Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - CHINA GENGSHENG MINERALS, INC. | exhibit31-1.htm |

| EX-32.1 - EXHIBIT 32.1 - CHINA GENGSHENG MINERALS, INC. | exhibit32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - CHINA GENGSHENG MINERALS, INC. | exhibit31-2.htm |

| EX-32.2 - EXHIBIT 32.2 - CHINA GENGSHENG MINERALS, INC. | exhibit32-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

20549

FORM 10-Q/A

(Amendment No.1)

(Mark one)

[ x ] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended: June 30, 2012

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______________to ________________

Commission File Number: 001-34649

CHINA GENGSHENG MINERALS,

INC.

(Exact Name of Registrant as Specified in Its

Charter)

| NEVADA | 91-0541437 |

| (State or Other jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

| CHINA GENGSHENG MINERALS, INC. | |

| No. 88 Gengsheng Road, Dayugou Town, Gongyi, Henan Province P.R. China | 451271 |

| (Address of Principal Executive Offices) | (Zip Code) |

(86) 371-64059863

(Registrant’s Telephone

Number, Including Area Code)

N/A

(Former Name, Former Address and Former

Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [ x ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [ x ] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one)

| Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [ ] | Smaller reporting company [ x ] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [ x ]

As of August 14, 2012, there were 26,803,044 shares of Common Stock of the Company, $0.001 par value, outstanding.

EXPLANATORY NOTE

This Amendment No. 1 on Form 10-Q/A (this “Amendment No. 1”) to the Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2012 (the “Quarterly Report”) of China GengSheng Minerals, Inc. (the “Company”) is being filed to include the following disclosure under the discussion of results of operations:

-

disclosure to separately quantify for each period presented the amount of the change in revenues and expenses that is due to foreign currency translations;

-

discussion on the restrictions on the net assets; and

-

disclosure concerning our accounts receivable and bills receivable.

Additionally, in this Amendment No.1, we also included currently dated certifications from the Company’s Principal Executive Officer and Principal Financial Officer as required by Section 302 of the Sarbanes-Oxley Act of 2002 and currently dated certifications from the Company’s Principal Executive Officer and Principal Financial Officer as required by Section 906 of the Sarbanes-Oxley Act of 2002.

Except as described above, no other changes have been made to the Quarterly Report, and this Amendment No. 1 does not amend or update any other information contained in the Quarterly Report.

Table of Contents

| Page | ||

| PART I - FINANCIAL INFORMATION | ||

| Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations. | 4 |

| PART II - OTHER INFORMATION | ||

| Item 6. | Exhibits. | 23 |

| SIGNATURES | 24 | |

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

Forward-Looking Statements:

The following discussion of the financial condition and results of operations should be read in conjunction with the consolidated financial statements and related notes thereto. The following discussion contains forward-looking statements. Unless the context requires otherwise, references to “we”, “us”, “our”, “the Registrant”, or the “Company” refer to China GengSheng Minerals, Inc. and its subsidiaries. The words or phrases “would be,” “will allow,” “expect to,” “intends to,” “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimate,” or similar expressions are intended to identify forward-looking statements. Such statements include those concerning our expected financial performance, our corporate strategy and operational plans. Actual results could differ materially from those projected in the forward-looking statements as a result of a number of risks and uncertainties, including: (a) those risks and uncertainties related to general economic conditions in China, including regulatory factors that may affect such economic conditions; (b) whether we are able to manage our planned growth efficiently and operate profitable operations, including whether our management will be able to identify, hire, train, retain, motivate and manage required personnel or that management will be able to successfully manage and exploit existing and potential market opportunities; (c) whether we are able to generate sufficient revenues or obtain financing to sustain and grow our operations; and (d) whether we are able to successfully fulfill our primary requirements for cash which are explained below under “Liquidity and Capital Resources.” Unless otherwise required by applicable law, we do not undertake, and we specifically disclaim any obligation, to update any forward-looking statements to reflect occurrences, developments, unanticipated events or circumstances after the date of such statement.

Conventions

In this Form 10-Q/A, unless indicated otherwise, references to:

-

“China GengSheng Minerals”, “we”, “us”, “our”, the “Registrant” or the “Company” refer to the combined business of China GengSheng Minerals, Inc., a Nevada corporation (formerly, China Minerals Technologies, Inc.) and its wholly-owned BVI subsidiary, GengSheng International Corporation, or GengSheng International, and GengSheng International’s wholly-owned Chinese subsidiary, Zhengzhou Duesail Fracture Proppant Co. Ltd., or Duesail, and Duesail’s wholly-owned subsidiary, Henan Yuxing Proppant Co., Ltd., or Yuxing and GengSheng International’s wholly-owned Chinese subsidiary, Henan GengSheng Refractories Co., Ltd., or Refractories, and Refractories’s majority-owned subsidiary, Henan GengSheng High-Temperature Materials Co., Ltd., or High Temperature, and Refractories’s wholly-owned subsidiary, Henan GengSheng Micronized Powder Materials Co., Ltd., or Micronized, and Henan GengSheng's wholly-owned subsidiary, GengSheng Shunda New Materials Co., Ltd, Southeast Prefecture, Guizhou or Shunda;

-

“Powersmart” or “GengSheng International” refer to GengSheng International Corporation, a BVI company (formerly, Powersmart Holdings Limited) that is wholly-owned by China GengSheng Minerals;

-

“Securities Act” refers to the Securities Act of 1933, as amended, and “Exchange Act” refer to Securities Exchange Act of 1934, as amended;

-

“China” and “PRC” refer to the People's Republic of China, and “BVI” refers to the British Virgin Islands;

-

“RMB” refers to Renminbi, the legal currency of China; and

-

“U.S. dollar,” “$” and “US$” refers to the legal currency of the United States. For all U.S. dollar amounts reported, the dollar amount has been calculated on the basis that RMB1 = $0.1574 for its December 31, 2011 audited balance sheet, and RMB1 = $0.1584 for its June 30, 2012 unaudited balance sheet, which were determined based on the currency conversion rate at the end of each respective period. The conversion rates of RMB1 = $0.1584 is used for the condensed consolidated statement of income and comprehensive income and consolidated statement of cash flows for the second quarter of 2012, and RMB1 = $0.15272 is used for the condensed consolidated statement of income and comprehensive income and consolidated statement of cash flows for the second quarter of 2011; both of which were based on the average currency conversion rate for each respective quarter.

Overview of Company

We are a Nevada holding company operating in the materials technology industry through our subsidiaries in China. We develop, manufacture and sell a broad range of mineral-based, heat-resistant products capable of withstanding high temperatures, saving energy and boosting productivity in industries such as steel and oil. Our products include refractory products, industrial ceramics, fracture proppants and fine precision abrasives.

Currently, we conduct our operations in China through our wholly owned subsidiaries, Henan GengSheng Refractories Co., Ltd. (“Refractories”), Zhengzhou Duesail Fracture Proppant Co., Ltd. (“Duesail”), Henan GengSheng Micronized Powder Materials Co., Ltd. (“Micronized”), Guizhou Southeast Prefecture GengSheng New Materials Co., Ltd. (“Prefecture”) and Henan Yuxing Proppant Co., Ltd., (“Yuxing”), and through our majority owned subsidiary, Henan GengSheng High-Temperature Materials Co., Ltd. (“High-Temperature”). Through our wholly owned BVI subsidiary, GengSheng International, and its wholly owned Chinese subsidiary, Refractories, which has an annual production capacity of approximately 127,000 tons, we manufacture refractories products. We manufacture fracture proppant products through Duesail, which has an annual production capacity of approximately 66,000 tons, and Yuxing, which has designed annual production capacity of approximately 60,000 tons. We manufacture fine precision abrasives products through Micronized, which has designed annual production capacity of approximately 22,000 tons. Through our majority owned subsidiary, High-Temperature, which has an annual production capacity of approximately 150,000 units, we manufacture industrial and functional ceramic products.

4

We sell our products to over 170 customers in the iron, steel, oil, glass, cement, aluminum, chemical and solar industries located in China and other countries in Asia, Europe and North America. Our refractory customers are companies in the steel, iron, petroleum, chemical, coal, glass and mining industries. Our fracture proppant products are sold to oil and gas companies. Our industrial ceramics are used in the utilities and petrochemical industries. Our fine precision abrasives are marketed to solar companies and optical equipment manufacturers. Our largest customers, measured by percentage of our revenue, mainly operate in the steel industry and oil industry. Currently, most of our revenues are derived from the sale of our monolithic refractory products and fracture proppants products to customers in China.

Our principal executive offices are located at No. 88 Gengsheng Road, Dayugou Town, Gongyi, Henan, People’s Republic of China 451271 and our telephone number is (86) 371-6405-9863.

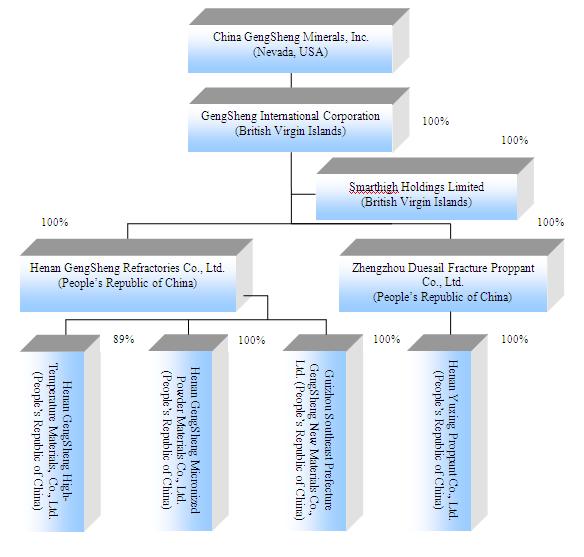

Corporate Structure

We conduct our operations in China through our wholly owned subsidiaries Refractories, Duesail, Yuxing, Micronized and Prefecture and through our majority owned subsidiary, High-Temperature.

The following chart reflects our organizational structure as of the date of this report.

5

Corporate History

We were originally incorporated under the laws of the State of Washington, on November 13, 1947, under the name Silver Mountain Mining Company. From our inception until 2001, we operated various unpatented mining claims and deeded mineral rights in the State of Washington, but we abandoned these operations entirely by 2001. On August 15, 2006, we changed our domicile from Washington to Nevada when we merged with and into Point Acquisition Corporation, a Nevada corporation. From about 2001 until our reverse acquisition of Powersmart on April 25, 2007, which is discussed in the next section entitled "Acquisition of Powersmart and Related Financing", we were a blank check company and had no active business operations. On June 11, 2007, we changed our corporate name from "Point Acquisition Corporation" to "China Minerals Technologies, Inc." and subsequently changed our name again to "China GengSheng Minerals, Inc." on July 26, 2007.

Acquisition of Powersmart and Related Financing

On April 25, 2007, we completed a reverse acquisition transaction through a share exchange with Powersmart Holdings Limited whereby we issued to the sole shareholder of Powersmart Holdings Limited, Shunqing Zhang, 16,887,815 shares of China GengSheng Minerals, Inc. common stock, in exchange for all of the issued and outstanding capital stock of Powersmart Holdings Limited. By this transaction, Powersmart Holdings Limited became our wholly owned subsidiary and Mr. Zhang became our controlling stockholder.

On April 25, 2007, we also completed a private placement financing transaction pursuant to which we issued and sold 5,347,594 shares of our common stock to certain accredited investors for $10 million in gross proceeds. In connection with this private placement, we paid a fee of $683,618 to Brean Murray Carret & Co., LL, or Brean Murray, and Civilian Capital, Inc. for services as placement agents for the private placement. We also issued to Brean Murray Carret & Co., LLC and Civilian Capital, Inc. warrants for the purchase of 374,331 shares of our common stock in the aggregate. The warrants are immediately exercisable, have piggyback registration rights and have a three-year term, expiring on April 26, 2010. On March 10, 2010, Brean Murray Carret & Co., LLC exercised the warrant cashlessly, which was converted to 108,349 shares of the Corporation’s common stock, and on April 21, 2010, Civilian Capital, Inc. exercised the warrant cashlessly, which was converted to 27,869 shares of the Corporation’s common stock.

Also, on April 25, 2007, our majority stockholder, Shunqing Zhang, entered into an escrow agreement with the private placement investors, pursuant to which, Mr. Zhang agreed to deposit in an escrow account a total of 2,673,796 shares of the Company's common stock owned by him, to be held for the benefit of the investors. Mr. Zhang agreed that if the Company did not attain a minimum after-tax net income threshold of $8,200,000 for the fiscal year ended December 31, 2007 and $13,500,000 for the fiscal year ended December 31, 2008, the escrow agent may deliver his escrowed shares to the investors, based upon a pre-defined formula agreed to between the investors and Mr. Zhang. However, if the after-tax net income threshold is met, the shares in escrow will be returned to Mr. Zhang. In addition, on April 25, 2007, Mr. Zhang entered into a similar escrow agreement with HFG International, Limited. Under such agreement, Mr. Zhang placed into escrow a total of 638,338 shares of the Company's common stock to cover the same minimum net income thresholds as described above with respect to the investor make-good. Similarly, if the thresholds were not achieved in either year, the escrow agent must release certain amounts of the make-good shares that were put into escrow. We met the after-tax net income threshold of $8,200,000 for the fiscal year ended December 31, 2007 and the pro rata shares in escrow were returned to Mr. Zhang, while we did not meet the after-tax net income threshold of $13,500,000 for the fiscal year ended December 31, 2008, and the pro rata shares in escrow were transferred to the investors on March 8, 2010.

On January 4, 2011, the Company and certain institutional investors entered into a securities purchase agreement pursuant to which the Company sold to such investors an aggregate of 2,500,000 shares of common stock at a price of $4.00 per share for aggregate gross proceeds to the Company of $10,000,000. Each purchaser received warrants, exercisable for $4.00 per share for the six-month period beginning July 10, 2011 and ending January 11, 2012, to purchase 40% of the shares of common stock purchased by the purchaser in the offering. The net proceeds from the offering was approximately $9,350,000. The Company paid an aggregate fee equal to 5.5% of the gross proceeds received to Rodman & Renshaw, LLC for services as placement agent. The shares of common stock, warrants to purchase common stock and shares of common stock issuable upon exercise of the investor warrants were issued pursuant to a prospectus supplement dated as of January 10, 2011, which was filed with the Securities and Exchange Commission in connection with a takedown from the Company’s shelf registration statement on Form S-3 (File No. 333-165486), which became effective on April 28, 2010, and the base prospectus dated as of April 28, 2010 contained in such registration statement.

6

Our Products

The following table set forth sales information about our product mix in each of the second quarter of 2012 and 2011, and the first six months of 2012 and 2011.

(All amounts, other than percentages, in thousands of U.S. dollars)

| Three Months Ended June 30 | Six Months Ended June 30 | |||||||||||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||||||||||

| Percentage | Percentage | Percentage | Percentage | |||||||||||||||||||||

| Revenue | of net | Revenue | of net | Revenue | of net | Revenue | of net | |||||||||||||||||

| revenues | revenues | revenues | revenues | |||||||||||||||||||||

| Refractories | $ | 11,616 | 59.2% | $ | 12,545 | 61.4% | $ | 21,558 | 64.7% | $ | 22,480 | 61.4% | ||||||||||||

| Industrial Ceramics | 529 | 2.7% | 492 | 2.4% | 861 | 2.5% | 722 | 2.0% | ||||||||||||||||

| Fracture Proppants | 4,221 | 21.5% | 5,936 | 29.0% | 5,219 | 15.7% | 11,136 | 30.4% | ||||||||||||||||

| Fine Precision Abrasive | 3,254 | 16.6% | 1,463 | 7.2% | 5,693 | 17.1% | 2,282 | 6.2% | ||||||||||||||||

| $ | 19,620 | 100.0% | $ | 20,436 | 100.0% | $ | 33,331 | 100.0% | $ | 36,620 | 100.0% | |||||||||||||

Refractories

Our largest product segment is the refractories segment, which accounted for approximately 59.2% of total revenue in the second quarter of 2012. Our refractory products have high-temperature resistant qualities and can function under thermal stress that is common in many heavy industrial production environments. Because of their unique high-temperature resistant qualities, the refractory products are used as linings and key components in many industrial furnaces, such as steel production furnaces, ladles, vessels, and other high-temperature processing machines that must operate at high temperatures for a long period of time without interruption. The majority of our customers are in the iron, steel, cement, chemical, coal, glass, petro-chemical and nonferrous industries.

We provide a customized solution for each order of our monolithic refractory materials based on customer-specific formulas. Upon delivery to customers, the monolithic materials are applied to the inner surfaces of our customers’ furnaces, ladles or other vessels to improve the productivity of that equipment. The product benefits our customers as it lowers the overall cost of production and improves financial performance. The reasons that the monolithic materials can help our customers improve productivity, lower production costs and achieve stronger financial performance include the following: (i) monolithic refractory castables can be cast into complex shapes which are unavailable or difficult to achieve by alternative products such as shaped bricks; (ii) monolithic refractory linings can be repaired, and in some cases, even reinstalled, without furnace cool-down periods or steel-production interruptions, and therefore improve the steel makers’ productivity; (iii) monolithic refractories can form an integral surface without joints, enhancing resistance to penetration, impact and erosion, and thereby improving the equipment’s operational safety and extending their useful service lives; (iv) monolithic refractories can be installed by specialty equipment either automatically or manually, thus saving construction and maintenance time as well as costs; and (v) monolithic refractories can be customized to specific requirements by adjusting individual formulas without the need to change batches of shaped bricks, which is a costly procedure. Our refractory products and their features are described as follows:

- Castable, coating, and dry mix materials. Offerings within this product line are used as linings in containers such as a tundish used for pouring molten metal into a mold. The primary advantages of these products are speed and ease of installation for heat treatment.

- Low-cement and non-cement castables. Our low-cement and non-cement castable products are typically used in reheating furnaces for producing steel. These castable products are highly durable and can last up to five years.

- Pre-cast roofs. These products are usually used as a component of electric arc furnaces. They are highly durable, and in the case of our corundum-based, pre-cast roof, products can endure approximately 160 to 220 complete operations of furnace heating.

We also have a production line for pressed bricks, which is a type of “shaped” refractory, for steel production. The annual designed production capacity of our shaped refractory products is approximately 15,000 metric tons.

Finally, we provide a full-service option to our steel customers, which include refractory product installation, testing, maintenance, repair and replacement. Refractory product sales are often enhanced by our on-site installation and technical support personnel. Our installation services include applying refractory materials to the walls of steel-making furnaces and other high temperature vessels to maintain and extend their lives. Our technical service staff assure that our customers can achieve their desired productivity objectives. They also measure the refractory wear at our customer sites to improve the quality of maintenance and overall performance of our customers’ equipment. Full-service customers contributed approximately 35.8% of the Company’s total sales in the first six months of 2012, compared with 32.4% in the same period of 2011. We believe that these services, together with our refractory products, provide us a strategic advantage.

7

Industrial Ceramics

Industrial Ceramics accounted for approximately 2.7% of the total revenue in the second quarter of 2012. Our industrial ceramic products, including abrasive balls and tiles, valves, electronic ceramics and structural ceramics, are components for a variety of end products such as fuses, vacuum interrupters, electrical components, mud slurry pumps, and high-pressure pumps. Such end use products are used in the electric power, electronic component, industrial pump, and metallurgy industries.

Fracture Proppants

Fracture Proppants accounted for approximately 21.5% of the total revenue in the second quarter of 2012. Our fracture proppant products are very fine ball-like pellets, used to reach pockets of oil and natural gas deposits that are trapped in the fractures under the ground. Oil drillers inject the pellets into those fractures, squeezing out the trapped oil or natural gas, which leads to higher yield. Our fracture proppant products are available in several different particle sizes (measured in millimeters). They are typically used to extract crude oil and natural gas, which increases the productivity of crude oil and natural gas wells. These products are highly resistant to pressure. In October 2007, our fracture proppant products were recognized by China National Petroleum Corporation (the “CNPC”), China Petroleum & Chemical Corporation (the “Sinopec”) and China National Offshore Oil Corporation (the “CNOOC”) as their supplier of fracture proppant products for their oil and gas-drilling operation.

Fine Precision Abrasives

Fine Precision Abrasives accounted for approximately 16.6% of our total revenue in the second quarter of 2012. Fine precision abrasives are used for producing a super-fine, super-consistent finish on certain products. A high-strength polyester backing provides a uniform base for a coating of micron-graded mineral particles that are uniformly dispersed for greater finishing efficiency. Our fine precision abrasives are made from silicon carbide (“SiC”). They are ultra-fine, high-strength pellets with uniform shape, and they are used for surface-polishing and slicing of precision instruments such as solar panels. Currently, the type of abrasives that we produce is in high demand among solar-energy companies. Solar energy companies use fine precision abrasives to cut silicon bars and to polish equipment surfaces so that they can be smooth and reflective. Our products can be utilized in a broad range of areas including machinery manufacturing, electronics, optical glass, architecture, industry development, semiconductor, silicon chip, plastic and lens.

Second Quarter of 2012 Summary

Our financial performance in the second quarter of 2012 is summarized as follows:

-

Sales revenue decreased by approximately $816,000, or 4.0%, to approximately $19.6 million for the second quarter of 2012, from approximately $20.4 million for the same period in 2011.

-

Gross profit decreased by approximately $2.2 million, or 42.7%, to approximately $3.1 million for the second quarter of 2012, from approximately $5.3 million for the same period in 2011. Gross profit margin was 15.6% for the second quarter of 2012, compared with 26.1% for the same period in 2011. The decrease in gross profit margin was largely attributed to the lower gross profit margin in our fine precision abrasives segment as sales of lower-grade products continued in the second quarter, the lower gross profit margin in fracture proppants segment as well as the rising costs of raw materials and energy in refractories segment. Net loss increased by approximately $3.5 million, to approximately $3.8 million for the second quarter of 2012, from a net loss of approximately $247,000 for the same period in 2011.

-

Our condensed consolidated balance sheet (unaudited) as of June 30, 2012 included current assets of approximately $136.9 million and total assets of approximately $178.9 million, with working capital of approximately $5.3 million.

Uncertainties that Affect our Financial Condition

Continued Industry Consolidation of Steel Makers Further Squeezed Our Profit in Refractories Segment

Although the crude steel output in China reached a new record of approximate 696 million metric tons in 2011, the steel industry still faces overcapacity and weak demand from both domestic and international market. In addition, the PRC government’s continued policy to squeeze out small to mid-sized steel makers reduced the overall demand for refractories. As refractories is our largest product segment and many of our customers are in the steel industry, the continued industry consolidation of steel makers have a deep impact on us and further squeezed our profit in the refractories segment.

8

Considerable Increase of Raw Material Prices and Decrease in Gross Profit Margin

In 2011, China saw its highest inflation rate in over 10 years. While the overall inflation started to ease in 2012, the increase in raw materials prices, labor costs and fuel and utilities costs continued to impact us. Also, in a fragmented market, hardly could the selling price of our products keep pace with the increase in raw materials prices on a timely basis.

Increase in Financing Costs Further Limited Our Ability to Expand Business

The unfavorable payment term offered by our customers in refractories segment and fine precision abrasives segment strained our working capital needs, and as a result significantly increased our financing costs, as banks charged higher interest rates when we discounted more bills receivables to meet our working capital needs.

Uncertainties Facing Our Fracture Proppants Segment

Starting from 2012, more and more Chinese manufacturers of fracture proppants products started to sell their products directly in the U.S. market. Since our sales of fracture proppants products in the U.S. market were mainly through wholesalers and distributors, the change in the market condition made it nearly impossible for us to continue sales in the U.S. market while still maintaining a reasonable profit margin. As a result, our sales in the U.S. market were discontinued temporarily in the first six months of 2012. We are currently looking at other alternatives to increase our sales of fracture proppants products, especially restore our profitable sales in the U.S. market; however, we cannot guarantee sales and gross profit margin in fracture proppants segment can maintain the level seen in 2011.

Deteriorating Market for Our Fine Precision Abrasives Segment

China’s solar industry is experiencing severe challenge with many large solar panel manufacturers struggling to survive. As a supplier of solar-energy companies, we are facing remarkable uncertainties in maintaining our current customers. If we cannot continue our sales of fine precision abrasives products to solar industry or have to reduce selling price significantly, our revenue will decline and we may need to discontinue our production.

Results of Operations

Comparison of Three-Month Periods ended June 30, 2012 and 2011

The following table summarizes the results of our operations during the three-month periods ended June 30, 2012 and 2011, and provides information regarding the dollar and percentage increase or (decrease) during the three-month periods ended June 30, 2012 and 2011.

(All amounts, other than percentages, in U.S. dollars)

| Three-Month Period | Three-Month Period | |||||||||||

| Ended June 30, 2012 | Ended June 30, 2011 | |||||||||||

| As a | As a | |||||||||||

| Dollars in | percentage of | Dollars in | percentage of | |||||||||

| Statement of operations data: | thousands | net revenues | thousands | net revenues | ||||||||

| Net Sales | 19,620 | 100.0% | 20,436 | 100.0% | ||||||||

| Cost of goods sold | 16,565 | 84.4% | 15,101 | 73.9% | ||||||||

| Gross profit | 3,055 | 15.6% | 5,335 | 26.1% | ||||||||

| Operating expenses | ||||||||||||

| General & administrative expenses | 1,937 | 9.9% | 1,630 | 8.0% | ||||||||

| Research and development expenses | 236 | 1.2% | 145 | 0.7% | ||||||||

| Selling expenses | 2,791 | 14.2% | 2,761 | 13.5% | ||||||||

| Total operating expenses | 4,964 | 25.3% | 4,536 | 22.2% | ||||||||

| (Loss) income from operations | (1,909 | ) | -9.7% | 799 | 3.9% | |||||||

| Government grant income | - | 0.0% | 17 | 0.1% | ||||||||

9

| Guarantee income | 148 | 0.7% | 123 | 0.6% | ||||||||

| Guarantee expenses | (108 | ) | -0.6% | (89 | ) | -0.4% | ||||||

| Equity in net loss of a non-consolidated affiliate | (9 | ) | 0.0% | - | 0.0% | |||||||

| Interest income | 186 | 0.9% | 63 | 0.3% | ||||||||

| Change in fair value of warranty liabilities | - | 0.0% | 650 | 3.2% | ||||||||

| Other income (expenses) | 38 | 0.2% | (34 | ) | -0.2% | |||||||

| Finance costs | (1,950 | ) | -9.9% | (1,571 | ) | -7.7% | ||||||

| (Loss) income before income taxes and noncontrolling interest | (3,604 | ) | -18.4% | (42 | ) | -0.2% | ||||||

| Income taxes | (202 | ) | -1.0% | (226 | ) | -1.1% | ||||||

| Noncontrolling interest | 12 | 0.1% | 21 | 0.1% | ||||||||

| Net loss attributable to Company’s common stockholders | (3,794 | ) | -19.3% | (247 | ) | -1.2% |

| Three-Month | Three-Month | Dollar ($) | Percentage | |||||||||

| Period Ended | Period Ended | Increase | Increase | |||||||||

| Dollars in thousands | June 30, 2012 | June 30, 2011 | (Decrease) | (Decrease) | ||||||||

| Net Sales | 19,620 | 20,436 | (816 | ) | -4.0% | |||||||

| Cost of goods sold | 16,565 | 15,101 | 1,464 | 9.7% | ||||||||

| Gross profit | 3,055 | 5,335 | (2,280 | ) | -42.7% | |||||||

| Operating expenses | ||||||||||||

| General & administrative expenses | 1,937 | 1,630 | 307 | 18.8% | ||||||||

| Research and development expenses | 236 | 145 | 91 | 62,8% | ||||||||

| Selling expenses | 2,791 | 2,761 | 30 | 1.1% | ||||||||

| Total operating expenses | 4,964 | 4,536 | 428 | 9.4% | ||||||||

| (Loss) income from operations | (1,909 | ) | 799 | (2,708 | ) | -339.0% | ||||||

| Government grant income | - | 17 | (17 | ) | -100.0% | |||||||

| Guarantee income | 148 | 123 | 25 | 20.3% | ||||||||

| Guarantee expenses | (108 | ) | (89 | ) | (19 | ) | 21.3% | |||||

| Equity in net loss of a non-consolidated affiliate | (9 | ) | - | (9 | ) | -100.0% | ||||||

| Interest income | 186 | 63 | 123 | 195.2% | ||||||||

| Change in fair value of warranty liabilities | - | 650 | (650 | ) | -100% | |||||||

| Other income (expenses) | 38 | (34 | ) | 72 | 211.8% | |||||||

| Finance costs | (1,950 | ) | (1,571 | ) | (379 | ) | 24.1% | |||||

| (Loss) income before income taxes and noncontrolling interest | (3,604 | ) | (42 | ) | (3,562 | ) | 8,481.0% | |||||

| Income taxes | (202 | ) | (226 | ) | 24 | -10.6% | ||||||

| Noncontrolling interest | 12 | 21 | (9 | ) | -42.9% | |||||||

| Net loss attributable to Company’s common stockholders | (3,794 | ) | (247 | ) | (3,547 | ) | 1,436.0% |

The average conversion rates between RMB and U.S. dollar used for the condensed consolidated statements of operations and comprehensive loss increased approximately 3.7% during the reporting period of 2012 compared with the reporting period of 2011. As substantially all of our revenues and most expenses are denominated in RMB, the appreciation in the value of RMB relative to the U.S. dollar affected our financial results reported in the U.S. dollar terms without giving effect to any underlying change in our business or results of operations.

Sales revenues. Sales revenues decreased approximately $816,000, or 4.0% to approximately $19.6 million for the three months ended June 30, 2012 from approximately $20.4 million in the same period of 2011. Excluding foreign currency translation, the revenue decreased approximately $1.5 million, or 7.2% compared with the same period of 2011. Our sales revenue is currently generated from sales of our mineral-based products, primarily our refractory products, fracture proppant products, fine precision abrasives products and industrial ceramic products. The decrease was mainly attributable to the decreased sales of our fracture proppant products.

In our refractory segment, we sold 22,842 metric tons of refractory products in the second quarter of 2012, compared with 27,686 metric tons sold in the same period of 2011. The revenue from our refractory products was approximately $11.6 million in the second quarter of 2012, compared with $12.5 million in the same period of 2011. Excluding foreign currency translation, the revenue decreased approximately $1.3 million, or 10.4% compared with the same period of 2011. The average selling price increased to $509 per metric ton compared with $452 per metric ton in the second quarter of 2011 and the price increase partially offset the impact of decrease in sales volume on our revenue. Excluding foreign currency translation, the average selling price increased to $491 per metric ton in the second quarter of 2012.

10

In our fracture proppant segment, we sold 16,030 metric tons of fracture proppant products in the second quarter of 2012, compared with 16,029 metric tons sold in the same period of 2011. Revenue was approximately $4.2 million in the second quarter of 2012, a decrease of 28.9% compared with approximately $5.9 million in the same period of 2011. Excluding foreign currency translation, the revenue decreased approximately $1.9 million, or 31.4% compared with the same period of 2011. Average selling price decreased to $263 per metric ton in the second quarter of 2012, compared with $373 per metric ton in the same period of 2011. Excluding foreign currency translation, the average selling price decreased to $254 per metric ton in the second quarter of 2012. The decrease in average selling price and revenue were primarily due to the increased sales in domestic market where the fracture proppant products are typically priced lower than in the U.S. market.

In our industrial ceramics segment, sales revenue was approximately $530,000 in the second quarter of 2012 compared with approximately $492,000 in the same period of 2011. Excluding foreign currency translation, the revenue was approximately $511,000.

In our fine precision abrasives segment, we realized sales of 1,172 ton in the second quarter of 2012, for revenue of approximately $3.3 million. Excluding foreign currency translation, the revenue was approximately $3.1 million. We sold 421 metric tons of fine precision abrasives products for approximately $1.5 million in the same period of 2011. The increase in sales revenue was primarily due to the increased sales to a major customer.

Cost of goods sold. Our cost of goods sold is primarily comprised of the cost of raw materials, components, labor and overhead. Our cost of goods sold increased approximately $1.5 million, or 9.7%, to approximately $16.6 million in the second quarter of 2012 from approximately $15.1 million in the same period of 2011. Excluding foreign currency translation, our cost of goods sold increased approximately $913,000, or 6.0% compared with the same period of 2011. As a percentage of net revenues, the cost of goods sold increased by 10.5% to 84.4% in the second quarter of 2012 from 73.9% in the same period of 2011. This increase was primarily due to the higher raw material costs and energy costs compared with the same period in 2011.

Gross profit. Our gross profit decreased approximately $2.2 million, or 42.7% to approximately $3.1 million in the second quarter of 2012 from approximately $5.3 million in the same period of 2011. Excluding foreign currency translation, our gross profit decreased approximately $2.4 million, or 44.6% compared with the same period of 2011. Gross profit as a percentage of net revenues was 15.6% in the second quarter of 2012, as compared with 26.1% in the same period of 2011. The percentage decrease was primarily attributable to the decreased gross profit margin in our fine precision abrasives segment and fracture proppants segment.

General and administrative expenses. Our general and administrative expenses consist of the expenses associated with staff and support personnel who manage our business activities and professional fees paid to third parties. Our general administrative expenses increased to approximately $1.9 million in the second quarter of 2012, from approximately $1.6 million in the same period in 2011. The increase was primarily due to the loss on disposal of equipment in our fine precision abrasives segment as we upgraded the production facilities and the increase in depreciation expenses and salary expenses. As a percentage of net revenues, administrative expenses increased to 9.9% in the second quarter of 2012 as compared with 8.0% in the same period in 2011.

Selling expenses. Our selling expenses include sales commissions, expenses of advertising and promotional materials, transportation expenses, benefits of sales personnel, after-sale support services and other sales related expenses. Selling expenses stayed flat at approximately $2.8 million in the second quarter of 2012. Excluding foreign currency translation, the selling expenses decreased approximately $60,000, or 2.2% compared with the same period of 2011. As a percentage of net revenues, our selling expenses increased to 14.2% in the second quarter of 2012, as compared with 13.5% in the same period in 2011.

Research and development expenses. Our research and development expenses increased to approximately $236,000 in the second quarter of 2012, compared with approximately $145,000 in the same period in 2011 due to more R&D activities in the second quarter of 2012. Excluding foreign currency translation, the research and development expenses were approximately $228,000.

Government grant income. Our government grant income was nil in the second quarter of 2012 compared with approximately $17,000 in the same period in 2011.

Finance costs. Our finance costs increased by approximately $379,000, or 24.1% to approximately $2.0 million in the second quarter of 2012, from approximately $1.6 million in the same period in 2011. Excluding foreign currency translation, our finance costs increased approximately $316,000, or 20.1% compared with the same period of 2011. As a percentage of net revenues, our finance costs were 9.9% in the second quarter of 2012 and 7.7% in the same period in 2011. This increase was primarily attributable to an increase of approximately $606,000 in interest expenses as we increased borrowing activities in the second quarter of 2012.

(Loss) income before income taxes and non-controlling interests. Our loss before income taxes and non-controlling interest was approximately $3.6 million in the second quarter of 2012, compared with approximately $42,000 in the same period of 2011. Excluding foreign currency translation, our loss before income taxes and non-controlling interest was approximately $3.5 million. The decrease was primarily attributable to the loss from operations and higher finance costs in the second quarter of 2012.

Income taxes. Our income taxes were approximately $202,000 in the second quarter of 2012, a decrease of approximately $24,000 or 10.6% from approximately $226,000 in the same period of 2011. Excluding foreign currency translation, our income taxes were approximately $194,000.

Net loss. Our net loss in the second quarter of 2012 was approximately $3.8 million, a decrease of approximately $3.5 million from approximately $247,000 in the same period in 2011. Excluding foreign currency translation, our net loss was approximately $3.7 million.The decrease was attributable to the factors described above.

11

Comparison of Six-Month Periods ended June 30, 2012 and 2011

The following table summarizes the results of our operations during the six-month periods ended June 30, 2012 and 2011, and provides information regarding the dollar and percentage increase or (decrease) during the six-month periods ended June 30, 2012 and 2011.

(All amounts, other than percentages, in U.S. dollars)

| Six-Month Period | Six-Month Period | |||||||||||

| Ended June 30, 2012 | Ended June 30, 2011 | |||||||||||

| As a | As a | |||||||||||

| Dollars in | percentage of | Dollars in | percentage of | |||||||||

| Statement of operations data: | thousands | net revenues | thousands | net revenues | ||||||||

| Net Sales | 33,331 | 100.0% | 36,620 | 100.0% | ||||||||

| Cost of goods sold | 27,560 | 82.7% | 26,998 | 73.7% | ||||||||

| Gross profit | 5,771 | 17.3% | 9,622 | 26.3% | ||||||||

| Operating expenses | ||||||||||||

| General & administrative expenses | 3,666 | 11.0% | 3,133 | 8.6% | ||||||||

| Research and development expenses | 399 | 1.2% | 287 | 0.8% | ||||||||

| Selling expenses | 5,271 | 15.8% | 4,733 | 12.9% | ||||||||

| Total operating expenses | 9,336 | 28.0% | 8,153 | 22.3% | ||||||||

| (Loss) income from operations | (3,565 | ) | -10.7% | 1,469 | 4.0% | |||||||

| Government grant income | 385 | 1.2% | 18 | 0.0% | ||||||||

| Guarantee income | 301 | 0.9% | 210 | 0.6% | ||||||||

| Guarantee expenses | (237 | ) | -0.7% | (176 | ) | -0.5% | ||||||

| Equity in net loss of a non-consolidated affiliate | (9 | ) | 0.0% | - | 0.0% | |||||||

| Interest income | 239 | 0.7% | 182 | 0.5% | ||||||||

| Change in fair value of warranty liabilities | - | 0.0% | 910 | 2.5% | ||||||||

| Other income (expenses) | 44 | 0.1% | (68 | ) | -0.2% | |||||||

| Finance costs | (3,700 | ) | -11.1% | (2,537 | ) | -6.9% | ||||||

| (Loss) income before income taxes and noncontrolling interest | (6,542 | ) | -19.6% | 8 | 0.0% | |||||||

| Income taxes | (214 | ) | -0.6% | (362 | ) | -1.0% | ||||||

| Noncontrolling interest | 49 | 0.1% | 27 | 0.1% | ||||||||

| Net loss attributable to Company’s common stockholders | (6,707 | ) | -20.1% | (327 | ) | -0.9% | ||||||

| Six-Month | Six-Month | Dollar ($) | Percentage | |||||||||

| Period Ended | Period Ended | Increase | Increase | |||||||||

| Dollars in thousands | June 30, 2012 | June 30, 2011 | (Decrease) | (Decrease) | ||||||||

| Net Sales | 33,331 | 36,620 | (3,289 | ) | -9.0% | |||||||

| Cost of goods sold | 27,560 | 26,998 | 562 | 2.1% | ||||||||

| Gross profit | 5,771 | 9,622 | (3,851 | ) | -40.0% | |||||||

| Operating expenses | ||||||||||||

| General & administrative expenses | 3,666 | 3,133 | 533 | 17.0% | ||||||||

| Research and development expenses | 399 | 287 | 112 | 39.0% | ||||||||

| Selling expenses | 5,271 | 4,733 | 538 | 11.4% | ||||||||

| Total operating expenses | 9,336 | 8,153 | 1,183 | 14.5% |

12

| (Loss) income from operations | (3,565 | ) | 1,469 | (5,034 | ) | -342.7% | ||||||

| Government grant income | 385 | 18 | 367 | 2,038.9% | ||||||||

| Guarantee income | 301 | 210 | 91 | 43.3% | ||||||||

| Guarantee expenses | (237 | ) | (176 | ) | (61 | ) | 34.7% | |||||

| Equity in net loss of a non-consolidated affiliate | (9 | ) | - | (9 | ) | -100.0% | ||||||

| Interest income | 239 | 182 | 57 | 31.3% | ||||||||

| Change in fair value of warranty liabilities | - | 910 | (910 | ) | -100% | |||||||

| Other income (expenses) | 44 | (68 | ) | 112 | 164.7% | |||||||

| Finance costs | (3,700 | ) | (2,537 | ) | (1,163 | ) | 45.8% | |||||

| (Loss) income before income taxes and noncontrolling interest | (6,542 | ) | 8 | (6,550 | ) | -81,875.0% | ||||||

| Income taxes | (214 | ) | (362 | ) | 148 | -40.9% | ||||||

| Noncontrolling interest | 49 | 27 | 22 | 81.5% | ||||||||

| Net loss attributable to Company’s common stockholders | (6,707 | ) | (327 | ) | (6,380 | ) | 1,951.1% |

Sales revenues. Sales revenues decreased approximately $3.3 million, or 9.0% to approximately $33.3 million for the six months ended June 30, 2012, from approximately $36.6 million in the same period of 2011. Excluding foreign currency translation, the revenue decreased approximately $4.5 million, or 12.2% compared with the same period of 2011. The decrease was mainly attributable to the decreased sales from our fracture proppant products.

In our refractory segment, we sold 42,985 metric tons of refractory products in the six months ended June 30, 2012, compared with 47,891 metric tons sold in the same period of 2011. The revenue from our refractory products was approximately $21.6 million in the six months ended June 30, 2012, compared with $22.5 million in the same period of 2011. Excluding foreign currency translation, the revenue decreased approximately $1.7 million, or 7.5% compared with the same period of 2011. The average selling price reached $502 per metric ton in the six months ended June 30, 2012, representing a 6.8% increase compared with $470 per metric ton in the same period of 2011. Excluding foreign currency translation, the average selling price increased to $484 per metric ton, or 3.0% in the six months ended June 30, 2012.

In our fracture proppant segment, we sold 18,703 metric tons of fracture proppant products in the six months ended June 30, 2012, compared with 28,542 metric tons sold in the same period of 2011. The decrease in sales volume was primarily due to the decreased sales in the U.S. market as we were unable to sell directly to the end users. Revenue was approximately $5.2 million in the six months ended June 30, 2012, a decrease of 53.1% compared with approximately $11.1 million in the same period of 2011. Excluding foreign currency translation, the revenue decreased approximately $6.1 million, or 54.8% compared with the same period of 2011. Average selling price decreased to $279 per metric ton in the six months ended June 30, 2012, compared with $390 per metric ton in the same period of 2011. Excluding foreign currency translation, the average selling price decreased to $269 per metric ton in the six months ended June 30, 2012. The decrease in average selling price was primarily due to the increased sales in domestic market where the fracture proppant products are typically priced lower than in the U.S. market.

In our industrial ceramics segment, sales revenue was approximately $861,000 in the six months ended June 30, 2012 compared with approximately $722,000 in the same period of 2011. Excluding foreign currency translation, the revenue was approximately $830,000.

In our fine precision abrasives segment, we realized sales of 2,055 ton in the six months ended June 30, 2012, for revenue of approximately $5.7 million. Excluding foreign currency translation, the revenue was approximately $5.5 million. We sold 623 metric tons of fine precision abrasives products for approximately $2.3 million in the same period of 2011. The increase in sales revenue was primarily due to the increased sales to a major customer.

Cost of goods sold. Our cost of goods sold increased approximately $562,000, or 2.1%, to approximately $27.6 million in the six months ended June 30, 2012 from approximately $27.0 million in the same period of 2011. Excluding foreign currency translation, our cost of goods sold decreased approximately $426,000, or 1.6% compared with the same period of 2011. As a percentage of net revenues, the cost of goods sold increased by 9.0% to 82.7% in the six months ended June 30, 2012 from 73.7% in the same period of 2011. This increase was primarily due to the higher raw material costs and energy costs compared with the same period in 2011.

Gross profit. Our gross profit decreased approximately $3.8 million, or 40.0% to approximately $5.8 million in the six months ended June 30, 2012 from approximately $9.6 million in the same period of 2011. Excluding foreign currency translation, our gross profit decreased approximately $4.1 million, or 42.2% compared with the same period of 2011. Gross profit as a percentage of net revenues was 17.3% in the six months ended June 30, 2012, as compared with 26.3% in the same period of 2011. The percentage decrease was primarily attributable to the decreased gross profit margin in our fine precision abrasives segment and fracture proppants segment.

General and administrative expenses. Our general administrative expenses increased to approximately $3.7 million in the six months ended June 30, 2012, from approximately $3.1 million in the same period in 2011. Excluding foreign currency translation, the general and administrative expenses increased approximately $401,000, or 12.8% compared with the same period of 2011. The increase was primarily due to the loss on disposal of equipment in our fine precision abrasives segment as we upgraded the production facilities, higher salary expenses and higher preliminary expenses related to Yuxing operation. As a percentage of net revenues, administrative expenses increased to 11.0% in the six months ended June 30, 2012 as compared with 8.6% in the same period in 2011.

Selling expenses. Selling expenses increased by approximately $538,000 to approximately $5.3 million in the six months ended June 30, 2012, compared with approximately $4.7 million in the same period in 2011. Excluding foreign currency translation, the selling expenses increased approximately $349,000, or 7.4% compared with the same period of 2011. As a percentage of net revenues, our selling expenses increased to 15.8% in the six months ended June 30, 2012, as compared with 12.9% in the same period in 2011. The increase in selling expenses was primarily attributable to the increase in the allowance for doubtful accounts and higher transportation expenses compared to the same period in 2011.

13

Research and development expenses. Our research and development expenses increased to approximately $399,000 in the six months ended June 30, 2012, compared with approximately $287,000 in the same period in 2011. Excluding foreign currency translation, the research and development expenses were approximately $385,000. The increase was mainly due to more R&D activities in the six months ended June 30, 2012.

Government grant income. Our government grant income was approximately $385,000 in the six months ended June 30, 2012 compared with approximately $18,000 in the same period in 2011. Excluding foreign currency translation, the government grant income was approximately $371,000.

Finance costs. Our finance costs increased by approximately $1.2 million, or 45.8% to approximately $3.7 million in the six months ended June 30, 2012, from approximately $2.5 million in the same period in 2011. Excluding foreign currency translation, our finance costs increased approximately $1.0 million, or 40.6% compared with the same period of 2011. As a percentage of net revenues, our finance costs were 11.1% in the six months ended June 30, 2012 and 6.9% in the same period in 2011. This significant increase was primarily attributable to an increase of approximately $481,000 in bills discounting charges as we discounted more bills receivable instead of holding them to maturity; and an increase of approximately $682,000 in interest expenses as we increased borrowing activities in the six months ended June 30, 2012.

(Loss) income before income taxes and non-controlling interests. Our loss before income taxes and non-controlling interest was approximately $6.5 million in the six months ended June 30, 2012, compared with an income of approximately $8,000 in the same period of 2011. Excluding foreign currency translation, our loss before income taxes and non-controlling interest was approximately $6.3 million. The decrease was primarily attributable to the loss from operations and higher finance costs in the six months ended June 30, 2012.

Income taxes. Our income taxes were approximately $214,000 in the six months ended June 30, 2012, a decrease of approximately $148,000 or 40.9% from approximately $362,000 in the same period of 2011. Excluding foreign currency translation, our income taxes were approximately $206,000.

Net loss. Our net loss in the six months ended June 30, 2012 was approximately $6.7 million, a decrease of approximately $6.4 million from approximately $327,000 in the same period in 2011. Excluding foreign currency translation, our net loss was approximately $6.5 million. The decrease was attributable to the factors described above.

Liquidity and Capital Resources

As of June 30, 2012, we had cash and cash equivalents of approximately $5.2 million and restricted cash of approximately $38.5 million. Our current assets were approximately $136.9 million and our current liabilities were approximately $131.7 million as of June 30, 2012 which resulted in a current ratio of approximately 1.04. Total equity as of June 30, 2012 was approximately $47.3 million. The following table sets forth a summary of our cash flows for the periods indicated:

| Six Months ended June 30, | ||||||

| (Dollars in thousands) | 2012 | 2011 | ||||

| Net cash used in operating activities | (13,305 | ) | (1,546 | ) | ||

| Net cash used in investing activities | (1,677 | ) | (8,318 | ) | ||

| Net cash provided by financing activities | 16,540 | 18,400 | ||||

| Net cash inflows | 1,569 | 8,564 | ||||

Operating Activities

Net cash used in operating activities was approximately $13.3 million in the six months ended June 30, 2012, compared with net cash used in operating activities of approximately $1.5 million in the same period of 2011. The increase in net cash used in operating activities was primarily due to the net loss, increase in trade receivables, bills receivables and decrease in bills payables in the six months ended June 30, 2012.

Investing Activities

Net cash used in investing activities in the six months ended June 30, 2012 was approximately $1.7 million, a decrease of approximately $6.6 million from net cash used in investing activities of approximately $8.3 million in the same period in 2011. The decrease in net cash used in investing activities in the six months ended June 30, 2012 was primarily due to fewer activities related to our construction of manufacturing and administrative facilities and no acquisition of land use right occurred.

Financing Activities

Net cash provided by financing activities was approximately $16.5 million in the six months ended June 30, 2012, compared with net cash provided by financing activities of approximately $18.4 million in the same period of 2011.

14

Loan Facilities

In the six months ended June 30, 2012, we secured new loans totaling approximately $50.0 million from banks for our working capital needs, and we repaid approximately $11.6 million in bank loans during the period. As a result, the balance of all bank loans and bank borrowings as of June 30, 2012 was approximately $84.6 million, which includes approximately $40.8 million short-term bank loans and approximately $43.8 million of bank borrowings secured by bank deposits.

As of June 30, 2012, the detail of all our short-term bank loans and bank borrowings are as follows:

All amounts, other than percentages, are in U.S. dollar.

| No | Type | Contracting Party | Valid Date | Duration | Amount |

|

1 |

Facility Bank Loan |

Shanghai Pudong Development Bank Village Bank |

2011-09-16 to 2012-09-14 |

1 year |

$792,000 |

|

2 |

Facility Bank Loan |

Shanghai Pudong Development Bank Village Bank |

2011-09-16 to 2012-09-15 |

1 year |

$396,000 |

|

3 |

Facility Bank Loan |

Shanghai Pudong Development Bank Village Bank |

2011-09-22 to 2012-09-21 |

1 year |

$712,800 |

|

4 |

Facility Bank Loan |

Shanghai Pudong Development Bank |

2011-09-22 to 2012-09-21 |

1 year |

$1,584,000 |

|

5 |

Facility Bank Loan |

Kaifeng Commercial Bank |

2011-09-27 to 2012-09-26 |

1 year |

$4,752,000 |

|

6 |

Facility Bank Loan |

Shanghai Pudong Development Bank |

2011-10-12 to 2012-10-11 |

1 year |

$1,584,000 |

|

7 |

Facility Bank Loan |

Shanghai Pudong Development Bank Village Bank |

2011-10-14 to 2012-10-13 |

1 year |

$427,680 |

|

8 |

Facility Bank Loan |

City Credit Cooperatives in Gongyi |

2011-12-12 to 2012-12-5 |

1 year |

$2,851,200 |

|

9 |

Facility Bank Loan |

Zhengzhou Bank |

2012-01-5 to 2013-01-04 |

1 year |

$4,752,000 |

|

10 |

Facility Bank Loan |

China Construction Bank |

2012-01-10 to 2013-01-09 |

1 year |

$3,168,000 |

|

11 |

Facility Bank Loan |

China EverBright Bank |

2012-01-20 to 2012-07-17 |

6 months |

$1,053,202 |

|

12 |

Facility Bank Loan |

Industrial and Commercial Bank of China |

2012-02-03 to 2013-01-08 |

1 year |

$2,851,200 |

|

13 |

Facility Bank Loan |

China EverBright Bank |

2012-02-16 to 2012-08-13 |

6 months |

$1,252,310 |

|

14 |

Facility Bank Loan |

Agricultural Bank of China |

2012-02-20 to 2013-02-19 |

1 year |

$1,853,280 |

|

15 |

Facility Bank Loan |

China CITIC Bank |

2012-03-01 to 2013-02-28 |

1 year |

$1,473,120 |

|

16 |

Facility Bank Loan |

Luoyang Bank |

2012-04-25 to 2013-04-24 |

1 year |

$3,168,000 |

|

17 |

Facility Bank Loan |

Agricultural Bank of China |

2012-04-28 to 2013-04-27 |

1 year |

$5,068,800 |

|

18 |

Facility Bank Loan |

Industrial and Commercial Bank of China |

2012-05-09 to 2013-05-08 |

1 year |

$712,800 |

|

19 |

Facility Bank Loan |

China CITIC Bank |

2012-06-26 to 2013-06-25 |

1 year |

$2,376,000 |

|

20 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-02 to 2012-08-10 |

6 months |

$126,720 |

|

21 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-02 to 2012-08-22 |

6 months |

$364,320 |

|

22 |

Bank Borrowing |

Luoyang Bank |

2012-03-06 to 2012-09-05 |

6 months |

$1,584,000 |

|

23 |

Bank Borrowing |

Puyang Commerical Bank |

2012-03-13 to 2012-09-12 |

6 months |

$1,584,000 |

|

24 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-15 to 2012-07-10 |

4 months |

$158,400 |

|

25 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-15 to 2012-07-18 |

5 months |

$47,520 |

|

26 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-15 to 2012-09-06 |

6 months |

$190,080 |

|

27 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-20 to 2012-08-28 |

6 months |

$70,963 |

15

|

28 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-20 to 2012-09-07 |

6 months |

$79,200 |

|

29 |

Bank Borrowing |

Puyang Commerical Bank |

2012-03-20 to 2012-09-14 |

6 months |

$1,520,640 |

|

30 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-21 to 2012-07-09 |

4 months |

$47,520 |

|

31 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-21 to 2012-08-29 |

6 months |

$31,680 |

|

32 |

Bank Borrowing |

Puyang Commerical Bank |

2012-03-22 to 2012-09-19 |

6 months |

$1,346,400 |

|

33 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-23 to 2012-08-24 |

6 months |

$47,520 |

|

34 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-03-23 to 2012-09-09 |

6 months |

$792,000 |

|

35 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-04-06 to 2012-09-28 |

6 months |

$633,600 |

|

36 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-04-06 to 2012-09-30 |

6 months |

$285,120 |

|

37 |

Bank Borrowing |

Puyang Commerical Bank |

2012-04-06 to 2012-10-05 |

6 months |

$3,168,000 |

|

38 |

Bank Borrowing |

Puyang Commerical Bank |

2012-04-09 to 2012-10-06 |

6 months |

$1,584,000 |

|

39 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-04-10 to 2012-08-03 |

4 months |

$79,200 |

|

40 |

Bank Borrowing |

Luoyang Bank |

2012-04-11 to 2012-09-08 |

5 months |

$475,200 |

|

41 |

Bank Borrowing |

Luoyang Bank |

2012-04-11 to 2012-09-19 |

6 months |

$475,200 |

|

42 |

Bank Borrowing |

Luoyang Bank |

2012-04-11 to 2012-09-21 |

6 months |

$792,000 |

|

43 |

Bank Borrowing |

Luoyang Bank |

2012-04-11 to 2012-09-27 |

6 months |

$1,425,600 |

|

44 |

Bank Borrowing |

Puyang Commerical Bank |

2012-04-11 to 2012-10-10 |

6 months |

$3,168,000 |

|

45 |

Bank Borrowing |

Puyang Commerical Bank |

2012-04-13 to 2012-10-12 |

6 months |

$4,672,800 |

|

46 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-04-17 to 2012-07-27 |

4 months |

$79,200 |

|

47 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-04-20 to 2012-09-15 |

5 months |

$79,200 |

|

48 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-04-28 to 2012-10-19 |

6 months |

$158,400 |

|

49 |

Bank Borrowing |

Puyang Commerical Bank |

2012-05-04 to 2012-11-03 |

6 months |

$3,168,000 |

|

50 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-05-06 to 2012-08-16 |

4 months |

$79,200 |

|

51 |

Bank Borrowing |

Puyang Commerical Bank |

2012-05-07 to 2012-11-04 |

6 months |

$950,400 |

|

52 |

Bank Borrowing |

Puyang Commerical Bank |

2012-05-09 to 2012-11-07 |

6 months |

$1,584,000 |

|

53 |

Bank Borrowing |

Puyang Commerical Bank |

2012-05-09 to 2012-11-08 |

6 months |

$792,000 |

|

54 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-05-11 to 2012-11-03 |

6 months |

$142,560 |

|

55 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-05-14 to 2012-11-09 |

6 months |

$158,400 |

|

56 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-05-17 to 2012-11-10 |

6 months |

$79,200 |

|

57 |

Bank Borrowing |

Puyang Commerical Bank |

2012-05-17 to 2012-11-16 |

6 months |

$2,851,200 |

|

58 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-05-30 to 2012-11-10 |

6 months |

$79,200 |

|

59 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-05-30 to 2012-11-17 |

6 months |

$95,040 |

|

60 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-05-31 to 2012-11-17 |

6 months |

$126,720 |

|

61 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-05 to 2012-09-07 |

6 months |

$15,840 |

|

62 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-05 to 2012-09-14 |

6 months |

$15,840 |

|

63 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-05 to 2012-09-16 |

6 months |

$31,680 |

|

64 |

Bank Borrowing |

Hana Bank |

2012-06-05 to 2012-11-25 |

6 months |

$633,600 |

16

|

65 |

Bank Borrowing |

Puyang Commerical Bank |

2012-06-07 to 2012-12-06 |

6 months |

$3,168,000 |

|

66 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-08 to 2012-11-21 |

6 months |

$79,200 |

|

67 |

Bank Borrowing |

Puyang Commerical Bank |

2012-06-08 to 2012-12-08 |

6 months |

$950,400 |

|

68 |

Bank Borrowing |

Puyang Commerical Bank |

2012-06-14 to 2012-12-14 |

6 months |

$633,600 |

|

69 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-15 to 2012-11-29 |

6 months |

$792,000 |

|

70 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-19 to 2012-12-18 |

6 months |

$950,400 |

|

71 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-20 to 2012-12-19 |

6 months |

$950,400 |

|

72 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-29 to 2012-09-02 |

4 months |

$15,840 |

|

73 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-29 to 2012-12-08 |

6 months |

$95,040 |

|

74 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-29 to 2012-12-12 |

6 months |

$158,400 |

|

75 |

Bank Borrowing |

Shanghai Pudong Development Bank Village Bank |

2012-06-29 to 2012-12-13 |

6 months |

$79,200 |

We have approximately $40.8 million of facility bank loans, maturing from July 17, 2012 to June 25, 2013 and approximately $43.8 million of bank borrowings secured by bank deposits. We will also consider refinancing debts. However, we cannot provide assurance that we will be able to refinance any of our debts on terms favorable to us in a timely manner.

Below is a brief summary of the payment obligations under material contracts to which we are a party:

On September 16, 2011, our subsidiary, Refractories, entered into a short-term working capital loan agreement with Shanghai Pudong Development Bank Village Bank of Gongyi (“SPDVB”), whereby SPDVB has agreed to loan approximately $792,000 (RMB 5 million) to Refractories for a term of one year, at an interest rate of 6.56% per year on all outstanding principal.

On September 16, 2011, our subsidiary, Duesail, entered into a short-term working capital loan agreement with SPDVB, whereby SPDVB has agreed to loan approximately $396,000 (RMB 2.5 million) to Duesail for a term of one year, at an interest rate of 8.53% per year on all outstanding principal.

On September 22, 2011, our subsidiary, Refractories, entered into a short-term working capital loan agreement SPDVB, whereby SPDVB has agreed to loan approximately $713,000 (RMB 4.5 million) to Refractories for a term of one year, at an interest rate of 6.56% per year on all outstanding principal.

On September 22, 2011, our subsidiary, Duesail, entered into a short-term working capital loan agreement with Shanghai Pudong Development Bank (“SPD”), whereby SPD has agreed to loan approximately $1.6 million (RMB 10 million) to Duesail for a term of one year, at an interest rate of 7.22% per year on all outstanding principal.

On September 27, 2011, our subsidiary, Duesail, entered into a short-term working capital loan agreement with Kaifeng Commercial Bank (“KCB”), whereby KCB has agreed to loan approximately $4.8 million (RMB 30 million) to Duesail for a term of one year, at an interest rate of 8.53% per year on all outstanding principal.

On October 12, 2011, our subsidiary, Refractories, entered into a short-term working capital loan agreement with SPD, whereby SPD has agreed to loan approximately $1.6 million (RMB 10 million) to Refractories for a term of one year, at an interest rate of 7.22% per year on all outstanding principal.

On October 14, 2011, our subsidiary, Refractories, entered into a short-term working capital loan agreement with SPDVB, whereby SPDVB has agreed to loan approximately $428,000 (RMB 2.7 million) to Refractories for a term of one year, at an interest rate of 6.56% per year on all outstanding principal.

On December 12, 2011, our subsidiary, Duesail, entered into a short term working capital loan agreement with City Credit Cooperatives in Gongyi (“CCCG”), whereby CCCG has agreed to loan approximately $2.9 million (RMB18 million) to Duesail for a term of one year, at an interest rate of 11.81% per year on all outstanding principal.

On January 5, 2012, our subsidiary, Refractories, entered into a short-term working capital loan agreement with Zhengzhou Bank (“ZB”), whereby ZB has agreed to loan approximately $4.8 million (RMB 30 million) to Refractories for a term of one year, at an interest rate of 6.56% per year on all outstanding principal.

17

On January 10, 2012, our subsidiary, Duesail, entered into a short term working capital loan agreement with China Construction Bank (“CCB”), whereby CCB has agreed to loan approximately $3.2 million (RMB 20 million) to Duesail for a term of one year, at an interest rate of 8.00% per year on all outstanding principle.

On January 20, 2012, our subsidiary, Micronized, entered into a short-term working capital loan agreement with China EverBright Bank (“CEB”), whereby CEB has agreed to loan approximately $1.1 million (RMB 6.6 million) to Micronized for a term of 6 months, at an interest rate of $7.625% per year on all outstanding principal.

On February 3, 2012, our subsidiary, Refractories, entered into a short-term working capital loan agreement with Industrial and Commercial Bank of China (“ICBC”), whereby ICBC has agreed to loan approximately $2.9 million (RMB 18 million) to Refractories for a term of one year, at an interest rate of 6.89% per year on all outstanding principal.

On February 16, 2012, our subsidiary, Micronized, entered into a short-term working capital loan agreement with CEB, whereby CEB has agreed to loan approximately $1.3 million (RMB 7.9 million) to Micronized for a term of 6 months, at an interest rate of $7.625% per year on all outstanding principal.

On February 20, 2012, our subsidiary, Micronized, entered into a short-term working capital loan agreement with Agricultural Bank of China (“ABC”), whereby ABC has agreed to loan approximately $1.9 million (RMB 11.7 million) to Micronized for a term of one year, at an interest rate of 6.56% per year on all outstanding principal.

On March 1, 2012, our subsidiary, Micronized, entered into a short-term working capital loan agreement with China CITIC Bank (“CITIC”), whereby CITIC has agreed to loan approximately $1.5 million (RMB 9.3 million) to Micronized for a term of one year, at an interest rate of 6.56% per year on all outstanding principal.

On April 25, 2012, our subsidiary, Refractories, entered into a short-term working capital loan agreement with Luoyang Bank (“LYB”), whereby LYB has agreed to loan approximately $3.2 million (RMB 20 million) to Refractories for a term of one year, at an interest rate of 7.22% per year on all outstanding principal.

On April 28, 2012, our subsidiary, Refractories, entered into a short-term working capital loan agreement with ABC, whereby ABC has agreed to loan approximately $5.1 million (RMB 32 million) to Refractories for a term of one year, at an interest rate of 8.53% per year on all outstanding principal.

On May 9, 2012, our subsidiary, Micronized, entered into a short-term working capital loan agreement with ICBC, whereby ICBC has agreed to loan approximately $713,000 (RMB 4.5 million) to Micronized for a term of one year, at an interest rate of 6.56% per year on all outstanding principal.

On June 26, 2012, our subsidiary, Refractories, entered into a short-term working capital loan agreement with CITIC, whereby CITIC has agreed to loan approximately $2.4 million (RMB 15 million) to Refractories for a term of one year, at an interest rate of 6.94% per year on all outstanding principal.

18

Statutory Reserves

Under PRC regulations, all our subsidiaries in the PRC may pay dividends only out of their accumulated profits, if any, determined in accordance with PRC GAAP. In addition, these companies are required to set aside at least 10% of their after-tax net profits each year, if any, to fund the statutory reserves until the balance of the reserves reaches 50% of their registered capital. The statutory reserves are not distributable in the form of cash dividends to the Company and can be used to make up cumulative prior year losses.

Special Reserve

Before the reorganization, a former subsidiary of Refractories, Gongyi GengSheng Refractories Co., Ltd., was entitled to a special tax concession (“Tax Concession”) because it employed the required number of disabled staff according to the relevant PRC tax rules. In particular, this Tax Concession exempted the subsidiary from paying enterprise income tax. However, these tax savings can only be used for future development of its production facilities or welfare matters, and cannot be distributed as cash dividends. Accordingly, the same amount of tax savings was set aside and taken to special reserve which is not available for distribution. This reserve as maintained by the subsidiary has been combined into Refractories upon the reorganization and is subject to the same restrictions in its usage.

Restrictions on net assets also include the conversion of local currency into foreign currencies, tax withholding obligations on dividend distributions, the need to obtain SAFE approval for loans to a non-PRC consolidated entity and the covenants or financial restrictions related to outstanding debt obligations. We did not have these restrictions on our net assets as of June 30, 2012 and December 31, 2011.

The following table provides the amount of our statutory reserves, special reserve, the amount of restricted net assets, consolidated net assets, and the amount of restricted net assets as a percentage of consolidated net assets, as of June 30, 2012 and December 31, 2011.

| As of June 30, 2012 (Unaudited) |

As of December 31, 2011 |

|||||

| Statutory reserves | $ | 4,554,936 | $ | 4,554,936 | ||

| Special reserve | 3,556,036 | 3,556,036 | ||||

| Total restricted net assets | $ | 8,110,972 | $ | 8,110,972 | ||

| Consolidated net assets | $ | 47,086,388 | $ | 53,589,986 | ||

| Restricted net assets as percentage of consolidated net assets | 17.2 | % | 15.1 | % |