Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - NAVISTAR INTERNATIONAL CORP | d497295d8k.htm |

| EX-99.1 - PRESS RELEASE - NAVISTAR INTERNATIONAL CORP | d497295dex991.htm |

NYSE:

NAV 1

ST

QUARTER 2013 EARNINGS

PRESENTATION

March 7

th

, 2013

Exhibit 99.2 |

2

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Safe Harbor

Statement

Information provided and statements contained in this report that are not purely

historical are forward-looking

statements

within

the

meaning

of

Section

27A

of

the

Securities

Act

of

1933,

as

amended, Section

21E of the Securities Exchange Act of 1934, as amended, and the Private

Securities Litigation Reform Act of 1995. Such forward-looking statements only

speak as of the date of this report and the Company assumes no obligation to

update the information included in this report. Such forward-looking

statements include information concerning our possible or assumed future

results of operations, including descriptions of our business strategy. These

statements often include words such as “believe,”

“expect,”

“anticipate,”

“intend,”

“plan,”

“estimate,”

or similar expressions. These statements are not guarantees of performance or

results and they involve risks, uncertainties, and assumptions. For a

further description of these factors, see the risk factors set forth in our

filings with the Securities and Exchange Commission, including our annual

report on Form 10-K for the fiscal year ended October 31, 2012. Although

we believe that these forward-looking statements are based on reasonable

assumptions, there are many factors that could affect our actual financial

results or results of operations and could cause actual results to differ

materially from those in the forward-looking statements. All future

written and oral forward-looking statements by us or persons acting on our

behalf are expressly qualified in their entirety by the cautionary

statements contained or referred to above. Except for our ongoing

obligations to disclose material information as required by the federal securities

laws, we do not have any obligations or intention to release publicly any revisions

to any forward- looking statements to reflect events or circumstances in

the future or to reflect the occurrence of unanticipated events.

|

3

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Other Cautionary Notes

The financial information herein contains audited and unaudited information and

has been prepared by management in good faith and based on data currently

available to the Company.

Certain non-GAAP measures are used in this presentation to assist the

reader in

understanding

our

core

manufacturing

business.

We

believe

this

information

is

useful

and

relevant

to

assess

and

measure

the

performance

of

our

core

manufacturing business as it illustrates manufacturing performance without regard

to selected historical legacy costs (i.e. pension and other postretirement

costs). It also excludes financial services and other items that may not

be related to the

core manufacturing business or underlying results. Management often uses this

information to assess and measure the underlying performance of our

operating segments.

We have chosen to provide this supplemental information to investors,

analysts,

and

other

interested

parties

to

enable

them

to

perform

additional

analyses of operating results. The non-GAAP numbers are reconciled to the most

appropriate GAAP number in the appendix of this presentation.

|

4

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

•

Cash

•

Structural Cost Reductions

•

ROIC actions

1st Quarter Actions |

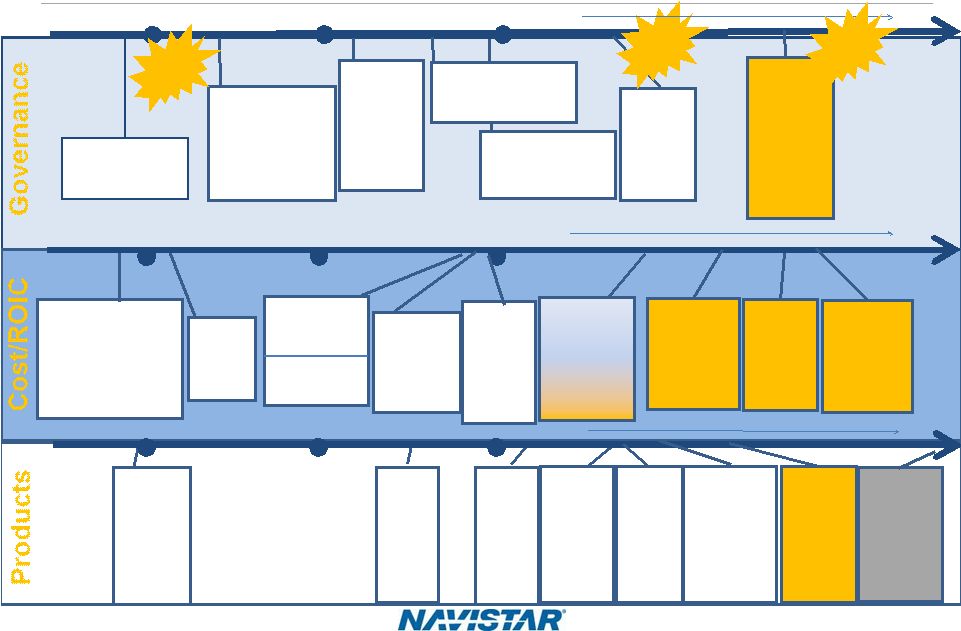

5

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

9/6

–

Announced

ROIC

focused

strategy

11/15 –

First

saleable

ProStar

with ISX

to roll off

line

Drive to Deliver Progress

8/27 –

Announced U.S.

Voluntary Separation

Package results and need

for Reduction In Force as

part of goal to reduce costs

by $150M-$175M. 10/31

completion date

Launch

ProStar with

13-L SCR in

April

12/11 –

Regular

production

of ProStar

with ISX

engines

10/23 –

Cummins

contract

finalized

9/6 –

Realigned Senior

Leadership –

weekly

meetings. Established

daily cash management

report and

manufacturing

excellence system

August

September

October

November

April

8/30 –

EPA

issued final

ruling

10/8 –

Company

adds two new

board

members:

Vincent J.

Intrieri and

Mark H.

Rachesky

August

September

October

August

September

October

10/24 –

ROIC

update -

elimination of

MxF15

Equity offering;

confirmed cash

guidance

10/16 –

Board approves

2013 operating plan and

addition of John C. Pope to

BOD

10/30 –

Announced

closure of

Garland

facility

10/26 –

Brazil

restructuring

complete;

approx. 700

jobs eliminated

8/27 –

Lewis

Campbell named

Executive Chairman

and CEO

12/10 –

Company

adds new

board

member:

Samuel J.

Merksamer

12/18 –

Announced

intent to sell

India equity to

Mahindra

2/12–

Sale of

equity interests

completed

9/6 –

3Q

Earnings

call

12/19 –

4Q

Earnings

call

12/14 –

“OK to

ship”-

five

days

ahead of

schedule

2/19 –

Annual

shareholder

meeting

1/7 –

Submitted

for EPA

certification

on 13Liter

12/19 –

End of

Year

manufacturing

cash balance of

$1.5B

1/6 –

Best In

Class

Benchmarking

Initiative

2/19 –

Announced

sublease of

Alabama

Facility

3/04 –

announced the

sale of

Workhorse

Custom

Chassis

November

April

November

April

3/7 –

1Q

Earnings

call

10/27

–

Board

approves

annual

incentive

plans

that

tie

to

increasing

shareholder

value |

6

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

•

•

Quality

Quality

•

•

Cost

Cost

•

•

Sense of Urgency

Sense of Urgency

•

•

Great Products

Great Products

•

•

Customer Satisfaction

Customer Satisfaction

•

•

People

People

Guiding

Principles Near-Term Priorities

2013

2013

Drive to Deliver

Drive to Deliver

Deliver Our

2013 Plans

Hit Our

Launches

Improve

Quality |

NYSE:

NAV A. J. Cederoth, Executive Vice President & CFO

1

ST

QUARTER 2013 RESULTS |

8

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

1Q 2013 Results

* Attributable to Navistar International Corporation

1Q 2013

GAAP

1Q 2012

GAAP

Change

Revenue (Millions)

$2,637

3,009

$(372)

Manufacturing Segment Profit

(Loss) (Millions)

$1

$(97)

$98

EBITDA (Millions)

$57

$(106)

$163

Profit (Loss) from Continuing

Operations * (Millions)

$(114)

$(144)

$30

Diluted Profit (Loss) Per Share*

from Continuing Operations

$(1.42)

$(2.06)

$0.64

Notes: (1) Shares outstanding were 80.2 million in 1Q 2013 compared to 69.9

million in 1Q 2012. (2) Diluted (Loss) Per Share from discontinued

operations were $(0.11) in 1Q 2013 and $(0.13) in 1Q 2012. Note:

This slide contains non-GAAP information; please see the REG G in

appendix for a detailed reconciliation. |

9

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

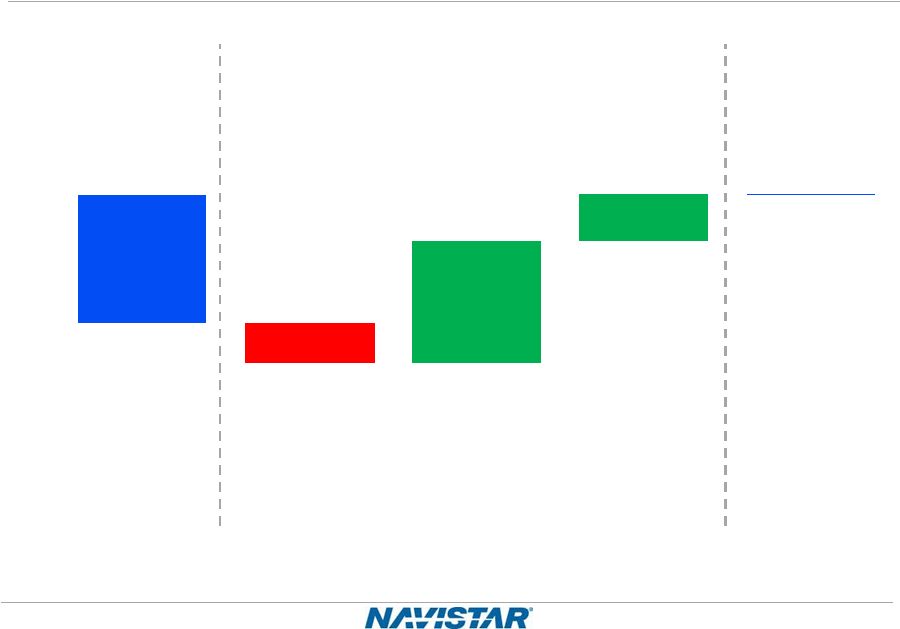

1Q 2012 vs. 1Q 2013

Manufacturing Segment Profit Walk

($97)

$1

($31)

$93

$36

($200)

($100)

$0

$100

1Q2012 Actual

Truck

Engine

Parts

1Q2013 Actual

Note:

This slide contains non-GAAP information; please see the REG G in

appendix for a detailed reconciliation. |

10

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

1Q 2013 Manufacturing Cash Update

Guidance**

Actual

2012 Year End Manufacturing Cash Balance*

$1,505

$1,505

EBITDA

$(50) -

$50

$57

CapEx/Cash Interest/Pension/OPEB Funding

$(215)

$(153)

Change in Net Working Capital

$(200)

$(190)

Debt Payments/Restructuring Cash/Other

$(90)

$(30)

1Q 2013 Manufacturing Cash Balance*

$950 -$1,050

$1,189

$ in millions

*Cash balance includes marketable securities.

**As shown on 12/19/2012

Note:

This slide contains non-GAAP information; please see the REG G in

appendix for a detailed reconciliation. |

11

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Guidance: 2Q 2013 Manufacturing Cash

Guidance**

1Q 2013 Manufacturing Cash Balance* Actual

$1,189

EBITDA

$(25) -

$25

CapEx/Cash Interest/Pension/OPEB Funding

$(189)

Change in Net Working Capital

$100 -

$150

Restructuring Cash/Other

$(75)

2Q 2013 Manufacturing Cash Balance* Guidance

$1,000 -

$1,100

$ in millions

* Cash balance includes marketable securities.

Note:

This slide contains non-GAAP information; please see the REG G in

appendix for a detailed reconciliation. |

12

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

•

Cash balance

•

Market share

•

EBITDA

2013 Key Indicators |

NYSE:

NAV Troy Clarke, President & COO

DRIVE TO DELIVER |

14

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Drive to Deliver Progress

Plan on Track

•

Product Launches on Schedule

•

Quality Continues to Improve

•

Exceeding Structural Cost Reductions |

15

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Hit Our Launches: ProStar Plus ISX 15 Liter |

16

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Hit Our Launches –

MxF13 On Track

Launch Schedule

•

Submitted test data to EPA

•

OBD compliance on track

•

Anticipate EPA/CARB certificates by end of March

to support end of April shipments

•

Small fleet of validation vehicles accumulating

miles

Build began ahead of schedule for 18

full production vehicles

FY2012

FY2013

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Test Units

1/7

Submit for

EPA

certification

3/05

Start Lead

Unit

Production

4/30

OK

To Ship |

17

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Quality

•

Navistar repair incidence is in line with industry

performance, and continues to improve toward best in

class

•

Repair cost per engine continues to improve

•

Once fixes have been identified and solutions validated,

field campaigns may be required

Bottom Line –

Quality continues to improve for Trucks and Engines

Actions demonstrate our commitment to our customers |

18

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

•

Supplements structural cost improvements already underway

•

Outgrowth of more functionally aligned organization

•

Function-by-function review compared to 15 heavy

manufacturing peers

•

Identifies more opportunities to improve cost structure, offset

potential risks

Driving Financial Improvement

Benchmarking Initiative

Already on track to exceed $175 million

structural cost improvement target |

Significant Progress on Business Portfolio

Actions taken to improve Return on Invested Capital (ROIC)

•

Discontinue non-core

engineering programs

•

Discontinue MaxxForce

15 Liter

•

Sale of equity interest in

Mahindra JV

•

Sublease portion of

Alabama facility to

FreightCar America

0

5

10

STRATEGIC FIT

LOW

HIGH

Grow/Sell

Grow

Close/Sell

Improve

19

NYSE: NAV

1Q 2013 Earnings –

3/7/2013 |

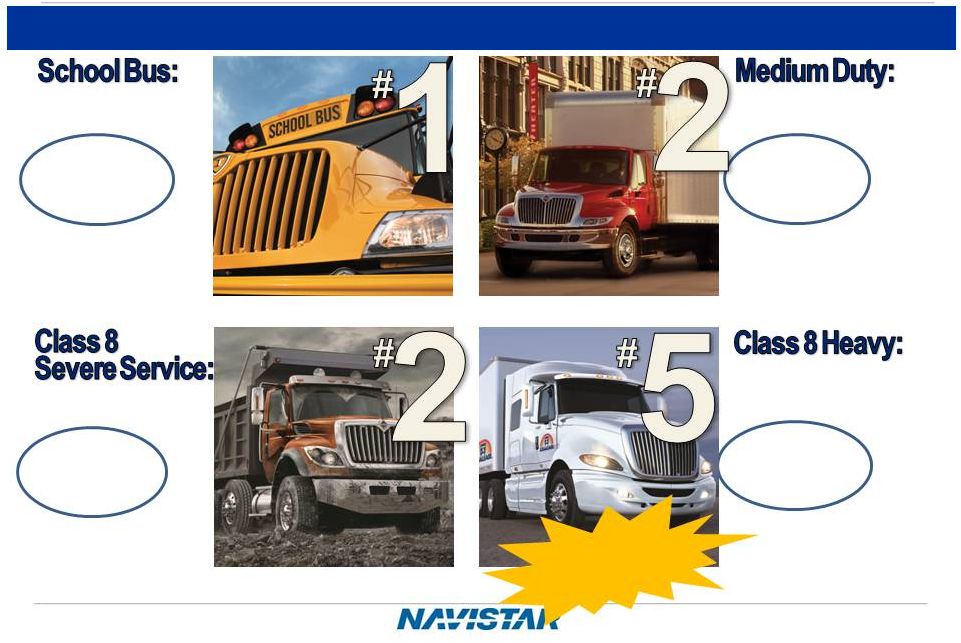

A

Leader in Several Commercial Vehicle Segments Market Share

1Q FY2013: ~38%

Note: Based on market share position determined by brand

Market Share

1Q FY2013: ~25%

Market Share

1Q FY2013: ~26%

Market Share

1Q FY2013: ~11%

Market Share

Trailing Six

Months: ~40%

Market Share

Trailing Six

Months: ~28%

Market Share

Trailing Six

Months: ~27%

Market Share

Trailing Six

Months: ~12%

Note:

See slide 24 for additional comments to this slides

EGR to SCR

Transition

U.S. and Canada School Bus & Class 6-8:

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

20 |

21

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

•

•

Quality

Quality

•

•

Cost

Cost

•

•

Sense of Urgency

Sense of Urgency

•

•

Great Products

Great Products

•

•

Customer Satisfaction

Customer Satisfaction

•

•

People

People

Guiding

Principles Near-Term Priorities

2013

2013

Drive to Deliver

Drive to Deliver

Deliver Our

2013 Plans

Hit Our

Launches

Improve

Quality |

NYSE:

NAV APPENDIX |

23

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Navistar Financial Corporation

Highlights

•

1Q 2013: $22 million Financial Services Segment Profit

•

Total U.S. financing availability of $1.0B as of January 31, 2013 (includes

bank facility availability of $500M)

•

Debt/Equity Leverage: 2½:1

Subsequent Events

•

Wholesale securitization completed in February for $200M

•

Better pricing and advance rate

•

Wholesale variable funding facility reduced from $750M to $500M in February

Retail Notes

Bank Facility

•

$840M facility refinanced in

December 2011, maturity

extended from 2012 to 2016

–

Funding for retail notes,

wholesale notes, retail

accounts, and dealer open

accounts

•

On balance sheet

•

NFSC wholesale trust as of

January 2013

–

$974M funding facility

–

Variable portion matures

August 2013

–

Term portion matures October

2013

•

On balance sheet

•

Broader product offering

•

Enhanced ability to support

large fleets

•

Better access to less

expensive capital

Dealer Floor Plan |

24

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

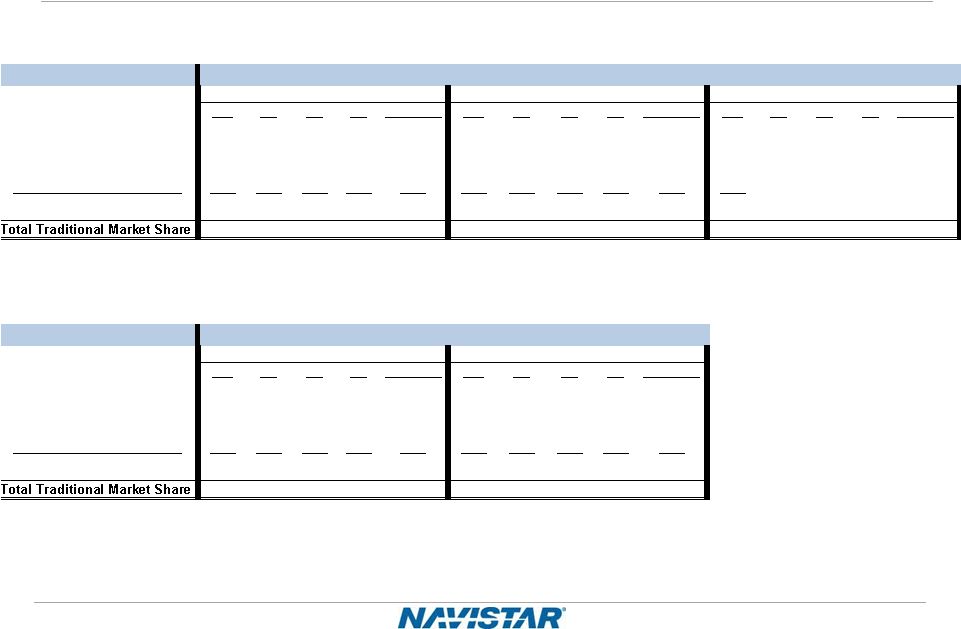

Market Share

NEW VIEW

Traditional Market Share

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

Q4

Full Year

School buses*

55%

45%

45%

40%

45%

41%

39%

38%

43%

41%

38%

Class 6 and 7 medium trucks

36%

36%

46%

44%

41%

27%

36%

36%

34%

33%

25%

Class 8 heavy trucks

17%

16%

17%

18%

17%

17%

15%

15%

13%

15%

11%

Class 8 severe service trucks

33%

32%

36%

37%

35%

31%

30%

30%

30%

30%

26%

Combined Class 8

21%

19%

21%

22%

21%

19%

18%

18%

17%

18%

14%

25%

24%

28%

28%

26%

22%

23%

23%

24%

23%

18%

OLD VIEW

Traditional Market Share

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

Q4

Full Year

School buses

49%

45%

47%

53%

49%

48%

48%

47%

49%

48%

Class 6 and 7 medium trucks

36%

36%

46%

44%

41%

27%

36%

36%

34%

33%

Class 8 heavy trucks

17%

16%

17%

18%

17%

17%

15%

15%

13%

15%

Class 8 severe service trucks

33%

32%

36%

37%

35%

31%

30%

30%

30%

30%

Combined Class 8

21%

19%

21%

22%

21%

19%

18%

18%

17%

18%

27%

26%

29%

29%

28%

22%

24%

24%

23%

23%

2011

2012

2012

2013

*Beginning in FY2013, Navistar has adjusted the way bus market share is

calculated. Navistar previously self reported retail deliveries and beginning FY2013 is using Polk

registrations as the data source to improve accuracy. Additionally, school

bus market share values now consist of class B/C/D buses. Historical data, which previously

contained only class C/D buses, has been adjusted to reflect this change in

methodology. All quarter data for bus is reported on a one month lag.

2011

Market Share –

U.S. & Canada School Bus and Class 6-8

Market Share –

U.S. & Canada School Bus and Class 6-8

We define our “traditional” markets to include U.S. and Canada School bus and Class 6

through 8 medium and heavy truck. We classify militarized commercial vehicles sold to the U.S.

and Canadian militaries as Class 8 severe service within our “traditional” markets. Beginning in 2011, our competitors are reporting certain RV and

commercial bus chassis units consistently with how we report these units. Our “traditional”

markets include CAT-branded units sold to Caterpillar under our North America supply

agreement. |

25

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

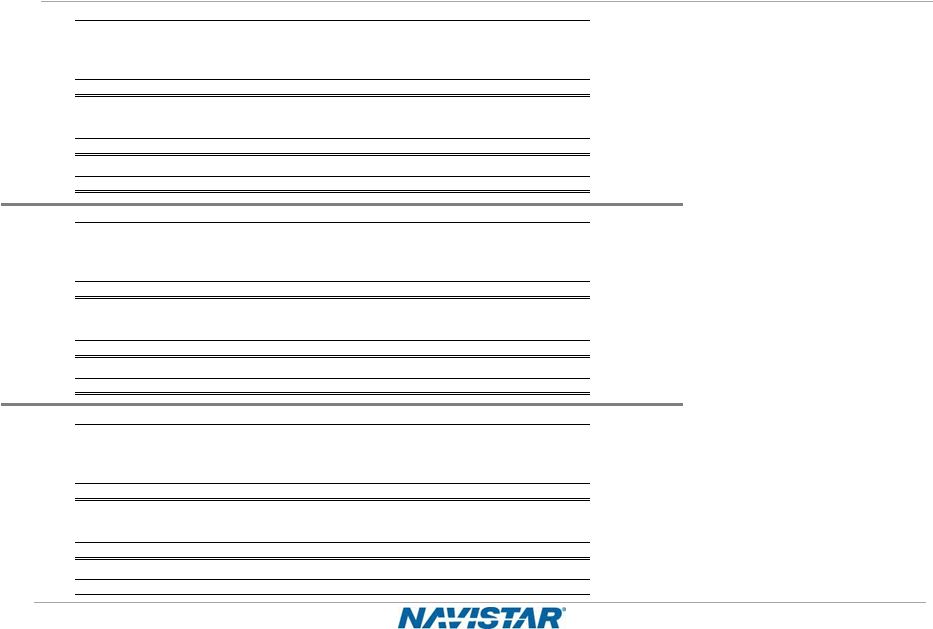

Worldwide Truck Chargeouts

We define our “traditional”

markets

to include U.S. and Canada School

bus and Class 6 through 8 medium

and heavy truck. We classify

militarized commercial vehicles

sold to the U.S. and Canadian

militaries as Class 8 severe service

within our “traditional”

markets. Our

“traditional”

markets include CAT-

branded units sold to Caterpillar

under our North America supply

agreement.

FISCAL YEAR 2011

Q1

Q2

Q3

Q4

FULL YEAR

BUS

2,100

2,000

2,200

2,900

9,200

MEDIUM

4,600

7,200

7,400

7,900

27,100

HEAVY

4,700

5,200

6,800

9,000

25,700

SEVERE

2,700

3,200

3,700

3,700

13,300

TOTAL

14,100

17,600

20,100

23,500

75,300

NON-TRADITIONAL MILITARY

100

400

200

700

1,400

EXPANSIONARY

4,900

6,900

8,000

9,500

29,300

WORLDWIDE TRUCK-Continued Ops

19,100

24,900

28,300

33,700

106,000

DISCONTINUED OPERATIONS

400

700

600

700

2,400

WORLDWIDE TRUCK-Total

19,500

25,600

28,900

34,400

108,400

FISCAL YEAR 2012

Q1

Q2

Q3

Q4

FULL YEAR

BUS

1,700

2,600

2,900

2,500

9,700

MEDIUM

4,300

7,100

5,800

4,700

21,900

HEAVY

8,000

7,200

6,300

5,600

27,100

SEVERE

3,300

3,600

3,600

3,100

13,600

TOTAL

17,300

20,500

18,600

15,900

72,300

NON-TRADITIONAL MILITARY

200

400

500

500

1,600

EXPANSIONARY

7,200

7,300

7,600

7,400

29,500

WORLDWIDE TRUCK-Continued Ops

24,700

28,200

26,700

23,800

103,400

DISCONTINUED OPERATIONS

200

200

400

900

1,700

WORLDWIDE TRUCK-Total

24,900

28,400

27,100

24,700

105,100

FISCAL YEAR 2013

Q1

Q2

Q3

Q4

FULL YEAR

BUS

2,100

-

-

-

2,100

MEDIUM

4,100

-

-

-

4,100

HEAVY

4,500

-

-

-

4,500

SEVERE

2,400

-

-

-

2,400

TOTAL

13,100

-

-

-

13,100

NON-TRADITIONAL MILITARY

300

-

-

-

300

EXPANSIONARY

6,600

-

-

-

6,600

WORLDWIDE TRUCK-Continued Ops

20,000

-

-

-

20,000

DISCONTINUED OPERATIONS

200

-

-

-

200

WORLDWIDE TRUCK-Total

20,200

0

0

0

20,200 |

26

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

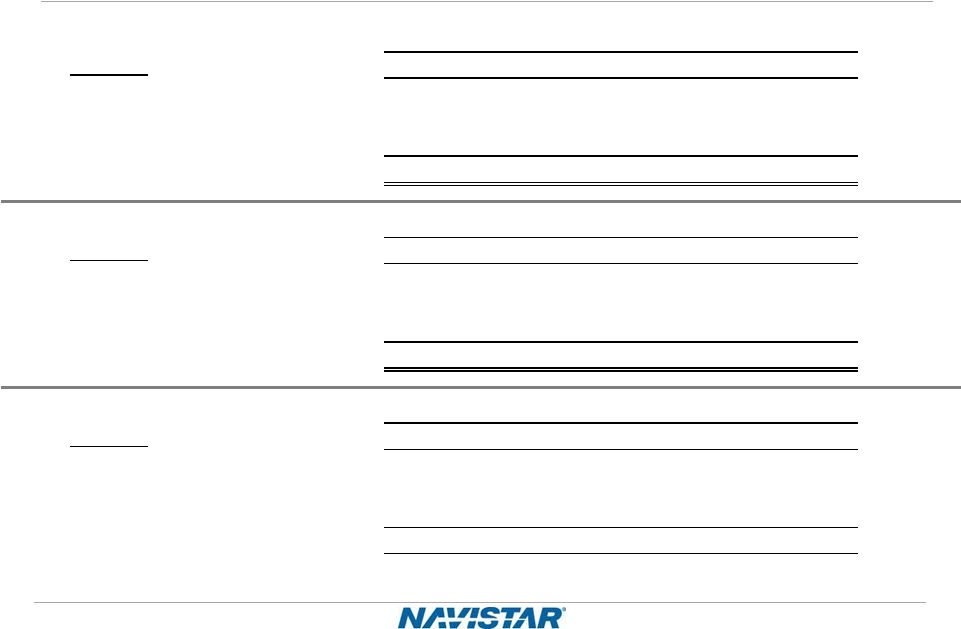

Navistar

Q1

Q2

Q3

Q4

Full Year

OEM sales - South America

27,200

37,100

38,200

36,100

138,600

Other OEM sales

4,500

4,400

3,700

3,600

16,200

Intercompany sales

17,300

23,500

22,300

25,700

88,800

Total Shipments

49,000

65,000

64,200

65,400

243,600

Navistar

Q1

Q2

Q3

Q4

Full Year

OEM sales - South America

24,100

25,300

28,600

28,700

106,700

Other OEM sales

2,200

2,000

3,000

2,900

10,100

Intercompany sales

21,600

23,400

20,600

17,500

83,100

Total Shipments

47,900

50,700

52,200

49,100

199,900

Navistar

Q1

Q2

Q3

Q4

Full Year

OEM sales - South America

25,700

-

-

-

25,700

Other OEM sales

1,900

-

-

-

1,900

Intercompany sales

16,400

-

-

-

16,400

Total Shipments

44,000

-

-

-

44,000

2013

2011

2012

Worldwide Engine Shipments |

27

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

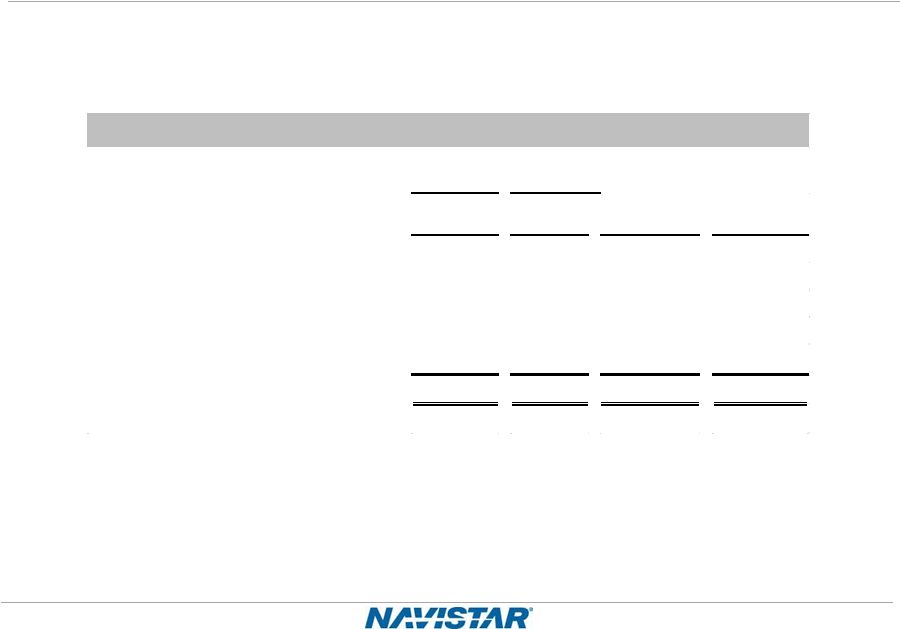

Order Receipts –

U.S. & Canada

(in units)

2012

2013

Change

Percentage

Change

"Traditional" Markets (U.S. and Canada)

School buses

2,100

1,500

(600)

-29%

Class 6 and 7 medium trucks

5,400

3,300

(2,100)

-39%

Class 8 heavy trucks

8,100

5,800

(2,300)

-28%

Class

8

severe

service

trucks

(A)

4,000

1,900

(2,100)

-53%

Total "traditional" markets

19,600

12,500

(7,100)

-36%

Combined class 8 trucks

12,100

7,700

(4,400)

-36%

Three Months Ended

January 31,

Order Receipts: U.S. & Canada (Units)

We define our “traditional” markets to include U.S. and Canada School bus and Class 6

through 8 medium and heavy truck. We classify militarized commercial vehicles sold to the U.S.

and Canadian militaries as Class 8 severe service within our “traditional” markets. Our

“traditional” markets include CAT-branded units sold to Caterpillar under our North

America supply agreement. |

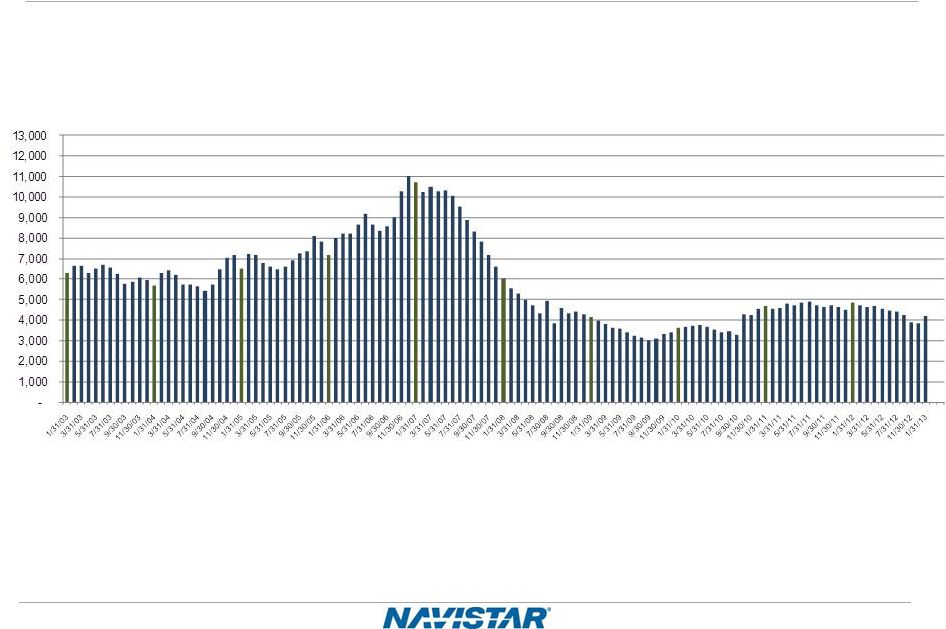

28

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

U.S. and Canada Dealer Stock Inventory*

*Includes U.S. and Canada Class 4-8 and school bus inventory, but does not

include U.S. IC Bus or Workhorse Custom Chassis inventory. Excludes the US

portion of IC Bus |

29

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Frequently Asked Questions

Q1:

What is included in Corporate and Eliminations?

A:

The primary drivers of Corporate and Eliminations are Corporate SG&A, pension

and OPEB expense (excluding amounts allocated to the segments), annual

incentive, manufacturing interest expense, and the elimination of intercompany sales and profit between

segments.

Q2:

What is included in your equity in loss of non-consolidated affiliates?

A:

Equity in loss of non-consolidated affiliates is derived from our ownership

interests in partially-owned affiliates that are not consolidated.

Q3:

What is your net income attributable to non-controlling interests?

A:

Net income attributable to non-controlling interests is the result of the

consolidation of subsidiaries in which we do not own 100%, and is primarily

comprised of Ford's non-controlling interest in our Blue Diamond Parts joint venture.

Q4:

How will the changing Department of Defense (DoD) budget affect Navistar in FY

2013? A:

We ended FY 2012 with approximately $1.1 billion in military revenues and based on

the current environment we expect military revenues for FY 2013 to be

approximately $750 million. The coming year will present challenges, but

Navistar’s commercial expertise

may

be

an

advantage

when

the

DoD

is

asked

to

“do

more

with

less.”

In

addition,

the

Company

continues

to

pursue

a

number of foreign military opportunities. Finally, the Company has a fleet of more

than 34,000 vehicles in operation in approximately 26 countries, including

more than 9,000 vehicles operating with Afghan Security Forces. These vehicles will require parts and

sustainment support throughout their lifecycles.

Q5:

How would Sequestration impact Navistar?

A:

The full impact of Sequestration is still not known. While we will likely see some

impact to the number of defense orders our business structure and product

portfolio lessen the risk. Q6:

What are your expected 2013 and beyond pension funding requirements?

A:

Future contributions are dependent upon a number of factors, principally the

changes in values of plan assets, changes in interest rates

and

the

impact

of

any

funding

relief

currently

under

consideration.

In

2013,

we

expect

to

contribute

$166

million

to

meet

the

minimum required contributions for all plans. We currently expect that from 2014

through 2016, the Company will be required to contribute

at

least

$200

million

per

year

in

to

the

Plans,

depending

on

asset

performance

and

discount

rates.

This

is

lower

than

our

previously

reported

expectations

due

to

the

impact

of

the

Moving

Ahead

for

Progress

in

the

21st

Century

Act

which

was

enacted

in

July 2012. |

30

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Frequently Asked Questions

Q7:

Why did the Company establish an additional valuation allowance on its domestic

deferred tax assets in the fourth quarter of 2012?

A:

On a quarterly basis, we are required to evaluate the need to establish a valuation

allowance for our deferred tax assets based on our assessment of whether it

is more likely than not that current or deferred tax benefits will be realized through the generation of

future taxable income. We give appropriate consideration to all available evidence,

both positive and negative, in assessing the need

for

a

valuation

allowance.

In

the

fourth

quarter

of

2012

we

concluded

that

with

the

continued

deterioration

of

our

domestic

performance and additional significant warranty charges, there was not sufficient

objective evidence of our ability to realize the benefits of domestic

deferred tax assets on a more likely than not basis and accordingly established a full domestic valuation

allowance.

Q8:

How will the establishment of the valuation allowance affect future tax expense?

A:

In the foreseeable future, our tax expense will be limited to our significant

foreign locations. Therefore, our effective tax rate could be impacted and

distortive in comparison to our peers without a valuation allowance. Q9:

What is your expectation for future cash tax payments?

A:

Our

cash

tax

payments

will

remain

low

in

2013

and

will

gradually

increase

as

we

utilize

available

net

operating

losses

(NOLs)

and

tax credits in the future years.

Q10:

What is the current balance of net operating losses as compared to other deferred tax

assets? A:

As of October 31, 2012 the Company has deferred tax assets for U.S. federal NOLs

valued at $319 million, state NOLs valued at $95

million,

and

foreign

NOLs

valued

at

$169

million,

for

a

total

undiscounted

cash

value

of

$583

million.

In

addition

to

NOLs,

the

Company has deferred tax assets for accumulated tax credits of $218 million and

other deferred tax assets of $2.1 billion resulting in net deferred tax

assets before valuation allowances of approximately $2.9 billion. Of this amount, $2.7 billion is subject to a valuation

allowance at the end of FY2012. |

31

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Frequently Asked Questions

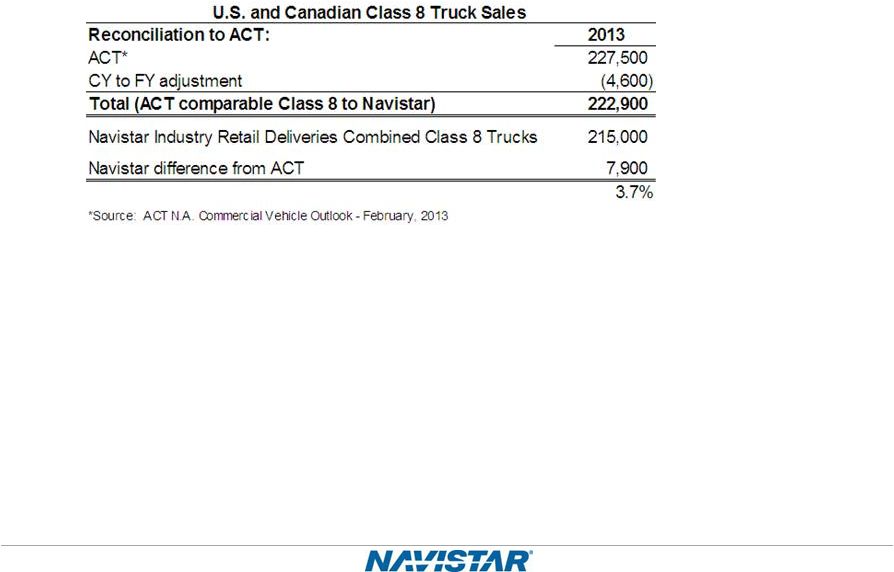

Q11:

How does your FY 2013 Class 8 industry compare to ACT Research?

A:

Q12:

What is your manufacturing interest expense for Fiscal Year 2013?

A:

Interest expense is forecasted at $242 million.

Q13:

What should we assume for capital expenditures in Fiscal Year 2013?

A:

We plan to continue capital spending within the traditionally guided range of $200

million to $300 million for products and development

although

we

expect

to

be

at

the

lower

end

of

the

range.

Capital

spending

related

to

Engineering

Integration

is

funded

through the RZFBs and is not included in that range. |

32

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Frequently Asked Questions

Q14:

For the manufacturing debt currently outstanding in your most recent financial

statement filings, what are the respective maturity dates and principal amounts

outstanding? A:

The amounts and maturity dates are as follows (the values shown below are the

amounts due and exclude the accounting impact of any OID or

bifurcation): Senior Secured Term Loan Credit Facility, due July 16,

2014 $998 million

8.25% Senior Notes due November 1, 2021

$900 million

3.0% Senior Subordinated Convertible Notes due October 15, 2014

$570 million

Debt of majority owned dealerships (various maturity dates)

$51 million

Financing arrangements and capital lease obligations (various maturity

dates) $93 million

Loan Agreement related to the 6.5% Tax Exempt Bonds due October 1, 2040

$225 million

Promissory Note due September 30, 2015

$28 million

Other (various maturity dates)

$68 million

Total

$2,933 million |

33

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

The

debt

balances

listed

above

include

accounting

impacts

of

any

OID

and

bifurcation.

Outstanding Debt Balances

Manufacturing operations:

Senior Secured Term Loan Credit Facility, due 2014, net of unamortized

discount of $9 and $8, respectively

………………………………………………………………………………………………..

$ 991

$

990 872

873

3.0% Senior Subordinated Convertible Notes, due 2014, net of

unamortized discount of $50 and $44, respectively

………………………………………………………………………………………………..

520

526

Debt of majority-owned dealerships

………………………………………………………………………

60

51

Financing arrangements and capital lease obligations

………………………………………………….…

140

93

Loan Agreement related to 6.5% Tax Exempt Bonds, due 2040

…………………………………….….…

225

225

Promissory Note

……………………………………………………………………………………..……

30

28

Other

…………………………………………………………………………………………………….…

67

68

Total manufacturing operations debt

………………………………………………………………..…

2,905

2,854

Less: Current portion

……………………………………………………………………………………...

172

125

Net long-term manufacturing operations debt

……………………………………………………..….

$ 2,733

$ 2,729

Financial Services operations:

Asset-backed debt issued by consolidated SPEs, at fixed and

variable rates, due serially through 2019

$ 994

$

811 763

726

Commercial paper, at variable rates, matured in 2013

………………………………………………...…

31

—

Borrowings secured by operating and finance leases, at various rates,

due serially through 2017 ……… 78

71

Total financial services operations debt

………………………………………………………………

1,866

1,608

Less: Current portion

…………………………………………………………………………..…………

1,033

811

Net long-term financial services operations debt

………………………………………..……………

$ 833

$

797 October

31,

2012

January 31,

2013

(in millions)

Bank revolvers, at fixed and variable rates, due dates from 2013

through 2019 …………………………

8.25% Senior Notes, due 2021, net of unamortized discount of $28 and

$27, respectively ……………… |

34

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

Manufacturing Cash Flow

Beginning Mfg. Cash

1

Balance

Fiscal 2010

Fiscal 2011

Fiscal 2012

Q1 2013

October 31, 2009

1,152

$

October 31, 2010

1,100

$

October 31, 2011

1,186

$

October 31, 2012

1,505

$

Approximate Cash Flows:

From Operations

409

680

(298)

(203)

From Investing / (Cap Ex)

(350)

(485)

(362)

(71)

From Financing / (Debt Pay Down)

(110)

(106)

977

(37)

Exchange Rate Effect

(1)

(3)

2

(5)

Net Cash Flow

(52)

$

86

$

319

$

(316)

$

Ending Mfg. Cash

1

Balance:

October 31, 2010

1,100

$

October 31, 2011

1,186

$

October 31, 2012

1,505

$

January 31, 2013

1,189

$

1

Cash = Cash, Cash Equivalents & Marketable Securities

|

35

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

SEC Regulation G Non-GAAP Reconciliation

The financial measures presented below are unaudited and not in accordance with, or an alternative for,

financial measures presented in accordance with U.S. generally accepted accounting principles

(GAAP). The non-GAAP financial information presented herein should be considered

supplemental to, and not as a substitute for, or superior to, financial measures calculated in accordance with

GAAP.

Manufacturing Segment Results: We believe

manufacturing segment results, which includes the segment results of our Truck, Engine, and Parts reporting segments,

provide meaningful information of our core manufacturing business and therefore we use it to

supplement our GAAP reporting by identifying items that may not be related to the core

manufacturing business. Management often uses this information to assess and measure the

performance of our operating segments. We have chosen to provide this supplemental information to investors, analysts

and other interested parties to enable them to perform additional analyses of operating results, to

illustrate the results of operations giving effect to the non-GAAP adjustments shown in the

below reconciliation, and to provide an additional measure of performance.

Earnings (loss) Before Interest, Income Taxes, Depreciation, and Amortization (“EBITDA”):

We define EBITDA as our consolidated net income (loss) from continuing operations attributable to

Navistar International Corporation, net of tax, plus manufacturing interest expense, income

taxes, and depreciation and amortization. We believe EBITDA provides meaningful information to

the performance of our business and therefore we use it to supplement our GAAP reporting. We have

chosen to provide this supplemental information to investors, analysts and other interested parties to

enable them to perform additional analyses of operating results.

Manufacturing Cash Flow and Manufacturing Cash, Cash Equivalents, and Marketable Securities: Manufacturing cash flow

is used and is presented to aid in developing an understanding of the ability of our operations to generate

cash for debt service and taxes, as well as cash for investments in working capital, capital

expenditures and other liquidity needs. This information is presented as a supplement to the

other data provided because it provides information which we believe is useful to investors for

additional analysis. Our manufacturing cash flow is prepared with marketable securities being treated as a cash

equivalent. Manufacturing cash, cash equivalents, and marketable securities represents the

Company’s consolidated cash, cash equivalents, and marketable securities excluding cash,

cash equivalents, and marketable securities of our financial services operations. We include

marketable securities with our cash and cash equivalents when assessing our liquidity position as our

investments are highly liquid in nature. We have chosen to provide this supplemental information to

investors, analysts and other interested parties to enable them to perform additional analyses

of operating results, to illustrate the results of operations giving effect to the non-GAAP

adjustments shown in the below reconciliation, and to provide an additional measure of performance. |

36

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

SEC Regulation G –

Manufacturing Cash Fiscal Year Comparison

Manufacturing cash, cash equivalents, and marketable securities reconciliation:

(Dollars in Millions)

October 31,

2010

October 31,

2011

October 31,

2012

January 31,

2013

Manufacturing segment cash and cash equivalents

534

$

488

$

1,059

$

438

$

Financial services segment cash and cash equivalents

51

51

28

59

Consolidated cash and cash equivalents

585

$

539

$

1,087

$

497

$

Manufacturing marketable securities

566

$

698

$

446

$

751

$

Financial services segment marketable securities

20

20

20

20

Consolidated marketable securities

586

$

718

$

466

$

771

$

Manufacturing segment cash and cash equivalents

534

$

488

$

1,059

$

438

$

Manufacturing marketable securities

566

698

446

751

Manufacturing segment cash, cash equivalents and marketable securities

1,100

$

1,186

$

1,505

$

1,189

$ |

37

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

SEC Regulation G –

Manufacturing Cash

(Dollars in Millions)

Manufacturing

Operations

Financial

Services

Operations

Adjustments

Condensed

Consolidated

Cash Flows

For the year ended October 31, 2010

Cash flows from operations

$ 409

$ 698

$

- $

1,107

Cash flows from investing / capital expenditures:

(350)

492

(576)

(434)

Cash flows from financing / debt pay down

(110)

(1,180)

(10)

(1,300)

Effect of exchange rate changes

(1)

1

-

-

Net cash flows

(52)

11

(586)

(627)

Beginning cash, cash equivalents and marketable securities

balance

1,152

60

-

1,212

Ending cash, cash equivalents and marketable securities balance

$ 1,100

$

71 $

(586) $

585 For the year ended October 31, 2011

Cash flows from operations

$ 680

$ 200

$

-

$ 880

Cash flows from investing / capital expenditures:

(485)

(206)

(132)

(823)

Cash flows from financing / debt pay down

(106)

6

-

(100)

Effect of exchange rate changes

(3)

-

-

(3)

Net cash flows

86

-

(132)

(46)

Beginning cash, cash equivalents and marketable securities

balance

1,100

71

(586)

585

Ending cash, cash equivalents and marketable securities balance

$

1,186

$

71

$

(718)

$

539

Manufacturing segment cash flow reconciliation: |

38

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

SEC Regulation G –

Manufacturing Cash

(Dollars in Millions)

Manufacturing

Operations

Financial

Services

Operations

Adjustments

Condensed

Consolidated

Cash Flows

For the year ended October 31, 2012

Cash flows from operations

$ (298)

$ 908

$

- $

610 Cash flows from investing / capital expenditures:

(362)

108

252

(2)

Cash flows from financing / debt pay down

977

(1,040)

-

(63)

Effect of exchange rate changes

2

1

-

3

Net cash flows

319

(23)

252

548

Beginning cash, cash equivalents and marketable securities

balance

1,186

71

(718)

539

Ending cash, cash equivalents and marketable securities balance

$ 1,505

$

48 $

(466) $ 1,087

For the three months ended January 31, 2013

Cash flows from operations

$ (203)

$ 269

$

-

$

66 Cash flows from investing / capital expenditures:

(71)

29

(305)

(347)

Cash flows from financing / debt pay down

(37)

(266)

-

(303)

Effect of exchange rate changes

(5)

(1)

-

(6)

Net cash flows

(316)

31

(305)

(590)

Beginning cash, cash equivalents and marketable securities

balance

1,505

48

(466)

1,087

Ending cash, cash equivalents and marketable securities balance

$ 1,189

$

79 $

(771) $

497 Manufacturing segment cash flow reconciliation: |

39

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

SEC Regulation G –

EBITDA reconciliation:

Three Months Ended

January 31,

(in millions)

2013

2012

Loss from continuing operations attributable to NIC, net of tax

$

)

$

(144

)

Plus:

Depreciation and amortization expense

……………...................................

78

Manufacturing interest expense

(A)

…........................................................

56

36

Less:

Income tax benefit (expense)

.................................................................

(15)

76

EBITDA

$

57

$

(106

)

(A)

Manufacturing interest expense is the net interest expense primarily generated

from borrowings that support our manufacturing and corporate operations,

adjusted to eliminate intercompany interest expense with our Financial Services segment. The

following table reconciles Manufacturing interest expense to the consolidated

interest expense. Three Months Ended

January 31,

(in millions)

2013

2012

Interest expense

...........................................................................................................................

$

74

$

61

Less:

Financial services interest

expense.....................................................................................

(18)

(25

)

Manufacturing

interest expense

…...............................................................................................

$

56

$

36

(114

100

Manufacturing segment profit (loss) reconciliation:

Three Months Ended

January 31,

(in millions)

2013

2012

Loss from continuing operations attributable to NIC, net of tax

.............................................................

$

(114)

$

(144)

Less:

Financial services segment profit

..................................................................................................

22

27

Corporate and eliminations

...........................................................................................................

(122

)

(150)

Income tax benefit (expense)

......................................................................................................

(15)

76

Manufacturing segment profit (loss)

.................................................................................................

$

1

$

(97)

.........................

................................

.................................................................................................

|

40

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

SEC Regulation G –

Significant Items included within our results:

Three Months Ended

January 31,

(in millions)

2013*

2012

Accelerated depreciation

(A)

..............................................................................................................

$

25

$

Charges for non-conformance penalties

(B)

......................................................................................

10

Legal settlement

(C)

...........................................................................................................................

(35)

Adjustments to pre-existing warranties

(D)

........................................................................................

—

8

Engineering integration costs

(E)

.......................................................................................................

—

______________

(A)

The charges for accelerated depreciation, of which $15 million was recognized in the Truck segment and

$10 million in the Engine segment, included $13 million for certain assets related to the

discontinuation of our MaxxForce15L engine and $12 million for certain assets related to the

planned closure of our Garland Facility. (B)

In the first quarter of 2013, our Engine segment recorded a charge of $10 million for NCPs, primarily

for certain 13L engine sales.

(C)

As a result of the legal settlement with Deloitte and Touch LLP in December 2012, we received cash

proceeds of $35 million, which was recorded as a gain to Other expense (income) in the first

quarter of 2013. (D)

The warranty adjustment represents an unanticipated increase in warranty spend for certain 2007 and

2010 emission standard engines, with the majority relating to the initial build of 2010

emission standard engines. Component complexity associated with meeting new emission standards

have contributed to higher repair costs, which have exceeded those that we have historically

experienced. In the first quarter of 2012, we recorded a charge for adjustments to

pre-existing warranties of $123 million, offset by a tax benefit of $42 million. Our Engine

segment recognized pre-tax charges of $112 million for adjustments to pre-existing

warranties.

(E)

Engineering integration costs relate to the consolidation of our truck and engine engineering

operations, as well as the relocation of our world headquarters. In the first quarter of 2012,

the charge included related costs of $12 million, offset by a tax benefit of $4 million. Our

Truck segment recognized pre-tax costs of $9 million relating to these actions in the first

quarter of 2012. *

There was no tax effect on the significant items included with our results in the first quarter of

2013, due to valuation allowance on our U.S. deferred tax assets.

|

41

NYSE: NAV

1Q 2013 Earnings –

3/7/2013

ROIC Definition

(PBT

1

+ Mfg Interest + Implied Interest on Operating Leases) X (1-Cash Tax

Rate) Paid-in-Capital –

Treasury Stock + Retained Earnings

2

+ Book Value of

Operating Leases + Book Value of Mfg Debt

3

–

Mfg Cash

4

1

–

Excludes significant items items such as restructuring, impairments, and

engineering integration expenses

2

–

If an Accumulated Deficit exists, then it will not be included in the

calculation 3

–

Excludes Financial Services Operation debt

4

–

Manufacturing Cash includes Cash and cash equivalents + Marketable

securities |