Attached files

| file | filename |

|---|---|

| 8-K - 8-K - SunCoke Energy, Inc. | d526843d8k.htm |

| EX-99.1 - EX-99.1 - SunCoke Energy, Inc. | d526843dex991.htm |

Q1 2013

Earnings Conference Call

April 25, 2013

Exhibit 99.2 |

Forward-Looking Statements

1

This slide presentation should be reviewed in conjunction with the First Quarter 2013 earnings

releases of SunCoke Energy, Inc. (SunCoke) and SunCoke Energy Partners, L.P.

(Partnership) and the conference call held on April 25, 2013 at 10:00 a.m. ET.

Some of the information included in this presentation constitutes “forward-looking

statements” as defined in Section 27A of the Securities Act of 1933, as amended and

Section 21E of the Securities Exchange Act of 1934, as amended. All statements in this presentation that express

opinions, expectations, beliefs, plans, objectives, assumptions or projections with respect to

anticipated future performance of SunCoke or the Partnership, in contrast with

statements of historical facts, are forward-looking statements. Such forward-looking statements are based on

management’s beliefs and assumptions and on information currently available.

Forward-looking statements include information concerning possible or assumed

future results of operations, business strategies, financing plans, competitive position, potential growth opportunities,

potential operating performance improvements, the effects of competition and the effects of

future legislation or regulations. Forward-looking statements include all

statements that are not historical facts and may be identified by the use of forward-looking terminology such as the words

“believe,” “expect,” “plan,” “intend,”

“anticipate,” “estimate,” “predict,” “potential,” “continue,” “may,” “will,” “should” or the negative of these

terms or similar expressions. Although

management believes that its plans, intentions and expectations reflected in or suggested by the forward-looking statements made in

this presentation are reasonable, no assurance can be given that these plans, intentions or

expectations will be achieved when anticipated or at all. Moreover, such

statements are subject to a number of assumptions, risks and uncertainties. Many of these risks are beyond the control of

SunCoke and the Partnership, and may cause actual results to differ materially from those

implied or expressed by the forward-looking statements. Each of SunCoke and

the Partnership has included in its filings with the Securities and Exchange Commission cautionary language

identifying important factors (but not necessarily all the important factors) that could cause

actual results to differ materially from those expressed in any forward-looking

statement. For more information concerning these factors, see the Securities and Exchange Commission filings

of SunCoke and the Partnership. All forward-looking statements included in this

presentation are expressly qualified in their entirety by such cautionary

statements. Although forward-looking statements are based on current beliefs and expectations, caution should be taken not to

place undue reliance on any such forward-looking statements because such statements speak

only as of the date hereof. SunCoke and the Partnership do not have any intention

or obligation to update publicly any forward-looking statement (or its associated cautionary language)

whether as a result of new information or future events or after the date of this

presentation, except as required by applicable law.

This presentation includes certain non-GAAP financial measures intended to supplement, not

substitute for, comparable GAAP measures. Reconciliations of non-GAAP financial

measures to GAAP financial measures are provided in the Appendix at the end of the presentation.

Investors are urged to consider carefully the comparable GAAP measures and the reconciliations

to those measures provided in the Appendix. |

SUNCOKE ENERGY,

INC. RESULTS |

Q1 2013

Highlights 3

•

Executed SunCoke Energy Partners initial public offering

–

Declared

first

quarterly

cash

distribution

prorated

for

the

date

of

the

IPO

–

Currently

expect

to

increase

quarterly

distribution

by

~2.5%

for

next

quarter and anticipate an overall increase of ~7% for the Q4 2013

distribution to be paid in early 2014

•

Completed VISA SunCoke JV, marking our entry to India

–

Invested $67.7 million for a 49% stake

•

Delivered improved coke performance driven by Middletown

facility

•

Improved coal productivity and reduced cash costs

•

Ended quarter with substantial financial flexibility

–

~$200 million cash attributable to SXC at quarter-end after India

investment, and $106 million of cash at SXCP

Photo courtesy of VISA Steel |

Q1 2013

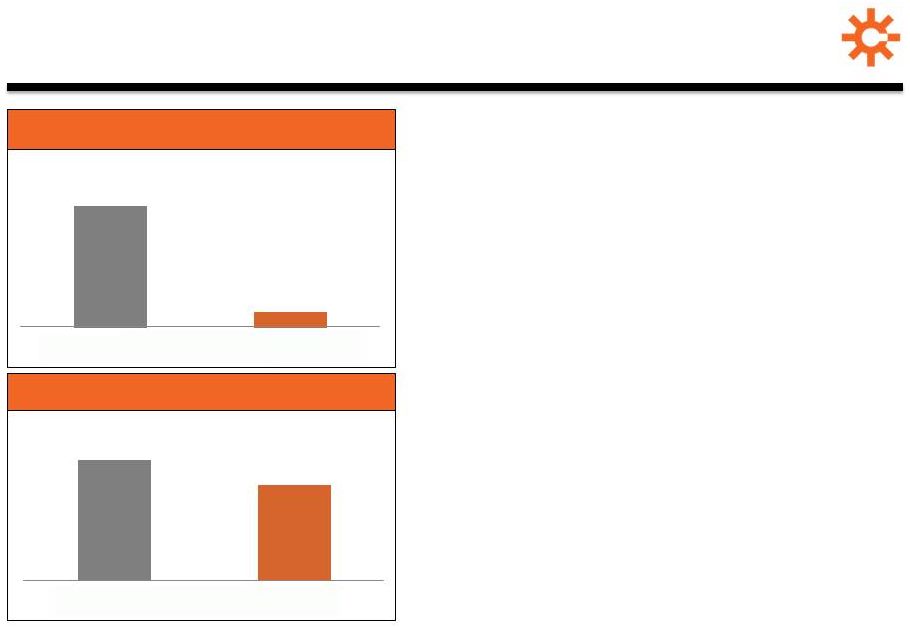

Earnings Overview Q1 2013 EPS of $0.03 reflects

•

Challenging coal price environment

•

Accelerated depreciation expense at

Indiana Harbor

•

($0.10) EPS impact related to debt

issuance costs and unfavorable tax items

•

Income attributable to SXCP public

holders ($0.07) in 2013

Adjusted EBITDA down on coal mining

segment performance, partially offset by

improved cokemaking results

Reaffirm 2013 consolidated Adjusted

EBITDA and EPS guidance of $205 million -

$230 million and $0.30 -

$0.55

(1)

For a definition and reconciliation of Adjusted EBITDA, please see appendix.

4

$0.24

$0.03

Q1 2012

Q1 2013

Earnings Per Share

(diluted)

$55.5

$52.3

Q1 2012

Q1 2013

Adjusted EBITDA

(1)

(in millions) |

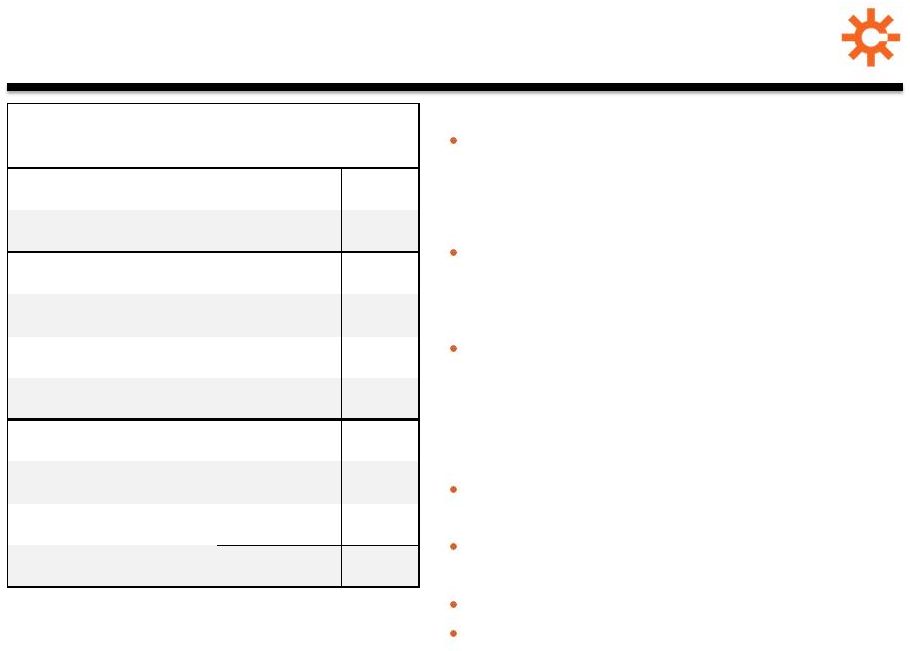

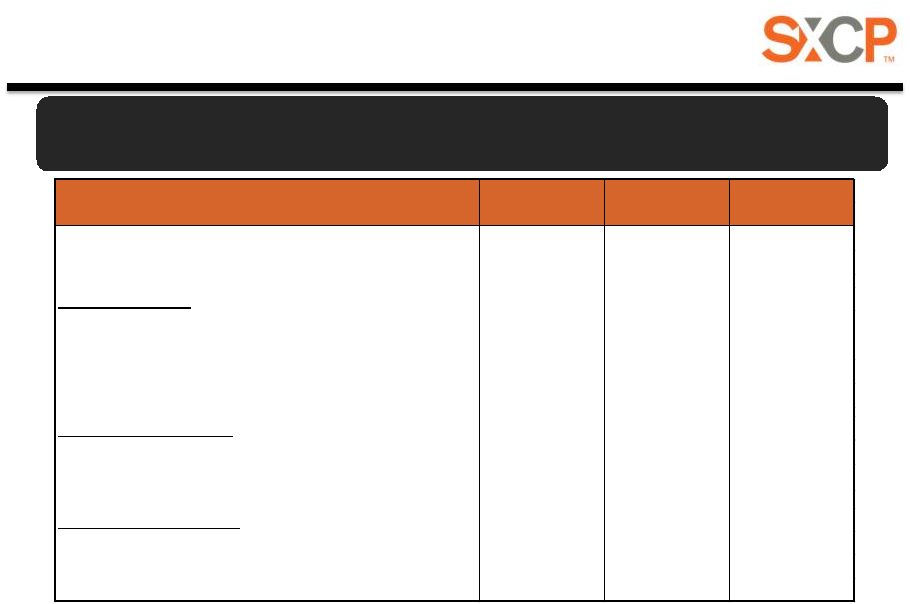

Q1 2013 Financial

Results (1) Coke Adjusted EBITDA includes Domestic Coke and International

segments. (2) For a definition and reconciliation of Adjusted EBITDA and Adjusted EBITDA

per ton, please see appendix.

($ in millions)

Q1'13

Q1'12

Q1'13

vs.

Q1'12

Domestic Coke Sales Volumes

1,058

1,078

(20)

Coal Sales Volumes

373

373

-

Revenue

$453.9

$481.3

($27.4)

Operating Income

$27.0

$33.9

($6.9)

Net Income Attributable to

Shareholders

$2.1

$16.9

($14.8)

Earnings Per Share

$0.03

$0.24

($0.21)

Coke Adjusted EBITDA

(1)

$62.7

$54.9

$7.8

Coal Adjusted EBITDA

(2)

($4.6)

$7.4

($12.0)

Corporate/Other

($5.8)

($6.8)

$1.0

Adjusted EBITDA

(2)

$52.3

$55.5

($3.2)

5

Reflects impact of lower coal prices in

coke and coal segments

Coke business performed well, led by

Middletown, which increased

$8.8 million

Coal weakness driven by $50/ton yr/yr

decline in prices, partially offset by

lower cash production costs

Accelerated depreciation at Indiana

Harbor ($0.06)

Write-off of unamortized debt issuance

costs and debt-related fees ($0.05)

Unfavorable tax items ($0.05)

Income attributable to SXCP public

holders in 2013 ($0.07)

Revenues lower by 5.7%

Adjusted EBITDA down 5.8%

EPS decline to $0.03 reflects |

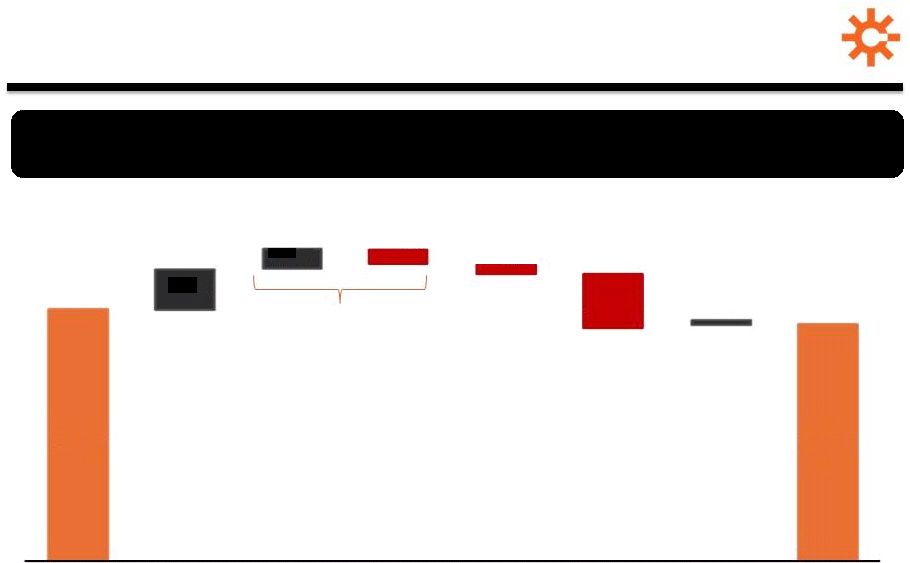

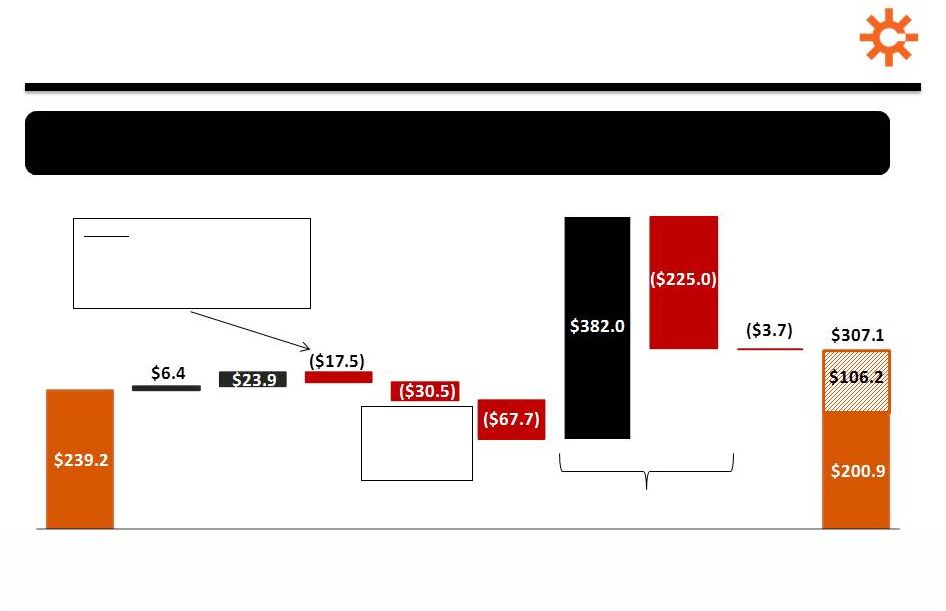

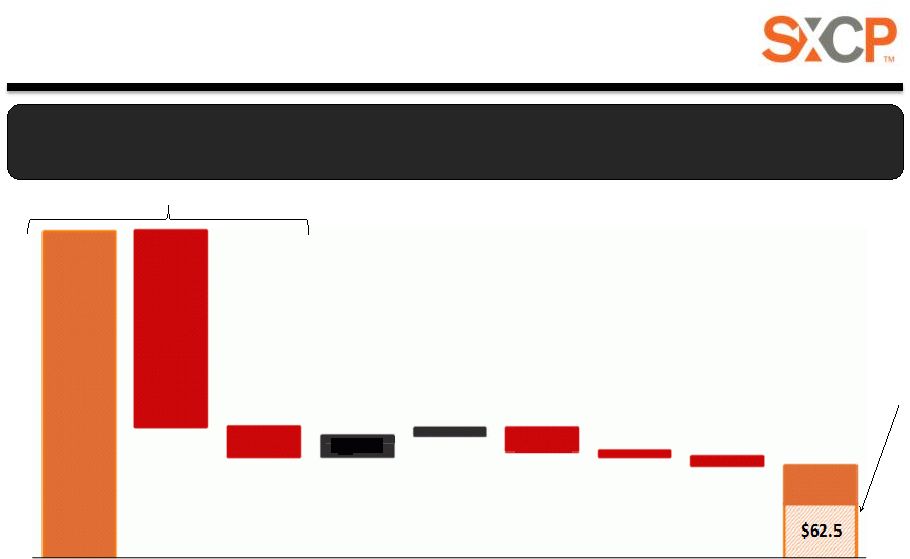

Adjusted

EBITDA (1)

Bridge –

Q1 ‘12 to Q1 ‘13

Weak coal mining segment results partially offset by

improved coke operations driven by Middletown

($ in millions)

(1)

For a definition and reconciliation of Adjusted EBITDA, please see the appendix

(2)

Includes a $2.8 million charge related to coke inventory reduction and a $1.5 million lower

cost or market adjustment on pad coal inventory at Indiana Harbor in 2012

•

$4.8M better

cost recovery

•

Favorable

comparison to

1Q12’s ($4.0M)

of start-up costs

and yield

performance

•Net

improvement of $1.2M 6

$55.5

$52.3

$8.8

$4.3

$1.0

($3.1)

($2.2)

($12.0)

Q1 2012

Adjusted

EBITDA (1)

Middletown

Indiana

Harbor (non-

recurring)(2)

Indiana

Harbor

Coke Business

(excl.

Middletown &

Indiana Harbor)

Coal Mining

Corporate

Costs

Q1 2013

Adjusted

EBITDA (1) |

Diluted EPS

Bridge – Q1 ‘12 to Q1 ‘13

EPS impacted by higher depreciation costs due to Indiana Harbor

refurbishment and approximately ($0.10) of non-recurring items

(1)

For a definition and reconciliation of Adjusted EBITDA, please see the appendix

$0.24

$0.03

$0.01

($0.02)

($0.02)

($0.06)

($0.05)

($0.07)

Q1 2012 EPS

(Diluted)

EBITDA

Depreciation,

Depletion &

Amortization

Indiana

Harbor

Accelerated

Depreciation

Financing

Costs

Taxes

Net

Income/(Loss)

Attributable

to NCI

Q1 2013 EPS

(Diluted)

Attributable

to SXC

Reflects ($0.05) impact

of unfavorable tax items

7 |

SXC Liquidity

Position Ended quarter with strong cash position and virtually undrawn revolver

even after making ~$68 million VISA SunCoke JV investment

($ in millions)

SXCP IPO transaction

Includes:

8

•

Includes

$16.2M for

Indiana

Harbor

(1)

Reflects timing of payment of a $24.5 million receivable due on the last day of quarter, but

paid first day of next (2)

Includes early payment on $11.8 million of accrued sales discounts

(3)

Excludes $6.5 million in offering expenses paid in 2012 and includes $0.7 million of

fees related to the amendment of SXC credit facility •

Accts

Receivable:

($27.0M)

(1)

•

Inventories: $18.9M

•

Accts Payable: $19.0M

•

Accrued

Liabilities:

($21.4M)

(2)

Q4 2012

Cash

Balance

Q1 2013

Net Income

Depreciation,

Depletion &

Amortization

Working

Capital, Deferred

Taxes & Other

Capital

Expenditures

VISA

SunCoke JV

SXCP Equity &

Debt

Offerings

(net of fees)(3)

SXC Debt

Paydown

Other Cash Used

In Financing

Activities

Q1 2013

Cash

Balance |

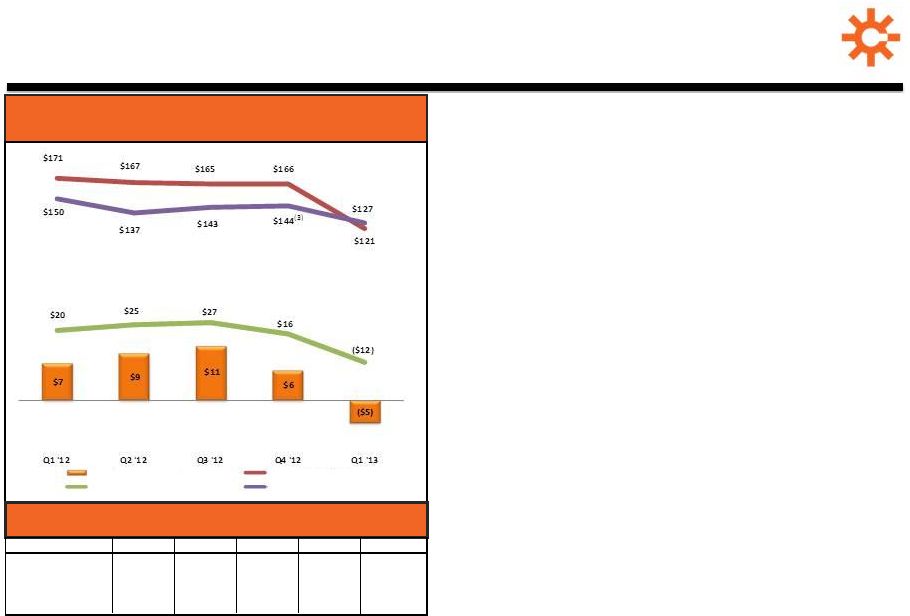

Domestic Coke

Business Summary 9

(1)

For a definition of Adjusted EBITDA and Adjusted EBITDA/Ton and reconciliations, see

appendix.

(2)

Includes a $2.8 million charge related to coke inventory reduction and a $1.5 million lower

cost or market adjustment on pad coal inventory at Indiana Harbor and $4.0 million of

non- recurring startup costs at Middletown.

(3)

Domestic

Coke

Production

Domestic Coke Adjusted EBITDA

(1)

Per Ton

Overall cokemaking business performed well, delivering

Adjusted EBITDA per ton of $58 in first quarter

(Tons in thousands)

($ in millions, except per ton amounts)

Includes $4.2 million favorable adjustment at Indiana Harbor due

to finalization of 2011 billing review. Jewell

Indiana Harbor

Haverhill

Granite City

Middletown

Domestic Coke Segment

Adjusted EBITDA/ton |

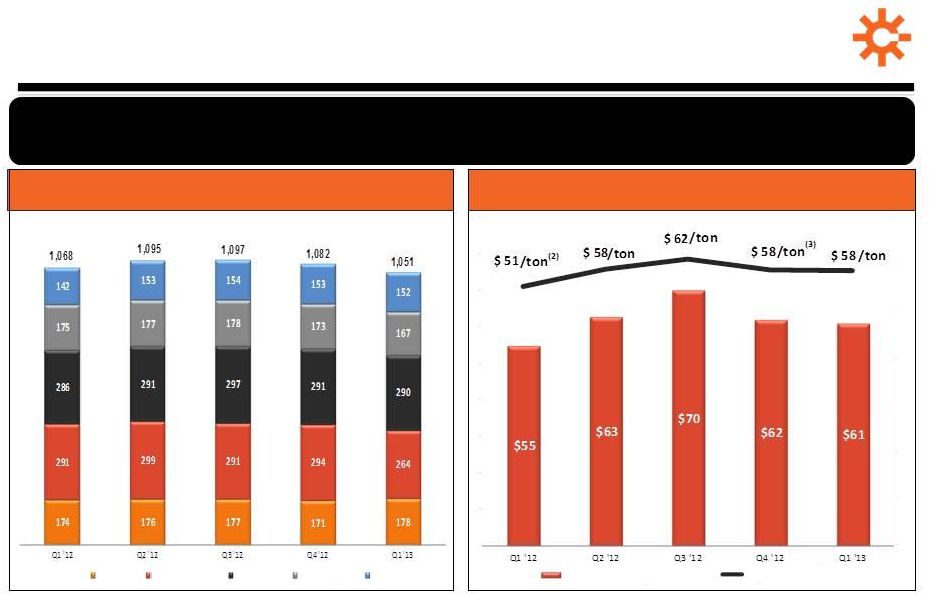

Coal Mining

Financial Summary Q1 2013 Adjusted EBITDA down

$12 million from Q1 2012

•

Driven by $50 decline in average sales price

•

Sales volume flat

Delivered significant improvement in

per ton cash production costs

•

Jewell underground costs down sequentially

and yr/yr

–

$129 in Q1 2013; $149

(3)

in Q4 2012;

$159 in Q1 2012

Coal action plan progress

•

Rationalized mining plans, idled mines and

reduced headcount

•

Upgraded equipment and training programs

•

Installed new cyclone system at prep plant

Expect Coal Mining segment to

deliver FY 2013 Adjusted EBITDA of

$0 –

($15) million; consistent with

guidance

Coal Mining Adjusted EBITDA

(1)

and Avg. Sales

Price/Ton

(2)

($ in millions, except per ton amounts)

(1)

(2)

(3)

Coal Sales, Production and Purchases

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Coal Sales

373

365

392

371

373

Coal Production

375

401

349

351

349

Purchased Coal

19

4

10

9

18

Reject Rate (%)

68

66

67

66

66

10

Coal Adjusted EBITDA

Average Sales Price

Coal Adj EBITDA / ton

Coal Cash Cost / ton

For a definition and a reconciliation of Adjusted EBITDA, please see the appendix. Avg.

Sales Price is weighted avg. price for all sales, including to affiliates and Jewell Coke.

Excludes Black Lung liability charge of $0.8 million and accrued potential fines and

penalties of $1.5 million. |

SUNCOKE ENERGY

PARTNERS, LP RESULTS |

SXCP Q1

2013 Financial Results Sustained solid results at Middletown and Haverhill

provide a strong platform for future growth

n/a -

Not applicable

* -

Proforma Jan 1-Mar 31, 2013 for offerings completed on January 24, 2013

12

Q1'13

Q1'12

Q1'13 vs Q1'12

($ in millions except where noted)

Actual

Actual

Change

Coke Production (in '000s of tons)

442

428

14

Coke Sales Volumes (in '000s of tons)

448

424

24

Financial Results:

Revenues

184.9

$

176.7

$

8.2

$

Operating Income

34.5

$

20.3

$

14.2

$

Net Income

(1)

23.9

$

12.4

$

11.5

$

Net Income attributable to SXCP

(1)

15.3

$

12.4

$

2.9

$

Profitability Measures:

Proforma* Adjusted EBITDA attributable to SXCP

(2)

26.5

$

n/a

-

Proforma* Adj. EBITDA per ton attributable to SXCP

(2)

91.19

$

n/a

-

Distributable Cash Flow

Proforma* Distributable Cash Flow

(2)

22.0

$

n/a

-

Minimum Quarterly Cash Distribution

13.2

$

n/a

-

Distribution Coverage Ratio

1.66x

n/a

-

(1)

Reflects impact of local income taxes

(2)

For a definition and related reconciliations of Adjusted EBITDA, Adjusted EBITDA/Ton and

Distributable Cash Flow, please see appendix |

SXCP Liquidity

Position Reserved for

environmental

remediation

A solid cash balance and undrawn $100 million revolver provide SXCP the

flexibility to seize potential new growth opportunities

•

Ongoing CapEx:

($1.2M)

•

Pre-funded

environmental

remediation:

($4.5M)

Includes

settlement of

accrued sales

discounts

($11.8M)

SXCP IPO transaction

13

$376.1

$23.9

$7.6

($225.0)

($33.1)

($25.8)

($5.7)

($11.8)

$43.7

SXCP Equity &

Debt Offering,

Net of Fees

Debt

Paydown

Distributions

to SXC from IPO

Q1 2013

Net Income

Depreciation,

Depletion &

Amortization

Working

Capital Changes

/ Other

Capital

Expenditures

Cash

Distribution to

SXC (for 35%

post-IPO)

Q1 2013

Cash

Balance

$106.2 |

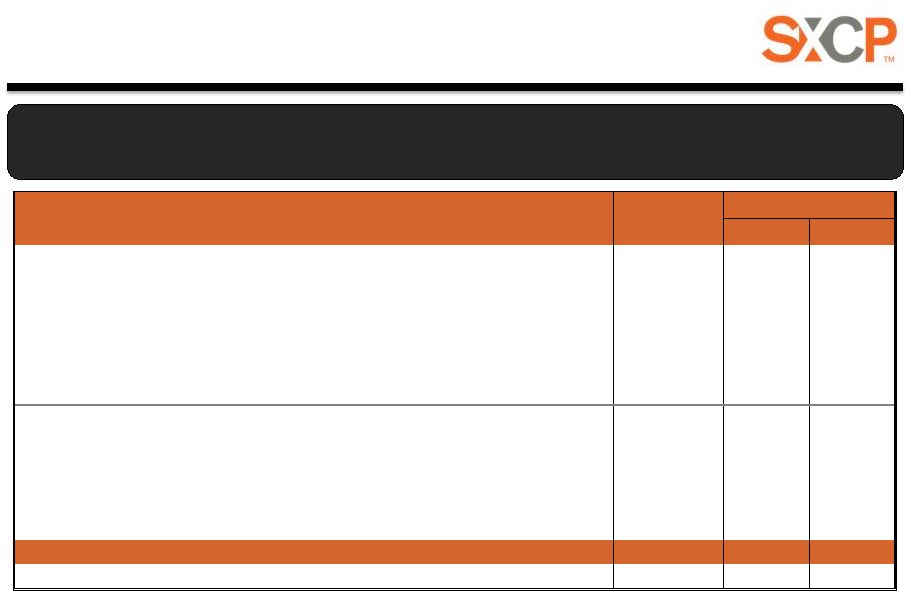

SXCP Updated

2013 Outlook (1)

Adjusted EBITDA equals SXCP’s 65% interest in Haverhill and Middletown’s Adjusted

EBITDA (i.e., 65% net income attributable to the controlling and noncontrolling interests plus depreciation

expense, interest expense, incremental public partnership expenses, and incremental corporate

expenses allocated to the MLP). (2)

Total unit coverage ratio calculated as cash available for distribution divided by total

distributions at the minimum distribution rate of $52.9 million. 14

Based on solid operating performance and outlook, we have increased our

Adjusted EBITDA and cash distribution coverage expectations for 2013

Prospectus

Revised 2013 Outlook

($ and units in millions, except per unit data)

2013 Forecast

High

Low

Adjusted EBITDA attributable to SXCP

(1)

$88.3

$93.0

$88.3

Less:

Cash interest ($150 million senior notes @ 7.375% plus $0.5 million revolver commitment

fee) 11.6

11.6

11.6

Accrual for replacement capital expenditures

3.7

3.7

3.7

Ongoing capital expenditures (65% share of Haverhill and Middletown attributable to

SXCP) 9.1

9.1

9.1

Public partnership expense

2.5

2.5

2.5

Estimated Distributable Cash Flow

$61.4

$66.1

$61.4

Excess distributable cash flow available for distribution

8.5

13.2

8.5

Total estimated minimum annual distribution

$52.9

$52.9

$52.9

Minimum annual distribution per unit

$1.65

$1.65

$1.65

Total unit coverage ratio

(2)

1.16x

1.25x

1.16x |

SXCP

Distribution Growth Outlook 15

•

Declared initial quarterly cash distribution of $0.3071

–

Reflects proration of the $0.4125 minimum quarterly distribution

rate for the January 24, 2013 closing of the IPO

•

Given confidence in current outlook, expect to increase

quarterly cash distribution rate

–

Currently expect to increase quarterly cash distribution by ~2.5% for

next quarter and anticipate an overall increase of ~7% for the Q4

2013 distribution to be paid in early 2014 |

2013 OUTLOOK

& PRIORITIES |

SXC: 2013

Guidance Summary Metric

Revised Guidance: 2013

Post SXCP IPO

Adjusted EBITDA

(1)

Consolidated

Attributable to SXC Shareholders

$205 –

$230 million

$165 –

$190 million

EPS Attributable to SXC Shareholders

(diluted)

$0.30 –

$0.55

Cash Flow from Operations

~$140 million

(3)

Capital Expenditures and Investments

(2)

~ $200 million

Effective Tax Rate

14% –

20%

Cash Tax Rate

12% –

20%

Domestic Coke Production

4.3+ million tons

Coal Production

~ 1.4 million tons

(1)

For a reconciliation of 2013E Adjusted EBITDA, please see reconciliation on slide 27

(2)

See appendix for details

(3)

Includes ~$38 million of sales discounts payable to customers of which ~$12million is

pre-funded at SXCP with IPO proceeds 17

Prior range

7-14% |

2013

Priorities Operational Excellence

Operational Excellence

•

Sustain momentum at coke

facilities

•

Execute Indiana Harbor Plan

•

Execute refurbishment

•

Resolve NOV

•

Renew coke contract

with return on

refurbishment capital

•

Implement environmental

project at Haverhill and

Granite City

•

Execute coal mining action

plan to decrease cash cost

•

Maintain top quartile safety

performance

Grow The Coke

Grow The Coke

Business

Business

•

Domestic

•

Obtain permit for next

potential U.S. facility

•

Identify and pursue

strategic acquisition

opportunities in the U.S.

and Canada

•

Evaluate adjacent business

lines to extend growth

opportunities

•

International

•

Closed VISA SunCoke joint

venture transaction

•

Identify potential follow-on

opportunities in India

Strategically Optimize

Strategically Optimize

Assets

Assets

•

SXCP

•

Achieve smooth launch,

governance and operation

of SXCP

•

Coal

•

Reposition mining

operations for near-term

weakness and long-term

strategic flexibility

•

Efficient Capital Allocation

•

Put SXC and SXCP balance

sheets to work

18 |

North America

M&A Growth Strategy FOCUS

Acquisition of existing

cokemaking facilities with long-

term off take agreements

FOCUS

Selective acquisition of met coal

related handling & processing

assets, with long-term off take

agreements and limited

commodity exposure

FOCUS

Investment in ferrous side of

steel value chain (concentrating,

pelletizing, transport/handling)

19

•

•

•

•

•

•

•

•

•

Cokemaking

Cokemaking

Coal Handling/

Coal Handling/

Processing

Processing

Iron Ore Processing

Iron Ore Processing

First priority for core

business

Opportunistic

acquisitions of

adjacent assets

Evaluation for future

value chain expansion

Customer concentration likely

to remain high

Degree of integration in steel

operations and environmental

issues will impact complexity

and timing of transaction

In active discussion with

owners of targeted assets

Potential to add value to core

business and diversify

customer base

Current opportunities available

and less complex assets implies

potentially shorter deal cycle

Initiated discussions with

potential parties

Potential to diversify customer

base and enhance value-add

to steel industry

Potential to deploy tolling/pass

through model

Researching qualifying income

status and market opportunity |

QUESTIONS |

www.suncoke.com

Investor Relations:

630-824-1907 |

APPENDIX

|

•

Adjusted

EBITDA

represents

earnings

before

interest,

taxes,

depreciation,

depletion

and

amortization

(“EBITDA”)

adjusted

for

sales

discounts

and

the

interest,

taxes,

depreciation,

depletion

and

amortization

attributable

to

equity

earnings

in

our

unconsolidated

affiliates.

EBITDA

reflects

sales

discounts

included

as

a

reduction

in

sales

and

other

operating

revenue.

The

sales

discounts represent the sharing with customers of a portion of nonconventional fuel

tax credits, which reduce our income tax expense.

However, we believe our Adjusted EBITDA would be inappropriately penalized if

these discounts were treated as a reduction

of

EBITDA

since

they

represent

sharing

of

a

tax

benefit

that

is

not

included

in

EBITDA.

Accordingly,

in

computing

Adjusted

EBITDA,

we

have

added

back

these

sales

discounts.

Our

Adjusted

EBITDA

also

includes

EBITDA

attributable

to

our

unconsolidated affiliates. EBITDA and Adjusted EBITDA do not represent and

should not be considered alternatives to net income or operating income

under GAAP and may not be comparable to other similarly titled measures in other businesses. Adjusted

EBITDA does not represent and should not be considered as an alternative to net

income as determined by GAAP, and calculations thereof may not be comparable

to those reported by other companies. We believe Adjusted EBITDA is an important measure of

operating performance and provides useful information to investors because it

highlights trends in our business that may not otherwise be apparent when

relying solely on GAAP measures and because it eliminates items that have less bearing on our

operating

performance.

Adjusted

EBITDA

is

a

measure

of

operating

performance

that

is

not

defined

by

GAAP

and

should

not

be

considered a substitute for net (loss) income as determined in accordance with

GAAP. •

Adjusted

EBITDA

attributable

to

SXC/SXCP

equals

Adjusted

EBITDA

less

Adjusted

EBITDA

attributable

to

noncontrolling

interests.

•

Adjusted

EBITDA/Ton

represents

Adjusted

EBITDA

divided

by

tons

sold.

When

applicable

to

Adjusted

EBITDA

attributable

to

SXC or SXCP, tons sold are prorated according to the respective ownership interest

of SXC or SXCP as applicable. Definitions

23 |

•

Distributable

Cash

Flow

equals

Adjusted

EBITDA

less

net

cash

paid

for

interest

expense,

on-going

capital

expenditures,

accruals

for replacement capital expenditures, and cash distributions to noncontrolling

interests. Distributable Cash Flow is a non-GAAP supplemental

financial measure that management and external users of the Partnership's financial statements, such as industry

analysts, investors, lenders, and rating agencies, use to assess:

•

the Partnership's operating performance as compared to other publicly traded

partnerships, without regard to historical cost basis;

•

the ability of the Partnership's assets to generate sufficient cash flow to make

distributions to the Partnership's unitholders; •

the Partnership's ability to incur and service debt and fund capital expenditures;

and •

the viability of acquisitions and other capital expenditure projects and the

returns on investment of various investment opportunities.

The Partnership believes that Distributable Cash Flow provides useful information

to investors in assessing the Partnership's financial condition and results

of operations. Distributable Cash Flow should not be considered an alternative to net income, operating income,

cash flows from operating activities, or any other measure of financial performance

or liquidity presented in accordance with generally accepted accounting

principles (GAAP). Distributable Cash Flow has important limitations as an analytical tool because it excludes

some, but not all, items that affect net income and net cash provided by operating

activities and used in investing activities. Additionally, because

Distributable Cash Flow may be defined differently by other companies in the industry, the Partnership's

definition of Distributable Cash Flow may not be comparable to similarly titled

measures of other companies, thereby diminishing their utility.

Definitions

24 |

Reconciliations

$ in millions

Q1 2013

FY 2012

Q4 2012

Q3 2012

Q2 2012

Q1 2012

FY 2011

Q4 2011

Q3 2011

Q2 2011

Q1 2011

Net Income

6.4

102.5

29.0

32.9

24.0

16.6

58.9

7.5

21.6

24.1

5.7

Subtract: Depreciation, depletion

and amortization

(23.9)

(80.8)

(23.3)

(18.9)

(20.2)

(18.4)

(58.4)

(16.0)

(14.7)

(14.7)

(13.0)

Subtract: Interest expense, net

(15.8)

(47.8)

(11.8)

(12.2)

(11.8)

(12.0)

(1.4)

(7.1)

(3.3)

4.5

4.5

Subtract: Income Tax

(4.8)

(23.4)

(3.5)

(7.6)

(7.0)

(5.3)

(7.2)

2.9

(5.1)

(1.9)

(3.1)

EBITDA

50.9

254.5

67.6

71.6

63.0

52.3

125.9

27.7

44.7

36.2

17.3

Add: Sales Discount

1.4

11.2

2.1

2.1

3.8

3.2

12.9

3.2

3.5

3.1

3.1

Add: Adjustment to

unconsolidated affiliate earnings

-

-

-

-

-

-

-

-

-

-

-

Adjusted EBITDA

52.3

265.7

69.7

73.7

66.8

55.5

138.8

30.9

48.2

39.3

20.4

Adjusted EBITDA attributable to

noncontrolling interests

(8.4)

(3.0)

(1.5)

(1.1)

(0.9)

0.5

4.0

0.8

(2.7)

(0.9)

6.8

Adjusted EBITDA attributable to

SXC

43.9

262.7

68.2

72.6

65.9

56.0

142.8

31.7

45.5

38.4

27.2

Reconciliations from Net Income to Adjusted EBITDA

25 |

$ in millions, except

per ton data Domestic

Coke

International

Coke

Jewell

Coal

Corporate

Combined

Q1 2013

Adjusted EBITDA

61.1

1.6

(4.6)

(5.8)

52.3

Sales Volume (thousands of tons)

1,058

216

373

Adjusted EBITDA per Ton

57.8

7.41

(12.3)

FY 2012

Adjusted EBITDA

249.4

11.9

33.4

(29.0)

265.7

Sales Volume (thousands of tons)

4,345

1,209

1,500

Adjusted EBITDA per Ton

57.4

9.8

22.3

Q4 2012

Adjusted EBITDA

62.4

10.2

6.0

(8.9)

69.7

Sales Volume (thousands of tons)

1,077

239

370

Adjusted EBITDA per Ton

57.9

42.7

16.2

Q3 2012

Adjusted EBITDA

69.8

0.9

10.7

(7.7)

73.7

Sales Volume (thousands of tons)

1,116

310

392

Adjusted EBITDA per Ton

62.5

2.9

27.3

Q2 2012

Adjusted EBITDA

62.4

0.7

9.3

(5.6)

66.8

Sales Volume (thousands of tons)

1,074

302

365

Adjusted EBITDA per Ton

58.1

2.3

25.5

Q1 2012

Adjusted EBITDA

54.8

0.1

7.4

(6.8)

55.5

Sales Volume (thousands of tons)

1,078

358

373

Adjusted EBITDA per Ton

50.8

0.3

19.8

Reconciliations of Segment Adjusted EBITDA and Adjusted EBITDA Per Ton

Reconciliations

26 |

2013E

Net

Income

to

Adjusted

EBITDA

Reconciliation

-

SXC

SXC –

Expected 2013E EBITDA Reconciliation

27

(1)

Represents SXC share of India JV interest, taxes and depreciation expense

(2)

Represents Adjusted EBITDA attributable to SXCP public unitholders and to DTE’s interest

in Indiana Harbor (in millions)

2013E

Low

2013E

High

Net Income

$40

$57

Depreciation, Depletion and Amortization

97

95

Total financing costs, net

55

55

Income tax expense

7

14

EBITDA

$199

$221

Sales discounts

6

6

Adjustment to unconsolidated affiliate earnings

(1)

–

3

Adjusted EBITDA

$205

$230

EBITDA attributable to noncontrolling interests

(2)

(40)

(40)

Adjusted EBITDA attributable to SXC

$165

$190 |

28

2013E

Net

Income

to

Adjusted

EBITDA

Reconciliation

-

SXCP

SXCP –

Expected 2013E EBITDA Reconciliation

(1)

Represents Adjusted EBITDA attributable to SXC’s 35% interest in Haverhill and

Middletown facilities (in millions)

2013E

Low

2013E

High

Net Income

79.2

$

89.9

$

Depreciation, Depletion and Amortization

32.0

31.0

Total financing costs, net

17.0

15.0

Income tax expense

4.7

4.7

EBITDA

132.9

$

140.6

$

Sales discounts

(0.6)

(0.6)

Adjusted EBITDA

132.3

$

140.0

$

EBITDA attributable to noncontrolling interest

(1)

(44.0)

(47.0)

Adjusted EBITDA attributable to SXCP

88.3

$

93.0

$ |

2013E Capital

Expenditures and Investments ($ in millions)

SXC

SXCP

Consolidated

On-Going

Approx.

$49

$9

$58

Environmental

Remediation

Approx.

-

$15

$15

Expansion

Approx.

60

-

60

Total CapEx

Approx.

$109

$24

$133

Investments

Approx.

$67

-

$67

Total CapEx &

Investments

Approx.

$176

$24

$200

For Year Ended December 31, 2013

•

Expansion includes approx.

$60m for Indiana Harbor

Refurbishment

•

SXCP expenditures prefunded

from IPO proceeds

•

To fund investment in

India JV (Visa SunCoke)

•

SXC includes approximately

$25m coke and $24m coal

•

SXCP includes 65% of $14m

expected at Haverhill and

Middletown

29 |

Proforma for

period

1/1/2013 -

Proforma

($ in Millions)

Q1'13

1/23/2013

Q1'13

Net cash (used in) provided by operating activities

5.7

$

(0.2)

$

5.5

$

Depreciation

(7.6)

(7.6)

Changes in

working capital and other 25.8

25.8

Net income

23.9

$

23.7

$

Add:

Depreciation

7.6

7.6

Financing expense, net 6.7

6.7

Income tax expense 3.9

3.9

Sales discounts (0.6)

(0.6)

Adjusted EBITDA

41.5

$

41.3

$

Adjusted EBITDA attributable to

NCI (11.4)

(3.4)

(14.8)

Adjusted EBITDA attributable to

Predecessor/SXCP 30.1

$

26.5

$

Less:

On-going capex

(0.7)

(0.7)

Replacement

capex accrual (0.9)

(0.9)

Cash interest

accrual (2.9)

(2.9)

Distributable cash

flow 25.6

$

22.0

$

Minimum Quarterly Cash Distribution

13.2

13.2

Distribution Coverage Ratio

1.94x

1.66x

Adjusted EBITDA per ton reconciliation

Adjusted EBITDA attributable to SXCP

26.5

$

Sales tons attributable to

SXCP 291

Adjusted EBITDA/ton

91.1

$

SXCP –

Adjusted EBITDA and Distributable

Cash Flow Reconciliations

30

(1)

SG&A expense for the time period prior to the January 24, 2013 IPO date (January 1

-23, 2013) (2)

Represents Adjusted EBITDA attributable to SXC’s 35% interest in Haverhill and

Middletown facilities prior to the IPO date (2)

Includes 65% of the total sales tons of Haverhill and Middletown

(1)

(2)

(3) |