Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF PRICEWATERHOUSECOOPERS LLP - ENANTA PHARMACEUTICALS INC | d401292dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on November 16, 2012

Registration No. 333-184779

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ENANTA PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| DELAWARE | 2834 | 04-3205099 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

500 Arsenal Street

Watertown, Massachusetts 02472

(617) 607-0800

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Jay R. Luly, Ph.D.

President and Chief Executive Officer

Enanta Pharmaceuticals, Inc.

500 Arsenal Street

Watertown, Massachusetts 02472

(617) 607-0800

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Nathaniel S. Gardiner, Esq. Stacie S. Aarestad, Esq. Edwards Wildman Palmer LLP 111 Huntington Avenue Boston, Massachusetts 02199 (617) 239-0100 |

Richard D. Truesdell, Jr., Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer þ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated November 16, 2012

Prospectus

Shares

COMMON STOCK

This is the initial public offering of common stock of Enanta Pharmaceuticals, Inc. We are selling shares of common stock. Prior to this offering, there has been no public market for our common stock. The initial public offering price of our common stock is expected to be between $ and $ per share.

We have applied to list our common stock on The NASDAQ Global Market under the symbol “ENTA.”

We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012 and, as such, may elect to comply with certain reduced public company reporting requirements for future filings.

| Per share | Total | |||

| Initial public offering price |

$ | $ | ||

| Underwriting discounts and commissions |

$ | $ | ||

| Proceeds to Enanta, before expenses |

$ | $ |

We have granted the underwriters an option to purchase up to additional shares of common stock to cover over-allotments, if any.

Investing in our common stock involves risk. See “Risk Factors” beginning on page 10.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2012.

| J.P. Morgan | Credit Suisse | |

| Leerink Swann | JMP Securities | |

, 2012

Table of Contents

We and the underwriters have not authorized anyone to provide any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where such offers and sales are permitted. The information in this prospectus or any free writing prospectus is accurate only as of its date, regardless of its time of delivery or of any sale of shares of our common stock offered hereby. Our business, financial condition, results of operations and prospects may have changed since that date. We will update this prospectus as required by law.

Until , 2012 (the 25th day after the date of this prospectus), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

This prospectus includes statistical and other industry and market data that we obtained from industry publications and research, surveys and studies conducted by third parties. Industry publications and third party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe these industry publications and third party research, surveys and studies are reliable, we have not independently verified such data.

The Enanta name and logo are our trademarks. This prospectus also includes trademarks, trade names and service marks of other persons. All other trademarks, trade names and service marks appearing in this prospectus are the property of their respective owners.

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including the more detailed information set forth under “Risk Factors” and our financial statements and the related notes appearing at the end of this prospectus, before making an investment decision. Some of the statements in this prospectus are forward-looking statements. See “Special Note Regarding Forward-Looking Statements.” In this prospectus, unless the context otherwise requires, references to “we,” “us,” “our,” or “Enanta” refer to Enanta Pharmaceuticals, Inc.

Overview

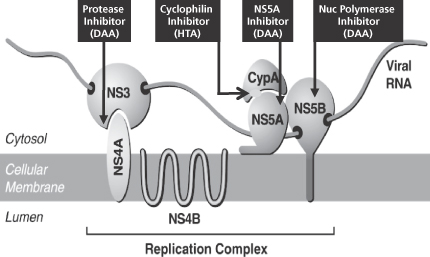

We are a research and development-focused biotechnology company that uses its robust chemistry-driven approach and drug discovery capabilities to create small molecule drugs in the infectious disease field. We are discovering and developing inhibitors designed for use against the hepatitis C virus, referred to as HCV. We believe that a successful approach to a complete cure for HCV in most patients will likely require treatment with a combination of drugs that attack different mechanisms necessary for replication and survival of HCV. Further, as there are many variants of HCV, we are developing inhibitors that may be used in multiple combination therapies, each designed and tested for effectiveness against one or more of those variants. Our development of inhibitors for validated HCV target mechanisms, as well as our collaborations with Abbott Laboratories and Novartis, should allow us to participate in multiple unique drug combinations as we seek the best combination therapies for HCV in its various forms. Total worldwide sales of HCV therapies were over $3.5 billion in 2011. We believe that annual worldwide sales of these therapies and future approved therapies could increase sales in this market to $10 to $20 billion within the next ten years. In addition to our HCV programs, we have used our internal research capabilities to discover a new class of antibiotics which we are developing for the treatment of multi-drug resistant bacteria, including methicillin-resistant Staphylococcus aureus bacteria, also referred to as MRSA. We have utilized our internal chemistry and drug discovery capabilities and our collaborations to generate all of our development-stage programs, and we have active research efforts to broaden our infectious disease drug pipeline.

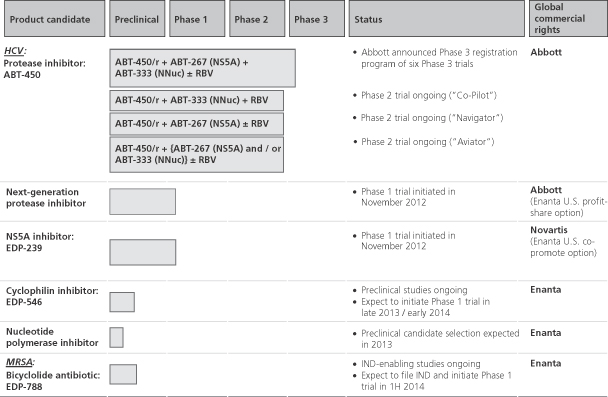

We are pursuing four fundamental, validated targets within the HCV field that represent a broad approach to the disease and specifically address the urgent unmet medical needs for the treatment of HCV. The following table summarizes our product development pipeline in HCV antivirals as well as MRSA antibiotics:

Note: “/r” refers to ritonavir; “NNuc” refers to non-nucleoside polymerase inhibitor; “RBV” refers to ribavirin.

1

Table of Contents

As detailed above, our only product candidate that has advanced beyond Phase 2 clinical trials is ABT-450. Phase 3 trials of ABT-450 in combination therapy started in October 2012. Phase 3 clinical trials are often lengthy and usually involve from many hundred to thousands of patients. We estimate that it will likely be at least two years before a New Drug Application, or NDA, for one of our collaborators’ combination therapies could be approved by the FDA.

From our inception through September 30, 2012, we have generated $173.9 million from our collaborations (including those with Abbott and Novartis) in the form of upfront, milestone and funded research payments as well as equity investments. The total of these amounts is more than double the amount of our funding from venture capital equity investments, the last of which occurred in 2006. As of September 30, 2012, we had $45.4 million in cash and investments. In addition, under our collaboration with Novartis, we are entitled to receive an $11.0 million milestone payment based on Novartis’ November 2012 initiation of dosing in a Phase 1 clinical trial that includes EDP-239. We are also eligible to receive over the next several years an aggregate of over $440 million based on potential future pre-commercialization milestones under our Abbott and Novartis collaborations, assuming successful clinical trial results for the respective collaboration programs and our collaborators’ continued development of our product candidates through successful regulatory and reimbursement approvals in the United States and other major markets. In addition, we are also eligible to receive tiered royalties ranging on a blended basis from the low double digits up to the high teens on worldwide net sales of any protease inhibitors or NS5A inhibitors under the collaborations, as well as sales milestones under our Novartis collaboration.

ABT-450/r, a Protease Inhibitor for HCV Infection

ABT-450, discovered through our collaboration with Abbott, is a potent protease inhibitor that has demonstrated in vitro potency against known resistant HCV mutants. In Phase 1 studies, ABT-450 co-administered with ritonavir, a commonly used boosting agent to increase the blood concentrations of many protease inhibitors, was shown to be safe and well tolerated. Co-administration of ABT-450 with ritonavir, which we refer to together as ABT-450/r, has enabled once-daily dosing of ABT-450. Phase 2 studies have demonstrated the efficacy of ABT-450/r in patients with chronic HCV. ABT-450/r is being tested for the treatment of HCV in several additional interferon-free Phase 2 studies in combination with Abbott’s non-nucleoside polymerase and NS5A inhibitors. In addition, Abbott has started Phase 3 studies of ABT-450/r for the treatment of HCV in combination with Abbott’s polymerase and NS5A inhibitors, plus ribavirin. While Abbott and other companies are developing interferon-free and interferon/ribavirin-free HCV therapies in clinical trials, the efficacy of this approach has not yet been proven conclusively, nor has it resulted yet in any product approved by the FDA.

We believe that a treatment regimen containing ABT-450/r may have significant advantages over currently approved HCV treatment regimens containing protease inhibitors because of the following key attributes:

| • | Improved Antiviral Activity. Compared to the current market leader, telaprevir (Incivek™, Vertex Pharmaceuticals), ABT-450 has demonstrated superior antiviral activity against HCV in patients. |

| • | No Interferon. Current HCV therapy still includes injected interferon, which is often associated with flu-like symptoms, fatigue, headaches and nausea during treatment. ABT-450/r, however, is being developed in a number of interferon-free regimens. |

| • | Tolerability. Serious side effects of current regimens containing protease inhibitors include rash, anemia, itching and gastrointestinal effects. In contrast, most side effects in clinical trials to date of ABT-450/r were mild to moderate. |

| • | Shorter Treatment Regimen. ABT-450/r is being tested in various treatment combinations that are only 12 weeks in duration, as compared to the 24 to 48 weeks of treatment required with current interferon-containing regimens. |

| • | More Convenient Treatment Regimen. ABT-450/r is being developed for oral, once-daily dosing. All of the combinations including ABT-450/r that Abbott is testing include only orally administered drugs dosed either once or twice daily. By comparison, current approved treatment regimens require dosing of a protease inhibitor approximately every 8 hours as well as weekly interferon injections. |

2

Table of Contents

In the first quarter of 2010, we and Abbott announced the advancement of ABT-450/r into Phase 2 clinical trials. The objective of the initial Phase 2 study was to assess the safety, tolerability, pharmacokinetics and antiviral activity of multiple-dose strengths of ABT-450/r in treatment-naïve adults (i.e., those who have not previously received treatment for HCV) infected with HCV genotype 1, the most common genotype globally. This study with ABT-450/r paved the way for additional Phase 2 combination studies that use interferon-free regimens.

The next Phase 2 study, which began in October 2010 and is known as the Pilot study, consisted of genotype 1 patients enrolled in an open-label trial of a 12-week interferon-free regimen consisting of ABT-450/r 150/100 mg once daily plus ABT-072 (Abbott’s non-nucleoside polymerase inhibitor) 400 mg once daily plus weight-based ribavirin, a commonly used oral antiviral, 1000-1200 mg/day twice daily. A rapid decrease in HCV RNA level, a commonly used measure of effectiveness of HCV therapies, was observed with treatment, and all patients had HCV RNA levels below the lower limit of quantitation, or LLOQ, by week 3. The treatment regimen was well tolerated and achieved a sustained virologic response 24 weeks after conclusion of treatment, or SVR24, in 91% of treatment-naïve, non-cirrhotic HCV genotype 1-infected patients. The 91% SVR24 results in treatment naïve HCV genotype 1-infected patients are superior to published SVR results for any currently approved HCV therapies. Adverse events, or AEs, were mild and did not result in any study interruptions or discontinuations.

The Phase 2 Co-Pilot study, which began in May 2011, consisted of HCV genotype 1, non-cirrhotic patients enrolled in an open-label trial of a 12-week interferon-free regimen consisting of ABT-450/r once daily plus ABT-333 (Abbott’s non-nucleoside polymerase inhibitor) 400 mg twice daily plus weight-based ribavirin twice daily (1000-1200 mg total daily dose). Two different doses of ABT-450/r were evaluated (250/100 mg; 150/100 mg) in treatment-naïve patients, 85% of whom were infected with the harder-to-treat genotype 1a virus (compared to genotype 1b); treatment-experienced patients were also assessed, 94% of whom were infected with genotype 1a. Results demonstrated a sustained virologic response 12 weeks after conclusion of treatment, or SVR12, in 93-95% of treatment-naïve HCV genotype 1-infected patients and in 47% of previous non-responders. Co-Pilot is the first 12-week interferon-free regimen to date with high SVR rates and activity that appears not to be affected by HCV genotype 1 subtype. AEs were mild or moderate, and the most common were fatigue, nausea and headache.

The Phase 2b Aviator study, which began in October 2011, consisted of HCV genotype 1, non-cirrhotic patients enrolled in an open-label trial of several 12-week interferon-free regimens consisting of two or three direct acting antivirals, or DAAs, with and without ribavirin. One combination in the study consisted of ABT-450/r 100/100 to 200/100 mg once daily, plus ABT-267 (Abbott’s NS5A inhibitor) 25 mg once daily, plus ABT-333 (Abbott’s non-nucleoside polymerase inhibitor) twice daily (400 mg total daily dose), plus weight-based ribavirin twice daily (1000-1200 mg total daily dose). As reported in an initial data abstract from the ongoing study, this regimen was evaluated in treatment-naïve patients and treatment-experienced patients who were null responders. Results from this ongoing trial demonstrated SVR12 in 99% of treatment-naïve HCV genotype 1-infected patients and in 93% of previous null responders (as compared with 47% SVR12 seen in the Co-Pilot study as detailed above). The most common AEs were fatigue (28% and 27%) and headache (28% and 31%) for treatment-naïve and previous null responders, respectively. Initial results from the Pilot, Co-Pilot and Aviator studies provide compelling support for the potential development of an interferon-free combination therapy containing ABT-450 for treatment of HCV.

Studies of additional interferon-free ABT-450/r combinations are underway. The Navigator study, which began in September 2011, is evaluating ABT-450/r with Abbott’s NS5A inhibitor ABT-267 with and without ribavirin.

In November 2012, Abbott announced the full scope of its initial Phase 3 registrational trials program for an HCV treatment regimen (including ABT-450) for genotype 1-infected patients, including six Phase 3 trials designed for a total of 2,200 patients using a combination of three DAAs—ABT-450/r (protease inhibitor), ABT-267 (NS5A inhibitor) and ABT-333 (non-nucleoside polymerase inhibitor)—with or without ribavirin. Abbott had previously reported the start of three of these Phase 3 clinical trials and announced that it expected regulatory filings in 2014. The first of these reported trials, Turquoise II, which is in patients with compensated cirrhosis, will include two co-formulated tablets of ABT-450/r and ABT-267, or ABT-450/r/ABT-267, once daily, plus ABT-333 in one tablet twice daily, plus ribavirin. The other two trials, Sapphire I and Sapphire II, will be double-blind, placebo-controlled trials of the same three DAAs, co-administered with ribavirin. Sapphire I is in treatment-naïve patients and Sapphire II is in patients who have had prior treatment with interferon plus ribavirin. Three additional Phase 3 trials will

3

Table of Contents

study the same three-DAA combination, with and without ribavirin, in treatment-naïve genotype 1a-infected patients, treatment-naïve genotype 1b-infected patients and treatment-experienced genotype 1b-infected patients, respectively. In addition, Abbott has announced that it is conducting additional exploratory clinical studies to determine if a co-formulated tablet of ABT-450/r and ABT-267 dosed once daily can provide high cure rates in specific HCV populations. Abbott has also announced that its development plan would support a target commercial launch of a combination HCV therapy in early 2015, and that there is a potential worldwide market opportunity of $2 billion or more for the combinations being developed. Abbott’s projections are subject to risks and uncertainties. One or more Phase 3 trials containing ABT-450/r could take longer than anticipated to complete or could have unexpected results, the FDA could find that the results of these trials are not adequate to support marketing approval and the FDA could require additional clinical trials as a condition for approval.

We believe that we, together with Abbott, will obtain exclusivity in ABT-450 in the United States and other major-market jurisdictions based on pending composition and use patent claims for ABT-450, which we expect will continue at least into 2029, assuming all such patents are issued. Additional HCV protease inhibitors discovered within the Enanta-Abbott collaboration are in preclinical studies.

EDP-239, an NS5A Inhibitor for HCV Infection

EDP-239 is the lead NS5A inhibitor discovered by Enanta. We entered into a collaboration with Novartis in February 2012, granting Novartis exclusive, worldwide rights to develop, manufacture and commercialize EDP-239. The compound has demonstrated potent activity against major genotypes in the replicon assay, which is a common in vitro test for determining potency of an active compound in reducing HCV replication. In addition, EDP-239 has additive to synergistic antiviral activity when used in combination with other anti-HCV therapeutics in the replicon assay. Preclinical studies support excellent permeability and absorption potentials in humans, with preferential targeting to the liver, which is the target site of infection. Human pharmacokinetic and pharmacodynamic modeling suggests a low, once-daily dose for future clinical testing. In November 2012, Novartis initiated a Phase 1 trial of EDP-239.

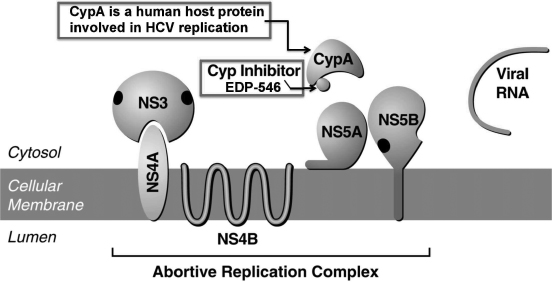

EDP-546, a Cyclophilin Inhibitor for HCV Infection

In anticipation of resistance arising to first-generation HCV therapy that targets viral proteins, we have been developing an alternative host-targeted antiviral, or HTA, approach that targets the human host protein, cyclophilin, which is essential for replication of HCV. We have demonstrated in replicon assays that one of our lead cyclophilin targeting inhibitors, EDP-546, is a potent inhibitor of HCV replication and is more potent than the clinical stage cyclophilin inhibitor alisporivir, under development by Novartis.

EDP-546 is an HTA with a high barrier to resistance which in preclinical studies has demonstrated a number of important attributes. EDP-546 has demonstrated the potential to have additive to synergistic antiviral activity when used in combination with DAAs and has not generated cross-resistance in HCV variants that are resistant to several DAAs. In addition, the superior metabolic stability profile of the drug compared to alisporivir suggests the potential for once-daily dosing of EDP-546.

A number of additional preclinical studies of EDP-546 have been initiated, and we expect to initiate a Phase 1 clinical trial in late 2013 or early 2014. In addition to EDP-546, we are continuing to generate and characterize a number of additional cyclophilin inhibitors in the discovery phase.

Nucleotide Polymerase Inhibitor Program for HCV Infection

We also have a program to develop nucleotide inhibitors to HCV NS5B polymerase, which is another DAA mechanism considered to have a high barrier to resistance. Our researchers have identified a promising nucleotide lead series with significant antiviral potency in vitro. One of our lead compounds has demonstrated better in vitro potency than a reference clinical stage nucleotide inhibitor, GS-7977, under development by Gilead Sciences.

We have an ongoing discovery effort in this inhibitor class and are considering a number of compounds for further development. We plan to select a candidate in 2013 that is suitable for advancement into preclinical studies.

4

Table of Contents

EDP-788 and Our Bicyclolide Antibiotics

Through our internal chemistry efforts, we have created a new family of macrolide antibiotics called Bicyclolides that overcomes resistance and possesses a significantly improved target product profile compared to existing macrolides such as Zithromax™ and BiaxinTM. Our lead Bicyclolide antibiotic product candidate is EDP-788, which we are developing for use as an intravenous drug in the hospital setting and for oral dosing in the home setting. EDP-788 is a prodrug, which means that it is inactive until it is converted in the body into an active compound. EDP-788 is a highly water-soluble molecule which, when administered in preclinical models, is cleanly and rapidly converted into the active compound.

The active compound generated from EDP-788 is EDP-322, a Bicyclolide we developed that demonstrates a broad spectrum of activity against many bacterial organisms, including MRSA. Preclinical safety studies performed with EDP-322 presented no significant concerns. EDP-322 was evaluated in normal healthy volunteers in two double-blind, randomized, placebo-controlled Phase 1 trials, evaluating pharmacokinetic and safety parameters. EDP-322 showed good pharmacokinetics and was well tolerated in all dose groups. Adverse events were limited to minor gastrointestinal effects attributed to inadequate water solubility of the drug, which we would not expect when dosing with the water-soluble EDP-788. Neither EDP-322, nor any other compound in the class of Bicyclolides, has yet been shown to be effective in pivotal clinical trials or resulted in any product approved by the FDA.

All current development activities are focused on intravenous and oral formulations of EDP-788, with additional IND-enabling studies in progress and the initiation of clinical trials planned for the first half of 2014. Our preclinical development of EDP-788 is funded under our contract with the National Institute of Allergy and Infectious Diseases, or NIAID, with potential for further NIAID funding of early clinical development.

Collaboration with Abbott Laboratories

In November 2006, we entered into a Collaborative Development and License Agreement with Abbott Laboratories to develop and commercialize HCV NS3 and NS3/4A protease inhibitors worldwide. Abbott has funded all research and development of our protease inhibitors since we entered into the collaboration and is responsible for all costs associated with the development, manufacturing and commercialization of ABT-450 and other compounds under this collaboration agreement. We received $57.2 million from Abbott upon signing the collaboration agreement and their simultaneous purchase of preferred stock from us in 2006, and we received a $40.0 million milestone payment in December 2010 following the successful completion of a Phase 2a clinical trial. Assuming Abbott’s successful development of the first protease inhibitor product, we will also be eligible to receive over $200 million of pre-commercialization milestone payments, as well as additional milestone payments for any follow-on protease inhibitor products and tiered royalties ranging on a blended basis from the low double digits up to the high teens on Abbott’s net sales, if any, allocable to any one of our collaboration’s protease inhibitors.

Collaboration with Novartis

In February 2012, we entered into a Collaboration and License Agreement with Novartis granting Novartis exclusive, worldwide rights to develop, manufacture and commercialize EDP-239, our lead compound from our NS5A inhibitor program. Novartis is responsible for all costs associated with the development, manufacture and commercialization of EDP-239, EDP-239-containing combinations and any follow-on NS5A inhibitors, as well as funding our efforts to discover follow-on NS5A inhibitors at least through February 2013. We received an upfront payment of $34.4 million in March 2012, and we are entitled to receive an $11.0 million milestone payment based on Novartis’ November 2012 initiation of dosing in a Phase 1 clinical trial that includes EDP-239. We are eligible to receive up to $395 million of additional payments if Novartis achieves specified clinical, regulatory, and commercial milestones. We are also eligible to receive tiered royalties ranging on a blended basis from the low double digits up to the high teens on any net sales allocable to our collaboration’s NS5A inhibitors.

Our Strategy

Our primary objective is to become a leader in the infectious disease field, with a focus on HCV and multi-drug resistant bacterial infections. Our strategy includes the following key elements:

| • | Develop compounds against four fundamental, validated HCV targets to give us multiple opportunities to participate in one or more of the potentially successful combination therapies for HCV in its various forms; |

5

Table of Contents

| • | Collaborate with large pharmaceutical partners to accelerate the development and commercialization of our lead HCV compounds in combination therapies; |

| • | Develop independently our own next generation HCV compounds and combination therapies with lower susceptibility to viral resistance; |

| • | Continue to leverage and fortify our intellectual property portfolio; and |

| • | Invest in research and early-stage development of product candidates for infectious diseases. |

Risks Associated with our Business

Our business is subject to a number of risks of which you should be aware before making an investment decision. These risks are discussed more fully in the “Risk Factors” section of this prospectus beginning on page 10. These risks include, among others, our financial prospects being substantially dependent upon the development and marketing efforts of Abbott and Novartis for any drug product candidates incorporating ABT-450 and EDP-239, respectively; substantial competition in the market for HCV and for anti-infectives generally; our lack of clinical development experience; our need to attract and retain senior management and key scientific personnel; risks associated with the lengthy, expensive and uncertain process of clinical development for and regulatory approval of our product candidates; difficulties in commercializing any future product candidates and achieving significant market acceptance of them; the potential for unfavorable pricing regulations, third-party reimbursement practices or related healthcare reform initiatives in the United States and in foreign jurisdictions; and the need to obtain and maintain adequate patent protection for our product candidates and avoid potential infringement of patents or other intellectual property rights of third parties.

We have not generated any revenue to date from product sales and have incurred significant operating losses since our inception in 1995 (other than during the years ended September 30, 2010, 2011 and 2012, when revenue from collaborations generated net income). As of September 30, 2012, we had an accumulated deficit of $115.4 million and we expect we may incur losses in one or more future years. We are unable to predict the extent of future losses or when we will become profitable based on product sales, if at all. Even if we or our collaborators succeed in developing and commercializing one or more of our product candidates, we may never generate sufficient revenue to sustain profitability.

Our Corporate Information

We were incorporated under the laws of the State of Delaware in 1995. Our principal executive offices are located at 500 Arsenal Street, Watertown, MA 02472 and our telephone number is (617) 607-0800. Our website address is www.enanta.com. The information contained on, or that can be accessed through, our website is not a part of this prospectus. We have included our website address in this prospectus solely as an inactive textual reference.

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, or the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As such, we are eligible to take advantage of certain exemptions from various reporting requirements applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 and reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements. We have not made a decision whether to take advantage of any or all of these exemptions. We could remain an “emerging growth company” for up to five years, or until the earliest of (a) the last day of the first fiscal year in which our annual gross revenue exceeds $1 billion, (b) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (c) the date on which we have issued more than $1 billion in nonconvertible debt during the preceding three-year period.

The Enanta name and logo are our trademarks. This prospectus also includes trademarks, trade names and service marks of other persons. All other trademarks, trade names and service marks appearing in this prospectus are the property of their respective owners.

6

Table of Contents

THE OFFERING

| Issuer |

Enanta Pharmaceuticals, Inc. |

| Common stock offered by us |

shares |

| Common stock to be outstanding after this offering |

shares |

| Over-allotment option |

The underwriters have an option for a period of 30 days to purchase up to additional shares of our common stock to cover over-allotments, if any. |

| Use of proceeds |

We estimate that the net proceeds from this offering will be approximately $ million, or approximately $ million if the underwriters exercise their over-allotment option in full, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us, assuming the shares are offered at $ per share, the midpoint of the estimated price range set forth on the cover of this prospectus. We intend to use the net proceeds from this offering for clinical development of our internal product candidates, new research and development, working capital and other general corporate purposes. |

| Risk factors |

You should read the “Risk Factors” section starting on page 10 of this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

| Proposed NASDAQ Global Market Symbol |

“ENTA” |

The number of shares of our common stock to be outstanding after this offering is based on 4,889,127 actual shares of our common stock outstanding as of September 30, 2012 and the conversion of all outstanding shares of our redeemable convertible preferred stock and our convertible preferred stock into an aggregate of 50,241,277 shares of our common stock upon the closing of this offering.

The number of shares of our common stock to be outstanding after this offering excludes:

| • | 7,635,307 shares of our common stock issuable upon the exercise of stock options outstanding as of September 30, 2012 at a weighted average exercise price of $0.48 per share; |

| • | 16,447 shares of our common stock issuable at an exercise price of $1.91 per share upon the exercise of warrants outstanding at September 30, 2012, which warrants prior to the closing of this offering are exercisable to purchase Series E redeemable convertible preferred stock; and |

| • | 613,844 additional shares of our common stock available for future issuance as of September 30, 2012 under our Amended and Restated 1995 Equity Incentive Plan. |

Unless otherwise indicated, all information in this prospectus assumes or gives effect to:

| • | the conversion of all outstanding shares of our redeemable convertible preferred stock and our convertible preferred stock into an aggregate of 50,241,277 shares of our common stock upon the closing of this offering; |

| • | no exercise of the outstanding options and warrants described above; |

| • | no exercise by the underwriters of their option to purchase up to additional shares of our common stock to cover over-allotments; |

| • | the amendment and restatement of our amended and restated certificate of incorporation and the amendment and restatement of our bylaws immediately prior to consummation of this offering; and |

| • | the -for- reverse stock split of our common stock to be effected prior to the closing of this offering. |

7

Table of Contents

SUMMARY FINANCIAL INFORMATION

You should read the following summary financial data together with our financial statements and the related notes appearing at the end of this prospectus and the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section of this prospectus.

We have derived the statement of operations data for the years ended September 30, 2010, 2011 and 2012 and the balance sheet data as of September 30, 2012 from our audited financial statements included elsewhere in this prospectus. Our historical results for any prior period are not necessarily indicative of results to be expected in any future period.

| Year Ended September 30, | ||||||||||||

| 2010 | 2011 | 2012 | ||||||||||

| (in thousands, except per share data) | ||||||||||||

| Statement of Operations Data: | ||||||||||||

| Revenue |

$ | 22,763 | $ | 41,882 | $ | 41,706 | ||||||

| Operating expenses: |

||||||||||||

| Research and development |

9,716 | 11,547 | 15,115 | |||||||||

| General and administrative |

6,105 | 5,036 | 5,302 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total operating expenses |

15,821 | 16,583 | 20,417 | |||||||||

|

|

|

|

|

|

|

|||||||

| Income from operations |

6,942 | 25,299 | 21,289 | |||||||||

| Other income (expense): |

||||||||||||

| Interest income |

14 | 83 | 118 | |||||||||

| Interest expense |

— | (3,161 | ) | — | ||||||||

| Change in fair value of warrant liability |

482 | (686 | ) | (8 | ) | |||||||

| Therapeutic tax credit |

— | 750 | — | |||||||||

| Gain on embedded derivative |

— | 670 | — | |||||||||

| Other income (expense), net |

309 | 355 | — | |||||||||

|

|

|

|

|

|

|

|||||||

| Total other income (expense), net |

805 | (1,989 | ) | 110 | ||||||||

|

|

|

|

|

|

|

|||||||

| Income before income tax |

7,747 | 23,310 | 21,399 | |||||||||

| Income tax benefit |

157 | — | — | |||||||||

|

|

|

|

|

|

|

|||||||

| Net income |

7,904 | 23,310 | 21,399 | |||||||||

| Accretion of redeemable convertible preferred stock to redemption value |

(5,452 | ) | (5,454 | ) | (5,367 | ) | ||||||

| Net income allocable to participating securities |

(2,236 | ) | (16,291 | ) | (14,663 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| Net income allocable to common stockholders |

$ | 216 | $ | 1,565 | $ | 1,369 | ||||||

|

|

|

|

|

|

|

|||||||

| Net income per share allocable to common stockholders(1): |

||||||||||||

| Basic |

$ | 0.04 | $ | 0.32 | $ | 0.29 | ||||||

| Diluted |

$ | 0.04 | $ | 0.31 | $ | 0.26 | ||||||

| Weighted average common shares outstanding(1): |

||||||||||||

| Basic |

4,873 | 4,824 | 4,693 | |||||||||

| Diluted |

6,746 | 8,005 | 10,666 | |||||||||

| Pro forma net income per share allocable to common stockholders (unaudited)(2): |

||||||||||||

| Basic |

$ | 0.39 | ||||||||||

| Diluted |

$ | 0.35 | ||||||||||

| Pro forma weighted average common shares outstanding (unaudited)(2): |

||||||||||||

| Basic |

54,934 | |||||||||||

| Diluted |

60,910 | |||||||||||

8

Table of Contents

| As of September 30, 2012 | ||||||||

| Actual | Pro Forma As Adjusted(3) |

|||||||

| (in thousands) | ||||||||

| Balance Sheet Data: |

||||||||

| Cash, cash equivalents and marketable securities |

$ | 45,418 | $ | |||||

| Working capital(4) |

41,574 | |||||||

| Total assets |

52,162 | |||||||

| Warrant liability |

2,001 | |||||||

| Redeemable convertible preferred stock |

158,955 | |||||||

| Convertible preferred stock |

327 | |||||||

| Total stockholders’ equity (deficit) |

(115,353 | ) | ||||||

| (1) | See Note 15 to our financial statements for further details on the calculation of basic and diluted net income per share allocable to common stockholders. |

| (2) | See Note 15 to our financial statements for further details on the calculation of pro forma net income per share allocable to common stockholders. |

| (3) | Gives effect to (1) the automatic conversion of all outstanding shares of our redeemable convertible preferred stock and convertible preferred stock into an aggregate of 50,241,277 shares of common stock upon the closing of this offering, (2) the automatic conversion of the warrants for Series E redeemable convertible preferred stock into warrants for 16,447 shares of common stock upon the closing of this offering, and (3) the issuance by us of shares of common stock at an initial offering price of $ per share, the midpoint of the estimated price range set forth on the cover page of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. A $1.00 increase (decrease) in the assumed initial public offering price of $ per share, the midpoint of the estimated price range set forth on the cover page of this prospectus, would increase (decrease) total stockholders’ equity and total capitalization on a pro forma as adjusted basis by approximately $ million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. The pro forma as adjusted data above is illustrative only and will be adjusted based on the actual initial public offering price and other terms of our initial public offering determined at pricing. |

| (4) | We define working capital as current assets less current liabilities. |

9

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below together with all of the other information contained in this prospectus, including our financial statements and the related notes appearing at the end of this prospectus and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” before deciding whether to invest in our common stock. If any of the following risks actually occur, our business, growth prospects, operating results and financial condition could suffer materially, the trading price of our common stock could decline and you could lose all or part of your investment. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations and stock price.

Risks Related to Our Business

Our financial prospects for the next several years are substantially dependent upon the development and marketing efforts of Abbott for combination therapies incorporating ABT-450 for the treatment of HCV. Abbott may act in its best interest rather than in our best interest, which could adversely affect our business.

We rely on Abbott to fund and conduct the clinical development and commercialization of ABT-450 and other protease inhibitors, over which Abbott has complete control. Our ability to generate significant revenue in the near term will depend primarily on the successful development, regulatory approval, marketing and commercialization by Abbott of combination therapies incorporating ABT-450. Such success is subject to significant uncertainty, and we have limited control over the resources, time and effort that Abbott may devote to ABT-450. Any of several events or factors could have a material adverse effect on our ability to generate revenue from Abbott’s potential commercialization of ABT-450 in combination therapies. For example, Abbott:

| • | may be unable to successfully complete the clinical development of ABT-450; |

| • | may have to comply with additional requests and recommendations from the FDA, including additional clinical trials; |

| • | may not make all regulatory filings and obtain all necessary approvals from the FDA and similar foreign regulatory agencies; |

| • | may not commit sufficient resources to the development, regulatory approval, marketing and distribution of ABT-450, whether for strategic reasons or otherwise due to a change in business priorities; |

| • | may cease to perform its obligations under the terms of our collaboration agreement; |

| • | may unilaterally terminate our collaboration agreement on specified prior notice without any reason and without any further commitment to continue development of any of our product candidates; |

| • | may not be able to manufacture our product candidate in compliance with requirements of the FDA and similar foreign regulatory agencies and in commercial quantities sufficient to meet market demand; |

| • | may not achieve market acceptance of combination therapies incorporating our product candidate by physicians, patients and third-party payors; |

| • | may not compete successfully with any such combination therapies against alternative products and therapies for HCV; and |

| • | may independently develop products that compete with our product candidate in the treatment of HCV. |

We will not have access to all information regarding the products being developed and potentially commercialized by Abbott, including information about clinical trial design and execution, safety reports from clinical trials, spontaneous safety reports if the product is later approved and marketed, regulatory affairs, process development, manufacturing, marketing and other areas known by Abbott. Thus, our ability to keep our stockholders informed about the status of product candidates under our collaboration will be limited by the degree to which Abbott keeps us informed. If Abbott does not perform in the manner we expect or fulfill its responsibilities in a timely manner, or at all, the clinical development, regulatory approval and commercialization

10

Table of Contents

efforts related to ABT-450 could be delayed or terminated or be commercially unsuccessful. In addition, Abbott has the right to make decisions regarding the development and commercialization of product candidates without consulting us, and may make decisions with which we do not agree. Conflicts between us and Abbott may arise if there is a dispute about the progress of the clinical development of a product candidate, the achievement and payment of a milestone amount, or the ownership of intellectual property developed during the course of our collaboration agreement. It may be necessary for us to assume responsibility at our own expense for the development of ABT-450 or other protease inhibitors. In that event, we would likely be required to limit the size and scope of one or more of our independent programs or increase our expenditures and seek additional funding which may not be available on acceptable terms or at all, and our business would be materially and adversely affected.

Our prospects for successful development of EDP-239 or any other NS5A inhibitor are dependent upon the development and marketing efforts of Novartis. Novartis may act in its best interest rather than in our best interest, which could adversely affect our business.

We rely on Novartis to fund and conduct the clinical development of EDP-239 and any other NS5A inhibitor product candidates under our collaboration, and for the successful regulatory approval, marketing and commercialization of one or more of them. Such success will be subject to significant uncertainty, and we have limited control over the resources, time and effort that Novartis may devote to our NS5A inhibitors. Moreover, Novartis may terminate the collaboration without any reason on 120 days notice to us. As with our Abbott collaboration, any of several events or factors could have a material adverse effect on our ability to generate revenue from Novartis’ development and commercialization of EDP-239, including ones similar to those described in the preceding risk factor regarding our Abbott collaboration.

If Novartis does not perform in the manner we expect or fulfill its responsibilities in a timely manner, or at all, the clinical development, regulatory approval and commercialization efforts related to EDP-239 could be delayed, terminated or be commercially unsuccessful. Conflicts between us and Novartis may arise if there is a dispute with Novartis similar to potential disputes with Abbott about any of the matters mentioned in the preceding risk factor. It may become necessary for us to assume the responsibility at our own expense for the development of EDP-239 or other NS5A inhibitors. In that event, we would likely be required to limit the size and scope of one or more of our independent programs or increase our expenditures and seek additional funding which may not be available on acceptable terms or at all, and our business would be materially and adversely affected.

We and our collaborators face substantial competition in the market for HCV drugs and for anti-infectives generally, which may result in others discovering, developing or commercializing products before us or doing so more successfully than we and our collaborators.

The pharmaceutical and biotechnology industries are intensely competitive and rapidly changing. Many large pharmaceutical and biotechnology companies, academic institutions, governmental agencies and other public and private research organizations are commercializing or pursuing the development of products that target HCV, MRSA and other infectious diseases that we may target in the future.

We expect our current and future product candidates to face intense and increasing competition as new products enter the HCV and antibacterial markets and advanced technologies become available, particularly in the case of HCV in combinations with existing products and other new products. Two drug products, Incivek™ (telaprevir) of Vertex and Victrelis™ (boceprevir) of Merck, were approved in 2011 by the FDA for the treatment of HCV in combination with interferon and ribavirin, which in combination were the previous standard of care. These and other potential new treatment regimens may render our HCV product candidates noncompetitive. In particular, our HCV product candidates may not be able to compete successfully with other products in development in multiple classes of inhibitors of HCV, including protease inhibitors, polymerase inhibitors (nucleoside and non-nucleoside), NS5A inhibitors and cyclophilin inhibitors, under development by companies such as Achillion, Astra-Zeneca, Boehringer Ingelheim, Bristol-Myers Squibb, Gilead, GlaxoSmithKline, Idenix, Johnson & Johnson, Medivir, Merck, Pfizer, Presidio, Roche and Vertex, as well as by our collaborators.

11

Table of Contents

Our MRSA program faces competition from other therapeutic products that address serious Gram-positive bacterial infections, such as Cubicin®, marketed by Cubist; vancomycin, marketed generically by Abbott, Shionogi and others; and Zyvox®, marketed by Pfizer, as well as future competition from drug candidates currently in clinical development.

Many of our competitors have substantially greater commercial infrastructure and better financial, technical and personnel resources than we have, as well as drug candidates in late-stage clinical development.

Our competitors may succeed in developing competing products and obtaining regulatory approval before we or our collaborators do with our product candidates, or they may gain acceptance for the same markets that we are targeting. If we are not “first to market” with one of our product candidates, our competitive position could be compromised because it may be more difficult for us to obtain marketing approval for that product candidate and successfully market that product candidate as a second competitor. In addition, any new product that competes with an approved product must demonstrate compelling advantages in efficacy, convenience, tolerability and safety in order to overcome price competition and to be commercially successful.

Competitive products in the form of other treatment methods or a vaccine for HCV or MRSA may render our product candidates licensed to others, as well as any future product candidates we may develop ourselves, obsolete or noncompetitive. Even if successfully developed and subsequently approved by the FDA, our product candidates will face competition based on their safety and effectiveness, the timing and scope of the regulatory approvals, the availability and cost of supply, marketing and sales capabilities, reimbursement coverage, price, patent position and other factors. If the product candidates developed under our collaboration agreements with Abbott and Novartis face competition from generic products, the collaboration agreements provide that the royalty rate applicable to such product candidates is reduced significantly by a specified percentage on a product-by-product, country-by-country basis. If we and our collaborators are not able to compete effectively against our current and future competitors, our business will not grow and our financial condition, operations and stock price will suffer.

We have no approved products and no clinical development experience, which makes it difficult to assess our ability to develop and commercialize our future product candidates.

To date, Abbott has been and will continue to be responsible for all of the clinical development of our ABT-450 and other protease inhibitor product candidates, and Novartis is responsible for all future clinical development of our EDP-239 and other NS5A product candidates. We have not yet demonstrated an ability to successfully overcome many of the risks and uncertainties associated with late stage clinical development, regulatory approval and commercialization of therapeutic products such as the ones we plan to develop independently. For example, to execute our business plan for development of our independent programs for cyclophilin inhibitors and nucleotide polymerase inhibitors for HCV and antibiotics for MRSA, we will need to successfully:

| • | execute clinical development of our future product candidates; |

| • | obtain required regulatory approvals for the development and commercialization of our future product candidates; |

| • | develop and maintain any future collaborations we may enter into for any of these programs; |

| • | build and maintain robust sales, distribution and marketing capabilities, either independently or in collaboration with future collaborators; |

| • | gain market acceptance for our future product candidates; and |

| • | manage our spending as costs and expenses increase due to clinical trials, regulatory approvals and commercialization. |

If we are unsuccessful in accomplishing these objectives, we may not be able to successfully develop and commercialize our future product candidates and expand our business or continue our operations.

12

Table of Contents

We may require substantial additional financing to achieve our goals if the development and commercialization of ABT-450 or EDP-239 is delayed or terminated. A failure to obtain this necessary capital when needed could force us to delay, limit, reduce or terminate our product development efforts.

Since our inception, most of our resources have been dedicated to the discovery and preclinical development of our product candidates. In particular, we have expended, and believe that we will continue to expend for the foreseeable future, substantial resources discovering and developing our proprietary preclinical product candidates. These expenditures will include costs associated with research and development, preclinical manufacturing of product candidates, conducting preclinical experiments and clinical trials and obtaining regulatory approvals, as well as commercializing any products later approved for sale. In our fiscal year ending September 30, 2013, we expect to incur up to $15 million of costs associated with research and development, which amount is exclusive of costs incurred by our collaborators in developing our licensed product candidates ABT-450 and EDP-239.

Because the outcome of planned and anticipated clinical trials of our product candidates by our collaborators is highly uncertain, we cannot reasonably estimate the timing or amounts, if any, of future milestone payments we will receive from these collaborators. If we do not continue to receive substantial milestone payments from the continued development of our product candidates, we may require substantial additional financing.

Our future capital requirements depend on many factors, including:

| • | whether our existing collaborations continue to generate substantial milestone payments, and ultimately royalties, to us; |

| • | the number and characteristics of the future product candidates we pursue; |

| • | the scope, progress, results and costs of researching and developing any of our future product candidates on our own, and conducting preclinical research and clinical trials; |

| • | the timing of, and the costs involved in, obtaining regulatory approvals for any future product candidates we develop independently; |

| • | the cost of commercialization activities, if any, of any future product candidates we develop independently that are approved for sale, including marketing, sales and distribution costs; |

| • | the cost of manufacturing our future product candidates and any products we successfully commercialize independently; |

| • | our ability to maintain existing collaborations and to establish new collaborations, licensing or other arrangements and the financial terms of such agreements; |

| • | the costs involved in preparing, filing, prosecuting, maintaining, defending and enforcing patents, including litigation costs and the outcome of such litigation; and |

| • | the timing, receipt and amount of sales of, or royalties on, ABT-450, EDP-239 and our future product candidates, if any. |

Additional funds may not be available when we need them, on terms that are acceptable to us, or at all. Our ability to raise funds will depend on financial, economic and market conditions and other factors, many of which are beyond our control. If adequate funds are not available to us on a timely basis, we may be required to delay, limit, reduce or terminate preclinical studies, clinical trials or other research and development activities for one or more of our product candidates.

If we are not successful in discovering further product candidates in addition to ABT-450 and EDP-239, our ability to expand our business and achieve our strategic objectives may be impaired.

Research programs designed to identify product candidates require substantial technical, financial and human resources, whether or not any product candidates are ultimately identified. Our research programs may initially show promise in identifying additional potential product candidates, yet fail to yield product candidates for clinical development or commercialization for many reasons, including the following:

| • | the research methodology used may not be successful in identifying additional potential product candidates; |

13

Table of Contents

| • | competitors may develop alternatives that render our future product candidates obsolete; |

| • | a future product candidate may, on further study, be shown to have harmful side effects or other characteristics that indicate it is unlikely to be effective or otherwise does not meet applicable regulatory criteria; and |

| • | a future product candidate may not be capable of being produced in commercial quantities at an acceptable cost, or at all. |

If we are unable to identify additional compounds suitable for preclinical and clinical development, we may not be able to obtain sufficient product revenue in future periods, which likely would result in significant harm to our financial position and adversely impact our stock price.

If we fail to attract and keep senior management and key scientific personnel, we may be unable to successfully develop our product candidates, conduct our clinical trials and commercialize our product candidates.

Our success depends in part on our continued ability to attract, retain and motivate highly qualified management, clinical and scientific personnel. We are highly dependent upon our senior management, particularly Jay R. Luly, Ph.D., our Chief Executive Officer and President, and Yat Sun Or, Ph.D., our Senior Vice President, Research and Development and Chief Scientific Officer, as well as other employees and consultants. Although none of these individuals has informed us to date that he intends to retire or resign in the near future, the loss of services of any of these individuals or one or more of our other members of senior management could delay or prevent the successful development of our future product candidates.

Although we have not historically experienced unique difficulties attracting and retaining qualified employees, we could experience such problems in the future. For example, competition for qualified personnel in the biotechnology and pharmaceutical field is intense. In addition, we will need to hire additional personnel as we expand our clinical development and commercial activities. We may not be able to attract and retain quality personnel on acceptable terms.

We have incurred a substantial cumulative net loss since our inception and anticipate that we may incur substantial operating losses in one or more years in the future. To date, our principal sources of revenue have been our collaboration agreements, including our current agreements with Abbott and Novartis, and future payments under these agreements are uncertain. We have had no products approved for commercial sale. As a result, our ability to achieve sustained profitability is unproven.

We have incurred cumulative net losses since our inception, and as of September 30, 2012, we had an accumulated deficit of $115.4 million. Our net income in the fiscal year ended September 30, 2010 resulted primarily from the conclusion of a previous collaboration which accelerated $16.2 million of deferred revenue into fiscal 2010 that was related to cash received and spent in prior years, and our net income in the fiscal year ended September 30, 2011 resulted primarily from a substantial milestone payment from Abbott. In the fiscal year ended September 30, 2012, our net income resulted primarily from a substantial upfront license payment from Novartis. We are entitled to receive an $11.0 million milestone payment based on Novartis’ November 2012 initiation of dosing in a Phase 1 clinical trial that includes EDP-239. There is no assurance, however, that we will recognize any additional collaboration revenue during fiscal 2013 or report net income in fiscal 2013 or subsequent years. To date, we have not commercialized any products or generated any revenue from product sales, directly or through any collaborator.

Our principal source of revenue has been our collaboration agreements, including our current agreements with Abbott and Novartis. Future milestone payments are uncertain because our collaborators may choose not to continue research or development activities for one or more potential product candidates. For example, under a prior collaboration for the development of an antibiotic product candidate in Japan, our collaborator decided in 2010 not to pursue further development of the licensed product candidate due to its limited potency against Haemophilus influenzae in clinical trials of community-acquired pneumonia, which then resulted in our collaboration being terminated. In addition, we may not achieve the specified milestones, our product candidates may not be approved by the FDA or other regulatory authorities or, if they are approved, may not be accepted in the market. If we are unable to develop and commercialize one or more of our product candidates, either alone or with our collaborators, or if any such product candidate does not achieve market acceptance, we may never

14

Table of Contents

generate sufficient product royalties or product sales. Even if we do generate product royalties or product sales, we may never achieve or sustain profitability on a quarterly or annual basis. Our failure to sustain profitability would depress the market price of our common stock and could impair our ability to raise capital, expand our business, diversify our product offerings or continue our operations. A decline in the market price of our common stock also could cause you to lose all or a part of your investment.

We may encounter difficulties in managing our growth and expanding our operations successfully.

As we seek to advance our product candidates through clinical trials, we will need to expand our development, regulatory, manufacturing, marketing and sales capabilities or contract with third parties to provide these capabilities for us. As our operations expand, we expect that we will need to manage additional relationships with various strategic partners, suppliers and other third parties. Future growth will impose significant added responsibilities on members of management. Our future financial performance and our ability to commercialize our product candidates and to compete effectively will depend, in part, on our ability to manage any future growth effectively. To that end, we must be able to manage our development efforts and clinical trials effectively and hire, train and integrate additional management, administrative and sales and marketing personnel. We may not be able to accomplish these tasks, and our failure to accomplish any of them could prevent us from successfully growing our company.

Our government funded contract for our antibiotic program is subject to termination and uncertain future funding and there is no certainty that we will be able to enter into new agreements to provide these funds.

Under our agreement with the National Institute of Allergy and Infectious Diseases, or NIAID, a division of the National Institutes of Health, an agency of the United States Department of Health and Human Services, to support our antibiotic program, NIAID has the option to make future payments to fund our early clinical development of EDP-788. If NIAID exercises each option under the agreement, the aggregate funding commitment will be $42.7 million, of which only $14.3 million has been committed for the first 30 months of our work under the agreement. After the first 30 months, NIAID has several options to decide whether it wants to continue the program in its sole discretion. In addition, the ability of government agencies such as NIAID to perform under these types of agreements is dependent upon adequate continued funding of the agencies and their programs. We have no control over the resources and funding NIAID may devote to our agreement, which may be subject to periodic renewal and which generally may be terminated by NIAID at any time. Any significant reductions in the funding of U.S. government agencies or in the funding areas targeted by our business could materially and adversely affect our antibiotic program and our results of operations and financial condition. If we fail to satisfy our contractual obligations under the agreement, the applicable Federal Acquisition Regulations allow the government to terminate the agreement in whole or in part, and we may be required to perform corrective actions, including but not limited to delivering to the government any incomplete work. If NIAID does not exercise future funding options under the agreement, terminates the agreement or fails to perform its responsibilities under the agreement, it could materially impact our antibiotic program and our financial results.

In addition, our contract related costs and fees, including allocated indirect costs, are subject to audits and adjustments by negotiation between us and the U.S. government. As part of the audit process, the government audit agency verifies that all charges made by a contractor against a contract are legitimate and appropriate. Audits may result in recalculation of contract revenues and non-reimbursement of some contract costs and fees. Any audits of our contract related costs and fees could result in material adjustments to our revenue. In addition, U.S. government contracts are conditioned upon the continuing availability of Congressional appropriations. Congress usually appropriates funds on a fiscal year basis even though contract performance may take several years. Consequently, at the outset of a major program, the contract is usually incrementally funded and additional funds are normally committed to the contract by the procuring agency as appropriations are made by Congress for future fiscal years. Any failure of NIAID to continue to fund our contract could have a material adverse effect on our business, results of operations and financial condition.

15

Table of Contents

Risks Related to Development, Clinical Testing and Regulatory Approval of Our Product Candidates

Clinical drug development involves a lengthy and expensive process with uncertain timelines and uncertain outcomes. If clinical trials are prolonged or delayed, we or our collaborators may be unable to commercialize our product candidates on a timely basis.

Clinical testing is expensive and, depending on the stage of development, can take a substantial time period to complete. Its outcome is inherently uncertain, and failure can occur at any time during clinical development. Phase 3 trials of ABT-450 in combination therapy started in October 2012 and none of the other product candidates in our pipeline has yet advanced beyond Phase 2 clinical trials. The recently started ABT-450 Phase 3 trials or any future Phase 3 trials may fail to demonstrate sufficient safety and efficacy. Moreover, regulatory and administrative delays may adversely affect our or our collaborators’ clinical development plans and jeopardize our or our collaborators’ ability to attain product approval, commence product sales and generate revenues.

Clinical trials can be delayed for a variety of reasons, including delays related to:

| • | reaching agreement on acceptable terms with prospective contract research organizations, or CROs, and clinical trial sites, the terms of which can be subject to extensive negotiation and may vary significantly among different CROs and trial sites; |

| • | failure of third-party contractors, such as CROs, or investigators to comply with regulatory requirements; |

| • | delay or failure in obtaining the necessary approvals from regulators or institutional review boards, or IRBs, in order to commence a clinical trial at a prospective trial site, or their suspension or termination of a clinical trial once commenced; |

| • | difficulty in recruiting suitable patients to participate in a trial; |

| • | difficulty in having patients complete a trial or return for post-treatment follow-up; |

| • | clinical sites deviating from trial protocol or dropping out of a trial; |

| • | problems with drug product or drug substance storage and distribution; |

| • | adding new clinical trial sites; |

| • | our inability to manufacture, or obtain from third parties, adequate supply of drug product sufficient to complete our preclinical studies and clinical trials; |

| • | governmental or regulatory delays and changes in regulatory requirements, policy and guidelines; or |

| • | varying interpretations of data by the FDA and similar foreign regulatory agencies. |

The results of any Phase 3 clinical trial may not be adequate to support marketing approval. These clinical trials are lengthy and usually involve from many hundreds to thousands of patients. In addition, if the FDA disagrees with our or our collaborator’s choice of the key testing criteria, or primary endpoint, or the results for the primary endpoint are not robust or significant relative to the control group of patients not receiving the experimental therapy or are subject to confounding factors, or are not adequately supported by other study endpoints, the FDA may refuse to approve our or our collaborator’s product candidate. The FDA also may require additional clinical trials as a condition for approving any of these product candidates. We estimate that it will likely be more than two years before an NDA for one of our or our collaborator’s product candidates could be approved by the FDA.

We could also encounter delays if a clinical trial is suspended or terminated by us, by the IRBs of the institutions in which such trial is being conducted, by any Data Safety Monitoring Board, or DSMB, for such trial, or by the FDA or other regulatory authorities. Such authorities may impose such a suspension or termination due to a number of factors, including failure to conduct the clinical trial in accordance with regulatory requirements or our clinical protocols, inspection of the clinical trial operations or trial site by the FDA or other regulatory authorities resulting in the imposition of a clinical hold, unforeseen safety issues or adverse side effects, failure to demonstrate a benefit from using a drug, changes in governmental regulations or administrative actions or lack of adequate funding to continue the clinical trial. In addition, delays can occur due

16

Table of Contents

to safety concerns arising from trials or other clinical data regarding another company’s product candidate in the same compound class as one of ours. For example, Novartis’ drug candidate that is a cyclophilin inhibitor was recently placed on clinical hold by the FDA based on a small number of cases of pancreatitis in clinical trial patients, one of which resulted in a patient’s death. This clinical hold could result in delays for development of other cyclophilin inhibitors such as our EDP-546, including delays due to additional preclinical or clinical testing protocols for all cyclophilin inhibitors. If we or our collaborators experience delays in the completion of, or termination of, any clinical trial of one of our product candidates, the commercial prospects of the product candidate will be harmed, and our or our collaborators’ ability to commence product sales and generate product revenues from the product candidate will be delayed. In addition, any delays in completing our clinical trials will increase our costs and slow down our product candidate development and approval process. Any of these occurrences may harm our business, financial condition and prospects significantly. In addition, many of the factors that cause, or lead to, a delay in the commencement or completion of clinical trials may also ultimately lead to the denial of regulatory approval of our product candidates.

If we or our collaborators are required to suspend or discontinue clinical trials due to side effects or other safety risks associated with our product candidates, or if we or our collaborators are required to conduct studies on the long-term effects associated with the use of our product candidates, efforts to commercialize our product candidates could be delayed or halted.