Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - HERON THERAPEUTICS, INC. /DE/ | Financial_Report.xls |

| EX-23.1 - EX-23.1 - HERON THERAPEUTICS, INC. /DE/ | d493558dex231.htm |

| EX-32.1 - EX-32.1 - HERON THERAPEUTICS, INC. /DE/ | d493558dex321.htm |

| EX-31.2 - EX-31.2 - HERON THERAPEUTICS, INC. /DE/ | d493558dex312.htm |

| EX-31.1 - EX-31.1 - HERON THERAPEUTICS, INC. /DE/ | d493558dex311.htm |

| EX-10.AG - EX-10.AG - HERON THERAPEUTICS, INC. /DE/ | d493558dex10ag.htm |

| EX-10.AH - EX-10.AH - HERON THERAPEUTICS, INC. /DE/ | d493558dex10ah.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

FOR ANNUAL & TRANSITION REPORTS PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

(MARK ONE)

[ x ] Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2012

or

[ ] Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from to

Commission File Number: 001-33221

A.P. PHARMA, INC.

(Exact name of registrant as specified in its charter)

| DELAWARE | 94-2875566 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

| 123 SAGINAW DRIVE, REDWOOD CITY, CALIFORNIA | 94063 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code:

(650) 366-2626

Securities registered pursuant to Section 12(b) of the Act:

NONE

Securities registered pursuant to Section 12(g) of the Act:

COMMON STOCK

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Exchange Act. Yes [ ] No [ x ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes [ ] No [ x ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ x ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [ x ] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check One)

Large accelerated filer [ ] Accelerated filer [ x ] Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [ x ]

The aggregate market value of the voting and non-voting common equity of the registrant held by non-affiliates of the registrant as of June 30, 2012 was $76,584,169(1) based upon the closing sale price on OTCQB reported for such date.

As of February 27, 2013, 305,628,293 shares of registrant’s Common Stock, $.01 par value, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required to be disclosed in Part III of this report is incorporated by reference from the registrant’s definitive Proxy Statement for the 2013 Annual Meeting of Stockholders, which proxy statement will be filed not later than 120 days after the end of the fiscal year covered by this report.

| (1) | Excludes 88,403,848 shares held by directors, officers and stockholders whose ownership exceeds 10% of the outstanding shares at June 30, 2012. Exclusion of such shares should not be construed as indicating that the holders thereof possess the power, directly or indirectly, to direct the management or policies of the registrant, or that such person is controlled by or under common control with the registrant. |

Table of Contents

| ITEM 1. |

4 | |||

| ITEM 1A. |

21 | |||

| ITEM 1B. |

40 | |||

| ITEM 2. |

40 | |||

| ITEM 3. |

40 | |||

| ITEM 4. |

40 | |||

| PART II | ||||

| ITEM 5. |

Market for the Registrant’s Common Stock, Related Stockholder Matters and Issuer Purchases of Equity Securities | 41 | ||

| ITEM 6. |

42 | |||

| ITEM 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

43 | ||

| ITEM 7A. |

50 | |||

| ITEM 8. |

51 | |||

| ITEM 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

76 | ||

| ITEM 9A. |

76 | |||

| ITEM 9B. |

77 | |||

| PART III | ||||

| ITEM 10. |

78 | |||

| ITEM 11. |

78 | |||

| ITEM 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

78 | ||

| ITEM 13. |

Certain Relationships and Related Transactions, and Director Independence |

78 | ||

| ITEM 14. |

78 | |||

| PART IV | ||||

| ITEM 15. |

79 | |||

| 80 | ||||

| 81 | ||||

2

Table of Contents

PART I

Introduction—Forward-Looking Statements

In this Annual Report on Form 10-K, the “Company,” “A.P. Pharma,” “we,” “us” and “our” refer to A.P. Pharma, Inc.

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended. All statements contained in this Form 10-K, other than statements of historical fact, are forward-looking statements. When used in this report or elsewhere by management from time to time, the words “believe,” “anticipate,” “intend,” “plan,” “estimate,” “expect,” “may,” “will,” “should,” “seeks” and similar expressions are forward-looking statements. Such forward-looking statements are based on current expectations, but the absence of these words does not necessarily mean that a statement is not forward-looking. Forward-looking statements made in this Form 10-K include, but are not limited to, statements about:

• uncertainties associated with the FDA’s response to our resubmitted New Drug Application;

• the progress of our research, development and clinical programs and timing of, and prospects for, regulatory approval and commercial introduction of APF530 and other future product candidates;

• the timing of market introduction of APF530 or other future product candidates;

• our ability to market, commercialize and achieve market acceptance for APF530 or other future product candidates;

• our ability to establish collaborations for our technology, APF530 and other future product candidates;

• uncertainties associated with obtaining and enforcing patents;

• our estimates for future performance; and

• our estimates regarding our capital requirements and our needs for, and ability to obtain, additional financing.

Forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Actual events or results may differ materially from those discussed in the forward-looking statements as a result of various factors. For a more detailed discussion of such forward-looking statements and the potential risks and uncertainties that may impact our actual results, see the “Risk Factors” section of this Form 10-K and the other risks and uncertainties described below under the headings: “Our Lead Product Candidate APF530,” “Development Pipeline,” “Our Technology Platform,” “Our Strategy,” “Patents and Trade Secrets,” “Competition,” and under “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These forward-looking statements reflect our view only as of the date of this report. Except as required by law, we undertake no obligations to update any forward looking statements and we disclaim any intent to update forward-looking statements after the date of this report to reflect subsequent developments. Accordingly, you should also carefully consider the factors set forth in other reports or documents that we file from time to time with the Securities and Exchange Commission.

3

Table of Contents

Company Overview

A.P. Pharma is a specialty pharmaceutical company developing products using its proprietary Biochronomer™ polymer-based drug delivery platform. This drug delivery platform is designed to improve the therapeutic profile of injectable pharmaceuticals by converting them from products that must be injected once or twice per day to products that need to be injected only once every one or two weeks.

Our lead product candidate, APF530, is being developed for the prevention of acute CINV for patients undergoing both moderately and highly emetogenic chemotherapy and for the prevention of delayed CINV for patients undergoing moderately emetogenic chemotherapy. One of the most debilitating side effects of cancer chemotherapy, CINV is a leading cause of premature discontinuations of treatment. There is only one injectable 5-HT3 antagonist approved for the prevention of delayed-onset CINV, so this indication represents an area of particular unmet medical need. APF530 contains the 5-HT3 antagonist granisetron formulated in the Company’s proprietary Biochonomer™ drug delivery system, which allows therapeutic drug levels to be maintained for five days with a single subcutaneous injection. The currently available intravenous and oral formulations of granisetron are approved only for the prevention of acute-onset CINV. Granisetron was selected for APF530 because it is widely prescribed by physicians based on a well-established record of safety and efficacy.

In May 2009, we filed the original New Drug Application (NDA) seeking approval for APF530 with the U.S. Food and Drug Administration (FDA) under Section 505(b)(2) of the Federal Food, Drug, and Cosmetic Act (FDCA). We are seeking regulatory approval of APF530 for the prevention of acute CINV for patients undergoing both moderately and highly emetogenic chemotherapy and for the prevention of delayed CINV for patients undergoing moderately emetogenic chemotherapy. The FDA issued a Complete Response Letter for APF530 in March 2010. We met with the FDA in February and March 2011 to clarify the work needed to address the issues identified in the letter. In September 2012, we resubmitted the NDA seeking approval for APF530 with the FDA. Based on this submission, the FDA set a Prescription Drug User Fee Act (PDUFA) action date of March 27, 2013.

We own the worldwide rights to APF530 and are in the early stage of building commercial infrastructure necessary to commercialize APF530 in the U.S. on our own. We are seeking corporate partners to commercialize APF530 in markets outside of the U.S.

Our core Biochronomer technology, on which APF530 and our other product candidates are based, consists of bioerodible polymers designed to release drugs over a defined period of time. We have completed over 100 in vivo and in vitro studies demonstrating that our Biochronomer technology is potentially applicable to a range of therapeutic areas, including prevention of CINV, pain management, control of inflammation and treatment of ophthalmic diseases. We have also completed comprehensive animal and human toxicology studies that have established that our Biochronomer polymers are safe and well tolerated. Furthermore, our Biochronomer technology can be designed to deliver drugs over periods varying from days to several months.

In addition to our lead drug candidate, we are evaluating applications of our Biochronomer delivery technology to determine potential pipeline candidates that we may develop following the possible approval of APF530.

4

Table of Contents

We were founded in February 1983 as a California corporation under the name AMCO Polymerics, Inc. (AMCO). AMCO changed its name to Advanced Polymer Systems, Inc. in 1984 and was reincorporated in the state of Delaware in 1987. We changed our name to A.P. Pharma, Inc. in May 2001 to reflect our new pharmaceutical focus. Our offices are located at 123 Saginaw Drive, Redwood City, California 94063. Our telephone number is (650) 366-2626. Our website is located at www.appharma.com. Information contained on, or that can be accessed through, our website is not part of this Annual Report on Form 10-K.

Our Lead Product Candidate—APF530

CINV Background

Prevention and control of nausea and vomiting, or emesis, are paramount in the treatment of cancer patients. The majority of patients receiving chemotherapy will experience some degree of emesis if not prevented with an antiemetic. Chemotherapy treatments can be classified as moderately emetogenic, meaning that 30–90% of patients would experience CINV, or highly emetogenic, meaning that over 90% of patients would experience CINV, if they were not treated with an antiemetic prior to chemotherapy. Onset of CINV within the first 24 hours is described as “acute,” and CINV that occurs more than 24 hours after treatment is described as “delayed.” Delayed CINV may persist for several days from the time of onset. Prevention of CINV is important because the distress caused by CINV can severely disrupt patient quality of life and can lead some patients to delay or discontinue chemotherapy.

Current Therapy

Chemotherapeutic agents activate or destroy cells in the lining of the gut, releasing a neurotransmitter called serotonin. When serotonin binds to 5-hydroxytryptamine type 3 (5-HT3) receptors, the patient experiences nausea and vomiting. Granisetron, like other 5-HT3 antagonists, inhibits the vomiting reflex by preventing serotonin from binding to 5-HT3 receptors. Physicians may combine 5-HT3 antagonists with other agents, such as corticosteroids or neurokinin-1 (NK1) antagonists, to better prevent CINV.

Current treatment options for preventing CINV include injectable 5-HT3 antagonists such as palonosetron (Aloxi®), ondansetron (formerly marketed by GlaxoSmithKline as Zofran®) and granisetron (formerly marketed by Roche as Kytril ®). Aprepitant (Emend ®), an NK1 antagonist, is also used to prevent CINV and is typically used in combination with an injectable 5-HT3 antagonist. As shown in the table below, several injectable 5-HT3 antagonists are approved for the prevention of acute CINV in patients receiving either moderately or highly emetogenic chemotherapy. Within the last several years, generic versions of granisetron and ondansetron have become available. Aloxi is the only injectable 5-HT3 antagonist approved for the prevention of delayed CINV in patients receiving moderately emetogenic chemotherapy. No injectable 5-HT3 antagonist is approved for the prevention of delayed CINV in patients receiving highly emetogenic chemotherapy.

5

Table of Contents

Approved Injectable 5-HT3 Antagonists

| Chemotherapy Regimen |

Acute CINV |

Delayed CINV | ||

| Moderately Emetogenic |

Granisetron (Kytril) Ondansetron (Zofran) Palonosetron (Aloxi) |

Palonosetron (Aloxi) | ||

| Highly Emetogenic |

Granisetron (Kytril) Ondansetron (Zofran) Palonosetron (Aloxi) |

None |

Despite evidence that delayed CINV affects as many as 50–70% of patients and that more patients experience delayed CINV than acute CINV, oncology nurses and physicians are likely to underestimate the magnitude of these problems in the patients for whom they care. This may occur in part since patients often do not report side effects they experience at home following chemotherapy treatments. Even though high percentages of chemotherapy patients experience such delayed nausea and emesis, presently Aloxi is the only injectable 5-HT3 antagonist approved for the prevention of delayed CINV. We believe that APF530, if approved, could become the second long-acting product given in a single injection that is capable of addressing this important medical need. Eisai Company, which markets Aloxi in the U.S., reported U.S. Aloxi sales of $448 million in calendar-year 2012. Based on our market research, we believe that the total U.S. market for injectable 5-HT3 antagonists for the prevention of CINV is approximately $900 million (branded market estimate using 2011 units based on data from Wolters Kluwer and the Aloxi average selling price).

Our Solution—APF530

Our lead product candidate, APF530, is being developed for the prevention of acute CINV in patients receiving moderately or highly emetogenic chemotherapy and for the prevention of delayed CINV in patients receiving moderately emetogenic chemotherapy. APF530 is delivered by a single subcutaneous injection and contains the 5-HT3 antagonist granisetron. Granisetron, for infusion and oral tablets, is approved for the prevention of acute CINV, but not delayed CINV. We selected granisetron for APF530 because it is widely prescribed by physicians based on a well-established record of safety and efficacy and because it became generically available in 2007.

In our pivotal Phase 3 clinical trial of APF530, in which we enrolled more than 1,300 patients, we successfully demonstrated that APF530’s efficacy in preventing CINV was statistically non-inferior to that of Aloxi. If we obtain regulatory approval for APF530, we believe that APF530 will represent an attractive treatment for the many cancer patients that suffer from CINV.

Phase 2 Clinical Trial

In September 2005, we completed an open-label Phase 2 clinical trial of APF530. We evaluated the safety, tolerability and pharmacokinetics of APF530 in 45 cancer patients undergoing either moderately or highly emetogenic chemotherapy. In addition, efficacy endpoints were evaluated relating to emetic events and the use of additional medication for treating CINV. APF530 was well tolerated in this study; there were no serious adverse events attributed to APF530, and fewer than 10% of participating patients had injection site reactions, all of which were mild.

6

Table of Contents

A substantial proportion of the patients in our Phase 2 clinical trial were complete responders, meaning they experienced no vomiting and received no additional medication for CINV during the observation period. These efficacy results compared favorably to similar data for Aloxi, as reported from its Phase 3 clinical trials. Based on these results, we designed our Phase 3 clinical program to directly compare APF530 to Aloxi in a prospective randomized trial design.

Pivotal Phase 3 Clinical Trial

In December 2005, we held our end-of-Phase 2 meeting with the FDA, at which we discussed our registration strategy and our proposed design for the pivotal Phase 3 clinical trial. Following this meeting, we finalized plans for our pivotal Phase 3 clinical trial in accordance with FDA input. The goals of the trial were to demonstrate the safety and efficacy of APF530 in the treatment of CINV following the administration of highly or moderately emetogenic chemotherapy and to establish an effective dose for APF530. The trial was structured to compare the two APF530 doses (containing 5 mg and 10 mg of granisetron) with the FDA-approved dose of Aloxi across four different primary efficacy endpoints:

• non-inferiority to Aloxi for the prevention of acute CINV in patients receiving moderately emetogenic chemotherapies;

• non-inferiority to Aloxi for the prevention of delayed CINV in patients receiving moderately emetogenic chemotherapies;

• non-inferiority to Aloxi for the prevention of acute CINV in patients receiving highly emetogenic chemotherapies; and

• superiority to Aloxi for the prevention of delayed CINV in patients receiving highly emetogenic chemotherapies. Superiority to Aloxi was chosen for this endpoint because Aloxi is not approved for this indication.

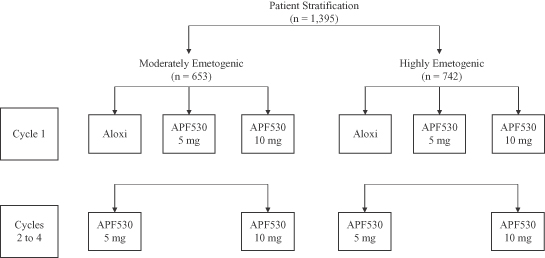

Our pivotal Phase 3 clinical trial was initiated in May 2006 as a multicenter, randomized, observer-blind, actively-controlled, double-dummy, parallel group study that compared the efficacy of APF530 to Aloxi. The trial stratified patients into two groups, one receiving moderately and the other receiving highly emetogenic chemotherapeutic agents in accordance with the Hesketh algorithm, which assigns emetogenic levels based on the chemotherapy agent, drug dosage and combinations employed. In each emetogenic group, patients were randomized during Cycle 1 to receive APF530 high dose (10 mg granisetron), APF530 low dose (5 mg granisetron) or the currently approved dose of Aloxi. For up to three subsequent treatment cycles (Cycles 2–4), the patients were re-randomized to receive either of the two APF530 doses. The diagram below provides further graphical representation of the patient stratification design and target enrollment for patient randomization in our clinical trial. The study completed patient enrollment of 1,395 patients in June 2008, and we announced top-line results on September 30, 2008.

7

Table of Contents

The 10 mg dose of APF530 achieved complete response (CR) rates that were numerically higher than, and statistically non-inferior to, Aloxi across all four assessments. The 5 mg dose of APF530 did not demonstrate non-inferiority to Aloxi for all endpoints. APF530 did not achieve the superiority endpoint for the delayed CINV assessment for highly emetogenic chemotherapies. Aloxi is not FDA approved for the prevention of delayed CINV in patients receiving highly emetogenic chemotherapies; therefore, APF530 needed to be statistically superior to Aloxi for this endpoint to receive FDA approval for this use. CR was defined as the absence of emetic episodes or use of anti-emetic rescue medications during a specified period of time. The time periods studied for CINV onset were 0 to 24 hours after chemotherapy, which is known as acute CINV, and 24 to 120 hours after chemotherapy, which is known as delayed CINV.

The results summarized below are the primary endpoints from the study, with such data being drawn from the first cycle of treatment:

Complete Response by Treatment–Cycle 1

| Emetogenicity Level |

Treatment Group | Statistics vs. Aloxi | ||||||||

| APF530 (5 mg) |

APF530 (10 mg) |

Aloxi | 5 mg |

10 mg | ||||||

| Moderately emetogenic |

(n=214) | (n=212) | (n=208) | |||||||

| • Acute CINV |

74.8% | 76.9% | 75.0% | NI (-9.8, 9.3) | NI (-7.5, 11.4) | |||||

| • Delayed CINV |

51.4% | 58.5% | 57.2% | I (-16.7, 5.1) | NI (-9.5, 12.1) | |||||

| Highly emetogenic |

(n=229) | (n=240) | (n=238) | |||||||

| • Acute CINV |

77.7% | 81.3% | 80.7% | NI (-12.1, 6.1) | NI (-8.2, 9.3) | |||||

| • Delayed CINV |

62.4% | 67.1% | 64.3% | NS (-12.6, 8.8) | NS (-7.7, 13.2) | |||||

(NI) Non-inferior efficacy was determined using a modified Bonferroni step down procedure. The lower bound of the adjusted Confidence Interval to establish non-inferiority was negative 15%. The Confidence Intervals shown for the moderately emetogenic and highly emetogenic levels are 97.5% and 98.3%, respectively. (NS) = No significant difference. (I) = Inferior efficacy.

8

Table of Contents

APF530 was generally well tolerated, with a side effect profile consistent with previous human use of granisetron and only one serious adverse event reported as possibly attributed to APF530. In Cycle 1, the data showed a low incidence of patients discontinuing therapy due to any adverse events (related or unrelated to study drugs): 0.5%, 0.9% and 0.9% in the moderately emetogenic patient group, and 2.0%, 3.5% and 1.2% in the highly emetogenic patient group for APF530 5 mg, APF530 10 mg and Aloxi, respectively. Further, of the patients completing the first cycle, 1,043 went on to receive a total of 2,374 additional doses of APF530 in Cycles 2 to 4. Of these patients, only 2 (or 0.2%) discontinued therapy due to treatment-related adverse events.

Additional data from the pivotal Phase 3 clinical trial comparing APF530 to Aloxi were released on November 5, 2008 and are reported below. These additional data included predetermined secondary efficacy endpoints and safety data that were not available at the time the top-line data were released. We believe that the overall clinical data package demonstrates the robustness of the APF530 clinical response within and across chemotherapy cycles. Some of the additional key findings follow:

• Collectively, the Phase 3 efficacy and safety data support the conclusion that 10 mg is the most effective dose of APF530 and, therefore, was the selected dose for the NDA.

• In patients receiving multiple cycles of APF530, CR rates were observed to generally increase over four cycles of chemotherapy, as shown in the following table:

Complete Response of APF530 10 mg Dose Over Four Chemotherapy Cycles

| Emetogenicity Level |

Cycle 1 | Cycle 2 | Cycle 3 | Cycle 4 | ||||||||||||

| Moderately Emetogenic |

(n=212) | (n=240) | (n=184) | (n=134) | ||||||||||||

| • Acute (0-24h) |

76.9% | 77.1% | 78.8% | 83.6% | ||||||||||||

| • Delayed (24-120h) |

59.0% | 62.1% | 61.4% | 66.4% | ||||||||||||

| • Overall (0-120h) |

54.2% | 58.8% | 60.3% | 63.4% | ||||||||||||

| Highly Emetogenic |

(n=240) | (n=263) | (n=202) | (n=148) | ||||||||||||

| • Acute (0-24h) |

81.3% | 84.8% | 89.6% | 87.8% | ||||||||||||

| • Delayed (24-120h) |

68.3% | 76.0% | 81.2% | 83.8% | ||||||||||||

| • Overall (0-120h) |

64.6% | 72.2% | 78.7% | 79.7% | ||||||||||||

• The Phase 3 clinical trial protocol predefined multiple primary and secondary endpoints, including complete response, complete control (no emesis, no rescue therapy and no greater-than-mild nausea) and total response (no emesis, no rescue therapy and no nausea) measured over defined time intervals (acute, delayed and overall). Although there were no significant differences between the APF530 10 mg dose and Aloxi, the response rates for the APF530 10 mg dose were numerically higher than Aloxi in all nine analyses for moderately emetogenic chemotherapy and in five of nine analyses for highly emetogenic chemotherapy. As noted above, however, APF530 did not achieve the primary endpoint of significant superiority to Aloxi in the highly emetogenic group at any dose.

9

Table of Contents

• The safety profile for APF530 was similar to that for Aloxi; the most notable adverse event was constipation, observed in 15.4% and 13.4% of patients receiving APF530 10 mg and Aloxi, respectively. Headache was observed in 10.0% and 9.7% of patients receiving the APF530 10 mg dose and Aloxi, respectively.

• Investigators were required to observe and record all reactions associated with the subcutaneous injection site on days one and five for each treatment cycle. Overall, greater than 90% of the recorded observations were mild in severity, the most common being injection-site redness and bruising. With each additional cycle of treatment, the frequency of injection site reactions decreased, indicating APF530 can safely be administered for multiple cycles.

• During the trial, patients received more than 1,600 separate injections of the APF530 10 mg dose. Assessment of any injection-site pain was made on days one and five of treatment: on day one, less than 0.1% of injections resulted in any reports of pain; on day five, approximately 4% of injections resulted in a report of pain. All but four of these reports of pain were recorded as mild, with the four recorded as moderate. Additional data from the pivotal Phase 3 clinical trial were presented at the annual meeting of the American Society of Clinical Oncology on June 1, 2009, and are reported below.

• CR rates for the APF530 10 mg dose were generally higher in patients who had received prior chemotherapy when compared to patients who had not received any previous chemotherapy. Additionally, in all instances, CR rates for APF530 in patients receiving prior chemotherapy were numerically higher than those observed for Aloxi. Based on previous clinical studies, many physicians believe that the risk of CINV increases with each additional cycle of chemotherapy. These new data may suggest potential utility for APF530 in treating patients who have received prior chemotherapy.

• Of the highly emetogenic chemotherapy regimens, those containing cisplatin are considered to be the most troublesome due to their ability to cause significant delayed CINV. The CR rates for patients receiving cisplatin- based regimens were numerically higher for the APF530 10 mg dose when compared to Aloxi in both acute and delayed CINV. Specifically, in acute CINV, APF530 had an 81.1% CR rate versus 75.5% for Aloxi, and, in delayed CINV, APF530 had a 66.0% CR rate versus 60.4% for Aloxi. These differences were not statistically significant.

• A pharmacokinetic analysis, conducted in a sub-group of patients, showed that a single APF530 10 mg dose maintained blood levels of granisetron for the entire five-day period.

Additional Clinical Studies

In the first quarter of 2012, at the request of the FDA, the Company completed a thorough QT study of APF530. The study was conducted to assess the potential for granisetron, the active drug in APF530, to prolong the QT interval across a wide range of plasma drug concentrations (the QT interval is a measure of the time between the start of the Q wave and the end of the T wave in the heart’s electrical cycle, and, in general, the QT interval represents electrical depolarization and repolarization of the left and right ventricles). Prolongation of the QT interval may increase the risk of fatal cardiac tachyarrhythmias. As such, the FDA requires a thorough QT study, which examines a drug’s potential to prolong the QT interval, for many drugs in development. Moxifloxacin, a drug known to prolong the QT interval, is a standard positive control used in thorough QT studies. The study met its protocol-specified primary end point and demonstrated that granisetron did not have an effect on cardiac repolarization as measured by prolongation of the QT interval. A pharmacokinetic/pharmacodynamic (PK/PD) analysis demonstrated that there was no relationship between plasma granisetron concentrations and the heart-rate-corrected QT interval (QTc) (slope of zero).

10

Table of Contents

This study was a randomized, double-blind, placebo-controlled, four-way, crossover trial in 56 healthy adults that compared the effects of: (1) APF530 at twice its proposed therapeutic dose; (2) intravenous granisetron at five times its therapeutic dose; (3) oral moxifloxacin (400 mg), a known pro-arrhythmic; and (4) placebo, on the surface electrocardiogram with primary focus on the QT interval. The primary end point was to determine that granisetron had no clinically meaningful effect on QTc, defined as the upper bound of the one-sided 95% confidence interval for placebo-adjusted, baseline-subtracted QTc being less than 10 milliseconds at all time points. The primary end point was met irrespective of heart-rate correction methodology (QTcF, QTcl, QTcB). Moxifloxacin, the study’s positive control, demonstrated QTc prolongation consistent with previous clinical experience.

Also in the first quarter of 2012, the Company completed a study of the metabolism of APF530 in healthy volunteers. This study was requested by the FDA to corroborate pre-clinical animal metabolism data for the polymer used in APF530 with metabolism data in humans. The study provided quantitative results confirming how the polymer is metabolized by the human body. The results of the study were consistent with preclinical studies, and these results were included in the resubmission of the NDA.

New Drug Application

In May 2009, we filed an NDA for APF530 with the FDA under Section 505(b)(2) of the FDCA. In March 2010, we received a Complete Response Letter from the FDA, which stated that the NDA we submitted in May 2009, requesting approval of APF530, could not be approved as it was initially submitted. The primary points raised in the FDA Complete Response Letter were as follows:

Dosing System

• The FDA expressed concerns relating to our former two-syringe administration system, including potential issues with the transfer of material from one syringe to the other syringe prior to patient administration, certain components used in the dosing system and the potential risk of improper administration of the drug product.

Chemistry, Manufacturing and Control

• The FDA conducted inspections of our facility and several of our contract manufacturing facilities. The FDA identified certain deficiencies during these inspections, and stated that satisfactory resolution of these deficiencies would be required for approval.

• During the NDA review, the FDA asked that we determine if terminal sterilization with gamma irradiation is a feasible approach to enhance the assurance of sterility. We have subsequently demonstrated that terminal sterilization is feasible, and the FDA has requested we change to terminal sterilization prior to approval.

• The FDA requested clarification and revision of certain analytical specifications proposed in our NDA.

Clinical

• The FDA did not request additional clinical efficacy studies, although the FDA has asked for the re-presentation and re-analysis of select existing Phase 3 clinical trial data.

• The FDA requested we perform two studies relating to bioavailability and metabolism.

11

Table of Contents

• The FDA did not accept our request to waive the requirement for a thorough QT study.

We met with the FDA in February and March 2011 to clarify the work needed to address the issues identified in the letter and resubmit the NDA. At the February 2011 meeting, we presented information concerning the clinical pharmacology of APF530 and a revised presentation format for certain clinical data from the Company’s Phase 3 clinical study. The FDA indicated that the Company would need to complete a thorough QT study prior to resubmitting its NDA and clarified the requirements for a previously requested metabolism study. The FDA also indicated that the revised presentation format for the clinical data was acceptable for resubmission. The FDA did not request that the Company conduct any additional efficacy studies. At the March 2011 meeting, the dosing system and the characterization and manufacturing of APF530 were discussed. The Company also presented the results of the additional analytical work it had completed since receipt of the Complete Response Letter.

Following these meetings, we performed a number of activities in order to address the items requested by the FDA, including the following:

• We changed our dosing system from the former two-syringe administration system employing a 1-inch needle to a single-syringe system employing a 5/8-inch needle.

• We conducted Human Factors studies to demonstrate that APF530 could be administered safely to patients.

• We modified our proposed Package Insert, product packaging and Instructions for Use to further ensure proper administration of the product.

• We demonstrated that terminal sterilization is feasible and changed our manufacturing process to incorporate terminal sterilization.

• We made other changes to our manufacturing and quality control/quality assurance processes to address concerns raised by the FDA.

• We conducted and completed thorough QT and metabolism studies based on protocols agreed upon with the FDA (see Additional Clinical Studies).

In September 2012, we resubmitted the NDA seeking approval for APF530. The FDA set a PDUFA action date of March 27, 2013.

Section 505(b)(2) of the FDCA permits the FDA, in its review of an NDA, to rely on studies that were not conducted by or for the applicant and to which the applicant has not obtained a right of reference. Such studies can be provided by published literature, or FDA can rely on previous findings of safety and efficacy for a previously approved drug. Section 505(b)(2) applications may be submitted for drug products that represent a modification (e.g., a new indication or new dosage form) of an eligible approved drug. In such cases, the additional information in 505(b)(2) applications necessary to support the change from the previously approved drug is frequently provided by new studies submitted by the applicant. Our 505(b)(2) application relies on the FDA’s previous finding of safety and effectiveness for the active ingredient in APF530, granisetron, together with the additional clinical and nonclinical data that we submitted to demonstrate the safety and effectiveness of our formulation of the drug product for the indications for which we are seeking approval.

12

Table of Contents

Development Pipeline

We have previously submitted Investigational New Drug (IND) applications to the FDA for two other product candidates, APF112 and APF580. APF112 utilizes our Biochronomer delivery technology to target post-surgical pain relief. This product is designed to provide up to 36 hours of localized pain relief by delivering mepivacaine directly to the surgical site. APF112 completed a Phase 2 clinical study in 2004, but failed to reach its primary endpoint. APF580 incorporates buprenorphine, an opiate, into our Biochronomer technology and is designed to provide analgesia lasting at least seven days following a single injection. An IND was filed in 2008, but no clinical studies have been conducted.

Since 2009, further development of these product candidates has been deferred in order to focus both managerial and financial resources on the development of APF530. We are currently evaluating potential applications of our Biochronomer delivery technology to determine potential pipeline candidates following the possible approval of APF530.

Research and Development

As of December 31, 2012, we had 23 employees engaged in research and development and quality control. Research and development expenses for 2012, 2011 and 2010 were $15.0 million, $8.2 million and $7.3 million, respectively.

Our Technology Platform

We have developed a broad family of polymers with unique attributes, known collectively as poly (ortho esters), under the trade name Biochronomer. We have completed over 100 in vivo and in vitro studies demonstrating that our Biochronomer technology is potentially applicable to a range of therapeutic areas, including pain management, prevention of nausea, control of inflammation and treatment of ophthalmic diseases. We have also completed comprehensive animal and human toxicology studies that have established that our Biochronomer polymers are safe and well tolerated.

Our Biochronomer technology can provide sustained levels of drugs for prolonged efficacy. The Biochronomer “links,” or bonds, are stable at neutral pH conditions. Upon coming into contact with water-containing media, such as internal body fluids, the water reacts with these bonds. This reaction is known as hydrolysis. During the hydrolysis of the Biochronomer links, acidic elements are produced in a local micro-environment, in a controlled manner, without impacting the overall neutrality of the drug delivery system. These elements assist in the continued, controlled erosion of the polymer with a simultaneous, controlled release of the active drug contained within the Biochronomer. By varying the amount of the acidic elements in the Biochronomer, different rates of hydrolysis may be effectively realized. In this manner, delivery times ranging from days to weeks to several months can be achieved.

Due to the inherent versatility of our Biochronomer technology, products can be designed to deliver drugs at a variety of implantation sites including: under the skin, at the site of a surgical procedure, in joints, in the eye or in muscle tissue. Our Biochronomers can be prepared in a variety of physical forms, ranging from hard, glassy materials to fluids of varying viscosity that are injectable at room temperature, by proper selection of monomers. A significant advantage of our Biochronomer technology is that drugs can be incorporated by simple mixing procedures, allowing the production of formulations in the form of injectable gels, microspheres, coatings and strands.

13

Table of Contents

Our Strategy

Our primary near-term objective is to obtain FDA approval of the NDA for APF530. We believe that there is significant market potential for APF530 for the prevention of acute CINV for both moderately and highly emetogenic chemotherapy, and for the prevention of delayed CINV in moderately emetogenic chemotherapy. We own the worldwide rights to APF530 and are in the early stages of building the commercial infrastructure necessary to commercialize APF530 in the U.S. on our own. We are seeking corporate partners to commercialize APF530 in markets outside of the U.S. Longer term, we intend to become a leading specialty pharmaceutical company focused on improving the effectiveness of existing pharmaceuticals using our proprietary drug delivery technologies.

Manufacturing and Supply

We do not currently own or operate manufacturing facilities for the production of clinical or commercial quantities of any of our product candidates. We rely on a small number of third-party manufacturers to produce our compounds and expect to continue to do so to meet the preclinical and clinical requirements of our potential product candidates and for all of our commercial needs. We do not have long-term agreements with any of these third-parties. We require in our manufacturing and processing agreements that all third-party contract manufacturers and processors produce active pharmaceutical ingredients (APIs) and finished products in accordance with the FDA’s current Good Manufacturing Practices (cGMP) and all other applicable laws and regulations. We maintain confidentiality agreements with potential and existing manufacturers in order to protect our proprietary rights related to our drug candidates.

With regard to our lead product candidate, APF530, we source the API, granisetron, from two suppliers. We use one supplier to source raw materials and prepare our proprietary polymer, and another supplier to formulate the bulk drug product. We ship the bulk APF530 to a contract manufacturer for filling into syringes. To date, APF530 has been manufactured in small quantities for preclinical studies and clinical trials. If APF530 is approved for commercial sale, we will need to manufacture the product in larger quantities. Significant scale-up of manufacturing will require additional process development and validation studies, which the FDA must review and approve. If approved, the commercial success of APF530, in the near-term, will be dependent upon the ability of our contract manufacturers to produce a product in commercial quantities at competitive costs of manufacture. If APF530 receives regulatory approval, we plan to scale-up manufacturing through our third-party manufacturers for APF530 with the objective of realizing important economies of scale. These scale-up activities will take time to implement, require additional capital investment, process development and validation studies, and FDA approval. We cannot guarantee that we will be successful in achieving competitive manufacturing costs through such scale-up activities.

Sales and Marketing

We own all worldwide rights to APF530 and are in the early stages of building commercial infrastructure necessary to commercialize APF530 in the U.S. on our own. In the fourth quarter of 2012 and first quarter of 2013, we made several key commercial operations executive appointments. We intend to establish a direct sales force if APF530 is approved. For markets outside of the U.S., we are seeking corporate partners to commercialize APF530.

We have engaged and will continue to engage in potential partnership discussions with domestic and international pharmaceutical companies.

14

Table of Contents

Patents and Trade Secrets

Patents and other proprietary rights are important to our business. It is our policy to seek patent protection for our inventions, and to rely upon trade secrets, know-how, continuing technological innovations and licensing opportunities to develop and maintain our competitive position.

As part of our strategy to protect our current product candidates and to provide a foundation for future products, we have filed a number of U.S. patent applications on inventions relating to the composition of a variety of polymers, specific products, product groups and processing technology. As of December 31, 2012, we had a total of 22 issued U.S. patents and an additional 54 issued (or registered) foreign patents. The patents on our bioerodible technologies expire between January 2016 and November 2026. APF530 is covered by multiple patents that have claims extending into 2024. Our policy is to actively seek in the United States and selected foreign countries patent protection for novel technologies and compositions of matter that are commercially important to the development of our business.

Although we believe the bases for these patents and patent applications are sound, they are untested, and there is no assurance that they will not be successfully challenged. There can be no assurance that any patent previously issued will be of commercial value, that any patent applications will result in issued patents of commercial value, or that our technology will not be held to infringe patents held by others.

We also rely on unpatented trade secrets and know-how to protect certain aspects of our production technologies. Our employees, consultants, advisors and corporate partners have entered into confidentiality agreements with us. These agreements, however, may not necessarily provide meaningful protection for our trade secrets or proprietary know-how in the event of unauthorized use or disclosure. In addition, others may obtain access to, or independently develop, these trade secrets or know-how.

Competition

The pharmaceutical industry is highly competitive. Many of our competitors have substantially greater financial, research, development, manufacturing, sales, marketing and distribution resources than we currently do. In addition, they may have significantly more experience in drug development, obtaining regulatory approval and establishing strategic collaborations. We expect any future products we develop to compete on the basis of, among other things, product efficacy and safety, time to market, price, extent of adverse side effects experienced and convenience of administration and drug delivery. We also expect to face competition in our efforts to identity appropriate collaborators or partners to help commercialize our product candidates in our target commercial areas.

APF530 is expected to face significant competition for the prevention of delayed CINV, principally from Eisai’s Aloxi (palonosetron). In addition to Aloxi, APF530 will compete with entrenched generic forms of granisetron (formerly marketed by Roche as Kytril) and ondansetron (formerly marketed by GlaxoSmithKline as Zofran). Generic versions of Aloxi may become available after its scheduled patent expiration date, which was recently extended to 2024. We are also aware of several companies that have developed, or are developing, both generic and new formulations of granisetron, including transdermal formulations such as ProStrakan’s Sancuso® (granisetron transdermal patch).

15

Table of Contents

There are several companies that are developing new formulations of existing drugs using novel drug delivery technologies. The following are some of our major competitors among drug delivery system developers: Alkermes, Inc., Durect Corporation and Pacira Pharmaceuticals, Inc.

Government Regulation and Product Approvals

The manufacturing and marketing of our potential products and our ongoing research and development activities are subject to extensive regulation by the FDA and comparable regulatory agencies in state and local jurisdictions and in foreign countries.

United States Regulation

Before any of our products can be marketed in the United States, they must be approved by the FDA. To secure approval, any drug we develop must undergo rigorous preclinical testing and clinical trials that demonstrate the product candidate’s safety and effectiveness for each chosen indication for use. These extensive regulatory processes control, among other things: the development, testing, manufacture, safety, efficacy, record keeping, labeling, storage, approval, advertising, promotion, sale and distribution of biopharmaceutical products.

In general, the process required by the FDA before investigational drugs may be marketed in the United States involves the following steps:

• preclinical laboratory and animal tests;

• submission of an IND, which must become effective before human clinical trials may begin;

• adequate and well-controlled human clinical trials to establish the safety and efficacy of the proposed drug for its intended use;

• pre-approval inspection of manufacturing facilities and selected clinical investigators; and

• FDA approval of an NDA or of an NDA supplement (for subsequent indications).

Preclinical Testing

In the United States, drug candidates are tested in animals until adequate proof-of-safety is established. These preclinical studies generally evaluate the mechanism of action of the product and assess the potential safety and efficacy of the product. Tested compounds must be produced according to applicable cGMP requirements, and preclinical safety tests must be conducted in compliance with FDA and international regulations regarding good laboratory practices (GLP). The results of the preclinical tests, together with manufacturing information and analytical data, are generally submitted to the FDA as part of an IND, which must become effective before human clinical trials may commence. The IND will automatically become effective 30 days after receipt by the FDA, unless before that time the FDA requests an extension or raises concerns about the conduct of the clinical trials as outlined in the application. If the FDA has any concerns, the sponsor of the application and the FDA must resolve the concerns before clinical trials can begin. Submission of an IND may not result in FDA authorization to commence a

16

Table of Contents

clinical trial. A separate submission to the existing IND must be made for each successive clinical trial conducted during product development, and the FDA must grant permission for each clinical trial to start and continue. Regulatory authorities may require additional data before allowing the clinical studies to commence or proceed from one phase to another and could demand that the studies be discontinued or suspended at any time if there are significant safety issues. Furthermore, an independent institutional review board (IRB), for each medical center proposing to participate in the conduct of the clinical trial must review and approve the clinical protocol and patient informed consent before the center commences the study.

Clinical Trials

Clinical trials for new drug candidates are typically conducted in three sequential phases that may overlap. In Phase 1, the initial introduction of the drug candidate into human volunteers, the emphasis is on testing for safety or adverse effects, dosage, tolerance, metabolism, distribution, excretion and clinical pharmacology. Phase 2 involves studies in a limited patient population to determine the initial efficacy of the drug candidate for specific targeted indications, to determine dosage tolerance and optimal dosage and to identify possible adverse side effects and safety risks. Once a compound shows evidence of effectiveness and is found to have an acceptable safety profile in Phase 2 evaluations, pivotal Phase 3 clinical trials are undertaken to more fully evaluate clinical outcomes and to establish the overall risk/benefit profile of the drug and to provide, if appropriate, an adequate basis for product labeling. During all clinical trials, physicians will monitor patients to determine effectiveness of the drug candidate and to observe and report any reactions or safety risks that may result from use of the drug candidate. The FDA, the IRB (or their foreign equivalents) or the sponsor may suspend a clinical trial at any time on various grounds, including a finding that the subjects are being exposed to an unacceptable health risk.

The data from the clinical trials, together with preclinical data and other supporting information that establishes a drug candidate’s safety, are submitted to the FDA in the form of an NDA, or NDA supplement (for approval of a new indication if the product candidate is already approved for another indication). Under applicable laws and FDA regulations, each NDA submitted for FDA approval is usually given an internal administrative review within 60 days following submission of the NDA. If deemed complete, the FDA will “file” the NDA, thereby triggering substantive review of the application.

The FDA can refuse to file any NDA that it deems incomplete or not properly reviewable. The FDA has established internal substantive review goals of six months for priority NDAs (for drugs addressing serious or life threatening conditions for which there is an unmet medical need) and ten months for regular NDAs. The FDA, however, is not legally required to complete its review within these periods, and these performance goals may change over time. Moreover, in many cases, the outcome of the review, even if generally favorable, is not an actual approval, but a “complete response” that describes additional work that must be done before the NDA can be approved. The FDA’s review of an NDA may involve review and recommendations by an independent FDA advisory committee. The FDA may deny approval of an NDA, or NDA supplement, if the applicable regulatory criteria are not satisfied, or it may require additional clinical data and/or an additional pivotal Phase 3 clinical trial. Even if such data are submitted, the FDA may ultimately decide that the NDA or NDA supplement does not satisfy the criteria for approval.

Data Review and Approval

Satisfaction of FDA requirements or similar requirements of state, local, and foreign regulatory agencies typically takes several years and requires the expenditure of substantial financial resources. Information generated in this process is susceptible to varying interpretations that could delay, limit or prevent regulatory approval at any stage of the process. Accordingly, the actual

17

Table of Contents

time and expense required to bring a product to market may vary substantially. We cannot assure you that we will submit applications for required authorizations to manufacture and/or market potential products or that any such application will be reviewed and approved by the appropriate regulatory authorities in a timely manner, if at all. Data obtained from clinical activities is not always conclusive and may be susceptible to varying interpretations which could delay, limit or prevent regulatory approval. Success in early stage clinical trials does not ensure success in later stage clinical trials. Even if a product candidate receives regulatory approval, the approval may be significantly limited to specific disease states, patient populations and dosages, or have conditions placed on it that restrict the commercial applications, advertising, promotion or distribution of these products.

Once issued, the FDA may withdraw product approval if ongoing regulatory standards are not met or if safety problems occur after the product reaches the market. In addition, the FDA may require testing and surveillance programs to monitor the safety or effectiveness of approved products which have been commercialized, and the FDA has the power to prevent or limit further marketing of a product based on the results of these post-marketing programs. The FDA may also request or require additional clinical trials after a product is approved, which are referred to as Phase 4 clinical studies. The results of Phase 4 clinical studies can confirm the effectiveness of a product candidate and can provide important safety information to augment the FDA’s voluntary adverse drug reaction reporting system. Any products manufactured or distributed by us pursuant to FDA approvals would be subject to continuing regulation by the FDA, including record-keeping requirements and reporting of adverse experiences with the drug. Drug manufacturers and their subcontractors are required to register their establishments with the FDA and certain state agencies and are subject to periodic unannounced inspections by the FDA and certain state agencies for compliance with cGMPs, which impose certain procedural and documentation requirements upon us and our third-party manufacturers. We cannot be certain that we, or our present or future suppliers, will be able to comply with the cGMP regulations and other FDA regulatory requirements. If our present or future suppliers are not able to comply with these requirements, the FDA may halt our clinical trials, require us to recall a drug from distribution, or withdraw approval of the NDA for that drug. Furthermore, even after regulatory approval is obtained, later discovery of previously unknown problems with a product may result in restrictions on the product or even complete withdrawal of the product from the market.

The FDA closely regulates the marketing and promotion of drugs. Approval may be subject to post-marketing surveillance and other record-keeping and reporting obligations, and involve ongoing requirements. Product approvals may be withdrawn if compliance with regulatory standards is not maintained or if problems occur following initial marketing. A company can make only those claims relating to safety and efficacy that are approved by the FDA. Failure to comply with these requirements can result in adverse publicity, warning letters, corrective advertising and potential civil and criminal penalties. Physicians may prescribe legally available drugs for uses that are not described in the product’s labeling and that differ from those tested by us and approved by the FDA. Such off-label uses are common across medical specialties. Physicians may believe that such off-label uses are the best treatment for many patients in varied circumstances. The FDA does not regulate the behavior of physicians in their choice of treatments. The FDA does, however, restrict manufacturers’ communications on off-label uses of approved drugs.

Section 505(b)(2) Applications

Some of our product candidates may be eligible for submission of applications for approval under the FDA’s Section 505(b)(2) approval process, which generally requires less information than the NDAs described above. Section 505(b)(2) was enacted as

18

Table of Contents

part of the Drug Price Competition and Patent Term Restoration Act of 1984, also known as the Hatch-Waxman Act, and allows approval of NDAs that rely, at least in part, on studies that were not conducted by or for the applicant and to which the applicant has not obtained a right of reference. Such studies can be provided by published literature, or FDA can rely on previous findings of safety and efficacy for a previously approved drug. Section 505(b)(2) applications may be submitted for drug products that represent a modification (e.g., a new indication or new dosage form) of an eligible approved drug. In such cases, the additional information in 505(b)(2) applications necessary to support the change from the previously approved drug is frequently provided by new studies submitted by the applicant. Because a Section 505(b)(2) application relies in part on previous studies or previous FDA findings or safety and effectiveness, preparing 505(b)(2) applications is generally less costly and time-consuming than preparing an NDA based entirely on new data and information from a full set of clinical trials. The law governing Section 505(b)(2) or FDA’s current policies may change in such a way as to adversely affect our applications for approval that seek to utilize the Section 505(b)(2) approach. Such changes could result in additional costs associated with additional studies or clinical trials and delays.

The FDA provides that reviews and/or approvals of applications submitted under Section 505(b)(2) will be delayed in various circumstances. For example, the holder of the NDA for the listed drug may be entitled to a period of market exclusivity during which the FDA will not approve, and may not even review, a Section 505(b)(2) application from other sponsors. If the listed drug is claimed by one or more patents that the NDA holder has listed with the FDA, the Section 505(b)(2) applicant must submit a certification with respect to each such patent. If the 505(b)(2) applicant certifies that a listed patent is invalid, unenforceable or not infringed by the product that is the subject of the Section 505(b)(2) application, it must notify the patent holder and the NDA holder. If, within 45 days of providing this notice, the NDA holder sues the 505(b)(2) applicant for patent infringement, the FDA will not approve the Section 505(b)(2) application until the earlier of a court decision favorable to the Section 505(b)(2) applicant or the expiration of 30 months. The regulations governing marketing exclusivity and patent protection are complex, and it is often unclear how they will be applied in particular circumstances.

In addition, both before and after approval is sought, we and our collaborators are required to comply with a number of FDA requirements. For example, we are required to report certain adverse reactions and production problems, if any, to the FDA, and to comply with certain limitations and other requirements concerning advertising and promotion for our products. Also, quality control and manufacturing procedures must continue to conform to cGMP after approval, and the FDA periodically inspects manufacturing facilities to assess compliance with continuing cGMP. In addition, discovery of problems, such as safety problems, may result in changes in labeling or restrictions on a product manufacturer or NDA holder, including removal of the product from the market.

DEA Regulation

Our research and development processes involve the controlled use of hazardous materials, including chemicals. Some of these hazardous materials are considered to be controlled substances and subject to regulation by the U.S. Drug Enforcement Agency (DEA). Controlled substances are those drugs that appear on one of five schedules promulgated and administered by the DEA under the Controlled Substances Act (CSA). The CSA governs, among other things, the distribution, recordkeeping, handling, security and disposal of controlled substances. We must be registered by the DEA in order to engage in these activities, and are subject to periodic and ongoing inspections by the DEA and similar state drug enforcement authorities to assess ongoing compliance with the DEA’s regulations. Any failure to comply with these regulations could lead to a variety of sanctions, including the revocation, or a denial of renewal, of the DEA registration, injunctions or civil or criminal penalties.

19

Table of Contents

Third-Party Payor Coverage and Reimbursement

Although none of our current product candidates have been approved or commercialized for any indication, if they are approved for marketing, commercial success of our product candidates will depend, in part, upon the availability of coverage and reimbursement from third-party payors at the federal, state and private levels. Government payor programs, including Medicare and Medicaid, private health care insurance companies and managed care plans have attempted to control costs by limiting coverage and the amount of reimbursement for particular procedures or drug treatments. The U.S. Congress and state legislatures, from time to time, propose and adopt initiatives aimed at cost containment. Ongoing federal and state government initiatives directed at lowering the total cost of health care will likely continue to focus on health care reform, the cost of prescription pharmaceuticals and on the reform of the Medicare and Medicaid payment systems. Examples of how limits on drug coverage and reimbursement in the United States may cause reduced payments for drugs in the future include:

• changing Medicare reimbursement methodologies;

• fluctuating decisions on which drugs to include in formularies;

• revising drug rebate calculations under the Medicaid program or requiring that new or additional rebates be provided to Medicare, Medicaid, other federal or state healthcare programs; and

• reforming drug importation laws.

Some third-party payors also require pre-approval of coverage for new or innovative devices or drug therapies before they will reimburse health care providers that use such therapies. While we cannot predict whether any proposed cost-containment measures will be adopted or otherwise implemented in the future, the announcement or adoption of these proposals could have a material adverse effect on our ability to obtain adequate prices for our product candidates and operate profitably.

Foreign Approvals

In addition to regulations in the United States, we will be subject to a variety of foreign regulations governing clinical trials and commercial sales and distribution of our products. Whether or not we obtain FDA approval for a product, we must obtain approval of a product by the comparable regulatory authorities of foreign countries before we can commence clinical trials or marketing of the product in those countries. The approval process varies from country to country, and the time may be longer or shorter than that required for FDA approval. The requirements governing the conduct of clinical trials, product licensing, pricing and reimbursement vary greatly from country to country.

We have not started the regulatory approval process in any jurisdiction other than the United States, and we are unable to estimate when, if ever, we will commence the regulatory approval process in any foreign jurisdiction. Foreign approvals may not be granted on a timely basis, or at all. Regulatory approval of prices is required in most countries other than the United States. The prices approved may be too low to generate an acceptable return to us. If we fail to obtain approvals from foreign jurisdictions, the geographic market for our product candidates would be limited.

20

Table of Contents

Employees

As of December 31, 2012, we had 32 full-time employees, 4 of whom hold Ph.D. degrees and 1 of whom is an M.D., and approximately 14 full-time equivalent contract workers. There were 23 employees engaged in research and development and quality control, and 9 individuals working in commercial operations, finance, information technology, human resources and administration.

We consider our relations with our employees to be good. None of our employees are covered by a collective bargaining agreement.

Available Information

We make available free of charge on or through our Internet website our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. Our Internet website address is “www.appharma.com.” The reference to our Internet website does not constitute incorporation by reference of the information contained on or hyperlinked from our Internet website. We file electronically with the SEC, our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K pursuant to Section 13(a) or 15(d) of the Exchange Act. The SEC maintains an Internet site that contains reports, proxy information and information statements, and other information regarding issuers that file electronically with the SEC. The address of that website is http://www.sec.gov. The materials are also available at the SEC’s Public Reference Room, located at 100 F Street, Washington, D.C. 20549. The public may obtain information through the public reference room by calling the SEC at 1-800-SEC-0330.

Our business is subject to various risks, including those described below. You should consider carefully these risk factors and all of the other information included in this Form 10-K. Any of these risk factors could materially adversely affect our business, operating results and financial condition. These risks are not the only ones we face. Additional risks not presently known to us or that we currently believe are immaterial may also significantly impair our business operations. In these circumstances, the market price of our common stock could decline, and you may lose all or part of your investment in our securities. Before you decide whether to purchase any of our common stock, you should carefully consider the risk factors set forth below as may be updated from time to time by our future filings under the Securities Exchange Act of 1934, as amended, or the Exchange Act.

Risks Related To Our Business

We are substantially dependent upon the success of our APF530 product candidate. Clinical trial results and the NDA resubmission for this product may not lead to regulatory approval.

We have invested a significant portion of our time and financial resources in the development of our most advanced product candidate, APF530, for which we are seeking U.S. Food and Drug Administration (FDA) approval for the prevention of acute chemotherapy-induced nausea and vomiting (CINV) associated with both moderately and highly emetogenic chemotherapy and for the prevention of delayed CINV associated with moderately emetogenic chemotherapy. Our near-term ability to generate revenues and our future success, in large part, depends on the approval and successful commercialization of APF530.

21

Table of Contents

We will not be able to commercialize APF530 until we obtain regulatory approval in the United States or foreign countries. In order to satisfy FDA or foreign regulatory approval standards for the commercial sale of APF530, we must have demonstrated in adequate and controlled clinical trials that APF530 is safe and effective. APF530 is designed to provide at least five days prevention of CINV. In September 2012, we resubmitted the New Drug Application (NDA) seeking approval for APF530 with the FDA, and the FDA has set a Prescription Drug User Fee Act (PDUFA) action date of March 27, 2013. If the FDA does not approve our NDA or requests additional work or changes to the NDA, our continued ability to commercialize APF530 could be seriously impaired, and our business would be adversely impacted. Obtaining regulatory approval of APF530 for the prevention of acute CINV for both moderately and highly emetogenic chemotherapy, and for the prevention of delayed CINV in moderately emetogenic chemotherapy, is subject to many variables. The FDA has inspected our facilities and those of our suppliers and has issued certain findings relating to cGMP processes for the manufacturing of APF530. We and our suppliers have responded to these findings, but there can be no assurance that these responses were sufficient. Further, the FDA’s review may not produce positive decisions as to:

• whether APF530 is safe and effective in its proposed use(s) and whether its benefits outweigh the risks;

• whether the proposed labeling (package insert) for APF530 is appropriate and what it should contain; and

• whether the methods used in manufacturing APF530 and the controls used to maintain its quality are adequate to preserve its identity, strength, quality and purity.

Deficiencies on any of the above, or other factors, could prevent or delay obtaining regulatory approval of APF530, which would impair our reputation, increase our costs and prevent us from earning revenue.

We may not obtain regulatory approval for APF530 or any of our product candidates. Regulatory approval may also be delayed or cancelled or may entail limitations on the indicated uses of a proposed product.

The process for obtaining approval of an NDA is time consuming, subject to unanticipated delays and costs, and requires the commitment of substantial resources. The regulatory process, particularly for pharmaceutical product candidates like ours, is uncertain, can take many years and requires the expenditure of substantial resources. Any product that we or our collaborative partners develop must receive all relevant regulatory agency approvals or clearances, if any, before it may be marketed in the United States or other countries. In particular, human pharmaceutical therapeutic products are subject to rigorous preclinical and clinical testing and other requirements by the FDA in the United States and similar health authorities in foreign countries. We may not receive necessary regulatory approvals or clearances to market APF530 or any other product candidate. In September 2012, we resubmitted the NDA seeking approval for APF530 with the FDA, and the FDA has set a PDUFA action date of March 27, 2013.

Our NDA resubmission for APF530 may not be approved, or approval may be delayed, as a result of changes in FDA policies for drug approval prior to the FDA’s decision on our NDA. For example, although many products have been approved by the FDA in recent years under Section 505(b)(2) under the Federal Food, Drug, and Cosmetic Act, objections have been raised to the FDA’s interpretation of Section 505(b)(2). If challenges to the FDA’s interpretation of Section 505(b)(2) are successful, the Agency may be required to change its interpretation, which could delay or prevent the approval of our NDA for APF530. The review of our resubmitted NDA may also be delayed due to the FDA’s internal resource constraints.

22

Table of Contents

Additionally, data obtained from preclinical and clinical activities are susceptible to varying interpretations that could delay, limit or prevent regulatory agency approvals or clearances. For example, the FDA may require additional clinical data to support approval, such as confirmatory studies and other data or studies to address questions or concerns that may arise during the FDA review process.

Delays in obtaining regulatory approval for APF530, or the issuance of a second Complete Response letter, would, among other consequences, delay the launch of APF530 and adversely affect our ability to generate revenue from sales of this product and adversely affect our ability to raise additional capital that would be necessary to sustain our operations. Given the additional delays that we would face prior to obtaining approval for APF530, if such approval is ever granted, we may need significant additional capital to fund our operations.

Even if granted, regulatory approvals may include significant limitations on the uses for which products may be marketed. Failure to comply with applicable regulatory requirements can, among other things, result in warning letters, imposition of civil penalties or other monetary payments, delay in approving or refusal to approve a product candidate, suspension or withdrawal of regulatory approval, product recall or seizure, operating restrictions, interruption of clinical trials or manufacturing, injunctions and criminal prosecution.

In addition, the marketing and manufacturing of drugs and biological products are subject to continuing FDA review, and later discovery of previously unknown problems with a product, its manufacture or its marketing may result in the FDA requiring further clinical research or restrictions on the product or the manufacturer, including withdrawal of the product from the market.

If APF530 is approved, but does not attain market acceptance by healthcare professionals and patients, our business prospects and results of operations will suffer.

Even if APF530 receives regulatory approval for commercial sale, the revenue that we may receive from the sale of APF530 may be less than expected and will depend on many factors that are outside of our control. Factors that may affect revenue from APF530, if approved, include;

• perception of physicians and other members of the health care community of the safety and efficacy relative to that of competing products;

• cost-effectiveness;

• patient and physician satisfaction with the product;

• ability to manufacture commercial product successfully and on a timely basis;

• cost and availability of raw materials;

• market size for the product;

• reimbursement policies of government and third-party payors;

23

Table of Contents

• unfavorable publicity concerning the product or similar drugs;

• the introduction, availability and acceptance of competing treatments, including those of our collaborators;

• adverse event information relating to the product;

• product liability litigation alleging injuries relating to the product;

• product labeling or product insert language required by the FDA or regulatory authorities in other countries;

• the regulatory developments related to the manufacture or continued use of the product;

• extent and effectiveness of sales and marketing and distribution support for the product; and

• our collaborators’ decisions as to the timing of product launches, pricing and discounting.

Our product revenue will be adversely affected if, due to these or other factors, the products we or our collaborators are able to commercialize do not gain significant market acceptance.