Attached files

| file | filename |

|---|---|

| 8-K - 8-K - PREFERRED APARTMENT COMMUNITIES INC | a8-k_supplementxnoxx6.htm |

Filed Pursuant To Rule 424(b)(3)

File No. 333-176604

File No. 333-176604

PREFERRED APARTMENT COMMUNITIES, INC.

SUPPLEMENT NO. 6 DATED JANUARY 29, 2013

TO THE PROSPECTUS, DATED NOVEMBER 18, 2011

SUPPLEMENT NO. 6 DATED JANUARY 29, 2013

TO THE PROSPECTUS, DATED NOVEMBER 18, 2011

This prospectus supplement (this "Supplement No. 6") is part of the prospectus of Preferred Apartment Communities, Inc., dated November 18, 2011 (the "Prospectus"), as supplemented by Supplement No. 1, dated May 3, 2012 ("Supplement No. 1"), Supplement No. 2, dated May 11, 2012 ("Supplement No. 2"), Supplement No. 3, dated August 23, 2012 ("Supplement No. 3"), Supplement No. 4, dated September 13, 2012 ("Supplement No. 4") and Supplement No. 5, dated December 31, 2012 ("Supplement No. 5"). This Supplement No. 6 supplements, modifies or supersedes certain information contained in the Prospectus. This Supplement No. 6 should be read, and will be delivered, with the Prospectus, Supplement No. 1, Supplement No. 2, Supplement No. 3 and Supplement No. 4 and Supplement No. 5. Except where the context suggests otherwise, the terms "company," "Company," "we," "us," and "our" refer to Preferred Apartment Communities, Inc., together with its consolidated subsidiaries, and "our manager" refers to Preferred Apartment Advisors, LLC, our external manager and advisor, a Delaware limited liability company.

The purpose of this Supplement No. 6 is to disclose the following:

• | the indirect acquisition by our operating partnership of three multifamily communities, one in each of Atlanta, Georgia; Austin, Texas; and suburban Raleigh, North Carolina; |

• | the company’s entry into financing arrangements with regard to such multifamily communities; |

• | the company’s consummation of a private placement of shares of its Series B Mandatorily Convertible Cumulative Perpetual Preferred Stock, liquidation value $1,000 per share, in a private placement to certain investors in exchange for aggregate cash consideration of $40,000,000; and |

• | update certain information with respect to the agreement of limited partnership of the company’s operating partnership. |

PREFERRED APARTMENT COMMUNITIES, INC.

TABLE OF CONTENTS

TABLE OF CONTENTS

Supplement No. 6 Page No. | Prospectus Page No. | |

Certain Operating Information | S-1 | N/A |

Status of the Offering | S-1 | N/A |

Accredited Investor Private Placement Offering | S-1 | N/A |

Prospectus Updates | S-3 | N/A |

Prospectus Summary | S-3 | 2, 7, 18, 23, 150 |

Distribution Policy | S-6 | 18, 69 |

Capitalization | S-8 | 72 |

Business | S-9 | 95 |

Description of Real Estate Investments | S-9 | 113 |

Certain Relationships and Related Transactions | S-16 | 143 |

Description of Securities | S-17 | 155, 158 |

Shares of Common Stock Eligible for Future Resale | S-20 | 163 |

Summary of our Organizational Documents | S-20 | 164 |

Summary of our Operating Partnership Agreement | S-20 | 168, 170, 172-174 |

Material U.S. Federal Income Tax Considerations | S-22 | 180, 191-193, 196 |

Exhibits | S-25 | N/A |

Exhibit A - Ashford Park Trailing Twelve Month Profit and Loss Statement for the Period Ended September 30, 2012 | S-25 | N/A |

Exhibit B - Lake Cameron Trailing Twelve Month Profit and Loss Statement for the Period Ended September 30, 2012 | S-26 | N/A |

Exhibit C - McNeil Ranch Trailing Twelve Month Profit and Loss Statement for the Period Ended September 30, 2012 | S-27 | N/A |

i

CERTAIN OPERATING INFORMATION

Status of the Offering

On November 18, 2011, we commenced this offering on a ‘‘reasonable best efforts’’ basis of up to 150,000 units, or Units, with each Unit consisting of one share of Series A Redeemable Preferred Stock and one detachable warrant to purchase 20 shares of our common stock. On March 30, 2012, we satisfied the escrow conditions of this offering, received and accepted aggregate subscriptions in excess of $2.0 million and issued 2,155 shares of Series A Redeemable Preferred Stock and 2,155 Series A Warrants to the holders of our Series A Redeemable Preferred Stock. As of January 10, 2013, we had received from this offering total gross proceeds of approximately $20,860,000 from the sale of 20,860 Units. As of January10, 2013, there were 129,140 Units available for sale pursuant to this offering.

On December 31, 2012, we extended the termination date of this offering to December 31, 2013, provided that this offering will be terminated if all the 150,000 Units are sold before such date

Our common stock is traded on the NYSE MKT (previously known as NYSE AMEX), or NYSE MKT, under the symbol "APTS." On January 28, 2013, the last reported sale price of our common stock on the NYSE MKT was $8.20 per share.

Accredited Investor Private Placement Offering

On January 17, 2013, we entered into securities purchase agreements dated as of January 16, 2013, or the Securities Purchase Agreements, with certain accredited investors, or the Investors, pursuant to which, among other things, we sold 40,000 shares of Series B Mandatorily Convertible Cumulative Perpetual Preferred Stock, liquidation value $1,000 per share, or the Series B Mandatorily Convertible Preferred Stock, in a private placement, or the Private Placement, to the Investors in exchange for aggregate cash consideration of $40,000,000. Each share of Series B Mandatorily Convertible Preferred Stock was sold to the Investors at an offering price of $1,000 per share. We used the net offering proceeds of the Private Placement to acquire three multifamily residential properties and to refinance the existing debt on these acquired properties. The closing process and funding under many of the Securities Purchase Agreements began on January 16, 2013. However, the closings under the Securities Purchase Agreements were not consummated until January 17, 2013.

Registration Rights Agreements

In connection with the Private Placement, on January 17, 2013, we entered into a registration rights agreement dated as of January 16, 2013, or the Registration Rights Agreement, with each of the Investors. Pursuant to the terms of the Registration Rights Agreement, we agreed to file a resale registration statement by no later than April 15, 2013 for the purpose of registering the resale of the underlying shares of common stock into which the shares of Series B Mandatorily Convertible Preferred Stock are convertible (following stockholder approval of the conversion of the Series B Mandatorily Convertible Preferred Stock into shares of common stock). Pursuant to the Registration Rights Agreement, we agreed to use commercially reasonable efforts to have such registration statement declared effective with the SEC within 120 days of such filing.

Placement Agency Agreement

In connection with the Private Placement, on January 11, 2013, we entered into a placement agency agreement, or the Placement Agency Agreement, with Wunderlich Securities, Inc., a Tennessee corporation, Compass Point Research & Trading, LLC, a Delaware limited liability company, and National Securities Corporation, a Washington corporation, or the Agents. Under the Placement Agency Agreement, the Agents agreed to use their "best efforts" on an "all-or-none" basis to sell a minimum amount of 28,000 shares of Series B Mandatorily Convertible Preferred Stock, and to use their "best efforts" to sell a maximum amount of 40,000 shares of Series B Mandatorily Convertible Preferred Stock. As compensation for such services, we agreed to pay the Agents a fee of 6.0% of the aggregate gross proceeds from the sale of such equity securities and to reimburse the Agents for all reasonable, documented out-of-pocket accountable expenses incurred by them in connection with the Private Placement, up to an aggregate amount equal to $57,500.

The Placement Agency Agreement contains customary representations and warranties and covenants of the company and is subject to customary closing conditions. In addition, the company and the Agents have agreed to indemnify each other against certain

S-1

liabilities, including indemnification of the Agents by the company for liabilities under the Securities Act and for liabilities arising from breaches of the representations, warranties or obligations contained in the Placement Agency Agreement.

Promissory Note and Loss Sharing Agreement

In connection with the purchase by his affiliates of 2,639 shares of Series B Mandatorily Convertible Preferred Stock in the Private Placement, on January 17, 2013, J. Steven Emerson, or the Maker, executed a promissory note, dated January 16, 2013, or the Promissory Note, in the aggregate principal amount of $2,639,000 in favor of the company. The Promissory Note had an interest rate of 0.5% per annum, beginning January 23, 2013 and maturing on January 25, 2013. On January 18, 2013, the purchase price for the 2,639 shares of Series B Mandatorily Convertible Preferred Stock referred to above was paid in full and the Promissory Note was canceled.

In connection with the Promissory Note, on January 17, 2013, the company and the Agents entered into a loss sharing agreement dated as of January 16, 2013, or the Loss Sharing Agreement, pursuant to which the Agents agreed to acquire part of the Promissory Note from us if the Maker defaulted on the Promissory Note. The Agents agreed that the consideration for such acquisition would have been made by a reduction of the fees otherwise payable to the Agents under the Placement Agency Agreement. As a result of the cancellation of the Promissory Note on January 18, 2013, the obligation of the Agents to acquire part of the Promissory Note from the company no longer exists.

S-2

PROSPECTUS UPDATES

Prospectus Summary

The following disclosure is added immediately following the first paragraph on page S-3 of Supplement No. 3.

"On January 17, 2013, we entered into securities purchase agreements dated as of January 16, 2013, or the Securities Purchase Agreements, with certain accredited investors, or the Investors, pursuant to which, among other things, we sold 40,000 shares of Series B Mandatorily Convertible Cumulative Perpetual Preferred Stock, liquidation value $1,000 per share, or the Series B Mandatorily Convertible Preferred Stock, in a private placement, or the Private Placement, to the Investors in exchange for aggregate cash consideration of $40,000,000. Each share of Series B Mandatorily Convertible Preferred Stock was sold to the Investors at an offering price of $1,000 per share. We used the net offering proceeds of the Private Placement to acquire three multifamily residential properties and to refinance part of the existing debt on these acquired properties. The closing process and funding under many of the Securities Purchase Agreements began on January 16, 2013. However, the closings under the Securities Purchase Agreements were not consummated until January 17, 2013."

The following disclosure is added immediately following the second paragraph on page S-1 of Supplement No. 4.

"On January 18, 2013, Williams Multifamily Acquisition Fund, LP, a Delaware limited partnership, or WMAF, Williams Multifamily Acquisition Fund GP, LLC, a Delaware limited liability company, or WMAF GP, Williams Multifamily Acquisition Venture, LLC, a Georgia limited liability company, or Williams LP, WRA and OREC (Williams) Holdings, Inc., a corporation formed under the laws of the Province of Ontario, Canada, or Oxford, entered into a Liquidation Agreement dated as of January 18, 2013, or the Liquidation Agreement, in connection with, among other things, the acquisition of up to three real estate investment properties: Ashford Park, Lake Cameron and McNeil Ranch, or, collectively, the Real Estate Investment Properties. We are not a party to the Liquidation Agreement.

The Liquidation Agreement provides that Williams LP has the right to exercise an option to purchase all the outstanding common stock of the separate real estate investment trusts, or the REIP Entities, that indirectly own the Real Estate Investment Properties (and thereby acquire the Real Estate Investment Properties) at the agreed-upon purchase prices included therein. On January 18, 2013, pursuant to the terms of two option exercise notices, or the Option Exercise Notices, Williams LP exercised its options to purchase all the common stock of the REIP Entities and thereby acquire indirectly the ownership of the Real Estate Investment Properties, and designated our operating partnership as the purchaser of all the common stock of the REIP Entities, with a final closing date for such purchases of January 23, 2013. Further, on January 23, 2013, pursuant to the terms of stock transfer agreements, or the Stock Transfer Agreements, among our operating partnership, WMAF and WMAF GP, all the shares of common stock of the REIP Entities that indirectly own the Real Estate Investment Properties were transferred from WMAF to our operating partnership.

On January 23, 2013, our operating partnership completed the purchase of all the common stock of Ashford Park REIT Inc., the indirect fee-simple owner of a 408 unit multifamily apartment community located in Atlanta, Georgia, or Ashford Park, for a total acquisition cost of approximately $39.4 million, subject to adjustments for customary pro rations in the acquisition of real estate. The $39.4 million acquisition cost included existing first mortgage debt of approximately $38.8 million, which has been paid in full, but excludes acquisition-related and financing-related transaction costs. In connection with the purchase of this asset, our manager received an acquisition fee equal to approximately $0.4 million. In connection with the acquisition of Ashford Park, on January 24, 2013, we refinanced the existing first mortgage debt with a portion of the net proceeds from the Private Placement and with a new loan of approximately $25.6 million originated by Prudential Affordable Mortgage Company, LLC, a Delaware limited liability company, or Prudential.

On January 23, 2013, our operating partnership completed the purchase of all the common stock of Lake Cameron REIT Inc., the indirect fee-simple owner of a 328 unit multifamily apartment community located in suburban Raleigh, North Carolina, or Lake Cameron, for a total acquisition cost of approximately $30.4 million, subject to adjustments for customary pro rations in the acquisition of real estate. The $30.4 million acquisition cost included existing first mortgage debt of approximately $17.5 million, which has been paid in full, but excludes acquisition-related and financing-related transaction costs. In connection with the purchase of this asset, our manager received an acquisition fee equal to approximately $0.3 million. In connection with the acquisition of Lake Cameron, on January 24, 2013, we refinanced the existing first mortgage debt on Lake Cameron with a portion of the net proceeds

S-3

from the Private Placement and with a new loan of approximately $19.8 million originated by Jones Lang LaSalle Operations, L.L.C., an Illinois limited liability company, or Jones Lang.

On January 23, 2013, our operating partnership completed the purchase of all the common stock of McNeil Ranch REIT Inc., the indirect fee-simple owner of a 192 unit multifamily apartment community located in Austin, Texas, or McNeil Ranch, for a total acquisition cost of was approximately $21.0 million, subject to adjustments for customary pro rations in the acquisition of real estate. The $21.0 million acquisition cost includes existing first mortgage debt of approximately $13.4 million, which has been paid in full, but excludes acquisition-related and financing-related transaction costs. In connection with the purchase of this asset, our manager received an acquisition fee equal to approximately $0.2 million. In connection with the acquisition McNeil Ranch, on January 24, 2013, we refinanced the existing first mortgage debt with a portion of the net proceeds from the Private Placement and with a new loan of approximately $13.6 million originated by Jones Lang."

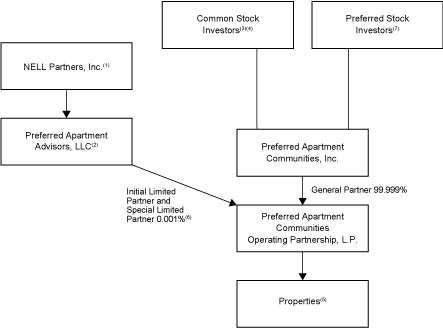

The following disclosure replaces in its entirety the section entitled "Prospectus Summary — Our Structure" on page 7 of the Prospectus and the chart on page 150 of the Prospectus.

"We were formed as a Maryland corporation on September 18, 2009. The following chart shows our structure after giving effect to this offering:

(1) | NELL Partners, Inc. is controlled by John A. Williams, our sponsor, and Leonard A. Silverstein, our President and Chief Operating Officer. | |

(2) | Our manager, Preferred Apartment Advisors, LLC, is controlled by NELL Partners, Inc. Other than the 1% Manager Revenue Interest (as defined in the section entitled "Our Manager and Management Agreement — 1% Manager Revenue Interest" included elsewhere in this prospectus) held by WOF, all interests of our manager are held by NELL Partners, Inc. | |

(3) | The common stock investors in our initial public offering own registered shares of common stock of Preferred Apartment Communities, Inc. The 500,000 shares of common stock acquired by WOF in the private placement offering are not registered shares. As of December 31, 2012, WOF owned 142,262 shares of our common stock. | |

S-4

(4) | NELL Partners owns 36,666 shares of common stock. John A. Williams and Leonard A. Silverstein share joint voting and investment power of these shares. Additionally, as of September 30, 2012, our officers and directors collectively own 139,777 shares of common stock. See "Principal Stockholders." | |

(5) | Each property is expected to be held in a single-purpose entity. | |

(6) | As the special limited partner of the operating partnership, our manager is entitled to receive a participation in net sales proceeds of our investments. See the section entitled "Our Manager and Management Agreement — Management Compensation — Special Limited Partnership Interest" included elsewhere in this prospectus for information relating to the calculation of distributions with respect to the special limited partnership interest and conditions under which it may be paid. | |

(7) | The shares of common stock issuable upon the redemption of the Series A Redeemable Preferred Stock will be registered shares. The shares of common stock issuable upon redemption of the Series B Mandatorily Convertible Preferred Stock are expected to be registered shares." | |

The following disclosure is added immediately following the first paragraph under the section entitled "Prospectus Summary — Distribution Policy" on page S-9 of Supplement No. 3.

"Holders of Series B Mandatorily Convertible Preferred Stock are entitled to receive, when, and as authorized by our board of directors and declared by us out of legally available funds, a dividend, on an as converted basis, that mirrors any dividend payable on shares of our common stock and also will be entitled to share in any other distribution made on our common stock on an as converted basis (other than dividends or other distributions payable in our common stock), for the period beginning with any dividends and other distributions in respect of the first quarter of 2013. Any dividends or other distributions on the Series B Mandatorily Convertible Preferred Stock for the first quarter of 2013 will be paid, on an as converted basis, pro rata from the date of issuance.

For the period beginning on May 16, 2013, but only to the extent that the Series B Mandatorily Convertible Preferred Stock remains outstanding during this period and subject to the preferential rights of holders of any shares of senior capital stock of the company, each share of the Series B Mandatorily Convertible Preferred Stock will bear a dividend, when and as authorized by our board of directors, equal to the excess, if any, of (i) 15.0% per annum, minus (ii) any dividend or other distribution payable by us on the Series B Mandatorily Convertible Preferred Stock pursuant to the previous paragraph in respect of the applicable quarterly period. Such dividends shall be cumulative from May 16, 2013 and shall be payable quarterly in arrears on or before July 15th, October 15th, January 15th and April 15th of each year or, if not a business day, the next succeeding business day. If the Series B Mandatorily Convertible Preferred Stock is converted to our common stock prior to May 16, 2013, then no additional dividends will be payable on the Series B Mandatorily Convertible Preferred Stock."

The following information replaces in its entirety the section entitled, "Prospectus Summary — Capital Structure" on page 23 of the Prospectus.

"Following this offering, the Series A Redeemable Preferred Stock will rank senior to our common stock and to the Class A Units and Class B Units issued by our operating partnership and on parity with the Series A Redeemable Preferred Limited Partnership Units issued by our operating partnership with respect to both payment of dividends and distribution of amounts upon liquidation. The Series B Mandatorily Convertible Preferred Stock ranks senior to our common stock and to the Class A Units and Class B Units issued by our operating partnership and on a parity with the Series A Redeemable Preferred Stock, the Series A Redeemable Preferred Limited Partnership Units issued by our operating partnership and the Series B Mandatorily Convertible Preferred Units issued by our operating partnership with respect to payment of dividends and distribution of amounts upon liquidation, dissolution or winding up. Our board of directors has the authority to issue shares of additional series of preferred stock that could be senior in priority to the Series A Redeemable Preferred Stock and to the Series B Mandatorily Convertible Preferred Stock; provided, however, that the affirmative vote or consent of the holders of at least two-thirds of the outstanding shares of Series B Mandatorily Convertible Preferred Stock, voting as a single class, shall be required to authorize, create, increase the number of or issue any shares of capital stock of the company that are senior to the Series B Mandatorily Convertible Preferred Stock or any security convertible into our capital stock that is senior to the Series B Mandatorily Convertible Preferred Stock or reclassify any other existing shares of our capital stock of into shares of our capital stock that are senior to the Series B Mandatorily Convertible Preferred Stock."

S-5

Distribution Policy

The following disclosure is added immediately following the first paragraph under the heading "Distribution Policy" on page S-20 of Supplement No. 3.

"Holders of Series B Mandatorily Convertible Preferred Stock are entitled to receive, when, and as authorized by our board of directors and declared by us out of legally available funds, a dividend, on an as converted basis, that mirrors any dividend payable on shares of our common stock and also will be entitled to share in any other distribution made on our common stock on an as converted basis (other than dividends or other distributions payable in our common stock), for the period beginning with any dividends and other distributions in respect of the first quarter of 2013. Any dividends or other distributions on the Series B Mandatorily Convertible Preferred Stock for the first quarter of 2013 will be paid, on an as converted basis, pro rata from the date of issuance.

For the period beginning on May 16, 2013, but only to the extent that the Series B Mandatorily Convertible Preferred Stock remains outstanding during this period and subject to the preferential rights of holders of any shares of senior capital stock of the company, each share of the Series B Mandatorily Convertible Preferred Stock will bear a dividend, when and as authorized by our board of directors, equal to the excess, if any, of (i) 15.0% per annum, minus (ii) any dividend or other distribution payable by us on the Series B Mandatorily Convertible Preferred Stock pursuant to the previous paragraph in respect of the applicable quarterly period. Such dividends shall be cumulative from May 16, 2013 and shall be payable quarterly in arrears on or before July 15th, October 15th, January 15th and April 15th of each year or, if not a business day, the next succeeding business day. If the Series B Mandatorily Convertible Preferred Stock is converted to our common stock prior to May 16, 2013, then no additional dividends will be payable on the Series B Mandatorily Convertible Preferred Stock."

The following disclosure replaces in its entirety the language added on page S-9 of Supplement No. 3 under the heading "Prospectus Summary – Distribution Policy" and the first paragraph on the top of page S-21 of Supplement No.3 and the table that follows, all under the heading "Distribution Policy".

The following tables set forth the dividends that have been authorized by the company's Board of Directors and, if applicable, paid by us from inception through January 29, 2013.

Common Stock

Quarter Ended | Amount Paid Per Share | Total Amount Paid | Date Paid | |||||||||

06/30/2011 | $ | 0.125 | $ | 646,487 | 07/15/2011 | |||||||

09/30/2011 | $ | 0.125 | $ | 646,675 | 10/17/2011 | |||||||

12/31/2011 | $ | 0.125 | $ | 646,916 | 01/17/2012 | |||||||

03/31/2012 | $ | 0.13 | $ | 673,181 | 04/16/2012 | |||||||

06/30/2012 | $ | 0.13 | $ | 677,477 | 07/16/2012 | |||||||

09/30/2012 | $ | 0.14 | $ | 729,699 | 10/15/2012 | |||||||

12/31/2012 | $ | 0.145 | $ | 761,616 | 1/15/2013 | |||||||

S-6

Series A Redeemable Preferred Stock

Month Ended | Amount Paid Per Share | Total Amount Paid | Date Paid | |||||||||

04/30/2012 | $ | 5.33 | (1) | $ | 11,486 | 05/21/2012 | ||||||

05/31/2012 | $ | 5.00/5.17 | (2) | $ | 25,406 | 06/20/2012 | ||||||

06/30/2012 | $ | 5.00/5.17 | (3) | $ | 42,793 | 07/20/2012 | ||||||

07/31/2012 | $ | 5.00/5.50 | (4) | $ | 50,879 | 08/20/2012 | ||||||

08/31/2012 | $ | 5.00/7.50/5.17 | (5) | $ | 54,119 | 09/20/2012 | ||||||

09/30/2012 | $ | 5.00/7.67/5.33 | (7) | $ | 58,061 | 10/20/2012 | ||||||

10/31/2012 | $ | 5.00/7.83/5.50 | (8) | $ | 61,553 | 11/20/2012 | ||||||

11/30/2012 | $ | 5.00/7.50/5.17 | (9) | $ | 66,641 | 12/20/2012 | ||||||

12/31/2012 | $ | 5.00/7.67/5.17 | (10) | $ | 79,868 | 1/22/2013 | ||||||

1/31/2013 | $ | 5.00/8.00/5.67 | (11)(6) | $ | (6) | 2/20/2013 | (6) | |||||

(1) | Comprised of $5.00 per share for the month of April 2012 and $0.33 per share prorated from the initial issuance of shares of Series A Redeemable Preferred Stock on March 30, 2012 purchased in this offering through the end of March 2012. | |

(2) | Comprised of (i) a dividend of $5.00 per share of Series A Redeemable Preferred Stock to all stockholders of record on May 31, 2012 that purchased Primary Series A Units in connection with our closing of this offering on March 31, 2012 and (ii) a dividend of $5.17 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of May 2012 and $0.17 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on April 30, 2012 through the end of April 2012. | |

(3) | Comprised of (i) a dividend of $5.00 per share of Series A Redeemable Preferred Stock to all stockholders of record on June 29, 2012 that purchased Primary Series A Units in connection with our closings of this offering prior to May 30, 2012 and (ii) a dividend of $5.17 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of June 2012 and $0.17 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on May 31, 2012 through the end of May 2012. | |

(4) | Comprised of (i) a dividend of $5.00 per share of Series A Redeemable Preferred Stock to all stockholders of record on July 31, 2012 that purchased Primary Series A Units in connection with our closings of this offering prior to June 28, 2012 and (ii) a dividend of $5.50 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of July 2012 and $0.50 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on June 28, 2012 through the end of June 2012. | |

(5) | Comprised of (i) a dividend of $5.00 per share of Series A Redeemable to all stockholders of record on August 31, 2012 that purchased Primary Series A Units in connection with our closings of this offering prior to July 17, 2012, (ii) a dividend of $7.50 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of August 2012 and $2.50 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on July 17, 2012 through the end of July 2012 and (iii) a dividend of $5.17 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of August 2012 and $0.17 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on July 31, 2012 through the end of July 2012. | |

(6) | This dividend was authorized by the Board of Directors and declared by the company, but has yet to be paid to the holders of the Series A Redeemable Preferred Stock. | |

S-7

(7) | Comprised of (i) a dividend of $5.00 per share of Series A Redeemable to all stockholders of record on September 30, 2012 that purchased Primary Series A Units in connection with our closings of this offering prior to August 16, 2012, (ii) a dividend of $7.67 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of September 2012 and $2.67 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on August 16, 2012 through the end of August 2012 and (iii) a dividend of $5.33 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of September 2012 and $0.33 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on August 30, 2012 through the end of August 2012. | |

(8) | Comprised of (i) a dividend of $5.00 per share of Series A Redeemable to all stockholders of record on October 31, 2012 that purchased Primary Series A Units in connection with our closings of this offering prior to September 30, 2012, (ii) a dividend of $7.83 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of October 2012 and $2.83 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on September 14, 2012 through the end of September 2012 and (iii) a dividend of $5.50 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of October 2012 and $0.50 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on September 28, 2012 through the end of September 2012. | |

(9) | Comprised of (i) a dividend of $5.00 per share of Series A Redeemable to all stockholders of record on November 30, 2012 that purchased Primary Series A Units in connection with our closings of this offering prior to October 17, 2012, (ii) a dividend of $7.50 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of November 2012 and $2.50 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on October 17, 2012 through the end of October 2012 and (iii) a dividend of $5.17 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of October 2012 and $0.17 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on October 31, 2012 through the end of October 2012. | |

(10) | Comprised of (i) a dividend of $5.00 per share of Series A Redeemable to all stockholders of record on December 31, 2012 that purchased Primary Series A Units in connection with our closings of this offering prior to November 15, 2012, (ii) a dividend of $7.67 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of December 2012 and $2.67 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on November 15, 2012 through the end of November 2012 and (iii) a dividend of $5.17 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of November 2012 and $0.17 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on November 30, 2012 through the end of November 2012. | |

(11) | Comprised of (i) a dividend of $5.00 per share of Series A Redeemable to all stockholders of record on January 31, 2012 that purchased Primary Series A Units in connection with our closings of this offering prior to December 14, 2012, (ii) a dividend of $8.00 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of January 2013 and $3.00 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on December 14, 2012 through the end of December 2012 and (iii) a dividend of $5.67 per share of Series A Redeemable Preferred Stock, comprised of $5.00 per share for the month of December 2012 and $0.67 per share prorated from the initial issuance of such shares of Series A Redeemable Preferred Stock on December 28, 2012 through the end of November 2012. | |

Capitalization

The following information replaces in its entirety the section entitled "Capitalization" on page S-23 of Supplement No. 3.

The following table sets forth (a) our actual capitalization at September 30, 2012, (b) the adjustments to reflect the effect of the issuance of a total of 150,000 shares of Series A Redeemable Preferred Stock in this offering, assuming the sale of the maximum offering after deducting estimated offering expenses, including selling commissions and the dealer manager fee, payable by us, (c) our capitalization as adjusted to reflect the effect of the issuance of 40,000 shares of Series B Preferred Stock on January 16, 2013, after deducting estimated offering expenses, including selling commissions, payable by us and (d) our capitalization as adjusted to reflect the effect of both (b) and (c) above. You should read this table together with the sections entitled "Estimated Use of Proceeds" and "Selected Financial Information" included elsewhere in this prospectus, as well as our consolidated financial statements and notes thereto and the section entitled "Management’s Discussion and Analysis of Financial Condition and Results of Operations" included in our most recent Annual Report on Form 10-K and our subsequent Quarterly Reports on Form 10-Q, which are incorporated by reference into this prospectus.

S-8

September 30 , 2012 | ||||||||||||||||

Actual | Series A Maximum Offering | Series B Offering | As Adjusted Series A and Series B | |||||||||||||

(unaudited) | ||||||||||||||||

Stockholders' equity: | ||||||||||||||||

Series A Redeemable Preferred Stock, par value $0.01 per share; 150,000 shares authorized 12,178 or 150,000 issued and outstanding | $ | 122 | $ | 1,378 | $ | — | $ | 1,500 | ||||||||

Series B Redeemable Preferred Stock, par value $0.01 per share; 40,000 shares authorized and 0 or 40,000 issued and outstanding | $ | — | $ | — | $ | 400 | $ | 400 | ||||||||

Common Stock, par value $0.01 per share; 400,066,666 shares authorized and 5,178,313 issued and outstanding | $ | 51,783 | $ | — | $ | — | $ | 51,783 | ||||||||

Additional paid-in capital(1) | $ | 51,953,388 | $ | 121,971,092 | $ | 36,999,600 | $ | 210,924,080 | ||||||||

Accumulated deficit | $ | (9,972,849 | ) | $ | — | $ | — | $ | (9,972,849 | ) | ||||||

Non-controlling interest | $ | 1 | $ | — | $ | — | $ | 1 | ||||||||

Total equity | $ | 42,032,445 | $ | 121,972,470 | $ | 37,000,000 | $ | 201,004,915 | ||||||||

(1) | Included in additional paid in capital for the actual, Series A maximum offering, and as adjusted Series A and Series B offering columns is the fair value of the Warrants that are included in the Units sold in this offering, which warrants were immediately separable from our Series A Redeemable Preferred Stock and which Warrants have, as of September 30, 2012, an aggregate estimated fair value of $398,831. Each Warrant is potentially exercisable into 20 shares of our common stock, beginning one year after the date of issuance and expires four years after the date of issuance. The weighted average fair value of each warrant is $32.75 (or approximately $1.64 on a per underlying share of common stock basis) and was calculated utilizing the Black-Scholes-Merton model with valuation assumptions as of September 30, 2012. The weighted average strike price of the warrants outstanding at September 30, 2012 was approximately $9.39. |

Business

The following disclosure is added immediately following the third paragraph under the heading "Business — Our Properties" on page S-27 of Supplement No. 3.

"On January 23, 2013, our operating partnership completed the purchase of all the common stock of Ashford Park REIT Inc., the indirect fee-simple owner of Ashford Park, for a total acquisition cost of approximately $39.4 million, subject to adjustments for customary pro rations in the acquisition of real estate. The $39.4 million acquisition cost includes existing first mortgage debt of approximately $38.8 million, which has been paid in full, but excludes acquisition-related and financing-related transaction costs. In connection with the purchase of this asset, our manager received an acquisition fee equal to approximately $0.4 million. In connection with the acquisition of Ashford Park, on January 24, 2013, we refinanced the existing first mortgage debt with a portion of the net proceeds from the Private Placement and with a new loan of approximately $25.6 million originated by Prudential.

On January 23, 2013, our operating partnership completed the purchase of all the common stock of Lake Cameron REIT Inc., the indirect fee-simple owner of Lake Cameron, for a total acquisition cost of approximately $30.4 million, subject to adjustments for customary pro rations in the acquisition of real estate. The $30.4 million acquisition cost includes existing first mortgage debt of approximately $17.5 million, which has been paid in full, but excludes acquisition-related and financing-related transaction costs. In connection with the purchase of this asset, our manager received an acquisition fee equal to approximately $0.3 million. In connection with the acquisition of Lake Cameron, on January 24, 2013, we refinanced the existing first mortgage debt on Lake Cameron with a portion of the net proceeds from the Private Placement and with a new loan of approximately $19.8 million originated by Jones Lang.

S-9

On January 23, 2013, our operating partnership completed the purchase of all the common stock of McNeil Ranch REIT Inc., the indirect fee-simple owner of McNeil Ranch, for a total acquisition cost of was approximately $21.0 million, subject to adjustments for customary pro rations in the acquisition of real estate. The $21.0 million acquisition cost includes existing first mortgage debt of approximately $13.4 million, which has been paid in full, but excludes acquisition-related and financing-related transaction costs. In connection with the purchase of this asset, our manager received an acquisition fee equal to approximately $0.2 million. In connection with the acquisition McNeil Ranch, on January 24, 2013, we refinanced the existing first mortgage debt with a portion of the net proceeds from the Private Placement and with a new loan of approximately $13.6 million originated by Jones Lang."

Description of Real Estate Investments

The following disclosure replaces in its entirety the section entitled "Description of Real Estate Investments--Properties Owned" on page S-44 of Supplement No. 3.

"The following table provides information as of January 29, 2013 (unless indicated otherwise) regarding our six multifamily communities.

| | | | | | | | |||||||||

Current Name of Multifamily Community | Location of Multifamily Community | Number of Units | Average Per Unit Monthly Rents(1) | Purchase Price | Mortgage Debt Amount | Interest Rate | Property Management Agent(2) | Annual Property Management Fee | ||||||||

Ashford Park | Atlanta, Georgia | 408 | $1,035 | $41,246,000 | (3) | $25,626,000 | (4) | 3.13% | PRM | 4.0% | ||||||

Lake Cameron | Suburban Raleigh, North Carolina | 328 | $819 | $31,500,000 | (3) | $19,773,000 | (4) | 3.13% | PRM | 4.0% | ||||||

McNeil Ranch | Austin, Texas | 192 | $1,097 | $21,915,000 | (3) | $13,646,000 | (4) | 3.13% | PRM | 4.0% | ||||||

Summit Crossing | Suburban Atlanta, Georgia | 345 | $931 | $33,304,434 | (5) | $20,862,000 | (6) | 4.71% | PRM | 4.0% | ||||||

Stone Rise | Suburban Philadelphia, Pennsylvania | 216 | $1,318 | $30,584,741 | (5) | $19,500,000 | (6) | 2.77% | (7) | PRM | 4.0% | |||||

Trail Creek | Hampton Roads, Virginia | 204 | $1,079 | $23,583,054 | (5) | $15,275,000 | (6) | 2.80% | (7) | PRM | 4.0% | |||||

S-10

(1) | Estimated as of September 30, 2012. Exclusive of additional amounts recoverable from tenants for utilities and rent concessions that may be offered to tenants. |

(2) | Each of our multifamily communities is operated under a management agreement between our manager and PRM, or the property manager, an affiliate of our manager. |

(3) | The purchase price is based on an estimate of the aggregate value of the tangible and identifiable intangible assets and liabilities acquired and inclusive of estimated closing costs and fees. |

(4) | Mortgage debt amount and interest rate at January 29, 2013. |

(5) | The purchase price of these acquired properties is based on the aggregate value of the tangible and identifiable intangible assets and liabilities acquired. |

(6) | Mortgage debt amount and interest rate at September 30, 2012. Interest rate varies monthly and is calculated by adding 2.77% to the British Banker’s Association’s one month LIBOR Rate for United States Dollar deposits, or LIBOR, for Stone Rise and 2.80% to LIBOR for Trail Creek. LIBOR was 0.245% on September 30, 2012. |

(7) | Variable monthly interest rates are capped at 7.25% and 6.85% for Stone Rise and Trail Creek, respectively. |

See the section entitled "Certain Relationships and Related Transactions — Agreements With Institutional and Other Investors — Real Estate Property Investments" contained elsewhere in this prospectus."

The following disclosure is added immediately preceding the section entitled "Description of Real Estate Investments — Depreciation" beginning on page S-48 of Supplement No. 3.

Liquidation Agreement

"On January 18, 2013, WMAF, WMAF GP, Williams LP, WRA and Oxford entered into the Liquidation Agreement, in connection with, among other things, the acquisition of up to three real estate investment properties: Ashford Park, Lake Cameron and McNeil Ranch, or, collectively, the Real Estate Investment Properties. We are not a party to the Liquidation Agreement. Oxford holds an indirect 95% interest, and affiliates of the company hold an indirect 5% interest, in the Real Estate Investment Properties through their ownership of WMAF.

The Liquidation Agreement provided that Williams LP had the right to exercise an option to purchase all the outstanding common stock of the separate real estate investment trusts, or the REIP Entities, that indirectly own the Real Estate Investment Properties (and thereby acquire the Real Estate Investment Properties) at the agreed-upon purchase prices included therein. The Liquidation Agreement generally is binding on the parties thereto, but the transactions contemplated thereby regarding the acquisition of the Real Estate Investment Properties were subject to certain conditions, including Williams LP giving affirmative notice of its desire to acquire all the common stock of the REIP Entities and designating our operating partnership as the purchaser of all the common stock of the REIP Entities. The Liquidation Agreement provides that the Real Estate Investment Properties will need to be acquired by January 25, 2013 for the Ashford Park and McNeil Ranch properties and March 31, 2013 for the Lake Cameron property.

On January 18, 2013, pursuant to the terms of the Option Exercise Notices, Williams LP exercised its options to purchase all the common stock of the REIP Entities and thereby acquire indirectly the ownership of the Real Estate Investment Properties, and designated our operating partnership as the purchaser of all the common stock of the REIP Entities, with a final closing date for such purchases of January 23, 2013. Further, on January 23, 2013, pursuant to the terms of stock transfer agreements, or the Stock Transfer Agreements, among our operating partnership, WMAF and WMAF GP, all the shares of common stock of the REIP Entities that indirectly own the Real Estate Investment Properties were transferred from WMAF to our operating partnership. John A. Williams, our Chief Executive Officer and Chairman, indirectly owns an approximate 1.56% interest in WMAF, Leonard A. Silverstein, our President and Chief Operating Officer and a board member, indirectly owns an approximate 0.16% interest in WMAF and William F. Leseman, our Executive Vice President – Property Management, indirectly owns an approximate 0.05% interest in WMAF. In connection with the acquisition of all of the Real Estate Investment Properties, from these indirect interests in WMAF, Mr. Williams, Mr. Silverstein and Mr. Leseman received approximately $331,175, $33,268 and $10,429, respectively. See "Risk Factors—We have affiliations with the property manager and the seller of the Real Estate Investment Properties and the terms of the acquisitions may not be as favorable to us as if they had been negotiated with an unaffiliated third party," Risk Factors- We may purchase real properties from persons with whom affiliates of our manager have prior business relationships, which may impact the purchase terms, and as a

S-11

result, affect your investment," "Risk Factors- Our manager and its affiliates receive fees and other compensation based upon our investments, which may impact operating decisions, and as a result, affect your investment," and "Risk Factors-- General Risks Related to Investments in Real Estate"

Ashford Park

On January 18, 2013, our operating partnership, under the terms the Liquidation Agreement, was designated as the Williams Purchaser (as defined in the Liquidation Agreement) and exercised its option to purchase all of the common stock of Ashford Park REIT Inc., the indirect fee-simple owner of Ashford Park. On January 23, 2013, our operating partnership closed on such purchase.

The total acquisition cost of Ashford Park was approximately $39.4 million, subject to adjustments for customary pro rations in the acquisition of real estate. The $39.4 million acquisition cost includes existing first mortgage debt of approximately $38.8 million, which has been paid in full, but excludes acquisition-related and financing-related transaction costs. In connection with the purchase of this asset, our manager received an acquisition fee equal to approximately $0.4 million. Other closing and financing related costs are expected to be approximately $1.5 million, including approximately $0.6 million for minor deferred maintenance and minor capital expenditures. In connection with the acquisition of Ashford Park, on January 24, 2013, we refinanced the existing first mortgage debt with a portion of the net proceeds from the Private Placement and with a new loan of approximately $25.6 million originated by Prudential.

Ashford Park is a multifamily community consisting of 408 units located in Atlanta, Georgia. The community consists of three buildings on a 10.6-acre landscaped setting. Ashford Park is comprised of a unit mix of 190 one-bedroom units, 182 two-bedroom units and 36 three-bedroom units. The property was constructed in 1992 and its apartment homes have an average size of 1,008 square feet. We believe the Ashford Park property is suitable and adequate for use as a multifamily apartment complex. We have no present intention to make major renovations, improvements or developments at the Ashford Park property.

There are currently ten other apartment communities in the area that we believe are competitive with Ashford Park. Including Ashford Park, these 11 communities include 4,410 units, have an average unit size of 1,036 square feet and an average year of construction of 2000. In addition to existing competitive properties, the submarket in which Ashford Park is located had no units delivered in the twelve months ended September 30, 2012 and no additional units are scheduled to be delivered through September 30, 2013. In addition to the specific competitive conditions described above, general competitive conditions affecting Ashford Park include those identified in the section entitled "Competition" included elsewhere in this prospectus.

On January 24, 2013, our subsidiary that owns Ashford Park obtained a non-recourse first mortgage loan, or the Ashford Loan, from Prudential in the original principal amount of approximately $25.6 million. Following execution of a Multifamily Loan and Security Agreement, or the Ashford Loan Agreement, and related documents, Prudential will sell, transfer, deliver and assign the Ashford Loan to the Federal Home Loan Mortgage Corporation, or the Lender. The Ashford Loan is secured by Ashford Park by a Multifamily Deed to Secure Debt, Assignment of Rents and Security Agreement, or the Ashford Mortgage. Our subsidiary that owns Ashford Park received net proceeds of approximately $25.3 million after payment of costs and fees associated with obtaining the Ashford Loan. The Ashford Loan bears interest at a fixed rate of interest equal to 3.13% per annum. The Ashford Loan requires monthly payments of accrued interest only from the period of March 1, 2013 to February 1, 2018. Beginning on March 1, 2018, the Ashford Loan will require monthly payments of accrued interest and principal based on a 30-year amortization period. All remaining indebtedness, including all interest and principal, is due by February 1, 2020. Subject to limited exceptions, our subsidiary that owns Ashford Park must pay additional charges for prepayment of any principal prior to the three-month period beginning on November 1, 2019. There are no guaranties of the Ashford Loan provided by us or our operating partnership.

In accordance with the terms of the Ashford Loan Agreement and the note related to the borrowing, the payment of the note may be accelerated at the option of the Lender if an event of default occurs. As defined in the Ashford Loan Agreement, events of default include, but are not limited to: failure to pay any amount due under the Ashford Loan Agreement or any related documents when due; failure to maintain insurance coverage required under the Ashford Loan Agreement; owning any real or personal property other than the mortgaged property and personal property related to the operation and maintenance of the mortgaged property; and any materially false or misleading representations or warranties made in connection with the Ashford Loan Agreement.

We expect that the initial basis in the property for federal income tax purposes will be equal to the purchase price. We plan to depreciate the property for federal income tax purposes on a straight-line basis using an estimated useful life of 27.5 years.

S-12

All the leased space is residential with leases ranging from an initial term of six months to one year. The average historical occupancy rate (determined by the total number of units actually occupied at the specific point in time indicated) for the last five years is as follows:

At December 31, 2011 | 93.1% |

At December 31, 2010 | 93.6% |

At December 31, 2009 | 90.7% |

At December 31, 2008 | 89.2% |

At December 31, 2007 | 89.2% |

No single tenant occupies 10% or more of Ashford Park.

The average historical effective net annual rental rate per unit (including any tenant concessions and abatements) at the property is as follows:

Year ending December 31, 2011 | $11,890 |

Year ending December 31, 2010 | $11,438 |

Year ending December 31, 2009 | $11,574 |

Year ending December 31, 2008 | $12,555 |

Year ending December 31, 2007 | $12,242 |

Property taxes paid on Ashford Park for the fiscal year ended December 31, 2011 were $665,518. Ashford Park was subject to a tax rate of 4.55% of its assessed value of $14,640,000.

Under a contract with our manager, the property manager will act as property manager of Ashford Park. We believe Ashford Park is adequately insured.

An unaudited trailing twelve month profit and loss financial report for Ashford Park for the period ended September 30, 2012 is included as Exhibit A hereto.

Lake Cameron

On January 18, 2013, our operating partnership, under the terms of the Liquidation Agreement, was designated as the Williams Purchaser (as defined in the Liquidation Agreement) and exercised its option to purchase all of the common stock of Lake Cameron REIT Inc., the indirect fee-simple owner of Lake Cameron. On January 23, 2013, our operating partnership closed on such purchase.

The total acquisition cost of Lake Cameron was approximately $30.4 million, subject to adjustments for customary pro rations in the acquisition of real estate. The $30.4 million acquisition cost includes existing first mortgage debt of approximately $17.5 million, which has now been paid in full, but excludes acquisition-related and financing-related transaction costs. In connection with the purchase of this asset, our manager received an acquisition fee equal to approximately $0.3 million. Other closing and financing related costs are expected to be approximately $0.9 million, including approximately $0.2 million for minor deferred maintenance and

S-13

minor capital expenditures. In connection with the acquisition of Lake Cameron, on January 24, 2013, we refinanced existing first mortgage debt on Lake Cameron with a new loan of approximately $19.8 million originated by Jones Lang.

Lake Cameron is a multifamily community consisting of 328 units located in suburban Raleigh, North Carolina. The community consists of one clubhouse, 14 residential and eight garage buildings on a 23.94-acre landscaped setting. Lake Cameron is comprised of a unit mix of 128 one-bedroom units, 164 two-bedroom units and 36 three-bedroom units. The property was constructed in 1997 and its apartment homes have an average size of 940 square feet. We believe the Lake Cameron property is suitable and adequate for use as a multifamily apartment complex. We have no present intention to make major renovations, improvements or developments at the Lake Cameron property.

There are currently seven other apartment communities in the area that we believe are competitive with Lake Cameron. Including Lake Cameron, these eight communities include 2,640 units, have an average unit size of 1,051 square feet and an average year of construction of 1998. In addition to existing competitive properties, the submarket in which Lake Cameron is located had 404 units delivered in the twelve months ended September 30, 2012 and 149 additional units are scheduled to be delivered through September 30, 2013. In addition to the specific competitive conditions described above, general competitive conditions affecting Lake Cameron include those identified in the section entitled "Competition" included elsewhere in this prospectus.

On January 24, 2013, our subsidiary that owns Lake Cameron obtained a non-recourse first mortgage loan, or the Lake Cameron Loan, from Jones Lang in the original principal amount of approximately $19.8 million. Following execution of a Multifamily Loan and Security Agreement, or the Lake Cameron Loan Agreement, and related documents, Jones Lang will sell, transfer, deliver and assign the Lake Cameron Loan to the Lender. The Lake Cameron Loan is secured by Lake Cameron by a Multifamily Deed of Trust, Assignment of Rents, Security Agreement and Fixture Filing, or the Lake Cameron Mortgage. Our subsidiary that owns Lake Cameron received net proceeds of approximately $19.5 million after payment of costs and fees associated with obtaining the Lake Cameron Loan. The Lake Cameron Loan bears interest at a fixed rate of interest equal to 3.13% per annum. The Lake Cameron Loan requires monthly payments of accrued interest only from the period of March 1, 2013 to February 1, 2018. Beginning on March 1, 2018, the Lake Cameron Loan will require monthly payments of accrued interest and principal based on a 30-year amortization period. All remaining indebtedness, including all interest and principal, is due by February 1, 2020. Subject to limited exceptions, our subsidiary that owns Lake Cameron must pay additional charges for prepayment of any principal prior to the three-month period beginning on November 1, 2019. There are no guaranties of the Lake Cameron Loan provided by us or our operating partnership.

In accordance with the terms of the Lake Cameron Loan Agreement and the note related to the borrowing, the payment of the note may be accelerated at the option of the Lender if an event of default occurs. As defined in the Lake Cameron Loan Agreement, events of default include, but are not limited to: failure to pay any amount due under the Lake Cameron Loan Agreement or any related documents when due; failure to maintain insurance coverage required under the Lake Cameron Loan Agreement; owning any real or personal property other than the mortgaged property and personal property related to the operation and maintenance of the mortgaged property; and any materially false or misleading representations or warranties made in connection with the Lake Cameron Loan Agreement.

We expect that the initial basis in the property for federal income tax purposes will be equal to the purchase price. We plan to depreciate the property for federal income tax purposes on a straight-line basis using an estimated useful life of 27.5 years.

All the leased space is residential with leases ranging from an initial term of six months to one year. The average historical occupancy rate (determined by the total number of units actually occupied at the specific point in time indicated) for the last five years is as follows:

S-14

At December 31, 2011 | 92.7% |

At December 31, 2010 | 93.3% |

At December 31, 2009 | 94.8% |

At December 31, 2008 | 87.5% |

At December 31, 2007 | 96.6% |

No single tenant occupies 10% or more of Lake Cameron.

The average historical effective net annual rental rate per unit (including any tenant concessions and abatements) at the property is as follows:

Year ending December 31, 2011 | $9,119 |

Year ending December 31, 2010 | $8,693 |

Year ending December 31, 2009 | $8,504 |

Year ending December 31, 2008 | $8,845 |

Year ending December 31, 2007 | $8,251 |

Property taxes paid on Lake Cameron for the fiscal year ended December 31, 2011 were $214,187. Lake Cameron was subject to a tax rate of .902% of its assessed value.

Under a contract with our manager, the property manager will act as property manager of Lake Cameron. We believe Lake Cameron is adequately insured.

An unaudited trailing twelve month profit and loss financial report for Lake Cameron for the period ended September 30, 2012 is included as Exhibit B hereto.

McNeil Ranch

On January 18, 2013, our operating partnership, under the terms of the Liquidation Agreement, was designated as the Williams Purchaser (as defined in the Liquidation Agreement) and exercised its option to purchase all of the common stock of McNeil Ranch REIT Inc., the indirect fee-simple owner of McNeil Ranch. On January 23, 2013, our operating partnership closed on such purchase.

The total acquisition cost of McNeil Ranch was approximately $21.0 million, subject to adjustments for customary pro rations in the acquisition of real estate. The $21.0 million acquisition cost includes existing first mortgage debt of approximately $13.4 million, which has been paid in full, but excludes acquisition-related and financing-related transaction costs. In connection with the purchase of this asset, our manager received an acquisition fee equal to approximately $0.2 million. Other closing and financing related costs are expected to be approximately $0.8 million, including approximately $0.2 million for minor deferred maintenance and minor capital expenditures. In connection with the acquisition of McNeil Ranch, we refinanced the existing first mortgage debt with a portion of the net proceeds from the Private Placement and with a new loan of approximately $13.6 million originated by Jones Lang.

McNeil Ranch is a multifamily community consisting of 192 units located in Austin, Texas. The community consists of sixteen residential buildings and one clubhouse on a 10.9-acre landscaped setting. McNeil Ranch is comprised of a unit mix of 86 one-

S-15

bedroom units, 70 two-bedroom units and 36 three-bedroom units. The property was constructed in 1999 and its apartment homes have an average size of 1,067 square feet. We believe the McNeil Ranch property is suitable and adequate for use as a multifamily apartment complex. We have no present intention to make major renovations, improvements or developments at the McNeil Ranch property.

There are currently eleven other apartment communities in the area that we believe are competitive with McNeil Ranch. Including McNeil Ranch, these 12 communities include 3,743 units, have an average unit size of 946 square feet and an average year of construction of 1999. In addition to existing competitive properties, the submarket in which McNeil Ranch is located had 244 units delivered in the twelve months ended September 30, 2012 and no additional units are scheduled to be delivered through September 30, 2013. In addition to the specific competitive conditions described above, general competitive conditions affecting Lake Cameron include those identified in the section entitled "Competition" included elsewhere in this prospectus.

On January 24, 2013, our subsidiary that owns McNeil Ranch obtained a non-recourse first mortgage loan, or the McNeil Ranch Loan, from Jones Lang in the original principal amount of approximately $13.6 million. Following execution of a Multifamily Loan and Security Agreement, or the McNeil Ranch Loan Agreement, and related documents, Jones Lang will sell, transfer, deliver and assign the McNeil Ranch Loan to the Lender. The McNeil Ranch Loan is secured McNeil Ranch by a Multifamily Deed of Trust, Assignment of Rents, Security Agreement and Fixture Filing, or the McNeil Mortgage, and together with the Ashford Mortgage and the Lake Cameron Mortgage, the Mortgages. Our subsidiary that owns McNeil Ranch received net proceeds of approximately $13.4 million after payment of costs and fees associated with obtaining the McNeil Ranch Loan. The McNeil Ranch Loan bears interest at a fixed rate of interest equal to 3.13% per annum. The McNeil Ranch Loan requires monthly payments of accrued interest only from the period of March 1, 2013 to February 1, 2018. Beginning on March 1, 2018, the McNeil Ranch Loan will require monthly payments of accrued interest and principal based on a 30-year amortization period. All remaining indebtedness, including all interest and principal, is due by February 1, 2020. Subject to limited exceptions, our subsidiary that owns McNeil Ranch must pay additional charges for prepayment of any principal prior to the three-month period beginning on November 1, 2019. There are no guaranties of the McNeil Ranch Loan provided by us or our operating partnership.

In accordance with the terms of the McNeil Ranch Loan Agreement and the note related to the borrowing, the payment of the note may be accelerated at the option of the Lender if an event of default occurs. As defined in the McNeil Ranch Loan Agreement, events of default include, but are not limited to: failure to pay any amount due under the McNeil Ranch Loan Agreement or any related documents when due; failure to maintain insurance coverage required under the McNeil Ranch Loan Agreement; owning any real or personal property other than the mortgaged property and personal property related to the operation and maintenance of the mortgaged property; and any materially false or misleading representations or warranties made in connection with the McNeil Ranch Loan Agreement.

We expect that the initial basis in the property for federal income tax purposes will be equal to the purchase price. We plan to depreciate the property for federal income tax purposes on a straight-line basis using an estimated useful life of 27.5 years.

All the leased space is residential with leases ranging from an initial term of six months to one year. The average historical occupancy rate (determined by the total number of units actually occupied at the specific point in time indicated) for the last five years is as follows:

At December 31, 2011 | 97.4% |

At December 31, 2010 | 94.8% |

At December 31, 2009 | 90.6% |

At December 31, 2008 | 90.6% |

At December 31, 2007 | 94.3% |

No single tenant occupies 10% or more of McNeil Ranch.

S-16

The average historical effective net annual rental rate per unit (including any tenant concessions and abatements) at the property is as follows:

Year ending December 31, 2011 | $12,628 |

Year ending December 31, 2010 | $12,061 |

Year ending December 31, 2009 | $12,231 |

Year ending December 31, 2008 | $12,542 |

Year ending December 31, 2007 | $12,073 |

Property taxes paid on McNeil Ranch for the fiscal year ended December 31, 2011 were $411,296. McNeil Ranch was subject to a tax rate of 2.475% of its assessed value.

Under a contract with our manager, the property manager will act as property manager of McNeil Ranch. We believe McNeil Ranch is adequately insured.

An unaudited trailing twelve month profit and loss financial report for McNeil Ranch for the period ended September 30, 2012 is included as Exhibit C hereto.

Certain Relationships and Related Transactions

The following disclosure is added under the immediately prior to the section entitled "Certain Relationships and Related Transactions — The Manager Loan" on page S-65 of Supplement No. 3.

Liquidation Agreement

"On January 18, 2013, WMAF, WMAF GP, Williams LP, WRA and Oxford, entered into the Liquidation Agreement in connection with, among other things, the acquisition of up to three real estate investment properties: Ashford Park, Lake Cameron and McNeil Ranch, or, collectively, the Real Estate Investment Properties. We are not a party to the Liquidation Agreement. Oxford holds an indirect 95% interest, and affiliates of the company hold an indirect 5% interest, in the Real Estate Investment Properties through their ownership of WMAF.

The Liquidation Agreement provides that Williams LP had the right to exercise an option to purchase all the outstanding common stock of the separate real estate investment trusts, or the REIP Entities, that indirectly own the Real Estate Investment Properties (and thereby acquire the Real Estate Investment Properties) at the agreed-upon purchase prices included therein. The Liquidation Agreement generally is binding on the parties thereto, but the transactions contemplated thereby regarding the acquisition of the Real Estate Investment Properties were subject to certain conditions, including Williams LP giving affirmative notice of its desire to acquire all the common stock of the REIP Entities and designating our operating partnership as the purchaser of all the common stock of the REIP Entities. The Liquidation Agreement provides that the Real Estate Investment Properties will need to be acquired by January 25, 2013 for the Ashford Park and McNeil Ranch properties and March 31, 2013 for the Lake Cameron property.

On January 18, 2013, pursuant to the terms of the Option Exercise Notices, Williams LP exercised its options to purchase all the common stock of the REIP Entities and thereby acquire indirectly the ownership of the Real Estate Investment Properties, and designated our operating partnership as the purchaser of all the common stock of the REIP Entities, with a final closing date for such purchases of January 23, 2013. Further, on January 23, 2013, pursuant to the terms of stock transfer agreements, or the Stock Transfer Agreements, among our operating partnership, WMAF and WMAF GP, all the shares of common stock of the REIP Entities that indirectly own the Real Estate Investment Properties were transferred from WMAF to our operating partnership. John A. Williams, our Chief Executive Officer and Chairman, indirectly owns an approximate 1.56% interest in WMAF, Leonard A. Silverstein, our President and Chief Operating Officer and a board member, indirectly owns an approximate 0.16% interest in WMAF and William F.

S-17

Leseman, our Executive Vice President – Property Management, indirectly owns an approximate 0.05% interest in WMAF. In connection with the acquisition of all of the Real Estate Investment Properties, from these indirect interests in WMAF, Mr. Williams, Mr. Silverstein and Mr. Leseman received approximately $331,175, $33,268 and $10,429, respectively."

The following disclosure replaces the first sentence of the first paragraph under the heading "Certain Relationships and Related Party Transactions--Real Estate Property Investments" on page S-65 of Supplement No. 3.

"As of the date of this prospectus, we have acquired six multifamily communities and entered into the Mezzanine Loan related to the construction of a multifamily community that we have an option to purchase."

The following disclosure is added immediately following the final paragraph under the heading "Certain Relationships and Related Party Transactions--Real Estate Property Investments" on page S-66 of Supplement No. 3.

"Each of Ashford Park, Lake Cameron and McNeil Ranch were acquired pursuant to the terms of the Liquidation Agreement between WMAF, WMAF GP, Williams LP, WRA and Oxford. We are not a party to the Liquidation Agreement. Oxford holds an indirect 95% interest, and affiliates of the company hold an indirect 5% interest, in the Real Estate Investment Properties through their ownership of WMAF. John A. Williams, our Chief Executive Officer and Chairman, indirectly owns an approximate 1.56% interest in WMAF, Leonard A. Silverstein, our President and Chief Operating Officer and a board member, indirectly owns an approximate 0.16% interest in WMAF and William F. Leseman, our Executive Vice President – Property Management, indirectly owns an approximate 0.05% interest in WMAF. In connection with the acquisition of each of Ashford Park, Lake Cameron and McNeil Ranch, from these indirect interests in WMAF, Mr. Williams, Mr. Silverstein and Mr. Leseman received approximately $331,175, $33,268 and $10,429, respectively."

Description of Securities

The following disclosure is added immediately preceding the section entitled, "Description of Securities – Common Stock Warrants" on page 155 of the Prospectus.

"Series B Mandatorily Convertible Preferred Stock

Our board of directors, including our independent directors, has created out of the authorized and unissued shares of our preferred stock, a series of preferred stock, designated as the Series B Mandatorily Convertible Preferred Stock.

The following is a brief description of the terms of our Series B Mandatorily Convertible Preferred Stock, which was offered to certain investors in the Private Placement described above. The description of our Series B Mandatorily Convertible Preferred Stock contained herein does not purport to be complete and is qualified in its entirety by reference to the Articles Supplementary for our Series B Mandatorily Convertible Cumulative Perpetual Preferred Stock, which has been filed with the SEC as exhibit 4.1 to that certain Current Report on Form 8-K, filed with the SEC on January 23, 2013.

Rank: The Series B Mandatorily Convertible Preferred Stock ranks senior to our common stock and to the Class A Units and Class B Units issued by our operating partnership and on a parity with the Series A Redeemable Preferred Stock, the Series A Redeemable Preferred Limited Partnership Units issued by our operating partnership and the Series B Mandatorily Convertible Preferred Stock issued by our operating partnership with respect to payment of dividends and distribution of amounts upon liquidation, dissolution or winding up.

Stated Value: Each share of Series B Mandatorily Convertible Preferred Stock has a "Stated Value" of $1,000.

Dividends: Subject to the preferential rights of the holders of any class or series of our capital stock ranking senior to the Series B Mandatorily Convertible Preferred Stock, if any such class or series is authorized in the future, the holders of Series B Mandatorily Convertible Preferred Stock are entitled to receive, when, and if authorized by our board of directors and declared by us out of legally available funds, a dividend, on an as converted basis, that mirrors any dividend payable on shares of our common stock and also will be entitled to share in any other distribution made on our common stock on an as converted basis (other than dividends or other distributions payable in our common stock), for the period beginning with any dividends and other distributions in respect of the

S-18

first quarter of 2013. Any dividends or other distributions on the Series B Mandatorily Convertible Preferred Stock for the first quarter of 2013 will be paid, on an as converted basis, pro rata from the date of issuance.

For the period beginning on May 16, 2013, but only to the extent that the Series B Mandatorily Convertible Preferred Stock remains outstanding during this period and subject to the preferential rights of holders of any shares of senior capital stock of the company, each share of the Series B Mandatorily Convertible Preferred Stock will bear a dividend, when and as authorized by the Board of Directors, equal to the excess, if any, of (i) 15.0% per annum, minus (ii) any dividend or other distribution payable by us on the Series B Mandatorily Convertible Preferred Stock pursuant to the previous paragraph in respect of the applicable quarterly period. Such dividends shall be cumulative from May 16, 2013 and shall be payable quarterly in arrears on or before July 15th, October 15th, January 15th and April 15th of each year or, if not a business day, the next succeeding business day. If the Series B Mandatorily Convertible Preferred Stock is converted to our common stock prior to May 16, 2013, then no additional dividends will be payable on the Series B Mandatorily Convertible Preferred Stock.

Mandatory Conversion: The Series B Mandatorily Convertible Preferred Stock will automatically convert into shares of our common stock on the later of (a) the close of business on the fifth business day and (b) approval of our listing application for such shares of our common stock by the NYSE MKT, in both cases, following the approval by the requisite holders of our common stock of the conversion of the Series B Mandatorily Convertible Preferred Stock into common stock and the issuance of common stock upon such conversion. Each share of Series B Mandatorily Convertible Preferred Stock shall convert into that number of shares of our common stock equal to (i) the sum of the Stated Value and all accrued and unpaid dividends thereon, divided by (ii) the conversion price of $7.00 per share, subject to adjustment as described below.

Adjustment. If the company, at any time prior to the conversion of the Series B Mandatorily Convertible Preferred Stock into shares of our common stock, (i) pays a dividend or make a distribution on the outstanding shares of its common stock payable in its common stock, (ii) subdivides the outstanding shares of its common stock into a larger number of shares, (iii) combines the outstanding shares of its common stock into a smaller number of shares, or (iv) issues any shares of its capital stock in a reclassification, recapitalization or other similar event affecting its common stock (subject to certain exceptions as specified in the Articles Supplementary for Series B Mandatorily Convertible Preferred Stock), then the conversion price in effect immediately prior to such event shall be adjusted (and/or any other appropriate actions shall be taken by the company) so that the holder of any share of Series B Mandatorily Convertible Preferred Stock thereafter converted shall be entitled to receive the number of shares of our common stock or other securities of the company that such holder would have owned or would have been entitled to receive upon or by reason of any of the events described above, had such share of Series B Mandatorily Convertible Preferred Stock been converted immediately prior to the occurrence of such event. No fractional adjustments shall be made in an amount of less than one cent per share.

Voting Rights: Holders of the Series B Mandatorily Convertible Preferred Stock generally will have no voting rights, unless their preferred dividends are in arrears for six or more quarterly periods (whether or not consecutive). Whenever such a preferred dividend default exists, holders of Series B Mandatorily Convertible Preferred Stock, voting as a single class with the holders of any other class or series of our preferred stock having similar voting rights, have the right to elect two additional directors to the Board of Directors. This right continues until all dividends accumulated on the Series B Mandatorily Convertible Preferred Stock have been fully paid or authorized and declared and a sum sufficient for the payment thereof set aside for payment. The term of office of each director elected by the holders of Series B Mandatorily Convertible Preferred Stock expires upon cure of the preferred dividend default.