Attached files

| file | filename |

|---|---|

| EX-99.1 - THE PRESS RELEASE, DEEMED "FILED" UNDER THE SECURITIES EXCHANGE ACT OF 1934 - WELLS FARGO & COMPANY/MN | d450286dex991.htm |

| 8-K - FORM 8-K - WELLS FARGO & COMPANY/MN | d450286d8k.htm |

4Q12 Quarterly Supplement

January 11, 2013

Exhibit 99.2 |

Wells Fargo

4Q12 Supplement 1

Appendix

Pages 23-38

-

Non-strategic/liquidating loan portfolio risk reduction

24

-

Purchased credit-impaired (PCI) portfolios

25

-

PCI nonaccretable difference

26

-

PCI accretable yield

27

-

PCI accretable yield (Commercial & Pick-a-Pay)

28

-

Pick-a-Pay mortgage portfolio

29

-

Pick-a-Pay credit highlights

30

-

Real estate 1-4 family first mortgage portfolio

31

-

Home equity portfolio

32

-

Credit card portfolio

33

-

Auto portfolios

34

-

Student lending portfolio

35

Tier 1 common equity under Basel I

36

Tier 1 common equity under Basel III

(Estimated)

37

Forward-looking statements and

additional information

38

Table of contents

4Q12 Results

-

4Q12 Results

Page 2

-

2012 Results

3

-

Strong diversification

4

-

Selected 4Q12 items

5

-

Independent Foreclosure Review Settlement

6

-

Balance Sheet and credit overview

7

-

Income Statement overview

8

-

Loans

9

-

Deposits

10

-

Net interest income

11

-

Noninterest income

12

-

Noninterest expense and efficiency ratio

13

-

Environmentally-elevated costs

14

-

Community Banking

15

-

Wholesale Banking

16

-

Wealth, Brokerage and Retirement

17

-

Credit quality

18-19

-

Mortgage servicing

20

-

Capital

21

-

Summary –

strong 4Q12

22 |

Wells Fargo

4Q12 Supplement 2

Record earnings of $5.1 billion, up 24% year-

over-year (YoY) and 3% linked quarter (LQ)

Record diluted earnings per common share of

$0.91, up 25% YoY and 3% LQ

Total revenue of $21.9 billion up 7% YoY and 3%

LQ on growth in noninterest income

Efficiency ratio of 58.8%

(1)

Pre-tax pre-provision profit

(2)

of $9.1 billion, up

12% YoY and down $49 million LQ

Strong credit performance

ROA = 1.46%, up 21 bps YoY and up 1 bp LQ

ROE = 13.35%, up 138 bps YoY and down

3 bps LQ

Capital levels remained strong

-

10.12% Tier 1 common equity ratio under Basel I

and estimated Tier 1 common equity ratio under

Basel III of 8.18%

(3)

4Q12 Results

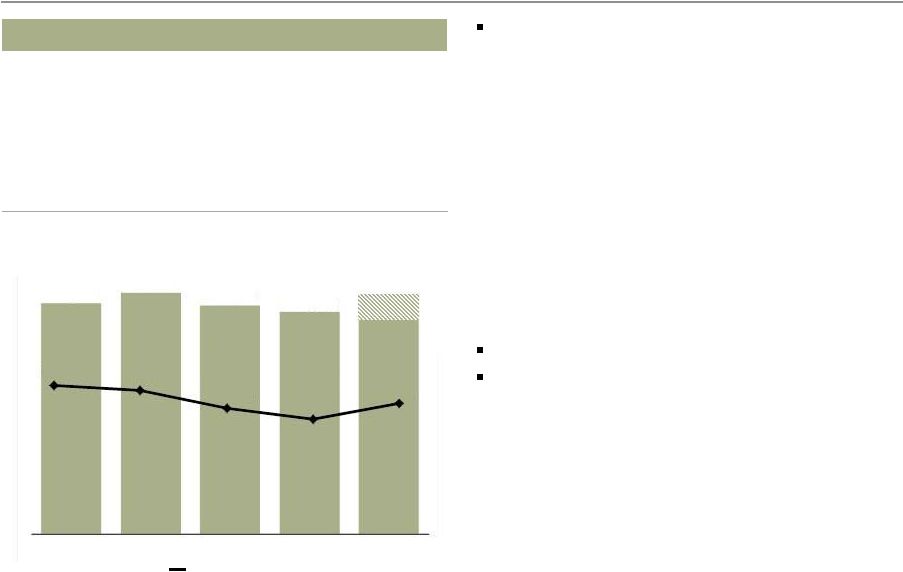

Wells Fargo Net Income

($ in millions)

4,107

4,248

4,622

4,937

5,090

4Q11

1Q12

2Q12

3Q12

4Q12

(2) Pre-tax pre-provision profit (PTPP) is total revenue less noninterest

expense. Management believes PTPP is a useful financial measure because it enables

investors and others to assess the Company’s ability to generate capital to cover credit

losses through a credit cycle. (3) Estimated Basel III calculation based on management’s current interpretation of

the Basel III capital rules proposed by federal banking agencies in notices of proposed

rulemaking announced in June 2012. The proposed rules and interpretations and assumptions used in estimating Basel III calculations are

subject to change depending on final promulgation of Basel III capital rules. See pages

36-37 for additional information regarding Tier 1 common equity ratios. (1) Efficiency ratio defined as noninterest

expense divided by total revenue (net interest income plus noninterest income). |

Wells Fargo

4Q12 Supplement 3

15.9

18.9

2011

2012

2012 Results

Revenue

($ in billions)

Net Income

($ in billions, except EPS)

Diluted earnings per common share

Period-end Loans

($ in billions)

Return on Assets

$2.82

$3.36

1.25%

1.41%

2011

2012

Return on Equity

11.93%

12.95%

2011

2012

769.6

799.6

2011

2012

Period-end Core Deposits

($ in billions)

872.6

945.7

2011

2012

80.9

86.1

2011

2012 |

Wells Fargo

4Q12 Supplement 4

Balanced Spread and

Fee Income

Diversified Fee

Generation

Deposit Service Charges

11%

Card Fees

6%

Other Banking Fees

11%

Mortgage Servicing, net

2%

Insurance

3%

Net Gains from Trading

2%

Noninterest Income

52%

Net Interest Income

48%

Diversified Loan

Portfolio

Commercial Loans

40%

Consumer Loans

55%

Strong diversification

Foreign Loans

5%

Mortgage Orig./Sales, net

25%

Trust, Investment & IRA fees

10%

Commissions & All Other

Investment Fees

19%

Other

Noninterest

Income

(1)

55%

40%

5%

52%

48%

11%

10%

19%

6%

11%

2%

25%

3%

2%

11%

11%

All data is for 4Q12. (1) Other noninterest income includes net gains (losses) on debt

securities available for sale, equity investments, operating leases and all other

noninterest income. |

Wells Fargo

4Q12 Supplement 5

Selected 4Q12 items

(Pre-tax except for tax expense and EPS)

$ in millions

EPS

(1)

Comments

Noninterest

income:

Above-average

quarterly

equity

gains

(2)

393

$

0.05

$

Equity gains reflect strong business results including

the gain on the sale of Becker Underwood

Noninterest

expense:

Elevated operating losses

(644)

(0.09)

Incremental accrual to fully reserve for Wells

Fargo's costs associated with the Independent

Foreclosure Review Settlement and additional

remediation-related costs

Wells Fargo Foundation Contribution

(250)

(0.03)

Included in other noninterest expense

Taxes

Lower tax expense

332

0.06

Effective tax rate of 27.4% included a $332 million

benefit associated with the realization for tax

purposes of a previously written-down Wachovia life

insurance investment

4Q12

(1) 4Q12 effective tax rate of 27.4% used in the calculations of EPS. (2) 4Q12 net gains

from equity investments of $715 million were $393 million higher than previous seven quarter average net gains of $322 million.

Selected item and Financial Statement line affected

|

Wells Fargo

4Q12 Supplement 6

Independent Foreclosure Review (IFR) Settlement

On 1/7/13, 10 servicers, including Wells Fargo, entered into settlement agreements with the OCC

and FRB As part of the settlement servicers have agreed to:

-

Make direct cash payments of $3.3 billion

-

Provide $5.2 billion in additional assistance, such as modifications to consumers

Wells Fargo’s portion of the cash settlement is $766 million

-

$644 million incremental accrual in 4Q12 to fully reserve for settlement and additional

remediation costs Wells Fargo has committed to an additional $1.2 billion for

foreclosure prevention -

Covered through allowance for credit losses and purchased credit-impaired nonaccretable

difference Settlement ends the Independent Foreclosure Review programs created by the

April 2011 Interagency Consent Order which cost Wells Fargo ~$125 million per quarter

in 2012 |

Wells Fargo

4Q12 Supplement 7

Balance Sheet and credit overview

Balance Sheet

Loans

Total period-end loans up $17.0 billion

-

Core loans increased $21.1 billion reflecting $8.7 billion in commercial growth

and the retention of $9.7 billion of 1-4 family conforming first mortgage

production

-

Non-strategic/liquidating

portfolio

decreased

$4.1

billion

(1)

Short-term investments/

Fed funds sold

Up $36.9 billion driven by strong deposit growth

Securities available for

sale (AFS)

Up $5.8 billion driven by new investments

-

Agency MBS purchases occurred late in the quarter as rates rose and yields

became more attractive

Deposits

Up $50.6 billion on growth across the franchise

Long-term debt

Down $3.4 billion as $4.4 billion in maturities were partially offset by $1.8 billion in

issuances

Common stock

repurchases

Purchased 42.1 million common shares in the quarter and an additional estimated

5.9

million

shares

through

a

forward

repurchase

transaction

that

is

expected

to

settle in 1Q13

Credit

Strong

credit

performance;

$250

million

reserve

release

(3)

on

strong

credit

and

incorporates estimated losses attributable to Hurricane Sandy

4Q12 effect of 3Q12

OCC guidance

(2)

implementation on credit

$394

million

increase

in

nonaccrual

loans

($264

million

from

the

completion

of

implementation and $130 million from 4Q12 activity)

$321 million in net charge-offs ($271 million from the completion of implementation

and $50 million from 4Q12 activity)

Period-end balances. All result comparisons are 4Q12 compared with 3Q12. (1) See pages 9

and 24 for additional information regarding core loans and the non-strategic/liquidating portfolio, which comprises the Pick-a-Pay,

liquidating home equity, legacy WFF indirect auto, legacy WFF debt consolidation, Education

Finance-government guaranteed, and legacy Wachovia commercial & industrial,

commercial real estate, foreign and other PCI loan portfolios.

(2) Office of the Comptroller of the Currency update to the Bank Accounting Advisory

Series issued third quarter 2012 (OCC guidance). The OCC guidance requires

write-down of performing consumer loans discharged in bankruptcy to net realizable collateral value.

(3) Provision expense minus net charge-offs. |

Wells Fargo

4Q12 Supplement 8

Income Statement overview

Total revenue

Revenue of $21.9 billion, up $735 million, or 3%

Net interest income

NII essentially flat

Net interest margin (NIM) down 10 bps to 3.56% driven by strong deposit growth

Noninterest income

Mortgage banking up $261 million

-

Net servicing income up $53 million

-

Gain on sale revenue up $208 million (despite $340 million in forgone revenue

resulting

from

the

retention

of

conforming

production)

on

higher

margins

and

lower repurchase reserve build

Trust & investment fees up $245 million on stronger investment banking and higher

asset based fees in retail brokerage

Market sensitive revenues

(1)

up $231 million

-

Gains on equity investments more than offset weaker trading and losses on debt

securities

Noninterest expense

Operating losses up $672 million reflecting the $644 million incremental accrual to fully

reserve for the settlement costs associated with the IFR Settlement and additional

remediation-related costs

All other expense up $267 million driven by the $250 million contribution to the

Foundation

Personnel expense down $88 million and included $82 million lower deferred

compensation expense (P&L neutral)

All result comparisons are 4Q12 compared with 3Q12.

(1) Includes net gains from trading activities, net gains (losses) on debt securities

available for sale and net gains from equity investments. |

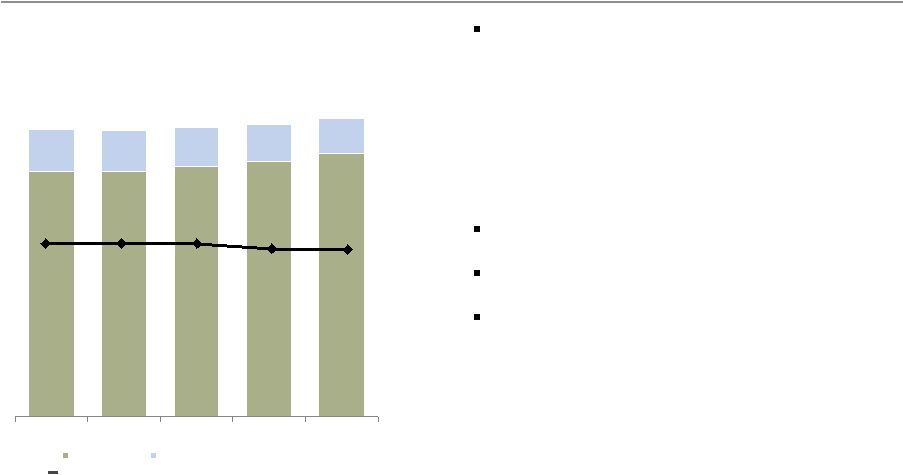

Wells Fargo

4Q12 Supplement 9

657.3

658.3

672.1

684.0

705.1

112.3

108.2

103.1

98.6

94.5

769.6

766.5

775.2

782.6

799.6

4Q11

1Q12

2Q12

3Q12

4Q12

Core loans

Non-strategic/liquidating loans

Loans

Strong core loan growth

Period-end loans up $30.0 billion YoY and $17.0

billion from 3Q12

-

Commercial loans up $8.7 billion LQ on growth

in C&I and CRE

-

Consumer loans up $8.3 billion LQ as growth in

first mortgage, auto, credit card and private

student lending was partially offset by a $2.6

billion decline in junior lien mortgage

•

Includes retention of $9.7 billion of 1-4 family

conforming first mortgages

Non-strategic/liquidating loans

(1)

down $17.8

billion YoY and $4.1 billion from 3Q12

Core loans grew $47.8 billion YoY and $21.1

billion LQ

Total average loan yield of 4.58% down 5 bps LQ

-

Core loan yield excluding the non-strategic/

liquidating portfolio was down 5 bps

-

Non-strategic/liquidating portfolio yield

of 5.17%

Period-end balances.

(1) See page 24 for additional information regarding the non-strategic/liquidating

portfolio, which comprises the Pick-a-Pay, liquidating home equity, legacy WFF

indirect auto, legacy WFF debt consolidation, Education Finance-government guaranteed, and

legacy Wachovia commercial & industrial, commercial real estate, foreign and other

PCI loan portfolios. Period–end Loans Outstanding

($ in billions)

(1)

Total average loan yield

4.81%

4.81%

4.83%

4.63%

4.58% |

Wells Fargo

4Q12 Supplement 10

Deposits

Strong growth and reduced average cost

Average deposits up $64.0 billion YoY and $29.6

billion LQ driven by growth across the franchise

Average core deposits of $928.8 billion up $63.9

billion YoY and $33.5 billion from 3Q12

-

118% of average loans

-

Average retail core deposits up 6% YoY and

10% annualized LQ

Average core checking and savings up $72.0

billion, or 9% YoY, and $34.9 billion, or 4% from

3Q12

-

94% of average core deposits

Average deposit cost of 16 bps down 2 bps

from 3Q12

Average Deposits and Rates

($ in billions)

Average Core Checking and Savings

($ in billions)

800.1

837.2

872.1

4Q11

3Q12

4Q12

0.22%

0.18%

0.16%

665.4

679.3

689.2

246.7

267.2

286.9

912.1

946.5

976.1

4Q11

3Q12

4Q12

Interest-bearing deposits

Noninterest-bearing deposits

Average deposit cost |

Wells Fargo

4Q12 Supplement 11

Tax-equivalent net interest income

(1)

essentially flat LQ

Average earning assets up $35.6 billion or 3%

LQ

-

Short-term investments/fed funds sold up

$25.5 billion

-

Loans up $10.5 billion

-

AFS securities up $2.9 billion

-

Trading assets up $2.5 billion

-

Mortgages held for sale declined $4.9 billion

NIM of 3.56%, down 10 bps, from 3Q12 on:

-

Strong deposit inflows with proceeds

invested in short-term investments/fed funds

sold = (8) bps

-

Continued balance sheet repricing = (5) bps

•

Securities (3) bps and loans (2) bps

-

Variable income = +3 bps

2012 tax-equivalent NII increase driven by lower

funding costs and growth in earning assets

2012 NIM decline driven by strong deposit flows

Net interest income

Net Interest Income (TE)

(1)

($ in millions)

Net Interest Margin (NIM)

(1)

11,083

11,058

11,213

10,820

10,841

4Q11

1Q12

2Q12

3Q12

4Q12

3.89%

3.91%

3.91%

3.66%

3.56%

43,459

43,931

2011

2012

3.94%

3.76%

Tax-equivalent net interest income is based on the federal statutory rate of 35% for the

periods presented. Net interest income was $10,892 million, $10,888 million, $11,037

million, $10,662 million, $10,643 million, $42,763 million and $43,230 million for 4Q11, 1Q12, 2Q12, 3Q12, 4Q12, 2011 and 2012

respectively.

|

Wells Fargo

4Q12 Supplement 12

Noninterest income

Deposit service charges up 3% LQ reflecting product

and pricing changes

Trust and investment fees up 8% LQ primarily due to

stronger investment banking and retail brokerage

asset-based fees

Other fees up $96 million, or 9% LQ, on stronger

investment banking advisory fees

Mortgage banking up $261 million, or 9%, LQ

-

Net servicing income up $53 million as higher

net MSR/servicing hedge results were partially

offset by higher unreimbursed foreclosure costs

-

Gain on sale revenue up $208 million on higher

margins and $83 million lower repurchase

reserve build

-

$340 million in forgone revenue from the

retention of conforming production

Insurance down 5% LQ reflecting crop insurance

seasonality

Trading gains down $254 million LQ on lower volumes

and $95 million lower deferred compensation plan

investment income

Equity gains up $551 million reflecting strong

business results including the gain on the sale of

Becker Underwood

9,713

10,748

10,252

10,551

11,305

4Q11

1Q12

2Q12

3Q12

4Q12

vs

vs

($ in millions)

4Q12

3Q12

4Q11

Noninterest income

Service charges on deposit accounts

$

1,250

3

%

15

Trust and investment fees

3,199

8

20

Card fees

736

(1)

8

Other fees

1,193

9

9

Mortgage banking

3,068

9

30

Insurance

395

(5)

(15)

Net gains from trading activities

275

(48)

(36)

(63)

n.m.

n.m.

Net gains from equity investments

715

n.m.

n.m.

Operating leases

170

(22)

183

Other

367

(11)

(52)

Total noninterest income

$

11,305

7

%

16

Net losses on debt securities available

for sale |

Wells Fargo

4Q12 Supplement 13

Noninterest expense and efficiency ratio

(1)

Noninterest expense up $784 million from 3Q12

and included $894 million in higher operating

losses and a foundation contribution

(2)

-

Personnel expense down $88 million, or 1%, on

lower benefits expense including lower deferred

compensation

-

Equipment expense up $32 million reflecting

seasonality

-

Other expense up $892 million and included:

•

Operating losses up $672 million on $644

million incremental accrual to fully reserve for

settlement costs associated with the IFR

Settlement and additional remediation-related

costs

•

Foundation contribution expense of $250

million

Efficiency ratio of 58.8% in 4Q12

Continue to target an efficiency ratio of 55%-

59%

Efficiency Ratio

12,508

12,993

12,397

12,112

12,896

894

(2)

12,002

60.7%

60.1%

58.2%

57.1%

58.8%

4Q11

1Q12

2Q12

3Q12

4Q12

(1) Efficiency ratio defined as noninterest expense divided by total revenue (net

interest income plus noninterest income). (2) Includes $644 million for IFR

Settlement and additional remediation-related costs and $250 million Foundation contribution.

vs

vs

($ in millions)

4Q12

3Q12

4Q11

Noninterest expense

Salaries

$

3,735

2

%

1

Commission and incentive compensation

2,365

-

5

Employee benefits

891

(16)

(12)

Equipment

542

6

(11)

Net occupancy

728

-

(4)

Core deposit and other intangibles

418

-

(10)

FDIC and other deposit assessments

307

(14)

(2)

Other

3,910

30

15

Total noninterest expense

$

12,896

6

%

3 |

Wells Fargo

4Q12 Supplement 14

Environmentally-elevated costs

($ in millions)

Expense description

4Q12

2012

OCC Consent Order:

Independent consultant expense

$

~100

~400

Internal costs associated with foreclosure reviews

~25

~100

Foreclosed asset expense

221

1,061

Mortgage repurchase reserve build

(1)

313

1,665

MSR servicing and foreclosure costs

(2)

127

677

(1)

Contra revenue item. Change in estimate.

(2) Contra revenue item. MSR valuation adjustments include costs to service and

unreimbursed foreclosure costs. |

Wells Fargo

4Q12 Supplement 15

Community Banking

Net income of $2.9 billion, up 14% YoY

and 5% LQ

Noninterest expense increased $631 million LQ

as higher operating losses and the contribution to

the Wells Fargo Foundation were only partially

offset by lower employee benefit costs

Regional Banking

Continued franchise and cross-sell growth

(1)

-

Consumer checking

(2)

essentially flat to

prior year

-

Business checking

(2)

up a net 3.7% YoY

-

Retail bank cross-sell of 6.05 products per

household up from 5.93 in 4Q11

Consumer Lending

Credit card penetration

(1) (3)

rose to 33.1%, up

from 32.1% in 3Q12 and 29.2% in 4Q11

Consumer auto originations of $5.4 billion, down

15% LQ and up 8% YoY

Mortgage originations of $125 billion down

10% LQ and up 4% YoY

-

12% of originations were from HARP

(4)

Quarter-end pipeline of $81 billion down 16% LQ

and up 13% YoY

Managed residential mortgage servicing of $1.9

trillion up 3% YoY

(1) Metrics reported on a one-month lag from reported quarter-end; for

example 4Q12 cross-sell is as of November 2012.

(2) Checking account growth is 12-months ending for each respective period.

(3) Household penetration as of November 2012 and defined as the percentage

of retail banking deposit households that have a credit card with Wells Fargo.

Household

penetration

has

been

redefined

to

include

legacy

Wells

Fargo

Financial accounts.

(4) Home Affordable Refinance Program.

vs

vs

($ in millions)

4Q12

3Q12

4Q11

Net interest income

$

7,166

(1)

%

(3)

Noninterest income

6,616

13

18

Provision for credit losses

1,757

8

(13)

Noninterest expense

8,033

9

10

Income tax expense

918

(27)

(15)

Segment earnings

$

2,869

5

%

14

($ in billions)

Avg loans, net

$

493.1

2

1

Avg core deposits

608.9

2

7

vs

vs

($ in billions)

4Q12

3Q12

4Q11

Consumer Lending

Credit card payment volumes (POS)

$

12.6

5

%

14

Credit card penetration

(1)(3)

33.1

%

10

bps

39

Home Mortgage

Applications

$

152

(19)

%

(3)

Application pipeline

81

(16)

13

Originations

125

(10)

4

Managed residential

mortgage servicing

($ in trillions)

$

1.9

-

3

4Q12

3Q12

4Q11

Regional Banking

Consumer checking account growth

(1)(2)

-

%

-

3.9

Business checking account growth

(1)(2)

3.7

3.9

3.7

Retail Bank household cross-sell

(1)

6.05

6.04

5.93 |

Wells Fargo

4Q12 Supplement 16

Wholesale Banking

Record net income of $2.0 billion, up 24% YoY

and 2% LQ

Net interest income up 2% LQ driven by strong

loan and deposit growth

-

Average loans up 1% and average core deposits

up 7%

Noninterest income down 1% LQ driven by lower

trading volumes

Provision was $60 million in 4Q12 and included

higher net charge-offs

Expenses up 3% LQ driven by higher personnel

expense and investments in the business

Key Metrics

Cross-sell

of

6.8

products

per

relationship

(1)

up

1% LQ and 4% YoY

Treasury Management

Commercial card spend volume of $4.3 billion up

6% LQ and 25% YoY

Investment Banking

2012 Investment Banking fees from Commercial

and Corporate Banking customers up 30%

from 2011

2012 U.S. investment banking market

share

(2)

of 5.1%

Asset Management

Total AUM up $1.4 billion LQ from growth in

long-term assets

(1) Cross-sell reported on a quarter lag.

(2) Source: Dealogic U.S. investment banking fee market share.

vs

vs

($ in millions)

4Q12

3Q12

4Q11

Net interest income

$

3,092

2

%

1

Noninterest income

2,901

(1)

24

Provision for credit losses

60

n.m.

94

Noninterest expense

3,007

3

2

Income tax expense

892

(19)

10

Segment earnings

$

2,032

2

%

24

($ in billions)

Avg loans, net

$

279.2

1

5

Avg core deposits

240.7

7

8

vs

vs

($ in billions)

4Q12

3Q12

4Q11

Key Metrics:

Cross-sell

(1)

6.8

1

%

4

Commercial card spend

volume

$

4.3

6

25

YTD U.S. investment banking

market

share

%

(2)

5.1

-

bps

-

Total AUM

$

451.8

-

%

-

Advantage Funds AUM

217.0

4

2 |

Wells Fargo

4Q12 Supplement 17

Wealth, Brokerage and Retirement

Record net income up 13% YoY and 4% LQ

Net interest income up 1% LQ; average core

deposits up 5%

Noninterest income up 2% LQ; excluding $37

million lower deferred compensation plan

investment results, noninterest income was up

4% due to higher asset-based fees

Noninterest expense was up 2%, excluding $34

million in lower deferred compensation expense,

expenses increased 4% due to higher personnel

expense

Provision expense down $15 million LQ on lower

net charge-offs; both current quarter and prior

quarter reflect credit reserve releases

Retail Brokerage

Managed

account

assets

up

2%

LQ

and

20%

YoY

driven by strong net flows and market

performance

Wealth Management

Wealth

Management

client

assets

up

2%

LQ

and

3% YoY

Retirement

IRA assets up 1% LQ and 11% YoY

Institutional Retirement plan assets up 2% LQ

and 13% YoY

(1) Includes deposits.

(2) Data as of November 2012.

vs

vs

($ in millions)

4Q12

3Q12

4Q11

Net interest income

$

689

1

%

(6)

Noninterest income

2,405

2

4

Provision for credit losses

15

(50)

(25)

Noninterest expense

2,513

2

-

Income tax expense

215

3

13

Segment earnings

$

351

4

%

13

($ in billions)

Avg loans, net

$

43.3

2

1

Avg core deposits

143.4

5

6

vs

vs

($ in billions, except where noted)

4Q12

3Q12

4Q11

Key Metrics:

WBR Clients Assets

(1)

($ in trillions)

$

1.4

1

%

7

Cross-sell

(2)

10.27

-

2

Retail

Brokerage

Financial Advisors

15,414

1

1

Managed account assets

$

304

2

20

Client assets

(1)

($ in trillions)

1.2

1

8

Wealth

Management

Client assets

(1)

204

2

3

Retirement

IRA Assets

297

1

11

Institutional Retirement

Plan Assets

266

2

13 |

Wells Fargo

4Q12 Supplement 18

2.6

2.4

2.2

2.4

2.1

4Q11

1Q12

2Q12

3Q12

4Q12

2.0

2.0

1.8

1.6

1.8

4Q11

1Q12

2Q12

3Q12

4Q12

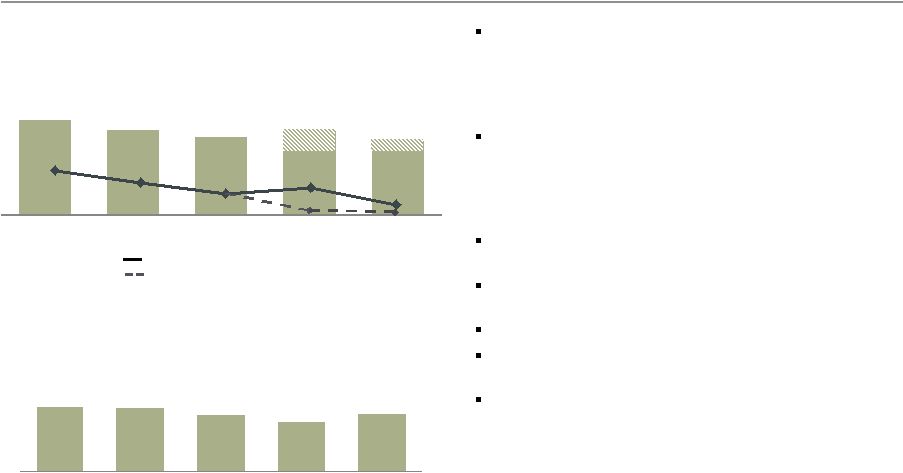

Credit quality

Trends showed continued improvement

Net charge-offs of $2.1 billion were down $277

million LQ; consumer losses included $321 million

from OCC guidance

(2)

vs. $567 million in 3Q12.

Excluding this effect:

-

0.89% net charge-off rate, down 3 bps LQ

NPAs declined $744 million LQ on a $558 million

decline in nonaccrual loans and a $186 million

decline in foreclosed assets

-

Included $394 million in NPLs from OCC

guidance

(3)

Provision expense of $1.8 billion, up $240 million

from 3Q12

Early stage consumer delinquency balances

decreased 7% and rates declined 18 bps LQ

Allowance for credit losses = $17.5 billion

Remaining PCI nonaccretable = 22.9% of

remaining UPB

(4)

Absent significant deterioration in the economy

we continue to expect future reserve releases in

2013, though at a lower level than 2012

Net Charge-offs

($ in billions)

Provision Expense

($ in billions)

1.36%

1.25%

1.15%

1.21%

1.05%

1.8

0.6

(1)

0.89%

Net charge-off rate (as reported)

Net charge-off rate (as adjusted)

0.3

(1)

1.8

0.92%

(1) OCC guidance. (2)

Includes $271 million from the completion of implementation and $50 million from 4Q12 activity.

(3) Includes $264 million from the completion of implementation and $130 million from

4Q12 activity.

(4) Unpaid principal balance for PCI loans that have not had a UPB

charge-off. |

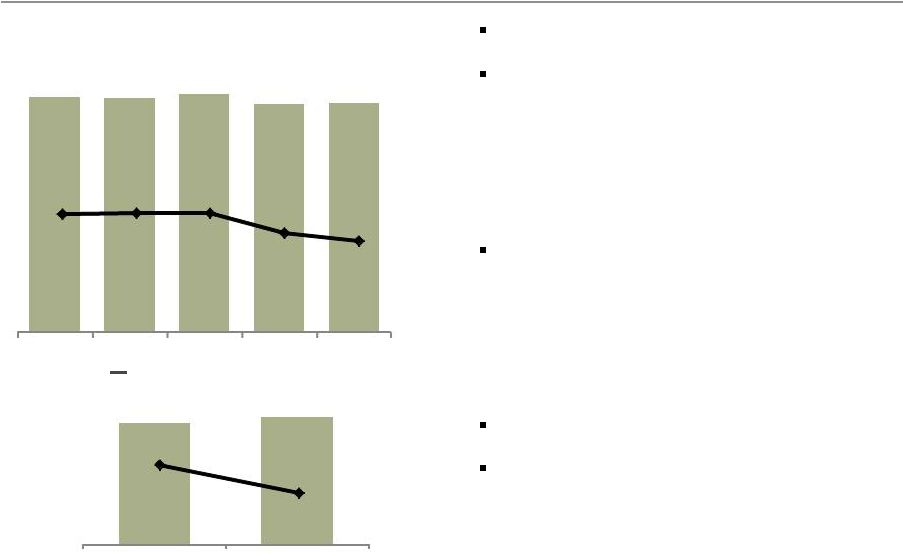

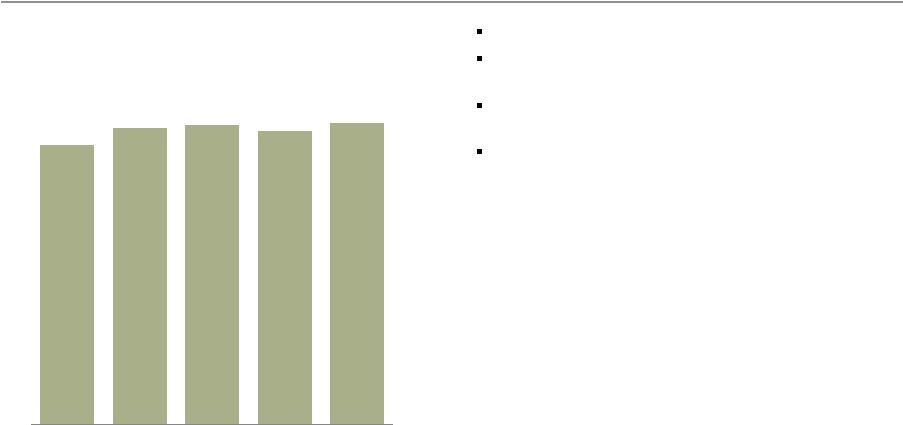

Wells Fargo

4Q12 Supplement 19

21.3

22.0

20.6

19.7

20.5

4.7

4.6

4.3

4.2

4.0

26.0

26.6

24.9

25.3

24.5

4Q11

1Q12

2Q12

3Q12

4Q12

Nonaccrual loans

Foreclosed assets

1.5

1.2

1.1

1.2

1.1

0.5

0.4

0.3

0.3

0.3

2.0

1.6

1.4

1.5

1.4

4Q11

1Q12

2Q12

3Q12

4Q12

Consumer

Commercial

8.3

6.8

6.6

6.9

6.5

$0

$5

$10

4Q11

1Q12

2Q12

3Q12

4Q12

2.40%

2.00%

1.94%

1.97%

1.79%

Credit quality

Nonperforming Assets

($ in billions)

Consumer Loans 30-89 DPD &

Still

Accruing

(3)(4)

(Balances and rates)

Loans

90+

DPD

and

Still

Accruing

(3)(4)

($ in billions)

(1)

1.4

(2)

(1)

Includes $1.7 billion at March 31, 2012, resulting from implementation of Interagency

Supervisory Guidance on Allowance for Loan and Lease Losses Estimation Practices for

Loans and Lines of Credit Secured by Junior Liens on 1-4 Family Residential Properties issued January 31, 2012.

(2)

OCC guidance impact.

(3)

Consumer includes mortgage loans held for sale 30-89 days and 90 days or more past due and

still accruing. (4) Excludes mortgage loans insured/guaranteed by the FHA or VA,

reverse mortgages, margin loans and student loans whose repayments are

predominantly guaranteed by guarantee agencies on behalf of the U.S. Department of Education

under the Federal Family Education Loan Program. Also excludes the carrying value of

PCI loans contractually delinquent. |

Wells Fargo

4Q12 Supplement 20

5.19

6.72

6.09

9.07

6.75

7.43

2.13

2.67

4.62

3.97

3.42

3.99

7.32%

9.40%

10.70%

13.04%

10.17%

11.42%

Wells Fargo

Citi

JPM Chase

Bank of

America

Industry

Industry ex

WFC

Deliquency Rate

Foreclosure Rate

3Q12 Servicing Portfolio Delinquency

Performance

(1)

Total

Outstanding

Repurchase

Demands

(3)

and

Agency New Demands for 2006-2008 Vintages

Mortgage servicing

Delinquency and outstanding repurchase demands

(1) Inside Mortgage Finance, data as of September 30, 2012. Industry excluding

WFC performance calculated based on IMF data.

(2) Industry is all large servicers ($6.0 trillion) including WFC, C, JPM and BAC.

(3) Includes mortgage insurance rescissions.

(2)

3Q12 Wells Fargo delinquency and foreclosure ratio

continued to be significantly lower than peers

Wells Fargo’s total delinquency and foreclosure

ratio for 4Q12 was 7.04%, down 28 bps LQ and

down from 7.96% in 4Q11

Number and balance of total outstanding

repurchase demands were down slightly LQ

and YoY

Agency demands outstanding

-

Agency repurchase demands outstanding

essentially flat from 3Q12 on lower resolutions

-

New agency demands in total and in the 2006-

2008 vintages down LQ

-

Demands on newer vintage originations

continued to emerge consistent with our

estimates

Non-Agency demands outstanding

-

Balance of non-agency repurchase demands

outstanding down LQ

Repurchase reserves of $2.2 billion increased $173

million LQ on lower losses/reserve usage and

included a $379 million reserve addition vs. $462

million in 3Q12

-

Incorporates current demand levels

-

Considers all vintages

-

Anticipates future expected demands

$3.84

$2.95

$2.49

$2.24

$2.02

$2.01

$1.86

$1.67

$2.00

$1.94

(1,000)

1,000

3,000

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

Number of Outstanding Demands

Agency New Demands for 2006-2008 Vintages

Original Loan Balance of Outstanding Demands ($ in B) |

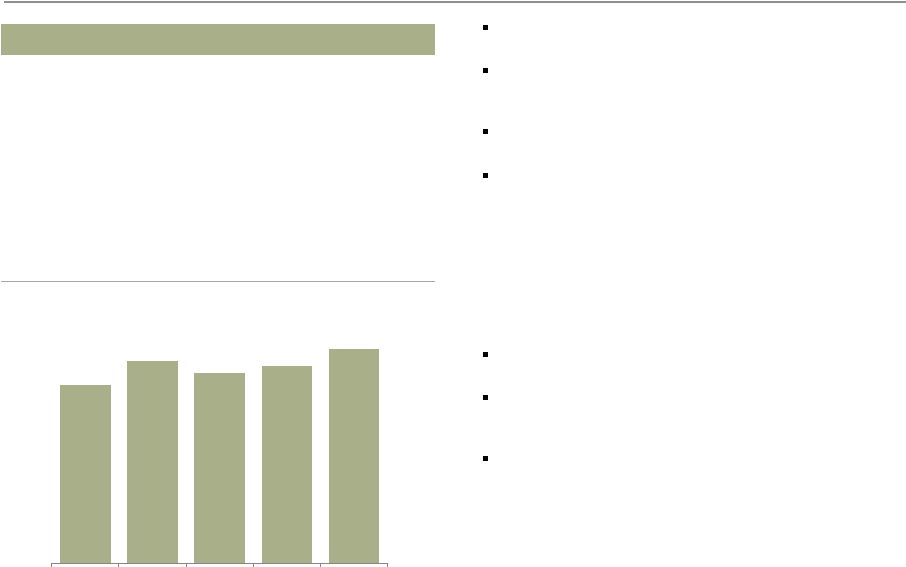

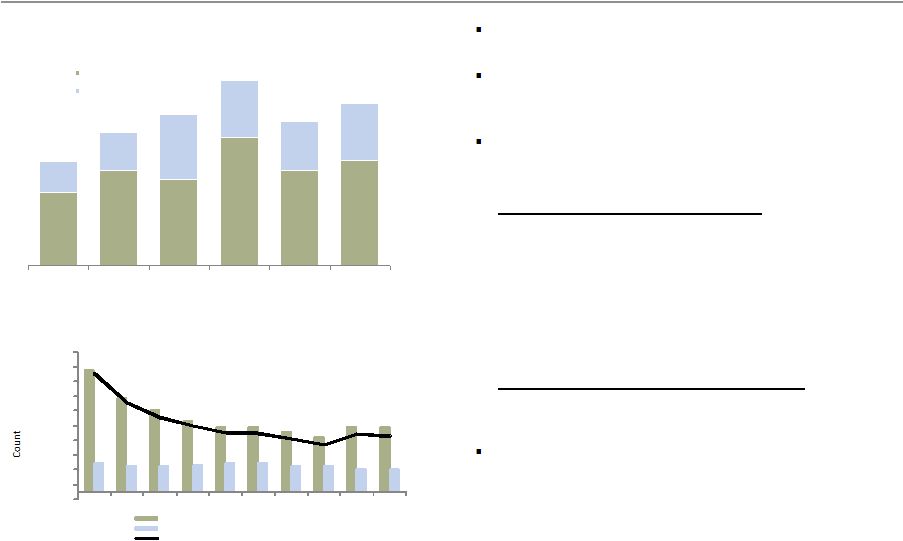

Wells Fargo

4Q12 Supplement 21

Capital

9.46%

9.98%

10.08%

9.92%

10.12%

4Q11

1Q12

2Q12

3Q12

4Q12

Capital remained strong

Tier 1 common equity ratio under Basel I

of 10.12% increased 20 bps LQ

Tier 1 common equity ratio under Basel III is

estimated

to

be

8.18%

at

12/31/12

(1)

Purchased 42.1 million common shares in 4Q12

and entered into a $200 million 4Q12 forward

repurchase transaction, estimated to be 5.9

million shares, that is expected to settle in 1Q13

Tier 1 Common Equity Ratio

Under Basel I

See Appendix page 36 for additional information on Tier 1 common equity.

4Q12 capital ratios are preliminary estimates.

(1) Estimated Basel III calculation based on management’s current interpretation of

the Basel III capital rules proposed by federal banking agencies in notices of proposed

rulemaking announced in June 2012. The proposed rules and interpretations and assumptions used in estimating Basel III calculations are subject to

change depending on final promulgation of Basel III capital rules. See pages 36-37 for

additional information regarding Tier 1 common equity ratios. |

Wells Fargo

4Q12 Supplement 22

Summary -

strong 4Q12

Record earnings of $5.1 billion, up $983 million, or 24% from 4Q11

Record diluted earnings per share of $0.91, up 25%

PTPP of $9.1 billion up $955 million, or 12%

Revenue up $1.3 billion, or 7%

4Q12 efficiency ratio

(1)

of 58.8% down 190 bps

Strong credit performance

Solid returns

-

ROA = 1.46%, up 21 bps

-

ROE = 13.35%, up 138 bps

Capital levels increased

Returned more capital to shareholders in 2012

(1)

Noninterest expense and our efficiency ratio may be affected by a variety of factors,

including business and economic cyclicality, seasonality, changes in our business

composition and operating environment, growth in our business and/or acquisitions, and unexpected expenses relating to, among

other things, litigation and regulatory matters.

All comparisons are 4Q12 vs. 4Q11. |

Wells Fargo

4Q12 Supplement 23

Appendix |

Wells Fargo

4Q12 Supplement 24

(1) Net of purchase accounting adjustments.

-$78.5

Non-strategic/liquidating loan portfolio risk reduction

-$4.1

-$5.1

-$4.5

-$4.1

($ in billions)

4Q12

3Q12

2Q12

1Q12

4Q11

4Q08

Pick-a-Pay mortgage

(1)

$

58.3

60.1

62.0

64.0

65.7

95.3

Liquidating home equity

4.6

5.0

5.2

5.5

5.7

10.3

Legacy WFF indirect auto

0.8

1.1

1.5

1.9

2.5

18.2

Legacy WFF debt consolidation

14.5

15.0

15.5

16.0

16.5

25.3

Education Finance -

gov't guaranteed

12.5

13.0

13.8

14.8

15.4

20.5

Legacy WB C&I, CRE and foreign PCI loans

(1)

3.2

3.8

4.3

5.2

5.7

18.7

Legacy WB other PCI loans

(1)

0.6

0.6

0.8

0.8

0.8

2.5

Total

$

94.5

98.6

103.1

108.2

112.3

190.8

-$96.3 |

Wells Fargo

4Q12 Supplement 25

Purchased credit-impaired (PCI) portfolios

Legacy Wachovia PCI loans continued to perform better than originally expected

($ in billions)

(1)

December 31, 2008

September 30, 2012

December 31, 2012

12/31/08 Nonaccretable difference

Addition of nonaccretable difference due to acquisitions

Losses from loan resolutions and write-downs

Release of nonaccretable difference since merger

12/31/12 Remaining nonaccretable difference

Additional provision since 2008 merger

Release of nonaccretable difference since 2008 merger

Net performance

Commercial

Pick-a-Pay

Other

consumer

Total

Life-to-date

net

performance

Nonaccretable

difference

rollforward

Adjusted

unpaid

principal

balance

$

29.2

62.5

6.5

98.2

5.9

33.1

1.5

40.5

5.0

32.0

1.4

38.4

$

10.4

26.5

4.0

40.9

0.2

-

-

0.2

(6.9)

(17.3)

(2.8)

(27.0)

(3.3)

(3.0)

(0.8)

(7.1)

(2)

0.4

6.2

0.4

7.0

$

(1.7)

-

(0.1)

(1.8)

3.3

3.0

0.8

7.1

(2)

1.6

3.0

0.7

5.3

(2) Reflects releases of $1.8 billion for loan resolutions and $5.3 billion from the

reclassification of nonaccretable difference to the accretable yield, which will result

in increasing income over the remaining life of the loan or pool of loans.

(1)

Includes write-downs taken on loans where severe delinquency (normally 180 days) or other

indications of severe borrower financial stress exist that indicate there will be a

loss of contractually due amounts upon final resolution of the loan. |

Wells Fargo

4Q12 Supplement 26

$135 million in nonaccretable difference reclassified to accretable yield this quarter

$86 million of the $509 million in losses from loan resolutions and write-downs in the

quarter was the result of the OCC guidance

$7.0

billion

in

nonaccretable

difference

remains

to

absorb

losses

on

PCI

loans

-

Remaining

nonaccretable

=

22.9%

of

unpaid

principal

balance

(UPB)

(5)

•

Remaining

Pick-a-Pay

nonaccretable

=

24.4%

of

Pick-a-Pay

UPB

(5)

PCI nonaccretable difference

Analysis of nonaccretable difference for PCI loans

($ in millions)

Pick-a-Pay

Total

Balance, September 30, 2012

$

557

6,679

Addition of nonaccretable difference due to acquisitions

7

-

-

Release of nonaccretable difference due to:

Loans

resolved

by

settlement

with

borrower

(1)

(5)

-

-

Loans

resolved

by

sales

to

third

parties

(2)

-

-

-

-

Reclassification

to

accretable

yield

for

loans

with

improving

credit-related

cash

flows

(3)

(127)

-

Use of nonaccretable difference due to:

Losses

from

loan

resolutions

and

write-downs

(4)

(10)

(447)

Balance, December 31, 2012

$

422

6,232

(52)

(509)

310

6,964

(5)

(8)

(135)

Other

consumer

Commercial

370

7,606

7

(1) Release of the nonaccretable difference for settlement with borrower, on

individually accounted PCI loans, increases interest income in the period of

settlement. Pick-a-Pay and Other consumer PCI loans do not reflect nonaccretable

difference releases for settlements with borrowers due to pool accounting for those

loans, which assumes that the amount received approximates the pool performance expectations.

(2) Release of the nonaccretable difference as a result of sales to third parties

increases noninterest income in the period of the sale. (3) Reclassification of nonaccretable difference to accretable yield for loans with

increased cash flow estimates will result in increased interest income as a prospective

yield adjustment over the remaining life of the loan or pool of loans. (4)

Write-downs to net realizable value of PCI loans are absorbed by the nonaccretable

difference when severe delinquency (normally 180 days) or other indications of severe

borrower financial stress exist that indicate there will be a loss of contractually due amounts upon final resolution of the loan.

(5) Unpaid principal balance of loans without write-downs. |

Wells Fargo

4Q12 Supplement 27

Accretable yield balance decreased $364 million LQ and included:

-

Accretion into interest income of $513 million, up modestly LQ

Balance of $18.5 billion expected to accrete to income over the remaining life of the

underlying loans PCI accretable yield

(1) Includes accretable yield released as a result of settlements with borrowers, which

is included in interest income. (2) Includes accretable yield released as a

result of sales to third parties, which is included in noninterest income. (3)

Represents changes in cash flows expected to be collected due to changes in interest rates on variable rate PCI loans, changes in prepayment

assumptions and the impact of modifications.

Cumulative

Accretable yield rollforward

since

($ in millions)

4Q12

3Q12

merger

Total, beginning of period

$

18,912

15,153

10,447

Addition of accretable yield due to acquisitions

3

-

131

Accretion

into

interest

income

(1)

(513)

(495)

(9,351)

Accretion

into

noninterest

income

due

to

sales

(2)

-

-

(242)

Reclassification from nonaccretable difference for loans with improving credit-related

cash flows 135

687

5,354

Changes

in

expected

cash

flows

that

do

not

affect

nonaccretable difference

11

3,567

12,209

Total, end of period

$

18,548

18,912

18,548

(3) |

Wells Fargo

4Q12 Supplement 28

PCI accretable yield (Commercial

(1)

and Pick-a-Pay)

Commercial accretion

(2)

decreased $22

million and accretable yield percentage

of 16.77% was in line with 3Q12

Pick-a-Pay accretable yield balance

declined to $16.9 billion while

accretable yield percentage increased to

4.7% reflecting the 3Q12 increase in

the balance

-

Weighted average life decreased to

12.5 years

Pick-a-Pay PCI Accretable Yield

($ in millions)

4Q12

3Q12

2Q12

PCI interest income

Accretion

$

312

287

303

Average carrying value

26,560

27,260

28,041

Accretable yield percentage

4.70

%

4.21

4.32

Accretable yield balance

$

16,879

17,189

13,466

Weighted average life (years)

12.5

12.7

11.4

Commercial

(1)

PCI Accretable Yield

($ in millions)

4Q12

3Q12

2Q12

PCI interest income

Accretion

and

resolution

income

$

182

204

323

Average carrying value

4,332

4,914

5,629

Accretable yield percentage

(2)

16.77

%

16.62

22.95

Accretable yield balance

$

941

978

1,008

Weighted average life (years)

2.9

2.8

2.2

(1) Includes both legacy Wachovia PCI loans as well as recently purchased PCI

loans.

(2) Includes resolution income. |

Wells Fargo

4Q12 Supplement 29

Pick-a-Pay mortgage portfolio

Carrying

value

of

$58.3

billion

in

first

lien

loans

outstanding,

down

$1.8

billion

from

3Q12

and

down

$37.0

billion from 4Q08 on paid-in-full loans and loss mitigation efforts

Adjusted unpaid principal balance of $63.8 billion, down $2.3 billion from 3Q12 and down $51.9

billion from 4Q08

$5.1 billion in modification principal forgiveness since acquisition reflects over 111,000

completed full-term modifications; additional $427 million of conditional

forgiveness that can be earned by borrowers through performance over the next 3 years

Modification redefault rate has been consistently better than the industry average (as

measured by 60+ DPD after six months)

49% of the adjusted UPB are option payment loans vs. 86% in 4Q08

($ in millions)

Product type

Adjusted

unpaid

principal

balance

% of total

Adjusted

unpaid

principal

balance

% of total

Adjusted

unpaid

principal

balance

% of total

Option

payment

loans

(1)

$

31,510

49

%

$

33,364

50

%

$

99,937

86

%

Non-option payment adjustable-rate and

fixed-rate

loans

(1)(2)

8,781

14

8,974

14

15,763

14

Full-term loan modifications

(1)

23,528

37

23,736

36

-

-

Total

adjusted

unpaid

principal

balance

(1)(2)

$

63,819

100

%

$

66,074

100

%

$

115,700

100

%

Total carrying value

58,274

60,080

95,315

At 12/31/2008

At 9/30/2012

(3)

At 12/31/2012

(3)

(1)

Adjusted unpaid principal includes write-downs taken on loans where severe delinquency

(normally 180 days) or other indications of severe borrower financial stress

exist that indicate there will be a loss of contractually due amounts upon final resolution of the loan.

(2)

Includes loans refinanced under the Consumer Relief Refinance Program. (3)

Reflects OCC guidance. |

Wells Fargo

4Q12 Supplement 30

Pick-a-Pay credit highlights

Non-PCI portfolio

Loans down 3% LQ driven by loans paid-in-full

85% of portfolio current

Nonaccrual loans increased $182 million,

or 5%, LQ

$209 million increase related to OCC guidance

$142 million of nonaccrual TDRs reclassified to

accruing TDR status based on borrower payment

performance

$4.2 billion in nonaccruals includes $1.9 billion

of nonaccruing TDRs

Net charge-offs of $138 million down $39

million LQ

45% of portfolio with LTV

(2)

80%

PCI portfolio

Carrying value down 2%

67% of portfolio current

Life-of-loan losses continued to be lower than

originally projected at time of merger

(1)

The carrying value, which does not reflect the allowance for loan losses, includes purchase

accounting adjustments, which, for PCI loans, are the nonaccretable

difference

and

the

accretable

yield,

and

for

all

other

loans,

an

adjustment

to

mark

the

loans

to

a

market

yield

at

date

of

merger

less

any

subsequent

charge-offs.

(2) The current loan-to-value (LTV) ratio is calculated as the net carrying

value (defined in (1) above) divided by the collateral value. (3)

The adjusted unpaid principal balance includes write-downs taken on loans where severe

delinquency (normally 180 days) or other indications of severe borrower financial

stress exist that indicate there will be a loss of contractually due amounts upon final resolution of the loan.

($ in millions)

4Q12

3Q12

Non-PCI

loans

Carrying

value

(1)

$

31,940

33,096

Nonaccrual loans

4,200

4,018

as a % of loans

13.15

%

12.14

Net charge-offs

$

138

177

as % of avg loans

1.68

%

2.09

90+ days past due

as % of loans

10.30

10.09

Current

average

LTV

(2)

83

%

84

Current average FICO

682

683

Contractual average loan size

$

202,000

204,000

Contractual average age of loans

8.79

years

8.54

% of loans in California

49

%

49

($ in millions)

4Q12

3Q12

PCI

loans

Adjusted

unpaid

principal

balance

(3)

$

32,003

33,107

Carrying

value

(1)

26,334

26,984

Current

average

LTV

(2)

88

%

90

Current average FICO

618

617

Contractual average loan size

$

299,000

304,000

Contractual average age of loans

6.75

years

6.50

% of loans in California

68

%

68 |

Wells Fargo

4Q12 Supplement 31

Real estate 1-4 family first mortgage portfolio

First lien mortgage loans up 4% as growth in core

first lien mortgage was partially offset by

continued run-off in the liquidating portfolio

Pick-a-Pay non-PCI portfolio down 3%

PCI portfolio down 3%

Debt consolidation first lien down 3%

Core first lien up $11.7 billion, or 7%, reflecting

strong origination volumes and the decision to

retain $9.7 billion of conforming production

•

Nonconforming mortgages increased $3.6

billion to $49.0 billion

Core net charge-offs up $47 million on higher

losses from OCC guidance

(1) Ratios on Legacy WFF debt consolidation first mortgage loan portfolio only.

(2) Ratios on non run-off first lien mortgage loan portfolio only.

($ in millions)

4Q12

3Q12

Total real estate 1-4 family first mortgage

$

249,900

240,554

Less consumer non-strategic/liquidating portfolios:

Pick-a-Pay non-PCI first lien mortgage

31,940

33,096

PCI first lien mortgage

26,838

27,535

Debt consolidation first mortgage portfolio

14,178

14,640

Core first lien mortgage

176,944

165,283

Nonaccrual loans

$

2,363

2,279

as % of loans

16.67 %

15.57

Net charge-offs

$

182

214

as % of average loans

5.03 %

5.77

Nonaccrual loans

$

4,892

4,898

as % of loans

2.76 %

2.96

Net charge-offs

$

329

282

as % of loans

0.74 %

0.69

Core

first

lien

mortgage

loan

performance

(2)

Legacy

WFF

debt

consolidation

first

mortgage

loan

performance

(1) |

Wells Fargo

4Q12 Supplement 32

Home equity portfolio

Core

Portfolio

(1)

Outstandings

down 3%

-

High

quality

new

originations

with

weighted

average CLTV of 61%, 778 FICO, and 30% total

debt service ratio

4Q12 losses decreased $313 million mainly due to

the implementation of OCC guidance in 3Q12

2+ delinquencies decreased $188 million

Delinquency rate for loans with a CLTV >100%

improved 38 bps

Liquidating

Portfolio

Outstandings down 6%

4Q12 losses decreased $47 million

2+ delinquencies declined $21 million

Delinquency rate for loans with a CLTV >100%

improved 34 bps

21%

in

1

lien

position

40% in junior lien position behind WFC owned or

serviced

1

lien

-

Current

1

lien,

Current

junior

lien

=

96.0%

-

Current 1 lien, Delinquent junior lien = 1.0%

-

Delinquent

1

lien,

Current

junior

lien

=

1.3%

-

Delinquent

1

lien,

Delinquent

junior

lien

=

1.7%

39%

in

junior

lien

position

behind

third

party

1

lien

st

st

st

st

st

st

($ in millions)

4Q12

3Q12

Core Portfolio

(1)

Outstandings

$

90,427

92,979

Net charge-offs

622

935

as % of avg loans

2.69

%

3.93

2+ payments past due

$

2,497

2,685

as % loans

2.77

%

2.90

% CLTV > 100%

(2)

34

35

2+ payments past due

3.52

3.90

% Unsecured balances

(3)

15

16

% 1st lien position

22

21

Liquidating

Portfolio

Outstandings

$

4,647

4,951

Net charge-offs

101

148

as % of avg loans

8.33

%

11.60

2+ payments past due

$

178

199

as % loans

3.82

%

4.03

% CLTV > 100%

(2)

71

72

2+ payments past due

3.73

4.07

% 1st lien position

4

4

st

Excludes purchased credit-impaired loans.

(1)

Includes equity lines of credit and closed-end junior liens associated with the

Pick-a-Pay portfolio totaling $1.3 billion at December 31, 2012 and $1.4

billion at September 30, 2012.

(2)

CLTV is calculated based on outstanding balance plus unused lines of credit

divided by estimated home value. Estimated home values are determined

predominantly based on automated valuation models updated through

December 2012.

(3)

Unsecured balances, representing the percentage of outstanding balances

above the most recent home value.

Total

home

equity

portfolio

$95

billion

= |

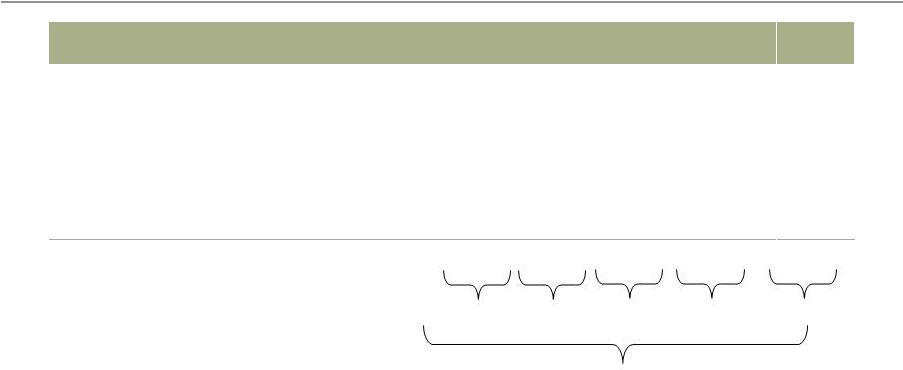

Wells Fargo

4Q12 Supplement 33

Credit card portfolio

Record $24.6 billion credit card outstandings, up

4% from 3Q12 on seasonal holiday spending and

8% YoY on strong account growth

-

Consumer credit card new accounts increased

11% YoY with household penetration increasing

to 33.1%

(1)

-

Record $12.6 billion purchase dollar volume in

4Q12, increased 5% LQ and 14% YoY

-

Purchase transactions grew 6% LQ and

17% YoY

Net charge-offs up $10 million, or 4 bps, LQ a

return to pre-recession seasonality and down $34

million, or 92 bps, YoY reflecting continued steady

improvement

(1) Household penetration as of November 2012 and defined as the percentage of retail

banking deposit households that have a credit card with Wells Fargo. Household

penetration has been redefined to include Wells Fargo Financial accounts. ($ in

millions) 4Q12

3Q12

Credit card outstandings

$

24,640

23,692

Net charge-offs

222

212

as % of avg loans

3.71

%

3.67

Key Metrics:

Purchase volume

$

12,609

12,066

Penetration

(1)

33.1

%

32.1 |

Wells Fargo

4Q12 Supplement 34

Auto portfolios

(1)

Core Consumer Portfolio

Core auto outstandings of $46.1 billion flat LQ and

up 9% YoY

4Q12 originations of $5.4 billion down 15% LQ

from prior quarter reflecting seasonality and

increased competition and up 8% YoY

Nonaccrual loans decreased $44 million LQ

Net charge-offs were up $48 million LQ reflecting

seasonality and include $26 million in losses from

OCC guidance

December Manheim index of 124.1, up 3% LQ

and down 1% from December 2011

30+ days past due increased $188 million LQ

reflecting seasonality

Commercial Portfolio

Loans of $7.4 billion up 12% LQ and 31% YoY as

dealer floorplan utilization rates hit highest levels

since the merger

Continued strong credit performance

(1)

Legacy Wells Fargo Financial indirect portfolio balance as of December 31, 2012, was $830

million. ($ in millions)

4Q12

3Q12

Auto outstandings

$

43,841

43,613

Nonaccrual loans

185

218

as % of loans

0.42

%

0.50

Net charge-offs

$

102

57

as % of avg loans

0.93

%

0.52

30+ days past due

$

797

609

as % of loans

1.82

%

1.40

Auto outstandings

$

2,306

2,357

Nonaccrual loans

35

46

as % of loans

1.52

%

1.95

Net charge-offs

$

9

6

as % of avg loans

1.46

%

1.02

30+ days past due

$

30

30

as % of loans

1.30

%

1.27

Commercial Portfolio

Auto outstandings

$

7,396

6,599

Nonaccrual loans

-

-

as % of loans

-

%

-

Net charge-offs (recoveries)

$

-

-

as % of avg loans

n.m.

%

n.m.

Core Indirect Consumer Portfolio

Core Direct Consumer Portfolio |

Wells Fargo

4Q12 Supplement 35

Student lending portfolio

$23.1 billion student lending outstandings down

2% LQ

Private Portfolio

$10.7 billion private loans outstandings up 1% LQ

and up 7% YoY

Applications decreased 57% LQ due to

peak season in 3Q12

Dollar originations decreased 54% LQ due

to seasonality

Continued to originate high quality loans with

an average FICO of 764 and 81% of new loans

co-signed

Net charge-offs up $11 million LQ due to

seasonality of repayments on loans

Government Portfolio

$12.5 billion liquidating government guaranteed

outstandings declined 4% LQ and 19% YoY

($ in millions)

4Q12

3Q12

Education

Finance

Total outstandings

$

23,119

23,504

Private

Portfolio

Private outstandings

$

10,654

10,553

Net charge-offs

38

27

as % of avg loans

1.41

%

1.02

30 days past due

$

233

231

as % of loans

2.19

%

2.19

Government

Guaranteed

Portfolio

Government outstandings

$

12,465

12,951 |

Wells Fargo

4Q12 Supplement 36

Tier 1 common equity under Basel I

(1)

Wells Fargo & Company and Subsidiaries

FIVE

QUARTER

TIER

1

COMMON

EQUITY

UNDER

BASEL

I

Dec. 31,

Sept. 30

June 30,

Mar. 31,

Dec. 31,

($ in billions)

2012

2012

2012

2012

2011

Total equity

158.9

$

156.1

149.4

146.8

141.7

Noncontrolling interests

(1.3)

(1.4)

(1.3)

(1.3)

(1.5)

Total Wells Fargo stockholders' equity

157.6

154.7

148.1

145.5

140.2

Adjustments:

Preferred equity

(12.0)

(11.3)

(10.6)

(10.6)

(10.6)

Goodwill and intangible assets (other than MSRs)

(32.9)

(33.4)

(33.5)

(33.7)

(34.0)

Applicable deferred assets

3.2

3.3

3.5

3.7

3.8

Deferred tax asset limitation

-

-

-

-

-

MSRs over specified limitations

(0.7)

(0.7)

(0.7)

(0.9)

(0.8)

Cumulative other comprehensive income

(5.6)

(6.4)

(4.6)

(4.1)

(3.1)

Other

(0.5)

(0.4)

(0.5)

(0.4)

(0.4)

Tier 1 common equity

(A)

109.1

$

105.8

101.7

99.5

95.1

Total risk-weighted assets

(2)

(B)

1,077.9

$

1,067.1

$

1,008.6

996.8

1,005.6

Tier 1 common equity to total risk-weighted assets

(2)

(A)/(B)

10.12

%

9.92

10.08

9.98

9.46

(1) Tier 1 common equity is a non-generally accepted

accounting principle (GAAP) financial measure that is used by investors, analysts and bank regulatory

agencies to assess the capital position of financial services

companies. Management reviews Tier 1 common equity along with other measures of capital as

part of its financial analyses and has included this non-GAAP

financial information, and the corresponding reconciliation to total equity, because of current

interest in such information on the part of market participants.

(2) Under the regulatory guidelines for risk-based

capital, on-balance sheet assets and credit equivalent amounts of derivatives and off-balance sheet items are

assigned to one of several broad risk categories according to the

obligor, or, if relevant, the guarantor or the nature of any collateral. The aggregate dollar

amount in each risk category is then multiplied by the risk weight

associated with that category. The Company’s December 31, 2012, risk-weighted assets

and resulting Tier 1 common equity to total risk-weighted assets

are preliminary and reflect total estimated on-balance sheet and total estimated derivative

and off-balance sheet risk-weighted assets of $861.6 billion

and $216.3 billion, respectively. Effective September 30, 2012, the Company refined its

determination of the risk weighting of certain unused lending

commitments that provide for the ability to issue standby letters of credit and commitments

to issue standby letters of credit under syndication arrangements

where the Company has an obligation to issue in a lead agent or similar capacity beyond

its contractual participation level.

(1) |

Wells Fargo

4Q12 Supplement 37

Tier 1 common equity under Basel III (Estimated)

(1)

Wells Fargo & Company and Subsidiaries

Dec. 31,

(in billions)

2012

Tier 1 common equity under Basel I

109.1

$

Adjustments

from

Basel

I

to

Basel

III

(3)(5)

:

Cumulative other comprehensive income related to AFS securities and

defined benefit pension plans

5.3

$

0.2

5.5

Threshold

deductions,

as

defined

under

Basel

III

(4) (5)

(0.7)

Tier 1 common equity anticipated under Basel III

(C)

113.9

$

Total

risk-weighted

assets

anticipated

(6)

(D)

1,393.1

$

Tier 1 common equity to total risk-weighted assets anticipated

under Basel III (C)/(D)

8.18

%

Other

Total adjustments from Basel I to Basel III

(1)

Tier 1 common equity is a non-generally accepted accounting

principle (GAAP) financial measure that is used by investors, analysts and bank regulatory

agencies to assess the capital position of financial services

companies. Management reviews Tier 1 common equity along with other measures of capital

as part of its financial analyses and has included this non-GAAP

financial information, and the corresponding reconciliation to total equity, because of

current interest in such information on the part of market

participants. (2)

The Basel III Tier 1 common equity and risk-weighted assets are

calculated based on management’s current interpretation of the Basel III capital rules

proposed by federal banking agencies in notices of proposed rulemaking

announced in June 2012. The proposed rules and interpretations and

assumptions used in estimating Basel III calculations are subject to

change depending on final promulgations of Basel III capital rules

(3)

Adjustments from Basel I to Basel III represent reconciling

adjustments, primarily certain components of cumulative other comprehensive income

deducted for Basel I purposes, to derive Tier 1 common equity under

Basel III. (4)

Threshold deductions, as defined under Basel III, include individual

and aggregate limitations, as a percentage of Tier 1 common equity, with respect to

MSRs, deferred tax assets and investments in unconsolidated financial

companies. (5)

Volatility in interest rates can have a significant impact on the

valuation of cumulative other comprehensive income and MSRs and therefore, may impact

adjustments from Basel I to Basel III, and MSRs subject to threshold

deductions, as defined under Basel III, in future reporting periods.

(6)

Under current Basel proposals, risk-weighted assets incorporate

different classifications of assets, with certain risk weights based on a borrower's credit

rating or Wells Fargo's own risk models, along with adjustments to

address a combination of credit/counterparty, operational and market risks, and other

Basel III elements. The amount of risk-weighted assets anticipated

under Basel III is preliminary and subject to change depending on final promulgation

of Basel III capital rulemaking and interpretations thereof by

regulatory authorities. TIER

1

COMMON

EQUITY

UNDER

BASEL

III

(ESTIMATED)

(1)(2)

under

Basel

III |

| Wells Fargo

4Q12 Supplement 38

Forward-looking statements and additional information

Forward-looking statements:

This Quarterly Supplement and management’s related presentation contain

forward-looking statements about our future financial performance.

These

forward-looking

statements

include

statements

using

words

such

as

“believe,”

“expect,”

“anticipate,”

“estimate,”

“target”, “should,”

“may,”

“can,”

“will,”

“outlook,”

“appears”

or similar expressions. These forward-looking statements may include,

among others, statements about: future credit quality and performance, including our current

expectation of future loan loss reserve releases; mortgage repurchase exposure;

exposure related to mortgage practices, including foreclosures and servicing; our

noninterest

expense

and

efficiency

ratio,

including

our

targeted

efficiency

ratio

range

as

part

of

our

expense

management

initiatives;

the future economic environment; loan growth; net interest income in a low interest rate

environment; our net interest margin, including our expectations regarding continued

pressure on our net interest margin given the low interest rate environment; reduction

or mitigation

of

risk

in

our

loan

portfolios;

future

effects

of loan modification programs; life-of-loan loss estimates; the

estimated impact of regulatory reform on our financial results and business and expectations

regarding our efforts to mitigate such impact;

our

estimated

Tier

1

common

equity

ratio

as

of December 31, 2012, under proposed Basel III capital rules; and future

common stock dividends, common share repurchases and other uses of capital. Investors

are urged to not unduly rely on forward- looking statements as actual results could

differ materially from expectations. Forward-looking statements speak only as of the date

made,

and

we

do

not

undertake

to

update

them

to

reflect

changes

or

events

that

occur

after

that

date.

For

more

information

about

factors that

could cause actual results to differ materially from expectations, refer

to pages 15-16 of Wells Fargo’s press release

announcing our fourth quarter 2012 results, as well as Wells Fargo’s reports filed with

the Securities and Exchange Commission, including the discussion under “Risk

Factors” in our Annual Report on Form 10-K for the year ended December 31,

2011. Purchased credit-impaired loan portfolio:

Loans that were acquired from Wachovia that were considered credit impaired were written down

at acquisition date in purchase accounting to an amount estimated to be collectible and

the related allowance for loan losses was not carried over to Wells Fargo’s

allowance. In addition, such purchased credit-impaired loans are not classified as

nonaccrual or nonperforming, and are not included in loans that were contractually 90+

days past due and still accruing. Any losses on such loans are charged against the nonaccretable

difference established in purchase accounting and are not reported as charge-offs (until

such difference is fully utilized). As a result of accounting for purchased loans with

evidence of credit deterioration, certain ratios of the combined company are not comparable to a

portfolio that does not include purchased credit-impaired loans.

In certain cases, the purchased credit-impaired loans may affect portfolio credit ratios

and trends. Management believes that the presentation of information adjusted to

exclude the purchased credit-impaired loans provides useful disclosure regarding the credit

quality of the non-impaired loan portfolio. Accordingly, certain of the loan balances and

credit ratios in this Quarterly Supplement have been adjusted to exclude the purchased

credit-impaired loans. References in this Quarterly Supplement to impaired loans mean

the

purchased

credit-impaired

loans.

Please

see

pages

31-33

of

the

press

release

for

additional

information

regarding

the

purchased

credit-impaired loans. |