Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - NOVANTA INC | d467865d8k.htm |

Investor Presentation

Investor Presentation

January 2013

January 2013

Exhibit 99.1 |

Factors affecting future performance…

Factors affecting future performance…

…and use of Non-GAAP financial measures

…and use of Non-GAAP financial measures

Forward-Looking Statements

Non-GAAP Measurement

Discontinued Operations

The statements in this presentation that relate to guidance, pro forma presentations, future plans,

goals, business opportunities, events or performance are forward-looking statements that

involve risks and uncertainties, including risks associated with business and economic

conditions, failure to achieve expected benefits of the NDS acquisition, failure to comply with

Food and Drug Administration regulations, customer and/or supplier contract cancellations, manufacturing

risks, competitive factors, ability to successfully introduce new products, uncertainties pertaining to

customer orders, demand for products and services, growth and development of markets for the

Company's products and services, and other risks identified in our filings made with the

Securities and Exchange Commission, including, most recently, our Form 10-K for the year

ended December 31, 2011. Actual results, events and performance may differ materially. Readers are

cautioned not to place undue reliance on these forward-looking statements, which speak only as of

the date of this presentation. The Company disclaims any obligation to update these

forward-looking statements as a result of developments occurring after the date of this

presentation. Readers are encouraged to refer to the risk disclosures described in the

Company’s Form 10-K for the year ended December 31, 2011 and subsequent filings with the SEC, as

applicable. Please see “Safe Harbor and Forward-Looking Information” in the Appendix

to this presentation for more information.

The Company’s statements regarding its adjusted EBITDA and net debt are non-GAAP financial

measures. Please see “Use of Non-GAAP Financial Measures” and the subsequent slides

in the Appendix to this presentation for the reasons we use these measures, a reconciliation of

these measures to the most directly comparable GAAP measures and other information relating to

these measures. The Company neither updates nor confirms any guidance regarding the future operating results of the

Company which may have been given prior to this presentation.

In June 2012, the Company committed to a plan for the sale of its Semiconductor Systems and Laser

Systems businesses. As a result, the Company began accounting for these businesses as

discontinued operations beginning in the second quarter of 2012. Unless otherwise noted, all

financial results in this presentation are GAAP measures for continuing operations. |

We

are a leading supplier… …of precision motion and laser

technology Expertise to Drive Results

Capabilities to Innovate & Grow

Positioned in Growth Segments

Global Presence and Reach

•

Leading provider of precision laser, optical and motion control technology

•

Founded

in

1968,

headquartered

in

Bedford,

MA

-

major

presence

in

North

America,

Europe, and Asia-Pacific

•

$271M in revenue and $43M in Adjusted EBITDA (LTM ending 9/30/12)

•

Approximately 1,200 employees for continuing operations

•

Trade on NASDAQ (GSIG)

Leading Technology Franchises |

Our

aspirations… Focus growth efforts on building out

key

platforms

(organic

and

M&A

Improve mix (growth, volatility) –

more

Medical,

less

Semiconductor

Simplify footprint and infrastructure

Organic growth mid to high

single digits

>20% Adj. EBITDA margins

Long term shareholder returns

above peer average

A leading provider of precision photonic and

motion technologies for OEM’s in demanding

markets –

delivering attractive shareholder

returns through sustained profitable growth

Strategic Priorities

Performance Goals

Strategic Vision

)

…are

clear

and

achievable |

At

year end… …we were midstream in our transformation

Revenue

Revenue

Growth

Growth

Potential

Potential

Adj. EBITDA**

Adj. EBITDA**

Value Chain

Value Chain

Focus

Focus

Structure

Structure

Mix

Mix

Growth

Growth

Strategy

Strategy

Performance

Performance

Focus

Focus

* pro forma Excel Technologies + GSI Group Inc results as reported in GSI Group Inc.

8K filed on 07/18/08 ** adjusted EBITDA, non-GAAP financial metric

***Continuing Operations 3Q 2012 LTM

~$480M*

Low single digit

~$70M

33% systems

67% OEM

<20 distinct P&L’s

>30 sites

>50% Semi

<10% Medical

Unrelated

acquisitions

Maximize margins

Pre

Pre

2008

2008

~$271M

Mid single digit

~$43M

~95% OEM

2 focused groups

<15 sites

~20% Semi

~20% Medical

Build out growth

platforms via focused

R&D and bolt-on M&A

Profit growth

Current

Current

***

***

$500M+

High single digit

$100M+

~100% OEM

2 focused groups

<10 sites

<15% Semi

~40% Medical

Current approach

plus selective

transformative M&A

Sustained profitable

revenue growth

Vision

Vision |

We

have positioned the business… …for success in 2013

Key

Accomplishments

2012

•

•

12 X 12 program substantially complete (India JV Pending)

12 X 12 program substantially complete (India JV Pending)

•

•

Laser

Laser

Systems

Systems

divested

divested

–

–

Semiconductor

Semiconductor

Systems

Systems

in

in

process

process

•

•

H2 2012 Restructuring Plan complete

H2 2012 Restructuring Plan complete

•

•

Growth Platforms delivered +$8M of incremental growth

Growth Platforms delivered +$8M of incremental growth

•

•

Significant talent upgrades across organization

Significant talent upgrades across organization

•

•

SOX compliant financial controls in place

SOX compliant financial controls in place

•

•

Balance

Balance

sheet

sheet

strengthened

strengthened

-

-

new

new

credit

credit

agreement

agreement

in

in

place

place

•

•

Strong progress on M&A pipeline

Strong progress on M&A pipeline

Closed Monday on Acquisition of

NDS Surgical Imaging for $82.5M |

We

now have a strong foundation… …to achieve our strategic goals

NDS Surgical Imaging

NDS Surgical Imaging

“A catalyst for realignment of our portfolio and a platform for

“A catalyst for realignment of our portfolio and a platform for

continued growth in the medical market.”

continued growth in the medical market.”

“Highly engineered photonic components, sold exclusively to the

“Highly engineered photonic components, sold exclusively to the

medical market, with high barriers to entry.”

medical market, with high barriers to entry.”

“A more predictable and sustainable revenue and profit stream.”

“A more predictable and sustainable revenue and profit stream.”

|

We

sought additional capabilities… We sought additional

capabilities… …to expand our medical market position

…to expand our medical market position

GSI Medical Strategy

GSI Medical Strategy

•

•

Gain overall scale & growth foundation

Gain overall scale & growth foundation

•

•

Obtain foundation for further growth

Obtain foundation for further growth

•

•

Leverage OEM sales channels

Leverage OEM sales channels

•

•

Play in highly differentiated segments

Play in highly differentiated segments

•

•

Strong bias for photonics

Strong bias for photonics

•

•

Seek leading market positions

Seek leading market positions

•

•

Focus on surgical & critical care

Focus on surgical & critical care

•

•

Leverage strength in peripherals

Leverage strength in peripherals

•

Thermal Printers: Patient

Monitoring, EKG, Pacemakers

•

Encoders: Robotic Surgery, DNA

sequencing

•

Scanners: OCT Retinal Scanning,

Laser Surgery, Drug Discovery

Analysis

•

Color Measurement: Robotic

Surgery, Displays

Strategic Goals

Medical Applications

Medical Market Study |

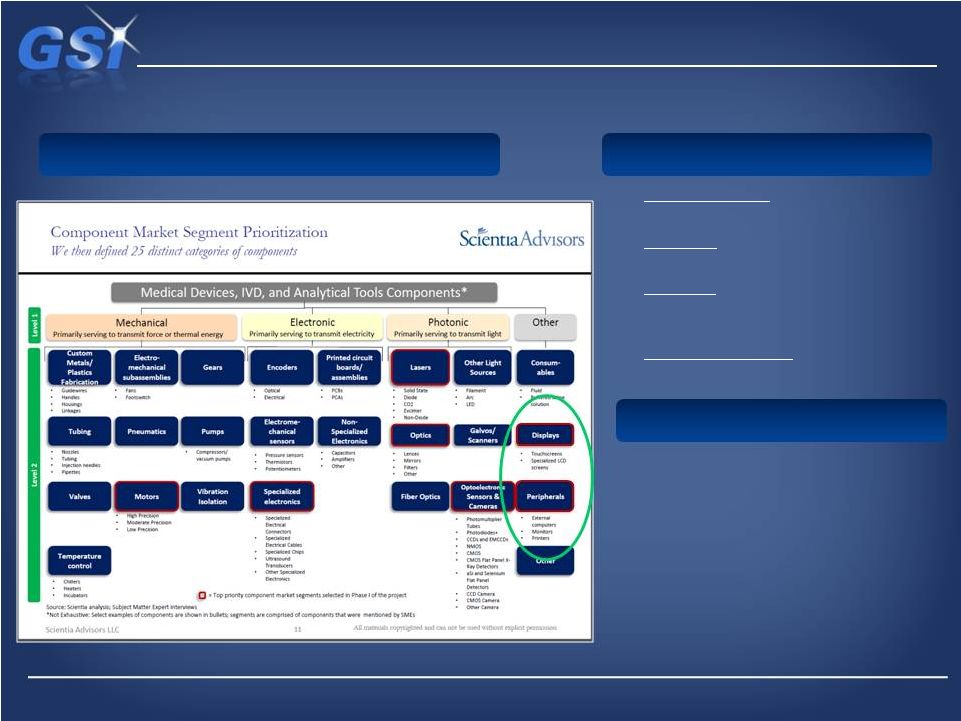

NDS

is the global leader… …in surgical visualization

NDS Profile

NDS Profile

•

Leading global player in surgical & radiology displays and related

accessories •

#1 market position in surgical, #2 in radiology

•

Based in San Jose, CA –

180 employees -

privately owned (Riverside Capital)

•

Revenue +$80M, Adjusted EBITDA margins in mid teens

•

Products sold to OEM’s for integration into surgical endoscopic systems

•

Class I and Class II medical devices (FDA controlled), extremely

high performance

•

Highly

proprietary

color

correction

algorithms

-

custom

matched

to

OEM

designs |

A

complete offering… A complete offering…

…in surgical visualization

…in surgical visualization

Product Offering

Product Offering

Displays

•

•

•

•

•

•

•

Wireless Imaging

•

•

•

•

Informatics

•

•

ConductOR –all-in-one platform,

enabling video format conversion,

image scaling, routing, switching

and IP streaming.

ScaleOR

–

medical-grade video

converter/scaler, supporting

analog and digital video in HD or

SD formats

Ultra high resolution (full HD to 55”)

120Hz refresh rate

Proprietary LED backlight design

Full Multi Mode Imaging (MMI)

Pixel-by-pixel custom color correction

Proprietary software algorithms match

correction to each OEM spec’s

Advanced image processing, digital signal

processing

ZeroWire

real-time full HD surgical video

Medical grade wireless connectivity

Full HD with less than one frame latency

Ultra Wide Band (UWB) frequency spectrum –

allows usage in the OR |

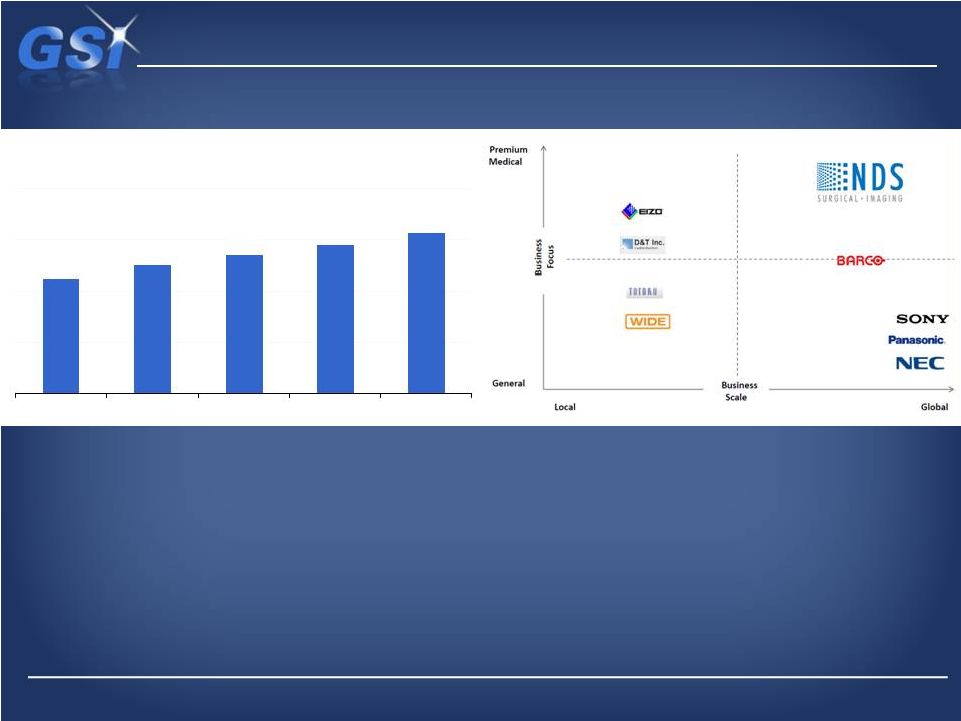

NDS

is the leader in the premium segment… …of this ~$500M

market …of this ~$500M market

Market Overview

Market Growth Drivers

•

Aging population -

increased procedures

•

Rising standard of care in developing world (China,

Brazil, Turkey)

•

Minimally Invasive Surgery (MIS) drives need for

integrated OR’s

•

New technologies (3D surgical cameras, LED and

OLED displays)

•

New applications (e.g. robotic surgery)

Product Requirements

•

FDA quality system compliance

•

Full HD pixel resolution with multi mode capability

•

Highly consistent unit-to-unit color rendition in

varying operating conditions

•

Compatibility with & correction for varying OEM

camera and optic system specifications

•

Wide range of supported input types including

ultra die band wireless capability

*Management Estimates

Medical Display Market ($M)

*

$450

$500

$540

$580

$625

2011

2012

2013

2014

2015 |

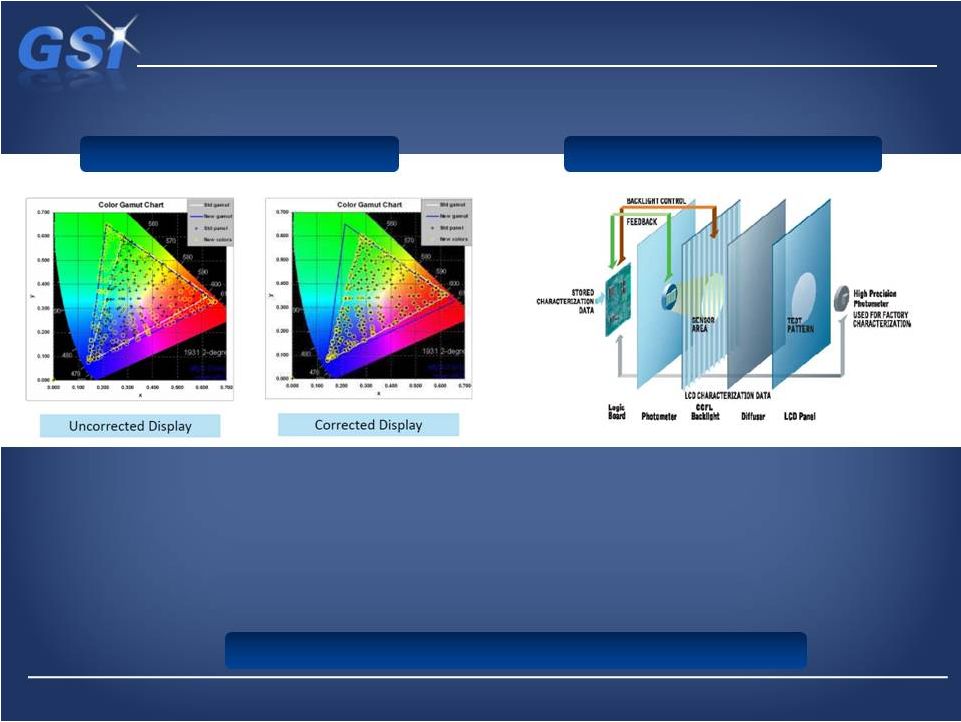

NDS

color correction technology… NDS color correction technology…

…provides a distinct advantage in the market

…provides a distinct advantage in the market

NDS Technology

NDS Technology

•

Real-time

pixel-by-pixel

Color

Response

Correction

•

Proprietary

technology

exclusive

to

NDS

•

Displays

conform

to

the

BT.709

HDTV

color

standard

•

Each display is fully factory characterized (unique

to NDS) –

no field calibration

•

Characterization data and the color correction are

stored in the display

•

Color correction is monitored and adjusted as the

operating conditions change

•

Most accurate calibration algorithms in market

Surgical Displays

Radiology Displays

IP Portfolio: 46 patents with ~50% issued

IP Portfolio: 46 patents with ~50% issued |

NDS

provides

a

substantial

platform…

…for

our

medical

components

growth

strategy

Strategic Fit

•

Substantial

base

of

medical

revenue

at

affordable

multiple

(less

than

7x

EBITDA)

•

Transforms

GSI

to

nearly

40%

medical

–

expect

less

cyclical

revenue

&

earnings

•

Significant

platform

for

further

medical

growth,

including

follow-on

acquisitions

•

Customer

overlap

with

GSI

medical

applications

–

OEM

sales

channel

leverage

enables deeper key account penetration

•

Technology is comparable

to GSI product lines:

-

OEM-focused

medical

peripherals

-

Application

oriented,

highly

engineered

photonics

-

Not

operations

intensive

-

light

assembly,

test

operations,

supply

chain

-

Proprietary

software

is

key

differentiator

–

leverages

GSI

color

measurement

-

Medium

volume

-

“tens

of

thousands”

of

units

per

year

•

Rationalization

opportunity

in

Bay

Area

–

a

key

location

for

GSI |

Revenue

Revenue

Growth

Growth

Potential

Potential

Adj. EBITDA**

Adj. EBITDA**

Value Chain

Value Chain

Focus

Focus

Structure

Structure

Mix

Mix

Growth

Growth

Strategy

Strategy

Performance

Performance

Focus

Focus

The NDS acquisition …

The NDS acquisition …

…a major milestone in our transformation

…a major milestone in our transformation

* pro forma Excel Technologies + GSI Group Inc results as reported in GSI Group Inc.

8K filed on 07/18/08 ** adjusted EBITDA, non-GAAP financial metric

~$480M*

Low single digit

~$70M

33% systems

67% OEM

<20 distinct P&L’s

>30 sites

>50% Semi

<10% Medical

Unrelated

acquisitions

Maximize margins

Pre

2008

$355M+

Mid to high single digit

$55M+

~95% OEM

2 focused groups

<15 sites

~16% Semi

~38% Medical

Build out growth

platforms via focused

R&D and bolt-on M&A

Profit growth

Pro

Forma

w/

NDS

$500M+

High single digit

$100M+

~100% OEM

2 focused groups

<10 sites

<15% Semi

~40% Medical

Current approach

plus selective

transformative M&A

Sustained profitable

revenue growth

Vision |

15

GSI in 2013

GSI in 2013 |

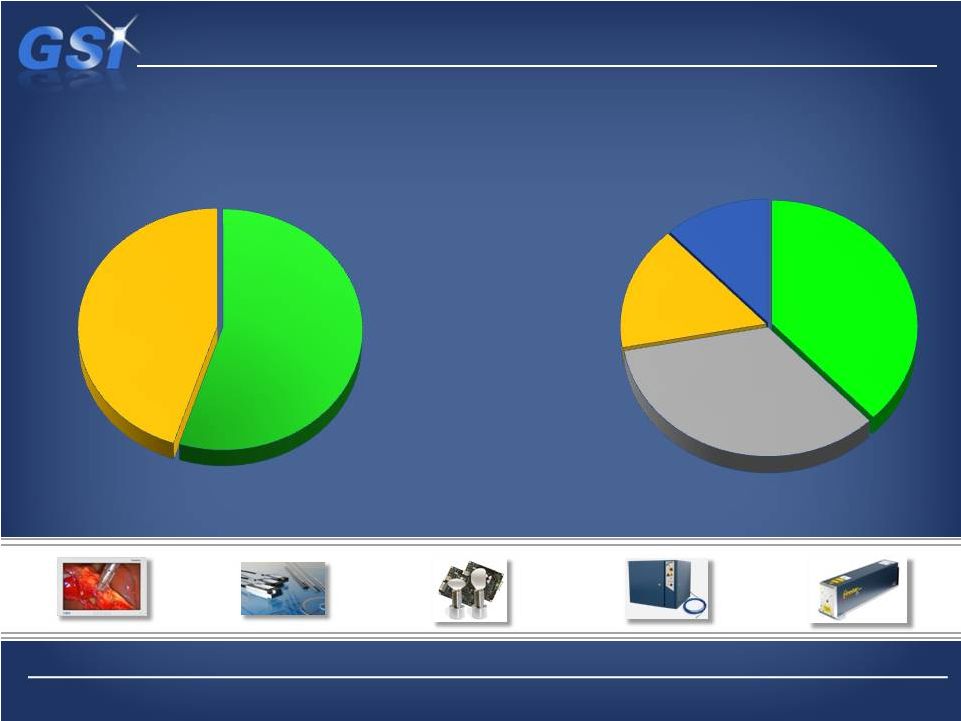

Medical

Medical

is

is

now

now

38%

38%

of

of

portfolio…

portfolio…

…with Microelectronics down to 16%

…with Microelectronics down to 16%

Laser

Laser

*

*

Precision

Precision

16

Scientific

Scientific

Medical

Medical

Micro-

Micro-

electronics

electronics

2013 Pro Forma Breakdown

2013 Pro Forma Breakdown

Industrial

Industrial

*Includes Beam delivery technologies

55%

45%

38%

35%

16%

11% |

We

are investing for growth… …in our three major platforms

Growth Platforms Updates

•

Beam

delivery

for

lasers –

market

growth

~8%

•

Leverage our #1 position in Galvanometers to enter Scan

Head market (modules)

•

Double addressable market up to ~$200M

•

FY’12

growth

forecast

of

~30%

-

numerous

new

design

wins

•

~$25M revenue opportunity by 2015

Scanning Solutions

Scanning Solutions

•

~$600M market growing ~20%

•

Strong offering in mid-power

•

Products to 3kW

•

Converting installed base to fiber

•

FY’12 growth forecast +180%

•

Major investments underway:

-

Lower cost architecture

-

Stronger global sales capability

-

New applications centers in U.S. and China

Fiber Lasers

Fiber Lasers

17

Source: Strategies Unlimited, Management Estimates

•

~$135M pro forma with NDS

•

Numerous opportunities with OEM’s

•

Significant channel leverage

•

Key Applications:

-

Surgical/Radiological Visualization

-

Robotic Surgery

-

OCT Retinal Scanning

-

Patient Monitoring

-

Defibrillation/EKG

Medical Components

Medical Components |

We

faced market challenges… We faced market challenges…

…driven by semiconductor market and macro economy

…driven by semiconductor market and macro economy

Challenges faced in 2012

Challenges faced in 2012

•

•

Prolonged downturn in semiconductor equipment market had

Prolonged downturn in semiconductor equipment market had

significant impact

significant impact

-

-

No demand recovery in 2H’12

No demand recovery in 2H’12

-

-

Divestitures processes impacted

Divestitures processes impacted

•

•

Organization bandwidth fully consumed with change initiatives

Organization bandwidth fully consumed with change initiatives

•

•

Talent

Talent

became

became

a

a

bottleneck

bottleneck

within

within

the

the

businesses

businesses

–

–

numerous

numerous

upgrades were necessary

upgrades were necessary

•

•

Economic/tax uncertainty impacted some M&A efforts

Economic/tax uncertainty impacted some M&A efforts

Economic Uncertainty for 2013 |

NDS

NDS

acquisition

acquisition

provides

provides

increased

increased

scale…

scale…

…with conservative view of base business

…with conservative view of base business

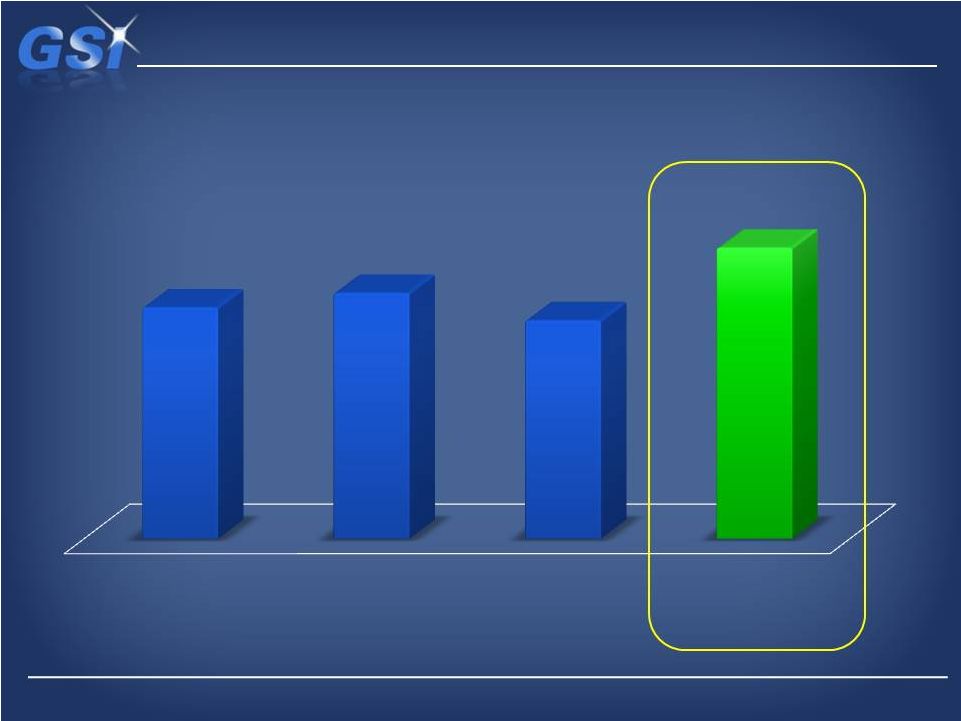

~$270M

~$270M

$304M

$304M

$286M

$286M

Revenue

Revenue

Outlook

Outlook

$355-$365M

$355-$365M

2010 Actual

2011 Actual

2012 Forecast

2013 Outlook

w/ NDS |

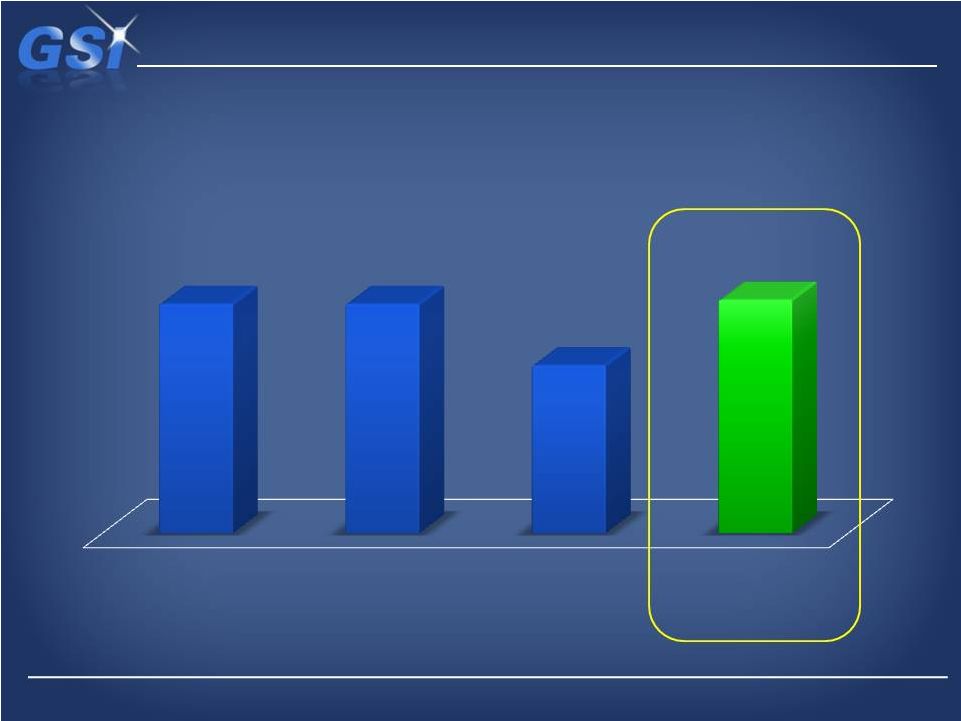

Base

EBITDA growth from 2012 cost actions… Base EBITDA growth from 2012 cost

actions… …with NDS adding ~$12M of EBITDA

…with NDS adding ~$12M of EBITDA

+$41M

+$41M

$56M

$56M

$56M

$56M

Adjusted

Adjusted

EBITDA

EBITDA

Outlook

Outlook

$55-$60M

$55-$60M

2010 Actual

2011 Actual

2012 Forecast

2013 Outlook

w/ NDS |

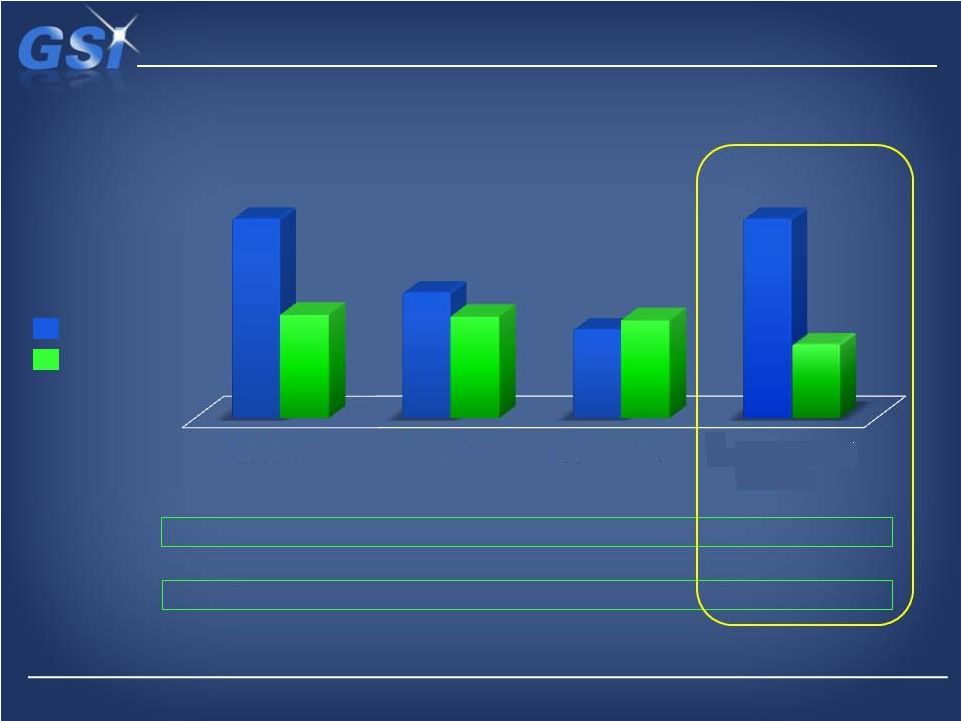

Demonstrated history of strong cash generation…

…enables pursuit of strategic goals

$108M

$68M

$48M

($50.8M)

($50.8M)

($13.2M)

($13.2M)

$5.4M

$5.4M

($68M)

($68M)

Net Debt*

Net Debt*

$57M

$55M

$53M

Total Debt

Total Debt

Cash Balance

Cash Balance

1.9x

1.9x

1.2x

1.2x

1.1x

1.1x

~1.9x

~1.9x

Debt/Adj

Debt/Adj

EBITDA

EBITDA

~$40M

~$108M

Capital Structure

Capital Structure

*Estimated Proforma as of March 31,

2013 *

2010 A

2011 A

3Q 2012 A

Proforma Fcst

w/ NDS |

We

are fully committed… We are fully committed…

…to

…to

delivering

delivering

on

on

our

our

agenda

agenda

for

for

2013

2013

Key Priorities for 2013

Key Priorities for 2013

•

•

Integrate NDS and pursue opportunities

Integrate NDS and pursue opportunities

•

•

Deliver on financial commitments in uncertain economy

Deliver on financial commitments in uncertain economy

•

•

Finalize remaining divestiture

Finalize remaining divestiture

•

•

Build momentum on Growth Platforms

Build momentum on Growth Platforms

•

•

Operational Excellence and cash generation

Operational Excellence and cash generation

•

•

Continued

Continued

focus

focus

on

on

acquisition

acquisition

pipeline

pipeline

–

–

follow-on

follow-on

deals

deals

•

•

Successful close-out of IRS settlement

Successful close-out of IRS settlement |

23

Appendix

Appendix |

Safe

Harbor and Forward Looking Information Certain statements in this presentation are

“forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and are based

on current expectations and assumptions that are subject to risks and uncertainties. All statements

contained in this presentation that do not relate to matters of historical fact should be

considered forward-looking statements, and are generally identified by words such as “expect,” “intend,” “anticipate,” “estimate,” “plan,”

“aim,” “pro forma,” and other similar expressions. These forward-looking

statements include, but are not limited to, statements related to: the Company’s expected

future financial performance as a result of the acquisition of NDS; the expected share of the

Company’s future revenues generated from the medical market; the Company’s

expectations regarding its ability to leverage its medical OEM sales channels and the NDS acquisition; the expected opportunities for growth as a

result of the NDS acquisition; anticipated sales performance; industry trends; market conditions; size

and growth of market potential; the Company’s optimism regarding its prospects for the

future; and other statements that are not historical facts.

These forward-looking statements are neither promises nor guarantees, but involve risks and

uncertainties that may cause actual results to differ materially from those contained in the

forward-looking statements. Our actual results could differ materially from those anticipated in these forward-looking statements for many

reasons, including, but not limited to, the following: economic and political conditions and the

effects of these conditions on our customers’ businesses and level of business activity;

our significant dependence upon our customers’ capital expenditures, which are subject to cyclical market fluctuations; our dependence upon our

ability to respond to fluctuations in product demand; our ability to continually innovate; delays in

our delivery of new products; our reliance upon third party distribution channels subject to

credit, business concentration and business failure risks beyond our control; fluctuations in our quarterly results and our failure to

meet or exceed the expectations of securities analysts or investors; customer order timing and other

similar factors beyond our control; changes in interest rates, credit ratings or foreign

currency exchange rates; risk associated with our operations in foreign countries; our increased use of outsourcing in foreign countries; our

failure to comply with local import and export regulations in the jurisdictions in which we operate;

our history of operating losses and our ability to sustain our profitability; our exposure to

the credit risk of some of our customers and in weakened markets; violations of our intellectual property rights and our ability to protect

our intellectual property against infringement by third parties; risk of losing our competitive

advantage; our ability to make acquisitions or divestitures that provide business benefits; our

failure to successfully integrate current and future acquisitions, including NDS, into our business; our failure to achieve the expected benefits

from our acquisitions, including our acquisition of NDS; our ability to retain key personnel; our

restructuring and realignment activities and disruptions to our operations as a result of

consolidation of our operations; product defects or problems integrating our products with other vendors’ products; failure to maintain

satisfactory compliance with the regulations of the United States Food and Drug Administration and

other governmental agencies; disruptions in the supply of or defects in raw materials, certain

key components or other goods from our suppliers, including certain sole-source suppliers for certain products; production

difficulties and product delivery delays or disruptions; changes in governmental regulation of our

business or products; disruption in our information technology systems or our failure to

implement new systems and software successfully; our failure to realize the full value of our intangible assets; any requirement to make

additional tax payments and/or recalculate certain of our tax attributes depending on the resolution

of the complaint we filed against the U.S. government; our ability to utilize our net operating

loss carry-forwards and other tax attributes; fluctuations in our effective tax rates and audit of our estimates of tax liabilities; being

subject to U.S. federal income taxation even though we are a non-U.S. corporation; being subject

to the Alternative Minimum Tax for U.S. federal income tax purposes; any need for additional

capital to adequately respond to business challenges or opportunities and repay or refinance our existing indebtedness, which

may not be available on acceptable terms or at all; volatility in the market for our common shares;

our dependence on significant cash flow to service our indebtedness and fund our operations;

our ability to access cash and other assets of our subsidiaries; the influence over our business of several significant

shareholders; provisions of our articles of incorporation may delay or prevent a change in control;

our significant existing indebtedness and restrictions in our new senior secured credit

agreement that may limit our ability to engage in certain activities; our intention not to pay dividends in the near future; and our failure to

maintain appropriate internal controls in the future.

Other important risk factors that could affect the outcome of the events set forth in these statements

and that could affect the Company’s operating results and financial condition are

discussed in Item 1A of our Annual Report on Form 10-K for the fiscal year ended December 31, 2011, and in the Company’s subsequent

filings with the SEC made prior to or after the date hereof. Such statements are based on the

Company’s management’s beliefs and assumptions and on information currently available

to the Company’s management. The Company disclaims any obligation to update any forward-looking statements as a result of

developments occurring after the date of this document except as required by law.

|

Use

of Non-GAAP Financial Measures Use of Non-GAAP Financial Measures

This press release includes a financial measure, Adjusted EBITDA, which is not a financial measure

prepared in accordance with generally accepted accounting principles (“GAAP”). The

Company defines Adjusted EBITDA as the net income attributable to GSI Group Inc. before

deducting interest, income taxes, depreciation, amortization, non-cash share-based

compensation, restructuring, restatement, acquisition and other non-recurring costs, income

from discontinued operations, net of tax, and other non-operating income/expense items, including foreign

exchange gains/losses and earnings from equity investment. Management believes Adjusted EBITDA

provides meaningful supplementary information regarding the Company’s operating results

because it excludes amounts that management does not consider as part of operating results when

assessing and measuring the operational and financial performance of the Company. Adjusted EBITDA is used by management to

evaluate operating performance, communicate financial results to the Board of Directors, benchmark

results against historical performance and the performance of peers, evaluate investment

opportunities including acquisitions and discontinued operations, and determine the bonus

payments for senior management and employees. The Company believes this non-GAAP measure

provides greater transparency and insight into management’s method of analysis. Because of the forward-looking nature of the forecasted Adjusted EBITDA figure included in

this press release, specific quantification of the amounts that would be required to reconcile

net income to Adjusted EBITDA are not available. The Company believes that there is a degree of

volatility with respect to the Company’s and NDS’s net income which preclude it from

providing accurate forecasted GAAP to non-GAAP reconciliations. Based on the above,

the Company believes that providing estimates of the amounts that would be required to reconcile the

forecasted Adjusted EBITDA figure would imply a degree of precision that would be confusing or

misleading to investors for the reasons identified above.

|

Last Twelve Months Ended

Twelve Months Ended

September 28, 2012

December 31, 2011

December 31, 2010

(in thousands of dollars)

Income from operations (GAAP)

$ 15,495

$ 35,848

$ 36,027

Depreciation and amortization

13,618

14,467

14,687

Share-based compensation

4,237

3,276

1,871

Restructuring, restatement and other nonrecurring costs (a)

9,370

2,406

3,319

Net income attributable to noncontrolling interest

(38)

(28)

(48)

Adjusted EBITDA (Non-GAAP)

$ 42,682

$ 55,969

$ 55,856

Non-GAAP EBITDA Reconciliation

(a)

(a)

Restructuring, restatement and other nonrecurring costs includes restructuring costs,

pre-petition and post-emergence professional fees associated with our bankruptcy

proceedings and fees related to third parties for services performed in connection with the review and investigation of revenue transactions examined

and the restatement of the Company’s 2004 through 2008 financial statements. |

Net

Debt & Leverage Ratios Non-GAAP Net Debt and Leverage Ratios

Twelve Months Ended

Twelve Months Ended

Twelve Months Ended

Twelve Months Ended

September 28, 2012

September 28, 2012

December 31, 2011

December 31, 2011

December 31, 2010

December 31, 2010

(in thousands of dollars, except ratio information)

Debt

Debt

($47,500)

($47,500)

($68,000)

($68,000)

($107,575)

($107,575)

Less: cash and cash equivalents

Less: cash and cash equivalents

52,863

52,863

54,835

54,835

56,781

56,781

Net debt (a)

Net debt (a)

$5,363

$5,363

($13,165)

($13,165)

($50,794)

($50,794)

Total Debt

Total Debt

($47,500)

($47,500)

($68,000)

($68,000)

($107,575)

($107,575)

Adjusted EBITDA (non-GAAP) (b)

$42,682

$42,682

$55,969

$55,969

$55,856

$55,856

Total Debt/Adjusted EBITDA

Total Debt/Adjusted EBITDA

1.1

1.1

1.2

1.2

1.9

1.9

Total Equity

Total Equity

$219,091

$219,091

$209,360

$209,360

$178,678

$178,678

Total Debt/Total Equity

Total Debt/Total Equity

22%

22%

32%

32%

60%

60%

(a)

Net debt is defined as total debt less cash and cash equivalents.

(b)

For Adjusted EBITDA calculation, refer to the Non-GAAP EBITDA Reconciliation

page. |