveying on the license area and produced 5,153 km of 2D and 141 sq. km of 3D seismic data, which we acquired with the License.

From January 2011 through December 2012, Cooper Basin explorers drilled 41 exploration wells and 68 development wells. New explorers reported an exploration success rate of 55% and development success rate of 97%. The Recent Drilling Activity Map (above) indicates the locations of nearby producing oil and gas fields, new oil discoveries in 2011 and 2012, and the drilling locations planned for 2013

The use of 3D seismic interpretation and control combined with a greater understanding of the geology and producing formations has been a critical factor in the increase of recent exploration drilling success rates.

| 3 |

Since the early 1980s, this area of the Cooper Basin on which the Prospect sits has produced in excess of 25 million barrels of oil. Drilling activity has recently increased in licensed areas bordering or in close proximity to the Prospect. Wells in the areas adjacent to the Prospect are vertical or near-vertical and do not require lateral drilling or “fracing” for commercial completion.

Production during the first quarter of 2013 in the licensed areas adjacent to the Prospect at PEL’s 92 and 91 was approximately 8,000 barrels of oil/condensate per day. (Source: Beach Energy and Drillsearch Quarterly Reports – March 2013)

Beach Energy reported during the first quarter of 2013 oil production of ≈350,000 barrels (net) at PEL 92 (Beach 75%, Cooper Energy 25%) up 20% from the previous quarter, mainly due to the Callawonga to Lycium flow-line being operational, enabling additional wells to be brought back on production. Complimenting this production is the recently connected Butlers-5 and -6 wells, with the Christies-6 and -7 development wells expected to be on line in Q2-2013. Beach also reported its PEL 91 production of ≈110 barrels (net) up 73% from the previous quarter, mainly due to the connection of Bauer-5, -6,-7 and -8 and optimized trucking.

The PEL 91 Joint Venture (Drillsearch 60%, Beach 40%) commenced a four-well exploration drilling program targeting prospects that are covered by the Aquilius and Limbatus 3D seismic surveys which were completed in 2011 and 2012, respectively. The exploration campaign is targeting an unrisked prospective gross recoverable of 4–9 million barrels of oil on a combined basis over four prospects. During the first quarter of 2013, Drillsearch delivered a new all-time record in both quarterly production and revenue. The first quarter of 2013 saw continued strong growth in oil production to 176,734 barrels, up 66% on the prior quarter.

The Prospect features ready access to markets via existing infrastructure including short haul trucking and expanding pipeline capacity, which includes a recently commissioned 18,000 Bbl/d main Trunk Line running from the Moomba Processing Facility to the Lycium Hub, just offset the Prospect’s border.

During 2012 we assembled a significant technical database consisting of geological, geophysical and engineering data, well logs, completion reports, drilling reports, research reports, production data, raw and processed 2D/3D seismic data, maps and other related materials. Our initial technical focus was on evaluating the potential of the Prospect’s Area B. We subsequently engaged Apex Engineering based in Calgary, Alberta on March 21, 2012 to complete an NI 51-101 compliant report, which resulted in the identification of over 110 seismic generated leads over approximately 30% of the approximately 585,000-acre block. This was complimented by the re-interpretation of 5,153 km of 2D seismic and the re-processing and re-interpretation of 141 sq. km of 3D seismic over the Lake Hope area in the eastern portion of the Prospect’s Area B by Hardin International Processing, Inc., and Bell & Murphy and Associates, LLC, both located in Dallas, Texas.

The ongoing technical assessment has also defined several drill-ready prospects in the Lake Hope 3D area of Area B. We plan to conduct a 133 sq. km 3D seismic program during 2013 in the western portion of Area B, which is directly on trend and in close proximity with the historic production and recent discoveries on Beach Energy’s operated PEL 92 to the North.

The South Australia Government has recently approved an Associated Activities Licence (AAL) to construct a 30 km rig access road thru the western corner of Area B and into the adjoining PEL 112. This block is operated by Terra Nova, which announced plans to drill the Wolverine #1 well in May/June 2013. The newly constructed road will provide us direct access to the area proposed and reduce costs for the planned 3D seismic program.

| 4 |

Terms of the License

On October 26, 2012, Discovery Energy SA Ltd, our Australian subsidiary (the "Subsidiary"), received the formal grant of the License from the South Australian Minister for Mineral Resources and Energy. The License is a "Petroleum Exploration Licence" regarding all regulated resources (including petroleum and any other substance that naturally occurs in association with petroleum) relating to the 584,651 gross acres comprising the Prospect land, provided, however, that the License does not permit using the Prospect land as a source of geothermal energy or a natural reservoir for the purpose of gas storage. The term of the License is for five years, with two further, 5-year renewal terms, subject to the provisions of the South Australian Petroleum and Geothermal Energy Act 2000.

The License is subject to a five-year work commitment that is described in “Item 1. Business - Plan of Operation - Proposed Initial Activities.” Failure to comply with the work program requirements could lead to the cancellation of the License.

The License requires that, prior to commencing any fieldwork, the Subsidiary post a minimum security deposit of AU$50,000 (US$51,815). Moreover, the License requires the Subsidiary to maintain insurance of the types and amounts of coverage that management believes are reasonable and customary, and are the industry standard throughout Australia.

The License requires the Subsidiary to pay certain fees and production payments to the native titleholders in accordance with the native title agreement and a similar agreement discussed immediately below. The License contains provisions regarding environmental matters and liabilities that management also believes are reasonable and customary, and are the industry standard throughout Australia.

Native Title Agreement

As a precondition to the issuance of the License, on September 3, 2012 the Subsidiary entered into an agreement (the "Native Title Agreement") with (a) the State of South Australia, (b) representatives of the Dieri Native Title Holders (the "Native Title Holders") on behalf of the Native Title Holders, and (c) the Dieri Aboriginal Corporation (the "Association"). The Native Title Holders have certain historic rights on the lands covered by the License.

The term of the Native Title Agreement commenced upon its execution, and it will terminate on the completion of the operations proposed or which may be undertaken by the Subsidiary in connection with the License and all subsequent licenses resulting from the License. By entering into the Native Title Agreement, the Native Title Holders agreed to the grant of the License and all subsequent licenses to the Subsidiary, and they also covenanted not to lodge or make any objection to any grant of licenses to the Subsidiary in respect of the License area unless the Subsidiary is in breach of an essential term under the Native Title Agreement. The Native Title Agreement provides that it will not terminate in the event of a breach of a payment obligation, but the parties may avail themselves of all other remedies available at law, which would involve recourse to the non-exclusive jurisdiction of the courts of the Commonwealth of Australia and the State of South Australia. Recourse for breach of operational obligations of the Subsidiary in favor of the Native Title Holders and the Association would be subject to the stipulated dispute resolution procedure involving negotiation and mediation before any party may commence court proceedings or arbitration.

| 5 |

In consideration of the Native Title Holders' entering into the Native Title Agreement, the Subsidiary remitted to them a one-time payment in the amount of AUS$75,000 (or US$80,377 based on the exchange rate charged to us in late November 2012 when the payment was made). Moreover, throughout the term of the License, the Subsidiary is obligated to pay to the State of South Australia for the benefit of the Native Title Holders production payments in amounts equal to 1% of the value at the wellhead of petroleum produced and sold from the lands covered by the License. Furthermore, for facilitating the administration of this Native Title Agreement, the Subsidiary will pay in advance to the Association an annual fee comprising 12% of a maximum administration fee (the "Maximum Administration Fee"), which is AUS$150,000 (or approximately US$158,300 based on exchanges rates in effect on April 21, 2013) (subject to adjustment for inflation). This 12% payment will be made for each year of the first five-year term of the License. After the first five-year term of the License, the payment will be four percent 4% of the Maximum Administration Fee for each year of the second and third five-year terms of the License.

The Subsidiary has virtually unlimited ability to assign and transfer (partially or entirely) its rights in the Native Title Agreement, provided certain procedural requirements are met. This ability should enhance the Subsidiary's ability to procure an industry joint venture partner.

The Native Title Agreement features extensive provisions governing aboriginal heritage protection in connection with the Subsidiary's activities relating to the License. Management believes that these provisions (as well as the other provisions of the Native Title Agreement) are reasonable and customary, and are the industry standard throughout Australia. Under the Native Title Agreement, the Native Title Holders authorize the Subsidiary to enter upon the License area at all times and to commence and proceed with petroleum operations, and, while the provisions governing aboriginal heritage protection could adversely affect operational strategy and could increase costs, the Native Title Holders and the Association covenant that they will not interfere with the conduct of those operations; will actively support the Subsidiary in procuring all approvals, consents and other entitlements and rights as are necessary to support the interests of the Subsidiary in furthering the project; will refrain from doing any act which would impeded or prevent the Subsidiary from exercising or enjoying any of the rights granted or consented to under the Native Title Agreement; and will observe all applicable laws in performing their obligations under the Native Title Agreement.

In connection with the entry into the Native Title Agreement, the Subsidiary entered into a similar agreement with other Aboriginal native titleholders and claimants with respect to a comparatively small amount of land also covered by the License. For all practical purposes, the terms of this additional agreement are the same as those contained in the Native Title Agreement. Payments made under this second agreement will reduce payments under the Native Title Agreement on a dollar-for-dollar basis, so that each of the two groups of native title holders and claimants will receive payments proportionately based on the amount of land that their respective claims represent relative to the total area covered by the License.

Acquisition of the License

On October 26, 2012, the Subsidiary received the formal grant of the License. This grant was the culmination of a series of transactions that began near the end of our fiscal 2012. The remainder of this section describes the consideration paid by us in having the License granted to the Subsidiary.

Liberty Petroleum Corporation. Liberty Petroleum Corporation ("Liberty") was the winning bidder for the License. We entered into agreements with Liberty whereby Liberty agreed to sell the License to us upon its issuance. Eventually, Liberty and we modified our agreements so that we would take the direct issuance of the License in place of Liberty. For Liberty’s agreements to allow us to be issued the License, we agreed to remit to Liberty the following consideration, which has a deemed value of US$3.95 million:

| 6 |

| * | Cash in the amount of $800,000 |

| * | Two promissory notes with an aggregate principal amount of $650,000, one in the amount of $500,000 now due on or before June 12, 2013, and the other in the amount of $150,000 due on or before July 26, 2013 – In connection with the extension of the due date of the $500,000 promissory note, we paid $100,000, so that now only $400,000 remains outstanding on this promissory note. |

| * | Twelve million shares of our common stock |

In addition to the preceding, Liberty was allowed to retain a 7.0% royalty interest relating to the Prospect.

Keith D. Spickelmier. Prior to our agreements with Liberty, Liberty had entered into an agreement (as amended and restated, the "Liberty Agreement") with Keith D. Spickelmier, now (but not then) our Chairman of the Board. This agreement granted to Mr. Spickelmier the right to negotiate an option to acquire the License upon its issuance. Per the terms of the Liberty Agreement, Mr. Spickelmier paid to Liberty a $50,000 initial deposit. In anticipation of the assignment of the Liberty Agreement to us, we paid to Liberty (a) an additional $100,000 deposit to extend the exclusive right provided for by the Liberty Agreement, and (b) an additional $200,000 deposit to modify certain terms of the Liberty Agreement, including the further extension of the exclusive right. The preceding amounts were part of the $800,000 that we paid to Liberty, as discussed above. Subsequent to the assignment to us of the Liberty Agreement and pursuant to its terms, we reached the agreements described above whereby we would take the direct issuance of the License in place of Liberty. The purchase price for the assignment of Mr. Spickelmier’s rights in the Liberty Agreement is as follows:

| * | $50,000 in cash – This amount was paid shortly after the assignment of the Liberty Agreement. |

| * | $100,000 deferred payment - This amount was paid after the issuance of the License. |

| * | Twenty million shares of our common shares – These shares were issued upon the assignment of the Liberty Agreement. |

| * | Fifty-five million shares of our common shares - These shares were issued to Mr. Spickelmier and his designees (all of whom constitute other members of our management) after the issuance of the License. |

Native Title Holders. As described in “Item 1. Business - Native Title Agreement” above, the Subsidiary entered into the Native Title Agreement as a precondition for receiving the License. It entered into a similar agreement with other Aboriginal native titleholders and claimants as also described above. For all practical purposes, the terms of this additional agreement are the same as those contained in the Native Title Agreement. In consideration of the Native Title Holders’ entering into the Native Title Agreement, the Subsidiary made to them a one-time payment in the amount of AUS$75,000(US$80,377). Throughout the term of the Native Title Agreement, the Subsidiary will be obligated to make additional payments that are further described in “Item 1. Business - Native Title Agreement.”

Government Payment. In connection with the issuance of the License, we made a nominal payment (less than US$3,500) to the Government of South Australia.

| 7 |

Plan of Operation

General

We intend to engage primarily in the exploration and development of oil and gas on the Prospect in an effort to develop oil and gas reserves. Our principal products will be crude oil and natural gas. Our development strategy will be directed in the multi-pay target areas of South Australia, with principal focus on the prolific Cooper/Eromanga Basin, towards initiating and rapidly expanding production rates and proving up significant reserves primarily through exploratory drilling. Our mission will be to generate superior returns for our stockholders by working with industry partners, suppliers and the community to build a focused exploration and production company with strong development assets in the oil and gas sector.

In the right circumstances, we might assume the entire risk of the drilling and development of the Prospect. More likely, we will determine that the drilling and development of the Prospect can be more effectively pursued by inviting industry participants to share the risk and the reward of the Prospect by financing some or all of the costs of drilling wells. Such arrangements are frequently referred to as "farm-outs." In such cases, we may retain a carried working interest or a reversionary interest, and we may be required to finance all or a portion of our proportional interest in the Prospect. Although this approach will reduce our potential return should the drilling operations prove successful, it will also reduce our risk and financial commitment to a particular prospect. Prospective participants regarding possible "farm-out" arrangements have already approached us.

There can be no assurance that we will be successful in our exploratory and production activities. The oil and gas business involves numerous risks, the principal ones of which are listed in "Item 1A. Risk Factors - RISKS RELATING TO OUR INDUSTRY - PARTICIPANTS IN THE OIL AND GAS INDUSTRY ARE SUBJECT TO NUMEROUS RISKS." As we become more involved in the oil and gas exploration and production business, we will give more detail information regarding these risks.

Although our primary focus is on the acquisition and development of the Prospect, we have received information about, and have had discussion regarding possible acquisition of or participation in, other oil or gas opportunities. None of these discussions has led to any agreement in principle. Nevertheless, given an attractive opportunity and our ability to consummate the same, we could acquire one or more other crude oil and natural gas properties, or participant in one or more other crude oil and natural gas opportunities.

Proposed Initial Activities

We have just begun the initial phase of our plan of operation. To date we have not commenced any drilling or other exploration activities on the Prospect, and thus we do not have any estimates of oil and gas reserves. Consequently we have not reported any reserve estimates to any governmental authority. We cannot assure anyone that we will find commercially producible amounts of oil and gas. Moreover, at the present time, we cannot finance the initial phase of our plan of operation solely through our own current resources. Therefore, we have undertaken certain financing activities described in "Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources" below. The success of the initial phase of our plan of operation depends upon our ability to obtain additional capital to acquire seismic data with respect to the Prospect, and to drill exploratory and developmental wells. We cannot assure anyone that we will obtain the necessary capital.

The License is subject to a five-year work commitment, which involves the following:

| 8 |

| * | Year 1 –Conduct geological and geophysical studies including interpretation of existing seismic data. In management’s view, the geotechnical work already completed is sufficient to satisfy this requirement, and we plan on filing with the South Australian government to obtain its approval in this regard. |

| * | Year 2 - Conduct a new 2D seismic survey totaling at least 250 kilometers (approximately 155 miles). We will seek approval to substitute our planned 3D survey discussed below for this requirement. |

| * | Year 3 - Acquire new 3D seismic data totaling at least 400 square kilometers (approximately 155 square miles) and drill two wells |

| * | Year 4 - Drill five wells |

| * | Year 5 - Drill five wells |

The prices of the equipment and services that we must employ to fulfill the work commitment vary based on both local and international demand for such products by others involved in exploration for and production of oil and gas. Recent high worldwide energy prices have resulted in growing demand, which lends support to higher prices being charged by suppliers. Therefore, we have no assurance that the steps in the work plan (e.g. shooting 130 square kilometers of 3D seismic) can be accomplished at current or lower costs.

Based on our research and technical analysis to date, we believe that acceleration of the License work plan can be justified. Hence, the initial phase of our plan of operation involved (among other things) conducting a 3D seismic survey of 130 square kilometers (approximately 50 sq. miles) and drilling of at least three exploration wells. This activity will take place on the Prospect’s Area B and exceeds, in our view, the near-term work requirements under the License. Subject to the availability of funds plus proper equipment and personnel, management feels that US$15.0 million or more can be productively invested within the first three years. Not only is this program contingent on our procurement of sufficient funds therefore, it may also be subject to governmental approval to vary the work commitment already in place.

We intend to seek a joint venture partner who or which might act as the operator of our wells. If we are unsuccessful in procuring such a partner, we will engage the services of a third party once we have identified a proposed drilling site. Management foresees no problem in procuring the services of one or more qualified operators and drillers in connection with the initial phase of our plan of operation, although a considerable increase in drilling activities in the area of our properties could make difficult (and perhaps expensive) the procurement of operating and drilling services. In all cases, the operator will be responsible for all regulatory compliance regarding the well, including any necessary permitting for the well. In addition to regulatory compliance, the operator will be responsible for hiring the drilling contractor, geologist and petroleum engineer to make final decisions relative to the zones to be targeted, well design, and bore-hole drilling and logging. Should the well be successful, the operator would thereafter be responsible for completing the well, installing production facilities and interconnecting with gathering or transmission pipelines if economically appropriate. We expect to pay third party operators (i.e. not joint venture partner with us) commercially prevailing rates.

The operator will be the caretaker of the well once production has commenced. Additionally, the operator will formulate and deliver to all interest owners an operating agreement establishing each participant's rights and obligations in that particular well based on the location of the well and the ownership. The operator will also be responsible for paying bills related to the well, billing working interest owners for their proportionate expenses in drilling and completing the well, and selling the production from the well. Unless each interest owner sells its production separately, the operator will collect sale proceeds from oil and gas purchasers, and, once a division order has been established and confirmed by the interest owners, the operator will issue the checks to each interest owner in accordance with its appropriate interest. The operator will not perform these functions when each interest owner sells its production separately, in which case the interest owners will undertake these activities separately. After production commences on a well, the operator also will be responsible for maintaining the well and the wellhead site during the entire term of the production or until such time as the operator has been replaced.

| 9 |

The principal oil, natural gas and gas liquids transportation hub for the region of South Australia surrounding the Prospect is located in the vicinity of Moomba. This processing and transportation center is approximately 60 km (36 miles) due east of the Prospect's eastern boundary. Large diameter pipelines deliver oil and gas liquids from Moomba south to Port Bonython (Whyalla). Natural gas is also moved south to Adelaide or east to Sydney. A gas transmission pipeline also connects Moomba to Ballera, which is located northeastward in the State of Queensland. From Ballera gas can be moved to Brisbane and Gladstone, where a Liquefied Natural Gas (LNG) project is under development. The Moomba treating and transportation facilities and the southward pipelines were developed and are operated by a producer consortium led by Santos Limited (no relation to us).

We cannot accurately predict the costs of transporting our production until we locate our first successful well. The cost of installing infrastructure to deliver our production to Moomba or elsewhere will vary depending upon distance traversed, negotiated handling/treating fees, and pipeline tariffs.

Markets and Marketing

The petroleum industry has been characterized historically by crude oil and natural gas commodity prices that fluctuate (sometimes dramatically), and supplier costs can rise significantly during industry booms. For example, crude oil and natural gas prices increased to historical highs in 2008 and then declined significantly over the last two quarters of 2008. Since this period, prices have improved, but have not returned to historical highs. Crude oil and gas prices and markets are likely to be volatile again in the future. Crude oil and natural gas are commodities and their prices are subject to wide fluctuations in response to relatively minor changes in supply and demand for oil and gas, market uncertainty, and a variety of additional factors beyond our control. Those factors include:

| * | international political conditions (including wars and civil unrest, such as the recent unrest in the Middle East); |

| * | the domestic and foreign supply of oil and gas; |

| * | the level of consumer demand; |

| * | weather conditions; |

| * | domestic and foreign governmental regulations and other actions; |

| * | actions taken by the Organization of Petroleum Exporting Countries (OPEC); |

| * | the price and availability of alternative fuels; and |

| * | overall economic conditions. |

Lower oil and natural gas prices may not only decrease our revenues on a per unit basis, but may also reduce the amount of oil and natural gas we can produce economically, if any. A sustained decline in oil and natural gas prices may materially affect our future business, financial condition, results of operations, liquidity and borrowing capacity, and may require a reduction in the carrying value of our oil and gas properties. While our revenues may increase if prevailing oil and gas prices increase significantly, exploration and production costs and acquisition costs for additional properties and reserves may also increase. We may or may not enter into hedging arrangements or use derivative financial instruments such as crude oil forward and swap contracts to hedge in whole or in part our risk associated with fluctuations in commodity prices.

| 10 |

We do not expect to refine any of our production, although we may have to treat or process some of our production to meet the quality standards of purchasing or transportation companies. Instead, we expect that all or nearly all of our production will be sold to a relatively small number of customers. Production from our properties will be marketed consistent with industry practices. We do not now have any long-term sales contracts for any crude oil and natural gas production that we realize, but we expect that we will generally sell any production that we develop pursuant to these types of contracts. We do not believe that we will have any difficulty in entering into long-term sales contracts for our production, although there can be no assurance in this regard.

The availability of a ready market for our production will depend upon a number of factors beyond our control, including the availability of other production in the Prospect’s region, the proximity and capacity of oil and gas pipelines, and fluctuations in supply and demand. Although the effect of these factors cannot be accurately predicted or anticipated, we do not anticipate any unusual difficulty in contracting to sell our production of oil and gas to purchasers at prevailing market prices and under arrangements that are usual and customary in the industry. However, there can be no assurance that market, economic and regulatory factors will not in the future materially adversely affect our ability to sell our production.

We expect that most of the natural gas that we are able to find (if any) will be transported through gas gathering systems and gas pipelines that are not owned by us. The Prospect is in fairly close proximity to gas pipelines suitable for carrying our production. Transportation capacity on gas gathering systems and pipelines is occasionally limited and at times unavailable due to repairs or improvements being made to the facilities or due to use by other gas shippers with priority transportation agreements or who own or control the relevant pipeline. If transportation space is restricted or is unavailable, our cash flow could be adversely affected.

Sales prices for oil and gas production are negotiated based on factors normally considered in the industry, such as the reported trading prices for oil and gas on local or international commodity exchanges, distance from the well to the pipeline, well pressure, estimated reserves, commodity quality and prevailing supply conditions. Historically, crude oil and natural gas market prices have experienced high volatility, which is a result of ever changing perceptions throughout the industry centered on supply and demand. We cannot predict the occurrence of events that may affect oil and gas prices or the degree to which such prices will be affected. However, the oil or gas prices realized by us should be equivalent to current market prices in the geographic region of the Prospect. Typically, oil prices in Australia reflect or are “benchmarked” against European commodity market trading settlement prices, namely Brent Crude. Recent price levels in this market have been at a premium to those settled in the United States, or (in other words) those “benchmarked” against West Texas Intermediate Crude. During certain periods, the differential has been substantial. We cannot predict the future level of this price differential or be assured that such differential will reflect a favorable premium for us in the future.

We will strive to obtain the best price in the area of our production. Our revenues, profitability and future growth will depend substantially on prevailing prices for crude oil and natural gas. Decreases in the prices of oil and gas would likely adversely affect the carrying value of any proved reserves we are successful in establishing and our prospects, revenues, profitability and cash flow.

Competition

We expect to operate in the highly competitive areas of oil and gas exploration, development and production. We believe that the level of competition in these areas will continue into the future and may even intensify. In the areas of oil and gas exploration, development and production, competitive advantage is gained through superior capital investment decisions, technological innovation and costs management. Our competitors include major oil and gas firms and a large number of independent oil and gas companies. Because we expect to have control over acreage sufficient for our exploration and production efforts for the foreseeable future, we do not expect to compete for the acquisitions of properties for the exploration for oil and gas. However, we will compete for the equipment, services and labor required to operate and to develop our properties and to transport our production. Many of our competitors have substantially larger operating staffs and greater financial and other resources. In addition, larger competitors may be able to absorb the burden of any changes in laws and regulations more easily than we can, which would adversely affect our competitive position. Moreover, most of our competitors have been operating for a much longer time than we, and have demonstrated the ability to operate through a number of industry cycles. The effect of the intense competition that we will face cannot now be determined.

| 11 |

Regulation

Our operations in South Australia and within the area of the Prospect are subject to the laws and regulations of the State of South Australia and the Commonwealth of Australia. The License was granted under the Petroleum and Geothermal Energy Act 2000 (SA) and our operations within and with respect to the License are governed by this Act and by the Petroleum and Geothermal Energy Regulations 2013 (SA). This legislation covers all phases of our operations including exploration, appraisal, development and production of oil and gas from the License area. Other legislation which we will be required to comply with at various stages of our operations include: Environment Protection Act 1993 (SA); Aboriginal Heritage Act 1988 (SA); Native Title (South Australia) Act 1994 (SA) and Native Title Act 1993 (Cth). As our oil and gas exploration and production operations in South Australia proceed, we will provide more detailed information regarding the material features and effects of these laws and regulations and such other legislation with which we will be required to comply.

Legal Proceedings

We are not now involved in any legal proceedings. There can be no assurance, however, that we will not in the future be involved in litigation incidental to the conduct of our business.

Employees

As of the date of this filing, we had no employees. We expect that we will have no employees for the foreseeable future, although we expect to enter into consulting agreements with members of our management at some time in the future. The market for qualified oil and gas professionals and craftsmen can be very competitive during periods of strong commodity prices. Such a period is currently being experienced. We anticipate that we will be able to offer compensation and an interesting work environment that will enable us to attract employees to meet our labor needs.

Facilities

We maintain our principal executive offices at One Riverway Drive, Suite 1700, Houston, Texas 77056 through an office rental package on essentially a month-to-month basis. Management believes that any needed additional or alternative office space can be readily obtained.

Our Historical Business

Our historical business involved the proposed exploration and development of a 75% interest in and to 18 mineral claims covering approximately 900.75 hectares (9.01 km2) called the Lourdeau Claims in the La Grande geological area of Quebec, Canada. Management intends to allow these claims to expire in accordance with their terms on July 18, 2013, so that management can devote its entire attention to our new business.

| 12 |

Item 1A. Risk Factors.

An investment in shares of our common stock is highly speculative and involves a high degree of risk. You should carefully consider all of the risks discussed below, as well as the other information contained in this Annual Report. If any of the following risks develop into actual events, our business, financial condition or results of operations could be materially adversely affected and the trading price of our common stock could decline.

RISKS RELATING TO OUR COMPANY

We WILL need additional capital to SATISFY A DEFERRED PAYMENT incurred in connection with the acquisition of THE PROSPECT, TO PROVIDE WORKING CAPITAL, and TO DEVELOP THE PROSPECT, which we may not be able to raise or WHICH may be available only on terms unfavorable to us.

In connection with the acquisition of the Prospect, we incurred deferred payments to Liberty in the form of two promissory notes in the original principal amounts of US$500,000 (originally due on or before April 26, 2013) and US$150,000 (due on or before July 26, 2013). On March 7, 2013, in consideration of a partial payment in the amount of $100,000 of the outstanding principal on the US$500,000 note, we and Liberty agreed to amend this note so that the remaining outstanding principal on and accrued interest on this note will be due and payable on of before June 12, 2013. These promissory notes will become due before we are able to commence production on the Prospect. Moreover, because of the acquisition of the Prospect, we have a work commitment with respect to the Prospect requiring us to expend stipulated amounts. In management’s view, the geotechnical work completed to-date meets the first year work commitment under the License. However, we will need additional funds to satisfy the work commitment in future years. Moreover, we will need working capital and further funds to explore and develop the Prospect in the manner that we prefer.

We are currently engage in active efforts to complete (a) a major capital raising transaction or (b) the sale of a portion of our interest in the Prospect to a joint venture partner for a cash payment and/or a work commitment, or (c) some combination of (a) and (b). In this connection, we have engaged the services of a corporate finance firm. We have no assurance that we will be successful in completing a transaction that will provide us with required funds. If required financing is not available on acceptable terms, we could be prevented from satisfying our debt obligations or developing the Prospect. In such event, we would be forced to seek an extension of the due date of the amount owed to Liberty or else default on this amount. If a default occurs, Liberty could exercise the rights of an unsecured creditor and possibly levy encumbrances on all or a large part of our assets. Moreover, our failure to honor our work commitment could result in our loss of the Prospect. If any of the preceding events were to occur, we could be forced to cease our new business plan altogether, which could result in a complete loss to our stockholders. Our future liquidity will depend upon numerous factors, including the success of our business efforts and our capital raising activities. Any debt financing undertaken to procure funds may involve restrictions limiting our operating flexibility. Moreover, if we obtain funds through the issuance of equity securities, the following results will or may occur:

| * | The percentage ownership of our existing members will be reduced |

| * | The new equity securities may have rights, preferences or privileges senior to those of the holders of our common stock. |

We have no assurance of our ability to raise funds for any purpose.

| 13 |

WE HAVE NOT ENGAGED IN THE OIL AND GAS EXPLORATION BUSINESS BEFORE.

Our company was incorporated on May 24, 2006 for the purpose of trying to develop commercially certain mineral claims. This business did not move forward. We have decided to focus our business on the exploration, development and production of oil and gas on a particular crude oil and natural gas prospect that is described in “Item 1 Business” (the “Prospect”). The Prospect is considered "undeveloped acreage," which the U.S. Securities and Exchange Commission (the "Commission") defines as "lease acreage on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil and gas regardless of whether such acreage contains proved reserves." We have no proved reserves. In view of our extremely limited history in the oil and gas exploration business, you may have difficulty in evaluating us and our business and prospects. You must consider our business and prospects in light of the risks, expenses and difficulties frequently encountered by companies in their early stage of development. For our business plan to succeed, we must successfully undertake most of the following activities:

| * | Complete a financing or similar transaction that will provide us with sufficient funds; |

| * | Drill successfully exploratory test wells on the Prospect to determine the presence of oil and gas in commercially viable quantities; |

| * | Develop the Prospect to a stage at which oil and gas are being produced in commercially viable quantities; |

| * | Procure purchasers of our commercial production of oil and gas upon such commencement; |

| * | Comply with applicable laws and regulations; |

| * | Identify and enter into binding agreements with suitable third parties (such as joint venture partners and contractors) for the Prospect; |

| * | Implement and successfully execute our business strategy; |

| * | Respond to competitive developments and market changes; and |

| * | Attract, retain and motivate qualified personnel. |

There can be no assurance that we will be successful in undertaking such activities. Our failure to undertake successfully most of the activities described above could materially and adversely affect our business, prospects, financial condition and results of operations. In addition, there can be no assurance that our exploration and production activities will produce oil and gas in commercially viable quantities, if any at all. Moreover, even if we succeed in producing oil and gas, we expect to incur operating losses until such time (if ever) as we produce and sell a sufficient volume of our commercial production to cover direct production costs as well as corporate overhead. There can be no assurance that sales of our oil and gas production will ever generate significant revenues, that we will ever generate positive cash flow from our operations or that (if ever attained) we will be able to sustain profitability in any future period.

Our auditor has given to us a “going concern” qualification, which questions our ability to continue as a going concern without additional financing.

Our independent certified public accountant has added an emphasis paragraph to its report on our financial statements for the year ended February 28, 2013 regarding our ability to continue as a going concern. Key to this determination is our lack of any historical revenues and its accumulated loss of $1,333,173 since inception. Management plans to try to fund our company primarily through the raising of capital through the sale of our equity securities, a farm-in transaction or the sale of ownership in our Australia Subsidiary, although there can be no assurance of success in this regard. There can be no assurance that we will be successful in achieving this objective, becoming profitable, or continuing our business without either a temporary interruption or a permanent cessation.

| 14 |

IF WE GROW OUR BUSINESS AS PLANNED, WE MAY NOT BE ABLE TO MANAGE PROPERLY OUR GROWTH, AND WE EXPECT OPERATING EXPENSES TO INCREASE, WHICH MAY IMPEDE OUR ABILITY TO ACHIEVE PROFITABILITY.

If we are successful in growing our business as we plan, our operations may expand rapidly and significantly. Any rapid growth could place a significant strain on our management, operational and financial resources. In order to manage the growth of our operations, we will be required to improve and expand existing operations; to implement new operational, financial and inventory systems, procedures and controls, including improvement of our financial and other internal management systems; and to train, manage and expand our employee base. If we are unable to manage growth effectively, our business, results of operations and financial condition will be materially adversely affected. In addition, if we are successful in growing our business as we plan, we expect operating expenses to increase, and as a result, we will need to generate increased quarterly revenue to achieve and maintain profitability. These additional costs and expenses could delay our ability to achieve continuing profitability.

Conducting business internationally may result in increased costs and other risks.

We plan on operating our business internationally in Australia. Operating internationally exposes us to a number of risks. Examples include a possible downturn in local economic conditions due to local policy decisions, increases in duties and taxes, and other adverse changes in laws and policies affecting our business, or governing the operations of foreign-based companies. Additional risks include currency fluctuations, interest rate movements, imposition of trade barriers, and restrictions on repatriation of earnings. If we are unable to address these risks adequately, our financial position and results of operations could be adversely affected.

RISKS RELATING TO OUR INDUSTRY

PARTICIPANTS IN THE OIL AND GAS INDUSTRY ARE SUBJECT TO NUMEROUS RISKS.

Participants in the oil and gas industry are subject to numerous risks over which we will have limited or no control. These risks include the following:

| * | Volatility in market prices of hydrocarbons, which could become and remain low resulting in impairments negatively affecting our financial performance |

| * | Difficulty in selecting drilling sites that result in production in commercially viable quantities |

| * | Formation problems that cannot be anticipated even with the best possible due diligence |

| * | Problems with availability, cost and quality of drilling equipment and personnel |

| * | Problems encountered in drilling, including, without limitation, fires, explosions, blow-outs and surface cratering, uncontrollable flows of natural gas oil and formation water, natural disasters such as hurricanes and other adverse, weather conditions, pipe cement subsea well or pipeline failures, casing collapses, ineffective hydraulic fracs, embedded oil field drilling and service tools, abnormally pressured formations, and environmental hazards such as natural gas leaks, oil spills, pipeline ruptures and discharges of toxic gases |

| * | Adverse hedging decisions |

| * | Regulatory burdens and liabilities, including environmental ones |

| * | Failure to address competition in a changing environment |

| 15 |

Any of the risks set forth above (as well as other risks not set forth above or not now foreseeable) could materially and adversely affect our future business, financial condition, results of operations, liquidity and ability to finance capital expenditures.

RISKS RELATING TO OUR MANAGEMENT

WE DEPEND ON CERTAIN KEY PERSONNEL.

We currently and in the future will substantially depend upon the efforts and skills of our current and expected future management. The loss of the services of any member of management, or the inability of any of time to devote sufficient attention to our operations, could materially and adversely affect our operations. Currently, no member of management has entered into a written employment agreement or any covenant not to compete agreement with us. As a result, any member of management may discontinue providing his services to us at any time and for any reason, and even thereafter commence competition with us. Moreover, we do not currently maintain key man life insurance on any member of management

OUR CURRENT MANAGEMENT RESOURCES MAY NOT BE SUFFICIENT FOR THE FUTURE, AND WE HAVE NO ASSURANCE THAT WE CAN ATTRACT ADDITIONAL QUALIFIED PERSONNEL.

There can be no assurance that the current level of management is sufficient to perform all responsibilities necessary or beneficial for management to perform. Our future success also depends on our continuing ability to attract, assimilate and retain highly qualified sales, technical and managerial personnel. Competition for these individuals is intense, and there can be no assurance that we can attract, assimilate or retain necessary personnel in the future.

OUR MANAGEMENT OWNS A LARGE PERCENTAGE OF OUR OUTSTANDING STOCK, AND CUMULATIVE VOTING IS NOT AVAILABLE TO STOCKHOLDERS.

Our current senior management owns approximately 71% of our outstanding common stock as of the date of this Report. Cumulative voting in the election of directors is not authorized in our First Amended and Restated Articles of Incorporation. Accordingly, it is not permitted as a matter of law. As a result, the holder or holders of a majority of our outstanding shares of common stock may elect all of our directors. Management's large percentage ownership of our outstanding common stock will enable them to maintain their positions as such and thus their control of our business and affairs.

OUR OBLIGATION TO INDEMNIFY MEMBERS OF MANAGEMENT COULD REQUIRE US TO PAY THEM FOR LOSSES CAUSED BY THEM, AND LIMITATIONS ON CLAIMS AGAINST SUCH MEMBERS COULD PREVENT OUR RECOVERY OF SUCH LOSSES FROM THEM.

The corporation law of Nevada allows a Nevada corporation to indemnify its directors and each of its officers, agent and/or employee to the extent that certain standards are met, and our First Amended and Restated Articles of Incorporation permits indemnification of our director, and our Bylaws requires indemnification of our director to the maximum extent permitted by law. If the required standards are met, we could be required to indemnify management for losses caused by them. Further, we may purchase and maintain insurance on behalf of any such persons whether or not we have the power to indemnify such person against the liability insured against. Moreover, the corporation law of Nevada allows a Nevada corporation to limit the liability of its directors to the corporation and its stockholders to a certain extent, and our First Amended and Restated Articles of Incorporation and Bylaws have eliminated the director’s liability to the maximum extent permitted by law. Consequently, because of the actions or omissions of our management, we could incur substantial losses and be prevented from recovering such losses from such persons. Further, the U.S. Securities and Exchange Commission maintains that indemnification for liabilities arising under the Securities Act is against the public policy expressed in the Securities Act, and is therefore unenforceable.

| 16 |

WE ARE REQUIRED TO COMPLY WITH SECTION 404 OF THE SARBANES OXLEY ACT OF 2002.

Pursuant to Section 404 of the Sarbanes-Oxley Act of 2002, in connection with this Annual Report and future Annual Reports, we are and will be required to furnish a report by management on our internal controls over financial reporting which will contain, among other matters, an assessment of the effectiveness of our internal control over financial reporting, including a statement as to whether or not our internal control over financial reporting is effective. This assessment must include disclosure of any material weaknesses in our internal control over financial reporting identified by our management. During the evaluation and testing process, if we identify one or more material weaknesses in our internal control over financial reporting, we will be unable to assert that such internal control is effective. If we are unable to assert that our internal control over financial reporting is effective, we could lose investor confidence in the accuracy and completeness of our financial reports. Furthermore, we expect that our compliance with the regulatory requirements described herein will likely increase our professional expenses.

WE HAVE NOT VOLUNTARILY IMPLEMENTED VARIOUS CORPORATE GOVERNANCE MEASURES, IN THE ABSENCE OF WHICH, SHAREHOLDERS MAY HAVE MORE LIMITED PROTECTIONS AGAINST INTERESTED DIRECTOR TRANSACTIONS, CONFLICTS OF INTEREST AND SIMILAR MATTERS.

Recent Federal legislation, including the Sarbanes-Oxley Act of 2002, has resulted in the adoption of various corporate governance measures designed to promote the integrity of the corporate management and the securities markets. Some of these measures have been adopted in response to legal requirements. Others have been adopted by companies in response to the requirements of national securities exchanges, such as the NYSE or The NASDAQ Stock Market, on which their securities are listed. Among the corporate governance measures that are required under the rules of national securities exchanges are those that address board of directors' independence, audit committee oversight, and the adoption of a code of ethics. Although we have adopted a Code of Ethics, we have not yet adopted any of these other corporate governance measures and, since our securities are not yet listed on a national securities exchange, we are not required to do so. We have not adopted corporate governance measures such as an audit or other independent committees of our board of directors because we have been a “shell” company for some period of time. Possibly if we were to adopt some or all of these corporate governance measures, shareholders would benefit from somewhat greater assurances that internal corporate decisions were being made by disinterested directors and that policies had been implemented to define responsible conduct. For example, in the absence of audit, nominating and compensation committees comprised of at least a majority of independent directors, decisions concerning matters such as compensation packages to our senior officers and recommendations for director nominees may be made by a majority of directors who have an interest in the outcome of the matters being decided. Although we intend to bolster our corporate governance during fiscal 2014 as funds are available therefor, prospective investors should bear in mind our current lack of corporate governance measures in formulating their investment decisions.

| 17 |

RISKS RELATING TO OUR COMMON STOCK

OUR COMMON STOCK HAS EXPERIENCED ONLY LIMITED TRADING.

Our common stock is quoted on the over-the-counter markets under the name "Discovery Energy Corp." and the symbol "DENR". Previously, our common stock was quoted on the OTC Bulletin Board under the name "Santos Resource Corp." and the symbol "SANZ". The volume of trading of our common stock has been extremely limited. There can be no assurance as to the prices at which the shares of our common stock will trade in the future. Until shares of our common stock become more broadly held and orderly markets develop and even thereafter, the prices of our common stock may fluctuate significantly. Prices for our common stock will be determined in the marketplace and may be influenced by many factors, including the following:

| * | The depth and liquidity of the markets for our common stock; |

| * | Investor perception of us and the industry in which we participate; |

| * | General economic and market conditions; |

| * | Responses to quarter-to-quarter variations in operating results; |

| * | Failure to meet securities analysts' estimates; |

| * | Changes in financial estimates by securities analysts; |

| * | Conditions, trends or announcements in the oil and gas industry; |

| * | Announcements of significant acquisitions, strategic alliances, joint ventures or capital commitments by us or our competitors; |

| * | Additions or departures of key personnel; |

| * | Sales of our common stock; |

| * | Accounting pronouncements or changes in accounting rules that affect our financial statements; and |

| * | Other factors and events beyond our control. |

The market price of our common stock could experience significant fluctuations unrelated to our operating performance. As a result, a stockholder (due to personal circumstances) may be required to sell such stockholder's shares of our common stock at a time when our stock price is depressed due to random fluctuations, possibly based on factors beyond our control.

FUTURE SALES OF OUR SHARES IN SIGNIFICANT VOLUMES COULD ADVERSELY AFFECT US.

Presently, 138,295,500 shares of our common stock are issued and outstanding. We believe that until recently few of these shares were eligible for public sale. However, because of the passage of time, we now believe that nearly all of these shares are either now or will soon be eligible for public sale. Most of these shares will have become eligible for public sale only recently. Accordingly, we cannot now determine the effect that the recently acquired eligibility of these shares for public sale will have on the market price of these shares or on us. However, the sale of a large number of these shares may dilute an investor's percentage of freely tradable shares, may have a depressive effect on the price of our common stock, and might also adversely affect our ability to raise additional equity capital

| 18 |

THE TRADING PRICE OF OUR COMMON STOCK MAY ENTAIL ADDITIONAL REGULATORY REQUIREMENTS, WHICH MAY NEGATIVELY AFFECT SUCH TRADING PRICE.

The trading price of our common stock historically has been below $5.00 per share. As a result of this price level, trading in our common stock is subject to the requirements of certain rules promulgated under the Securities Exchange Act of 1934, as amended. These rules require additional disclosure by broker-dealers in connection with any trades generally involving any non-NASDAQ equity security that has a market price of less than $5.00 per share, subject to certain exceptions. Such rules require the delivery, before any penny stock transaction, of a disclosure schedule explaining the penny stock market and the risks associated therewith, and impose various sales practice requirements on broker-dealers who sell penny stocks to persons other than established customers and accredited investors (generally institutions). For these types of transactions, the broker-dealer must determine the suitability of the penny stock for the purchaser and receive the purchaser's written consent to the transaction before sale. The additional burdens imposed upon broker-dealers by such requirements may discourage broker-dealers from effecting transactions in our common stock. As a consequence, the market liquidity of our common stock could be severely affected or limited by these regulatory requirements.

PROVISIONS OF OUR CERTIFICATE OF INCORPORATION AND BYLAWS MAY DELAY OR PREVENT A TAKEOVER, WHICH MAY NOT BE IN THE BEST INTERESTS OF OUR SHAREHOLDERS.

Provisions of our First Amended and Restated Articles of Incorporation and Bylaws may be deemed to have anti-takeover effects, which include when and by whom special meetings of our shareholders may be called, and may delay, defer or prevent a takeover attempt. In addition, our First Amended and Restated Articles of Incorporation authorizes the issuance of up to 10,000,000 shares of preferred stock with such rights and preferences, as may be determined by our board of directors. Of this authorized preferred stock, no shares are currently issued and outstanding. Our board of directors may, without shareholder approval, issue up to 10,000,000 preferred stock with dividends, liquidation, conversion or voting rights that could adversely affect the voting power or other rights of our common shareholders.

STOCKHOLDERS HAVE NO GUARANTEE OF DIVIDENDS.

The holders of our common stock are entitled to receive dividends when, as and if declared by the Board of Directors out of funds legally available therefore. To date, we have paid no cash dividends. The Board of Directors does not intend to declare any dividends in the foreseeable future, but instead intends to retain all earnings, if any, for use in our business operations. If we obtain additional financing, our ability to declare any dividends will probably be limited contractually.

Item 1B. Unresolved Staff Comments.

Not applicable.

Item 2. Properties.

We maintain our principal executive offices at One Riverway Drive, Suite 1700, Houston, Texas 77056 through an office rental package on essentially a month-to-month basis. Management believes that any needed additional or alternative office space can be readily obtained.

For information about our oil and gas property, see "Item 1 - Business" above.

Item 3. Legal Proceedings.

We are not presently a party to any pending legal proceeding.

Item 4. Mine Safety Disclosures.

Not applicable.

| 19 |

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is quoted in the over-the-counter markets under the name "Discovery Energy Corp." and the symbol "DENR". Previously, our common stock was quoted on the OTC Bulletin Board under the name "Santos Resource Corp." and the symbol "SANZ". Set forth below are the ranges of closing prices of our common stock for the periods indicated, as reported in the over-the-counter markets. The market quotations reflect inter-dealer prices, without retail mark-up, mark-down or commissions and may not necessarily represent actual transactions. Our common stock began trading on June 15, 2009. The following table reports high and low closing prices, on a quarterly basis, for our common stock within the two most recent fiscal years:

| Common Stock | ||||||||

| 2012 | High | Low | ||||||

| First Quarter | $ | .155 | $ | .155 | ||||

| Second Quarter | $ | .155 | $ | .155 | ||||

| Third Quarter | $ | .155 | $ | .155 | ||||

| Fourth Quarter | $ | .155 | $ | .155 | ||||

| Common Stock | ||||||||

| 2013 | High | Low | ||||||

| First Quarter | $ | .20 | $ | .155 | ||||

| Second Quarter | $ | .20 | $ | .20 | ||||

| Third Quarter | $ | .20 | $ | .20 | ||||

| Fourth Quarter | $ | .45 | $ | .45 | ||||

As of May 17, 2013, we had 68 common shareholders of record and 138,295,500 common shares outstanding.

We have not paid any cash dividends on our common stock, and we do not intend to pay any dividends for the foreseeable future.

Between November 30, 2012 and the date of this Report, we issued shares of our common stock in two private transaction. The first issuance involved the conversion of a short-term convertible promissory note having a principal balance of $25,000 into 300,000 shares of our common stock. The issuances of these shares is claimed to be exempt pursuant to Regulation S under the Securities Act of 1933 (the “Securities Act”). The offer or sale is made only to one person (who was not a "U.S. person") in an "offshore transaction," no "directed selling efforts" were made in the United States, and "offering restrictions" were implemented (each of the preceding terms in quotation marks being defined in Regulation S).

The second issuance involved the private placement of 4.0 million of our shares for a purchase price of $500,000. This issuance of shares is claimed to be exempt pursuant to Rule 506 of Regulation D under the Securities Act. No advertising or general solicitation was employed in offering these securities. The offering and sale was made only to one accredited investor, and subsequent transfers were restricted in accordance with the requirements of the Securities Act.

| 20 |

Equity Compensation Plans

We have one equity compensation plan for our directors, officer, employees and consultants pursuant to which options, rights or shares may be granted or issued. This plan is named the “Discovery Energy Corp. 2012 Equity Incentive Plan” (the “Plan”). Information on the material terms of the Plan is given below. The following table provides information as of February 28, 2013 with respect to our compensation plans (including individual compensation arrangements), under which securities are authorized for issuance aggregated as to (i) compensation plans previously approved by stockholders, and (ii) compensation plans not previously approved by stockholders:

Equity Compensation Plan Information

| Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted- average | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) | ||||||||||

| Plan category | (a) | (b) | (c) | |||||||||

| Equity compensation plans approved by security holders | -0- | -0- | -0- | |||||||||

| Equity compensation plans not approved by security holders | -0- | -0- | 5,853,000 | |||||||||

| Total | -0- | -0- | 5,853,000 | |||||||||

The following is a description of the material features of the Plan: