Attached files

| file | filename |

|---|---|

| EX-1.1 - EXHIBIT 1.1 - PBF Energy Inc. | d445931dex11.htm |

| EX-5.1 - EXHIBIT 5.1 - PBF Energy Inc. | d445931dex51.htm |

| EX-23.4 - EXHIBIT 23.4 - PBF Energy Inc. | d445931dex234.htm |

| EX-23.1 - EXHIBIT 23.1 - PBF Energy Inc. | d445931dex231.htm |

| EX-23.2 - EXHIBIT 23.2 - PBF Energy Inc. | d445931dex232.htm |

| EX-23.3 - EXHIBIT 23.3 - PBF Energy Inc. | d445931dex233.htm |

Table of Contents

As filed with the Securities and Exchange Commission on December 3, 2012

Registration Statement No. 333-177933

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 7

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

PBF ENERGY INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 2911 | 45-3763855 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

One Sylvan Way, Second Floor

Parsippany, New Jersey 07054

Telephone: (973) 455-7500

(Name, address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Michael D. Gayda

President

PBF Energy Inc.

One Sylvan Way, Second Floor

Parsippany, New Jersey 07054

Telephone: (973) 455-7500

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Todd E. Lenson, Esq. | Jeffrey Dill, Esq. | William M. Hartnett, Esq. | ||

| Jordan M. Rosenbaum, Esq. |

PBF Energy Inc. | Douglas S. Horowitz, Esq. | ||

| Stroock & Stroock & Lavan LLP 180 Maiden Lane New York, New York 10038 Telephone: (212) 806-5400 |

Senior Vice President, General Counsel One Sylvan Way, Second Floor Parsippany, New Jersey 07054 Telephone: (973) 455-7500 |

Cahill Gordon & Reindel LLP 80 Pine Street New York, New York 10005 Telephone: (212) 701-3000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer ¨ | Accelerated Filer ¨ | Non-accelerated Filer þ | Smaller Reporting Company ¨ | |||

| (Do not check if a smaller reporting company) | ||||||

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title Of Each Class Of Securities To Be Registered |

Amount to be Registered(1) |

Proposed Maximum Aggregate Offering Price per Unit(2) |

Proposed Maximum Aggregate Offering Price(2) |

Amount of Registration fee | ||||

| Class A Common Stock, par value $0.001 per share |

18,975,000 | $27.00 | $512,325,000 | $67,702(3) | ||||

|

| ||||||||

|

| ||||||||

| (1) | Includes 2,475,000 shares of Class A common stock subject to underwriters’ option to purchase additional shares of Class A common stock. |

| (2) | Estimated solely for the purpose of determining the amount of the registration fee in accordance with Rule 457(o) under the Securities Act of 1933. |

| (3) | $11,460 of which has been previously paid. |

The Registrant hereby amends this registration statement on such date as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Prospectus (Subject to completion)

Issued December 3, 2012

16,500,000 Shares

Class A Common Stock

PBF Energy Inc. is offering shares of its Class A common stock. We intend to use a significant portion of the net proceeds from this offering to purchase equity interests in our business from certain of our existing owners. Prior to this offering, there has been no public market for our Class A common stock. The initial public offering price of our Class A common stock is expected to be between $25.00 and $27.00 per share.

Immediately following this offering, the holders of our Class A common stock will collectively own 100% of the economic interests in PBF Energy Inc., and have 17.2% of the voting power of PBF Energy Inc. The holders of our Class B common stock will have the remaining 82.8% of the voting power of PBF Energy Inc. As a result, we expect to be a “controlled company” within the meaning of the corporate governance standards of the New York Stock Exchange.

We have applied to list our Class A common stock on the New York Stock Exchange under the symbol “PBF”.

Investing in our Class A common stock involves risks. See “Risk Factors” beginning on page 17.

Price $ Per Share

| Price to Public |

Underwriting Discounts and Commissions |

Proceeds to Company | ||||

| Per Share |

$ | $ | $ | |||

| Total |

$ | $ | $ |

We have granted the underwriters a 30-day option to purchase up to 2,475,000 additional shares of Class A common stock on the same terms as set forth above. See the section of this prospectus entitled “Use of Proceeds” and “Underwriting.”

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities nor passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2012.

| Citigroup |

Morgan Stanley | |

| Credit Suisse |

Deutsche Bank Securities | |

| UBS Investment Bank | Barclays | Wells Fargo Securities | ||

| RBC Capital Markets | Credit Agricole CIB | BNP PARIBAS | Scotiabank / Howard Weil |

| Simmons & Company International | Santander | Tudor, Pickering, Holt & Co. | ||

Table of Contents

Until , 2012 (25 days after the commencement of this offering), all dealers that buy, sell or trade shares of our Class A common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

We have not authorized anyone to provide any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so.

For investors outside the United States: we have not and the underwriters have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of Class A common stock and the distribution of this prospectus outside the United States.

Unless otherwise indicated or the context otherwise requires, all financial data presented in this prospectus reflects the consolidated business and operations of PBF Energy Inc. and its consolidated subsidiaries, and has been prepared in accordance with generally accepted accounting principles in the United States of America, or GAAP.

i

Table of Contents

Unless otherwise noted or indicated by context, the following terms used in this prospectus have the following meanings:

“API gravity” refers to American Petroleum Institute gravity.

“ASCI” refers to the Argus Sour Crude Index, a pricing index used to approximate market prices for sour, heavy crude oil.

“Bakken” refers to both a crude oil production region generally covering North Dakota, Montana and Western Canada, and the crude oil that is produced in that region.

“barrel” refers to a common unit of measure in the oil industry, which equates to 42 gallons.

“blendstocks” refers to various compounds that are combined with gasoline or diesel from the crude oil refining process to make finished gasoline and diesel; these may include natural gasoline, FCC unit gasoline, ethanol, reformate or butane, among others.

“bpd” refers to an abbreviation for barrels per day.

“CAPP” refers to the Canadian Association of Petroleum Producers.

“catalyst” refers to a substance that alters, accelerates, or instigates chemical changes, but is not produced as a product of the refining process.

“CBOB” refers to conventional blendstock for oxygenate blending.

“coke” refers to a coal-like substance that is produced from heavier crude oil fractions during the refining process.

“complexity” refers to the number, type and capacity of processing units at a refinery, measured by the Nelson Complexity Index, which is often used as a measure of a refinery’s ability to process lower quality crude in an economic manner.

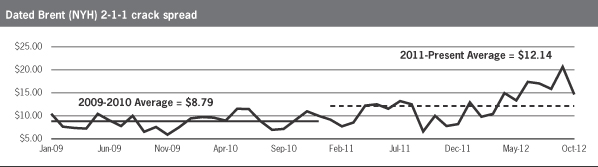

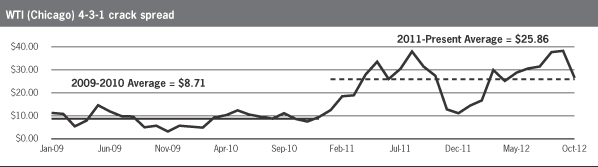

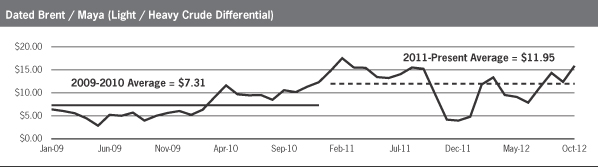

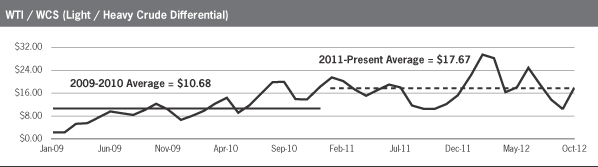

“crack spread” refers to a simplified calculation that measures the difference between the price for light products and crude oil. For example, we reference (a) the 2-1-1 crack spread, which is a general industry standard that approximates the per barrel refining margin resulting from processing two barrels of crude oil to produce one barrel of gasoline and one barrel of heating oil or ULSD, and (b) the 4-3-1 crack spread, which is a benchmark utilized by our Toledo refinery that approximates the per barrel refining margin resulting from processing four barrels of crude oil to produce three barrels of gasoline and one-half barrel of jet fuel and one-half barrel of ULSD.

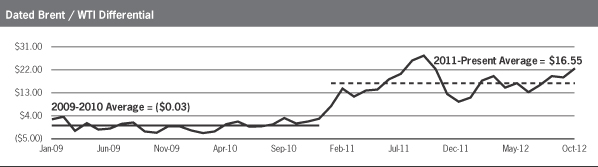

“Dated Brent” refers to Brent blend oil, a light, sweet North Sea crude oil, characterized by an API gravity of 38° and a sulfur content of approximately 0.4 weight percent that is used as a benchmark for other crude oils.

“distillates” refers primarily to diesel, heating oil, kerosene and jet fuel.

“downstream” refers to the downstream sector of the energy industry generally describing oil refineries, marketing and distribution companies that refine crude oil and sell and distribute refined products. The opposite of the downstream sector is the upstream sector, which refers to exploration and production companies that search for and/or produce crude oil and natural gas underground or through drilling or exploratory wells.

ii

Table of Contents

“EPA” refers to the United States Environmental Protection Agency.

“ethanol” refers to a clear, colorless, flammable oxygenated liquid. Ethanol is typically produced chemically from ethylene, or biologically from fermentation of various sugars from carbohydrates found in agricultural crops and cellulosic residues from crops or wood. It is used in the United States as a gasoline octane enhancer and oxygenate.

“feedstocks” refers to crude oil and partially refined petroleum products that are processed and blended into refined products.

“FCC” refers to fluid catalytic cracking.

“FCU” refers to fluid coking unit.

“FOB” refers to free on board, a transportation term that pertains to the port of loading. The buyer assumes responsibility for the goods at the port of loading and is responsible for freight transport, insurance, and any other costs associated with moving goods to their final destination port.

“GHG” refers to greenhouse gas.

“Group I base oils or lubricants” refers to conventionally refined products characterized by a sulfur content less than 0.03% with a viscosity index between 80 and 120. Typically, these products are used in a variety of automotive and industrial applications.

“heavy crude oil” refers to a relatively inexpensive crude oil with a low API gravity characterized by high relative density and viscosity. Heavy crude oils require greater levels of processing to produce high value products such as gasoline and diesel.

“KV” refers to Kilovolts.

“light crude oil” refers to a relatively expensive crude oil with a high API gravity characterized by low relative density and viscosity. Light crude oils require lower levels of processing to produce high value products such as gasoline and diesel.

“light products” refers to the group of refined products with lower boiling temperatures, including gasoline and distillates.

“light-heavy differential” refers to the price difference between light crude oil and heavy crude oil.

“LPG” refers to liquefied petroleum gas.

“Maya” refers to Maya crude oil, a heavy, sour crude oil characterized by an API gravity of approximately 22° and a sulfur content of approximately 3.3 weight percent that is used as a benchmark for other heavy crude oils.

“MLP” refers to master limited partnership.

“MMbbls” refers to an abbreviation for million barrels.

“MMBTU” refers to million British thermal units.

“MMSCFD” refers to million standard cubic feet per day.

“MSCG” refers to Morgan Stanley Capital Group Inc.

iii

Table of Contents

“MW” refers to Megawatt.

“Nelson Complexity Index” refers to the complexity of an oil refinery as measured by the Nelson Complexity Index, which is calculated on an annual basis by the Oil and Gas Journal. The Nelson Complexity Index assigns a complexity factor to each major piece of refinery equipment based on its complexity and cost in comparison to crude distillation, which is assigned a complexity factor of 1.0. The complexity of each piece of refinery equipment is then calculated by multiplying its complexity factor by its throughput ratio as a percentage of crude distillation capacity. Adding up the complexity values assigned to each piece of equipment, including crude distillation, determines a refinery’s complexity on the Nelson Complexity Index. A refinery with a complexity of 10.0 on the Nelson Complexity Index is considered ten times more complex than crude distillation for the same amount of throughput.

“NYH” refers to the New York Harbor market value of petroleum products.

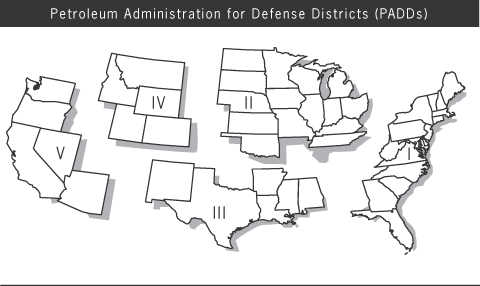

“PADD 1” refers to the Petroleum Administration for Defense District 1 region of the United States, which covers the following states: Connecticut, Delaware, District of Columbia, Florida, Georgia, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, North Carolina, Pennsylvania, Rhode Island, South Carolina, Vermont, Virginia and West Virginia.

“PADD 2” refers to the Petroleum Administration for Defense District 2 region of the United States, which covers the following states: Illinois, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, Oklahoma, South Dakota, Tennessee and Wisconsin.

“Platts” refers to Platts, a division of The McGraw-Hill Companies.

“PPM” refers to parts per million.

“RBOB” refers to reformulated blendstock for oxygenate blending.

“refined products” refers to petroleum products, such as gasoline, diesel and jet fuel, that are produced by a refinery.

“sour crude oil” refers to a crude oil that is relatively high in sulfur content, requiring additional processing to remove the sulfur. Sour crude oil is typically less expensive than sweet crude oil.

“Sunoco” refers to Sunoco, Inc. (R&M).

“sweet crude oil” refers to a crude oil that is relatively low in sulfur content, requiring less processing to remove the sulfur than sour crude oil. Sweet crude oil is typically more expensive than sour crude oil.

“Syncrude” refers to a blend of Canadian synthetic oil, a light, sweet crude oil, typically characterized by an API gravity between 30° and 32° and a sulfur content of approximately 0.1-0.2 weight percent.

“throughput” refers to the volume processed through a unit or refinery.

“turnaround” refers to a periodically required shutdown and comprehensive maintenance event to refurbish and maintain a refinery unit or units that involves the inspection of such units and occurs generally on a periodic cycle.

“ULSD” refers to ultra-low-sulfur diesel.

iv

Table of Contents

“WCS” refers to Western Canadian Select, a heavy, sour crude oil blend typically characterized by an API gravity between 20° and 22° and a sulfur content of approximately 3.5 weight percent that is used as a benchmark for heavy Western Canadian crude oil.

“WTI” refers to West Texas Intermediate crude oil, a light, sweet crude oil, typically characterized by an API gravity between 38° and 40° and a sulfur content of approximately 0.3 weight percent that is used as a benchmark for other crude oils.

“WTS” refers to West Texas Sour crude oil, a sour crude oil characterized by an API gravity between 30° and 33° and a sulfur content of approximately 1.28 weight percent that is used as a benchmark for other sour crude oils.

“yield” refers to the percentage of refined products that is produced from crude oil and other feedstocks.

v

Table of Contents

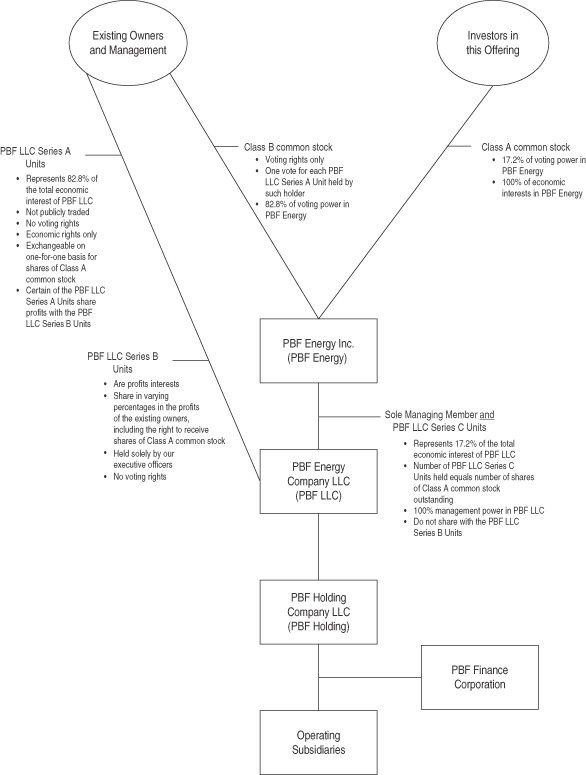

This summary highlights selected information contained elsewhere in this prospectus and may not contain all of the information that may be important to you. You should read this entire prospectus carefully, including the information set forth in “Risk Factors” and our financial statements and related notes included elsewhere in this prospectus before making an investment decision. In this prospectus, unless the context otherwise requires, references to the “Company,” “we,” “our,” “us” or “PBF” refer (1) prior to the consummation of the Offering Transactions described under “Organizational Structure—Offering Transactions,” to PBF Energy Company LLC, or PBF LLC, and its consolidated subsidiaries, including PBF Holding Company LLC, or PBF Holding, and (2) after the Offering Transactions described under “Organizational Structure—Offering Transactions,” to PBF Energy Inc., or PBF Energy, and, in each case, unless the context otherwise requires, its consolidated subsidiaries, including PBF LLC, PBF Holding, PBF Investments LLC, or PBF Investments, Toledo Refining Company LLC, or Toledo Refining, Paulsboro Refining Company LLC, or Paulsboro Refining, and Delaware City Refining Company LLC, or Delaware City Refining.

Our Company

We are one of the largest independent petroleum refiners and suppliers of unbranded transportation fuels, heating oil, petrochemical feedstocks, lubricants and other petroleum products in the United States. We were formed in 2008 to pursue acquisitions of crude oil refineries and downstream assets in North America. We currently own and operate three domestic oil refineries and related assets, which we acquired in 2010 and 2011. Our refineries have a combined processing capacity, known as throughput, of approximately 540,000 bpd, and a weighted average Nelson Complexity Index of 11.3.

Our three refineries are located in Toledo, Ohio, Delaware City, Delaware and Paulsboro, New Jersey. Our Midcontinent refinery at Toledo processes light, sweet crude, has a throughput capacity of 170,000 bpd and a Nelson Complexity Index of 9.2. The majority of Toledo’s WTI based crude is delivered via pipelines that originate in both Canada and the United States. Since our acquisition of Toledo in 2011, we have added additional truck and rail crude unloading capabilities that provide feedstock sourcing flexibility for the refinery and enables Toledo to run a more cost-advantaged crude slate. Our East Coast refineries at Delaware City and Paulsboro have a combined refining capacity of 370,000 bpd and Nelson Complexity Indices of 11.3 and 13.2, respectively. These high conversion refineries process primarily medium and heavy, sour crudes and have historically received the bulk of their feedstock via ships and barges on the Delaware River. Importantly, in May 2012 we commenced crude shipments via rail into a newly developed crude rail unloading facility at our Delaware City refinery. Currently, crude delivered to this facility is consumed at our Delaware City refinery. In the future we plan to transport some of the crude delivered by rail from Delaware City via barge to our Paulsboro refinery. The Delaware City rail unloading facility allows our East Coast refineries to source WTI based crudes from Western Canada and the Midcontinent, which provides significant cost advantages versus traditional Brent based international crudes. We are in the process of expanding the rail crude unloading capacity at Delaware City from 40,000 bpd to more than 110,000 bpd by early 2013 and have entered into agreements to lease approximately 2,400 crude railcars (comprised of approximately 1,600 coiled and insulated railcars that are capable of transporting Western Canadian bitumen without diluent and approximately 800 general purpose railcars) that are currently scheduled to be delivered through the second quarter of 2014 and which will be utilized to transport crude by rail to Delaware City.

Our Business

We produce a variety of products at each of our refineries, including gasoline, ULSD, heating oil, jet fuel, lubricants, petrochemicals and asphalt. We sell our products throughout the Northeast and Midwest of the United States, as well as in other regions of the United States and Canada, and are able to ship products to other international destinations. The majority of our finished products are sold through long-term offtake and supply agreements. For example, we sell the bulk of our gasoline, diesel and heating oil through long-term offtake agreements with MSCG and Sunoco.

1

Table of Contents

The following table provides summary operating information concerning each of our three refineries:

| Refinery |

Approximate Throughput Capacity (bpd) |

Nelson Complexity Index |

Estimated Replacement Cost |

Benchmark Crack Spread |

||||||||||

| Toledo |

170,000 | 9.2 | $ | 2.4 billion | |

WTI |

| |||||||

| (Chicago) 4-3-1 | ||||||||||||||

| Delaware City |

190,000 | 11.3 | $ | 3.1 billion | |

Dated Brent |

| |||||||

| (NYH) 2-1-1 | ||||||||||||||

| Paulsboro |

180,000 | 13.2 | $ | 2.7 billion | |

Dated Brent |

| |||||||

| (NYH) 2-1-1 | ||||||||||||||

|

|

|

|

|

|

||||||||||

| Total |

540,000 | 11.3 | $ | 8.2 billion | ||||||||||

| (weighted average) | ||||||||||||||

For the year ended December 31, 2011 and the nine months ended September 30, 2012, we had (a) pro forma total revenues of $16.0 billion and $15.2 billion, respectively; (b) pro forma Adjusted EBITDA of $480.7 million and $732.6 million, respectively; and (c) pro forma net income of $280.7 million and $503.3 million, respectively. Our pro forma results for the year ended December 31, 2011 do not include any adjustments for Delaware City to reflect incremental revenue and operating expenses that we expect to generate in connection with the re-start because the refinery was not operational when it was acquired and the transaction was accounted for as an acquisition of assets, not a business combination. For a definition and reconciliation of pro forma Adjusted EBITDA to pro forma net income, see “—Summary Historical and Pro Forma Financial and Other Data.”

Our History and Acquisitions

| March 2008 |

PBF was formed. | |

| June 2010 |

The idle Delaware City refinery and its related assets were acquired from Valero Energy Corporation, or Valero, for approximately $220.0 million. | |

| December 2010 |

The Paulsboro refinery was acquired from Valero for approximately $357.7 million, excluding working capital. | |

| March 2011 |

The Toledo refinery was acquired from Sunoco for approximately $400.0 million, excluding working capital. | |

| October 2011 |

Delaware City became operational. | |

Delaware City Acquisition and Re-Start. We acquired the idle Delaware City refinery and its related assets, including a petroleum product terminal, a petroleum products pipeline and an electric generation facility, on June 1, 2010 from affiliates of Valero for approximately $220.0 million in cash. In the fourth quarter of 2009, due to, among other reasons, financial losses caused by one of the worst recessions in recent history, the prior owner shut down the refinery. We were therefore able to acquire the refinery at an attractive price. In addition, at the time of acquisition, we reached an agreement with the State of Delaware that provided for a five-year operating permit and up to approximately $45.0 million of economic support to re-start the facility, and negotiated a new long-term contract with the relevant union at the refinery. We believe that the refinery’s ability to process lower quality crudes will allow us to capture a higher margin as these lower quality crudes are typically priced at discounts to benchmark crudes, and to compete effectively in a region where product demand significantly exceeds refining capacity.

Since our acquisition, we have invested more than $500.0 million in turnaround and re-start projects at Delaware City, as well as in the recent strategic development of a crude rail unloading facility. The re-start process

2

Table of Contents

included the decommissioning of the gasifier unit located on the property which allowed us to decrease emissions and improve the reliability of the refinery. We made significant operating improvements in the first year of operations by modifying the crude slate and product yield, changing operations of the conversion units and re-starting certain units. Through these capital investments and by restructuring certain operations, we have lowered the annual operating expenses of the Delaware City refinery relative to its pre-acquisition operating expense levels by more than 40%. During the first years of the refinery’s operations we anticipate saving in excess of $100.0 million in capital expenditures we otherwise would have expected to make if not for our reconfiguration of the refinery and the terms of our environmental operating agreement issued by the State of Delaware. In 2012, we are spending approximately $57.0 million, $20.0 million of which has been spent as of September 30, 2012, to expand and upgrade the existing on-site rail infrastructure, including the expansion of the crude rail unloading facilities that will be capable of discharging approximately 110,000 bpd.

Paulsboro Acquisition. We acquired the Paulsboro refinery (including an associated natural gas pipeline) on December 17, 2010 from Valero for approximately $357.7 million, excluding working capital. The purchase price excludes inventory purchased on our behalf by MSCG and Statoil Marketing & Trading (US) Inc., or Statoil.

Toledo Acquisition. We acquired the Toledo refinery on March 1, 2011 from Sunoco for approximately $400.0 million, excluding working capital. We also purchased refined and certain intermediate products in inventory for approximately $299.6 million, and MSCG purchased the refinery’s crude oil inventory on our behalf. Additionally, included in the terms of the sale is a five-year participation payment of up to $125.0 million payable to Sunoco based upon post-acquisition earnings of the refinery, of which $103.6 million was paid in 2012. We currently anticipate paying the balance of the participation payment in April 2013. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Pro Forma Contractual Obligations and Commitments” for additional information regarding the terms of the participation payment to Sunoco.

Industry Overview and Market Outlook

The United States has historically been the largest consumer of petroleum-based products in the world. According to the U.S. Energy Information Administration’s, or EIA’s, 2012 Refinery Capacity Report, there were 134 operating oil refineries in the United States in January 2012, with a total refining capacity of approximately 16.7 million bpd and a weighted average Nelson Complexity Index of approximately 10.9. Of the total operating refining capacity in the United States, approximately 55.2%, or 9.2 million bpd, is currently owned and operated by independent refining companies compared to 2002 when approximately 31.6%, or 5.1 million bpd, was owned by independent refining companies. The remaining capacity is controlled by integrated oil companies. Because of this trend, the refining industry increasingly must rely on its own operations for its profitability.

We believe our three refineries currently benefit from secular growth in North American crude production because of our ability to access lower cost WTI price based crudes. According to a recent EIA publication, average United States crude oil production in 2013 is expected to grow by approximately 1.5 million bpd, to 6.9 million bpd from 5.4 million bpd in 2009, an increase of approximately 28%. This level of United States crude oil production would represent the highest level since 1993. In addition, CAPP projects that Canadian crude oil production will increase by 800,000 bpd, from 3.0 million bpd in 2011 to 3.8 million bpd in 2015. As a result of the recent and projected growth in North American crude production, the United States has reduced its reliance on imported crude. The EIA estimates that crude imported from foreign sources (crude from outside North America) since 2008 has declined by approximately 1.3 million bpd or 13.3%, to 8.5 million bpd as of September 30, 2012 and is forecasted to decline by an additional 500,000 bpd by 2013. With the addition of our crude rail unloading facilities at Delaware City and our investment in a crude railcar fleet, we expect our East Coast refineries to capitalize on the growth in both Canadian and United States crude oil production, while maintaining the flexibility to source waterborne crude.

3

Table of Contents

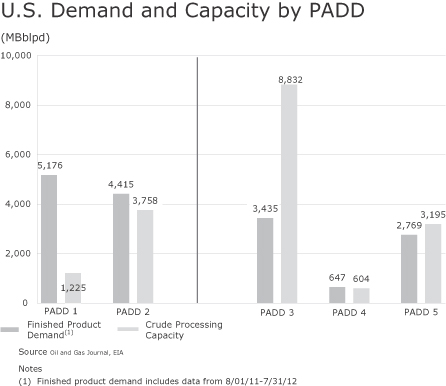

Supply and demand dynamics can vary by region, creating differentiated margin opportunities at any given time for refiners depending on the location of their facilities. Our Toledo refinery is located in the Midcontinent (PADD 2) and our Delaware City and Paulsboro refineries are both located on the East Coast (PADD 1). In both of these regions, product demand exceeds refinery capacity. We expect that this demand/capacity imbalance may continue. For example, since 2009 16 refineries representing approximately 2.6 million bpd of refining capacity have been closed or idled in the Atlantic Basin (which includes PADD 1). This Atlantic Basin reduction has occurred across the United States, Europe and the Caribbean and directly affects our East Coast refineries because we compete with operating refineries in these markets. In addition, the supply reduction provides opportunities to export products to markets formerly served by refineries that are now closed or idled outside of the United States.

Refining is primarily a margin-based business where both the feedstock (primarily crude oil) and refined petroleum products are commodities with fluctuating prices. Refiners create value by selling refined petroleum products at prices higher than the costs of acquiring crude oil and other feedstocks, and by managing operating costs. Refining is an industry that historically has seasonal influences as a result of differentiated consumer demand for key refined products during certain months of the year. Most importantly, demand for gasoline is generally higher during the summer months than during the winter months due to seasonal increases in highway traffic and construction work. Decreased demand during the winter months can lower gasoline prices. Consequently, refining margins and profitability have historically generally been stronger in the second and third calendar quarters of each year relative to the first and fourth calendar quarters.

Our Competitive Strengths

We believe that we have the following competitive strengths:

Strategically located refineries with cost and supply advantages. Our Midcontinent Toledo refinery advantageously sources a substantial portion of its WTI based crude slate from sources in Canada and throughout the Midcontinent. The balance of the crude oil is delivered by truck from local sources and by rail to a nearby terminal. Recent increases in production volumes of crudes from Western Canada and the Midcontinent combined with limitations on takeaway capacity in the Midcontinent, including at Cushing, Oklahoma where WTI is priced, have resulted in a price discount for WTI based crudes compared to Brent based crudes. We believe that our access to WTI based crudes at Toledo provides us with a cost advantage versus facilities that do not have similar access to such crudes and must process Brent based feedstocks.

Our Delaware City and Paulsboro refineries have similar supply advantages given that they have the flexibility to source crudes from around the world via the Delaware River, and can source currently price advantaged WTI based crudes from Western Canada and the Midcontinent through our Delaware City crude rail unloading facility and through third party rail unloading terminals on the East Coast. The 2,400 crude railcars that we have entered into agreements to lease will enable us to transport this crude to each of our refineries. This transportation flexibility allows our East Coast refineries to process the most cost advantaged crude available.

Our three refineries currently have access to inexpensive natural gas, a primary component of a refinery’s operating costs. This access provides us with a competitive advantage versus other refineries, such as those located in Europe and the Caribbean, that are forced to purchase more expensive natural gas or run fuel oil in the refining process.

Future crude supply may emerge from the development of other crude oil producing basins, including the Utica Shale play (located in portions of the Appalachian Basin and Canada), which could potentially bring significant oil production online in regional proximity to all three of our refineries, providing an attractive feedstock source with low associated transportation cost.

Complex assets with a valuable product slate located in high-demand regions. Our refinery assets are located in regions where product demand exceeds refining capacity. Our refineries have a weighted average

4

Table of Contents

Nelson Complexity Index of 11.3, which allows us the flexibility to process a variety of crudes. Our East Coast refineries have the highest Nelson Complexity Indices on the East Coast, allowing them to process lower cost, heavier, more sour crude oils and giving us a cost advantage over other refineries in the same region. The complexity of our refining assets allows us to produce a higher percentage of more valuable light products. For example, our East Coast refineries produce a greater percentage of distillates versus gasoline than other East Coast refineries and have 100% of the East Coast’s heavy coking capacity. In addition, our Paulsboro refinery produces Group I base oils which are typically priced at a premium to both gasoline and distillates. Similarly, our Toledo refinery is a high conversion refinery with high gasoline and distillate yields and also produces high-value petrochemical products.

Significant scale and diversification. We currently operate three refineries with a combined crude throughput of 540,000 bpd making us the fifth largest independent refiner in the United States. Our refineries provide us diversification through crude slates, end products, customers and geographic locations. Our scale provides us buying power advantages, and we benefit from the cost efficiencies that result from operating three large refineries.

Recent capital investments and restructuring initiatives to improve financial returns. Since 2006, over $2.8 billion of capital has been invested in our three refineries to improve their operating performance, to meet environmental and regulatory standards, and to minimize the need for near-term capital expenditures. For example, since our acquisition of Delaware City, we have invested more than $500.0 million in turnaround and re-start projects that will improve the cost structure and profitability of the refinery, as well as in the recent strategic development of a crude rail unloading facility. In addition, we are spending approximately $57.0 million to expand and upgrade the rail unloading infrastructure that will allow us to discharge more than 110,000 bpd of cost advantaged, WTI based crudes for both our Delaware City and Paulsboro refineries by the first quarter of 2013. In conjunction with the re-start of Delaware City in 2011, we undertook a significant restructuring of the operations to improve its operating cost position, including reductions in labor costs compared to operations before shutdown by Valero, reductions in energy costs and reductions in other ongoing operating and maintenance expenses. Management estimates that the Delaware City restructuring has reduced the refinery’s annual operating expenses by over $200.0 million relative to pre-acquisition operating expense level (without including the rail upgrades). We made significant operating improvements in the first year of operations by modifying the crude slate and product yield, changing operations of the conversion units and re-starting certain units.

Experienced management team with a demonstrated track record of acquiring, integrating and operating refining assets. Our management team is led by our Executive Chairman of the Board of Directors, Thomas D. O’Malley, who has more than 30 years experience in the refining industry and has led the acquisition of more than 20 refineries during his career. In addition, our executive management team, including our Chief Executive Officer, Thomas J. Nimbley, our President, Michael D. Gayda, and our head of Commercial Operations, Donald F. Lucey, has a proven track record of successfully operating refining assets. Our core management team has significant experience working together, including while at Tosco Corporation and Premcor Inc. These executives have a long history of acquiring refineries at attractive prices and integrating these operations into a single, consolidated platform. For example, we believe we acquired the Paulsboro, Delaware City and Toledo refineries at or near the bottom of the refining cycle at a small fraction of replacement cost. These acquisitions were made at lower prices on a per barrel basis and significantly lower prices on a complexity barrel basis than other comparable acquisitions over the past five years.

Support from strong financial sponsors and management with a substantial investment. Our financial sponsors, funds affiliated with The Blackstone Group L.P., or Blackstone, and First Reserve Management, L.P., or First Reserve, have a long history of successful investments across the energy industry. Together, our financial sponsors and management have invested substantial equity in PBF LLC to date, with management investing over $23.5 million. In addition, Thomas D. O’Malley, our Executive Chairman of the Board of Directors, certain of his affiliates and family

5

Table of Contents

members, and certain of our other executives, purchased $25.5 million aggregate principal amount of senior secured notes in the notes offering described under “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Factors Affecting Comparability—Senior Secured Notes Offering.”

Our Business Strategy

Our primary goal is to create stockholder value by improving our market position as one of the largest independent refiners and suppliers of petroleum products in the United States. We intend to execute the following strategies to achieve our goal:

Maintain efficient refinery operations. We intend to operate our refineries as reliably and efficiently as possible and further improve our operations by maintaining our costs at competitive levels, seeking to optimize utilization of our refinery asset base, and making focused high-return capital improvements designed to generate incremental profits.

We are continuously looking for ways to improve our overall operating efficiencies. For example, our refineries in Paulsboro and Delaware City are located approximately 30 miles apart from one another on the Delaware River. Both refineries have the capability to process heavy, sour crudes and have complementary operating units, and we exchange certain feedstocks and intermediates between the refineries in an effort to optimize profitability. We are able to recognize cost savings associated with the sharing of crude oil shipments for these refineries. In addition to allowing us to share crude cargoes transported to our East Coast refineries via water, the construction of our new crude rail unloading facility at Delaware City will also help us realize better crude economics, because we will be able to deliver crude via rail through our own facilities and process WTI based crudes at both Paulsboro and Delaware City. We employ a small, centralized corporate staff that provides capital control and oversight and have experienced managers making operational decisions at our refineries.

Continue to grow through acquisitions and internal projects. We believe that we will encounter attractive acquisition opportunities as a result of the continuing strategic divestitures by major integrated oil companies and the rationalization of specific refinery assets. In selecting future acquisitions and internal projects, we intend to consider, among other things, the following criteria: performance through the cycle, access to advantageous crude supplies, attractive refined product end market fundamentals, access to storage, distribution and logistics infrastructure, acquisition price and our ability to maintain a conservative capital structure, and synergies with existing assets. In addition, we own a number of energy-related logistical assets that qualify for the favorable tax treatment that is permitted through an MLP structure. We continue to evaluate our strategic alternatives for these assets.

Promote operational excellence in reliability and safety. We will continue to devote significant time and resources toward improving the reliability and safety of our operations. We will seek to improve operating performance through our commitment to our preventive maintenance program and to employee training and development programs. We will continue to emphasize safety in all aspects of our operations. We believe that a superior reliability record, which can be measured and managed like all other aspects of our business, is inherently tied to safety and profitability.

Create an organization highly motivated to maintain earnings and improve return on capital. We have created an organization in which employees are highly motivated to maintain earnings and improve return on capital. Our cash incentive compensation plan, which covers all non-unionized employees, is solely based on achieving earnings above designated levels. Our equity incentive plan provides participating employees with an equity stake in us and aligns their interests with our investors’ interests.

6

Table of Contents

Risk Factors

An investment in our Class A common stock involves a number of risks, including changes in industry-wide refining margins and crude oil price differentials, competition and other material factors, that could materially affect our business, financial condition and results of operations, and cause the trading price of our Class A common stock to decline. For a discussion of these risks and other considerations that could negatively affect us, including risks related to this offering and our Class A common stock, see “Risk Factors” and “Forward-Looking Statements.”

Corporate Structure and Financial Sponsors

Following this offering we will be a holding company and our sole asset will be an equity interest in PBF LLC. See “Organizational Structure” on page 40.

We will be the sole managing member of PBF LLC and operate and control all of the business and affairs and consolidate the financial results of PBF LLC and its subsidiaries. PBF LLC is a holding company for the companies that directly or indirectly own and operate our business. Prior to this offering, each of Blackstone and First Reserve owned approximately 48% of the outstanding capital interests in PBF LLC (which we refer to as the “PBF LLC Series A Units”), and Mr. O’Malley, our other executive officers and directors and certain employees beneficially owned the remaining outstanding PBF LLC Series A Units (we refer to all of the holders of the PBF LLC Series A Units as “our existing owners”). In addition, certain of our officers hold interests in PBF LLC, which are profits interests (which we refer to as the “PBF LLC Series B Units”) and certain of our existing owners and other employees hold options and warrants to purchase PBF LLC Series A Units.

Immediately prior to this offering, the limited liability company agreement of PBF LLC will be amended and restated to, among other things, designate PBF Energy as the sole managing member of PBF LLC and establish a new series of membership interests (which we refer to as the “PBF LLC Series C Units”) which will be held solely by PBF Energy. The PBF LLC Series A Units will be held solely by our existing owners (and their permitted transferees). The PBF LLC Series C Units rank on a parity with the PBF LLC Series A Units as to distribution rights, voting rights and rights upon liquidation, winding up or dissolution. Profits and losses of PBF LLC will be allocated, and all distributions generally will be made, pro rata to the holders of PBF LLC Series A Units and PBF LLC Series C Units.

The PBF LLC Series B Units are profits interests held by certain of our officers which had no taxable value at the date of issuance, have no voting rights and are designed to increase in value only after our financial sponsors achieve certain levels of return on their investment in PBF LLC Series A Units. Under the limited liability company agreement of PBF LLC, distributions initially are made to the holders of PBF LLC Series A Units and PBF LLC Series C Units in proportion to the number of units owned by them. Once the financial sponsors receive a full return of their capital contributions with respect to their PBF LLC Series A Units, distributions and other payments made on account of the PBF LLC Series A Units held by our financial sponsors will then be shared by our financial sponsors with the holders of PBF LLC Series B Units. Accordingly, the amounts paid to the holders of PBF LLC Series B Units will reduce only the amounts otherwise payable to the PBF LLC Series A Units held by our financial sponsors, and will not reduce or otherwise impact any amounts payable to PBF Energy (the holder of our PBF LLC Series C Units), the holders of our Class A common stock or any other holder of PBF LLC Series A Units. For a further discussion of the PBF LLC Series B Units, please see “Executive Compensation—Compensation Discussion and Analysis—Summary of PBF LLC Series B Units.”

We also will enter into an exchange agreement pursuant to which our existing owners will have the right to cause PBF LLC to exchange their PBF LLC Series A Units for shares of our Class A common stock on a one-for-one basis, subject to equitable adjustments for stock splits, stock dividends and reclassifications, and

7

Table of Contents

further subject to the rights of the holders of PBF LLC Series B Units to share in a portion of the profits realized by our financial sponsors upon the sale of the shares of Class A common stock received by them upon such exchange.

Blackstone. Blackstone is one of the world’s leading investment and advisory firms and is an experienced and active investor in the energy and natural resources sector. Blackstone has substantial prior experience as an acquiror and owner of petroleum refineries, having acquired Premcor in 1997 and overseen several acquisitions and capital projects to expand and upgrade refining capacity of that company until its acquisition by Valero in 2005 for total consideration of approximately $6.9 billion. Blackstone has a long-standing relationship with Thomas D. O’Malley, having recruited him to serve as Chairman and Chief Executive Officer of Premcor in early 2002. Blackstone seeks to create positive economic impact and long-term value for its investors, the companies it invests in, the companies it advises and the broader global economy. Blackstone does this through the commitment of its extraordinary people and flexible capital. Blackstone’s alternative asset management businesses include the management of private equity funds, real estate funds, hedge fund solutions, credit-oriented funds and closed-end mutual funds. Through its different investment businesses, as of September 30, 2012, Blackstone had total assets under management of approximately $204.6 billion. Blackstone also provides various financial advisory services, including financial and strategic advisory, restructuring and reorganization advisory and fund placement services.

First Reserve. Founded in 1983, First Reserve is a leading global investment firm dedicated to the energy industry with over $23 billion of raised capital since inception. With offices in North America, Europe and Asia, First Reserve is well positioned to make strategic investments on a global basis across the energy value chain. First Reserve seeks to create value for its investors by applying its deep industry knowledge, decades of investing and operational experience, highly talented management team and powerful network of global relationships to its investments and through active monitoring of its portfolio companies.

* * *

PBF Energy is a Delaware corporation incorporated on November 7, 2011 with its principal executive offices located at One Sylvan Way, Second Floor, Parsippany, NJ 07054 and our telephone number is (973) 455-7500. Our website address is http://www.pbfenergy.com. The information on our website is not part of this prospectus.

8

Table of Contents

The Offering

| Class A common stock to be offered by PBF Energy |

16,500,000 shares |

| Over-allotment option |

2,475,000 shares |

| Class A common stock outstanding after the offering |

16,500,000 shares (or 95,676,893 shares if all outstanding PBF LLC Series A Units held by our existing owners were exchanged for newly-issued shares of Class A common stock on a one-for-one basis). |

| Class B common stock outstanding after the offering |

37 shares, or one share for each holder of PBF LLC Series A Units. |

| Voting power held by holders of Class A common stock after the offering |

17.2% (or 100% if all outstanding PBF LLC Series A Units held by our existing owners were exchanged for newly-issued shares of Class A common stock on a one-for-one basis). |

| Voting power held by holder of Class B common stock after the offering |

82.8% (or 0% if all outstanding PBF LLC Series A Units held by our existing owners were exchanged for newly issued shares of Class A common stock on a one-for-one basis). |

| Use of proceeds |

The proceeds to PBF Energy from this offering, before deducting underwriting discounts, will be approximately $429.0 million (or $493.4 million if the underwriters exercise in full their option to purchase additional shares of Class A common stock). |

| PBF Energy intends to use $390.0 million of the proceeds from this offering (or $454.4 million if the underwriters exercise in full their option to purchase additional shares of Class A common stock), to purchase PBF LLC Series A Units (which will be reclassified as PBF LLC Series C Units in connection with such acquisition) from Blackstone and First Reserve, as described under “Organizational Structure—Offering Transactions.” Accordingly, we will not retain any of these proceeds. See “Principal Stockholders” for further information. |

| PBF Energy intends to use all of the remaining proceeds from this offering, or $39.0 million, to purchase newly-issued PBF LLC Series C Units from PBF LLC, as described under “Organizational Structure—Offering Transactions.” We intend to cause PBF LLC to use these proceeds to pay the expenses of |

9

Table of Contents

| this offering, including aggregate underwriting discounts of $21.5 million (or $24.7 million if the underwriters exercise in full their option to purchase additional shares of Class A common stock) and other offering expenses estimated at $7.8 million. Any remaining proceeds will be used for general corporate purposes, including to potentially repay amounts outstanding under our ABL Revolving Credit Facility. See “Use of Proceeds.” |

| Voting rights |

Each share of our Class A common stock entitles its holder to one vote on all matters to be voted on by stockholders generally. |

| Our existing owners hold all of the shares of Class B common stock. The shares of Class B common stock have no economic rights but entitle the holder, without regard to the number of shares of Class B common stock held, to a number of votes on matters presented to stockholders of PBF Energy that is equal to the aggregate number of PBF LLC Series A Units held by such holder. See “Description of Capital Stock—Class B Common Stock.” |

| Holders of our Class A common stock and Class B common stock vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise required by applicable law. |

| Dividend policy |

We currently intend to pay quarterly cash dividends of approximately $0.20 per share on our Class A common stock following this offering, commencing after the completion of the first quarter of 2013. The declaration, timing and amount of any such dividends will be at the sole discretion of our board of directors and will depend on a variety of factors, including general economic conditions, our financial condition and operating results, our available cash and current and anticipated cash needs, capital requirements, plans for expansion, tax, legal, regulatory and contractual restrictions and implications, including under our outstanding debt documents, and such other factors as our board of directors may deem relevant. |

| Because we are a holding company, our cash flow and ability to pay dividends depends upon the financial results and cash flows of our operating subsidiaries and the distribution or other payment of cash to us in the form of dividends or otherwise from PBF LLC. |

10

Table of Contents

| Exchange rights of our existing owners |

Prior to this offering, we will enter into an exchange agreement pursuant to which our existing owners will have the right to cause PBF LLC to exchange their PBF LLC Series A Units for shares of Class A common stock of PBF Energy on a one-for-one basis, subject to equitable adjustment for stock splits, stock dividends and reclassifications, and further subject to the rights of the holders of PBF LLC Series B Units to share in a portion of the profits realized by our financial sponsors upon the sale of the shares of Class A common stock received by them upon such exchange. |

Under the amended and restated certificate of incorporation of PBF Energy, each holder of Class B common stock will be entitled, without regard to the number of shares of Class B common stock held by such holder, to one vote for each PBF LLC Series A Unit held by such holder. Accordingly, as our existing owners exchange their PBF LLC Series A Units for shares of Class A common stock pursuant to the exchange agreement, the voting power afforded to our existing owners by their shares of Class B common stock will be automatically and correspondingly reduced.

| Directed Share Program |

At our request, the underwriters have reserved up to 412,500 shares of our Class A common stock offered hereby for sale to certain of our employees and certain other participants. We do not know if these persons will choose to purchase all or any portion of these reserved shares, but any purchases they do make will reduce the number of shares available to the general public. See “Risk Factors—Risks Related to This Offering and Ownership of Our Class A Common Stock—Certain participants in our directed share program must hold their shares for a minimum of 180 days following the date of the final prospectus related to this offering and accordingly will be subject to market risks not imposed on other investors in the offering” and “Underwriting.” |

| Risk factors |

For a discussion of factors you should consider before buying the shares, see “Risk Factors.” |

| New York Stock Exchange symbol |

“PBF” |

11

Table of Contents

Unless we specifically state otherwise, all information in this prospectus:

| • | assumes no exercise by the underwriters of their over-allotment option to purchase 2,475,000 additional shares of our Class A common stock; |

| • | does not reflect 79,176,893 shares (or 76,701,893 shares if the underwriters exercise in full their option to purchase additional shares of Class A common stock) of Class A common stock issuable upon exchange of PBF LLC Series A Units outstanding immediately following this offering; and |

| • | excludes (a) outstanding options and warrants to purchase 2,181,230 PBF LLC Series A Units, at a weighted average exercise price of $10.24 per unit, 1,586,210 of which will be vested and exercisable as of the date of the closing of this offering, and (b) an additional 5,000,000 shares authorized and reserved for issuance under our equity incentive plan, including 675,000 shares issuable upon the exercise of stock options that we intend to grant to our officers and employees at the time of this offering. See “Executive Compensation — Compensation Discussion and Analysis — Equity Compensation,” “Executive Compensation — Compensation Discussion and Analysis — 2012 Equity Incentive Plan,” “Executive Compensation — Compensation Discussion and Analysis — IPO Date Stock Option Awards and Cash Bonus to Employees” and “Certain Relationships and Related Transactions — Investments in PBF LLC.” |

12

Table of Contents

Summary Historical and Pro Forma Financial and Other Data

The following table sets forth our summary historical and pro forma consolidated financial data at the dates and for the periods indicated. The historical financial data is that of PBF LLC. PBF LLC will be considered our predecessor for accounting purposes, and its consolidated financial statements will be our historical consolidated financial statements following this offering.

The summary historical consolidated financial data as of December 31, 2010 and 2011 and for the years ended December 31, 2009, 2010 and 2011 have been derived from audited financial statements of PBF LLC included elsewhere in this prospectus. The summary historical consolidated financial data as of December 31, 2009 has been derived from audited financial statements of PBF LLC not included in this prospectus. As a result of the Paulsboro and Toledo acquisitions, the historical consolidated financial results of PBF LLC only include the results of operations for Paulsboro and Toledo from December 17, 2010 and March 1, 2011, respectively. The information as of and for the nine months ended September 30, 2011 and 2012 was derived from the unaudited condensed consolidated financial statements of PBF LLC (included elsewhere in this prospectus) which include all adjustments, consisting of normal recurring adjustments, which management considers necessary for a fair presentation of the financial position and the results of operations for such periods. Results for the interim periods are not necessarily indicative of the results for the full year.

The summary unaudited pro forma consolidated financial data have been derived by the application of pro forma adjustments to the historical consolidated financial statements of PBF LLC included elsewhere in this prospectus. The summary unaudited pro forma consolidated statements of operations data for the year ended December 31, 2011 and for the nine months ended September 30, 2012 give effect to the acquisition of Toledo, the senior secured notes offering (as described under “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Factors Affecting Comparability—Senior Secured Notes Offering”), the Offering Transactions (as described under “Organizational Structure”), and the use of the estimated net proceeds from this offering as if they had occurred on January 1, 2011. The summary unaudited pro forma consolidated balance sheet data as of September 30, 2012 gives effect to cash distributions to our existing owners made prior to the completion of this offering (as described under “Dividend Policy”), the Offering Transactions and the use of the estimated net proceeds from this offering as if they had occurred on September 30, 2012.

You should read this information in conjunction with the consolidated financial statements of PBF LLC and the related notes thereto, and the statements of assets acquired and liabilities assumed and the related statements of revenues and direct expenses of Toledo and the related notes thereto, included elsewhere in this prospectus, and the sections entitled “Organizational Structure,” “Unaudited Pro Forma Consolidated Financial Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Selected Financial Data.” Our summary unaudited pro forma consolidated financial information is presented for informational purposes only. The pro forma adjustments are based upon available information and certain assumptions that we believe are reasonable. Our summary unaudited pro forma consolidated financial information does not purport to represent what our results of operations or financial position would have been if we operated as a public company during the periods presented and may not be indicative of our future performance.

13

Table of Contents

| Year Ended December 31, 2009(3) |

Year Ended December 31, 2010 |

Pro Forma | Nine Months Ended September 30, 2011 |

Nine Months Ended September 30, 2012 |

Pro Forma | |||||||||||||||||||||||

| Year Ended December 31, 2011 |

Year Ended December 31, 2011 |

Nine Months Ended September 30, 2012 |

||||||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||||

| Statement of operations data: |

||||||||||||||||||||||||||||

|

Revenues(1) |

$ | 228 | $ | 210,671 | $ | 14,960,338 | $ | 15,961,529 | $ | 10,183,897 | $ | 15,188,327 | $ | 15,188,327 | ||||||||||||||

| Cost and expenses |

||||||||||||||||||||||||||||

| Cost of sales, excluding depreciation |

— | 203,971 | 13,855,163 | 14,719,566 | 9,147,063 | 13,871,884 | 13,871,884 | |||||||||||||||||||||

| Operating expenses, excluding depreciation |

— | 25,140 | 658,831 | 699,557 | 457,722 | 537,880 | 537,880 | |||||||||||||||||||||

| General and administrative expenses |

6,294 | 15,859 | 86,183 | 89,857 | 71,533 | 78,042 | 78,042 | |||||||||||||||||||||

| Acquisition related expenses(2) |

— | 6,051 | 728 | 172 | 684 | — | — | |||||||||||||||||||||

| (Gain) on sale of asset |

— | (2,430 | ) | (2,430 | ) | |||||||||||||||||||||||

| Depreciation and amortization expense |

44 | 1,402 | 53,743 | 57,952 | 35,636 | 67,419 | 67,419 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| 6,338 | 252,423 | 14,654,648 | 15,567,104 | 9,712,638 | 14,552,795 | 14,552,795 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (Loss) income from operations |

(6,110 | ) | (41,752 | ) | 305,690 | 394,425 | 471,259 | 635,532 | 635,532 | |||||||||||||||||||

| Other (expense) income |

||||||||||||||||||||||||||||

| Change in fair value of catalyst lease obligation |

— | (1,217 | ) | 7,316 | 7,316 | 4,848 | (6,929 | ) | (6,929 | ) | ||||||||||||||||||

| Change in fair value of contingent consideration |

— | — | (5,215 | ) | (5,215 | ) | (4,829 | ) | (2,076 | ) | (2,076 | ) | ||||||||||||||||

| Interest income (expense), net |

10 | (1,388 | ) | (65,120 | ) | (95,603 | ) | (44,127 | ) | (86,753 | ) | (86,892 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (Loss) income before taxes |

(6,100 | ) | (44,357 | ) | 242,671 | 300,923 | 427,151 | 539,774 | 539,635 | |||||||||||||||||||

| Income taxes |

— | — | — | 20,239 | — | — | 36,295 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net (loss) income |

$ | (6,100 | ) | $ | (44,357 | ) | $ | 242,671 | 280,684 | $ | 427,151 | $ | 539,774 | 503,340 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Less—Net (loss) income attributable to noncontrolling interest |

249,027 | 446,572 | ||||||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||||||

| Net (loss) income attributable to PBF Energy Inc. |

$ | 31,657 | $ | 56,768 | ||||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||||||

| Balance sheet data (at end of period): |

||||||||||||||||||||||||||||

| Total assets |

$ | 19,150 | $ | 1,274,393 | $ | 3,621,109 | $ | 3,611,186 | $ | 3,872,150 | $ | 3,932,507 | $ | 3,909,103 | ||||||||||||||

| Total long-term debt(4) |

— | 325,064 | 804,865 | 824,260 | 713,255 | 732,961 | 732,961 | |||||||||||||||||||||

| Total equity |

18,694 | 456,739 | 1,107,615 | 936,700 | 1,296,131 | 1,633,326 | 1,467,888 | |||||||||||||||||||||

| Selected financial data: |

||||||||||||||||||||||||||||

| Adjusted EBITDA(5) |

$ | (6,066 | ) | $ | (28,699 | ) | $ | 388,219 | $ | 480,666 | $ | 507,070 | $ | 732,603 | $ | 732,603 | ||||||||||||

| Capital expenditures(6) |

$ | 70 | $ | 72,118 | $ | 551,544 | $ | 551,544 | $ | 504,034 | $ | 129,505 | $ | 129,505 | ||||||||||||||

| (1) | Consulting services income provided to a related party was $10 and $221 for the years ended December 31, 2010 and 2009, respectively. No consulting services income was earned subsequent to 2010. |

| (2) | Acquisition related expenses consist of consulting and legal expenses related to the Paulsboro and Toledo acquisitions as well as non-consummated acquisitions. |

| (3) | December 31, 2009 balance sheet data is that of PBF Investment LLC. See footnote 1, Description of Business and Basis of Presentation, in the PBF LLC consolidated financial statements. |

| (4) | Total long-term debt includes current maturities and our Delaware Economic Development Authority loan of $20.0 million. |

| (5) | We believe Adjusted EBITDA is an important measure of operating performance and provides useful information to investors because it highlights trends in our business that may not otherwise be apparent when relying solely on GAAP measures and eliminates items that have less bearing on our operating performance. |

14

Table of Contents

| Adjusted EBITDA, as presented herein, is a supplemental measure of performance that is not required by, or presented in accordance with, GAAP. We use this non-GAAP financial measure as a supplement to our GAAP results in order to provide a more complete understanding of the factors and trends affecting our business. Adjusted EBITDA is a measure of operating performance that is not defined by GAAP and should not be considered a substitute for net income as determined in accordance with GAAP. |

| Also, because Adjusted EBITDA is not calculated in the same manner by all companies, it is not necessarily comparable to other similarly titled measures used by other companies. Adjusted EBITDA has its limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of the limitations of Adjusted EBITDA are: |

| • | Adjusted EBITDA does not reflect our cash expenditures, or future requirements, for capital expenditures or contractual commitments; |

| • | Although depreciation and amortization are non-cash charges, the asset being depreciated or amortized often will have to be replaced and Adjusted EBITDA does not reflect the cash requirements for such replacements; |

| • | Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital requirements; and |

| • | Adjusted EBITDA does not reflect the significant interest expense, or the cash requirements necessary to make payments of interest or principal on our indebtedness. |

The following table reconciles net income (loss) (or, on a pro forma basis, net income attributable to PBF Energy Inc.) to Adjusted EBITDA:

| Pro Forma | Pro Forma | |||||||||||||||||||||||||||

| Year Ended December 31, 2009 |

Year Ended December 31, 2010 |

Year Ended December 31, 2011 |

Year Ended December 31, 2011 |

Nine Months Ended September 30, 2011 |

Nine Months Ended September 30, 2012 |

Nine Months Ended September 30, 2012 |

||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||||

| Net income (loss) |

$ | (6,100 | ) | $ | (44,357 | ) | $ | 242,671 | $ | 280,684 | (f) | $ | 427,151 | $ | 539,774 | $ | 503,340 | (g) | ||||||||||

| Income taxes |

— | — | — | 20,239 | — | — | 36,295 | |||||||||||||||||||||

| Interest (income) expense, net |

(10 | ) | 1,388 | 65,120 | 95,662 | 44,127 | 86,753 | 86,892 | ||||||||||||||||||||

| Depreciation and amortization |

44 | 1,402 | 53,743 | 57,952 | 35,636 | 67,419 | 67,419 | |||||||||||||||||||||

| Stock-based compensation |

— | 2,300 | 2,516 | 2,516 | 1,911 | 1,707 | 1,707 | |||||||||||||||||||||

| Acquisition related expense(a) |

— | 6,051 | 728 | |

172 |

|

684 | — | — | |||||||||||||||||||

| Non-cash change in market value of inventory repurchase obligation(b) |

— | 2,043 | 18,771 | 18,771 | (4,932 | ) | 9,716 | 9,716 | ||||||||||||||||||||

| Non-cash deferral of gross profit on finished product sales(c) |

— | 1,257 | 6,771 | 6,771 | 2,512 | 18,229 | 18,229 | |||||||||||||||||||||

| Change in fair value of catalyst lease obligations(d) |

— | 1,217 | (7,316 | ) | (7,316 | ) | (4,848 | ) | 6,929 | 6,929 | ||||||||||||||||||

| Change in fair value of contingent consideration(e) |

— | — | 5,215 | 5,215 | 4,829 | 2,076 | 2,076 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Adjusted EBITDA |

$ | (6,066 | ) | $ | (28,699 | ) | $ | 388,219 | $ | 480,666 | $ | 507,070 | $ | 732,603 | $ | 732,603 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (a) | See footnote (2) above. |

| (b) | Certain of our crude and feedstock supply agreements require that we repurchase inventory held by our counterparties at a future date at the then fair market value. We are required to record these repurchase obligations at their fair market value at the end of each reporting period. The change in fair market value based on changes in commodity prices is a non-cash charge or benefit included in cost of sales. We add back the impact of the change in market value of these future inventory repurchase obligations in arriving at Adjusted EBITDA to better reflect Adjusted EBITDA on a cash-basis. |

| (c) | We sell our production of light finished products at our Paulsboro and Delaware City refineries to a single counterparty. On a daily basis, the counterparty purchases and pays for the products as they are produced, delivered to the refineries’ storage tanks, and legal title passes to the counterparty. Revenue and gross profit on these product sales are deferred until the products are shipped out of our storage facility, which typically occurs within an average of six days. We add back the non-cash deferral of the gross profit on these product sales in arriving at Adjusted EBITDA to better reflect Adjusted EBITDA on a cash-basis. |

15

Table of Contents

| (d) | We entered into agreements pursuant to which certain precious metals catalyst located at our Delaware City and Toledo refineries were sold and leased back for three one-year periods. We have recorded these transactions as capital leases as we are required to repurchase the precious metals catalyst at its market value at lease termination. We elected the fair value option for accounting for the catalyst repurchase obligations and the change in fair value of the underlying precious metals is recorded in the income statement as a non-cash charge or benefit each reporting period. We add back the impact of the change in fair value of these future precious metal catalyst repurchase obligations in arriving at Adjusted EBITDA to better reflect Adjusted EBITDA on a cash-basis. |

| (e) | In connection with the Toledo acquisition, the seller will be paid an amount equal to 25% of the amount by which the purchased assets’ EBITDA exceeds $125.0 million in a given calendar year through 2016 (pro-rated for 2011 and 2016). The aggregate amount of such payments cannot exceed $125.0 million. The purchased assets’ EBITDA is calculated using calendar year earnings we have earned solely from the purchase of Toledo including reasonable direct and allocated overhead expenses, less any significant extraordinary or non-recurring expenses, and any fees or expenses incurred by us in connection with the Toledo acquisition. A charge or benefit is recorded each reporting period reflecting the change in the estimated fair value of the contingent consideration we expect to pay in connection with our acquisition of the Toledo refinery. We add back the impact of the change in fair value of the contingent consideration in arriving at Adjusted EBITDA to better reflect Adjusted EBITDA on a cash-basis. |

| (f) | Includes net income attributable to PBF Energy Inc. of $31,657 and net income attributable to noncontrolling interests of $249,027. |

| (g) | Includes net income attributable to PBF Energy Inc. of $56,768 and net income attributable to noncontrolling interests of $446,572. |

| (6) | Includes expenditures for construction in progress, property, plant and equipment and deferred turnaround costs. |

16

Table of Contents

An investment in our Class A common stock involves a number of risks. You should carefully consider, in addition to the other information contained in this prospectus (including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes), the following risks before investing in our Class A common stock. These risks could materially affect our business, financial condition and results of operations, and cause the trading price of our Class A common stock to decline. You could lose part or all of your investment. You should bear in mind, in reviewing this prospectus, that past experience is no indication of future performance. You should read the section titled “Forward-Looking Statements” immediately following these risk factors for a discussion of what types of statements are forward-looking statements, as well as the significance of such statements in the context of this prospectus.

Risks Relating to Our Business and Industry

We have incurred losses in the past and may incur losses in the future. If we incur losses over an extended period of time, the value of our Class A common stock could decline.