Attached files

| file | filename |

|---|---|

| EX-1.1 - FORM OF UNDERWRITING AGREEMENT - Performant Financial Corp | d468140dex11.htm |

| EX-5.1 - OPINION OF PILLSBURY WINTHROP SHAW PITTMAN LLP - Performant Financial Corp | d468140dex51.htm |

| EX-23.1 - CONSENT OF KPMG LLP, INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - Performant Financial Corp | d468140dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on January 28, 2013

Registration No. 333-186110

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No.1

to

Form S-1

REGISTRATION STATEMENT

Under

THE SECURITIES ACT OF 1933

PERFORMANT FINANCIAL CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 7389 | 20-0484934 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

333 North Canyons Parkway

Livermore, California 94551

(925) 960-4800

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Lisa Im

Chief Executive Officer

333 North Canyons Parkway

Livermore, California 94551

(925) 960-4800

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Blair W. White, Esq. | Joshua N. Korff, Esq. | |

| David E. Lillevand, Esq. | Michael Kim, Esq. | |

| Matthew Hallinan, Esq. | Kirkland & Ellis LLP | |

| Pillsbury Winthrop Shaw Pittman LLP | 601 Lexington Avenue | |

| Four Embarcadero Center, 22nd Floor | New York, New York 10022 | |

| San Francisco, California 94111 | (212) 446-4800 | |

| (415) 983-1000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) | ||||||

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and the selling stockholders are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued January 28, 2013

7,000,000 Shares

COMMON STOCK

The selling stockholders are offering 7,000,000 shares of common stock. We will not receive any proceeds from the sale of shares by the selling stockholders.

Our common stock is listed on The NASDAQ Global Select Market under the symbol “PFMT.” On January 25, 2013, the last sale of our common stock as reported on The NASDAQ Global Select Market was $11.34 per share.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 13.

PRICE $ A SHARE

| Price to Public | Underwriting Discounts and Commissions |

Proceeds to Selling Stockholders |

||||||||||

| Per Share |

$ | $ | $ | |||||||||

| Total |

$ | $ | $ | |||||||||

The selling stockholders identified in this prospectus have granted the underwriters an option for a period of 30 days to purchase, on the same terms and conditions as set forth above, up to an additional 1,050,000 shares of our common stock. We will not receive any of the proceeds from the sale of shares by these selling stockholders if the underwriters exercise their option to purchase additional shares of common stock.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to purchasers on , 2013.

| GOLDMAN, SACHS & CO. | MORGAN STANLEY | |

| WELLS FARGO SECURITIES |

CREDIT SUISSE |

WILLIAM BLAIR

, 2013

Table of Contents

You should rely only on the information contained in this prospectus and any free writing prospectus we may specifically authorize to be delivered or made available to you. We have not, and the selling stockholders and the underwriters have not, authorized anyone to provide you with additional or different information. The information contained in this prospectus or any free writing prospectus is accurate only as of its date, regardless of its time of delivery or of any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

This prospectus is an offer to sell only the shares offered hereby but only under circumstances and in jurisdictions where it is lawful to do so.

Table of Contents

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including our consolidated financial statements and the related notes and the information set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in each case included elsewhere in this prospectus. Unless expressly indicated or the context otherwise requires, in this prospectus, “Performant,” “we,” “us,” “our,” and the “Company” refer to Performant Financial Corporation and, where appropriate, its subsidiaries.

Overview

We provide technology-enabled recovery and related analytics services in the United States. Our services help identify and recover delinquent or defaulted assets and improper payments for both government and private clients in a broad range of markets. Our clients typically operate in complex and regulated environments and outsource their recovery needs in order to reduce losses on billions of dollars of defaulted student loans, improper healthcare payments and delinquent state tax and federal treasury receivables. We generally provide our services on an outsourced basis, where we handle many or all aspects of our clients’ recovery processes.

We believe we have a leading position in our markets based on our proprietary technology-enabled services platform, long-standing client relationships and the large volume of funds we have recovered for our clients. In 2011, we provided recovery services on approximately $8.7 billion of combined student loans and other delinquent federal and state receivables and recovered approximately $189 million in improper Medicare payments. Our clients include 12 of the 32 public sector participants in the student loan industry and these relationships average more than 10 years in length, including a 22-year relationship with the U.S. Department of Education. In the healthcare market, we are currently one of four prime Medicare Recovery Audit Contractors, or RACs, in the United States for the Centers for Medicare and Medicaid Services, or CMS.

We utilize our technology platform to efficiently provide recovery and analytics services in the markets we serve. We have continuously developed and refined our technology platform for almost two decades by using our extensive domain and data processing expertise. We believe our technology platform allows us to achieve higher workforce productivity versus more traditional labor-intensive outsourcing business models, as we generated in excess of $130,000 of revenues per employee during 2011, based on the average number of employees during the year. In addition, we believe that our platform is easily adaptable to new markets and processes. For example, we utilized the same basic platform previously used primarily for student loan recovery activities to enter the healthcare market.

Our revenue model is generally success-based as we earn fees based on a percentage of the aggregate amount of funds that we enable our clients to recover. Our services do not require any significant upfront investments by our clients and we offer our clients the opportunity to recover significant funds otherwise lost. Furthermore, our business model does not require significant capital expenditures for us and we do not purchase loans or obligations. We believe we benefit from a significant degree of revenue visibility due to reasonably predictable recovery outcomes in a substantial portion of our business. For the year ended December 31, 2011, we generated approximately $163.0 million in revenues, $12.4 million in net income, $57.8 million in adjusted EBITDA and $25.0 million in adjusted net income. For the nine months ended September 30, 2012, we generated approximately $154.1 million in revenues, $17.0 million in net income, $52.2 million in adjusted EBITDA and $23.5 million in adjusted net income, and our total debt was $150.5 million at September 30, 2012. See “Adjusted EBITDA and Adjusted Net Income” below for a definition of adjusted EBITDA and adjusted net income and reconciliations of adjusted EBITDA and adjusted net income to net income determined in accordance with generally accepted accounting principles.

1

Table of Contents

Industry Overview

We operate in markets characterized by strong growth, a complex regulatory environment and a significant amount of delinquent, defaulted or improperly paid assets.

Student Lending

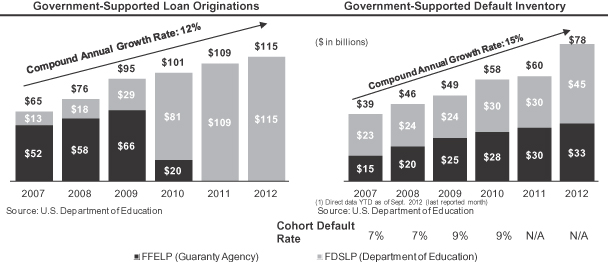

According to the Department of Education, total government-supported student loan originations were estimated to be approximately $115 billion in the year ended September 30, 2012, and the aggregate dollar amount of these loans has grown at a compound annual growth rate of 11% from 2002 through 2012. The “cohort default rate,” which is the measure utilized by the Department of Education to track the percentage of government-supported loan borrowers that enter repayment in a certain year ended September 30 and default by the end of the next year ended September 30, has risen from approximately 5% in 2006 to approximately 9% in 2010, the last year for which data is available.

Healthcare

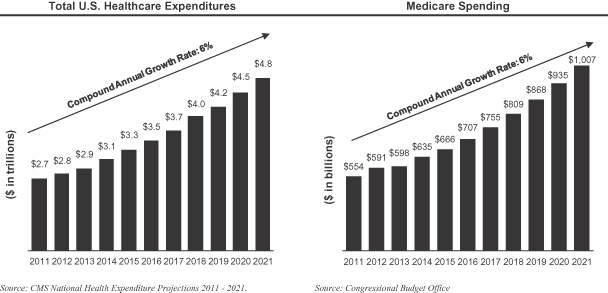

According to CMS, U.S. healthcare spending reached $2.7 trillion in 2011 and is forecast to grow at a 6% annual rate through 2021. CMS indicates that government-related healthcare spending for 2011 totaled approximately $1.2 trillion. This government-related spending included approximately $554 billion of payments under Medicare, of which $43 billion, or 8%, was estimated to be improper. Medicare improper payments generally involve incorrect coding, procedures performed which were not medically necessary, incomplete documentation or claims submitted based on outdated fee schedules, among other issues.

Other Markets

We believe that the demand for recovery of delinquent state taxes will grow as state governments struggle with revenue generation and face significant budget deficits. According to the Center on Budget and Policy Priorities, an independent think tank, 43 U.S. states faced budget shortfalls totaling $107 billion in the year ended September 30, 2012, with at least 31 states anticipating deficits for fiscal year 2013. The federal agency market consists of government debt subrogated to the Department of the Treasury. For the year ended September 30, 2011, federal agency recoveries in this market totaled more than $6.2 billion, a significant portion of which were made by private firms on behalf of the Department of Financial Management Service, a bureau of the Department of the Treasury.

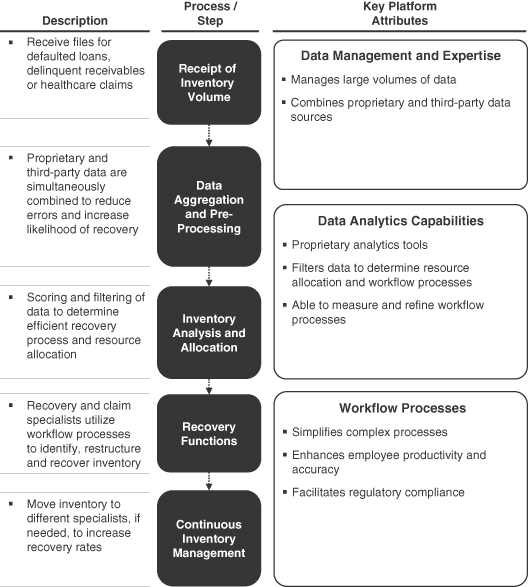

Our Platform

Our technology-enabled services platform is based on over two decades of experience in recovering large amounts of funds on behalf of our clients across several markets. The components of our platform include our data management expertise, analytics capabilities and technology-based workflow processes. Our platform integrates these components to allow us to achieve optimized outcomes for our clients in the form of increased efficiency and productivity and high recovery rates. We believe our platform and workflow processes are also intuitive and easy to use for our recovery and claims specialists and allow us to increase our employee retention and productivity.

Our Competitive Strengths

We believe that our business is difficult to replicate, as it incorporates a combination of several important and differentiated elements, including:

| • | Scalable and flexible technology-enabled services platform. We have built a proprietary technology platform that is highly flexible, intuitive and easy to use for our recovery and claims specialists. Our platform is easily configurable and deployable across multiple markets and processes. |

2

Table of Contents

| • | Advanced, technology-enabled workflow processes. Our technology-enabled workflow processes, developed over many years of operational experience in recovery services, disaggregate otherwise complex recovery processes into a series of simple, efficient and consistent steps that are easily configurable and applicable to different types of recovery-related applications. |

| • | Enhanced data and analytics capabilities. Our data and analytics capabilities allow us to achieve strong recovery rates for our clients. We have collected recovery-related data for over two decades, which we combine with large volumes of client and third-party data to effectively analyze our clients’ delinquent or defaulted assets and improper payments. We have also developed a number of analytics tools that we use to score our clients’ recovery inventory, determine the optimal recovery process and allocation of resources, and achieve higher levels of recovery results for our clients. |

| • | Long-standing client relationships. We believe our long-standing focus on achieving superior recovery performance for our clients and the significant value our clients derive from this focus have helped us achieve long-tenured client relationships, strong contract retention and better access to new clients and future growth opportunities. |

| • | Extensive domain expertise in complex and regulated markets. We have extensive experience and domain expertise in providing recovery services for government and private institutions that generally operate in complex and regulated markets. We have demonstrated our ability to develop domain expertise in new markets such as healthcare and state tax and federal Treasury receivables. |

| • | Proven and experienced management team. Our management team has significant industry experience and has successfully grown our revenue base and service offerings beyond the original student loan market into healthcare and delinquent state tax and private financial institutions receivables. |

Our Growth Strategy

Key elements of our growth strategy include the following:

| • | Expand our student loan recovery volume. We have long-standing relationships with some of the largest participants in the government-supported student loan market, and we believe there are significant opportunities within this growing market to increase the volume of student loans placed with us by existing and new clients. |

| • | Expand our recovery services in the healthcare market. As healthcare spending grows, we expect the need for recovery services to increase in the public and private healthcare markets. We intend to expand our recovery services for existing clients, such as CMS, and offer analytics services to potential clients in the private healthcare market. |

| • | Pursue strategic alliances and acquisitions. We intend to selectively consider opportunities to grow through strategic alliances or acquisitions that are complementary to our business. |

Recent Developments (Unaudited)

Three-months and year ended December 31, 2012

Our consolidated financial statements for the three-months and year ended December 31, 2012 are not yet available. Our expectations with respect to our unaudited results for the period discussed below are based upon management estimates. The preliminary financial results presented below are subject to the completion of our financial closing procedures and any adjustments that may result from the completion of the audit of our 2012 consolidated financial statements. Accordingly, these results may change and those changes may be material. This summary is not meant to be a comprehensive statement of our unaudited financial results for these periods and our actual results may differ from these estimates. For additional information regarding the various risks and uncertainties inherent in estimates of this type, see “Information Regarding Forward-Looking Statements,” elsewhere in this prospectus.

3

Table of Contents

We are providing the following preliminary estimates of our financial results and operating metrics for the three-months ended December 31, 2012:

GAAP

| • | Revenues are expected to be between $53.5 million and $56.5 million, representing a sequential quarterly increase of approximately 3.0% at the midpoint of the range. The estimated increase is the result of increased revenues from the student lending and healthcare markets. Revenues from the student lending market are estimated to be between $33.9 million and $34.6 million, representing a sequential quarterly increase of approximately 3.8% at the midpoint of the range. Revenues from the healthcare market are estimated to be between $14.2 million and $16.0 million, representing a sequential quarterly increase of approximately 11.7% at the midpoint of the range, reflecting higher claim recovery volumes from CMS under our RAC contract. Revenues from other markets are estimated to be between $5.4 million and $5.9 million. |

| • | Net income is estimated to be between $5.5 million and $6.8 million, representing a sequential quarterly decrease of approximately 3.2% at the midpoint of the range, due to increased operating expenses consistent with the growth of our recovery activities under our RAC contract and expenses we have incurred to process Periodic Interim Payment providers, or PIP, claims under our RAC contract where we have not been able to recognize related revenues but expect to in the future. We have also incurred additional expenses associated with being a public company. |

Non-GAAP

| • | Adjusted EBITDA is expected to be between $16.1 million and $18.1 million, representing a sequential quarterly decrease of approximately 6.4% at the midpoint of the range is primarily due to the increase in operating expenses as described above. |

| • | Adjusted net income is estimated to be between $6.7 million and $8.0 million, representing a sequential quarterly decrease of approximately 9.8% at the midpoint of the range is primarily due to the increase in our operating expenses as described above. |

Operating Metrics

| • | Student Loan Placement Volume is estimated to be between $1.9 billion and $2.2 billion and Placement Revenue as a Percentage of Placement Volume is estimated to be between 1.50% and 1.70%. |

| • | Healthcare Net Claim Recovery Volume is estimated to be between $125.0 million and $140.0 million and Claim Recovery Fee Rate is estimated to be approximately 11.3%. |

We are providing the following preliminary estimates of our financial results and operating metrics for the year ended December 31, 2012:

GAAP

| • | Revenues are expected to be between $207.6 million and $210.6 million, representing a sequential annual increase of approximately 28.3% at the midpoint of the range. The estimated increase is due to greater audit and recovery activities from the student lending and healthcare markets. Revenues from the student lending market are estimated to be between $132.1 million and $132.8 million, representing an annual increase of approximately 8.3% at the midpoint of the range. Revenues from the healthcare market are estimated to be between $53.3 million and $55.1 million, representing an annual increase of approximately 151.5% at the midpoint of the range, reflecting higher claim recovery volumes from CMS under our RAC contract. Revenues from other markets are estimated to be between $22.2 million and $22.7 million. |

4

Table of Contents

| • | Net income is estimated to be between $22.5 million and $23.8 million, representing a sequential annual estimated increase of approximately 87.2% at the midpoint of the range, due to greater audit and recovery activities from the student lending and healthcare markets. |

Non-GAAP

| • | Adjusted EBITDA is expected to be between $68.3 million and $70.3 million, representing a sequential annual estimated increase of approximately 20.0% at the midpoint of the range, primarily due to the increase in our estimated net income as described above. |

| • | Adjusted net income is estimated to be between $30.2 million and $31.5 million, representing an estimated increase of approximately 23.5% at the midpoint of the range, primarily due to the increase in our estimated net income as described above. |

Operating Metrics

| • | Student Loan Placement Volume is estimated to be between $5.5 billion and $5.8 billion and Placement Revenue as a Percentage of Placement Volume is estimated to be between 2.25% and 2.40%. |

| • | Healthcare Net Claim Recovery Volume is estimated to be between $470.0 million and $485.0 million and Claim Recovery Fee Rate is estimated to be approximately 11.3%. |

See “—Summary Consolidated Financial Data—Adjusted EBITDA and Adjusted Net Income” for a definition of adjusted EBITDA and adjusted net income, the reasons for providing these financial measures and the limitations of these measures, which do not reflect all items of income and expense as reported under GAAP. Also, see below for reconciliations of the estimated and actual adjusted EBITDA and adjusted net income amounts set forth above to estimated or actual net income determined in accordance with GAAP.

Operating Metrics

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Operating Metrics” for the definition of the operating metrics used above and the purposes for which management uses these metrics.

5

Table of Contents

The following tables present a reconciliation of estimated adjusted EBITDA and estimated adjusted net income for the three-months and the year ended December 31, 2012, to estimated net income for these periods and adjusted EBITDA and adjusted net income for the three months ended September 30, 2012 and the year ended December 31, 2011, to actual net income for these periods:

| Three Months Ended | Year Ended | |||||||||||||||

| September 30, 2012 |

December 31, 2012 |

December 31, 2011 |

December 31, 2012 |

|||||||||||||

| (in thousands) | ||||||||||||||||

| Reconciliation of Adjusted EBITDA: |

||||||||||||||||

| Net income |

$ | 6,383 | $ | 5,525 to 6,830 | $ | 12,372 | $ | 22,503 to 23,808 | ||||||||

| Provision for income taxes |

4,601 | 4,257 to 4,951 | 7,516 | 15,955 to 16,649 | ||||||||||||

| Interest expense |

3,175 | 3,087 | 13,530 | 12,416 | ||||||||||||

| Interest income |

(2 | ) | — | (125 | ) | (64 | ) | |||||||||

| Debt extinguishment costs(1) |

— | — | — | 3,679 | ||||||||||||

| Depreciation and amortization |

2,445 | 2,501 | 7,766 | 9,503 | ||||||||||||

| Impairment of trade name(2) |

— | — | 13,400 | — | ||||||||||||

| Non-core operating expenses(3) |

— | — | 2,548 | 47 | ||||||||||||

| Advisory fee(4) |

932 | — | 634 | 2,640 | ||||||||||||

| Stock based compensation |

734 | 731 | 120 | 1,614 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA |

$ | 18,268 | $ | 16,100 to 18,100 | $ | 57,761 | $ | 68,292 to 70,291 | ||||||||

| Three Months Ended | Year Ended | |||||||||||||||

| September 30, 2012 |

December 31, 2012 |

December 31, 2011 |

December 31, 2012 |

|||||||||||||

| (in thousands) | ||||||||||||||||

| Reconciliation of Adjusted Net Income: |

||||||||||||||||

| Net income |

$ | 6,383 | $ | 5,525 to 6,830 | $ | 12,372 | $ | 22,503 to 23,808 | ||||||||

| Debt extinguishment costs(1) |

— | — | — | 3,679 | ||||||||||||

| Impairment of trade name(2) |

— | — | 13,400 | — | ||||||||||||

| Non–core operating expenses(3) |

— | — | 2,548 | 47 | ||||||||||||

| Advisory fee(4) |

931 | — | 634 | 2,640 | ||||||||||||

| Stock based compensation |

734 | 731 | 120 | 1,614 | ||||||||||||

| Amortization of intangibles(5) |

932 | 933 | 3,043 | 3,674 | ||||||||||||

| Deferred financing amortization costs(6) |

344 | 296 | 1,254 | 1,161 | ||||||||||||

| Tax adjustments(7) |

(1,177 | ) | (784 | ) | (8,400 | ) | (5,126 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted net income |

$ | 8,147 | $ | 6,701 to 8,006 | $ | 24,971 | $ | 30,191 to 31,496 | ||||||||

| (1) | Represents debt extinguishment costs comprised of approximately $3.3 million of fees paid to lenders in connection with our new credit facility and approximately $0.3 million of unamortized debt issuance costs in connection with our old credit facility. |

| (2) | Represents impairment expenses to write off the carrying amount of the trade name intangible asset due to the plan to retire the Diversified Collection Services, Inc. trade name. |

| (3) | Represents professional fees and settlement costs related to strategic corporate development activities and a $1.2 million legal settlement in 2011. |

| (4) | Represents expenses incurred under an advisory services agreement with Parthenon Capital Partners, which was terminated in April 2012. See Note 11 “Related Party Transactions.” |

| (5) | Represents amortization of capitalized expenses related to the acquisition of Performant by an affiliate of Parthenon Capital Partners in 2004 and an acquisition in the first quarter of 2012 to enhance our analytics capabilities. |

| (6) | Represents amortization of capitalized financing costs related to debt offerings conducted in 2009, 2010 and 2012. |

| (7) | Represents tax adjustments assuming a marginal tax rate of 40%. |

6

Table of Contents

Risks Associated With Our Business

Our business is subject to numerous risks and uncertainties including those highlighted in the section titled “Risk Factors” immediately following the prospectus summary. Some of these risks include, among others, that:

| • | Revenues generated from our five largest clients represented 74% of our revenues for the year ended December 31, 2011, and any termination of or deterioration in our relationship with any of these clients would result in a decline in our revenues; |

| • | Many of our contracts with our clients for the recovery of student loans and other receivables are subject to periodic renewal or re-bidding processes, are not exclusive and do not commit our clients to provide specified volumes of business and, as a consequence, there is no assurance that we will be able to maintain our revenues and operating results; |

| • | We face significant competition in all of the markets in which we operate and an inability to compete effectively in the future could harm our relationships with our clients, which would impact our ability to maintain our revenues and operating results; |

| • | The U.S. federal government accounts for a significant portion of our revenues, and any loss of business from, or change in our relationship with, the U.S. federal government would result in a significant decrease in our revenues and operating results; |

| • | Future legislative or regulatory changes affecting the markets in which we operate could impair our business and operations; |

| • | Our business relationship with the Department of Education has accounted for a significant portion of our revenues and will take on increasing importance as a result of Student Aid and Fiscal Responsibility Act of 2010, or SAFRA. Our failure to maintain this relationship would significantly decrease our revenues; |

| • | We could lose clients as a result of consolidation among the Guaranty Agencies, or GAs, which would decrease our revenues; |

| • | Our ability to derive revenues under our RAC contract will depend in part on the number and types of potentially improper claims that we are allowed to pursue by CMS, and our results of operations may be harmed if CMS limits the scope of claims we are allowed to pursue; |

| • | A failure of our operating systems or technology infrastructure, or those of our third-party vendors and subcontractors, could disrupt the operation of our business; |

| • | If our security measures are breached or fail and unauthorized access is obtained to our clients’ confidential data, our services may be perceived as insecure, the attractiveness of our recovery services to current or potential clients may be reduced, and we may incur significant liabilities; |

| • | We are subject to extensive regulations regarding our recovery practices and the use and disclosure of confidential personal and healthcare information and failure to comply with these regulations could cause us to incur liabilities and expenses; and |

| • | Our recovery business is subject to extensive regulation and consumer protection laws and our failure to comply with those regulations and laws may subject us to liability and result in significant costs. |

Corporate Information

We commenced our operations in 1976 under the corporate name Diversified Collection Services, Inc., or DCS. We were incorporated in Delaware on October 8, 2003 under the name DCS Holdings, Inc. and subsequently changed our name to Performant Financial Corporation in 2005. Our principal executive offices are

7

Table of Contents

located at 333 North Canyons Parkway, Livermore, California 94551 and our telephone number is (925) 960-4800. Our website address is www.performantcorp.com. The information on or accessible through our website is not part of this prospectus.

Our Principal Stockholder

Our principal stockholder, an affiliate of Parthenon Capital Partners, acquired its interest in us in 2004 and prior to this offering beneficially owns approximately 64.8% of our outstanding common stock. Parthenon Capital Partners is a private equity investment firm with approximately $2 billion of capital under management. Parthenon Capital Partners was founded in March of 1998 and focuses on investing in select middle-market companies. The firm invests in a variety of industry sectors with particular expertise in business and financial services, healthcare, distribution/logistics, and technology-enabled services.

8

Table of Contents

THE OFFERING

| Common stock offered by the selling stockholders |

7,000,000 shares |

| Common stock to be outstanding after this offering |

45,320,606 shares |

| Option to purchase additional shares offered by the selling stockholders |

1,050,000 shares |

| Use of proceeds |

We will not receive any of the proceeds from the sale of shares in this offering. See “Use of Proceeds” and “Principal and Selling Stockholders.” |

| NASDAQ Global Select Market symbol |

“PFMT” |

The number of shares of common stock that will be outstanding after this offering is based on the number of shares outstanding as of September 30, 2012, and excludes:

| • | 7,912,719 shares of common stock issuable upon the exercise of options outstanding as of September 30, 2012, at a weighted-average exercise price of approximately $3.79 per share; and |

| • | 1,935,891 shares of common stock reserved for future issuance under our 2012 Stock Incentive Plan. |

Unless expressly indicated or the context otherwise requires, all information in this prospectus assumes:

| • | no exercise by the underwriters of their right to purchase up to an additional 1,050,000 shares of common stock from the selling stockholders to cover over-allotments; and |

| • | no exercise of options outstanding as of September 30, 2012. |

9

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

We have derived the summary consolidated statement of operations data for 2009, 2010 and 2011 from our audited consolidated financial statements included elsewhere in this prospectus. We have derived the summary consolidated statement of operations data for the nine months ended September 30, 2011 and 2012 and the consolidated balance sheet data as of September 30, 2012 from our unaudited consolidated financial statements included elsewhere in this prospectus. The unaudited consolidated financial statements include, in the opinion of management, all adjustments, which consist only of normal recurring adjustments, that management considers necessary for the fair statement of the financial information set forth in those statements. Our historical results are not necessarily indicative of the results that may be expected in the future. The following summary consolidated financial data should be read together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus.

| Year Ended December 31, |

Nine Months

Ended September 30, |

|||||||||||||||||||

| 2009 | 2010 | 2011 | 2011 | 2012 | ||||||||||||||||

| (Restated)(1) | (Restated)(1) | (Restated)(1) | ||||||||||||||||||

| (in thousands, except share and per share amounts) | ||||||||||||||||||||

| Consolidated Statement of Operations Data: | ||||||||||||||||||||

| Revenues |

$ | 109,832 | $ | 123,519 | $ | 162,974 | $ | 120,333 | $ | 154,099 | ||||||||||

| Operating expenses: |

||||||||||||||||||||

| Salaries and benefits |

53,728 | 58,113 | 67,082 | 50,437 | 59,426 | |||||||||||||||

| Other operating expense |

32,110 | 33,655 | 49,199 | 35,193 | 53,053 | |||||||||||||||

| Impairment of trade name |

— | — | 13,400 | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating expenses |

85,838 | 91,768 | 129,681 | 85,630 | 112,479 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from operations |

23,994 | 31,751 | 33,293 | 34,703 | 41,620 | |||||||||||||||

| Debt extinguishment costs(2) |

— | — | — | — | (3,679) | |||||||||||||||

| Interest expense |

(16,017) | (15,230) | (13,530) | (10,213) | (9,329) | |||||||||||||||

| Interest income |

104 | 118 | 125 | 94 | 64 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before provision for income taxes |

8,081 | 16,639 | 19,888 | 24,584 | 28,676 | |||||||||||||||

| Provision for income taxes |

3,071 | 6,664 | 7,516 | 9,839 | 11,698 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 5,010 | $ | 9,975 | $ | 12,372 | $ | 14,745 | $ | 16,978 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Accrual for preferred stock dividends |

5,128 | 5,771 | 6,495 | 4,785 | 2,038 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) available to common shareholders |

(118) | 4,204 | 5,877 | 9,960 | 14,940 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) per share attributable to common shareholders(3) |

||||||||||||||||||||

| Basic |

$ | (0.00) | $ | 0.10 | $ | 0.14 | $ | 0.23 | $ | 0.34 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted |

$ | (0.00) | $ | 0.09 | $ | 0.13 | $ | 0.22 | $ | 0.32 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted average shares |

||||||||||||||||||||

| Basic |

42,962 | 42,962 | 42,962 | 42,962 | 43,519 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted |

42,962 | 45,019 | 45,742 | 44,646 | 47,164 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | The consolidated financial statements have been restated for the presentation of our Redeemable Preferred Stock, which affects our balance sheets and the calculation of net income (loss) per share attributable to common shareholders, which affects our statements of operations. See Note 1 to our consolidated financial statements. |

| (2) | Represents debt extinguishment costs comprised of approximately $3.3 million of fees paid to lenders in connection with our new credit facility and approximately $0.3 million of unamortized debt issuance costs in connection with our old credit facility. |

| (3) | Please see Note 1 to our consolidated financial statements for an explanation of the calculations of our basic and diluted net income per share of common stock. |

10

Table of Contents

| As of September

30, 2012 |

||||

| (in thousands) | ||||

| Consolidated Balance Sheet Data: |

||||

| Cash and cash equivalents |

$ | 32,204 | ||

| Total assets |

$ | 207,628 | ||

| Total debt |

$ | 150,529 | ||

| Total liabilities |

$ | 190,312 | ||

| Total stockholders’ equity (deficit) |

$ | 17,316 | ||

Adjusted EBITDA and Adjusted Net Income

To provide investors with additional information regarding our financial results, we have disclosed in the table below and within this prospectus adjusted EBITDA and adjusted net income, both of which are non-GAAP financial measures. We have provided a reconciliation below of adjusted EBITDA to net income and adjusted net income to net income, the most directly comparable GAAP financial measure to these non-GAAP financial measures.

We have included adjusted EBITDA and adjusted net income in this prospectus because they are key measures used by our management and board of directors to understand and evaluate our core operating performance and trends and to prepare and approve our annual budget. Accordingly, we believe that adjusted EBITDA and adjusted net income provide useful information to investors and analysts in understanding and evaluating our operating results in the same manner as our management and board of directors.

Our use of adjusted EBITDA and adjusted net income has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are:

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future, and adjusted EBITDA does not reflect cash capital expenditure requirements for such replacements or for new capital expenditure requirements; |

| • | adjusted EBITDA does not reflect interest expense on our indebtedness; |

| • | adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| • | adjusted EBITDA does not reflect tax payments; |

| • | adjusted EBITDA and adjusted net income do not reflect the potentially dilutive impact of equity-based compensation; |

| • | adjusted EBITDA and adjusted net income do not reflect the impact of certain non-operating expenses resulting from matters we do not consider to be indicative of our core operating performance; and |

| • | other companies may calculate adjusted EBITDA and adjusted net income differently than we do, which reduces its usefulness as a comparative measure. |

Because of these limitations, you should consider adjusted EBITDA and adjusted net income alongside other financial performance measures, including net income and our other GAAP results.

11

Table of Contents

The following tables present a reconciliation of adjusted EBITDA and adjusted net income for each of the periods indicated:

| Year Ended December 31, |

Nine Months Ended September 30, |

|||||||||||||||||||

| 2009 | 2010 | 2011 | 2011 | 2012 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Reconciliation of Adjusted EBITDA: |

||||||||||||||||||||

| Net income |

$ | 5,010 | $ | 9,975 | $ | 12,372 | $ | 14,745 | $ | 16,978 | ||||||||||

| Provision for income taxes |

3,071 | 6,664 | 7,516 | 9,839 | 11,698 | |||||||||||||||

| Interest expense |

16,017 | 15,230 | 13,530 | 10,213 | 9,329 | |||||||||||||||

| Interest income |

(104 | ) | (118 | ) | (125 | ) | (94 | ) | (64 | ) | ||||||||||

| Debt extinguishment costs(1) |

— | — | — | — | 3,679 | |||||||||||||||

| Depreciation and amortization |

9,624 | 7,213 | 7,766 | 5,712 | 7,002 | |||||||||||||||

| Impairment of trade name(2) |

— | — | 13,400 | — | — | |||||||||||||||

| Non-core operating expenses(3) |

— | 1,108 | 2,548 | 2,438 | 47 | |||||||||||||||

| Advisory fee(4) |

684 | 759 | 634 | 326 | 2,641 | |||||||||||||||

| Stock based compensation |

580 | 629 | 120 | 83 | 883 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

$ | 34,882 | $ | 41,460 | $ | 57,761 | $ | 43,262 | $ | 52,193 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Year Ended December 31, |

Nine Months Ended September 30, |

|||||||||||||||||||

| 2009 | 2010 | 2011 | 2011 | 2012 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Reconciliation of Adjusted Net Income: |

||||||||||||||||||||

| Net income |

$ | 5,010 | $ | 9,975 | $ | 12,372 | $ | 14,745 | $ | 16,978 | ||||||||||

| Debt extinguishment costs(1) |

— | — | — | — | 3,679 | |||||||||||||||

| Impairment of trade name(2) |

— | — | 13,400 | — | — | |||||||||||||||

| Non–core operating expenses(3) |

— | 1,108 | 2,548 | 2,438 | 47 | |||||||||||||||

| Advisory fee(4) |

684 | 759 | 634 | 327 | 2,640 | |||||||||||||||

| Stock based compensation |

580 | 629 | 120 | 83 | 883 | |||||||||||||||

| Amortization of intangibles(5) |

5,795 | 3,043 | 3,043 | 2,282 | 2,741 | |||||||||||||||

| Deferred financing amortization costs(6) |

3,027 | 1,997 | 1,254 | 946 | 865 | |||||||||||||||

| Tax adjustments(7) |

(4,034 | ) | (3,014 | ) | (8,400 | ) | (2,430 | ) | (4,341 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted net income |

$ | 11,062 | $ | 14,497 | $ | 24,971 | $ | 18,391 | $ | 23,492 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | Represents debt extinguishment costs comprised of approximately $3.3 million of fees paid to lenders in connection with our new credit facility and approximately $0.3 million of unamortized debt issuance costs in connection with our old credit facility. |

| (2) | Represents impairment expense to write off the carrying amount of the trade name intangible asset due to the plan to retire the Diversified Collection Services, Inc. trade name. |

| (3) | Represents professional fees and settlement costs related to strategic corporate development activities and a $1.2 million legal settlement in 2011. |

| (4) | Represents expenses incurred under an advisory services agreement with Parthenon Capital Partners, which was terminated in April 2012. See “Certain Relationships and Related Party Transactions—Arrangements with Our Investors—Advisory Services Agreement.” |

| (5) | Represents amortization of capitalized expenses related to the acquisition of Performant by an affiliate of Parthenon Capital Partners in 2004, the impairment expense to reduce the carrying amount of the intangible asset due to our decision to terminate a client contract in 2009 and an acquisition in the first quarter of 2012 to enhance our analytics capabilities. |

| (6) | Represents amortization of capitalized financing costs related to debt offerings conducted in 2009, 2010 and 2012. |

| (7) | Represents tax adjustments assuming a marginal tax rate of 40%. |

12

Table of Contents

Investing in our common stock involves substantial risks. In addition to the other information in this prospectus, you should carefully consider the following factors before investing in our common stock. Any of the risk factors we describe below could adversely affect our business, financial condition and results of operations. The market price of our common stock could decline if one or more of these risks and uncertainties actually occurs, causing you to lose all or part of your investment in our shares. Certain statements in “Risk Factors” are forward-looking statements. See “Information Regarding Forward-Looking Statements” included elsewhere in this prospectus.

Risks Related to Our Business

Revenues generated from our five largest clients represented 74% of our revenues for the year ended December 31, 2011, and any termination of or deterioration in our relationship with any of these clients would result in a decline in our revenues.

We derive a substantial majority of our revenues from a limited number of clients, including the Department of Education, CMS and three GAs. Revenues from our five largest clients represented 74% of our revenues for the year ended December 31, 2011. We expect that our revenues will become increasingly concentrated with our major clients as a result of rising business volumes under our RAC contract, which accounted for approximately 25% of our revenues in the nine months ended September 30, 2012, compared to approximately 13% of our revenues in 2011. If we lose one of these clients or if the terms of our relationships with any of these clients become less favorable to us, our revenues would decline, which would harm our business, financial condition and results of operations.

Many of our contracts with our clients for the recovery of student loans and other receivables are subject to periodic renewal or re-bidding processes, are not exclusive and do not commit our clients to provide specified volumes of business and, as a consequence, there is no assurance that we will be able to maintain our revenues and operating results.

Substantially all of our existing contracts for the recovery of student loan and other receivables, which represented approximately 75% of our revenues in 2011, enable our clients to unilaterally terminate their contractual relationship with us at any time without penalty, potentially leading to loss of business or renegotiation of terms. Our contracts generally are subject to a periodic rebidding process at the end of the contract term. Further, most of our contracts in these markets allow our clients to unilaterally change the volume of loans and other receivables that are placed with us at any given time. In addition, most of our contracts are not exclusive, with our clients retaining multiple service providers with whom we must compete for placements of loans or other obligations. Therefore, despite our contractual relationships with our clients, our contracts do not provide assurance that we will generate a minimum amount of revenues or that we will receive a specific volume of placements.

Our revenues and operating results would be negatively affected if our student loans and receivables clients, which include four of our five largest clients in 2011, do not renew their agreements with us upon contract expiration, reduce the volume of student loan placements provided to us, modify the terms of service, including the success fees we are able to earn upon recovery of defaulted student loans, or any of these clients establish more favorable relationships with our competitors. For example, we have been advised that our contractual arrangement with the Department of Education may be modified as a result of the Department of Education’s decision to have its recovery vendors promote IBR to defaulted student loans. The IBR program provides flexibility on the required monthly payment for student loan borrowers at an amount intended to be affordable based on a borrower’s income and family size. As a result of the increased application of the IBR program to defaulted student loans, we expect that there will be an increase in the number of loans that become eligible for rehabilitation because more defaulted student loan borrowers will be able to make qualifying payments. In this connection, we have been advised that the Department of Education may make certain changes

13

Table of Contents

to its contractual arrangements with its recovery vendors, although the nature of the changes remains uncertain. Any changes in the contingency fee percentages or other compensation terms that we are paid under existing and future contracts could have a significant impact on our revenues and operating results.

We face significant competition in all of the markets in which we operate and an inability to compete effectively in the future could harm our relationships with our clients, which would impact our ability to maintain our revenues and operating results.

We operate in very competitive markets. In providing our services to the student loan and other receivables markets, we face competition from many other companies. Initially, we compete with these companies to be one of typically several firms engaged to provide recovery services to a particular client and, if we are successful in being engaged, we then face continuing competition from the client’s other retained firms based on the client’s benchmarking of the recovery rates of its several vendors. Those recovery vendors who produce the highest recovery rates from a client often will be allocated additional placements and in some cases additional success fees. Accordingly, maintaining high levels of recovery performance, and doing so in a cost-effective manner, are important factors in our ability to maintain and grow our revenues and net income and the failure to achieve these objectives could harm our business, financial condition and results of operations.

Similarly, we faced a highly competitive bidding process to become one of the four prime RAC contractors that provide recovery services for improper Medicare payments. We expect that CMS will issue a request for proposals in connection with the re-bidding for the RAC contracts in the first half of 2013. Although our RAC contract is currently set to expire in 2014, CMS may terminate our RAC contract as early as August 2013 in connection with the re-bidding process for new RAC contracts. We expect that this process will be competitive. The failure to retain this contract or a significant adverse change in the terms of this contract, which generated approximately 25% of our revenues in the nine months ended September 30, 2012, would seriously harm our ability to maintain or increase our revenues and operating results.

Some of our current and potential competitors in the markets in which we operate may have greater financial, marketing, technological or other resources than we do. The ability of any of our competitors and potential competitors to adopt new and effective technology to better serve our markets may allow them to gain market strength. Increasing levels of competition in the future may result in lower recovery fees, lower volumes of contracted recovery services or higher costs for resources. Any inability to compete effectively in the markets that we serve could adversely affect our business, financial condition and results of operations.

The U.S. federal government accounts for a significant portion of our revenues, and any loss of business from, or change in our relationship with, the U.S. federal government would result in a significant decrease in our revenues and operating results.

We have historically derived and are likely to continue to derive a significant portion of our revenues from the U.S. federal government. For the year ended December 31, 2011, revenues under contracts with the U.S. federal government accounted for approximately 27% of our total revenues. Furthermore, federal government revenues increased to approximately 41% in the nine months ended September 30, 2012, primarily as a result of increasing revenues from our RAC contract with CMS. In addition, fees payable by the U.S. federal government are expected to become a larger percentage of our total revenues over the next several years as a result of legislation that has transferred responsibility for all new student loan origination to the Department of Education. The continuation and exercise of renewal options on existing government contracts and any new government contracts are, among other things, contingent upon the availability of adequate funding for the applicable federal government agency. Changes in federal government spending could directly affect our financial performance. For example, the Obama Administration’s proposed budget for the year ending September 30, 2013, included a proposal designed to redirect federal government spending to an alternative federal program by decreasing the amount that GAs are compensated when they rehabilitate defaulted loans. While the Obama Administration’s budget proposal was not approved by Congress, in June 2012, a bill

14

Table of Contents

containing similar provisions reducing the compensation of GAs for rehabilitation of defaulted student loans was subsequently introduced in the U.S. Senate. The loss of business from the U.S. federal government, or significant policy changes or financial pressures within the agencies of the U.S. federal government that we serve would result in a significant decrease in our revenues, which would adversely affect our business, financial condition and results of operations.

Future legislative or regulatory changes affecting the markets in which we operate could impair our business and operations.

The two principal markets in which we provide our recovery services, government-supported student loans and the Medicare program, are a subject of significant legislative and regulatory focus and we cannot anticipate how future changes in government policy may affect our business and operations. For example, SAFRA significantly changed the structure of the government-supported student loan market by assigning responsibility for all new government-supported student loan originations to the Department of Education, rather than originations by private institutions and backed by one of 31 government-supported GAs. This legislation, and any future changes in the legislation and regulations that govern these markets, may require us to adapt our business to the new circumstances and we may be unable to do so in a manner that does not adversely affect our business and operations.

Our business relationship with the Department of Education has accounted for a significant portion of our revenues and will take on increasing importance to our business as a result of SAFRA. Our failure to maintain this relationship would significantly decrease our revenues.

The majority of our historical revenues from the student loan market have come from our relationships with the GAs. As a result of SAFRA, the Department of Education will ultimately become the sole source of revenues in this market, although the GAs will continue to service their existing student loan portfolios for many years to come. As a result, over time, defaults on student loans originated by the Department of Education will predominate and our ability to maintain the revenues we had previously received from a number of GA clients will depend on our relationship with a single client, the Department of Education. While we have 22 years of experience in performing student loan recovery services for the Department of Education, we are one of 17 unrestricted recovery service providers on the current Department of Education contract. In 2011, student loan recovery work for the Department of Education generated revenues of $17.9 million, or approximately 11% of our total revenues. The Department of Education is expected to initiate a contract re-compete process during the first half of 2013. If our relationship with the Department of Education terminates or deteriorates or if the Department of Education, ultimately as the sole holder of defaulted student loans, requires its contractors to agree to less favorable terms, our revenues would significantly decrease, and our business, financial condition and results of operations would be harmed.

We could lose clients as a result of consolidation among the GAs, which would decrease our revenues.

As a result of SAFRA, which terminated the ability of the GAs to originate government-supported student loans, some have speculated that there may be consolidation among the 31 GAs. If GAs that are our clients are combined with GAs with whom we do not have a relationship, we could suffer a loss of business. We currently have relationships with 11 of the 31 GAs and three of our GA clients were each responsible for more than 10% of our total revenues in 2011. The consolidation of our GA clients with others and the failure to provide recovery services to the consolidated entity could decrease our revenues, which could negatively impact our business, financial condition and results of operations.

Our ability to derive revenues under our RAC contract will depend in part on the number and types of potentially improper claims that we are allowed to pursue by CMS, and our results of operations may be harmed if the scope of claims that we are allowed to pursue is limited.

While we are the prime contractor responsible for review of Medicare records for all Part A and Part B claims in our region pursuant to the terms of our RAC contract with CMS, we are not permitted to seek the

15

Table of Contents

recovery of an improper claim unless that particular type of claim has been pre-approved by CMS to ensure compliance with applicable Medicare payment policies, as well as national and local coverage determinations. While the revenues we earn under our contract with CMS are determined primarily by the aggregate volume of Medicare claims in our region and our ability to successfully identify improper payments within these claims, the long-term growth of the revenues we derive under our RAC contract will also depend in part on CMS expanding the scope of potentially improper claims that we are allowed to pursue under our RAC contract. If we are unable to continue to identify improper claims within the types of claims that we are permitted to pursue from time to time or if CMS does not expand the scope of potentially improper claims that we are allowed to pursue, our results of operations could be adversely affected.

Further, the improper claims approved by CMS and identified by us may be challenged by affected parties. For example, in November 2012 the American Hospital Association and four hospitals filed a lawsuit against Kathleen Sebelius, the Secretary of the Department of Health and Human Services. The lawsuit claims, among other things, that CMS is acting improperly in completely denying payment for claims initially made under Medicare Part A (inpatient) that should have been made under Medicare Part B (outpatient), rather than remitting the difference between the Part A and Part B payments. This type of improper claim has accounted for a substantial portion of the claims we have identified under our RAC contract. If healthcare providers are able to limit the scope of improper claims, our revenues may be harmed.

Our results of operations may fluctuate on a quarterly or annual basis and cause volatility in the price of our stock.

Our revenues and operating results could vary significantly from period-to-period and may fail to match our past performance because of a variety of factors, some of which are outside of our control. Any of these factors could cause the price of our common stock to fluctuate. Factors that could contribute to the variability of our operating results include:

| • | the amount of defaulted student loans and other receivables that our clients place with us for recovery; |

| • | the timing of placements of student loans and other receivables which are entirely in the discretion of our clients; |

| • | our ability to successfully identify improper Medicare claims and the number and type of potentially improper claims that CMS authorizes us to pursue under our RAC contract; |

| • | the loss or gain of significant clients or changes in the contingency fee rates or other significant terms of our business arrangements with our significant clients; |

| • | technological and operational issues that may affect our clients and regulatory changes in the markets we service; and |

| • | general industry and macroeconomic conditions. |

For example, a technology system upgrade at the Department of Education has caused fluctuations in our quarterly operating results. This upgrade significantly decreased the volume of student loan placements by the Department of Education to all recovery vendors, including us. As a result, the dollar amount of placements that we received from the Department of Education in the nine months ended September 30, 2012 was 45% lower than in the comparable nine months ended September 30, 2011. While in the fourth quarter of 2012, we and the other recovery vendors have received substantially larger placement volume as a result of the completion of this technology system upgrade, the majority of the revenues from these placements will be delayed because we do not begin to earn rehabilitation revenues from a given placement until at least nine months after receipt of a placement. In addition, for approximately twelve months beginning in September 2011, this technology system upgrade prevented the Department of Education from processing a significant portion of rehabilitated student

16

Table of Contents

loans and accordingly we were not able to recognize a significant amount of the revenues associated with rehabilitation of loans for this client. However, the Department of Education continued to pay us based on invoices submitted and we recorded these cash receipts as deferred revenues on our balance sheet. This led to deferred revenues of $2.5 million as of September 30, 2012.

Further, our claim recovery volume is currently impacted by a system adjustment that is being implemented by CMS for its PIP providers. PIP providers are reimbursed for Medicare claims through different processes than other healthcare providers, and CMS is in the process of making certain system adjustments in order to allow these claims to be processed. Prior to April 2012, we were not permitted to audit Medicare claims for these PIP providers, which we estimate to account for approximately 20% of Medicare claims in our region. The improper payments to PIP providers that we have identified were not processed by CMS from April 2012 until January 2013, when a small portion of such payments began to be processed manually. As a result, we will not recognize any revenues from identified improper payments to PIP providers as of December 31, 2012, but we have incurred expenses related to these claims. We estimate that this delayed our recognition of approximately $6 million in revenues in 2012, although we expect to begin recognizing a portion of these revenues starting in the first quarter of 2013. CMS remains in the process of implementing the necessary changes to its systems that would allow these claims to be processed automatically and allow us to recognize these revenues. While we believe that this delay in automatic processing is temporary, we are uncertain as to when automatic processing will begin and the failure of CMS to process these and future claims on a timely basis will delay our recognition of the revenues until this is resolved. Because our revenues are dependent on many factors, some of which are outside of our control, we may experience significant fluctuations in our results of operations and as a result volatility in our stock price.

Downturns in domestic or global economic conditions and other macroeconomic factors could harm our business and results of operations.

Various macroeconomic factors influence our business and results of operations. These include the volume of student loan originations in the United States, together with tuition costs and student enrollment rates, the default rate of student loan borrowers, which is impacted by domestic and global economic conditions, rates of unemployment and similar factors, and the growth in Medicare expenditures resulting from changes in healthcare costs. Changes in these factors could lead to a reduction in overall recovery rates by our clients, which in turn could adversely affect our business, financial condition and results of operations. In addition, during the global financial crisis beginning in 2008, the market for securitized student loan portfolios was disrupted, resulting in delays in the ability of some GA clients to resell rehabilitated student loans and as a result delaying our ability to recognize revenues from these rehabilitated loans.

We may not be able to maintain or increase our profitability, and our recent financial results may not be indicative of our future financial results.

We may not succeed in maintaining our profitability on a quarterly or annual basis and could incur quarterly or annual losses in future periods. We expect to incur additional operating expenses associated with being a public company and we intend to continue to increase our operating expenses as we grow our business. We also expect to continue to make investments in our proprietary technology platform and hire additional employees and subcontractors as we expand our healthcare recovery and other operations, thus incurring additional expenses. If our revenues do not increase to offset these increases in expenses, our operating results could be adversely affected. Our historical revenues and net income growth rates are not indicative of future growth rates.

We may not be able to manage our growth effectively and our results of operations could be negatively affected.

Our business has expanded significantly, especially in recent years with the expansion of our services in the healthcare market, and we intend to maintain our focus on growth. However, our continued focus on growth

17

Table of Contents

and the expansion of our business may place additional demands on our management, operations and financial resources and will require us to incur additional expenses. We cannot be sure that we will be able to manage our growth effectively. In order to successfully manage our growth, our expenses will increase to recruit, train and manage additional qualified employees and subcontractors and to expand and enhance our administrative infrastructure and continue to improve our management, financial and information systems and controls. If we cannot manage our growth effectively, our expenses may increase and our results of operations could be negatively affected.

A failure of our operating systems or technology infrastructure, or those of our third-party vendors and subcontractors, could disrupt the operation of our business.

A failure of our operating systems or technology infrastructure, or those of our third-party vendors and subcontractors, could disrupt our operations. Our operating systems and technology infrastructure are susceptible to damage or interruption from various causes, including acts of God and other natural disasters, power losses, computer systems failures, Internet and telecommunications or data network failures, operator error, computer viruses, losses of and corruption of data and similar events. The occurrence of any of these events could result in interruptions, delays or cessations in service to our clients, reduce the attractiveness of our recovery services to current or potential clients and adversely impact our financial condition and results of operations. While we have backup systems in many of our operating facilities, an extended outage of utility or network services may harm our ability to operate our business. Further, the situations we plan for and the amount of insurance coverage we maintain for losses as result of failures of our operating systems and infrastructure may not be adequate in any particular case.

If our security measures are breached or fail and unauthorized access is obtained to our clients’ confidential data, our services may be perceived as insecure, the attractiveness of our recovery services to current or potential clients may be reduced, and we may incur significant liabilities.

Our recovery services involve the storage and transmission of confidential information relating to our clients and their customers, including health, financial, credit, payment and other personal or confidential information. Although our data security procedures are designed to protect against unauthorized access to confidential information, our computer systems, software and networks may be vulnerable to unauthorized access and disclosure of our clients’ confidential information. Further, we may not effectively adapt our security measures to evolving security risks, address the security and privacy concerns of existing or potential clients as they change over time, or be compliant with federal, state, and local laws and regulations with respect to securing confidential information. Unauthorized access to confidential information relating to our clients and their customers could lead to reputational damage which could deter our clients and potential clients from selecting our recovery services, or result in termination of contracts with those clients affected by any such breach, regulatory action, and claims against us.

In the event of any unauthorized access to personal or other confidential information, we may be required to expend significant resources to investigate and remediate vulnerabilities in our security procedures, and we may be subject to fines, penalties, litigation costs, and financial losses that are either not insured against or not fully covered through any insurance maintained by us. If one or more of such failures in our security and privacy measures were to occur, our business, financial condition and results of operations could suffer.

Our business may be harmed if we lose members of our management team or other key employees.

We are highly dependent on members of our management team and other key employees and our future success depends in part on our ability to retain these people. Our inability to continue to attract and retain members of our management team and other key employees could adversely affect our business, financial condition and results of operations.

18

Table of Contents

The growth of our healthcare business will require us to hire and retain employees with specialized skills and failure to do so could harm our ability to grow our business.

The growth of our healthcare business will depend in part on our ability to recruit, train and manage additional qualified employees. Our healthcare-related operations require us to hire registered nurses and experts in Medicare coding. Finding, attracting and retaining employees with these skills is a critical component of providing our healthcare-related recovery and audit services, and our inability to staff these operations appropriately represents a risk to our healthcare service offering and associated revenues. An inability to hire qualified personnel, particularly to serve our healthcare clients, may restrain the growth of our business.

We rely on subcontractors to provide services to our clients and the failure of subcontractors to perform as expected could harm our business operations and our relationships with our clients.

We engage subcontractors to provide certain services to our clients. These subcontractors participate to varying degrees in our recovery activities with regards to all of the services we provide. While most of our subcontractors provide specific services to us, we engage one subcontractor to provide all of the audit and recovery services under our contract with CMS within a portion of our region. According to CMS, the geographic area allocated to this subcontractor accounted for approximately 17% of total Medicare spending in our region in 2009. While we believe that we perform appropriate due diligence before we hire subcontractors, our subcontractors may not provide adequate service or otherwise comply with the terms set forth in their agreements. In the event a subcontractor provides deficient performance to one or more of our clients, any such client may reduce the volume of services we are providing under an existing contract or may terminate the relevant contract entirely and we may face claims for breach of contract. Any such disruption in our relations with our clients as a result of services provided by any of our subcontractors could adversely affect our revenues and operating results.

If our software vendors or utility and network providers fail to deliver or perform as expected our business operations could be adversely affected.

Our recovery services depend in part on third-party providers, including software vendors and utility and network providers. Our ability to service our clients depends on these third-party providers meeting our expectations and contractual obligations in a timely and effective manner. Our business could be materially and adversely affected, and we might incur significant additional liabilities, if the services provided by these third-party providers do not meet our expectations or if they terminate or refuse to renew their relationships with us on similar contractual terms.

We are subject to extensive regulations regarding the use and disclosure of confidential personal information and failure to comply with these regulations could cause us to incur liabilities and expenses.

We are subject to a wide array of federal and state laws and regulations regarding the use and disclosure of confidential personal information and security. For example, the federal Health Insurance Portability and Accountability Act of 1996, as amended, or HIPAA, and related state laws subject us to substantial restrictions and requirements with respect to the use and disclosure of the personal health information that we obtain in connection with our audit and recovery services under our contract with CMS and we must establish administrative, physical and technical safeguards to protect the confidentiality of this information. Similar protections extend to the type of personal financial and other information we acquire from our student loan, state tax and federal receivables clients. We are required to notify affected individuals and government agencies of data security breaches involving protected health and certain personally identifiable information. These laws and regulations also require that we develop, implement and maintain written, comprehensive information security programs containing safeguards that are appropriate to protect personally identifiable information or health information against unauthorized access, misuse, destruction or modification. Federal law generally does not preempt state law in the area of protection of personal information, and as a result we must also comply with

19

Table of Contents

state laws and regulations. Regulation of privacy, data use and security requires that we incur significant expenses, which could increase in the future as a result of additional regulations, all of which adversely affects our results of operations. Failure to comply with these laws and regulations can result in penalties and in some cases expose us to civil lawsuits.