Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - BUCKEYE PARTNERS, L.P. | d448068d8k.htm |

Wells Fargo

Securities 11

Annual

Pipeline,

MLP

and

Energy

Symposium

December 4, 2012

©

Copyright 2012 Buckeye Partners, L.P.

Exhibit 99.1

th |

LEGAL

NOTICE/FORWARD-LOOKING STATEMENTS ©

Copyright 2012 Buckeye Partners, L.P.

2

This presentation contains “forward-looking statements” that we believe to be

reasonable as of the date of this presentation. These statements, which include

any statement that does not relate strictly to historical facts, use terms such as “anticipate,” “assume,” “believe,” “estimate,”

“expect,” “forecast,” “intend,” “plan,”

“position,” “predict,” “project,” or “strategy” or the negative connotation or other variations of such terms

or other similar terminology. In particular, statements, express or implied, regarding

future results of operations or ability to generate sales, income or cash flow, to make

acquisitions, or to make distributions to unitholders are forward-looking statements. These forward-looking

statements are based on management’s current plans, expectations, estimates, assumptions

and beliefs concerning future events impacting Buckeye Partners, L.P. (the

“Partnership” or “BPL”) and therefore involve a number of risks and uncertainties, many of which are beyond

management’s control. Although the Partnership believes that its expectations

stated in this presentation are based on reasonable assumptions, actual results may

differ materially from those expressed or implied in the forward-looking statements. The factors listed in the “Risk Factors”

sections of, as well as any other cautionary language in, the Partnership’s public

filings with the Securities and Exchange Commission, provide examples of risks,

uncertainties and events that may cause the Partnership’s actual results to differ materially from the expectations it describes

in its forward-looking statements. Each forward-looking statement speaks only as

of the date of this presentation, and the Partnership undertakes no obligation to

update or revise any forward-looking statement.

|

INVESTMENT

HIGHLIGHTS •

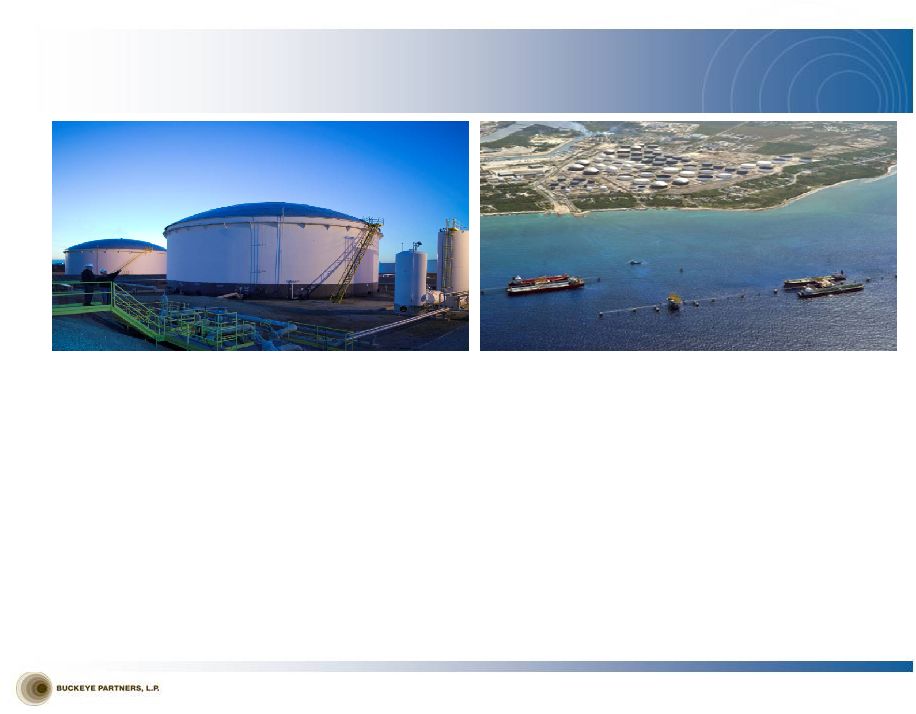

Over 125 years of continuous operations, with a 26-year track record as a publicly traded

MLP on the NYSE

•

Market capitalization near $5.0 billion

•

Lower cost of capital realized from elimination of GP IDRs

•

Investment grade credit rating with a conservative approach toward financing growth

•

Increased

geographic

and

product

diversity

resulting

from

recent

acquisitions

•

Growth opportunities to unlock significant value from acquisition of assets from

major

petroleum

companies

-

“Terminal

Franchise”

•

Opportunities

for

significant

internal

growth

projects

on

legacy

and

recently

acquired

assets

•

Paid cash distributions each quarter since formation in 1986

Petroleum storage tanks at our Macungie terminal in Pennsylvania

Aerial view of BORCO’s six offshore jetties with tank farm in the distance

©

Copyright 2012 Buckeye Partners, L.P.

3 |

MANAGEMENT

OBJECTIVES Achieving Financial and Operational Excellence

•

The current management team has consistently executed on each element of our strategy to

transform Buckeye into a best-in-class asset manager by:

•

Implementing best practices across our business, including acquired assets

•

Improving our cost structure through an organizational restructuring in 2009

•

Expanding our asset portfolio through conservatively financed, accretive acquisitions, and

organic growth projects

•

Diversifying

our

legacy

business

into

new

geographies,

products,

and

asset

classes

•

Reducing cost of capital through the buy-in of our general partner

•

We continue to be committed to our mission of delivering superior returns through our

talented, valued employees and our core strengths of:

•

Best-in-class customer service

•

Operational excellence that provides consistent, reliable performance to optimize the assets

we own and operate

•

An unwavering commitment to safety, environmental responsibility, regulatory compliance, and

personal integrity

•

An entrepreneurial approach toward asset acquisition and development

©

Copyright 2012 Buckeye Partners, L.P.

4 |

CEO SUCCESSION

AND STRATEGIC ORGANIZATIONAL REALIGNMENT CEO succession effective 1Q 2012:

•

Clark C. Smith, Buckeye’s President and Chief Operating Officer,

succeeded Forrest E. Wylie as Chief Executive Officer, and joined the

Board of Directors of Buckeye’s general partner.

•

Forrest E. Wylie continues to serve as Non-Executive Chairman of the

Board, where he remains active in developing our strategic vision.

©

Copyright 2012 Buckeye Partners, L.P.

5

Board of Directors

Forrest E. Wylie

Chairman

Clark C. Smith

Chief Executive Officer

Robert A. Malecky

President, Domestic

Pipelines and Terminals

Domestic

Pipelines

BORCO

Terminal

Yabucoa

Terminal

Natural Gas

Storage

Mark S. Esselman

Global

Human Resources

Keith E. St.Clair

Chief Financial

Officer

Khalid A. Muslih

Corp. Development &

Strategic Planning

Development

& Logistics

Mary F. Morgan

President, International

Pipelines and Terminals

Energy

Services

Jeremiah J. Ashcroft,

III

President,

Buckeye Services

Domestic

Terminals

Strategic Organizational Realignment, effective 1Q 2012; Buckeye

operations organized into three business units, each headed by a

President.

•

Domestic Pipelines & Terminals

•

International Pipelines & Terminals

•

Buckeye Services

Management Structure after Reorganization

Strategic Organizational Realignment rationale: Previous structure organized around functions (e.g., commercial, operations, etc.). Growth has resulted in increased complexities in each of Buckeye’s business areas,

requiring focus and ownership of skilled executives on a daily basis. Allows business unit Presidents to focus on all aspects of performance–including

commercial, operational, and financial performance–of their respective business

unit. Presidents of business units accountable for overall performance of those units.

William H. Schmidt, Jr.

General Counsel |

ORGANIZATIONAL

OVERVIEW Three Business Operating Units

Domestic Pipelines & Terminals

•

Over 6,000 miles of pipeline with ~100 delivery locations

•

Approximately 100 liquid petroleum product terminals

•

Approximately 41 million barrels of liquid petroleum product storage

capacity

International

Pipelines

&

Terminals

•

Over 28 million barrels of storage capacity at 2 terminal facilities

in The Bahamas (~23 million) and Puerto Rico (~5 million)

•

Deep water berthing capability to handle ULCCs and VLCCs

in The Bahamas

•

Announced expansion underway to add approximately 4.7 million

barrels

at

Bahamian

facility;

1.9

million

barrels

placed

in

service

2

half

2012

Buckeye Services

Natural Gas Storage

•

~30 Bcf of working natural gas storage capacity in Northern California

Energy Services

•

Markets refined petroleum products in areas served by Domestic

Pipelines &

Terminals

•

5 terminals with ~1 million barrels of storage capacity

Development & Logistics

•

Operates and/or maintains third-party pipelines under agreements with major

oil and chemical companies

(1) See Appendix for Non-GAAP Reconciliations

©

Copyright 2012 Buckeye Partners, L.P.

6

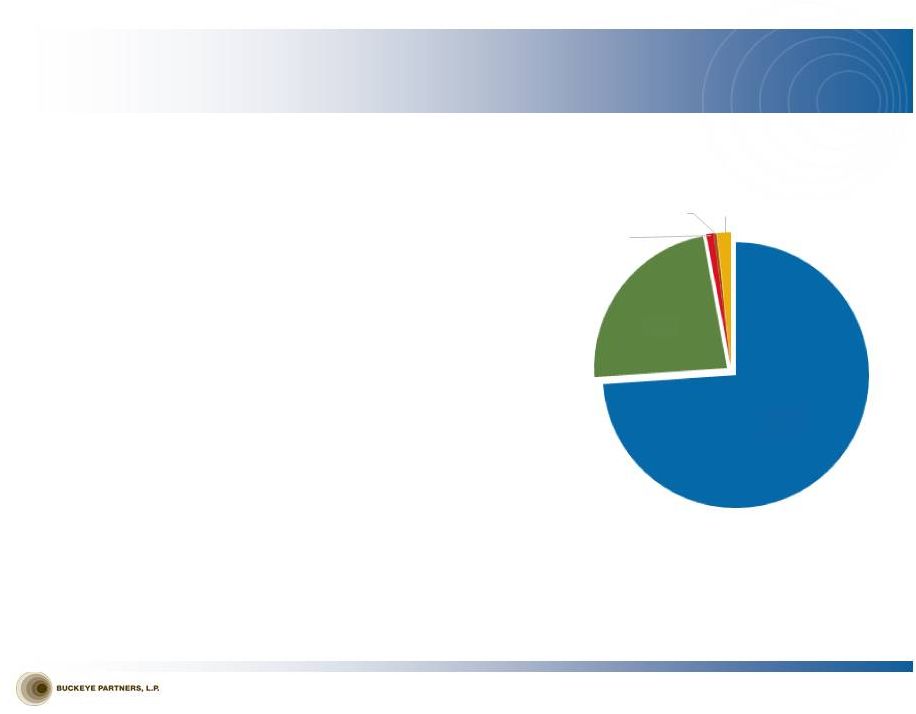

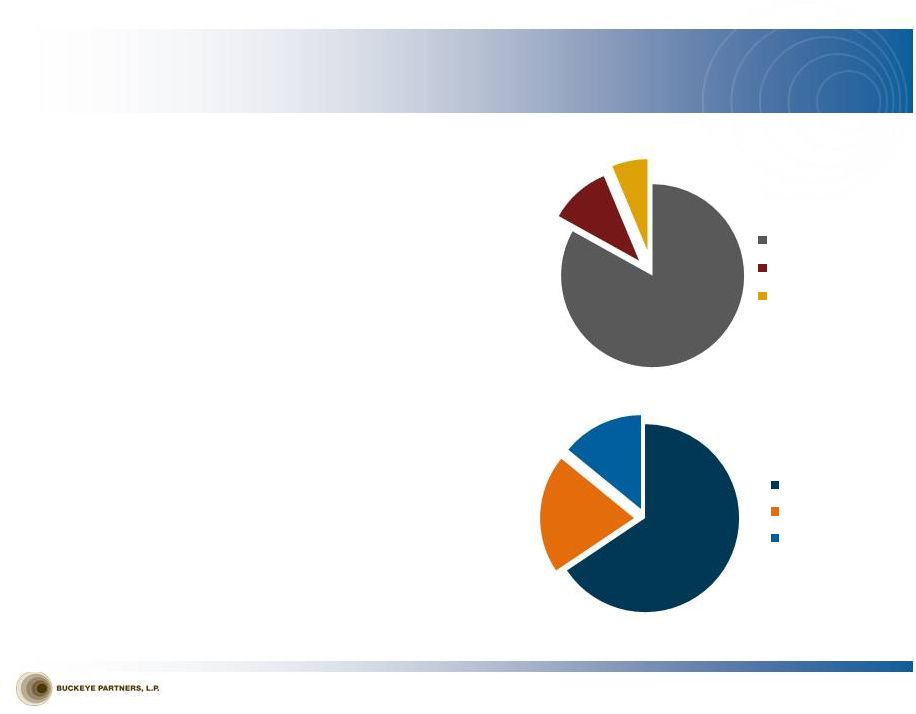

74.0%

23.1%

0.9%

0.4%

1.6%

2011 ADJUSTED EBITDA

(1)

nd |

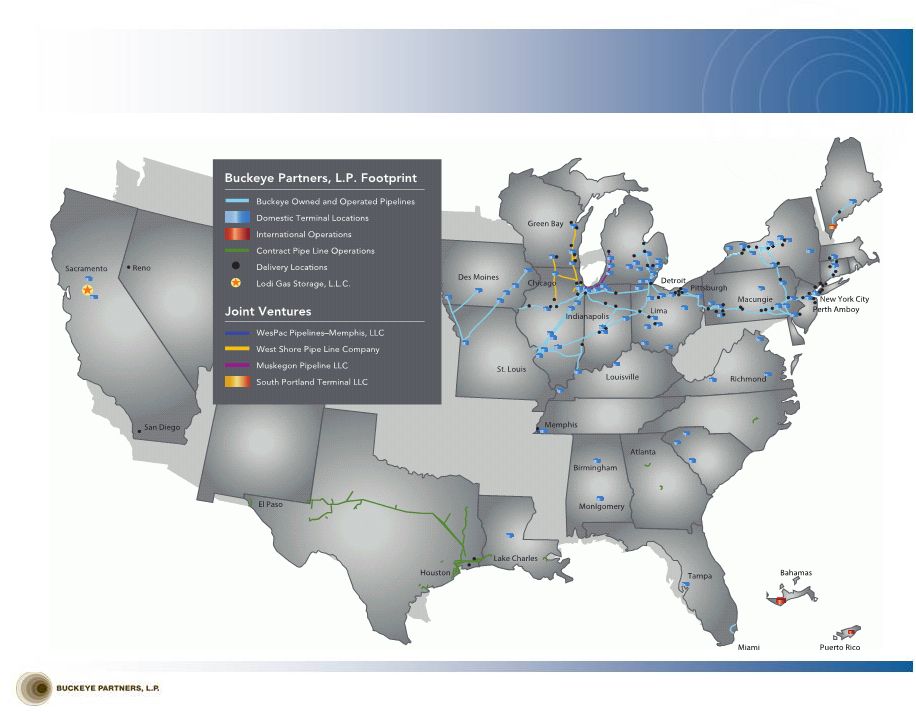

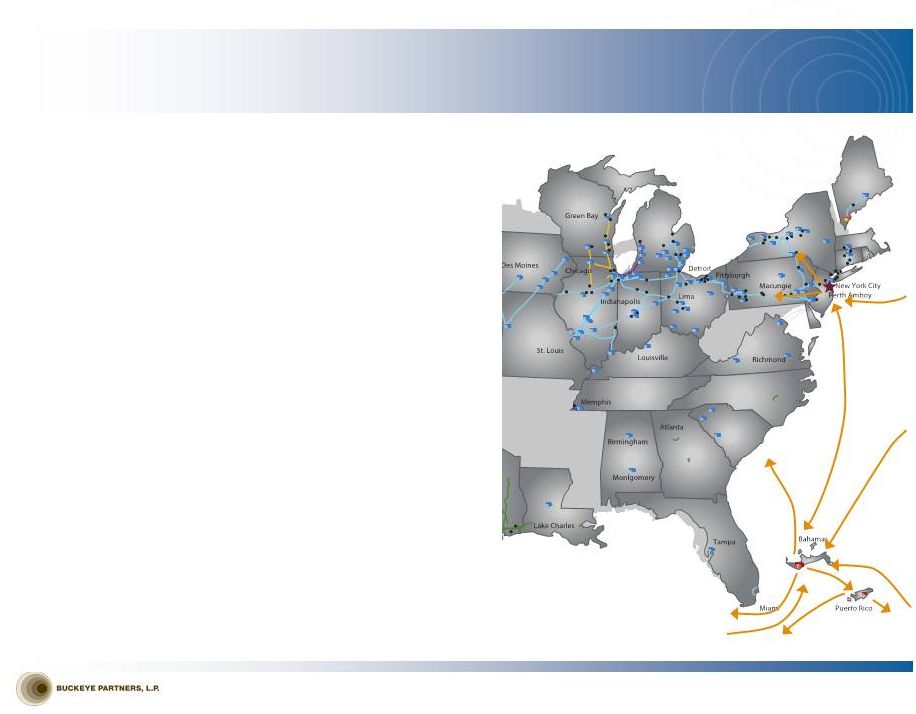

BUCKEYE SYSTEM

MAP ©

Copyright 2012 Buckeye Partners, L.P.

7 |

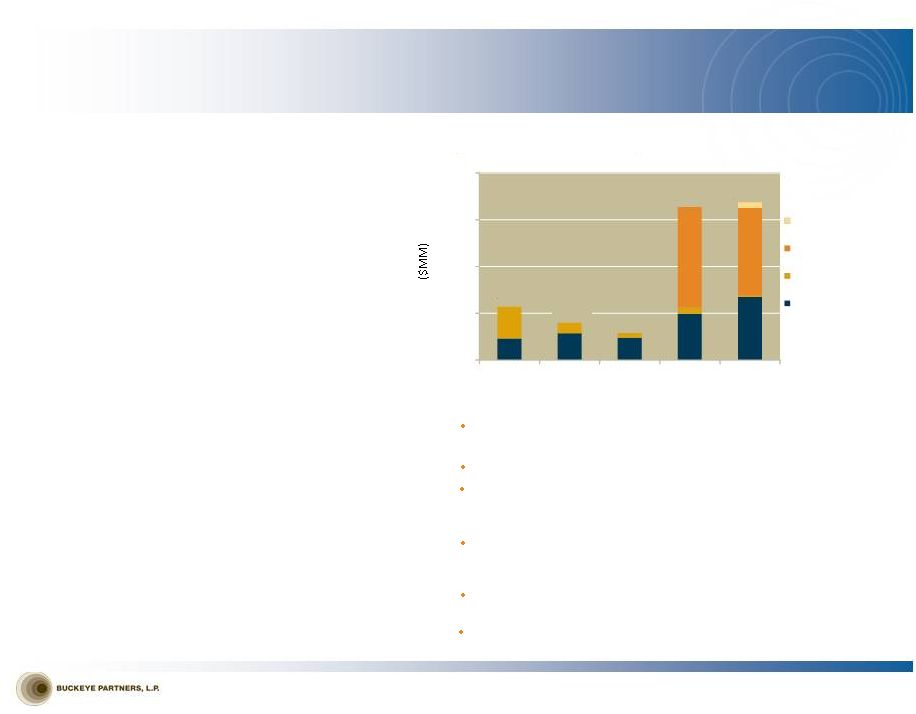

VALUE

CREATION/GROWTH DRIVERS $4 Billion Invested Since 2008

Recent Transactions

(1)

2012

•

Perth Amboy, New Jersey Marine Terminal,

$260.0 million

2011

•

BORCO Marine Terminal, $1.7 billion

•

BP Pipeline & Terminal Assets, $165.0 million

•

Maine Terminals and Pipeline, $23.5 million

2010

•

Buy-in of BPL’s general partner, 20 million units issued

•

Yabucoa, Puerto Rico Terminal, $32.6 million

•

Opelousas, Louisiana Terminal, $13.0 million

•

Additional Equity Interest in West Shore Pipe Line Company,

$13.5 million

2009

•

Blue/Gold Pipeline and Terminal Assets, $54.4 million

2008

•

Lodi Natural Gas Storage, $442.4 million

•

Farm & Home Oil Company

(2)

, $146.2 million

(3)

•

Niles and Ferrysburg, Michigan Terminals, $13.9 million

•

Albany, New York Terminal, $46.9 million

©

Copyright 2012 Buckeye Partners, L.P.

8

(1)

Excludes acquisitions with a value of $10 million or lower

(2)

Now Buckeye Energy Services

(3)

Buckeye sold the retail division of Farm & Home Oil Company in 2008 for $52.6

million (4)

Estimate provided is mid-point of expected organic growth capital spend range

Organic Growth Capital Spending

$0

$80

$160

$240

$320

2008

2009

2010

2011

2012P

Perth Amboy

BORCO

Natural Gas

Storage

Legacy Assets (excl.

NGS)

$91.5

$261.9

$63.8

$46.5

$270.0

Major Capital Projects in Current Year

Transformation of Perth Amboy terminal into highly efficient, multi-

product storage, blending, and throughput facility

Significant expansion and product diversity plans at BORCO facility

Transformation of our Albany marine terminal to handle crude via

rail and ship; represents another connection for us to crude-rich

Bakken shale play

Propylene rail loading and storage project and storage expansion

and unit train rack construction at two terminals within our

Chicago complex

Pipeline expansion between our Linden, NJ and Macungie, PA

terminals to increase capacity to Western PA

Butane blending and vapor recovery installations planned for

numerous terminal facilities across our system |

Domestic

Pipelines & Terminals ©

Copyright 2012 Buckeye Partners, L.P.

9 |

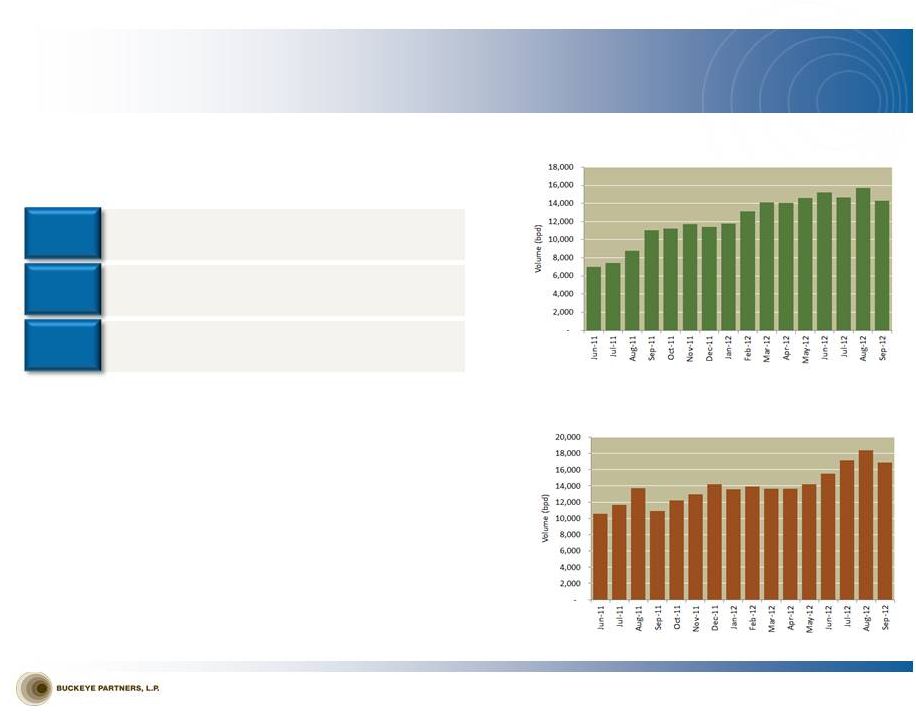

DOMESTIC

PIPELINES & TERMINALS OVERVIEW ©

Copyright 2012 Buckeye Partners, L.P.

10

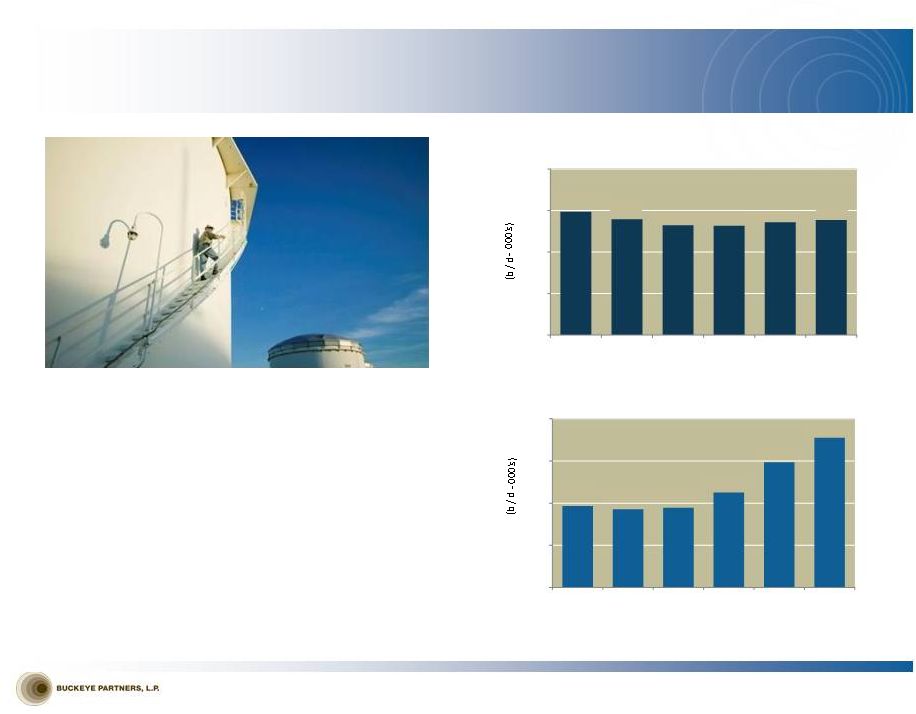

Petroleum storage tanks at our Macungie terminal in Pennsylvania

•

Pipelines & Terminals segment represents Buckeye’s

largest segment contribution to Adjusted EBITDA

•

Over 6,000 miles of pipeline located primarily in the

Northeast and Midwest United States moving over 1.3

million barrels of liquid petroleum products per day

with more than 100 delivery points

•

Approximately 100 liquid petroleum product storage

terminals located throughout the United States

•

Approximately 41 million barrels of storage capacity

(1)

YTD as of September 30, 2012

(2)

Terminal Throughput Volumes

(1)

Pipeline Throughput Volumes

(1)(2)

1,483.4

1,395.4

1,323.1

1,316.3

1,358.1

1,386.7

0

500

1,000

1,500

2,000

2007

2008

2009

2010

2011

2012

482.3

464.4

471.9

562.5

742.8

888.3

0

250

500

750

1000

2007

2008

2009

2010

2011

2012

Pipeline volumes exclude contribution from the Buckeye NGL Pipeline

sold in January of 2010

|

BP PIPELINES

& TERMINALS ACQUISITION ©

Copyright 2012 Buckeye Partners, L.P.

11

•

Transaction closed in June 2011

•

Total transaction purchase price of $165 million

•

33 liquid products terminals expanding Buckeye’s

footprint in the Midwest as well as providing

geographic diversity with terminals in the Southeast

and on the West Coast

•

643 miles of refined product pipeline in Iowa and

Northern Ohio

•

590-mile “Lower V”

pipeline system that originates

in Dubuque, Iowa and runs southwest into Missouri

and then northwest back into Iowa

•

53 miles of pipelines in Northern Ohio

Transaction Overview

Benefits to Buckeye

•

Represents a key step in Buckeye’s continued expansion

and geographic diversification efforts

•

Facilitates participation in several growth markets

outside Buckeye’s previous system footprint

•

Provides stable tariff and fee-based revenue streams,

supported by multi-year throughput commitments by BP

•

Acquisition was accretive to distributable cash flow

•

Commercial development of these assets has exceeded

plan

•

Execution of our Best Practices Initiative strategies:

•

Rapid realization of operating synergies with

Buckeye’s existing assets

•

Headcount reduction pursuant to synergy realization

•

Process improvement resulting in efficient, cost-

effective operations

•

Operation of integrated assets under Buckeye

business strategy, which includes utilization of assets

at the lowest costs per unit |

BP

ACQUISITION—STRONG RESULTS Successful Execution of Terminal Growth Franchise

©

Copyright 2012 Buckeye Partners, L.P.

12

•

Pipeline and terminal volumes have exceeded plan since

inception

•

Continued growth expected with several additional new

contracts still to be signed in the short term

•

Belton, SC and Fairfax, VA are select examples that

highlight significant growth through incremental third-

party business, and new products and service offerings

Terminal Growth

Franchise

–

Ability

to

quickly

integrate

these spun-

off assets while unlocking significant value through

commercialization and application of our best practices formula

32

34

13.1

Belton, SC

Fairfax, VA

Number of new third-party terminal customers

Percentage increase in Adj. EBITDA contribution

from these assets for June 2012 vs. June 2011

Percentage of volume growth across all 33 acquired

terminals since inception |

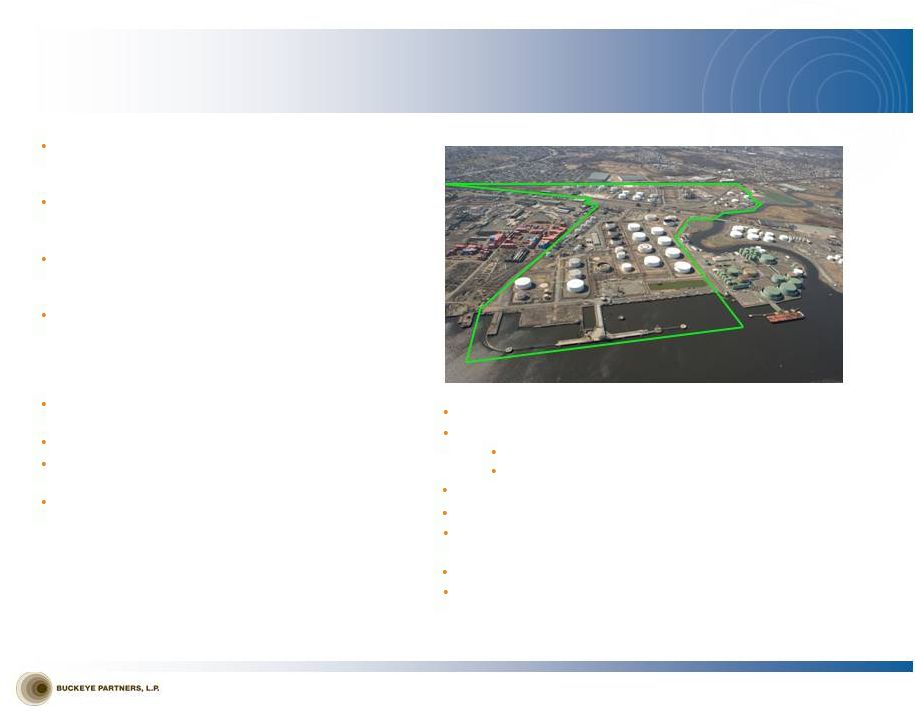

PERTH AMBOY

ACQUISITION OVERVIEW ©

Copyright 2012 Buckeye Partners, L.P.

13

Note: Facility

located in Perth

Amboy, NJ.

Green line

indicates

approximate

property

boundaries

(1)

Includes acquisition purchase price and capital spent on tanks, terminal piping, dock and truck

rack improvements, and ~6 miles of new pipeline to be constructed from Perth Amboy to Buckeye’s Linden, NJ complex.

(2)

One of the barge docks is currently out of service.

Facility Overview

Acquisition of a New York Harbor marine terminal for

liquid petroleum products from Chevron for $260

million in cash

Unique opportunity to acquire key link in the product

logistics chain to unlock significant long-term value

across the Buckeye enterprise

Near-term plans to transform existing terminal into a

highly efficient, multi-product storage, blending, and

throughput facility

Anticipated growth capital investment in the facility of

~$200-250 million over the next three years at

attractive annual Adjusted EBITDA investment multiple

of 4 –

5x, resulting in all-in Adjusted EBITDA

investment multiple of 7 –

8x

(1)

Transaction supported by multi-year storage, blending,

and throughput commitments from Chevron

Closed on July 26, 2012

Expected to be accretive to distributable cash flow per

unit in 2013

Portion of purchase price funded indirectly by

February 2012 registered direct offering of LP units

Located in New York Harbor as a NYMEX delivery point

Approximately 4.0 MMBbls total storage capacity

~2.7 MMBbls of active refined product storage

~1.3 MMBbls of refurbishable storage

4 docks (1 ship, 3 barge

(2)

) with water draft up to 37'

Pipeline, water, rail, and truck access

~250 acre site with significant undeveloped acreage for expansion

potential

Close proximity for integration with Buckeye’s Linden complex

Assessing opportunities for handling Bakken-sourced crude at this

facility via rail and ship

Transaction Overview |

PERTH AMBOY

COMMERCIAL STRATEGY PADD

(1)

1 Market Opportunity

•

The PADD 1 region has ~36% of the U.S.

population and relies on PADD 3 and international

imports and transfers of refined products to meet

market demand

•

All U.S. Northeast product not produced by local

refineries must be supplied either through import

or inter-PADD transfers, increasing storage

capacity demand in the New York Harbor

•

New York Harbor NYMEX delivery point: nexus of

U.S. Northeast petroleum flows

•

Significantly more trading liquidity than

Philadelphia market

©

Copyright 2012 Buckeye Partners, L.P.

14

(1)

Petroleum Administration for Defense Districts

Buckeye Business Strategy

•

Pipeline constraints and poor facility configurations

(tank-to-tank communication) at some existing

terminals in New York Harbor result in inefficiencies

•

Ability to complement storage with local product

distribution via truck rack

•

Strong interest expressed for a Bakken/Utica crude

solution, bunker fuel growth, and asphalt

terminalling/supply

•

Facilitates U.S. Northeast product flow and logistics

•

Secures and diversifies access to product supply

•

Extension of the product value chain with BORCO

•

Opportunity to tie-in imports and exports to/from the

U.S.

We believe optimal facility configuration with simultaneous operations and high-speed

takeaway capacity will give Perth Amboy competitive advantages in the marketplace

•

Multi-mode takeaway capacity (pipe, water,

rail, truck) connected to the Buckeye system

and inland distribution network

•

Balanced focus on imports/exports for clean

products (gasoline, distillates, jet) and dirtier fuels

(crude, fuel oil, asphalt)

•

Perth Amboy is in a highly attractive location

in the New York Harbor with access to the

large local PADD 1 market |

LONG-TERM

VISION – “Connecting the Dots…”

•

Global supply and demand imbalances expected to persist, but

they will likely continue to shift as the rate of change accelerates

•

Anticipate new sources of product supply in the future

•

New global refining capacity coming online will seek deficit markets

•

Northeast U.S. refineries face long-term challenges from high cost and

low investment

•

We believe New York Harbor and Buckeye’s pipeline system are

critical components to facilitate Northeast product flow logistics

•

Perth Amboy is expected to function as a premier access point for

refined petroleum products moving into PADD 1

•

A component of our strategy in acquiring BORCO was to help facilitate

product flow into the Buckeye system in PADD 1

•

BORCO, Perth Amboy, and Yabucoa are key components of a

long-term marine terminal strategy

•

Create

a

more

fully

integrated

and

flexible

system

with

superior

trade

flow connectivity, service capabilities, and tankage versatility

•

Execution on this strategy will continue to differentiate

Buckeye’s service offerings and provide sustainability and

optionality for further growth in our core businesses

©

Copyright 2012 Buckeye Partners, L.P.

15

BORCO

Yabucoa |

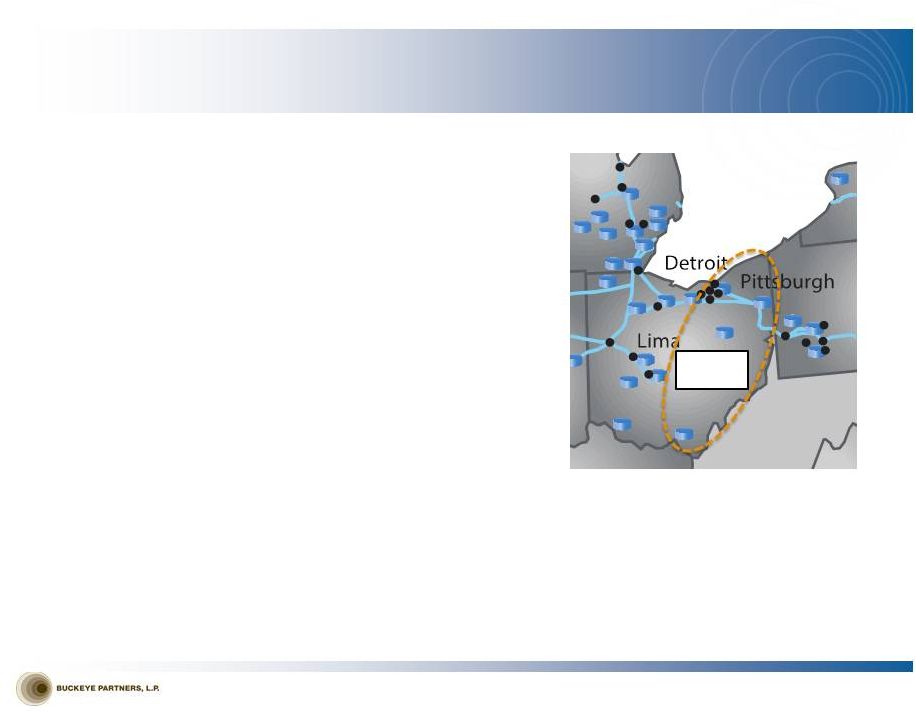

DOMESTIC

PIPELINES & TERMINALS GROWTH POTENTIAL NY Harbor to PA Expansion

(completed 4/1/12):

•

Increased Buckeye’s ability to handle NY Harbor

barrels destined for the Pennsylvania market

•

Incremental 30,000 bpd of pipeline capacity

Bakken Crude:

•

Multi-year agreement to support transformation

of the Albany marine terminal to handle crude

via rail and ship for major oil refiner

•

Contracted to offload approximately 8,600 bpd

of Bakken crude for refinery customer at

Woodhaven, MI facility

•

Perth Amboy well-suited for handling via rail

Butane Blending:

•

Significant growth driven by strong blending

margins

•

Improved blending efficiencies and oversight

•

Opportunities for further locational deployment

of blending capabilities

Propylene Rail Facility

(in progress):

•

Construction of new propylene storage at East

Chicago facility

•

Add rail loading capability at that facility

©

Copyright 2012 Buckeye Partners, L.P.

16

Utica Shale

Opportunity:

•

Development is

in early stages,

but industry

consensus is that

crude logistics

solutions will be

needed

•

Buckeye has

presence in area

and has

opportunity to

utilize existing

infrastructure,

including ROW

and underutilized

lines, to be key

logistics provider

Miami and JFK Airports Pipeline Expansions (potential):

•

Reviewing expansion options as a result of jet fuel volume growth

Chicago Complex Crude Oil Storage Opportunity (potential):

•

Opportunity to leverage asset footprint in Chicago to take

advantage of changing crude oil slates in the market

PROJECTS

Primary

Utica Shale |

FERC ORDER

DEVELOPMENTS Buckeye Pipe Line’s Market-Rate Program

Program

Background

and

“Show

Cause”

Proceeding

•

In 1991, FERC approved Buckeye Pipe Line Company, L.P.’s (“BPL Co.”) use of an

innovative rate-setting system. •

In its 15 competitive markets, BPL Co. sets tariff rates in response to competitive forces,

subject to a cap •

Rates in the other five markets, including NYC, are tied to changes in rates in the

competitive markets •

On March 1, 2012, BPL Co. filed for routine, system-wide rate increases; a single airline

shipper in the NYC area protested. •

On March 30, 2012, FERC issued an order rejecting the rate increases and initiated a review of

the program. •

BPL Co.’s response, which was filed May 15, affirmed that the program has functioned

reasonably, has adjusted rates in line with the pipeline industry, and has not caused

undue discrimination among its shippers. •

On June 29, 2012, the initial protesting party filed comments contending that BPL Co.’s

program has not been reasonable and should be discontinued; three companies intervened

without taking a position, and three companies and a committee representing jet fuel consumers

at

an

airport

supported

the

position

of

the

protesting

party.

Additional

filings

were

made

by

the

parties

in

July

and

August.

One

of

the

intervenors withdrew from the proceeding in October.

•

In

2011,

BPL

Co.

generated

approximately

$295

million

of

the

revenue

in

Buckeye’s

Pipelines

&

Terminals

operating

segment

and

deliveries

of

jet

fuel

to

the

NYC

airports

generated

approximately

$30

million

of

BPL

Co.’s

revenues.

FERC’s

order

does

not

affect

any

pipelines

or terminals owned by Buckeye’s other operating subsidiaries.

•

Although Buckeye believes the program should be preserved, FERC may discontinue or modify it

to conform to its generic rate-setting methodology of indexing or one of the

alternative methodologies (market-based, cost-based, or settlement-based rates).

Airlines’

Complaint

•

On September 20, 2012, four airlines filed a complaint at FERC challenging BPL Co.’s

tariff rates for transporting jet fuel to three NYC airports –

the

same

movements

that

were

the

subject

of

the

March

protest

that

led

to

the

“show

cause”

proceeding.

•

The complaint is not directed at BPL Co.’s rates for service to other destinations, and

it has no impact on the pipeline systems and terminals owned by Buckeye’s other

operating subsidiaries. •

On October 10, 2012, BPL Co. filed its answer to the complaint, and additional filings were

made by the parties in October and November. No third parties have filed to

intervene in the complaint proceeding. •

While

we

cannot

predict

when

FERC

will

act

on

the

airlines’

complaint

or

what

FERC

may

do,

all

parties

have

expressed

a

willingness

to explore settlement by participating in FERC’s standard settlement processes. We

believe it is likely that FERC will initiate a settlement process, though we cannot

predict whether the process will be successful. ©

Copyright 2012 Buckeye Partners, L.P.

17 |

FERC ORDER

DEVELOPMENTS (Continued) Buckeye Pipe Line’s Market-Rate Program

Market-Based Rates Application for New York City Market

•

On October 15, 2012, BPL Co. filed an application with FERC seeking authority to charge

market-based rates for deliveries of refined petroleum products to the NYC

market. •

If

FERC

grants

the

application,

BPL

Co.

would

be

permitted

prospectively

to

set

its

rates

in

response

to

competitive

forces,

and

the

airlines’

cost-based

challenges

to

BPL

Co.’s

jet

fuel

delivery

rates

to

the

NYC

airports

would

be

moot

with

respect

to

future

rates.

•

Buckeye believes that the New York City-area market is robust and highly

competitive. The New York Harbor is one of the world’s most active refined

petroleum products markets. Within this market, BPL Co.’s customers have access to numerous existing alternatives, via

pipeline,

barge,

and

truck,

to

transport

refined

products.

The

three

airports

are

located

near

other

active

products

pipelines

or

barge

docks and, with reasonable investment, should be able to access alternative jet fuel supplies

efficiently and economically. •

Any protests or comments on BPL Co.’s market-based rates application are due by

December 14th. Buckeye cannot predict when FERC will act on the application

or what it will do. Depending

on

the

outcome

of

these

proceedings,

the

level

of

some

or

all

of

BPL

Co.’s

rates

could

be

subject

to

change,

which

could

have

a material impact on our revenues.

©

Copyright 2012 Buckeye Partners, L.P.

18 |

International Pipelines & Terminals

©

Copyright 2012 Buckeye Partners, L.P.

19 |

BORCO

•

World-class marine storage terminal for crude oil, fuel oil, and

refined petroleum products

•

23.3 MMBbls capacity

•

Located in Freeport, Bahamas, 80 miles from Southern Florida and

920 miles from New York Harbor

•

Deep-water access (up to 91 feet) and the ability to berth VLCCs

and ULCCs

•

Significant amount of capacity under long-term (3-5 year) take or

pay contracts

•

World-class customer base

•

Variable revenue generation from ancillary services such as

berthing, blending, bunkering, and transshipping

•

Hub for international logistics

•

Expansion project approved for 4.7 million barrels with 1.9 million

barrels delivered to date; room to double storage capacity

if

market conditions permit

International Pipelines & Terminals Yabucoa, Puerto Rico

•

Well maintained facility with superior blending/manufacturing

facilities

•

4.6 million barrels of refined petroleum product, fuel oil, and crude

oil storage capacity

•

Strategic location supports a strong local market and also provides

regional growth opportunities

•

Long-term fee-based revenues supported by multi-year volume

commitments from Shell

©

Copyright 2012 Buckeye Partners, L.P.

20

INTERNATIONAL PIPELINES AND TERMINALS

(1)

Excludes non-cash amortization of unfavorable storage contracts.

83%

11%

6%

BORCO 2011 REVENUE

(1)

Storage (take or pay)

Berthing (variable)

Other Ancillary (variable)

66%

20%

14%

BORCO 2011 LEASED CAPACITY

Fuel Oil

Crude Oil

Refined Products |

BORCO BERTHING

CAPABILITIES SIX OFFSHORE JETTIES AND INLAND DOCK

©

Copyright 2012 Buckeye Partners, L.P.

21

BERTH 5

Fuel Oil

Clean Products

BERTH 6

Crude Oil

Fuel Oil

Clean Products

BERTH 7

Fuel Oil

Clean Products

BERTH 8

Crude Oil

Fuel Oil

Clean Products

BERTH 10

Crude Oil

Fuel Oil

Berth 12

(Inland Dock)

Fuel Oil

Clean Products

BERTH 9

Crude Oil

Fuel Oil |

BORCO INTERNAL

GROWTH PROJECTS EXPANSION AND OTHER GROWTH OPPORTUNITIES

Significant Land Available for Expansion

©

Copyright 2012 Buckeye Partners, L.P.

22

•

Expansion project at BORCO well underway

•

Phase 1 to add approximately 3.5 million barrels of storage

capacity

•

1.1 million barrels of fuel oil storage in operation as of July

2012

•

~0.8

million

barrels

of

refined

products

storage

in

operation

as

of October 2012

•

~1.6 million barrels of refined products storage to be in-

service in first quarter of 2013

•

Initiation of Phase 2 expansion of 1.2 million barrels of crude oil

storage expected to be in service in the third quarter of 2013

•

Longer-term opportunity to double storage capacity in Greenfield

•

Offshore

jetty

(2

berths)

and

inland

dock

construction

completed

and operations initiated in the fourth quarter of 2011

Other Internal Growth Opportunities

•

Crude Unit

•

Strong interest in setting up crude topping unit at BORCO

•

Driver: need for low sulfur fuel oil

•

Strategic alliance could also support GC exports as

shale/Canadian crude floods into GC (export after “minor

processing”)

•

Bunkering

Opportunities

–

Blended

Fuel

Oil

•

BORCO is the logical, geographical, optimum spot for a new

“Bunker filling station”

•

2014 Panama Canal expansion to allow passage of Suezmax

vessels expected to lead to 20-30% increase in traffic, BORCO

location ideal to service the incremental vessels

BORCO

Expansion

Capacity

(1)

–millions

of

barrels

(1)

Graph reflects expected midpoint of capital spend range. Dates represent expected date that

capacity is placed in service. $50

$100

$150

$200

$250

0

1

2

3

4

5

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2012

2013

Yellowfield 2

Bluefield 2

Bluefield 1

Yellowfield 1

•

Approximately 75% of total expansion capacity is already leased

Capex |

Buckeye

Services ©

Copyright 2012 Buckeye Partners, L.P.

23 |

BUCKEYE SERVICES

OVERVIEW ©

Copyright 2012 Buckeye Partners, L.P.

24

Contract operations

Project origination

Asset development

Engineering design

Project management

Natural Gas Storage

•

Buckeye’s Lodi Gas Storage facility is a high performance natural gas storage facility

with approximately 30 Bcf of working gas capacity in Northern California serving the

greater San Francisco Bay Area •

Revenue is generated through firm storage services and hub services

•

The

facilities

collectively

have

a

maximum

injection

and

withdrawal

capability

of

approximately

550

million

cubic

feet

per

day

(MMcf/day)

and

750

MMcf/day,

respectively

•

Energy Services

Development & Logistics

Buckeye Development & Logistics (“BDL”)

operates

and/or maintains third-party pipelines under

agreements with major oil and chemical companies

BDL is also responsible for identifying and

completing potential acquisitions and organic

growth projects for Buckeye

BDL services offered to customers

Lodi’s

facilities

are

designed

to

provide

high

deliverability

natural

gas

storage

service

and

have

a

proven

track

record of safe and reliable operations

Energy Services

Buckeye Energy Services (“BES”) markets a wide

range of refined petroleum products and other

ancillary products in areas served by Buckeye’s

pipelines and terminals

Strategy for mitigating basis risk included a

reduction of refined product inventories in the

Midwest and focusing on fewer, more strategic

locations for transacting business

Recently reduced costs by right-sizing the

infrastructure for reduced geographic focus

Contributed almost $32 million in revenues to

Domestic Pipelines & Terminals over last 12

months while also providing valuable insight on

demand and pricing support for our terminalling

and storage business |

Financial

Overview ©

Copyright 2012 Buckeye Partners, L.P.

25 |

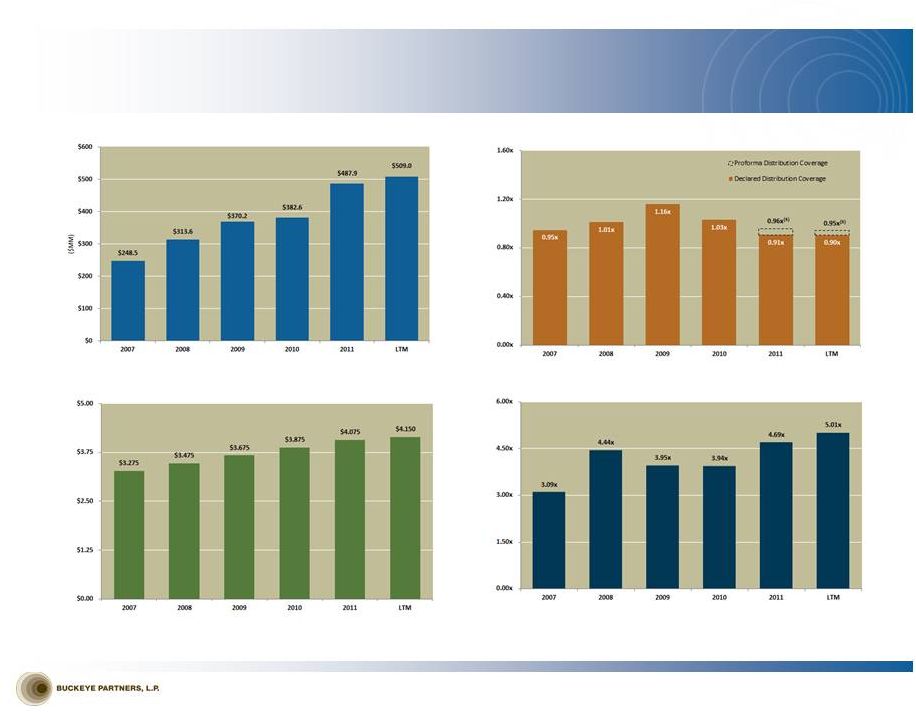

FINANCIAL

PERFORMANCE ©

Copyright 2012 Buckeye Partners, L.P.

26

Adjusted

EBITDA

($MM)

(1)(2)

Cash Distributions per Unit

Cash

Distribution

Coverage

(2)(3)

(1)

LTM as of September 30, 2012

(2)

See Appendix for Non-GAAP Reconciliations

(3)

Distributable cash flow divided by cash distributions declared for the respective periods

(4)

Long-term debt less cash and cash equivalents divided by Adjusted EBITDA

Net LT

Debt/Adjusted

EBITDA

(1)(4)(6)

(5) Pro forma distribution coverage excludes $17.1 million of acquisition and

integration expenses incurred in 2011 and

$15.3 million during the LTM period ended September 30, 2012 (6) For purposes of

calculating the leverage, Adjusted EBITDA is adjusted for pro forma impacts of acquisitions |

INVESTMENT

SUMMARY Stability and Growth

•

Proven 26-year track record as a publicly traded partnership through varying economic and

commodity price cycles

•

Management

continues

to

drive

operational

excellence

through

its

best

practices

initiative

•

Recent acquisitions provide Buckeye with increased geographic and product diversity, including

access to international logistics opportunities, and provide significant near-term

growth projects •

July 2012 acquisition of marine terminal facility in Perth Amboy, NJ from Chevron furthers

Buckeye’s strategy to create a fully integrated and flexible system that offers

unparalleled connectivity and service capabilities; provides significant near-term

growth opportunities at attractive multiple •

World-class

BORCO

marine

storage

terminal

with

23.3

million

barrels

of

storage

capacity

for

crude

oil

and

liquid

petroleum products in Freeport, Bahamas with approved expansion project of 4.7 million

barrels, including 1.9 million barrels operational in the second half of 2012; serves

as important logistics hub for international petroleum product flows

•

Diversified portfolio of assets provides balanced mix of stability and growth and is well

positioned to take advantage of changing supply and demand fundamentals for crude and

refined petroleum products to drive improved returns to unitholders

©

Copyright 2012 Buckeye Partners, L.P.

27 |

Non-GAAP

Reconciliations ©

Copyright 2012 Buckeye Partners, L.P.

28 |

BASIS OF

REPRESENTATION; EXPLANATION OF NON-GAAP MEASURES ©

Copyright 2012 Buckeye Partners, L.P.

29

Buckeye’s equity-funded merger with Buckeye GP Holdings, L.P. (“BGH”) in

the fourth quarter of 2010 has been treated as a reverse merger for accounting

purposes. As a result, the historical results presented herein for periods prior to the

completion of the merger are those of BGH, and the diluted weighted average number of

LP units outstanding increase from 20.0 million in the fourth quarter of 2009 to 44.3 million in the fourth quarter of 2010. Additionally, Buckeye incurred

a non-cash charge to compensation expense of $21.1 million in the fourth quarter of 2010

as a result of a distribution of LP units owned by BGH GP Holdings, LLC to certain

officers of Buckeye, which triggered a revaluation of an equity incentive plan that had been instituted in 2007.

Adjusted EBITDA and distributable cash flow are measures not defined by GAAP. Adjusted EBITDA

is the primary measure used by our senior management, including our Chief Executive

Officer, to (i) evaluate our consolidated operating performance and the operating performance of our business segments, (ii) allocate

resources and capital to business segments, (iii) evaluate the viability of proposed projects,

and (iv) determine overall rates of return on alternative investment opportunities.

Distributable cash flow is another measure used by our senior management to provide a clearer picture of Buckeye’s cash available for distribution

to its unitholders. Adjusted EBITDA and distributable cash flow eliminate (i) non-cash

expenses, including, but not limited to, depreciation and amortization expense

resulting from the significant capital investments we make in our businesses and from intangible assets recognized in business combinations, (ii) charges

for obligations expected to be settled with the issuance of equity instruments, and (iii)

items that are not indicative of our core operating performance results and business

outlook. Buckeye believes that investors benefit from having access to the same financial measures used

by senior management and that these measures are useful to investors because they aid

in comparing Buckeye’s operating performance with that of other companies with similar operations. The Adjusted EBITDA and

distributable cash flow data presented by Buckeye may not be comparable to similarly titled

measures at other companies because these items may be defined differently by other

companies. Please see the attached reconciliations of each of Adjusted EBITDA and distributable cash flow to net income.

This presentation references forward-looking estimates of Adjusted EBITDA and investment

multiples projected to be generated by the Perth Amboy terminal. A reconciliation of

estimated Adjusted EBITDA to GAAP net income is not provided because GAAP net income generated by the Perth Amboy terminal for the

applicable periods is not accessible. Buckeye has not yet completed the necessary

valuation of the various assets to be acquired, a determination of the useful lives of

these assets for accounting purposes, or an allocation of the purchase price among the various types of assets. In addition, interest and debt expense is a

corporate-level expense that is not allocated among Buckeye’s segments and could not

be allocated to the Perth Amboy terminal operations without unreasonable effort.

Accordingly, the amount of depreciation and amortization and interest and debt expense that will be included in the additional net income generated as a

result of the acquisition of the Perth Amboy terminal is not accessible or estimable at this

time. The amount of such additional resulting depreciation and amortization and

applicable interest and debt expense could be significant, such that the amount of additional net income would vary substantially from the

amount of projected Adjusted EBITDA. |

NON-GAAP

RECONCILIATIONS ©

Copyright 2012 Buckeye Partners, L.P.

30

Net Income to Adjusted EBITDA ($M)

(1)

LTM as of September 30, 2012.

(2)

On November 19, 2010, Buckeye merged with Buckeye GP Holdings L.P.

(3)

In

2010,

Buckeye

revised

its

definition

of

Adjusted

EBITDA

to

exclude

non-cash

unit-based

compensation

expense,

the

2010

non-cash

equity

plan

modification

expense

and

income

attributable

to

noncontrolling

interests

affected

by

the

merger

for

periods

prior

to

our

buy-in

of

our

general

partner.

These

amounts

were

excluded

from

Adjusted

EBITDA

presented

for

2008,

2009

and

2010

in

our

Annual

Report

on

Form

10-K

for

the

year

ended

December

31,

2010,

as

amended.

Adjusted

EBITDA

for

2007

has

been

restated

in

this

presentation

to

exclude

these

amounts

for

comparison

purposes.

2007

2008

2009

2010

2011

LTM

(1)

Net income attributable to BPL

22,921

26,477

49,594

43,080

108,501

251,141

Interest and debt expense

51,721

75,410

75,147

89,169

119,561

114,428

Income tax expense (benefit)

760

801

(343)

(919)

(192)

1,177

Depreciation and amortization

40,236

50,834

54,699

59,590

119,534

136,793

EBITDA

115,638

153,522

179,097

190,920

347,404

503,539

Net

income

attributable

to

noncontrolling

interests

affected

by

merger

(2)

131,941

153,546

90,381

157,467

-

-

Amortization of unfavorable storage contracts

-

-

-

-

(7,562)

(10,994)

Gain on sale of equity investment

-

-

-

-

(34,727)

(615)

Non-cash deferred lease expense

-

4,598

4,500

4,235

4,122

3,956

Non-cash unit-based compensation expense

968

1,909

4,408

8,960

9,150

13,152

Equity plan modification expense

-

-

-

21,058

-

-

Asset impairment expense

-

-

59,724

-

-

-

Goodwill impairment expense

-

-

-

-

169,560

-

Reorganization expense

-

-

32,057

-

-

-

Adjusted EBITDA

(3)

248,547

313,575

370,167

382,640

487,947

509,038

Adjusted Segment EBITDA

Pipelines & Terminals

238,830

253,790

302,164

346,447

361,018

390,983

International Operations

-

-

-

(4,655)

112,996

122,553

Natural Gas Storage

-

41,814

41,950

29,794

4,204

3,639

Energy Services

-

9,443

19,335

5,861

1,797

(19,540)

Development & Logistics

9,717

8,528

6,718

5,193

7,932

11,403

Total Adjusted EBITDA

(3)

248,547

313,575

370,167

382,640

487,947

509,038 |

NON-GAAP

RECONCILIATIONS ©

Copyright 2012 Buckeye Partners, L.P.

31

Net Income to Distributable Cash Flow ($M)

(1)

LTM as of September 30, 2012.

(2)

On November, 19, 2010, Buckeye merged with Buckeye GP Holdings L.P.

(3)

In 2011, Buckeye revised its definition of Distributable Cash Flow to exclude amortization of

deferred financing costs and debt discounts. Distributable Cash Flow for 2007-2010 have been restated to exclude those amounts for

comparison purposes.

2007

2008

2009

2010

2011

LTM

(1)

Net income attributable to BPL

22,921

26,477

49,594

43,080

108,501

251,141

Depreciation and amortization

40,236

50,834

54,699

59,590

119,534

136,793

Net income attributable to noncontrolling interests affected by merger

(2)

131,941

153,546

90,381

157,467

-

-

Gain on sale of equity investment

-

-

-

-

(34,727)

(615)

Non-cash deferred lease expense

-

4,598

4,500

4,235

4,122

3,956

Non-cash unit-based compensation expense

968

1,909

4,408

8,960

9,150

13,152

Equity plan modification expense

-

-

-

21,058

-

-

Asset impairment expense

-

-

59,724

-

-

-

Reorganization expense

-

-

32,057

-

-

-

Non-cash senior administrative charge

950

1,900

475

-

-

-

Amortization of unfavorable storage contracts

-

-

-

-

(7,562)

(10,994)

Write-off of deferred financing costs

-

-

-

-

3,331

-

Amortization

of

deferred

financing

costs

and

debt

discounts

(3)

1,448

1,737

3,134

4,411

4,289

3,476

Goodwill impairment expense

-

-

-

-

169,560

-

Maintenance capital expenditures

(33,803)

(28,936)

(23,496)

(31,244)

(57,467)

(56,662)

Distributable Cash Flow

164,661

212,065

275,476

267,557

318,731

340,247

Distributions for Coverage ratio

(4)

173,689

209,412

237,687

259,315

351,245

376,177

Coverage Ratio

0.95x

1.01x

1.16x

1.03x

0.91x

0.90x

Represents cash distributions declared for limited partner units (LP units) outstanding as of

each respective period. 2012 amounts reflect actual cash distributions paid on LP units for the quarters ended March 31, 2012 and

June 30, 2012 and estimated cash distributions paid on LP units for the quarter ended September

30, 2012. Distributions with respect to the Class B units outstanding on the record date for each quarter ended during 2011 and

2012 were paid in additional Class B units rather than in cash.

(4) |