Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - SHAW GROUP INC | ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - SHAW GROUP INC | ex31-1.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K/A

Amendment No. 1

|

R

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the fiscal year ended August 31, 2012

|

|

|

or

|

|

|

£

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the transition period from to

|

|

Commission file number: 1-12227

THE SHAW GROUP INC.

(Exact name of registrant as specified in its charter)

|

LOUISIANA

|

72-1106167

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

4171 Essen Lane

Baton Rouge, Louisiana 70809

(Address of principal executive offices, including zip code)

(225) 932-2500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

Common Stock — no par value

|

New York Stock Exchange

|

Securities registered pursuant to Section 12(g) of the Act:

None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes R No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No R

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. R

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer R

|

Accelerated filer o

|

||

|

Non-accelerated filer o (Do not check if a smaller reporting company)

|

Smaller reporting company o

|

||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No R

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant was approximately $1.2 billion (computed by reference to the closing sale price of the registrant’s common stock on the New York Stock Exchange (NYSE) on February 29, 2012. Common stock held as of such date by each officer and director and by each person who owns 5% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of the registrant’s common stock outstanding at December 19, 2012 was 66,663,781.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Explanatory Note

As previously announced, on July 30, 2012, we entered into a Transaction Agreement (the “Transaction Agreement”) with Chicago Bridge & Iron Company N.V., a limited liability company (naamloze vennootschap) with a corporate seat in Amsterdam, the Netherlands (“CB&I”), and Crystal Acquisition Subsidiary Inc, a Louisiana corporation and wholly-owned subsidiary of CB&I (“Merger Sub”). The Transaction Agreement provides that, upon the terms and subject to the conditions set forth in the Transaction Agreement, Merger Sub will merge with and into the Company (the “Transaction”), with the Company surviving the Merger as a wholly-owned subsidiary of CB&I. We currently expect to complete the Transaction during the first quarter of calendar 2013. The CB&I shareholders approved the Transaction on December 18, 2012 and our shareholders approved the Transaction on December 21, 2012. The Transaction is also subject to a pending regulatory approval and certain other closing conditions. In light of the proposed transaction, we do not anticipate holding an annual meeting of shareholders in 2013.

This Amendment No. 1 on Form 10-K/A (the Amendment) amends our Annual Report on Form 10-K for the fiscal year ended August 31, 2012, originally filed with the Securities and Exchange Commission (SEC) on October 19, 2012 (the Form 10-K). We are filing this Amendment to amend Part III of the Form 10-K to include the information required by and not included in Part III of the Form 10-K because we no longer intend to file our definitive proxy statement within 120 days of the end of our fiscal year ended August 31, 2012. Because no financial statements are contained within this Amendment, we are not including certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002.

Except as described above, this Amendment does not reflect events occurring after the date of the Form 10-K, nor does it modify or update the disclosure contained in the Form 10-K in any way other than as required to reflect the amendments discussed above and reflected below. Accordingly, this Amendment should be read in conjunction with our Form 10-K and our other filings made with the SEC on or subsequent to the filing of our Form 10-K on October 19, 2012.

TABLE OF CONTENTS

| PART III | ||||

| ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 1 | ||

| ITEM 11. | EXECUTIVE COMPENSATION | 5 | ||

| ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 50 | ||

| ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 53 | ||

| ITEM 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES | 54 | ||

| PART IV | ||||

| ITEM 15. | EXHIBITS, FINANCIAL STATEMENT SCHEDULES | 56 | ||

| SIGNATURE | 60 | |||

| EXHIBIT INDEX | ||||

PART III

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

INFORMATION ABOUT DIRECTORS

The following provides information about our current directors. Below each director’s biography, we have included an assessment of the qualifications and experience of such director.

|

J.M. BERNHARD, JR.

Age: 58

Director Since: 1987

|

Board Committees:

• Executive

|

Company Positions:

• Chairman of the Board, Chief Executive Officer and President

|

Mr. Bernhard, our founder, has been our Chief Executive Officer and a director since the Company began in 1987. Mr. Bernhard served as our President from 1987 until 2003. Our Board re-elected him as President in November 2006, and he has continually served in that position ever since. He has been Chairman of our Board since August 1990. Prior to founding the Company, Mr. Bernhard was vice president and general manager of Sunland Services, a pipe fabrication and industrial construction company that the Company later acquired. He is also a member of numerous trade and civic organizations. He graduated from Louisiana State University in 1976 with a degree in Construction Management.

Under Mr. Bernhard’s leadership, the Company has grown dramatically through a series of strategic acquisitions. The Company has been named to the Fortune 500 list seven times and is one of the youngest companies to appear on such list. In addition, the Company has been recognized twice as one of the Fortune 500 Magazine’s “Most Admired Companies.” The Company also has been named “Contractor of the Year” by Associated Builders and Contractors.

Mr. Bernhard is our longest-serving Board member. For over 20 years, he has contributed to the Company his operational, financial and strategic experience garnered from his career and involvement in the fabrication, engineering, and construction industry. In addition to these qualifications, attributes and skills, Mr. Bernhard offers the perspective, institutional knowledge and deep understanding of our business. As the only member of our management team to serve on our Board, Mr. Bernhard contributes a level of understanding of the Company not easily attainable by an outside director.

In fiscal year 2012, Mr. Bernhard assumed operational leadership after the retirement of our former Chief Operating Officer and he negotiated the pending acquisition of the Company by CB&I for cash and stock, in which shareholders will receive a 72% premium over the closing price for last trading day prior to announcement upon consummation of the transaction (for further discussion please see our current report on the Form 8-K filed with the SEC on July 30, 2012).

|

JAMES F. BARKER

Age: 65

Director Since: January 2004

|

Board Committees:

• Audit

• Compensation

|

Private Directorships:

• President, Clemson University

|

Mr. Barker has served as president of Clemson University since December 1999. He earned his bachelor of architecture degree from Clemson in 1970 and his master of architecture and urban design degree from Washington University in St. Louis in 1973. Before returning to Clemson in 1986 to serve as dean of the College of Architecture, he was dean of the School of Architecture at Mississippi State University. Mr. Barker is a fellow of the American Institute of Architects.

As president of a large public university with an annual budget in excess of $800 million, Mr. Barker understands the management concerns created by varied interests and business units within an organization operating in a public domain. His ability to make policy and financial decisions for the entire organization under stakeholder stresses positively contributes to our Board’s deliberations. His experience administering and managing the finances of a university and of several non-profit organizations make him a valued member of our Board.

|

THOS. E. CAPPS

Age: 77

Director Since: July 2007

|

Board Committees:

• Audit

|

Public Directorships:

• Amerigroup Corp.

Private Directorships:

•Associated Electric & Gas Insurance Services Ltd.

|

Mr. Capps served as chief executive officer of Dominion Resources, Inc. (NYSE: D) from January 2000 to December 2005; as president from September 1995 to December 2003; as chairman from September 1995 to January 2000; as vice chairman of the board of directors from January 2000 to August 2000; and as president and chief executive officer from September 1995 to January 2000. Dominion Resources is a publicly-held power and energy company that supplies electricity, natural gas and other energy sources and operates generation facilities. Mr. Capps is a member of the board of directors of Amerigroup Corp. (NYSE: AGR) of Virginia Beach, a publicly-held, managed-healthcare company, and Associated Electric & Gas Insurance Services Ltd., which operates as a non-assessable mutual insurance company in the U.S., offering insurance and risk management products and services to the utility and related energy industry.

Mr. Capps brings his nearly twenty year’s experience with Dominion Resources, Inc., to our Board. This knowledge of power sources, power generation and supply contributes to our Board’s understanding of both our clients’ and the Company’s needs and capacities. His enduring leadership as chairman, president and chief executive officer of Dominion Resources evidences his ability to manage a breadth of public company matters. His experience supervising financial and accounting personnel and broad understanding of accounting principles, internal controls over financial reporting and audit committee functions are important contributions to our Audit Committee.

1

|

DANIEL A. HOFFLER

Age: 64

Director Since: January 2006

|

Board Committees:

• Compensation (Chair)

• Nominating and Corporate Governance

|

Private Directorships:

• Armada Hoffler

|

Mr. Hoffler is the chairman of the board of directors of Armada Hoffler, a premier commercial real estate development and construction organization located in Virginia, which he founded over 25 years ago. Before founding Armada Hoffler, Mr. Hoffler was employed as vice president of marketing for Eastern International, Inc., a commercial real estate development and construction company specializing in construction of warehouse and office buildings. Prior to that, Mr. Hoffler was employed as a regional manager for Dun and Bradstreet, a credit information provider. From 1992 through 1996, Mr. Hoffler served on the University of Virginia Board of Visitors. In 1987, he was chosen as the Outstanding Citizen of Hampton Roads, Virginia. In 1986, Mr. Hoffler was appointed to a five-year term in the Virginia Governor’s Advisory Board for Industrial Development for the Commonwealth of Virginia.

Mr. Hoffler’s vast experience in real estate development and construction and his understanding of debt and equity markets complements the experience and knowledge base of our other directors. His unique skill set relating to design-build collaborations and public/private partnerships combined with his understanding of financial markets assist our Board in evaluating creative and value-creating Company initiatives. As founder of his company, he understands issues relating to the growth of a business and the concerns involved in running a profitable company. His business leadership and experience in growing a company make him uniquely qualified to serve as the Chair of our Compensation Committee.

|

DAVID W. HOYLE

Age: 73

Director Since: January 1995

|

Board Committees:

• Audit

• Nominating and Corporate Governance (Chair)

• Executive

|

Public Directorships:

• Citizens South Banking Corporation

Government Positions:

• Secretary of Revenue, North Carolina

|

For the past 25 years, Secretary Hoyle has been self-employed, primarily as a real estate developer. From 1992 until 2010, he served as a Senator in the North Carolina General Assembly. He served as chairman of the North Carolina Senate Finance Committee for 12 years. In October 2010, he was sworn in as Secretary of Revenue for the State of North Carolina. Secretary Hoyle was the chairman of the board of directors of Citizens South Banking Corporation, a bank holding company, and the chairman emeritus of the board of directors of its wholly-owned subsidiary, Citizens South Bank, until May 2012, when the bank was sold to Park Sterling Bank. His government leadership and integrity serve the Company well in his capacity as Chair of the Nominating and Corporate Governance Committee.

Secretary Hoyle contributes his knowledge of banking, tax and real estate development issues and experience with financial management to our Board’s deliberations. His long tenure in the North Carolina Senate evidences his understanding of governance, leadership skills, and knowledge of working with government bodies. With 15 years’ service on our Board, his institutional knowledge and historical perspective are vital assets to our Board and our shareholders.

|

MICHAEL J. MANCUSO

Age: 70

Director Since: August 2006

|

Board Committees:

• Audit (Chair)

• Executive

|

Public Directorships:

• SPX Corporation

Former Public Directorships Held During the Past Five Years:

• LSI Logic Corporation

• CACI International Inc.

|

Mr. Mancuso was named vice president and chief financial officer of Computer Services Corporation (NYSE: CSC), a publicly-held leading provider of information technology and professional services to large corporations and governments, on December 1, 2008. He retired from that position in May 2012. In June 2006, after 13 years’ service, Mr. Mancuso retired from General Dynamics Corporation (NYSE: GD), a company engaged in the field of mission-critical information systems and technologies, land and expeditionary combat systems, armaments and munitions, shipbuilding and marine systems and business aviation. Mr. Mancuso had served as senior vice president and chief financial officer of General Dynamics from 1994 until his retirement from General Dynamics in 2006. Before joining General Dynamics, Mr. Mancuso spent seven years with United Technologies, where he served as vice president and chief financial officer for the Commercial Engine Business of the Pratt & Whitney Group. He joined United Technologies Defense and Space Systems Group in 1986 as group financial manager, moved to the aerospace and defense section in 1989 as director, financial planning and analysis, and spent three years as vice president, finance and administration for the Hamilton standard division. His background also includes 21 years with General Electric. Mr. Mancuso also serves on the board of directors for SPX Corporation (NYSE: SPW), a publicly-held industrial manufacturer headquartered in Charlotte, North Carolina. From 2007 until 2009, Mr. Mancuso also served on the board of directors for LSI Logic Corporation (NYSE: LSI), a publicly-held leading provider of silicon systems and software technologies, headquartered in Milpitas, California. From 2007 until 2008, Mr. Mancuso also served on the board of directors for CACI International Inc. (NYSE: CACI), a publicly-held provider of information technology and professional services to the U.S. federal government and commercial markets in North America and internationally, headquartered in Arlington, Virginia.

Mr. Mancuso brings a strong background in operations, finance and financial reporting with large publicly traded companies to our Board. As former chief financial officer of a leading information technology company and former chief financial officer of a major technology and defense company, he has the financial background and operational experience to understand and to provide guidance in evaluating complex business and financial issues facing large public companies. His strategic and financial perspective, and long involvement with government and international operations, brings a valuable perspective to our Board and to his leadership as chair of our Audit Committee.

2

|

ALBERT D. McALISTER

Age: 61

Director Since: April 1990

|

Board Committees:

• Compensation

• Nominating and Corporate Governance

• Executive

|

Private Directorships:

• McAlister & McAlister

• President’s Advisory Board, Clemson University

|

Since 1975, Mr. McAlister has been a partner in the law firm of McAlister &McAlister in Laurens, South Carolina. Mr. McAlister is a director of a private charitable foundation and a member of the Clemson University – President’s Advisory Board.

Mr. McAlister contributes to our Board the skills and experience gained from his years of legal service to various businesses and corporations and as a litigator. As a founder of his firm, he has sophisticated legal experience and a reputation for resolving complex legal matters. Having served the Company as a director from nearly its inception, he is a repository of institutional knowledge and historical perspective and has been a key advisor to our management as we have grown from a start-up to a Fortune 500 company.

|

STEPHEN R. TRITCH

Age: 63

Director Since: April 2009

|

Board Committees:

• Nominating and Corporate Governance

|

Public Directorships:

• Koppers Holdings, Inc.

Private Directorships:

• PaR Systems

• Board of Trustees, University of Pittsburgh (Chair)

• Board of Trustees, Senator John Heinz History

Center, Pittsburgh, PA

• UPMC Health System

|

Mr. Tritch is the retired chairman of Westinghouse Electric Company (Westinghouse) and served in that capacity from July 1, 2008, to July 1, 2010. Westinghouse is a pioneering nuclear power company and a leading supplier of nuclear plant products and technologies to utilities throughout the world. From July 2002 to July 2008, Mr. Tritch served as president and chief executive officer of Westinghouse. Mr. Tritch had been employed by Westinghouse since 1971. Mr. Tritch was appointed in 2007 by then-President George W. Bush to the President’s Export Council. Mr. Tritch is also chairman of the board of trustees at the University of Pittsburgh; first vice chairman of the UPMC Health System; a member of the board of trustees for the Senator John Heinz History Center in Pittsburgh for which he previously served as chairman until July 2010; and a member of the board of directors of Koppers Holdings, Inc. (NYSE: KOP), a publicly-held company and a leading producer of carbon compounds and treated wood products, headquartered in Pittsburgh, Pennsylvania. He is also a member of the board of PaR Systems, a privately-held robotic systems supplier, headquartered in Minneapolis, Minnesota.

Mr. Tritch’s experience with Westinghouse makes him a valued member of our Board as the Company continues to grow in the nuclear power plant field. He brings a wealth of knowledge about the nuclear power industry and understanding of the unique issues involved in this complex and historically significant industry sector. Mr. Tritch’s broad experience with nuclear power technology companies and his insight into global electric power production complement the spectrum of experience on our Board.

INFORMATION ABOUT EXECUTIVE OFFICERS

The following provides information about our current executive officers. Each executive officer has been elected to serve until his successor is duly appointed or elected by our Board or his earlier removal or resignation from office.

|

J.M. BERNHARD, JR.

Age: 58

Shaw Employee Since: 1987

|

Company Positions:

• Chairman of the Board of Directors

• President and Chief Executive Officer

|

|

For biographical information on Mr. Bernhard, see “Information about Directors.”

|

GEORGE P. BEVAN

|

Company Position:

|

|

|

Age: 65

|

• President, Environmental & Infrastructure (E&I) Group

|

|

|

Shaw Employee Since: September 1994

|

||

Mr. Bevan joined us in September 1994 as Vice President of Business Development. He held that position until February 1996, when he was appointed Executive Vice President of Corporate Development. Mr. Bevan served as Executive Vice President of Corporate Development until September 2003, when he was appointed as our Vice President of Government Affairs and President of one of our subsidiaries. He served in those positions until April 2005 and then again from May 2006 through March 2007. From April 2005 through May 2006, Mr. Bevan worked for us as a consultant on Hurricane Katrina and Rita related matters while he was employed by the Sterling Group, a re-processor of PVC. In March 2007, Mr. Bevan was appointed President of the Infrastructure Division and then Commercial and State & Local Government (CSL) Division of our Environmental & Infrastructure Group. He served as CSL Division President until his June 2008 appointment as President of our Environmental & Infrastructure Group. More recently, Mr. Bevan has assumed additional responsibilities as lead for Shaw / CB&I transition team.

3

|

DAVID L. CHAPMAN, SR.

|

Company Position:

|

|

|

Age: 66

|

• President, Fabrication & Manufacturing (F&M) Group

|

|

|

Shaw Employee Since: April 2002

|

||

Mr. Chapman joined us in April 2002 as President of our Fabrication & Manufacturing Division, which is now known as the Fabrication & Manufacturing Group. Mr. Chapman has over 40 years of experience in the industrial fabrication business. From 1993 to 2002, Mr. Chapman was employed by Turner Industries Group, a large industrial contracting company, where he served as president of International Piping Systems, Turner International Piping Systems and International Painting Corporation.

|

JOHN DONOFRIO

|

Company Position:

|

|

|

Age: 51

|

• Executive Vice President, General Counsel and Corporate Secretary

|

|

|

Shaw Employee Since: October 2009

|

||

Mr. Donofrio joined us in October 2009. From 2005 to October 2009, Mr. Donofrio served as senior vice president, general counsel and chief compliance officer of Visteon Corporation, a leading global supplier of innovative products to automotive manufacturers. Previously, from 2000 to 2005, Mr. Donofrio was vice president and general counsel of Honeywell Aerospace, a global manufacturer of aerospace components and systems. Before joining Honeywell, he was a partner with the law firm of Kirkland & Ellis in Washington, D.C. and New York. Mr. Donofrio currently serves on the board of directors of FARO Technologies, Inc. (NASDAQ: FARO), a publicly-held leader in portable computer-aided measurement hardware and software headquartered in Lake Mary, Florida. Mr. Donofrio is also an adjunct professor of law at Louisiana State University, where he teaches Corporate Governance.

|

BRIAN K. FERRAIOLI

|

Company Position:

|

|

|

Age: 57

|

• Executive Vice President and Chief Financial Officer

|

|

|

Shaw Employee Since: July 2007

|

||

Mr. Ferraioli joined us in July 2007 as our Executive Vice President, Finance, and served in that position until October 2007, when he was appointed to his current position. Immediately prior to joining us and since November 2002, Mr. Ferraioli served as vice president and controller of Foster Wheeler AG. Prior to that, and until November 2002, Mr. Ferraioli served in various corporate and operating unit executive financial positions with Foster Wheeler AG and with its subsidiaries in the U.S. and Europe. Foster Wheeler is a diversified engineering and construction company and power equipment supplier. Mr. Ferraioli is also a member of the Dean’s Advisory Council at Louisiana State University’s E.J. Ourso College of Business, and he serves on the Energy Advisory Council to the Federal Reserve Bank of Atlanta.

|

ELI SMITH

|

Company Position:

|

|

|

Age: 60

|

• President, Power Group

|

|

|

Shaw Employee Since: May 2009

|

||

Mr. Smith joined us in May 2009, as Senior Vice President of procurement and contracts, and held this position until September 2010, when he was appointed President and Chief Operating Officer of the Power Group where he oversaw operations and project execution. On July 16, 2012, he was promoted to President of the Power Group, with the same operational and project execution responsibilities, plus additional general administrative and overhead functions. Before joining Shaw, Mr. Smith was the Principal vice president and corporate manager of contracts and procurement for Bechtel Corporation. From 1974 to 1996, he served in various senior management positions in the U.S. Army Corps of Engineers.

|

JAMES C. WILEMS

|

Company Position:

|

|

|

Age: 45

|

• Interim Vice President and Chief Accounting Officer

|

|

|

Shaw Employee Since: July 2011

|

||

Mr. Wilems joined the Company in 2011 as senior director, corporate accounting and served in that position until November 2012, when he was appointed to his current position. He is responsible for the financial accounting, accounting policy and external financial reporting for the Company.

Prior to joining the Company, he served as senior manager – international financial reporting standards/post-merger integration lead at Accenture PLC, a global management consulting, technology services and outsourcing firm in Atlanta, Georgia from 2010 to 2011. From 2003 to 2010, Mr. Wilems worked for BDO Seidman, LLP, a global public accounting firm in Atlanta, Georgia, where he served as assurance partner and audit and accounting director from 2005 to 2010. Mr. Wilems was also director of external reporting from 2001 to 2003 for ENSCO International, Inc., a multi-national, publicly held, oil and gas contract driller and as an assurance manager at Arthur Andersen, LLP from 1992 to 2000. Mr. Wilems graduated from the Center for Internal Auditing at Louisiana State University and is a member of the American Institute of Certified Public Accountants.

4

CODES OF CONDUCT

Our Board has formally adopted a Code of Corporate Conduct and an Insider Trading Policy, both of which apply to all of our employees, officers and directors. Our Board formally adopted a separate Code of Ethics for our Chief Executive Officer and Senior Financial Officers, which applies to our Chief Executive Officer, Chief Financial Officer, Chief Accounting Officer and all other senior financial and accounting executives. We intend to satisfy the disclosure requirement regarding any amendment to, or waiver of, a provision of the Code of Ethics for the Company’s Chief Executive Officer, Chief Financial Officer, Chief Accounting Officer and Controller, or persons performing similar functions, by posting such information on the Company’s website. There were no amendments to, or waivers of, any provision of the Code of Corporate Conduct or the Code of Ethics for the Company’s Chief Executive Officer, Chief Financial Officer, Chief Accounting Officer and Controller, or any persons performing similar functions during fiscal year 2012. Copies of these codes are available on our website at www.shawgrp.com on the “About Shaw” page under the “Corporate Governance” link.

SECTION 16(a) BENEFICIAL OWNERSHIP REPORTING COMPLIANCE

Section 16(a) of the Exchange Act requires our directors, executive officers and certain beneficial owners of more than 10% of our common stock to file with the SEC reports of ownership (Form 3) and changes in ownership (Forms 4 and 5) of our common stock. The reporting persons are required to furnish us with copies of all reports filed pursuant to Section 16(a).

Based solely upon review of the SEC reports and written representations to us from certain reporting persons, we believe that during fiscal year 2012, all applicable filing obligations under Section 16(a) have been met by all of the reporting persons.

AUDIT COMMITTEE

Our Board has certain standing committees, including our Audit Committee. Our Board, in its business judgment, has determined that our Audit Committee is comprised entirely of directors who satisfy the standards of independence established under the rules and regulations of the SEC, the NYSE listing standards and our Corporate Governance Principles. Messrs. Barker, Capps, Hoyle and Mancuso (chairman) are the members of our Audit Committee. Our Board has determined that each member of our Audit Committee has the requisite accounting and related financial management expertise under the NYSE listing standards. Additionally, our Board determined that Mr. Mancuso is qualified as an “audit committee financial expert” under the rules and regulations of the SEC.

ITEM 11. EXECUTIVE COMPENSATION

COMPENSATION DISCUSSION AND ANALYSIS

INTRODUCTION

This Compensation Discussion and Analysis (CD&A) explains how our Compensation Committee established goals, reviewed performance and decided compensation for our Named Executive Officers (NEOs) in fiscal year 2012. The NEOs for fiscal year 2012 were:

|

|

·

|

J.M. Bernhard, Jr., Chairman of the Board of Directors, President and Chief Executive Officer;

|

|

|

·

|

Brian K. Ferraioli, Executive Vice President and Chief Financial Officer;

|

|

|

·

|

David L. Chapman, Sr., President, Fabrication & Manufacturing Group;

|

|

|

·

|

George P. Bevan, President, Environmental & Infrastructure Group; and

|

|

|

·

|

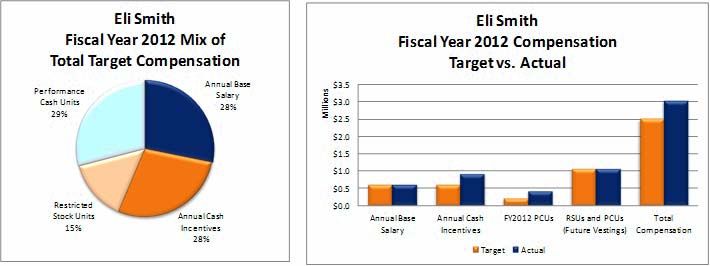

Eli Smith, President, Power Group.

|

5

EXECUTIVE SUMMARY

We maintain several executive pay program design features and corporate governance practices to ensure a strong link between executive pay, Company performance and shareholder value based on the following, which are discussed in more detail in this CD&A:

Summary Highlights

|

•

|

Strong financial performance and creation of shareholder value exemplified by stock price increasing 81%, from $23.31 to $42.08 over fiscal year 2012.

|

|

•

|

Between 57% and 65% of our NEO’s total target compensation is performance based.

|

|

•

|

Annual cash incentives reflect pay-for-results philosophy, as evidenced by our Chief Executive Officer payout levels over the past three fiscal years at approximately 18% of target for fiscal year 2010, 0% of target for fiscal year 2011 and 200% of target for fiscal year 2012.

|

|

•

|

To further strengthen our pay for results philosophy, we implemented new performance-based long-term incentive awards based on how well our stock performs compared to our peers, more specifically, relative total shareholder return (TSR), which for fiscal year 2012 earned maximum performance levels of 200%.

|

|

•

|

Elimination of tax gross-up provisions from Chief Executive Officer and one other NEO’s employment agreements during the past two years.

|

|

•

|

Elimination of all guaranteed annual cash incentive payments for NEOs.

|

|

•

|

Compensation best practices include: a three year minimum vesting requirement, minimum stock ownership guidelines, limited Company-paid personal use of corporate aircraft (limited circumstances discussed below), compliance with a maximum share issuance burn rate commitment and a management incentive clawback policy

|

Pay For Results Philosophy

Between 57% and 65% of the NEOs’ annual target total compensation for fiscal year 2012 was performance-based, with the amount to be realized based on annual financial results (annual cash incentives) or multi-year stock price performance (long-term incentives).

|

|

·

|

Target Compensation. Target compensation levels are set higher than average, commensurate with the Company’s setting of aggressive Management Incentive Program (MIP) target goals and relative TSR goals in order to incentivize executives in ways that are in alignment with shareholders, and which also attracts and retains high-caliber, industry-leading executives.

|

|

|

·

|

Actual Compensation. Actual compensation levels are commensurate with actual Company and individual performance. In years where the Company’s performance failed to achieve targets, actual incentive compensation was reduced or eliminated. In fiscal year 2012, the Company’s performance exceeded targets, so actual compensation increased. The Company’s strong fiscal year 2012 earnings before interest expense, income taxes, depreciation and amortization (EBITDA) performance (increased 1,773% from fiscal year 2011, excluding the results from our investment in the Westinghouse segment) and the strong stock price appreciation (up 81% from August 31, 2011), resulted in increased levels of actual compensation for all of our NEOs (annual cash and long-term incentive compensation), reflecting our pay-for-results philosophy, at levels ranging from 100-200% of respective targets. For additional disclosure related to our fiscal year 2012 EBITDA, including a reconciliation of our Generally Accepted Accounting Principles (GAAP) results to our non-GAAP results, please see “EXECUTIVE COMPENSATION – Non-GAAP Financial Measure” below.

|

2012 Pay Outcomes Were Commensurate with 2012 Performance

Fiscal year 2012 annual cash incentive compensation and long-term performance cash incentive compensation were commensurate with the Company’s fiscal year 2012 financial, operational and stock performance, reflecting the Company’s “pay-for-results” philosophy as described below:

The Company’s exceptional performance for fiscal year 2012 was realized in part due to the leadership and vision of our NEOs and their fiscal year 2012 compensation levels are commensurate with Company performance.

6

|

|

·

|

Above Target Annual Cash Incentive Compensation Earned.

|

The Company’s fiscal year 2012 performance exceeded financial and operational target goals and significantly improved from fiscal year 2011, which resulted in earned annual cash incentive awards for our NEOs, at various levels based on business unit and individual performance, ranging from 100% to 200% of target.

For fiscal year 2012, the Company’s consolidated financial results, excluding the results from our investment in the Westinghouse segment, were $314.6 million for EBITDA and $148.8 million for operating cash flow. These exceeded our target goals with achievement levels of 105% and 127%, respectively. The EBITDA results represented a significant improvement (1,773%) from prior year’s EBITDA loss of $18.8 million.

Also in fiscal year 2012, the Company accomplished several key strategic initiatives and operational achievements, as summarized below, which culminated in the agreement to be acquired by CB&I at a premium of 72% over the closing price for the last trading day prior to announcement (for further discussion please see our current report on Form 8-K filed with the SEC on July 30, 2012):

|

|

–

|

Successfully completed the divestiture of substantially all of the business within the Energy & Chemicals (E&C) business unit which resulted in cash proceeds of $290 million;

|

|

|

–

|

exercised the put options of our subsidiary NEH to sell its investment in the Westinghouse Group to Toshiba;

|

|

|

–

|

increased amounts of construction activities related to our Power business unit’s EPC contracts on four nuclear power reactors in the United States after our clients obtained the combined operating licenses (COLs) from the NRC;

|

|

|

–

|

generated record earnings for third straight year within our Plant Service’s business unit, which continues to perform at what we believe is an industry leading level;

|

|

|

–

|

expanded and improved profitability for our pipe fabrication facilities within our F&M business unit;

|

|

|

–

|

executed a share buyback program via a $150 million Dutch auction tender offer; and

|

|

|

–

|

developed a company-wide process improvement initiative.

|

|

|

·

|

Long-Term Incentive Compensation Tied to Stock Performance.

|

As of August 31, 2012, our stock had appreciated 81% from the August 31, 2011 closing price and our fiscal year 2012 relative TSR was 72.63%, which exceeded our maximum performance goal of 25% relative TSR; therefore, our NEOs earned 200% of target PCUs.

To further our pay-for-results philosophy, our executive officers participated in a new long-term incentive award program under our 2008 Omnibus Incentive Plan, as amended (the “Omnibus Plan”) in fiscal year 2012. This was awarded in the form of performance cash units (PCUs), the payout of which is based on the performance measure of TSR. The PCUs were awarded in addition to restricted stock units (RSUs) that vest over the next three years, providing ongoing alignment with shareholders based on the Company’s future stock price performance. TSR performance for fiscal year 2012 increased by 85.49%. Thus, our executives, like our shareholders, have been rewarded by our stock’s exceptional performance as follows:

|

|

–

|

Actual relative TSR performance of 72.63% as compared to median TSR of PCU Peer Group far exceeded the maximum goal of 25%; therefore, maximum payout of 200% was earned for the first 25% of target PCUs awarded to our executives in fiscal year 2012.

|

Compensation Best Practices

Over the past two years, the Compensation Committee, in conjunction with executive management, has performed a detailed annual assessment of the key elements of our executive compensation program. As a result of these assessments, the Company has continued to strengthen our executive compensation practices to ensure a strong link between executive pay, Company performance, and shareholder value. The Committee and the Board have adopted Executive Compensation Guidelines (the Guidelines) memorializing several of these practices, some of which are highlighted below. See “Incentive Compensation and Other Programs” for additional details regarding implementation of PCUs, the payout of which is based on the performance measure of TSR, and “Benefits and Other Compensation – Employment Agreements” for additional details regarding amendment to Chief Executive Officer’s employment agreement.

7

We have proactively changed or eliminated pay practices that were viewed negatively by shareholders and institutional advisory firms such as ISS and Glass Lewis.

|

Compensation Best Practice

|

Fiscal Year Implemented

|

|

Three-Year Minimum Vesting Requirements for LTI awards

|

2010

|

|

Minimum Stock Ownership Guidelines as a Multiple of Base Salary (6x Chief Executive Officer, 2.5x and 1.5x for Other Executive Officers)

|

2010

|

|

No Future Guaranteed Management Incentive Program (MIP) Payments for Executive Officers

|

2010

|

|

Limited Company-Paid Personal Use of Corporate Aircraft (exceptions for employee relocation and Chief Executive Officer safety only)

|

2010

|

|

No New Excise Tax Gross-Up Provisions

|

2010

|

|

Maximum Share Issuance Burn Rate Commitment (1.95% per year for fiscal years 2011-2013)

|

2011

|

|

Addition of Management Incentive Clawback Policy

|

2011

|

|

Amendment of Mr. Chapman’s Employment Agreement (Removed Excise Tax Gross-Up and Guaranteed MIP)

|

2011

|

|

Amendment of Chief Executive Officer’s Employment Agreement (Eliminated Tax Gross-Up and Clarified Terms of the Deferred Compensation/SERP Award)

|

2012

|

|

Implementation of PCUs, the Payout of Which Is Based on the Performance Measure of TSR and Elimination of Stock Options

|

2012

|

In the latter part of fiscal year 2011 and first quarter of fiscal year 2012, a detailed assessment of the contractual obligations contained in our executive employment agreements was performed by the Compensation Committee, in conjunction with executive management and our compensation consultant, Pay Governance, LLC. As a result of these assessments, the Company implemented the following changes to our Chief Executive Officer’s employment agreement on December 12, 2011.

|

|

·

|

Eliminated Tax Gross-Up in Chief Executive Officer’s Employment Agreement. The Company removed a tax gross-up provision which would have been applicable if any payment or benefit in connection with a change in control would have constituted an “excess parachute payment” under 280G of the Internal Revenue Code, and replaced it with a “net best” provision.

|

|

|

·

|

Clarification of Chief Executive Officer’s Deferred Compensation Award. The Company converted a $15 million, plus accumulated interest, deferred compensation award that was owed to Mr. Bernhard to a Supplemental Executive Retirement Plan (SERP) to make it clear that this award is a retirement benefit. There were no changes in the economics or timing of payments as part of this conversion; however, the conversion to a SERP is fully compliant with Section 409A of the Internal Revenue Code and eliminates prior misconceptions associated with the language in his employment agreement regarding the deferred compensation award and non-compete provision. Mr. Bernhard’s SERP is near the market median for company-provided retirement benefits for long-service chief executive officers, including founders, of similarly-sized companies.

|

COMPENSATION PHILOSOPHY, OBJECTIVES, PLANS AND PROGRAMS

The Company’s executive compensation philosophy is designed to:

|

|

·

|

Maximize shareholder value by recruiting, incentivizing and retaining top executive leadership with the skills to enable the Company to achieve our long- and short-term business goals, thus aligning the interests of our executives with those of our shareholders; and

|

|

|

·

|

Provide a balanced mix of base salary, annual cash incentives and long-term equity incentives, emphasizing performance-based compensation that generally targets to provide actual compensation that is consistent with our performance and is between the 50th and 75th percentile of our Market Peer Group (as defined below),.

|

8

The elements of our compensation program help us to realize our compensation philosophy and objectives:

|

|

·

|

Base Salary. Base salary provides a competitive and stable component of income to our executives, as a majority of their total compensation is variable from year to year.

|

|

|

·

|

Annual Cash Incentive Compensation under the MIP. This program provides competitively based short-term incentive opportunities for our executives to earn annual cash awards for achieving financial, operational and strategic benchmarks that are established by the Compensation Committee each fiscal year. See “Incentive Compensation and Other Programs” for additional details regarding goal setting and determination of MIP awards.

|

|

|

·

|

Long-Term Incentive Compensation. Long-term incentive compensation ensures that our executives’ interests are aligned with those of our shareholders. During fiscal year 2012, the Company further strengthened the “pay-for-results” component of our long-term incentive compensation program by implementing PCUs, the payout of which is based on TSR as the performance measure. For further discussion, see “Incentive Compensation and Other Programs” below.

|

|

|

·

|

Benefits and Other Compensation. Our benefit and other compensation programs comprise a minimal portion of our NEOs total annual compensation and all programs offered, including perquisites, are in line with standard market practices.

|

See “Compensation Discussion of Our Named Executive Officers” for additional information regarding the elements of compensation of our NEOs.

ROLE OF COMPENSATION COMMITTEE

Our Board has delegated to the Compensation Committee the primary responsibility for overseeing our executive compensation program. In performing this duty, the Compensation Committee takes the following actions in the first quarter of each fiscal year regarding the actual performance for the most recently completed fiscal year and recommendations for the newly begun fiscal year:

Approval of Total Compensation for our Named Executive Officers and Other Key Executives. The Compensation Committee reviews and discusses a schedule for each executive, which includes:

|

|

·

|

Analysis of compensation elements: base salary, target and actual annual cash incentive compensation, long-term incentive compensation and total target and actual compensation;

|

|

|

·

|

Comparative compensation analysis for each compensation element showing actual, target and market amounts for the most recently completed fiscal year and target recommendations compared to market for the newly began fiscal year;

|

|

|

·

|

Competitive market information for the prior and current fiscal year are provided at the 50th and 75th percentiles for our Market Peer Group (as defined below);

|

|

|

·

|

A summary of the annual performance of the executive, which were assessed and rated on a standard scale; and

|

|

|

·

|

A summary of any one-time compensation recommended for approval, if applicable.

|

Approval and Administration of Annual Incentive Programs and of Performance Goals. The Compensation Committee discusses, determines and approves the following annual cash and long-term incentive compensation goals and awards, after consideration of, among other things, management’s recommendation, the prior fiscal year’s goals and actual performance and the current fiscal year’s goals and alignment with Company and shareholder interests:

|

|

·

|

Annual cash incentive awards, which includes:

|

|

|

–

|

Achievement of the prior fiscal year’s financial and operational performance goals;

|

|

|

–

|

Pool of MIP funds for business units;

|

|

|

–

|

Total awards under MIP (including individual amounts for our NEOs as discussed above); and

|

|

|

–

|

Financial and operational performance goals for the new fiscal year that will serve as the benchmarks for the annual cash incentive compensation under MIP.

|

9

|

|

·

|

Long-term incentive awards, which includes:

|

|

|

–

|

Appropriate mix of long-term incentive components to ensure achievement of our compensation objectives;

|

|

|

–

|

Achievement of performance measure under PCU awards, and the resulting earned PCU awards;

|

|

|

–

|

Establishment of performance measure and peer group for the new fiscal year’s target PCU awards; and

|

|

|

–

|

Ensuring compliance with our available share pool and annual burn rate commitment.

|

Assessment of Compensation Risk. The Compensation Committee also reviews and discusses with management the compensation risk analysis conducted to determine whether the Company has any compensation programs that are reasonably likely to have a material adverse affect on the Company. During fiscal year 2012, a detailed analysis was performed by Human Resources and Internal Audit where each compensation element and program was categorized and then analyzed for potential risk on a scale of low, moderate and high for the following: (i) program design and metrics; (ii) compensation mix and time horizon; (iii) compensation process around design, award determination, and payouts; (iv) compensation program governance and oversight; and (v) mitigating controls. At the conclusion of our assessment, we determined that our compensation elements and programs have an appropriate mix of: (i) short-term compensation: annual base salary and cash incentives that have a pay-for-results program design, which includes an annual employee performance evaluation process before consideration of base salary merit increases, and set metrics for our cash incentive programs that include earnings and cash flow at both the consolidated and business unit levels in addition to discretionary factors such as safety performance, legal, and regulatory compliance as examples; (ii) long-term compensation: equity, cash and non-qualified deferred compensation, including the newly implemented PCU program, and all support retention of key talent; and (iii) benefits that are offered at appropriate levels. Therefore, we have concluded that the Company does not have any compensation programs that are reasonably likely to have a material adverse affect on the Company.

ROLE OF EXECUTIVE OFFICERS IN THE COMPENSATION PROCESS

Annually, the Chief Executive Officer and Senior Vice President of Human Resources make a compensation recommendation to the Compensation Committee for certain key executives, including each of the other NEOs. Their compensation recommendation is based on a review of the competitive market assessment for our executive officers, individual performance for each executive officer and the overall performance of the Company and business unit, if applicable. The compensation recommendation for the Chief Executive Officer is prepared by the Senior Vice President of Human Resources and is based on the competitive market assessment and the overall performance of the Company. (For discussion on the competitive market assessment, see “Executive Compensation Comparative Analysis” below.) These recommendations are the basis of discussion with the Compensation Committee; however, the Compensation Committee has final decision-making authority and approves the executive compensation program and the level of equity, cash, or incentive compensation to be awarded.

Meetings of the Compensation Committee discussing compensation strategies, program design and corporate governance matters are generally attended by the Chief Executive Officer, Chief Financial Officer, General Counsel, the Senior Vice President of Human Resources, and, when requested by the Committee, the Committee’s compensation consultant. At the October 16, 2012 Compensation Committee meeting, the Committee approved for our executive officers, including our NEOs: (i) fiscal year 2012 performance-based award payout levels for MIP and the first 25% of the fiscal year 2012 PCU award, as earned per the terms of the award; and (ii) fiscal year 2013 target compensation, which included base salary and target levels for MIP and LTI awards.

ROLE OF COMPENSATION CONSULTANT

Annually, the Compensation Committee engages an independent third-party consultant to provide advice on the design, administration and monitoring of the Company’s executive compensation programs. The compensation consultant provides data and recommendations for compensation programs that are compliant with applicable regulations, performance driven, cost effective and aligned with our overall compensation philosophy. Specifically, the compensation consultant provides guidance to our Compensation Committee on competitive compensation benchmarking and annual performance results compared to our Market Peer Group (as defined below). For further discussion of these processes, see “Executive Compensation Comparative Analysis” below.

During fiscal year 2012, the Compensation Committee directly engaged Pay Governance for executive compensation advisory services, including but not limited to, executive compensation comparative analysis discussed below. Pay Governance has not provided, and will not provide in the future, other services to the Company.

10

EXECUTIVE COMPENSATION COMPARATIVE ANALYSIS

Comparative Analysis

As part of its executive compensation advisory role, Pay Governance provided a competitive market assessment of our executive compensation programs for fiscal year 2012. The assessment: (i) provided an overview of the competitiveness of our executive compensation program; (ii) measured the value of each pay component relative to the market; and (iii) developed a framework for executive compensation planning and decisions. Since there were insufficient direct peers participating in the survey, Pay Governance developed a survey comparator group for benchmarking target compensation levels based on companies in manufacturing and similar industries as the Company with annual revenues of at least $2 billion (and median revenues near the Company). The resulting survey comparator group consists of 38 similarly-sized companies ($6.4 billion median revenue) specializing in engineering, construction, environmental services and manufacturing industries (Market Peer Group). Pay Governance obtained the information for the Market Peer Group from the 2011 Towers Watson General Industry Executive Compensation Database.

The results of this year’s target compensation benchmarking were generally consistent with last year and, as discussed below, confirmed that the Company was achieving its target compensation goal of regular annual compensation generally ranging between the market 50th and 75th percentiles.

After reviewing Pay Governance’s recommendations, the Committee determined that the Market Peer Group is the appropriate comparator group, even though we may not be compared to or compete directly with some of these companies for talent or client contracts. The companies in this group are similarly-sized in our general industry, and executive management in these companies possess similar qualifications to our executive officers.

|

Market Peer Group

|

|

|

AMETEK

|

Jacobs Engineering

|

|

Ball

|

KBR

|

|

Bemis

|

MeadWestvaco

|

|

Bovis Lend Lease

|

Owens Corning

|

|

Bucyrus International

|

Owens-Illinois

|

|

Cameron International

|

Parket Hannifin

|

|

Caterpillar

|

Parsons

|

|

Cooper Industries

|

Regal-Benoit

|

|

Corning

|

Rockwell International

|

|

Eaton

|

Sealed Air

|

|

Fluor

|

Snap-on

|

|

Fortune Brands

|

Sonoco Products

|

|

Greif

|

SPX

|

|

Grupo Ferrovial

|

Terex

|

|

HD Supply

|

Textron

|

|

Holcim

|

Thomas & Betts

|

|

Illinois Tool Works

|

3M

|

|

Ingersoll-Rand

|

Timken

|

|

ITT – Corporate

|

USG

|

Although the elements of the compensation paid to executive officers vary among the companies in the Market Peer Group, we recognize that we deliver a relatively larger portion of compensation in cash than do our Market Peer Group companies. The primary reason for this is that we have limited shares available to make equity grants and are thus focused on managing our share burn rate. In addition, our Chief Executive Officer already maintains a large equity stake in the Company, thus the Compensation Committee allocates a relatively larger portion of target compensation to our annual cash incentive plan than do some of our Market Peer Group companies. The Compensation Committee applies this approach consistently across other executive positions. For these reasons, our performance-based cash component of total compensation is disproportionate relative to the overall Market Peer Group. See “Compensation Discussion of our Named Executive Officers” for further information regarding each NEO’s target and actual total compensation for 2012.

11

COMPENSATION DISCUSSION OF OUR NAMED EXECUTIVE OFFICERS

Fiscal Year 2012 Target Total Compensation for our Named Executive Officers

The Compensation Committee generally targets total NEO compensation to range between the 50th and 75th percentiles of our Market Peer Group. Actual executive compensation depends on the actual performance of the Company and the individual. The Compensation Committee believes that setting challenging targets, will encourage executives to perform their best.

The tables and discussion provided below for each NEO reflect the compensation elements and corresponding target and earned actual compensation amounts as reviewed and approved by the Compensation Committee. While the majority of these amounts can easily be compared to the amounts reflected in the Summary Compensation Table, the PCU amounts differ. As is required to comply with SEC regulations, the amounts reflected in the “Stock Awards” column of the Summary Compensation Table represent the total grant date fair value, calculated using a Monte Carlo simulation model, of PCUs awarded during fiscal year 2012. In contrast, the CD&A tables below report the target values of the PCUs on the grant date. These differences result in the actual compensation reported in the CD&A tables below being higher than the compensation reported in the Summary Compensation Table. See “INCENTIVE COMPENSATION AND OTHER PROGRAMS – Fiscal Year 2012 Performance Results” for additional information regarding the measurement period and payout calculation of PCUs.

As discussed in “INCENTIVE COMPENSATION AND OTHER PROGRAMS - Long-Term Incentive Compensation,” the core PCU program is designed to be a three-year performance period with earned awards paid at the end of the three years. To address the negative financial impact to the executive from our transition to PCUs from previous stock option awards, which were four-year service based vesting of 25% per year, three Relative TSR performance periods began in fiscal year 2012, which include the one-time supplemental transition award. Only the first performance period ended on August 31, 2012 and therefore, is reflected in actual compensation below. The remaining two performance periods will be reflected as actual compensation in the fiscal year such periods end, which are August 31, 2013 and 2014.

As discussed in “EXECUTIVE SUMMARY” and in more detail below, the Company and business units exceeded financial, stock and operational targets for fiscal year which resulted in maximum incentive awards for most of our NEOs.

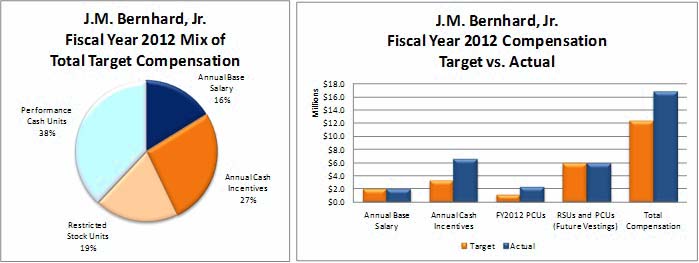

J.M. Bernhard, Jr.

Leadership and Performance Highlights. Since 1987, through Mr. Bernhard’s vision and leadership as founder, Chief Executive Officer, President and Chairman of the Board, the Company has grown from a local industrial pipe fabrication and manufacturing business to a Fortune 500 company that is among the premier engineering and construction companies in the world.

|

|

·

|

Since 2005, under his leadership and guidance through strategic acquisitions and business ventures, our revenues increased from $3.3 billion to $6.0 billion and we have expanded our workforce from 19,000 to 25,000 globally.

|

|

|

·

|

Over the past five years, Mr. Bernhard has strengthened our leadership team and profitability by promoting and bringing in top talent to complete our corporate executive management team with individuals who have deep industry experience and are visionary leaders in their respective areas of responsibility. Mr. Bernhard equally focused on operations by compiling a team of presidents for each of our business units, again through promoting and or hiring top talent from our competitors, whose main focus is best in class project execution and increasing profitability.

|

|

|

·

|

In fiscal year 2012, Mr. Bernhard assumed operational leadership after the retirement of former our Chief Operating Officer, and successfully negotiated the agreement to be acquired by CB&I at a premium of 72% over the closing price for the last trading day prior to announcement (for further discussion please see our current report on Form 8-K filed with the SEC on July 30, 2012). He also led several key strategic initiatives, such as: (i) initiated the process for exercising the “put” options of our subsidiary NEH to sell its investment in the Westinghouse Group back to Toshiba; (ii) negotiated and oversaw the divestiture of substantially all of the assets of the E&C business unit for approximately $290 million in cash proceeds; (iii) devised and oversaw the execution of a share buyback program via a $150 million Dutch auction tender offer; (iv) drove the Company to meet or exceed all key fiscal year 2012 financial targets; (v) served as primary thought leader for resolving complex legal settlements; and (vi) developed and kicked off company-wide process improvement initiative.

|

Fiscal Year 2012 Compensation Summary.

|

|

·

|

Mr. Bernhard’s base salary and annual incentive targets remained unchanged from the prior fiscal year, but his long term incentive targets increased due to the implementation of the new performance based LTI awards (PCUs), for which he received a one-time supplemental transition grant for a target of $2,350,000 in addition to normal annual LTI target levels. The core PCU program is designed to be a three-year performance period with earned awards paid at the end of the three years. To address the negative financial impact to the executive from our transition to PCUs from previous stock option awards, which incrementally vested over a four-year service period, three Relative TSR performance periods began in fiscal year 2012, which include the one-time supplemental transition award. Mr. Bernhard’s target total compensation for fiscal year 2012 was $12,350,000, which increased from his fiscal year 2011 target of $10,000,000.

|

12

|

|

·

|

For fiscal year 2012, Mr. Bernhard’s performance based target compensation totaled $8,000,000 (or 65%) of total target compensation. As discussed above, Mr. Bernhard provided outstanding operational and strategic leadership throughout fiscal year 2012, which resulted in strong financial performance, especially as compared to prior years, and record stock performance for fiscal year 2012. As a result, the Compensation Committee approved an annual cash incentive payout at 200% of target for Mr. Bernhard and the earned maximum payout level of 200% for the first 25% of the PCU award per the terms of the award. See “INCENTIVE COMPENSATION AND OTHER PROGRAMS – Annual Cash Incentive Compensation” and “-Long-Term Incentive Compensation” below.

|

|

Elements of Compensation

|

Fiscal Year

2012 Target

Compensation

|

Fiscal Year

2012 Actual

Compensation

|

Actual Market

Position (1)

|

||||||

|

Annual Base Salary

|

$ | 2,000,000 | $ | 2,000,000 |

Above 75th

|

||||

|

Incentive Compensation (vested in 2012):

|

|||||||||

|

Annual Cash Incentive Compensation

|

$ | 3,300,000 | $ | 6,600,000 | (2) |

Above 75th

|

|||

|

Performance Cash Units

(FY2012 Performance Period)

|

$ | 1,175,000 | $ | 2,350,000 | (2) |

Below 50th

|

|||

|

Compensation Subtotal

|

$ | 6,475,000 | $ | 10,950,000 | |||||

|

Incentive Compensation (future vesting):

|

|||||||||

|

Restricted Stock Units

(Vestings FY2013, FY2014, and FY2015)

|

$ | 2,350,000 | (3) | $ | 2,350,000 | (3) |

Below 50th

|

||

|

Performance Cash Units

(FY2013 & FY2014 Performance Periods)

|

$ | 3,525,000 | (4) | $ | 3,525,000 | (4) |

Below 50th

|

||

|

Total Compensation, Excluding Other Compensation (5)

|

$ | 12,350,000 | $ | 16,825,000 |

Above 75th

|

||||

|

|

(1)

|

Market Position of Market Peer Group for Chief Executive Officer for companies with median revenues of $6.4 billion; compensation components are shown on the chart to indicate placement against market position for Fiscal Year 2012 Actual Compensation.

|

|

|

(2)

|

For further discussion of annual cash incentive compensation and earned PCU compensation, please see “INCENTIVE COMPENSATION AND OTHER PROGRAMS” below.

|

|

|

(3)

|

Amount represents the value of equity at the time of award by the Compensation Committee, which have a three-year service based vesting of 33% per year.

|

|

|

(4)

|

Two additional PCU measurement periods began in fiscal year 2012 that are shown at target levels until the end of the performance period ends and earned PCUs are calculated. The first with a $1,175,000 target and a 2-year measurement period ending on August 31, 2013 and the second with a $2,350,000 target and a 3-year measurement period ending on August 31, 2014.

|

|

|

(5)

|

Total compensation excludes all other compensation reflected in the “Summary Compensation Table for the Fiscal Years Ended August 31, 2012, 2011 and 2010” below.

|

13

Brian K. Ferraioli

Leadership and Performance Highlights.

|

|

·

|

Mr. Ferraioli joined us in July 2007 as our Executive Vice President, Finance, and served in that position until October 2007, when he was appointed to his current position. Over the last five years, Mr. Ferraioli has made numerous strategic personnel and policy changes within our organization to enable our continued growth and success. More recently, under his leadership: (i) we have amended our credit facility for lender commitments up to $1.45 billion; (ii) we have increased our restricted and unrestricted cash and cash equivalents, escrowed cash and restricted and unrestricted short-term investment balance from $0.9 billion at August 31, 2008 to $1.4 billion at August 31, 2012, and repeatedly generated strong operating cash flows; and (iii) Standards & Poor’s increased the Company’s credit rating to an investment grade of BBB- with a stable outlook.

|

|

|

·

|

In fiscal year 2012, Mr. Ferraioli provided proactive financial leadership at both corporate and business unit level ensuring the Company met or exceeded all key financial targets. He served as key advisor to our Chief Executive Officer on numerous strategic business decisions, which culminated in the agreement to be acquired by CB&I at a premium of 72% over the closing price for last trading day prior to announcement (for further discussion please see our current report on Form 8-K filed with the SEC on July 30, 2012), such as: (i) exercised the put options of our subsidiary NEH to sell its investment in the Westinghouse Group back to Toshiba; (ii) successfully completed the divestiture of substantially all of the assets of the E&C business unit for approximately $290 million in cash proceeds; (iii) executed a share buyback program via a $150 million Dutch auction tender offer; and (iv) resolved complex legal settlements. Mr. Ferraioli continued to strengthen our financial and accounting function through the following actions in fiscal year 2012: (i) ensured shareholders and investors understood the numerous complex transactions; (ii) successfully recruited a Chief Accounting Officer with high potential talent and a strong public accounting background; and (iii) supported a significant investment and upgrade in our enterprise resource planning (ERP) system.

|

Fiscal Year 2012 Compensation Summary.

|

|

·

|

Mr. Ferraioli’s base salary and annual incentive targets remained unchanged from the prior fiscal year, but his long term incentive targets increased due to the implementation of the new performance based LTI awards (PCUs), for which he received a one-time supplemental transition grant for a target of $700,000 in addition to normal annual LTI target levels. The core PCU program is designed to be a three-year performance period with earned awards paid at the end of the three years. To address the negative financial impact to the executive from our transition to PCUs from previous stock option awards, which incrementally vested over a four-year service period, three Relative TSR performance periods began in fiscal year 2012, which include the one-time supplemental transition award. Mr. Ferraioli’s target total compensation for fiscal year 2012 was $3,550,000, which increased from his fiscal year 2011 target of $2,850,000.

|

|

|

·

|

For fiscal year 2012, Mr. Ferraioli’s performance based target compensation totaled $2,200,000 (or 62%) of total target compensation. As discussed above Mr. Ferraioli provided outstanding operational and strategic leadership throughout fiscal year 2012 which resulted in strong financial performance, especially as compared to prior years, and record stock performance for fiscal year 2012. As a result, the Compensation Committee approved an annual cash incentive payout at 200% of target for Mr. Ferraioli and the earned maximum payout level of 200% for the first 25% of the PCU award per the terms of the award. See “INCENTIVE COMPENSATION AND OTHER PROGRAMS – Annual Cash Incentive Compensation” and “-Long-Term Incentive Compensation” below.

|

|

|

·

|

Additionally, in light of the significant strategic initiatives underway, in October 2011, the Chief Executive Officer recommended, and the Compensation Committee approved, a $1 million non-qualified deferred compensation award, with a two-year cliff vesting period, to be given to Mr. Ferraioli in order to better ensure his retention with the Company.

|

14

|

Elements of Compensation

|

Fiscal Year

2012 Target

Compensation

|

Fiscal Year

2012 Actual

Compensation

|

Actual Market

Position (1)

|

||||||

|

Annual Base Salary

|

$ | 650,000 | $ | 650,000 |

Above 75th

|

||||

|

Incentive Compensation (vested in 2012):

|

|||||||||

|

Annual Cash Incentive Compensation

|

$ | 800,000 | $ | 1,600,000 | (2) |

Above 75th

|

|||

|

Performance Cash Units

(FY2012 Performance Period)

|

$ | 350,000 | $ | 700,000 | (2) |

50th to 75th

|

|||

|

Compensation Subtotal

|

$ | 1,800,000 | $ | 2,950,000 | |||||

|

Incentive Compensation (future vesting):

|

|||||||||

|

Restricted Stock Units

(Vestings FY2013, FY2014, and FY2015)

|

$ | 700,000 | (3) | $ | 700,000 | (3) |

50th to 75th

|

||

|

Performance Cash Units

(FY2013 & FY2014 Performance Periods)

|

$ | 1,050,000 | (4) | $ | 1,050,000 | (4) |

50th to 75th

|

||

|

Total Compensation, Excluding Other Compensation (5)

|

$ | 3,550,000 | $ | 4,700,000 |

Above 75th

|

||||

|

|

(1)

|

Market Position of Market Peer Group for Chief Financial Officer for companies with median revenues of $6.4 billion; compensation components are shown on the chart to indicate placement against market position for Fiscal Year 2012 Actual Compensation.

|

|

|

(2)

|

For further discussion of annual cash incentive compensation and earned PCU compensation, please see “INCENTIVE COMPENSATION AND OTHER PROGRAMS” below.

|

|

|

(3)

|

Amount represents the value of equity at the time of award by the Compensation Committee, which have a three-year service based vesting of 33% per year.

|

|

|

(4)

|

Two additional PCU measurement periods began in fiscal year 2012 that are shown at target levels until the end of the performance period ends and earned PCUs are calculated. The first with a $350,000 target and a 2-year measurement period ending on August 31, 2013 and the second with a $700,000 target and a 3-year measurement period ending on August 31, 2014.

|

|

|

(5)

|

Total compensation excludes all other compensation reflected in the “Summary Compensation Table for the Fiscal Years Ended August 31, 2012, 2011 and 2010” below.

|

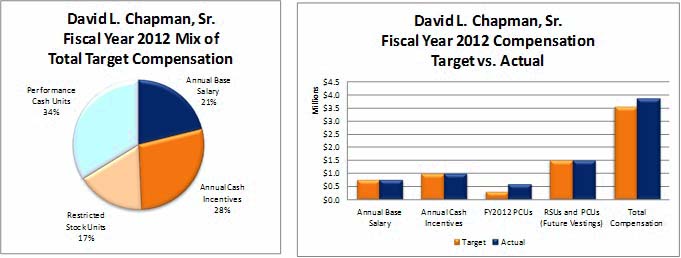

David L. Chapman, Sr.

Leadership and Performance Highlights.

|

|

·

|

Mr. Chapman joined us in April 2002 as President of our Fabrication & Manufacturing Division, which is now known as the Fabrication & Manufacturing Group. Under Mr. Chapman’s leadership for the past decade, Fabrication & Manufacturing consistently provides our highest operating profit margins as compared to our other business units. Under his leadership, we have expanded our fabrication and manufacturing operations into Mexico, the United Arab Emirates and Brazil through a joint venture and started operations on our nuclear modular facility in Lake Charles, Louisiana. Mr. Chapman’s industry expertise and leadership has enabled the Fabrication & Manufacturing business unit to consistently achieve one of our highest levels of business unit operating profit margins and puts him at high risk for recruitment by competitors. Accordingly, our Compensation Committee deems these levels appropriate and key to his retention.

|

|

|

·

|