Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Howmet Aerospace Inc. | d466244d8k.htm |

| EX-99.1 - TRANSCRIPT OF ALCOA INC. FOURTH QUARTER 2012 EARNINGS CALL - Howmet Aerospace Inc. | d466244dex991.htm |

4

Quarter Earnings Conference

January 8, 2013

Exhibit 99.2

[Alcoa Logo]

th |

Cautionary Statement

2

[Alcoa Logo]

Forward-Looking Statements

This presentation contains statements that relate to future events and expectations and as

such constitute forward-looking statements. Forward-looking statements include those

containing such words as “anticipates,” “estimates,”

“expects,” “forecasts,” “intends,” “outlook,” “plans,” “projects,” “should,” “targets,” “will,” or other words of similar meaning. All

statements that reflect Alcoa’s expectations, assumptions, or projections about the

future other than statements of historical fact are forward-looking statements, including, without

limitation, forecasts concerning global demand growth for aluminum, end-market

conditions, supply/demand balances, and growth opportunities for aluminum in automotive,

aerospace and other applications, trend projections, targeted financial results or operating

performance, and statements about Alcoa’s strategies, outlook, and business and

financial prospects. Forward-looking statements are subject to a number of known and

unknown risks, uncertainties, and other factors and are not guarantees of future

performance. Important factors that could cause actual results to differ materially from

those in the forward-looking statements include: (a) material adverse changes in aluminum

industry conditions, including global supply and demand conditions and fluctuations in

London Metal Exchange-based prices for primary aluminum, alumina, and other products,

and fluctuations in indexed-based and spot prices for alumina; (b) deterioration in

global economic and financial market conditions generally; (c) unfavorable changes in the

markets served by Alcoa, including automotive and commercial transportation, aerospace,

building and construction, distribution, packaging, defense, and industrial gas turbine; (d)

the impact of changes in foreign currency exchange rates on costs and results, particularly

the Australian dollar, Brazilian real, Canadian dollar, euro, and Norwegian kroner; (e)

increases in energy costs, including electricity, natural gas, and fuel oil, or the

unavailability or interruption of energy supplies; (f) increases in the costs of other raw materials,

including calcined petroleum coke, caustic soda, and liquid pitch; (g) Alcoa’s

inability to achieve the level of revenue growth, cash generation, cost savings, improvement in

profitability and margins, fiscal discipline, or strengthening of competitiveness and

operations (including moving its alumina refining and aluminum smelting businesses down on the

industry cost curves and increasing revenues in its Global Rolled Products and Engineered

Products and Solutions segments) anticipated from its restructuring programs and

productivity improvement, cash sustainability, and other initiatives; (h) Alcoa's inability

to realize expected benefits, in each case as planned and by targeted completion dates, from

sales of non-core assets, or from newly constructed, expanded, or acquired facilities,

such as the upstream operations in Brazil and the investments in hydropower projects in

Brazil, or from international joint ventures, including the joint venture in Saudi Arabia;

(i) political, economic, and regulatory risks in the countries in which Alcoa operates or sells

products, including unfavorable changes in laws and governmental policies, civil unrest, or

other events beyond Alcoa’s control; (j) the outcome of contingencies, including legal

proceedings, government investigations, and environmental remediation; (k) the business or

financial condition of key customers, suppliers, and business partners; (l) adverse

changes in tax rates or benefits; (m) adverse changes in discount rates or investment

returns on pension assets; (n) the impact of cyber attacks and potential information

technology or data security breaches; and (o) the other risk factors summarized in Alcoa's

Form 10-K for the year ended December 31, 2011, Forms 10-Q for the quarters ended

March 31, 2012, June 30, 2012 and September 30, 2012, and other reports filed with the

Securities and Exchange Commission. Alcoa disclaims any obligation to update publicly

any forward-looking statements, whether in response to new information, future events or

otherwise, except as required by applicable law. Non-GAAP Financial Measures

Some of the information included in this presentation is derived from

Alcoa’s consolidated financial information but is not presented in Alcoa’s financial statements prepared in

accordance with U.S. generally accepted accounting principles (GAAP). Certain of these data

are considered “non-GAAP financial measures” under SEC rules. These non-GAAP

financial measures supplement our GAAP disclosures and should not be considered an

alternative to the GAAP measure. Reconciliations to the most directly comparable GAAP

financial measures and management’s rationale for the use of the non-GAAP financial

measures can be found in the Appendix to this presentation and on our website at

www.alcoa.com under the “Invest” section. Any reference during the discussion

today to EBITDA means adjusted EBITDA, for which we have provided calculations and

reconciliations in the Appendix and on our website. |

Chuck McLane

Executive Vice President and Chief Financial Officer

3

January 8, 2013

[Alcoa Logo] |

4 Quarter 2012 Financial Overview

See appendix for reconciliations to GAAP and additional information

4

[Alcoa Logo]

Income

from

Continuing

Operations

of

$242

million,

or

$0.21

per

share;

Excluding

impact

of

restructuring

and

other

special

items:

•

Income

from

continuing

operations

of

$64

million,

or

$0.06

per

share

Revenue

at

$5.9

billion

Adjusted

EBITDA

of

$597

million

Midstream

and

Downstream

achieve

record

fourth

quarter

results

Positive

Free

Cash

Flow

of

$535

million

Days

Working

Capital

at

24

days,

an

all-time

low

Debt-to-Capital

of

35%,

Net

Debt-to-Capital

of

30%

Cash

on

hand

of

$1.9

billion

Net

Debt

of

$7.0

billion,

lowest

year

end

since

2006

th |

Income Statement Summary

5

$ Millions, except per-share amounts

4Q11

3Q12

4Q12

Sequential

Change

Revenue

$5,989

$5,833

$5,898

$65

Cost of Goods Sold

$5,228

$5,266

$4,968

($298)

COGS % Revenue

87.3%

90.3%

84.2%

(6.1 % pts.)

Selling,

General Administrative, Other

$268

$234

$277

$43

SGA % Revenue

4.5%

4.0%

4.7%

0.7 % pts.

Other Income, Net

($40)

($2)

($345)

($343)

Restructuring and Other Charges

$232

$2

$60

$58

Effective Tax Rate

31.0%

15.9%

35.8%

19.9 % pts.

(Loss) Income from Continuing Operations

($193)

($143)

$242

$385

(Loss) Income Per Diluted Share

($0.18)

($0.13)

$0.21

$0.34

[Alcoa Logo] |

[Alcoa

Logo] Restructuring and Other Special Items

See appendix for Adjusted Income reconciliation

6

$ Millions, except per-share amounts

3Q12

4Q12

Income Statement

Classification

Segment

(Loss)/Income

($143)

$242

(Loss)/Income

($0.13)

$0.21

Tapoco

Asset Sale

-

$161

Other Income, Net

Primary

Metals /

Corporate

Restructuring-Related

($2)

($54)

Restructuring

and

Other Charges

Corporate

Discrete Tax Items

($26)

$58

Income Taxes

Corporate

Mark-to-Market Energy Contracts

($3)

$12

Other Income, Net

Corporate

Interest Income

-

$8

Other Income, Net

Corporate

Massena

Fire

($9)

($7)

Revenue, COGS

and

Other

Income, Net

Primary

Metals/EPS

Environmental Reserve

($120)

-

COGS

Corporate

Litigation Reserve

($15)

-

COGS

Corporate

Special

Items

($175)

$178

Income

from

Continuing

Ops

excl

Special

Items

$32

$64

$0.03

$0.06

from

Continuing

Ops

Per

Diluted

Share

Income

per

Diluted

Share

excl

Special

Items |

[Alcoa

Logo] 4th

Quarter 2012 vs. 3rd

Quarter 2012 Earnings Bridge

See appendix for Adjusted Income reconciliation

7

Income from Continuing Operations Excluding Restructuring & Other Special Items

($ millions) +$78m

-$1m

-$38m

64

32

14

Productivity

4Q 2012

Cost

Increases Curtailment

/ Other

37

Raw

Materials

13

Energy

Portovesme

7

3Q 2012

LME

79

1

25

Price

/Mix

8

Volume

34

Currency

th

rd

[Alcoa Logo] |

[Alcoa

Logo] Alumina

8

1

Quarter Outlook

Alumina 4Q12 Results and 1Q13 Outlook

4Q 11

3Q 12

4Q 12

Production (kmt)

4,178

4,077

4,079

3

Party Shipments (kmt)

2,378

2,368

2,440

3

Party Revenue ($ Millions)

847

764

803

ATOI ($ Millions)

125

(9)

41

48%

of 3

party shipments on spot or alumina price

index with

30 day lag

for 2013

Production

and shipments decrease by 90 kmt

Crusher move

in Australia drives mining cost increase

of $5 million

Productivity

improvements continue

Higher

3

party shipments

driven by lower internal

shipments

API and spot pricing

more stable than LME aluminum

pricing

Productivity

of

$10 million

Higher

fuel oil

and

natural gas

prices

Working capital improved 1 day vs. prior year quarter

Productivity of $190 million

for full year 2012

4

Quarter Performance Bridge

4

Quarter Business Highlights

4

Quarter Results

4Q

2012

$41

Cost

Decr.

$9

Raw Mat.

$3

3Q

2012

-$9

Product.

$10

Energy

-$2

Price/ Mix

-$21

Volume

-$7

Currency

$6

LME

$52

Market

Performance

$ Millions

+$58m

$8m

-

th

th

th

st

rd

rd

rd

rd |

9

Production decrease due to completed Italy curtailment

Price/Mix improvement as regional premiums rise

Productivity

of $11 million

Seasonal energy

price increases

Completed Tapoco Hydropower asset sale

Productivity of $245 million

for full year 2012

4

Quarter Results

4

Quarter Business Highlights

1

Quarter Outlook

Pricing

to follow 15 day lag

to LME

Production

and shipments decrease by 20 kmt

Carbon pricing

expected to remain level

Rockdale and Anglesea power

generation outages of

$15 million

Saudi Arabia JV

equity costs of $20 million

Primary Metals 4Q12 Results and 1Q13 Outlook

4Q 11

3Q 12

4Q 12

Production (kmt)

962

938

912

3

rd

Party Shipments (kmt)

805

768

768

3

rd

Party Revenue ($ Millions)

1,991

1,794

1,890

3

rd

Party Price ($/MT)

2,374

2,222

2,325

ATOI ($ Millions)

(32)

(14)

316

Quarter Performance Bridge

$ Millions

market

performance

4Q

2012

Tapoco

Sale

PV

Curtail

Cost

Decreases

Volume

Price

/Mix

3Q

2012

Prod-

uctivity

-

Currency

Energy

Raw

Materials

LME

th

th

st

[Alcoa Logo]

4

th |

ATOI ($ Millions)

4Q 11

3Q 12

4Q 12

Global Rolled Products,

excl Russia, China & Other

32

89

62

Russia, China & Other

(6)

9

7

Total ATOI

26

98

69

Adjusted EBITDA/mt

225

395

344

4

th

Quarter Results

4

Quarter Business Highlights

1

Quarter Outlook

4

Quarter Performance Bridge

$6

$4

$69

$98

4Q 2012

Other Items

-$4

Cost Increase

-$8

Productivity

Price/Mix

Volume

-$27

3Q 2012

Record 4Q ATOI

and adjusted

EBITDA per metric ton

ATOI

up

165%

vs. year-over-year quarter

Seasonal decline

in Packaging volume

Aerospace

and automotive remained strong

Productivity

of

$6 million

Working capital improved 8 days vs. prior year quarter

Aerospace and automotive

demand expected to

remain strong

European and North America industrial flat

and

uncertain

Productivity

improvements continue

$ Millions

[Alcoa Logo]

Global Rolled Products

Global Rolled Products 4Q12 Results and 1Q13 Outlook

10

See appendix for Adjusted EBITDA reconciliation

th

th

st |

[Alcoa

Logo] Engineered Products and Solutions

See appendix for Adjusted EBITDA reconciliation

11

Engineered Products and Solutions 4Q12 Results and 1Q13 Outlook

$ Millions

4Q 11

3Q 12

4Q 12

Party Revenue

1,355

1,367

1,348

ATOI

122

160

137

Adjusted EBITDA Margin

16.2%

20.3%

17.7%

Quarter Results

Quarter Outlook

4

Quarter Performance Bridge

Quarter Business Highlights

$ Millions

Record 4Q ATOI

and adjusted EBITDA margin

4Q

adjusted

EBITDA

margin

at

17.7%,

up

1.5

points

year-over-year

Year-over-year

ATOI

up

$15

million

on

$7

million

less

revenue

Productivity

of $2 million

Aerospace

market

remains

strong

European

Non-Residential

Construction

market

continues

to

decline

–

Normal

seasonal

decline

in

N.A.

market

Heavy

Duty

truck

market

flat

in

N.A.

and

Europe

Share gains

through innovation continue

across all

market sectors

Productivity

improvements continue

th

4

th

4

th

1

st

3

rd

$2

$137

-$2

-$4

-$12

-$6

-$1

$160 |

[Alcoa

Logo] See appendix for Free Cash Flow and Net Debt-to-Capital

reconciliations 4 Quarter Cash Flow Overview

12

($ Millions)

4Q11

3Q12

4Q12

Net (Loss) Income

($163)

($175)

$257

DD&A

$368

$366

$363

Change in Working Capital

$797

$88

$539

Pension Contributions

($119)

($163)

($46)

Taxes / Other Adjustments

$259

$147

($180)

Cash from Operations

$1,142

$263

$933

Dividends to Shareholders

($33)

($32)

($33)

Change in Debt

$52

($273)

($692)

Distributions to Noncontrolling Interest

($4)

($1)

($24)

Contributions from Noncontrolling Interest

$33

$22

$39

Other Financing Activities

$1

$2

($2)

Cash from Financing Activities

$49

($282)

($712)

Capital Expenditures

($486)

($302)

($398)

Other Investing Activities

($97)

$40

$605

Cash from Investing Activities

($583)

($262)

$207

4Q12 FCF

$535 million

$1.9 billion

of cash

3 Day DWC

reduction vs.

4Q 2011

Quarter

2012 Cash Flow Overview

Debt-to-Cap

at 35%;

Net Debt-to-

Cap at 30%

th

4

th |

[Alcoa

Logo] 13

2012 FULL YEAR RESULTS |

[Alcoa

Logo] Executing and Delivering in a Challenging Environment

See appendix for Adjusted EBITDA reconciliation

14

Delivering Results

Productivity &

Overhead

Working Capital

Capital Spend

and Investments

Maintain

Debt-to-Capital

Target: $850m

Actual: $1.3b

Positive Free

Cash Flow

Target: 1.5 days

Actual: 3.5 days

Target: $1.7b

Actual: $1.4b

Target: 30%-35%

Actual: 34.8%

API

or

spot

pricing

net

benefit

of

$35M

4%

point

reduction

on

smelting

cost

curve

Record

annual

midstream

ATOI

of

$358M;

35%

YOY

improvement

Record

midstream

full

year

adjusted

EBITDA/mt

of

$390

Downstream

delivered

record

annual

ATOI

of

$612M;

14%

YOY

improvement

All-time

high

full

year

adjusted

EBITDA

margin

of

19.2%

for

downstream

Net

debt

at

$7.0

billion,

lowest

year

end

since

2006

Achieving Our Targets |

[Alcoa

Logo] Taking Necessary Steps to Maintain Liquidity

15

See appendix for Free Cash Flow reconciliation

($ Millions)

2012

Cash from Operations

$1,497

Capital Expenditures

($1,261)

Free Cash Flow

$236

Saudi Arabia Investments

($164)

Proceeds from sale of assets

$615

$687 |

[Alcoa Logo]

Generating Positive FCF Amid A Volatile Environment

16

See appendix for Free Cash Flow reconciliation

Free Cash Flow

($ millions)

-39

246

-506

656

164

526

-440

1,005

176

87

-22

761

-186

-90

-742

-409

535

2009

-$257

2010

$1,246

2011

$906

2012

$236 |

[Alcoa Logo]

Exceeding $850 Million Productivity and Overhead Target

*All figures are pretax and pre-minority interest. 2009/2010 represent net

productivity; 2011/2012 represent gross productivity 17

1

5,542

1,291

1,099

742

2,410

Total

2012

2011

2010

2009

Alcoa Productivity ($millions)* |

[Alcoa Logo]

2012 Actions More Than Offset Significant Headwinds

See appendix for Adjusted Income reconciliation

18

Income from Continuing Operations Excluding Restructuring & Other Special Items ($ millions)

-$885m

+$1,005m

-$670m

262

812

Cost

Increases

/ Other

559

Raw

Materials

91

Energy

20

Productivity

786

Price

/Mix

127

Volume

92

Currency

129

LME

1,014

2011

2012 |

[Alcoa Logo]

Achieving Sustainable Days Working Capital Reductions

See appendix for days working capital reconciliation

19

3 days

lower

Days Working Capital since Fourth Quarter 2008

3 days

lower

10 days

lower

33

33

32

38

38

39

43

44

41

48

50

55

20

25

30

35

40

45

50

55

43

30

33

27

-3

days

24

3 days

lower

Record Low

4

th

Quarter |

[Alcoa Logo]

Significantly Strengthening Our Liquidity Position

See appendix for Net Debt-to-Capital reconciliation

20

Net debt

reduction of 29%

since 2008

Debt to Cap

Net Debt

Cash

Debt, Net Debt and Debt

-

to

-

Capital %

(millions)

Commitment to Investment Grade: Improving Net Debt Position

Net debt

reduction of 29%

since 2008

762

1,481

1,543

1,939

1,861

2009

9,819

8,338

2008

10,578

9,816

2012

8,829

6,968

2011

9,371

7,432

2010

9,165

7,622

38.7%

42.5%

34.9%

35.3%

34.8% |

[Alcoa Logo]

New Aggressive Targets Set to Maximize Cash In 2013

21

Positive

Free Cash

Flow

Maintain 30%-35% Debt-to-Capital

Manage Growth Capital of $550M

Generate Productivity Gains of $750M

Target Saudi JV Investment of $350M

Overarching 2013 Financial Target

Control Sustaining Capital of $1.0B

Taking the right actions

2013 Targets: Key Actions to Execute 2013 Cash Sustainability Program

|

[Alcoa Logo]

Successfully Executing for Cash; Continued Focus in 2013

22

Debt to Cap

Net Debt

Cash |

[Alcoa Logo]

Klaus Kleinfeld

Chairman and Chief Executive Officer

January 8, 2013 |

[Alcoa Logo]

Source: Alcoa analysis

2013 Market Conditions

24

Alcoa End Markets: Current Assessment of 2013 vs. 2012

North America

China

Global

Europe

Aerospace

Automotive

Heavy Truck &

Trailer

Beverage Can

Packaging

Commercial Building

and Construction

Industrial Gas

Turbine |

[Alcoa Logo]

Aluminum Market Fundamentals Are Intact

25

2012: Aluminum Demand Strong and

Outpacing 10-Year Forecast

Global Aluminum Demand Grows in 2013

Inventories Stable; Financing Driving Premiums

Markets Essentially Balanced |

[Alcoa Logo]

26

Source: Alcoa analysis, Brook Hunt, CRU, Harbor Intelligence

Short Term Demand Exceeding Long Term Expectations

In 2010, we said demand to roughly double…

25.4

46.1

Rest of World

China

2012

20.7

2010

39.5

23.0

16.5

2020 Forecast

39.5

Rest of World

China

73.4

35.7

37.7

2010

23.0

16.5

Million MT

12%

5%

9%

4%

Million MT

…run rate ahead of projection

6.5%

CAGR

8.0%

CAGR |

[Alcoa Logo]

27

Source: Alcoa analysis, IMF, OECD

Global Aluminum Demand Accelerates to 7% in 2013

2013 Primary Aluminum Consumption (mmt), Annualized Growth (%) and Change (% pts)

by Region (1)

Other includes Middle East, Latin America ex Brazil, Eastern Europe and Rest of

World -1%

-2%

2013 Global Demand

(4Q12 estimate)

49.4 mmt

Annualized Growth

(4Q12 estimate)

1%

1%

3%

3%

2%

0%

1%

2%

Russia

Brazil

India

Other

(1)

Asia ex. China

North America

Europe

China

Change in Growth

(2012 to 2013 in % pts.)

1%

Global

1%

World ex China

2013 Global Demand

Growth Rate 7% vs. 2012

(World ex China 4%)

2012

2013E

China

Europe

North America

Asia ex. China

Other

(1)

India

Brazil

Russia

23.0

6.5

6.2

5.9

3.8

2.0

1.0

1.0

11%

9%

4%

4%

5%

7%

6%

7%

6%

9%

1%

4%

5%

6% |

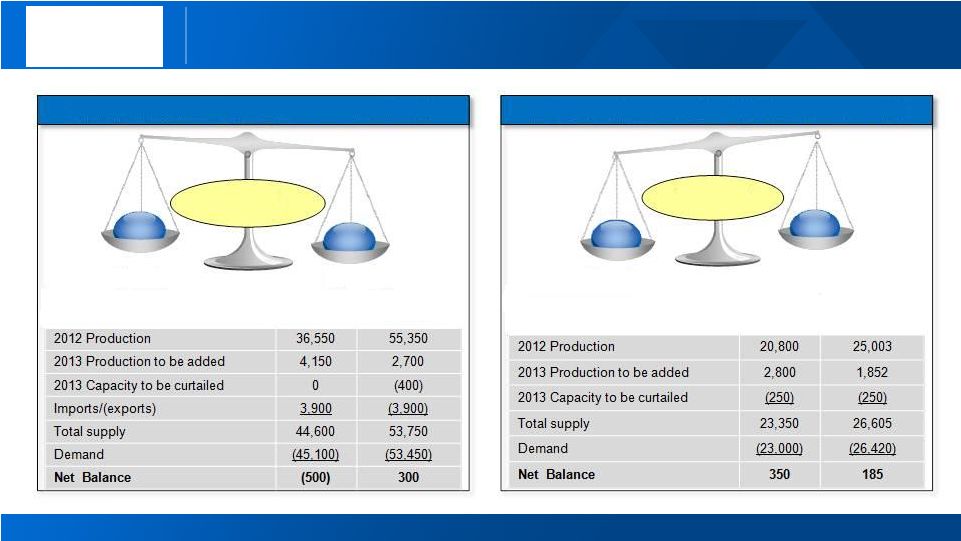

[Alcoa Logo]

2013E Aluminum Supply/Demand Balance

Supply

Demand

Surplus

535

‘000 mt

China

Rest of

World

2013E Alumina Supply/Demand Balance

‘000 mt

China

Rest of

World

Supply

Demand

Deficit

(200)

Source: Alcoa analysis, Brook Hunt, CRU, CNIA, NBS, Chinese Customs

Markets Essentially Balanced in 2013

28 |

[Alcoa Logo]

29

Source: Alcoa analysis, LME, SHFE, CRU, IAI, Marubeni Corp.

Primary Aluminum Inventories Remain Below 2009 Peak

Decline 28 days

from the ’09 peak

Cancelled Warrants:

1.6M

tons

above year end 2011;

all-time record high

China

stocks: Only

7 days

of

global demand

Producer

stocks

: Record

low <

10

days

Days of

Consumption

Days of

Consumption

102 days

LME Price

$2,214/MT

Days of

Consumption

80 days

LME Price

$2,686/MT

Days of

Consumption

74 days

LME Price

$2,098/MT

Global Inventories

Global Inventories vs. LME Price Over Time |

[Alcoa Logo]

Source: Month end pricing -

Platts Metals Week and Metal Bulletin

Regional Premiums Continue To Be Strong

30

0

50

100

150

200

250

300

$0

$50

$100

$150

$200

$250

$300

Regional Premiums over time

$ per metric

ton

$ per metric

ton |

[Alcoa Logo]

Macro Events Continue to Drive Price Movements

Movement in LME Cash Prices After Economic Announcements

Nov 20

th

Greece Aid

Resolution

LME $1,952

Dec 7

th

Positive U.S. Labor

News

LME $2,078

Positive China PMI

LME $1,916

Dec 31

st

Improved Sentiment

Cliff Deal Will Be

Reached

LME $2,040

Dec 18

th

Uncertainty over Fiscal

Cliff Negotiations

LME $2,081

31

Source: LME, Bloomberg

Nov 22

nd |

[Alcoa Logo]

2012/2013 Common Thread: Disciplined Execution

32

Solid operating performance in a volatile year

Achieving strategic investment milestones

Financial targets set to maximize cash |

[Alcoa Logo]

Alumina: Focused on Sustainable Cost Reductions

33

Clear Strategic Direction:

Improving cost competitiveness

0

100

200

300

400

500

600

700

0

20,000

40,000

60,000

80,000

100,000

120,000

Cumulative Production

(000MT)

Alcoa 2010

30

th

Percentile

Alumina Cost Curve

Alcoa 2015

23

rd

Percentile

Refining Cost Curve Holding Steady

$/mt

-7 points

Alcoa 2012

30

th

Percentile

Atlantic refinery curtailments: 390k mtpy

Creeping low-cost capacity: increased

production

in Australia by 400tpd in 2012

Productivity

gains: ~$190 million for

2012 and ~$390 million since 2010

First

concrete

pour

Saudi

Arabia

refinery in February 2012

2012 Strategic Actions

Progress on energy solutions in Spain

at |

[Alcoa Logo]

Primary Metals: Moving Down the Cost Curve

34

Smelting Cost Curve Down 4% Points

-10 points

Clear Strategic Direction: Improving cost competitiveness

Curtailments:

240k mtpy

in Spain and Italy

Permanent

closures: 291k mtpy

Securing

energy solutions:

Power contracts for Mt. Holly and Intalco

Estreito

hydro electric dam

commissioned

Brazilian

regulatory improvements

Spanish

energy framework implemented

and ~

$480 million

since 2010

2012 Strategic Actions

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

20,000

40,000

60,000

Cumulative Production (000MT)

Alcoa 2015

41

st

Percentile

Alcoa 2010

51

st

Percentile

Aluminum Cost Curve

$/mt

Alcoa 2012

47

th

Percentile

Saudi Arabia JV First Hot Metal achieved

in December 2012

Productivity

gains:

~

$245 million

for 2012

Tapoco

sale

: ~

$600 million

gross proceeds

in the U.S. |

[Alcoa Logo]

Global Rolled Products: Generating Record Margins

See appendix for Adjusted EBITDA reconciliations

35

273

253

249

276

226

201

108

119

314

327

390

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Revenue growth from new products and share gains

GRP-Growing profitability at record levels

$ Billions

Adjusted EBITDA per MT

10-YR Average ~ $235/MT

$7.6

2013 Target

Normalized

$8.4b

2012

Actual

$7.4b

2010

Actual

$6.3b

$2,019

$2,143**

** 2010 LME price of $2,143 assumed to normalize 2013 target

LME:

$2,143

Midstream Strategy: Profitable Growth

* $1.5 billion revenue growth from share gains and new products and $1.0 billion

revenue growth from metal and market |

[Alcoa Logo]

Engineered Products & Solutions: Growing Profitably

See appendix for Adjusted EBITDA reconciliations

36

Downstream Strategy: Profitable Growth

Record margins exceeding historical levels

Adjusted EBITDA Margin

$ Billions

8%

9%

12%

11%

12%

13%

15%

13%

17%

18%

19%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

$5.6

2012

$5.5

2010

$4.6

$6.2

Markets

Revenue growth from share gains and innovation

* $1.0 billion revenue growth from share gains and innovation and $600 million revenue

growth from the market |

[Alcoa

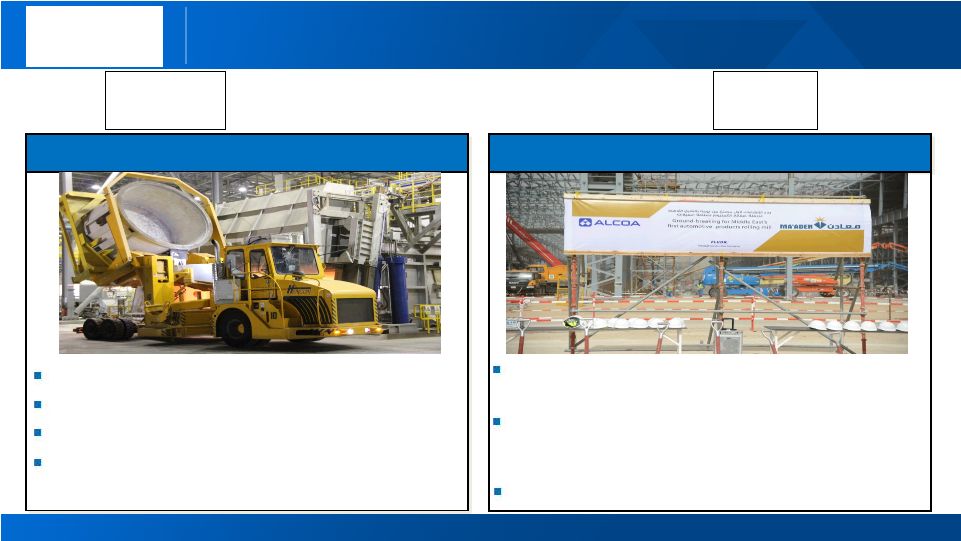

Logo] Saudi Arabia JV: Achieving Significant Milestones

37

[Alcoa Logo]

Achieved smelter First Hot Metal

Auto capability groundbreaking

Lowest cost, integrated aluminum facility in the world

Successful commissioning of first smelting pots First hot metal in 25 months from

first concrete Expected to produce ~250k tons in 2013

Contributes 2% point reduction on the smelting cost curve

Integrated

rolling and surface treatment

complex

Expanding

capability

to produce up to

100k tons

of downstream products, including

automotive

heat-treated and non-heat-treated sheet

Production

planned to start at the

end of 2014

[Ma’aden Logo] |

[Alcoa Logo]

Focus Remains on Cash In 2013

38

Positive

Free Cash

Flow

Maintain 30%-35% Debt-to-Capital

Manage Growth Capital of $550M

Generate Productivity Gains of $750M

Target Saudi JV Investment of $350M

Overarching 2013 Financial Target

Control Sustaining Capital of $1.0B

Taking the right actions

Key Actions to Execute 2013 Cash Sustainability Program

|

[Alcoa Logo]

Market and Fundamentals Intact; Sentiment Moves Price

39 |

[Alcoa Logo]

Executing Mid-Term Strategy; Continued Cash Focus

40 |

41

[Alcoa Logo] |

[Alcoa Logo]

Kelly Pasterick

Director, Investor Relations

Alcoa

390 Park Avenue

New York, NY 10022-4608

Telephone: (212) 836-2674

www.alcoa.com

Additional Information

42 |

[Alcoa Logo]

Annual Sensitivity Summary

Currency Annual Net Income Sensitivity

+/-

$100/MT = +/-

$240 million

LME Aluminum Annual Net Income Sensitivity

Australian $

+/-

$11 million

per 0.01 change in USD / AUD

Brazilian $

+/-

$ 3 million

per 0.01 change in BRL / USD

Euro €

+/-

$ 2 million

per 0.01 change in USD / EUR

Canadian $

+/-

$ 5 million

per 0.01 change in CAD / USD

Norwegian Kroner

+/-

$ 5 million

per 0.10 change in NOK / USD

43 |

[Alcoa Logo]

Revenue Change by Market

0%

1%

(1%)

(7%)

(4%)

5%

(8%)

37%

5%

5%

3%

7%

5%

(11%)

2%

8%

6%

(17%)

(5%)

(5%)

4Q’12 Third-Party Revenue

Sequential

Change

Year-Over-Year

Change

44

16%

3%

6%

5%

8%

2%

13%

2%

13%

32%

Aerospace

Automotive

B&C

Comm. Transport

Industrial Products

IGT

Packaging

Distribution/Other*

Alumina

Primary Metals |

[Alcoa Logo]

Reconciliation of ATOI to Consolidated Net (Loss) Income

Attributable to Alcoa

45

(in millions)

4Q

11

2011

1

Q

12

2

Q12

3

Q

12

4

Q

12

20

12

$

$

$

$

$

$

$

Unallocated amounts (net of tax):

Impact of LIFO

Interest expense

Noncontrolling interests

Corporate expense

Restructuring and other charges

Discontinued operations

Other

Alcoa

$

$

$

$

$

$

$

235

(7)

(81)

32

(62)

(2)

–

(258)

(143)

563

8

(78)

(15)

(87)

(56)

–

(93)

242

1,369

20

(319)

29

(282)

(75)

–

(551)

191

275

19

(80)

17

(69)

(10)

–

(154)

(2)

296

–

(80)

(5)

(64)

(7)

–

(46)

94

1,893

(38)

(340)

(194)

(290)

(196)

(3)

(221)

611

241

11

(81)

(28)

(71)

(161)

2

(104)

(191)

Consolidated net (loss) income attributable to

Total segment ATOI |

[Alcoa Logo]

Reconciliation

of Adjusted Income

46

(Loss) income from continuing operations attributable to Alcoa – as adjusted is a non-GAAP

financial measure. Management believes that this measure is meaningful to investors because management reviews the operating results of Alcoa excluding the impacts of restructuring and other charges, discrete

tax items, and other special items (collectively, “special items”). There can be no

assurances that additional special items will not occur in future periods. To compensate for this limitation, management believes that it is appropriate to consider both (Loss) income from continuing operations attributable to

Alcoa determined under GAAP as well as (Loss) income from continuing operations attributable to Alcoa

– as adjusted. * Discrete tax items include the following:

•

for the quarter ended December 31, 2012, a benefit related to the interim period treatment of

losses in jurisdictions for which no tax benefit was recognized during the nine months ended September 30, 2012 ($39); a benefit for a capital loss on an investment ($13); and a net benefit for other

miscellaneous items ($6);

•

for the quarter ended September 30, 2012, an unfavorable impact related to the interim period

treatment of losses in jurisdictions for which no tax benefit was recognized ($35), a benefit as a result of including the anticipated gain from the sale of the Tapoco Hydroelectric Project in the calculation of the

estimated annual effective tax rate ($12), and a net charge for other miscellaneous items ($3);

•

for the quarter ended December 31, 2011, charges for a tax rate change in Hungary and a tax law

change regarding the utilization of net operating losses in Italy ($8), a charge related to the 2010 change in the tax treatment of federal subsidies received related to prescription drug benefits provided

under certain retiree health benefit plans ($7), and a net benefit for other miscellaneous items ($3);

•

for the year ended December 31, 2012, a benefit for a capital loss on an investment ($13); a

benefit as a result of including the then anticipated gain from the sale of the Tapoco Hydroelectric Project in the calculation of the estimated annual effective tax rate applied to the results for the nine months

ended September 30, 2012 ($12); a charge related to prior year U.S. taxes on certain depletable assets

($8); and a net benefit for other miscellaneous items ($5); and •

for the year ended December 31, 2011, charges for a tax rate change in Hungary and a tax law

change regarding the utilization of net operating losses in Italy ($8); a charge related to the 2010 change in the tax treatment of federal subsidies received related to prescription drug benefits provided under

certain retiree health benefit plans ($7); a net benefit for adjustments made related to the filing of

2010 tax returns in various jurisdictions ($5); and a net benefit for other miscellaneous items ($8).

** Other special items include the following:

•

for the quarter ended December 31, 2012, a gain on the sale of the Tapoco Hydroelectric Project

($161: $275 is included in the Primary Metals segment and $(114) is included in Corporate); a net favorable change in certain mark-to-market energy derivative contracts ($12); interest income on an

escrow deposit ($8); and uninsured losses related to fire damage to the cast house at the Massena, NY

location ($7); •

for the quarter ended September 30, 2012, an increase in the environmental reserve mostly

related to the Grasse River remediation in Massena, NY and two new remediation projects at the smelter sites in Baie Comeau, Quebec, Canada and Mosjøen, Norway ($120), a litigation reserve ($15),

uninsured losses related to fire damage to the cast house at the Massena, NY location ($9), and a net

unfavorable change in certain mark-to-market energy derivative contracts ($3); •

for the quarter ended December 31, 2011, a gain on the sale of land in Australia ($18),

uninsured losses, including costs related to flood damage to a plant in Pennsylvania caused by Hurricane Irene, ($14), a net favorable change in certain mark-to-market energy derivative contracts ($8), and the write

off of inventory related to the permanent closure of a smelter in the U.S ($4);

•

for the year ended December 31, 2012, a gain on the sale of the Tapoco Hydroelectric Project

($161: $275 is included in the Primary Metals segment and $(114) is included in Corporate); a net increase in the environmental reserve related to the Grasse River remediation in Massena, NY, remediation

at two former locations, East St. Louis, IL and Sherwin, TX, and two new remediation projects at the

smelter sites in Baie Comeau, Quebec, Canada and Mosjøen, Norway ($133); a litigation reserve ($33); uninsured losses related to fire damage to the cast house at the Massena, NY location ($28);

interest income on an escrow deposit ($8); and a net favorable change in certain mark-to-market

energy derivative contracts ($5); and •

for the year ended December 31, 2011, a net favorable change in certain mark-to-market

energy derivative contracts ($36); a net charge comprised of expenses for the early repayment of Notes set to mature in 2013 due to the premiums paid under the tender offers and call option and gains from the

termination of related “in-the-money” interest rate swaps ($32); uninsured losses,

including costs related to flood damage to a plant in Pennsylvania caused by Hurricane Irene, ($25); a gain on the sale of land in Australia ($18); costs related to acquisitions of the aerospace fastener business of

TransDigm Group Inc. and full ownership of carbothermic smelting technology from ORKLA ASA ($8); and

the write off of inventory related to the permanent closure of a smelter in the U.S ($4).

(in millions, except per-

share amounts)

(Loss) Income

Diluted EPS

Quarter ended

Year ended

Quarter ended

Year ended

December 31,

September 30,

December 31,

December 31,

December 31,

December 31,

September 30,

December 31,

December 31,

December 31,

2011

2012

2012

2011

2012

2011

2012

2012

2011

2012

Net (loss) income

attributable to Alcoa

$ (191)

$ (143)

$ 242

$ 611

$ 191

$ (0.18)

$ (0.13)

$ 0.21

$ 0.55

$ 0.18

Income (loss) from

discontinued

operations

2

–

–

(3)

–

(Loss) income from

continuing

operations

attributable to Alcoa

(193)

(143)

242

614

191

(0.18)

(0.13)

0.21

0.55

0.18

Restructuring and other

charges

155

2

54

181

73

Discrete tax items*

12

26

(58)

2

(22)

Other special items**

(8)

147

(174)

15

20

(Loss) income from

continuing operations

attributable to Alcoa

-

as adjusted

$ (34)

$ 32

$ 64

$ 812

$ 262

(0.03)

0.03

0.06

0.72

0.24 |

[Alcoa Logo]

Reconciliation

of Alcoa Adjusted EBITDA

47

($ in millions)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

4Q11

3Q12

4Q12

Net

income (loss)

attributable to

Alcoa

420

938

1,310

1,233

2,248

2,564

(74)

(1,151)

$

254

611

191

$

(191)

(143)

$

242

Add:

Net income (loss)

attributable to

noncontrolling

interests

181

212

233

259

436

221

61

138

194

(29)

28

(32)

15

Cumulative effect

of accounting

changes

(34)

47

–

2

–

–

–

–

–

–

–

–

–

–

Loss (income)

from discontinued

operations

101

–

27

50

(22)

250

303

166

8

3

–

(2)

–

–

Provision (benefit)

for income taxes

307

367

546

464

853

1,623

342

(574)

148

255

162

(74)

(33)

143

Other (income)

expenses, net

(175)

(278)

(266)

(478)

(236)

(1,920)

(59)

(161)

5

(87)

(341)

(40)

(2)

(345)

Interest expense

350

314

271

339

384

401

407

470

494

524

490

125

124

Restructuring and

other charges

398

(28)

(29)

266

507

268

939

237

207

281

87

232

2

60

Provision for

depreciation,

depletion, and

amortization

1,037

1,227

1,252

1,244

1,234

1,311

1,450

1,479

1,460

367

366

362

Adjusted EBITDA

2,585

2,682

3,234

3,362

4,795

359

2,704

3,260

2,020

445

282

597

Sales

18,879

21,370

28,950

26,901

18,439

21,013

24,951

23,700

5,833

5,898

Adjusted EBITDA

Margin

14%

14%

19%

16%

12%

2%

13%

13%

9%

7%

5%

10%

17,691

15%

1,110

1,142

15%

24,149

120

3,313

5,422

5,989

29,280

Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and

amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales

minus the following items: Cost of goods sold; Selling, general administrative, and other expenses;

Research and development expenses; and Provision for depreciation, depletion, and amortization. Adjusted EBITDA

is a non-GAAP financial measure. Management believes that this measure is meaningful to

investors because Adjusted EBITDA provides additional information with respect to Alcoa’s operating performance and the

Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not

be comparable to similarly titled measures of other companies. $

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

365

$

$

$

$

$

$ |

[Alcoa Logo]

Reconciliation

of Alumina Adjusted EBITDA

48

($ in millions, except

per metric ton

amounts

)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

4Q11

3Q12

4Q12

After-tax operating

income (ATOI)

$ 315

$ 415

$ 632

$ 682

$ 1,050

$ 956

$

727

$ 112

$ 301

$ 607

$ 90

$ 125

$ (9)

$ 41

Add:

Depreciation,

depletion, and

amortization

139

147

153

172

192

267

268

292

406

444

455

112

120

107

Equity (income)

loss

(1)

–

(1)

–

2

(1)

(7)

(8)

(10)

(25)

(5)

2

(2)

(1)

Income taxes

130

161

240

246

428

340

277

(22)

60

179

(27)

33

(22)

2

Other

(14)

(55)

(46)

(8)

(6)

2

(26)

(92)

(5)

(44)

(8)

(43)

(1)

(4)

Adjusted EBITDA

$ 569

$ 668

$ 978

$ 1,092

$ 1,666

$

1,564

$ 1,239

$ 282

$ 752

$ 1,161

$ 505

$ 229

$

86

$ 145

Production

(thousand metric

tons) (kmt)

13,027

13,841

14,343

14,598

15,128

15,084

15,256

14,265

15,922

16,486

16,342

4,178

4,077

4,079

Adjusted EBITDA/

Production ($ per

metric ton)

$ 44

$ 48

$ 68

$ 75

$ 110

$ 104

$ 81

$ 20

$ 47

$ 70

$ 31

$ 55

$ 21

$ 36

Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and

amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales

minus the following items: Cost of goods sold; Selling, general administrative, and other expenses;

Research and development expenses; and Provision for depreciation, depletion, and amortization. The Other line

in the table above includes gains/losses on asset sales and other nonoperating items. Adjusted

EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors

because Adjusted EBITDA provides additional information with respect to Alcoa’s operating

performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not be

comparable to similarly titled measures of other companies. |

[Alcoa Logo]

Reconciliation

of Primary Metals Adjusted EBITDA

($ in millions, except

per metric ton

amounts)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

4Q11

3Q12

4Q12

After-tax operating

income (ATOI)

$ 650

$ 657

$ 808

$ 822

$ 1,760

$ 1,445

$ 931

$ (612)

$ 488

$ 481

$ 309

$ (32)

$ (14)

$ 316

Add:

Depreciation,

depletion, and

amortization

300

310

326

368

395

410

503

560

571

556

532

136

130

134

Equity (income) loss

(44)

(55)

(58)

12

(82)

(57)

(2)

26

(1)

7

27

3

5

11

Income taxes

266

256

314

307

726

542

172

(365)

96

92

106

(37)

(19)

157

Other

(47)

12

20

(96)

(13)

(27)

(32)

(176)

(7)

2

(422)

1

2

(423)

Adjusted EBITDA

$ 1,125

$ 1,180

$ 1,410

$ 1,413

$ 2,786

$ 2,313

$ 1,572

$ (567)

$ 1,147

$ 1,138

$ 552

$ 71

$ 104

$ 195

Production

(thousand metric

tons) (kmt)

3,500

3,508

3,376

3,554

3,552

3,693

4,007

3,564

3,586

3,775

3,742

962

938

912

Adjusted EBITDA /

Production ($ per

metric ton)

$ 321

$ 336

$ 418

$ 398

$ 784

$ 626

$ 392

$ (159)

$ 320

$ 301

$ 148

$ 74

$ 111

$ 214

Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and

amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following

items: Cost of goods sold; Selling, general administrative, and other expenses; Research and

development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses on

asset sales and other nonoperating items. Adjusted EBITDA is a non-GAAP financial

measure. Management believes that this measure is meaningful to investors because Adjusted EBITDA provides additional information with respect to

Alcoa’s operating performance and the Company’s ability to meet its financial

obligations. The Adjusted EBITDA presented may not be comparable to similarly titled measures of other companies.

49 |

[Alcoa Logo]

Reconciliation of Global Rolled Products Adjusted

EBITDA

($ in millions, except

per metric ton

amounts)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

4Q11

3Q12

4Q12

After-tax operating

income (ATOI)

$ 225

$ 222

$ 254

$ 278

$ 233

$ 178

$ (3)

$ (49)

$ 220

$ 266

$ 358

$ 26

$ 98

$ 69

Add:

Depreciation,

depletion, and

amortization

184

190

200

220

223

227

216

227

238

237

229

58

57

58

Equity loss

4

1

1

–

2

–

–

–

–

3

6

3

1

2

Income taxes

90

71

75

121

58

92

35

48

92

104

167

10

44

31

Other

(8)

(5)

1

1

20

1

6

(2)

1

1

(2)

1

(2)

–

Adjusted EBITDA

$ 495

$ 479

$ 531

$ 620

$ 536

$ 498

$ 254

$ 224

$ 551

$ 611

$ 758

$ 98

$ 198

$ 160

Total shipments

(thousand metric

tons) (kmt)

1,814

1,893

2,136

2,250

2,376

2,482

2,361

1,888

1,755

1,866

1,943

436

501

465

Adjusted EBITDA

/

Total shipments

($ per metric ton)

$ 273

$ 253

$ 249

$ 276

$ 226

$ 201

$ 108

$ 119

$ 314

$ 327

$ 390

$ 225

$ 395

$ 344

Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and

amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following

items: Cost of goods sold; Selling, general administrative, and other expenses; Research and

development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses

on asset sales and other nonoperating items. Adjusted EBITDA is a non-GAAP financial

measure. Management believes that this measure is meaningful to investors because Adjusted EBITDA provides additional information with

respect to Alcoa’s operating performance and the Company’s ability to meet its financial

obligations. The Adjusted EBITDA presented may not be comparable to similarly titled measures of other companies.

50 |

[Alcoa Logo]

Reconciliation of Engineered Products and Solutions

Adjusted EBITDA

51

($ in millions)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

4Q11

3Q12

4Q12

After-tax operating

income (ATOI)

$ 63

$ 124

$ 156

$ 271

$ 365

$ 435

$ 533

$ 315

$ 415

$ 539

$ 612

$ 122

$ 160

$ 137

Add:

Depreciation,

depletion, and

amortization

150

166

168

160

152

163

165

177

154

158

158

39

39

40

Equity loss

(income)

–

–

–

–

6

–

–

(2)

(2)

(1)

–

–

–

–

Income taxes

39

55

65

116

155

192

222

139

195

260

297

59

79

69

Other

35

11

106

(11)

(2)

(7)

2

1

–

(1)

(8)

–

(1)

(7)

Adjusted EBITDA

$ 287

$ 356

$ 495

$ 536

$ 676

$ 783

$ 922

$ 630

$ 762

$ 955

$ 1,059

$ 220

$ 277

$ 239

Total sales

$ 3,492

$ 3,905

$ 4,283

$ 4,773

$ 5,428

$ 5,834

$ 6,199

$ 4,689

$ 4,584

$ 5,345

$ 5,525

$ 1,355

$ 1,367

$ 1,348

Adjusted EBITDA

Margin

8%

9%

12%

11%

12%

13%

17%

18%

19%

16%

20%

18%

Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and

amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to

Sales minus the following items: Cost of goods sold; Selling, general administrative, and other

expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. The

Other line in the table above includes gains/losses on asset sales and other nonoperating items.

Adjusted EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to

investors because Adjusted EBITDA provides additional information with respect to Alcoa’s

operating performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented

may not be comparable to similarly titled measures of other companies.

15%

13% |

[Alcoa Logo]

Reconciliation

of Free Cash Flow

52

(in

millions)

Quarter ended

Year ended

March 31,

2011

June 30,

2011

September 30,

2011

December 31,

2011

March 31,

2012

June 30,

2012

September30,

2012

December 31,

2012

December 31,

2011

December 31,

2012

Cash from

operations

$

(236)

$ 798

$ 489

$ 1,142

$ (236)

$ 537

$ 263

$ 933

$ 2,193

$ 1,497

Capital

expenditures

(204)

(272)

(325)

(486)

(270)

(291)

(302)

(398)

(1,287)

(1,261)

Free cash

flow

$ (440)

$ 526

$ 164

$ 656

$ (506)

$ 246

$ (39)

$ 535

$ 906

$ 236

Free Cash Flow is a non-GAAP financial measure. Management believes that this measure is meaningful

to investors because management reviews cash flows generated from operations after taking into

consideration capital expenditures due to the fact that these expenditures are considered necessary to

maintain and expand Alcoa’s asset base and are expected to generate future cash flows from operations.

It is important to note that Free Cash Flow does not represent the residual cash flow available for

discretionary expenditures since other non-discretionary expenditures, such as mandatory debt service

requirements, are not deducted from the measure.

|

[Alcoa Logo]

Reconciliation of Free Cash Flow, con’t

53

Cash from

operations

$ 608

$ (271)

$

$

184

$ 1,124

$ 199

$ 300

$ 392

$ 1,370

Capital

expenditures

Free cash

flow

328

$ (409)

$ (742)

$

(90)

$ (186)

$ 761

$ (22)

$ 87

$ 176

$ 1,005

(418)

(221)

(213)

(216)

(365)

(471)

(370)

(363)

(1,017)

Free Cash Flow is a non-GAAP financial measure. Management believes that this measure is

meaningful to investors because management reviews cash flows generated from operations after taking into consideration capital expenditures due to

the fact that these expenditures are considered necessary to maintain and expand Alcoa’s asset

base and are expected to generate future cash flows from operations. It is important to note that Free Cash Flow does not represent the residual

cash flow available for discretionary expenditures since other non-discretionary expenditures, such

as mandatory debt service requirements, are not deducted from the measure. Quarter ended

(in millions)

December 31,

2008

March 31,

2009

June 30,

2009

September 30,

2009

December 31,

2009

March 31,

2010

June 30,

2010

September 30,

2010

December 31,

2010 |

[Alcoa Logo]

Days

Working Capital

54

($ in millions)

Quarter ended

December 31,

2011

March 31,

2012

June 30,

2012

September 30,

2012

December 31,

2012

Receivables from customers, less

allowances

$ 1,571

$ 1,526

$ 1,575

$ 1,619

$ 1,322

Add: Deferred

purchase price receivable*

–

254

141

81

71

Receivables from customers, less

allowances, as adjusted

1,571

1,780

1,716

1,700

1,393

Add: Inventories

2,899

3,097

3,051

2,973

2,825

Less: Accounts payable, trade

2,692

2,734

2,633

2,590

2,692

Working Capital

$ 1,778

$ 2,143

$ 2,134

$ 2,083

$ 1,526

Sales

$ 5,989

$ 6,006

$ 5,963

$ 5,833

$ 5,898

Days Working Capital

27

32

33

33

24

Days Working Capital = Working Capital divided by

(Sales/number of days in the quarter).

.

.

*

The deferred purchase price receivable relates to an arrangement to sell certain customer

receivables to a financial institution on a recurring basis. Alcoa is adding back

this receivable for the purposes of the Days Working Capital calculation. |

[Alcoa Logo]

Reconciliation

of Net Debt

55

(in millions)

December 31,

2006

2007

2008

2009

2010

2011

2012

Short-term borrowings

$ 46

0

$ 563

$ 478

$ 176

$ 92

$ 62

$ 53

Commercial paper

340

856

1,535

–

–

224

–

Long-term debt due within

one year

510

202

56

669

231

445

465

Long-term debt, less amount

due within one year

5,909

6,371

8,509

8,974

8,842

8,640

8,311

Total debt

7,2

19

7,992

10,578

9,819

9,165

9,371

8,829

Less: Cash and cash

equivalents

Net debt

$ 6,71

3

$ 7,509

$ 9,816

$ 8,338

$ 7,622

$ 7,432

$ 6,968

Net debt is a non-GAAP financial measure. Management believes that this measure is meaningful

to investors because management assesses Alcoa’s leverage position after factoring in available cash that could be used to repay outstanding

debt.

506

483

762

1,481

1,543

1,939

1,861 |

[Alcoa Logo]

Reconciliation

of Net Debt-to-Capital

56

($

in millions)

Debt-to-Capital

Cash and Cash

Net Debt-to-

Capital

Total Debt

$

Commercial paper

–

one year

465

due within one year

8,311

Numerator

1,861

$

6,968

Total Capital

Total debt

$

Total equity

Denominator

Ratio

December 31, 2012

Short-term borrowings

Long-term debt due within

Long-term debt, less amount

53

$

8,829

16,507

$

34.8%

$

1,861

$

23,475

29.7%

$

Net debt-to-capital is a non-GAAP financial measure. Management believes that this measure

is meaningful to investors because management assesses Alcoa’s leverage position after

factoring in available cash that could be used to repay outstanding debt.

8,829

25,336

Equivalents |

[Alcoa Logo]

Composition of Upstream Production Costs

57

Refining Cost Structure

Smelting Cost Structure

1

Natural gas information corresponds to Point Comfort, as Australia is priced on a

rolling 16 quarter average Fuel Oil

14%

Natural gas

10%

Caustic

11%

Bauxite

23%

Conversion

42%

Alumina

32%

Carbon

15%

Power

25%

Materials

6%

Conversion

22%

Input Cost

Inventory flow

Pricing

convention

Annual ATOI

Sensitivity

Fuel oil

1 –

2 months

Prior month

$4m per $1/bbl

Natural gas

N/A

Spot

1

$16m per $1/GJ

1

Caustic soda

3 -

6 months

Spot & semi-

annual

$9m per

$10/DMT

Input Cost

Inventory flow

Pricing convention

Annual ATOI

Sensitivity

Coke

1 -

2 months

Spot, quarterly &

semi-annual

$9m per

$10/MT

Pitch

1 -

2 months

Spot, quarterly &

semi-annual

$2.5m per

$10/MT |