Attached files

| file | filename |

|---|---|

| 8-K - THE BANCORP, INC. FORM 8-K - Bancorp, Inc. | bancorp8k.htm |

| EX-99.1 - EXHIBIT 99.1 - Bancorp, Inc. | ex99-1.htm |

Exhibit 99.2

Follow-On Offering of Common Stock

NASDAQ: TBBK

December 2012

NASDAQ: TBBK

December 2012

Safe Harbor Regarding Forward-Looking Statements

This presentation may contain forward-looking information about The Bancorp, Inc. (“the Company”) that is intended to be covered

by the safe harbor for forward-looking statements provided by the Private Securities Litigation Reform Act of 1995. Actual results

and trends could differ materially from those set forth in such statements due to various risks, uncertainties and other factors. Such

risks, uncertainties and other factors that could cause actual results and experience to differ from those projected include, but are not

limited to, the following: ineffectiveness of the Company’s business strategy due to changes in current or future market conditions;

the effects of competition, and of changes in laws and regulations, including industry consolidation and development of competing

financial products and services; interest rate movements; changes in credit quality; volatilities in the securities markets; and

deteriorating economic conditions, and other risks and uncertainties, including those detailed in the Company’s filings with the

Securities and Exchange Commission. The statements are valid only as of the date hereof and the Company disclaims any

obligation to update this information except as may be required by applicable law.

by the safe harbor for forward-looking statements provided by the Private Securities Litigation Reform Act of 1995. Actual results

and trends could differ materially from those set forth in such statements due to various risks, uncertainties and other factors. Such

risks, uncertainties and other factors that could cause actual results and experience to differ from those projected include, but are not

limited to, the following: ineffectiveness of the Company’s business strategy due to changes in current or future market conditions;

the effects of competition, and of changes in laws and regulations, including industry consolidation and development of competing

financial products and services; interest rate movements; changes in credit quality; volatilities in the securities markets; and

deteriorating economic conditions, and other risks and uncertainties, including those detailed in the Company’s filings with the

Securities and Exchange Commission. The statements are valid only as of the date hereof and the Company disclaims any

obligation to update this information except as may be required by applicable law.

Free Writing Prospectus Statement

The Company has filed a registration statement (including a prospectus and a related prospectus supplement) with the SEC (File No.

333-185226) for the offering to which this communication relates. Before you invest, you should read the prospectus and the

prospectus supplement in that registration statement, the preliminary prospectus supplement and other documents that the

Company has filed with the SEC for more complete information about the Company and the offering. You may obtain these

documents without charge by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, copies of the preliminary

prospectus supplement and the prospectus relating to the offering may be obtained from Sandler O'Neill + Partners, L.P., 1251

Avenue of the Americas, 6th Floor, New York, NY 10020, (866) 805-4128.

333-185226) for the offering to which this communication relates. Before you invest, you should read the prospectus and the

prospectus supplement in that registration statement, the preliminary prospectus supplement and other documents that the

Company has filed with the SEC for more complete information about the Company and the offering. You may obtain these

documents without charge by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, copies of the preliminary

prospectus supplement and the prospectus relating to the offering may be obtained from Sandler O'Neill + Partners, L.P., 1251

Avenue of the Americas, 6th Floor, New York, NY 10020, (866) 805-4128.

Forward-Looking Statements

2

Issuer: The Bancorp, Inc. (“The Bancorp” or the "Company")

Ticker / Exchange: TBBK / NASDAQ Global Select Market

Offering: Follow-on Public Offering

Type of Security: Common Stock

Transaction Size: $50.0 Million

Over-Allotment Option: 15%

Use of Proceeds: General corporate purposes

Book-Running Manager: Sandler O’Neill + Partners, L.P.

Co-Manager: Sterne, Agee & Leach, Inc.

Offering Summary

2

4 Offering Rationale:

– Increase tangible common equity (TCE/TA¹ to 10.4%) to further enable balance sheet growth and profitability enhancement

through continued business line expansion and organic growth opportunities

through continued business line expansion and organic growth opportunities

4 Strategic Goal:

– Create and grow a stable, profitable institution with the optimum reliance on capital, risk management and technology, and

manage it with knowledgeable and experienced management and senior officers

manage it with knowledgeable and experienced management and senior officers

4 Tactical Approach:

– Deposits - Utilize a branchless banking network to gather scalable deposits through strong contractual relationships at costs

significantly below peers

significantly below peers

– Assets - Focus on asset classes including loans and securities appropriate to our expertise to achieve returns above risk-

adjusted peer net interest margins

adjusted peer net interest margins

– Non Interest Income - Grow non-interest income disproportionately in relation to non interest expense through our deposit and

asset approaches

asset approaches

– Operating Leverage - Leverage infrastructure investment to grow earnings by creating efficiencies of scale

(1) Assumes net proceeds received in the offering of $47.0 million (based on gross proceeds of $50.0 million and total deal expenses of 6.0%); see non-GAAP reconciliation in Appendix

Source: Company filings

Planning For Growth With Safety And Soundness

3

4 Experienced senior management team with 12% fully-diluted insider ownership¹ and a track record of

performance and shareholder returns at previous institutions

performance and shareholder returns at previous institutions

4 Unprecedented market opportunity for growth across business lines

− The Company has experienced considerable growth through strategic initiatives and targeted acquisitions and is well-

positioned to further leverage its existing infrastructure to capitalize on opportunities in its markets of operation

positioned to further leverage its existing infrastructure to capitalize on opportunities in its markets of operation

4 Low-cost, stable funding base through multi-channel deposit gathering strategy in niche products

− $2.8 billion of total deposits at an overall cost of 0.37% for the quarter ended September 30, 2012

4 Asset quality compares favorably to peers due to disciplined underwriting and long-standing relationships with a

significant percentage of the Company's borrowers

significant percentage of the Company's borrowers

− Community bank assets originated by experienced lenders in relatively stable markets

− NPAs / Assets of 1.07% at September 30, 2012²

4 Strong capital and asset quality, in conjunction with robust compliance and regulatory infrastructure, permits the

Company to be on the offensive and forward-thinking at a time when many competitors are forced to operate in a

reactionary manner

Company to be on the offensive and forward-thinking at a time when many competitors are forced to operate in a

reactionary manner

Investment Highlights

4

(1) Insider ownership, including Senior Management and Board, of 12% based on March 9, 2012 proxy

(2) NPAs include nonaccrual loans, accruing loans 90+ days past due and other real estate owned

Source: Company filings

Strong Senior Management Team With A Wealth Of Experience

4 Highly experienced senior management team with an aggregate of over 200 years of experience providing middle

market banking services

market banking services

– Management has a significant history together as most are former executives of a prior bank which was sold in November 1999

4 Insider ownership of 12% (fully-diluted)¹

5

(1) Insider ownership, including Senior Management and Board, of 12% based on March 9, 2012 proxy

Source: Company filings

4 The Bancorp is uniquely positioned to take advantage of recent industry trends, regulatory changes, and

competitor dislocation, all of which will enable strong growth for The Bancorp and create a compelling use of

capital in the near and longer term

competitor dislocation, all of which will enable strong growth for The Bancorp and create a compelling use of

capital in the near and longer term

4 Industry trends are from "paper to plastic", "credit to debit", and "manual to electronic", all of which support The

Bancorp's continued strong growth and are unique strengths of The Bancorp's unique market positioning

Bancorp's continued strong growth and are unique strengths of The Bancorp's unique market positioning

4 Through The Bancorp's affinity relationships, the company will continue to provide fee based services and

aggregate low-cost deposit bases as more financial services firms turn to partners with scale, strong regulatory

standing and compliance records, and niche experience

aggregate low-cost deposit bases as more financial services firms turn to partners with scale, strong regulatory

standing and compliance records, and niche experience

4 The Bancorp’s ability to leverage large affinity relationships for the distribution of its products and services

provides outsized forward growth opportunity

provides outsized forward growth opportunity

4 Recent legislative changes will push larger companies to partner with firms like The Bancorp to protect current

revenue

revenue

4 Because of these strong growth trends and favorable industry dynamics, The Bancorp's competitive position has

improved dramatically over the last several years through enhanced scale, reputation, personnel and capabilities

improved dramatically over the last several years through enhanced scale, reputation, personnel and capabilities

Unprecedented Market Opportunity For Growth

6

4 A commercial bank founded in 2000 headquartered in Wilmington, Delaware with approximately $3.1 billion in assets, $1.9 billion in

outstanding loan balances and $2.8 billion of deposits at September 30, 2012

outstanding loan balances and $2.8 billion of deposits at September 30, 2012

4 Employs a primarily branchless deposit strategy that delivers a full array of commercial and consumer banking services both locally

and nationally through private label banking products

and nationally through private label banking products

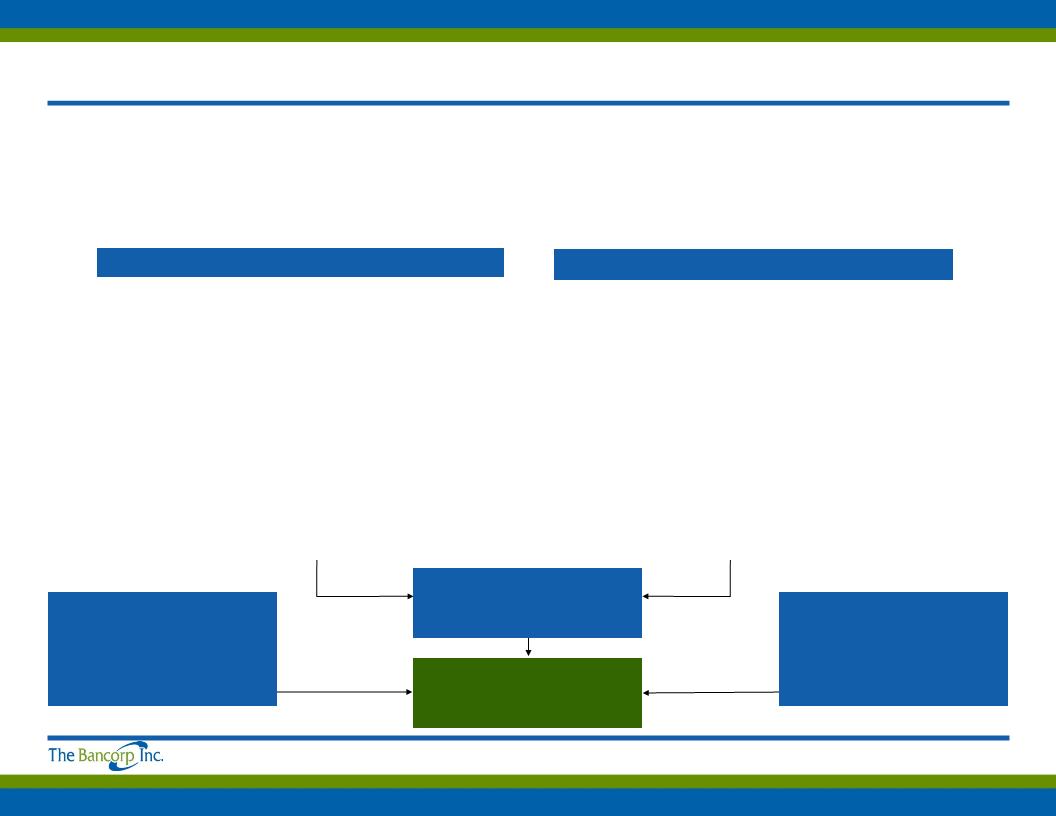

Business Model: A Distinct Business Strategy

|

Net Interest Margin

|

|

ASSETS

|

|

• Above-peer credit quality, well-collateralized loans

to businesses and individuals in the Philadelphia/Wilmington market area: § Commercial lending, commercial & residential

real estate, construction lending • Well-Capitalized Automobile Fleet Leasing

• Wealth Management Lending:

§ Securities backed loans

• Government Guaranteed Lending Program for National

Franchises (75% guaranteed by US government) • Securities Portfolio:

§ Primarily highly rated government obligations

|

7

|

Non-Interest Income Sources:

Prepaid Cards

Healthcare

Payment Acceptance

Wealth Management

|

|

Non-Interest Income Sources:

Automobile Leasing Fleet

Community Bank

|

|

INCOME

|

|

DEPOSITS

|

|

• Private-Label Banking: stable, lower-cost core deposits

§ Healthcare (Health Savings Accounts and Flexible

Spending Accounts) § Payment Acceptance (Credit, Debit Card and ACH

Processing) § Prepaid Cards

§ Wealth Management (Deposits and Loans for Clients of

Wealth firms) • Community Bank

|

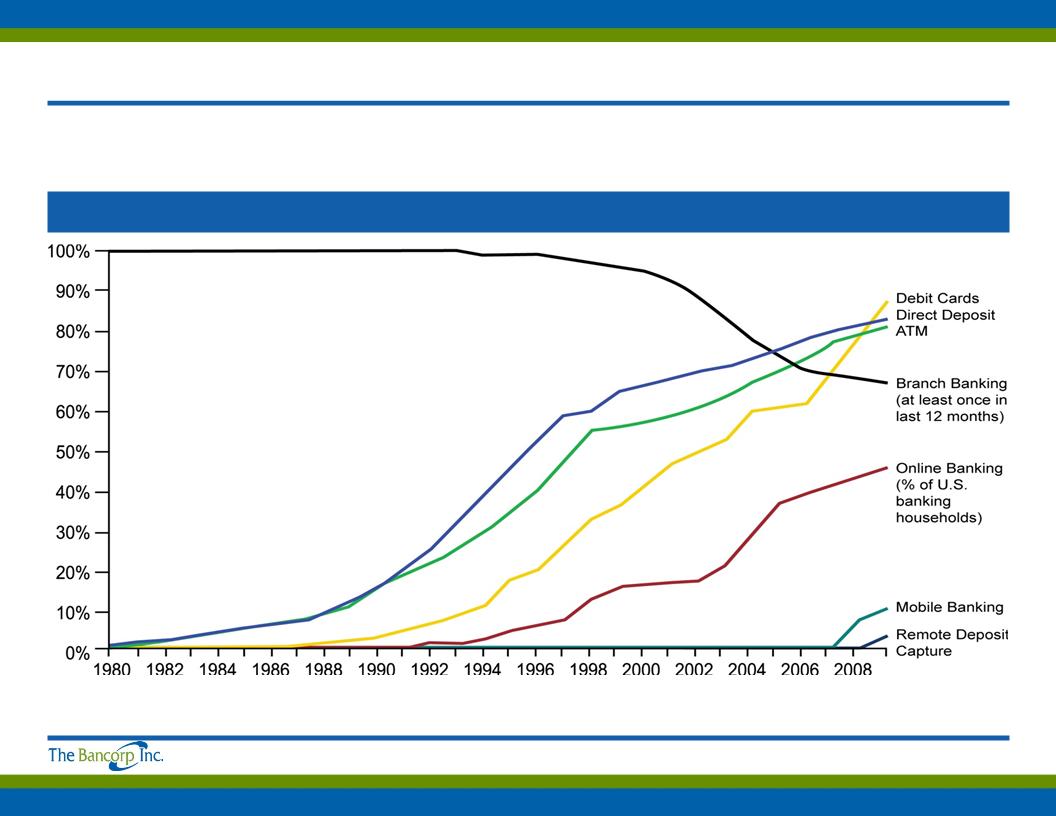

Planning For Growth: Consumer Distribution Channel Penetration

Source: Federal Reserve, FRB Boston, FRB Philadelphia, SRI Consulting, University of Michigan, Mintel, Celent, Bank of America, comScore, Nielsen Mobile, Wall Street Journal, Mercatus Analytics

Consumer Trends By Percent of U.S. Households From 1980 Through 2009

4 TBBK’s business model is uniquely structured to take advantage of evolving consumer banking trends, positioning the bank for

growth and increased profitability in an environment that presents significant challenges to the traditional banking model

growth and increased profitability in an environment that presents significant challenges to the traditional banking model

8

Prepaid Gross Dollar Volume¹ And Cardholder Growth²

(1) Gross Dollar Volume is the total amount spent on all cards outstanding within a given period. The bar graph represents the gross dollar volume for the period segmented by the program contract

date.

date.

(2) Number of active cards as of year-end of the stated year with the exception of 2012, which is end of the third quarter.

Source: Company documents

9

4 Scalable growth model and a rapidly growing industry have supported significant growth

Revenue Composition

Source: Company filings

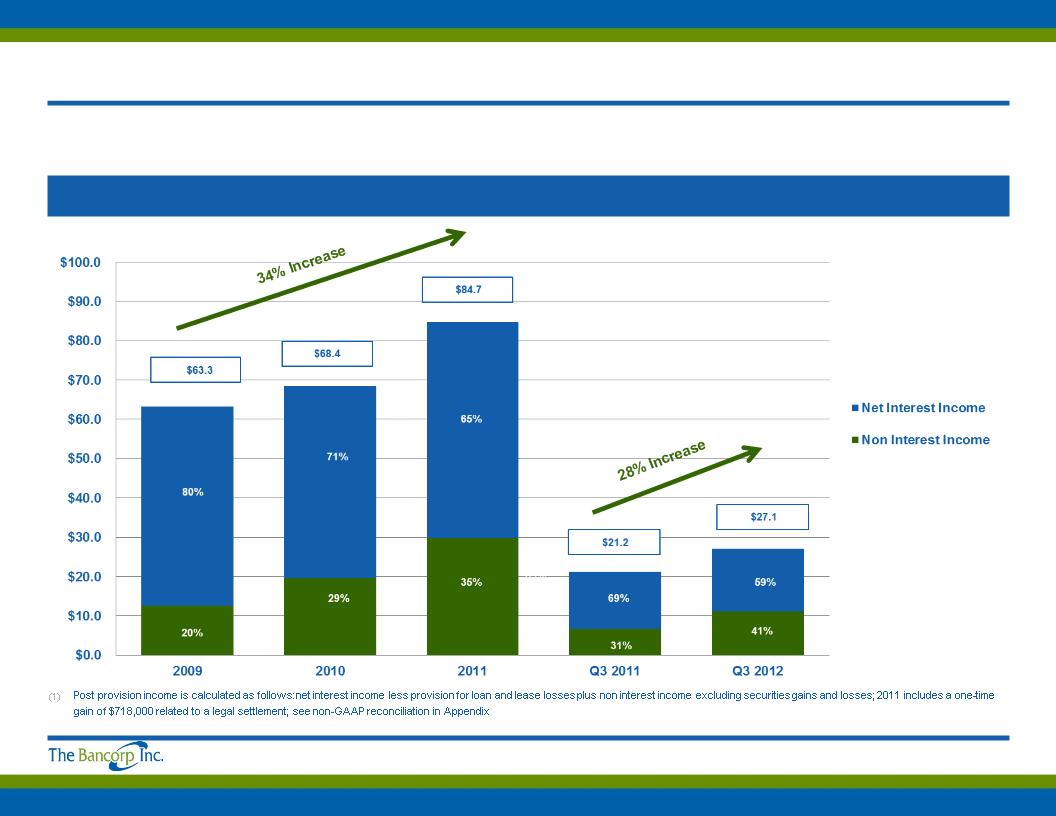

Post Provision Income ($M)¹

4 34% revenue growth over the last two years and continued strong growth throughout 2012

10

4 Solid growth in net interest income despite difficult interest rate environment

Compressed Interest Rate Environment

Net Interest Income ($M)

11

Source: Company filings

Non Interest Income-Generating Strategies: Growth And Sustainability

(2) CAGR calculated 2009 through 2011

Source: Company filings

Continued Growth In Non Interest Income ($M)¹

4 54% CAGR over the last two years and continued strong growth in 2012 due to growth of both current and new

relationships

relationships

12

4 Non interest income is approximately half of non interest expense, driving improving operating earnings

4 Cost of customer acquisition continues to decline due to strength of affinity relationships

Scalable Business Model

13

Non Interest Income / Non Interest Expense (%)¹

(1) Excludes gains on investment securities and nonrecurring expenses; 2011 includes a one-time gain of $718,000 related to a legal settlement

Source: Company filings

Operating Leverage

Adjusted Operating Earnings ($M)1,2,3

(1) As a supplement to GAAP, Bancorp has provided this non-GAAP performance result. The Bancorp believes that this non-GAAP financial measure is useful because it allows investors to assess its

operating performance. Management utilizes adjusted operating earnings to measure the combined impact of changes in net interest income, non-interest income and certain other expenses.

Adjusted operating earnings exclude the impact of the provision for loan losses, income taxes, securities gains and losses and certain non-recurring items. Other companies may calculate adjusted

operating earnings differently. Although this non-GAAP financial measure is intended to enhance investors’ understanding of Bancorp’s business and performance, it should not be considered, and

is not intended to be, a substitute for GAAP.

operating performance. Management utilizes adjusted operating earnings to measure the combined impact of changes in net interest income, non-interest income and certain other expenses.

Adjusted operating earnings exclude the impact of the provision for loan losses, income taxes, securities gains and losses and certain non-recurring items. Other companies may calculate adjusted

operating earnings differently. Although this non-GAAP financial measure is intended to enhance investors’ understanding of Bancorp’s business and performance, it should not be considered, and

is not intended to be, a substitute for GAAP.

(2) CAGR calculated 2009 through 2011

(3) For reconciliation detail, please see Appendix.

Source: Company documents

14

4 TBBK employs a multi-channel growth strategy for loan origination, with the primary driver being its regional commercial banking

operations.

operations.

Primary Asset Generating Strategies: Business Line Overview

4 Automobile Fleet Leasing

− Well-collateralized automobile fleet leasing

− Average transaction: 8-15 automobiles, $350,000

− 32% of portfolio leased by state and federal agencies

4 Wealth Management

− 17 affinity groups, managing $400 billion in assets

− SEI Investments, Legg Mason, Genworth Financial Trust Company

− Generates securities backed and other loans

4 Government Guaranteed Lending

− Loans from $150,000 to $5.0 million primarily to franchisees such as UPS

Stores, Massage Envy, FASTSIGNS and Save a Lot which have a 75%

guaranty by the U.S. Small Business Administration. Approved Franchise and

Medical Guidance lines total $494+ million.

Stores, Massage Envy, FASTSIGNS and Save a Lot which have a 75%

guaranty by the U.S. Small Business Administration. Approved Franchise and

Medical Guidance lines total $494+ million.

4 Securities

− High credit quality tax exempt municipal obligations

− U.S. Government agency securities primarily 4-5 year average lives and other

highly rated mortgage-backed securities

highly rated mortgage-backed securities

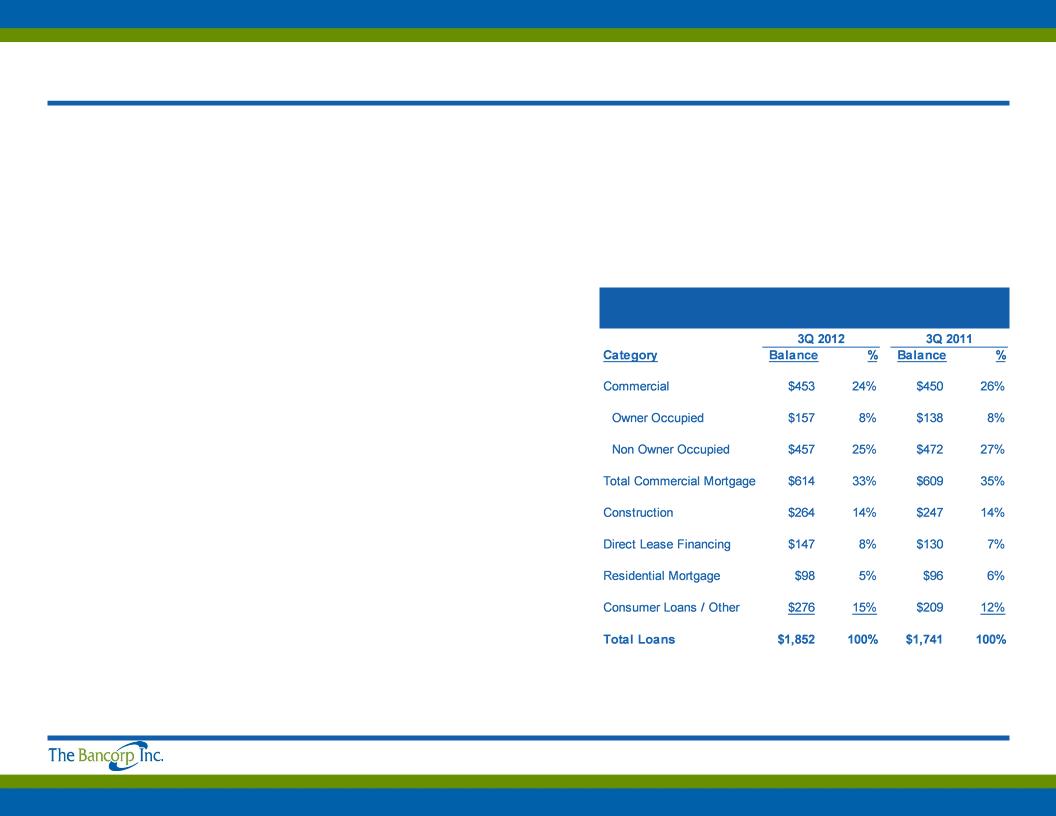

Loan Composition ($M)

15

Source: Company filings

4 Community Bank

− Offers traditional community banking products and services targeting the highly fragmented Philadelphia/Wilmington banking market

Asset Quality Overview

16

(1) Regional peers include publicly traded Mid-Atlantic commercial banks with assets between $1 billion and $4 billion as of September 30, 2012; graphs represent median values

(2) Texas Ratio = (Nonaccrual Loans + Restructured Loans + Loans 90 + days past due + OREO)/(Loss Reserves + Tangible Equity). TBBK computed with consolidated capital.

Source: Company, SNL Financial

Non-Accrual Loans / Total Loans¹

Loan Loss Reserves / Gross Loans¹

Loan Loss Reserves / Nonaccrual Loans¹

Texas Ratio1,2

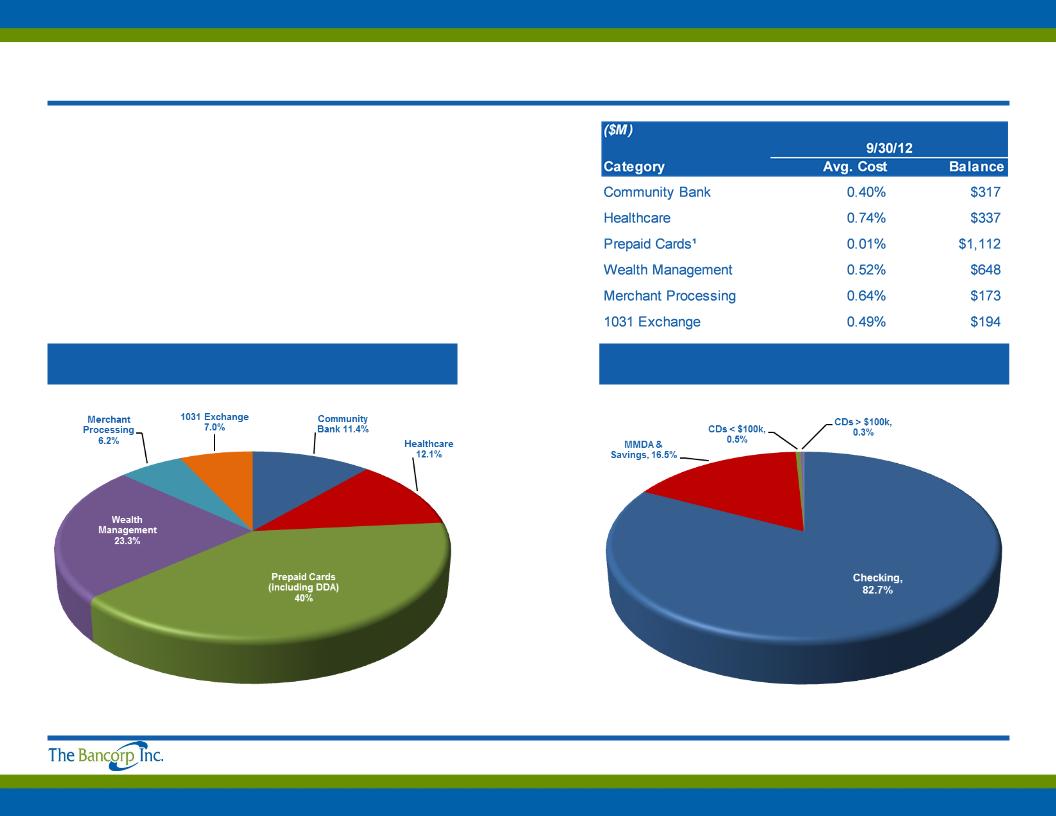

4 Significant growth in prepaid card, healthcare and other

deposit business lines support significantly lower

average cost of deposits

deposit business lines support significantly lower

average cost of deposits

4 Total deposits of $2.8 billion with an average cost of

0.37% in 3Q 2012

0.37% in 3Q 2012

Growth Engine: Where Do Deposits Come From?

Deposit Type

Deposit Business Line Concentration

(1) Includes demand deposit accounts

Source: Company filings

17

4 The Bancorp has long-term, often exclusive agreements in place with its private label banking partners

4 We have retained 99% of maturing contracts

Deposit-Generating Strategies: Sticky And Long-Term

(1) Does not include deposits associated with a third party with which TBBK disengaged in 2012

Source: Company filings

18

Planning For Growth With Safety And Soundness

19

(1) Assumes net proceeds received in the offering of $47.0 million (based on gross proceeds of $50.0 million and total deal expenses of 6.0%); see non-GAAP reconciliation in Appendix

Source: Company filings

4 Offering Rationale:

– Increase tangible common equity (TCE/TA¹ to 10.4%) to further enable balance sheet growth and profitability enhancement

through continued business line expansion and organic growth opportunities

through continued business line expansion and organic growth opportunities

4 Strategic Goal:

– Create and grow a stable, profitable institution with the optimum reliance on capital, risk management and technology, and

manage it with knowledgeable and experienced management and senior officers

manage it with knowledgeable and experienced management and senior officers

4 Tactical Approach:

– Deposits - Utilize a branchless banking network to gather scalable deposits through strong contractual relationships at costs

significantly below peers

significantly below peers

– Assets - Focus on asset classes including loans and securities appropriate to our expertise to achieve returns above risk-

adjusted peer net interest margins

adjusted peer net interest margins

– Non Interest Income - Grow non-interest income disproportionately in relation to non interest expense through our deposit and

asset approaches

asset approaches

– Operating Leverage - Leverage infrastructure investment to grow earnings by creating efficiencies of scale

Appendix

Capital Ratios And Selected Financial Data

21

(1) Excludes FHLB and ACBB stock

Source: Company documents and filings

Current Loan Portfolio And Asset Quality Overview

22

Source: Company filings

4 Commercial lending is substantially all in greater Philadelphia/Wilmington metropolitan area

− Consists of the 12 counties surrounding Philadelphia and Wilmington, including Philadelphia, Delaware,

Chester, Montgomery, Bucks and Lehigh Counties in Pennsylvania; New Castle County in Delaware; and

Mercer, Burlington, Camden, Ocean and Cape May Counties in New Jersey.

Chester, Montgomery, Bucks and Lehigh Counties in Pennsylvania; New Castle County in Delaware; and

Mercer, Burlington, Camden, Ocean and Cape May Counties in New Jersey.

4 Philadelphia/Wilmington and the surrounding markets encompass a large population, stable economic activity

and attractive demographics.

and attractive demographics.

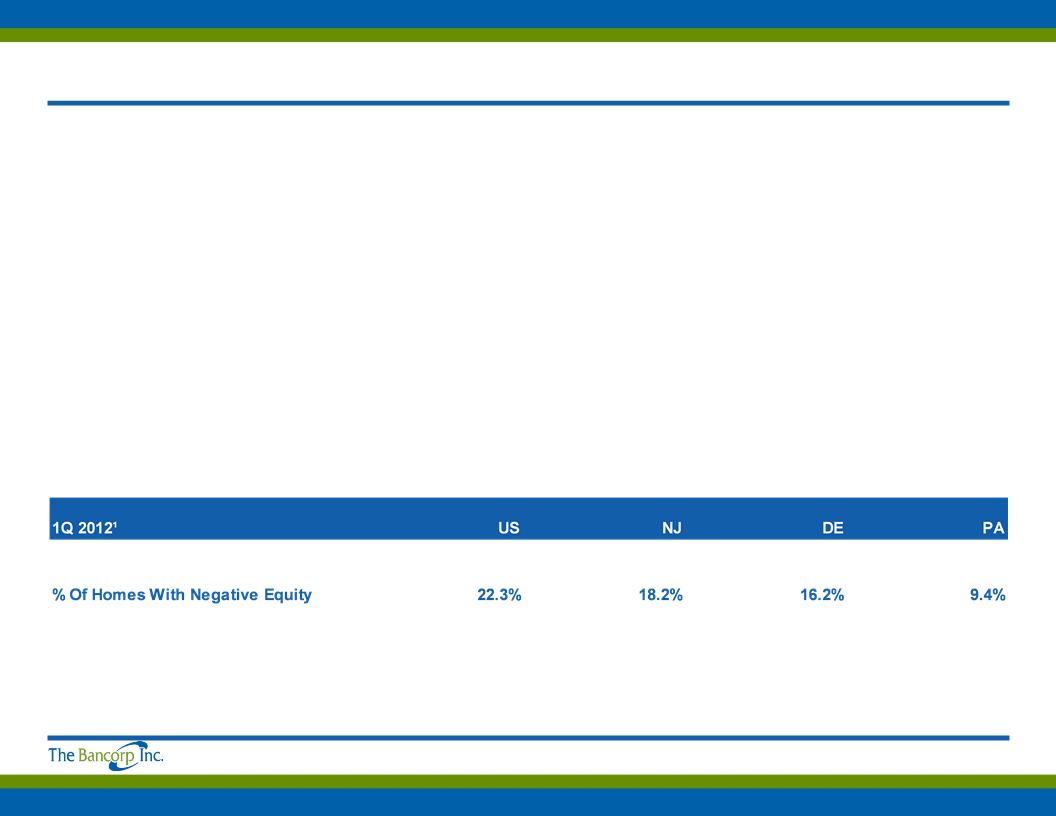

4 Throughout the current down cycle and in prior cycles, the Philadelphia region has exhibited significant stability,

which is reflected in a lower negative equity compared to the rest of the nation, as shown below.

which is reflected in a lower negative equity compared to the rest of the nation, as shown below.

Real Estate Lending Business Targets Attractive, Stable Markets

Source: Company documents

23

Non-GAAP Reconciliation

24

Source: Company filings

Post Provision Income Reconciliation

25

(1) 2011 includes a one-time gain of $718,000 related to a legal settlement

Source: Company filings

Adjusted Operating Earnings Reconcilement

26

Source: Company filings