Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K Q1-13 RESULTS RELEASE - DYCOM INDUSTRIES INC | form8k.htm |

| EX-99.1 - EXHIBIT 99.1 - DYCOM INDUSTRIES INC | exhibit991.htm |

Exhibit 99.2

Review of Acquisition of

Quanta Services’ Telecommunications

Infrastructure Services Subsidiaries

Infrastructure Services Subsidiaries

Fiscal 2013

1st Quarter Presentation

November 20, 2012

2

Participants

|

Steven E. Nielsen

President & Chief Executive Officer Timothy R. Estes

Chief Operating Officer

H. Andrew DeFerrari

Chief Financial Officer Richard B. Vilsoet

General Counsel |

3

Forward-Looking Statements and

Non-GAAP Information

Non-GAAP Information

Forward-Looking Statements and

Non-GAAP Information

Non-GAAP Information

Fiscal 2013 first quarter results are unaudited. This presentation contains “forward-looking statements” which are statements

relating to future events, including a proposed acquisition, future financial performance, strategies, expectations, and the

competitive environment. All statements, other than statements of historical facts, contained in this presentation, including

statements regarding the Company’s future financial position, future revenue, prospects, plans and objectives of

management, are forward-looking statements. Additionally, forward -looking statements include statements of expectations

regarding the proposed acquisition, including expected benefits and synergies of the transaction, future financial and

operating results, future opportunities for the combined businesses and other statements regarding events or developments

that the Company believes or anticipates will or may occur in the future as a result of the transaction. Words such as

“believe,” “expect,” “anticipate,” “estimate,” “intend,” “forecast,” “may,” “should,” “could,” “project,” “looking ahead” and similar

expressions, as well as statements in future tense, identify forward-looking statements. You should not read forward looking

statements as a guarantee of future performance or results. They will not necessarily be accurate indications of whether or

at what time such performance or results will be achieved. Forward-looking statements are based on information available

at the time those statements are made and/or management’s good faith belief at that time with respect to future

events, including the Company’s ability to consummate the proposed acquisition. Such statements are subject to risks and

uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the

forward-looking statements. Important factors that could cause such differences include, but are not limited to factors

described under Item 1A, “Risk Factors” of the Company’s Annual Report on Form 10-K for the year ended July 28, 2012,

and other risks outlined in the Company’s periodic filings with the Securities and Exchange Commission (“SEC”). The

forward-looking statements in this presentation are expressly qualified in their entirety by this cautionary statement. Except

as required by law, the Company may not update forward-looking statements even though its situation may change in the

future.

relating to future events, including a proposed acquisition, future financial performance, strategies, expectations, and the

competitive environment. All statements, other than statements of historical facts, contained in this presentation, including

statements regarding the Company’s future financial position, future revenue, prospects, plans and objectives of

management, are forward-looking statements. Additionally, forward -looking statements include statements of expectations

regarding the proposed acquisition, including expected benefits and synergies of the transaction, future financial and

operating results, future opportunities for the combined businesses and other statements regarding events or developments

that the Company believes or anticipates will or may occur in the future as a result of the transaction. Words such as

“believe,” “expect,” “anticipate,” “estimate,” “intend,” “forecast,” “may,” “should,” “could,” “project,” “looking ahead” and similar

expressions, as well as statements in future tense, identify forward-looking statements. You should not read forward looking

statements as a guarantee of future performance or results. They will not necessarily be accurate indications of whether or

at what time such performance or results will be achieved. Forward-looking statements are based on information available

at the time those statements are made and/or management’s good faith belief at that time with respect to future

events, including the Company’s ability to consummate the proposed acquisition. Such statements are subject to risks and

uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the

forward-looking statements. Important factors that could cause such differences include, but are not limited to factors

described under Item 1A, “Risk Factors” of the Company’s Annual Report on Form 10-K for the year ended July 28, 2012,

and other risks outlined in the Company’s periodic filings with the Securities and Exchange Commission (“SEC”). The

forward-looking statements in this presentation are expressly qualified in their entirety by this cautionary statement. Except

as required by law, the Company may not update forward-looking statements even though its situation may change in the

future.

This presentation includes certain “Non-GAAP” financial measures as defined by SEC rules. We believe that the

presentation of certain Non-GAAP financial measures provides information that is useful to investors because it allows for a

more direct comparison of our performance for the period with our performance in the comparable prior-year periods. As

required by the SEC, we have provided a reconciliation of those measures to the most directly comparable GAAP measures

on the Regulation G slides included as slides 19 through 22 of this presentation. We caution that Non-GAAP financial

measures should be considered in addition to, but not as a substitute for, our reported GAAP results.

presentation of certain Non-GAAP financial measures provides information that is useful to investors because it allows for a

more direct comparison of our performance for the period with our performance in the comparable prior-year periods. As

required by the SEC, we have provided a reconciliation of those measures to the most directly comparable GAAP measures

on the Regulation G slides included as slides 19 through 22 of this presentation. We caution that Non-GAAP financial

measures should be considered in addition to, but not as a substitute for, our reported GAAP results.

4

Overview of the Transaction

n Purchase price of approximately $275 million, subject to

adjustments for working capital and other specified items

adjustments for working capital and other specified items

n Subsidiaries acquired represent substantially all of Quanta’s

domestic telecommunications infrastructure services operations

domestic telecommunications infrastructure services operations

n Financed through a new $400 million senior secured credit facility

n Expected to close by December 31, 2012

5

Strategic Rationale

n Strengthens our customer base, geographic scope, and technical

service offerings

service offerings

n Reinforces our rural engineering and construction capabilities,

wireless construction resources, and broadband construction

competencies

wireless construction resources, and broadband construction

competencies

n Creates scale as industry announcements indicate customer

expenditures will be growing

expenditures will be growing

n Attractive financing environment drives strong investment returns

n Experienced management team with solid industry reputation

6

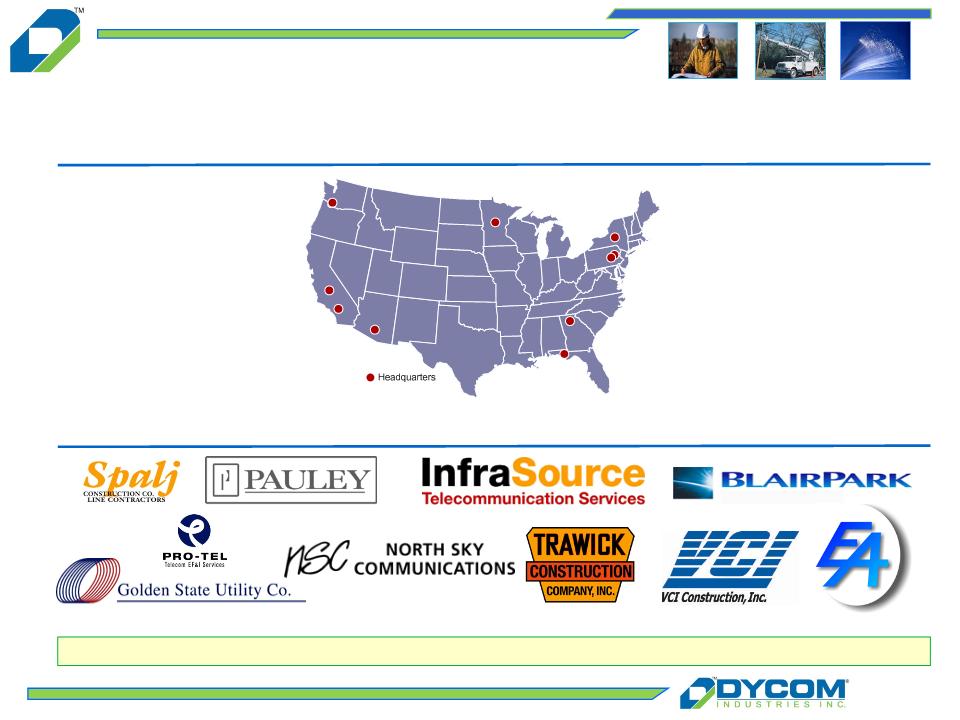

Nationwide Operations

Well-known subsidiaries strengthen Dycom’s geographic reach

Operating Headquarter Locations

Subsidiaries

7

Dycom Pro Forma Customer Mix

Note: Dycom financials reflect July 2012 fiscal year end. Quanta’s telecommunications infrastructure services subsidiaries reflects trailing twelve months ended September 30, 2012.

Transaction strengthens existing customer relationships and diversifies customer base

|

Revenue:

|

$1.2 billion

|

$0.5 billion

|

$1.7 billion

|

8

Financing and Liquidity

n Financing to be provided by a new, five-year $400 million senior

secured credit facility

secured credit facility

} $125 million term loan A

} Revolver borrowings

n Terms and covenants that reflect a larger combined business

n Ample cash flows expected to reduce borrowings in the near to

intermediate term

intermediate term

n Acquisition structured to produce attractive tax benefits

n Strong balance sheet and ample liquidity

9

Looking Ahead

n Revenue from acquired subsidiaries for calendar year 2013

expected to range from $400 million to $450 million

expected to range from $400 million to $450 million

n One-time transaction and integration costs of approximately $12

million to $15 million

million to $15 million

n Excluding one-time costs, currently expecting $0.05 to $0.10 per

share of earnings accretion on an annual basis, after non-cash

amortization expense

share of earnings accretion on an annual basis, after non-cash

amortization expense

n Pleased to grow our company with a strong complementary

management team and dedicated employees

management team and dedicated employees

Dycom Fiscal 2013

1st Quarter Results

11

Q1-2013 Overview

n Contract revenue of $323.3 million as compared to $319.6 million in the prior

year quarter

year quarter

n Contract revenue grew organically 2.4%, excluding storm restoration services

of $3.7 million in Q1-12

of $3.7 million in Q1-12

n Adjusted EBITDA of $40.4 million at 12.5% of revenue in Q1-13

n Non-GAAP Net income of $0.36 per share diluted compared to $0.38 per

share diluted in Q1-12

share diluted in Q1-12

n Repurchased 1,047,000 common shares at an average price of $14.52 per

share during the quarter

share during the quarter

See “Regulation G Disclosure” slides 19-22 for a reconciliation of GAAP to Non-GAAP financial measures.

12

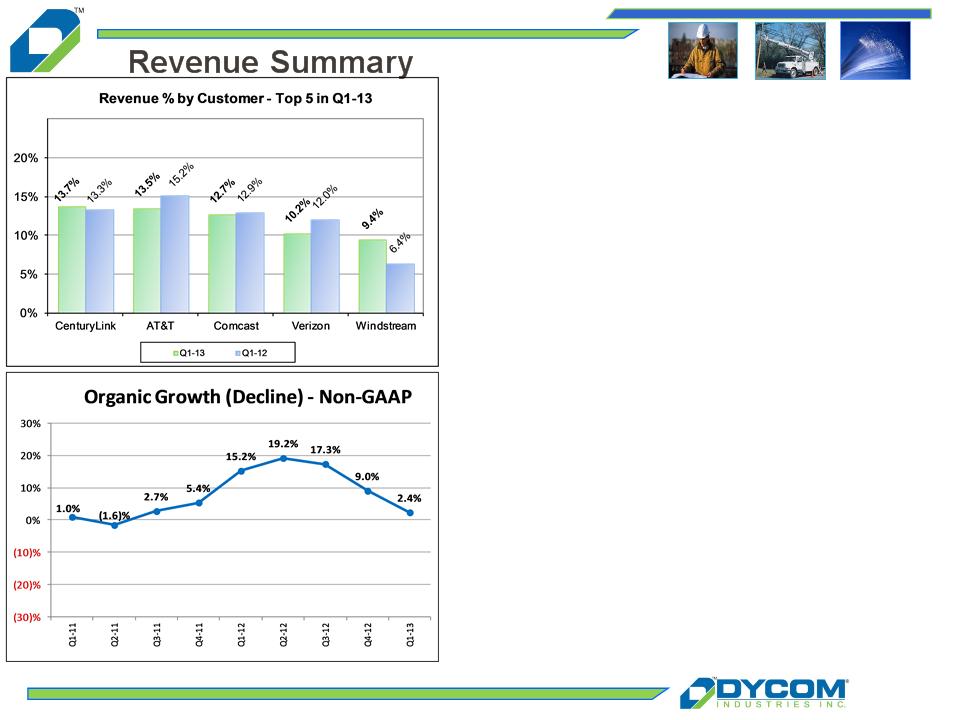

Note: See “Regulation G Disclosure” slides 19-22 for reconciliation of GAAP to Non-GAAP financial measures.

n Top 5 customers represented 59.6% of revenue in

Q1-13 and 59.9% in Q1-12

Q1-13 and 59.9% in Q1-12

Ø CenturyLink, Dycom’s largest customer, grew

organically 8.4% year over year

organically 8.4% year over year

Ø Windstream, Dycom’s fifth largest customer, grew

in excess of 47% year over year

in excess of 47% year over year

n Organic revenue growth of 2.4%, excluding revenue from

storm restoration services in each period

storm restoration services in each period

Ø Revenue from Top 5 customers up 1.8%

organically

organically

Ø Combined revenue from other customers up 3.1%

organically

organically

13

Backlog and Awards

Current Awards and Extensions

|

Customers

|

Description

|

Area

|

Approximate Term

(in years) |

|

nAT&T

|

Construction and Maintenance Services

|

South Carolina

|

3

|

|

nCharter Communications

|

Construction and Maintenance Services

|

Alabama

|

1

|

|

nTime Warner Cable

|

Underground Facility Locating

|

California

|

1

|

|

nQuestar Gas

|

Pipeline Construction Projects

|

Utah

|

1

|

|

nVarious

|

Rural broadband

|

Kentucky, Georgia, North Carolina,

Missouri |

1

|

14

Summary Results

|

($ in millions,

except per share data)

|

Q1-12

|

Q1-13

|

|

Net Income-Non

GAAP |

$ 13.0

|

$ 12.3

|

|

Fully Diluted EPS-

Non-GAAP |

$0.38

|

$0.36

|

Organic revenue growth of 2.4%, after adjusting for storm work

in Q1-12

in Q1-12

Adjusted EBITDA remains strong at $40.4 million

Non-GAAP EPS of $0.36 per common share diluted

Revenue from Telecommunications customers 86.3% of total

Note: The organic revenue percentage of 2.4% excludes storm restoration

services of $3.7 million in Q1-12. Non-GAAP net income for Q1-13

excludes $0.7 million of pre-tax acquisition related costs. See “Regulation G

Disclosure” slides 19-22 for a reconciliation of GAAP to Non GAAP

financial measures.

services of $3.7 million in Q1-12. Non-GAAP net income for Q1-13

excludes $0.7 million of pre-tax acquisition related costs. See “Regulation G

Disclosure” slides 19-22 for a reconciliation of GAAP to Non GAAP

financial measures.

15

Selected Information

(a) Amounts may not foot due to rounding.

(b) Percentages disclosed under the financial amounts for Q1-13 and Q1-12 represent the percentage of contract revenues for the applicable

period.

period.

(c) Excludes $0.7 million in acquisition related costs.

Q1-13

Q1-12

Change (a)

($ in millions)(b)

Contract Revenues

$

323.3

$

319.6

$

3.7

Cost of Earned Revenues

$

257.1

79.5%

$

255.2

79.9%

$

1.9

General & Administrative-

Non-GAAP(c)

Non-GAAP(c)

$

28.1

8.7%

$

25.4

7.9%

$

2.8

Depreciation &

Amortization

Amortization

$

15.3

4.7%

$

16.0

5.0%

$

(0.6)

Interest Expense, net

$

4.2

1.3%

$

4.2

1.3%

$

-

Other Income, net

$

1.6

0.5%

$

3.0

0.9%

$

(1.3)

Net Income-Non-GAAP

$

12.3

3.8%

$

13.0

4.1%

$

(0.7)

Adjusted EBITDA - Non-

GAAP

GAAP

$

40.4

12.5%

$

40.4

12.6%

$

-

Organic Revenue growth of 2.4%,

excluding revenues from storm restoration services

in Q1-12

excluding revenues from storm restoration services

in Q1-12

nGrowth within existing contracts

nRural broadband projects

Adjusted EBITDA of $40.4 million

nGrowth in operations

nMargin Improvement

Note: See “Regulation G Disclosure” slides 19-22 for a reconciliation of GAAP to Non-GAAP financial measures.

16

Cash Flow and Liquidity

Strong Operating Cash Flows

nCash flow of $27.7 million during the quarter

nCapital expenditures, net of disposals, of

$10.5 million

$10.5 million

Balance Sheet Strength

nAmple liquidity from cash on hand of $54.7

million and $180.9 million of availability under

Senior Credit Agreement as of October 27,

2012

million and $180.9 million of availability under

Senior Credit Agreement as of October 27,

2012

nRepurchased 1,047,000 shares of common

stock at an average price of $14.52 per share

during Q1-13

stock at an average price of $14.52 per share

during Q1-13

17

Summary

n Firm end market opportunities

} Industry participants aggressively extending or deploying

fiber networks to provide wireless backhaul services

fiber networks to provide wireless backhaul services

} Broadband stimulus funding network construction for rural

service providers

service providers

} Cable operators continuing to deploy fiber to small and

medium businesses

medium businesses

} Wireless carriers upgrading from 3G to 4G technologies

} Telephone companies deploying FTTX to enable video

offerings

offerings

n Increased market share as our customers consolidate vendor

relationships and reward scale

relationships and reward scale

18

Looking Ahead

(Excludes effects of announced acquisition for revenues and

operating results)

operating results)

n Revenue trends which are improving year over year, excluding storm restoration services

n Margins, general and administrative expenses and other income in-line with previous

expectations

expectations

n Subject to our pending acquisition, strong cash flows dedicated to debt repayment

n Confident that solid operations will continue for a sustained period

Q2 - 2013:

n Revenues which are slightly up year over year, after excluding approximately $9 million of

expected storm restoration revenues during Q2-2013

expected storm restoration revenues during Q2-2013

n Gross margins up 75 to 100 basis points year over year

n General and administrative expense which declines slightly on a sequential basis reflecting

lower performance-based incentive compensation

lower performance-based incentive compensation

n Depreciation and amortization which is slightly down on a sequential basis

n Other income which decreases sequentially by approximately $0.8 million from Q1-13

19

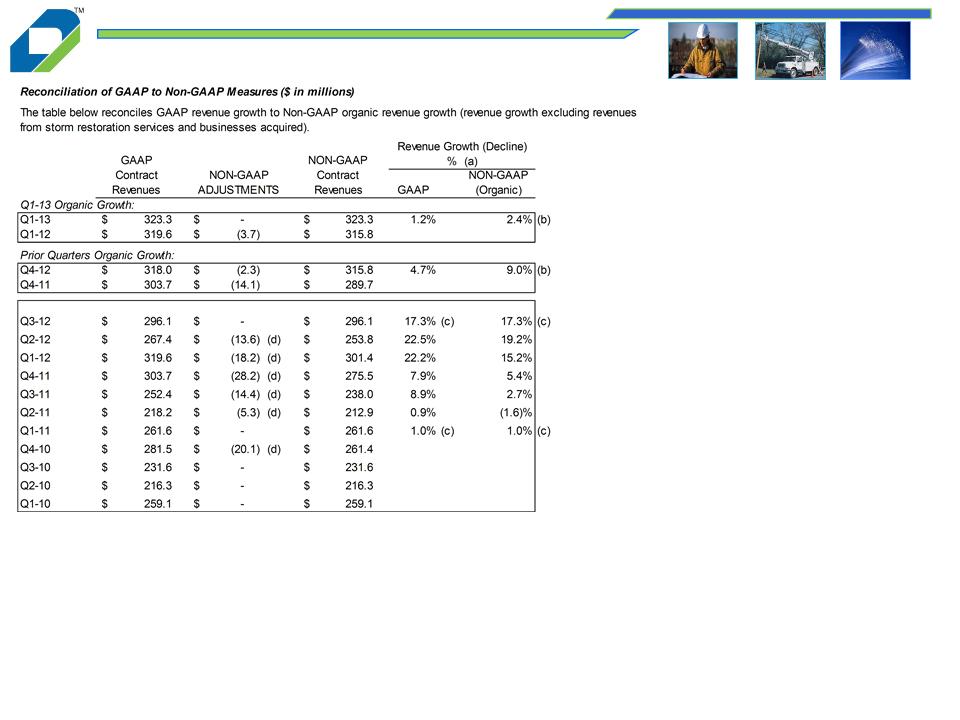

Appendix: Regulation G Disclosure

The above table presents the Non-GAAP financial measure of Adjusted EBITDA for the three months ended October 27, 2012 and October 29, 2011

and a reconciliation of Adjusted EBITDA to the most directly comparable GAAP measure. Adjusted EBITDA is a Non-GAAP financial measure within

the meaning of Regulation G promulgated by the Securities and Exchange Commission. The Company defines Adjusted EBITDA as earnings before

interest, taxes, depreciation and amortization, gain on sale of fixed assets, stock-based compensation expense, and acquisition-related costs. The

Company believes this Non-GAAP financial measure provides information that is useful to the Company’s investors. The Company believes that this

information is helpful in understanding period-over-period operating results separate and apart from items that may, or could, have a disproportionate

positive or negative impact on the Company’s results of operations in any particular period. Additionally, the Company uses this Non-GAAP financial

measure to evaluate its past performance and prospects for future performance. Adjusted EBITDA is not a recognized term under GAAP and does not

purport to be an alternative to net income, operating cash flows, or a measure of earnings. Because all companies do not use identical calculations,

this presentation of Non-GAAP financial measures may not be comparable to other similarly titled measures of other companies.

and a reconciliation of Adjusted EBITDA to the most directly comparable GAAP measure. Adjusted EBITDA is a Non-GAAP financial measure within

the meaning of Regulation G promulgated by the Securities and Exchange Commission. The Company defines Adjusted EBITDA as earnings before

interest, taxes, depreciation and amortization, gain on sale of fixed assets, stock-based compensation expense, and acquisition-related costs. The

Company believes this Non-GAAP financial measure provides information that is useful to the Company’s investors. The Company believes that this

information is helpful in understanding period-over-period operating results separate and apart from items that may, or could, have a disproportionate

positive or negative impact on the Company’s results of operations in any particular period. Additionally, the Company uses this Non-GAAP financial

measure to evaluate its past performance and prospects for future performance. Adjusted EBITDA is not a recognized term under GAAP and does not

purport to be an alternative to net income, operating cash flows, or a measure of earnings. Because all companies do not use identical calculations,

this presentation of Non-GAAP financial measures may not be comparable to other similarly titled measures of other companies.

20

(a) Year-over-year growth (decline) percentage is calculated as follows: (i) revenues in the quarterly period less (ii) revenues in the comparative prior year quarter

period; divided by (ii) revenues in the comparative prior year quarter period.

period; divided by (ii) revenues in the comparative prior year quarter period.

(b) Q1-13 organic growth excludes storm restoration revenues of $3.7 million in Q1-12 . Q4-12 organic growth excludes storm restoration revenues of $2.3 million in Q4

-12 and $14.1 million in Q4-11.

-12 and $14.1 million in Q4-11.

(c) For Q3-12, GAAP and Non-GAAP revenue growth percentages are the same as revenues from business acquired in 2011 were included for the full quarter in each

period and there were no other Non-GAAP adjustments in either period. For Q1-11, GAAP and Non-GAAP revenue growth percentages are the same as there were no

Non-GAAP adjustments in either period.

period and there were no other Non-GAAP adjustments in either period. For Q1-11, GAAP and Non-GAAP revenue growth percentages are the same as there were no

Non-GAAP adjustments in either period.

(d) Non-GAAP adjustments in Q2-12, Q3-11 and Q2-11 reflect revenues from businesses acquired during Q2-11. Non-GAAP adjustments in Q1-12 reflect storm

restoration revenues ($3.7 million) and revenues from businesses acquired during Q2-11 ($14.5 million). Non-GAAP adjustments in Q4-11 for fiscal 2011 fourth

quarter year-over-year organic growth reflects storm restoration revenues ($14.1 million) and revenues from businesses acquired during Q2-11 ($14.1 million). Non-

GAAP adjustments in Q4-10 result from the Company’s 52/53 week fiscal year. The Q4-10 Non-GAAP adjustments reflect the impact of the additional week in Q4-10

and are calculated by dividing contract revenues by 14 weeks. The result, representing one week of contract revenues, is subtracted from the GAAP-contract revenues

to calculate 13 weeks of revenue for Q4-10 on a Non-GAAP basis for comparison purposes.

restoration revenues ($3.7 million) and revenues from businesses acquired during Q2-11 ($14.5 million). Non-GAAP adjustments in Q4-11 for fiscal 2011 fourth

quarter year-over-year organic growth reflects storm restoration revenues ($14.1 million) and revenues from businesses acquired during Q2-11 ($14.1 million). Non-

GAAP adjustments in Q4-10 result from the Company’s 52/53 week fiscal year. The Q4-10 Non-GAAP adjustments reflect the impact of the additional week in Q4-10

and are calculated by dividing contract revenues by 14 weeks. The result, representing one week of contract revenues, is subtracted from the GAAP-contract revenues

to calculate 13 weeks of revenue for Q4-10 on a Non-GAAP basis for comparison purposes.

Appendix: Regulation G Disclosure

Amounts may not foot due to rounding.

21

Appendix: Regulation G Disclosure

(a) Year-over-year growth percentage is calculated as follows: (i) revenues in the quarterly period less (ii) revenues in the comparative prior year quarter period; divided

by (ii) revenues in the comparative prior year quarter period.

by (ii) revenues in the comparative prior year quarter period.

Amounts may not foot due to rounding.

22

Appendix: Regulation G Disclosure

The items reconciling "GAAP" to “Non-GAAP” financial measures are specifically described below:

(a) Acquisition related costs.

(b) Provision for income taxes includes the tax effect of the other reconciling items identified herein.

Review of Acquisition of

Quanta Services’ Telecommunications

Infrastructure Services Subsidiaries

Infrastructure Services Subsidiaries

Fiscal 2013

1st Quarter Presentation

November 20, 2012