Attached files

| file | filename |

|---|---|

| EX-99.1 - PRESS RELEASE ISSUED BY U.S. BANCORP - US BANCORP \DE\ | d466775dex991.htm |

| 8-K - FORM 8-K - US BANCORP \DE\ | d466775d8k.htm |

U.S.

Bancorp 4Q12 Earnings

Conference Call

U.S. Bancorp

4Q12 Earnings

Conference Call

January 16, 2013

Richard K. Davis

Chairman, President and CEO

Andy Cecere

Vice Chairman and CFO

Exhibit 99.2 |

2

Forward-looking Statements and Additional Information

The

following

information

appears

in

accordance

with

the

Private

Securities

Litigation

Reform

Act

of

1995:

This presentation contains forward-looking statements about U.S. Bancorp.

Statements that are not historical or current facts, including statements

about beliefs and expectations, are forward-looking statements and are based on

the information available to, and assumptions and estimates made

by,

management

as

of

the

date

made.

These

forward-looking

statements

cover,

among

other

things,

anticipated

future

revenue

and

expenses

and

the

future

plans

and

prospects

of

U.S.

Bancorp.

Forward-looking

statements

involve

inherent

risks

and

uncertainties,

and

important

factors could cause actual results to differ materially from those

anticipated. Global and domestic economies could fail to recover from the recent

economic downturn or could experience another severe contraction, which could

adversely affect U.S. Bancorp’s revenues and the values of its assets

and liabilities. Global financial markets could experience a recurrence of significant turbulence, which could reduce the availability of

funding to certain financial institutions and lead to a tightening of credit, a

reduction of business activity, and increased market volatility. Continued

stress in the commercial real estate markets, as well as a delay

or failure of recovery in the residential real estate markets, could cause

additional credit losses and deterioration in asset values. In

addition, U.S. Bancorp’s business and financial performance is likely to be negatively impacted

by effects of recently enacted and future legislation and regulation. U.S.

Bancorp’s results could also be adversely affected by continued

deterioration

in

general

business

and

economic

conditions;

changes

in

interest

rates;

deterioration

in

the

credit

quality

of

its

loan

portfolios

or

in

the

value of the collateral securing those loans; deterioration in the value of

securities held in its investment securities portfolio; legal and regulatory

developments; increased competition from both banks and non-banks; changes in

customer behavior and preferences; effects of mergers and acquisitions and

related integration; effects of critical accounting policies and judgments; and management’s ability to effectively manage credit

risk, residual value risk, market risk, operational risk, interest rate risk and

liquidity risk. For discussion of these and other risks that may cause actual

results to differ from expectations, refer to U.S. Bancorp’s Annual Report on

Form 10-K for the year ended December 31, 2011, on file with the Securities and

Exchange Commission, including the sections entitled “Risk

Factors”

and

“Corporate

Risk

Profile”

contained

in

Exhibit

13,

and

all

subsequent

filings

with

the

Securities

and

Exchange

Commission

under

Sections 13(a), 13(c), 14 or 15(d) of the Securities Exchange Act of 1934.

Forward-looking statements speak only as of the date they are made, and

U.S. Bancorp undertakes no obligation to update them in light of new information or future events.

This

presentation

includes

non-GAAP

financial

measures

to

describe

U.S.

Bancorp’s

performance.

The

reconciliations

of

those

measures

to

GAAP

measures

are

provided

within

or

in

the

appendix

of

the

presentation.

These

disclosures

should

not

be

viewed

as

a

substitute

for

operating

results

determined in accordance with GAAP, nor are they necessarily comparable to

non-GAAP performance measures that may be presented by other

companies. |

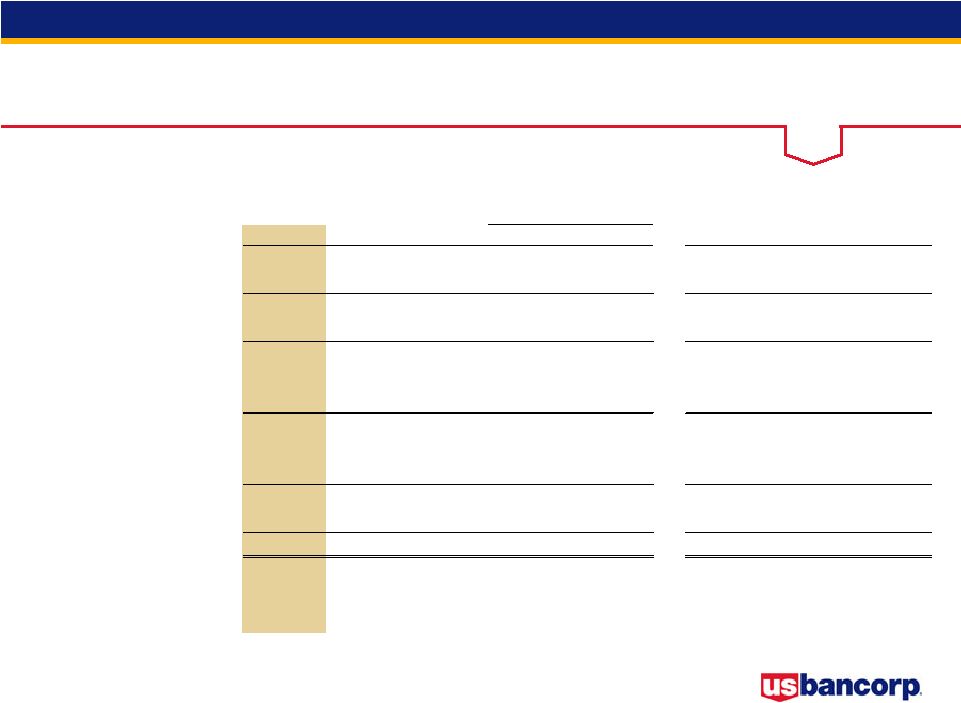

3

4Q12 Earnings

Conference Call

2012 Full Year Highlights

Record net income of $5.6 billion; $2.84 per diluted common share

Record total net revenue of $20.3 billion, up 6.2% vs. 2011

•

Net interest income growth of 6.0% vs. 2011

•

Noninterest income growth of 6.4% vs. 2011

Industry-leading profitability measures, including ROA of 1.65%, ROCE of 16.2%

and efficiency ratio of 51.5%

Positive operating leverage

Average loan growth of 6.9% vs. 2011

Strong average deposit growth of 10.6% vs. 2011

Net

charge-offs

declined

26.2%

vs.

2011

and

nonperforming

assets

(excluding

covered

assets) declined 18.9% vs. 2011

Capital generation continues to strengthen capital position

•

Tier 1 common equity ratio of 9.0% vs. 8.6% in 2011

•

Repurchased 59 million shares of common stock during 2012

•

In total, returned $3.4 billion of our earnings in 2012 to shareholders

|

4

4Q12 Earnings

Conference Call

4Q12 Highlights

Net income of $1.4 billion; $0.72 per diluted common share

4Q12 results included an $80 million expense accrual for a mortgage

foreclosure-related regulatory settlement; reduced diluted EPS by

$0.03 4Q11 results included a $263 million merchant settlement gain and a

$130 million expense accrual related to mortgage servicing matters;

increased EPS by $0.05

Net revenue of $5.1 billion, up 0.2% vs. 4Q11 (5.6% excluding 4Q11

merchant settlement gain) Positive operating leverage on a

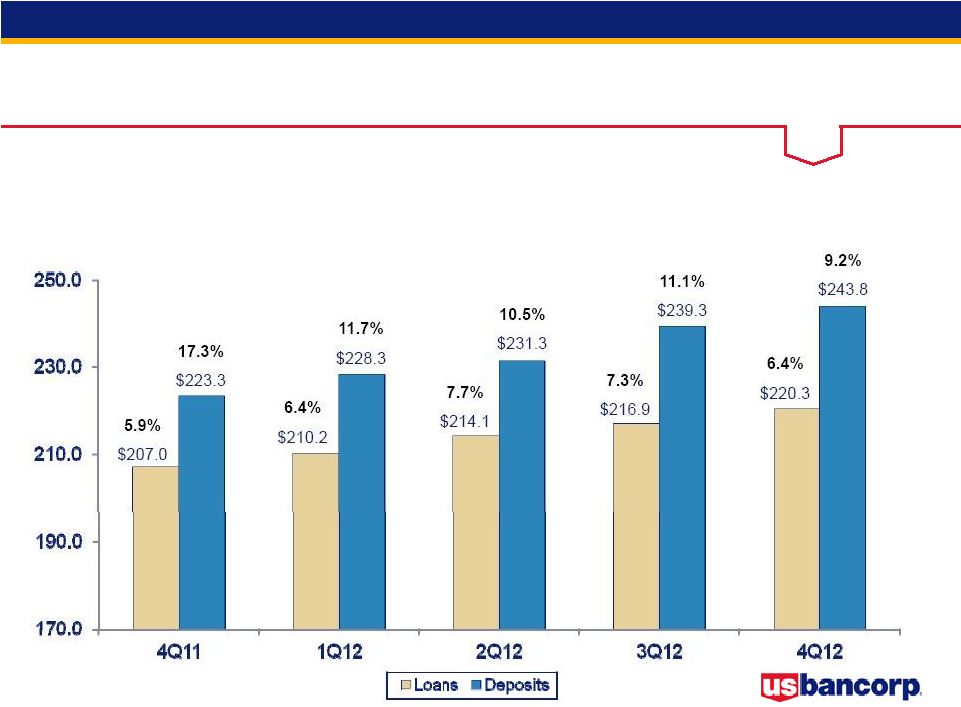

year-over-year basis Average loan growth of 6.4% vs. 4Q11 and average

loan growth of 1.5% vs. 3Q12 Strong average deposit growth of 9.2% vs. 4Q11

and 1.9% vs. 3Q12 Net charge-offs declined 13.0% vs. 3Q12 (3Q12 included

$54 million of incremental charge-offs due to a regulatory

clarification) Nonperforming assets declined 5.8% vs. 3Q12 (4.6% excluding

covered assets) Capital generation continues to reinforce capital

position •

Tier 1 common equity ratio of approximately 8.1% using proposed rules for Basel

III standardized approach released June 2012

•

Tier 1 common equity ratio of 9.0%; Tier 1 capital ratio of 10.8%

•

Repurchased 13 million shares of common stock during 4Q12

|

5

4Q12 Earnings

Conference Call

Performance Ratios

ROCE and ROA

Efficiency Ratio and

Net Interest Margin

Return on Avg Common Equity

Return on Avg Assets

Efficiency Ratio

Net Interest Margin

Efficiency

ratio

computed

as

noninterest

expense

divided

by

the

sum

of

net

interest

income

on

a

taxable-equivalent

basis

and

noninterest

income

excluding

securities

gains

(losses)

net |

6

4Q12 Earnings

Conference Call

* Gain on merchant processing agreement settlement

Taxable-equivalent basis

Revenue Growth

$ in millions |

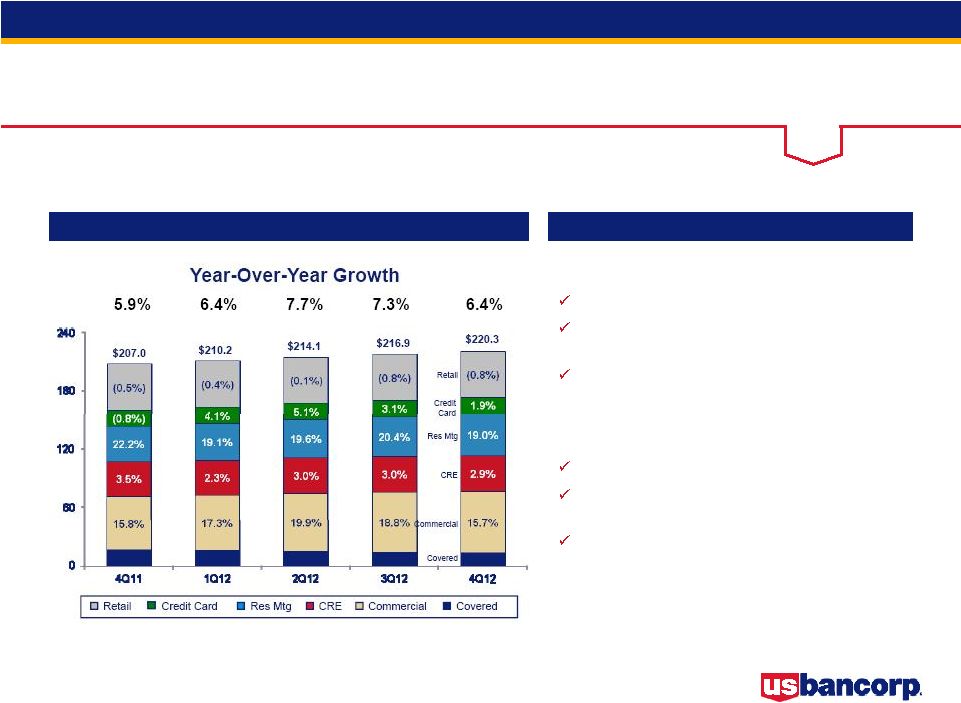

7

4Q12 Earnings

Conference Call

Loan and Deposit Growth

Average Balances

Year-Over-Year Growth

$ in billions |

8

4Q12 Earnings

Conference Call

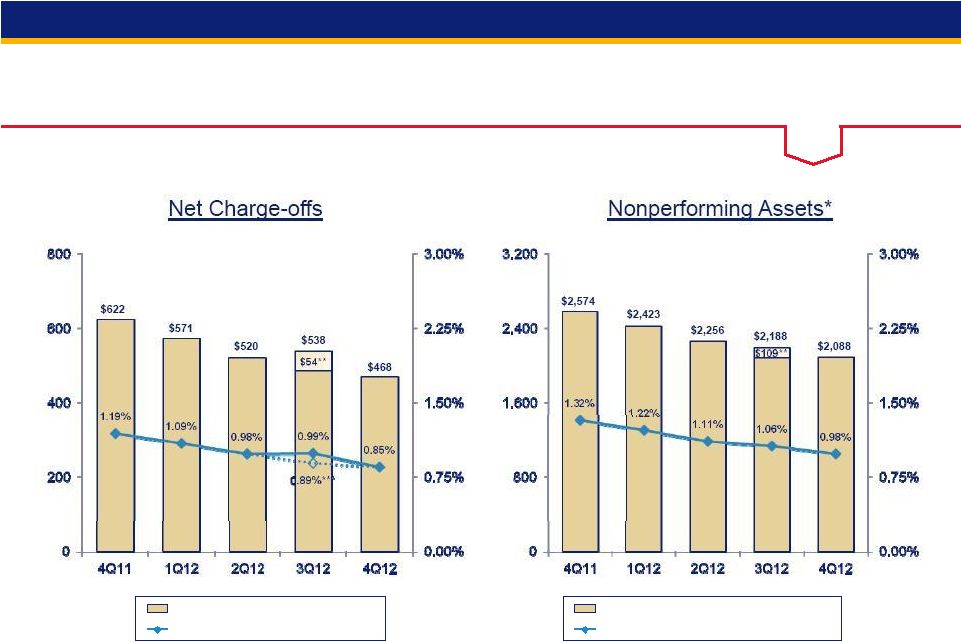

Credit Quality

*

Excluding

Covered

Assets

(assets

subject

to

loss

sharing

agreements

with

FDIC)

**

Related

to

a

regulatory

clarification

in

the

treatment

of

residential

mortgage

and

other

consumer

loans

to

borrowers

who

have

exited

bankruptcy

but

continue

to

make

payments

on

their

loans

***

Excluding

$54

million

of

incremental

charge-offs

$ in millions

Net Charge-offs (Left Scale)

NCOs to Avg Loans (Right Scale)

Nonperforming Assets (Left Scale)

NPAs to Loans plus ORE (Right Scale) |

9

4Q12 Earnings

Conference Call

FY

FY

4Q12

3Q12

4Q11

vs 3Q12

vs 4Q11

2012

2011

% B/(W)

Net Interest Income

2,783

$

2,783

$

2,673

$

-

4.1

10,969

$

10,348

$

6.0

Noninterest Income

2,329

2,396

2,431

(2.8)

(4.2)

9,319

8,760

6.4

Total Revenue

5,112

5,179

5,104

(1.3)

0.2

20,288

19,108

6.2

Noninterest Expense

2,686

2,609

2,696

(3.0)

0.4

10,456

9,911

(5.5)

Operating Income

2,426

2,570

2,408

(5.6)

0.7

9,832

9,197

6.9

Net Charge-offs

468

538

622

13.0

24.8

2,097

2,843

26.2

Excess Provision

(25)

(50)

(125)

--

--

(215)

(500)

--

Income before Taxes

1,983

2,082

1,911

(4.8)

3.8

7,950

6,854

16.0

Applicable Income Taxes

608

650

583

6.5

(4.3)

2,460

2,066

(19.1)

Noncontrolling Interests

45

42

22

7.1

104.5

157

84

86.9

Net Income

1,420

1,474

1,350

(3.7)

5.2

5,647

4,872

15.9

Preferred Dividends/Other

71

70

36

(1.4)

(97.2)

264

151

(74.8)

NI to Common

1,349

$

1,404

$

1,314

$

(3.9)

2.7

5,383

$

4,721

$

14.0

Diluted EPS

0.72

$

0.74

$

0.69

$

(2.7)

4.3

2.84

$

2.46

$

15.4

Average Diluted Shares

1,880

1,897

1,911

0.9

1.6

1,896

1,923

1.4

% B/(W)

Earnings Summary

$ in millions, except per-share data

Taxable-equivalent basis |

10

4Q12 Earnings

Conference Call

Notable Items

$ in millions

4Q12

4Q11

Revenue Items

Merchant processing agreement settlement

-

$

263

$

Expense Items

Mortgage servicing matters

80

130

|

11

4Q12 Earnings

Conference Call

4Q12 Results -

Key Drivers

vs. 4Q11

Net Revenue growth of 0.2% (5.6% excluding notable items)

•

Net

interest

income

growth

of

4.1%;

net

interest

margin

of

3.55%

vs.

3.60%

in

4Q11

•

Noninterest income decline of 4.2% (7.4% increase excluding notable items)

Noninterest expense decline of 0.4% (1.6% increase excluding notable items)

Provision for credit losses lower by $54 million

•

Net charge-offs lower by $154 million

•

Provision lower than NCOs by $25 million vs. $125 million in 4Q11

vs. 3Q12

Net Revenue decline of 1.3%

•

Net

interest

income

growth

of

0.0%;

net

interest

margin

of

3.55%

vs.

3.59%

in

3Q12

•

Noninterest income decline of 2.8%

Noninterest expense growth of 3.0% (0.1% decline excluding notable items)

Provision for credit losses lower by $45 million

•

Net charge-offs lower by $70 million

•

Provision lower than NCOs by $25 million vs. $50 million in 3Q12

|

12

4Q12 Earnings

Conference Call

4Q12

3Q12

2Q12

1Q12

4Q11

Shareholders' equity

39.0

$

38.7

$

37.8

$

35.9

$

34.0

$

Tier 1 capital

31.2

30.8

30.0

30.0

29.2

Total risk-based capital

37.8

37.6

36.4

36.4

36.1

Tier 1 common equity ratio

9.0%

9.0%

8.8%

8.7%

8.6%

Tier 1 capital ratio

10.8%

10.9%

10.7%

10.9%

10.8%

Total risk-based capital ratio

13.1%

13.3%

13.0%

13.3%

13.3%

Leverage ratio

9.2%

9.2%

9.1%

9.2%

9.1%

Tangible common equity ratio

7.2%

7.2%

6.9%

6.9%

6.6%

Tangible common equity as a % of RWA

8.6%

8.8%

8.5%

8.3%

8.1%

Basel III

Tier 1 common equity ratio using Basel III

proposals published prior to June 2012

-

-

-

8.4%

8.2%

Tier 1 common equity ratio approximated

using proposed rules for the Basel III

standardized approach released June 2012

8.1%

8.2%

7.9%

-

-

Capital Position

$ in billions

RWA = risk-weighted assets |

13

4Q12 Earnings

Conference Call

Mortgage Repurchase

Mortgages Repurchased and Make-whole Payments

Mortgage Representation and Warranties Reserve

$ in millions

4Q12

3Q12

2Q12

1Q12

4Q11

Beginning Reserve

$220

$216

$202

$160

$162

Net Realized Losses

(32)

(32)

(31)

(25)

(31)

Additions to Reserve

52

36

45

67

29

Ending Reserve

$240

$220

$216

$202

$160

Mortgages

repurchased

and make-whole

payments

$57

$58

$58

$55

$61

Repurchase activity lower than

peers due to:

•

Conservative credit and

underwriting culture

•

Disciplined origination process -

primarily conforming

loans

(

95% sold to GSEs)

Do not participate in private

placement securitization market

Outstanding repurchase and

make-whole requests balance

= $131 million

Repurchase requests expected to

remain relatively stable over next

few quarters |

continues

continues

Momentum

Momentum |

15

4Q12 Earnings

Conference Call

Appendix |

16

4Q12 Earnings

Conference Call

Average Loans

Average Loans

Key Points

$ in billions

vs. 4Q11

Average total loans grew over $13 billion, or 6.4%

Average total loans, excluding covered loans,

were higher by 8.6%

Average total commercial loans increased $8.7

billion, or 15.7%; average residential mortgage

loans increased $6.9 billion, or 19.0%

vs. 3Q12

Average total loans grew by $3.4 billion, or 1.5%

Average total loans, excluding covered loans,

were higher by 2.0%

Average total commercial loans increased $1.7

billion, or 2.8%; average residential mortgage

loans increased $2.2 billion, or 5.3% |

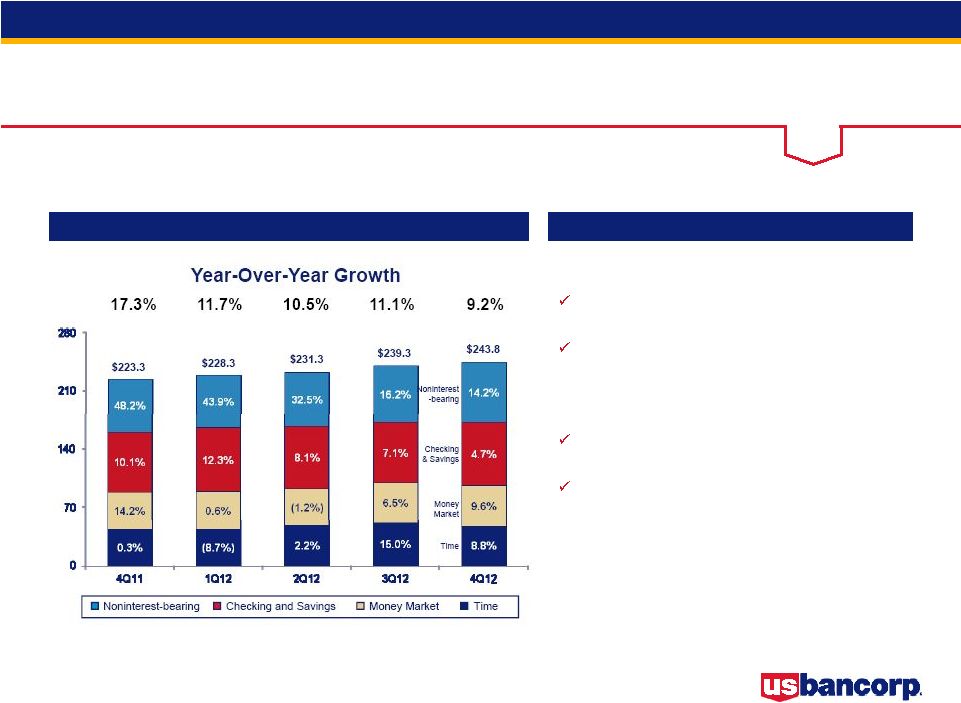

17

4Q12 Earnings

Conference Call

Average Deposits

Average Deposits

Key Points

$ in billions

vs. 4Q11

Average total deposits increased by $20.5

billion, or 9.2%

Average low cost deposits (NIB, interest

checking, money market and savings)

increased by $16.8 billion, or 9.3%

vs. 3Q12

Average total deposits increased by $4.5

billion, or 1.9%

Average low cost deposits increased by $9.0

billion, or 4.8% |

18

4Q12 Earnings

Conference Call

Net Interest Income

Net Interest Income

Key Points

$ in millions

Taxable-equivalent basis

vs. 4Q11

Average earning assets grew by $17.1 billion,

or 5.8%

Net interest margin lower by 5 bp (3.55% vs.

3.60%) driven by:

•

Higher balances in lower yielding investment

securities and lower loan rates

•

Partially offset by lower rates on deposits and long-

term debt and a reduction in cash balances held at

the Federal Reserve

vs. 3Q12

Average earning assets grew by $3.3 billion,

or 1.1%

Net interest margin lower by 4 bp (3.55% vs.

3.59%) driven by:

•

Reduction in the yield on the investment securities

portfolio and lower loan rates |

19

4Q12 Earnings

Conference Call

Noninterest Income

Noninterest Income

Key Points

$ in millions

Payments = credit and debit card revenue, corporate payment products revenue and

merchant processing; Service charges = deposit service charges, treasury

management fees and ATM processing services vs. 4Q11

Noninterest income declined by $102 million, or

4.2%, driven by:

•

Lower other income due to the merchant settlement gain as well

as a gain related to the Company’s investment in Visa, both of

which were recorded in 4Q11

•

Lower merchant processing revenue (6.3% decline) due to rates

and the 4Q11 reversal of an accrual for a terminated revenue

sharing agreement and lower ATM processing services revenue

(25.2% decline) due to a 1Q12 classification change

•

Mortgage banking revenue increase of $173 million

•

Higher trust and investment management fees (12.7% increase)

•

Higher credit and debit card revenue (4.8% increase) and

corporate payment revenue (4.1% increase)

vs. 3Q12

Noninterest income declined by $67 million, or 2.8%,

driven by:

•

Mortgage banking revenue decrease of $43 million

•

Lower other income due to the net impact of the gain on sale of a

credit card portfolio and the charge related to an investment under

the equity method of accounting, both of which were recorded in

3Q12

•

Lower corporate payment revenue (11.4% decline) due to

seasonally lower volumes

•

Higher credit and debit card revenue (13.6% increase) principally

due to seasonally higher sales and prepaid card fees and trust

and investment management fees (4.2% increase) due to

seasonally higher billing income and business expansion

4Q11

1Q12

2Q12

3Q12

4Q12

Non-operating gains

263

$

-

$

-

$

-

$

-

$

Total

263

$

-

$

-

$

-

$

-

$

Notable Noninterest Income Items |

20

4Q12 Earnings

Conference Call

Noninterest Expense

Noninterest Expense

Key Points

$ in millions

vs. 4Q11

Noninterest expense was lower by $10 million, or

0.4%, driven by:

•

Lower other expense due to the $130 million mortgage-

servicing related expense accrual recorded in 4Q11 partially

offset by the $80 million accrual for a mortgage foreclosure-

related regulatory settlement in the current quarter, as well as

declines in FDIC insurance expense and other real estate

owned costs

•

Lower net occupancy and equipment (6.0% decline)

principally reflecting the change in classification of ATM

surcharge revenue passed through to others

•

Lower marketing and business development (8.0% decline)

due to the timing of charitable contributions

•

Higher professional services (26.7% increase) principally due

to mortgage servicing review-related projects

•

Higher compensation (2.5% increase) and employee benefits

(14.4% increase)

vs. 3Q12

Noninterest expense was higher by $77 million, or

3.0%, driven by:

•

Higher other expense due to the mortgage foreclosure-related

regulatory settlement accrual and higher costs related to

investments in affordable housing and other tax-advantaged

projects, partially offset by lower litigation and insurance-

related costs

•

Higher professional services expense (15.3% increase) due to

mortgage servicing review-related projects

All Other

4Q11

1Q12

2Q12

3Q12

4Q12

Mortgage servicing matters

130

$

-

$

-

$

-

$

80

$

Total

130

$

-

$

-

$

-

$

80

$

Notable Noninterest Expense Items |

21

4Q12 Earnings

Conference Call

Credit Quality

-

Commercial Loans

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Strong

new

lending

activity

resulted

in

3.3%

linked

quarter

loan

growth

and

18.4%

year-over-year

growth even though utilization rates remained at historically low levels

Nonperforming loans and net charge-offs continued to improve

year-over-year and on a linked quarter basis

Increases

in

early

and

late

stage

delinquencies

primarily

relate

to

government

payment

products

4Q11

3Q12

4Q12

Average Loans

$49,437

$56,655

$58,552

30-89 Delinquencies

0.48%

0.29%

0.48%

90+ Delinquencies

0.09%

0.07%

0.10%

Nonperforming Loans

0.55%

0.23%

0.18%

$ in millions

Revolving Line Utilization Trend |

22

4Q12 Earnings

Conference Call

Credit Quality

-

Commercial Leases

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Net charge-offs and nonperforming loans continue to improve both on a linked

quarter and year- over-year basis

Delinquencies remain stable

4Q11

3Q12

4Q12

Average Loans

$5,834

$5,537

$5,377

30-89 Delinquencies

0.96%

0.93%

0.89%

90+ Delinquencies

0.00%

0.02%

0.00%

Nonperforming Loans

0.54%

0.35%

0.29%

$ in millions |

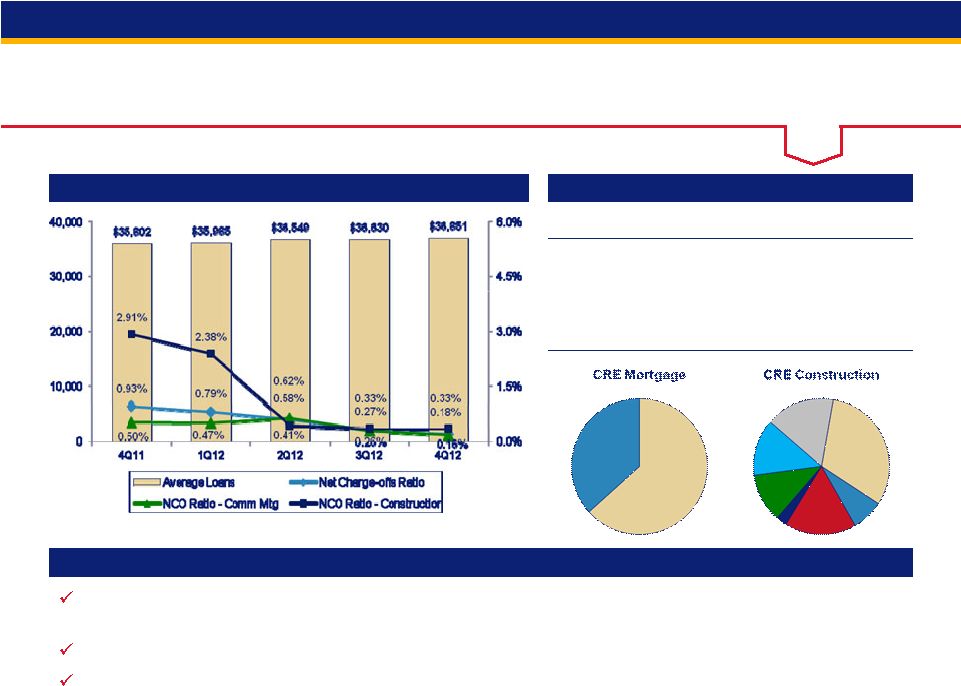

23

4Q12 Earnings

Conference Call

Credit Quality

-

Commercial Real Estate

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Net charge-off ratio of 0.18%, down from 0.27% on a linked quarter basis and

from the 2Q10 peak of 2.67%

Late

stage

delinquencies

continue

to

decline

on

a

linked

quarter

basis,

ending

at

0.02%

Nonperforming loans improved on both a linked quarter and on a

year-over-year basis, ending at 1.48% 4Q11

3Q12

4Q12

Average Loans

$35,802

$36,630

$36,851

30-89 Delinquencies

0.38%

0.18%

0.43%

90+ Delinquencies

0.04%

0.03%

0.02%

Nonperforming Loans

2.51%

1.71%

1.48%

Performing TDRs

537

583

531

$ in millions

Investor

$19,487

Owner

Occupied

$11,275

Multi-family

$1,914

Retail

$460

Residential

Construction

$1,036

Condo

Construction

$157

A&D

Construction

$704

Office

$818

Other

$1,000 |

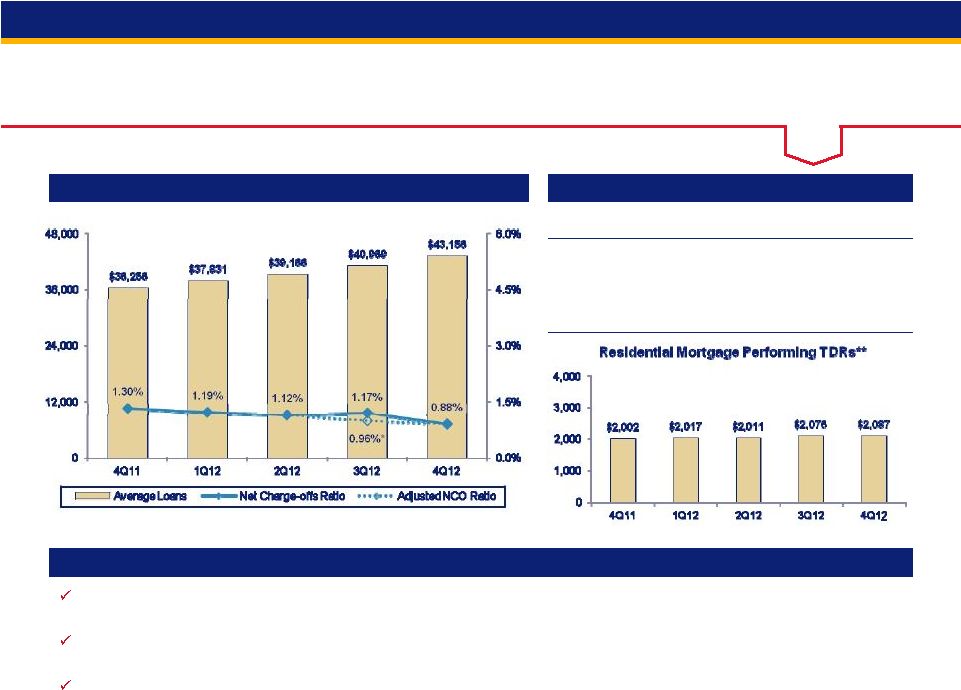

24

4Q12 Earnings

Conference Call

Credit Quality

-

Residential Mortgage

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Strong growth in high quality originations (weighted average FICO 764, weighted

average LTV 65%) as average loans increased 5.3% over 3Q12, driven by demand

for refinancing Over 70% of the balances have been originated since the

beginning of 2009, the origination quality metrics and performance to date

have significantly outperformed prior vintages with similar seasoning

Delinquencies and nonperforming loans continue to decline as housing values

improve 4Q11

3Q12

4Q12

Average Loans

$36,256

$40,969

$43,156

30-89 Delinquencies

1.09%

0.93%

0.79%

90+ Delinquencies

0.98%

0.72%

0.64%

Nonperforming Loans

1.75%

1.81%

1.50%

$ in millions

** Excludes GNMA loans, whose repayments are insured by the FHA or guaranteed by

the Department of VA ($1,778 million 4Q12) *

Excluding

$22

million

related

to

a

regulatory

clarification

in

the

treatment

of

loans

to

borrowerswho

have

exited

bankruptcy

but

continue

to

make

payments

on

their

loans |

25

4Q12 Earnings

Conference Call

4Q11

3Q12

4Q12

Average Loans

$16,271

$16,551

$16,588

30-89 Delinquencies

1.37%

1.41%

1.33%

90+ Delinquencies

1.36%

1.18%

1.27%

Nonperforming Loans

1.29%

0.99%

0.85%

Credit Quality -

Credit Card

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Net charge-offs continue to remain low

Late state delinquencies increased due to normal seasonal patterns

Nonperforming loans have decreased for six consecutive quarters

$ in millions

* Excluding portfolio purchases where the acquired loans were recorded at fair

value at the purchase date |

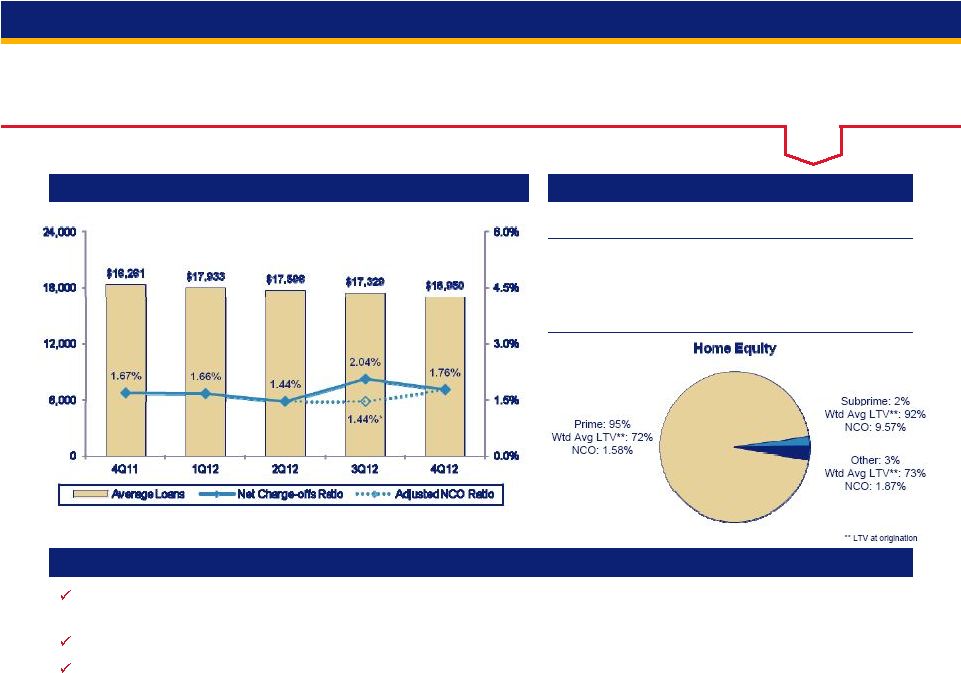

26

4Q12 Earnings

Conference Call

Credit Quality -

Home Equity

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

High-quality originations (weighted average FICO 763, weighted average CLTV

71%) originated primarily through the retail branch network to existing bank

customers on their primary residence Early and late stage delinquencies have

improved year-over-year and on a linked quarter basis Net charge off

dollars are down year-over-year, however, the net charge off ratio has increased due to declining

loan balances

4Q11

3Q12

4Q12

Average Loans

$18,281

$17,329

$16,950

30-89 Delinquencies

0.90%

0.81%

0.76%

90+ Delinquencies

0.73%

0.32%

0.30%

Nonperforming Loans

0.22%

1.05%

1.13%

$ in millions

*

Excluding

$26

million

related

to

a

regulatory

clarification

in

the

treatment

of

loans

to

borrowerswho

have

exited

bankruptcy

but

continue

to

make

payments

on

their

loans |

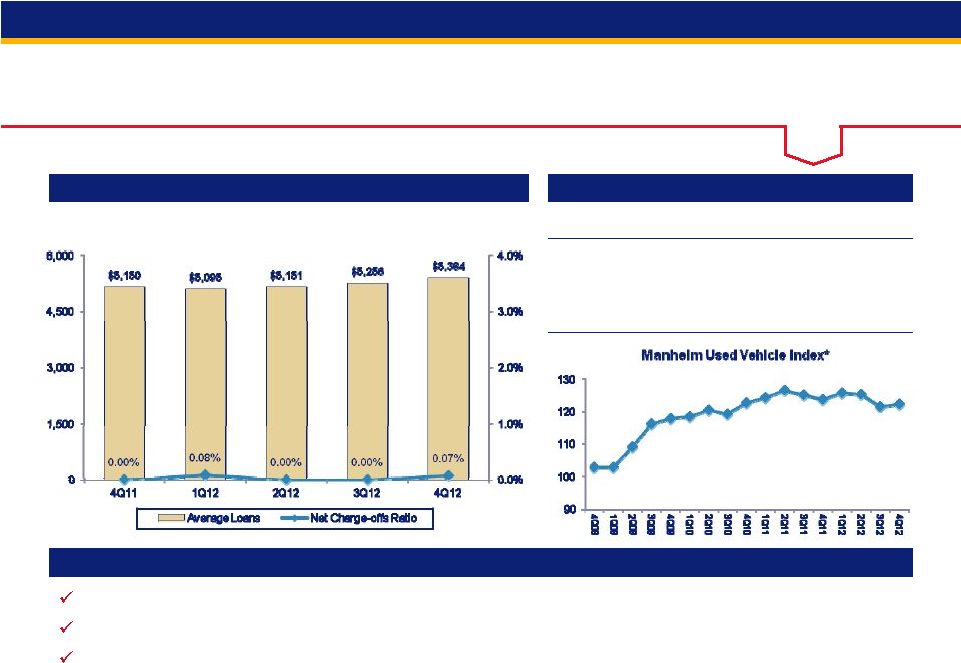

27

4Q12 Earnings

Conference Call

Credit Quality -

Retail Leasing

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

High-quality originations (weighted average FICO 772)

Retail leasing delinquencies have stabilized at very low levels

Strong used auto values continued to contribute to historically low net

charge-offs 4Q11

3Q12

4Q12

Average Loans

$5,150

$5,256

$5,384

30-89 Delinquencies

0.19%

0.17%

0.22%

90+ Delinquencies

0.02%

0.02%

0.02%

Nonperforming Loans

0.00%

0.02%

0.02%

$ in millions

*

Manheim

Used

Vehicle

Value

Index

source:

www.manheimconsulting.com,

January

1995

=

100,

quarter

value

=

average

monthly

ending

value |

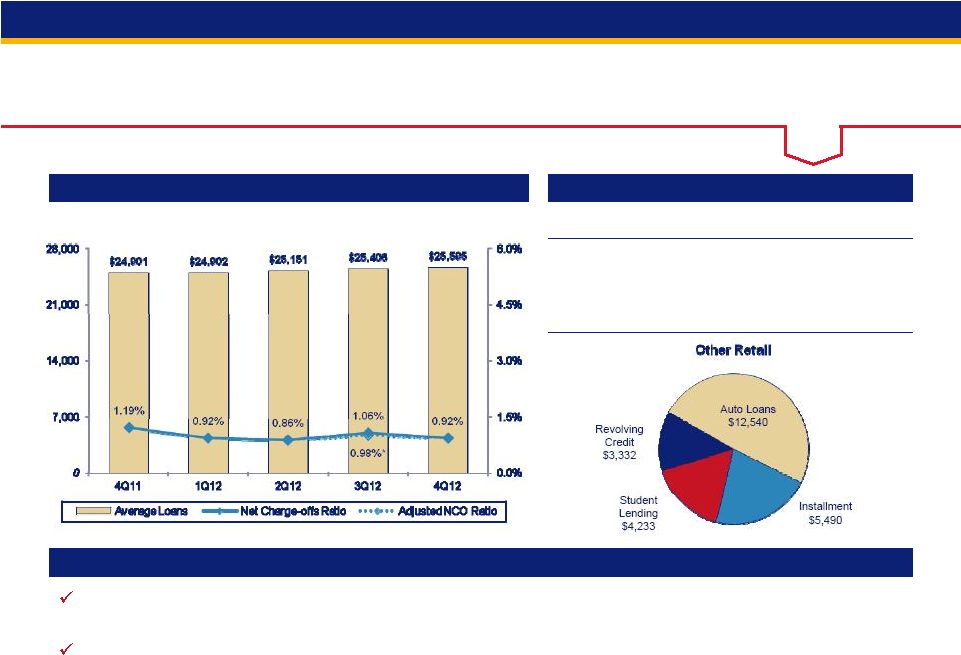

28

4Q12 Earnings

Conference Call

Credit Quality -

Other Retail

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Average balances increased modestly year-over-year, growth in Auto Loans

(9.2%) more than offset declines in Student Lending loan balances

Delinquencies and nonperforming loans remain stable and at very low levels

4Q11

3Q12

4Q12

Average Loans

$24,901

$25,406

$25,595

30-89 Delinquencies

0.68%

0.59%

0.59%

90+ Delinquencies

0.20%

0.16%

0.17%

Nonperforming Loans

0.11%

0.12%

0.11%

$ in millions

* Excluding $5 million related to a regulatory clarification in the treatment of

loans to borrowers who have exited bankruptcy but continue to make payments on their loans |

29

4Q12 Earnings

Conference Call

Non-GAAP Financial Measures

$ in millions

4Q12

3Q12

2Q12

1Q12

4Q11

Total equity

40,267

$

39,825

$

38,874

$

36,914

$

34,971

$

Preferred stock

(4,769)

(4,769)

(4,769)

(3,694)

(2,606)

Noncontrolling interests

(1,269)

(1,164)

(1,082)

(1,014)

(993)

Goodwill (net of deferred tax liability)

(8,351)

(8,194)

(8,205)

(8,233)

(8,239)

Intangible assets (exclude mortgage servicing rights)

(1,006)

(980)

(1,118)

(1,182)

(1,217)

Tangible common equity (a)

24,872

24,718

23,700

22,791

21,916

Tier 1 capital, determined in accordance with prescribed regulatory

requirements using Basel I definition 31,203

30,766

30,044

29,976

29,173

Trust preferred securities

-

-

-

(1,800)

(2,675)

Preferred stock

(4,769)

(4,769)

(4,769)

(3,694)

(2,606)

Noncontrolling interests, less preferred stock not eligible for Tier I

capital (685)

(685)

(685)

(686)

(687)

Tier 1 common equity using Basel I definition (b)

25,749

25,312

24,590

23,796

23,205

Tangible common equity (as calculated above)

22,791

21,916

Adjustments

1

434

450

Tier 1 common equity using Basel III proposals published prior to June 2012

(c) 23,225

22,366

Tangible common equity (as calculated above)

24,872

24,718

23,700

Adjustments

2

126

157

153

Tier 1 common equity approximated using proposed rules for the Basel III

standardized approach released June 2012 (d) 24,998

24,875

23,853

Total assets

353,855

352,253

353,136

340,762

340,122

Goodwill (net of deferred tax liability)

(8,351)

(8,194)

(8,205)

(8,233)

(8,239)

Intangible assets (exclude mortgage servicing rights)

(1,006)

(980)

(1,118)

(1,182)

(1,217)

Tangible assets (e)

344,498

343,079

343,813

331,347

330,666

Risk-weighted assets, determined in accordance with prescribed

regulatory requirements using Basel I definition (f) 287,611

282,033

279,972

274,847

271,333

Risk-weighted assets using Basel III proposals published prior to June

2012 (g) -

-

-

277,856

274,351

Risk-weighted assets, determined in accordance with prescribed

regulatory requirements using Basel I definition 287,611

282,033

279,972

Adjustments3

21,233

22,167

23,240

Risk-weighted assets approximated using proposed rules for the Basel III

standardized approach released June 2012 (h) 308,844

304,200

303,212

Ratios

Tangible common equity to tangible assets (a)/(e)

7.2%

7.2%

6.9%

6.9%

6.6%

Tangible common equity to risk-weighted assets using Basel I definition

(a)/(f) 8.6%

8.8%

8.5%

8.3%

8.1%

Tier 1 common equity to risk-weighted assets using Basel I definition

(b)/(f) 9.0%

9.0%

8.8%

8.7%

8.6%

Tier 1 common equity to risk-weighted assets using Basel III proposals

published prior to June 2012 (c)/(g) -

-

-

8.4%

8.2%

Tier 1 common equity to risk-weighted assets approximated using proposed

rules for the Basel III standardized approach released June 2012 (d)/(h)

8.1%

8.2%

7.9%

-

-

4Q12 risk-weighted assets are preliminary data, subject to change prior

to filings with applicable regulatory agencies

1

Principally net losses on cash flow hedges included in accumulated other

comprehensive income 2

Includes net losses on cash flow hedges included in accumulated other

comprehensive income, unrealized losses on securities transferred from available-for-sale to held-to-maturity included in accumulated

other comprehensive income and disallowed mortgage servicing rights

3

Includes higher risk-weighting for residential mortgages, unfunded loan

commitments, investment securities and purchased mortgage servicing rights, and other adjustments |

U.S.

Bancorp 4Q12 Earnings

Conference Call

U.S. Bancorp

4Q12 Earnings

Conference Call

January 16, 2013 |