Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - AMERICAN POWER CORP. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - AMERICAN POWER CORP. | exh32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - AMERICAN POWER CORP. | exh31_2.htm |

| EX-32.2 - EXHIBIT 32.2 - AMERICAN POWER CORP. | exh32_2.htm |

| EX-31.1 - EXHIBIT 31.1 - AMERICAN POWER CORP. | exh31_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended: September 30, 2012

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ____________ to _____________

Commission file number: 000-53683

(Exact name of registrant as specified in its charter)

|

Nevada

|

26-0693872

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

16 Market Square Center

1400 16th Street Suite 400

Denver, CO 80202

(Address of principal executive offices)

Tel: 720.932.8389

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Exchange Act: None

Securities registered pursuant to Section 12(g) of the Exchange Act: Common Stock, $0.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[ ] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

[ ] Yes [X] No

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [X] Yes [ ] No

Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] |

| Accelerated filer | [ ] |

| Non-accelerated filer | [ ] (Do not check if a smaller reporting company) |

| Smaller reporting company | [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

[ ] Yes [X] No

As of March 31, 2012, the aggregate market value of the shares of the registrant’s common stock held by non-affiliates was approximately $6,997,259. As of March 31, 2012, American Power’s stock was trading at $0.14 per share and the Company had 49,980,419 shares outstanding held by non-affiliates. Shares of the registrant’s common stock held by each executive officer and director and each by each person who owns 10% or more of the outstanding common stock have been excluded from the calculation in that such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

There were 102,512,909 shares of the registrant’s common stock outstanding as of December 27, 2012.

DOCUMENTS INCORPORATED BY REFERENCE

None.

AMERICAN POWER CORPORATION

TABLE OF CONTENTS

|

Page

|

||

|

PART I

|

4

|

|

ITEM 1.

|

BUSINESS

|

4

|

|

ITEM 1A.

|

RISK FACTORS

|

9

|

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

15

|

|

ITEM 2.

|

PROPERTIES

|

15

|

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

20

|

|

ITEM 4.

|

MINE SAFETY DISCLOSURES

|

20

|

|

PART II

|

21

|

|

ITEM 5.

|

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

21

|

|

ITEM 6.

|

SELECTED FINANCIAL DATA

|

21

|

|

ITEM 7.

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

22

|

|

ITEM 7A.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

24

|

|

ITEM 8.

|

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

24

|

|

ITEM 9.

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

|

24

|

|

ITEM 9A.

|

CONTROLS AND PROCEDURES

|

24

|

|

ITEM 9B.

|

OTHER INFORMATION

|

25

|

|

PART III

|

25

|

|

ITEM 10.

|

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

25

|

|

ITEM 11.

|

EXECUTIVE COMPENSATION

|

27

|

|

ITEM 12.

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

28

|

|

ITEM 13.

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

|

29

|

|

ITEM 14.

|

PRINCIPAL ACCOUNTANT FEES AND SERVICES

|

29

|

|

PART IV

|

30

|

|

ITEM 15.

|

EXHIBITS, FINANCIAL STATEMENT SCHEDULES

|

30

|

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. These forward-looking statements are subject to a number of risks and uncertainties, many of which are beyond our control. All statements, other than statements of historical fact, contained in this report, including statements regarding future events, our future financial performance, business strategy and plans and objectives of management for future operations, are forward-looking statements. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “should” or “will” or the negative of these terms or other comparable terminology. Although we do not make forward-looking statements unless we believe we have a reasonable basis for doing so, we cannot guarantee their accuracy. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks outlined under “Risk Factors” or elsewhere in this report, which may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time and it is not possible for us to predict all risk factors, nor can we address the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause our actual results to differ materially from those contained in any forward-looking statements. The factors affecting these risks and uncertainties include, but are not limited to:

|

·

|

estimated quantities and quality of coal, oil and natural gas reserves;

|

|

·

|

fluctuations in the price of coal, oil, and natural gas;

|

|

·

|

inability to efficiently manage our operations;

|

|

·

|

the inability of management to effectively implement our strategies and business plans;

|

|

·

|

potential default under our secured obligations or material debt agreements;

|

|

·

|

inability to hire or retain sufficient qualified personnel;

|

|

·

|

inability to attract and obtain additional development capital;

|

|

·

|

increases in interest rates or our cost of borrowing;

|

|

·

|

deterioration in general economic conditions;

|

|

·

|

the occurrence of natural disasters, unforeseen weather conditions, or other events or circumstances that could impact our operations or could impact the operations of companies or contractors we depend upon in our operations;

|

|

·

|

inability to achieve future sales levels or other operating results; and

|

|

·

|

changes in U.S. GAAP or in the legal, regulatory and legislative environments in the markets in which we operate.

|

You should not place undue reliance on any forward-looking statement, each of which applies only as of the date of this report. Except as required by law, we undertake no obligation to update or revise publicly any of the forward-looking statements after the date of this report to conform our statements to actual results or changed expectations.

AVAILABLE INFORMATION

We file annual, quarterly and other reports and other information with the U.S. Securities and Exchange Commission ("SEC"). You can read these SEC filings and reports on the SEC’s website at www.sec.gov. You can also obtain copies of the documents at prescribed rates by writing to the Public Reference Section of the SEC at 100 F Street, NE, Washington, DC 20549 on official business days between the hours of 10:00 am and 3:00 pm. Please call the SEC at (800) SEC-0330 for further information on the operations of the public reference facilities. We will provide a copy of our annual report to security holders, including audited financial statements, at no charge upon receipt of a written request to us at American Power Corporation, 16 Market Square Center, 1400 16th Street Suite 400, Denver, CO 80202.

2

INDUSTRY AND MARKET DATA

The market data and certain other statistical information used throughout this report are based on independent industry publications, government publications, reports by market research firms or other published independent sources. In addition, some data is based on our good faith estimates.

USE OF TERMS

Except as otherwise indicated by the context, all references in this report to “we,” “us,” “our,” the “Company,” “AMPW,” and “American Power” refer to American Power Corporation, unless the context requires otherwise. We report our financial information on the basis of a September 30 fiscal year end.

3

PART I

ITEM 1.BUSINESS.

Overview

The Company was incorporated in the State of Nevada as a for-profit company on August 7, 2007. At the time of our incorporation, we were incorporated under the name “Teen Glow Makeup, Inc.” and our original business plan was to create a line of affordable teen makeup for girls. On November 20, 2009, Johannes Petersen acquired the majority of the shares of our issued and outstanding common stock in accordance with two stock purchase agreements by and between Mr. Petersen and Ms. Pamela Hutchinson and Ms. Andrea Mizushima, respectively. On March 30, 2010, we changed our intended business purpose to that of coal, oil, and natural gas exploration, development and production.

Our current primary business focus is to acquire, explore and develop coal, oil and gas properties in the United States, with a particular focus on the Rocky Mountains region. On March 30, 2010, our Board of Directors approved the proposal to change the Company’s name and to effect a 340-for-1 forward stock split. The Certificate of Change for the forward stock split was filed and approved by the Nevada Secretary of State on April 28, 2010. Also on April 28, 2010, Articles of Amendment were filed and approved with the Nevada Secretary of State to change the name of the Corporation to American Power Corporation. The Articles of Amendment also changed the authorized amount of capital stock to Five Hundred Million (500,000,000) shares of Common Stock, par value $0.001.

Business Description and Plan of Operation

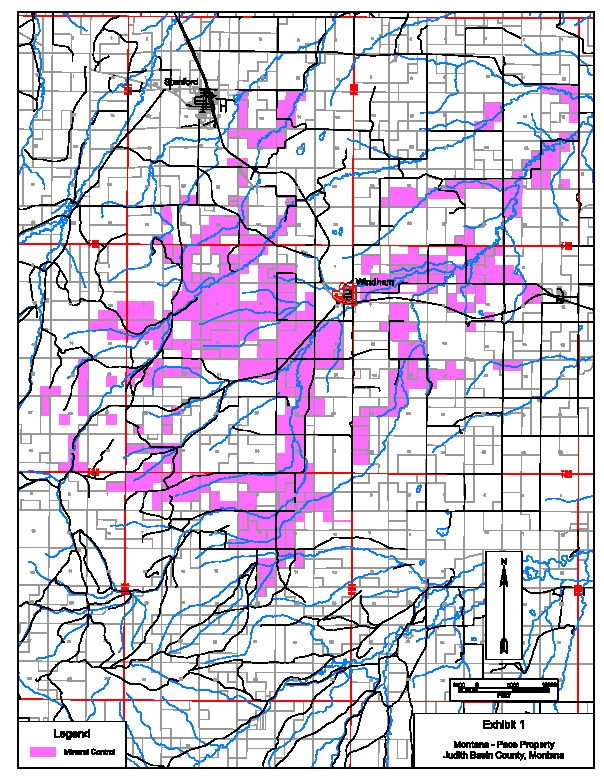

We have acquired certain coal and minerals rights located in the Judith Basin County, Montana, collectively described as the “PACE Coal Property.” Our PACE Coal Property and other uncontrolled properties make up the “PACE Coal Project." These rights are speculative in nature and additional exploration work is required to determine their value. Our plan of operation is to explore the PACE Coal Project and acquire and explore new properties which we believe are prospective for coal and/or hydrocarbons. To December 2011, the Company had completed a total of 14,076 feet of drilling and 18 drill sites have been completed. All drill locations corresponding to Phases I and II have been fully completed while one drill location corresponding to Phase III has been completed. Drilling operations were suspended in December 2011 due to weather considerations and are expected to resume in the spring of 2013 after finding capable drilling contractors and securing adequate financing. Our technical team has designated 14 Phase III drill holes as priority drill holes. These priority drill holes are expected to further define mineralization, provide additional coal quality data, and provide information to determine if any remaining Phase III drill holes will require coring. Although we have obtained encouraging preliminary results from the first two phases of the exploration drilling program at the PACE Coal Project, there can be no assurance that an economic coal and/or hydrocarbon reserve exists on the PACE Coal Project or on any other the exploration prospects we could eventually acquire.

We commissioned the preparation of a preliminary Mine Feasibility Study for the PACE Coal Project with the project data obtained during the 2011 drilling season and data from previous exploration work carried out by Mobil Oil Co. This preliminary study was completed by our engineering consultant Weir International, Inc. (“Weir”) in September 2012. Controlled property in the PACE Coal Project is comprised of acreage where the Company owns the coal and mineral rights but not the surface rights. Uncontrolled property in the PACE Coal Project is comprised of acreage where the Company owns neither the coal and mineral rights nor the surface rights; thus, the uncontrolled property will have to be successfully acquired by purchase or lease to develop the mine plan. The Mine Feasibility Study includes information on the geology and mineralization of the PACE Coal Project, a mine plan suitable to geology and production requirements and projections for production capacity, productivity, staffing levels, equipment and facilities, capital expenditures, operating costs and coal sales. According to the preliminary Mine Feasibility Study, 191.3 million tons of coal are expected to be produced over a 15-year mine life. At full production, the mine plan projects annual production of thermal coal at 7.9 million saleable tons (14.9 million ROM tons) per year, utilizing three continuous miner units and one longwall mining unit. Capital expenditures are estimated at approximately $402 million for future initial mine development and $730 million for sustaining capital over the 15-year mine plan. In addition, we estimate the cost of leasing uncontrolled coal properties to be $5.5 million plus royalties to be calculated as a percentage of actual production. The PACE Coal Project clean coal quality, based on the exploration data, is projected to be 11,750 Btu/lb and 2.28 percent sulfur (3.88 Lbs SO2/MBtu). The calorific value (Btu/lb) is among the highest in the major coal producing regions in the western United States.

Upon completion of Phase III of our planned exploration drilling program, we expect to obtain a final reserve study setting forth the quantity and classification of proven and probable coal reserves and a valuation thereof and final mine feasibility study by the summer of 2013. These final studies will incorporate the drilling results of all three phases of the exploration program.

Even if we complete our proposed exploration programs and are successful in identifying the presence of coal and/or hydrocarbons, we will have to spend substantial funds on further drilling, engineering studies, environmental and mine feasibility studies before we will know if we have a commercially viable coal, oil, and gas deposit or reserve.

4

Market Overview for Plan of Operation

Coal production in the United States in 2011 reached a level of 1,095.6 million short tons (1,084.4 million short tons in 2010) according to data from the Energy Information Administration (EIA), an increase of 1.0% from the 2010 level driven by export demand. Wyoming continued to be the largest coal-producing state with 438.7 million short tons, 0.9% lower than the 2010 level. By rank, bituminous coal represented 48.0% of total coal production in 2011, followed by subbituminous coal with 44.4%, while lignite and anthracite coal represented 7.4% and 0.2% of the total, respectively.

Coal consumption in the United States in 2011 reached a level of 1,002.9 million short tons (1,048.5 million short tons in 2010), a decrease of 4.4% from the 2010 level, with all coal-consuming sectors, except coke users, having lower consumption for the year. The electric power sector (electric utilities and independent power producers), which consumes about 93% of all coal in the US, is the overriding force for determining total domestic coal consumption. Coal consumption in the electric power sector decreased 4.4% to end 2011 at 932.5 million short tons (975.1 million short tons in 2010). In 2011, domestic consumption of metallurgical coal by the coking industry rose 1.6% to 21.4 million short tons (21.1 million short tons in 2010). In contrast, consumption of steam coal by the electric power, industrial, and commercial and institutional sectors decreased 4.4%, 6.2%, and 9.3%, respectively. Mild winter weather led to a decline in total electricity generation, leaving high stock levels. Natural gas prices also declined during 2011, allowing facilities that can use both coal and natural gas to alternate between fuels and company that have portfolios of coal and natural gas plants to utilize their gas plants more.

Total coal stocks increased to 231.9 million short tons at the end of 2011, compared to 231.7 million short tons at the end of 2010 (equivalent to a 0.1% increase from the 2010 level).

According to data for 2011, the average sales price of coal increased 15.2 % to $41.01 per short ton. However, the change in average sales price of coal from underground mines was greater (16.0%) than the change in average sales price of coal from surface mines (11.9%).

Western Region (includes Montana)

The Western Region is the largest coal–producing region in the US. In 2011, coal production in the Western Region of the United States (587.6 million short tons) declined 0.7% from 2010. The region, which includes Wyoming, was affected by the decrease in coal-fired electricity generation and limited access to foreign markets. Western production during 2011 was also affected by flooding in Montana.

In 2011, Montana, the second largest coal–producing state in the Western region, produced a total of 42.0 million short tons (44.7 million short tons in 2010), a sharp decrease of 6.1%. In 2011, surface production totaled 36.9 million short tons (40.3 million short tons in 2010) while underground production totaled 5.1 million short tons (4.4 million short tons in 2010). A total of six mines in Montana produced 36.5 million short tons of subbituminous coal, 5.1 million short tons of bituminous coal and 0.4 million short tons of lignite coal in 2011.

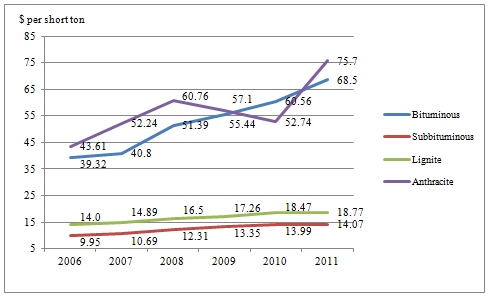

According to data from the EIA, domestic coal prices in 2011 averaged $41.01 per short ton. By coal rank, the average price in 2011 for bituminous coal was $68.50 per short ton, $14.07 per short ton for subbituminous coal, $18.77 per short ton for lignite coal and $75.70 per short ton for anthracite coal.

5

The following chart shows the average market price by coal rank for the period 2006–2011:

Due to its characteristics (i.e., bituminous coal, high energy content and sulfur content), we consider the coal in the PACE Coal property to be more comparable to the Illinois Basin coal. According to the EIA, the Illinois Basin coal price (11,800 Btu, 5.0 SO2) was $47.90 per short ton on December 14, 2012.

Internationally, Atlantic prices have declined as reduced European imports combined with warmer than expected Northern Hemisphere winter and falling industrial production, leaving power plants with ample inventory. At the same time, the U.S. domestic market’s depression exacerbated the supply–side issues in the form of increased U.S. exports and decreased U.S. imports. This freed up additional tonnage from Colombia, as it exported almost 4.5Mt less coal to the U.S. in 2011 than 2010. China and India will likely be the key drivers of the global seaborne market, where robust electricity generation continues to drive strong thermal coal demand.

Upon completion of the final reserve and mine feasibility studies, we will consider commissioning a market study to determine the relevant market price for our coal as well as the impact of transportation costs, access to ports and export facilities, among other variables, on the final sale price for both domestic and overseas markets.

Government Approvals

The Company requires to obtain drilling permits from the Montana Department of Environmental Quality in order to carry out drilling operations on its PACE Coal Project. In 2011, the Company received drilling permits that allowed it to carry out exploration activities on the project. Further drilling, or modifications to our drilling plan will require modification of our drilling permits by the Montana Department of Environmental Quality. The Company would also require additional permits from the state and federal governments once it moves, if at all, to the development and mining phase of the project.

We are required to obtain drilling permits from the Montana Department of Environmental Quality (“Montana DEQ”) in order to carry out drilling operations on our PACE Coal Project. In 2011, we received Prospecting Permit No. X2011335, which allowed us to carry out exploration activities on the project from July 29, 2011 to July 29, 2012. We applied for two amendments to the original exploration permit to obtain permits for Phase II and Phase III drill holes. The permits were obtained on September 12, 2011 and October 25, 2011.

The current Prospecting Permit ID: X2011335 (and the Notice of Intent Permit ID: N2011007), which was issued, and renewed, by the Montana DEQ per a letter dated April 24, 2012, affects only privately owned surface and private minerals. Because both the mineral and surface ownership are privately owned, the only governmental permit that is required for our current exploration activities is by the Montana DEQ, and no additional permits are required by the Bureau of Land Management (BLM) or U.S. Forest Service.

Further drilling, or modifications to our drilling plan, will require modification of our drilling permits by the Montana DEQ. We would also be required to obtain additional permits from the state and federal governments if we move to the development and mining phase of the project.

Existing or Probable Governmental Regulations

Federal, state and local authorities regulate the U.S. coal mining industry with respect to matters such as employee health and safety, permitting and licensing requirements, air quality standards, water pollution, plant and wildlife protection, reclamation and restoration of mining properties after mining has been completed, discharge of materials into the environment, surface subsidence from underground mining and the effects of mining on groundwater quality and availability. Numerous federal, state and local governmental permits and approvals are required for coal mining activities.

We comply with all relevant government regulations at the federal, state and local level. We believe that we have obtained all permits currently required to conduct our mining exploration activities. We do not believe there are any matters that pose a material risk to maintaining our existing permits or that materially hinder our ability to secure future permits.

If we are able to move forward with the development and eventual operation of the PACE Coal Project, we would be subject to the following regulatory requirements.

6

Mine Safety and Health. Companies are subject to health and safety standards both at the federal and state level. The regulations are comprehensive and affect numerous aspects of mining operations, including training of mine personnel, mining procedures, blasting, the equipment used in mining operations and other matters. The Mine Safety and Health Administration (MSHA) is the agency responsible for monitoring compliance with the federal mine health and safety standards. MSHA has various enforcement tools that it can use, including the issuance of monetary penalties and orders of withdrawal from a mine or part of a mine. MSHA has recently taken a number of actions to identify mines with safety issues, and has engaged in targeted enforcement, awareness, outreach and rulemaking activities to reduce the number of mining fatalities, accidents and illnesses. There has also been an industry–wide increase in the monetary penalties assessed for citations of a similar nature.

Black Lung. Under the Black Lung Benefits Revenue Act of 1977 and the Black Lung Benefits Reform Act of 1977, as amended in 1981, each U.S. coal mine operator must pay federal black lung benefits and medical expenses to claimants who are current and former employees and last worked for the operator after July 1, 1973. Coal mine operators must also make payments to a trust fund for the payment of benefits and medical expenses to claimants who last worked in the coal industry prior to July 1, 1973. Historically, less than 7% of the miners currently seeking federal black lung benefits are awarded these benefits. The trust fund is funded by an excise tax on U.S. production of up to $1.10 per ton for deep–mined coal and up to $0.55 per ton for surface–mined coal, neither amount to exceed 4.4% of the gross sales price.

Environmental Laws. Coal companies are subject to various federal and state environmental laws. Some of these laws, discussed below, would place many requirements on any future coal mining operation. Federal and state regulations require regular monitoring of mines and other facilities to ensure compliance.

Surface Mining Control and Reclamation Act. In the U.S., the Surface Mining Control and Reclamation Act of 1977 (SMCRA), which is administered by the Office of Surface Mining Reclamation and Enforcement (OSM), established mining, environmental protection and reclamation standards for all aspects of U.S. surface mining as well as many aspects of deep mining. Mine operators must obtain SMCRA permits and permit renewals for mining operations from the OSM. Where state regulatory agencies have adopted federal mining programs under SMCRA, the state becomes the regulatory authority.

The Abandoned Mine Land Fund, which is part of SMCRA, requires a fee on all coal produced in the U.S. The proceeds are used to rehabilitate lands mined and left unreclaimed prior to August 3, 1977 and to pay health care benefit costs of orphan beneficiaries of the Combined Fund created by the Coal Industry Retiree Health Benefit Act of 1992. The fee was $0.35 per ton of surface–mined coal and $0.15 per ton of deep–mined coal, effective through September 30, 2007. Pursuant to the Tax Relief and Health Care Act of 2006, from October 1, 2007 through September 30, 2012, the fee is $0.315 per ton of surface–mined coal and $0.135 per ton of underground mined coal. From October 1, 2012 through September 30, 2021, the fee will be reduced to $0.28 per ton of surface–mined coal and $0.12 per ton of underground-mined coal. SMCRA stipulates compliance with many other major environmental programs. These programs include the Clean Air Act; Clean Water Act; Resource Conservation and Recovery Act (RCRA); and Comprehensive Environmental Response, Compensation, and Liability Acts (CERCLA, commonly known as Superfund). Besides OSM, other federal regulatory agencies are involved in monitoring or permitting specific aspects of mining operations. The U.S. Environmental Protection Agency (EPA) is the lead agency for states or tribes with no authorized programs under the Clean Water Act, RCRA and CERCLA. The U.S. Army Corps of Engineers regulates activities affecting navigable waters and waters of the U.S., including wetlands, and the U.S. Bureau of Alcohol, Tobacco and Firearms regulates the use of explosive blasting materials.

Clean Air Act. The Clean Air Act and the comparable state laws that regulate the emissions of materials into the air affect U.S. coal mining operations both directly and indirectly. Direct impacts on coal mining and processing operations may occur through the Clean Air Act permitting requirements and/or emission control requirements relating to particulate matter. It is possible that the more stringent national ambient air quality standards (NAAQS) will directly impact future mining operations by, for example, requiring additional controls of emissions from mining equipment and vehicles. In addition, in September 2009, the EPA adopted new rules tightening and adding additional particulate-matter emissions limits for coal preparation and processing plants constructed, reconstructed or modified after April 28, 2008. The Clean Air Act indirectly, but more significantly, affects the coal industry by extensively regulating the air emissions of sulfur dioxide, nitrogen oxides, mercury, particulate matter and other substances emitted by coal–based electricity generating plants. Air emissions programs that may affect future operations, directly or indirectly, include, but are not limited to, the Acid Rain Program, NOx SIP Call, the Clean Air Interstate Rule (CAIR), New Source Performance Standards (NSPS), Maximum Achievable Control Technology (MACT) emissions limits for Hazardous Air Pollutants, the Regional Haze program and New Source Review. In addition, in recent years, the EPA has adopted more stringent NAAQS for particulate matter, nitrogen oxide and sulfur dioxide. The EPA has also proposed a more stringent ozone standard but withdrew it last year; the ozone standard is due for reconsideration in 2013. Many of these programs and regulations have resulted in litigation, which has not been completely resolved.

7

On July 6, 2011, the EPA finalized its final Cross State Air Pollution Rule (CSAPR) to address interstate transport of emissions from coal–based electrical generation plants. The rule, which was developed to replace CAIR and includes a supplemental rulemaking finalized on December 15, 2011, imposes state–by–state budgets on nitrogen oxides and sulfur dioxide emissions from coal–based electrical generation plants in 23 states from Texas eastward (not including the New England states or Delaware) and provides for an allowance trading program to meet those budgets. While CSAPR has an initial compliance deadline of January 1, 2012, the rule was challenged and, on December 30, 2011, the U.S. Court of Appeals for the District of Columbia stayed CSAPR and advised that the EPA is expected to continue administering CAIR until the pending challenges are resolved. Expedited briefing on the merits of the challenge is underway. On December 16, 2011, the EPA issued the Mercury and Air Toxic Standards, which impose MACT emission limits on hazardous air emissions from new and existing coal–based electric generating plants. The rule also revised NSPS for nitrogen oxides, sulfur dioxides and particulate matter for coal–based electricity generating plants. The rule provides three years for compliance, or up to four years for existing sources if necessary. In December 2009, the EPA published its finding that atmospheric concentrations of greenhouse gases endanger public health and welfare within the meaning of the Clean Air Act, and that emissions of greenhouse gases from new motor vehicles and new motor vehicle engines are contributing to air pollution that is endangering public health and welfare within the meaning of the Clean Air Act. In May 2010, the EPA published final greenhouse gas emission standards for new motor vehicles pursuant to the Clean Air Act. Both the endangerment finding and motor vehicle standards are the subject of litigation.

Because the Clean Air Act specifies that the prevention of significant deterioration (PSD) program applies once emissions of regulated pollutants exceed either 100 or 250 tons per year (depending on the type of source), millions of sources previously unregulated under the Clean Air Act could be subject to greenhouse gas reduction measures. The EPA published a rule in June 2010 to limit the number of greenhouse gas sources that would be subject to the PSD program. In the so–called “tailoring rule,” the EPA limited the regulation of greenhouse gases from certain stationary sources to those that emit more than 75,000 tons of greenhouse gases per year (for sources that would be subject to PSD permitting regardless of greenhouse gas emissions due to other emissions) or 100,000 tons of greenhouse gases per year (for sources not subject to PSD permitting for any other air emissions), measured by “carbon dioxide equivalent.” Whether the EPA has the statutory authority under the Clean Air Act to adopt the tailoring rule is the subject of litigation. In December 2010, the EPA announced a settlement with states and environmental groups that had filed litigation challenges to the EPA’s decisions not to establish greenhouse gas emission standards for fossil fuel–fired power plants and for petroleum refineries under section 111 of the Clean Air Act. In the settlement, the EPA agreed (1) to sign proposed new source performance standards for new and modified electric utility steam generating units under section 111(b), as well as proposed guidelines for states’ development of emission standards for existing electric utility steam generating units under section 111(d), by July 26, 2011; and (2) to take final action on the proposed section 111(b) standards and section 111(d) guidelines by May 26, 2012. The EPA has not yet proposed these rules. Whatever the EPA determines the new source performance standards to be, this will then be the minimum requirement for best available control technology requirements under the PSD program.

Clean Water Act. The Clean Water Act of 1972 affects U.S. coal mining operations by requiring both technology–based and, if necessary, water quality–based effluent limitations and treatment standards for wastewater discharge through the National Pollutant Discharge Elimination System (NPDES). Regular monitoring, reporting requirements and performance standards are requirements of NPDES permits that govern the discharge of pollutants from mine–related point sources into water. Section 404 of the Clean Water Act requires mining companies to obtain U.S. Army Corps of Engineers permits to place material in streams for the purpose of creating slurry ponds, water impoundments, refuse areas, valley fills or other mining activities. States are empowered to develop and apply “in stream” water quality standards. These standards are subject to change and must be approved by the EPA. Discharges must either meet state water quality standards or be authorized through available regulatory processes such as alternate standards or variances. “In stream” standards vary from state to state. Additionally, through the Clean Water Act section 401 certification program, states have approval authority over federal permits or licenses that might result in a discharge to their waters. States consider whether the activity will comply with their water quality standards and other applicable requirements in deciding whether or not to certify the activity.

Resource Conservation and Recovery Act. RCRA, which was enacted in 1976, affects U.S. coal mining operations by establishing “cradle to grave” requirements for the treatment, storage and disposal of hazardous wastes. Typically, the only hazardous wastes generated at a mine site are those from products used in vehicles and for machinery maintenance. Coal mine wastes, such as overburden and coal cleaning wastes, are not considered hazardous wastes under RCRA. Subtitle C of RCRA exempted fossil fuel combustion wastes from hazardous waste regulation until the EPA completed a report to Congress and made a determination on whether the wastes should be regulated as hazardous. In a 1993 regulatory determination, the EPA addressed some high volume–low toxicity coal combustion materials generated at electric utility and independent power producing facilities. In May 2000, the EPA concluded that coal combustion materials do not warrant regulation as hazardous wastes under RCRA. The EPA has retained the hazardous waste exemption for these materials. The EPA is evaluating national waste guidelines for coal combustion materials placed at a mine. National guidelines for mine–fills may affect the cost of ash placement at mines. The EPA revisited its May 2000 determination and proposed new requirements for coal combustion residue (CCR) management on June 21, 2010. That proposal contains two options: (1) to continue to regulate CCR as a non–hazardous waste, or (2) to regulate CCR as special waste under the hazardous waste regulations.

CERCLA (Superfund). CERCLA affects U.S. coal mining and hard rock operations by creating liability for investigation and remediation in response to releases of hazardous substances into the environment and for damages to natural resources. Under CERCLA, joint and several liability may be imposed on waste generators, site owners or operators and others, regardless of fault. Under the EPA’s Toxic Release Inventory process, companies are required annually to report the use, manufacture or processing of listed toxic materials that exceed defined thresholds, including chemicals used in equipment maintenance, reclamation, water treatment and ash received for mine placement from power generation customers.

8

Endangered Species Act. The U.S. Endangered Species Act and counterpart state legislation is intended to protect species whose populations allow for categorization as either endangered or threatened. With respect to obtaining mining permits, protection of endangered or threatened species may have the effect of prohibiting, limiting the extent or causing delays that may include permit conditions on the timing of soil removal, timber harvesting, road building and other mining or agricultural activities in areas containing the affected species.

Use of Explosives. Surface mining operations are subject to numerous regulations relating to blasting activities. The storage of explosives is also subject to federal regulatory requirements.

Number of Employees

The Company has no employees and three consultants (of which two, Mr. Johannes Petersen and Mr. Alvaro Valencia, are directors).

ITEM 1A.RISK FACTORS.

We operate in a highly competitive environment in which there are numerous factors which can influence our business, financial position, or results of operations and which can also cause the market value of our common stock to decline. Many of these factors are beyond our control and therefore, are difficult to predict. The following section sets forth what we believe to be the principal risks that could affect us, our business or our industry, and which could result in a material adverse impact on our financial results or cause the market price of our common stock to fluctuate or decline.

RISKS ASSOCIATED WITH OUR BUSINESS

We have no history of revenues from operations, we may never operate profitably and investors may lose all of their investment in our company.

We have no history of revenues from operations. We are an exploration stage company with only a limited operating history upon which to base an evaluation of our current business and future prospects. Further, we do not have an established history of locating and developing mineral and oil and gas properties. As a result, the revenue and income potential of our business is unproven and there can be no assurance that we will ever operate profitably. The exploration and development of mineral properties requires substantial capital, often over a substantial period of time. We anticipate that we will incur increased operating expenses without realizing any revenues over the next several years. We therefore expect to incur significant losses into the foreseeable future. If we are unable to successfully develop the PACE Coal Property or other properties we acquire in the future, we will not be able to establish revenues, earn profits, or continue operations, and our stock may become worthless, causing our investors to lose all of their investment in our company.

Our independent auditors have raised substantial doubt about our ability to continue as a going concern.

At June 30, 2012, March 31, 2012 and September 30, 2011, we had net losses of $1,537,429, $1,141,719 and $1,952,064, respectively. As such, our independent auditors have included in their auditor report an explanatory paragraph that states that our continuing losses from operations raise substantial doubt as to our ability to continue as a going concern. Our ability to continue as a going concern is contingent upon our ability to obtain additional financing as we continue exploration of the PACE Coal Property. If we are unable to obtain future financing to meet our working capital requirements, we will have to delay our exploration and development plans or cease operations altogether.

We currently own rights with respect to a sole mineral property which increases the risks associated with our operations.

The PACE Coal Project is currently our sole project. The agreements, as amended, under which we acquired the PACE Coal Property require us to make future payments to the sellers of the property, which payment obligations are secured by the property, and to complete of a final reserve study and mine feasibility study by April 9, 2013. With respect to the obligation to compete a final feasibility study, under our current drilling schedule, we believe we are unlikely to meet the April 9, 2013 deadline and plan to request an extension as our Phase II drilling progresses. If we are unable to make these payments or complete these other obligations and cannot obtain waivers or amendments to address these breaches, we may lose our interest in the property. In addition, we must acquire by purchase or lease the uncontrolled property in the PACE Coal Project necessary to develop the mine plan. The Company plans to evaluate all available exploration data to delineate the extent of the potential reserves and mineralized material, estimate their recoverability and determine requirements for additional exploration and analytical testing. The Company commissioned the preparation of a preliminary Mine Feasibility Study for the PACE Coal Project with the project data obtained during the 2011 drilling season. The studies were completed in September 2012.

We are subject to all of the risks inherent in the mining industry.

As an exploration stage company, our work is highly speculative and involves unique and greater risks than are generally associated with other businesses. There can be no assurance that the PACE Coal Project or any of the properties we acquire contain or will contain a commercially viable ore body or reserves until additional exploration work is done and an evaluation based on such work concludes that development of and production from the ore body is technically, economically, and legally feasible. We are subject to all of the risks inherent in the mining industry, including, without limitation, the following (some of which we discuss in more detail below):

9

|

·

|

Success in discovering and developing commercially viable quantities of minerals is the result of a number of factors, including the quality of management, the interpretation of geological data, the level of geological and technical expertise, and the quality of land available for exploration;

|

|

·

|

Exploration for minerals is highly speculative and involves substantial risks, even when conducted on properties known to contain significant quantities of mineralization, and most exploration projects do not result in the discovery of commercially mineable deposits of ore;

|

|

·

|

Operations are subject to a variety of existing laws and regulations relating to exploration and development, permitting procedures, safety precautions, property reclamation, employee health and safety, air and water quality standards, pollution and other environmental protection controls, all of which are subject to change and are becoming more stringent and costly to comply with;

|

|

·

|

A large number of factors beyond our control, including fluctuations in metal and minerals prices and production costs, inflation, the proximity and liquidity of minerals markets and processing equipment, government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals, and environmental protection, and other economic conditions, will affect the economic feasibility of mining;

|

|

·

|

Once mineralization is discovered, it may take several years from the initial phases of drilling until production is possible, during which time the economic feasibility of production may change;

|

|

·

|

Substantial expenditures are required to establish proven and probable ore reserves through drilling, to determine metallurgical processes to extract the metals or minerals from the ore and, in the case of new properties, to construct mining and processing facilities; and

|

|

·

|

If we proceed to development of a mining operation, our mining activities would be subject to substantial operating risks and hazards, including metal bullion losses, environmental hazards, industrial accidents, labor disputes, encountering unusual or unexpected geologic formations or other geological or grade problems, encountering unanticipated ground or water conditions, cave-ins, pit-wall failures, flooding, rock falls, periodic interruptions due to inclement weather conditions or other unfavorable operating conditions and other acts of God. Some of these risks and hazards are not insurable or may be subject to exclusion or limitation in any coverage which we obtain or may not be insured due to economic considerations.

|

Loss of key personnel and failure to attract qualified managers, technologists, independent engineers, and geologists could limit our growth and negatively impact our operations.

We depend upon our consultants to a substantial extent. In particular, we depend upon Mr. Alvaro Valencia, our President and Chief Executive Officer, and Mr. Johannes Petersen, our Secretary and Chief Financial Officer, for their skills, experience, knowledge of the company, and industry contacts. The loss of Mr. Valencia or Mr. Petersen could have a material adverse effect on our business, results of operations or financial condition.

As we grow, we may increasingly require field managers with experience in our industry and skilled engineers, geologists, and technologists to operate diagnostic, seismic, and 3D equipment. It is impossible to predict the availability of qualified managers, technologists, skilled engineers, and geologists or the compensation levels that will be required to hire them. In particular, there is a very high demand for qualified technologists who are particularly necessary to operate systems similar to the ones that we intend to operate. We may not be able to hire and retain a sufficient number of technologists, engineers, and geologists and we may be required to pay bonuses and higher independent contractor rates to our technologists, engineers, and geologists, which would increase our expenses. The loss of the services of any member of our senior management or our inability to hire qualified managers, technologists, skilled engineers, and geologists at economically reasonable compensation levels could adversely affect our ability to operate and grow our business.

Complying with federal and state regulations is an expensive and time-consuming process, and any failure to comply could result in substantial penalties.

Our exploration efforts are directly or indirectly subject to extensive and continually changing regulation affecting mining and the oil and natural gas industry. Many departments and agencies, both federal and state, are authorized by statute to issue, and have issued, rules and regulations binding on the mining and oil and natural gas industry and our individual participants. The failure to comply with such rules and regulations can result in substantial penalties. The regulatory burden on the mining and oil and natural gas industry increases our cost of doing business and, consequently, will affect our profitability.

If operations on the properties we acquire are found to be in violation of any of the laws and regulations to which we are subject, we may be subject to the applicable penalties associated with the violation, including civil and criminal penalties, damages, fines, and the curtailment of operations. Any penalties, damages, fines, or curtailment of operations, individually or in the aggregate, could adversely affect our ability to operate our business and our financial results. In addition, many of these laws and regulations have not been fully interpreted by the regulatory authorities or the courts, and their provisions are open to a variety of interpretations. Any action against us for violation of these laws or regulations, even if we successfully defend against it, could cause us to incur significant legal expenses and divert management’s attention from the operation of our business.

10

We may experience competition from other mining and energy exploration and production companies, and this competition could adversely affect our revenues and our business.

The market for coal, oil, and natural gas properties is generally highly competitive. Many existing competitors, as well as potential new competitors, have longer operating histories, greater name recognition, substantial track records, and significantly greater financial, technical, and technological resources than us. This may allow them to devote greater resources to the development and promotion of their coal, oil, and natural gas exploration and production projects. Many of these competitors offer a wider range of coal, oil, and natural gas opportunities not available to us and may attract business partners, consequently resulting in a decrease of our business opportunities. These competitors may also engage in more extensive research and development, adopt more aggressive strategies and make more attractive offers to existing and potential purchasers and partners. Furthermore, competitors may develop technology and exploration strategies that are equal or superior to us and achieve greater market recognition. In addition, current and potential competitors have established or may establish cooperative relationships among themselves or with third parties to better address the needs of our target market. As a result, it is possible that new competitors may emerge and rapidly acquire significant market share.

There can be no assurance that we will be able to compete successfully against our current or future competitors or that competition will not have a material adverse effect on our business, results of operations and financial condition.

We will need to increase the size of our organization, and may experience difficulties in managing growth.

We expect to experience a period of significant expansion in headcount, facilities, infrastructure, and overhead and anticipate that further expansion will be required to address potential growth and market opportunities. Future growth will impose significant added responsibilities on members of management, including the need to identify, recruit, maintain, and integrate additional independent contractors and managers. Our future financial performance and our ability to compete effectively will depend, in part, on our ability to manage any future growth effectively.

Coal, oil and natural gas prices are volatile, and low prices could have a material adverse impact on our business.

Our growth and future profitability and the carrying value of our properties depend substantially on prevailing coal, oil, and natural gas prices. Prices also affect the amount of cash flow available for capital expenditures, if any, and our ability to borrow and raise additional capital. The amount we will be able to borrow under any credit facility will be based in part on changing expectations of future prices. Lower prices may also reduce the amount of coal, oil, and natural gas that we can economically produce and have an adverse effect on the value of our properties. Prices for coal, oil, and natural gas have increased significantly and have been more volatile over the past twelve months. Historically, the markets for coal, oil, and natural gas have been volatile, and they are likely to continue to be volatile in the future. Among the factors that can cause volatility are:

|

·

|

the domestic and foreign supply of coal, oil, and gas;

|

|

·

|

the ability of members of the Organization of Petroleum Exporting Countries, or OPEC, and other producing countries to agree upon and maintain oil prices and production levels;

|

|

·

|

the level of consumer product demand;

|

|

·

|

the growth of consumer product demand in emerging markets, such as China and India;

|

|

·

|

labor unrest in coal, oil, and natural gas producing regions;

|

|

·

|

weather conditions, including hurricanes and other natural disasters;

|

|

·

|

the price and availability of alternative fuels;

|

|

·

|

the price of foreign imports; and

|

|

·

|

worldwide economic conditions.

|

11

These external factors and the volatile nature of the energy markets make it difficult to estimate future prices of coal, oil, and natural gas and our resulting ability to raise capital.

Assets we acquire may prove to be worth less than we paid because of uncertainties in evaluating recoverable reserves and potential liabilities.

Our initial growth is expected to result from acquisitions of mineral and oil and gas properties. Successful acquisitions require an assessment of a number of factors, including estimates of recoverable reserves, exploration potential, future energy prices, operating and capital costs, and potential environmental and other liabilities. Such assessments are inexact and their accuracy is inherently uncertain. Typically, we acquire interests in properties on an “as is” basis with limited remedies for breaches of representations and warranties.

As a result of these factors, we may not be able to acquire coal, oil, and natural gas properties that contain economically recoverable reserves or be able to complete such acquisitions on acceptable terms.

Actual future production, coal, oil, and natural gas prices, revenues, taxes, development expenditures, operating expenses, and quantities of recoverable coal, oil, and natural gas reserves will vary from those estimated. Any significant variance could materially affect the estimated quantities and the value of any potential reserves.

Exploration and development drilling efforts may not be successful.

We require significant amounts of undeveloped leasehold acreage in order to further our development efforts. Exploration, development, drilling, and production activities are subject to many risks, including the risk that commercially productive reservoirs will not be discovered. We invest in property, including undeveloped leasehold acreage, which we believe will result in projects that will add value over time. However, we cannot guarantee that all of our prospects will result in viable projects or that we will not abandon our initial investments. Additionally, we cannot guarantee that the leasehold acreage we acquire will be profitably developed, that new wells drilled on the properties will be productive or that we will recover all or any portion of our investment in such leasehold acreage, mines, or wells. Drilling for oil and natural gas may involve unprofitable efforts, not only from dry wells but also from wells that are productive but do not produce sufficient net reserves to return a profit after deducting operating and other costs. We rely to a significant extent on 3D seismic data and other advanced technologies in identifying leasehold acreage prospects and in determining whether or not to participate in a new well. The 3D seismic data and other technologies we use do not allow us to know conclusively prior to acquisition of leasehold acreage or the drilling of a well whether oil or natural gas is present or may be produced economically.

The unavailability or high cost of drilling rigs, equipment, supplies, personnel, and energy field services could adversely affect our ability to execute our exploration and development plans on a timely basis and within our budget.

Our industry is cyclical and, from time to time, there is a shortage of drilling rigs, equipment, supplies, or qualified personnel to operate our properties. During these periods, the costs and delivery times of rigs, equipment, and supplies are substantially greater. In addition, the demand for, and wage rates of, qualified drilling rig crews rise as the number of active rigs in service increases. As a result of increasing levels of exploration and production in response to strong prices of oil and natural gas, the demand for oilfield services has risen, and the costs of these services are increasing, while the quality of these services may suffer. If the unavailability or high cost of drilling rigs, equipment, supplies, or qualified personnel is particularly severe in Colorado and Montana, we could be materially and adversely affected because we expect our properties to be concentrated in those states.

Title to the properties in which we have, or will have, an interest in may be impaired by title defects.

We seek to confirm the validity of our rights to title to, or contract rights with respect to, each mineral property in which we have a material interest. Title insurance generally is not available, and our ability to ensure that we have obtained a secure claim to individual mineral properties or mining concessions is limited. We generally do not conduct surveys of our properties until they have reached the development stage, and therefore, the precise area and location of such properties could be in doubt. Accordingly, our mineral properties could be subject to prior unregistered agreements, transfers or claims, and title could be affected by, among other things, undetected defects. In addition, we might be unable to operate our properties as permitted or to enforce our rights with respect to our properties. Generally, under the terms of the operating agreements affecting our properties, any monetary loss is to be borne by all parties to any such agreement in proportion to their interests in such property. If there are any title defects or defects in the assignment of rights in properties in which we hold an interest, we will suffer a financial loss.

12

Our decision to acquire a property will depend in part on the evaluation of data obtained from engineering studies, geophysical and geological analyses, and seismic and other information, the results of which are often incomplete or inconclusive.

Our reviews of acquired properties may be inherently incomplete because it is not always feasible to perform an in-depth review of the individual properties involved in each acquisition. Even a detailed review of records and properties may not necessarily reveal existing or potential problems, nor will it permit a buyer to become sufficiently familiar with the properties to assess fully their deficiencies and potential. Inspections may not always be performed on every well and environmental problems, such as ground water contamination, plugging, or orphaned well liability are not necessarily observable even when an inspection is undertaken.

We are subject to complex laws and regulations, including environmental regulations, which can adversely affect the cost, manner, or feasibility of doing business.

The exploration and development of mineral and natural gas and oil properties in the United States is subject to extensive laws and regulations, including environmental laws and regulations. We may be required to make large expenditures to comply with environmental and other governmental regulations. Matters subject to regulation include, but are not limited to:

|

·

|

location and density of wells;

|

|

·

|

the handling of drilling fluids and obtaining discharge permits for drilling operations;

|

|

·

|

accounting for and payment of royalties on production from state, federal, and Indian lands;

|

|

·

|

bonds for ownership, development, and production of coal, natural gas, and oil properties;

|

|

·

|

transportation of natural gas and oil by pipelines;

|

|

·

|

operation of wells and reports concerning operations; and

|

|

·

|

taxation.

|

Under these laws and regulations, we could be liable for personal injuries, property damage, oil spills, discharge of hazardous materials, remediation and clean-up costs, and other environmental damages. Failure to comply with these laws and regulations also may result in the suspension or termination of our operations and subject us to administrative, civil, and criminal penalties. Moreover, these laws and regulations could change in ways that substantially increase our costs. Accordingly, any of these liabilities, penalties, suspensions, terminations, or regulatory changes could materially adversely affect our financial condition and results of operations enough to possibly force us to cease our business operations.

RISKS ASSOCIATED WITH OUR COMMON STOCK

The price of our common stock is volatile and you may not be able to resell your shares at a favorable price.

Regardless of whether an active trading market for our common stock develops, the market price of our common stock is volatile and you may not be able to resell your shares at or above the price you paid for such shares. The following factors could affect our stock price:

|

·

|

the status of the PACE Coal Project;

|

|

·

|

our operating and financial performance and prospects;

|

|

·

|

quarterly variations in the rate of growth of our financial indicators, such as net income per share, net income, and revenues;

|

|

·

|

changes in revenue or earnings estimates or publication of research reports by analysts about us or the coal exploration and production industry;

|

|

·

|

potentially limited liquidity;

|

|

·

|

actual or anticipated variations in our reserve estimates and quarterly operating results;

|

|

·

|

changes in coal, natural gas, and oil prices;

|

|

·

|

sales of our common stock by significant stockholders and future issuances of our common stock;

|

13

|

·

|

increases in our cost of capital;

|

|

·

|

changes in applicable laws or regulations, court rulings, and enforcement and legal actions;

|

|

·

|

commencement of or involvement in litigation;

|

|

·

|

changes in market valuations of similar companies;

|

|

·

|

additions or departures of key management personnel;

|

|

·

|

general market conditions, including fluctuations in and the occurrence of events or trends affecting the price of natural gas and oil; and

|

|

·

|

domestic and international economic, legal, and regulatory factors unrelated to our performance.

|

We have no plans to pay dividends on our common stock.

We do not anticipate paying any cash dividends on our common stock in the foreseeable future. We currently intend to retain future earnings, if any, to finance the expansion of our business. Our future dividend policy is within the discretion of our board of directors and will depend upon various factors, including our business, financial condition, results of operations, capital requirements, investment opportunities, and restrictions imposed by our debentures and credit facility.

Because our common stock is deemed a “penny stock,” an investment in our common stock should be considered high risk and subject to marketability restrictions.

Since our common stock is a penny stock, as defined in Rule 3a51-1 under the Securities Exchange Act, it will be more difficult for investors to liquidate their investment even if and when a market develops for the common stock. Until the trading price of the common stock rises above $5.00 per share, if ever, trading in the common stock is subject to the penny stock rules of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) specified in Rules 15g-1 through 15g-10. Those rules require broker-dealers, before effecting transactions in any penny stock, to:

|

·

|

Deliver to the customer, and obtain a written receipt for, a disclosure document;

|

|

·

|

Disclose certain price information about the stock;

|

|

·

|

Disclose the amount of compensation received by the broker-dealer or any associated person of the broker-dealer;

|

|

·

|

Send monthly statements to customers with market and price information about the penny stock; and

|

|

·

|

In some circumstances, approve the purchaser’s account under certain standards and deliver written statements to the customer with information specified in the rules.

|

Consequently, the penny stock rules may restrict the ability or willingness of broker-dealers to sell the common stock and may affect the ability of holders to sell their common stock in the secondary market and the price at which such holders can sell any such securities. These additional procedures could also limit our ability to raise additional capital in the future.

If we fail to remain current on our reporting requirements, we could be removed from the OTC Bulletin Board, which would limit the ability of broker-dealers to sell our securities and the ability of stockholders to sell their securities in the secondary market.

Companies trading on the OTC Bulletin Board, such as us, must be reporting issuers under Section 12 of the Exchange Act and must be current in their reports under Section 13, in order to maintain price quotation privileges on the OTC Bulletin Board. More specifically, FINRA has enacted Rule 6530, which determines the eligibility of issuers quoted on the OTC Bulletin Board by requiring an issuer to be current in its filings with the Commission. Pursuant to FINRA Rule 6530(e), if we file our reports late with the Commission three times in a two-year period or our securities are removed from the OTC Bulletin Board for failure to timely file twice in a two-year period then we will be ineligible for quotation on the OTC Bulletin Board. As a result, the market liquidity for our securities could be severely adversely affected by limiting the ability of broker-dealers to sell our securities and the ability of stockholders to sell their securities in the secondary market.

14

FINRA sales practice requirements may limit a stockholder’s ability to buy and sell our stock.

In addition to the “penny stock” rules described above, FINRA has adopted rules that require that, in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low-priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low-priced securities will not be suitable for at least some customers. FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock and have an adverse effect on the market for our shares.

We will need additional capital to finance our planned growth, which we may not be able to raise or may only be available on terms unfavorable to us or our stockholders, which may result in our inability to fund our working capital requirements and harm our operational results.

We have and expect to continue to have substantial capital expenditure and working capital needs. We will need to rely on borrowings under our credit facility or raise additional cash to fund our exploration and acquisition plans, pay outstanding long-term debt, and implement our growth strategy.

If low coal, natural gas, and oil prices, operating difficulties or other factors, many of which are beyond our control, cause our revenues or cash flows from operations to decrease, we may be limited in our ability to spend the capital necessary to complete our development, production, and exploration programs. If our resources or cash flows do not satisfy our operational needs, we will require additional financing, in addition to anticipated cash generated from our operations, to fund our planned growth. Additional financing might not be available on terms favorable to us or at all. If adequate funds were not available or were not available on acceptable terms, our ability to fund our operations, take advantage of unanticipated opportunities, develop or enhance our business or otherwise respond to competitive pressures would be significantly limited. In such a capital restricted situation, we may curtail our acquisition, drilling, development, and exploration activities or be forced to sell some of our assets on an untimely or unfavorable basis.

If we raise additional funds through the issuance of equity or convertible debt securities, the percentage ownership of our stockholders would be reduced, and these newly issued securities might have rights, preferences, or privileges senior to those of existing stockholders.

|

ITEM 1B.UNRESOLVED STAFF COMMENTS.

|

Not applicable.

|

ITEM 2.PROPERTIES.

|

Ownership of Coal Rights

On March 31, 2010, the Company, Future Gas Holdings, Ltd. (“Future Gas”) and JBM Energy Company, LLC (“JBM Energy”) entered into an Assignment and Assumption of Coal Agreement (the “Assignment and Assumption of Coal Agreement”) to transfer and assign all of the rights and obligations of Future Gas under a Coal Buy and Sell Agreement, dated as of February 4, 2010, by and between Future Gas and JBM Energy (the “Coal Buy and Sell Agreement”).

Pursuant to the Coal Buy and Sell Agreement, Future Gas agreed to purchase all coal mineral rights owned by JBM Energy in certain real property located in Judith Basin County, Montana, as described in the quit claim deed attached to the Coal Buy and Sell Agreement, for a purchase price of $1,950,000, with JBM Energy retaining a royalty interest of Twenty–Five Cents ($0.25) per ton on all coal when and as mined from the coal property. The purchase price of $1,950,000 was to be paid by Future Gas to JBM Energy on the following terms and schedules: Fifty Thousand U.S. Dollars ($50,000) upon execution of the Coal Buy and Sell Agreement and One Hundred Fifty Thousand U.S. Dollars ($150,000) on the closing date of the Coal Buy and Sell Agreement. The remaining balance of One Million Seven Hundred Fifty Thousand U.S. Dollars ($1,750,000) was to be paid by Future Gas executing and delivering to JBM on the closing date of the Coal Buy and Sell Agreement, a negotiable promissory note payable to JBM, bearing interest at the rate of five percent (5%) per annum. Payments under the Coal Buy and Sell Agreement and the promissory note were to be secured by a mortgage on the coal property and the other mineral property being conveyed by JBM Energy to Future Gas at closing. Pursuant to the Assignment and Assumption of Coal Agreement, on April 9, 2010, we executed a promissory note in favor of JBM Energy on the same terms described above (the “JBM Note”).

On March 26, 2012, we entered into an Amended and Restated Coal Buy Sell Agreement (the “Coal Amendment”), by and between the Company and JBM Energy, amending and restating the terms of the Coal Buy and Sell Agreement. The Coal Amendment extended the date upon which we must complete a reserve study and mine feasibility study from April 9, 2012 to April 9, 2013. In connection with the Coal Amendment, we also entered into an amended and restated JBM Note as of March 26, 2012, with a current principal balance of $1,350,000, an interest rate of 5% per annum. This note was replaced by a second amended and restated promissory note in favor of JBM Energy on December 11, 2012 (the “Amended JBM Note”). The current principal balance under the Amended JBM Note is $ 1,350,000, and we are required to make the following additional payments:

(a) $100,000 upon the earlier of (i) sixty (60) days following the effective date of the registration statement on Form S-1 which we are filing under that certain Amended and Restated Standby Equity Distribution Agreement, dated as of June 30, 2012, by and between the Company and YA Global Master SPV Ltd. (the “Amended SEDA”) and (ii) March 9, 2013.

(b) Commencing on April 9, 2013, the remaining principal balance of $1,250,000 shall be paid in twelve monthly installments of $100,000 each, plus accrued interest on the unpaid principal balance, with the final principal payment of $50,000 due on April 9, 2014.

(c) Interest payments are due on each of March 9, 2013 and April 9, 2013.

We have the right to prepay all or any part of the principal balance at any time without penalty. Upon repayment of the Amended JBM Note, a quit claim deed will be delivered to us conveying the coal mineral rights which are the subject of the Coal Amendment.

15

Ownership of Mineral Rights

On March 31, 2010, the Company, Mr. Russell Pace, Jr. (“Pace”) and Future Gas entered into an Assignment and Assumption of Mineral Agreement (the “Assignment and Assumption of Mineral Agreement”) to transfer and assign all of Future Gas’ rights and obligations under the Mineral Buy and Sell Agreement, dated February 4, 2010, by and between Pace and Future Gas (the “Mineral Buy and Sell Agreement”).

Pursuant to the Mineral Buy and Sell Agreement, Pace sold to Future Gas all of the oil, gas, iron ore and all other minerals of whatever nature, except coal, located in Judith Basin County, Montana, as described in the quit claim deed attached to the Mineral Buy and Sell Agreement, for a purchase price of $1,950,000, with Pace retaining a royalty interest equal to twenty percent (20%) of all royalties or other payments received by Future Gas as a result of any lease of the mineral property being conveyed to Future Gas in the Mineral Buy and Sell Agreement, or any portion thereof, and twenty percent (20%) of all net cash proceeds and/or other considerations received by Future Gas from the sale or other disposition of the mineral property being conveyed to Future Gas in the Mineral Buy and Sell Agreement or any portion thereof. The purchase price of $1,950,000 was to be paid by Future Gas executing and delivering to Pace on the closing date of the Mineral Buy and Sell Agreement a negotiable promissory note payable to Pace, bearing interest at the rate of five percent (5%) per annum. Payments under the Mineral Buy and Sell Agreement and the promissory note were to be secured by a mortgage on the coal property and the other mineral property being conveyed by Pace. Pursuant to the Assignment and Assumption of Mineral Agreement, on April 9, 2010, we executed a promissory note in favor of Pace on the same terms described above (the “Pace Note”).