Attached files

| file | filename |

|---|---|

| 8-K - 8-K - JONES LANG LASALLE INC | d502522d8k.htm |

Investor Presentation

March 2013

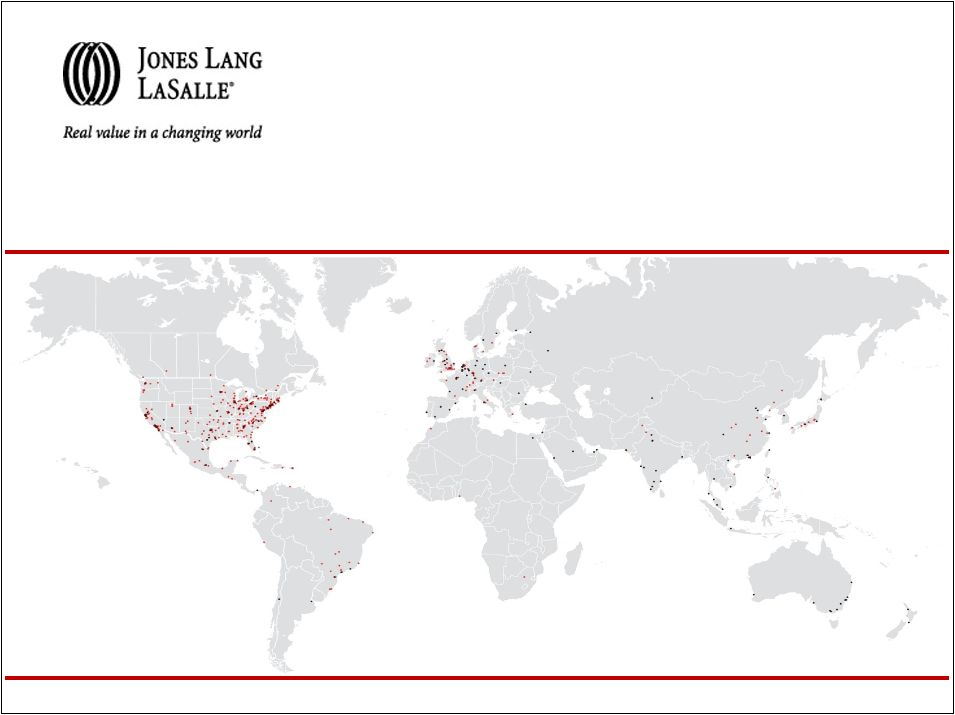

..48,000 employees….200 offices….70 countries….1 global platform..

Exhibit 99.1 |

Table of Contents

I.

Company Description

II.

Global Growth Strategy

III.

Financial Overview

IV.

Appendix

2 |

Company

Description |

Global

real estate services Premier global investment manager

•

LaSalle Investment Management provides outstanding

performance and service for clients with global real estate

investment portfolios

Shareholder opportunity

Jones Lang LaSalle

Shareholder value

2012 Fee Revenue =

$3.6 billion

Value-creating real estate services and investment management firm

•

Investment expertise including core, value-

add, opportunistic and private investing

across major property types

•

More than 300 institutional clients worldwide

•

Leading global markets positions

•

Consolidator in a consolidating industry

•

Productivity and margin expansion

•

Strategic, fully integrated services for real estate

owners, occupiers and investors

•

Productivity and cost solutions for corporate clients

seeking to optimize space and location

•

Industry leader recognized for deep market

knowledge and execution expertise

•

Strong cash-generating business model

•

Revenue growth

•

Investment-grade balance sheet

•

Effective tax and interest expense management

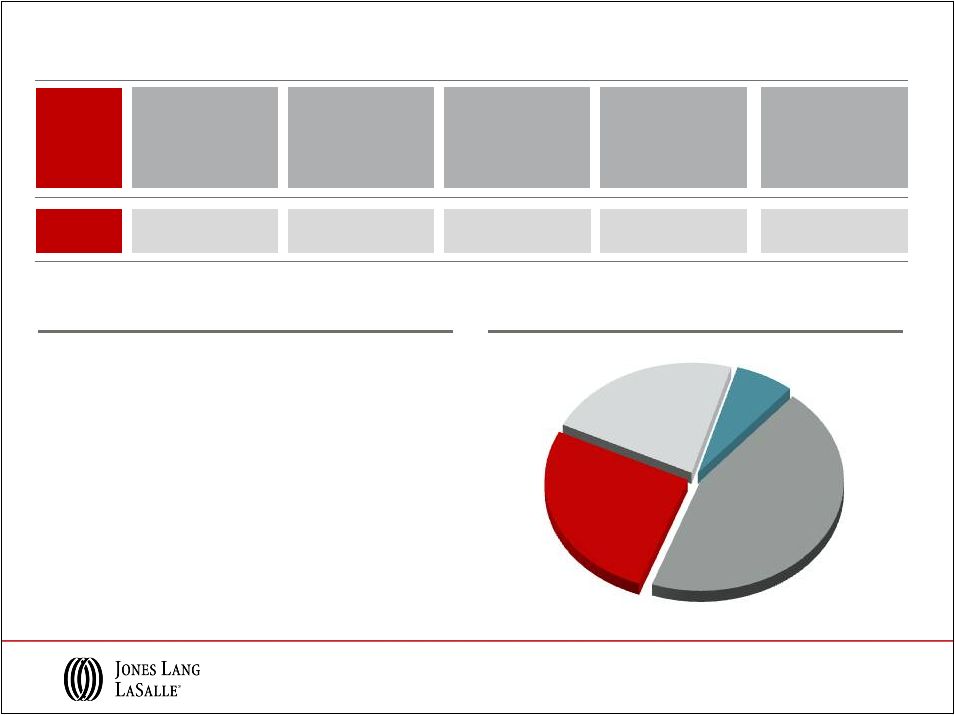

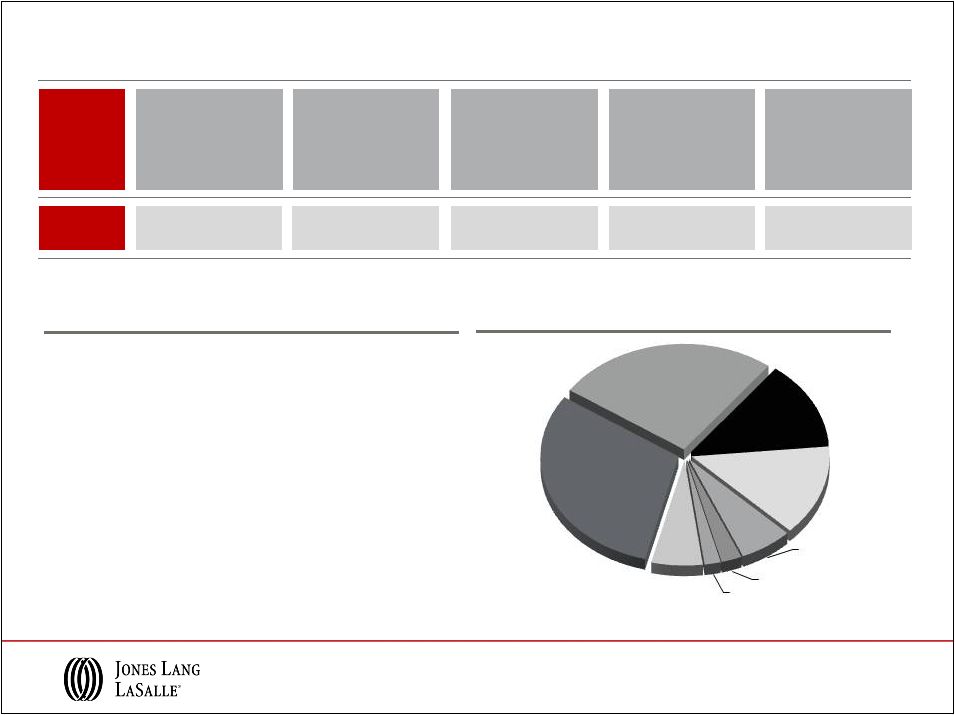

4

Advisory &

10%

Leasing

35%

Capital

Markets

14%

Project &

Development

Services

10%

Property &

Facility Mgmt.

23%

LaSalle Inv.

Mgmt.

7%

Other |

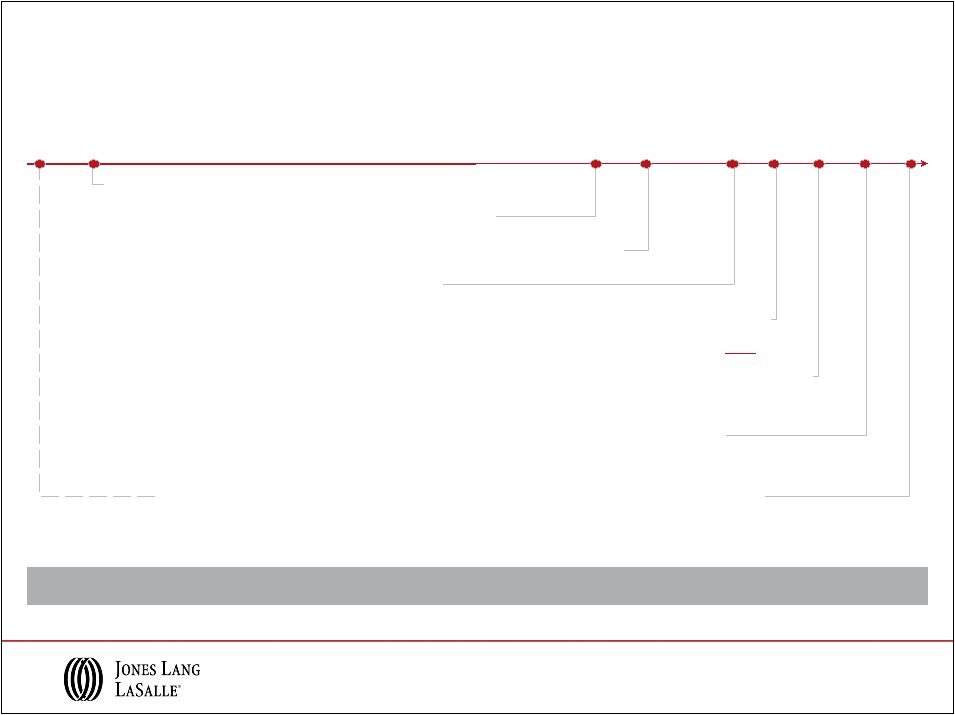

Jones

Lang Wootton founded in London 1783

1968

1997

1999

LaSalle Partners founded, operating primarily in the Americas

LaSalle Partners initial public offering

LaSalle Partners and Jones Lang Wootton merge to create Jones Lang LaSalle

Integrated

global

platform

(NYSE

ticker

“JLL”)

Transformational M&A Extends Market Positions

2011

2008

The Staubach Company and Jones Lang LaSalle combine operations

Largest merger in JLL history transforms U.S. local markets position

King Sturge (est. 1760) and Jones Lang LaSalle merge EMEA operations

Enhances strength and depth of service capabilities in the UK and EMEA

1760

14% compound annual revenue growth rate since 1999 merger between LaSalle Partners and

JLW 1957

Jones Lang Wootton expands into Asia Pacific

2007

Jones Lang LaSalle acquires Meghraj Property Consultants Private

Ltd. (est. 1995)

Establishes dominant market-leading position in India

5 |

Jones Lang LaSalle Growth in a Consolidating Industry

Commercial Real Estate Services

•

Corporate real estate decisions frequently

de-centralized

•

Fragmented competitive landscape with

several large regional players

•

Investor capital deployed within

countries/regions

•

Market share spread across numerous

niche/middle-market competitors

•

Clients moving towards centralized,

sophisticated global CRE decisions

•

Global service providers positioned for

growth in recovering markets

•

Investor capital flows cross-border to

capture opportunity

•

Market share trending to established

brands; new entrants continue

Jones Lang LaSalle

($ in millions)

6

(1)

Based on peak share price in each year

Americas

6x

EMEA

3x

Asia

Pacific

5x

LIM

2x

(1)

~4x

~5x

~5x

$67

$340

2002

2012

Adjusted Operating

Income

$786

$3,836

2002

2012

Market Cap

$860

$3,640

2002

2012

Fee Revenue

2

0

1

3

2

0

0

2 |

Market Share Expansion Drives Growth and Cash Flow

(In millions, except EPS)

2010

2011

2012

Growth

Revenue

$2,926

$3,585

$3,933

34%

Adjusted Net

Income

$166

$215

$245

48%

Adjusted

EBITDA

$337

$395

$436

29%

Adjusted

EPS

$3.77

$4.83

$5.48

45%

Market

Trends

Emerging markets

to lead global

expansion

Demand for

local and global

services

Outsourcing

growth

continues

Top asset

managers winning

investor mandates

Industry

consolidation

JLL Performance

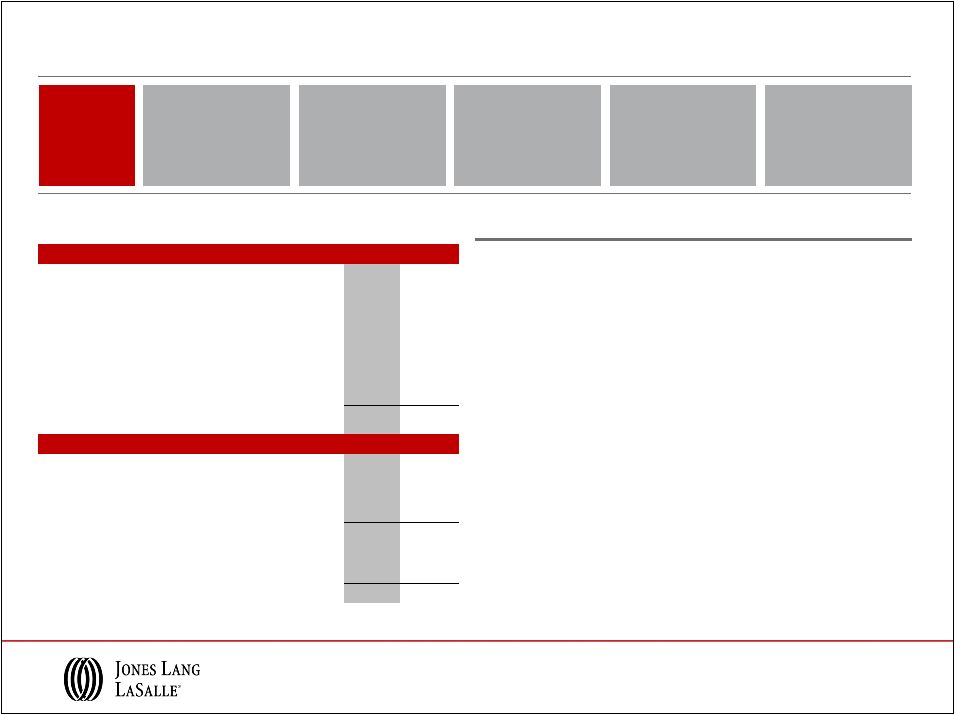

7

(1)

Other Financing Activities include change in working capital, debt issue costs and

share activity related to taxes on stock awards Deferred

Acquisition

Obligations

23%

New

Acquisitions

32%

CapEx

23%

Dividends

4%

Other

Financing

Activities

8%

Co-Investment

10%

3-Year Cash

from Earnings = $962M (1) |

Leading Brand Well-Positioned for Growth

•

Capitalize on leading global markets positions for

improved transactional and annuity revenue

•

Continue Corporate Solutions leadership; capture

emerging sectors (e.g. Healthcare, Infrastructure)

•

Leverage LaSalle’s investment performance and

client loyalty for continued wins and capital raising

•

Pursue growth within G5 strategy and financial

objectives

8

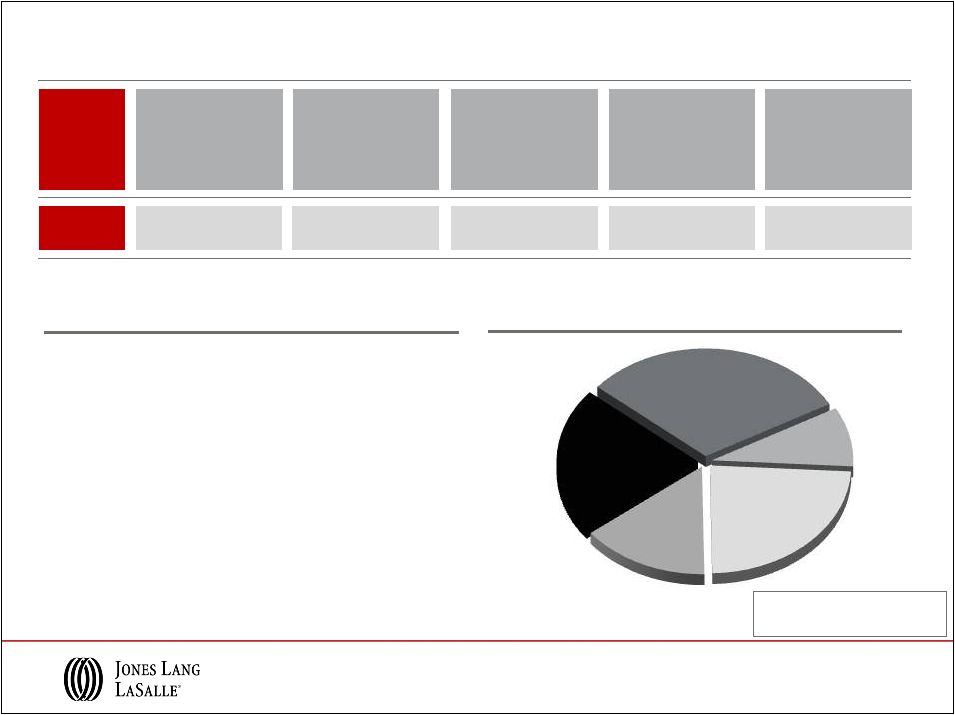

Jones Lang LaSalle Opportunity

2012 Revenue = $3.9B

United

States 43%

United

Kingdom

13%

France 4%

Germany 3%

Other

Europe 10%

Australia 7%

Greater

China (incl.

Hong Kong)

6%

Japan 4%

India 3%

Singapore

2%

Other 5% |

Global

Growth Strategy |

Jones Lang LaSalle Global Growth Strategy

G2

G1

G4

G3

G5

Connections

Build our local and regional

leasing and capital markets

businesses

Strengthen our winning

positions in Corporate

Solutions

Capture the leading

share of global capital

Grow LaSalle Investment

Management’s leadership

position

flows for investment sales

10 |

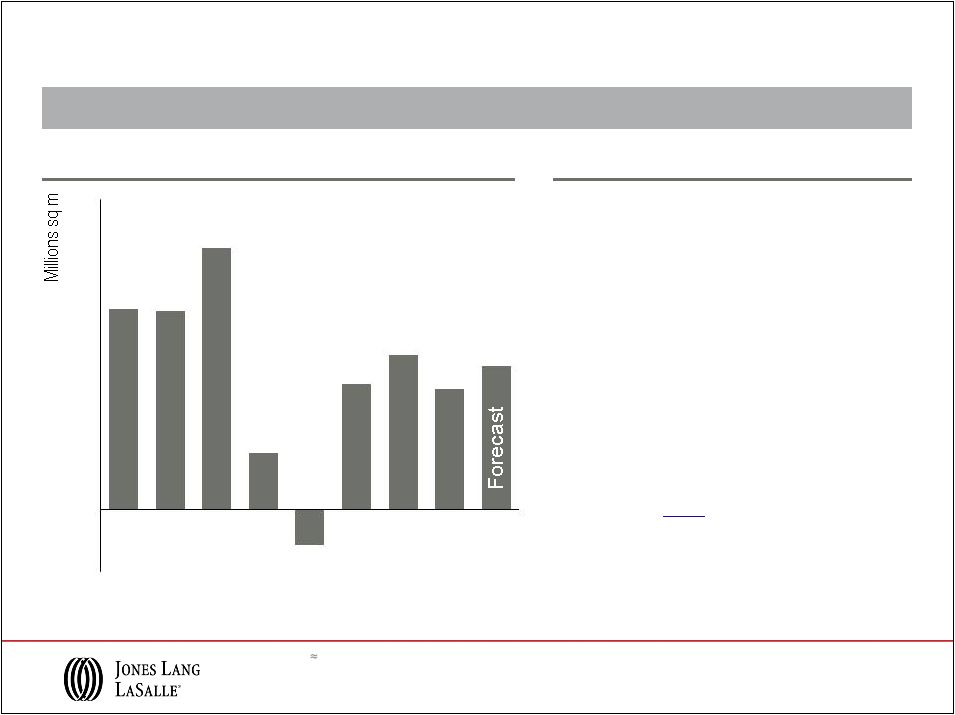

Leasing Trends and Expectations in Global Office Demand

Click here

to see the complete

JLL Global Markets Perspective

Note:

1

square

meter

10.8

square

feet

24 markets in Europe; 25 markets in Asia Pacific; 44 markets in the US. Asia

related to Grade A only. Source: Jones Lang LaSalle, January 2013

Modest leasing activity growth expected in 2013

11

Net Absorption Trends

Leasing Volumes

•

Overall, 0-5% growth over 2012 expected in

2013

with

momentum

building

in

2

nd

half

•

Americas growth estimates 0-5%

•

EMEA market recovery remains

constrained, flat to 2012

•

Asia Pacific demand is mixed, with full-year

expectations to be down 5-10% vs. 2012

16.2

16.0

21.1

4.6

-2.9

10.1

12.5

9.7

11.6

-

5

0

5

10

15

20

25

2005

2006

2007

2008

2009

2010

2011

2012

2013 |

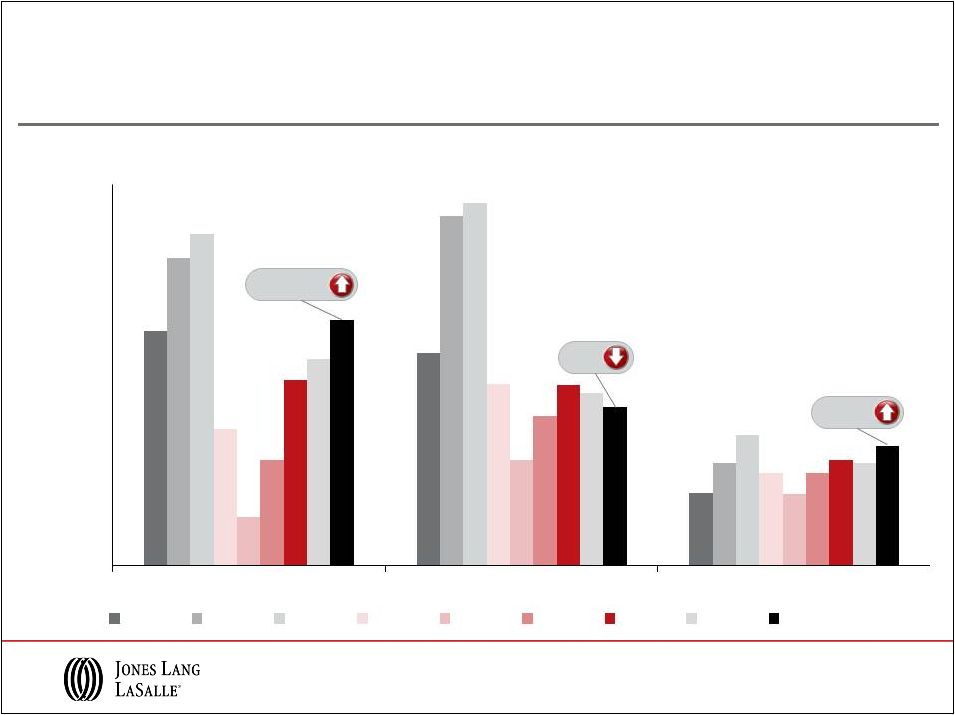

($ in

billions) Global Capital Flows for Investment Sales

* EMEA: In US$ terms, unchanged in Euro terms.

Source: Jones Lang LaSalle, January 2013

Direct Commercial Real Estate Investment, 2005-2013

2013 volumes set to approach $500 billion, up

10-15% Exceptional end to 2012

pushes full-year volumes

slightly ahead of 2011

12

+15-20%

-5%

+15%

0

50

100

150

200

250

300

350

Americas

EMEA

Asia Pacific

2005

2006

2007

2008

2009

2010

2011

2012

2013 Projection |

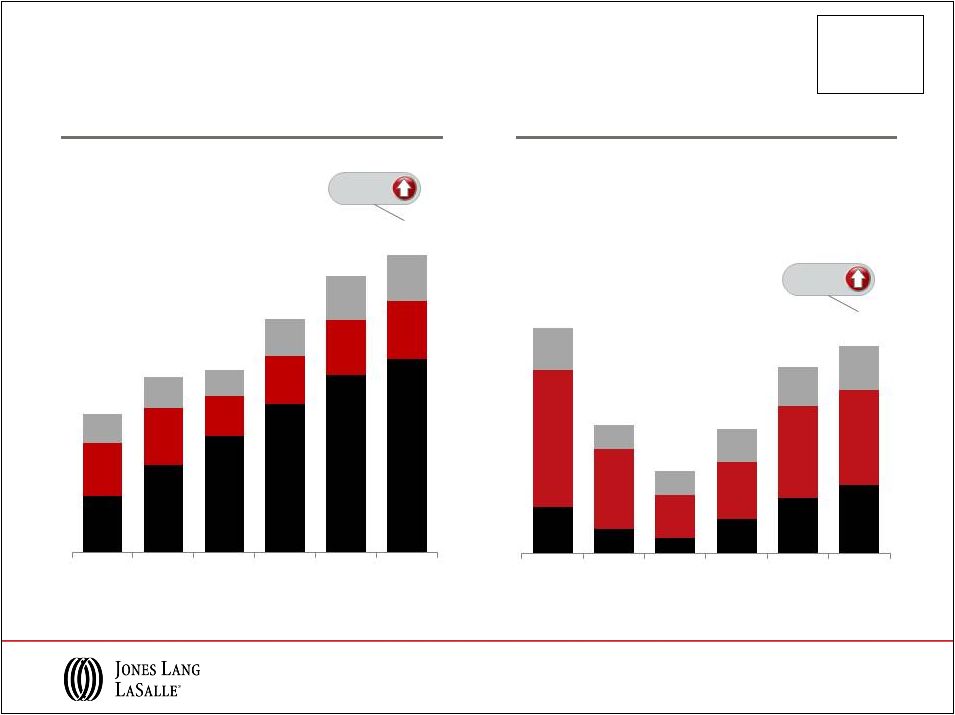

JLL Leasing and Capital Markets Revenue

Leasing

*July 2008: Staubach Company acquired, annual

revenue = $375 million

Asia Pacific

EMEA

Americas

*May 2011: King Sturge acquired, annual revenue =

$260 million

Capital Markets

13

($ in millions)

($ in millions)

$241

$373

$500

$638

$760

$830

$227

$247

$173

$203

$236

$250

$125

$133

$108

$159

$192

$198

2007

2008*

2009

2010

2011

2012

$114

$61

$38

$84

$136

$169

$339

$196

$107

$141

$229

$235

$104

$60

$58

$81

$95

$109

2007

2008

2009

2010

2011*

2012

$593

$781

$753

$1,000

$1,188

$1,278

$557

$317

$203

$306

$460

$513

+13%

+9% |

Corporate Solutions

JLL Service Offerings

JLL Client Wins

Competitive

Advantages

Global

Position

Expertise across services & geographies to capitalize on market trends

Space

optimization

Portfolio

transparency

Energy

management

Transformational

outsourcing

14

Middle Market

Large Corporates

Integrated

Facility

Management

Transaction

Advisory

Services

Project

Management

Lease

Administration

Labwell

Lab

Management

Energy &

Sustainability

Services

Strategic

Consulting

Corporate

Finance /

CMG

Client

Relationship

Management

Corporate

Retail

Services

Middle Market

Large Corporates

Wins

48

Expansions

39

Renewals

47

Wins

58

Wins

62

Expansions

38

Renewals

41

Wins

51

0

50

100

150

200

2

0

1

1

2

0

1

2 |

($

millions) 2005 to 2012 Advisory Fees

LaSalle Investment Management

Global Financial

Crisis

Stabilized

Advisory Fees

Building Advisory Fees in

Healthy Markets

Competitive

Advantages

Diversified

global

platform

Proven performance history with long-standing client relationships

Core, Value Add,

Opportunistic,

Public Equity

300+

institutional

clients

Consistent client

services delivery

model

Financial backing

of well-capitalized

parent company

Current AUM by Fund Type

Q4 2012 AUM =

$47 B

($ in billions)

15

Separate

Accounts

$20.4

Fund

Management

$16.4

Public

Securities

$10.2

$128

$178

$245

$278

$242

$238

$245

$228

67%

47%

68%

78%

93%

92%

90%

88%

0%

20%

40%

60%

80%

100%

$0

$50

$100

$150

$200

$250

$300

$350

2005

2006

2007

2008

2009

2010

2011

2012

Advisory Fees

Advisory Fees as % of Revenue |

Consolidating Industry Leads to JLL Opportunity

Transformative Results

The Staubach

Company

King Sturge

Meghraj

Trinity Funds

Management

Strategy

Establish leading U.S. local

market tenant rep position

Strengthen local market

scale, particularly in the UK

Augment India corporate business

with leading local presence

Gain scale and credibility

in Australia for LaSalle

Purchase Price

$613 million

£197 million

$60 million

A$9 million

Payment

Structure

36% upfront;

64% deferred over 5 years

50% upfront;

50% deferred over 5 years

50% upfront:

50% deferred over 5 years

100% upfront

EBITDA

multiple

8.0x notional,

7.0x on PV basis

7.5x notional,

7.0x on PV basis

7.5x

4.0x

Strategic

Align with

G5 strategy

Enhance service

delivery for clients

Cultural

alignment

Meet

financial goals

Financial

Profit growth to

shareholders

Neutral to accretive

EBITDA multiples

EPS accretive within

12-18 months

Maintain investment

grade strength

16 |

Financial Overview |

Consolidated 2012 Earnings Scorecard

Note: 2012 and 2011 adjusted for restructuring and intangible amortization. See

Appendix for U.S. GAAP results. 2012

Fee

Revenue

Adjusted

Net Income

$245M

Adjusted

EPS

$5.48

Adjusted

EBITDA

$436M

Adjusted EBITDA

Margin

12.0%

Gross revenue : $3.9B

18

2011

$215M

$4.83

$395M

11.7%

$3.4B

US GAAP: $164M

US GAAP: $3.70

EBITDA: $339M

EBITDA margin: 9.5%

Gross Revenue: $3.6B

US GAAP: $208M

US GAAP: $4.63

EBITDA: $391M

EBITDA margin: 9.9%

•

Broad-based fee revenue increase of 10% in

local currency versus 2011

•

Solid Leasing performance and continued

growth in Property & Facility Management

•

2012 Adjusted EPS up 13% to $5.48

•

Market share growth and cost discipline

contributing to performance across the firm

2012 Highlights

Revenue Contribution

$3.6B

Margin is calculated on a fee revenue basis. See Appendix for calculation of fee

revenue. Americas

44%

EMEA

27%

Asia

Pacific

22%

LIM

7% |

2012 Real Estate Services Revenue

($ in millions; % change in local currency

over FY 2011)

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). Fee revenue presentation of

Property & Facility Management, Project & Development Services and Total RES Operating Revenue excludes gross

contract costs.

19

Leasing

$829.6

9%

$250.0

11%

$198.2

4%

$1,277.8

9%

Capital Markets & Hotels

$168.5

25%

$235.1

5%

$109.3

15%

$512.9

13%

Property & Facility

Management

$458.7

32%

$155.2

9%

$398.4

10%

$1,012.3

19%

Fee Revenue

$375.0

15%

$155.2

9%

$319.9

13%

$850.1

13%

Project & Development

Services

$182.9

4%

$219.8

28%

$83.5

6%

$486.2

14%

Fee Revenue

$182.1

4%

$106.5

16%

$67.2

16%

$355.8

9%

Advisory,

Consulting & Other

$107.0

9%

$189.1

10%

$86.1

6%

$382.2

9%

Total RES Operating

Revenue

$1,746.7

15%

$1,049.2

12%

$875.5

9%

$3,671.4

13%

Fee Revenue

$1,662.2

11%

$935.9

9%

$780.7

11%

$3,378.8

10%

Americas

EMEA

Asia Pacific

Total RES |

2012

Highlights •

Full-year fee revenue up 11% from 2011

•

Increases in both Capital Markets and

Leasing revenue outpaced the overall market

indicating gains in market share

•

Compensation expense accelerated by

elimination of the Stock Ownership Plan

(“SOP”) and Staubach acquisition payment in

Q4; Full-year 2012 EBITDA margin flat to 2011

after adjusting for these items

Americas Real Estate Services

2012

Segment

Profile

Fee Revenue

$1,662M

Operating Income

$168M

Operating Income

Margin

10.1%

EBITDA

$210M

EBITDA Margin

12.7%

YoY Growth: 11%

Note: Margin

is

calculated

on

a

fee

revenue

basis.

See

Appendix

for

calculation

of

fee

revenue.

EBITDA

margin

for

2012

and

2011

would

have

been

~13.0%

after

adjusting

2012

compensation

expense

for

the

Staubach

acquisition

payment

and

adjusting

2011

compensation expense for the elimination of SOP.

20

2011

Revenue by Geography

$1,504M

$163M

10.8%

$201M

13.4%

Brazil 3%

Canada 2%

Mexico 1%

Other

Americas 2%

United

States

92% |

EMEA Real Estate Services

2012

Segment

Profile

Fee Revenue

$936M

Adj. Operating

Income

$58M

Adj. Operating

Income Margin

6.2%

EBITDA

$75M

EBITDA Margin

8.0%

YoY Growth: 9%

Note: Operating income has been adjusted to exclude $5 million of King Sturge

intangibles amortization. Margin is calculated on a fee revenue

basis. See Appendix for calculation of fee revenue. 21

2011

2012 Highlights

•

Broad-based fee revenue increase of 9% in

local currency versus 2011 led by 16%

increase in Project & Development Services

revenue

•

Solid performance in large markets and

positive earnings contribution from previous

loss-makers (e.g. Netherlands, MENA)

•

EBITDA margin of 8.0% compared with 6.5%

in 2011 driven by management actions

throughout the year

Revenue by Geography

$888M

$39M

4.4%

$57M

6.5%

U.K. 41%

France 17%

Germany

12%

Russia 4%

Spain 4%

Netherlands

3%

Belgium 3%

Italy 2%

MENA 2%

Other EMEA

12% |

Asia Pacific Real Estate Services

2012

Segment

Profile

Fee Revenue

$781M

Operating Income

$65M

Operating Income

Margin

8.4%

EBITDA

$78M

EBITDA Margin

10.0%

YoY Growth: 11%

22

2011

2012 Highlights

•

Fee revenue growth of 9% in local currency

vs. prior year despite decrease in overall

market activity

•

Winning Corporate Solutions business

continues to generate profitable, recurring

revenue

•

Strong finish with significant EBITDA margin

improvement in Q4 2012

Revenue by Geography

$713M

$66M

9.3%

$78M

11.0%

Australia

31%

Greater

China (inc.

Hong Kong)

26%

India 13%

Japan 14%

Singapore

6%

Thailand 2%

New Zealand

2%

Other

Asia

6%

Note: Margin is calculated on a fee revenue basis. See Appendix for calculation

of fee revenue. |

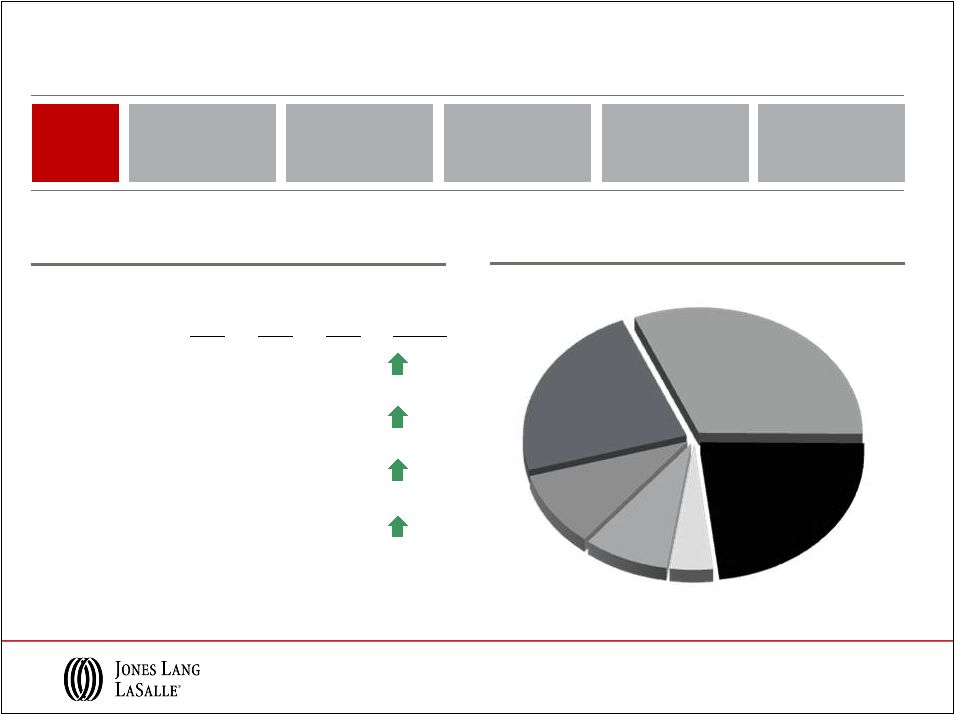

LaSalle Investment Management

2012

Segment

Profile

Revenue

$285M

Operating Income

$72M

Operating Income

Margin

25.2%

EBITDA

$74M

EBITDA Margin

25.9%

Note: AUM data reported on a one-quarter lag.

YoY Growth: 12%

23

2011

$275M

$57M

20.7%

$60M

21.7%

2012 Highlights

•

Large incentive fees and equity earnings

reflect good performance for clients and

contributed to EBITDA margin of 25.9%

•

New mandates and strategic partnerships

gaining traction; AUM in separate accounts

up 14% vs. last year

•

$4.7 billion of capital invested in 2012

stabilizing advisory fees

•

Smaller incentive fees and equity earnings

expected for 2013

Separate Accounts $20.4

Fund Management $16.4

($ in billions)

Q4 2012 AUM = $47 Billion

U.K.

$14.5

Continental

Europe

$4.2

North

America

$11.2

Asia

Pacific

$6.9

Public

Securities

$10.2 |

Credit

Facility Capacity

$1.1B

Solid Cash Flows and Balance Sheet Position

2012 Key

Statistics

Cash from

Earnings

$335M

Total

Net Debt

$538M

Net Interest

Expense

$35.2M

Investment Grade

Ratings

Baa2

|

BBB-

2012 Highlights

($ in millions)

24

Cash Flows

2012

2011

Primary Uses

Capital Expenses

(1)

(95)

(92)

New Acquisitions

(28)

(252)

Deferred Acquisition Obligations

(144)

(164)

Co-Investment

(29)

(46)

Dividends

(18)

(13)

Net Cash Outflows

$ (314)

$ (567)

Balance Sheet

Cash

$ 152

$ 184

Short Term Borrowings

32

65

Credit Facility

169

463

Net Bank Debt

$ 49

$ 344

LT Senior Notes

275

-

Deferred Acquisition Obligations

214

299

Total Net Debt

$ 538

$ 643

•

Significant cash generation with $105 million of

net debt reduction

•

Issued $275 million, investment-grade 4.4%

Senior Notes

•

Accelerated $115 million of the final $156 million

Staubach deferred payment to December 2012

•

Strong Leasing performance resulted in

Staubach earn out of $36 million

(1)

Includes $12 million in 2012 of investments in a joint-venture entity required to

be consolidated under U.S. GAAP, but are offset in Financing

Activities

on

the

statement

of

cash

flows.

Net

of

this

JV

gross-up

and

cash

received

from

tenant

improvement

allowances, cash spent on capital expenditures was $80 million.

-

Diversified funding sources and extended maturities until 2022

-

$5 million paid in 2012, $31 million to be paid in H1 2013 and

recorded in Deferred Acquisition Obligations as of 12/31/12

-

Remaining $41 million to be paid as previously scheduled

|

Continuing growth in corporate

outsourcing

On-going industry consolidation

trends continue

Key Takeaways

JLL

Integrated

global

services

Industry leading

research and

market expertise

Superior client

relationship

management

Strong

brand

Investment-grade

balance sheet

JLL actions for continued success

Optimism returning to global markets

Steady institutional capital flows

into global real estate

Leverage global positions to grow market share

and continue client success in local markets

Increase productivity and manage costs to

improve margin

Maintain financial strength and flexibility to

respond to opportunities and challenges

Continue to invest selectively and strategically

to capitalize on market consolidation

25 |

Appendix |

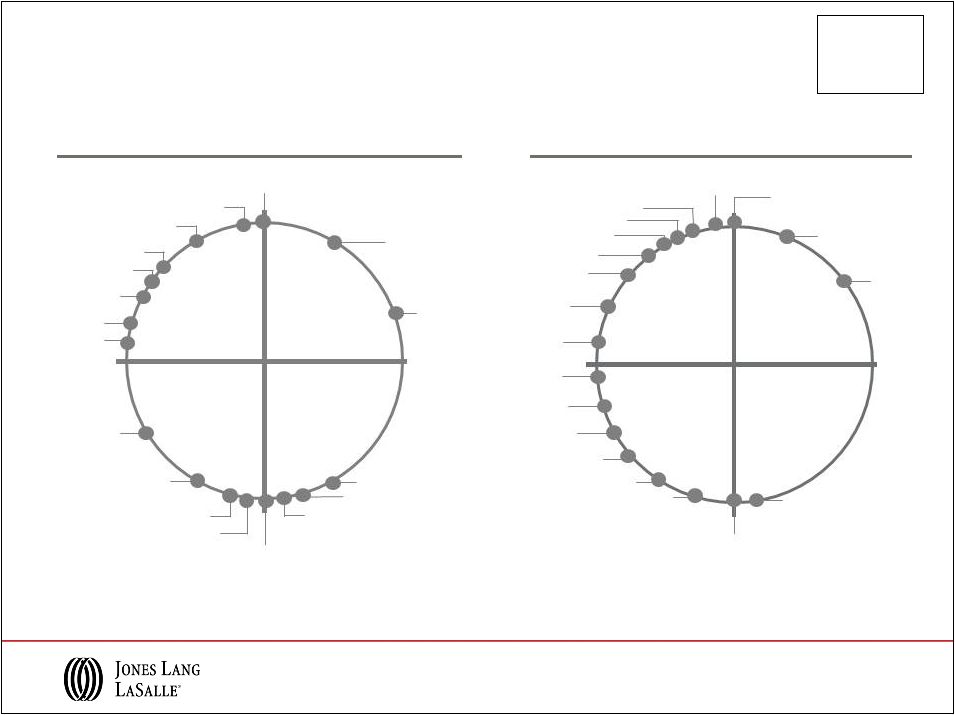

as of

Q4 2012 Leasing Values

Source: Jones Lang LaSalle

Rental Value

growth slowing

Rental Value

growth

accelerating

Rental Values

bottoming out

Rental Values

falling

Madrid

Istanbul, Johannesburg,

Mumbai, New York,

Chicago,

Brussels,

Dubai, Frankfurt

Amsterdam,

Beijing,

Paris,

Shanghai

Milan

Seoul

Berlin

London,

Houston

Dallas,

London

Washington DC

Boston

Sao Paulo,

Stockholm

Hong Kong,

Singapore

Moscow,

Sydney

Los Angeles, Mexico City, Tokyo

Asia Pacific

EMEA

Americas

as of Q4 2012

Capital Values

Capital Value

growth slowing

Capital Value

growth

accelerating

Capital Values

bottoming out

Capital Values

falling

Milan

Madrid

Brussels,

Seoul

Hong Kong,

Paris,

Shanghai

Amsterdam,

Beijing,

Boston, Chicago, Los

Angeles, New York,

Shanghai

Sao Paulo

Dallas

Toronto

Mexico City,

Sydney

Moscow

Washington DC

Stockholm

Frankfurt

Berlin

London

Tokyo

Mumbai

Houston

JLL Property Clocks

27

San Francisco

Toronto

San Francisco

SM |

FY 2012 Real Estate Services Revenue

($ in millions; % change in USD

over FY 2011)

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). Fee revenue presentation of

Property & Facility Management, Project & Development Services and Total RES Operating Revenue excludes gross

contract costs.

28

Leasing

$829.6

9%

$250.0

6%

$198.2

3%

$1,277.8

7%

Capital Markets & Hotels

$168.5

24%

$235.1

3%

$109.3

15%

$512.9

12%

Property & Facility

Management

$458.7

31%

$155.2

5%

$398.4

9%

$1,012.3

17%

Fee Revenue

$375.0

14%

$155.2

5%

$319.9

12%

$850.1

12%

Project & Development

Services

$182.9

3%

$219.8

21%

$83.5

3%

$486.2

10%

Fee Revenue

$182.1

2%

$106.5

11%

$67.2

13%

$355.8

7%

Advisory,

Consulting & Other

$107.0

9%

$189.1

6%

$86.1

6%

$382.2

7%

Total RES Operating

Revenue

$1,746.7

15%

$1,049.2

8%

$875.5

7%

$3,671.4

11%

Fee Revenue

$1,662.2

11%

$935.9

5%

$780.7

10%

$3,378.8

8%

Americas

EMEA

Asia Pacific

Total RES |

Q4 2012 Real Estate Services Revenue

($ in millions; % change in USD

over December QTD 2011)

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). Fee revenue presentation of

Property & Facility Management, Project & Development Services and Total RES Operating Revenue excludes

gross contract costs.

Leasing

$278.9

8%

$83.7

3%

$76.6

11%

$439.2

7%

Capital Markets & Hotels

$59.4

23%

$94.9

8%

$40.1

82%

$194.4

12%

Property & Facility

Management

$133.2

13%

$42.4

0%

$108.3

7%

$283.9

9%

Fee Revenue

$111.1

10%

$42.4

0%

$88.9

13%

$242.4

9%

Project & Development

Services

$51.9

4%

$64.5

25%

$26.8

28%

$143.2

13%

Fee Revenue

$51.7

4%

$30.5

6%

$19.2

21%

$101.4

3%

Advisory,

Consulting & Other

$31.5

3%

$66.8

7%

$26.5

17%

$124.8

8%

Total RES Operating

Revenue

$554.9

9%

$352.3

4%

$278.3

18%

$1,185.5

9%

Fee Revenue

$532.6

8%

$318.3

0%

$251.3

20%

$1,102.2

8%

Americas

EMEA

Asia Pacific

Total RES

29 |

Fee Revenue / Expense Reconciliation

•

Reimbursable vendor, subcontractor and out-of-pocket costs reported as revenue

and expense in JLL financial statements have been steadily increasing

•

Margins diluted as gross accounting requirements increase revenue and costs without

corresponding profit •

Business managed on a “fee”

basis to focus on margin expansion in the base business

($ in millions)

2012

2011

Consolidated Revenue

3,932.8

$

3,584.5

$

Consolidated Operating Expenses

3,598.0

3,277.2

Adjusted Operating Income Margin

8.6%

8.9%

Gross Contract Costs:

Property & Facility Management

83.7

20.4

Project & Development Services

0.8

0.5

Total Gross Contract Costs

84.5

20.9

Property & Facility Management

-

-

Project & Development Services

113.3

85.7

Total Gross Contract Costs

113.3

85.7

Property & Facility Management

78.5

82.3

Project & Development Services

16.3

21.6

Total Gross Contract Costs

94.8

103.9

Consolidated Fee Revenue

3,640.2

$

3,374.0

$

Consolidated Fee-based Operating Expenses

3,305.4

$

3,066.7

$

Adjusted Operating Income Margin (fee based)

9.3%

9.4%

YTD

Asia Pacific

Americas

EMEA

30

Note: Consolidated revenue and fee revenue exclude equity earnings (losses).

Restructuring and acquisition charges are excluded from operating

expenses. Restructuring and acquisition charges as well as intangible amortization related to the King

Sturge acquisition are excluded from operating expenses when calculating adjusted

operating income margin. |

Reconciliation of GAAP Net Income to Adjusted Net Income

Twelve Months Ended

December 31,

($ in millions)

2012

2011

2010

GAAP Net income attributable to common shareholders

$ 207.6

$ 164.0

$ 153.5

Shares (in 000s)

44,799

44,367

44,084

GAAP earnings per share

$ 4.63

$ 3.70

$ 3.48

GAAP Net income attributable to common shareholders

$ 207.6

$ 164.0

$ 153.5

Restructuring and acquisition charges, net

34.1

41.9

4.9

Intangible amortization, net

3.7

8.6

-

Non-cash co-investment charges, net

-

-

7.9

Adjusted net income

$ 245.4

$ 214.5

$ 166.3

Shares (in 000s)

44,799

44,367

44,084

Adjusted earnings per share

$ 5.48

$ 4.83

$ 3.77

and Earnings per Share

31 |

Reconciliation of Operating Income to Adjusted Operating

Income and GAAP Net Income to Adjusted EBITDA

Twelve Months Ended

December 31,

($ in millions)

2012

2011

2010

Operating Income

$289.4

$251.2

$260.7

Restructuring and acquisition charges

45.4

56.1

6.4

Intangible amortization

4.9

11.5

-

Non-cash co-investment charges

-

-

10.4

Adjusted Operating Income

$339.7

$318.8

$277.5

GAAP Net income attributable to common

shareholders

$207.6

$ 164.0

$ 153.5

Interest expense, net of interest income

35.2

35.6

45.8

Provision for income taxes

69.2

56.4

49.0

Depreciation and amortization

78.8

82.8

71.6

EBITDA

$390.8

$338.8

$319.9

Restructuring and acquisition charges

45.4

56.1

6.4

Non-cash co-investment charges

-

-

10.4

Adjusted EBITDA

$436.2

$394.9

$336.8

32 |

Forward-looking statements

©

Jones Lang LaSalle IP, Inc. 2013. All rights reserved. No part of this publication may be

reproduced by any means, whether graphically, electronically, mechanically or

otherwise howsoever, including without limitation photocopying and recording on

magnetic tape, or included in any information store and/or retrieval system

without prior written permission of Jones Lang LaSalle IP, Inc.

33

Statements in this presentation regarding, among other things, future financial results

and performance, achievements, plans and objectives and dividend payments may be

considered forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995. Such statements involve known and

unknown risks, uncertainties and other factors which may cause actual results,

performance, achievements, plans and objectives of Jones Lang LaSalle to be materially

different from those expressed or implied by such forward-looking statements.

Factors that could cause actual results to differ materially include those

discussed under “ Business, ” “Risk Factors,”

“Management’s Discussion and Analysis of Financial Condition and Results of

Operations,” “Quantitative and Qualitative

Disclosures about Market Risk,”

“Cautionary Note Regarding Forward-Looking Statements” and

elsewhere in Jones Lang LaSalle’s Annual Report on Form 10

-K for the year ended December 31, 2012 and in other reports filed with

the Securities and Exchange Commission. There can be no assurance that future

dividends will be declared since the actual declaration of future dividends, and the establishment

of record and payment dates, remains subject to final determination by the Company’s

Board of Directors. Statements speak only as of the date of this

presentation. Jones Lang LaSalle expressly disclaims any obligation or undertaking

to update or revise any forward-looking statements contained herein to reflect

any change in Jones Lang LaSalle’s expectations or results, or any change in

events. |