Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - GULFMARK OFFSHORE INC | d484801d8k.htm |

GulfMark Offshore, Inc

GulfMark Offshore, Inc

2013 Credit Suisse Energy Summit

2013 Credit Suisse Energy Summit

Exhibit 99.1 |

Forward Looking Statements

Forward Looking Statements

2

NYSE:

GLF

www.GulfMark.com Cautionary Statement Regarding

Forward-Looking Statements

Certain statements and information in this presentation may constitute “forward-looking statements” within the meaning of the

Private Securities Litigation Reform Act of 1995. The words “believe,” “expect,”

“anticipate,” “plan,” “intend,” “foresee,” “should,” “would,”

“could” or other similar expressions are intended to identify forward-looking

statements, which are generally not historical in nature. These forward-looking statements

are based on our current expectations and beliefs concerning future developments and their potential effect on

us. While management believes that these forward-looking statements are reasonable as and when

made, there can be no assurance that future developments affecting us will be those that we

anticipate. All comments concerning our expectations for future revenues are based on our

forecasts for our existing operations. Our forward-looking statements involve significant risks and uncertainties (some of which are

beyond our control) and assumptions that could cause actual results to differ materially from our

historical experience and our present expectations or projections. Among the important factors

that could cause actual results to differ materially from those in the forward- looking

statements include, but are not limited to: the price of oil and gas and its effect on offshore drilling, vessel utilization and day rates;

industry volatility; fluctuations in the size of the offshore marine vessel fleet in areas where the

Company operates; changes in competitive factors; delays or cost overruns on construction

projects, and other material factors that are described from time to time in the Company’s

filings with the SEC, including the registration statement and the Company’s Annual Report on

Form 10-K for the year ended December 31, 2011, Quarterly Reports on Form 10-Q and

Current Reports on Form 8-K. Consequently, the forward-looking statements contained herein

should not be regarded as representations that the projected outcomes can or will be achieved. These

forward-looking statements speak only as of the date hereof. We undertake no obligation to

publicly update or revise any forward-looking statements after the date they are made,

whether as a result of new information, future events or otherwise.

|

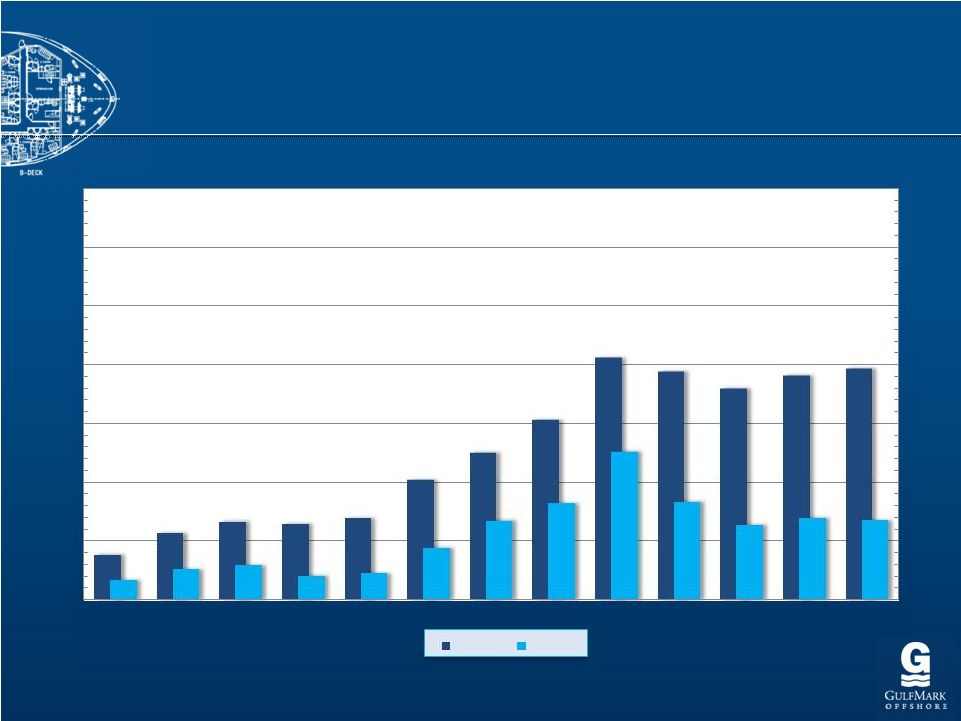

Long Term Revenue & EBITDA

Long Term Revenue & EBITDA

(in millions of dollars)

(in millions of dollars)

3

* Note: Adjusted for Special Items, See Supporting Information at the end of this

Presentation $0

$100

$200

$300

$400

$500

$600

$700

$0

$100

$200

$300

$400

$500

$600

$700

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012 TTM

Revenue

EBITDA* |

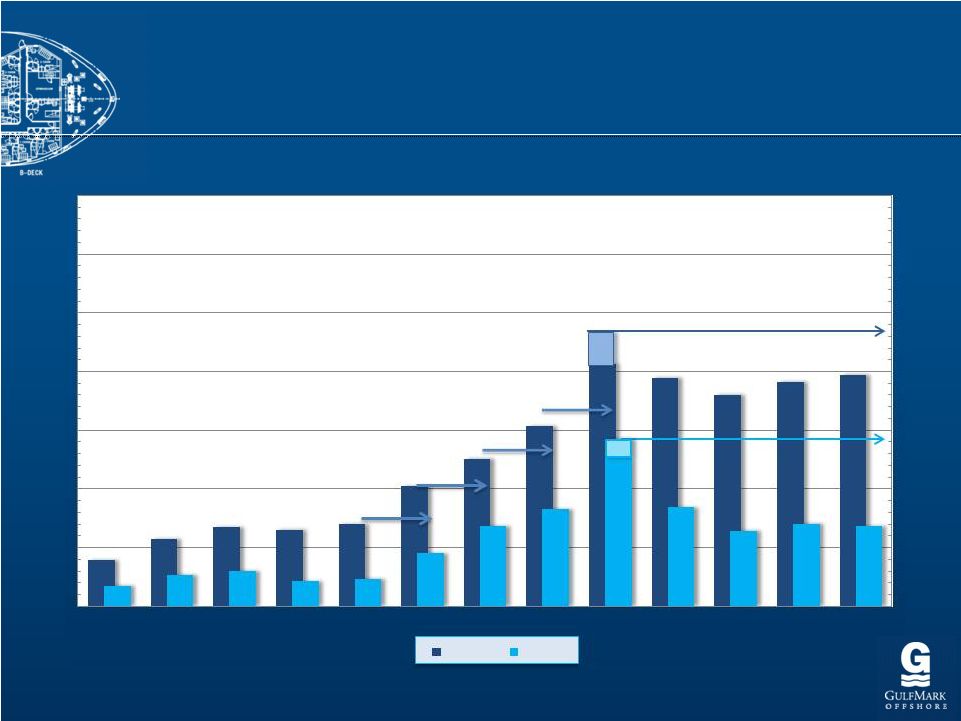

Pro

Forma Prior Peak Revenue & EBITDA Pro Forma Prior Peak Revenue &

EBITDA (in millions of dollars)

(in millions of dollars)

4

* Note: Adjusted for Special Items, See Supporting Information at the end of this

Presentation •

Pro Forma for July 1, 2008 Acquisition

•

Prior Up-Cycle Incremental EBITDA Margins Average 72%

•

Substantial Fleet Upgrades Since 2008

•

11 New Vessels Beginning in 2013

68%

100%

53%

71%

$0

$100

$200

$300

$400

$500

$600

$700

$0

$100

$200

$300

$400

$500

$600

$700

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012 TTM

Revenue

EBITDA* |

5

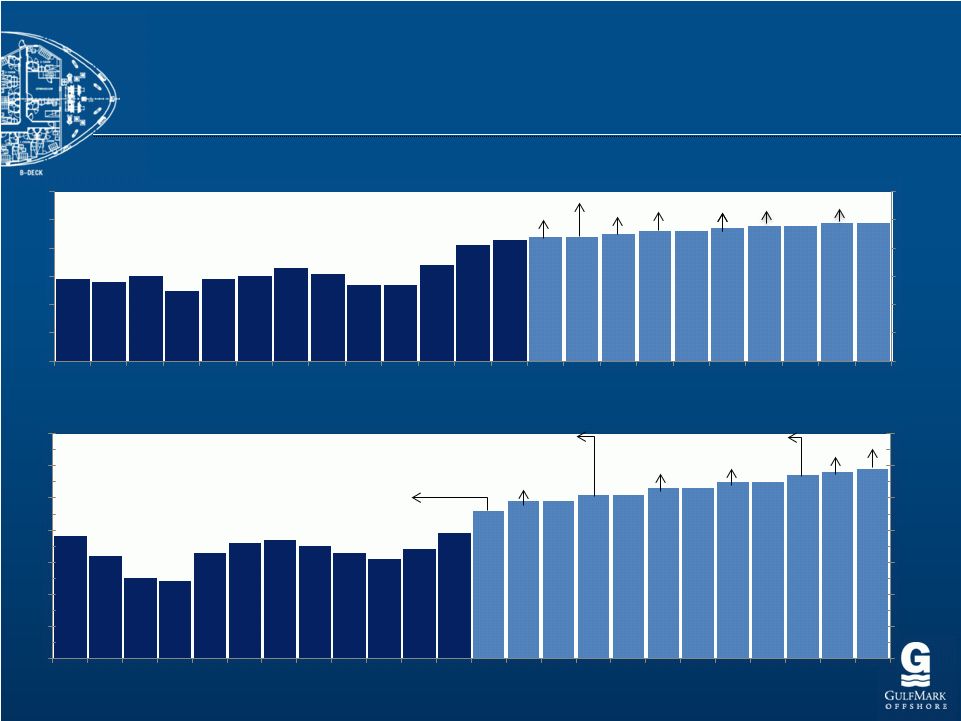

Total Revenue in Backlog

Total Revenue in Backlog

(in thousands of dollars)

(in thousands of dollars)

Day Rate in

Backlog

$0

$2,500

$5,000

$7,500

$10,000

$12,500

$15,000

$17,500

$20,000

$22,500

$25,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000 |

6

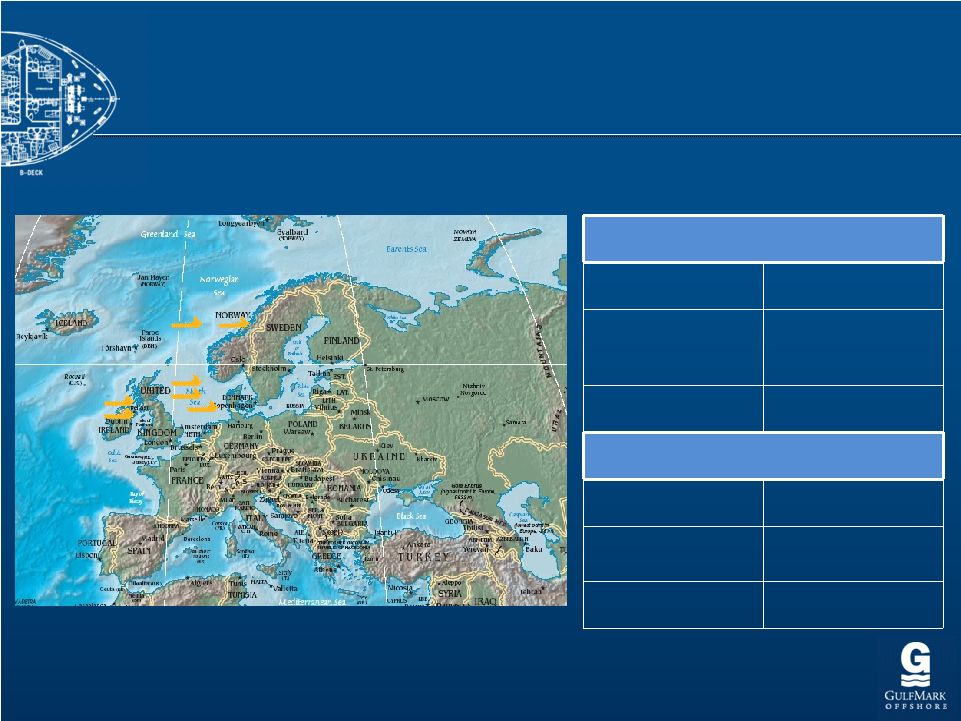

Global Vessel Diversification

Global Vessel Diversification

Revenue Breakout by Region

–

Twelve Months Ended

September 30, 2012

US

Gulf

PSV

15

West

Africa

PSV

1

Mexico

AHTS

2 Trinidad

PSV

2 FSV

1

North

Sea

PSV

20

AHTS

1

SpV

1 Worldwide

PSV

AHTS

FSV

SpV

Total

70

SE

Asia

PSV

4

AHTS 12

Brazil

PSV

6

SpV

1

FSV

2 2

48

17

AHTS

3

2 |

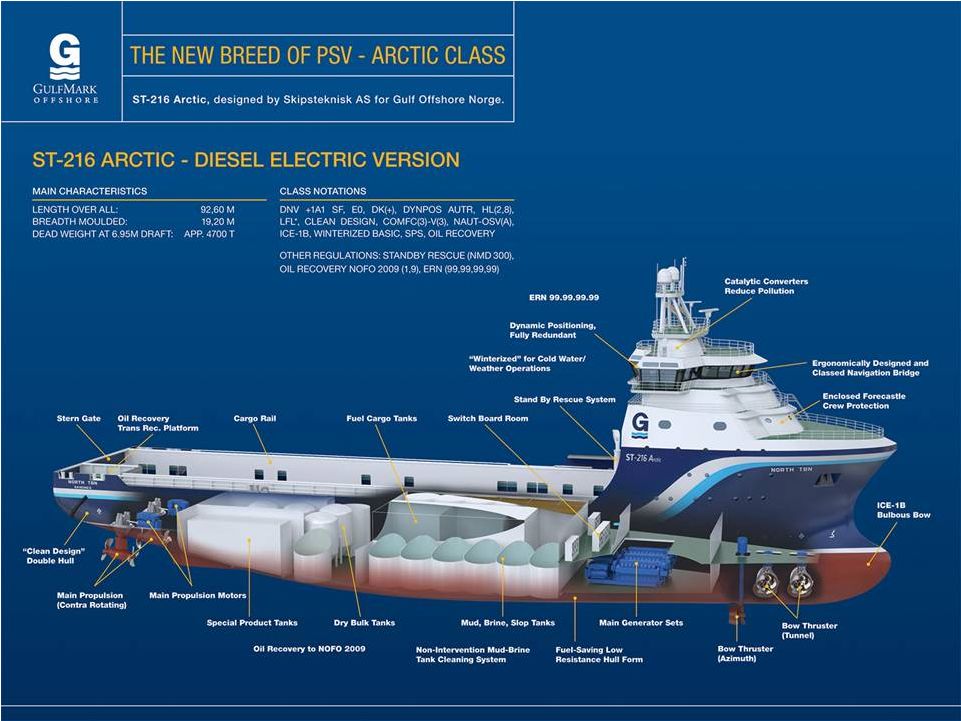

The GulfMark Fleet

The GulfMark Fleet

7 |

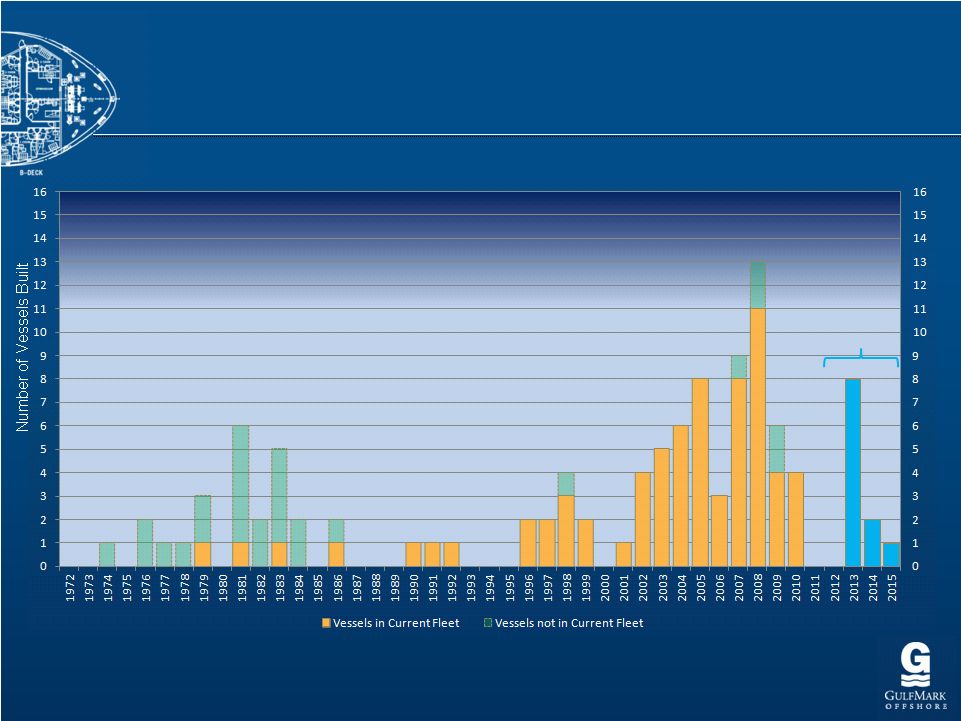

Young & Versatile Fleet

Young & Versatile Fleet

8

Number of Vessels GulfMark Built Per Year

New Build

Deliveries |

Building For Our Future

Building For Our Future

9

Significant number of new generation rigs on order

Increasing Activity both in the North Sea and New Frontiers

Industry call for higher specification vessels to meet increasing regulatory

demands:

•

Deeper Waters and Harsher Environments

•

Increased cargo carrying capacity and flexibility

•

Enhanced Green

Footprint and offering greater safety support |

10

New Build Program Overview

New Build Program Overview

Two MMC 887 300 Class DP 2 (Europe)

One MMC 879 280 Class DP2 (Europe)

Two UT 755 XL 250 Class DP2 (Europe)

Two ST-216 300 Class Arctic DP2 (Europe)

Two 280 Class PSV DP2 (US)

Two 300 Class PSV DP2 (US) |

New Build and Vessel Enhancement

New Build and Vessel Enhancement

Program Summary

Program Summary

11

•

North Sea

•

7 Newbuild Vessels

•

North Sea vessels hedged in EUR

•

DP2 Green PSVs (300 Class (2), 300 Class Arctic (2), 280 Class (1), 250 Class

(2)) •

Staggered delivery of Newbuilds-

2Q 2013 through 1Q 2014

•

U.S. GOM

•

4 Newbuild US Flagged Vessels for Approximately $170 million

•

DP2 Green PSVs (280 Class(2), 300 Class (2))

•

Staggered delivery -

3Q 2013 through 1Q 2015 |

12

2012 Phase 1: 190’

to 230’

Three

Vessels

Completed

2011-12

Avg. Cost Per Vessel

$2.2 million

Avg. Incremental Days Out of Service

77

Avg. Day Rate % Increase

+40%

Avg. Utilization Percentage Increase

18%

Estimated Payback Period (Including

Opportunity Cost)

10.5 months

Return on Net Capital Employed

117%

U.S.

GOM

–

Stretch

Program

•

Completed Three 190’

Vessels in 2011-2012, Will Complete Three More During Q1 2013

•

Four Additional 190’

Vessels Will Become Stretch Program Candidates During 2015

•

Next Steps –

210 Class 260 Class

•

10 Vessel Candidates, Regulatory Approval Expected Q1 2013

New Build and Vessel Enhancement

New Build and Vessel Enhancement

Program Summary, Cont’d

Program Summary, Cont’d |

Building For Our Future: 2013 & Beyond

Building For Our Future: 2013 & Beyond

(U.S. dollars, in millions)

(U.S. dollars, in millions)

13

Vessels Under

Construction

Vessel Type

Initial

Operating

Region

Estimated

Construction

Cost

Estimated

Average Annual

EBITDA

Implied EBITDA

Multiple

300 Class

PSV

North Sea

$37.0

$8.2

4.5x

300 Class

PSV

North Sea

$37.0

$8.2

4.5x

280 Class

PSV

North Sea

$34.0

$7.7

4.4x

300 Class Arctic

PSV

North Sea

$58.0

$10.8

5.4x

300 Class Arctic

PSV

North Sea

$60.0

$10.8

5.6x

250 Class

PSV

North Sea

$31.0

$7.4

4.2x

250 Class

PSV

North Sea

$31.0

$7.4

4.2x

US 280 Class

PSV

Americas

$36.0

$6.5

5.5x

US 280 Class

PSV

Americas

$36.0

$6.5

5.5x

US 300 Class

PSV

Americas

$48.0

$8.8

5.5x

US 300 Class

PSV

Americas

$48.0

$8.8

5.5x

Total

$456.0

$91.1

5.0x |

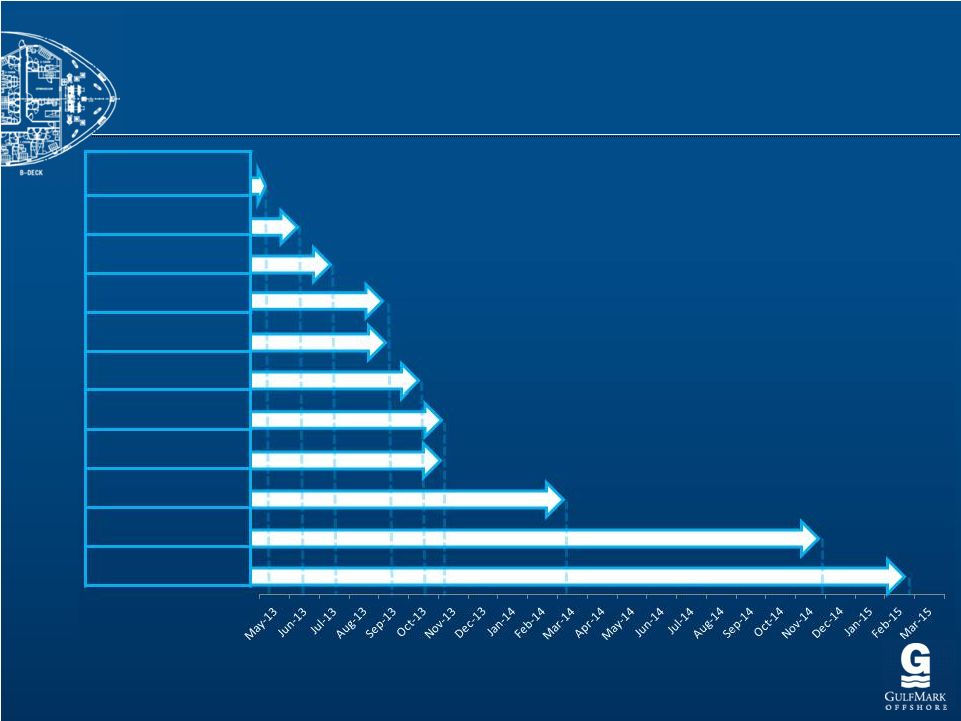

New Build Delivery Schedule

New Build Delivery Schedule

14

280 Class Europe

300 Class Artic Europe

280 Class Europe

300 Class Europe

280 Class US

250 Class Europe

300 Class Artic

280 Class US

250 Class Europe

300 Class US

300 Class US |

Market

Market

Drivers

Drivers

15 |

Rig Growth in the North Sea

Rig Growth in the North Sea

16

Source: IHS Petrodata , Carnegie Research

Floating Rigs

Active

41

Scheduled

Arrivals/Activations

(by 2014)

16

% Increase

39%

Jackups

Active

42

Scheduled Arrivals

(by 2014)

7

% Increase

17% |

Rig Growth in the North Sea

Rig Growth in the North Sea

17

Source: IHS Petrodata

Jackups

Jackups

Floating Rigs

Floating Rigs

0

10

20

30

40

50

60

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

0

10

20

30

40

50

60

West Hercules,

COSL Promoter,

Leiv Eriksson

Stena Carron,

Island Innovator

Eirik Raude

Songa Equinox,

Ocean Patriot

Deepsea Aberdeen,

Songa Endurance

Songa Encourage, Bollsta Dolphin

Songa Enabler

Atwood Advantage, Sedco 712

North Dragon

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Noble Regina Allen

Prospecter 1

ENSCO 120

West Linus

Maersk XL

Enhanced 1

Maersk XL

Enhanced 2

Maersk XL

Enhanced 3 |

Floating Rig Growth in the U.S. GOM

Floating Rig Growth in the U.S. GOM

18

Source:

IHS

Petrodata

–

August

2012

Floating Rigs in U.S. GOM

Active

36

Scheduled Arrivals

(by 2014)

11

% Increase

31% |

Floating Rig Growth in the U.S. GOM

Floating Rig Growth in the U.S. GOM

19

Source: Barclays, IHS Petrodata

0

5

10

15

20

25

30

35

40

45

50

55

0

5

10

15

20

25

30

35

40

45

50

55

Helix 534,

ENSCO

8506

West Auriga

Noble Globetrotter II

Ocean Confidence

West

Vela, Maersk Drsh Tbn 1

Pacific

Sharav

Deepwater Invictus

Noble Bob Douglas, Maersk Deepwater Advanced 2

Moratorium and Recovery

Planned |

Worldwide Sub Sea –

Worldwide Sub Sea –

Driving the Future

Driving the Future

20

Source:

Douglas-Westwood’s World Subsea Vessel Operations Market Forecast

2012-2016 Subsea Demand Expected to Increase 33% and

Annual Expenditure double to $20.3 Billion by 2016

Set to Top $77 Billion Over Next Five Years

Increase of 63% Over Previous Five Year Period

Sub Sea Work Requires Newer, More Specialized

Vessels and Support Equipment

Between 2013 and 2017, $91bn Will be Spent on Floating

Production

Systems

(FPS)

-

an

Increase

of

100%

over

the

Preceding Five-Year Period.

A Total of 121 Floating Production Units are Forecast to

be Installed -

a 37% Increase

Sub

Sea

Activity

is

Continuing

to

Expand

FPSO

Spending

–

Projected |

Financial Information

Financial Information

21 |

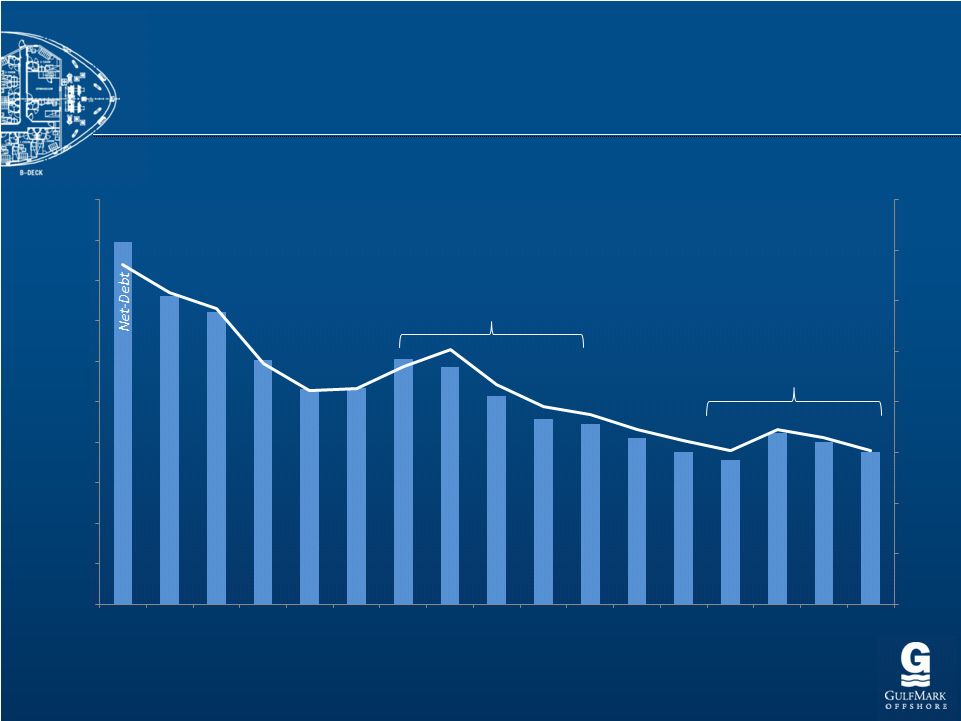

22

Consistent Reduction in

Consistent Reduction in

Net Debt Position

Net Debt Position

0%

5%

10%

15%

20%

25%

30%

35%

40%

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Net-Debt to

Total Book

Capitalization

Finalization of Previous

New-

Build Program

Initiation of Current

New-Build Program |

23

Investment Highlights

Investment Highlights

Industry Leaders in QHSE Performance & People Development

Global Presence and Diverse Operations Expertise

Financial Stability & Flexibility to Pursue Opportunities

Growth through Both Acquisition and New Construction

Young, Versatile, High-Specification Fleet |

Reconciliation of Adjusted EBITDA

Reconciliation of Adjusted EBITDA

24

EBITDA is defined as net income (loss) before interest expense, net,

income tax provision, and depreciation and amortization, which includes impairment. Adjusted

EBITDA is calculated by adjusting EBITDA for certain items that we

believe are non-cash or unusual, consisting of: (i) loss from unconsolidated ventures; (ii) minority

interest;

and

(iii)

other

(income)

expense,

net.

EBITDA

and

Adjusted

EBITDA

are

not

measurements

of

financial

performance

under

GAAP

and

should

not

be

considered

as an alternative to cash flow data, a measure of liquidity or an

alternative to income from operations or net income as indicators of our operating performance or any other

measures

of

performance

derived

in

accordance

with

GAAP.

EBITDA

and

Adjusted

EBITDA

are

presented

because

we

believe

they

are

used

by

security

analysts,

investors and other interested parties in the evaluation of companies

in our industry. However, since EBITDA and Adjusted EBITDA are not measurements determined in

accordance with GAAP and are thus susceptible to varying calculations,

EBITDA and Adjusted EBITDA as presented may not be comparable to other similarly titled

measures of other companies.

Net (loss) income

$24.0

$0.5

($4.6)

$38.4

$89.7

$99.0

$183.8

$50.6

($34.7)

$49.9

$47.8

Interest expense, net

10.9

12.8

17.0

18.4

14.4

4.8

12.8

19.9

20.7

21.6

22.6

Income tax (benefit)

3.0

0.2

(6.5)

3.4

3.0

30.2

11.7

(2.1)

(12.7)

4.7

5.5

Depreciation & Amortization

21.4

28.0

26.1

28.9

28.5

30.6

44.3

53.0

57.0

59.6

59.6

EBITDA

59.3

$

41.5

$

32.0

$

89.1

$

135.6

$

164.6

$

252.6

$

121.5

$

30.2

$

135.8

$

135.5

$

Adjustments:

Impairment

-

-

-

-

-

-

-

46.2

97.7

1.8

2.7

Debt refinancing costs

-

-

6.5

-

-

-

-

-

-

-

3.8

Accounting Change

-

-

7.3

-

-

-

-

-

-

-

-

Other

(2.5)

1.3

(1.5)

(0.5)

0.1

0.3

(1.6)

1.2

(0.1)

2.3

0.0

Adjusted EBITDA

$56.8

$42.8

$44.3

$88.6

$135.7

$164.9

$251.0

$168.8

$127.8

$139.9

$142.0

2002

2003

2004

2005

2006

2007

2008

2009

2010

2012 TTM

2011 |