Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - BANCORPSOUTH INC | d491151d8k.htm |

BancorpSouth, Inc.

Investor Presentation

2013 KBW Boston Bank Conference

Exhibit 99.1 |

Forward Looking Information

2

Certain statements contained in this presentation and the accompanying slides may not be based on

historical facts and are “forward-looking statements” within the meaning of

Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as

amended. These forward-looking statements may be identified by reference to a future period

or by the use of forward-looking terminology, such as “anticipate,”

“believe,” “estimate,” “expect,” “foresee,” “may,” “might,” “will,” “intend,” “could,” “would” or “plan,” or future or conditional verb

tenses, and variations or negatives of such terms. These forward-looking statements

include, without limitation, statements about maturities of our CDs, our strategic focus,

revenue growth opportunities, fee revenue growth, improvement of asset quality, geographic expansion of mortgage originators,

expansion of insurance agencies, results of operations and financial condition. We caution you not to

place undue reliance on the forward-looking statements contained in this presentation, in

that actual results could differ materially from those indicated in such forward-looking statements as a

result of a variety of factors. These factors include, but are not limited to, conditions in the

financial markets and economic conditions generally, the ongoing debt crisis and the downgrade

of the sovereign credit ratings for various nations, the adequacy of the Company’s provision and allowance for

credit losses to cover actual credit losses, the credit risk associated with real estate construction,

acquisition and development loans, losses resulting from the significant amount of the

Company’s other real estate owned, limitations on the Company’s ability to declare and pay dividends, the short-term

and long-term impact of changes to banking capital standards on the Company’s regulatory

capital and liquidity, the impact of legal or administrative proceedings, the availability of

capital on favorable terms if and when needed, liquidity risk, governmental regulation, including the Dodd Frank Act, an

supervision of the Company’s operations, the impact of regulations on service charges on the

Company’s core deposit accounts, the susceptibility of the Company’s business to

local economic conditions, the soundness of other financial institutions, changes in interest rates, the impact of monetary

policies and economic factors on the Company’s ability to attract deposits or make loans,

volatility in capital and credit markets, reputational risk, the impact of hurricanes or other

adverse weather events, any requirement that the Company write down goodwill or other intangible assets, diversification

in the types of financial services the Company offers, competition with other financial services

companies, risks in connection with completed or potential acquisitions, the Company’s

growth strategy, interruptions or breaches in the Company’s information system security, the failure of certain

third party vendors to perform, dilution caused by the Company’s issuance of any additional

shares of its common stock to raise capital or acquire other banks, bank holding companies,

financial holding companies and insurance agencies, the effectiveness of the Company’s internal controls, other

factors generally understood to affect the financial results of financial services companies and other

factors detailed from time to time in the Company’s press releases and filings with the

Securities and Exchange Commission. Forward-looking statements speak only as of the date they were made, and,

except as required by law, we do not undertake any obligation to update or revise forward-looking

statements to reflect events or circumstances after the date of this presentation. Certain

tabular presentations may not reconcile because of rounding. Unless otherwise noted, any quotes in this

presentation can be attributed to company management. |

About

BancorpSouth, Inc. (NYSE:BXS) Total assets of $13.4 billion

Headquartered in Tupelo, MS

292 locations with reach throughout an 8-state footprint

Customer-focused business model with comprehensive line of

financial products and banking services for individuals and small to

mid-size businesses

Strong core capital base consisting of 100% common equity

Market capitalization of $1.4 billion

3

Data as of December 31, 2012 |

Community Bank Structure –

8 State Footprint

4 |

COMMUNITY BANK

Personal Banking

Business Banking

Deposit Offerings

Business Loans

Consumer Lending

Full Range of Deposit Products

Home Equity Lending

Treasury Management

Mobile/Internet Banking

Merchant Services

Prepaid Cards

Payroll and HR Management

Insurance

164 Licensed Producers in 29 Locations

Commercial, P&C, and Life Insurance

Trust and Wealth Management

$6.9 billion total Assets Under Management

Mortgage

107 Originators in 72 Locations

$2.0 Billion in Production in 2012

5

Equipment Finance and Leasing

Territory Managers Covering 14 States

Portfolio Balance of $500 Million

Wide Range of Product Offerings

All Information as of December 31, 2012 |

Diversified Loan Portfolio

Loans By Category

Loans By Geography

6

Commercial &

Industrial

17%

Consumer Mortgages

22%

Home

Equity

6%

Agricultural

3%

Construction,

Acquisition & Dev.

9%

Commercial Real

Estate

20%

Credit Cards

1%

Other

7%

AL & FL

Panhandle

8%

AR**

13%

MS**

30%

MO

5%

Greater

Memphis

6%

TN**

8%

TX & LA

20%

Other*

10%

$8.6B Portfolio

C&I Owner-Occupied

15% |

Core

Deposit Franchise 100%

core

deposits

–

no

reliance

on

brokered deposits

Noninterest bearing deposits have

grown approximately 12% since

December 31, 2011

Cost of total deposits for the quarter

ended December 31, 2012 was 0.47%

Approximately $802 million in CDs

maturing over the next two quarters at a

weighted average rate of approximately

0.73%

$11.1B Total

Deposit Composition

7

Non-Interest

Bearing

23%

Interest Bearing

DDA

43%

Time

24%

Savings

10%

As of and for the period ended December 31, 2012

(except where otherwise indicated) |

Diversified Revenue Stream

*Excludes net securities gains of $0.4 million and negative MSR valuation adjustment

of $3.2 million Approximately 40% of Total Revenue is Derived from Noninterest

Sources Total Noninterest Revenue of $282.9M*

8

Total Revenue of $697.5M*

Net Interest

Revenue

59%

Noninterest

Revenue

41%

Insurance

Commissions

32%

Mortgage

lending

21%

Card and

merchant fees

11%

Service

charges

20%

Trust income

4%

Other

12%

Percentages and amounts based on data for the twelve months ended December 31,

2012 |

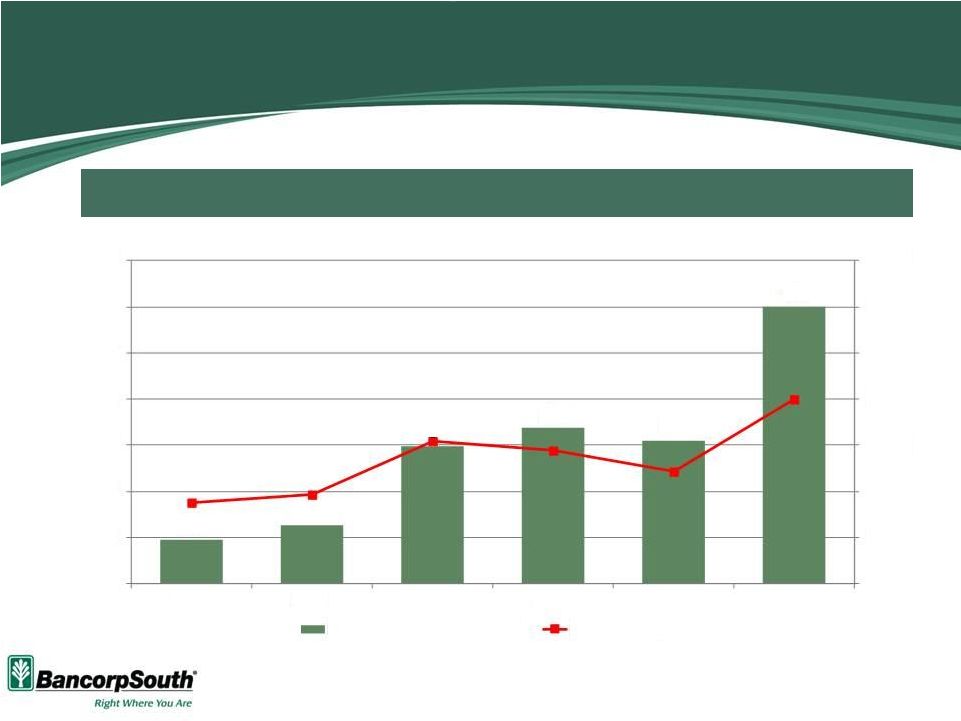

9

Insurance Commissions

Dollars in millions

*Pre-tax

Premium Dollars Written

Commission Revenue

Margin*

30%

27%

21%

19%

20%

17%

$71

$87

$81

$82

$87

$90

$0

$200

$400

$600

$800

$1,000

$0

$20

$40

$60

$80

$100

2007

2008

2009

2010

2011

2012

Insurance Commission Revenue

Premium Dollars Written

Insurance Commissions Account for Approximately 1/3 of Noninterest Revenue

|

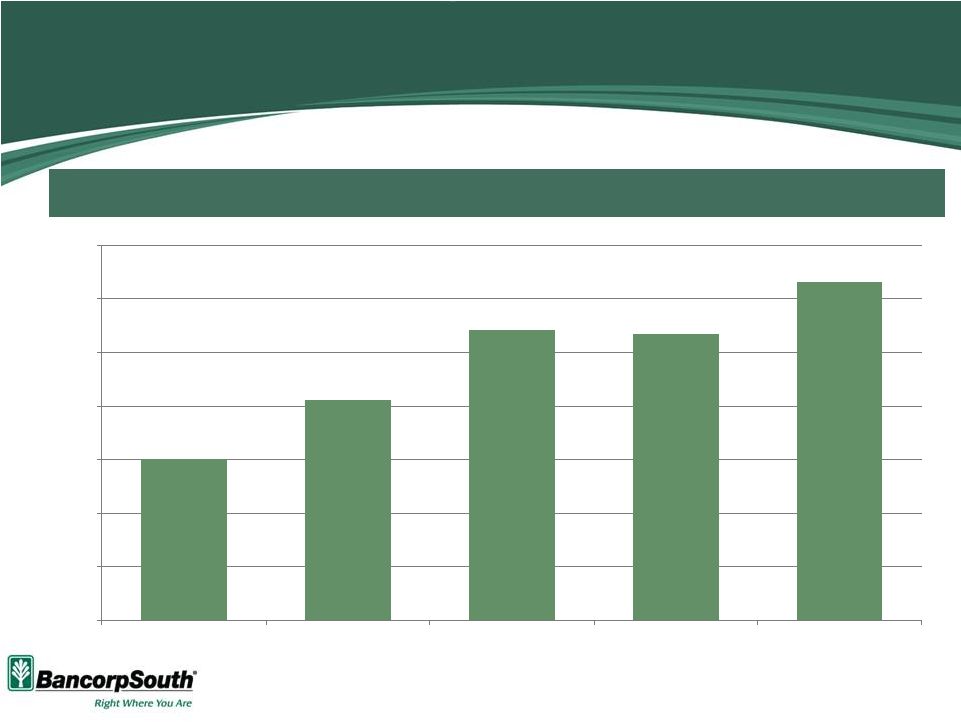

10

Mortgage Lending Revenue

Dollars in millions

*Excludes MSR valuation adjustments

Revenue

Production

$10

$13

$30

$34

$31

$60

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$0

$10

$20

$30

$40

$50

$60

$70

2007

2008

2009

2010

2011

2012

Mortgage Lending Revenue*

Mortgage Production

Record Mortgage Production of $2.0 Billion for 2012 |

11

Financial Highlights |

Fourth Quarter Financial Highlights

At and for the three months ended December 31, 2012

12

Net income of $17.0 million, or $0.18 per diluted share

Mortgage production of $549 million, which contributed to $17.2

million

of mortgage lending revenue

OREO sales of $27.9 million contributed to a 19.5% decline in OREO

and a 10.3% reduction in total NPAs

NPLs decreased $13.8 million, or 5.6%, and NPAs declined $38.7 million,

or 10.3%

Continued improvement in many other credit quality indicators

including classified loans, net charge-offs, and near term delinquencies

Capital ratios continue to improve |

Net

Income Meaningful Improvement in Profitability Levels

13

Dollars in millions

$120.4

$82.7

$22.9

$37.6

$84.3

$0

$25

$50

$75

$100

$125

2008

2009

2010

2011

2012

. |

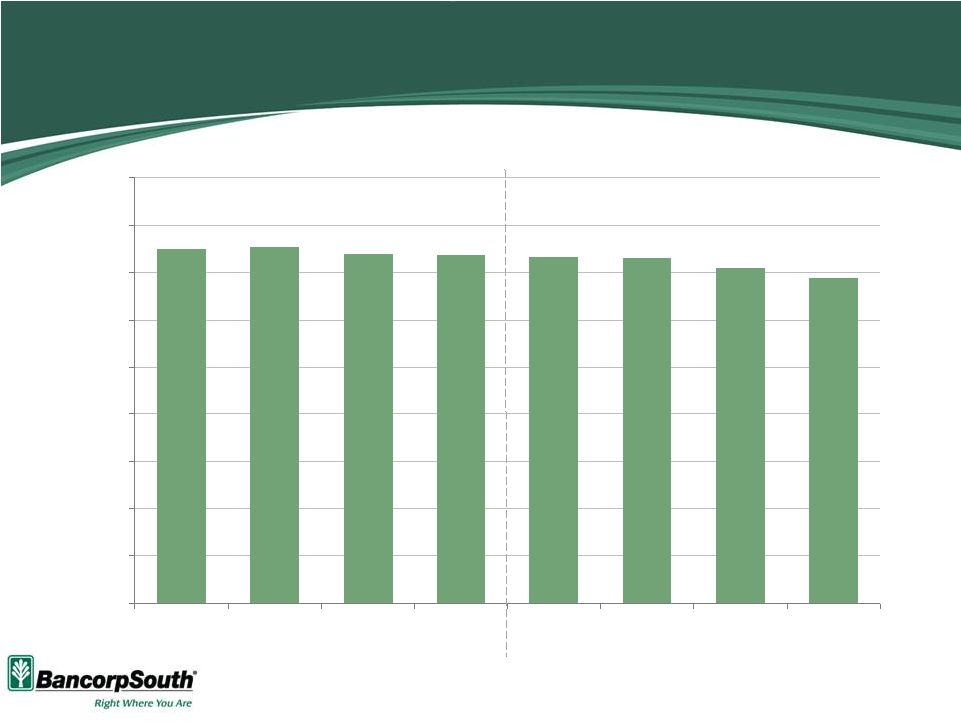

3.75%

3.77%

3.70%

3.69%

3.66%

3.65%

3.55%

3.44%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

2008

2009

2010

2011

3/31/12

6/30/12

9/30/12

12/31/12

Net Interest Margin

Fiscal Year

Quarter Ended

Shown on a fully taxable equivalent basis

14 |

NPA

Improvement Total NPAs Declined Approximately $160 Million, or 32%, During

2012 15

$409

$394

$425

$380

$363

$322

$285

$267

$247

$234

$83

$133

$136

$151

$163

$174

$168

$144

$128

$103

$492

$528

$561

$531

$525

$496

$453

$411

$376

$337

$0

$125

$250

$375

$500

$625

9/30/10

12/31/10

3/31/11

6/30/11

9/30/11

12/31/11

3/31/12

6/30/12

9/30/12

12/31/12

NPLs

OREO

Dollars in millions

NPAs include NPLs and other real estate owned

NPLs include non-accrual loans, loans 90+ days past due and restructured

loans |

Dollars in millions

Data for quarters ended as of dates shown

Payments Received on Non-Accrual Loans

16

Payments of $106 million received on non-accrual loans during 2012

$15.1

$20.6

$27.1

$26.7

$31.6

$0

$5

$10

$15

$20

$25

$30

$35

12/31/11

3/31/12

6/30/12

9/30/12

12/31/12 |

$0

$100

$200

$300

$400

12/31/11

3/31/12

6/30/12

9/30/12

12/31/12

Non-Accrual Lns Paying as Agreed

All Other Non-Accrual Lns

Non-Accrual Loans

Dollars in millions

“Paying

as

Agreed”

includes

loans

<

30

days

past

due

with

payments

occurring

at

least

quarterly

55%

57%

56%

56% of non-accrual loans were paying as agreed as of December 31, 2012

51%

17

54% |

Dollars in millions

Data for quarters ended as of dates shown

Positive Trend in Net Charge-Offs

% Avg. Loans

18

$51

$51

$52

$33

$23

$24

$23

$12

$13

$11

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

$0

$10

$20

$30

$40

$50

$60

9/30/10

12/31/10

3/31/11

6/30/11

9/30/11

12/31/11

3/31/12

6/30/12

9/30/12

12/31/12

Net charge-offs

Net charge-offs / average loans |

19

Strategic Focus |

Strategic Focus

Revenue Growth Opportunities

Pursue quality loan growth

Continue to focus on fee revenue growth

Expand mortgage originators geographically

Continue to seek opportunities for expansion in insurance

Efficiency Opportunities

Efficiency

ratio

of

78%

in

2012

–

focus

on

expense

reduction

in

all

areas

of

the bank

20 |

Summary

Meaningful increases in profitability levels

Consistent core earnings with approximately 40% of total revenue

derived from noninterest sources

Record mortgage loan production

Growth in other noninterest revenue sources including insurance commissions

Continued progress in improving asset quality

7

th

consecutive quarter of improvement in total NPLs and NPAs

Revenue growth opportunities

Efficiency and expense control

Data as of and for the year ended December 31, 2012

21 |