Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - SUNRISE REAL ESTATE GROUP INC | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - SUNRISE REAL ESTATE GROUP INC | v326730_ex32-1.htm |

| EX-31.1 - EXHIBIT 31.1 - SUNRISE REAL ESTATE GROUP INC | v326730_ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - SUNRISE REAL ESTATE GROUP INC | v326730_ex31-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-Q/A

Amendment No.1

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2012

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission File Number 000-32585

SUNRISE REAL ESTATE GROUP, INC.

(Exact name of registrant as specified in its charter)

| Texas | 75-2713701 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

No. 638, Hengfeng Road 25th Fl, Building A

Shanghai, PRC 200070

(Address of Principal Executive Offices) (Zip Code)

Issuer's telephone number: + 86-21-6167-2800

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer ¨ | Smaller reporting company x |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date: May 17, 2012 - 28,691,925 shares of Common Stock

EXPLANATORY NOTE

The purpose of this Amendment No. 1 on Form 10-Q/A is to amend and restate the consolidated financial statements for the three months ended March 31, 2012 contained in the previously filed Quarterly Report on Form 10-Q of Sunrise Real Estate Group, Inc. (the “Company” or “us”) for the quarter ended March 31, 2012, filed with the Securities and Exchange Commission on May 21, 2012 (the “Form 10-Q”), to make the necessary accounting corrections resulting from a miscalculation in our underwriting sales revenue and cost of sales for the year ended December 31, 2011 under the Statement of Financial Accounting Standards No. 66 (“SFAS 66”). This amendment restates the following items:

- Part I, Item 1- Financial Statements;

- Part II Item 6 - Exhibits.

The only changes to the 10Q are with respect to the financial results for the period ended December 31, 2011. There are no other changes to the Form 10-Q other than those set forth in this amendment. This amendment does not reflect events occurring after the filing of the Form 10-Q, other than the amendments noted above and the filing of certifications of our principal executive officer and principal financial officer pursuant to Rule 13a-14 of the Securities Exchange Act of 1934 and Section 906 of the Sarbanes-Oxley Act, nor does it modify or update disclosures therein in any way other than as required to reflect the amended sections of the Form 10-Q as set forth in this amendment. Among other things, forward-looking statements made in the Form 10-Q have not been revised to reflect events that occurred or facts that became known to us after the filing of the Form 10-Q, and such forward-looking statements should be read in their historical context.

| 2 |

FORM 10-Q/A

For the Quarter Ended March 31, 2012

INDEX

| Page | |

| PART I. FINANCIAL INFORMATION | 4 |

| Item 1. Financial Statements | 4 |

| Consolidated Balance Sheets | 4 |

| Consolidated Statements of Operations | 5 |

| Consolidated Statements of Cash Flows | 6 |

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | 18 |

| Item 3. Quantitative and Qualitative Disclosures About Market Risk | 25 |

| Item 4. Controls and Procedures | 26 |

| PART II. OTHER INFORMATION | 26 |

| Item 1. Legal Proceedings | 26 |

| Item 1A Risk Factors | 26 |

| Item 2. Unregistered Sales of Equity Securities and Use of Proceeds | 27 |

| Item 3. Defaults Upon Senior Securities | 27 |

| Item 4. Mine Safety Disclosures | 27 |

| Item 5. Other Information | 27 |

| Item 6. Exhibits | 27 |

| SIGNATURES | 27 |

| 3 |

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

Sunrise Real Estate Group, Inc.

Unaudited Condensed Consolidated Balance Sheets

(Expressed in US Dollars)

| March 31, | December 31, | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | (Audited) | |||||||

| ASSETS | ||||||||

| Current assets | ||||||||

| Cash and cash equivalents | $ | 3,940,520 | $ | 1,377,093 | ||||

| Restricted cash (Note 3) | 1,350,428 | 1,349,014 | ||||||

| Accounts receivable | 1,199,315 | 1,139,843 | ||||||

| Promissory deposits (Note 4) | 3,547,654 | 3,543,938 | ||||||

| Amount due from related company (Note 12) | 7,812 | 317,415 | ||||||

| Inventory (Note 5) | 1,082,917 | - | ||||||

| Other receivables and deposits (Note 6) | 9,161,046 | 863,813 | ||||||

| Total current assets | 20,289,692 | 8,591,116 | ||||||

| Property, plant and equipment – net (Note 7) | 2,396,770 | 2,405,829 | ||||||

| Investment properties (Note 8) | 6,763,577 | 6,920,532 | ||||||

| Long-term Investment (Note 9) | 3,744,732 | 4,253,206 | ||||||

| Total assets | $ | 33,194,771 | $ | 22,170,683 | ||||

| LIABILITIES AND SHAREHOLDERS’ DEFICIT | ||||||||

| Current liabilities | ||||||||

| Bank loans (Note 10) | $ | 11,121,173 | $ | 11,109,524 | ||||

| Promissory notes payable (Note 11) | 2,681,661 | 1,725,039 | ||||||

| Accounts payable | 465,000 | 481,741 | ||||||

| Amount due to directors (Note 12) | 5,493,406 | 5,185,842 | ||||||

| Amount due to related party (Note 12) | 87,381 | 87,289 | ||||||

| Other payables and accrued expenses (Note 13) | 3,011,692 | 3,487,632 | ||||||

| Other tax payable (Note 14) | 21,941 | 69,402 | ||||||

| Income tax payable | 24,343 | 224,319 | ||||||

| Total current liabilities | $ | 22,906,597 | $ | 22,370,788 | ||||

| Long-term bank loans | - | - | ||||||

| Long-term promissory notes payable | - | - | ||||||

| Deposits received from underwriting sales(Note 15) | 2,963,544 | 3,091,616 | ||||||

| Total liabilities | $ | 25,870,141 | $ | 25,462,404 | ||||

| Commitments and contingencies (Note 16) | ||||||||

| Shareholders’ deficit | ||||||||

| Common stock, par value $0.01 per share; 200,000,000 shares authorized; 28,691,925 shares issued and outstanding as of March 31, 2012 and December 31, 2011 | 286,919 | 286,919 | ||||||

| Additional paid-in capital | 4,581,523 | 4,570,008 | ||||||

| Statutory reserve (Note 17) | 782,987 | 782,987 | ||||||

| Accumulated losses | (11,464,028 | ) | (10,406,798 | ) | ||||

| Non-controlling interests of consolidated subsidiaries | 12,661,625 | 985,704 | ||||||

| Accumulated other comprehensive income (Note 18) | 475,604 | 489,459 | ||||||

| Total shareholders’ deficit | 7,324,630 | (3,291,721 | ) | |||||

| Total liabilities and shareholders’ deficit | $ | 33,194,771 | $ | 22,170,683 | ||||

See accompanying notes to consolidated financial statements.

| 4 |

Sunrise Real Estate Group, Inc.

Unaudited Condensed Consolidated Statements of Operations

(Expressed in US Dollars)

| Three Months Ended March 31, | ||||||||

| 2012 | 2011 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Net Revenues | $ | 1,719,535 | $ | 2,604,624 | ||||

| Cost of Revenues | ($ | 1,148,887 | ) | ($ | 1,739,341 | ) | ||

| Gross Profit | 570,648 | 865,283 | ||||||

| Operating Expenses | (284,220 | ) | (338,904 | ) | ||||

| General and Administrative Expenses | (1,035,876 | ) | (692,190 | ) | ||||

| Operating Profit/(Loss) | (749,448 | ) | (165,811 | ) | ||||

| Other Income, Net (Note 19) | 1,866,770 | - | ||||||

| Interest Income | $ | 3,398 | $ | 3,757 | ||||

| Interest Expenses | (491,451 | ) | (198,407 | ) | ||||

| Profit/(Loss) Before Income Tax and Non-controlling Interest | 629,269 | (360,461 | ) | |||||

| Income Tax | (15,675 | ) | (8,328 | ) | ||||

| Profit/(Loss) Before Non-controlling Interest | 613,594 | (368,789 | ) | |||||

| Return on Investment | (572,443 | ) | - | |||||

| Non-controlling Interest of Consolidated Subsidiaries | (1,098,382 | ) | (123,514 | ) | ||||

| Net Profit/(Loss) | ($ | 1,057,231 | ) | ($ | 492,303 | ) | ||

| Profit/(Loss) Per Share – Basic and Fully Diluted | ($ | 0.04 | ) | ($ | 0.02 | ) | ||

| Weighted average common shares outstanding – Basic and Fully Diluted |

28,691,925 | 23,691,925 | ||||||

See accompanying notes to unaudited condensed consolidated financial statements.

| 5 |

Sunrise Real Estate Group, Inc.

Consolidated Statements of Cash Flows

Increase/(Decrease) in Cash and Cash Equivalents

(Expressed in US Dollars)

| Three Months Ended March 31, | ||||||||

| 2012 | 2011 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Cash flows from operating activities | ||||||||

| Net Profit/(Loss) | ($ | 1,057,231 | ) | ($ | 492,303 | ) | ||

| Adjustments to reconcile net profit/(loss) to | ||||||||

| net cash used in operating activities | ||||||||

| Depreciation of property, plant and equipment | 240,581 | 227,410 | ||||||

| Loss on disposal of property, plant and equipment | 572,442 | |||||||

| Non-controlling interest | 1,098,382 | 123,514 | ||||||

| Change in: Restricted cash | ||||||||

| Inventory | (1,081,989 | ) | - | |||||

| Accounts receivable | (58,226 | ) | (355,320 | ) | ||||

| Other receivables and deposits | (8,289,216 | ) | (4,252,718 | ) | ||||

| Amount due from related party | 309,670 | |||||||

| Accounts payable | (17,231 | ) | (30,368 | ) | ||||

| Other payables and accrued expenses | (479,186 | ) | 4,312,748 | |||||

| Deposit from underwriting sales | (131,201 | ) | (58,977 | ) | ||||

| Interest payable on promissory notes | 75,004 | 31,748 | ||||||

| Interest payable on amount due to director | 245,026 | (11,259 | ) | |||||

| Other tax payable | (47,494 | ) | 5,686 | |||||

| Income tax payable | (200,039 | ) | (228,757 | ) | ||||

| Net cash used in operating activities | (8,820,708 | ) | (728,596 | ) | ||||

| Cash flows from investing activities | ||||||||

| Acquisition of property, plant and equipment | (64,041 | ) | (5,936 | ) | ||||

| Long-term investment | (60,000 | ) | ||||||

| Net cash used in investing activities | (124,041 | ) | (5,936 | ) | ||||

| Cash flows from financing activities | ||||||||

| Funds received from capital increase | 10,568,471 | |||||||

| Proceeds from promissory note | 869,882 | - | ||||||

| Repayment to director | - | (13,641 | ) | |||||

| Advance from director | 53,835 | - | ||||||

| Net cash (used in)/provided by financing activities | 11,492,188 | (13,641 | ) | |||||

| Effect of exchange rate changes on cash and cash equivalents | 15,988 | (5,852 | ) | |||||

| Net (decrease)/increase in cash and cash equivalents | 2,563,427 | (754,025 | ) | |||||

| Cash and cash equivalents at beginning of period | 1,377,093 | 2,973,997 | ||||||

| Cash and cash equivalents at end of period | $ | 3,940,520 | $ | 2,219,972 | ||||

| Supplemental disclosure of cash flow information | ||||||||

| Cash paid during the period: | ||||||||

| Income tax paid | 215,900 | 224,783 | ||||||

| Interest paid | 158,974 | 192,975 | ||||||

See accompanying notes to unaudited condensed consolidated financial statements.

| 6 |

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Expressed in US Dollars)

NOTE 1 – ORGANIZATION AND DESCRIPTION OF BUSINESS

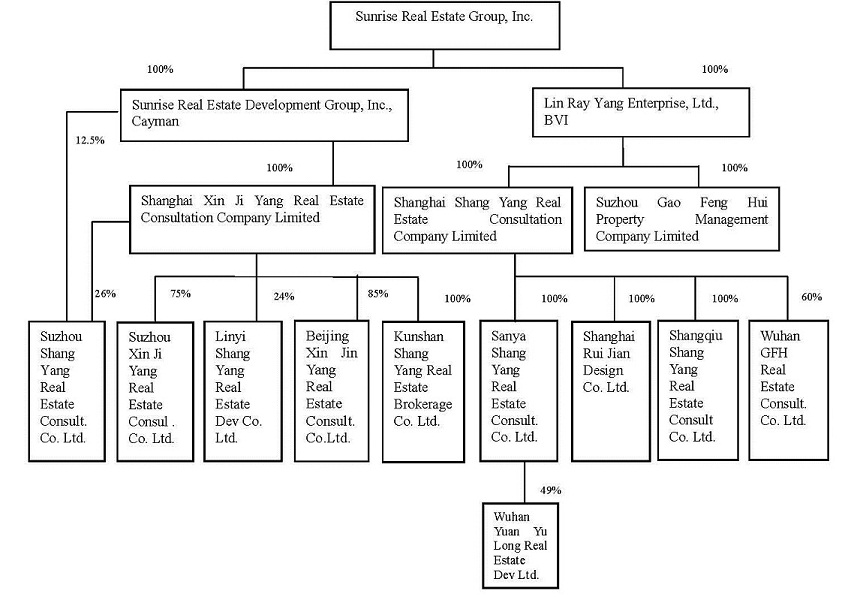

Sunrise Real Estate Development Group, Inc. (“CY-SRRE”) was established in the Cayman Islands on April 30, 2004 as a limited liability company. CY-SRRE was wholly owned by Ace Develop Properties Limited, a corporation, (“Ace Develop”), of which Lin Chi-Jung, an individual, is the principal and controlling shareholder. Shanghai Xin Ji Yang Real Estate Consultation Company Limited (“SHXJY”) was established in the People’s Republic of China (the “PRC”) on August 14, 2001 as a limited liability company. SHXJY was originally owned by a Taiwanese company, of which the principal and controlling shareholder was Lin Chi-Jung. On June 8, 2004, all the fully paid up capital of SHXJY was transferred to CY-SRRE. On June 25, 2004 SHXJY and two individuals established a subsidiary, namely, Suzhou Xin Ji Yang Real Estate Consultation Company Limited (“SZXJY”) in the PRC, at which point in time, SHXJY held a 90% equity interest in SZXJY. On August 9, 2005, SHXJY sold a 10% equity interest in SZXJY to a company owned by a director of SZXJY, and transferred a 5% equity interest in SZXJY to CY-SRRE. Following the disposal and the transfer, CY-SRRE effectively held an 80% equity interest in SZXJY. On November 24, 2006, CY-SRRE, SHXJY, a director of SZXJY and a third party established a subsidiary, namely, Suzhou Shang Yang Real Estate Consultation Company Limited (“SZSY”) in the PRC, with CY-SRRE holding a 12.5% equity interest, SHXJY holding a 26% equity interest and the director of SZXJY holding a 12.5% equity interest in SZSY. At the date of incorporation, SRRE and the director of SZXJY entered into a voting agreement that SRRE is entitled to exercise the voting right in respect of his 12.5% equity interest in SZSY. Following that, SRRE effectively holds 51% equity interest in SZSY. On September 24, 2007, CY-SRRE sold a 5% equity interest in SZXJY to a company owned by a director of SZXJY. Following the disposal, CY-SRRE effectively holds 75% equity interest in SZXJY. In January of 2012, SHXJY invested 24% and established a company in Linyi, named Linyi Shang Yang Real Estate Development Company Limited and acquired approximately 103,385 square meters for the purpose of developing into villa-style residential housings. In an agreement with Zhang Shu Qing, a majority shareholder of 51%, we have her 51% voting power and thus effectively have 75% of voting power.

LIN RAY YANG Enterprise Ltd. (“LRY”) was established in the British Virgin Islands on November 13, 2003 as a limited liability company. LRY was owned by Ace Develop, Planet Technology Corporation (“Planet Tech”) and Systems & Technology Corporation (“Systems Tech”). On February 5, 2004, LRY established a wholly owned subsidiary, Shanghai Shang Yang Real Estate Consultation Company Limited (“SHSY”) in the PRC as a limited liability company. On January 10, 2005, LRY and a PRC third party established a subsidiary, Suzhou Gao Feng Hui Property Management Company Limited (“SZGFH”), in the PRC, with LRY holding 80% of the equity interest in SZGFH. On May 8, 2006, LRY acquired 20% of the equity interest in SZGFH from the third party. Following the acquisition, LRY effectively holds 100% of the equity interest in SZGFH. In 2011 we established Wuhan Yuan Yu Long Real Estate Development Company Limited ("WHYYL") and have a 49% ownership, the purpose of this project company was for a residence development project in Wuhan.

On August 31, 2004, Sunrise Real Estate Group, Inc. (“SRRE”), CY-SRRE and Lin Chi-Jung, an individual and agent for the beneficial shareholder of CY-SRRE, i.e., Ace Develop, entered into an exchange agreement under which SRRE issued 5,000,000 shares of common stock to the beneficial shareholder or its designees, in exchange for all outstanding capital stock of CY-SRRE. The transaction closed on October 5, 2004. Lin Chi-Jung is Chairman of the Board of Directors of SRRE, the President of CY-SRRE and the principal and controlling shareholder of Ace Develop.

Also on August 31, 2004, SRRE, LRY and Lin Chi-Jung, an individual and agent for beneficial shareholders of LRY, i.e., Ace Develop, Planet Tech and Systems Tech, entered into an exchange agreement under which SRRE issued 10,000,000 shares of common stock to the beneficial shareholders, or their designees, in exchange for all outstanding capital stock of LRY. The transaction was closed on October 5, 2004. Lin Chi-Jung is Chairman of the Board of Directors of SRRE, the President of LRY and the principal and controlling shareholder of Ace Develop. Regarding the 10,000,000 shares of common stock of SRRE issued in this transaction, SRRE issued 8,500,000 shares to Ace Develop, 750,000 shares to Planet Tech and 750,000 shares to Systems Tech.

As a result of the acquisition, the former owners of CY-SRRE and LRY hold a majority interest in the combined entity. Generally accepted accounting principles require in certain circumstances that a company whose shareholders retain the majority voting interest in the combined business be treated as the acquirer for financial reporting purposes. Accordingly, the acquisition has been accounted for as a “reverse acquisition” arrangement whereby CY-SRRE and LRY are deemed to have purchased SRRE. However, SRRE remains the legal entity and the Registrant for Securities and Exchange Commission reporting purposes. All shares and per share data prior to the acquisition have been restated to reflect the stock issuance as a recapitalization of CY-SRRE and LRY.

| 7 |

SRRE was initially incorporated in Texas on October 10, 1996, under the name of Parallax Entertainment, Inc. (“Parallax”). On December 12, 2003, Parallax changed its name to Sunrise Real Estate Development Group, Inc. On April 25, 2006, Sunrise Estate Development Group, Inc. filed Articles of Amendment with the Texas Secretary of State, changing the name of Sunrise Real Estate Development Group, Inc. to Sunrise Real Estate Group, Inc., effective from May 23, 2006.

Figure 1: Company Organization Chart

| 1. Beijing Xin Jin Yang Real Estate Consultation Company Limited is currently in the process of being dissolved in 2012. |

| 2. Kunshan Shang Yang Real Estate Brokerage Company Limited is currently in the process of being dissolved in 2012. |

SRRE and its subsidiaries, namely, CY-SRRE, LRY, Shanghai Xin Ji Yang Real Estate Consultation Company Limited (“SHXJY”), Shanghai Shang Yang Real Estate Consultation Company, Ltd. (“SHSY”), Suzhou Gao Feng Hui Property Management Company, Ltd, (“SZGFH”), Suzhou Shang Yang Real Estate Consultation Company (“SZSY”), Suzhou Xin Ji Yang Real Estate Consultation Company, Ltd. (“SZXJY”), Linyi Shang Yang Real Estate Development Company Ltd (“LYSH”), Shangqiu Shang Yang Real Estate Consultation Company, Ltd., (“SQSY”), Wuhan Gao Feng Hui Consultation Company Ltd. (“WHGFH”), Sanya Shang Yang Real Estate Consultation Company, Ltd. (“SYSH”), Shanghai Rui Jian Design Company, Ltd., (“SHRJ”), and Wuhan Yuan Yu Long Real Estate Development Company, Ltd. (“WHYYL”) are sometimes here inafter collectively referred to as “the Company,” “our,” or “us”.

| 8 |

The principal activities of the Company are property development, property brokerage services, real estate marketing services, property leasing services and property management services in the PRC.

NOTE 2 –SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Accounting and Principles of Consolidation

The consolidated financial statements are prepared in accordance with generally accepted accounting principles in the United States of America that include the financial statements of SRRE and its subsidiaries. All inter-company transactions and balances have been eliminated.

Going Concern

The Company’s financial statements are prepared according to the accounting principles generally accepted in the United States of America applicable to a going concern, which contemplates the realization of assets and liquidation of liabilities in the normal course of business. The Company has accumulated losses of $11,396,762 as of March 31, 2012. The Company’s net working capital deficiency and significant accumulated losses raise substantial doubt about its ability to continue as a going concern.

However, management believes that the Company is able to generate sufficient cash flow to meet its obligations on a timely basis and ultimately to attain successful operations in respect of the agency sales and property management operations. Accordingly, the accompanying financial statements do not include any adjustments that may be necessary if the Company is unable to continue as a going concern.

Use of Estimates

The preparation of financial statements in accordance with generally accepted accounting principles requires management to make estimates and assumptions that affect reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents

Cash and cash equivalents include cash in hand and all highly liquid investments with an original maturity of three months or less.

Foreign Currency Translation and Transactions

The functional currency of SRRE, CY-SRRE and LRY is United States Dollars (“US$”) and the financial records are maintained and the financial statements prepared in US $. The functional currency of all the companies located in China is Renminbi (“RMB”) and the financial records and statements are maintained and prepared in RMB.

Foreign currency transactions during the period are translated into each company’s denominated currency at the exchange rates ruling at the transaction dates. Gain and loss resulting from foreign currency transactions are included in the consolidated statement of operations. Assets and liabilities denominated in foreign currencies at the balance sheet date are translated into each company’s denominated currency at period end exchange rates. All exchange differences are dealt with in the consolidated statements of operations.

The financial statements of the Company’s operations based outside of the United States have been translated into US$ in accordance with ASC 830. Management has determined that the functional currency for each of the Company’s foreign operations is its applicable local currency. When translating functional currency financial statements into US$, period-end exchange rates are applied to the consolidated balance sheets, while average period rates are applied to consolidated statements of operations. Translation gains and losses are recorded in translation reserve as a component of shareholders’ equity.

The exchange rates as of March 31, 2012 and December 31, 2011 are US$1: RMB6.2943 and US$1: RMB6.3009, respectively.

| 9 |

Property, Plant, Equipment and Depreciation

Property, plant and equipment are stated at cost. Depreciation is computed using the straight-line method to allocate the cost of depreciable assets over the estimated useful lives of the assets as follows:

| Estimated Useful Life (in years) | |

| Furniture and fixtures | 5-10 |

| Computer and office equipment | 5 |

| Motor vehicles | 5 |

| Properties | 20 |

Maintenance, repairs and minor renewals are charged directly to the statement of operations as incurred. Additions and improvements are capitalized. When assets are disposed of, the related cost and accumulated depreciation thereon are removed from the accounts and any resulting gain or loss is included in the statement of operations.

Investment property

Investment properties are stated at cost. Depreciation is computed using the straight-line method to allocate the cost of depreciable assets over the estimated useful lives of 20 years.

Significant additions that extend property lives are capitalized and are depreciated over their respective estimated useful lives. Routine maintenance and repair costs are expensed as incurred. The Company reviews its investment property for impairment whenever events or changes in circumstances indicate that the carrying amount of an investment property may not be recoverable.

Revenue Recognition

Agency commission revenue from property brokerage is recognized when the property developer and the buyer complete a property sales transaction, and the property developer grants confirmation to us to be able to invoice them accordingly. The time when we receive the commission is normally at the time when the property developer receives from the buyer a portion of the sales proceeds in accordance with the terms of the relevant property sales agreement, or the balance of the bank loan to the buyer has been funded, or recognized under the sales schedule or other specific items of agency sales agreement with developer. At no point does the Company handle any monetary transactions nor act as an escrow intermediary between the developer and the buyer.

Revenue from marketing consultancy services is recognized when services are provided to clients, fees associated to services are fixed or determinable, and collection of the fees is assured.

Rental revenue from property management and rental business is recognized on a straight-line basis according to the time pattern of the leasing agreements.

The Company accounts for underwriting sales in accordance with ASC 976-605 “Accounting for Sales of Real Estate” (SFAS 66). The commission revenue on underwriting sales is recognized when the criteria in SFAS No. 66 have been met, generally when title is transferred and the Company no longer has substantial continuing involvement with the real estate asset sold. If the Company provides certain rent guarantees or other forms of support where the maximum exposure to loss exceeds the gain, it defers the related commission income and expenses by applying the deposit method. In future periods, the commission income and related expenses are recognized when the remaining maximum exposure to loss is reduced below the amount of income deferred.

All revenues represent gross revenues less sales and business tax.

Net Earnings per Common Share

The Company computes net earnings per share in accordance with ASC 260, “Earnings per Share.” Under the provisions of ASC 260, basic net earnings per share is computed by dividing the net earnings available to common shareholders for the period by the weighted average number of shares of common stock outstanding during the period. The calculation of diluted net earnings per share recognizes common stock equivalents, however; potential common stock in the diluted EPS computation is excluded in net loss periods, as their effect is anti-dilutive.

Income Taxes

The Company accounts for income taxes in accordance with ASC 740 “Accounting for Income Taxes.” Under SFAS No. 109, deferred tax liabilities or assets at the end of each period are determined using the tax rate expected to be in effect when taxes are actually paid or recovered. Valuation allowances are established when necessary to reduce deferred tax assets to the amount expected to be realized.

| 10 |

We continue to account for income tax contingencies using a benefit recognition model. Beginning January 1, 2007, if we considered that a tax position is 'more likely than not' of being sustained upon audit, based solely on the technical merits of the position, we recognize the benefit. We measure the benefit by determining the amount that is greater than 50% likely of being realized upon settlement, presuming that the tax position is examined by the appropriate taxing authority that has full knowledge of all relevant information. These assessments can be complex and we often obtain assistance from external advisors.

Under the benefit recognition model, if our initial assessment fails to result in the recognition of a tax benefit, we regularly monitor our position and subsequently recognize the tax benefit if there are changes in tax law or analogous case law that sufficiently raise the likelihood of prevailing on the technical merits of the position to more likely than not; if the statute of limitations expires; or if there is a completion of an audit resulting in a settlement of that tax year with the appropriate agency.

Uncertain tax positions, represented by liabilities on our balance sheet, are now classified as current only when we expect to pay cash within the next 12 months. Interest and penalties, if any, continue to be recorded in Provision for taxes on income and are classified on the balance sheet with the related tax liability.

Historically, our policy had been to account for income tax contingencies based on whether we determined our tax position to be 'probable' under current tax law of being sustained, as well as an analysis of potential outcomes under a given set of facts and circumstances. In addition, we previously considered all tax liabilities as current once the associated tax year was under audit.

Segment information

The segments are generally determined based on the management of the businesses and on the basis of separate groups of operating activities, each with general operating autonomy over diversified products and services. The Company believes that it operates in one business segment. Management views the business as consisting of several revenue streams; however it is not possible to attribute assets or indirect costs to the individual streams other than direct expenses.

Recent Accounting Pronouncements

In 2011, new guidance was introduced to eliminate the current option to report other comprehensive income and its components in the statement of stockholders’ equity, and require an entity to present items of net income and other comprehensive income in one continuous statement, referred to as the statement of comprehensive income, or in two separate, but consecutive, statements. This guidance would be effective in the first quarter of 2012, with early adoption permitted. This pronouncement only changes the way we present other comprehensive income and its components, and does not impact our results of operations, financial position or cash flows.

In May 2011, the FASB issued ASU No. 2011-04, “Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs.” This ASU clarifies the concepts related to highest and best use and valuation premise, blockage factors and other premiums and discounts, the fair value measurement of financial instruments held in a portfolio and of those instruments classified as a component of shareowners’ equity. The ASU includes enhanced disclosure requirements about recurring Level 3 fair value measurements, the use of nonfinancial assets, and the level in the fair value hierarchy of assets and liabilities not recorded at fair value. The provisions of this ASU are effective prospectively for interim and annual periods beginning on or after December 15, 2011. Early application is prohibited. This ASU is not expected to have an impact currently on our financial statements or disclosures as there are presently no recurring Level 3 fair value measurements.

On August 17, 2010, the FASB and IASB issued an ED on lease accounting. The ED, released by the FASB as a proposed ASU, creates a new accounting model for both lessees and lessors and eliminates the concept of operating leases. The proposed ASU, if finalized, would converge the FASB’s and IASB’s accounting for lease contracts in most significant areas.

The Company does not anticipate that the adoption of the above statements will have a material effect on the Company's financial condition and results of operations.

| 11 |

NOTE 3 – RESTRICTED CASH

This restricted cash is the covenant from the bank loan described in Note 10.

NOTE 4- PROMISSORY DEPOSITS

The amount of $1,228,095 represents the deposits placed with several property developers in respect of a number of real estate projects where the Company is appointed as sales agent.

The balance of $2,319,559 represents the deposit for participating in a land auction in Sandong, the PRC.

NOTE 5 – INVENTORY

The amount of $1,082,917 belongs to Linyi Shang Yang Real Estate Development Company. This amount consists mainly of development, construction and property costs and expenses.

NOTE 6 - OTHER RECEIVABLES AND DEPOSITS

| March 31 | December 31 | |||||||

| 2012 | 2011 | |||||||

| Advances to staff | $ | 71,335 | $ | 65,632 | ||||

| Rental deposits | 108,525 | 99,927 | ||||||

| Prepaid rental | 201,136 | - | ||||||

| Prepayment for Linyi project | 8,499,754 | 482,219 | ||||||

| Other receivables | 280,297 | 216,035 | ||||||

| $ | 9,161,046 | $ | 863,813 | |||||

NOTE 7 – PROPERTY, PLANT AND EQUIPMENT – NET

| March 31, | December 31, | |||||||

| 2012 | 2011 | |||||||

| Furniture and fixtures | $ | 83,017 | $ | 77,292 | ||||

| Computer and office equipment | 235,016 | 242,346 | ||||||

| Motor vehicles | 794,740 | 789,943 | ||||||

| Properties | 2,465,276 | 2,399,866 | ||||||

| 3,578,049 | 3,509,447 | |||||||

| Less: Accumulated depreciation | (1,181,280 | ) | (1,103,618 | ) | ||||

| $ | 2,396,770 | $ | 2,405,829 | |||||

All above properties as of March 31, 2012 and as of December 31, 2011 were pledged to secure a bank loan in note 10.

NOTE 8 – INVESTMENT PROPERTIES

| March 31, | December 31, | |||||||

| 2012 | 2011 | |||||||

| Investment property | $ | 9,837,602 | $ | 9,827,298 | ||||

| Less: Accumulated depreciation | (3,074,025 | ) | (2,906,766 | ) | ||||

| $ | 6,763,577 | $ | 6,920,532 | |||||

The investment properties included one floor and four units of a commercial building in Suzhou, the PRC. The investment properties were acquired by the Company for long-term investment purposes.

All above properties as of March 31, 2012 and as of December 31, 2011 were pledged to secure a bank loan in note 10.

| 12 |

As of March 31, 2012, the four units of the investment properties were leased to a related party of the Company of 19% ownership, 82% of the total area of the one remaining floor was leased out.

NOTE 9 – LONG-TERM INVESTMENT

In mid 2011, we invested in a project company in Wuhan where the initial investment amount was $4,151,375 for a 49% equity stake. The purpose of this project company was for a residence development project in Wuhan. This investment is for our expansion into the real estate development business. We use the equity method of accounting for this long-term investment. The land is approximately 27,950 square meters with an estimated development period of three years, and we began the initial construction of the residence development project in the first quarter of 2012 The company’s total assets was $11,670,027 which consists primarily of inventory in the amount of $10,703,050 and cash and cash equivalent of $845,995, the total liability was $4,462,947 which consists primarily of promissory notes in the amount of $4,448,469 and a loss of $1,169,252 at the first quarter of 2012. As we used the equity accounting method, we decreased this investment by $572,933. The balance of this investment is $3,578,442 as of March 31 2012.

We invested $60,000 for a 40% equity stake to a new real estate agency company in February 2012. We use the equity method of accounting for this long-term investment. The company will not commence its operations until the second quarter of 2012 and therefore there was no profit or loss recorded for the period ended March 31, 2012.

The remaining amount of $106,290 was invested in various real estate agency sales related projects. All of the equity stakes we have in these projects are less than 20%. We used the cost method for accounting purposes for these investments.

NOTE 10 – BANK LOANS

Bank loans included two bank loans, as listed below:

The balance includes a bank loan of $8,738,064, which bears interest at 130% of the three-year prime rate as announced by the People’s Bank of China (the rate for 2012 was 6.65%) and is secured by the properties mentioned in Note 8 above. This loan is due on April 30, 2013 and can be extended automatically for another 3 years; however, the bank does an annual routine loan renewal request with the Company.

The remaining bank loan of $2,383,109 bears interest at 130% of three-year prime rate as announced by the People’s Bank of China (the rate for 2012 was 6.65%) and is secured by the properties mentioned in Note 7 above. This loan is due on April 30, 2013 and can be extended automatically for another 3 years; however, the bank does an annual routine loan renewal request with the Company.

NOTE 11 – PROMISSORY NOTES PAYABLE

The promissory notes payable consist of the following five unsecured notes to independent individual third parties.

The first note of $341,250,bears an interest at a rate of 15% per annum, consists of principal of $300,000 and interest of $41,250. This loan’s terms of repayment are not specifically defined.

The second note of $365,410 bears an interest rate of 15% per annum consists of principal of $317,748 and interest of $47,662. This loan’s terms of repayment are not specifically defined.

The third note of $915,709 bears an interest rate of 15% per annum consists of principal of $842,032 and interest of $73,678. This loan’s terms of repayment are not specifically defined.

The fourth note of $824,158 bears an interest rate of 15% per annum consists of principal of $794,370 and interest of $29,789. This loan’s terms of repayment are not specifically defined.

The fifth note of $235,134 bears no interest and the terms of repayment are not specifically defined.

| 13 |

NOTE 12 – AMOUNTS WITH RELATED PARTIES AND DIRECTORS

A related party is an entity that can control or significantly influence the management or operating policies of another entity to the extent one of the entities may be prevented from pursuing its own interests. A related party may also be any party the entity deals with that can exercise that control.

Amount due to directors

The total amount due to directors for March 31, 2012 was $5,493,406. The amounts due are as follows:

Amount due to Lin Chi-Jung

As of March 31, 2012, the balance includes one amount to and six loans obtained from Lin Chin-Jung.

The amount of $56,498 represented the salary payable and rental reimbursement to Lin Chin-Jung outstanding as of March 31, 2012.

A loan includes a principal of $106,898 is unsecured, consists of a principal of $103,778 and an interest of $3,120. This loan’s term is not specifically defined.

A loan includes a principal of $252,609. This loan’s interest rate is 18%, per annum consists of a principal of $238,311 and an interest of $14,298. This loan’s terms of repayment are not specifically defined.

A loan includes a principal of $4,420,880 bears an interest rate of 15%, per annum consists of a principal of $3,965,874 and an interest of $455,006. This loan’s the terms of repayment are not specifically defined. This loan is for the investment of Wuhan development project stated in note 8 in addition to any expenses related to the investment.

An unsecured loan of $592,536 bears an interest rate of 18% per annum consists of a principal of $476,622 and an interest of $115,914. This loan’s terms of repayment are not specifically defined

An unsecured loan includes a principal of $47,662, which is without interest and the terms of repayment are not specifically defined.

Amount due to Lin Chao-Chin

A balance of $9,264 represented the salary payable and rental reimbursement to Lin Chao-Chin outstanding as of March 31, 2012.

Amount due to Lin Hsin Hung

The amount of $7,059 represents the salary payable to Lin Hsin Hung.

Amout due from related company

This amount of $7,812 is due from WHYYL, our Wuhan project development company.

Amount due to related party

A balance of $87,381 is due to a related party of the Company of 19% ownership.

NOTE 13 - OTHER PAYABLES AND ACCRUED EXPENSES

| March 31, | December 31, | |||||||

| 2012 | 2011 | |||||||

| Accrued staff commission & bonus | $ | 585,055 | $ | 772,669 | ||||

| Rental deposits received | 527,038 | 529,308 | ||||||

| Accrual for onerous contracts | 16,563 | - | ||||||

| Other payables | 239,393 | 226,227 | ||||||

| Accrued legal fee | 87,149 | 87,149 | ||||||

| Customer deposits | 873,806 | 1,190,306 | ||||||

| Dividend payable for non-controlling interest | 255,093 | 254,826 | ||||||

| Rental deposits | 427,595 | 427,147 | ||||||

| $ | 3,011,692 | $ | 3,487,632 | |||||

| 14 |

NOTE 14– OTHER TAX PAYABLE

Other tax payable mainly represents the outstanding payables of business tax, urban real estate tax and land appreciation tax in the PRC.

NOTE 15 –DEPOSITS RECEIVED FROM UNDERWRTING SALES

The Company accounts for its underwriting sales revenue with underwriting rent guarantees in accordance with ASC 976-605 “Accounting for Sales of Real Estate” (SFAS 66). Under SFAS 66, the deposit method should be used for the revenue from the sales of floor space with underwriting rent guarantees until the revenues generated by sub-leasing properties exceed the guaranteed rental amount due to the purchasers.

NOTE 16- COMMITMENTS AND CONTINGENCIES

Operating Lease Commitments

During the years ended March 31, 2012 and 2011, the Company incurred lease expenses amounting to $12,932 and $233,050, respectively. As of March 31, 2012, the Company had commitments under operating leases, requiring annual minimum rentals as follows:

| March 31, | December 31, | |||||||

| 2012 | 2011 | |||||||

| Within one year | $ | 10,541 | $ | 24,770 | ||||

| Two to five years | - | - | ||||||

| Operating lease commitments | $ | 10,541 | $ | 24,770 | ||||

During the year of 2005 and 2006, SZGFH entered into leasing agreements with certain buyers of the Sovereign Building underwriting project to lease the properties for them. These leasing agreements on these properties are for 62% of the floor space that was sold to third party buyers. In accordance with the leasing agreements, the owners of the properties can have a rental return of 8.5% and 8.8% per annum for a period of 5 years and 8 years, respectively. In regards to the leasing agreements, we have negotiated with the buyers and have lowered the annual rental return rate for the remaining leasing period from 8.5% for 5 years to 5.8%, and from 8.8% for 8 years to 6%. As of March 31, 2012, 55% of the buyers agreed upon the lowered rate, 3% of the buyers did not agreed to a lowered rate and 42% of the buyers agreed to cancel the leasing agreements. The leasing period started in the second quarter, 2006, and the Company has the right to sublease the leased properties to cover these lease commitments in the leasing period. As of March 31, 2012, 82 sub-leasing agreements have been signed, the area of these sub-leasing agreements represented 88% of total area with these lease commitments.

As of March 31, 2012, the lease commitments are as follows:

| March 31,, | December 31, | |||||||

| 2012 | 2011 | |||||||

| Within one year | $ | 1,168,333 | $ | 1,451,207 | ||||

| Two to five years | 1,189,042 | 1,922,302 | ||||||

| Over five years | - | - | ||||||

| Operating lease commitments arising from the promotional package | $ | 2,357,375 | $ | 3,373,509 | ||||

An accrual for onerous contracts was recognized which is equal to the difference between the present value of the sublease income and the present value of the associated lease expense at the appropriate discount rate. The accrual for onerous contracts was $16,563 as of March 31, 2012 and $0 as of December 31, 2011.

According to the leasing agreements, the Company has an option to terminate any agreement by paying a predetermined compensation. As of March 31, 2012, the compensation to terminate all leasing agreements is $1,245,074. According to the sub-leasing agreements that have been signed through March 31, 2012, the rental income from these sub-leasing agreements will be $1,113,476 within one year and $534,884 within two to five years. However, no assurance can be given that we can collect all of the rental income.

| 15 |

NOTE 17 – STATUTORY RESERVE

According to the relevant corporation laws in the PRC, a PRC company is required to transfer at least 10% of its profit after taxes, as determined under accounting principles generally accepted in the PRC, to the statutory reserve until the balance reaches 50% of its registered capital. The statutory reserve can be used to make good on losses or to increase the capital of the relevant company.

NOTE 18 – ACCUMULATED OTHER COMPREHENSIVE INCOME

As of March 31, 2012 and 2011, the only component of accumulated other comprehensive income was translation reserve.

NOTE 19 – OTHER INCOME, NET

The amount $1,866,770 was a subsidy from the government for Linyi’s land purchase and to develop a real estate residential project. This subsidy’s purpose is to promote developers and companies to expand their business in the city of Linyi.

NOTE 20 – CONCENTRATION OF CUSTOMERS

During the years ended March 31, 2012 and 2011, the following customer accounted for more than 10% of total net revenue:

|

Percentage of Net Revenue for the years ended March 31, |

Percentage of Accounts Receivable as at March 31, | ||||||

| 2012 | 2011 | 2012 | 2011 | ||||

| Customer A | * | 13% | * | * | |||

| Customer B | 11% | * | * | * | |||

| Customer C | 25% | * | * | * | |||

* less than 10%

NOTE 21 – RESTATEMENT

The Company discovered errors to previously issued financial statements for the fiscal year ended December 31, 2011. The error was a miscalculation in our underwriting sales revenue and cost of sales under the Statement of Financial Accounting Standards No. 66 (“SFAS 66”).

The adjustment relates to the overstated of our net revenue by $305,495 and the cost of revenue by $107,028. As a result, our net revenue, cost of revenue and net losses was restated to $8,972,536, $6,231,262 and $1,416,822 respectively.

The adjustment also affected our balance sheet and cash flow of operation as summarized below.

| 16 |

The following summarizes the above restatements.

| Previously Reported | Adjustment | As Restated | ||||||||||||

| Balance Sheets | Deposits received from underwriting sales | 2,888,194 | 203,422 | 3,091,616 | ||||||||||

| Total liabilities | 25,258,982 | 203,422 | 25,462,404 | |||||||||||

| Accumulated losses | (10,208,331 | ) | (198,467 | ) | (10,406,798 | ) | ||||||||

| Accumulated other comprehensive income | 494,414 | (4,955 | ) | 489,459 | ||||||||||

| Total shareholders’ deficit | (3,088,299 | ) | (203,422 | ) | (3,291,721 | ) | ||||||||

| Statements of Operations | Net Revenues | 9,278,031 | (305,495 | ) | 8,972,536 | |||||||||

| Cost of Revenues | (6,338,290 | ) | 107,028 | (6,231,262 | ) | |||||||||

| Gross Profit | 2,939,741 | (198,467 | ) | 2,741,274 | ||||||||||

| Net Loss | (1,218,355 | ) | (198,467 | ) | (1,416,822 | ) | ||||||||

| Cash Flows | Net Loss | (1,218,355 | ) | (198,467 | ) | (1,416,822 | ) | |||||||

| Deposit from underwriting sales | (725,033 | ) | 198,468 | (526,565 | ) | |||||||||

| Net cash used in operating activities | (4,875,741 | ) | 1 | (4,875,740 | ) | |||||||||

| Effect of exchange rate changes on cash and cash equivalents | 61,380 | 1 | 61,381 | |||||||||||

NOTE 22 – SUBSEQUENT EVENT

None

| 17 |

ITEM 2 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANICAL CONDITION AND RESULTS OF OPERATIONS

RISKS ASSOCIATED WITH FORWARD-LOOKING STATEMENTS INCLUDED IN THIS FORM 10-Q

In addition to historical information, this Form 10-Q contains forward-looking statements. Forward-looking statements are based on our current beliefs and expectations, information currently available to us, estimates and projections about our industry, and certain assumptions made by our management. These statements are not historical facts. We use words such as "anticipates", "expects", "intends", "plans", "believes", "seeks", "estimates", and similar expressions to identify our forward-looking statements, which include, among other things, our anticipated revenue and cost of our agency and investment business.

Because we are unable to control or predict many of the factors that will determine our future performance and financial results, including future economic, competitive, and market conditions, our forward-looking statements are not guarantees of future performance. They are subject to risks, uncertainties, and errors in assumptions that could cause our actual results to differ materially from those reflected in our forward-looking statements. We believe that the assumptions underlying our forward-looking statements are reasonable. However, the investor should not place undue reliance on these forward-looking statements. They only reflect our view and expectations as of the date of this Form 10-Q. We undertake no obligation to publicly update or revise any forward-looking statement in light of new information, future events, or other occurrences.

There are several risks and uncertainties, including those relating to our ability to raise money and grow our business and potential difficulties in integrating new acquisitions with our current operations, especially as they pertain to foreign markets and market conditions. These risks and uncertainties can materially affect the results predicted. The Company’s future operating results over both the short and long term will be subject to annual and quarterly fluctuations due to several factors, some of which are outside our control. These factors include but are not limited to fluctuating market demand for our services, and general economic conditions.

The following Management’s Discussion and Analysis (“MD&A”) is intended to help the reader understand Sunrise Real Estate Group, Inc. (“SRRE”). MD&A is provided as a supplement to, and should be read in conjunction with, our financial statements and the accompanying notes.

| 18 |

OVERVIEW

In October 2004, the former shareholders of Sunrise Real Estate Development Group, Inc. (Cayman Islands) (“CY-SRRE”) and LIN RAY YANG Enterprise Ltd. (“LRY”) acquired a majority of our voting interests in a share exchange. Before the completion of the share exchange, SRRE had no continuing operations, and its historical results would not be meaningful if combined with the historical results of CY-SRRE, LRY and their subsidiaries.

As a result of the acquisition, the former owners of CY-SRRE and LRY hold a majority interest in the combined entity. Generally accepted accounting principles require in certain circumstances that a company whose shareholders retain the majority voting interest in the combined business be treated as the acquirer for financial reporting purposes. Accordingly, the acquisition has been accounted for as a “reverse acquisition” arrangement whereby CY-SRRE and LRY are deemed to have purchased SRRE. However, SRRE remains the legal entity and the Registrant for Securities and Exchange Commission reporting purposes. The historical financial statements prior to October 5, 2004 are those of CY-SRRE and LRY and their subsidiaries. All equity information and per share data prior to the acquisition have been restated to reflect the stock issuance as a recapitalization of CY-SRRE and LRY.

SRRE and its subsidiaries, namely, CY-SRRE, LRY, Shanghai Xin Ji Yang Real Estate Consultation Company Limited (“SHXJY”), Shanghai Shang Yang Real Estate Consultation Company, Ltd. (“SHSY”), Suzhou Gao Feng Hui Property Management Company, Ltd, (“SZGFH”), Suzhou Shang Yang Real Estate Consultation Company (“SZSY”), Suzhou Xin Ji Yang Real Estate Consultation Company, Ltd. (“SZXJY”), Linyi Shang Yang Real Estate Development Company Ltd (“LYSH”), Shangqiu Shang Yang Real Estate Consultation Company, Ltd., (“SQSY”), Wuhan Gao Feng Hui Consultation Company Ltd.(WHGFH), Sanya Shang Yang Real Estate Consultation Company, Ltd. (“SYSH”), Shanghai Rui Jian Design Company, Ltd., (“SHRJ”), and Wuhan Yuan Yu Long Real Estate Development Company, Ltd. (“WHYYL”) are sometimes hereinafter collectively referred to as “the Company,” “our,” or “us”.

The principal activities of the Company are property development, property brokerage services, real estate marketing services, property leasing services and property management services in the PRC.

RECENT DEVELOPMENTS

Our major business was agency sales, whereby our Chinese subsidiaries contracted with property developers to market and sell their newly developed property units. For these services we earned a commission fee calculated as a percentage of the sales prices. We have focused our sales on the whole China market, especially in secondary cities. To expand our agency business, we have established subsidiaries in Shanghai, Suzhou, Beijing, Kunshan and Hainan, and branches in Nanchang, Yangzhou, Nanjing, Chongqing, Wuhan, Linyi and Shangqiu

During 2005 and 2006, SZGFH entered into leasing agreements with certain buyers of the Sovereign Building underwriting project to lease the properties for them. These leasing agreements on these properties are for 62% of the floor space that was sold to third party buyers. In accordance with the leasing agreements, the owners of the properties can have a rental return of 8.5% and 8.8% per annum for a period of 5 years and 8 years, respectively. In regards to the leasing agreements, we have negotiated with the buyers and have lowered the annual rental return rate for the remaining leasing period from 8.5% for 5 years to 5.8%, and from 8.8% for 8 years to 6%.Till the end of March 31, 2012, 55% of the buyers agreed upon the lowered rate, 3% of the buyers did not agreed to a lowered rate and 42% of the buyers agreed to cancel the leasing agreements. The leasing period started in the second quarter of 2006, and the Company has the right to sublease the leased properties to cover these lease commitments in the leasing period. As of March 31, 2012, 82 sub-leasing agreements have been signed and the area of these sub-leasing agreements represented 88% of the total area with these lease commitments.

In mid 2011, we established a project company in Wuhan where we have a 49% stake. The purpose of this project company is for a residence development project in Wuhan. During the fourth quarter of 2011, the project company was in the process of acquiring land and obtaining the appropriate license and certificate for the development project. In the first quarter of 2012, we began its initial construction. The land is approximately 27,950 square meters with an estimated development period of three years.

In January 2012, we established a Linyi Shang Yang Real Estate Development Company Limited(“LYSY”) with 24% stake in the company. During the first quarter of 2012, we acquired approximately 103,385 square meters for the purpose of developing villa-style residential housing, and began the initial construction.

We invested $60,000 for 40% equity stake to a new real estate agency company in February 2012. The company will not commence its operations until the second quarter of 2012 and therefore there were no profit or loss recorded for the period ended March 31, 2012.

| 19 |

Due to the lack of business and the continuing losses of the Beijing Xin Jin Yang and Kunshan Shang Yang subsidiaries, we are dissolving these two subsidiaries in 2012.

RECENTLY ISSUED ACCOUNTING STANDARDS

In 2011, new guidance was introduced to eliminate the current option to report other comprehensive income and its components in the statement of stockholders’ equity, and require an entity to present items of net income and other comprehensive income in one continuous statement, referred to as the statement of comprehensive income, or in two separate, but consecutive, statements. This guidance would be effective in the first quarter of 2012, with early adoption permitted. This pronouncement only changes the way we present other comprehensive income and its components, and does not impact our results of operations, financial position or cash flows.

In May 2011, the FASB issued ASU No. 2011-04, “Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs.” This ASU clarifies the concepts related to highest and best use and valuation premise, blockage factors and other premiums and discounts, the fair value measurement of financial instruments held in a portfolio and of those instruments classified as a component of shareowners’ equity. The ASU includes enhanced disclosure requirements about recurring Level 3 fair value measurements, the use of nonfinancial assets, and the level in the fair value hierarchy of assets and liabilities not recorded at fair value. The provisions of this ASU are effective prospectively for interim and annual periods beginning on or after December 15, 2011. Early application is prohibited. This ASU is not expected to have an impact currently on our financial statements or disclosures as there are presently no recurring Level 3 fair value measurements.

On August 17, 2010, the FASB and IASB issued an ED on lease accounting. The ED, released by the FASB as a proposed ASU, creates a new accounting model for both lessees and lessors and eliminates the concept of operating leases. The proposed ASU, if finalized, would converge the FASB’s and IASB’s accounting for lease contracts in most significant areas.

The Company does not anticipate that the adoption of the above statements will have a material effect on the Company's financial condition and results of operations.

APPLICATION OF CRITICAL ACCOUNTING POLICIES

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Critical accounting policies for us include revenue recognition, net earnings per common share, income taxes and segment information.

Revenue Recognition

Agency commission revenue from property brokerage is recognized when the property developer and the buyer complete a property sales transaction, and the property developer grants confirmation to us to be able to invoice them accordingly. The time when we receive the commission is normally at the time when the property developer receives from the buyer a portion of the sales proceeds in accordance with the terms of the relevant property sales agreement, or the balance of the bank loan to the buyer has been funded, or recognized under the sales schedule or other specific items of agency sales agreement with developer. At no point does the Company handle any monetary transactions nor act as an escrow intermediary between the developer and the buyer.

Revenue from marketing consultancy services is recognized when services are provided to clients, fees associated to services are fixed or determinable, and collection of the fees is assured.

Rental revenue from property management and rental business is recognized on a straight-line basis according to the time pattern of the leasing agreements.

The Company accounts for underwriting sales in accordance with the FASB guidance of ASC Topic 360, “Property, Plant and Equipment”. The commission revenue on underwriting sales is recognized when the criteria in ASC 360 have been met, generally when title is transferred and the Company no longer has substantial continuing involvement with the real estate asset sold. If the Company provides certain rent guarantees or other forms of support where the maximum exposure to loss exceeds the gain, it defers the related commission income and expenses by applying the deposit method. In future periods, the commission income and related expenses are recognized when the remaining maximum exposure to loss is reduced below the amount of income deferred.

| 20 |

All revenues represent gross revenues less sales and business tax.

Net Earnings per Common Share

The Company computes net earnings per share in accordance with SFAS No. 128, “Earnings per Share.” Under the provisions of SFAS No. 128, basic net earnings per share is computed by dividing the net earnings available to common shareholders for the period by the weighted average number of shares of common stock outstanding during the period. The calculation of diluted net earnings per share recognizes common stock equivalents, however; potential common stock in the diluted EPS computation is excluded in net loss periods, as their effect is anti-dilutive.

Income Taxes

The Company accounts for income taxes in accordance with SFAS No. 109 “Accounting for Income Taxes.” Under SFAS No. 109, deferred tax liabilities or assets at the end of each period are determined using the tax rate expected to be in effect when taxes are actually paid or recovered. Valuation allowances are established when necessary to reduce deferred tax assets to the amount expected to be realized.

Segment Information

The segments are generally determined based on the management of the businesses and on the basis of separate groups of operating activities, each with general operating autonomy over diversified products and services. The Company believes that it operates in one business segment. Management views the business as consisting of several revenue streams; however it is not possible to attribute assets or indirect costs to the individual streams other than direct expenses.

RESULTS OF OPERATIONS

We provide the following discussion and analyses of our changes in financial condition and results of operations for the year ended March 31, 2012 with comparisons to the historical year ended March 31, 2011.

Revenue

The following table shows the net revenue detail by line of business:

| Three months ended March 31 | |||||||||

| 2012 | % to total | 2011 | % to total | % change | |||||

| Agency sales | 1,139,990 | 74 | 1,855,354 | 71 | (39) | ||||

| Underwriting sales | 0 | 0 | 159,666 | 6 | (100) | ||||

| Property management | 409,371 | 26 | 589,604 | 23 | (31) | ||||

| Net revenue | 1,549,361 | 100 | 2,604,624 | 100 | (41) | ||||

The net revenue in the first quarter, 2012 was $1,549,361, which decreased by 41% from $2,604,624 in the first quarter of 2011. In the first quarter of 2012, agency sales represented 74% of net revenue, underwriting sales represented 0% and property management represented 26%. The decrease in net revenue in the first quarter of 2012 was mainly due to the decrease in our agency sales.

Agency sales

Agency sales represented 74% of our net revenue in the first quarter of 2012 and revenue from agency sales decreased by 39% compared with same period in 2011. The primary reason was that:

a) There were 13 agency sales projects contributing to our net revenue in the first quarter of 2012, compared to 17 agency sales projects in the same period in 2011.

b) There were 3 projects that contributed $571,842 in revenue in the first quarter of 2011, but closed during 2011.

| 21 |

Because of our diverse market locations, the risk of market fluctuations has been decreased on our business operations in agency sales in 2012, and we are continually seeking stable growth in our agency sales business in 2012. The macro policies in 2011 and carrying over to 2012 aimed to cool real estate prices and has affected many business in the real estate industry. This effect is evident in our decrease in our agency sales. We are continually seeking stable growth in our agency sales business in 2012. However, there can be no assurance that we will be able to do so.

Underwriting Sales

In February 2004, SHSY entered into an agreement to underwrite an office building in Suzhou, known as Suzhou Sovereign Building. Being the sole distribution agent for this office building, SHSY committed to a sales target of $56.53 million. Property underwriting sales are comparatively a higher risk business model compared to our pure commission based agency business. Under this higher risk business model, the Underwriting Model, our commission is not calculated as a percentage of the selling price; instead, our commission revenue is equivalent to the price difference between the final selling price and underwriting price. We negotiate with a developer for an underwriting price that is as low as possible, with the guarantee that all or a majority of the units will be sold by a specific date. In return, we are given the flexibility to establish the final selling price and earn the price difference between the final selling price and the underwriting price. The risk of this kind of arrangement is that if there is any unsold unit on the expiration date of the agreement, we may have to absorb the unsold property units from developers at the underwriting price and hold them in our inventory or as investments.

We started selling units in the Sovereign Building in January, 2005. As of March 1 2007, we had sold or acquired all of the units in the building, and we achieved the sales target by selling 47,093 square meters with a total sales price of $75.96 million.

The Company accounts for its underwriting sales revenue with underwriting rent guarantees in accordance with SFAS No. 66 “Accounting for Sales of Real Estate” (SFAS 66). Under SFAS 66, the deposit method should be used for the revenue from the sales of floor space with underwriting rent guarantees until the revenues generated by sub-leasing properties exceed the guaranteed rental amount due to the purchasers. Based on this accounting principle, a significant portion of underwriting revenue was deferred. In early 2009, the Company negotiated the rental payments with purchasers in the Sovereign Building. As of March 31, 2012, 55% of the buyers agreed upon the lowered rate and 3% of the buyers did not agree to a lowered rate and 42% of the buyers canceled the leasing agreements. Based on the new agreements, a portion of underwriting sales can be realized.

Property Management

During 2005 and 2006, SZGFH entered into leasing agreements with certain buyers of the Sovereign Building underwriting project to lease the properties for them. These leasing agreements on these properties are for 62% of the floor space that was sold to third party buyers. In accordance with the leasing agreements, the owners of the properties can have a rental return of 8.5% and 8.8% per annum for a period of 5 years and 8 years, respectively. In regards to the leasing agreements, we have negotiated with the buyers and have lowered the annual rental return rate for the remaining leasing period from 8.5% for 5 years to 5.8%, and from 8.8% for 8 years to 6%. As of March 31, 2012, 55% of the buyers agreed upon the lowered rate, 3% of the buyers did not agree to a lowered rate and 42% of the buyers agreed to cancel the leasing agreements. The leasing period started in the second quarter, 2006, and the Company has the right to sublease the leased properties to cover these lease commitments in the leasing period. As of March 31, 2012, 82 sub-leasing agreements have been signed and the area covered by these sub-leasing agreements represented 88% of the total area subject to these lease commitments.

We expect that the income from the sub-leasing business will be on a stable growth trend in 2012 and that it can cover the lease commitments in the leasing period as a whole. We expect that these properties will be leased out in 2012 and the gross margin will be improved. However there can be no assurance that we will achieve these objectives.

| 22 |

Cost of Revenue

The following table shows the cost of revenue detail by line of business:

| Three months ended March 31, | |||||||||

| 2012 | % to total | 2011 | % to total | % change | |||||

| Agency sales | 720,175 | 65 | 1,186,664 | 68 | (39) | ||||

| Underwriting sales | 0 | 0 | 23,532 | 1 | (100) | ||||

| Property management | 389,738 | 35 | 529,145 | 31 | (26) | ||||

| Cost of revenue | 1,109,913 | 100 | 1,739,341 | 100 | (36) | ||||

The cost of revenue in the first quarter of 2012 was $1,109,913, a decrease of 36% from $1,739,341 in the same period in 2011. In the first quarter of 2012, agency sales represented 65% of cost of revenue, underwriting sales represented 0% and property management represented 35%. The decrease in cost of revenue in first quarter of 2012 was mainly due to the decrease in our agency sales.

Agency sales

The cost of revenue for agency sales in the first quarter, 2012 was $720,175, a decrease of 39% from $1,186,664 in the same period in 2011. This decrease was mainly due to the decrease in our commissions and consulting fees in the first quarter of 2012, compared to the same period in 2011, the decrease of such expenses was $176,620 and $368,072 respectively.

Underwriting Sales

The cost of underwriting sales represents selling costs, such as staff costs and advertising expenses, associated with underwriting sales.

Property management

The cost of revenue for property management in the first quarter of 2012 was $389,738, decreased by 26% from $529,145 in the same period in 2011. This was mainly due to lower business for the property management as a whole.

An accrual for onerous contracts recognized which is equal to the difference between the present value of the sublease income and the present value of the associated lease expense at the appropriate discount rate. The accrual for onerous contracts was $ 16,563 as of March 31, 2012 and $0 as of December 31, 2011.

Operating Expenses

The following table shows operating expenses detail by line of business:

| Three months ended March 31, | |||||||||

| 2012 | % to total | 2011 | % to total | % change | |||||

| Agency sales | 255,145 | 90 | 291,457 | 86 | (12) | ||||

| Property management | 29,075 | 10 | 47,447 | 14 | (39) | ||||

| Property Development | 0 | 0 | 0 | - | - | ||||

| Operating expenses | 284,220 | 100 | 338,904 | 100 | (16) | ||||

The operating expenses in the first quarter, 2012 were $284,220, a decrease of 16% from $338,904, in the same period in 2011. In the first quarter of 2012, agency sales represented 90% of operating expenses and property management represented 10%. The decrease in operating expenses in the first quarter of 2012 was mainly due to the decrease in our agency sales.

| 23 |

Agency sales

The operating expenses for agency sales in the first quarter of 2012 were $255,145 which decreased by 12% from $291,457 in the same period in 2011. This decrease was mainly due to the decrease in fit-out fee, there was $48,858 of such fee in the first quarter of 2011, and none in 2012.

Property management

The operating expenses for property management in the first quarter, 2012 were $29,075, decreased by 39% from $47,447 in the same period in 2011. This decrease was mainly due to the decrease in sales commission, which decreased $16,483 in the first quarter of 2012 compared to 2011.

General and Administrative Expenses

The general and administrative expenses in the first quarter of 2012 were $1,035,876, increased by 50% from $692,190 in the same period in 2011. This increase was mainly due to the increase in staff cost, office expense and fit-out fee of $75,684, $99,106 and $49,102 compared to the same period in 2011, respectively.

Interest Expenses

Interest expenses in the first quarter, 2012 were $491,451 increased by 155% from $192,975 in the same period in 2011. The interest expenses were mainly incurred for bank loans, promissory notes payable and amount due to directors.

Major Related Party Transaction

A related party is an entity that can control or significantly influence the management or operating policies of another entity to the extent one of the entities may be prevented from pursuing its own interests. A related party may also be any party the entity deals with that can exercise that control.

Amount due to directors

The total amount due to directors for March 31, 2012 was $5,493,406. The amounts due are as follows:

Amount due to Lin Chi-Jung

As of March 31, 2012, the balance includes one amount to and six loans obtained from Lin Chin-Jung.

The amount of $56,498 represented the salary payable and rental reimbursement to Lin Chin-Jung outstanding as of March 31, 2012.

A loan includes a principal of $106,898 is unsecured, consists of a principal of $103,778 and an interest of $3,120. This loan’s term is not specifically defined.

A loan includes a principal of $252,609. This loan’s interest rate is 18%, per annum consists of a principal of $238,311 and an interest of $14,298. This loan’s terms of repayment are not specifically defined.

A loan includes a principal of $4,420,880 bears an interest rate of 15%, per annum consists of a principal of $3,965,874 and an interest of $455,006. This loan’s the terms of repayment are not specifically defined. This loan is for the investment of Wuhan development project stated in note 8 in addition to any expenses related to the investment.

An unsecured loan of $592,536 bears an interest rate of 18% per annum consists of a principal of $476,622 and an interest of $115,914. This loan’s terms of repayment are not specifically defined

An unsecured loan includes a principal of $47,662, which is without interest and the terms of repayment are not specifically defined.

Amount due to Lin Chao-Chin

A balance of $9,264 represented the salary payable and rental reimbursement to Lin Chao-Chin outstanding as of March 31, 2012.

| 24 |

Amount due to Lin Hsin Hung

The amount of $7,059 represents the salary payable to Lin Hsin Hung.

Amout due from related company

This amount of $7,812 is due from WHYYL, our Wuhan project development company.

Amount due to related party

A balance of $87,381 is due to a related party of the Company of 19% ownership.

LIQUIDITY AND CAPITAL RESOURCES

In the first quarter of 2012, our principal sources of cash were revenues from our agency sales and property management business. Most of our cash resources were used to fund our property development investment and revenue related expenses, such as salaries and commissions paid to the sales force, daily administrative expenses and the maintenance of regional offices.

We ended the period with a cash position of $3,940,520.

The Company’s operating activities used cash in the amount of $8,820,708, which was primarily attributable to the other receivables and deposits.

The Company’s investing activities used cash resources of $124,041, which was primarily attributable to the acquisition of property, plant and equipment and long-term investments.

The Company’s financing activities obtained cash resources of $11,492,188, which was primarily attributable to funds received from capital increase.

The potential cash needs for 2012 will be the repayments of our bank loans and promissory notes, the rental guarantee payments and promissory deposits for various property projects as well as our development projects in Wuhan and Linyi.

Capital Resources

We currently have two bank loans payable, including an $8,738,064 loan 2,383,109 loan. Both of the loans are due on April 30, 2013 and can be extended automatically for another 3 years, however, the bank does an annual routine loan renewal request with the Company.

Taking into account of our cash position, available credit facilities and cash generated from operating activities, we believe that we have sufficient funds to operate our existing business for the next twelve months. If our business otherwise grows more rapidly than we currently predict, we plan to raise funds through the issuance of additional shares of our equity securities in one or more public or private offerings. We will also consider raising funds through credit facilities obtained with lending institutions. There can be no guarantee that we will be able to obtain such funds through the issuance of debt or equity or obtain funds that are with terms satisfactory to management and our board of directors.

OFF BALANCE SHEET ARRANGEMENTS

The Company has no off-balance sheet arrangements.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

A smaller reporting company is not required to provide the information required by this item.

| 25 |

ITEM 4. CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

Under the supervision and with the participation of our management, including our Chief Executive Officer and Principal Financial Officer, we evaluated the effectiveness of the design and operation of our disclosure controls and procedures (as defined in Rule 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934 (the "Exchange Act") as of March 31, 2012.