Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - China United Insurance Service, Inc. | v326580_ex32-1.htm |

| EX-32.2 - EXHIBIT 32.2 - China United Insurance Service, Inc. | v326580_ex32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - China United Insurance Service, Inc. | v326580_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - China United Insurance Service, Inc. | v326580_ex31-1.htm |

| EXCEL - IDEA: XBRL DOCUMENT - China United Insurance Service, Inc. | Financial_Report.xls |

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2012

OR

| ¨ | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE EXCHANGE ACT |

For the transition period from ______ to __________

COMMISSION FILE NUMBER: 333-174198

CHINA UNITED INSURANCE SERVICE, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 98-6088870 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

Building 4F, Hesheng Plaza No. 26

Yousheng S Rd. Jinshui District, Zhengzhou,

Henan People’s Republic of China

(Address of principal executive offices)

+86371-63976529

(Registrant’s Telephone Number, Including Area Code)

N/A

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Check whether the issuer (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company filer. See definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one):

| Large Accelerated Filer ¨ | Non-Accelerated Filer ¨ | |

| Accelerated Filer ¨ | Smaller Reporting Company x |

Indicate by check mark whether the registrant is a shell company as defined in Rule 12b-2 of the Exchange Act. Yes ¨ No x

As of November 12, 2012, there are 29,100,503 shares of common stock issued and outstanding, and 1,000,000 preferred shares issued and outstanding.

TABLE OF CONTENTS

| PART I. | FINANCIAL INFORMATION | |

| ITEM 1. | CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) | F-1 |

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 1 |

| ITEM 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURE ABOUT MARKET RISK | 8 |

| ITEM 4. | CONTROLS AND PROCEDURES | 9 |

| PART II. | OTHER INFORMATION | |

| ITEM 1. | LEGAL PROCEEDINGS | 9 |

| ITEM 1A. | RISK FACTORS | 9 |

| ITEM 2. | UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS | 9 |

| ITEM 3. | DEFAULTS UPON SENIOR SECURITIES | 9 |

| ITEM 4. | MINE SAFETY DISCLOSURES | 9 |

| ITEM 5. | OTHER INFORMATION | 10 |

| ITEM 6. | EXHIBITS | 10 |

| SIGNATURES | 11 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This report contains forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievement expressed or implied by the forward-looking statements. These risks and uncertainties include, but are not limited to, the factors described under Part 1 Item 2 “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” In some cases, you can identify forward-looking statements by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “would” and similar expressions intended to identify forward-looking statements. Forward-looking statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

Forward-looking statements represent our estimates and assumptions only as of the date of this report. You should read this report and the documents that we reference in this report, or that we filed as exhibits to this report completely and with the understanding that our actual future results may be materially different from what we expect.

Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

OTHER PERTINENT INFORMATION

References in this report to “we,” “us,” “our” and the “Company” and words of like import refer to China United Insurance Service, Inc., its subsidiaries and variable interest entities.

References to China or the PRC refer to the People’s Republic of China (excluding Hong Kong, Macao and Taiwan). References to Taiwan refer to Taiwan, Republic of China.

Our business is conducted in Taiwan and China using NT$, the currency of Taiwan and RMB, the currency of China, respectively, and our financial statements are presented in United States dollars (“USD” or “$”). In this report, we refer to assets, obligations, commitments and liabilities in our financial statements in USD. These dollar references are based on the exchange rate of NT$ and RMB to USD, determined as of a specific date. Changes in the exchange rate will affect the amount of our obligations and the value of our assets in terms of USD which may result in an increase or decrease in the amount of our obligations (expressed in USD) and the value of our assets, including accounts receivable (expressed in USD).

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

CHINA UNITED INSURANCE SERVICE, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

| September 30, 2012 | June 30, 2012 | |||||||

| (Unaudited) | (Audited) | |||||||

| ASSETS | ||||||||

| Current assets | ||||||||

| Cash and equivalents | $ | 12,252,645 | $ | 1,258,211 | ||||

| Marketable securities | 131,062 | - | ||||||

| Accounts receivable, net | 2,842,957 | 184,767 | ||||||

| Other current assets | 409,411 | 48,640 | ||||||

| Total current assets | 15,636,075 | 1,491,618 | ||||||

| Property, plant and equipment, net | 1,075,962 | 114,945 | ||||||

| Goodwill | 118,581 | 118,855 | ||||||

| Other assets | 499,690 | 113,217 | ||||||

| TOTAL ASSETS | $ | 17,330,308 | $ | 1,838,635 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities | ||||||||

| Taxes payable | $ | 515,196 | $ | 405,723 | ||||

| Other current liabilities | 3,583,654 | 286,909 | ||||||

| Due to related parties | 767,856 | 445,332 | ||||||

| TOTAL CURRENT LIABILITIES | 4,866,706 | 1,137,964 | ||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Preferred stock, par value $0.00001, 10,000,000 authorized, 1,000,000 issued and outstanding as of September 30, 2012, none issued and outstanding as of June 30, 2012 | 10 | - | ||||||

| Common stock, par value $0.00001, 100,000,000 authorized, 29,100,503 issued and outstanding as of September 30, 2012, 20,100,503 issued and outstanding as of June 30, 2012 | 291 | 201 | ||||||

| Additional paid-in capital | 4,674,593 | 2,674,692 | ||||||

| Accumulated other comprehensive income (loss) | 177,563 | (55,250 | ) | |||||

| Retained earnings (accumulated deficit) | 3,367,721 | (1,918,972 | ) | |||||

| Sub-total | 8,220,178 | 700,671 | ||||||

| Non-controlling interest | 4,243,424 | - | ||||||

| TOTAL STOCKHOLDERS’ EQUITY | 12,463,602 | 700,671 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 17,330,308 | $ | 1,838,635 | ||||

The accompanying notes are an integral part of these consolidated financial statements.

| F-1 |

CHINA UNITED INSURANCE SERVICE, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME AND OTHER COMPREHENSIVE INCOME / (LOSS) (UNAUDITED)

| Three months ended September 30, | ||||||||

| 2012 | 2011 | |||||||

| Revenues | $ | 3,219,300 | $ | 660,262 | ||||

| Cost of revenue | 2,165,622 | 531,363 | ||||||

| Gross profit | 1,053,678 | 128,899 | ||||||

| Operating expenses: | ||||||||

| General and administrative | 1,030,271 | 350,643 | ||||||

| Income (loss) from operations | 23,407 | (221,744 | ) | |||||

| Other income (expenses) | ||||||||

| Interest income | 646 | 1,080 | ||||||

| Bargain gain on purchase of subsidiaries | 5,280,042 | - | ||||||

| Other – net | 43,324 | (1,322 | ) | |||||

| Total other income (expenses) | 5,324,012 | (242 | ) | |||||

| Income (loss) before income taxes | 5,347,419 | (221,986 | ) | |||||

| Income tax expense | (10,819 | ) | 72,419 | |||||

| Net income (loss) | 5,358,238 | (294,405 | ) | |||||

| Net income attributable to the non-controlling interests | (71,544 | ) | - | |||||

| Net income (loss) attributable to parent's shareholders | 5,286,694 | (294,405 | ) | |||||

| Other comprehensive income | 232,814 | 5,431 | ||||||

| Comprehensive income (loss ) | $ | 5,519,508 | $ | (288,974 | ) | |||

| Weighted average shares outstanding: | ||||||||

| Basic and diluted | 24,122,242 | 20,000,000 | ||||||

| Income (loss) per share: | ||||||||

| Basic and diluted | $ | 0.23 | (0.01 | ) | ||||

The accompanying notes are an integral part of these consolidated financial statements.

| F-2 |

CHINA UNITED INSURANCE SERVICE, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

| Three months ended September 30 | ||||||||

| 2012 | 2011 | |||||||

| Cash flows from operating activities: | ||||||||

| Net income (loss) | $ | 5,358,238 | $ | (294,405 | ) | |||

| Adjustments to reconcile net income to net cash provided by (used in) operating activities: | ||||||||

| Depreciation | 40,244 | 13,819 | ||||||

| Bargain gain purchase of subsidiaries | (5,280,042 | ) | - | |||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | (477,798 | ) | 37,942 | |||||

| Other current assets | 129,275 | (34,964 | ) | |||||

| Other assets | (5,702 | ) | - | |||||

| Taxes payable | (500,734 | ) | 58,894 | |||||

| Other current liabilities | (1,332,087 | ) | (22,127 | ) | ||||

| Net cash used in operating activities | (2,068,606 | ) | (240,841 | ) | ||||

| Cash flows from investing activities: | ||||||||

| Cash acquired in acquisition | 12,766,882 | - | ||||||

| Purchase of marketable securities | (3,228 | ) | - | |||||

| Purchase of property, plant and equipment | (7,859 | ) | (10,196 | ) | ||||

| Net cash provided by (used in) investing activities | 12,755,795 | (10,196 | ) | |||||

| Cash flows from financing activities: | ||||||||

| Proceeds from related party borrowing | 90,942 | 109,130 | ||||||

| Net cash provided by financing activities | 90,942 | 109,130 | ||||||

| Effect of exchange rate changes on cash and equivalents | 216,303 | 17,447 | ||||||

| Net increase/(decrease) in cash and equivalents | 10,994,434 | (124,460 | ) | |||||

| Cash and equivalents, beginning balance | 1,258,211 | 1,297,213 | ||||||

| Cash and equivalents, ending balance | $ | 12,252,645 | $ | 1,172,753 | ||||

| Supplementary disclosure of cash flow information | ||||||||

| Interest paid | $ | - | $ | - | ||||

| Income tax paid | $ | 495,612 | $ | 4,491 | ||||

The accompanying notes are an integral part of these consolidated financial statements.

| F-3 |

CHINA UNITED INSURANCE SERVICE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2012 AND 2011 (UNAUDITED)

NOTE 1 – ORGANIZATION AND PRINCIPAL ACTIVITIES

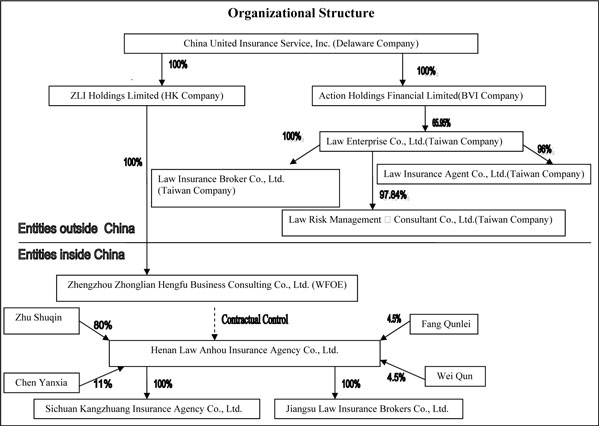

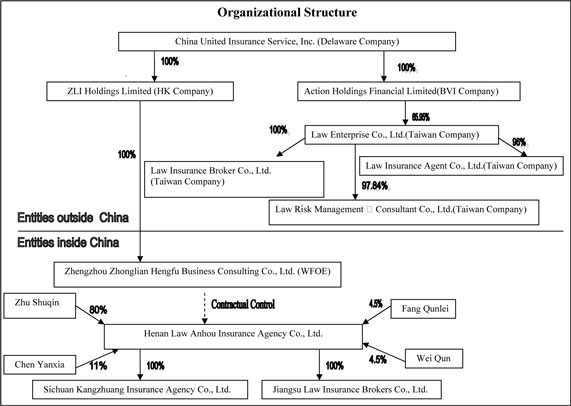

China United Insurance Service, Inc. (“China United” or the “Company”) is a Delaware corporation organized on June 4, 2010 by Mao Yi Hsiao, a Taiwanese citizen, as a listing vehicle for ZLI Holdings Limited (“CU Hong Kong”) to be quoted on the United States Over the Counter Bulletin Board (the “OTCBB”).

CU Hong Kong, a wholly owned Hong Kong-based subsidiary of China United, was founded by China United, on July 12, 2010 under Hong Kong law. On October 20, 2010, CU Hong Kong founded a wholly foreign owned enterprise, Zhengzhou Zhonglian Hengfu Business Consulting Co., Ltd. (“CU WFOE”) in Henan province in the People’s Republic of China (“PRC”).

On January 16, 2011, the Company issued 20,000,000 shares of common stock, $0.00001 par value, to several non U.S. persons for $300,000. The issuance was made pursuant to an exemption from registration in Regulation S under the Securities Act of 1933, as amended. As a result of the issuance of 20,000,000 shares, the owners of Henan Anhou (accounting acquirer) owned 100% of the Company. Accordingly, this transaction was accounted for as a recapitalization of Henan Anhou. The historical financial statements presented are those of the accounting acquirer for all periods presented. On January 28, 2011, the Company increased the number of authorized shares from 30,000,000 to 100,000,000 and 10,000,000 shares of preferred stock.

Henan Law Anhou Insurance Agency Co., Ltd. (“Henan Anhou”, formerly known as Zhengzhou Anhou Insurance Agency Co., Ltd.) was incorporated in the PRC on August 20, 2003. Henan Anhou provides insurance agency services in the PRC.

Sichuan Kangzhuang Insurance Agency Co., Ltd. (“Sichuan Kangzhuang”) was founded on July 10, 2006 in the Sichuan province in the PRC and provides insurance agency services in the PRC. On August 23, 2010, at Sichuan Kangzhuang’s general meeting of shareholders, its shareholders voted to sell their shares to Henan Anhou for RMB532,622 ($78,318). On September 6, 2010, the equity transfer agreements were signed between Henan Anhou and each shareholder of Sichuan Kangzhuang. Sichuan Kangzhuang then had net liabilities of RMB219,123 ($32,134). Goodwill of RMB751,745 ($110,452) was therefore recorded. Goodwill in the balance sheet differs from the acquisition date amount due to changes in exchange rates.

Jiangsu Law Insurance Broker Co., Ltd. (“Jiangsu Law”) was founded on May 18, 2005 in Jiangsu Province in the PRC. Jiangsu Law provides insurance brokerage services in the PRC. On August 12, 2010, at Jiangsu Law’s general meeting of shareholders, its shareholders voted to sell their shares to Henan Anhou for RMB518,000 ($75,475) and Henan Anhou increased Jiangsu Law’s paid-in capital to RMB10,000,000 ($1,355,150) from RMB5,180,000 ($625,113), on January 18, 2011, to meet the PRC paid-in capital requirements for insurance brokerage companies. On September 28, 2010, the equity transfer agreements were signed between Henan Anhou and each shareholder of Jiangsu Law. The consideration is due upon request and had not been paid as at September 30, 2012. On acquisition date, Jiangsu Law had net assets of RMB2,286,842 ($341,425). Based on the purchase price allocation, the fair value of the identifiable assets and liabilities assumed exceeded the fair value of the consideration paid. As a result, the Company recorded a gain on acquisition of RMB1,768,842 ($267,156).

On January 17, 2011, CU WFOE and Henan Anhou and its shareholders entered into a series of agreements known as variable interest agreements (the “VIE Agreements”) pursuant to which CU WFOE has effective control over Henan Anhou.

| F-4 |

On July 2, 2012, the Board of Directors and stockholders of the Company approved, in connection with a reclassification of 1,000,000 issued and outstanding shares of common stock (the “Reclassified Shares”), par value $0.00001 per share held by Mao Yi Hsiao (“Mr. Mao”) into 1,000,000 shares of Series A Convertible Preferred Stock, par value $0.00001 per share (the “Series A Preferred Stock”) on a share-for-share basis (the “Reclassification”), the issuance of 1,000,000 shares of Series A Preferred Stock to Mr. Mao and cancellation of 1,000,000 common stock held and submitted by Mr. Mao pursuant to the Reclassification. All of the 1,000,000 shares of Series A Preferred Stock are reclassified from the 1,000,000 common stock held by Mr. Mao and no additional consideration was paid by Mr. Mao in connection with the Reclassification. Each holder of common stock is entitled to one vote for each share of common stock held of record by such holder as of the applicable record date on any matter that is submitted to a vote of the stockholders of the Company; while each holder of Series A Preferred Stock is entitled to ten votes for each share of Series A Preferred Stock held of record by such holder as of the applicable record date on any matter that is submitted to a vote of the stockholders of the Company.

On August 24, 2012, the Company acquired all of the issued and outstanding shares (representing 100% of voting equity interest) of Action Holdings Financial Limited (“AHFL”), an LLC incorporated under the laws of the British Virgin Islands on April 30, 2012, together with its subsidiaries in Taiwan. Pursuant to the provisions of the Acquisition Agreement and for all of the issued and outstanding shares of AHFL, the Company will pay New Taiwan Dollar (NT$) NT$15 million ($500,815) on or prior to March 31, 2013 and NT$7.5 million ($250,095) subsequent to March 31, 2013 in cash in two installments, subject to terms and conditions therein. In addition the Company agreed to (i) issue eight million shares of common stock of the Company to the shareholders of AHFL; (ii) issue two million shares of common stock of the Company to certain employees of Law Broker; and (iii) create an employee stock option pool, consisting of available options, exercisable for up to two million shares of common stock of the Company.

On August 17, 2012, AHFL purchased 13,593,015 shares of common stock of Law Enterprise Co., Ltd. (“Law Enterprise”), a company limited by shares incorporated under the laws of Taiwan on January 30, 1996, from certain shareholders at $NT12.8 ($0.44) per share, which was 65.95% of ownership interest in Law Enterprise’s. As of August 24, 2012, Law Enterprise holds (i) 100% of Law Insurance Broker Co., Ltd. (“Law Broker”), a company limited by shares incorporated in Taiwan on October 9, 1992; (ii) 97.84% of Law Risk Management & Consultant Co., Ltd. (“Law Management”), a company limited by shares incorporated in Taiwan on December 5, 1987; and (iii) 96% of Law Insurance Agent Co., Ltd. (“Law Agent”), an LLC incorporated in Taiwan on June 3, 2000.

Law Enterprise is a holding company for its operating subsidiaries in Taiwan. Law Broker primarily engages in insurance brokerage and insurance agency service business across Taiwan, while Law Management and Law Agent are not in operation.

The corporate structure after the acquisition is:

| F-5 |

| F-6 |

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of China United and its subsidiaries as shown in the organization structure in Note 1 above. The results of operations of AHFL and subsidiaries are included since August 31, 2012 the date of acquisition for accounting convenience.. All significant intercompany transactions and balances were eliminated in consolidation.

Basis of Presentation

The Company’s financial statements are prepared in accordance with generally accepted accounting principles in the United States of America (“US GAAP"). The functional currency for our subsidiaries in Taiwan is $NT, for the VIEs in China is Renminbi (“RMB”).

Noncontrolling Interest

Noncontrolling interest consists of direct and indirect equity interest in AHFL and subsidiaries arising from the acquisition of AHFL by CUIS.

The Company follows Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 810, “Consolidation,” which governs the accounting for and reporting of noncontrolling interests (“NCIs”) in partially owned consolidated subsidiaries and the loss of control of subsidiaries. Certain provisions of this standard indicate, among other things, that NCIs be treated as a separate component of equity, not as a liability, that increases and decreases in the parent’s ownership interest that leave control intact be treated as equity transactions rather than as step acquisitions or dilution gains or losses, and that losses of a partially owned consolidated subsidiary be allocated to the NCI even when such allocation might result in a deficit balance. This standard also required changes to certain presentation and disclosure requirements.

The net income (loss) attributed to the NCI is separately designated in the accompanying statements of operations and other comprehensive income (loss). Losses attributable to the NCI in a subsidiary may exceed the NCI’s interests in the subsidiary’s equity. The excess attributable to the NCI is attributed to those interests. The NCI shall continue to be attributed its share of losses even if that attribution results in a deficit NCI balance.

Use of Estimates

The preparation of the consolidated financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the dates of the consolidated financial statements and the amounts of revenues and expenses during the reporting periods.

Management makes these estimates using the best information available when the estimates are made; however, actual results could differ materially from those estimates.

| F-7 |

Risks and Uncertainties

The Company is subject to risks from, among other things, competition associated with the industry in general, other risks associated with financing, liquidity requirements, rapidly changing customer requirements, limited operating history, and foreign currency exchange rates.

Comprehensive Income

The Company follows Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 220 (“ASC 220”), “Reporting Comprehensive Income”, which establishes standards for the reporting and display of comprehensive income, its components and accumulated balances in a full set of general purpose financial statements. ASC 220 defines comprehensive income as net income and all changes to stockholders' equity, except those due to investments by stockholders, changes in paid-in capital and distributions to stockholders, including adjustments to minimum pension liabilities, accumulated foreign currency translation, and unrealized gains or losses on marketable securities.

Foreign Currency Transactions

The consolidated financial statements were translated into United States Dollars (“USD”) in accordance with FASB ASC Topic 830 "Foreign Currency Transaction". According to the statement, all assets and liabilities were translated at the exchange rate on the balance sheet dates; stockholders’ equity is translated at historical rates and statement of operations items are translated at the weighted average exchange rate for the period. The resulting translation adjustments are reported under other comprehensive income in accordance with ASC 220 “Comprehensive Income". Gains and losses resulting from the translation of foreign currency transactions are reflected in the consolidated statements of income and other comprehensive income (loss).

Cash and Equivalents

For Statements of Cash Flows purposes, the Company considers cash on hand, bank deposits, and other highly-liquid investments with maturities of three months or less when purchased, such as commercial paper, to be cash and equivalents.

The Company maintains cash with banks in PRC and Taiwan. Cash accounts are not insured or otherwise protected. Should any bank holding cash become insolvent, or if the Company is otherwise unable to withdraw funds, the Company would lose the cash with that bank; however, the Company has not experienced any losses in such accounts and believes it is not exposed to any significant risks on its cash in bank accounts.

Marketable Securities

The Company invests part of its excess cash in equity securities and government bonds. Such investments are included in “Marketable securities” on the accompanying consolidated balance sheets. Equity securities investments are classified as trading securities and reported at fair value (“FV”) with changes in FV recorded in “Other Income”. Bonds are classified as available-for-sale and reported at FV with unrealized gains and losses included in “Accumulated other comprehensive income (loss).”

Accounts Receivable

The Company reviews its accounts receivable regularly to determine if a bad debt allowance is necessary at each period-end. Management reviews the composition of accounts receivable and analyzes the age of receivables outstanding, customer concentrations, customer credit worthiness, current economic trends and changes in customer payment patterns to evaluate the necessity of making such allowance.

| F-8 |

Property, Plant and Equipment

Property, plant and equipment are recorded at cost. Gain or loss on disposal of property, plant or equipment is recorded in income at disposal. Expenditures for betterments, renewals and additions are capitalized. Repairs and maintenance expenses are expensed as incurred.

Depreciation for financial reporting purposes is provided using the straight-line method over a useful life of three to ten years with salvage of 10% to 25%. Property, plant and equipment mainly consist of office furniture, computers and leasehold improvements.

Impairment of Long-Lived Assets

In accordance with ASC 360, “Property, Plant and Equipment”, the Company reviews the carrying values of long-lived assets whenever facts and circumstances indicate an asset may be impaired. Recoverability of assets to be held and used is measured by comparing the carrying amount of an asset to future net undiscounted cash flows expected to be generated by it. If an asset is considered impaired, the impairment recognized is measured by the amount by which the carrying amount of the asset exceeds its FV. Assets to be disposed of are reported at the lower of the carrying amount or FV, less costs of disposal. No impairment was recognized for the three months ended September 30, 2012 or 2011.

Goodwill

Goodwill arose from the acquisition of Sichuan Kangzhuang (Note 8). Goodwill is the excess of the cost of an acquisition over the fair value (“FV”) of the net assets acquired. Goodwill is tested for impairment annually or more frequently if events or changes in circumstances indicate it might be impaired, using the prescribed two-step process under US GAAP. The first step screens for potential impairment of goodwill to determine if the FV of the reporting unit is less than its carrying value, while the second step measures the amount of goodwill impairment, if any, by comparing the implied FV of goodwill to its carrying value. As of September 30, 2012, there are no indications of any impairment.

Revenue Recognition

The Company’s revenue is from insurance agency and brokerage services. The Company, through its subsidiaries, sells insurance products to customers, and obtains commissions from the respective insurance companies according to the terms of each insurance company service agreement. The Company recognizes revenue when the following have occurred: persuasive evidence of an agreement between the insurance company and insured exists, services were provided, the fee for such services is fixed or determinable and collectability of the fee is reasonably assured. Insurance agency services are considered complete, and revenue is recognized, when an insurance policy becomes effective. The customers are entitled to a 10-day cancellation period from the date of the issuance of the policies, in which the customers can cancel the contract without any fees. The Company is notified of such cancellations by the insurance carriers. For the three months ended September 30, 2012 and 2011, policy cancellations were $ 10,617 and nil, respectively.

The Company pays commissions to its sub-agents when an insurance product is sold by the sub-agent. The Company recognizes commission revenue on a gross basis. The commissions paid by the Company to its sub-agents are recorded as costs of revenue.

Income Taxes

The Company utilizes ASC 740, “Income Taxes”, which requires recognition of deferred tax assets and liabilities for the expected future tax consequences of events included in the financial statements or tax returns. Under this method, deferred taxes are recognized for the tax consequences in future years of differences between the tax bases of assets and liabilities and their financial reporting amounts at each period end based on enacted tax laws and statutory tax rates applicable to the periods in which the differences are expected to affect taxable income. Valuation allowances are established, when necessary, to reduce deferred tax assets to the amount expected to be realized.

| F-9 |

When tax returns are filed, it is likely some positions taken would be sustained upon examination by the taxing authorities, while others are subject to uncertainty about the merits of the position taken or the amount of the position that would be ultimately sustained. The benefit of a tax position is recognized in the financial statements in the period during which, based on all available evidence, management believes it is more-likely-than-not that the position will be sustained upon examination, including the resolution of appeals or litigation processes, if any. Tax positions taken are not offset or aggregated with other positions. Tax positions that meet the more-likely-than-not recognition threshold are measured as the largest amount of tax benefit that is more than 50% likely of being realized upon settlement with the applicable taxing authority. The portion of the benefits associated with tax positions taken that exceeds the amount measured as described above is reflected as a liability for unrecognized tax benefits in the accompanying balance sheets along with any associated interest and penalties that would be payable to the taxing authorities upon examination. Interest associated with unrecognized tax benefits is classified as interest expense and penalties are classified in selling, general and administrative expenses in the statements of operations and other comprehensive income (loss). As of September 30, 2012 and 2011, the Company did not have any uncertain tax positions.

The Company was not subjected to income tax examinations by taxing authorities during the current or past fiscal years. During the three months ended September 30, 2012 and 2011, the Company did not recognize any interest or penalties.

Fair Values of Financial Instruments

ASC 820, “Fair Value Measurements and Disclosures”, defines FV, establishes a three-level valuation hierarchy for disclosures of FV measurement and enhances disclosures requirements for FV measures. The carrying amounts reported in the balance sheets for receivables and current liabilities each qualify as financial instruments and are reasonable estimates of FV because of the short period of time between the origination of such instruments and their expected realization and their current market rate of interest. The three levels are defined as follows:

• Level 1 inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets.

• Level 2 inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the assets or liability, either directly or indirectly, for substantially the full term of the financial instruments.

• Level 3 inputs to the valuation methodology are unobservable and significant to the FV.

Concentration of Risk

Financial instruments that potentially subject the Company to significant concentrations of credit risk consist principally of cash and equivalents and accounts receivable. As of September 30, 2012 and June 30, 2012 (audited), substantially all of the Company’s cash and equivalents and restricted cash was held by major financial institutions in Taiwan, which management believes are of high credit quality. With respect to accounts receivable, the Company generally does not require collateral and does not have an allowance for doubtful accounts.

The Company has two principal insurance companies, Fubong Life Insurance Co., Ltd. (“Fubong”) and Far Glory Life Insurance (“Far Glory”), for which it acts as an insurance agent. As of September 30, 2012 and June 30, 2012, the Company’s revenue from sale of insurance policies underwritten by these two companies was:

| F-10 |

Three months ended

| September 30, 2012 | September 30, 2011 | |||||||

| Fubong | $ | 553,010 | $ | - | ||||

| Far Glory | 1,145,581 | - | ||||||

As of September 30, 2012 and June 30, 2012 (audited), the Company’s receivables from these two companies were:

| September 30, 2012 | June 30, 2012 | |||||||

| Fubong | $ | 552,876 | $ | - | ||||

| Far Glory | 1,148,317 | - | ||||||

The Company's operations are in PRC and Taiwan. Accordingly, the Company's business, financial condition and results of operations may be influenced by the political, economic, foreign currency exchange and legal environments in PRC and Taiwan, and by the state of their economy. The Company’s results may be adversely affected by changes in the political and social conditions in PRC and Taiwan, and by changes in governmental policies with respect to laws and regulations, anti-inflationary measures, and rates and methods of taxation, among other things.

Operating Leases

Leases, where substantially all the rewards and risks of ownership of assets remain with the leasing company that do not meet the capitalization criteria of ASC 840 “Leases”, are accounted for as operating leases. Rentals under operating leases are expensed on the straight-line basis over the lease term.

Segment Reporting

The Company follows ASC 280, “Segment Reporting”, for its segment reporting. For three months ended September 30, 2012 and 2011, the Company’s chief operating decision maker managed and reviewed its business as a single operating segment providing insurance brokerage and agency services across PRC and Taiwan (combined referred as “Greater China”). All revenues are derived from Greater China and all long-lived assets are in Greater China.

Contingencies

Certain conditions may exist as of the date the financial statements are issued, which could result in a loss to the Company but which will be resolved when one or more future events occur or fail to occur. The Company’s management assesses such contingent liabilities, and such assessment inherently involves judgment. In assessing loss contingencies arising from legal proceedings pending against the Company or unasserted claims that may rise from such proceedings, the Company’s management evaluates the perceived merits of any legal proceedings or unasserted claims as well as the perceived merits of the amount of relief sought or expected to be sought.

If the assessment of a contingency indicates it is probable that a material loss will be incurred and the amount of the liability can be reasonably estimated, then the estimated liability is accrued in the Company’s financial statements. If the assessment indicates a potential material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, then the nature of the contingent liability, together with an estimate of the range of possible loss if determinable and material would be disclosed.

Statement of Cash Flows

In accordance with ASC 230, “Statement of Cash Flows”, cash flows from the Company's operations are calculated based upon the local currencies and an average exchange rate is used. As a result, amounts related to assets and liabilities reported on the consolidated statements of cash flows may not necessarily agree with changes in the corresponding balances on the consolidated balance sheets. Cash from operating, investing and financing activities is net of the effect of acquisition described in Note 9.

| F-11 |

Variable Interest Entities

The Company follows ASC 810-10-05-8”, "Consolidation of VIEs” which states that a VIE is a corporation, partnership, limited liability corporation, trust or any other legal structure used to conduct activities or hold assets that either (1) has an insufficient amount of equity to carry out its principal activities without additional subordinated financial support, (2) has a group of equity owners that are unable to make significant decisions about its activities, or (3) has a group of equity owners that do not have the obligation to absorb losses or the right to receive returns generated by its operations.

Due to PRC legal restrictions on foreign ownership and investment in insurance agency and brokerage businesses in China, especially those on qualifications as well as capital requirement of the investors, the Company operates its insurance agency and brokerage business primarily through Henan Anhou, a VIE owned by four individual shareholders, and two subsidiaries of Henan Anhou.

On January 17, 2011, CU WFOE and Henan Anhou and its shareholders entered into VIE Agreements which included:

| ¨ | Exclusive Business Cooperation Agreement (“EBCA”) through which: (1) CU WFOE has the right to provide Henan Anhou with complete technical support, business support and related consulting services during the term of this Agreement; (2) Henan Anhou agrees to accept all the consultations and services provided by CU WFOE. Henan Anhou further agrees that unless with CU WFOE's prior written consent, during the term of this Agreement, Henan Anhou shall not directly or indirectly accept the same or any similar consultations and/or services provided by any third party and shall not establish similar cooperation relationship with any third party regarding the matters contemplated by this Agreement; (3) Henan Anhou shall pay CU WFOE fees equal to 90% of the net income of Henan Anhou, and the payment is quarterly, and (4) CU WFOE retains all exclusive and proprietary rights and interests in all rights, ownership, interests and intellectual properties arising out of or created during the performance of this Agreement. |

The term of this Agreement is 10 years. Subsequent to the execution of this Agreement, both CU WFOE and Henan Anhou shall review this Agreement on an annual basis to determine whether to amend or supplement the provisions. The term of this Agreement may be extended if confirmed in writing by CU WFOE prior to the expiration thereof. The extended term shall be determined by CU WFOE, and Henan Anhou shall accept such extended term unconditionally.

During the term of this Agreement, unless CU WFOE commits gross negligence, or a fraudulent act, against Henan Anhou, Henan Anhou may not terminate this Agreement prior to its expiration date. Nevertheless, CU WFOE shall have the right to terminate this Agreement upon giving 30 days prior written notice to Henan Anhou at any time.

| ¨ | Power of Attorney under which each shareholder of Henan Anhou executed an irrevocable power of attorney to authorize CU WFOE to act on behalf of the shareholder to exercise all of his/her rights as equity owner of Henan Anhou, including without limitation to: (1) attend shareholders' meetings of Henan Anhou; (2) exercise all the shareholder's rights and shareholder's voting rights that he/she is entitled to under the laws of PRC and Henan Anhou's Articles of Association, including but not limited to the sale or transfer or pledge or disposition of the shareholder’s shareholding in part or in whole, and (3) designate and appoint on behalf of the shareholder the legal representative, the director, supervisor, the chief executive officer and other senior management members of Henan Anhou. |

| F-12 |

| ¨ | Option Agreement under which the shareholders of Henan Anhou irrevocably granted CU WFOE or its designated person an exclusive and irrevocable right to acquire, at any time, the entire portion of Henan Anhou’s equity interest held by each shareholder of Henan Anhou, or any portion thereof, to the extent permitted by PRC law. The purchase price for the shareholders’ equity interests in Henan Anhou shall be the lower of (i) RMB 1 ($0.15) and (ii) the lowest price allowed by relevant laws and regulations. If appraisal is required by the laws of PRC when CU WFOE exercises the Equity Interest Purchase Option (as defined in the Option Agreement), the Parties shall negotiate in good faith and based on the appraisal result make necessary adjustment to the Equity Interest Purchase Price (as defined in the Option Agreement) so that it complies with any and all then applicable laws of PRC. The term of this Agreement is 10 years, and may be renewed at CU WFOE's election. |

| ¨ | Share Pledge Agreement under which the owners of Henan Anhou pledged their equity interests in Henan Anhou to CU WFOE to guarantee Henan Anhou’s performance of its obligations under the EBCA. Pursuant to this agreement, if Henan Anhou fails to pay the exclusive consulting or service fees in accordance with the EBCA, CU WFOE shall have the right, but not the obligation, to dispose of the owners of Henan Anhou’s equity interests in Henan Anhou. This Agreement shall be continuously valid until all payments due under the EBCA have been repaid by Henan Anhou or its subsidiaries. |

As a result of the agreements among CU WFOE, the shareholders of Henan Anhou and Henan Anhou, CU WFOE is considered the primary beneficiary of Henan Anhou, CU WFOE has effective control over Henan Anhou. Therefore, CU WFOE consolidates the results of operations of Henan Anhou and its subsidiaries. Accordingly the results of operations, assets and liabilities of Henan Anhou and its subsidiaries are consolidated in Company’s financial statements from the earliest period presented. However, the VIE is monitored by the Company to determine if any events have occurred that could cause its primary beneficiary status to change. These events include:

| a. | The legal entity's governing documents or contractual arrangements are changed in a manner that changes the characteristics or adequacy of the legal entity's equity investment at risk. |

| b. | The equity investment or some part thereof is returned to the equity investors, and other interests become exposed to expected losses of the legal entity. |

| c. | The legal entity undertakes additional activities or acquires additional assets, beyond those that were anticipated at the later of the inception of the entity or the latest reconsideration event, that increase the entity's expected losses. |

| d. | The legal entity receives an additional equity investment that is at risk, or the legal entity curtails or modifies its activities in a way that decreases its expected losses. |

Recent Accounting Pronouncements

In January 2011, the FASB issued ASU 2011-01, Receivables (Topic 310), to temporarily delay the effective date of the disclosures about troubled debt restructurings (“TDR”) in ASU 2010-20 (Receivables (Topic 310): Disclosures about the Credit Quality of Financing Receivables and the Allowance for Credit Losses) for public entities. The delay is intended to allow the Board time to complete its deliberations on what constitutes a TDR. Under the existing effective date in Update 2010-20, public-entity creditors would have provided disclosures about TDR for periods beginning on or after December 15, 2010. The deferral in this update will result in more consistent disclosures about TDR. This amendment does not apply to nonpublic entities and does not defer the effective date of the other disclosure requirements in Update 2010-20. The deferral in this amendment is effective upon issuance. The Company does not expect this update to have any material effect on its consolidated financial statements.

| F-13 |

In January 2011, the FASB issued ASU 2011-02 Receivables Topic 310 "A Creditor's Determination of Whether a Restructuring is a Troubled Debt Restructuring". The amendments in ASU 2011-02 provide additional guidance to clarify when a loan modification or restructuring is considered a TDR to address current diversity in practice and lead to more consistent application of US GAAP for debt restructurings. In evaluating whether a restructuring constitutes a TDR, a creditor must separately conclude that both of the following exist:

| 1. | The restructuring constitutes a concession. |

| 2. | The debtor is experiencing financial difficulties. |

The amendments to Topic 310 clarify the guidance regarding the evaluation of both considerations above. Additionally, the amendments clarify that a creditor is precluded from using the effective interest rate test in the debtor's guidance on restructuring of payables (paragraph 470-60-55-10) when evaluating whether a restructuring constitutes a TDR. ASU No. 2011-02 is effective for fiscal years beginning on or after June 15, 2011. The adoption of ASU 2011-02 did not have a material effect on the Company’s consolidated financial statements.

In April, 2011, the FASB issued ASU 2011-03 Transfers and Servicing (Topic 860), “Reconsideration of Effective Control for Repurchase Agreements”. The amendments in this ASU 2011-03 remove from the assessment of effective control:

| 1. | The criterion requiring the transferor to have the ability to repurchase or redeem the financial assets on the substantially agreed terms, even in the event of default by the transferee; and |

| 2. | The collateral maintenance implementation guidance related to that criterion. |

Other criteria applicable to the assessment of effective control are not changed by the amendments in Topic 860. The guidance in this Update is effective for the first interim or annual period beginning on or after December 15, 2011. The guidance should be applied prospectively to transactions or modifications of existing transactions that occur on or after the effective date. Early adoption is not permitted. The adoption of this ASU did not have a material effect on the Company’s consolidated financial statements.

In June 2011, the FASB issued ASU 2011-04 Fair Value Measurement (Topic 820), “Amendments to achieve Common Fair Value Measurement and Disclosure Requirements in US GAAP and International Financial Reporting Standards (“IFRS”)”. The amendments in this Update change the wording used to describe the requirements in US GAAP for measuring FV and for disclosing information about FV measurements. The amendments include the following:

| 1. | Those that clarify the Board’s intent about the application of existing FV measurement and disclosure requirements. |

| 2. | Those that change a particular principle or requirement for measuring FV or for disclosing information about fair value measurements. |

| F-14 |

In addition, to improve consistency in application across jurisdictions some changes in wording are necessary to ensure that US GAAP and IFRS FV measurement and disclosure requirements are described in the same way (for example, using the word shall rather than should to describe the requirements in US GAAP).

The amendments in this Update are to be applied prospectively. For public entities, the amendments are effective during interim and annual periods beginning after December 15, 2011. Early application by public entities is not permitted. The adoption of this ASU did not have a material effect on the Company’s consolidated financial statements.

In June 2011, the FASB issued ASU 2011-05 Comprehensive Income (Topic 220), “Presentation of Comprehensive Income”. In this Update, an entity has the option to present the total of comprehensive income, the components of net income, and the components of other comprehensive income either in a single continuous statement of comprehensive income or in two separate but consecutive statements. In both choices, an entity is required to present each component of net income along with total net income, each component of other comprehensive income along with a total for other comprehensive income, and a total amount for comprehensive income. Regardless of whether an entity chooses to present comprehensive income in a single continuous statement or in two separate but consecutive statements, the entity is required to present on the face of the financial statements reclassification adjustments for items that are reclassified from other comprehensive income to net income in the statement(s) where the components of net income and the components of other comprehensive income are presented.

The amendments in Topic 860 should be applied retrospectively. For public entities, the amendments are effective for fiscal years, and interim periods within those years, beginning after December 15, 2011, and early adoption is permitted. The adoption of this ASU did not have a material impact on the Company's consolidated financial statements.

In July 2012, the FASB issued ASU 2012-02, Intangibles-Goodwill and Other (Topic 350) - Testing Indefinite-Lived Intangible Assets for Impairment. The ASU provides entities with an option to first assess qualitative factors to determine whether events or circumstances indicate it is more likely than not the indefinite-lived intangible asset is impaired. If an entity concludes it is more than 50% likely that an indefinite-lived intangible asset is not impaired, no further analysis is required. However, if an entity concludes otherwise, it would be required to determine the FV of the indefinite-lived intangible asset to measure the amount of impairment, if any, as currently required under US GAAP. The ASU is effective for annual and interim impairment tests performed for fiscal years beginning after September 15, 2012. Early adoption is permitted. The adoption of this pronouncement will not have a material impact on our financial statements.

NOTE 3 – CASH AND EQUIVALENTS

As of September 30, 2012 and June 30, 2012 our cash and equivalents primarily consisted of cash and certificates of deposits with original maturities of three months or less.

NOTE 4 - MARKETABLE SECURITIES

Marketable securities consisted of equity securities and available-for-sale bonds, which are classified as Level 1 securities, and were as follows:

| September 30, 2012 | ||||||||||||||||

| Cost or | Gross | Gross | Total | |||||||||||||

| Amortized | Unrealized | Unrealized | Estimated | |||||||||||||

| Cost | Gains | Losses | Fair Value | |||||||||||||

| Level 1 securities: | ||||||||||||||||

| Equity securities | $ | 25,133 | $ | - | $ | - | $ | 25,133 | ||||||||

| Government bonds | 105,929 | - | (1,685 | ) | 104,244 | |||||||||||

| $ | 131,062 | $ | - | $ | (1,685 | ) | $ | 129,377 | ||||||||

| F-15 |

NOTE 5 – OTHER CURRENT ASSETS

The Company’s other current assets consisted of the following, as of September 30, 2012 and June 30, 2012 (audited):

| September 30, 2012 | June 30, 2012 | |||||||

| Prepaid rent | $ | 70,412 | $ | 34,371 | ||||

| Deductible business tax credit | 250,105 | - | ||||||

| Other | 88,894 | 14,270 | ||||||

| Total other current assets | $ | 409,411 | $ | 48,640 | ||||

NOTE 6– PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment consisted of the following, as of September 30, 2012 and June 30, 2012 (audited):

| September 30, 2012 | June 30, 2012 | |||||||

| Office Equipment | $ | 353,001 | $ | 304,509 | ||||

| Office Furniture | 1,965,676 | 57,018 | ||||||

| Leasehold improvement | 612,874 | - | ||||||

| Transportation equipment | 99,238 | - | ||||||

| Other equipment | 148,865 | - | ||||||

| Total | 3,179,654 | 460,994 | ||||||

| Less: Accumulated Depreciation | (2,103,692 | ) | (346,049 | ) | ||||

| Total property, plant and equipment, net | $ | 1,075,962 | $ | 114,945 | ||||

| F-16 |

NOTE 7– OTHER ASSETS

The Company’s other assets mainly consist of deposits and restricted cash. Restricted cash is a deposit in bank by the Company in conformity with Provisions on the Supervision and Administration of Specialized Insurance Agencies, and cannot be withdrawn without the permission of the China Insurance Regulatory Commission. Deposits include long-term leasing deposits.

NOTE 8 – GOODWILL

On September 6, 2010, Henan Anhou paid RMB532,622 ($78,318) to acquire 100% of Sichuan Kangzhuang from its previous shareholders. Sichuan Kangzhuang then had net liabilities of RMB219,123 ($32,134). Goodwill of RMB751,745 ($110,452) was therefore recorded. Goodwill in the balance sheet differs from the acquisition date amount due to changes in exchange rates. As of September 30, 2012, there are no indications of any impairment. No intangible assets are identified in the acquisition date. At the date of acquisition, Sichuan Kangzhuang has no unfulfilled customer contract or software. Sichuan Kangzhuang’s business process and accounting system are not unique and the management planned to use unified operating platform after the acquisition. Sichuan Kangzhuang’s business is mainly with retailing customers, and the management considered there is no customer relationship or customer list that will probably create future business opportunities for the Company.

On September 28, 2010, Henan Anhou acquired 100% of Jiangsu Law for RMB518,000 ($75,475). Jiangsu Law then had net assets of RMB2,286,842 ($341,425). Based on the purchase price allocation, the FV of the identifiable assets and liabilities assumed exceeded the FV of the consideration paid. As a result, the Company recorded a gain on acquisition of RMB1,768,842 ($267,156). We believe the gain on acquisition resulted from the sellers’ intent to exit the insurance business. To comply with the PRC requirements for the insurance brokerage companies, Henan Anhou contributed cash to increase the paid-in capital of Jiangsu Law to RMB10,000,000 ($1,355,150) from RMB5,180,000 ($625,113) on January 18, 2011.

NOTE 9 – ACQUISITION DURING THE PERIOD

On August 24, 2012, the Company acquired all of the issued and outstanding shares of AHFL for $2,750,910. NT$15 million ($500,815) and NT$7.5 million ($250,095) payable in cash in two installments, as well as issue 10 million shares of common stock at market price of $0.20 per share. The FV of the identifiable assets and liabilities of AHFL at acquisition date was $8,047,654. The company recorded the $5,280,043 excess of purchase price over the FV of assets and liabilities acquired as bargain gain on purchase. We believe the gain on acquisition resulted from the sellers' strategic intent to enter PRC market, which has a higher growth rate than Taiwan, and to become the shareholder of an OTCBB company.

We use August 31, 2012 as the closest available date to value the FV of the identifiable assets and liabilities of AHFL at acquisition date. The consolidated statement of income and other comprehensive income for the three months ended September 30, 2012 contains AHFL’s statement of income and other comprehensive income for September 2012. The consolidated balance sheets as of September 30, 2012 contains AHFL’s balance sheets as of September 30, 2012.

| F-17 |

A summary of AHFL’s assets and liabilities acquired as of the dates of acquisition is presented below:

| August 31, 2012 | ||||

| (Unaudited) | ||||

| ASSETS | ||||

| Current assets | ||||

| Cash and equivalents | $ | 12,766,882 | ||

| Marketable securities | 127,834 | |||

| Accounts receivable, net | 2,180,392 | |||

| Other current assets | 490,046 | |||

| Total current assets | 15,565,154 | |||

| Property, plant and equipment, net | 976,446 | |||

| Other assets | 380,771 | |||

| TOTAL ASSETS | $ | 16,922,371 | ||

| LIABILITIES | ||||

| Current liabilities | ||||

| Taxes payable | $ | (611,250 | ) | |

| Other current liabilities | (4,076,879 | ) | ||

| Advance to related party | (31,582 | ) | ||

| TOTAL CURRENT LIABILITIES | (4,719,711 | ) | ||

| BARGAIN GAIN | $ | (5,280,042 | ) | |

| NON CONTROLLING INEREST | $ | (4,171,708 | ) | |

| PURCHASE CONSIDERATION | $ | 2,750,910 | ||

NOTE 10 –OTHER CURRENT LIABILITIES

Other current liabilities are as follows, as of September 30, 2012 and June 30, 2012 (audited):

| September 30, 2012 | June 30, 2012 | |||||||

| Commission payable | $ | 2,117,090 | $ | 16,604 | ||||

| Due to previous shareholders of AHFL | 750,910 | - | ||||||

| Due to previous shareholders of Jiangsu Law | 81,710 | 81,899 | ||||||

| Others | 633,944 | 188,406 | ||||||

| Total other current liabilities | $ | 3,583,654 | $ | 286,909 | ||||

Commissions due to sub-agents and salary payable to administration staff are usually settled within 12 months. Due to previous shareholders of AHFL is the balance described in Note 9. Due to previous shareholders of Jiangsu Law is the remaining balance of the acquisition cost. The acquisition agreement between the parties has not specified the exact time for payment of the acquisition price or imposed any interest for late payment. Others are mainly for operating expenses payable within the credit terms provided by suppliers.

NOTE 11– INCOME TAX

CU WFOE, the Company’s subsidiary, and the VIEs in the PRC, are governed by the Income Tax Law of the PRC concerning the private-run enterprises, which are generally subject to tax at 25% on income reported in the statutory financial statements after appropriated adjustments. Except for Jiangsu Law, according to the requirement of local tax authorities, the tax basis is deemed as 10% of total revenue, instead of net income. The tax rate of Jiangsu Law is also 25%.

According to tax regulations by Chinese tax authorities effective January 1, 2008, commissions paid to sub-agents in excess of 5% of the commission revenue were not tax deductible. Therefore, as of June 30 2012, Henan Anhou and Sichuan Kangzhuang accrued income tax payable of $400,229 for non-deductible commissions occurred before June 30, 2012.

| F-18 |

According to China State Administration of Taxation #15 Announcement in 2012, effective from 2011, such commissions can be fully deducted. Also, such tax payable over three years can be reversed. Therefore we reversed the tax payable of $57,867 that was accrued before September 30, 2009 for such originally non-deductible commission and credited as income tax benefit. This leads to income tax benefit of $10,819 for the three months ended September 30, 2012.

The Company’s subsidiaries in Taiwan are governed by the Income Tax Law of Taiwan, and are generally subject to tax at 17% on income reported in the statutory financial statements after appropriate adjustments.

The balance of income tax payable as of September 30, 2012 mainly is the income tax accrued for the un-deductible commission paid to sub-agents before 2011 and is due upon written request of the local tax bureau.

The following table reconciles the US statutory rates to the Company’s effective tax rate for the three months ended September 30, 2012 and 2011:

| 2012 | 2011 | |||||||

| US statutory rate (benefit) | 34 | % | 34 | % | ||||

| Tax rate difference | (1 | )% | (4 | )% | ||||

| Tax basis difference | - | % | (19 | )% | ||||

| Non-deductible commission expense | 1 | % | (44 | )% | ||||

| Gain on bargain purchase of subsidiary | (34 | )% | - | % | ||||

| Tax (benefit) per financial statements | - | % | (33 | )% | ||||

| F-19 |

NOTE 12 - RELATED PARTY TRANSACTIONS

Due to related parties

The related parties listed below loaned money to the Company for working capital. Due to related parties consisted of the following as of September 30, 2012 and June 30, 2012 (audited):

| September 30, 2012 | June 30, 2012 | |||||||

| Due to Mr. Mao (Principal Shareholder of the Company) | $ | 233,453 | $ | 1,871 | ||||

| Due to Ms. Zhu (Shareholder of Henan Anhou) | 532,219 | 441,272 | ||||||

| Due to Mr. Zhu (Legal Representative of Jiangsu Law) | 2,184 | 2,189 | ||||||

| Total | $ | 767,856 | $ | 445,332 | ||||

During the three months ended September 30, 2012, Mr. Mao paid $ 233,453 in expenses on behalf of the Company, for the professional services fees related to the acquisition of AHFL. During the three months ended September 30, 2012, Ms. Zhu lent $90,947 to Henan Anhou to fund its operation. The amounts are interest-free, unsecured and repayable on demand.

NOTE 13 – COMMITMENTS

Operating Leases

The Company has operating leases for its offices. The rental expenses for the three months ended September 30, 2012 and 2011 are $399,163 and $60,757, respectively. At September 30, 2012, total future minimum lease payments under operating leases were as follows, by years:

| 2013 | $ | 1,172,627 | ||

| 2014 | 389,538 | |||

| 2015 | 65,325 | |||

| Total | $ | 1,627,491 |

NOTE 14– FINANCIAL RISK MANAGEMENT AND FAIR VALUES

The Company has exposure to credit, liquidity and market risks which arise in the normal course of its business. This note presents information about the Company's exposure to each of these risks, the Company's objectives, policies and processes for measuring and managing risk, and the Company's management of capital. Further quantitative disclosures are included throughout these consolidated financial statements.

The Board of Directors (“BOD”) has overall responsibility for the establishment and oversight of the Company's risk management framework. The Company's risk management policies are established to identify and analyze the risks faced by the Company, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly to reflect changes in market conditions and the Company's activities. The Company, through its training and management standards and procedures, aims to develop a disciplined and constructive control environment in which all employees understand their roles and obligations.

The Company's BOD oversees how management monitors compliance with the Company's risk management policies and procedures and reviews the adequacy of the risk management framework in relation to the risks faced by the Company.

| (a) | Credit risk |

The Company's credit risk arises principally from accounts and other receivables, pledged deposits and cash and equivalents. Management has a credit policy in place and monitors exposures to these credit risks on an ongoing basis. The carrying amounts of trade and other receivables, pledged deposits and cash and cash equivalents represent the Company's maximum exposure to credit risks. Accounts receivable are due within 30 days from the date of billing.

| F-20 |

| (b) | Liquidity risk |

The BOD of the Company is responsible for the Company's overall cash management and raising borrowings to cover expected cash demands. The Company regularly monitors its liquidity requirements, to ensure it maintains sufficient reserves of cash and readily realizable marketable securities and adequate committed lines of funding from major financial institutions to meet its liquidity requirements in the short and longer term.

| (c) | Currency risk |

The functional currency for the subsidiaries in Taiwan is $NT, and the functional currency for the subsidiaries and VIEs in PRC is RMB. The financial statements of the Company are in USD. The fluctuation of $NT and RMB will affect our operating results expressed in USD. The Company reviews its foreign currency exposures. The management does not consider its present foreign exchange risk to be significant.

NOTE 15– GEOGRAPHICAL SALES

The geographical distribution of China United’s revenue for the three months ended September 30, 2012 and 2011 is as follows:

| Geographical Areas | 2012 | 2011 | ||||||

| PRC | $ | 743,921 | $ | 660,262 | ||||

| Taiwan | 2,475,379 | - | ||||||

| $ | 3,219,300 | $ | 660,262 | |||||

NOTE 16– CONDENSED FINANCIAL INFORMATION OF US PARENT

China United is a holding company and owns no operating assets and has no significant operations independent of its subsidiaries. Set forth below are condensed financial statements for China United on a stand-alone, unconsolidated basis as of September 30, 2012 and June 30, 2012 (audited), and for the three months ended September 30, 2012 and 2011.

CHINA UNITED INSURANCE SERVICE, INC.

BALANCE SHEETS

SEPTEMBER 30, 2012 AND JUNE 30, 2012

| September 30, 2012 | June 30, 2012 | |||||||

| ASSETS | ||||||||

| Investment in subsidiaries | $ | 9,172,959 | $ | 641,254 | ||||

| TOTAL ASSETS | $ | 9,172,959 | $ | 641,254 | ||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||

| Other current liabilities | $ | 752,781 | $ | - | ||||

| Due to related party | 200,000 | 583 | ||||||

| TOTAL LIABILITIES | $ | 952,781 | $ | 583 | ||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Preferred stock, par value, $0.00001, 100,000,000 authorized, 1,000,000

issued and outstanding as of September 30, 2012, none issued and outstanding as of June 30, 2012 | 10 | - | ||||||

| Common stock, par value $0.00001, 100,000,000 authorized, 29,100,503 and 20,000,000 issued and outstanding at September 30, 2012 and June 30, 2012, respectively | 291 | 200 | ||||||

| Additional paid-in capital | 4,674,593 | 2,614,691 | ||||||

| Accumulated other comprehensive loss | 177,563 | (55,250 | ) | |||||

| Accumulated deficit | 3,367,721 | (1,918,972 | ) | |||||

| TOTAL STOCKHOLDERS’ EQUITY | 8,220,178 | 640,671 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 9,172,959 | $ | 641,254 | ||||

| F-21 |

CHINA UNITED INSURANCE SERVICE, INC.

STATEMENTS OF OPERATIONS

THREE MONTHS ENDED SEPTEMBER 30,

| 2012 | 2011 | |||||||

| Revenues | $ | - | $ | - | ||||

| Cost of revenue | - | - | ||||||

| Gross profit | - | - | ||||||

| Operating expenses: | - | |||||||

| General and administrative | 200,000 | - | ||||||

| Loss from operations | (200,000 | ) | - | |||||

| Other expenses | ||||||||

| Equity income from subsidiaries | 206,651 | (278,908 | ) | |||||

| Bargain gain on purchase of subsidiaries | 5,280,042 | (278,908 | ) | |||||

| Income (loss) before income taxes | 5,358,249 | (278,908 | ) | |||||

| Income tax expense | - | - | ||||||

| Net income (loss) | $ | 5,286,693 | $ | (278,908 | ) | |||

NOTE 17 – PRO FORMA CONSOLIDATED STATEMENT OF INCOME (UNAUDITED)

The basis of pro forma consolidated statements of income of the Company is as if the Acquisition Agreement were signed on July 1, 2010 and 2011, and AHFL’s acquisition of Law Enterprise happened on the same date. The pro forma consolidated statements of income were derived from the statement of income for the three months ended September 30, 2012 and 2011 of AHFL and CUIS. The company recorded the excess of purchase price over the fair value of assets and liabilities acquired as bargain gain on purchase in the pro forma consolidated statements of income.

CHINA UNITED INSURANCE SERVICE, INC. AND SUBSIDIARIES

PRO FORMA CONSOLIDATED STATEMENTS OF OPERATIONS AND OTHER COMPREHENSIVE INCOME

| Year Ended June 30 2012 | ||||||||||||||||

| CUIS | AHFL | Pro Forma Adjustment | Pro Forma | |||||||||||||

| Revenues | $ | 743,921 | $ | 8,923,089 | $ | - | $ | 9,667,010 | ||||||||

| Cost of revenue | 440,608 | 6,057,569 | - | 6,498,177 | ||||||||||||

| Gross profit | 303,313 | 2,865,520 | - | 3,168,833 | ||||||||||||

| Operating expenses: | ||||||||||||||||

| General and administrative | 290,980 | 1,684,415 | - | 1,975,395 | ||||||||||||

| Income (loss) from operations | 12,333 | 1,181,105 | - | 1,193,438 | ||||||||||||

| Other income / (expenses) | ||||||||||||||||

| Interest income | 646 | - | - | 646 | ||||||||||||

| Gain on acquisition of subsidiary | - | - | 5,280,042 | 5,280,042 | ||||||||||||

| Other - net | 1,123 | 1,816,168 | - | 1,817,291 | ||||||||||||

| 1,769 | 1,816,168 | 5,280,042 | 7,097,979 | |||||||||||||

| Income before income taxes | 14,102 | 2,997,273 | 5,280,042 | 8,291,417 | ||||||||||||

| Income tax expense (benefit) | (53,959 | ) | 223,280 | - | 169,321 | |||||||||||

| Net income | 68,061 | 2,773,993 | 5,280,042 | 8,122,096 | ||||||||||||

| Net income attributable to the non-controlling interests | - | 368,193 | - | 368,193 | ||||||||||||

| Net income attributable to CUIS’s shareholders | 68,061 | 2,405,800 | 5,280,042 | 7,753,903 | ||||||||||||

| Weighted average shares outstanding: | ||||||||||||||||

| Basic and diluted | 23,433,833 | |||||||||||||||

| Earning per share: | ||||||||||||||||

| Basic and diluted | $ | 0.33 | ||||||||||||||

| F-22 |

CHINA UNITED INSURANCE SERVICE, INC. AND SUBSIDIARIES

PRO FORMA CONSOLIDATED STATEMENTS OF OPERATIONS AND OTHER COMPREHENSIVE INCOME

| Year Ended June 30 2011 | ||||||||||||||||

| CUIS | AHFL | Pro Forma Adjustment |

Pro Forma | |||||||||||||

| Revenues | $ | 660,262 | $ | 8,152,007 | $ | - | $ | 8,812,269 | ||||||||

| Cost of revenue | 531,363 | 5,532,281 | - | 6,063,644 | ||||||||||||

| Gross profit | 128,899 | 2,619,726 | - | 2,748,625 | ||||||||||||

| Operating expenses: | ||||||||||||||||

| General and administrative | 350,643 | 1,500,576 | - | 1,851,219 | ||||||||||||

| Income (loss) from operations | (221,744 | ) | 1,119,150 | - | 897,406 | |||||||||||

| Other income / (expenses) | ||||||||||||||||

| Interest income | 1,080 | 399,973 | - | 401,053 | ||||||||||||

| Gain on acquisition of subsidiary | - | - | - | - | ||||||||||||

| Other - net | (1,322 | ) | 1,328,874 | - | 1,327,552 | |||||||||||

| (242 | ) | 1,728,847 | - | 1,728,605 | ||||||||||||

| Income before income taxes | (221,986 | ) | 2,847,997 | - | 2,626,011 | |||||||||||

| Income tax expense | 72,419 | 0 | - | 72,419 | ||||||||||||

| Net income (loss) | (294,405 | ) | 2,847,997 | - | 2,553,592 | |||||||||||

| Net income attributable to the non-controlling interests | - | - | - | - | ||||||||||||

| Net income (loss) attributable to CUIS’s shareholders | (294,405 | ) | 2,847,997 | - | 2,553,592 | |||||||||||

| Weighted average shares outstanding: | ||||||||||||||||

| Basic and diluted | 23,433,833 | |||||||||||||||

| Earning per share: | ||||||||||||||||

| Basic and diluted | $ | 0.11 | ||||||||||||||

| F-23 |

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read this Management’s Discussion and Analysis in conjunction with the Consolidated Financial Statements and Related Notes.

Overview

China United Insurance Service, Inc. (“China United” or the “Company”) is a Delaware corporation organized on June 4, 2010 by Mao Yi Hsiao, a Taiwanese citizen, as a listing vehicle for ZLI Holdings Limited (“CU Hong Kong”) to be quoted on the Over the Counter Bulletin Board (the “OTCBB”). CU Hong Kong, a wholly owned Hong Kong-based subsidiary of China United, was founded by China United on July 12, 2010 under Hong Kong laws. On October 20, 2010, CU Hong Kong founded a wholly foreign owned enterprise, Zhengzhou Zhonglian Hengfu Business Consulting Co., Ltd. (“CU WFOE”) in Henan province in the People’s Republic of China (“the PRC”).

On January 16, 2011, China United issued 20,000,000 shares of common stock, $0.00001 par value per share, to several non US persons for $300,000 in cash invested in the Company’s subsidiaries. The issuance was made pursuant to an exemption from registration contained in Regulation S under the Securities Act of 1933, as amended. The consideration was paid as of June 30, 2012. On January 28, 2011, the Company increased the number of authorized shares from 30,000,000 shares of common stock to 100,000,000 shares of common and 10,000,000 shares of preferred stock.

Henan Law Anhou Insurance Agency Co., Ltd. (“Henan Anhou”, formerly known as Zhengzhou Anhou Insurance Agency Co., Ltd.) was incorporated in the PRC on August 20, 2003. Henan Anhou provides insurance agency services in the PRC. On August 16, 2010, Ms. Zhu Shuqin contributed RMB8,000,000 ($1,175,440) in cash to Henan Anhou and controlled 80% of Henan Anhou shares.

Sichuan Kangzhuang Insurance Agency Co., Ltd. (“Sichuan Kangzhuang”) was founded on July 10, 2006 in Sichuan province in the PRC and provides insurance agency services in the PRC. On August 23, 2010, at Sichuan Kangzhuang’s general meeting of shareholders, its shareholders voted to sell their shares to Henan Anhou for RMB532,622 ($83,444). On September 6, 2010, the equity transfer agreements were signed between Henan Anhou and each shareholder of Sichuan Kangzhuang.

Jiangsu Law Insurance Broker Co., Ltd. (“Jiangsu Law”) was founded on September 19, 2005 in Jiangsu Province in the PRC and provides insurance brokerage services in the PRC. On August 12, 2010, at Jiangsu Law’s general meeting of shareholders, its shareholders voted to sell their shares to Henan Anhou for RMB518,000 ($81,153) and Henan Anhou increased Jiangsu Law’s paid-in capital to RMB10,000,000 ($1,566,661) from RMB5,180,000 ($811,531) on January 18, 2011 to meet the PRC paid-in capital requirements for insurance brokerage companies. On September 28, 2010, the equity transfer agreements were signed between Henan Anhou and each shareholder of Jiangsu Law.

Recent Acquisition of AHFL

On August 24, 2012, the Company acquired all of the issued and outstanding shares of Action Holdings Financial Limited (“AHFL”), a limited liability company (“LLC”) incorporated under the laws of British Virgin Islands on April 30, 2012, together with its subsidiaries in Taiwan. Subsequent to the acquisition, AHFL became a 100% owned subsidiary of the Company.

| 1 |

AHFL holds 65.95% of the issued and outstanding shares of Law Enterprise Co., Ltd. (“Law Enterprise”), a company limited by shares incorporated under the laws of Taiwan on January 30, 1996. Law Enterprise holds (i) 100% Law Insurance Broker Co., Ltd. (“Law Broker”), a company limited by shares incorporated in Taiwan on October 9, 1992; (ii) 97.84% of Law Risk Management & Consultant Co., Ltd. (“Law Management”), a company limited by shares incorporated in Taiwan on December 5, 1987; and (iii) 96% of Law Insurance Agent Co., Ltd. (“Law Agent” collectively with “Law Enterprise”, “Law Broker” and “Law Agent”, the “Taiwan Subsidiaries”, each a “Taiwan Subsidiary”), a LLC incorporated in Taiwan on June 3, 2000.

Law Enterprise is a holding company of its operating subsidiaries in Taiwan. Law Broker primarily engages in insurance brokerage and insurance agency service business across Taiwan, while Law Management and Law Agent are not active. We operate our Taiwan business primarily through Law Broker.

Due to PRC legal restrictions on foreign ownership and investment in insurance agency and brokerage businesses in China, especially those on qualifications and capital requirements of the investors, we operate our business primarily through our Consolidated Affiliated Entities (“CAE”) in China. We do not hold equity interests in our CAE. However, through the variable interest entities (“VIE”) Agreements with these CAE and their respective shareholders, we effectively control, and are able to derive substantially all of the economic benefits from, these CAE.

Our CAE in China are VIE through which all of our insurance services are operated. It is through the VIE Agreements that we have effective control of the CAE, which allows us to consolidate the financial results of the CAE in our financial statements. If Henan Anhou and its shareholders fail to perform their obligations under the VIE Agreements, we could be limited in our ability to enforce the VIE Agreements that give us effective control. Furthermore, if we are unable to maintain effective control of our CAE, we would not be able to continue to consolidate the CAE’s financial results with our financial results. During fiscal years ended June 30, 2011 and 2012, 100% of our revenues in our consolidated financial statements were derived from our CAE. For more information see “Risk Factors-Risks Related to Our Corporate Structure.”

| 2 |

| 3 |

On January 17, 2011, CU WFOE and Henan Anhou and its shareholders entered into a series of agreements known as variable interest agreements (the “VIE Agreements”) pursuant to which CU WFOE has executed effective control over Henan Anhou through these contractual arrangements.

As of September 30, 2012, through our CAE, we had two insurance agencies and one brokerage and 37 service outlets with 1,075 full-time sales professionals, 37 part-time sales professionals and 67 administrative staff in Henan, Sichuan and Jiangsu provinces in China. In addition, through Law Insurance Broker Co., Ltd., we had 22 sales and service outlets (including the headquarters) and 1,309 full-time sales professionals, 373 part-time sales professionals and 151 administrative staff in Taiwan.

Critical Accounting Policies