Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - REGIONS FINANCIAL CORP | d493509d8k.htm |

Citi

US Financial Services Conference

March 6, 2013

David Turner

Chief Financial Officer

1

Exhibit 99.1 |

Why

Regions? Competitive Position

•

Strong market presence

•

Competitive product set

•

Stronger company today than three years ago

•

Revenue growth on par with peers

•

Disciplined expense management

Opportunity for

Outperformance

•

Improving efficiency ratio

•

Stable net interest margin

•

Significant credit leverage remains

•

Low loan to deposit ratio

Moving Forward

•

Creating shared value for our customers, communities,

associates and shareholders

•

Business plan to support growth

2

Proven Track Record |

A

leading southeastern banking franchise Company Snapshot

December 2012

Associates

23,427

Assets

$121B

Loans

$74B

Deposits

$95B

Branches

1,711

ATMs

2,054

Market Cap*

$10.8B

* As of February 27, 2013

Regions Branches

Deposit Market Share

Regions Insurance Group

3

#1

#2

#1

#1

#6

#4

#4

#

•

14 largest full-service bank

•

Operating in sixteen states; however,

seven states represent 85% of total

deposits

•

Primary business lines: Consumer

Services, Business Services and

Wealth Management

•

Full line insurance brokerage firm

offering all lines of personal and

commercial insurance

th |

4

Top 10 MSAs

Deposits

Market

Rank

’10-’15

Population

Growth

Birmingham, AL

$10.1

1

Nashville, TN

$7.0

1

Tampa, FL

$5.0

4

Miami, FL

$4.0

11

Memphis, TN

$3.9

2

Atlanta, GA

$3.3

6

St. Louis, MO

$3.0

4

Jackson, MS

$2.9

2

New Orleans, LA

$2.4

4

Mobile, AL

$2.3

1

($ in billions)

National Average: 3.9%

Source: SNL Financial

Note: Core Markets include AL, FL, LA, MS, AR, TN

Rank

Name

Market

Share

1

Bank of America

11.1%

2

Wells Fargo

9.9%

3

Regions

9.4%

4

SunTrust

6.7%

5

JPMorgan Chase

3.8%

6

BB&T

3.0%

7

Capital One

2.2%

8

First Horizon

2.0%

9

Hancock

1.7%

10

Citi

1.6%

Weighted Average Deposit

Market Share in Regions’

Core Markets

Characterized by high market share, high growth markets

3.4%

9.6%

3.7%

1.4%

4.3%

10.1%

2.0%

4.4%

8.8%

1.0%

Footprint positioning |

5

Balance Sheet

4Q12

4Q09

Improvement

Deposit Costs

0.22%

1.15%

93 bps

Total Funding Costs

0.50%

1.45%

95 bps

Time Deposits as % of Total Deposits

14%

32%

Reduced by half

Low-Cost Deposits

$82.0B

$67.1B

22%

Profitability

Mortgage Revenue

$90MM

$46MM

96%

Net Interest Margin

(1)

3.10%

2.72%

38 bps

Efficiency Ratio

(2)

64.42%

67.88%

346 bps

Credit Risk Profile

Non-Performing Assets

$1.9B

$4.4B

57%

Net Charge-Offs

$180MM

$692MM

74%

Allowance for Loan Losses / Loans

2.59%

3.43%

84 bps

Capital and Liquidity

Tier 1 Common Ratio

(3)

10.8%

7.1%

370 bps

Loan to Deposit Ratio

78%

92%

More liquid

Stronger company today

(1)

4Q12 from continuing operations; 4Q09 as reported

(2)

Annual Ratio

(3)

Non-GAAP -

see appendix for reconciliation |

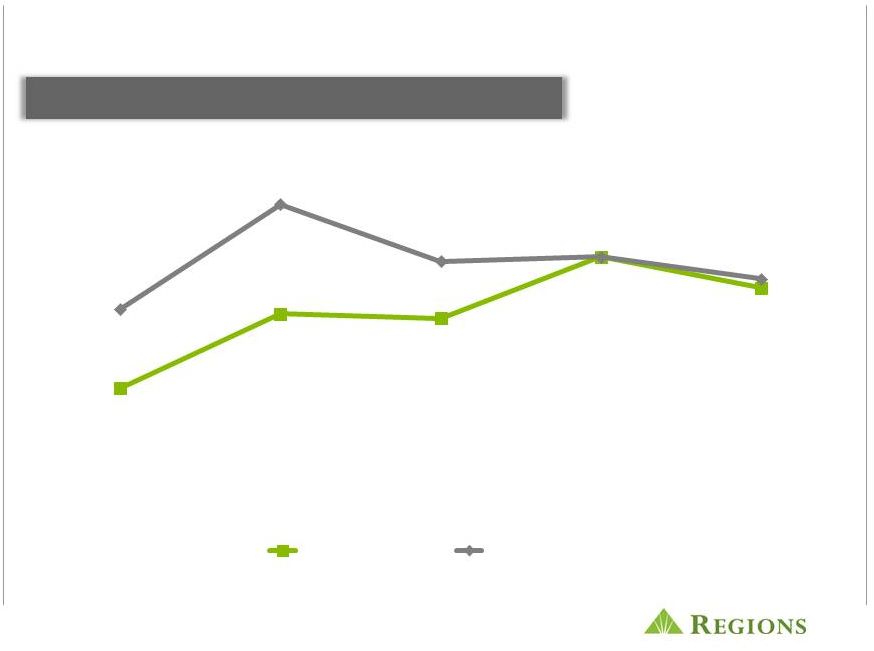

6

Revenue growth –

continuing to make progress

Peer banks include BBT, CMA, FHN, FITB, HBAN, KEY, MTB, PNC, STI, USB, WFC,

ZION Note: Net interest income on FTE basis and non-interest revenue

adjusted to exclude non-recurring items Source: SNL Financial

Growth in Total Revenue Linked Quarter vs Peers

-2.0%

-0.3%

-0.4%

1.0%

0.3%

-0.2%

2.2%

0.9%

1.0%

0.5%

4Q11

1Q12

2Q12

3Q12

4Q12

Regions

Peer Median |

Regions has the second lowest expense to assets

ratio vs peers and reduced expenses faster than

almost all our peers

Non-Interest Expense

(1)

/ Average Assets

Full Year 2012 vs. Full Year 2011 % Change

2.6%

2.8%

3.0%

3.0%

3.1%

3.2%

3.3%

3.4%

3.5%

3.5%

3.5%

3.9%

4.3%

Bank

#1

RF

Bank

#3

Bank

#4

Bank

#5

Bank

#6

Bank

#7

Bank

#8

Bank

#9

Bank

#10

Bank

#11

Bank

#12

Bank

#13

-4%

-2%

-1%

0%

2%

4%

4%

4%

5%

5%

9%

11%

12%

Bank

#1

RF

Bank

#3

Bank

#4

Bank

#5

Bank

#6

Bank

#7

Bank

#8

Bank

#9

Bank

#10

Bank

#11

Bank

#12

Bank

#13

7

(1) 4Q12 Adjusted to exclude non-core items, ratios are annualized –

Peer banks include: BBT, CMA, FHN, FITB, HBAN, KEY, MTB, PNC, STI, USB, WFC, ZION

Source: SNL Financial

See

appendix

for

reconciliation |

8

Focused on improved efficiency

(1) Non-GAAP –

See appendix for reconciliation

Note: Results from Continuing Operations

Peer banks include: BBT, CMA, FHN, FITB, HBAN, KEY, MTB, PNC, STI, USB, WFC, ZION

Source: SNL Financial

Target:

Mid to High

50s

Efficiency Ratio

(1)

70.1%

67.9%

64.6%

65.0%

64.2%

65.3%

62.8%

64.3%

62.7%

4Q11

1Q12

2Q12

3Q12

4Q12

Regions

Peer Median

64.3% |

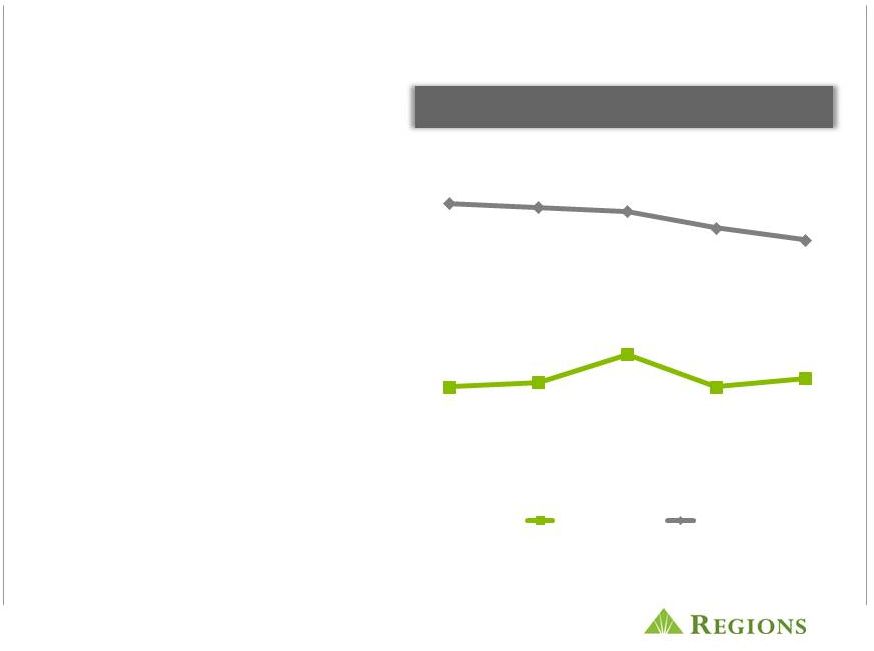

•

Net interest margin was up 2

bps linked quarter, primarily

due to lower deposit costs

and interest recoveries

•

Opportunities to protect the

margin through:

•

Continued reduction of

deposit costs

•

Retention of 15-year

fixed rate mortgages

•

Liability management

opportunities

•

Outlook is for a relatively

stable margin in 2013

Net interest margin improves

Note: Peer banks include BBT, CMA, FHN, FITB, HBAN, KEY, MTB, PNC, STI, USB, WFC,

ZION Source: SNL Financial

Net Interest Margin vs. Peers

4Q11

1Q12

2Q12

3Q12

4Q12

3.53%

3.51%

3.52%

3.44%

3.47%

3.08%

3.16%

3.09%

3.10%

3.08%

Regions

Peer Average

9 |

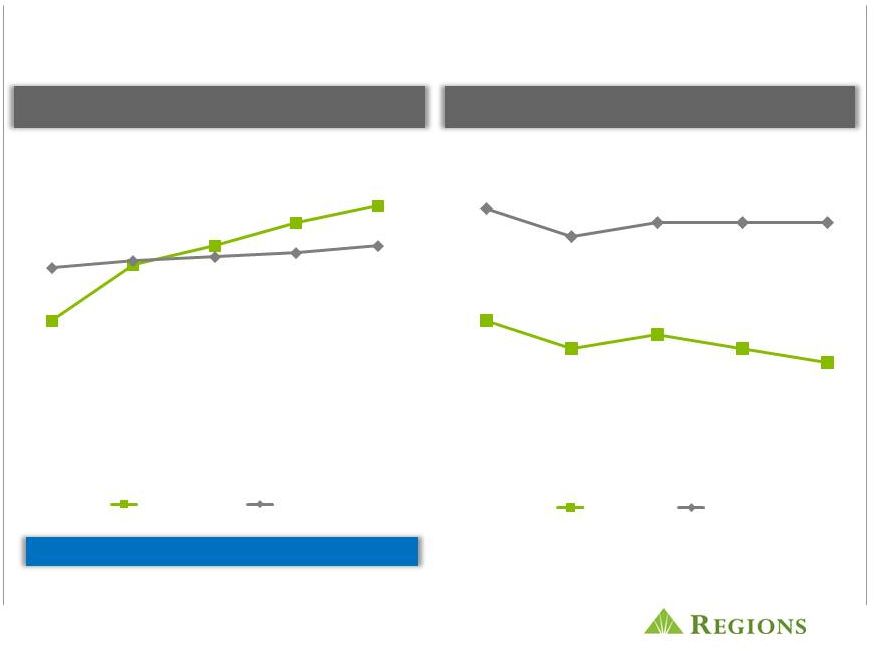

Continued asset quality improvement

Significant credit leverage remains

Note: Peer banks include BBT, CMA, FHN, FITB, HBAN, KEY, MTB, PNC, STI, USB, WFC,

ZION Source: SNL Financial

58% decrease Y-O-Y

Allowance for Loan Losses / Total Loans

Net Charge-Offs and Ratio

($ in millions)

10

$430

$332

$265

$262

$180

2.16%

1.73%

1.39%

1.38%

0.96%

4Q11

1Q12

2Q12

3Q12

4Q12

Net Charge-Offs

Net Charge-Offs as % of Average Loans

3.54%

2.59%

2.34%

1.89%

4Q11

1Q12

2Q12

3Q12

4Q12

Regions

Peer Group Median |

11

(1)

Non-GAAP

–

See

appendix

for

reconciliation

Note: Peer banks include BBT, CMA, FHN, FITB, HBAN, KEY, MTB, PNC, STI, USB, WFC,

ZION Source: SNL Financial

Estimated Basel III

(1)

at the end of 4Q12 was 8.9%

Loan to Deposit Ratio

Tier 1 Common Ratio

(1)

8.5%

9.6%

10.0%

10.5%

10.8%

9.6%

9.7%

9.8%

9.9%

10.0%

4Q11

1Q12

2Q12

3Q12

4Q12

Regions

Peer Median

81%

79%

80%

79%

78%

89%

87%

88%

88%

88%

4Q11

1Q12

2Q12

3Q12

4Q12

Regions

Peer Median

Solid capital and liquidity |

12

•

Getting

a

full

and

detailed

view

of

customer

financial

needs

–

360°

View

•

Deepening customer relationships through cross-sell

•

Going

to

market

as

One

bank,

One

team,

One

Regions

–

making referrals

and meeting needs

•

Providing service quality that creates exceptional loyalty and retention

communities, our associates and our

shareholders through…

Creating

for our customers, our

shared value |

13

Transportation/

Restaurant

Technology &

Defense

Energy

Healthcare

(Houston)

(Atlanta)

(Charlotte)

(Nashville)

Business Services –

key focus areas for 2013

•

Acquire, retain and deepen

relationships through

•

Maintain disciplined focus on

specialized industries to drive

growth:

•

Healthcare

•

Restaurant

•

Transportation

•

Technology & Defense

•

Energy

•

We are still in the Investor Real

Estate business, where appropriate

•

Get paid for the risks we take

•

Stay focused on prudent Risk

Management disciplines

Transition to growth through shared value |

14

Wealth Management -

key focus areas for 2013

•

Broaden and deepen relationships

•

Grow trust assets under management

•

Roll out branch-based Financial Consultants in

partnership with Cetera

•

Enhance performance management and

coaching culture

•

Stay focused on prudent risk management

disciplines

•

Listen

to

customers’

goals

and

deliver

products

and services they need

•

Expand service and product offerings

Transition to growth through shared value |

•

Deepen relationships

•

Attract, retain and expand quality consumer

households

•

Stabilize

and

grow

quality

earning

assets

–

get

paid for the risks we take

•

Leverage NOW Banking products to bank the

under-banked markets

•

Continue to prudently grow credit cards,

mortgage and indirect lending

•

Remain focused on disciplined risk management,

compliance and regulatory issues

•

Provide trustworthy advice, guidance and

education to help our customers succeed

financially

•

Leverage technology to improve channel

capabilities, sales and efficiency

Consumer Services –

key focus areas for 2013

Transition to growth through shared value

15 |

Moving

forward in 2013 •

Through

, maximize opportunities to deepen quality customer relationships •

Grow households

•

Positioned for continued increases in loan production

•

Indirect auto portfolio

•

Commercial and Industrial

•

Credit card

•

Retention of 15-year fixed rate mortgages

•

Continue to leverage Now Banking suite of products

•

Improve efficiency through investments in technology

•

Further enhancements to lower-cost delivery channels

•

Enhanced services and technology platforms within Wealth Management

•

Continue to seek opportunities to reduce expenses

•

Commitment to positive operating leverage

16 |

Why

Regions? Competitive Position

•

Strong market presence

•

Competitive product set

•

Stronger company today than three years ago

•

Revenue growth on par with peers

•

Disciplined expense management

Opportunity for

Outperformance

•

Improving efficiency ratio

•

Stable net interest margin

•

Significant credit leverage remains

•

Low loan to deposit ratio

Moving Forward

•

Creating shared value for our customers, communities,

associates and shareholders

•

Business plan to support growth

17

Proven Track Record |

Appendix

18 |

The

foregoing list of factors is not exhaustive. For discussion of these and other factors that may cause actual results to differ from expectations, look under

the captions “

Forward-Looking Statements”

and “

Risk Factors" of Regions' Annual Report on Form 10-K for the year ended December 31,

2012. This

presentation

may

include

forward-looking

statements

which

reflect

Regions’

current

views

with

respect

to

future

events

and

financial

performance.

The

Private

Securities

Litigation

Reform

Act

of

1995

(“the

Act”)

provides

a

“safe

harbor”

for

forward-looking

statements

which

are

identified

as

such

and

are

accompanied

by

the

identification

of

important

factors

that

could

cause

actual

results

to

differ

materially

from

the

forward-looking

statements.

For

these

statements,

we,

together

with

our

subsidiaries,

claim

the

protection

afforded

by

the

safe

harbor

in

the

Act.

Forward-looking

statements

are

not

based

on

historical

information,

but

rather

are

related

to

future

operations,

strategies,

financial

results

or

other

developments.

Forward-looking

statements

are

based

on

management’s

expectations

as

well

as

certain

assumptions

and

estimates

made

by,

and

information

available

to,

management

at

the

time

the

statements

are

made.

Those

statements

are

based

on

general

assumptions

and

are

subject

to

various

risks,

uncertainties

and

other

factors

that

may

cause

actual

results

to

differ

materially

from

the

views,

beliefs

and

projections

expressed

in

such

statements.

These

risks,

uncertainties

and

other

factors

include,

but

are

not

limited

to,

those

described

below:

Forward-looking statements

›

Possible acceleration of prepayments on mortgage-backed securities due to low interest

rates and the related acceleration of premium amortization on those securities.

›

The Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank

Act”) became law in July 2010, and a number of legislative, regulatory and

tax proposals remain pending. Future and proposed rules, including those that may be part of the Basel III process, are expected to require banking

institutions to increase levels of capital and to meet more stringent liquidity requirements.

All of the foregoing may have significant effects on Regions and the financial

services industry, the exact nature and extent of which cannot be determined at this time.

›

Regions' ability to develop competitive new products and services in a timely manner and the

acceptance of such products and services by Regions' customers and potential

customers. ›

Regions' ability to keep pace with technological changes.

›

Possible additional loan losses, impairment of goodwill and other intangibles, and adjustment

of valuation allowances on deferred tax assets and the impact on earnings and

capital. ›

Possible

changes

in

interest

rates

may

increase

funding

costs

and

reduce

earning

asset

yields,

thus

reducing

margins.

Increases

in

benchmark

interest

rates

would also increase debt service requirements for customers whose terms include a variable

interest rate, which may negatively impact the ability of borrowers to pay as

contractually obligated. ›

Possible

changes

in

general

economic

and

business

conditions

in

the

United

States

in

general

and

in

the

communities

Regions

serves

in

particular,

including

any prolonging or worsening of the current challenging economic conditions including

unemployment levels. ›

Possible changes in consumer and business spending and saving habits could affect Regions'

ability to increase assets and to attract deposits. ›

Possible changes in the creditworthiness of customers and the possible impairment of the

collectability of loans. ›

Possible changes in trade, monetary and fiscal policies, laws and regulations and other

activities of governments, agencies, and similar organizations, may have an adverse

effect on business. ›

Possible stresses in the financial and real estate markets, including possible deterioration

in property values. ›

Regions' ability to manage fluctuations in the value of assets and liabilities and

off-balance sheet exposure so as to maintain sufficient capital and liquidity to

support Regions' business.

›

Regions' ability to expand into new markets and to maintain profit margins in the face of

competitive pressures. ›

The effects of any damage to Regions reputation resulting from developments related to any of

the items identified above. ›

Possible regulations issued by the Consumer Financial Protection Bureau or other regulators

which might adversely impact Regions' business model or

products and services.

›

Regions' ability to effectively manage credit risk, interest rate risk, market risk,

operational risk, legal risk, liquidity risk, reputational risk, counterparty risk,

international risk and regulatory and compliance risk.

›

Regions’

ability to ensure adequate capitalization which is impacted by inherent uncertainties in

forecasting credit losses. ›

The

cost

and

other

effects

of

material

contingencies,

including

litigation

contingencies,

and

any

adverse

judicial,

administrative

or

arbitral

rulings

or

proceedings.

›

The effects of increased competition from both banks and non-banks.

›

The effects of geopolitical instability and risks such as terrorist attacks.

›

Changes

in

accounting

policies

or

procedures

as

may

be

required

by

the

Financial

Accounting

Standards

Board

or

other

regulatory

agencies.

›

Regions’

ability to receive dividends from its subsidiaries.

›

The

effects

of

the

failure

of

any

component

of

Regions’

business

infrastructure

which

is

provided

by

a

third

party.

›

The effects of weather and natural disasters such as floods, droughts, wind, tornados and

hurricanes, and the effects of man-made disasters. ›

Possible downgrades in ratings issued by rating agencies.

›

The effects of problems encountered by larger or similar financial institutions that

adversely affect Regions or the banking industry generally. ›

Possible

changes

in

the

speed

of

loan

prepayments

by

Regions’

customers

and

loan

origination

or

sales

volumes.

19

The words "believe," "expect," "anticipate," "project," and

similar expressions often signify forward-looking statements. You should not place

undue reliance on any forward-looking statements, which speak only as of the date made.

We assume no obligation to update or revise any forward-looking statements that

are made from time to time. |

Non-GAAP reconciliation: non-interest income /

expense, fee income ratios and efficiency ratios

($ amounts in millions)

12/31/12

9/30/12

6/30/12

3/31/12

12/31/11

Continuing Operations

Non-interest expense (GAAP)

902

$

869

$

842

$

913

$

1,124

$

33

$

3.8%

(222)

$

-19.8%

Adjustments:

REIT investment early termination costs

(42)

-

-

-

-

(42)

NM

(42)

NM

Loss on early extinguishment of debt

(11)

-

-

-

-

(11)

NM

(11)

NM

Securities impairment, net

-

-

(2)

-

(2)

-

-

2

-100.0%

Branch consolidation and property and equipment charges

-

-

-

-

2

-

-

(2)

-100.0%

Goodwill impairment

-

-

-

-

(253)

-

-

253

-100.0%

Adjusted non-interest expense (non-GAAP)

F

849

$

869

$

840

$

913

$

871

$

(20)

$

-2.3%

(22)

$

-2.5%

Net interest income (GAAP)

818

$

817

$

838

$

827

$

849

$

1

$

0.1%

(31)

$

-3.7%

Taxable equivalent adjustment

13

13

12

12

9

-

-

4

44.4%

Net interest income, taxable-equivalent basis

831

830

850

839

858

1

0.1%

(27)

-3.1%

Non-interest income (GAAP)

536

$

533

$

507

$

524

$

507

$

3

$

0.6%

29

$

5.7%

Adjustments:

Securities gains, net

(12)

(12)

(12)

(12)

(7)

-

-

(5)

71.4%

Leveraged lease termination gains, net

-

-

(7)

(7)

(10)

-

-

10

-100.0%

Adjusted non-interest income (non-GAAP)

G

524

521

488

505

490

3

0.6%

34

6.9%

Adjusted total revenue (non-GAAP)

H

1,355

$

1,351

$

1,338

$

1,344

$

1,348

$

4

$

0.3%

7

$

0.5%

Adjusted fee income ratio (non-GAAP)

G/H

38.7%

38.6%

36.5%

37.6%

36.4%

Adjusted efficiency ratio (non-GAAP)

F/H

62.7%

64.3%

62.8%

67.9%

64.6%

Quarter Ended

vs. 3Q12

vs. 4Q11

4Q12

4Q12

20

The table below presents computations of the efficiency ratio(non-GAAP), which is a

measure of productivity, generally calculated as non-interest expense divided by total revenue. The table also shows the fee income

ratio ratio (non-GAAP), generally calculated as non-interest income divided by total

revenue. Management uses these ratios to monitor performance and believes these measures provide meaningful information to

investors. Non-interest-expense (GAAP) is presented excluding certain

adjustments to arrive at adjusted non-interest expense (non-GAAP), which is the numerator for the efficiency ratio. Non-interest income (GAAP) is

presented excluding certain adjustments to arrive at adjusted non-interest income

(non-GAAP), which is the numerator for the fee income ratio. Net interest income on a taxable-equivalent basis and non-interest income

are added together to arrive at total revenue. Adjustments are made to arrive at

adjusted total revenue (non-GAAP), which is the denominator for the fee income and efficiency ratios. Regions believes that the exclusion

of these adjustments provides a meaningful base for period-to-period comparisons,

which management believes will assist investors in analyzing the operating results of the Company and predicting future performance.

These non-GAAP financial measures are also used by management to assess the performance

of Regions' business. It is possible that the activities related to the adjustments may recur; however, management does not

consider the activities related to the adjustments to be indications of ongoing

operations. Regions believes that presentation of these non-GAAP financial measures will permit investors to assess the performance of the

Company on the same basis as that applied by management. |

21

Non-GAAP reconciliation: tier 1 common

($ amounts in millions)

12/31/12

9/30/12

6/30/12

3/31/12

12/31/11

As of and for Quarter Ended

TIER 1 COMMON RISK-BASED RATIO - CONSOLIDATED

Stockholders' equity (GAAP)

15,499

$

14,901

$

14,455

$

17,534

$

16,499

$

Accumulated other comprehensive (income) loss

(65)

(202)

(54)

60

69

Non-qualifying goodwill and intangibles

(4,826)

(4,836)

(4,852)

(4,881)

(4,900)

Disallowed deferred tax assets

(35)

(238)

(336)

(345)

(432)

Disallowed servicing assets

(33)

(33)

(33)

(36)

(35)

Qualifying non-controlling interests

93

93

92

92

92

Qualifying trust preferred securities

501

846

846

846

846

Tier 1 capital (regulatory)

11,134

$

10,531

$

10,118

$

13,270

$

12,139

$

Qualifying non-controlling interests

(93)

(93)

(92)

(92)

(92)

Qualifying trust preferred securities

(501)

(846)

(846)

(846)

(846)

Preferred stock

(482)

-

-

(3,429)

(3,419)

Tier 1 common equity (non-GAAP)

N

10,058

$

9,592

$

9,180

$

8,903

$

7,782

$

Risk-weighted assets (regulatory)

O

92,811

91,723

91,779

92,546

91,449

Tier 1 common risk-based ratio (non-GAAP)

N/O

10.8%

10.5%

10.0%

9.6%

8.5%

The following table provides calculations of Tier 1 capital (regulatory) and "Tier 1 common

equity" (non-GAAP). Traditionally, the Federal Reserve and other banking

regulatory bodies have assessed a bank's capital adequacy based on Tier 1 capital, the calculation of

which is prescribed in amount by federal banking regulations. In connection with the

Company's Comprehensive Capital Analysis and Review ("CCAR"), these regulators are supplementing their assessment of the capital

adequacy of a bank based on a variation of Tier 1 capital, known as Tier 1 common equity. While

not prescribed in amount by federal banking regulations, analysts and banking regulators have

assessed Regions' capital adequacy using the Tier 1 common equity measure. Because Tier 1 common equity is not formally defined

by GAAP or prescribed in any amount by federal banking regulations, this measure is considered to be a

non-GAAP financial measure and other entities may calculate it differently than Regions'

disclosed calculations. Since analysts and banking regulators may assess Regions' capital adequacy using Tier 1 common

equity, management believes that it is useful to provide investors the ability to assess Regions'

capital adequacy on this same basis. Tier 1 common equity is often expressed as a percentage of risk-weighted assets. Under the

risk-based capital framework, a company's balance sheet assets and credit equivalent

amounts of off-balance sheet items are assigned to one of four broad risk categories. The aggregated dollar amount in each category is then

multiplied by the risk-weighted category. The resulting weighted values from each of the

four categories are added together and this sum is the risk-weighted assets total that, as

adjusted, comprises the denominator of certain risk-based capital ratios. Tier 1 capital is then divided by this denominator (risk-weighted assets) to

determine the Tier 1 capital ratio. Adjustments are made to Tier 1 capital to arrive at Tier 1

common equity (non-GAAP). Tier 1 common equity (non-GAAP) is also divided by the

risk-weighted assets to determine the Tier 1 common equity ratio (non-GAAP). The amounts disclosed as risk-weighted assets are calculated

consistent with banking regulatory requirements.

|

Non-GAAP reconciliation: basel III

Estimate based on June

2012 U.S. Notices of

Proposed Rulemaking

($ amounts in millions)

12/31/2012

Stockholders' equity (GAAP)

$15,499

(4,968)

Adjustments, including other comprehensive income related to cash flow hedges,

disallowed deferred tax assets, threshold deductions and other

adjustments (780)

Basel III tier 1 common equity (non-GAAP)

9,751

Basel I risk-weighted assets (regulatory)

92,811

109,941

Basel III tier 1 common ratio (non-GAAP)

8.87%

The following table provides calculations of Tier 1 common, based on Regions’ current

understanding of Basel III requirements, as proposed by the U.S. Notices of Proposed Rulemaking

released in June 2012. Regions currently calculates its risk-based capital ratios under guidelines adopted by the Federal Reserve

based on the 1988 Capital Accord (“Basel I”) of the Basel Committee on Banking Supervision

(the “Basel Committee”). In December 2010, the Basel Committe released its final

framework for Basel III, which will strengthen international capital and liquidity regulation. In June 2012, U.S. Regulators released three

separate Notices of Proposed Rulemaking covering U.S. implementation of the Basel III

framework. When implemented by U.S. bank regulatory agencies and fully

phased-in, Basel III will change capital requirements and place greater emphasis on common equity. The Federal Reserve has announced a delay in the

implementation date of the final rules. However, when implemented there will be a phase in

period of up to 6 years. The calculations provided below are estimates, based on

Regions’ current understanding of the framework, including the Company’s reading of the requirements, and informal feedback received

through the regulatory process. Regions’ understanding of the framework is evolving and

will likely change as the regulations are finalized. Because the Basel III implementation

regulations are not formally defined by GAAP and have not yet been finalized and codified, these measures are considered to be non-GAAP

financial measures, and other entities may calculate them differently from Regions’ disclosed

calculations. Since analysts and banking regulators may assess Regions’ capital

adequacy using the Basel III framework, we believe that it is useful to provide investors the ability to assess Regions’ capital adequacy on the

same basis.

22

(1)

Under Basel III, regulatory capital must be reduced by purchased credit card relationship intangible

assets. These assets are partially allowed in Basel I capital.

(2)

Regions continues to develop systems and internal controls to precisely calculate risk-weighted

assets as required by Basel III. The amount included above is a reasonable approximation,

based on our understanding of the requirements. Non-qualifying

goodwill

and

intangibles

(1)

Basel

III risk-weighted assets (non-GAAP)

(2) |

|