Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - AutoWeb, Inc. | abtlex99_1.htm |

| 8-K - AUTOBYTEL FORM 8-K - AutoWeb, Inc. | abtlform8_k.htm |

Exhibit 99.2

Autobytel

Moderator: Jeffrey Coats

November 8, 2012

5:00 p.m. ET

| Operator: | Good day, ladies and gentlemen and welcome to your Autobytel 2012 3rd quarter financial results conference call. At this time, all participants will be on a listen only mode, but later we will conduct a question and answer session, and instructions will be given at that time. If anyone should require audio assistance, you can press star then zero and an audio operator will assist you. And as a reminder, today's conference is being recorded. And now, I'd like to introduce your host for today, Roger Pondel. Roger, please go ahead. |

| Roger Pondel: | Thank you, John, and good afternoon, everyone. Welcome to Autobytel's 2012 third quarter conference call. Today, I am joined by Jeffrey Coats, President and Chief Executive Officer, and Curt DeWalt, Senior Vice President and Chief Financial Officer. |

Before we begin, I must remind you that during today's call, including the question and answer session, any projections and forward-looking statements made regarding future events for Autobytel's future financial performance are covered by the Safe Harbor statements contained in today's press release, in the slides accompanying this presentation and in the company's public filings with the SEC. Actual events and results may differ materially from those forward-looking statements. Specifically, please refer to the company's Form 10-K for the year ended December 31, 2011 and Form 10-Q for the quarter ended September 30, 2012, which was filed prior to this call, as well as other filings made by Autobytel with the SEC. These filings identify factors that could cause results to differ materially from those forward-looking statements.

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 2

Slides are included with today's presentation to help illustrate some of the points being made and discussed during the call. You can access the slides by clicking on the link in today's press release or by visiting Autobytel's website at www.autobytel.com. When there, go to "Investor Relations" and click on "Events & Presentations."

Also, please note that during this call we will be discussing EBITDA, cash flow, cash net income and cash net income per diluted share, which are non-GAAP financial measures as defined by SEC Regulation G. Reconciliations of these non-GAAP financial measures to the most directly comparable GAAP measures are included in the slides being used on this call and that are posted on Autobytel's website.

With that, I will turn the call over to Jeff.

| Jeff Coats: | Thank you, Roger. Good afternoon, everyone. |

I'm pleased to again report significant improvement in our business, including our sixth consecutive quarter of profitability, our seventh consecutive quarter of positive cash flow and our highest quarterly revenue since the second quarter of 2008.

During the third quarter, customer demand for purchase requests, also known as leads, which is our core product offering, remained strong. On the supply side, consumer traffic and lead volume strengthened. While the fourth quarter will likely be impacted by normal seasonal trends, October was good compared with the same month last year. In addition, we expect to show revenue gains in the 3% to 5% range for the full year, 2012.

I will come back to update you on some of our key initiatives after Curt provides the financial review. Curt?

| Curt DeWalt: | Thank you, Jeff. |

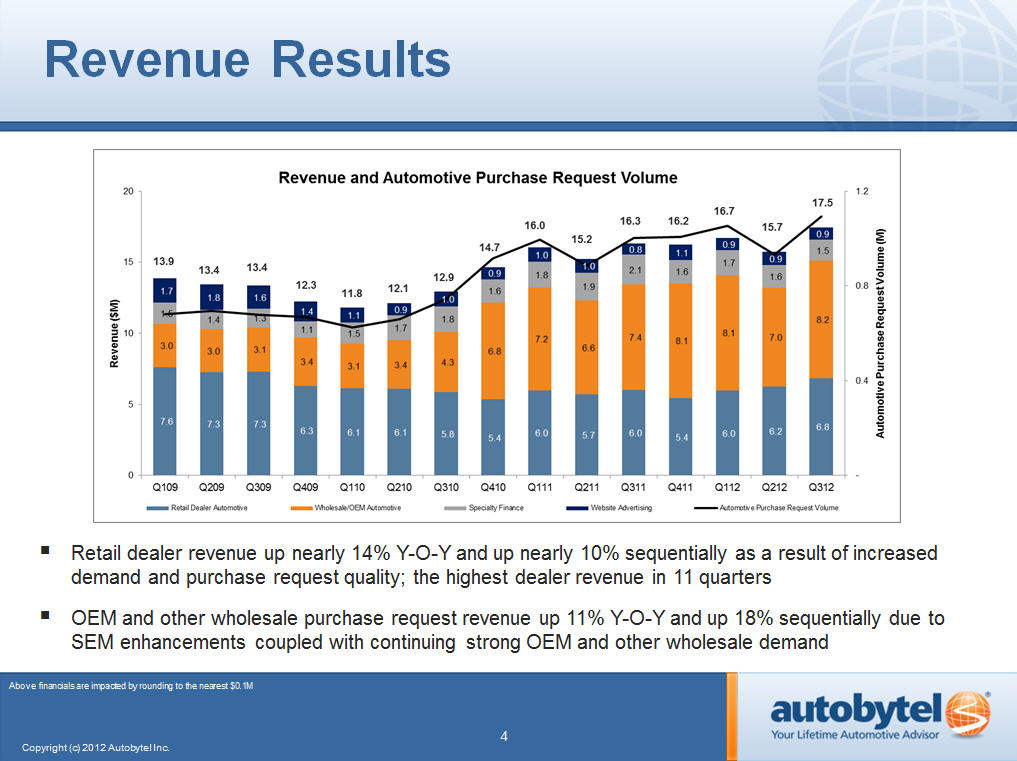

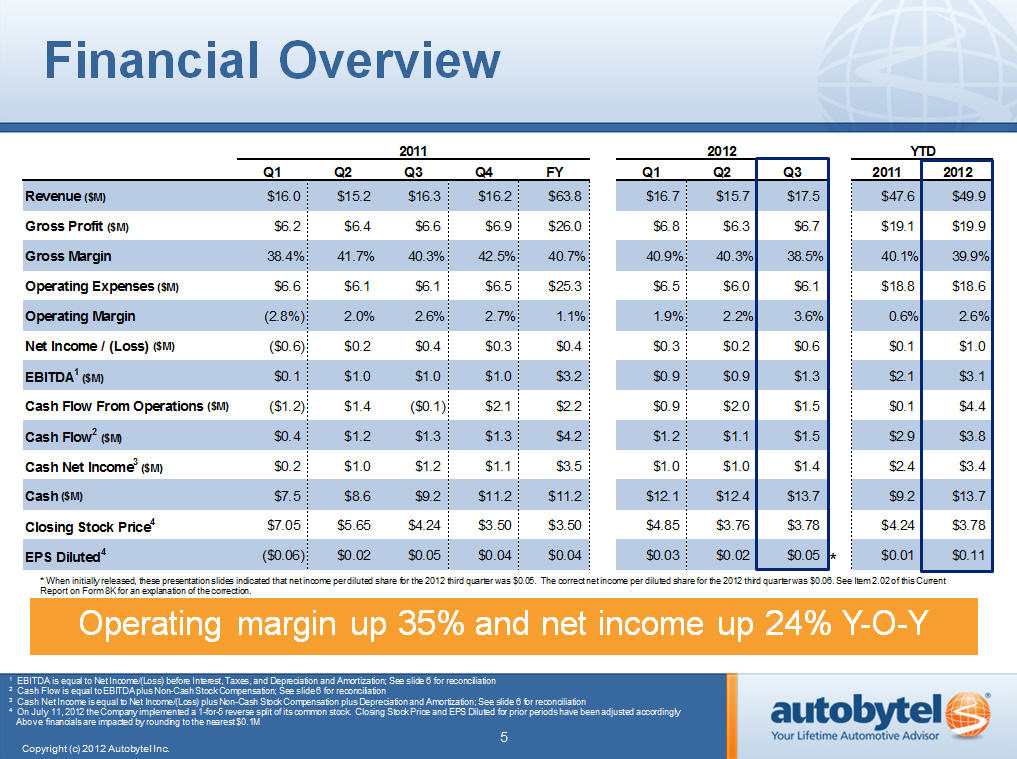

As you can see on Slide 4, total revenues for 2012 third quarter increased 7% to $17.5 million from $16.3 million for the prior-year quarter, primarily reflecting increases in both retail and wholesale automotive purchase requests. 11% sequential growth was driven by purchase request volume increases. As a reminder, the first and third quarters are generally our strongest from a seasonal perspective. As Jeff mentioned, although we anticipate the usual seasonal sequential pattern, we do expect to see year-over-year revenue improvement for the coming fourth quarter.

2

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 3

Also on Slide 4, you'll see quarterly revenues by source for the third quarter of 2012. Total automotive purchase request revenue rose 12% to $15.1 million, up from $13.5 million for last year's third quarter, reflecting 11% year-over-year growth in revenue generated from wholesale customers, and 14% growth from retail customers. On a sequential basis, automotive purchase request revenue improved 14%.

Finance request revenue, which accounts for less than 10% of our total revenue, declined 29% year-over-year and 7% sequentially, as a result of continuing softness in lead supply. Substantially all of our finance-related leads are aggregated from outside third-party providers, and given tight supply in the marketplace, these leads have become more expensive to acquire and to generate internally. On a positive note, there's been significant increase in dealer demand from customers looking for specialty financing. Due to the increase in demand, the scarcity of high quality supply, as well as a more favorable lending climate, dealers are willing to pay more to obtain high quality finance leads. We've increased efforts to generate more of these leads internally, and believe we'll be able to improve this business over time.

Advertising revenue increased approximately 13% year-over–year, boosted by our mobile revenue.

We delivered approximately 1.1 million automotive purchase requests for the 2012 third quarter, up approximately 1 million from the prior-year period. 69% of those [were] delivered in the wholesale channel and the remaining 31% in the retail channel. We delivered approximately 83,000 finance requests in the third quarter of 2012, versus 121,000 one year ago.

On Slide 5, you can see gross profit improved to $6.7 million for the 2012 third quarter, up slightly from $6.6 million for the third quarter of 2011. Gross margin total 38.5% versus 40.3% in last year's third quarter, while year-to-date gross margin totaled 39.9% and 40.1%, respectively.

3

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 4

The decline in gross margin during the quarter was a result of investments in generating additional lead volume and further investment in our online content, both of which are designed to drive increased growth. However, we did not sacrifice incremental net income growth, as you can see from our profit generation this quarter, which also yielded a 140 basis point increase in operating margin on a sequential basis, and a 100 basis point increase year-over-year.

Total operating expenses for both 2012 and 2011 third quarters was $6.1 million. Total operating expenses as a percent of revenues declined to 34.9% from 37.7% for the 2011 third quarter. For 2012 third quarter, operating expenses included a $68,000, or $0.01 per diluted share, one-time impairment charge related to a long-lived asset.

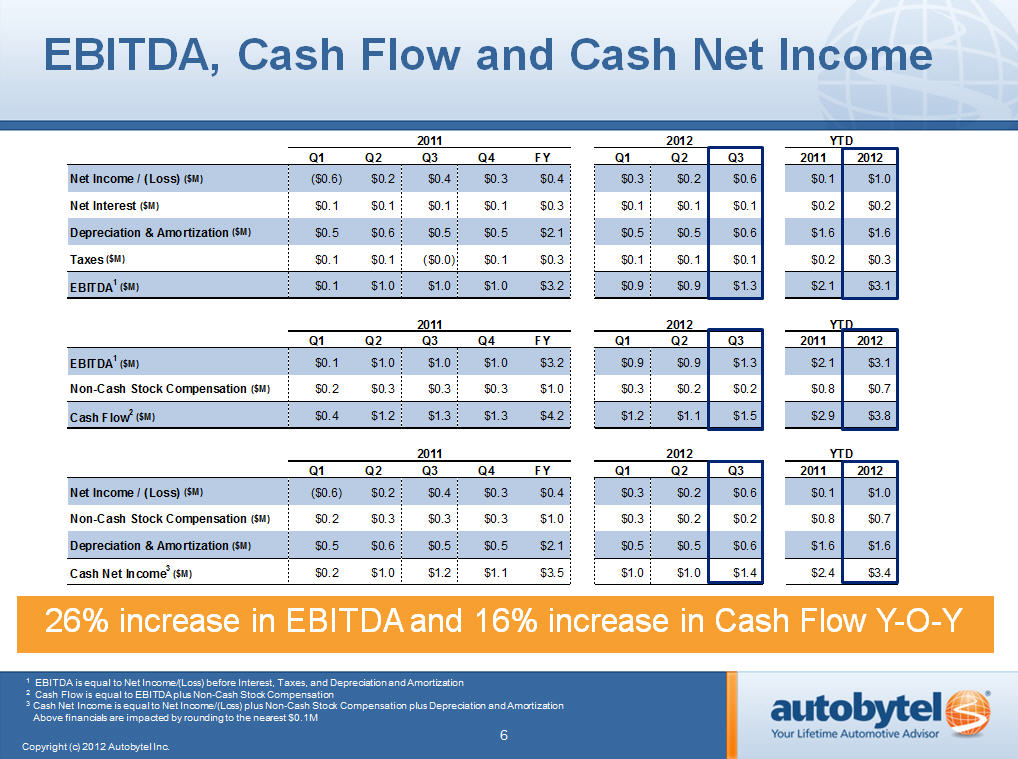

As you'll see on Slide 6, non-cash stock based compensation for the 2012 third quarter was $209,000, compared with $268,000 for the 2011 third quarter.

Amortization and depreciation totaled $607,000 for the most recent third quarter, versus $524,000 for the prior-year third quarter.

This brings EBITDA to $1.3 million for the third quarter of 2012, compared with $1.0 million for last year's third quarter.

We generated net income of $551,000, or $0.05* per diluted share, for the 2012 third quarter, based on 10.1 million diluted average weighted shares outstanding. Excluding the one-time impairment charge, net income per diluted share would have been $0.06*. This compares with last year's third quarter net income of $446,000, or $0.05 per diluted share, based on 9.5 million average weighted shares outstanding. As a reminder, all EPS and share counts reflect the 1-for-5 reverse stock split which became effective July 11th.

Cash provided by operations grew substantially to $1.5 million for the most recent third quarter, compared with cash used in operations of $93,000 for the third quarter of 2011. For the year-to-date period, cash provided by operations totaled $4.4 million, compared with $120,000 for the same period in 2011.

*When initially presented, the speaker indicated that net income per diluted share for the 2012 third quarter was $0.05 and that, excluding the one-time impairment charge, net income per diluted share for the 2012 third quarter was $0.06. The correct net income per diluted share for the 2012 third quarter was $0.06, and excluding the one-time impairment charge, was $0.07. See Item 2.02 of this Current Report on Form 8K for an explanation of the correction.

4

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 5

Also as seen on Slide 6, cash net income, which we derive by adding back depreciation, amortization and stock based compensation to net income, totaled $1.4 million, or $0.14 per diluted share for the third quarter of 2012, versus $1.2 million, or $0.13 per diluted share for the same period last year. On a year-to-date basis, we achieved cash net income of $3.4 million, or $0.36 per diluted share for 2012, compared with $2.4 million, or $0.25 per diluted share for 2011.

At the end of September, our cash and cash equivalents balance had grown to $13.7 million, up from $11.2 million at the end of 2011, and $9.2 million one year ago.

Year–to-date results can be found in the press release we issued earlier this afternoon.

With that, I'll turn the call back to Jeff.

| Jeff Coats: | Thank you, Curt. |

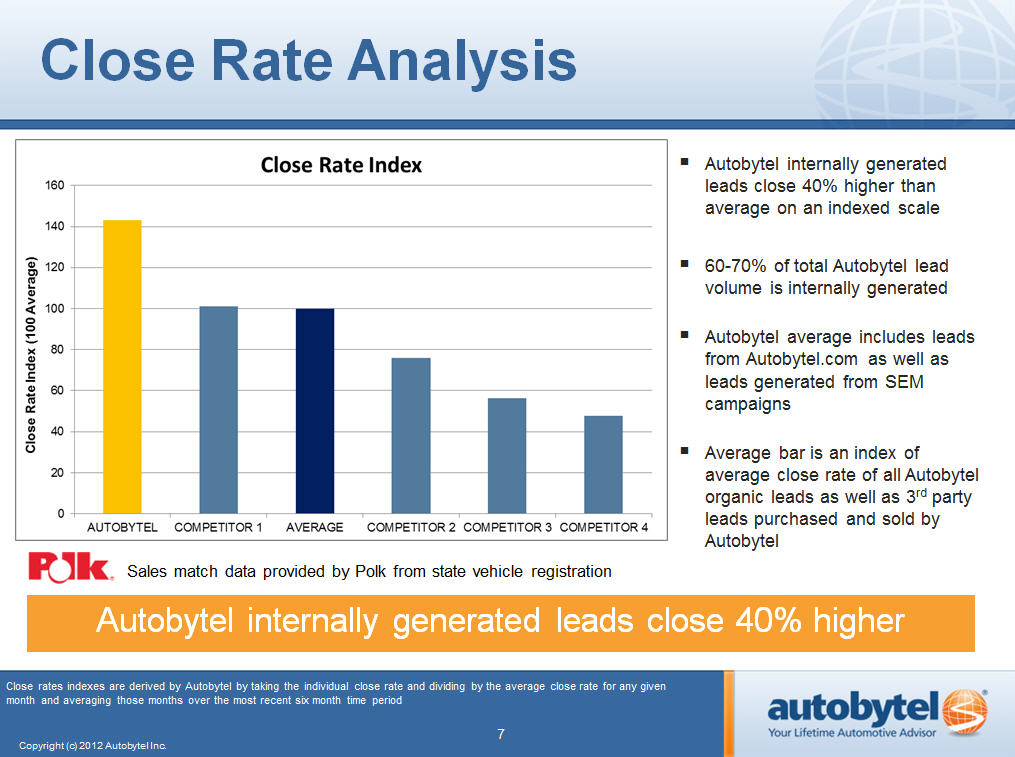

I'd like to spend some time today discussing our recent purchase request quality initiatives with R.L. Polk. As you know, we have been a strong advocate of the importance of quality, or sales conversion rates, for quite some time. High conversion rates are a key reason Autobytel's purchase requests are so valuable to dealers and OEMs, which we of course believe is a competitive advantage for us. Our focus on quality is the reason we've been able to steadily increase purchase request volume and gain market share.

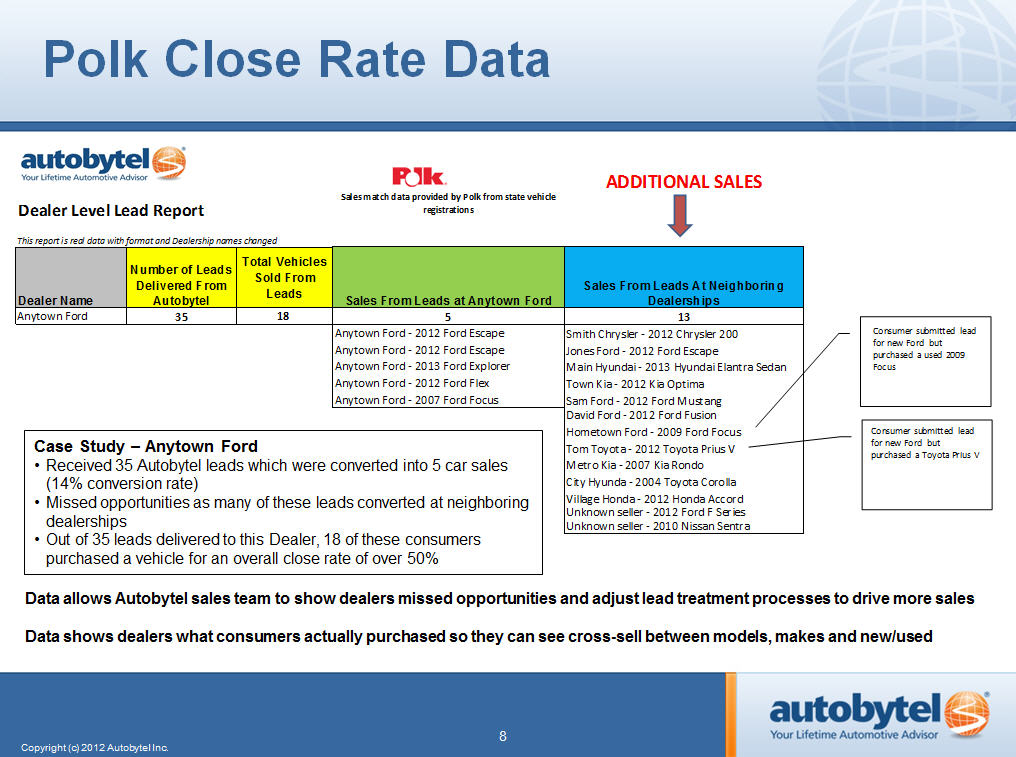

Until our collaboration with R.L. Polk, there was very little transparency into purchase request quality throughout the industry. Now, by cross referencing Polk's state vehicle registration data with the automotive purchase requests we deliver to our clients, we are able to establish reliable data on an ongoing basis regarding consumer crossover between makes, and purchase request conversion at the dealer level. In addition to providing this valuable information regularly to our dealer and OEM partners so that they can accurately measure the return on their investments with us, we use the data internally to better manage and focus our own internal lead generation and lead acquisition activities, including supplier lead quality.

5

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 6

On Slide 7, you can see that Autobytel purchase requests, which make up the majority of our purchase request volume, closed at an indexed rate 40% higher than average. The Autobytel close rate includes all Autobytel internally-generated leads. The average is an index of the average close rate we see from all leads including Autobytel leads as well as third party leads that we purchase. This data once again shows the high quality of Autobytel leads compared to other available sources.

On a monthly basis, dealers and OEMs now have access to a more comprehensive view of consumers' purchase timeframes, as well as new-to-used vehicle shopping patterns. As you can see on Slide 8, among other data, we now provide information that shows a dealer where consumers actually bought their vehicles, be it at our customer's dealership, a same-make dealership or a competitive-make dealership. This actionable information allows them to adapt their marketing efforts based on actual consumer behavior. We can also show auto manufacturers how purchase requests for their brands performed compared to segment and industry averages. In effect, we are placing information in the hands of the people who have the opportunity to implement more strategic marketing approaches for targeting in-market automotive consumers.

In addition to the quantitative evidence of the value we are providing to customers, we are getting great marketplace feedback, and we are generating positive buzz. Our retail and wholesale sales groups report significant inbound interest from dealers across the country, as well as several OEMs, just since we published our first case study on purchase request quality in mid-October. Our folks also reported that our Polk collaboration was a hot topic at the recent Digital Dealer and Driving Sales conferences held two weeks ago.

We are continually learning from our relationship with Polk and will use this new intelligence to further improve purchase request quality and customer relationships. As an integral part of our business going forward, we are working to extend and expand the available data for the benefit of our dealer and OEM customers. And, we are only in the very beginning stages of using this data to create additional opportunities for our company. We believe this will translate into increased automotive purchase request volume and profitability for Autobytel.

6

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 7

Our quality efforts have already begun to pay off. We are very excited about the recent growth we've seen in dealer-facing revenue. Back on Slide 4 you can see that dealer revenue grew 14% year-over-year as a result of increased demand and lead quality. This quarter represented the highest level of dealer revenue in 11 quarters, and we are currently investing in additional sales and customer support personnel to allow us to take full advantage of the dealer opportunity.

An essential part of our focus on improving sales conversion rates for our customers is the ongoing enhancement of autobytel.com. Over the last year, we have made substantial site improvements, as you can see on Slide 9. In addition to our expanded Dealer Directory, which includes a comprehensive listing of all U.S. franchise dealers, and the MyGarage ownership feature, which provides a single place for automotive ownership information, our new mobile site is performing very nicely.

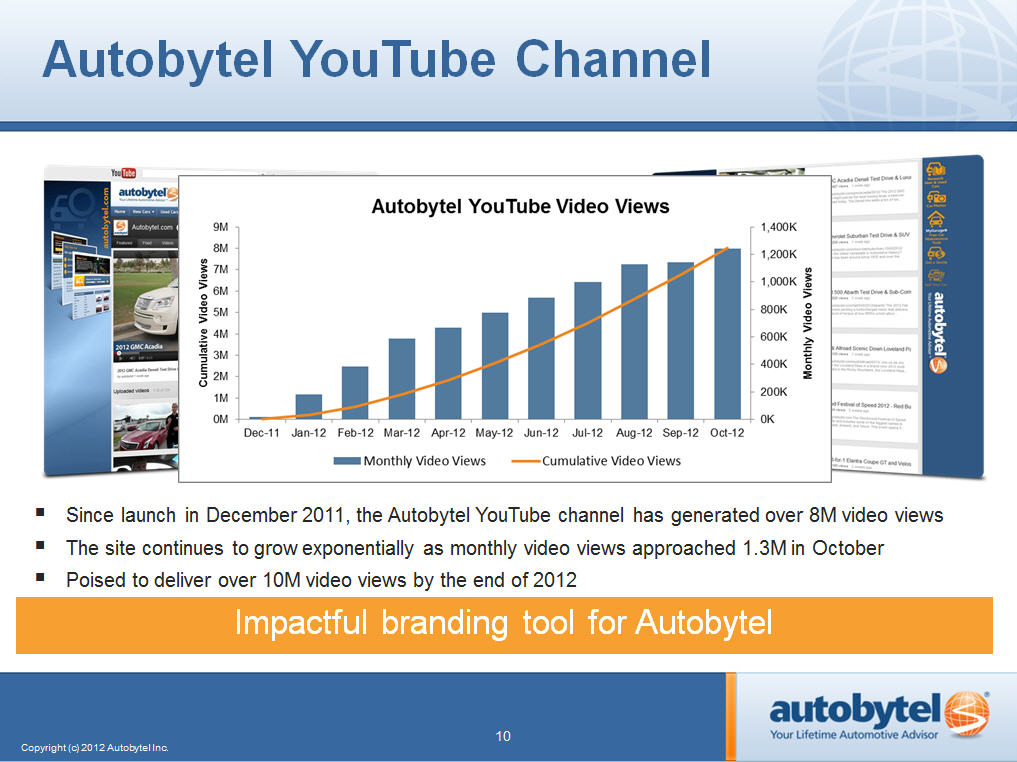

We are improving our visibility and usefulness to consumers from several angles. As you can see on Slide 10, Autobytel's YouTube video channel continues its rapid growth and is further enhancing our brand recognition. At just over 4.5 million views since last time we spoke in August, our channel now has more than 8 million views. That's nearly three times greater than one of our key competitors and twice that of another. From new car reviews to highlights of the Space Shuttle Endeavor being moved through southern California by a Toyota Tundra, we continue to provide consumers with information that is both fun and easy to interact with.

Before we turn it over to your questions, I'd like to discuss ad revenue, which remains a good long-term opportunity for us. As you know, during the previous upfront cycle, we were focused on meeting customer delivery expectations within our existing share of individual OEM budgets. Because of the enhanced consumer experience being provided by Autobytel, and the launch of the mobile version of autobytel.com, thus far during 2012, we are over-delivering on those commitments. This over-delivery has set us up nicely for the 2013 upfronts, through which advertising is currently being negotiated for the coming year. It's still very early, as manufacturers continue their budget planning, but we've gotten early indication that dollar commitments for Autobytel should be meaningfully higher for 2013, given our improvement in page views and performance.

7

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 8

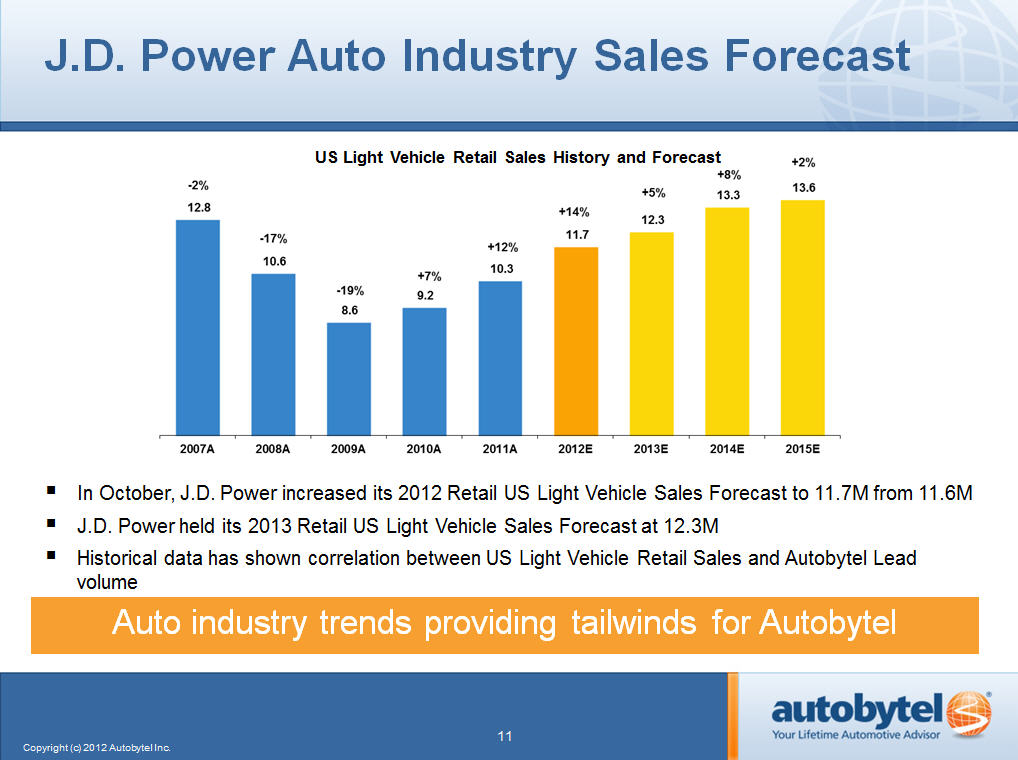

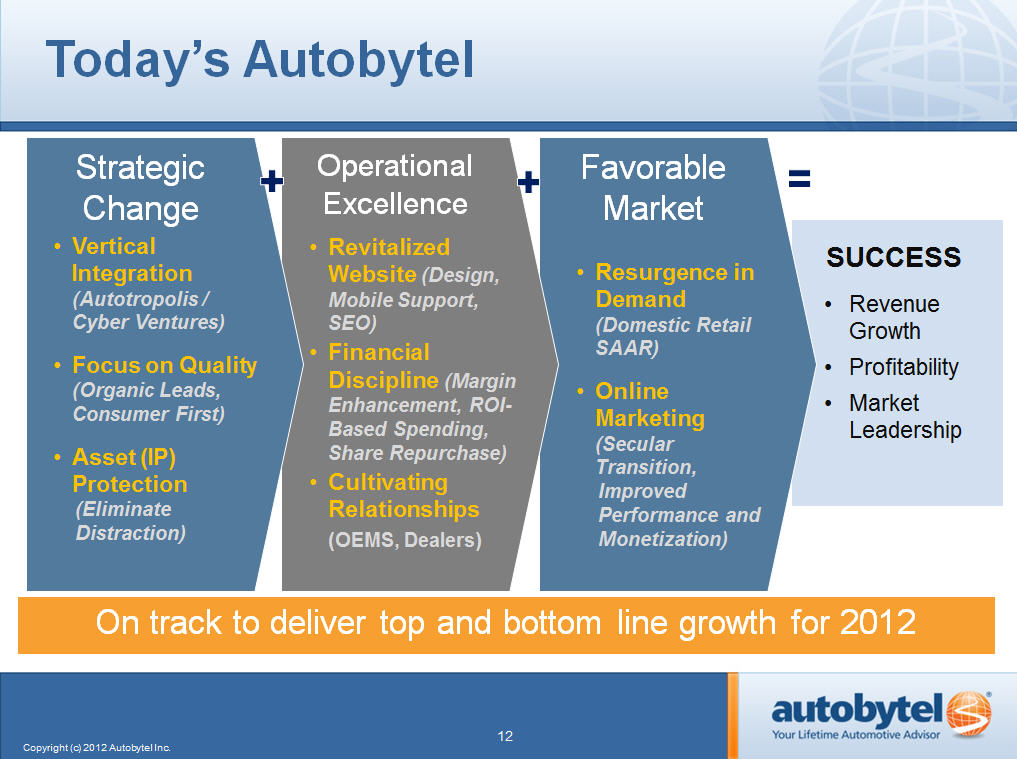

As summarized on Slides 12 and 13, through a combination of strategic changes and focused execution, we have successfully repositioned Autobytel to once again be a leader in our core business. With the automotive market trends continuing on a favorable path, as you can see back on Slide 11, and an ongoing shift toward digital activities, we are making strategic investments to capitalize on these opportunities and are establishing a platform that we believe will contribute to consistent growth for many years to come.

We provided guidance this year that we are now comfortable we will exceed. Accordingly, we are raising our guidance today to reflect that outperformance. We currently anticipate that net income will triple for 2012 from last year, and, as I stated earlier, we also expect year-over-year revenue growth in the range of 3% to 5% for the full year 2012.

With that, John, we'll now take questions.

| Operator: | OK, so at this time, ladies and gentlemen, if you have a question or comment, press the star followed with the one key and you'll be placed into the question queue. So, again, if any questions or comments, press the star followed with the one key and you'll be placed into the question queue. |

And we'll take our first question from Sameet Sinha from B. Riley. Please go ahead with your question.

| Sameet Sinha: | I have a few questions here. You made an interesting comment about mobile revenue. Can you talk a little more about that? I know you launched your mobile website some time back. Are these views, in your opinion, are they incremental to the desktop views? And also, if you can talk with us about the CPMs on these mobile views. |

Continuing on that trend, do you get legion – I mean, MPs from mobile devices as well? Secondly, a question on new products. I know in the past you have spoken about having new products to kind of diversify your revenue mix. Any chance that you could shed some more light on it and when we could see some of these new ones coming out?

8

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 9

And in terms of the upfront for 2013, since you're getting initial feedback, any sense of how much CPM increases are you seeing there? Thank you.

| Jeff Coats: | Sameet, nice to talk to you. You're going to have to probably prompt me again as I go through this. So, we do – we're seeing a nice increase in mobile. We believe that in the automotive industry, everything is going to mobile to make it easier for people to shop. That's why we built a mobile-enhanced version of our site – to make it easier. It's not an app. |

We do believe the page views for our mobile is incremental. From a CPM standpoint, the CPMs are a bit higher from a mobile standpoint, but as you know, we don't really talk about the details of those numbers. So, I'm not really prepared today to go any further than that.

The upfronts for 2013 are going very well for us. We are seeing larger dollar commitments as a result of the growth in page views. There will be some overall CPM improvements, largely as part of mix, but there are some CPM increases that are coming through as a result of the upfront. We're still pretty early. A lot of stuff doesn't get nailed down until toward the end of the year.

And our mobile site does support lead generation. I think that's one of the questions that you asked. Yes, it does. And we're further enhancing things for that.

I think there was a question in there about new products. We are working on new products, both from a dealer centric point of view. I would expect that we'll have something out in the marketplace probably later in 2013, but what we are really focused on right now - we really view our partnership with Polk as providing to us incredibly valuable information that we can then provide to our dealer customers and even to our OEM customers for the dealers that are part of their programs.

9

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 10

As you can see somewhat from the slide that we have in the presentation, which really shows dealers – and for the first time in our history we're actually able to talk to dealers and know upfront how many cars they sold from the leads we provided to them, and what happened to the consumers associated with the other leads that we also sold them. So that slide, which is Slide number 8, will show you really where those consumers did end up buying a car. Some of them will have submitted Ford leads through us using the example on these slides and then just ended up buying from another Ford dealer. Some of the important stuff that this data shows is that consumers do cross over from new-to-used after they submit a new lead, and it also shows that consumers do cross over makes after they submit a lead because several of these – and this is actual data that we've dropped in here from a specific example. We've changed the names of all the dealerships, but this shows you the cross over between makes after a consumer has submitted a Ford lead.

So, this kind of data is actually pretty new and extremely actionable in the auto space, so, we're very excited about this. So, for the time being, for the foreseeable future, we'll be focused on getting this message out there because these are specific dealer reports on the dealer-by-dealer basis.

Did I hit everything?

| Sameet Sinha: | Yes, yes, definitely. One final question. In terms of expenses, you keep threatening us with incremental expenses going forward, but we still haven't seen that and the Op Ex is fairly flat. Should we assume that your incremental of expenses are basically in the cost of goods line? That's why your gross margin is going down, or do you think there are going to be some upgrading expense increments also going forward? |

| Jeff Coats: | Well, I wouldn't exactly agree that we threaten you with incremental expenses. We just talk about the fact that we see great growth opportunities in our business, and we're investing in order to accelerate those growth opportunities in our business. |

10

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 11

One of the reasons that you're not seeing an increase in our operating expense line is because we're also, at the same time, doing a damn good job of managing our operating expenses, so, we've been able to offset some of the investments that we make through operating expenses with reductions in other areas. And we would, you know, expect to continue to do that. Some of the investments are in cost of goods sold, particularly the ones related to lead generation as we beef up our internal lead generation team and as we create new and increased content. The video content that we create that's on the YouTube channel and other written content is in our cost of goods sold line.

So, you know, we believe we actually continue to do a good job of managing our expenses and balancing, you know, where it makes sense to invest and take expenses out of other areas. The comment that I made about investing in the sales force, that will be in the operating expense line. We have not invested in our sales force other than replacing positions for quite some time, but we're very excited about what we've been able to do in terms of growing our dealer facing revenue. And that's even before we begin having any meaningful information back from the Polk partnership to use to go out and talk to dealers about.

So, we believe that by arming our sales force with all of this incredibly important information that is actionable for dealers, you know, we're going to drive our revenue up, and our productivity is going to increase pretty meaningful as a result of that.

| Sameet Sinha: | OK, thank you. |

| Operator: | OK, thank you. And we'll take our next question from Jared Schramm from Roth Capital. So, Jared, please, go ahead. |

| Jared Schramm: | You there? |

| Jeff Coats: | Yes. Hi, Jared. |

| Jared Schramm: | OK, sorry. So, it appears that the R.L. Polk study to date has been quite a success for you. Is this something that you're going to look to continue in perpetuity or will you take the data you have thus far and just replicate that as you pitch the product to wholesalers and retailers? |

11

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 12

| Jeff Coats: | This is something that we would basically expect to continue in perpetuity. It's ongoing. We update this data on a regular basis working with Polk. So, it's a living, breathing part of what we're doing today. We basically update the information with new feeds from Polk on a monthly basis, so, it will continue to be an integral part of what we're doing as we go forward. |

And candidly, what we're also doing is encouraging our competitors and our suppliers to participate in a program like this with Polk because it's a great thing for everybody in the auto space to overall improve the quality of the leads that are being sold to the dealers and the manufacturers. Everybody benefits at the end of the day, and so, we're strongly encouraging all of our competitors to join us in doing this.

| Jared Schramm: | And turning to finance requests, any deeper color on what you're seeing in that space there? You know, it appears the environment seems to be lightening up as far as requirements are concerned. Just wanted to get your take on what you're seeing, particularly in the finance request arena. |

| Jeff Coats: | Well, you know, historically, that's really been a business that we aggregate leads. So, we would buy the vast majority of all the leads that we turned around and sold to our dealer customers. Starting about, actually, about August of last year, there started to be some ripple effects in that market, I think, as a result of more players coming into it. Subprime was starting to kick up. Some of the larger lending institutions were beginning to enter the SEM markets related to subprime. Prices started going up. And what's really happened over the course of the last year is there are actually a handful of long time participants in the market and some brand new very large participants in the market that are bidding up the available supply to prices that approach what has historically been the retail price that we would all sell these leads for. |

12

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 13

As you can imagine, that's not something that we have found terribly palatable. We have begun ramping up our internal efforts. We're beefing our SEM team in order to focus on this more. We are ramping up our efforts on autobytel.com in order to expand our finance section. We're looking at a partnership with a couple of large providers of finance-related opportunities, tools, in terms of what we're doing. So, we do believe that we will be able to turn that business around. We do believe we will be able to ramp up the volume of leads that we generate internally. We will continue to focus on the quality end of that market. We could have continued to boost our revenue by buying poor quality stuff. We, of course, chose not to do that. That's a short term fool's errand from the way I look at this. And so, we have kept our reputation intact and are looking to grow that business as we move forward.

We've also seen, even recently over the last couple of months, the volume issues have moderated a little bit. I think some of the people that were grossly overpaying for months, perhaps have recognized that their return on investment is not what they would like it to be, and they're pulling back. So, we're still optimistic about the future of that.

| Jared Schramm: | That's helpful. And lastly here, turning to just purchase requests. You mentioned in your - as you're looking to buy from third party aggregators that supply has got a little tighter. Is that due to fewer aggregators being around right now to kicking out leads, or is that just the demand side has really kicked up and is making that supply go a little shorter? |

| Jeff Coats: | It's a combination of both. There are fewer suppliers out in the marketplace today, in large part because there was a large number of them that were generating and selling some very poor quality stuff. Some of those guys have gone out of business. Some of those guys are cleaning up their act and they're improving the quality of what they're doing. You know, one of the benefits of our new relationship with Polk is we can use that information and get a much better handle on the true quality of the leads that we're buying from some of our suppliers and help them understand how they can do better at, you know, generating quality through their own methods. And, you know, those that we see that are improving their quality, we are and are prepared to increase our purchases from to the detriment of those that don't. So, we view it as kind of a positive. |

13

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 14

| Jared Schramm: | OK, thank you very much. |

| Jeff Coats: | Thank you, Jared. |

| Operator: | OK, thank you. And before we take our next question, I would like to remind everyone how to queue up for questions. You can press the star followed with the one key, and you'll be placed into the question queue. |

And we'll take our next question from George Santana from Ascendiant. Please go ahead, George.

George Santana: (Inaudible) you my question. How about a few of them for you – small ones on the Polk data. Thanks so much for sharing some color on that. How far along in the process are you on that? And what I mean by that, are you showing that's all dealers, in other words, on the national basis? Or are you still rolling this out by territory?

| Jeff Coats: | I think it's probably fair to say we're still in the rolling-out process. I mean, you know, these reports have to be pulled on a dealer–by-dealer basis. You know, we've got about 3,800 dealers on our programs today of new and used programs, so, they've got to pulled dealer–by-dealer. We are looking for ways to improve that process. We're also in additional discussions with Polk in order to deepen the type of information that we get and as well as to speed up the timing of some of the information that we get. |

So, I think the good news out of this is we've able to pick up our progress, generate increased revenue, increase our profitability even before we've had any meaningful benefit from the Polk data for any reasonable amount of time. I mean, really, it's only been in the last probably three months that we've had enough of this data that we've worked with and that we and Polk feel comfortable we are, you know, seeing the right results from in order to go out and use it with dealers.

14

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 15

But, we are, in fact, gearing that up, and candidly, that's one of the reasons why we're interested in investing and increasing our sales force is to get that message out there, both to the dealers we already have on our programs, but equally important to go out there and sit down with dealers that we don't have on our program that we see as a result of the Polk data having purchased or sold cars to consumers that have come through our process.

| George Santana: | That's great. So, this will be an ongoing process, and you mentioned it's one in perpetuity, but it's - I can imagine that kind of data takes some time to compile. |

| Jeff Coats: | Yes. They aggregate it from all 50 DMVs around the country, so, you know, it takes them a while to gather it after the end of every month, clean it. So, there is, you know, probably a 60 to 90-day lag time on getting the data. We're working to reduce that, but it's still highly actionable data because what we're doing is showing dealers, you know, where they could have sold vehicles in addition to discussions about the ones they did sell. |

| George Santana: | And are you - do you actually have anecdotal data that you've shown this info to a dealer and they've said, sign me up? |

| Jeff Coats: | Yes, we definitely have examples of those conversations. Absolutely. |

| George Santana: | That's great to hear. You also mentioned your sales force. How many salespeople are actually out there for you, and how does that compare, and what do you envision going forward? |

| Jeff Coats: | We've got - we have currently 18 people in the field or 18 positions in the field. There are a couple of open positions that we're replacing. We have about 20 people internally that do both sales and customer support. I would say the total increase in that would probably be, you know, less than 20% over all of that. What we're really looking to do - and the way we've done this is it's quite scientific and it's based upon where we know we have high volumes of customers that we could use additional support. Either sales support or frontline sales support or sales people because of the volume of opportunity or interest that we have. And, you know, in the most popular areas around the country, for the most part. |

15

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 16

| George Santana: | So, the increase of less than 20%, is that from last year or where you envision that you will go? |

| Jeff Coats: | I'm sorry, George. Could you ask me that one more time? |

| George Santana: | You said you envision the total increase or - it represented a total increase of less than 20%. I'm not sure if that is less than 20% increase from where you were last year or you don't need that many more bodies in order to fully staff a sales force. |

| Jeff Coats: | It would probably - what I mean is a 20% increase from where we are right now. |

| George Santana: | I see. To get to where you need? |

| Jeff Coats: | Well, to get to where we feel like we can more aggressively cover the most populous areas of the country. |

| George Santana: | OK. Yes, perhaps on a tangent there, what do you need to do and how much of an investment would it require to build up your internally-generated finance leads? |

| Jeff Coats: | We've pretty much done what we think we need to do. We've beefed up our internal group with - largely by hire - making an additional hire. There really aren't a lot of other expenses associated with that other than just the way we normally generate those volumes of leads. It's not going to be a big increase in OpEx or in cost of revenue related to beginning to generate those. |

| George Santana: | I see, OK. Also, is there an update on - last quarter, you mentioned something about Yahoo! and Detroit Trading and TrueCar? |

16

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 17

| Jeff Coats: | To the best of our understanding and I don't really want to be too detailed because, to be perfectly honest, I'm not privy to all the details. Yahoo! and TrueCar have changed the nature of their relationship. As you know from the press releases that were put out, Detroit Trading is managing the lead volume out of Yahoo! Autos. We have a very strong relationship with Yahoo! and with Detroit Trading. And as far as we're aware, we are one of the large purchasers of leads coming from Yahoo! Autos that we in turn sell to our dealer customers. |

| George Santana: | And they're scrubbing fine - well, I guess you can't really say. But you wouldn't be buying them if they were not of high quality, right? |

| Jeff Coats: | We would not be buying them if they were not good quality. |

| George Santana: | OK. You know, finally, and certainly you guys deserve a lot of credit for driving profitability, operating cash flow, but what do I tell an investor who's looking at your company going, well, you know, this is great, but you have revenue growth of 3% to 5%. Can this be, in 2013, 2014, a double digit grower at least on the top line with hopefully operating leverage that gets you to significantly greater profitability? |

| Jeff Coats: | I would say it's not inconceivable that we could reach those levels. Certainly the ability to do that is enhanced by adding to our sales and sales support operations in order to increase the number of dealers on our programs. So, I think it is possible. I forgot the last part of what you asked. I apologize. |

| George Santana: | It's just more if you expect the top line revenue - not trying to ask you to commit to any number, of course, but, you know, can this business be there? You know, certainly the economy has been difficult. We see auto sales returning. We see people getting auto loans again. So, that will help; the advertising, as you're - as you're mentioning, but if you're going on top line - hopefully, part of the story is that you have significant operating leverage and the profitability will grow faster. |

| Jeff Coats: | Let me just say this. There's nothing structurally that would prevent us from being able to do that. And one of the reasons we are continuing to invest in the business is so that we can accelerate our growth and take advantage of the opportunities that we see in front of us. |

17

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 18

| George Santana: | Great. Thank you, guys. |

| Jeff Coats: | Thank you, George: |

| Operator: | OK, thank you. And we'll take a follow up question from Sameet Sinha. Sameet, please go ahead. |

| Sameet Sinha: | Thank you. So, in terms of the sales force expansion for, especially for a dealer group, can you talk to us about the compensation structure? How does that work, and could this be marginally incremental? And second thing is, any impact from Hurricane Sandy? Obviously, a lot of dealer inventories, stocks, (inaudible) of it's partly destroyed. Can you just give us some initial feedback that you're getting? |

| Jeff Coats: | Let me answer the second part of your question first. It's really, so far, too soon for us to tell to what extent there will be an impact directly on our business. Having said that, the eastern seaboard corridor is one of the most populous corridors in the country, and we do have a lot of dealer customers in those markets. We know that some of our dealer customers, particularly in New Jersey, still don't have power and have not reopened their operations. So, you know, we do expect to see some, but thus far, we don't think it's going to be, you know, a difficult impact on our business. Having said that, we're also aware, and I think NBC put out a report earlier today estimating that up the eastern seaboard there's probably approximately 250,000 vehicles that will have to be replaced over the coming months. And we would expect to be part of that replacement process as consumers look online, figure out what they want to try to buy once they get their insurance check and go through that process. |

I doubt we'll see too much of benefit to ourselves in that in the fourth quarter. There might be some in December. December usually is a pretty robust month. You know, I don't know if this December is going to be affected by concerns over the fiscal cliff and taxes going up and all that kind of stuff. It remains to be seen. But the good news or the silver lining in that cloud for the automotive industry is there will be 250,000 cars approximately that have got to be replaced. It'll start this year, and it'll probably be relatively robust in the first few months of 2013.

18

Autobytel

Moderator: Jeffrey Coats

11-08-2012/5:00 p.m. ET

Confirmation # 41912510

Page 19

And for the first part of your question, we really don't talk about compensation in that granular detail. So, I really can't answer that question for you.

| Sameet Sinha: | OK, thank you. |

| Jeff Coats: | Thank you, Sameet. |

| Operator: | OK, thank you. So, I'd like to turn the call back to Jeff Coats for any concluding remarks. |

| Jeff Coats: | Thanks, folks, for joining us today. We look forward to reporting to you on our continued progress. Thanks. |

| Operator: | OK, ladies and gentlemen, that does conclude your conference. You may now disconnect and have a great day. |

END

19

20

21

22

23

24

25

26

27

28

29

30

31

32