Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - EQUITY LIFESTYLE PROPERTIES INC | d492824d8k.htm |

Exhibit 99.1

ELS Equity LifeStyle Properties

OUR STORY

• One of the nation’s largest real estate networks with 383 properties containing over 142,000 sites in 32 states and British Columbia

• Unique business model

Own the land

Low maintenance costs/customer turnover costs

Lease developed sites

• High-quality real estate locations

>80 properties with lake, river or ocean frontage

>100 properties within 10 miles of coastal United States

Property locations are strongly correlated with population migration

Property locations in retirement and vacation destinations

• Stable, Predictable Financial Performance and Fundamentals

Balance Sheet Flexibility

• In business for more than 40 years

ELS

1

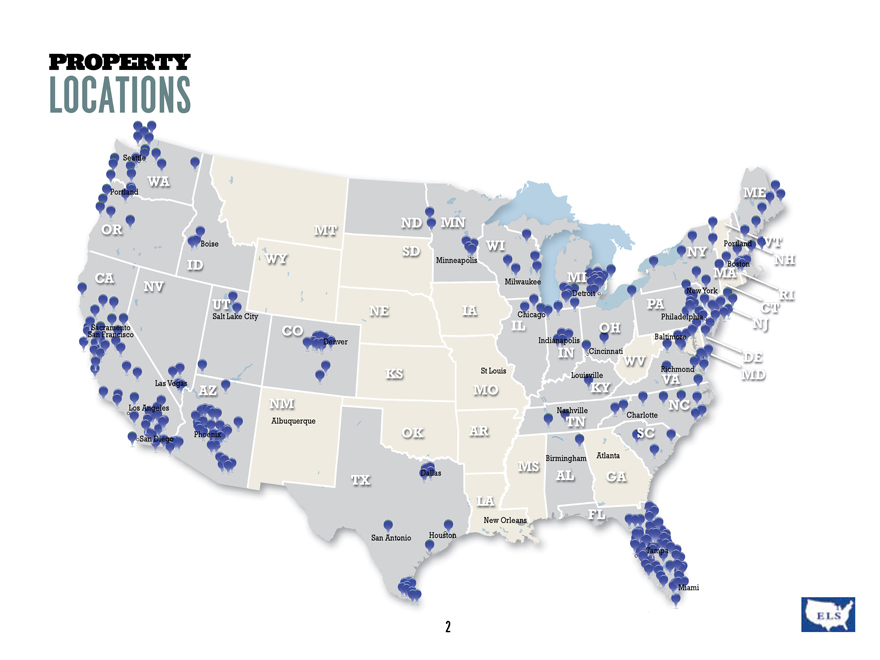

PROPERTY

LOCATIONS

Seattle

WA

Portland

ME

OR

MT

ND MN

Boise

SD

WI

NY Portland VT

ID

WY

Minneapolis

Boston NH

CA

MI

MA

NV

Milwaukee

Detroit

New York

RI

UT

NE

IA

Chicago

PA

CT

Salt Lake City

Philadelphia

Sacramento

CO

IL

OH

NJ

San Francisco

Baltimore

Denver

Indianapolis

IN Cincinnati WV

DE

Las Vegas

KS

St Louis

Louisville

Richmond VA

MD

AZ

MO

KY

Los Angeles

NM

Nashville

NC

Albuquerque

TN

Charlotte

San Diego Phoenix

OK

AR

SC

Birmingham Atlanta

Dallas

MS

TX

AL

GA

LA

New Orleans

FL

San Antonio

Houston

Tampa

Miami

ELS

2

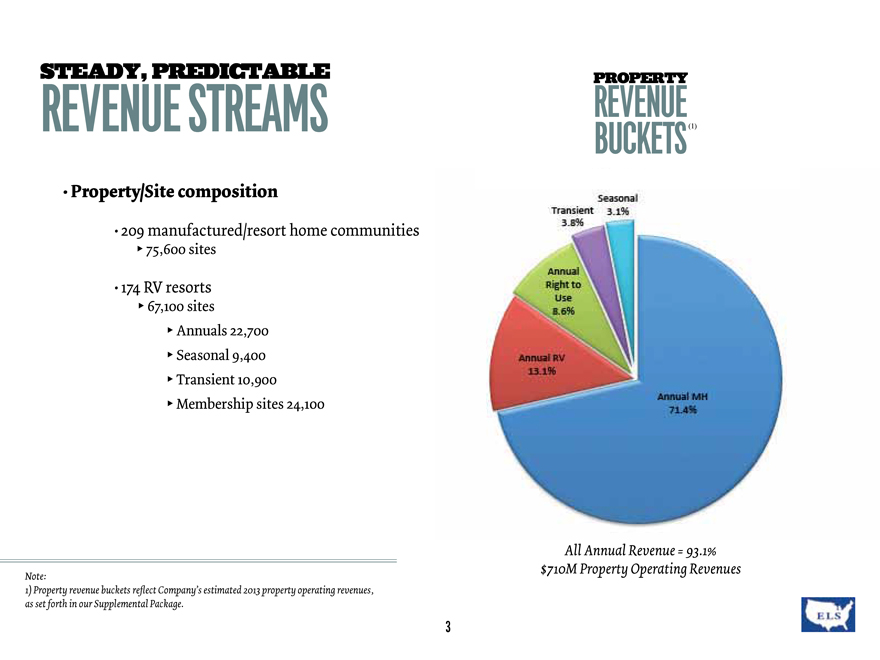

STEADY, PREDICTABLE

REVENUE STREAMS

• Property/Site composition

• 209 manufactured/resort home communities

75,600 sites

• 174 RV resorts

67,100 sites

Annuals 22,700

Seasonal 9,400

Transient 10,900

Membership sites 24,100

Note:

1) Property revenue buckets reflect Company’s estimated 2013 property operating revenues,

as set forth in our Supplemental Package.

PROPERTY

REVENUE BUCKETS(1)

Seasonal 3.1%

Transient 3.8%

Annual Right to Use 8.6%

Annual RV 13.1%

Annual MH 71.4%

All Annual Revenue = 93.1% $ 710 M Property Operating Revenues

ELS

3

OUR CUSTOMERS

• Customers own the units they place on our sites

Manufactured homes

Resort cottages (park models)

Recreational Vehicles

• We offer a lifestyle and a variety of product options to meet our customers’ needs

• We seek to create long-term relationships with our customers

Manufactured Home

RV Resort Cottage

RV Site

ELS

4

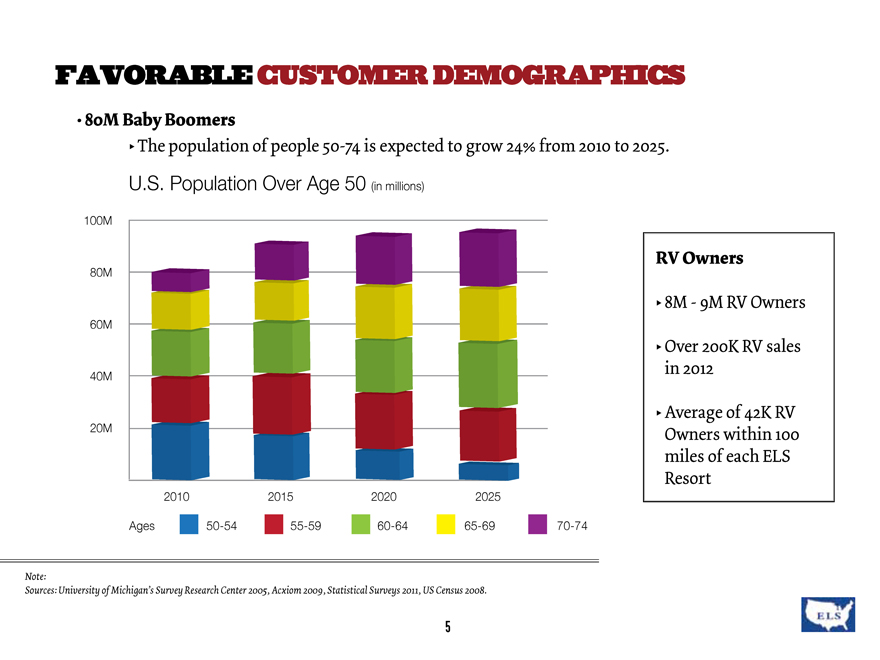

FAVORABLE CUSTOMER DEMOGRAPHICS

• 80M Baby Boomers

The population of people 50-74 is expected to grow 24% from 2010 to 2025.

U.S. Population Over Age 50 (in millions)

100M

80M

60M

40M

20M

2010

2015

2020

2025

Ages

50-54

55-59

60-64

65-69

70-74

RV Owners

8M - 9M RV Owners

Over 200K RV sales in 2012

Average of 42K RV

Owners within 100 miles of each ELS

Resort

Note:

Sources: University of Michigan’s Survey Research Center 2005, Acxiom 2009, Statistical Surveys 2011, US Census 2008.

ELS

5

|

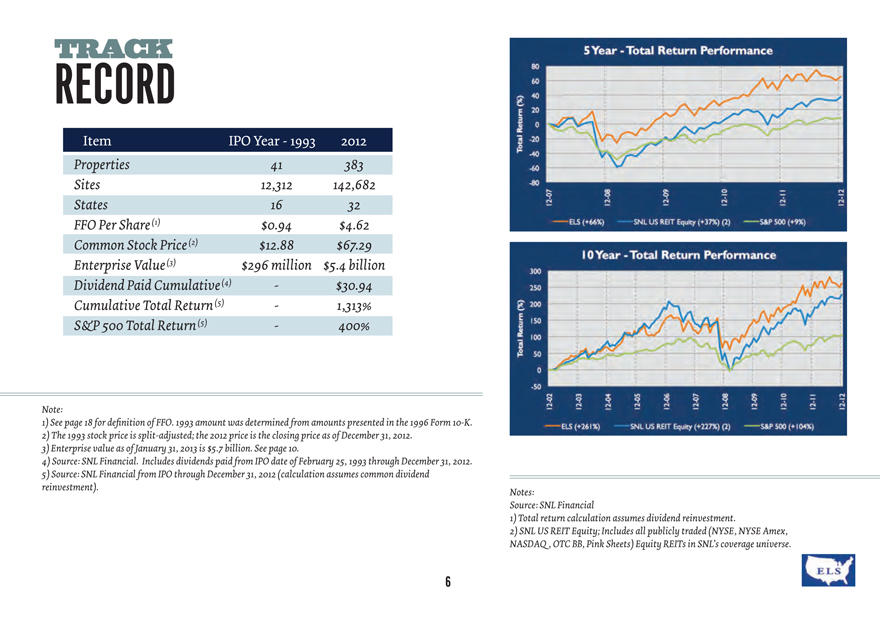

TRACK

RECORD

Item

IPO Year-1993

2012

Properties

41

383

Sites

12,312

142,682

States

16

32

FFO Per Share (1)

$0.94

$4.62

Common Stock Price (2)

$12.88

$71.60

Enterprise Value (3)

$296 million

$5.9 billion

Dividend Paid Cumulative (4)

-

$30.94

Cumulative Total Return (5)

-

1,313%

S&P 500 Total Return (5)

-

400%

5 Year-Total Return Performance

Total Return (%)

ELS SNL US REIT Equity S&P 500

10 Year - Total Return Performance

Total Return (%)

ELS SNL US REIT Equity S&P 500

Note:

1) See page 18 for definition of FFO. 1993 amount was determined from amounts presented in the 1996 Form 10-K.

2) The 1993 stock price is split-adjusted; the 2012 price is the closing price as of December 31, 2012.

3) Enterprise value as of January 31, 2013 is $5.9 billion. See page 10.

4) Source: SNL Financial. Includes dividends paid from IPO date of February 25, 1993 through December 31, 2012.

5) Source: SNL Financial from IPO through December 31, 2012 (calculation assumes common dividend reinvestment).

Notes:

Source: SNL Financial

1) Total return calculation assumes dividend reinvestment.

2) SNL US REIT Equity; Includes all publicly traded (NYSE, NYSE Amex, NASDAQ, OTC BB, Pink Sheets) Equity REITs in SNL’s coverage universe.

ELS

6

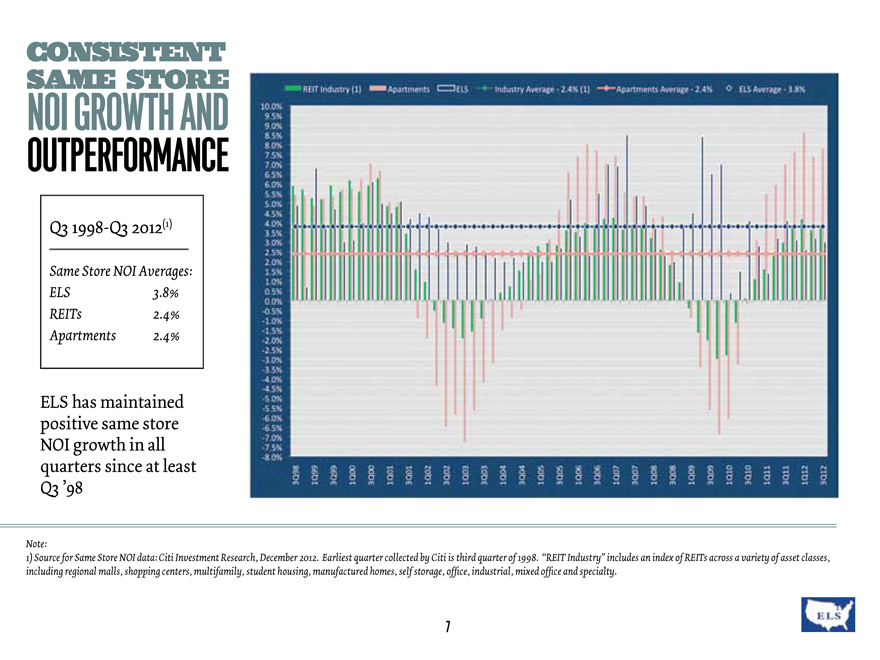

CONSISTENT

SAME STORE

NOI GROWTH AND

OUTPERFORMANCE

Q31998-Q32012(1)

Same Store NOI Averages:

ELS

3.8%

REITs

2.4%

Apartments

2.4%

ELS has maintained positive same store NOI growth in all quarters since at least

Q3’98

REIT Industry (1)

Apartment

ELS

Industry Average

Average Apartment

ELS Average

Note:

1) Source for Same Store NOI data: Citi Investment Research, December 2012. Earliest quarter collected by Citi is third quarter of 1998. “REIT Industry” includes an index of REITs across a variety of asset classes, including regional malls, shopping centers, multifamily, student housing, manufactured homes, self storage, office, industrial, mixed office and specialty.

ELS

7

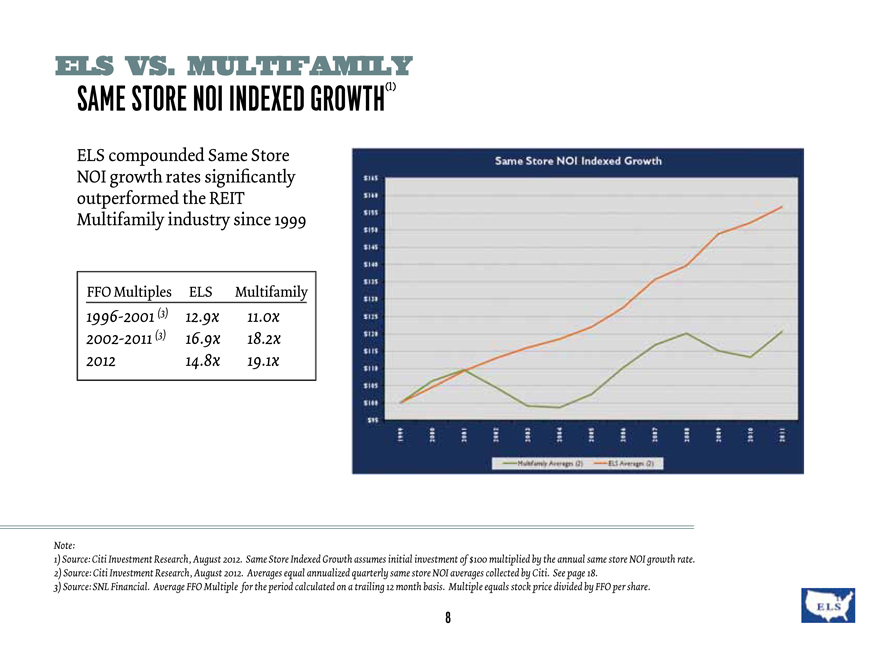

ELS VS. MULTIFAMILY

SAME STORE NOI INDEXED GROWTH(1)

ELS compounded Same Store NOI growth rates significantly outperformed the REIT Multifamily industry since 1999

FFO Multiples

ELS

Multifamily

1996-2001 (3)

12.9x

11.0x

2002-2011 (3)

16.9x

18.2x

2012

14.8x

19.1x

Same Store NOI Indexed Growth

Note:

1) Source: Citi Investment Research, August 2012. Same Store Indexed Growth assumes initial investment of $100 multiplied by the annual same store NOI growth rate.

2) Source: Citi Investment Research, August 2012. Averages equal annualized quarterly same store NOI averages collected by Citi. See page 18.

3) Source: SNL Financial. Average FFO Multiple for the period calculated on a trailing 12 month basis. Multiple equals stock price divided by FFO per share.

ELS

8

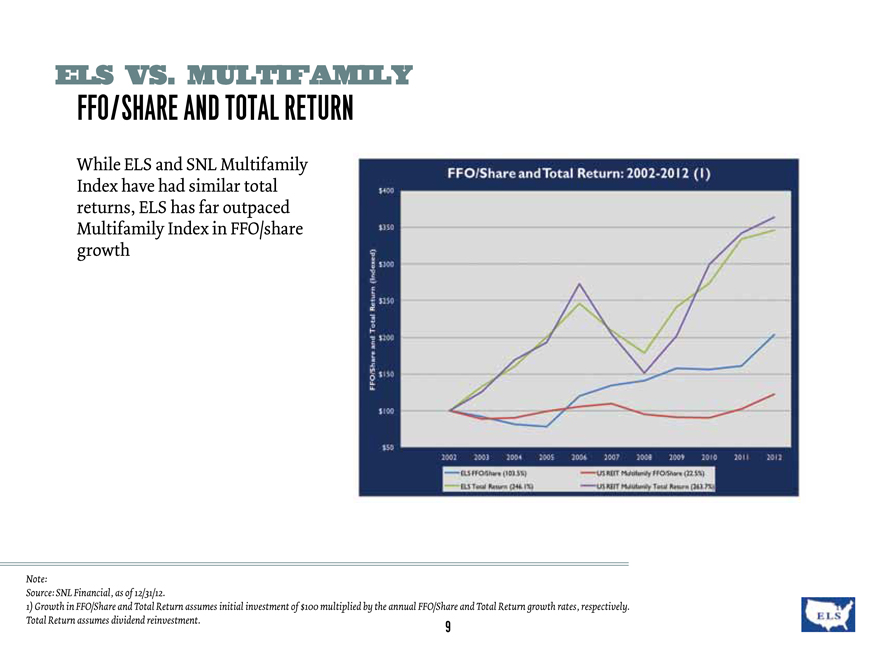

ELS VS. MULTIFAMILY

FFO/SHARE AND TOTAL RETURN

While ELS and SNL Multifamily Index have had similar total returns, ELS has far outpaced Multifamily Index in FFO/share growth

FFO/Share and Total Return: 2002-2012 (1)

FFO/Share and Total Return (Indexed)

Note:

Source: SNL Financial, as of 12/31/12.

1) Growth in FFO/Share and Total Return assumes initial investment of $100 multiplied by the annual FFO/Share and Total Return growth rates, respectively.

Total Return assumes dividend reinvestment.

ELS

9

|

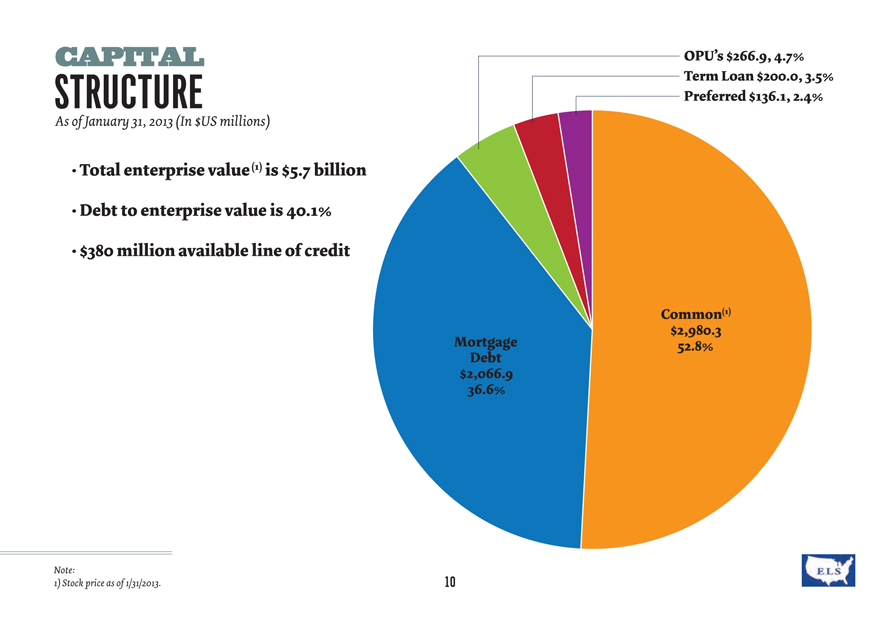

CAPITAL

STRUCTURE

As of January 31, 2013 (In $US millions)

• Total enterprise value (1) is $5.9 billion

• Debt to enterprise value is 42.2%

• $380 million available line of credit

OPU’s $266.9, 4.6%

Term Loan $200.0, 3.4%

Preferred $136.1, 2.3%

Common(1)

$2,980.3

Mortgage

51.0%

Debt

$2,266.9

38.7%

Note:

1) Stock price as of 1/31/2013. 10

ELS

SAFE HARBOR

STATEMENT

Under the Private Securities Litigation Reform Act of 1995:

The forward-looking statements contained in this presentation are subject to certain economic risks and uncertainties described under the heading “Risk Factors” in the Company’s 2011 Annual Report on Form 10-K and the Company’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2012. See Form 8-K filed January 29, 2013 for the full text of our forward-looking statements. The Company assumes no obligation to update or supplement forward-looking statements that become untrue because of subsequent events. All projections are based on 2013 budgets and proforma expectations on recent investments.

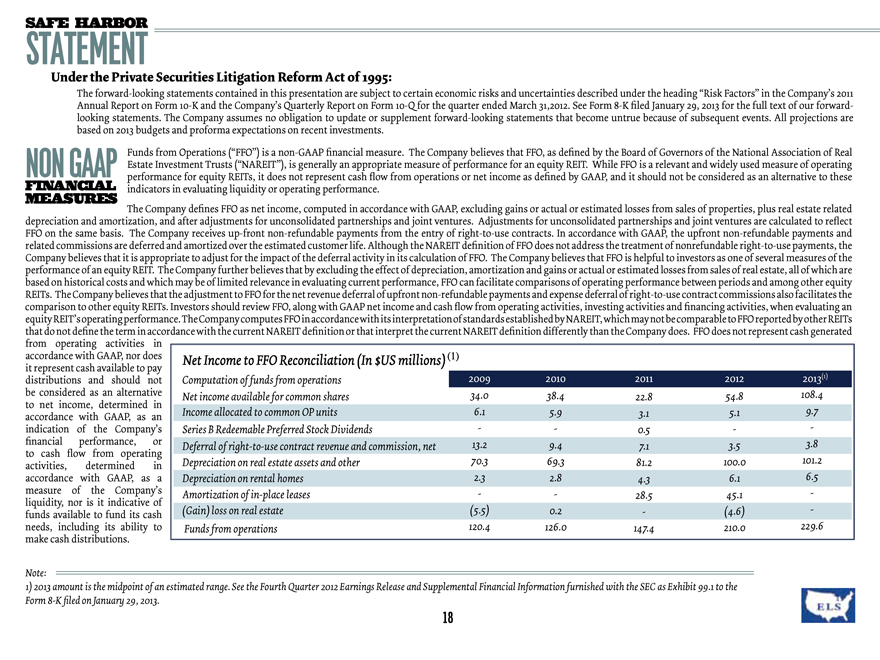

NON GAAP

FINANCIAL

MEASURES

Funds from Operations (“FFO”) is a non-GAAP financial measure. The Company believes that FFO, as defined by the Board of Governors of the National Association of Real Estate Investment Trusts (“NAREIT”), is generally an appropriate measure of performance for an equity REIT. While FFO is a relevant and widely used measure of operating performance for equity REITs, it does not represent cash flow from operations or net income as defined by GAAP, and it should not be considered as an alternative to these indicators in evaluating liquidity or operating performance.

The Company defines FFO as net income, computed in accordance with GAAP, excluding gains or actual or estimated losses from sales of properties, plus real estate related depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. Adjustments for unconsolidated partnerships and joint ventures are calculated to reflect FFO on the same basis. The Company receives up-front non-refundable payments from the entry of right-to-use contracts. In accordance with GAAP, the upfront non-refundable payments and related commissions are deferred and amortized over the estimated customer life. Although the NAREIT definition of FFO does not address the treatment of nonrefundable right-to-use payments, the Company believes that it is appropriate to adjust for the impact of the deferral activity in its calculation of FFO. The Company believes that FFO is helpful to investors as one of several measures of the performance of an equity REIT. The Company further believes that by excluding the effect of depreciation, amortization and gains or actual or estimated losses from sales of real estate, all of which are based on historical costs and which may be of limited relevance in evaluating current performance, FFO can facilitate comparisons of operating performance between periods and among other equity REITs. The Company believes that the adjustment to FFO for the net revenue deferral of upfront non-refundable payments and expense deferral of right-to-use contract commissions also facilitates the comparison to other equity REITs. Investors should review FFO, along with GAAP net income and cash flow from operating activities, investing activities and financing activities, when evaluating an equity REIT’s operating performance. The Company computes FFO in accordance with its interpretation of standards established by NAREIT, which may not be comparable to FFO reported by other REITs that do not define the term in accordance with the current NAREIT definition or that interpret the current NAREIT definition differently than the Company does. FFO does not represent cash generated from operating activities in accordance with GAAP, nor does it represent cash available to pay distributions and should not be considered as an alternative to net income, determined in accordance with GAAP, as an indication of the Company’s financial performance, or to cash flow from operating activities, determined in accordance with GAAP, as a measure of the Company’s liquidity, nor is it indicative of funds available to fund its cash needs, including its ability to make cash distributions.

Net Income to FFO Reconciliation (In $US millions)(1)

Computation of funds from operations

2009

2010

2011

2012

2013(1)

Net income available for common shares

34.0

38.4

22.8

54.8

108.4

Income allocated to common OP units

6.1

5.9

3.1

5.1

9.7

Series B Redeemable Preferred Stock Dividends

-

-

0.5

-

-

Deferral of right-to-use contract revenue and commission, net

13.2

9.4

7.1

3.5

3.8

Depreciation on real estate assets and other

70.3

69.3

81.2

100.0

101.2

Depreciation on rental homes

2.3

2.8

4.3

6.1

6.5

Amortization of in-place leases

-

-

28.5

45.1

-

(Gain) loss on real estate

(5.5)

0.2

-

(4.6)

-

Funds from operations

120.4

126.0

147.4

210.0

229.6

Note:

1) 2013 amount is the midpoint of an estimated range. See the Fourth Quarter 2012 Earnings Release and Supplemental Financial Information furnished with the SEC as Exhibit 99.1 to the Form 8-K filed on January 29, 2013.

ELS

18