Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - GreenLink International Inc. | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - GreenLink International Inc. | ex31x1.htm |

| EX-32.1 - EXHIBIT 32.1 - GreenLink International Inc. | ex32x1.htm |

| EX-32.2 - EXHIBIT 32.2 - GreenLink International Inc. | ex32x2.htm |

| EX-31.2 - EXHIBIT 31.2 - GreenLink International Inc. | ex31x2.htm |

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended: September 30, 2012

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to _________

Commissions file number 0-32051

E-DEBIT GLOBAL CORPORATION

(Exact name of Registrant as specified in its charter)

|

COLORADO

|

98-0233968

|

|

(State or other jurisdiction

of incorporation or organization)

|

(IRS Employer Identification No.) |

#12, 3620 – 29th Avenue NE

Calgary, Alberta Canada T1Y 5Z8

Telephone (403) 290-0264

(Issuer's telephone number)

(Former name, former address and former

fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

|

Non-accelerated filer o

|

Smaller reporting company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS

DURING THE PRECEDING FIVE YEARS

Indicate by check mark whether the registrant filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Exchange Act after the distribution of securities under a plan confirmed by a court. Yes o No o

APPLICABLE ONLY TO CORPORATE ISSUERS

State the number of shares outstanding of each of the issuer's classes of common equity, as of the latest practicable date: As of November 2, 2012, there were 330,709,344 outstanding shares of the Registrant's Common Stock, no par value and 70,855,900 shares of Preferred Stock, no par value.

E-DEBIT GLOBAL CORPORATION

INDEX TO THE FORM 10-Q

For the quarterly period ended September 30, 2012

|

PAGE

|

|||

| PART I. FINANCIAL INFORMATION | |||

|

ITEM 1.

|

UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

|

||

|

Condensed Consolidated Balance Sheets

|

3

|

||

|

Condensed Consolidated Statements of Operations

|

4

|

||

|

Condensed Consolidated Statements of Comprehensive Income

|

6

|

||

| Condensed Consolidated Statements of Changes in Stockholders’ Deficit | 7 | ||

|

Condensed Consolidated Statements of Cash Flows

|

8

|

||

|

Notes to Condensed Financial Statements

|

9

|

||

|

ITEM 2.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

23

|

|

|

ITEM 3.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK.

|

30

|

|

|

ITEM 4.

|

CONTROLS AND PROCEDURES

|

30

|

|

| Part II. OTHER INFORMATION | |||

|

ITEM 1.

|

LEGAL PROCEEDINGS

|

30

|

|

|

ITEM 2.

|

UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

|

30

|

|

|

ITEM 3.

|

DEFAULTS UPON SENIOR SECURITIES

|

31

|

|

|

ITEM 4.

|

MINE SAFETY DISCLOSURES

|

31

|

|

|

ITEM 5.

|

OTHER INFORMATION

|

31

|

|

|

ITEM 6.

|

EXHIBITS

|

31

|

|

2

PART I - FINANCIAL INFORMATION

ITEM 1. UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

E-DEBIT GLOBAL CORPORATION

Condensed Consolidated Balance Sheet

|

ASSETS

|

September 30,

2012

(Unaudited)

|

December 31, 2011

(Derived from audited financial statements)

|

||||||

|

CURRENT ASSETS

|

||||||||

|

Cash

|

$ | 28,297 | $ | 96,492 | ||||

|

Restricted cash

|

1,141,826 | 595,044 | ||||||

|

Accounts receivable net of allowance for doubtful

accounts of $23,240 and $13,172

|

31,908 | 37,342 | ||||||

|

Other receivable – related parties

|

10,567 | 6,917 | ||||||

|

Inventory

|

— | 14,058 | ||||||

|

Prepaid expense and deposit

|

4,607 | 20,017 | ||||||

|

Total current assets

|

1,217,205 | 769,870 | ||||||

|

Property and equipment, net of depreciation

|

166,291 | 232,113 | ||||||

|

Property and equipment, idle

|

385,393 | 364,625 | ||||||

|

Investment, at cost

|

20 | 20 | ||||||

|

Deposit – related party

|

— | 156,668 | ||||||

|

Intangible Assets, net of amortization

|

53,946 | 79,389 | ||||||

|

Total assets

|

$ | 1,822,855 | $ | 1,602,685 | ||||

|

LIABILITIES AND STOCKHOLDERS’ DEFICIT

|

||||||||

|

CURRENT LIABILITIES

|

||||||||

|

Accounts payable

|

1,371,520 | 1,051,828 | ||||||

|

Accrued liabilities

|

145,708 | 156,287 | ||||||

|

Loans payable

|

484,757 | 358,754 | ||||||

|

Indebtedness to related parties

|

1,225,472 | 1,081,259 | ||||||

|

Shareholder loans

|

296,193 | 285,194 | ||||||

|

Total current liabilities

|

3,523,650 | 2,933,322 | ||||||

|

Total liabilities

|

3,523,650 | 2,933,322 | ||||||

|

STOCKHOLDERS’ DEFICIT

|

||||||||

|

Preferred stock – authorized 200,000,000 shares, no par value,

70,855,900 shares issued and outstanding at

September 30, 2012 and 70,855,900 at December 31, 2011

|

1,400,855 | 1,400,855 | ||||||

|

Common stock - authorized 10,000,000,000 shares, no par value;330,709,344 shares issued and outstanding at

September 30, 2012 and 95,249,344 at December 31, 2011

|

2,287,030 | 2,051,570 | ||||||

|

Additional paid-in capital

|

654,018 | 654,018 | ||||||

|

Accumulated other comprehensive income

|

67,039 | 115,911 | ||||||

|

Accumulated deficit

|

(6,109,737 | ) | (5,552,991 | ) | ||||

|

Total stockholders’ deficit

|

(1,700,795 | ) | (1,330,637 | ) | ||||

|

Total liabilities and stockholders’ deficit

|

$ | 1,822,855 | $ | 1,602,685 | ||||

See accompanying notes to consolidated financial statements

3

E-DEBIT GLOBAL CORPORATION

Condensed Consolidated Statements of Operations

For the Nine Months Ended September 30,

(Unaudited)

|

2012

|

2011

|

|||||||

|

Revenue -

|

||||||||

|

Equipment and supplies

|

$ | 3,018 | $ | 20,229 | ||||

|

Residual and interchange income

|

1,761,765 | 2,534,018 | ||||||

|

Other

|

57,724 | 35,719 | ||||||

|

Total revenue

|

1,822,507 | 2,589,966 | ||||||

|

Cost of sales -

|

||||||||

|

Equipment and supplies

|

13,492 | 81,741 | ||||||

|

Residual and interchange costs

|

1,142,926 | 1,723,160 | ||||||

|

Other

|

438,294 | 465,699 | ||||||

|

Total cost of sales

|

1,594,712 | 2,270,600 | ||||||

|

Gross profit

|

227,795 | 319,366 | ||||||

|

Operating expenses -

|

||||||||

|

Depreciation and amortization

|

78,007 | 59,014 | ||||||

|

Consulting fees

|

129,237 | 148,736 | ||||||

|

Legal and accounting fees

|

54,957 | 57,246 | ||||||

|

Salaries and benefits

|

374,865 | 413,955 | ||||||

|

Travel, delivery and vehicle expenses

|

38,963 | 40,236 | ||||||

|

Other

|

273,019 | 322,810 | ||||||

|

Total operating expenses

|

949,048 | 1,041,997 | ||||||

|

(-Loss-) from operations

|

(721,253 | ) | (722,631 | ) | ||||

|

Other income (expense) -

|

||||||||

|

Interest expense

|

(108,990 | ) | (106,217 | ) | ||||

|

Gain on sale

|

263,418 | — | ||||||

|

Other income

|

10,079 | 73,956 | ||||||

|

Net (-loss-) before income taxes

|

(556,746 | ) | (754,892 | ) | ||||

|

Provision for income taxes

|

— | — | ||||||

|

Net (-loss-)

|

$ | (556,746 | ) | $ | (754,892 | ) | ||

|

Basic net (-loss-) per common share

|

$ | (0.00 | ) | $ | (0.01 | ) | ||

|

Weighted number of shares outstanding

|

147,573,788 | 92,974,344 | ||||||

See accompanying notes to consolidated financial statements

4

E-DEBIT GLOBAL CORPORATION

Condensed Consolidated Statements of Operations

For the three Months Ended September 30,

(Unaudited)

|

2012

|

2011

|

|||||||

|

Revenue -

|

||||||||

|

Equipment and supplies

|

$ | 2,963 | $ | 6,439 | ||||

|

Residual and interchange income

|

591,496 | 892,726 | ||||||

|

Other

|

10,200 | 16,339 | ||||||

|

Total revenue

|

604,659 | 915,504 | ||||||

|

Cost of sales -

|

||||||||

|

Equipment and supplies

|

3,039 | 67,108 | ||||||

|

Residual and interchange costs

|

376,337 | 585,018 | ||||||

|

Other

|

130,021 | 154,065 | ||||||

|

Total cost of sales

|

509,397 | 806,191 | ||||||

|

Gross profit

|

95,262 | 109,313 | ||||||

|

Operating expenses -

|

||||||||

|

Depreciation and amortization

|

24,305 | 19,780 | ||||||

|

Consulting fees

|

39,692 | 48,850 | ||||||

|

Legal and accounting fees

|

9,872 | 13,531 | ||||||

|

Salaries and benefits

|

121,324 | 123,323 | ||||||

|

Travel, delivery and vehicle expenses

|

25,578 | 7,700 | ||||||

|

Other

|

81,813 | 136,203 | ||||||

|

Total operating expenses

|

302,584 | 349,387 | ||||||

|

Income (-Loss-) from operations

|

(207,322 | ) | (240,074 | ) | ||||

|

Other income (expense) -

|

||||||||

|

Interest expense

|

(22,480 | ) | (40,302 | ) | ||||

|

Other income

|

10,079 | 38,911 | ||||||

|

Net (-loss-) before income taxes

|

(219,723 | ) | (241,465 | ) | ||||

|

Provision for income taxes

|

— | — | ||||||

|

Net (-loss-)

|

$ | (219,723 | ) | $ | (241,465 | ) | ||

|

Basic net (-loss-) per common share

|

$ | (0.00 | ) | $ | (0.00 | ) | ||

|

Weighted number of shares outstanding

|

252,222,677 | 94,274,344 | ||||||

See accompanying notes to consolidated financial statements

5

E-DEBIT GLOBAL CORPORATION

Condensed Consolidated Statements of Comprehensive Income

(Unaudited)

|

Three Months Ended September 30,

|

Nine Months Ended September 30,

|

|||||||||||||||

|

2012

|

2011

|

2012

|

2011

|

|||||||||||||

|

Net (-loss-)

|

$ | (219,723 | ) | $ | (241,465 | ) | $ | (556,746 | ) | $ | (754,892 | ) | ||||

|

Other comprehensive (-loss-), net of tax

|

||||||||||||||||

|

Foreign currency translation adjustment

|

(47,560 | ) | 52,708 | (48,872 | ) | 49,574 | ||||||||||

|

Other comprehensive (-loss-), net of tax

|

(47,560 | ) | 52,708 | (48,872 | ) | 49,574 | ||||||||||

|

Comprehensive (-loss-)

|

$ | (267,283 | ) | $ | (188,757 | ) | $ | (605,618 | ) | $ | (705,318 | ) | ||||

See accompanying notes to consolidated financial statements

6

E-DEBIT GLOBAL CORPORATION

Condensed Consolidated Statements of Changes in Stockholders’ Deficit

(Unaudited)

|

|

||||||||||||||||||||||||||||||||

|

|

|

|

||||||||||||||||||||||||||||||

|

Preferred Stock

|

Common Stock

|

Additional

Paid-in |

Accumulated

Other |

Accumulated

|

Total

Stockholders’ |

|||||||||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

Capital

|

Income

|

(Deficit)

|

(Deficit)

|

|||||||||||||||||||||||||

|

Balance, December 31, 2011

|

70,855,900 | $ | 1,400,855 | 95,249,344 | $ | 2,051,570 | $ | 654,018 | $ | 115,911 | $ | (5,552,991 | ) | $ | (1,330,637 | ) | ||||||||||||||||

|

Exercise of convertible notes to a creditor for settlement of debts

|

— | — | 185,460,000 | 185,460 | — | — | — | 185,460 | ||||||||||||||||||||||||

|

Exercise of convertible notes to a creditor for settlement of debts

|

— | — | 50,000,000 | 50,000 | — | — | — | 50,000 | ||||||||||||||||||||||||

|

Other comprehensive loss, net of tax

|

— | — | — | — | — | (48,872 | ) | — | (48,872 | ) | ||||||||||||||||||||||

|

Net loss for the nine months ended September 30, 2012

|

— | — | — | — | — | — | (556,746 | ) | (556,746 | ) | ||||||||||||||||||||||

|

Balance, September 30, 2012

|

70,855,900 | $ | 1,400,855 | 330,709,344 | $ | 2,287,030 | $ | 654,018 | $ | 67,039 | $ | (6,109,737 | ) | $ | (1,700,795 | ) | ||||||||||||||||

See accompanying notes to consolidated financial statements

7

E-DEBIT GLOBAL CORPORATION

Condensed Consolidated Statement of Cash Flows

For the Nine Months Ended September 30,

(Unaudited)

|

2012

|

2011

|

|||||||

|

Cash flows from operating activities:

|

||||||||

|

Net (loss) income from operations

|

$ | (556,746 | ) | $ | (754,892 | ) | ||

|

Reconciling adjustments -

|

||||||||

|

Depreciation and amortization

|

78,007 | 59,014 | ||||||

|

Impairment of inventory and receivable

|

— | 109,212 | ||||||

|

Changes in operating assets and liabilities

|

||||||||

|

Restricted cash

|

(546,782 | ) | (53,999 | ) | ||||

|

Accounts receivable

|

1,784 | (56,544 | ) | |||||

|

Inventory

|

14,058 | 1,040 | ||||||

|

Prepaid expenses and other

|

15,410 | 13,346 | ||||||

|

Cash overdraft

|

— | (20,918 | ) | |||||

|

Other

|

— | (247 | ) | |||||

|

Accounts payable and accrued liabilities

|

893,673 | 459,461 | ||||||

|

Net cash (used for) provided by operations

|

(100,596 | ) | (244,527 | ) | ||||

|

Cash flows from investing activities:

|

||||||||

|

Purchase of equipment

|

— | (15,545 | ) | |||||

|

Disposal of equipment

|

— | — | ||||||

|

Net cash (used for) provided by investing activities

|

— | (15,545 | ) | |||||

|

Cash flows from financing activities:

|

||||||||

|

Proceeds from loans

|

126,003 | — | ||||||

|

Proceeds from related parties

|

164,235 | 317,725 | ||||||

|

Repayments to related parties

|

(208,965 | ) | (42,841 | ) | ||||

|

Net cash provided by financing activities

|

81,273 | 274,884 | ||||||

|

Foreign currency translation adjustment

|

(48,872 | ) | 49,574 | |||||

|

Net change in cash and cash equivalents

|

(68,195 | ) | 64,386 | |||||

|

Cash (overdraft) at beginning of year

|

96,492 | — | ||||||

|

Cash (overdraft) at end of year

|

$ | 28,297 | $ | 64,386 | ||||

|

Supplemental schedules:

|

||||||||

|

Cash paid for interest

|

$ | 27,924 | $ | 57,462 | ||||

|

Cash paid for income taxes

|

$ | — | $ | — | ||||

|

Noncash investing and financing activities

|

||||||||

|

Shares issued for the settlement of debt

|

$ | 235,460 | $ | 81,700 | ||||

See accompanying notes to consolidated financial statements

8

E-DEBIT GLOBAL CORPORATION

Notes to Condensed Consolidated Financial Statements

September 30, 2012 and 2011

(Unaudited)

Note 1 – Basis of Presentation and Nature of Operations

The accompanying consolidated balance sheet as of December 31, 2011 has been derived from audited financial statements and the accompanying unaudited consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information and the interim reporting requirements of Regulation S-X. The accompanying consolidated financial statements included herein have been prepared by E-Debit Global Corporation (the “Company”) without audit, pursuant to the rules and regulations of the Securities and Exchange Commission for reporting on Form 10-Q. In management's opinion, all adjustments (consisting only of normal recurring adjustments) considered necessary for a fair presentation have been included. Certain information and footnote disclosure normally included in the financial statements prepared in accordance with generally accepted accounting principles have been condensed or omitted as allowed by such rules and regulations, and E-Debit Global Corporation believes that the disclosures are adequate to make the information presented not misleading. It is suggested that these financial statements be read in conjunction with the December 31, 2011 audited financial statements and the accompanying notes thereto contained in the Annual Report on Form 10-K filed with the Securities and Exchange Commission. While management believes the procedures followed in preparing these financial statements are reasonable, the accuracy of the amounts are in some respects dependent upon the facts that will exist, and procedures that will be accomplished by E-Debit Global Corporation later in the year. The results of operations for the interim periods are not necessarily indicative of the results of operations for the full year. In management’s opinion all adjustments necessary for a fair presentation of the Company’s financial statements are reflected in the interim periods included.

Westsphere Asset Corporation, Inc. (Company) was incorporated in Colorado on July 21, 1998 as Newslink Networks TDS, Inc. and changed its name to Westsphere Asset Corporation Inc. on April 29, 1999. On April 2, 2010, the Company officially changed its name to E-Debit Global Corporation.

On September 18, 2012, the Company amended its articles of incorporation to increase its authorized capital to Ten Billion (10,000,000,000) shares of no par value common stock and Two Hundred Million (200,000,000) of no par value preferred stock.

The Company’s primary business is the sale and operation of cash vending (ATM) and point of sale (POS) machines in Canada.

Note 2 – Recent Accounting Pronouncements

Effective January 1, 2012, we retrospectively adopted new guidance issued by the Financial Accounting Standards Board by presenting a total for comprehensive income and the components of net income and other comprehensive income in two separate but consecutive statements. The adoption of this guidance resulted only in a change in how we present other comprehensive income in our consolidated financial statements and did not have any impact on our results of operations, financial position, or cash flows.

A variety of proposed or otherwise potential accounting standards are currently under study by standard setting organizations and various regulatory agencies. Due to the tentative and preliminary nature of those proposed standards, management has not determined whether implementation of such proposed standards would be material to our consolidated financial statements.

9

Note 3 – Fair Value Measurements

The carrying amounts of current assets and current liabilities approximate fair value because of the short-term nature or the current rates at which the Company could borrow funds with similar remaining maturities. These fair value estimates are subjective in nature and involve uncertainties and matters of significant judgment, and, therefore, cannot be determined with precision. Changes in assumptions could significantly affect these estimates. The Company does not hold or issue financial instruments for trading purposes, nor does it utilize derivative instruments.

The FASB ASC clarifies that fair value is an exit price, representing the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. It also requires disclosure about how fair value is determined for assets and liabilities and establishes a hierarchy for which these assets and liabilities must be grouped, based on significant levels of inputs as follows:

|

Level 1:

|

Quoted prices in active markets for identical assets or liabilities. | |

|

Level 2:

|

Quoted prices in active markets for similar assets and liabilities and inputs that are observable for the asset or liability.

|

|

|

Level 3:

|

Unobservable inputs in which there is little or no market data, which require the reporting entity to develop its own assumptions.

|

The determination of where assets and liabilities fall within this hierarchy is based upon the lowest level of input that is significant to the fair value measurement.

Note 4 - Restricted cash

The Company relies on a contractual agreement with Moneris Solution Corporation to settle daily ATM vault cash dispensements throughout our ATM Network into our bank account. The ATM vault cash will be settled to the cash owners within 24 hours turn around.

Note 5 - Accounts Receivable

Accounts receivable consists of amounts due from customers. The nature of the receivables consists of equipment sales, parts and accessories, and service provided. The Company considers accounts more than 180 days old to be past due, since the Company can withhold the transactions revenue owed to the customers should their receivables become past due. The account is deemed uncollectible and written off when the site locations are out of business and or in receivership. The Company uses the allowance method for recognizing bad debts. When an account is deemed uncollectible, it is written off against the allowance.

| September 30, 2012 | December 31, 2011 | |||||||

| Accounts Receivable | ||||||||

|

Equipment

|

- | $ | 5,579 | |||||

|

Services

|

- | 462 | ||||||

|

Other

|

55,148 | 44,473 | ||||||

|

|

55,148 | $ | 50,514 | |||||

| Less: Allowance for doubtful accounts | (23,240 | ) | (13,172 | ) | ||||

| $ | 31,908 | $ | 37,342 | |||||

The bad debt expense for the nine months ended September 30, 2012 and September 30, 2011 totaled $10,923 and $56,260, respectively. The bad debt is reflected in the accompanying consolidated Statements of Operations as Other operating expenses.

Note 6 – Inventory

Inventory consists of the following elements:

| Quantity | Cost | |||||||

| December 31, 2011 | ||||||||

|

ATM

|

6 | $ | 14,058 | |||||

|

Parts and accessories

|

- | - | ||||||

|

Total

|

$ | 14,058 |

| Quantity | Cost | |||||||

| September 30, 2012 | ||||||||

|

ATM

|

- | $ | - | |||||

|

Parts and accessories

|

- | - | ||||||

|

Total

|

$ | - |

Inventories are valued at the lesser of cost (on a first-in, first-out method) or net realizable value.

10

Note 7 – Property and Equipment

Property and equipment in service consists of the following elements:

|

Cost

|

Accumulated

Depreciation/

Amortization

|

Net

Book Value

|

Depreciation

Rate

and

Method

|

||||||||||

|

December 31, 2011 -

|

|||||||||||||

|

Office furniture and equipment

|

$ | 60,772 | $ | 31,274 | $ | 29,498 |

20% DB

|

||||||

|

Computer hardware and software

|

175,699 | 118,420 | 57,279 |

30% DB

|

|||||||||

|

ATM machines

|

236,845 | 93,317 | 143,528 |

30% DB

|

|||||||||

|

Other

|

8,252 | 6,444 | 1,808 |

Var

|

|||||||||

| $ | 481,568 | $ | 249,455 | $ | 232,113 | ||||||||

|

September 30, 2012 -

|

|||||||||||||

|

Office furniture and equipment

|

$ | 63,116 | $ | 37,729 | $ | 25,387 |

20% DB

|

||||||

|

Computer hardware and software

|

182,475 | 139,525 | 42,950 |

30% DB

|

|||||||||

|

ATM machines

|

173,200 | 76,413 | 96,787 |

30% DB

|

|||||||||

|

Other

|

8,571 | 7,404 | 1,167 |

Var

|

|||||||||

| $ | 427,362 | $ | 261,071 | $ | 166,291 | ||||||||

There are no leased ATMs included in the Company’s property and equipment for the nine months ended September 30, 2012 and for the year ended December 31, 2011.

Depreciation and amortization have been provided in amounts sufficient to recover asset costs over their estimated useful lives. All components of property and equipment are being depreciated or amortized. Depreciation and amortization expense for the nine months ended September 30, 2012 and September 30, 2011 totaled $78,007 and $59,014, respectively.

Property and equipment, idle consists of the following elements:

|

Cost

|

||||

|

December 31, 2011 -

|

||||

|

Computer hardware and software

|

$ | 364,625 | ||

| $ | 364,625 | |||

|

September 30, 2012 -

|

||||

|

Computer hardware and software

|

$ | 385,393 | ||

| $ | 385,393 | |||

The property and equipment, idle was related to the purchase of computer hardware and software for the card management system in June 2010. The software and computer hardware was purchased as a turnkey operating system which focused on a loyalty based platform. As of September 30, 2012, the system is being expanded from its loyalty based platform to a cash based platform. The Company is expecting the expansion of the system to be completed by the end of 2012.

11

Note 8 – Deferred Costs/Intangible Assets

On the 9th of November 2007, E-Debit contracted with ACI Worldwide through its wholly owned subsidiary Westsphere Systems Inc. (WSI) to provide its ACI ‘Base 24 On Demand” (AOD) hosted solution for ATM and POS transaction acquiring where WSI shares responsibilities with ACI as the transaction processor. ACI hosts the processing environment which is set up to specific requirements as set out by WSI, which supports WSI ATM and POS devices, debit and credit transaction processing and card management requirement that is unique and scalable to WSI’s current and future requirements and not shared with other ACI customers. ACI supplies software acquisition, operation and maintenance, facilities, operations and environment development and maintenance and disaster recovery infrastructure and services; whereby WSI supports, authorizes and distributes all settlements and revenues distributions through its account maintenance software developed by WSI and specific to ACI On Demand processing platform.

As a result Westsphere Systems Inc. processed all transactions through its association with ACI hosted transaction processing solution eliminating the costs, restrictions, and potential risks of relying on third party processors. Most importantly, the investment in the WSI role within the processing environment, or switch, will also enable E-Debit’s direct entry into new and emerging markets such as card management and processing.

The Company determined that it would be more appropriate to capitalize the development costs instead of expensing them as incurred. The Company’s decision was based on the criteria that ACI has established the technological feasibility for the software to provide a solution for ATM and POS transaction acquiring which is called ACI ‘Base 24 On Demand’ (AOD) and where all research and development activities for the other components of the product or process have been completed by them. E-Debit was working with ACI to setup specific requirements as set out by WSI which will supports WSI ATM and POS devices, debit and credit transactions processing and card management requirement that is unique and scalable to WSI’s current and future requirements and not shared with other ACI customers.

The development costs commenced in 2007 and were capitalized as deferred costs. The Company is amortizing these costs over its expected life.

E-Debit officially launched its switch in January 2009 and commenced rollover of ATMs to process all transactions through its association with ACI. The deferred costs were reclassified as intangible assets upon the completion of all the specific requirements including coding and testing in year 2009.

The Company assessed the useful life of the intangible asset in relation to its five-year contract with ACI commencing November 2008. The Company also determined the technology may be outdated at the end of the term of the contract and an enhancement of the software may be required at that time.

Depreciation is calculated using a declining balance method.

Intangible assets consist of the following elements:

|

Cost

|

Accumulated

Amortization

|

Net

Book Value

|

Depreciation

Method

|

||||||||||

|

December 31, 2011 -

|

|||||||||||||

|

License – ACI

|

$ | 164,340 | $ | 98,605 | $ | 65,735 |

Straight-line

|

||||||

|

Patent

|

14,688 | 13,884 | 804 |

Straight-line

|

|||||||||

|

License – Paragon

|

17,846 | $ | 4,996 | 12,850 |

Straight-line

|

||||||||

| $ | 196,874 | $ | 117,485 | $ | 79,389 | ||||||||

|

September 30, 2012 -

|

|||||||||||||

|

License – ACI

|

$ | 170,678 | $ | 128,009 | $ | 42,669 |

Straight-line

|

||||||

|

Patent

|

15,255 | 14,545 | 710 |

Straight-line

|

|||||||||

|

License – Paragon

|

18,535 | $ | 7,968 | 10,567 |

Straight-line

|

||||||||

| $ | 204,468 | $ | 150,522 | $ | 53,946 | ||||||||

12

Depreciation and amortization have been provided in amounts sufficient to recover asset costs over their estimated useful lives. Depreciation and amortization expense for the nine months ended September 30, 2012 and September 30, 2011 totaled $27,910 and $19,162, respectively. This depreciation and amortization expense was part of the totaled which are reflected in the accompanying consolidated statements of operations as Depreciation and amortization.

Expected future depreciation and amortization of the intangible assets are as follows:

|

Year

|

Amount

|

|||

|

2012

|

$ | 25,973 | ||

|

2013

|

$ | 27,973 | ||

Note 9 – Loans Payable

In September 2007, Vencash entered into a loan agreement with an initial term of twelve months totaling $101,693 ($100,000 CDN) with an external arms-length investor, bearing interest at 12% per annum, with blended monthly payments of interest only of $1,004 ($1,000 CDN). The initial term may be automatically extended for further six (6) month terms (a “renewal period”) after the end of the initial term or terminated subject to mutual termination agreements. The investor must give a written notice not less than 90 days before the end of the initial term or renewal period, whichever the case may be, to not renew the loan agreement. Vencash must notify the investor not less than 60 days before the end of the initial term or renewal period, its intention to terminate the loan. Currently, no written notice has been received from the investor to Vencash or vice versa. The purpose of the loan is to supply vault cash to Vencash’s customer-owned ATM equipment and site locations. Vencash supplies vault cash to these site locations because its customers do not have sufficient vault cash for these site locations.

The loan amount has been forwarded to an armored car company that supplies vault cash to these site locations. The armored car company is accountable for the rotation of the cash and has signed a note receivable for the amount.

As of September 30, 2012, the balance is $101,693 ($100,000 CDN). This loan is included in the accompanying consolidated balance sheet as Loans payable.

In November 2007, Westsphere’s subsidiary Westsphere Systems Inc. (WSI) raised $133,218 ($131,000 CDN) through a loan agreement with an initial term of twenty-four months with an external arms-length investor, bearing interest at 12% per annum, with blended monthly payments of interest only of $1,315 ($1,310 CDN). The initial term may be automatically extended for further twelve month terms (a “renewal period”) after the end of the initial term or terminated subject to mutual termination agreements. The investor must give a written notice not less than 90 days before the end of the initial term or renewal period, whichever the case may be, to not renew the loan agreement. Vencash must notify the investor not less than 30 days before the end of the initial term or renewal period, its intention to terminate the loan. Currently, no written notice has been received from the investor to WSI or vice versa. The purpose of the loan was to fund the switch development project. In February 2010, the loan was reduced by $62,212 ($65,000 CDN) in exchange for 622,123 common shares at $0.10 per share. In May 2012, the loan was reduced by $1,002 ($998 CDN) in offsetting against the expenses. In September 2012, the loan was reduced by $60 ($60 CDN) in offsetting against the expenses. As of September 30, 2012, the balance is $66,042 ($64,942 CDN). This loan is reflected in the accompanying consolidated balance sheet as loans payable.

On December 20, 2011 the Company and its subsidiaries jointly and severally entered into a Demand Loan Agreement and related GSA with an arms-length third party investor for a loan of $203,386 ($200,000 CDN) at a prime lending rate of Canadian Prime plus four (4%) percent. Under the GSA, this debt is collateralized by all of the Company’s assets. Upon demand the company has forty-five (45) days to repay the Demand Loan and interest. As of September 30, 2012, the balance is $214,434 ($210,864 CDN). This loan is included in the accompanying consolidated balance sheet as Loans payable.

13

On August 15, 2012 the Company and its subsidiaries jointly and severally entered into a Demand Loan Agreement and related GSA with an arms-length third party investor for a loan of $101,693 ($100,000 CDN) at a prime lending rate of Canadian Prime plus four (4%) percent. Under the GSA, this debt is collateralized by all of the Company’s assets. Upon demand the company has forty-five (45) days to repay the Demand Loan and interest. As of September 30, 2012, the balance is $102,588 ($100,880 CDN). This loan is included in the accompanying consolidated balance sheet as Loans payable.

Note 10 – Commitments and Contingencies

The Company leases real estate (office and warehouse space) under non-cancellable operating leases that expire on varying dates through 2014.

The Company leases additional real estate (office and warehouse space) for an “Initial Term” commencing June 1, 2010 on a month to month basis. The company may renew the Lease on a monthly basis by giving notice to the Landlord.

The Company also has various obligations for auto and equipment leases through 2016.

The Company’s real estate leases and one auto lease are signed with an affiliated company that is controlled by the Company’s president.

Minimum future rental payments under non-cancellable operating leases having remaining terms in excess of one year are as follows:

|

Real Estate

|

Other

|

|||||||

|

2012

|

$ | 18,097 | $ | 4,166 | ||||

|

2013

|

$ | 73,264 | $ | 12,013 | ||||

|

2014

|

$ | 12,211 | $ | 11,583 | ||||

|

2015

|

$ | — | $ | 6,953 | ||||

|

2016

|

$ | — | $ | 2,319 | ||||

|

September 30, 2012

|

December 31, 2011

|

|||||||

|

Rental expense

|

$ | 81,983 | $ | 83,475 | ||||

The Company leases telephone equipment under a non-cancellable capital lease commencing January 2011 and expiring in May 2015 with the option to purchase at the expiration of the 48 month lease term. As of September 30, 2012, the cost of telephone equipment under capital lease at the Company is $22,204 with accumulated amortization of $9,714.

Minimum future capital lease payments under non-cancellable capital lease having remaining terms in excess of one year are as follows:

|

Capital Lease

|

|

|

2012

|

$1,705

|

|

2013

|

$6,648

|

|

2014

|

$6,648

|

|

2015

|

$2,216

|

On April 7, 2004, the Company sued Fred and Linda Sebastian to recover an outstanding loan of $80,000 (CDN) plus interest and court costs. The Company has reserved this amount due to the uncertainty of recovery. The defendant has withdrawn the counterclaim. As of March 2008, no further actions were filed by either party.

14

On May 28, 2004 Peter Gregory filed an action in the Ontario Superior Court of Justice against Vencash Capital Corporation. Peter Gregory was a former Vencash distributor and agent who filed the action related to a claim of wrongful dismissal from Vencash of $260,000 (CDN). On July 30, 2004 Vencash filed a Statement of Defence and Counterclaim in the amount of $1,600,000 for breach of contract, breach of confidence, breach of fiduciary duties, interference with economic relations, damages for inducing breach of contract, and punitive damages. The Company believes the claim by Gregory to be without merit. In January 2012, the Company received a copy of notice of garnishment from our bank institution against Vencash’s bank account for the total amount not to exceed $31,649 CDN. The Company did not receive the notification for the judgement and is presently seeking legal advice. This notice was rescinded by the bank upon delivery. As of November 1, 2012 the Company has not been contacted further relating to the action initiated by Gregory. The company is currently reviewing the related correspondence and in consultation with legal counsel upon completion of the review will respond to any further action initiated by Gregory in this regard.

On January 25, 2009, Victory ATM filed an action in the Nova Scotia Superior Court against Vencash Capital Corporation. Victory ATM was formerly a customer of Vencash distributor Bullion Investments Inc. and claimed that supplied vault cash to a contracted armoured car company had been misappropriated for a total of approximately $45,000 CDN. The Company has filed a statement of defense stating that Vencash had no care control or access to the vault cash supplied by Victory ATM and the only role that Vencash played was processing the Victory ATM in their designated site locations. The Company believes the claim by Victory ATM to be without merit and has not accrued a liability for the claim. As of November 1, 2012 the Company has not been contacted further and per our knowledge no court actions have been initiated to date. Our Nova Scotia legal counsel has advised that she will continue to monitor this situation and upon discussion with Victory ATM legal counsel will make application to the courts to have the claim initiated against Vencash terminated.

Since 2009, Interac, MasterCard and VISA have mandated a hardware and software security upgrade for ATMs, Debit Terminals and the Corporation’s Switch.

Security upgrades are required under Interac, MasterCard, and VISA rules. These upgrades include the requirements to have:

|

(a)

|

EMV (Europay, MasterCard, VISA) certified chip card (the replacement technology for the historical magnetic stripe cards)software/readers, and

|

|

(b)

|

network approved encrypted PIN pad ("EPP") devices, installed on all ATMs and debit terminals:

thereby providing the ability to accept EMV chip card transactions. This has required and will also require further upgrading the Corporation’s Switch to process EMV chip card transactions, and adding additional encryption methods to Corporations managed ATMs and Debit terminals, Triple DES Encryption.

|

The Corporation’s understanding of the deadlines mandated by Interac and MasterCard for conversion of ATMs and debit terminals (i.e. to read the EMV microchip on a card rather than a magnetic stripe) are as follows:

|

(a)

|

50% of all ATMs must be upgraded with an EMV certified chip pin entry device by December 31, 2011 and 100% of ATMs must be upgraded by December 31, 2012;

|

|

(b)

|

35% of debit terminals must be upgraded with an EMV certified chip pin entry device by December 31, 2010, 60% must be converted by December 31, 2012, and 100% must be upgraded by December 31, 2015.

|

VISA's rule changes do not require a switch to the new technology by any particular date. However, both MasterCard and VISA rules provide that after March 31, 2011, certain liabilities (i.e. in respect of transaction errors or frauds) will be reallocated to industry participants who are still accessing the MasterCard and VISA networks using non-upgraded equipment, cards or software.

In addition to the security upgrades to ATM and Debit Terminals, in order to access Interac, cards (i.e. the debit cards issued by financial institutions) must be upgraded (i.e. reissued) to have EMV chips installed: 65% by December 31 2011 and 100% by December 31, 2012.

15

The result of non-compliance can include penalties, fines, sanctions and contractual penalties by the applicable Network(s) and ultimately disconnection of the ATM and Debit Terminal device or card from the Network for failure to comply by the end dates. The Corporation will be investing maintenance capital and upgrading its IT department to meet these upgrade deadlines. The Corporation’s customers who own their own equipment are encouraged to make the necessary changes to their equipment and in some cases the Corporation has the contractual right to make the necessary changes for the customer (and charge the customer for the cost of the change).

The Company and/or its subsidiaries are in compliance with EMV requirements.

Note 11 – Related Party transactions

Investment, at cost:

In October 2010, E-Debit decided to sell 41 common shares (41%) of the issued and outstanding shares held in its wholly owned subsidiary, 1105725 Alberta Ltd. o/a Personal Financial Solutions (PFS) at $1.00 per share. The common shares were sold to a number company that is controlled by an officer of E-Debit. The purchaser agrees that the current outstanding advances made to the company by E-Debit will remain outstanding and owed by the related party to E-Debit. As a result of the sale transaction, E-Debit remains a 10% shareholder in Personal Financial Solutions. E-Debit did not restate its financial statements to deconsolidate the PFS subsidiary, as PFS’s balances are immaterial to E-Debit’s consolidated financial statements. PFS has had no active business activities for the last four years. PFS had total assets and an accumulated deficit of $497 and $37,826, respectively, at December 31, 2010.

The 10% or $10 interest in Personal Financial Solutions is reflected in the accompanying consolidated balance sheet as investment, at cost.

In May 2011, E-Debit decided to sell 90 common shares (90%) of the issued and outstanding shares held in its wholly owned subsidiary, Cash Direct Financial Services Ltd. (CDF) at $1.00 per share. The common shares were sold to a number company that is controlled by the president of E-Debit. The purchaser agrees that the current outstanding advances made to the company by E-Debit will remain outstanding and owed by the related party to E-Debit. As a result of the sale transaction, E-Debit remains a 10% shareholder in Cash Direct Financial Services. E-Debit did not restate its financial statements to deconsolidate the CDF subsidiary, as CDF’s balances are immaterial to E-Debit’s consolidated financial statements. CDF has had no active business activities for the last two years. CDF had total assets and an accumulated deficit of $475 and $15,145, respectively, at April 30, 2011.

The 10% or $10 interest in Cash Direct Financial Services is reflected in the accompanying consolidated balance sheet as investment, at cost.

Other receivable – related parties:

The other receivable – related parties was from the sale transaction of 41% of the subsidiary 1105725 Alberta Ltd. o/s Personal Financial Solutions (PFS) in October 2010 and sale transaction of 90% of the subsidiary Cash Direct Financial Services Ltd. (CDF) in May 2011, and sale transactions to E-Debit’s directors.

The purpose of the sale of the subsidiaries was to save administration and audit costs to E-Debit since PFS and CDF have had no active business activities for the last four years. As of December 31, 2011 and September 30, 2012, the Company setup as allowance for doubtful collections of $51,386 and $53,469 for the related parties’ receivables as the repayment of the receivables was unknown.

The following table summarizes the Company’s others receivable to related parties transactions as of September 30, 2012 and December 31, 2011:

|

2012

|

2011

|

|||||||

|

1105725 Alberta Ltd. o/a

Personal Financial Solutions

|

$

|

40,635

|

$

|

39,127

|

||||

| Cash Direct Financial Services Ltd. | 12,834 | 12,259 | ||||||

| Trans Amored Canada | 4,580 | - | ||||||

|

Accounts receivable – directors

|

|

5,987

|

|

6,917

|

||||

|

|

$

|

64,036

|

$

|

58,303

|

||||

| Less: Allowance for doubtful accounts | (53,469 | ) | (51,386 | ) | ||||

| $ | 10,567 | $ | 6,917 | |||||

The current outstanding advances are reflected in the accompanying consolidated balance sheet as other receivable – related parties and totaled $10,567 and $6,917, respectively, at September 30, 2012 and December 31, 2011.

16

Deposit – related party:

The deposit – related party consists of an amount due from a contractor, Trans Armored Canada (TAC). The deposit carries no interest rate, and requires no monthly payments. The purpose of this deposit is to supply vault cash to E-Debit’s wholly owned subsidiary Vencash Payment Solutions Inc. (VPSI)’s customer-owned ATM equipment and site locations. The Company earns revenues from surcharge transactions generated from these ATMs.

VPSI supplies vault cash to these site locations because its customers do not have sufficient vault cash for these site locations. VPSI has subcontracted TAC to deliver vault cash to these site locations. TAC is accountable for the rotation of the cash. The deposit is receivable on demand.

Presently, the Company’s President and Chief Executive Officer sits as a member of the board of directors which represents 50% of TAC’s board of directors and the Company has the option to purchase 20% ownership in TAC.

On April 30, 2012 the Company concluded the sale of a portion of the Company’s eastern Canada ATMs estate to an arms-length investor. As a result, VPSI is no longer required to supply vault cash to its customer-owned ATM equipment and site locations and the deposit is to be returned to VPSI.

In May 2012, the Company and TAC mutually agreed to offset the full amount of deposit against the accounts payable owed to TAC.

The following table summarizes the Company’s deposit - related party transactions as of September 30, 2012 and December 31, 2011:

| 2012 | 2011 | |||||||

| Trans Armored Canada | - | $ | 156,668 | |||||

| Less: Allowance for doubtful accounts | - | - | ||||||

| - | $ | 156,668 | ||||||

The current outstanding deposit is reflected in the accompanying consolidated balance sheet as deposit – related party and totaled $0 and $156,668, respectively, at September 30, 2012 and December 31, 2011. The decrease in the full amount of deposit was primarily caused by the offsetting to payables in May 2012.

Indebtedness to related parties:

The Company expensed $24,779 ($24,675 CDN) during the third quarter of 2012 for consulting and management services to an affiliated company that is controlled by the Company’s president. This expense is reflected in the accompanying consolidated Statements of Operations as a Consulting fees.

In February 2011, the Company and its subsidiary, Westsphere Systems Inc., jointly signed the General Security Agreement (GSA) for the current debts owed to related parties and shareholders. The Company has requested that the related parties and shareholders individually or collectively advance loans up to one million five hundred thousand ($1,500,000) dollars in Canadian Funds to the Company. The terms of loans are “On Demand” with initial thirty-six months (36) terms which can be renewed from the date initial funds were advanced. The interest rate is Eight (8%) percent annually calculated and paid quarterly. Under the GSA, these debts are collateralized by the Company’s Accounts Receivables, Inventory, Equipment, Intangibles, Leasehold, Real and Immovable Property, and Proceeds.

17

In December 2011, the Company and its subsidiaries jointly and severally, signed a General Security Agreement (GSA) as well as loan agreements related to the loan from an arms-length investor for $200,000 CDN. As a result the aforementioned GSA dated February 2011 was cancelled in order that this new loan and GSA could be filed in priority to other loans advanced to the Company by related parties.

Upon completion of the first party claim related to the December loan and GSA the Company and its subsidiaries jointly and severally signed a GSA for the current debts owed to related parties and shareholders. The Company has requested that the related parties and shareholders individually or collectively advance loans up to one million seven hundred and fifty thousand ($1,750,000) dollars in Canadian Funds ($1,779,631 USD) to the Company. The terms of loans are “On Demand” with initial thirty-six months (36) terms which can be renewed from the date initial funds were advanced. The interest rate is Eight (8%) percent annually calculated and paid quarterly. Under the GSA, these debts are collateralized by the Company’s Accounts Receivables, Inventory, Equipment, Intangibles, Leasehold, Real and Immovable Property, and Proceeds.

The total amount owed to related parties as of September 30, 2012 is 1,521,665. The remaining credit available to be drawn against related to this GSA and Line of Credit is $257,966.

The following table summarizes the Company’s indebtedness to related parties’ transactions as at September 30, 2012:

|

Payable to:

|

Amount

|

Terms/Maturities

|

Interest Rate

|

|||

|

A loan advanced from E-Debit’s President for working capital.

|

$ | 109,985 |

Demand loans

|

8% per annum

|

||

|

A loan advanced from an affiliated company that is controlled by E-Debit’s President for working capital.

|

769,543 |

Demand loans

|

8% per annum

|

|||

|

A loan advanced from E-Debit’s vice President for working capital.

|

7,503 |

Demand loans

|

8% per annum

|

|||

|

A loan advanced from E-Debit’s officers for working capital.

|

7,665 |

Demand loans

|

8% per annum

|

|||

|

A loan advanced from E-Debit’s directors for working capital.

|

86,318 |

Demand loans

|

8% per annum

|

|||

|

A loan advanced from an affiliated company that is controlled by E-Debit’s director for working capital.

|

164,687 |

Demand loans

|

No interest

|

|||

|

Officers’ and Directors’ bonuses payable carried forward from year 2002

|

34,008 |

Demand loans

|

No interest

|

|||

|

A loan advanced from an affiliated company that is controlled by E-Debit’s President for working capital.

|

45,763 |

Demand loans

|

No interest

|

|||

|

Total

|

$ | 1,225,472 | ||||

The indebtedness to related parties consists of loans that are payable on demand by the related parties. The interest rate is Eight (8%) percent annually calculated and paid quarterly attached to the related party loans. There is no interest attached to a loan advanced from E-Debit’s director of $164,687, the Officers’ and Directors’ bonuses payable carried forward from year 2002 of $34,008, and the loan advanced from an affiliated company that is controlled by E-Debit’s President for working capital of $45,763. The above obligations are reflected in the accompanying consolidated balance sheet as indebtedness to related parties.

18

Note 12 – Shareholder loans

In December 2011, the Company and its subsidiaries jointly and severally signed the General Security Agreement (GSA) for the current debts owed to related parties and shareholders. The Company has requested that the related parties and shareholders individually or collectively advance loans up to one million seven hundred and fifty thousand ($1,750,000) dollars in Canadian Funds to the Company. The terms of loans are “On Demand” with initial thirty-six months (36) terms which can be renewed from the date initial funds were advanced. The interest rate is Eight (8%) percent annually calculated and paid quarterly. Under the GSA, these debts are collateralized by the Company’s Accounts Receivables, Inventory, Equipment, Intangibles, Leasehold, Real and Immovable Property, and Proceeds.

The following table summarizes the Company’s shareholder loans transactions as at September 30, 2012:

|

Payable to:

|

Amount

|

Terms/Maturities

|

Interest Rate

|

|||

|

A loan advanced from E-Debit’s vice President for working capital.

|

55,932 |

Demand loans

|

8% per annum

|

|||

|

A loan advanced from E-Debit’s directors for working capital.

|

144,160 |

Demand loans

|

8% per annum

|

|||

|

A loan advanced from E-Debit’s vice President for working capital.

|

45,253 |

Demand loans

|

12% per annum

|

|||

|

A loan advanced from E-Debit’s shareholder for working capital.

|

50,848 |

Demand loans

|

9% per annum

|

|||

|

Total

|

$ | 296,193 |

|

|||

E-Debit’s shareholder loans related to cash advanced from E-Debit’s vice president total $55,932 and the directors total $144,160 have an interest rate of 8% per annum calculated and paid quarterly with no specific terms of repayment. The remaining balance of shareholder loans totaling $96,101 consist of a loan advance from E-Debit’s vice president totaling $45,253 has an interest rate of 12% per annum with no specific terms of repayment, and a loan advance from a shareholder of $50,848 has an interest rate of 9% per annum with no specific terms of repayment. The above obligations are reflected in the accompanying consolidated balance sheet as shareholder loans.

Note 13 – Common and Preferred Stock

In May 2012, the Company Board of Directors has authorized the holders of its Common Stock the right to convert their Common Stock to Series “A” Preferred Shares of the Corporation commencing the 1st of June 2012 and ending on the 30th of November 2012. The Board of Directors reserved the right to extend the conversion period.

A contingency exists due to insufficient authorized preferred stock to convert all the common stock. The Company proposed to increase the number of authorized preferred stock to be voted on at the shareholder meeting in September 2012.

On September 18, 2012, the Company amended its articles of incorporation to increase its authorized capital to Ten Billion (10,000,000,000) shares of no par value common stock and Two Hundred Million (200,000,000) of no par value preferred stock.

The Corporation’s Series “A” Preferred Shares have the following conditions and rights attached:

|

(a)

|

Upon any sale, liquidation, dissolution or winding up of the Corporation, whether voluntary or involuntary, before any distribution or payment shall be made to the holders of any stock ranking junior to the Corporation’s Series “A” Preferred Stock, the holders of the Series “A” Preferred Stock shall be entitled to be paid out of the assets of the Corporation any dividends declared by the Board of Directors, in the form of stock, cash or otherwise, shall be distributed to the Corporation’s shareholders as follows: (a) ninety-five percent (95%) of such dividend shall be distributed to the holders of the Series “A” Preferred Shares on a pro rata basis; and (b) the remaining five (5%) shall be equally distributed to any holder of the Corporations Stock including Series “A” Preferred shareholders, on a pro rata basis.

|

19

|

(b)

|

In the case of a sale of any of the Corporation's business operations or in the event of a wind up or a liquidation of the Corporation's assets, the remaining cash to be distributed to the shareholders shall be distributed on the same basis as described in paragraph (a) above.

|

|

(c)

|

The Board of Directors will determine the amount of proceeds to be distributed from the sale of any of the Company's assets and will determine whether any dividend will be issued by the Corporation. The Board of Directors will determine the date that such dividend or distribution will be paid.

|

|

(d)

|

During the period commencing on June 1, 2012 and concluding on November 30, 2012, each holder of shares of common stock shall have the right to surrender their shares of common stock in exchange for shares of preferred stock on a basis of 1:1. Each shareholder shall exercise this right by delivering to the Corporation or the Corporation’s transfer agent the certificates representing such shareholder’s shares of common stock, duly endorsed with appropriate signature guarantees affixed thereto, on or before the date determined above in this subsection (d).

|

|

(e)

|

Each share of Series “A” Preferred stock shall have voting rights of twenty votes per share for any election or other vote placed before the shareholders of the Company.

|

|

(f)

|

Upon conversion the Board of Directors shall exercise the right to vote the preferred shares at any duly called meeting of the shareholders in the same manner as previously issued preferred shares.

|

|

(g)

|

Series “A” Preferred Stock are anti-dilutive to reverse splits in relation to the voting rights of the Corporation’s Series “A” Preferred Stock, and therefore in the case of a reverse split, the voting rights of the Series “A” Preferred Stock after the reverse split shall be equal to the ratio established prior to the reverse split. The voting rights of Series “A” Preferred Stock, however, would increase proportionately in the case of forward splits, and may not be diluted by a reverse split following a forward split.

|

|

(h)

|

Excepting for Section (g) above, a consolidation or split of one class of the Corporation’s stock the Board of Directors shall determine the effect on any other class of shares.

|

|

(i)

|

Upon conversion of a common share to a preferred share, the preferred shareholder will have the right to convert such preferred share to share of common stock upon delivery of 21 days written notice to the Corporation, at the closing trading price on the date that notice is given for the conversion per share payable to the Corporation.

|

|

(j)

|

Upon receipt of notice of the request to convert from preferred share to common stock, share certificates will be issued with the following share trading restrictions. 1/3 of the total shares to be converted will be restricted from trading for a period of 1 months from the date of conversion; 1/3 of the total shares to be converted will be restricted from trading for a period of 3 months from the date of conversion; and 1/3 of the total shares to be converted will be restricted from trading for a period of 6 months from the date of conversion.

|

20

On August 10, 2012, the Board of Directors authorized all holders of the Corporation’s outstanding indebtedness by way of loan agreements, promissory notes or other security instruments to convert their debt to common stock of the Corporation at a conversion price which would have been the average of the previous 5 day closing trading price of the Corporation’s stock currently listed on the OTC QB under trading symbol “WSHE” or $0.001 per share whichever is greater at the time the Convertible Note Holders would have notified the Corporation in writing of its request to convert.

The Company’s Board of Directors would have had the right at its sole discretion and determination to obtain from the converting note-holder or its authorized assigns an irrevocable proxy to vote the converted common stock related to the conversion at any duly constituted meeting of the shareholders while the debt holder or its authorized assigns held an interest in the common stock.

The Company’s Board of Directors also resolved that the common stock issued as a result of any conversion of debt by way of the issued Convertible Note would not qualify for conversion to the Corporation’s preferred share at the time of conversion or any time in the future and request for conversion from common stock to preferred is prohibited and will be rejected.

On October 10, 2012, the Board of Directors amended the August 10, 2012 Directors resolution regarding the issuance of convertible notes. The Board determined that in addition to the terms and conditions as set out in the Debt Settlement Resolution, any debt settlement commencing after the 10th day of October, 2012 must be approved by the President of the Corporation and authorized by a majority of the Board of Directors of the Corporation to become effective. This resolution invites the debt holders to discuss the option to convert their debt into equity but the Company has no obligation to do so and the debt holder have no contractual right to make any conversion. The Company has the right to accept or reject the request to convert by the debt holders on a case by case basis. The terms and conditions of any agreed to conversion will be disclosed in the appropriate SEC filings.

On August 15, 2012, two of the creditors of $185,460 and $50,000 debt (as further discussed below) exercised their convertible notes totaling of $235,460 for 235,460,000 at $0.001 per share, being the greater of the previous five day average closing trading price. These shares will be restricted for six (6) months until February 15, 2013 pursuant to rule 144 of the Securities and Exchange Commission.

The Company issued 185,460,000 shares of common stock to a creditor in conversion of $185,460 ($185,460 CDN), of convertible debt at the rate of $0.001 per share, being the greater of the previous five day average closing trading price. These shares will be restricted for six (6) months until February 15, 2013. The security holder has assigned an irrevocable proxy to vote to the Company Board of Directors. This proxy shall not be revocable until the transfer of the title and ownership to the shares from the record holder to an arm’s length non related third party.

The Company issued 50,000,000 shares of common stock to a creditor in conversion of $50,000 ($50,000 CDN), of convertible debt at the rate of $0.001 per share, being the greater of the previous five day average closing trading price. These shares will be restricted for six (6) months until February 15, 2013. The security holder has assigned an irrevocable proxy to vote to the Company Board of Directors. This proxy shall not be revocable until the transfer of the title and ownership to the shares from the record holder to an arm’s length non related third party.

Note 14 – Other Revenue

On April 30, 2012 the Company concluded the sale of a portion of the Company’s eastern Canada ATMs site location contracts to an investor for a total of $263,418 ($266,000 CDN). This sale transaction is included in the accompanying consolidated income statement as Gain on sale.

Note 15 – Subsequent Events

In September 2012 the Company entered into an agreement to sell a portion of the Company’s western Canada ATMs site location contracts to an investor for an amount to be determined. On October 25, 2012 the Company concluded the sales of a portion of the Company’s western Canada ATMs site location contracts to an investor for a total of $184,439 ($183,000 CDN).

On October 10, 2012, the Board of Directors amended the August 10, 2012 Directors resolution regarding the issuance of convertible notes. The Board determined that in addition to the terms and conditions as set out in the Debt Settlement Resolution, any debt settlement commencing after the 10th day of October, 2012 must be approved by the President of the Corporation and authorized by a majority of the Board of Directors of the Corporation to become effective. This resolution invites the debt holders to discuss the option to convert their debt into equity but the Company has no obligation to do so and the debt holder have no contractual right to make any conversion. The Company has the right to accept or reject the request to convert by the debt holders on a case by case basis. The terms and conditions of any agreed to conversion will be disclosed in the appropriate SEC filings.

21

Note 16 – Going Concern

The accompanying financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which contemplate continuation of the Company as a going concern. The Company has recurring net losses from operations, and had a working capital deficit and a stockholders’ deficit at September 30, 2012 and 2011. These conditions raise substantial doubt as to the Company's ability to continue as a going concern. These financial statements do not include any adjustments that might result from the outcome of this uncertainty. These financial statements do not include any adjustments relating to the recoverability and classification of recorded asset amounts, or amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern.

Management recognizes that the Company must generate additional resources to enable it to continue operations. Management intends to raise additional funds through debt financing and equity financing or through other means that it deems necessary, with a view to moving forward and sustaining a prolonged growth in its strategy phases. However, no assurance can be given that the Company will be successful in raising additional capital. Furthermore, management is in the process of negotiations with a third party investor to potentially purchase part or all of the Company’s ATM estate. In addition, there is no demand for payment on the accounts payable to related parties of $1,225,472 and shareholder loans of $296,193 as these liabilities are owed to internal officers and directors. Further, even if the Company raises additional capital, there can be no assurance that the Company will achieve profitability or positive cash flow. If management is unable to raise additional capital and expected significant revenues do not result in positive cash flow, the Company will not be able to meet its obligations and may have to cease operations.

22

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OR PLAN OF OPERATION

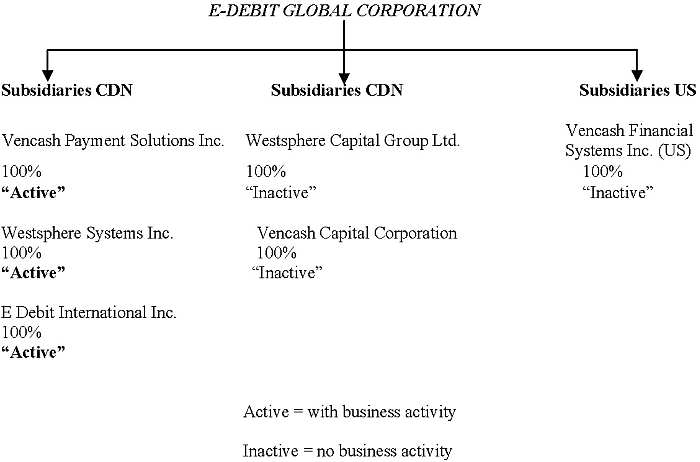

Current Corporate Structure – September 30, 2012

23

Plan of Operations

Results of Operations – Three Month Period

During the three (3) month period of operations ended September 30, 2012, E-Debit and its subsidiaries generated a net loss of $219,723, while a net loss of $241,465 was realized for the same period from the previous year. The decrease in net loss of $21,742 over the same period from the previous year was mainly caused by a decrease in other operating expense of $54,390, a decrease in consulting fees of $9,158, and a decrease in interest expense of $17,822. The decrease in net loss is partially offset against a decrease in gross profit of $14,051, an increase in travel, delivery and vehicle expenses of $17,878 and a decrease in other income of $28,832 over the same period from the previous year.

The decrease in other operating expense was mainly caused by the decrease in bad debt expense of $53,570.

The decrease in consulting fees was caused by a decrease adjustment in the monthly consulting fee contract effective May 2012.

The decrease in interest expense was due to a refund of $12,193 interest charged from a vendor.

The decrease in gross profit of $14,051 was primarily caused by a decrease in residual and interchange income of $301,230. The decrease is partially offset against a decrease in residual and interchange costs of $208,681 and a decrease in equipment and supplies of $64,069.

The decrease in residual and interchange income was mainly caused by the sale of a portion of the Company’s eastern Canada ATMs site location contracts in April 2012 and a decrease in processing of ABM transactions over the same period from the previous year.

On August 15, 2012 the Company and its subsidiaries jointly and severally entered into a Demand Loan Agreement and related GSA with an arms-length third party investor for a loan of $101,693 ($100,000 CDN) at a prime lending rate of Canadian Prime plus four (4%) percent. Under the GSA, this debt is collateralized by all of the Company’s assets. Upon demand the company has forty-five (45) days to repay the Demand Loan and interest. As of September 30, 2012, the balance is $102,588 ($100,880 CDN). This loan is included in the accompanying consolidated balance sheet as Loans payable.

On August 10, 2012, the Board of Directors authorized all holders of the Corporation’s outstanding indebtedness by way of loan agreements, promissory notes or other security instruments to convert their debt to common stock of the Corporation at a conversion price which would have been the average of the previous 5 day closing trading price of the Corporation’s stock currently listed on the OTC QB under trading symbol “WSHE” or $0.001 per share whichever is greater at the time the Convertible Note Holders would have notified the Corporation in writing of its request to convert.

The Company’s Board of Directors would have had the right at its sole discretion and determination to obtain from the converting note-holder or its authorized assigns an irrevocable proxy to vote the converted common stock related to the conversion at any duly constituted meeting of the shareholders while the debt holder or its authorized assigns held an interest in the common stock.

The Company’s Board of Directors also resolved that the common stock issued as a result of any conversion of debt by way of the issued Convertible Note would not qualify for conversion to the Corporation’s preferred share at the time of conversion or any time in the future and request for conversion from common stock to preferred is prohibited and will be rejected.

On October 10, 2012, the Board of Directors amended the August 10, 2012 Directors resolution regarding the issuance of convertible notes. The Board determined that in addition to the terms and conditions as set out in the Debt Settlement Resolution, any debt settlement commencing after the 10th day of October, 2012 must be approved by the President of the Corporation and authorized by a majority of the Board of Directors of the Corporation to become effective. This resolution invites the debt holders to discuss the option to convert their debt into equity but the Company has no obligation to do so and the debt holder have no contractual right to make any conversion. The Company has the right to accept or reject the request to convert by the debt holders on a case by case basis. The terms and conditions of any agreed to conversion will be disclosed in the appropriate SEC filings.

24

On August 15, 2012, two of the creditors of $185,460 and $50,000 debt (as further discussed below) exercised their convertible notes totaling of $235,460 for 235,460,000 at $0.001 per share, being the greater of the previous five day average closing trading price. These shares will be restricted for six (6) months until February 15, 2013 pursuant to rule 144 of the Securities and Exchange Commission.

The Company issued 185,460,000 shares of common stock to a creditor in conversion of $185,460 ($185,460 CDN), of convertible debt at the rate of $0.001 per share, being the greater of the previous five day average closing trading price. These shares will be restricted for six (6) months until February 15, 2013. The security holder has assigned an irrevocable proxy to vote to the Company Board of Directors. This proxy shall not be revocable until the transfer of the title and ownership to the shares from the record holder to an arm’s length non related third party.

The Company issued 50,000,000 shares of common stock to a creditor in conversion of $50,000 ($50,000 CDN), of convertible debt at the rate of $0.001 per share, being the greater of the previous five day average closing trading price. These shares will be restricted for six (6) months until February 15, 2013. The security holder has assigned an irrevocable proxy to vote to the Company Board of Directors. This proxy shall not be revocable until the transfer of the title and ownership to the shares from the record holder to an arm’s length non related third party.